UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21460

Pioneer Series Trust II

(Exact name of registrant as specified in charter)

60 State Street, Boston, MA 02109

(Address of principal executive offices) (ZIP code)

Christopher J. Kelley, Amundi Asset Management, Inc.,

60 State Street, Boston, MA 02109

(Name and address of agent for service)

Registrant’s telephone number, including area code: (617) 742-7825

Date of fiscal year end: December 31, 2022

Date of reporting period: January 1, 2022 through December 31, 2022

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

Pioneer AMT-Free Municipal Fund

Annual Report | December 31, 2022

visit us: www.amundi.com/us

Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/221

President’s Letter

Dear Shareholders,

On February 13, 2023 Amundi US celebrated the 95th anniversary of Pioneer Fund, the second-oldest mutual fund in the United States. We recognized the anniversary with ringing of the closing bell at the New York Stock Exchange, which seemed fitting for this special milestone.

Pioneer Fund was launched on February 13, 1928 by Phil Carret, the father of value investing and a leading innovator in the asset management industry. Mr. Carret began investing in the 1920s and founded Pioneer Investments (now Amundi US) in 1928, and was one of the first investors to realize he could uncover value through rigorous, innovative, fundamental research techniques.

Consistent with Mr. Carret’s investment philosophy, Pioneer Fund focuses on investing in what the managers believe are high-quality companies with sustainable business models and attractive long-term growth and income potential across the spectrum of large-cap growth and value companies. The current portfolio management team is led by Jeff Kripke, who has been in that role since 2015. Employing many of the same techniques utilized in the 1920s, Jeff and his team have adapted Mr. Carret’s philosophy to a new age of “Active” investing.

The last few years have seen investors face some unprecedented challenges, from a global pandemic that shuttered much of the world’s economy for months, to geopolitical strife, to rising inflation that has reached levels not seen in decades. Now, more than ever, Amundi US believes active management – that is, making active investment decisions, not just in managing Pioneer Fund, but across all of our portfolios – can help mitigate the risks during periods of market volatility.

At Amundi US, active management begins with our own fundamental, bottom-up research process. Our team of dedicated research analysts and portfolio managers analyzes each security under consideration, communicating frequently with the management teams of the companies and other entities issuing the securities, and working together to identify those securities that we believe best meet our investment criteria for our family of funds. Our risk management approach begins with each security under consideration, as we strive to develop a deep understanding of the potential opportunity, while considering any potential risk factors.

2Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/22

Today, as shareholders, we have many options. It is our view that active management can serve shareholders well, not only when markets are thriving, but also during periods of market stress. As you consider your long-term investment goals, we encourage you to work with your financial professional to develop an investment plan that paves the way for you to pursue both your short-term and long-term goals.

We greatly appreciate the trust you have placed in us and look forward to continuing to serve you in the future.

Lisa M. Jones

Head of the Americas, President and CEO of US

Amundi Asset Management US, Inc.

February 2023

Any information in this shareowner report regarding market or economic trends or the factors influencing the Fund’s historical or future performance are statements of opinion as of the date of this report. Past performance is no guarantee of future results.

Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/223

Portfolio Management Discussion | 12/31/22

In the following interview, Lead Portfolio Manager David Eurkus outlines the investment environment for tax-free bonds during the 12-month period ended December 31, 2022, and the factors that affected the performance of Pioneer AMT-Free Municipal Fund during the period. Mr. Eurkus, a Managing Director, Director of Municipals, and a portfolio manager at Amundi Asset Management US, Inc. (Amundi US), is responsible for the day-to-day management of the Fund, along with Jonathan Chirunga, a Managing Director, Director of High-Yield Municipals, and a portfolio manager at Amundi US.

| Q | How did the Fund perform during the 12-month period ended December 31, 2022? |

| A | Pioneer AMT-Free Municipal Fund’s Class A shares returned -17.05% at net asset value during the 12-month period ended December 31, 2022, while the Fund’s benchmark, the Bloomberg Municipal Bond Index (the Bloomberg Index), returned -8.53%. During the same 12-month period, the average return of the 168 mutual funds in Morningstar’s Municipal National Long Funds Category was -11.88%. |

| Q | How would you describe the investment environment in the municipal bond market during the 12-month period ended December 31, 2022? |

| A | Consistent with the negative returns for the broader fixed-income market, municipal issues suffered unusually poor performance in 2022. |

| | Two main factors played a role in the market’s sizable downturn. First the US Federal Reserve (Fed) sought to combat inflation by ending its pandemic-era quantitative-easing program and raising interest rates. The Fed increased the target range of its benchmark federal funds rate seven times over the course of the calendar year, bringing the target range from a starting point of 0.00%‒0.25% at the beginning of the 12-month period, to 4.25%‒4.50% by year-end. These represented the most aggressive increases in short-term interest rates since the early 1980s. Government bond yields rose sharply in response. The 10-year US Treasury note, which came into 2022 with a yield of 1.44%, had climbed to 3.88% by year-end. |

4Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/22

| | The second major factor in the underperformance of municipal bonds, and fixed-income securities in general, was that the rise in prevailing yields was accompanied by increasing yield spreads for municipals relative to US Treasuries. (Yield, or credit spreads, are commonly defined as the differences in yields between Treasuries and other types of fixed-income securities with similar maturities.) The combination of Russia’s major new invasion of Ukraine in February 2022, ongoing supply-chain disruptions, and questions about the direction of the US economy led to underperformance for the bond market’s “spread sectors” in relation to Treasuries over the period. (Spread sectors are nongovernmental fixed-income market sectors that typically offer higher yields, at greater risk, than governmental investments.) Investors’ increasing aversion to riskier assets also contributed to substantial outflows from the municipal market, which further weighed on the prices of municipal bonds. Longer-dated municipal bonds were particularly poor performers over the 12-month period, due to their above-average sensitivity to changes in interest rates. Similarly, higher-quality bonds – which have typically been more vulnerable to moves in prevailing rates than lower-quality issues – underperformed the overall market. |

| | Despite these headwinds, municipal bond market fundamentals remained firm during the period, in our view, aided by the gradual reopening of the economy, the lingering effects of substantial federal aid packages enacted during the pandemic in 2020-2021, and steady tax receipts. In addition, the default rate in the municipal market remained low over the calendar year, which we believe helps to illustrate the gap between price performance and underlying issuer strength. |

| Q | What factors affected the Fund’s performance relative to the benchmark Bloomberg Index during the 12-month period ended December 31, 2022? |

| A | The Fund’s benchmark-relative underperformance for the period was entirely the result of its long-duration stance versus the Bloomberg Index, which amplified the adverse effects of rising yields. (Duration is a measure of the sensitivity of the price, or the value of principal, of a fixed-income investment to a change in interest rates, expressed as a number of years.) The negative effects of the portfolio’s long-duration positioning were |

Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/225

| | especially pronounced in the “AAA” and “AA” credit-rating tiers. Our preference for investing the Fund in revenue bonds over general obligation (GO) bonds was another detractor from relative returns during the period. However, we believe the former category offers defensive characteristics, due to the dedicated revenue streams associated with revenue bonds. We have remained selective with regard to investing the portfolio in GO bonds, with an emphasis on issuers with improving demographics, strong local economies, and above-average exposure to science- and technology-related industries. |

| | During a period of significant underperformance, no specific investments or strategies stood out as positive contributors to the Fund’s relative returns over the full 12-month period, although the portfolio’s overweights to “AAA” and “AA” municipals did help relative results in the first half of the period, as higher-quality municipal bonds outperformed in the second calendar quarter of 2022. Those positive effects soon wore off, however, as higher-quality municipals ended up underperforming the overall market for the full 12-month period, due to their interest-rate sensitivity. |

| Q | Did the Fund’s distributions*to shareholders change during the 12-month period ended December 31, 2022? |

| A | The Fund’s monthly distribution rate increased over the 12-month period, particularly over the final six months, reflecting the replacement of portfolio securities that had matured or been called away with municipal bonds offered at higher prevailing yields. |

| Q | Did the Fund have any exposure to derivative securities during the 12-month period ended December 31, 2022? |

| A | No. The Fund had no exposure to derivatives during the period. |

| Q | What is your investment outlook? |

| A | We see the potential for further market volatility given the broad uncertainty surrounding inflation, Fed monetary policies, and developments on the geopolitical front. However, credit conditions have remained stable across the municipal bond space, |

| * | Distributions are not guaranteed. |

6Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/22

| | and we foresee very low odds of a wholesale rise in default risk. The ratio of ratings upgrades to downgrades within the municipal market has remained favorable as well. In our view, those factors indicate that the recent weakness in prices has not been accompanied by a meaningful decline in market fundamentals. In addition, we have seen record tax payments into states, as well as budget surpluses. Meanwhile, even as corporate and government debt levels have risen significantly since the financial crisis of 2008, the municipal bond market has continued to hover at around $4 trillion in outstanding debt over time. |

| | We would also note that the market downturn in 2022 has caused the ratio of tax-exempt yields to US Treasury yields to rise, which has often been, historically, an indication of improving value in the market. Not least, current expectations are that the large amount of municipal debt scheduled to mature in the coming year may provide continued support for the supply-and-demand outlook. |

| | We have continued to position the Fund’s portfolio with investments in sectors vital to the US economy, including hospitals, public/private universities, and transportation issuers (such as toll roads). We have maintained a bias toward municipal bonds rated AA and AAA, as we believe a focus on higher-quality issues may enhance capital preservation at a time of elevated recession risk. |

| | Finally, despite the benchmark-relative underperformance over the past year caused mainly by duration positioning, we have maintained the Fund’s long-duration stance versus the Bloomberg Index, as non-traditional sources of volatility in the fixed-income market ‒ such as inflation spikes caused by the policy responses to COVID-19 as well as geopolitical instability from the war in Ukraine ‒ have been key drivers of the sharp increase in interest rates. We believe the steepening yield curve has created attractive values in longer-term bonds, as the yield ratios of municipal bonds-to-Treasuries on the 30-year portion of the curve have reached levels well above historical averages. |

Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/227

Please refer to the Schedule of Investments on pages 17–33 for a full listing of Fund securities.

