Exhibit 99.2

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

Excellon Resources Inc. (the “Company” or “Excellon”) has prepared this Management’s Discussion and Analysis of Financial Results (“MD&A”) for the year ended December 31, 2021 in accordance with the requirements of National Instrument 51-102 (“NI 51-102”).

This MD&A contains information as at March 31, 2022 and provides information on the operations of the Company for the years ended December 31, 2021 and 2020 and subsequent to the period end, and should be read in conjunction with the audited consolidated financial statements for the years ended December 31, 2021 and 2020 which have been filed on SEDAR and EDGAR. The audited consolidated financial statements for the years ended December 31, 2021 and 2020 have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”). All figures in this MD&A are in thousands of United States dollars ($’000) unless otherwise noted.

This MD&A also refers to Adjusted loss, Adjusted loss per share, Production Cost per Tonne, Cash Cost per Silver Ounce Payable, and All-in Sustaining Cost (“AISC”) per Silver Ounce Payable, all of which are Non-IFRS measures. Refer to the “Financial Review” and “Non-IFRS measures” sections of this MD&A for an explanation of these measures and reconciliation to the Company’s reported financial results.

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

| 1 | Page |

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

BUSINESS AND STRATEGIC PRIORITIES

Excellon’s vision is to create wealth by realizing strategic opportunities through discipline and innovation for the benefit of the Company’s employees, communities and shareholders. The Company is advancing a precious metals growth pipeline that includes: Platosa, a high-grade silver mine producing in Mexico since in 2005; Kilgore, an advanced gold exploration project in Idaho with strong economics and significant growth and discovery potential; and an option on Silver City, a high-grade epithermal silver district in Saxony, Germany with 750 years of mining history and no modern exploration. The Company also aims to continue capitalizing on current market conditions by acquiring undervalued projects.

The common shares of Excellon trade on the Toronto Stock Exchange (the “TSX”), the NYSE American, LLC exchange (the “NYSE American”) under the symbol “EXN” and on the Frankfurt Stock Exchange under the symbol “E4X2”.

On April 2, 2020, the Company announced a temporary suspension of mining, milling and exploration activities at its Mexican operations in accordance with the Mexican Presidential Order to mitigate the spread of COVID-19 (the “Suspension”). The Suspension impacted all industries considered non-essential across Mexico. For the Company, the Suspension resulted in the suspension of mining operations, though essential care and maintenance activities required at the Company’s operations were permitted to continue. At Platosa, such essential care and maintenance included ongoing labour costs and water pumping to maintain water levels of the mine, incurring a cost during the Suspension of approximately $3.3 million during a period of negligible revenues. The Suspension and associated care and maintenance costs impacted the comparable twelve-month period in 2020 and should be considered throughout this MD&A. The Mexican Government subsequently declared mining an essential service, and companies were allowed to commence activities to restart operations on June 1, 2020, provided they met the COVID-19 guidelines established by the Mexican Government. The Company recommenced mining and exploration activities in June 2020 and concentrate shipments resumed on July 6, 2020.

Exploration Activities

The Company advanced its exploration programs in the United States, Mexico and Germany including:

| ● | Continued drilling of priority targets at Grauer Wolf and Trinity, with ongoing soil sampling over the Bräunsdorf claim block focused on the Hartha prospect (Saxony, Germany). |

| ● | Additional drilling at Platosa to define and expand mineralization at the 623, NE-1 and NE-1S mantos with ongoing work to define remnant ore in areas previously considered mined-out including: underground mapping, chip sampling, modelling and underground drilling at Guadalupe, Guadalupe Sur and Pierna. |

| ● | Follow-up drilling on a wide zone of high-grade mineralization (2,860 g/t silver equivalent (“AgEq”) over 7.5 metres) intersected below Manto 623 and defined a new high-grade subvertical mineralized zone – Zone 817. Production commenced from this zone in Q1 2022. |

| ● | Regional prospecting and soil sampling seeking to follow up and extend target areas within the Kilgore Project. |

| ● | Ongoing work to interpret recently received results of screen metallics assays performed on historical core allowing assessment of coarse gold distribution in various lithologies and optimization of assay techniques for the upcoming 2022 drill program. |

| ● | Final Decision Notice received in Q4 2021 from the United States Forest Service (“USFS”) allowing ground disturbing activities, including drilling. |

| ● | Commencement of geophysical surveys on the Matrix Creek prospect within the Oakley claims to image subsurface structures associated with gold mineralization and generate drill targets. |

| 2 | Page |

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

Strong and consistent mine production

The Company’s Mexican operations delivered records for mined and processed tonnage in 2021, along with the most silver ounces produced since 2013. In Q4 2021, the Company recorded its sixth consecutive quarter of over 20,000 tonnes mined and milled following the restart in late Q2 2020 – a first since production commenced in 2005.

Mexican Operations

Optimizations at Platosa and Miguel Auza made in mid-2020 have been sustained and improvement efforts focusing on equipment reliability, human resource development and more effective planning and technical support continued to progress into Q1 2022 (see discussion under “Financial Review – Summary of Financial Results – Cost of Sales”). Mine-planning and geology teams were strengthened at Platosa in the first half of 2021. In the beneficiation plant, intensive supervisor and operator training completed in Q3 2021 led to improved flotation circuit performance and mill recoveries starting late in Q3 2021 which continued into Q4 2021.

The Company conducted extensive underground drilling over the past six quarters, including 320 holes totaling 20,462 metres during 2021. Much of this drilling successfully improved definition of mineralized bodies in advance of mining operations and incrementally added tonnage to the mineralized body. A key goal of this drilling was to define tonnage in an area of deposit, the “Gap Zone,” that had not been sufficiently drilled with historic vertical holes from surface and which held significant potential for additional mineralization connecting the shallower parts of the mineralized body with the deepest defined extents. Drilling in the Gap Zone did not define material amounts of mineralization.

The Company continues work to define remnant ore in areas previously considered mined-out. Ongoing underground exploration is testing for other potential vertical zones of mineralization. In Q1 2022, the Company also drilled two holes totaling 500 metres from surface to test anomalous mineralization approximately 90 metres southeast of Manto 623, results are pending.

Over the course of 2021, cost increases impacted the operation in various areas, particularly energy (associated with rising natural gas prices from the polar vortex of February 2021, which were subsequently sustained in part throughout 2021) and labour, the two largest cost centres. Additionally, legislative changes in Mexico further materially increased labour costs.

As announced on January 5, 2002, while the Company continued to aggressively drill to expand and define the mineral resource in recent years and throughout Q4 2021, current mining is entering an area of the deposit that steepens significantly, with fewer vertical-tonnes-per-metre than historically encountered. The last two years have seen an increase in the challenges faced in Mexico, particularly the impact on dewatering rates of the Suspension in Q2 2020 and the polar vortex in February 2021, along with increased consumable prices and certain legislative changes. The Company continues to explore from underground and surface and to refine the operation and has been assessing whether maintaining a consistent production schedule beyond mid-2022 at achievable dewatering rates and with acceptable capital expenditures is possible without additional mineralization being defined. Based on exploration results in Q4 2021 and to date, the Company currently expects to wind down operations at Platosa during Q3 2022, subject to results from ongoing exploration programs. As a result, the Company performed an impairment test on its Mexican operations and recorded an impairment loss of approximately $15.8 million as at December 31, 2021.

| 3 | Page |

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

On March 7, 2022, the Company reported that the Sindicato Nacional Minero Metalúrgico (the “Platosa Union”) commenced a labour action at the Platosa Mine in Durango, Mexico. Despite an agreement in principle on the terms of the 2022 collective bargaining arrangement following numerous concessions, the agreement was reneged on, and despite additional concessions, a labour action was ordered. If the labour action is not resolved in a reasonable amount of time, the economic viability of the Platosa Mine, cash flows, earnings, results of operations and financial condition of the Company may be impacted.

Provision for litigation

The Company recorded a $22.2 million provision in Q3 2021 as required under IFRS’s International Accounting Standard 37 – Provisions, Contingent Liabilities and Contingent Assets, since receiving the formal written decision regarding the litigation involving the Company’s subsidiary, San Pedro Resources (“San Pedro”), in respect of the La Antigua mineral concession (“La Antigua”) as announced on August 10, 2021 (the “Judgment”). The Judgment is solely against San Pedro and the Company believes that the plaintiff has no recourse against the Company’s other assets in Mexico (including Platosa), Idaho, Saxony or Canada. San Pedro is a wholly-owned, indirect subsidiary of the Company that holds the Miguel Auza processing facility and the original Miguel Auza mineral concessions, including the Evolución mineral resource disclosed in September 2020. The book value of San Pedro’s assets included in the consolidated balance sheet after impairment is $3.1 million, including plant, property and equipment ($1.4 million), VAT recoverable ($1.3 million) and materials, supplies and other ($0.4 million).

