Exhibit 99.2

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

Excellon Resources Inc. (the “Company” or “Excellon”) has prepared this Management’s Discussion and Analysis of Financial Results (“MD&A”) for the year ended December 31, 2020 in accordance with the requirements of National Instrument 51-102 (“NI 51-102”).

This MD&A contains information as at March 16, 2021 and provides information on the operations of the Company for the years ended December 31, 2020 and 2019 and subsequent to the period end, and should be read in conjunction with the audited consolidated financial statements for the years ended December 31, 2020 and 2019 which have been filed on SEDAR and EDGAR. The audited consolidated financial statements for the years ended December 31, 2020 and 2019 have been prepared in accordance with International Financial Reporting Standards (“IFRS”). All figures in this MD&A are in thousands of United States dollars ($’000) unless otherwise noted.

This MD&A also refers to Production Cost per Tonne, Cash Cost per Silver Ounce Payable, value of metal content in products sold and All-in Sustaining Cost (“AISC”) per Silver Ounce Payable, all of which are Non-IFRS measures. Please refer to the sections of this MD&A entitled “Production Cost per Tonne”, “Total Cash Cost per Silver Ounce Payable” and “All-in Sustaining Cost per Silver Ounce Payable” for an explanation of these measures and reconciliation to the Company’s reported financial results.

| 1 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

BUSINESS AND STRATEGIC PRIORITIES

Excellon’s vision is to create wealth by realizing strategic opportunities through discipline and innovation for the benefit of the Company’s employees, communities and shareholders. The Company is advancing a precious metals growth pipeline that includes: Platosa, Mexico’s highest-grade silver mine since production commenced in 2005; Kilgore, a high-quality gold development project in Idaho with strong economics and significant growth and discovery potential; and an option on Silver City, a high-grade epithermal silver district in Saxony, Germany with 750 years of mining history and no modern exploration. The Company also aims to continue capitalizing on current market conditions by acquiring undervalued projects.

The common shares of Excellon trade on the Toronto Stock Exchange and the NYSE American, LLC exchange (the “NYSE American”) under the symbol “EXN” and on the Frankfurt Stock Exchange under the symbol “E4X2”.

Acquisition of Otis Gold Corp.

On April 22, 2020, the Company completed a plan of arrangement to acquire Otis Gold Corp. (“Otis”). Otis shareholders received 0.046 (adjusted for the Consolidation as defined below) of a common share of the Company for each Otis common share held, resulting in the issuance of 8,130,630 Excellon common shares valued at $16.4 million. The acquisition also resulted in outstanding Otis stock options and warrants being converted to Excellon stock options and warrants, resulting in the issuance of 531,895 Excellon stock options and 305,060 Excellon warrants exercisable at C$3.30 until March 29, 2022, valued at $0.6 million.

As part of the acquisition, the Company acquired the Kilgore Gold Project located in Clark County, Idaho, USA, consisting of 614 federal lode mining claims unencumbered by any underlying royalties, and the Oakley Project which includes Blue Hill Creek, Matrix Creek, Cold Creek and other properties in Idaho, USA. The Oakley Project is under an option agreement between Excellon and Centerra Gold Inc. (“Centerra”).

Listing on the NYSE American and share consolidation

The Company completed a consolidation of its common shares at a ratio of five pre-consolidation common shares for one post-consolidation common share effective September 10, 2020 (the “Consolidation”) and listed its common shares on the NYSE American effective September 23, 2020.

As a result of the Consolidation, shares issuable pursuant to the Company’s outstanding stock options, warrants, restricted share units and other convertible securities were proportionally adjusted on the same basis. All common share numbers, numbers of shares issuable under stock options, warrants and restricted share units and related per-share amounts in this MD&A have been retrospectively adjusted to reflect the Consolidation.

C$17.91 Million convertible debenture financing

On August 4, 2020, the Company closed a private placement (the “Financing”) of secured convertible debentures (the “Debentures”) for total proceeds of C$17,910,000.

The Debentures have a term of 36 months and are convertible into common shares of the Company prior to maturity at a conversion price of C$5.30 per common share. The Debentures bear interest at an annual rate of 5.75%, payable in cash semi-annually. Interest on the Debentures may alternatively be paid in common shares of the Company at the Company’s option based on the 10-day volume-weighted average price of the common shares prior to the payment date and an effective annual interest rate of 10%. The Debentures are secured against the Company’s assets in Mexico.

| 2 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

On or after July 30, 2022 and prior to maturity, the Company may accelerate the conversion of the entire issuance of Debentures, provided that the 20-day VWAP of the common shares on or after such 24-month anniversary is equal to greater than C$12.50.

The Company also issued 1,006,542 common-share purchase warrants to purchasers of the Debentures and 136,887 common share purchase warrants to brokers, with an exercise price of C$5.75 and an expiry date of July 30, 2023.

Restart of Mexican operations following COVID-19 Suspension

On April 2, 2020, the Company announced the temporary suspension of mining, milling and exploration activities at its Mexican operations (the “Suspension”) in accordance with the Mexican presidential order to mitigate the spread of COVID-19. The Mexican government subsequently declared mining an essential service and companies were permitted to restart operations on June 1, 2020, provided they met the COVID-19 guidelines established by the Mexican government.

The Suspension materially impacted the Company’s business as mining and milling operations were limited throughout Q2 2020 and only began resuming in mid-June. Metal production and revenues were, therefore, negligible during the period, while care-and-maintenance and ongoing labour costs were significant.

The Company restarted the mining, milling and exploration activities at its Mexican operations in June, including the resumption of concentrate shipments, and reached full production on July 1, 2020. COVID-19 prevention, health screening, contact tracing, testing and quarantine protocols were developed and implemented as part of the Company’s restart plans and to date have proven effective in protecting the workforce from confirmed COVID-19 cases that originated from community spread.

Record mined tonnage in the second half of 2020

The Company achieved record tonnes mined at Platosa in the second half of 2020. Platosa continued to outperform 2019 productivity while reducing operating costs, improving its safety performance and managing the ongoing threat posed by COVID-19. Metallurgical recoveries at Miguel Auza improved on an annual basis, while plant reliability has substantially increased. During 2020, the Platosa operation realized improvements in shift scheduling, mining method, offtake arrangements and electricity costs, while completing the phase-2 tailings management facility raise and strengthening the management and technical teams.

Transition to private electricity supplier at Platosa

On October 12, 2020 the Company obtained final regulatory approvals and completed the transition to a private Mexican energy provider for the Platosa Mine. Electricity costs, one of the Platosa Mine’s largest operating costs, were significantly reduced on a per-unit basis in Q4 2020.

In mid-February 2021, a polar vortex in the American southwest affected energy infrastructure in south Texas which led to supply shocks and record-high natural gas prices. This event disrupted electricity generation throughout northern Mexico including private energy providers for an 8-day period, after which natural gas supplies and prices returned to normal levels. The Company mitigated the cost impact by shedding electrical loads while maintaining budgeted production levels and estimates the incremental electricity cost to be $0.5 million during this period.

| 3 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

Exploration activities

The Company advanced its exploration programs in USA, Mexico and Germany including:

| ● | 110 km2 of geophysical surveying on the Kilgore Property in Clark County, Idaho, USA and the staking of 175 claims, increasing the exploration property size by approximately 28%. |

| ● | Successful drill permitting, land access and ramp-up of the drilling program at the Silver City Project in Saxony, Germany. |

| ● | Initial diamond drilling results from the first holes drilled on the Silver City Project for precious metals including: |

| ○ | A new discovery at Grauer Wolf, the fourth target drilled at Silver City with 1,043 g/t silver equivalent (“AgEq”) over 1.3 metres (954 g/t Ag, 0.1 g/t Au, 0.7% Pb and 2.0% Zn), within 194 g/t AgEq over 8.1 metres (173 g/t Ag, 0.1 g/t, Au, 0.4% Pb and 0.3% Zn); | |

| ○ | 1,042 g/t AgEq over 0.45 metres (911 g/t Ag, 0.4 g/t Au, 2.8% Pb and 0.9% Zn), within 231 g/t AgEq over 2.30 metres (183 g/t Ag, 0.4 g/t, Au 0.5% Pb and 0.2% Zn) in initial drilling on the Peter Vein; | |

| ○ | 505 g/t AgEq over 0.71 metres (356 g/t Ag, 2.0 g/t Au), within 191 g/t AgEq (134 g/t Ag and 0.8 g/t Au) in the first hole at Reichenbach (Großvoigtsberg), a new, near-surface discovery in an area with minimal historic mining; and | |

| ○ | 319 g/t AgEq over 0.35 metres (300 g/t Ag, 0.2 g/t Au and 0.2% Zn), within 101 g/t AgEq (87 g/t Ag, 0.2 g/t Au) in the first hole at Bräunsdorf. |

| ● | Underground drilling at the Platosa Mine identified multiple significant opportunities to define additional mineralization at Platosa, including further definition and expansion of the Rodilla NE-1S and Pierna Mantos, with diamond drilling results including: |

| ○ | 1,170 g/t AgEq over 4.2 metres (741 g/t Ag, 7.5% Pb, 4.8% Zn and 0.9 g/t Au) in EX20UG485, including 1,812 g/t AgEq over 2.0 metres (1,153 g/t Ag, 12.3% Pb, 6.1% Zn and 1.7 g/t Au); and | |

| ○ | 1,422 g/t AgEq over 8.9 metres (1,023 g/t Ag, 9.3% Pb, 4.5% Zn and 0.1 g/t Au) in EX20UG491, including 4,623 g/t AgEq over 2.2 metres (3,499 g/t Ag, 29.7% Pb, 10.3% Zn and 0.1 g/t Au). |

| ● | Drilling is underway to define newly-discovered mineralization in an area of the Platosa deposit that was never effectively drilled from surface – the Gap Zone – with 300 metres of potential mineralized strike connected to the 10-20 Target, where drilling has intersected massive sulphide clasts 250 metres to the south of the Platosa deposit that could indicate potential for an extension of the Platosa mineralized footprint. |