All investments are subject to risk, including the possible loss of principal. In the past several years, financial markets have experienced increased volatility and heightened uncertainty. The market prices of securities may go up or down, sometimes rapidly or unpredictably, due to general market conditions, such as real or perceived adverse economic, political, or regulatory conditions, recessions, inflation, changes in interest or currency rates, lack of liquidity in the bond markets, the spread of infectious illness or other public health issues, armed conflict including Russia's military invasion of Ukraine, sanctions against Russia, other nations or individuals or companies and possible countermeasures, market disruptions caused by tariffs, trade disputes or other government actions, or adverse investor sentiment. These conditions may continue, recur, worsen or spread.

The market price of securities may fluctuate when interest rates change. When interest rates rise, the prices of fixed-income securities in the Fund will generally fall. Conversely, when interest rates fall, the prices of fixed-income securities in the Fund will generally rise.

Investments in the Fund are subject to possible loss due to the financial failure of issuers of underlying securities and their inability to meet their debt obligations.

The value of municipal securities can be adversely affected by changes in financial condition of municipal issuers, lower revenues, and regulatory and political developments.

A portion of income may be subject to local, state, federal, and/or alternative minimum tax. Capital gains, if any, are subject to a capital gains tax.

At times, the Fund's investments may represent industries or sectors that are interrelated or have common risks, making them more susceptible to any economic, political, or regulatory developments or other risks affecting those industries and sectors.

Before investing, consider the product’s investment objectives, risks, charges and expenses. Contact your investment professional or Amundi Asset Management US, Inc., for a prospectus or summary prospectus containing this information. Read it carefully.

Any information in this shareholder report regarding market or economic trends or the factors influencing the Fund’s historical or future performance are statements of opinion as of the date of this report. Past performance is not a guarantee of future results.

8Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/22

Portfolio Summary | 12/31/22

Portfolio Diversification

(As a percentage of total investments)*

State Diversification

(As a percentage of total investments)*

10 Largest Holdings

| (As a percentage of total investments)* |

| 1. | Central Puget Sound Regional Transit Authority Green Bond, Series S-1, 5.00%, 11/1/46 | 2.64% |

| 2. | Massachusetts Development Finance Agency Harvard University, Series A, 5.00%, 7/15/40 | 2.61 |

| 3. | Board of Regents of the University of Texas System, Series B, 5.00%, 8/15/49 | 2.52 |

Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/229

Portfolio Summary | 12/31/22

| (As a percentage of total investments)* |

| 4. | Brookhaven Development Authority Children's Healthcare Of Atlanta, Inc., Series A, 4.00%, 7/1/49 | 1.71% |

| 5. | Pennsylvania Turnpike Commission, Series A, 4.00%, 12/1/51 | 1.62 |

| 6. | Tobacco Settlement Financing Corp., Series B-1, 5.00%, 6/1/47 | 1.52 |

| 7. | County of Miami-Dade Water & Sewer System Revenue, Series B, 4.00%, 10/1/49 | 1.50 |

| 8. | Hillsborough County Industrial Development Authority Tampa General Hospital, 3.50%, 8/1/55 | 1.32 |

| 9. | Massachusetts Health & Educational Facilities Authority Massachusetts Institute of Technology, Series K, 5.50%, 7/1/32 | 1.31 |

| 10. | New Jersey Health Care Facilities Financing Authority, 4.00%, 7/1/51 | 1.30 |

| | |

| * | Excludes short-term investments and all derivative contracts except for options purchased. The Fund is actively managed, and current holdings may be different. The holdings listed should not be considered recommendations to buy or sell any securities. |

+ Amount rounds to less than 0.1%.

10Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/22

Prices and Distributions | 12/31/22

Net Asset Value per Share

| Class | 12/31/22 | 12/31/21 |

| A | $12.67 | $15.63 |

| C | $12.56 | $15.49 |

| Y | $12.61 | $15.57 |

| | | |

Distributions per Share: 1/1/22 - 12/31/22

| Class | Net

Investment

Income | Short-Term

Capital Gains | Long-Term

Capital Gains |

| A | $0.3040 | $— | $— |

| C | $0.1963 | $— | $— |

| Y | $0.3423 | $— | $— |

Index Definitions

The Bloomberg Municipal Bond Index is an unmanaged, broad measure of the municipal bond market. Index returns are calculated monthly, assume reinvestment of dividends and do not reflect any fees, expenses or sales charges. It is not possible to invest directly in an index.

The index defined here pertains to the “Value of $10,000 Investment” and “Value of $5 Million Investment” charts on pages 12–14.

Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/2211

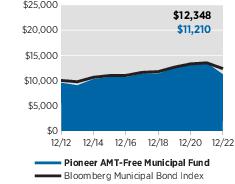

| Performance Update | 12/31/22 | Class A Shares |

Investment Returns

The mountain chart on the right shows the change in value of a $10,000 investment made in Class A shares of Pioneer AMT-Free Municipal Fund at public offering price during the periods shown, compared to that of the Bloomberg Municipal Bond Index.

Average Annual Total Returns

(As of December 31, 2022) |

| Period | Net

Asset

Value

(NAV) | Public

Offering

Price

(POP) | Bloomberg

Municipal

Bond Index |

| 10 Years | 1.62% | 1.15% | 2.13% |

| 5 Years | -0.30 | -1.21 | 1.25 |

| 1 Year | -17.05 | -20.81 | -8.53 |

Expense Ratio

(Per prospectus dated April 1, 2022) |

| Gross |

| 0.79% |

Value of $10,000 Investment

Call 1-800-225-6292 or visit www.amundi.com/us for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate, and shares, when redeemed, may be worth more or less than their original cost.