The Company continues to pursue avenues through its labour, community and government relationships and is investigating remedies under international law. In the interim, San Pedro continues to operate in the ordinary course (subject to the labour action noted above). San Pedro generates minimal cash flows from milling fees charged to the Platosa Mine for ore processing and holds minimal working capital. The Platosa Mine is owned and operated by an entirely separate subsidiary.

Exploration Plans

At Silver City, four holes totaling 8,340 metres were drilled by the end of Q4 2021, with an additional three drill holes (1,150 metres) planned for Q1 2022. In Q1 2022, drilling followed-up on mineralization intersected at Grauer Wolf target area, along with continuing soil sample lines over key areas to assist in future drill targeting.

At Platosa underground drilling will continue to test remnant mineralization above the water table in areas previously considered mined out. Surface drilling commenced Q1, 2022, with two holes totaling 500 metres testing mineralization extents southeast of the 623 Manto. The Company aims to define potentially mineable volumes of mineralization on an expedited basis.

At Kilgore, the Company aims to improve the understanding of the deposit setting on a local and regional scale through re-logging core to enhance the underlying structural and lithologic framework while improving the characterization of host rocks through lithogeochemistry. Portable XRF analysis of pulps from the historical holes as well as sampling and assaying of previously unsampled or unassayed core is also ongoing and will be supplemented by analysis of selected core intervals using screen metallic assaying to better categorize the distribution and presence of coarse gold.

The Company filed an updated Plan of Operations (“PoO”) with the USFS in Q2 2020 and the USFS filed a final National Environmental Policy Act Environmental Assessment (“EA”) in Q2 2021. USFS filed a decision notice to allow ground disturbing activities, including drilling, to commence as of November 12, 2021. The Company plans to commence drilling at Kilgore in mid-2022. In Q1 2022, an application was filed by an NGO requesting that the Court reopen the matter with the USFS concerning its approval of the Kilgore 2021 EA.

| 4 | Page |

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

Regional exploration programs, including geophysics, mapping, prospecting, soil geochemistry and modelling, are planned for Oakley, Kilgore and the new exploration licences at Silver City (Mohorn, Oederan and Frauenstein), and will be carried out in H1 2022.

Exploration also continues at the Oakley project, subject to the option agreement between Excellon and Centerra Gold Inc. (“Centerra”).

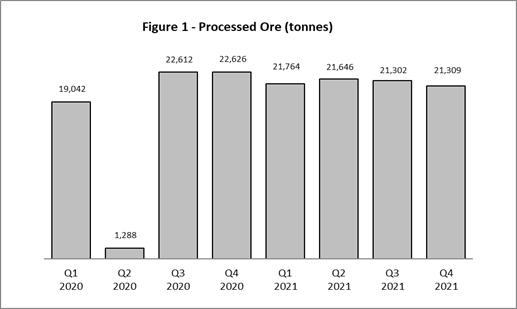

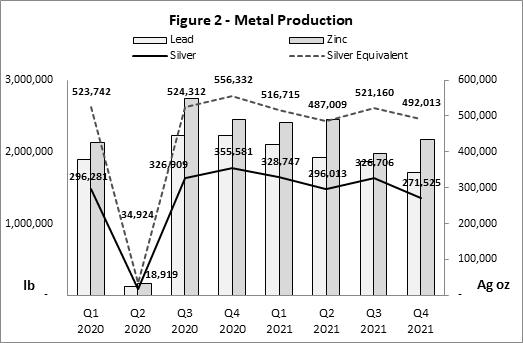

Platosa Mine production statistics for the periods indicated are as follows:

| Q4 | Q4 | |||||||||||||||

| 2021 | 2020 | 2021(1) | 2020(1) | |||||||||||||

| Tonnes Mined: | 20,954 | 21,455 | 85,530 | 66,501 | ||||||||||||

| Tonnes Milled: | 21,309 | 22,626 | 86,021 | 65,567 | ||||||||||||

| Grades: | ||||||||||||||||

| Silver (g/t) | 438 | 536 | 494 | 519 | ||||||||||||

| Lead (%) | 4.65 | 5.42 | 5.01 | 5.37 | ||||||||||||

| Zinc (%) | 5.50 | 6.12 | 6.03 | 6.57 | ||||||||||||

| Recoveries: | ||||||||||||||||

| Silver (%) | 90.5 | 91.2 | 89.5 | 91.4 | ||||||||||||

| Lead (%) | 78.5 | 82.9 | 80.0 | 83.7 | ||||||||||||

| Zinc (%) | 83.7 | 80.1 | 79.0 | 78.9 | ||||||||||||

| Metal Production: | ||||||||||||||||

| Silver – (oz) | 271,525 | 355,581 | 1,222,991 | 997,690 | ||||||||||||

| Lead – (lb) | 1,717,525 | 2,223,465 | 7,612,332 | 6,470,637 | ||||||||||||

| Zinc – (lb) | 2,167,840 | 2,452,728 | 9,014,028 | 7,488,825 | ||||||||||||

| AgEq (oz) (2) | 492,013 | 556,332 | 2,017,639 | 1,639,310 | ||||||||||||

| Payable: (3) | ||||||||||||||||

| Silver – (oz) | 287,953 | 323,139 | 1,141,281 | 928,240 | ||||||||||||

| Lead – (lb) | 1,762,293 | 2,049,065 | 7,073,488 | 6,087,239 | ||||||||||||

| Zinc – (lb) | 1,697,098 | 2,088,975 | 7,101,992 | 6,442,712 | ||||||||||||

| AgEq (oz) (2) | 479,566 | 499,644 | 1,810,199 | 1,501,354 | ||||||||||||

| Average realized prices: (4) | ||||||||||||||||

| Silver – ($US/oz) | $ | 23.30 | $ | 24.46 | $ | 25.12 | $ | 21.59 | ||||||||

| Lead – ($US/lb) | $ | 1.06 | $ | 0.87 | $ | 1.00 | $ | 0.83 | ||||||||

| Zinc – ($US/lb) | $ | 1.53 | $ | 1.21 | $ | 1.37 | $ | 1.08 | ||||||||

| Toll milling (3rd party) ore processed (t) | - | - | - | 4,785 | ||||||||||||

| Silver ounces produced | 271,525 | 355,581 | 1,222,991 | 997,690 | ||||||||||||

| Silver ounces payable | 287,953 | 323,139 | 1,141,281 | 928,240 | ||||||||||||

| Silver equivalent (“AgEq”) ounces produced (2) | 492,013 | 556,332 | 2,017,639 | 1,639,310 | ||||||||||||

| AgEq ounces payable (2) (3) | 479,566 | 499,644 | 1,810,199 | 1,501,354 | ||||||||||||

| Production cost per tonne (5) | $ | 314 | $ | 252 | $ | 291 | $ | 299 | ||||||||

| Total cash cost per silver ounce payable | $ | 15.61 | $ | 12.73 | $ | 13.01 | $ | 15.38 | ||||||||

| AISC per silver ounce payable (6) | $ | 24.82 | $ | 21.49 | $ | 24.78 | $ | 26.80 | ||||||||

| 5 | Page |

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

| (1) | Period deliveries remain subject to assay and price adjustments on final settlement with concentrate purchaser. Data has been adjusted to reflect final assay and price adjustments for prior-period deliveries settled during the period. As further discussed in “Business and Strategic Priorities,” above, results for the comparative year ended December 31, 2020 were impacted by the Suspension. |

| (2) | AgEq ounces established using average realized metal prices during the respective period applied to the recovered metal content of the concentrates to calculate the revenue contribution of base metal sales during the period. |

| (3) | Payable metal is based on the metals delivered and sold during the period, net of payable deductions under the Company’s offtake arrangements, and will therefore differ from produced ounces. |

| (4) | Average realized price is calculated on current period sale deliveries and does not include the impact of prior period provisional adjustments in the period. |

| (5) | Production cost per tonne includes mining and milling costs, excluding depletion and amortization, inventory adjustments and future mine closure related accruals. |

| (6) | AISC per silver ounce payable excludes general and administrative and share-based payment costs attributable to the Company’s non-producing projects and includes underground drilling costs. The comparatives have been revised to conform with the current allocation. |

Operational Highlights

2021 Production (compared to 2020)

| ● | AgEq production increased 23% to 2.0 million oz (2020 – 1.6 million AgEq oz) |

| ● | AgEq ounces payable sold increased 21% to 1.8 million AgEq ozs (2020 – 1.5 AgEq ozs) |

| ● | Total cash cost net of by-products per silver ounce payable decreased 15% to $13.01 (2020 – $15.38) |

| ● | AISC per silver ounce payable decreased 8% to $24.78 (2020 – $26.80) |

| ● | Production cost per tonne decreased 3% to $291 per tonne (2020 – $299 per tonne) |

Q4 2020 Production (compared to Q4 2020)

| ● | AgEq production decreased 12% to 492,013 oz (Q4 2020 – 556,332 AgEq oz), including: |

| ○ | Silver production decreased 24% to 271,525 oz (Q4 2020 – 355,581 oz) | |

| ○ | Lead production decreased 23% to 1.7 million lb (Q4 2020 – 2.2 million lb) | |

| ○ | Zinc production decreased 12% to 2.2 million lb (Q4 2020 – 2.5 million lb) |

| ● | Total cash cost net of byproducts per silver ounce payable increased 23% to $15.61 (Q4 2020 – $12.73) |

| ● | AISC per silver ounce payable increased 15% to $24.82 (Q4 2020 – $21.49) |

| ● | Production cost per tonne increased 25% to $314 (Q4 2020 – $252) |

| 6 | Page |

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

Impact of COVID-19 on the Company’s Business and Operations

In December 2019, a novel strain of coronavirus known as COVID-19 surfaced in Wuhan, China and spread around the world, with resulting business and social disruption. COVID-19 was declared a worldwide pandemic by the World Health Organization on March 11, 2020. The speed and extent of the spread of COVID-19 and its variants, and the duration and intensity of resulting business disruption and related financial and social impact, are uncertain. Further, the extent and manner in which COVID-19, and measures taken by governments, the Company or others to attempt to reduce the spread of COVID-19 and its variants, may affect the Company and cannot be predicted with certainty.