Sprott Credit Facility

On March 16, 2020, the Company announced the closing of a US$6-million bridge-loan credit facility (the “Sprott Credit Facility”) with Sprott Private Resource Lending II (Collector), LP (“Sprott Lending”). The Facility bore interest at 10% per annum, compounded and payable monthly, and was due and payable in full on or before September 14, 2020. In consideration for the Sprott Lending Facility, Excellon issued 107,291 common shares (adjusted for the Consolidation) to Sprott Lending. On August 4, 2020, the Company repaid the $6.0 million Sprott Credit Facility in full.

| 4 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

Updated Mineral Resource Estimate (“MRE”) on the Evolución Project in Zacatecas, Mexico

In Q3 2020, the Company completed a MRE for the Calvario and Lechuzas Zones on the Evolución Project in Zacatecas, Mexico, as further described under “Exploration and Evaluation Review – Evolución Project,” below.

Corporate update

On September 30, 2020, the Company announced the appointment of Paul Keller, P. Eng. as Chief Operating Officer and Alfred Colas, CPA, CA as Chief Financial Officer and the appointment of Anna Ladd-Kruger to the Company’s Board of Directors, as a non-independent director.

Mexican Operations

The operation continued to realize improvements from organizational changes implemented at the site prior to the Suspension. Improvements were realized in lower consumable costs, lower workforce costs, and improved mine efficiency evidenced by higher mine extraction by month and increased equipment reliability. Ongoing focus on business improvements and lower electricity prices from the newly activated power contract at Platosa are expected to continue improving the operation’s economics.

Improvements to the mine pumping infrastructure and new wells will continue into 2021. Additions of inline boosters to the well pumps have improved the overall system efficiency, reducing electricity draw and costs associated with the water table pump-down.

Mine infill diamond drilling was a major focus in the second half of 2020 and will continue in 2021. Three underground drill rigs are performing this task and will continue into the middle of 2021. With the high commodity prices experienced and forecast, the focus is also on adding tonnage to the operational plans currently being pursued, and planned mining zones are expected to improve mining efficiency in the current year.

Exploration Plans

Exploration plans were delayed in 2020 due to COVID-19 but 2020 exploration activities resumed in Q3, with an underground drill rig focused on definition and expansion of existing resources, complemented by surface rigs testing for continued expansion of the known mantos to the south of 623 and regional targets at PDN. An additional rig was deployed at the end of Q3 2020 for drilling at Jaboncillo. The Company plans to drill and test the Jaboncillo, PDN and 10-20 targets during the first six months of 2021. The Company also intends to continue exploration with one to two rigs from underground with the intention of further defining and expanding the resource.

At the Silver City Project, the Company has applied for a new Drilling Operation Plan (“DOP”) for 2021 drilling on four priority targets where the Company has intersected high grade mineralization, while also testing new targets over a strike length of 12-18 kilometres. In Q1 2021, the Company announced the expansion of the Silver City Project through the addition of three new licenses: Frauenstein (5,700 ha), Mohorn (5,700 ha) and Oederon (6,300 ha). Each of these licenses had significant historical silver production dating back to the 11th century.

| 5 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

At the Kilgore Project, the Company aims to improve understanding of the deposit setting on a local and regional scale through: re-logging core to enhance the underlying structural and lithologic framework, improving characterization of host rocks through lithogeochemistry, and sampling and assaying of silver mineralization to potentially improve project economics. The Company also plans further regional exploration, prospecting and geophysics to generate new targets and has hired a project manager and exploration manager to advance the project.

The Company filed an updated Plan of Operations with the United States Forest Service (“USFS”) in Q2 2020, and the USFS is now in the process of revising the National Environmental Policy Act Environmental Assessment (“EA”) accordingly. The Company is informed by the USFS that the process to prepare a Revised EA and Decision Notice (“DN”) will be complete by mid-2021. If the DN is received within that timeframe, the Company could commence drilling in Q3 2021.

Exploration also continues at the Oakley Project, subject to the option agreement between Excellon and Centerra Gold Inc. (“Centerra”). During Q3 2020, the Company advanced work to support future drilling, including soil geochemistry, IP and surveys, an airborne regional magnetic survey (LIDAR) and mapping.

| 6 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

Production

As noted above, results for the year ended December 31, 2020 were significantly affected by the Suspension. Metal production and revenues during Q2 2020 were negligible while ongoing labour and other care and maintenance costs were significant. Concentrate deliveries from the mill resumed in early July.

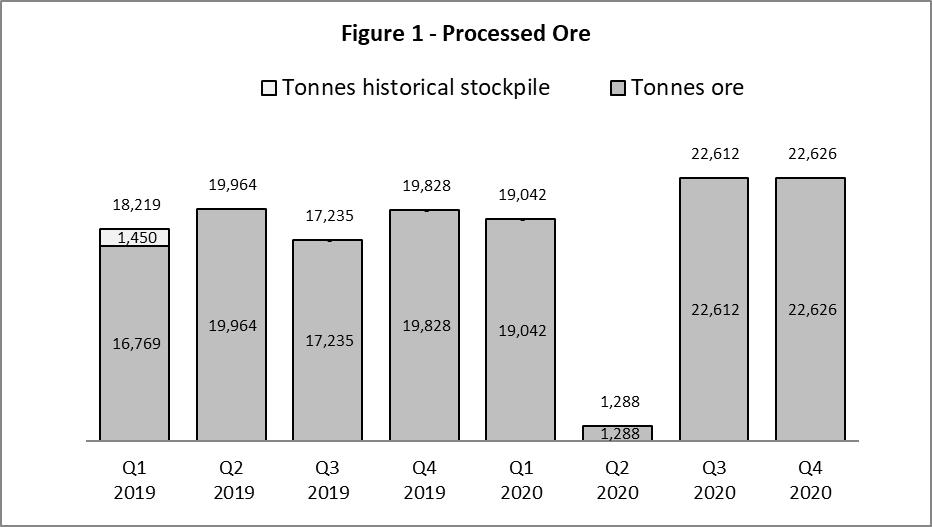

Platosa Mine production statistics for the periods indicated are as follows:

| Q4 | Q4 | |||||||||||||||

| 2020(1) | 2019(1) | 2020(1) | 2019(1) | |||||||||||||

| Tonnes Mined from Platosa: | 21,455 | 19,622 | 66,501 | 74,876 | ||||||||||||

| Ore processed (t): | 22,626 | 19,828 | 65,567 | 73,797 | ||||||||||||

| Historical stockpile processed (t): | - | - | - | 1,450 | ||||||||||||

| Platosa ore processed (t): | 22,626 | 19,828 | 65,567 | 75,247 | ||||||||||||

| Ore grades: | ||||||||||||||||

| Silver (g/t) | 536 | 435 | 519 | 497 | ||||||||||||

| Lead (%) | 5.42 | 4.84 | 5.37 | 4.82 | ||||||||||||

| Zinc (%) | 6.12 | 6.39 | 6.57 | 6.93 | ||||||||||||

| Historical stockpile grades: | ||||||||||||||||

| Silver (g/t) | - | - | - | 123 | ||||||||||||

| Lead (%) | - | - | - | 1.22 | ||||||||||||

| Zinc (%) | - | - | - | 1.44 | ||||||||||||

| Blended head grade: | ||||||||||||||||

| Silver (g/t) | 536 | 435 | 519 | 490 | ||||||||||||

| Lead (%) | 5.42 | 4.84 | 5.37 | 4.75 | ||||||||||||

| Zinc (%) | 6.12 | 6.39 | 6.57 | 6.82 | ||||||||||||

| Recoveries: | ||||||||||||||||

| Silver (%) | 91.2 | 91.7 | 91.4 | 89.9 | ||||||||||||

| Lead (%) | 82.9 | 80.2 | 83.7 | 79.2 | ||||||||||||

| Zinc (%) | 80.1 | 76.5 | 78.9 | 77.7 | ||||||||||||

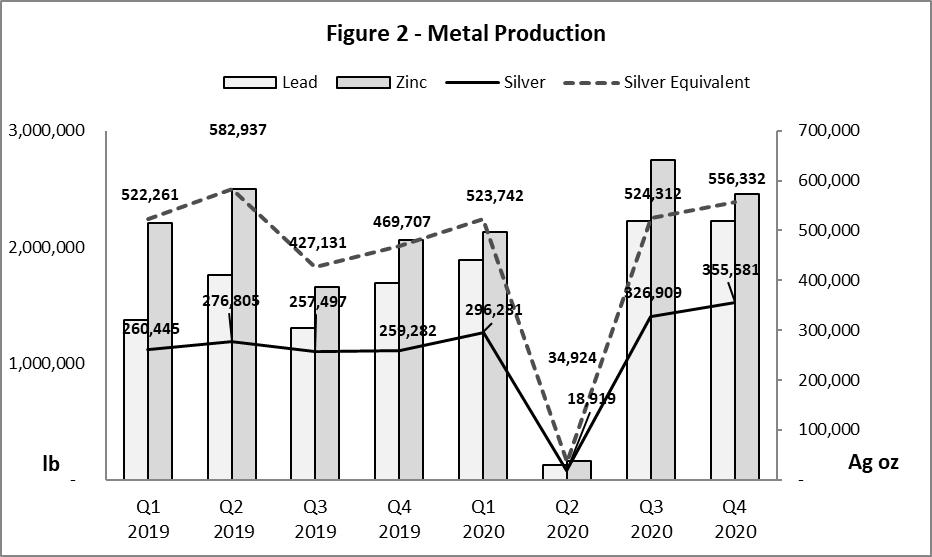

| Metal Production: | ||||||||||||||||

| Silver – (oz) | 355,581 | 259,282 | 997,690 | 1,054,029 | ||||||||||||

| Lead – (lb) | 2,223,465 | 1,690,610 | 6,470,637 | 6,134,888 | ||||||||||||

| Zinc – (lb) | 2,452,728 | 2,062,018 | 7,488,825 | 8,425,221 | ||||||||||||

| Silver equivalent (oz) (2) | 556,332 | 469,707 | 1,639,310 | 2,002,036 | ||||||||||||

| Payable: (3) | ||||||||||||||||

| Silver – (oz) | 323,139 | 232,034 | 928,240 | 962,355 | ||||||||||||

| Lead – (lb) | 2,049,065 | 1,563,313 | 6,087,239 | 5,766,608 | ||||||||||||

| Zinc – (lb) | 2,088,975 | 1,614,046 | 6,442,712 | 7,410,202 | ||||||||||||

| Silver equivalent (oz) (2) | 499,644 | 408,899 | 1,501,354 | 1,823,005 | ||||||||||||

| Average realized prices: (4) | ||||||||||||||||

| Silver – ($US/oz) | 24.46 | $ | 17.12 | 21.59 | $ | 16.07 | ||||||||||

| Lead – ($US/lb) | 0.87 | $ | 0.87 | 0.83 | $ | 0.88 | ||||||||||

| Zinc – ($US/lb) | 1.21 | $ | 1.04 | 1.08 | $ | 1.12 | ||||||||||

| Toll milling (3rd party) ore processed (t) | - | 6,398 | 4,785 | 14,231 | ||||||||||||

| Silver ounces produced | 355,581 | 259,282 | 997,690 | 1,054,029 | ||||||||||||

| Silver ounces payable | 323,139 | 232,034 | 928,240 | 962,355 | ||||||||||||

| Silver equivalent (“AgEq”) ounces produced (2) | 556,332 | 469,707 | 1,639,310 | 2,002,036 | ||||||||||||

| AgEq ounces payable (2) (3) | 499,644 | 408,899 | 1,501,354 | 1,823,005 | ||||||||||||

| Production cost per tonne (5) | $ | 252 | $ | 286 | $ | 299 | $ | 300 | ||||||||

| Total cash cost per silver ounce payable | $ | 12.73 | $ | 14.36 | $ | 15.38 | $ | 13.01 | ||||||||

| AISC per silver ounce payable | $ | 21.19 | $ | 26.76 | $ | 26.46 | $ | 23.57 | ||||||||

| 7 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

| (1) | Period deliveries remain subject to assay and price adjustments on final settlement with concentrate purchaser(s). Data has been adjusted to reflect final assay and price adjustments for prior period deliveries settled during the period. Tonnes Mined and Ore processed are in DMT. | |

| (2) | AgEq ounces established using average realized metal prices during the period indicated applied to the recovered metal content of the concentrates to reflect the revenue contribution of base metal sales during the period. | |

| (3) | Payable metal is based on the metals delivered and sold during the period, net of payable deductions under the Company’s offtake arrangements, and will therefore differ from produced ounces. | |

| (4) | Average realized price is calculated on current period sale deliveries and does not include the impact of prior period provisional adjustments in the period. | |

| (5) | Production cost per tonne includes mining and milling costs, excluding depletion and amortization and inventory adjustments. |

Operational Highlights

| ● | Q4 2020 Production (compared to Q4 2019) |

| ○ | Silver production increased by 37% to 355,581 oz (Q4 2019 – 259,282 oz), exceeding Q3 2020 as the strongest quarter of silver production since Q2 2014 | |

| ○ | Silver-equivalent (“AgEq”) production increased by 18% to 556,332 AgEq oz (Q4 2019 – 469,707 AgEq oz), while sales increased by 22% to 499,644 AgEq oz (Q4 2019 – 408,899 AgEq oz) | |

| ○ | Total cash cost net of by-products per silver ounce payable decreased by 11% to $12.73 (Q4 2019 – $14.36) | |

| ○ | AISC per silver ounce payable decreased by 21% to $21.19 (Q4 2019 – $26.76) | |

| ○ | Production cost per tonne decreased by 12% to $252 per tonne (Q4 2019 – $286 per tonne) |

| ● | Record production in the second half (“H2”) of 2020 (compared to H2 2019) including: |

| ○ | Tonnes mined (43,332) and milled (45,237) from Platosa following restart in late Q2 2020 | |

| ○ | AgEq production increased by 20% to 1,080,644 oz (H2 2019 – 896,838 AgEq oz) | |

| ○ | Production cost per tonne decreased by 23% to $239 per tonne (H2 2019 – $311 per tonne) |

| 8 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

| ● | 2020 Production (compared to 2019) |

| ○ | AgEq production decreased by 18% to 1.6 million oz (2019 – 2.0 million AgEq oz) | |

| ○ | AgEq ounces payable sold decreased by 18% to 1.5 AgEq ozs (2019 – 1.8 AgEq ozs) | |

| ○ | Total cash cost net of by-products per silver ounce payable rose by 18% to $15.38 (2019 – $13.01) | |

| ○ | AISC per silver ounce payable increased by 12% to $26.46 (2019 – $23.57) | |

| ○ | Production cost per tonne decreased by $1 per tonne to $299 per tonne (2019 – $300 per tonne) |

Operations Commentary

Production levels from Platosa recovered fully in H2 2020 following the Suspension. The mine achieved record quarterly tonnes mined in Q3 2020, and record tonnes mined and milled in the second half of 2020, while maintaining safe and cost-effective practices.

The Miguel Auza Mill performed well throughout 2020 and continues to deliver strong and improving recoveries.

During this period, the Company realized savings related to the measures implemented during the Suspension including:

| ○ | reducing the workforce by approximately 35% (20% reduction in labour costs) – labour accounts for approximately 30% of operational expenditures; | |

| ○ | improving the terms of treatment charges for zinc, due to improvements in the global market for zinc concentrates; | |

| ○ | modifying mining methods to increase efficiency and safety, while reducing costs, among other operational improvements; and | |

| ○ | modifying shift schedules to improve workforce utilization. |

In addition, in early Q4 2020, the Company finalized the transition to a private natural gas-powered electricity supplier for the Platosa Mine, as a result electricity costs were significantly lower on a per-unit basis in Q4 2020.

During the Suspension, the Company shut down mining activities at its Platosa Mine and processing at its Miguel Auza Mill, while maintaining critical pumping and routine maintenance of critical infrastructure. The Company began ramp-up of operations in mid-June, following the implementation of new safety protocols. The Company continues to closely monitor the workforce and employees with risk factors for severe COVID-19 illness are removed from the workplace. COVID-19 management does not have a significant impact on operations at the current time.

| 9 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

The previous eight quarters of production at Platosa are summarized below:

| 10 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

Analysis of the components of mine operating results is as follows:

| Q4 | Year ended December 31, | |||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| Ore processed | 22,626 | 19,828 | 65,567 | 75,247 | ||||||||||||

Production in Q4 2020 was 22,626 tonnes, a 14% improvement over the same quarter in 2019 and driven by reduced downtime for the mill and more efficient and consistent mine production. The twelve-month period was affected by the Suspension.

| Head grades | Ag (g/t) | 536 | 435 | 519 | 497 | |||||||||||||

| Pb (%) | 5.42 | 4.84 | 5.37 | 4.82 | ||||||||||||||

| Zn (%) | 6.12 | 6.39 | 6.57 | 6.93 |

Silver grades in Q4 2020 were 23% above Q4 2019 through improved mine planning combined with geotechnical and dilution control measures. The production feed included higher lead production by 12% and lower zinc production by 4% in Q4 2020 compared to Q4 2019.