NAV results represent the percent change in net asset value per share. POP returns reflect deduction of the maximum 4.50% sales charge. NAV returns would have been lower had sales charges been reflected. All results are historical and assume the reinvestment of dividends and capital gains. Other share classes are available for which performance and expenses will differ.

Performance results reflect any applicable expense waivers in effect during the periods shown. Without such waivers Fund performance would be lower. Waivers may not be in effect for all funds. Certain fee waivers are contractual through a specified period. Otherwise, fee waivers can be rescinded at any time. See the prospectus and financial statements for more information.

The performance table and graph do not reflect the deduction of fees and taxes that a shareowner would pay on Fund distributions or the redemption of Fund shares.

Please refer to the financial highlights for a more current expense ratio.

12Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/22

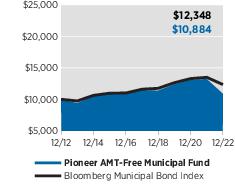

| Performance Update | 12/31/22 | Class C Shares |

Investment Returns

The mountain chart on the right shows the change in value of a $10,000 investment made in Class C shares of Pioneer AMT-Free Municipal Fund during the periods shown, compared to that of the Bloomberg Municipal Bond Index.

Average Annual Total Returns

(As of December 31, 2022) |

| Period | If

Held | If

Redeemed | Bloomberg

Municipal

Bond Index |

| 10 Years | 0.85% | 0.85% | 2.13% |

| 5 Years | -1.04 | -1.04 | 1.25 |

| 1 Year | -17.68 | -18.50 | -8.53 |

Expense Ratio

(Per prospectus dated April 1, 2022) |

| Gross |

| 1.53% |

Value of $10,000 Investment

Call 1-800-225-6292 or visit www.amundi.com/us for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate, and shares, when redeemed, may be worth more or less than their original cost.

Class C shares held for less than one year are also subject to a 1% contingent deferred sales charge (CDSC). “If Held” results represent the percent change in net asset value per share. “If Redeemed” returns reflect deduction of the CDSC for the one-year period, assuming a complete redemption of shares at the last price calculated on the last business day of the period, and no CDSC for the five- and 10-year periods. All results are historical and assume the reinvestment of dividends and capital gains. Other share classes are available for which performance and expenses will differ.

Performance results reflect any applicable expense waivers in effect during the periods shown. Without such waivers Fund performance would be lower. Waivers may not be in effect for all funds. Certain fee waivers are contractual through a specified period. Otherwise, fee waivers can be rescinded at any time. See the prospectus and financial statements for more information.

The performance table and graph do not reflect the deduction of fees and taxes that a shareowner would pay on Fund distributions or the redemption of Fund shares.

Please refer to the financial highlights for a more current expense ratio.

Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/2213

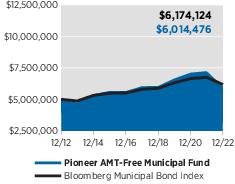

| Performance Update | 12/31/22 | Class Y Shares |

Investment Returns

The mountain chart on the right shows the change in value of a $5 million investment made in Class Y shares of Pioneer AMT-Free Municipal Fund during the periods shown, compared to that of the Bloomberg Municipal Bond Index.

Average Annual Total Returns

(As of December 31, 2022) |

| Period | Net

Asset

Value

(NAV) | Bloomberg

Municipal

Bond Index |

| 10 Years | 1.86% | 2.13% |

| 5 Years | -0.08 | 1.25 |

| 1 Year | -16.88 | -8.53 |

Expense Ratio

(Per prospectus dated April 1, 2022) |

| Gross | Net |

| 0.59% | 0.49% |

Value of $5 Million Investment

Call 1-800-225-6292 or visit www.amundi.com/us for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate, and shares, when redeemed, may be worth more or less than their original cost.

Class Y shares are not subject to sales charges and are available for limited groups of eligible investors, including institutional investors. All results are historical and assume the reinvestment of dividends and capital gains. Other share classes are available for which performance and expenses will differ.

Performance results reflect any applicable expense waivers in effect during the periods shown. Without such waivers Fund performance would be lower. Waivers may not be in effect for all funds. Certain fee waivers are contractual through a specified period. Otherwise, fee waivers can be rescinded at any time. See the prospectus and financial statements for more information.

The net expense ratio reflects the contractual expense limitation currently in effect through May 1, 2025 for Class Y shares. There can be no assurance that Amundi US will extend the expense limitations beyond such time. Please see the prospectus and financial statements for more information.

Please refer to the financial highlights for more current expense ratios.

14Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/22

Comparing Ongoing Fund Expenses

As a shareowner in the Fund, you incur two types of costs:

| (1) | ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Fund expenses; and |

| (2) | transaction costs, including sales charges (loads) on purchase payments. |

This example is intended to help you understand your ongoing expenses (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 at the beginning of the Fund’s latest six-month period and held throughout the six months.