COVID-19 and these measures have had and may continue to have an adverse impact on many aspects of the Company’s business including employee health, workforce productivity and availability, travel restrictions, contractor availability, delays in receiving assay results from commercial labs, supply availability, ability to sell or deliver concentrate and the Company’s ability to maintain its controls and procedures regarding financial and disclosure matters, some of which, individually or when aggregated with other impacts, may be material to the Company. Measures taken by governments, the Company or others could result in the Company reducing or suspending operations at Platosa or exploration activities at its projects, including Platosa, Kilgore, Oakley, Evolución or Silver City.

In 2021, none of the Company’s projects were suspended or restricted. Although the Company believes the risk for business interruption remains low, unexpected interruptions could still occur given the uncertainty surrounding the recurring wave of rising cases in certain regions where the Company operates and considering the surge in the “Omicron” variant of the virus. Government vaccination programs for COVID-19 are underway in all of the regions in which the Company operates. Vaccination programs are now progressing well in Mexico, with 99% of the Company’s workforce double-vaccinated and 37% triple-vaccinated.

The Company has taken action to prevent the spread of the outbreak at its sites and protect its employees, contractors and the communities in which it operates. The Company is continually modifying its response to the pandemic to align with industry best practices. The enhanced health and safety measures continue to focus on screening employees and contractors before entering the Company’s sites for potential symptoms of COVID-19, contact tracing of individuals that may have been exposed to the virus, cleaning and disinfection services, maintaining disinfection stations in high-traffic areas and facilitating physical distancing. Some of the measures implemented to manage the COVID-19 outbreak are expected to remain in place for the foreseeable future and may marginally increase the production costs at the Company’s operations. These costs relate mostly to increased sanitizing personnel, personal protective equipment (“PPE”) and testing of employees and contractors.

The Company continues to assess the logistical challenges to its supply chain and distribution methods to deliver its concentrate products from the Miguel Auza mill to third-party refineries and smelters. The Company has observed limited impact to the supply chain to date. The Company has sufficient stock of critical components and has worked closely with its key suppliers to secure future delivery of materials, inventory of PPE, reagents and other critical parts at all sites. Similarly, the Company has not experienced significant disruption to its distribution network and ability to deliver its products to smelting and refining facilities or ability to sell finished products to its customers. However, further measures taken by governments, the Company or others related to COVID-19 may adversely affect the Company’s availability of supplies or its ability to sell or deliver concentrate.

There are significant uncertainties with respect to future developments and their impact on the Company related to the COVID-19 pandemic, including the duration, severity and scope of the outbreak and any current or further measures taken by governments, the Company and others in response to the pandemic. While mining is classified as an essential business by the Mexican government, further suspension or reduction of operations by the Company may be required in response to additional government measures or other measures that the Company otherwise deems appropriate.

Operations Commentary

Mine performance in Q4 2021 continued to benefit from leadership updates in the superintendencies of geology, technical services and maintenance, which have led to improvements in mine planning, geological interpretation and equipment reliability. Supervisor and operator training to maximize flotation circuit performance was ongoing during the quarter with oversight from a seasoned operator and consultant. Operational changes to reagents late in Q3 2021 improved lead and zinc recoveries to near design levels of over 80%, which have been sustained through Q4 2021 and into Q1 2022.

Mill feed grades were lower in Q4 2021 versus Q4 2020 mainly reflecting grade variations in the mantos mineralized body. This variability modified the chemistry within the feed to the processing facility, which impacted recoveries. In particular, increased levels of lead oxide and resulting higher lead:lead-oxide ratio in the mill feed reduced recoveries of lead and silver in the lead concentrate.

| 7 | Page |

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

Metal production in Q4 2021 was below Q4 2020 mainly due to the lower grades and recoveries discussed above. The Company’s metal production in terms of AgEq ounces may be strongly influenced by metal prices, with the ratio of silver to lead and zinc prices determining the AgEq ounces derived from revenues associated with lead and zinc production (e.g. higher base metals relative to silver prices lead to increased AgEq ounce production attributable from base metals). Ore stockpiles at December 31, 2021 comprised 2,015 tonnes of mineralized material, reflecting unprocessed and unsold production of approximately 39,250 AgEq ounces.

The previous eight quarters of production at Platosa are summarized below:

| 8 | Page |

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

Analysis of the components of mine operating results is as follows:

| Q4 | Year ended December 31, | |||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||

| Mill feed processed | 21,309 | 22,626 | 86,021 | 65,567 | ||||||||||||

Production in Q4 2021 was 21,309 tonnes, 6% lower than Q4 2020, but in line with typical throughput levels. The significant increase in tonnes mined for the year ended December 31, 2021 versus the prior year mainly reflects the impact of the Suspension in Q2 2020 (as discussed in “Strategic and Business Priorities,” above).

Head grades | Ag (g/t) | 438 | 536 | 494 | 519 | |||||||||||||

| Pb (%) | 4.65 | 5.42 | 5.01 | 5.37 | ||||||||||||||

| Zn (%) | 5.50 | 6.12 | 6.03 | 6.57 |

Silver grades in Q4 2021 were 18% lower than the comparative period, reflecting variation in the mantos mineralization.

Overall, silver, lead and zinc grades decreased 5%, 7% and 8%, respectively, compared to 2020.

| Recoveries | Ag (%) | 90.5 | 91.2 | 89.5 | 91.4 | |||||||||||||||

| Pb (%) | 78.5 | 82.9 | 80.0 | 83.7 | ||||||||||||||||

| Zn (%) | 83.7 | 80.1 | 79.0 | 78.9 |

| 9 | Page |

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

| Q4 | Year ended December 31, | |||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||

Recoveries were lower than Q4 2020 due to lower feed grades and flotation performance. Grind size, reagent additions and cell operating-parameter modifications took place late in Q3 2021 and extended to year end. Metallurgical investigation was performed on concentrate and feed samples in XPS lab (QUEMSCAN) under the supervision of Excellon’s independent metallurgical consultancy as further optimization efforts were underway. Overall recovery performance in Q4 for lead and silver was impacted by high lead:lead-oxide ratios and lower feed grades.

| Metal Production | Ag (oz) | 271,525 | 355,581 | 1,222,991 | 997,690 | |||||||||||||

| Pb (lb) | 1,717,525 | 2,223,465 | 7,612,332 | 6,470,637 | ||||||||||||||

| Zn (lb) | 2,167,840 | 2,452,728 | 9,014,028 | 7,488,825 | ||||||||||||||

| AgEq (oz) | 492,013 | 556,332 | 2,017,639 | 1,639,310 |

Silver, lead and zinc production decreased by 24%, 23% and 12%, respectively, relative to Q4 2020 driven by lower feed grades and recoveries. AgEq ounce production decreased by 12% relative to Q4 2020, as lower-feed grade and recoveries affected metal production and a larger stockpile of mineralized material remained to be processed at quarter-end, with such negative impacts partially offset by an improved ratio of base metal to silver prices in Q4 2021 relative to Q4 2020.

The Suspension resulted in lower AgEq production for the year ended December 31, 2020 compared to 2021.

EXPLORATION AND EVALUATION REVIEW

Refer to the Company’s Annual Information Form (“AIF”) for a detailed overview of the Company’s exploration projects, including mineral resource estimates.

Platosa Property

The Platosa Mine is an operating underground polymetallic (silver, lead and zinc) mine, located in northeastern Durango State, Mexico. It is located approximately 5 kilometres north of the town of Bermejillo and 45 kilometres north of the city of Torreón. The deposit consists of a series of high-grade carbonate-replacement deposits (CRD) occurring as mantos. Excellon Resources Inc. (Excellon) operates and owns 100% of the Platosa Mine through its wholly owned subsidiary, Minera Excellon de Mexico S.A. de C.V.