Overall, the mine plan and execution resulted in an increase of 4% and 11% in silver and lead grades, respectively, and a decrease of 5% in zinc grades in 2020 as compared to 2019.

| Recoveries | Ag (%) | 91.2 | 91.7 | 91.4 | 89.9 | |||||||||||||||

| Pb (%) | 82.9 | 80.2 | 83.7 | 79.2 | ||||||||||||||||

| Zn (%) | 80.1 | 76.5 | 78.9 | 77.7 |

Optimization initiatives at the flotation circuit focussed on the reduction of zinc concentrate hydrophobicity in the thickeners, by decreasing the froth addition. Grade Variability impacted recovery near the start of the year. The Company later introduced a blending strategy to improve feed consistency and recovery. The operation also identified certain negative impacts to recovery from lead oxides. Maintaining a lead oxide/sulphide ratio below 10% improved recoveries of silver and lead and resulted in higher recovery and concentrate quality. As a net result:

| ● | Silver recoveries slightly decreased by 1% in Q4 2020 relative to Q4 2019. |

| ● | Lead and zinc recoveries increased by 3% and 5%, respectively, over the same period. |

| ● | Overall recoveries in 2020 for silver, lead, and zinc increased by 2%, 6%, and 2% respectively as compared to 2019 due to modifications and improvements made to the mill flotation circuits early in 2020, and better management of the thickening process and reagent use. |

| Ag (oz) | 355,581 | 259,282 | 997,690 | 1,054,029 | ||||||||||||||

| Metal Production | Pb (lb) | 2,223,465 | 1,690,610 | 6,470,637 | 6,134,888 | |||||||||||||

| Zn (lb) | 2,452,728 | 2,062,018 | 7,488,825 | 8,425,221 | ||||||||||||||

| AgEq (oz) | 556,332 | 469,707 | 1,639,310 | 2,002,036 |

Silver, lead, and zinc production increased by 37%, 32%, and 19% respectively in Q4 2020 over the prior-year quarter driven by near-record mined tonnes from Platosa and significant improvements in metal recoveries.

The Suspension resulted in lower AgEq production for the year ended December 31, 2020 compared to 2019.

| 11 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

EXPLORATION AND EVALUATION REVIEW

Platosa Property

In Q4 2020, the Company continued exploration on the Platosa project. At Jaboncillo, the Company is following up on drilling completed in 2019 that intersected multiple gossanous horizons with pyritic breccias, arsenopyrite and relict base-metal sulphides. Petrographic studies conducted in Q2 2020 confirmed the presence of base-metal sulphide species including sphalerite and galena. These observations confirm that the system is productive for base metal sulphides on multiple structures over an approximate strike length of one kilometre. In Q3 2020 drilling resumed in this area targeting an economically significant component to the system.

Drilling at PDN commenced in Q4 2020, targeting areas where intense dolomitization and sanding along structures was intersected in preliminary drill holes, indicating the movement of hydrothermal fluids that are believed to be the expression of a potential skarn system at depth. This potential for a skarn body at PDN has been defined through IP, magnetics and gravity surveys.

During early Q1 2020, the Company commenced an underground drill program focused on further defining and expanding the Pierna, Rodilla and NE-1 mantos. The program was paused during the Suspension and recommenced in Q3 2020.

Highlights on the Platosa Project for Q4 2020 included:

| ● | Underground drilling to define and delineate additional mineralization near mine infrastructure; | |

| ● | Identification of a zone of vertical mineralization (the Gap Zone) in NE-1 and NE-1S mantos inadequately tested with vertical holes drilled from surface; and | |

| ● | Drilling near Platosa, commenced drilling at PDN and mobilized an additional surface drill rig to start drilling at Jaboncillo |

Evolución Project

The Company commenced a proof-of-concept drilling program on Evolución during Q2 2018, targeting four priority targets believed to be indicative of the distal part of a larger epithermal system. The Company increased the drilling program to 6,000 metres based on initial success on the Lechuzas structure. Drilling in Q4 2018 and into Q1 2019 tested strike and dip extensions of the mineralization encountered at Lechuzas with the purpose of tracking higher grades and more robust widths. During Q1 2019, the Company announced results from the Lechuzas structure, which defined a mineralized envelope of 600 metres along strike and 500 metres down dip. This envelope was extended by a further 250 metres along strike through 2019 and into Q1 2020 and remains open in multiple directions. As part of this drilling program, re-assaying of samples from the Calvario vein and re-modelling of the region were undertaken. The Company has incorporated this work into an updated mineral resource estimate and associated technical report.

| 12 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

Exploration activities were limited through Q3 2020 due to COVID-19, but field work resumed in Q4 2020, including detailed mapping and prospecting on numerous regional targets throughout the Evolución concession.

In Q3 2020, the Company completed a MRE for the Calvario and Lechuzas Zones on the Evolución Project. The updated MRE incorporates 17,120 metres of additional surface drilling completed in the resource area from June 2018 to December 31, 2019. Highlights of the MRE include:

| ● | Updated MRE incorporates 17,120 metres of additional surface drilling completed in the resource area from June 2018 to December 31, 2019; | |

| ● | Indicated resource of 6,407,000 tonnes at 170 g/t Ageq representing 35,091,000 AgEq ounces; | |

| ● | Inferred resource of 14,960,000 tonnes at 135 g/t AgEq representing 64,813,000 AgEq ounces; and | |

| ● | Expansion drilling being planned to test the strike extension of the mineralized zones and follow up on parallel structures, where grab samples taken during detailed mapping in 2020 returned values of up to 2.30 g/t gold, 203 g/t silver and 10.4% lead. |

On October 30, 2020 the Company announced the filing on SEDAR (www.sedar.com) of a technical report on the Evolución Project by SRK Consulting (Canada) Inc. under National Instrument 43-101 (“NI 43-101”).

Approximately 12% of the tonnage within the MRE (26% of the indicated tonnage and 6% of the inferred tonnage) is located within the La Antigua concession (part of the Evolución Project), which is the subject of litigation between a subsidiary of Excellon and a plaintiff. The initial decision in respect of this litigation does not affect Excellon’s contractual rights to this concession.

The MRE was prepared in accordance with the Canadian Institute of Mining, Metallurgy and Petroleum’s (CIM) “Mineral Resources and Mineral Reserves Best Practices” guidelines (November 2019) and is classified per the CIM “Definition Standards for Mineral Resources and Mineral Reserves” (May 2014).

Silver City Project

In Q3 2019, the Company entered into an agreement (the “Globex Agreement”) with Globex Mining Enterprises Inc. (“Globex”) for an option to acquire a 100% interest in the Bräunsdorf exploration license for the Silver City Project. The Silver City Project (Bräunsdorf exploration license) is a 164 km2 silver district in Saxony, Germany and encompasses a 36-km long epithermal vein system situated west of the city of Freiberg (30 km southwest of Dresden). The immediate exploration license and surrounding area have a long and rich history of silver mining dating back to the 12th century with numerous historic mine camps, small mines and prospects, many of which have only been explored and/or mined to shallow depths, seldom exceeding 200 metres below surface. Historically reported veins ranged from 0.5 to 10 metres width, with grades of over 3,500 g/t silver and no assaying for either gold or zinc, which were not historically available.

From late 2019 into early 2020 the project continued to advance, with an induced polarization (“IP”) survey completed over two targets on the northern part of the license. Three lines were completed over the Munzig target, an area of historical high-grade production, with records indicating veins from 2 to 10 metres wide grading up to 1,000 g/t Ag. Two lines were completed over the Steinberg target, which followed up on surface sampling that contained anomalous silver, arsenic and lead. High-resistivity and chargeability anomalies were detected at both targets and defined within prospective settings that were included for testing as part of initial drilling which commenced in Q3 2020.

| 13 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

Fluid inclusion studies completed in 2019 by the University of Freiberg on samples from historical mine workings covered a strike length of approximately 15 km of the main vein system. These studies confirmed systematic vertical mineral zonation within the larger epithermal system and an expected vertical extent of the productive zones between 300-400 metres. Compilation of historical reports, maps and images from the Freiberg archives have allowed the Company to model historically mined areas, providing more detailed information on targets ahead of drilling. In Q1 2020 permitting documentation was submitted to regulators and the drilling permit was received during Q2 2020.

The Company commenced drill testing of initial targets in Q3 2020 and completed 3,684 metres of diamond drilling at five targets. The Company continued to engage with local land and business owners to secure access to properties for drilling and regional exploration, and provided presentations on the mining life cycle and updates on the Company’s activities in the areas. A collaborative R&D 2D passive seismic survey at Munzig was completed by Sisprobe and the Company received a Mineral Liberation Analysis report identifying the silver species carrying mineralization and the presence of native silver.

Refer to drilling results from the Silver City Project discussed in the 2020 Highlights section, above, under Exploration Activities.

In Q4 2020, the Company began work on the DOP to secure drilling permits for the 2021 drilling program, and planning of the 2021 exploration program including target generation, logistics, discussions and negotiations with contractors for drilling, consulting, and geophysics services.