Using the Tables

Actual Expenses

The first table below provides information about actual account values and actual expenses. You may use the information in this table, together with the amount you invested, to estimate the expenses that you paid over the period as follows:

| (1) | Divide your account value by $1,000

Example: an $8,600 account value ÷ $1,000 = 8.6 |

| (2) | Multiply the result in (1) above by the corresponding share class’s number in the third row under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period. |

Expenses Paid on a $1,000 Investment in Pioneer AMT-Free Municipal Fund

Based on actual returns from July 1, 2022 through December 31, 2022.

| Share Class | A | C | Y |

Beginning Account

Value on 7/1/22 | $1,000.00 | $1,000.00 | $1,000.00 |

Ending Account Value

(after expenses) on 12/31/22 | $976.30 | $972.80 | $977.60 |

Expenses Paid

During Period* | $3.89 | $7.71 | $2.44 |

| | |

| * | Expenses are equal to the Fund’s annualized expense ratio of 0.78%, 1.55%, and 0.49% for Class A, Class C, and Class Y shares, respectively, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the partial year period). |

Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/2215

Comparing Ongoing Fund Expenses (continued)

Hypothetical Example for Comparison Purposes

The table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the tables are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as sales charges (loads) that are charged at the time of the transaction. Therefore, the table below is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

Expenses Paid on a $1,000 Investment in Pioneer AMT-Free Municipal Fund

Based on a hypothetical 5% return per year before expenses, reflecting the period from July 1, 2022 through December 31, 2022.

| Share Class | A | C | Y |

Beginning Account

Value on 7/1/22 | $1,000.00 | $1,000.00 | $1,000.00 |

Ending Account Value

(after expenses) on 12/31/22 | $1,021.27 | $1,017.39 | $1,022.74 |

Expenses Paid

During Period* | $3.97 | $7.88 | $2.50 |

| | |

| * | Expenses are equal to the Fund’s annualized expense ratio of 0.78%, 1.55%, and 0.49% for Class A, Class C, and Class Y shares, respectively, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the partial year period). |

16Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/22

Schedule of Investments | 12/31/22

Principal

Amount

USD ($) | | | | | | Value |

| | UNAFFILIATED ISSUERS — 99.7% | |

| | Municipal Bonds — 99.7% of Net Assets(a) | |

| | Arizona — 0.3% | |

| 3,940,000 | Arizona Industrial Development Authority, 3.00%, 2/1/45 | $ 2,922,850 |

| | Total Arizona | $ 2,922,850 |

| | California — 6.2% | |

| 10,000,000(b) | Alameda Corridor Transportation Authority, California Revenue Capital Appreciation Senior Lien, 10/1/31 (NATL Insured) | $ 7,522,600 |

| 16,695,000(b)(c) | Anaheim Public Financing Authority, Public Improvements Project, Series C, 9/1/36 (AGM Insured) | 10,126,686 |

| 36,350,000(b) | California County Tobacco Securitization Agency, Capital Appreciation, Stanislaus County, Subordinated, Series D, 6/1/55 | 2,732,066 |

| 6,400,000 | California Educational Facilities Authority, Stanford University, Series U6, 5.00%, 5/1/45 | 7,363,648 |

| 2,985,000 | California Educational Facilities Authority, Stanford University, Series U-7, 5.00%, 6/1/46 | 3,435,048 |

| 2,000,000 | City of Oroville, Oroville Hospital, 5.25%, 4/1/49 | 1,936,240 |

| 3,000,000 | Long Beach Bond Finance Authority, Series A, 5.50%, 11/15/37 | 3,264,900 |

| 2,180,000(d) | Pomona Unified School District, Series A, 6.55%, 8/1/29 (NATL Insured) | 2,396,430 |

| 5,000,000(d)(e) | San Diego Unified School District, Series R2, 6.63%, 7/1/40 | 4,346,650 |

| 3,500,000 | San Francisco City & County Airport Comm-San Francisco International Airport, Series B, 5.00%, 5/1/47 | 3,629,150 |

| 7,000,000(d) | State of California, 3.00%, 10/1/49 | 5,349,470 |

| 12,000,000 | University of California, Series BH, 4.00%, 5/15/46 | 11,597,640 |

| 7,130,000 | University of California, Series Q, 4.00%, 5/15/41 | 7,105,402 |

| | Total California | $ 70,805,930 |

| | Colorado — 2.0% | |

| 7,040,000 | Colorado Health Facilities Authority, Advent Health Obligated Group, Series A, 3.00%, 11/15/51 | $ 5,151,590 |

| 5,000,000 | Dominion Water & Sanitation District, 5.875%, 12/1/52 | 4,908,800 |

| 5,000,000 | Metro Wastewater Reclamation District, Series A, 2.50%, 4/1/45 | 3,388,700 |

| 5,000,000 | University of Colorado, Series 2, 4.00%, 6/1/38 | 4,992,400 |

| 5,000,000 | University of Colorado, Series 2, 4.00%, 6/1/39 | 4,918,200 |

| | Total Colorado | $ 23,359,690 |

The accompanying notes are an integral part of these financial statements.

Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/2217

Schedule of Investments | 12/31/22 (continued)

Principal

Amount

USD ($) | | | | | | Value |

| | Connecticut — 0.5% | |

| 2,000,000 | Mohegan Tribal Finance Authority, 7.00%, 2/1/45 (144A) | $ 2,003,780 |

| 5,985,000(d) | State of Connecticut, Series B, 2.00%, 6/1/36 | 4,307,943 |

| | Total Connecticut | $ 6,311,723 |

| | District of Columbia — 1.6% | |

| 10,000,000 | District of Columbia Tobacco Settlement Financing Corp., Asset-Backed, 6.75%, 5/15/40 | $ 10,305,000 |

| 84,000,000(b) | District of Columbia Tobacco Settlement Financing Corp., Asset-Backed, Series C, 6/15/55 | 7,549,080 |

| | Total District of Columbia | $ 17,854,080 |

| | Florida — 11.1% | |

| 2,935,000 | Broward County Water & Sewer Utility Revenue, Series A, 3.00%, 10/1/41 | $ 2,398,746 |

| 5,000,000 | Central Florida Expressway Authority, Senior Lien, 2.125%, 7/1/36 (AGM Insured) | 3,785,900 |

| 1,000,000 | Central Florida Expressway Authority, Senior Lien, 5.00%, 7/1/39 | 1,042,090 |

| 2,615,000 | City of Tampa, Baycare Health Care, Series A, 5.00%, 11/15/46 | 2,647,949 |

| 6,145,000 | County of Hillsborough, 3.00%, 8/1/41 | 5,063,050 |

| 5,375,000 | County of Hillsborough Utility Revenue, 3.00%, 8/1/36 | 5,084,642 |

| 4,500,000 | County of Hillsborough Utility Revenue, 3.00%, 8/1/37 | 4,014,360 |

| 3,500,000 | County of Hillsborough Utility Revenue, Series A, 2.00%, 8/1/40 | 2,452,345 |

| 2,360,000(d) | County of Miami-Dade, Series A, 4.00%, 7/1/38 | 2,366,584 |

| 2,455,000(d) | County of Miami-Dade, Series A, 4.00%, 7/1/39 | 2,455,295 |

| 10,000,000 | County of Miami-Dade Water & Sewer System Revenue, Series B, 3.00%, 10/1/49 | 7,398,000 |

| 18,500,000 | County of Miami-Dade Water & Sewer System Revenue, Series B, 4.00%, 10/1/49 | 16,990,955 |

| 2,500,000 | County of Orange, Water Utility System Revenue, 3.00%, 10/1/32 | 2,466,075 |

| 4,645,000 | County of Orange, Water Utility System Revenue, 3.00%, 10/1/34 | 4,503,188 |

| 20,000,000 | Hillsborough County Industrial Development Authority, Tampa General Hospital, 3.50%, 8/1/55 | 14,993,400 |

| 1,000,000 | Sarasota County Public Hospital District, Sarasota Memorial Hospital Project, 4.00%, 7/1/48 | 916,170 |

| 15,000,000 | Sarasota County Public Hospital District, Sarasota Memorial Hospital Project, 4.00%, 7/1/52 | 13,246,200 |

The accompanying notes are an integral part of these financial statements.

18Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/22

Principal

Amount

USD ($) | | | | | | Value |

| | Florida — (continued) | |

| 16,500,000 | State of Florida, Department of Transportation Turnpike System Revenue, Series B, 3.00%, 7/1/49 | $ 12,283,095 |

| 5,000,000 | State of Florida, Department of Transportation Turnpike System Revenue, Series B, 4.00%, 7/1/47 | 4,954,050 |

| 4,645,000(d) | State of Florida, Department Transportation Right of Way, Series A, 3.25%, 7/1/37 | 4,389,479 |

| 7,660,000(d) | State of Florida, Department Transportation Right of Way, Series A, 4.00%, 7/1/39 | 7,705,041 |

| 5,000,000 | State of Florida Department of Transportation Turnpike System Revenue, 4.00%, 7/1/43 | 4,911,700 |

| | Total Florida | $ 126,068,314 |

| | Georgia — 5.0% | |

| 1,500,000 | Brookhaven Development Authority, Children's Healthcare Of Atlanta, Inc., Series A, 3.00%, 7/1/46 | $ 1,176,105 |

| 4,800,000 | Brookhaven Development Authority, Children's Healthcare Of Atlanta, Inc., Series A, 4.00%, 7/1/44 | 4,623,456 |

| 20,665,000 | Brookhaven Development Authority, Children's Healthcare Of Atlanta, Inc., Series A, 4.00%, 7/1/49 | 19,336,654 |

| 2,040,000(d) | County of Fulton, Library Bond, 3.25%, 7/1/37 | 1,847,302 |

| 2,870,000(d) | County of Fulton, Library Bond, 3.50%, 7/1/39 | 2,607,682 |

| 4,790,000(d) | County of Fulton, Library Bond, 4.00%, 7/1/40 | 4,684,859 |

| 10,000,000 | County of Fulton Water & Sewerage Revenue, Series A, 2.25%, 1/1/42 | 7,097,300 |

| 4,000,000 | Forsyth County Water & Sewerage Authority, 3.00%, 4/1/44 | 3,222,160 |

| 4,000,000 | Gainesville & Hall County Hospital Authority, Series A, 4.00%, 2/15/51 | 3,586,160 |

| 2,000,000 | Main Street Natural Gas, Inc., Series A, 4.00%, 5/15/39 | 1,837,100 |