The Company continued exploration at Platosa throughout 2021, including underground drilling to test and define mineralization around existing infrastructure. The Platosa project highlights include:

| ● | Underground drilling to define and delineate additional mineralization near mine infrastructure with 79 holes drilled totaling 4,138 metres in Q4 2021, for an aggregate 320 holes drilled totaling 20,462 metres in 2021 | |

| ● | Drilling from surface into historically mined areas totaling 10,066 metres in 2021 | |

| ● | Advancing underground development to support further drilling of Guadalupe South, Guadalupe North, NE-1 and NE-1S | |

| ● | Underground mapping and chip sampling to define remnant ore | |

| ● | Follow up drilling on a wide zone of high-grade mineralization (2,860 g/t AgEq over 7.5 metres) 10 metres below Manto 623, and defining a sub-vertical zone of high-grade mineralization |

| 10 | Page |

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

At Jaboncillo, approximately 11 kilometres northwest of the Platosa Mine, the Company continued to follow up on drilling completed in 2019 that intersected multiple gossanous horizons with pyritic breccias, arsenopyrite and relict base-metal sulphides. Petrographic studies conducted in Q2 2020 confirmed the presence of base-metal sulphide species, including sphalerite and galena. These observations confirm that the system is productive for base-metal sulphides on multiple structures over an approximate strike length of one kilometre. In Q3 2020 drilling resumed in this area, targeting an economically significant component to the system. Between Q1 2021 and Q3 2021 eleven holes, totalling 5,637 metres, were completed, with several holes intersecting jasperoid rich zones, and intervals of disseminated sulphides.

Drilling on a skarn target at PDN, approximately two kilometres north of the Platosa Mine, was undertaken in Q1 2021 with one hole drilled totaling 600 metres. Drilling targeted areas where intense dolomitization and sanding along structures was intersected in preliminary drill holes, indicating the movement of hydrothermal fluids that are believed to be the expression of a potential skarn system at depth. Drilling in Q4 2020 intersected confirmatory silver grades of 218 g/t Ag over 0.75 meters. This potential for a skarn body at PDN has been defined through induced polarization, magnetics and gravity surveys.

Evolución Project

The Evolución Project is an exploration-stage project comprising 22 mineral concessions totaling 45,000 hectares, and 35 kilometres of strike in one of the world’s premier silver districts. It is an intermediate stage polymetallic silver-zinc-lead-gold exploration project on the border of northern Zacatecas and southern Durango, on the high plateau of central Mexico.

The Company’s overall goals on the project are to (i) discover Fresnillo-style epithermal mineralization and subsequently define mineral resources thereon; and (ii) continue growing the existing Evolución mineral resource in advance of an economic study of the deposit in due course. In H1 2021, the Company completed detailed mapping at 1:1000 scale across the entire licence. Data collected in the field relating to the structural setting and associated mineralization in the Evolución licence are being compiled and evaluated by a PhD candidate. This work will contribute to understanding the potential scale and timing of mineralization on the project. During 2021 the Company incurred costs of $512 on the Evolución project including exploration work of $226 and concession holding costs of $286.

| 11 | Page |

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

Silver City Project

The Silver City Project is an exploration-stage project that comprises the Bräunsdorf, Frauenstein, Mohorn and Oederan exploration licences in Saxony, Germany and totals approximately 340 km2. In Q3 2019, the Company entered into an agreement with Globex Mining Enterprises Inc. (“Globex”) to earn into an option to acquire a 100% interest in the Bräunsdorf exploration licence (the “Globex Agreement”). The terms of the Globex Agreement are described in the Company’s AIF. The Bräunsdorf licence is a 164 km2 silver district that encompasses a 36-km long epithermal vein system situated west of the city of Freiberg (30 km southwest of Dresden). The immediate exploration licence and surrounding area have a long and rich history of silver mining dating back to the 11th century with numerous historic mine camps, small mines and prospects, many of which have only been explored and/or mined to shallow depths, seldom exceeding 200 metres below surface. Historically reported veins ranged from 0.5 to 10 metres width, with grades of over 3,500 g/t silver and no assaying for either gold or zinc, which were not historically available.

The Company’s near-term exploration goals at Silver City are to (i) confirm the strike and plunge of historical mine workings and (ii) identify new mineralized bodies that were not historically discovered and exploited. With initial drilling success, the Company aims to define economic mineral resources on the project and advance them toward permitting and development. At the current stage and with the current information available, the cost and timeframe to do so is not ascertainable.

In Q2 2021 the Drilling Operation Plan (“DOP”) for the 2021 program was approved, and drilling commenced in late Q2 2021 with two drill rigs. The Company permitted up to approximately 22,000 metres of drilling on the Bräunsdorf licence for 2021, with the planned drill program totalling 12,000 metres. During Q4 2021, nine holes totalling 2,972 metres were completed for a total of 24 holes (8,360 metres) in 2021, with the first drill core submitted to the laboratory in early Q3. An additional three holes totaling 1,222 metres were completed in Q1 2022.

Drilling in 2021 followed up on results from the initial, 16-hole diamond drilling program completed in 2020 totaling 3,678 metres. The DOP contemplates drilling on four priority follow-up targets identified in the 2020 program including:

| ● | Peter Vein: a historically significant mine where initial drilling encountered 1,042 g/t AgEq over 0.45 metres (911 g/t Ag, 0.4 g/t Au, 2.8% Pb and 0.9% Zn), within 231 g/t AgEq over 2.30 metres (183 g/t Ag, 0.4 g/t Au, 0.5% Pb and 0.2% Zn) | |

| ● | Reichenbach (Großvoigtsberg): a new, near-surface discovery in an area with minimal historic mining, where initial drilling encountered 505 g/t AgEq over 0.71 metres (356 g/t Ag, 2.0 g/t Au), within 191 g/t AgEq over 1.90 metres (134 g/t Ag and 0.8 g/t Au) | |

| ● | Bräunsdorf: a historically significant mine, where initial drilling encountered 319 g/t AgEq over 0.35 metres (300 g/t Ag, 0.2 g/t Au and 0.2% Zn), within 101 g/t AgEq over 2.05 metres (87 g/t Ag, 0.2 g/t Au) | |

| ● | Grauer Wolf: a new high-grade discovery in an area with no historic drilling, where initial drilling encountered 1,043 g/t AgEq over 1.3 metres (954 g/t Ag, 0.1 g/t Au, 0.7% Pb and 2.0% Zn) less than 100 metres from surface, within 194 g/t AgEq over 8.1 metres (173 g/t Ag, 0.1 g/t, Au, 0.4% Pb and 0.3% Zn), and 331 g/t AgEq over 1.2 metres (325 g/t Ag, 0.1 g/t Au, 0.03% Pb and 0.03% Zn) in the hanging wall |

The results of the 2021 drill program at Silver City (with assays for four holes pending) include:

| ● | 1,633 g/t AgEq over 0.35 metres (1,470 g/t Ag, 0.2 g/t Au, 2.9% Pb and 2.1% Zn) within 257 g/t AgEq over 2.90 metres (232 g/t Ag, 0.4% Pb and 0.3% Zn) in SC21GVB020 at Peter Vein |

| ● | 1,296 g/t AgEq over 0.35 metres (1,260 g/t Ag, 0.2 g/t Au, 0.6% Pb and 0.3% Zn) within 592 g/t AgEq over 1.05 metres (508 g/t Ag, 0.1 g/t Au, 1.4% Pb and 1.2% Zn) in SC21GWO033 at Grauer Wolf |

| ● | 266 g/t AgEq over 0.65 metres (228 g/t Ag, 0.1 g/t Au, 0.7% Pb and 0.5 % Zn) within 169 g/t AgEq over 1.93 metres (137 g/t AgEq, 0.3% Pb and 0.6% Zn) in SC21GWO030 at Grauer Wolf |

| ● | 383 g/t AgEq over 0.38 metres (7.0 g/t Ag and 5.0 g/t Au) in SC21REI027 at Reichenbach |

| 12 | Page |

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

A total of five soil sampling profiles have been completed over Peter Vein and Grauer Wolf target areas. The goal of the program is to test the geochemical response along the strike of the known mineralization and to identify new drill targets. Eleven more profiles are planned to be completed in Q1 2022 over Trinity, Hartha and on the Braunsdorf, Oederan and Mohorn licences.

Based on initial drilling results at the Bräunsdorf licence, the Company expanded the Silver City Project ground position in Q1 2021 to 34,150 hectares through the application for three additional permits (Frauenstein, Mohorn and Oederan). The concessions were granted following applications to the Sächsisches Oberbergamt (the “Saxon Mining Authority”) in Freiberg and are held by the Company’s subsidiary, Saxony Silver Corp. As in the case of the Bräunsdorf licences, historical records of these licences document centuries of high-grade silver production to shallow depths, with recent confirmation samples assaying multi-kilo silver and significant gold. The licences are early-stage and will be mapped and prospected over the remainder of 2021 in preparation for more advanced exploration work and potential drilling in 2022.

During 2021 and Q4 2021, the Company incurred costs on the project as set out in Note 21 of the Company’s financial statements.

