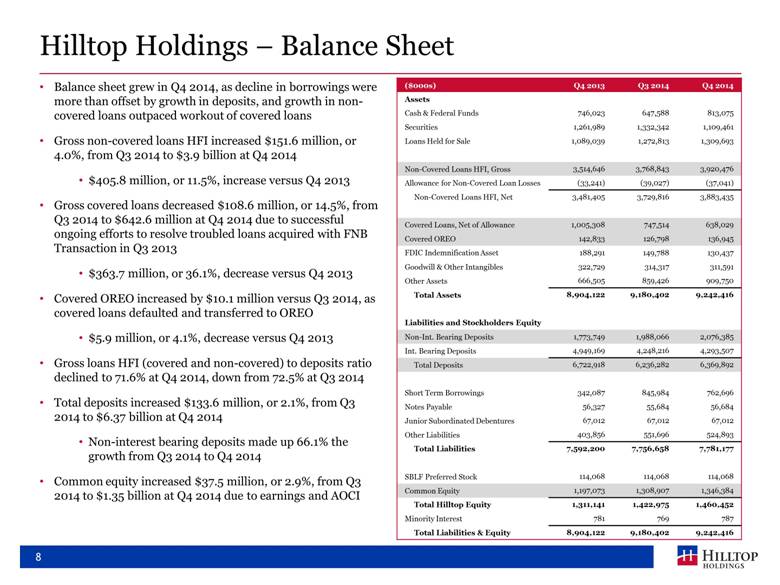

| Hilltop Holdings – Balance Sheet Balance sheet grew in Q4 2014, as decline in borrowings were more than offset by growth in deposits, and growth in non-covered loans outpaced workout of covered loans Gross non-covered loans HFI increased $151.6 million, or 4.0%, from Q3 2014 to $3.9 billion at Q4 2014 $405.8 million, or 11.5%, increase versus Q4 2013 Gross covered loans decreased $108.6 million, or 14.5%, from Q3 2014 to $642.6 million at Q4 2014 due to successful ongoing efforts to resolve troubled loans acquired with FNB Transaction in Q3 2013 $363.7 million, or 36.1%, decrease versus Q4 2013 Covered OREO increased by $10.1 million versus Q3 2014, as covered loans defaulted and transferred to OREO $5.9 million, or 4.1%, decrease versus Q4 2013 Gross loans HFI (covered and non-covered) to deposits ratio declined to 71.6% at Q4 2014, down from 72.5% at Q3 2014 Total deposits increased $133.6 million, or 2.1%, from Q3 2014 to $6.37 billion at Q4 2014 Non-interest bearing deposits made up 66.1% the growth from Q3 2014 to Q4 2014 Common equity increased $37.5 million, or 2.9%, from Q3 2014 to $1.35 billion at Q4 2014 due to earnings and AOCI 8 ($000s) Q4 2013 Q3 2014 Q4 2014 Assets Cash & Federal Funds 746,023 647,588 813,075 Securities 1,261,989 1,332,342 1,109,461 Loans Held for Sale 1,089,039 1,272,813 1,309,693 Non-Covered Loans HFI, Gross 3,514,646 3,768,843 3,920,476 Allowance for Non-Covered Loan Losses (33,241) (39,027) (37,041) Non-Covered Loans HFI, Net 3,481,405 3,729,816 3,883,435 Covered Loans, Net of Allowance 1,005,308 747,514 638,029 Covered OREO 142,833 126,798 136,945 FDIC Indemnification Asset 188,291 149,788 130,437 Goodwill & Other Intangibles 322,729 314,317 311,591 Other Assets 666,505 859,426 909,750 Total Assets 8,904,122 9,180,402 9,242,416 Liabilities and Stockholders Equity Non-Int. Bearing Deposits 1,773,749 1,988,066 2,076,385 Int. Bearing Deposits 4,949,169 4,248,216 4,293,507 Total Deposits 6,722,918 6,236,282 6,369,892 Short Term Borrowings 342,087 845,984 762,696 Notes Payable 56,327 55,684 56,684 Junior Subordinated Debentures 67,012 67,012 67,012 Other Liabilities 403,856 551,696 524,893 Total Liabilities 7,592,200 7,756,658 7,781,177 SBLF Preferred Stock 114,068 114,068 114,068 Common Equity 1,197,073 1,308,907 1,346,384 Total Hilltop Equity 1,311,141 1,422,975 1,460,452 Minority Interest 781 769 787 Total Liabilities & Equity 8,904,122 9,180,402 9,242,416 |