| 5,000,000 | Metropolitan Atlanta Rapid Transit Authority, Series C, 3.50%, 7/1/38 | 4,561,650 |

| 2,750,000 | Private Colleges & Universities Authority, Emory University, Series A, 5.00%, 10/1/43 | 2,767,600 |

| | Total Georgia | $ 57,348,028 |

| | Illinois — 1.0% | |

| 1,000,000 | Illinois Finance Authority, Art Institute Of Chicago, 4.00%, 3/1/38 | $ 982,430 |

| 1,500,000 | Illinois Finance Authority, Northwestern Memorial Healthcare, Series A, 4.00%, 7/15/36 | 1,504,545 |

| 2,175,000 | Illinois Finance Authority, Northwestern Memorial Healthcare, Series A, 4.00%, 7/15/37 | 2,174,456 |

| 3,000,000 | Illinois Finance Authority, Northwestern Memorial Healthcare, Series A, 4.00%, 7/15/47 | 2,778,690 |

The accompanying notes are an integral part of these financial statements.

Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/2219

Schedule of Investments | 12/31/22 (continued)

Principal

Amount

USD ($) | | | | | | Value |

| | Illinois — (continued) | |

| 90,000 | Illinois Finance Authority, Presence Health Network, Series C, 5.00%, 2/15/33 | $ 95,033 |

| 1,000,000 | Illinois Finance Authority, Presence Health Network, Series C, 5.00%, 2/15/36 | 1,050,910 |

| 2,595,000(c) | Metropolitan Pier & Exposition Authority, Mccormick Place Convention, 7.00%, 7/1/26 | 2,786,745 |

| | Total Illinois | $ 11,372,809 |

| | Indiana — 0.3% | |

| 3,000,000 | Indiana University, Series A, 4.00%, 6/1/42 | $ 2,950,260 |

| | Total Indiana | $ 2,950,260 |

| | Maine — 0.4% | |

| 1,250,000 | Maine Health & Higher Educational Facilities Authority, Series C, 5.125%, 7/1/52 (AGM ST AID WITHHLDG Insured) | $ 1,298,462 |

| 1,000,000 | Maine Health & Higher Educational Facilities Authority, Series C, 5.50%, 7/1/47 (AGM ST AID WITHHLDG Insured) | 1,071,700 |

| 1,000,000 | Maine Turnpike Authority, 3.00%, 7/1/40 | 808,310 |

| 1,250,000 | Maine Turnpike Authority, 4.00%, 7/1/45 | 1,201,038 |

| | Total Maine | $ 4,379,510 |

| | Maryland — 2.6% | |

| 7,415,000(d) | County of Anne Arundel, 3.00%, 10/1/44 | $ 5,821,813 |

| 900,000(f) | Maryland Economic Development Corp., Senior Lien-Chesapeake Bay, Series A, 5.00%, 12/1/16 | 537,750 |

| 400,000(f) | Maryland Economic Development Corp., Senior Lien-Chesapeake Bay, Series B, 5.00%, 12/1/16 | 239,000 |

| 3,745,000 | University System of Maryland, Series A, 4.00%, 4/1/41 | 3,665,643 |

| 5,175,000 | Washington Suburban Sanitary Commission, Consolidated Public Improvement, 3.00%, 6/1/35 (CNTY GTD Insured) | 4,761,673 |

| 5,180,000 | Washington Suburban Sanitary Commission, Consolidated Public Improvement, 3.00%, 6/1/37 (CNTY GTD Insured) | 4,553,427 |

| 6,165,000 | Washington Suburban Sanitary Commission, Consolidated Public Improvement, 3.00%, 6/1/45 (CNTY GTD Insured) | 4,959,188 |

| 6,000,000 | Washington Suburban Sanitary Commission, Consolidated Public Improvement, 3.00%, 6/1/47 (CNTY GTD Insured) | 4,720,440 |

| | Total Maryland | $ 29,258,934 |

The accompanying notes are an integral part of these financial statements.

20Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/22

Principal

Amount

USD ($) | | | | | | Value |

| | Massachusetts — 17.4% | |

| 3,485,000(d) | Cape Cod Regional Technical High School District, School Project Loan Chapter 70 B, 4.00%, 11/15/37 | $ 3,503,924 |

| 3,485,000(d) | Cape Cod Regional Technical High School District, School Project Loan Chapter 70 B, 4.00%, 11/15/38 | 3,493,050 |

| 1,475,000(d) | City of Attleboro, Municipal Purpose Loan, 3.125%, 2/15/35 | 1,413,153 |

| 1,520,000(d) | City of Attleboro, Municipal Purpose Loan, 3.25%, 2/15/36 | 1,450,414 |

| 1,565,000(d) | City of Attleboro, Municipal Purpose Loan, 3.25%, 2/15/37 | 1,478,409 |

| 1,055,000(d) | City of Beverly, 3.125%, 10/15/39 | 913,335 |

| 5,075,000(d) | City of Cambridge, Municipal Purpose Loan, 3.00%, 2/15/35 | 4,964,010 |

| 1,860,000(d) | City of Revere, 2.125%, 9/1/41 (ST AID WITHHLDG Insured) | 1,225,256 |

| 2,000,000(d) | City of Revere, 2.25%, 9/1/43 (ST AID WITHHLDG Insured) | 1,296,820 |