Kilgore Project

The Kilgore project is an advanced exploration-stage volcanic and sediment hosted epithermal gold property located five miles from Kilgore, Clark County, Idaho. Excellon has a 100% undivided interest in 788 unpatented federal lode claims totaling 6,788 hectares on USFS lands. The property includes historical mine workings dating back to the early 1900’s with further drilling in the 1980’s that revealed the potential for mineralization well outside of the existing resource area, with limited follow up to date. Kilgore displays similar geological characteristics to Kinross Gold’s Round Mountain Mine, which has produced over 15 million ounces of gold to date.

In 2019, Otis Gold Corp. (“Otis”) completed a preliminary economic assessment that contemplated a low capital intensity, low operating cost, open-pit, heap-leach mining operation. Since acquiring Otis in Q2 2020 and filing a business acquisition report with respect to such transaction on May 29, 2020, the Company has been reassessing all aspects of the Kilgore project and believes that opportunities exist to enhance the project through:

| ● | Geological remodeling of the existing mineral resource, including relogging historical core to better define geological units and lithologies | |

| ● | Re-assaying historical drilling with metallic screen assays along with multi-element ICP to compliment historical fire-assayed samples | |

| ● | Geophysical surveying to image prospective ground to generate drill targets and constrain structural and lithologic controls of mineralization | |

| ● | Diamond drilling to infill and expand the mineral resource to follow-up on advances in the geological model and define mineral potential along strike, laterally and at depth | |

| ● | Metallurgical drilling in support of further metallurgical studies, particularly in the underlying Aspen formation based on additional petrographic information | |

| ● | Engineering review of potential infrastructure locations, processing options and new mining technologies; | |

| ● | continuing environmental studies |

| 13 | Page |

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

The Company’s contemplated drilling programs will also target higher-grade mineralization and structures at depth, predominantly in the Aspen formation, seeking to define the potential for gold mineralization that may be amenable to underground mining.

Subject to the timing for, completion of, and results from the foregoing, the Company currently expects to prepare an updated preliminary economic assessment on the Kilgore Project.

The next phase of advanced exploration on the Kilgore Project was approved by the USFS in Q4 2021. The Company filed an updated PoO with the USFS in Q2 2020 and the USFS filed the final Environmental Assessment (“EA”) in Q2 2021. The EA contemplates a total of 130 drill stations (with up to three holes per station) and construction of up to 70,977 feet of road to support drilling activities, with the project duration expected to be up to five years. The final EA and the supporting reports and studies are available on the website of the Company’s subsidiary, Excellon Idaho Gold Inc.: www.excellonidaho.com

During Q4 2021, the Company continued relogging of historical core and integrating this data into a stronger geological model with emphasis placed on timing of emplacement of multiple phases of mineralization and the controls on mineralization. This work is being integrated into 2022 drill targeting. Regional prospecting, soil and stream sediment sampling covering regional target areas and sampling of outcrops are ongoing. This work is largely focused on and around the GK claim block to the west of the Kilgore deposit. The program is intended to discover and define new zones of mineralization and develop future drill targets. Geological mapping at 1:5000 scale was completed on the Mine Ridge area with the goal of improving the accuracy of the Kilgore geological model by incorporating refined surface geology mapping. ASTER remote sensing was completed in Q3 2021 and will be used for identification of alteration zones and target generation for 2022 drill programs. Portable XRF analysis of pulp samples is ongoing. This data will be used to improve the characterization of host rock and alterations. To better understand the distribution and the extent to which coarse gold affects the precision of assaying, 289 samples were submitted for screen metallics analysis.

During Q4 2021 the Company continued to assess screen metallics analytical methods against all historical core assays. Following the previous analysis of 289 samples in Q3, further sampling and testing is recommended to better understand the effects of coarse gold on assaying precision.

During Q4 2021, in-depth review of historical geophysics surveys and geochemical data was integrated into 2022 drill targeting.

During Q4 2021, the Company undertook soil sample surveys and prospecting covering areas around the Dogbone claim block to the southwest of the Kilgore deposit. This program is intended to test historical anomalous gold in soils and extension westward of previous sampling efforts. Assay results are pending.

During Q4 2021, the USFS completed the EA initiated in Q3 2020. A Decision Notice finding “No Significant Impact” was issued allowing for ground disturbing activities, including drilling to commence. In Q1 2022, an application was filed by an NGO requesting that the Court reopen the matter with the USFS concerning its approval of the Kilgore 2021 EA.

During 2021 and Q4 2021, the Company incurred costs on the project as set out in Note 21 of the Company’s financial statements.

Oakley Project

On April 22, 2020, the Company acquired 100% ownership of the exploration-stage Oakley project in Cassia County, Idaho as part of the Otis acquisition. The Oakley Project is an exploration-stage project hosting gold-silver, epithermal hot spring-type mineralization at two targets: Blue Hill Creek and Cold Creek, and detachment-related gold-silver mineralization at Matrix Creek. The Oakley project has been optioned to Centerra pursuant to an option agreement that is summarized in the Company’s AIF (the “Oakley Agreement”).

| 14 | Page |

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

Drilling concluded at Cold Creek in Q3 2021, with eleven holes totaling 1,582 metres drilled in this program. Permitting for the drilling at Blue Hill Creek is in progress with anticipated start of the drilling in H1 2022. Work is being funded by Centerra pursuant to the terms of the Oakley Agreement. The Cold Creek claims cover approximately 14 km2, including a structurally complex north to south valley with bounding faults that has created at least three prospective geologic zones along the western and eastern margins. The current drill program tested targets within these zones, as follows:

| ● | Eastern Margin: A historically undrilled area of receptive units with gold in soil anomalies above shallow bedrock |

| ● | Bound Block: This area is bound by large structures on the east and west and has demonstrated surface and subsurface gold mineralization. Reverse circulation (“RC”) drilling from the late 1980’s returned anomalous grades that have not been followed up on. More recent work delivered anomalous gold in soil and rock samples, with basin-wide resistivity and chargeability anomalies |

| ● | Western Margin: A historically underexplored area of structural complexity with hydrothermal material at surface. RC drilling from the late 1980’s intersected 18.3 metres grading 0.46 g/t gold from surface. More recent work has identified gold in soil anomalies corresponding with a chargeability anomaly from IP surveying |

Highlights include:

| ● | 0.4 g/t Au over 13.6 metres hosted in metasediments, which historically have not been the focus of exploration. |

| ● | 1.4 g/t Au over 5.6 metres near-surface testing the Eastern Margin. |

During Q4 2021, Centerra elected to act as project manager pursuant to the Oakley Agreement. Additionally, Centerra commissioned geophysical CSAMT surveys within the Matrix Creek claim block; final reports are pending.

Mineral Resources

The Company’s mineral resource estimates have been prepared in accordance with NI 43-101 and the CIM’s ‘Mineral Resources and Mineral Reserves Best Practices’ guidelines (as applicable) and classified per the CIM ‘Definition Standards for Mineral Resources and Mineral Reserves’ (May 2014). The associated technical reports for the Platosa, Kilgore and Oakley projects can be found at www.sedar.com under the profiles for Excellon (in respect of Platosa) and Otis (in respect of Kilgore and Oakley). The technical reports for each of the projects are also available on the Company’s website at www.excellonresources.com.

For additional discussion of the Company’s mineral resource estimates and the Company’s other exploration projects, the reader should refer to the Company’s AIF, available on the Company’s website www.excellonresources.com and on www.sedar.com.

QUALIFIED PERSONS

Mr. Jorge Ortega, M.Sc., P.Geo., Vice President Exploration and a Qualified Person, as defined in NI 43-101, has reviewed and approved the scientific and technical information relating to geological interpretation and results contained in this MD&A. Paul Keller, P. Eng., Chief Operating Officer and a Qualified Person, as defined in NI 43-101, has reviewed and approved the scientific and technical information relating to production results contained in this MD&A.

| 15 | Page |

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

CORPORATE RESPONSIBILITY (“CR”)

CR Performance at Platosa and Miguel Auza

Management continues to evaluate and monitor compliance with legal requirements and manage CR risk. The operations continue to report on key trailing indicators of CR performance and elements of the Visible Felt Leadership process. Trailing indicators of safety performance through December 31, 2021, as measured by recordable injury frequency (“RIF”) and lost time injury frequency (“LTIF”), declined by 53% and 45%, respectively, in 2021 relative to 2020. Injury severity declined by 56% in 2021 relative to 2020.

The 2020 Environmental, Social, and Governance Report (ESG report) for our operations in Mexico was completed and published in February 2022. Preparation is underway on the 2019 and 2021 ESG reports, which are expected to be filed in H1 2022.

No significant environmental incidents were reported at either Platosa or Miguel Auza during 2021 and Q4 2021. The Company continued engagement with a range of stakeholders surrounding the Platosa and Miguel Auza business units. There were no community-related grievances reported during 2021.

The Comisión Nacional del Agua (“CNA”), the federal water regulatory agency in Mexico, has commenced an administrative procedure with the Company to review the management of water that the Company pumps from the Platosa mine. CNA has also initiated informal discussions about water management with local farmers but did not formally communicate with Excellon during Q4 2021.