The Company holds the option to earn a 100% interest in the Silver City Project by meeting the following obligations under the Globex Agreement:

| (i) | Pay C$100,000 and issue 226,837 common shares to Globex (completed September 23, 2019); | |

| (ii) | Pay C$100,000 and issue common shares to Globex equivalent to C$325,000 based on the 5-day volume weighted average price (“VWAP”) on or before September 23, 2020 (completed September 21, 2020); | |

| (iii) | Pay C$100,000 and issue common shares to Globex equivalent to C$425,000 based on the 5-day VWAP on or before September 23, 2021; | |

| (iv) | Pay C$200,000 and issue common shares to Globex equivalent to C$625,000 based on the 5-day VWAP on or before September 23, 2022; and | |

| (v) | Upon completion of the payments and issuances set out above, grant Globex a gross metals royalty on the exploration or production license on the Silver City Project of 3.0% for precious metals and 2.5% for other metals, which may be reduced to 2% and 1.5%, respectively, upon a payment of US$1,500,000. |

The total value of cash and shares over the three-year term is C$500,000 and C$1.6 million, respectively. The Company may accelerate any of the payments, issuances or the royalty grant at any time during the term of the option. Additionally, the Company may terminate the option at any time provided that the work commitments under the exploration license in respect of the first year of the option have been satisfied.

| 14 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

In addition, the Company has agreed to make: (i) a one-time payment of C$300,000 following the announcement of a maiden resource on the Silver City Project and (ii) a one-time payment of C$700,000 upon the achievement of commercial production from the Silver City Project.

Kilgore Project

The Company aims to better understand the deposit setting on a local and regional scale through: re-logging core to enhance the underlying structural and lithologic framework; improving characterization of host rocks through lithogeochemistry; and sampling and assaying of silver mineralization to potentially improve project economics. The Company also looks forward to continuing regional exploration, prospecting and geophysics to generate new targets and is building a dedicated team to advance this project.

The Company filed an updated Plan of Operations with the USFS in Q2 2020, and the USFS is now in the process of revising the EA accordingly. The Company is informed by the USFS that the process to prepare a Revised EA and DN will be complete by mid-2021. If the DN is received within that timeframe, the Company could commence drilling in Q3 2021. Drilling was originally planned to commence in August 2020. Once approved, the new EA may still be challenged by environmental groups which could result in further delays.

In Q3 2020 the Company completed Aster analysis of the Kilgore project area and regional package; conducted regional mapping, prospecting, and stream sediment sampling of regional target areas and continued the ongoing environmental and baseline surveys and re-logging and sampling of historical core.

In Q4 2020, the Company progressed mapping, prospecting, and stream sediment sampling of regional target areas. Selection and shipment of samples for whole-rock geochemistry analysis, and re-logging and sampling of historical core and digitizing paper logs continued. Work commenced on an updated geological model of the Kilgore deposit and the 2021 drilling program was evaluated.

Oakley Project

In Q3 2020, the Company increased the Oakley Project by approximately 2,500 acres (1,012 hectares) to approximately 7,000 acres (2,833 hectares) through staking of an additional 125 Federal Lode Mining claims on land managed by the Bureau of Land Management (“BLM”) at the Cold Creek, Blue Hill Creek and Matrix Creek Prospects and applying for 960 acres (388 hectares) of Idaho state-managed land as “mineral leases,” adding to the current 320 acres (129.5 hectares) of mineral leases for a total of 1,280 acres (518 hectares). The Company completed soil sampling across the newly staked ground with 1,347 samples sent for gold and multi-element analysis and completed a 1,330 line-kilometer, airborne magnetic survey across the entire project area including the expanded footprint. Detailed geologic mapping was completed over the Cold Creek Prospect and 20,200 line-meters of ground IP and resistivity survey and a LIDAR (Light Detection and Ranging) survey was completed.

In Q4 2020, the Company completed planning and continued permitting of the 2021 drilling program, and the additional ground IP and resistivity survey lines.

The Oakley Project has been optioned to Centerra pursuant to an option agreement (the “Oakley Agreement”) date February 26, 2020 pursuant to which Centerra can earn up to a 70% interest in exchange for total exploration expenditures of $7 million and cash payments to the Company of $550,000 over a six-year period. Specific terms of the Oakley Agreement include:

| 15 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

| (i) | Centerra can earn a 51% interest in Oakley (the “First Option”) by incurring $4.5 million in exploration expenditures and by making cash payments of $250,000 over a three-year period as follows: |

| a. | Cash payment of $75,000 (complete) on signing and commitment to spend a minimum of $500,000 on exploration expenditures in Year One; | |

| b. | Cash payment of $75,000 (received in February 2021) and $1.5 million in exploration expenditures in Year Two; and | |

| c. | Cash payment of $100,000 and $2.5 million in exploration expenditures in Year Three. |

| (ii) | Centerra then has an option to acquire a further 19% of the Oakley Project, for a total of 70% (the “Second Option”), by incurring an additional $3 million in exploration expenditures and making a cash payment of $300,000 over three years. |

During the term of the Oakley Agreement, Centerra will be the operator of the project. The Company will act as project manager and will be paid 10% of the approved exploration expenditures for technical oversight and project management.

Subsequent to either the First Option or the Second Option, at Centerra’s option, the parties shall form a joint venture and fund expenditures going forward on a pro rata basis.

Should the Company’s interest fall below 10% during the joint venture, that interest will automatically convert to a 2% net smelter return royalty which is not subject to a buyback provision.

Beschefer Option to Wallbridge Mining Company Limited

In October 2018, a wholly-owned subsidiary of the Company entered into an option agreement (the “Beschefer Agreement”) in respect of the Beschefer Project in Quebec with Wallbridge Mining Company Ltd. (“Wallbridge”). Wallbridge agreed to incur an aggregate of $4.5 million in exploration expenditures and issue a total of 7,000,000 common shares of Wallbridge (“Wallbridge Shares”) over three years to earn a 100% interest in the property. On September 21, 2019 the parties amended the original option agreement to increase the total number of shares to 8,000,000 and extend the option period by one year.

The Company received 500,000 Wallbridge Shares upon entering the Beschefer Agreement. In January 2020, a review by Wallbridge of the property status on Beschefer revealed that the claims had lapsed in December 2019 resulting in both Wallbridge and Excellon losing rights to the property. Due to the reorganization of the claims in Quebec to eliminate sub-parcels, some of the claims under the Beschefer Agreement were assigned to contiguous properties upon the lapse of the claims. In Q1 2020, in satisfaction of the Beschefer Agreement, the Company’s subsidiary signed a release and quitclaim on the Beschefer Property and agreed to accept an additional 3,000,000 Wallbridge Shares and 500,000 warrants with an exercise price of $1.00 and a term of five years.

Mineral Resources

The Company’s Mineral Resource Estimates have been prepared in accordance with NI-43-101 and the Canadian Institute of Mining, Metallurgy and Petroleum’s (CIM) ‘Mineral Resources and Mineral Reserves Best Practices’ guidelines (November 2003) and classified per the CIM ‘Definition Standards for Mineral Resources and Mineral Reserves’ (May 2014). The associated technical reports for the Platosa, Evolución, Kilgore and Oakley projects can be found at www.sedar.com under the profiles for Excellon (in respect of Platosa and Evolución) and Otis (in respect of Kilgore and Oakley). The technical reports for each of the projects are also available on the Company’s website at www.excellonresources.com.

| 16 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

Further, for additional discussion of the Company’s mineral resource estimates and the Company’s other exploration projects, the reader should refer to the Company’s AIF for the year ended December 31, 2019 and the Company’s AIF for the year ended December 31, 2020, which will be filed on SEDAR on or about March 31, 2021, both of which is or will be available on the Company’s website www.excellonresources.com and on www.sedar.com.

QUALIFIED PERSONS

Mr. Ben Pullinger, B.Sc., P.Geo., Excellon’s Senior Vice President Geology & Corporate Development and a Qualified Person, as defined in NI 43-101, has reviewed and approved the scientific and technical information relating to geological interpretation and results contained in this MD&A. Paul Keller, P. Eng., Excellon’s Chief Operating Officer and a Qualified Person, as defined in NI 43-101, has reviewed and approved the scientific and technical information relating to production results contained in this MD&A.

CORPORATE RESPONSIBILITY REVIEW

In Q4 2020, the Company maintained its focus on ensuring that its COVID-19 prevention and response measures continued to be followed and that they worked effectively. Management at business units and exploration projects have done an excellent job implementing our protocols and continue to emphasize the same measures in the communities surrounding our operations. Since the Suspension, the Company’s operations have not been materially affected by the pandemic. Refer to “Business Environment and Risks – COVID-19 Risk – Public Health Crisis due to Pandemic Diseases” below.

CR Performance at Platosa and Miguel Auza

Management continues to evaluate and monitor compliance with legal requirements and manage CR risk and the Company’s operations continue to report on the key trailing CR performance indicators and elements of the Visible Felt Leadership process. Trailing safety performance through December 31, 2020, as measured by recordable injury frequency (RIF) and lost time injury frequency (LTIF) improved 31 percent and 21 percent, respectively, from 2019. Injury severity declined by 15 percent in 2020 compared to 2019.

Work is underway on the Company’s Corporate Responsibility Report and will cover the 2019 and 2020 periods, following delays due to the Suspension.