The Company is committed to evaluating with CNA how best to manage such water going forward, to support Platosa’s operations and deliver a sustainable benefit to the residents of the surrounding Mapimí region. Water management is critical for the Platosa operation, and although the Company does not currently foresee any material changes to water management, such changes could impact mining operations in the future.

Tailings Management at Miguel Auza

There are two tailings management facilities (“TMF”) at Miguel Auza. TMF #1 is located immediately northwest of the concentrator and has been decommissioned, rehabilitated with a soil cover and re-vegetated. TMF #2 is located on land owned by Excellon, approximately one kilometer north of the Miguel Auza concentrator. Approval for the construction and operation of the facility was received in Q1 2017. Construction of the stage-2 raise of the TMF #2 was completed in early Q4 2020 and currently has enough capacity to accommodate processing of Platosa’s 2022 production plan.

During Q4 2021, the Company continued work with Golder consulting engineers to draft a Dam-Breach Analysis on TMF #2 stages 1 to 5, which is aligned with the Safety Guidelines (CDA, 2020) from the Canadian Dam Association. The Operations, Maintenance, and Surveillance (OMS) Manual is being updated to be consistent with the Guide to the Management of Tailings Facilities (MAC 2019) from Mining Association of Canada. The Engineer of Record providing tailings-management services, including the design of the stage-3A raise of TMF #2, is a Canadian-based international engineering firm that was engaged by the Company in early 2021.

| 16 | Page |

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

Summary of Quarterly Financial Results

Annual financial statement highlights for the previous three years are as follows:

| (in $000’s) | 2021 | 2020 | 2019 | |||||||||

| Revenues | 37,955 | 26,202 | 26,469 | |||||||||

| Production costs (1) | (26,207 | ) | (19,981 | ) | (23,216 | ) | ||||||

| Depletion and amortization | (7,300 | ) | (4,649 | ) | (4,708 | ) | ||||||

| Cost of sales | (33,507 | ) | (24,630 | ) | (27,924 | ) | ||||||

| Gross profit (loss) | 4,448 | 1,572 | (1,455 | ) | ||||||||

| Expenses: | ||||||||||||

| General and administrative | (6,689 | ) | (6,896 | ) | (4,822 | ) | ||||||

| Exploration and holding expense | (7,194 | ) | (4,032 | ) | (3,853 | ) | ||||||

| Other (expense) income | (758 | ) | (373 | ) | 782 | |||||||

| Provision for litigation | (22,282 | ) | - | - | ||||||||

| Impairment loss | (16,540 | ) | - | - | ||||||||

| Net finance (expense) income | (3,680 | ) | (2,508 | ) | 295 | |||||||

| Income tax expense | (5,078 | ) | (3,783 | ) | (1,022 | ) | ||||||

| Net loss for the year | (57,773 | ) | (16,020 | ) | (10,075 | ) | ||||||

| Adjusted loss for the year (2) | (14,311 | ) | (16,020 | ) | (10,075 | ) | ||||||

| Loss per share – basic and diluted | (1.77 | ) | (0.55 | ) | (0.49 | ) | ||||||

| Adjusted loss per share (2) | (0.44 | ) | (0.55 | ) | (0.49 | ) | ||||||

| Operating cash flows before changes in working capital | 1,652 | (3,733 | ) | (4,314 | ) | |||||||

| Total assets | 41,560 | 73,279 | 55,582 | |||||||||

| Total liabilities | 46,047 | 22,837 | 13,390 | |||||||||

| Total equity | (4,487 | ) | 50,442 | 42,192 | ||||||||

| Non-current liabilities | 11,896 | 10,845 | 3,842 | |||||||||

| (1) | 2021 production costs include $1.6 million related to future mine closure accruals. |

| (2) | 2021 adjusted loss and adjusted loss per share excludes $22.3 million related to the Provision for litigation, impairment losses of $16.5 million, deferred-tax asset derecognition of $3.1 million and $1.6 million related to future mine closure accruals. |

| 17 | Page |

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

Financial statement highlights for the quarter ended December 31, 2021 and the last eight quarters are as follows:

Q4 2021 | Q3 2021 | Q2 2021 | Q1 2021 | Q4 2020 | Q3 2020 | Q2 2020 | Q1 2020 | |||||||||||||||||||||||||

| (in $000’s) | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||

| Revenues (1) | 9,306 | 9,151 | 9,717 | 9,781 | 10,097 | 9,857 | 687 | 5,561 | ||||||||||||||||||||||||

| Production costs (2) | (8,673 | ) | (5,567 | ) | (5,814 | ) | (6,153 | ) | (5,986 | ) | (5,875 | ) | (2,641 | ) | (5,479 | ) | ||||||||||||||||

| Depletion and amortization | (1,928 | ) | (1,809 | ) | (1,773 | ) | (1,790 | ) | (1,445 | ) | (1,269 | ) | (666 | ) | (1,269 | ) | ||||||||||||||||

| Cost of sales | (10,601 | ) | (7,376 | ) | (7,587 | ) | (7,943 | ) | (7,431 | ) | (7,144 | ) | (3,307 | ) | (6,748 | ) | ||||||||||||||||

| Gross profit (loss) | (1,295 | ) | 1,775 | 2,130 | 1,838 | 2,666 | 2,713 | (2,620 | ) | (1,187 | ) | |||||||||||||||||||||

| Expenses: | ||||||||||||||||||||||||||||||||

| General and administrative | (1,255 | ) | (1,453 | ) | (1,640 | ) | (2,342 | ) | (1,886 | ) | (1,502 | ) | (2,345 | ) | (1,163 | ) | ||||||||||||||||

| Exploration and holding expense | (1,783 | ) | (2,538 | ) | (1,800 | ) | (1,073 | ) | (1,400 | ) | (2,001 | ) | (258 | ) | (373 | ) | ||||||||||||||||

| Other income (expense) (1) | 89 | (6 | ) | (188 | ) | (651 | ) | (6 | ) | (934 | ) | 1,172 | (605 | ) | ||||||||||||||||||

| Provision for Litigation | (5 | ) | (22,277 | ) | - | - | - | - | - | - | ||||||||||||||||||||||

| Impairment loss | (15,788 | ) | (752 | ) | - | - | - | - | - | - | ||||||||||||||||||||||

| Net finance (expense) income | (1,242 | ) | (688 | ) | (1,025 | ) | (725 | ) | (679 | ) | (292 | ) | 554 | (2,091 | ) | |||||||||||||||||

| Income tax (expense) recovery | (167 | ) | (4,921 | ) | (22 | ) | 31 | (4,703 | ) | 1,776 | 97 | (953 | ) | |||||||||||||||||||

| Net loss | (21,446 | ) | (30,860 | ) | (2,545 | ) | (2,922 | ) | (6,008 | ) | (240 | ) | (3,400 | ) | (6,372 | ) | ||||||||||||||||

| Adjusted loss (3) | (4,069 | ) | (4,775 | ) | (2,545 | ) | (2,922 | ) | (6,008 | ) | (240 | ) | (3,400 | ) | (6,372 | ) | ||||||||||||||||

| Loss per share | (0.65 | ) | (0.94 | ) | (0.08 | ) | (0.09 | ) | (0.19 | ) | (0.01 | ) | (0.12 | ) | (0.28 | ) | ||||||||||||||||

| Adjusted loss per share (3) | (0.12 | ) | (0.15 | ) | (0.08 | ) | (0.09 | ) | (0.19 | ) | (0.01 | ) | (0.12 | ) | (0.28 | ) | ||||||||||||||||

| Net cash from operations before working capital changes | (217 | ) | (9 | ) | 959 | 919 | 1,931 | 223 | (4,038 | ) | (1,849 | ) | ||||||||||||||||||||

| (1) | Refer to Note 18 of the Q1 2021 Condensed Consolidated Financial Statements for detail of the revision of the 2020 quarterly financial information related to the reclassification of foreign exchange differences on provisionally priced sales. |

| (2) | Q4 2021 production costs include $1.6 million related to future mine closure accruals. |

| (3) | Q4 2021 adjusted loss and adjusted loss per share excludes impairment losses of $15.8 million and $1.6 million related to future mine closure accruals (included in Production costs). Q3 2021 adjusted loss and adjusted loss per share excludes $22.3 million related to the Provision for litigation, the related $0.8 million impairment loss and $3.1 million deferred-tax asset derecognition expenses (included in Income tax expense). |

Quarter to quarter revenue variances are a function of metal prices, treatment and refining costs and production results. Production results can differ from period to period depending on geology, mining conditions, labour and equipment availability. These, in turn, affect mined tonnages, grades and mill recoveries and, ultimately, the quantity of metal produced and revenues received. The Company currently expenses exploration costs related to Platosa (unless associated with resource expansion), Silver City, Kilgore and Evolución. These exploration costs do not relate to the mining operation and vary from period to period, creating volatility in earnings. The following is a discussion of the material variances between Q4 2021 and Q4 2020 and the year ended December 31, 2021 versus the year ended December 31, 2020.

| Q4 | Year ended December 31, | |||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||

| Revenue | 9,306 | 10,097 | 37,955 | 26,202 | ||||||||||||

| Gross profit (loss) (1) | (1,295 | ) | 2,666 | 4,448 | 1,572 | |||||||||||

| Adjusted loss (2) | (4,069 | ) | (6,008 | ) | (14,311 | ) | (16,020 | ) | ||||||||

| 18 | Page |

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

| (1) | Q4 2021 and 2021 gross loss includes $1.6 million related to future mine closure accruals, adjusting to remove the impact of these accruals would result in gross profit of $0.3 million in Q4 2021 and $6.0 million in 2021. |

| (2) | Q4 2021 adjusted loss excludes impairment losses of $15.8 million and $1.6 million related to future mine closure cost accruals. In addition, 2021 adjusted loss and adjusted loss per share excludes the $22.3 million Provision for litigation expense, and the related impairment losses of $0.8 million and $3.1 million in deferred-tax asset derecognition. |

Revenues decreased by $0.8 million or 8% during Q4 2021 compared to Q4 2020, driven by a 4% decrease in AgEq ounces payable and a 5% decrease in the realized silver price, partly offset by a 22% and 26% increase in realized lead and zinc prices, respectively. Revenues for the 12-month period increased by $11.8 million or 45%, driven by a 21% increase in AgEq ounces payable and a 16%, 20% and 27% increase in the realized silver, lead and zinc price, respectively, compared to the prior year. As discussed above, the Suspension resulted in negligible metal sales and revenue during Q2 2020, impacting 2020 results.

Gross profit decreased by $4.0 million in Q4 2021 relative to Q4 2020. This variance was primarily driven by the $0.8 million decrease in revenue, $0.5 million related to increased depletion and amortization and a $2.7 million increase in production costs, which included $1.6 million related to future mine closure accruals. Gross profit improved by $2.9 million for the 12-month period, driven by higher revenues of $11.8 million as discussed earlier, partly offset by increased production, depletion and amortization costs (increased by $6.2 million and $2.7 million, respectively) following the Suspension in Q2 2020.

Adjusted loss decreased by $1.9 million in Q4 2021 over Q4 2020, despite the $4.0 million decrease in gross profit discussed above, and mainly driven by the lower income tax expense by $4.5 million, general and administrative expenses by $0.6 million, partly offset by increased finance and exploration expenses of $0.6 million and $0.4 million respectively. For the 12-Mos 2021, adjusted loss decreased by $1.7 million, mainly driven by the $2.9 million improvement in gross profit in 2021 as discussed above, and a $1.8 million decrease in income tax expenses (after adjusting for the deferred-tax asset derecognition related to the Provision for litigation), partially offset by an increase of $3.2 million in exploration and holding expenses and $1.2 million increase in finance expenses, relative to 2020.

| Q4 | Year ended December 31, | |||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||

| Cost of sales | 10,601 | 7,431 | 33,507 | 24,630 | ||||||||||||

The components of cost of sales including production costs and depletion and amortization charges are as follows:

| Labour | 1,666 | 1,607 | 6,241 | 5,120 | ||||||||||||

| Consumables | 1,176 | 924 | 4,080 | 2,923 | ||||||||||||

| Electricity | 1,524 | 1,297 | 6,113 | 5,575 | ||||||||||||

| Transport | 467 | 454 | 2,034 | 1,544 | ||||||||||||

| Other operational | 777 | 790 | 2,534 | 1,910 | ||||||||||||

| Mine and mill administrative | 1,072 | 626 | 4,044 | 2,766 | ||||||||||||

| Inventory adjustment | 407 | 288 | (423 | ) | 143 | |||||||||||

| Incremental future mine closure accruals | 1,584 | - | 1,584 | - | ||||||||||||

| Production costs (including inventory adjustments) | 8,673 | 5,986 | 26,207 | 19,981 | ||||||||||||

| Depletion and amortization | 1,928 | 1,445 | 7,300 | 4,649 | ||||||||||||

| Cost of sales | 10,601 | 7,431 | 33,507 | 24,630 |

| 19 | Page |

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

Production costs increased by $2.7 million or 45% during Q4 2021 relative to Q4 2020, mainly driven by $1.6 million incremental accruals related to future mine closure costs, $0.3 million increase in consumables and $0.2 million increase in electricity costs reflecting increased consumption due to the expansion of the dewatering system and higher unit costs driven by increased natural gas prices.

For the 12-Mos 2021, production costs increased by $6.2 million or 31% relative to 2020, mostly reflecting increased tonnage mined and processed 2021 as tonnage produced in 2020 was substantially reduced by the Suspension. Production costs in 12-Mos 2021 were increased relative to 2020 by production bonuses ($0.3 million impact) tied to higher mine productivity, higher costs for electricity ($0.5 million) reflecting the impact of supply shocks and natural-gas price spikes during the Q1 2021 polar vortex in the southwestern U.S., higher accrued costs ($0.4 million) for increased profit-sharing obligations pursuant to labour law reforms in Mexico during Q3 2021 and $1.6 million related to future mine closure cost accruals.

Despite cost pressures during 2021, optimizations made at Platosa in mid-2020 contributed to the offsetting of production costs including: (i) a 30% reduction in workforce from restructuring amid the Suspension ($1.2 million gross annual savings), partially offset by higher bonus payments to unionized workers due to the improved production profile from Q3 2020 onward; (ii) the change to a private, natural gas-generated electricity supplier ($2.0 million gross annual savings), initially realizing a 30% drop in effective power costs to $0.06/kWh although higher natural gas prices have partly offset this saving; and (iii) improved offtake terms on concentrate sales.

Depletion and amortization expense in Q4 2021 was $0.5 million higher than Q4 2020, due to the amortization of assets commissioned since Q4 2020; while the $2.7 million increase in depletion and amortization expense in the 12-Mos 2021 reflects a 29% increase in production and related depletion compared to 2020, which had lower production due to the Suspension.

| Q4 | Year ended December 31, | |||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||

| Exploration and holding expense | 1,783 | 1,400 | 7,194 | 4,032 | ||||||||||||

Increased exploration and holding expense in Q4 2021 primarily reflects increased drilling expenditures at the Silver City Project of $0.4 million. Holding expense includes concession and mineral claim fees of $0.1 million in Q4 2021 and $0.7 million in 12-Mos 2021 (Q4 2020 – $0.1 million; 12-Mos 2020 – $0.6 million). Exploration commenced at the Oakley Project during Q2 2021, with expenditures funded and accounted for by Centerra pursuant to the Oakley Agreement.

Exploration programs were limited by the initial outbreak of COVID-19 globally in 2020 resulting in lower expenditures during 2020. In 2021 the Company invested $2.4 million in exploration and holding costs at Platosa and Evolución in Mexico (2020 – $1.6 million), $1.6 million at Kilgore in Idaho, USA (2020 – $0.7 million) and $3.2 million at Silver City in Saxony, Germany (2020 – $1.7 million). Refer to “Exploration and Evaluation Review,” above, for a summary of the Company’s exploration work during the period.

| 20 | Page |

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

| Q4 | Year ended December 31, | |||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||

| General and administrative expense | 1,255 | 1,886 | 6,689 | 6,896 | ||||||||||||

General and administrative expense decreased by $0.6 million or 34% in Q4 2021 driven by lower share-based payment expenses in Q4 2021 ($0.2 million) and the $0.3 million impact of the Company’s listing on the NYSE American in Q4 2020. Overall, general and administrative expenses decreased by $0.2 million for 12-Mos 2021 reflecting decreases in share-based payment expenses ($0.3 million) and corporate development and legal costs ($0.5 million), partly offset by increases in salaries ($0.1 million) and higher insurance expense ($0.4 million) due to the listing on the NYSE American in Q3 2020.

| Other (income) expense | (89 | ) | 6 | 758 | 373 |

Other expense includes realized and unrealized foreign exchange gains and losses, unrealized gains and losses on marketable securities and warrants, interest income and other non-routine income or expenses, if any.

Other expenses in Q4 2021 are consistent with Q4 2020. The 12-month variance of $0.4 million reflects changes in the values of marketable securities and warrants, which had high market values and unrealized gains of $0.6 million in 2020 but lower market values and unrealized losses of $0.9 million in 2021, partly offset by a decrease in foreign exchange losses of $0.7 million between these periods.

| Impairment loss | 15,788 | - | 16,540 | - |

On January 5, 2022, the Company announced that it was assessing the economic viability of mining at Platosa beyond mid-2022. Underground and surface drilling continued throughout Q1 2022. Based on these results and consideration of current and expected economic factors, the Company now expects to wind down operations at Platosa during Q3 2022, subject to results from ongoing exploration programs. In Q4 2021 the Company recorded an impairment loss of $15.8 million (Q4 2020 – $Nil) on the Platosa Mine and Miguel Auza processing facility. In Q3 2021, the Company had recorded an impairment loss of $0.8 million on Miguel Auza reflecting the impact of the Judgment against San Pedro.

| Finance expense | 1,242 | 679 | 3,680 | 2,508 |

Net finance expense in Q4 2021 comprises primarily $1.1 million of interest expense on the 5.75% secured convertible debentures (the “Convertible Debentures”) issued in Q3 2020, which are recorded at amortized cost and accreted to the principal amount over the term of the Convertible Debentures. This interest expense consists of $0.4 million in coupon interest at a 10% rate, paid in common shares at the Company’s election (Q4 2020 – $0.4 million), and $0.7 million of accretion of the face value of the Convertible Debentures (Q4 2020 – $0.4 million). Net finance expenses for Q4 2020 included a $0.2 million unrealized gain on currency hedges, which have since been settled at a net realized loss of $40,000.