There were no significant environmental incidents reported at either Platosa or Miguel Auza during Q4 2020. The Company continued engagement with a range of stakeholders surrounding the Platosa and Miguel Auza business units. There were no community-related grievances reported during Q4 2020.

The Company has continued discussions with the Comisión Nacional del Agua (“CONAGUA”), the federal water regulatory agency in Mexico, regarding the management of water that the Company pumps from the Platosa mine. The Company is committed to evaluating with CONAGUA how best to manage such water going forward, to support Platosa’s operations and deliver a sustainable benefit to the residents of the surrounding Mapimí region. Water management is critical for the Platosa operation and though the Company does not currently foresee any material changes to water management, such changes could impact mining operations in the future.

| 17 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

Tailings Management at Miguel Auza

There are two tailings management facilities (“TMF”) at Miguel Auza. TMF #1 is located immediately northwest of the concentrator and has been decommissioned, rehabilitated with a soil cover and re-vegetated. TMF #2 is located on land owned by Excellon approximately one kilometre north of the Miguel Auza concentrator. Approval for the construction and operation of the facility was received on January 31, 2017. Construction of the stage-2 raise for TMF #2 was completed in early Q4 2020.

Corporate, operations and consulting engineers progressed the development of an operations, maintenance and surveillance manual (“OMS Manual”) aligned with guidelines of the Mining Association of Canada. The final version of the OMS Manual was delivered in early Q2 2020 and the Company continues to implement the requirements of the OMS Manual.

Summary of Annual Financial Results

Annual financial statement highlights for the previous three years are as follows:

| (in $000’s) | 2020 | 2019 | 2018 | |||||||||

| Revenues | 26,202 | 26,469 | 24,313 | |||||||||

| Production costs | (19,981 | ) | (23,216 | ) | (19,566 | ) | ||||||

| Depletion and amortization | (4,649 | ) | (4,708 | ) | (4,016 | ) | ||||||

| Cost of sales | (24,630 | ) | (27,924 | ) | (23,582 | ) | ||||||

| Gross profit (loss) | 1,572 | (1,455 | ) | 731 | ||||||||

| Expenses: | ||||||||||||

| Corporate administration | (6,896 | ) | (4,822 | ) | (4,521 | ) | ||||||

| Exploration | (4,032 | ) | (3,853 | ) | (3,897 | ) | ||||||

| Other (expense) income | (373 | ) | 782 | 4 | ||||||||

| Finance (expense) income | (2,508 | ) | 295 | 1,899 | ||||||||

| Income tax expense | (3,783 | ) | (1,022 | ) | (1,916 | ) | ||||||

| Net loss for the year | (16,020 | ) | (10,075 | ) | (7,700 | ) | ||||||

| Loss per share – basic and diluted | (0.55 | ) | (0.49 | ) | (0.40 | ) | ||||||

| Operating cash flows before changes in working capital | (3,733 | ) | (4,314 | ) | (2,908 | ) | ||||||

| Total assets | 73,279 | 55,582 | 50,155 | |||||||||

| Total liabilities | 22,837 | 13,390 | 9,978 | |||||||||

| Total equity | 50,442 | 42,192 | 40,177 | |||||||||

| Non-current liabilities | 10,845 | 3,842 | 2,479 | |||||||||

| 18 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

Summary of Quarterly Financial Results

Financial statement highlights for the quarter ended December 31, 2020 and 2019 and the last eight quarters are as follows:

Q4 2020 | Q3 2020 | Q2 2020 | Q1 2020 | Q4 2019 | Q3 2019 | Q2 2019 | Q1 2019 | |||||||||||||||||||||||||

| (in $000’s) | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||

| Revenues | 9,029 | 9,667 | 891 | 6,615 | 6,414 | 6,203 | 8,674 | 5,179 | ||||||||||||||||||||||||

| Production costs | (5,986 | ) | (5,875 | ) | (2,641 | ) | (5,479 | ) | (5,757 | ) | (6,050 | ) | (6,797 | ) | (4,612 | ) | ||||||||||||||||

| Depletion and amortization | (1,445 | ) | (1,269 | ) | (666 | ) | (1,269 | ) | (1,250 | ) | (1,140 | ) | (1,149 | ) | (1,169 | ) | ||||||||||||||||

| Cost of sales | (7,431 | ) | (7,144 | ) | (3,307 | ) | (6,748 | ) | (7,007 | ) | (7,190 | ) | (7,946 | ) | (5,781 | ) | ||||||||||||||||

| Gross profit (loss) | 1,598 | 2,523 | (2,416 | ) | (133 | ) | (593 | ) | (987 | ) | 728 | (602 | ) | |||||||||||||||||||

| Expenses: | ||||||||||||||||||||||||||||||||

| General and administrative | (1,886 | ) | (1,502 | ) | (2,345 | ) | (1,163 | ) | (1,282 | ) | (1,151 | ) | (1,028 | ) | (1,361 | ) | ||||||||||||||||

| Exploration | (1,400 | ) | (2,001 | ) | (258 | ) | (373 | ) | (1,023 | ) | (858 | ) | (967 | ) | (1,005 | ) | ||||||||||||||||

| Other income (expense) | 1,062 | (744 | ) | 968 | (1,659 | ) | 1,222 | (200 | ) | 34 | (274 | ) | ||||||||||||||||||||

| Net finance (expense) income | (679 | ) | (292 | ) | 554 | (2,091 | ) | 753 | (71 | ) | (335 | ) | (52 | ) | ||||||||||||||||||

| Income tax (expense) recovery | (4,703 | ) | 1,776 | 97 | (953 | ) | (258 | ) | 365 | (640 | ) | (491 | ) | |||||||||||||||||||

| Net loss | (6,008 | ) | (240 | ) | (3,400 | ) | (6,372 | ) | (1,181 | ) | (2,903 | ) | (2,208 | ) | (3,785 | ) | ||||||||||||||||

| Loss per share | (0.19 | ) | (0.01 | ) | (0.12 | ) | (0.28 | ) | (0.05 | ) | (0.14 | ) | (0.11 | ) | (0.19 | ) | ||||||||||||||||

| Net cash from operations before changes in working capital | 2,529 | (166 | ) | (4,318 | ) | (1,778 | ) | (1,707 | ) | (1,658 | ) | 208 | (977 | ) | ||||||||||||||||||

Quarter to quarter revenue variances are a function of metal prices, costs and production results. Production results can differ from period to period depending on geology, mining conditions, labour, and equipment availability. These in turn affect mined tonnages, grades and mill recoveries and ultimately the quantity of metal produced and revenues received. The Company currently expenses exploration costs, specifically exploration costs related to Silver City, Kilgore, Evolución and Platosa (unless associated with resource expansion). These exploration costs do not relate to the mining operation and vary from period to period creating volatility in earnings. The following is a discussion of the material variances between Q4 2020 and Q4 2019 and the year ended December 31, 2020 versus the year ended December 31, 2019.

| 19 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

| Q4 | Twelve months ended December 31, | |||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| Revenue | 9,029 | 6,414 | 26,202 | 26,469 | ||||||||||||

| Gross profit (loss) | 1,598 | (593 | ) | 1,572 | (1,455 | ) | ||||||||||

| Net Loss | (6,008 | ) | (1,181 | ) | (16,020 | ) | (10,075 | ) | ||||||||

Revenues increased by 41% during Q4 2020, driven by a 39% increase in silver ounces payable and a 43% increase in the average realized silver price relative to the comparative period. Revenues for the 12-month period were impacted by the Suspension. Also refer to “Provisionally Priced Sales” below.

Gross profit improved to $1.6 million in Q4 2020 driven by increased revenues, while gross profit for the 12-month period was $1.6 million despite the Suspension in Q2 2020.

Net loss increased by $4.8 million between Q4 2020 and Q4 2019 mainly reflecting a $4.7 million non-cash charge in deferred tax expense, due to the de-recognition of deferred-tax assets. Yearly net loss in 2020 increased by $5.9 million compared to 2019 mainly reflecting a $3.8 million non-cash charge in deferred tax expense and a $2.8 million increase in net finance expenses including $2.0 million in interest expense on the convertible debentures and the Sprott Credit Facility.

| Cost of Sales | (7,431 | ) | (7,007 | ) | (24,630 | ) | (27,924 | ) |

Cost of sales in Q4 2020 is $0.4 million higher than Q4 2019 reflecting the volume impact of a 22% increase in silver-equivalent ounces sold in Q4 2020 partially offset by the impact of operational efficiencies realized through 2020 including lower personnel costs and a lower-cost private electricity contract that came into effect in early Q4 2020. Yearly cost of sales decreased by $3.3 million or 12% in 2020 versus 2019 reflecting a 18% reduction in AgEq ounces sold due to the Suspension, partly offset by care and maintenance costs incurred ($1.9 million) during the Suspension.

| Exploration | (1,400 | ) | (1,023 | ) | (4,032 | ) | (3,853 | ) |

Higher exploration expense in Q4 2020, by $0.4 million above the prior-year quarter, primarily reflects increased exploration activity at the Silver City Project and Platosa Mine.

| Other (expenses) income | 1,062 | 1,222 | (373 | ) | 782 |

Other expenses include realized and unrealized foreign exchange gains and losses, unrealized gains and losses on marketable securities and warrants, interest income and other non-routine income or expenses, if any.