Net finance expense of $3.7 million for 12-Mos 2021 is $1.2 million higher than the comparative period. Interest on the Convertible Debentures, increased by $2.2 million of which $0.8 million relates to coupon interest (paid in shares), and $1.4 million relates to non-cash accretion interest expense. This increase was partially offset by a $0.4 million unrealized loss on currency hedges in 2020, which have since been settled at a net realized loss of $40,000 and $0.7 million interest in 2020 on the $6 million credit facility with Sprott Private Resource Lending II (Collector), LP (the “Credit Facility”) which was repaid in Q3 2020.

| 21 | Page |

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

Provisionally Priced Sales

Sales are recorded using the metal price received for sales that settle during the reporting period. For sales that have not been settled, an estimate is used, based on the expected month of settlement and the forward price of the metal at the end of the reporting period. The difference between the estimate and the final price received is recognized by adjusting sales in the period in which the sale is settled (i.e. the finalization adjustment). The finalization adjustment recorded for these sales depends on the actual price when the sale settles, which occurs in the first, third or fourth month after shipment under the terms of the current concentrate purchase agreements.

Invoiced revenues are derived from the value of payable metal content net of treatment and refining charges (“TC/RCs”) incurred by the metallurgical complex of the customer. TC/RCs are a cost associated with processing of metal concentrates in refined metal products, though such cost is deducted from gross revenues rather than incurred as a cost of sales (as revenue received by the Company is net of TC/RCs). Therefore, as discussed in the calculation of total cash cost per silver ounce payable, below, TC/RCs are added to cost of sales to reflect the total cost of producing a payable silver ounce. Offtake agreements may also include price participation for the offtaker for settlements at metal prices above specified levels. The value of the metal content of the products sold is as follows (in $’000s):

| Three months ended | Twelve months ended | |||||||||||||||

| December 31 | December 31 | |||||||||||||||

| 2021 | 2020(2) | 2021 | 2020 | |||||||||||||

| $ | $ | $ | $ | |||||||||||||

| Silver | 6,726 | 8,378 | 28,265 | 20,625 | ||||||||||||

| Lead | 1,939 | 1,756 | 7,250 | 5,022 | ||||||||||||

| Zinc | 2,734 | 2,635 | 9,935 | 6,899 | ||||||||||||

| Value of metal content in products sold (1) | 11,399 | 12,769 | 45,450 | 32,546 | ||||||||||||

| Adjustment for treatment and refining charges (TC/RC) | (2,093 | ) | (2,672 | ) | (7,495 | ) | (6,840 | ) | ||||||||

| Revenues from concentrate sales | 9,306 | 10,097 | 37,955 | 25,706 | ||||||||||||

| Revenues from toll milling services | - | - | - | 496 | ||||||||||||

| Total revenues | 9,306 | 10,097 | 37,955 | 26,202 | ||||||||||||

| (1) | Value of metal content in products sold is a non-IFRS measure. |

| (2) | Refer to Note 18 of the Q1 2021 Condensed Consolidated Financial Statements for detail of the revision of the 2020 quarterly financial information related to the reclassification of foreign exchange differences on provisionally priced sales. |

Production Cost Per Tonne, Total Cash Cost Net of By-Product Credits Per Silver Ounce Payable, All-In Sustaining Cost (AISC) Per Silver Ounce Payable and Adjusted loss and adjusted loss per share are non-IFRS measures that do not have a standardized meaning. The calculation of these measures may differ from that used by other companies in the industry. The Company uses these measures internally to evaluate the underlying operating performance of the Company for the reporting periods presented. These measures should not be considered in isolation or as a substitute for measures of performance prepared in accordance with generally accepted accounting principles and are not necessarily indicative of operating expenses as determined under generally accepted accounting principles. Management believes that these measures are key performance indicators of the Company’s operational efficiency and are increasingly used across the global mining industry and are intended to provide investors with information about the cash generating capabilities of the Company’s operations.

| 22 | Page |

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

| Q4 | Year ended December 31, | |||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||

| Production cost per tonne | $ | 314 | $ | 252 | $ | 291 | $ | 299 | ||||||||

A reconciliation between production cost per tonne (excluding depletion and amortization and inventory adjustments) and the Company’s cost of sales as reported in the Company’s financial statements is provided below. Changes in inventories of ore and concentrate are excluded from the calculation of Production Cost per Tonne. Changes in inventories reflect the net cost of ore stockpiles and concentrate inventory (i) sold during the current period but produced in a previous period (an addition to direct mining and milling costs) or (ii) produced but not sold in the current period (a deduction from direct mining and milling costs). Excluding changes in inventories and future mine closure accruals aligns cost of sales incurred during the period with the tonnage produced during the period.

| $ 000’s | $ 000’s | $ 000’s | $ 000’s | |||||||||||||

| Cost of sales | 10,601 | 7,431 | 33,507 | 24,630 | ||||||||||||

| Adjustments – increase/(decrease): | ||||||||||||||||

| San Sebastián processing cost (Hecla bulk sample) | - | - | - | (234 | ) | |||||||||||

| Future mine closure accruals | (1,584 | ) | - | (1,584 | ) | - | ||||||||||

| Depletion and amortization | (1,928 | ) | (1,445 | ) | (7,300 | ) | (4,649 | ) | ||||||||

| Changes in inventories | (407 | ) | (288 | ) | 423 | (143 | ) | |||||||||

| Production costs (excluding inventory adjustments) | 6,682 | 5,698 | 25,046 | 19,604 | ||||||||||||

| Tonnes milled | 21,309 | 22,626 | 86,021 | 65,567 | ||||||||||||

| Production cost per tonne milled ($/tonne) | $ | 314 | $ | 252 | $ | 291 | $ | 299 |

Production cost per tonne milled increased by 25% in Q4 2021 relative to Q4 2020 due to a 6% decrease in tonnes milled in Q4 2021 and a 17% increase in production costs, as discussed under “Cost of Sales” above.

Production cost per tonne milled decreased by 3% for 12-Mos 2021 as 12-Mos 2020 was impacted by the negligible tonnage produced in Q2 2020 due to the Suspension.

| Q4 | Year ended December 31, | |||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||

| Total cash cost per silver ounce payable | $ | 15.61 | $ | 12.73 | $ | 13.01 | $ | 15.38 | ||||||||

The calculation of total cash cost per silver ounce payable reflects the cost of production adjusted for by-product credits and various non-cash costs included in cost of sales, particularly:

| (i) | changes in inventories of ore and concentrate are reflected in cost of sales to match cost of sales with the revenues from payable metals in the period by either allocating the cost of metal produced in prior periods or deferring the cost of metal to be sold in future periods; |

| (ii) | TC/RCs are added to cost of sales to reflect the total cost of producing a payable silver ounce as, per industry standard, revenues received by the Company are net of TC/RCs; and |

| (iii) | Future mine closure related costs are excluded from cost of sales. |

The Company expects total cash costs net of by-product revenues to vary from period to period as planned production and underground development access different areas of the mine with varying grades and characteristics.

| 23 | Page |

Management’s Discussion & Analysis of Financial Results

For the year ended December 31, 2021

The following is a reconciliation of total cash cost per silver ounce payable, net of by-product credits, to cost of sales as reported in the Company’s financial statements:

| Q4 | Year ended December 31, | |||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||

| $ 000’s | $ 000’s | $ 000’s | $ 000’s | |||||||||||||

| Cost of sales | 10,601 | 7,431 | 33,507 | 24,630 | ||||||||||||

| Adjustments – increase/(decrease): | ||||||||||||||||

| San Sebastián processing cost (Hecla bulk sample) | - | - | - | (234 | ) | |||||||||||

| Future mine closure related costs | (1,584 | ) | - | (1,584 | ) | - | ||||||||||

| Depletion and amortization | (1,928 | ) | (1,445 | ) | (7,300 | ) | (4,649 | ) | ||||||||

| TC/RCs | 2,094 | 2,285 | 7,495 | 6,840 | ||||||||||||

| Royalties (1) | (15 | ) | (235 | ) | (83 | ) | (388 | ) | ||||||||

| By-product credits (2) | (4,673 | ) | (3,924 | ) | (17,185 | ) | (11,922 | ) | ||||||||