Other expenses are consistent with the previous quarter. The 12-month variance of $1.2 million between 2020 and 2019 is driven by unrealized foreign exchange losses, loss on disposal of the Beschefer project, discount on the shares for debt issued during the year, partly offset by the unrealized gain on marketable securities and warrants.

| Finance (expenses) income | (679 | ) | 753 | (2,508 | ) | 295 |

| 20 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

Net finance expenses consist primarily of interest on the Convertible Debentures and the Sprott Credit Facility, mark-to-market of currency hedges and accretion of the rehabilitation provision for the mine and mill.

The 12-month variances are mainly driven by higher interest expense on the convertible debentures and interest on the Sprott Credit Facility ($2.0 million), and unrealized loss from MXN/USD currency hedges for $0.5 million.

Provisionally Priced Sales

Sales are recorded using the metal price received for sales that settle during the reporting period. For sales that have not been settled, an estimate is used, based on the expected month of settlement and the forward price of the metal at the end of the reporting period. The difference between the estimate and the final price received is recognized by adjusting sales in the period in which the sale is settled (i.e. finalization adjustment). The finalization adjustment recorded for these sales depends on the actual price when the sale settles, which occurs in either the first, second or third month after shipment under the terms of the current concentrate purchase agreements.

Invoiced revenues are derived from the value of metal content adjusted for treatment and refining charges incurred by the metallurgical complex of the customer. The terms agreed under the zinc and lead concentrate purchase agreements include price participation for settlement at metal prices above specified levels. The value of the metal content of the products sold, before treatment and refining charges, is as follows (in thousands of US dollars):

| Three months ended | Twelve months ended | |||||||||||||||

| December 31 | December 31 | December 31 | December 31 | |||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| $ | $ | $ | $ | |||||||||||||

| Silver | 7,390 | 3,822 | 20,625 | 15,428 | ||||||||||||

| Lead | 1,605 | 1,326 | 5,022 | 5,046 | ||||||||||||

| Zinc | 2,318 | 1,652 | 6,899 | 8,331 | ||||||||||||

| Value of metal content in products sold (1) | 11,313 | 6,800 | 32,546 | 28,805 | ||||||||||||

| Adjustment for treatment and refining charges (TC/RC) | (2,284 | ) | (798 | ) | (6,840 | ) | (3,256 | ) | ||||||||

| Revenues from concentrate sales | 9,029 | 6,002 | 25,706 | 25,549 | ||||||||||||

| Revenues from toll milling services | - | 412 | 496 | 920 | ||||||||||||

| Total revenues | 9,029 | 6,414 | 26,202 | 26,469 | ||||||||||||

Production Cost Per Tonne, Total Cash Cost Net of By-Product Credits Per Silver Ounce Payable and All-In Sustaining Cost (AISC) Per Silver Ounce Payable are non-IFRS measures that do not have a standardized meaning. The calculation of these measures may differ from that used by other companies in the industry. The Company uses these measures internally to evaluate the underlying operating performance of the Company for the reporting periods presented. These measures should not be considered in isolation or as a substitute for measures of performance prepared in accordance with generally accepted accounting principles and are not necessarily indicative of operating expenses as determined under generally accepted accounting principles. Management believes that these measures are key performance indicators of the Company’s operational efficiency and are increasingly used across the global mining industry and are intended to provide investors with information about the cash generating capabilities of the Company’s operations.

(1) Value of metal content in products sold is a non-IFRS measure.

| 21 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

Due to the Suspension, the Company does not consider the Non-IFRS measures for year ended December 31, 2020 stated below to be representative of the Company’s business and normal operations, as the care-and-maintenance costs associated with the Suspension were not matched by any material amount of revenue or payable metals, unlike in previous quarters.

| Q4 | Twelve months ended December 31, | |||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| Production cost per Tonne | $ | 252 | $ | 286 | $ | 299 | $ | 300 | ||||||||

The Company excludes inventory adjustments from the calculation of Production Cost per Tonne to improve period-over-period comparisons. A reconciliation between production cost per tonne (excluding depletion and amortization and inventory adjustments) and the Company’s cost of sales as reported in the Company’s financial statements is provided below.

| $ 000’s | $ 000’s | $ 000’s | $ 000’s | |||||||||||||

| Cost of Sales | 7,431 | 7,007 | 24,630 | 27,924 | ||||||||||||

| Adjustments – increase/(decrease): | ||||||||||||||||

| San Sebastián processing cost (Hecla bulk sample) | - | (222 | ) | (234 | ) | (482 | ) | |||||||||

| Depletion and amortization | (1,445 | ) | (1,250 | ) | (4,649 | ) | (4,708 | ) | ||||||||

| Inventory adjustments | (288 | ) | 142 | (143 | ) | (193 | ) | |||||||||

| Production Costs (excluding inventory adjustments) | 5,698 | 5,677 | 19,604 | 22,541 | ||||||||||||

| Tonnes milled | 22,626 | 19,828 | 65,567 | 75,247 | ||||||||||||

| Production cost per tonne milled ($/tonne) | 252 | 286 | 299 | 300 | ||||||||||||

The 12% decrease in cost per tonne milled in Q4 2020 versus the prior year mainly reflects the volume impact of a 14% increase in tonnes milled relative to the comparative period, partially offset by higher dewatering costs and associated higher electricity usage. On a full-year basis, in 2020 costs per tonne milled are in line with 2019 comparative costs as both production costs and tonnes milled in 2020 reflect the Suspension. After adjusting for $1.9 million in care and maintenance costs incurred during the Suspension, the annual production cost per tonne milled is $269 or a 10 % decrease compared to 2019, mainly reflecting the reduced headcount and private electricity contract entered into during the year.

| Q4 | Twelve months ended December 31, | |||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| Total cash cost per silver ounce payable | $ | 12.73 | $ | 14.36 | $ | 15.38 | $ | 13.01 | ||||||||

The calculation of total cash cost per silver ounce payable reflects the cost of production adjusted for by-product and various non-cash costs included in cost of sales. Changes in inventory have not been adjusted from cost of sales, as these costs are associated with the payable silver ounces sold in the period. The Company expects total cash costs net of by-product revenues to vary from period to period as planned production and underground development access different areas of the mine with varying ore grades and characteristics.

| 22 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

Following is a reconciliation of total cash cost per silver ounce payable, net of by-product credits to cost of sales as reported in the Company’s financial statements:

| Q4 | Twelve months ended December 31, | |||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| $ 000’s | $ 000’s | $ 000’s | $ 000’s | |||||||||||||

| Cost of sales | 7,431 | 7,007 | 24,630 | 27,924 | ||||||||||||

| Adjustments - increase/(decrease): | ||||||||||||||||

| San Sebastián processing cost (Hecla bulk sample) | - | (222 | ) | (234 | ) | (482 | ) | |||||||||

| Depletion and amortization | (1,445 | ) | (1,250 | ) | (4,649 | ) | (4,708 | ) | ||||||||

| Third party smelting and refining charges (1) | 2,285 | 798 | 6,840 | 3,256 | ||||||||||||

| Royalties (2) | (235 | ) | (22 | ) | (388 | ) | (90 | ) | ||||||||

| By-product credits (3) | (3,924 | ) | (2,978 | ) | (11,922 | ) | (13,376 | ) | ||||||||

| Total cash cost net of by-product credits | 4,112 | 3,333 | 14,277 | 12,524 | ||||||||||||

| Silver ounces payable | 323,139 | 232,034 | 928,240 | 962,355 | ||||||||||||

| Total cash cost per silver ounce payable ($/oz) | 12.73 | 14.36 | 15.38 | 13.01 | ||||||||||||

| (1) | Treatment and refining charges recorded in net revenues as is industry standard and added back here to derive total costs. |

| (2) | Advance royalty payments on the Miguel Auza property unrelated to production from Platosa. |

| (3) | By-product credits comprise revenues from sales of lead and zinc. |

Silver production in Q4 2020 was 39% above Q4 2019; however, this improved production generated concentrates that attracted higher treatment and refining charges (“TC/RCs”), which are netted from sales revenues and increased by $1.4 million or by 175% in Q4 2020 relative to Q4 2019. The increased TC/RCs were in line with charges in the global zinc and lead concentrate industry, which saw a marked increase in TC/RCs starting in 2019 and continued into 2020. Q4 2020 TC/RCs were pursuant to a renegotiated offtake agreement in respect of zinc concentrate, which delivered lower charges, but the operation incurred higher penalties for deleterious elements, particularly antimony, during the period. The Company plans to mitigate these penalties through increased ore blending in the future and has negotiated improved lead-concentrate terms for 2021. After adjusting for $1.9 million in care and maintenance costs incurred during the Suspension, the annual total cash cost per silver ounce payable is $13.22, or a 2% increase compared to 2019, despite an over 200% increase in TC/RCs during the year.

| Q4 | Twelve months ended December 31, | |||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| AISC Per Silver Ounce Payable (including non-cash items) | $ | 21.19 | $ | 26.76 | $ | 26.46 | $ | 23.57 | ||||||||

Excellon adopted the AISC measure to provide further transparency on the costs associated with producing silver and to assist stakeholders of the Company in assessing operating performance, its ability to generate free cash flow from current operations and overall value. The AISC measure is a non-IFRS measure based on guidance announced by the World Gold Council in June 2013.

| 23 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

Excellon defines AISC per silver ounce payable as the sum of total cash costs (including treatment charges and net of by-product credits), capital expenditures that are sustaining in nature, corporate general and administrative costs (including non-cash share-based compensation), capitalized and expensed exploration that is sustaining in nature, and environmental reclamation costs (non-cash), all divided by the total payable silver ounces sold during the period.

Capital expenditures to develop new operations or capital expenditures related to major projects at existing operations where these projects will materially increase production are classified as non-sustaining and are excluded. The definition of sustaining versus non-sustaining is similarly applied to capitalized and expensed exploration costs. Exploration costs to develop new operations or that relate to major projects at existing operations where these projects are expected to materially increase production are classified as non-sustaining and are excluded.

Costs excluded from AISC are non-sustaining capital expenditures and exploration costs (as described above), finance costs, tax expense, and any items that are deducted for the purposes of adjusted earnings, if any.

The table below presents details of the calculation for AISC per silver ounce payable.

| Q4 | Twelve months ended December 31, | |||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| $ 000’s | $ 000’s | $ 000’s | $ 000’s | |||||||||||||

| Total cash costs net of by-product credits | 4,112 | 3,333 | 14,277 | 12,524 | ||||||||||||

| General and administrative costs (cash) | 1,250 | 1,015 | 4,238 | 3,448 | ||||||||||||

| Share based payments (non-cash) | 294 | 184 | 1,876 | 1,102 | ||||||||||||

| Accretion and amortization of reclamation costs (non-cash) | 50 | (21 | ) | 163 | 150 | |||||||||||

| Sustaining exploration (manto resource exploration/drilling) | 79 | 81 | 259 | 257 | ||||||||||||

| Sustaining capital expenditures (1) | 1,062 | 1,620 | 3,751 | 5,204 | ||||||||||||

| Total sustaining costs | 2,735 | 2,879 | 10,287 | 10,161 | ||||||||||||

| All-in sustaining costs | 6,847 | 6,212 | 24,564 | 22,686 | ||||||||||||

| Silver ounces payable | 323,139 | 232,034 | 928,240 | 962,355 | ||||||||||||

| AISC per silver ounce payable ($/oz) (3) | 21.19 | 26.76 | 26.46 | 23.57 | ||||||||||||

| AISC excluding non-cash items, per silver ounce payable ($/oz) | 20.13 | 26.06 | 24.28 | 22.26 | ||||||||||||

| Realized silver price per ounce sold (2) | 24.46 | 17.12 | 21.59 | 16.07 | ||||||||||||

| (1) | Sustaining capital expenditure includes sustaining property plant and equipment acquisitions and capitalized development costs. | |

| (2) | Average realized silver price is calculated on current period sale deliveries and does not include the impact of prior period provisional adjustments in the period. | |

| (3) | After adjusting for $1.9 million in care and maintenance costs incurred during the Suspension, the 2020 AISC per silver ounce payable is $24.30 or a 3% increase compared to 2019. |

The former corporate secretary of the Company is a partner in a firm that provides legal services to the Company. During 2020, the Company incurred legal services of $50 (2019 – $74). As at December 31, 2020, the Company had a $8 outstanding payable balance due to the firm (as at December 31, 2019 – $nil).

| 24 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

COMMON SHARE DATA AS AT MARCH 16, 2021

| Common shares issued and outstanding | 32,372,114 | |||

| Stock options | 847,437 | |||

| DSUs | 491,330 | |||

| RSUs | 397,593 | |||

| Warrants ($7.00) | 1,092,400 | |||

| Warrants ($3.30) | 302,760 | |||

| Warrants ($5.75) | 1,143,428 | |||

| Fully diluted common shares (1) | 36,647,062 |

| (1) | Conversion of all outstanding Convertible Debentures would result in the issuance of an additional 3,379,245 common shares of the Company. |

LIQUIDITY AND CAPITAL RESOURCES

The primary source of funds available to the Company is cash flow generated by the Platosa Mine and equity and debt financings. The Company has raised equity and debt to fund its exploration program and certain capital and operating expenditures at the mine. A continuous review of the Company’s capital expenditure programs ensures the Company’s capital resources are utilized in a responsible and sustainable manner to conserve cash during periods of low commodity prices and economic and market uncertainty.

| December 31, 2020 | December 31, 2019 | |||||||

| Cash and Cash Equivalents | 8,380 | 6,344 | ||||||

The Company’s cash position increased by $2.0 million in the year ended December 31, 2020 as a result of:

| (i) | $3.7 million used by operations with a $4.0 million improvement in working capital, for a net total of $0.3 million generated by operating activities, after spending $4.0 million on exploration; |

| (ii) | $10.5 million invested in capital expenditures reflecting $8.3 million in dewatering costs, mine development and mining equipment, $0.1 million on the acquisition of mineral rights and $2.0 million on transaction costs and a loan advanced on the acquisition of Otis; and |

| (iii) | Net $12.2 million sourced from financing activities, including $12.8 million from Convertible Debentures and $0.4 million from stock option and warrant exercises, partially offset by interest and lease-related payments of $1.0 million, and also including the receipt and repayment of a $6.0 million bridge loan from Sprott Lending. |

| December 31, 2020 | December 31, 2019 | |||||||

| Working Capital | 9,801 | 7,646 | ||||||

Working capital increased by $2.2 million at December 31, 2020 relative to December 31, 2019, reflecting an increase in current assets of $4.6 million primarily reflecting the acquisition of marketable securities and warrants of $2.0 million and increase in VAT recoverable of $1.6 million, partially offset by an increase in current liabilities of $2.4 million, primarily reflecting a $1.5 million increase relating to VAT payable and $1.0 million increase in trade and other payables.

| 25 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

| Q4 | Twelve months ended December 31, | |||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| Net cash from operations before changes in working capital ($000’s) | 2,529 | (1,707 | ) | (3,733 | ) | (4,314 | ) | |||||||||

The $4.2 million increase in Q4 2020 versus the prior-year quarter for cash flows before changes in working capital principally reflects higher revenues and lower direct mining and milling costs as described in the Revenue and Cost of Sales sections above, partially offset by a $0.4 million increase in exploration expenses in the current quarter. The $0.6 million decrease for the year ended December 31, 2020 versus the prior year primarily reflects the impact of the Suspension offset by the increase in revenues and lower direct mining and milling costs as described above.

| Q4 | Twelve months ended December 31, | |||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| Investing Activities ($000’s) | (3,156 | ) | (2,176 | ) | (10,516 | ) | (5,802 | ) | ||||||||

The 12-month variances include capital expenditures of $2.6 million in dewatering capital, mine development and mining equipment, and $2.0 million on transaction costs and a loan advanced on the acquisition of Otis.

| Financing Activities ($000’s) | 63 | 661 | 12,230 | 8,339 |

For the year ended December 31, 2020, $12.2 million was sourced from financing activities, including $12.8 million from Debentures and $0.4 million in proceeds from stock option and warrant exercises, partially offset by interest and lease-related payments of $1.0 million.

The Company issued the Debentures in Q3 2020, accessed the capital markets in 2019 and arranged a bridge loan (since repaid) in connection with the acquisition of Otis. The Company has also implemented cost reductions and business improvements at its operations. With recent metal price increases, the Company expects to be able to generate positive cash flows from the Platosa mining operation in 2021, although such cash flow may not be sufficient to fund all of the Company’s exploration activities. In the event that cash flows from operations are insufficient, failure to obtain additional financing could result in delay or indefinite postponement of further exploration and development of the Company’s projects and the possible loss of such properties. There can be no assurances that the Company will be able to obtain adequate funding or that the terms of such financing will be favourable. The Company’s ability to generate positive cash flows is also impacted by financial market conditions, most notably metal prices as the Company derives its revenues from the sale of silver, lead and zinc and bears the associated treatment and refining costs. The Company is also exposed to currency exchange risk and accordingly manages this exposure with currency hedges as described below in “Financial Instruments”. In addition, the Company faces continued uncertainty related to the COVID-19 outbreak; please see “Business Environment & Risks” section below.

| 26 | Page |

Management’s Discussion & Analysis of Financial Results

For year ended December 31, 2020

Financial Instruments

All financial assets and financial liabilities, other than derivatives, are initially recognized at the fair value of consideration paid or received, net of transaction costs as appropriate, and subsequently carried at fair value or amortized cost. The carrying values of cash and cash equivalents, trade receivables and other liabilities approximate their fair value, unless otherwise noted.

The Company’s financial performance is sensitive to changes in commodity prices, foreign exchange and interest rates, and the Company may periodically consider hedging such exposure. The Company’s Board of Directors together with executive management has overall responsibility for the establishment and oversight of the Company’s risk management framework. The Company may continue to address its price-related exposure to foreign exchange through the use of options, futures, forwards and derivative contracts.

The Mexican peso (“MXN”) and the Canadian dollar (“C”) are the functional currencies of the Company, with currency exposures arising from transactions and balances in currencies other than the functional currencies.