| 4,875,000(d) | City of Somerville, 2.125%, 10/15/40 | 3,425,906 |

| 4,980,000(d) | City of Somerville, 2.125%, 10/15/41 | 3,403,083 |

| 3,765,000(d) | City of Somerville, 4.00%, 5/1/52 | 3,603,067 |

| 15,000,000(d) | Commonwealth of Massachusetts, Series C, 2.75%, 3/1/50 | 10,237,800 |

| 1,300,000(d) | Concord & Carlisle Regional School District, 3.00%, 3/15/29 | 1,300,689 |

| 1,300,000(d) | Concord & Carlisle Regional School District, 3.00%, 3/15/31 | 1,294,488 |

| 1,300,000(d) | Concord & Carlisle Regional School District, 3.00%, 3/15/33 | 1,283,399 |

| 7,345,000(d) | Dennis-Yarmouth Regional School District, 2.375%, 10/1/51 | 4,409,424 |

| 1,500,000 | Massachusetts Development Finance Agency, Berklee College Music, 5.00%, 10/1/35 | 1,584,060 |

| 4,000,000 | Massachusetts Development Finance Agency, Boston University, Series X, 5.00%, 10/1/48 | 4,017,640 |

| 12,690,000 | Massachusetts Development Finance Agency, Broad Institute, 4.00%, 4/1/41 | 12,571,602 |

| 2,000,000 | Massachusetts Development Finance Agency, Broad Institute, 5.00%, 4/1/37 | 2,141,860 |

| 25,865,000 | Massachusetts Development Finance Agency, Harvard University, Series A, 5.00%, 7/15/40 | 29,566,799 |

| 2,500,000 | Massachusetts Development Finance Agency, Lawrence General Hospital, Series A, 5.50%, 7/1/44 | 2,091,975 |

| 4,000,000 | Massachusetts Development Finance Agency, Lowell General Hospital, Series G, 5.00%, 7/1/44 | 4,017,880 |

The accompanying notes are an integral part of these financial statements.

Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/2221

Schedule of Investments | 12/31/22 (continued)

Principal

Amount

USD ($) | | | | | | Value |

| | Massachusetts — (continued) | |

| 400,000 | Massachusetts Development Finance Agency, Milford Regional Medical Center, Series F, 5.625%, 7/15/36 | $ 381,552 |

| 500,000 | Massachusetts Development Finance Agency, Milford Regional Medical Center, Series F, 5.75%, 7/15/43 | 452,440 |

| 450,000 | Massachusetts Development Finance Agency, Northeastern University, Series A, 5.00%, 3/1/39 | 457,614 |

| 8,000,000 | Massachusetts Development Finance Agency, Partner’s Healthcare System, 4.00%, 7/1/35 | 8,047,600 |

| 5,000,000 | Massachusetts Development Finance Agency, Partner’s Healthcare System, 4.00%, 7/1/41 | 4,798,300 |

| 2,700,000 | Massachusetts Development Finance Agency, Partner’s Healthcare System, Series 1, 4.00%, 7/1/45 | 2,544,831 |

| 875,000(g) | Massachusetts Development Finance Agency, Tufts University, Series Q, 4.00%, 8/15/38 | 876,120 |

| 1,000,000 | Massachusetts Development Finance Agency, Wellforce, Series C, 3.00%, 10/1/45 (AGM Insured) | 743,140 |

| 6,600,000 | Massachusetts Development Finance Agency, WGBH Educational Foundation, Series A, 5.75%, 1/1/42 (AMBAC Insured) | 8,331,246 |

| 4,080,000(b) | Massachusetts Development Finance Agency, WGBH Educational Foundation, Series B, 1/1/38 (AGC Insured) | 2,098,344 |

| 835,000 | Massachusetts Development Finance Agency, Woods Hole Oceanographic Institution, 5.00%, 6/1/38 | 900,648 |

| 1,000,000 | Massachusetts Development Finance Agency, Woods Hole Oceanographic Institution, 5.00%, 6/1/43 | 1,067,890 |

| 500,000 | Massachusetts Development Finance Agency, Woods Hole Oceanographic Institution, 5.00%, 6/1/48 | 528,905 |

| 11,950,000 | Massachusetts Health & Educational Facilities Authority, Massachusetts Institute of Technology, Series K, 5.50%, 7/1/32 | 14,778,565 |

| 2,000,000 | Massachusetts School Building Authority, Series A, 3.00%, 8/15/38 | 1,737,000 |

| 2,500,000 | Massachusetts School Building Authority, Series A, 4.00%, 8/15/40 | 2,464,125 |

| 2,420,000 | Massachusetts Water Resources Authority, General, Series B, 5.25%, 8/1/36 (AGM Insured) | 2,947,052 |

| 10,000,000(d) | Town of Brookline, 3.00%, 3/15/45 | 7,916,100 |

| 4,000,000(d) | Town of Hingham, 2.00%, 2/15/40 | 2,743,960 |

| 1,000,000(d) | Town of Hingham, 3.00%, 2/15/36 | 905,060 |

The accompanying notes are an integral part of these financial statements.

22Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/22

Principal

Amount

USD ($) | | | | | | Value |

| | Massachusetts — (continued) | |

| 1,600,000(d) | Town of Lexington, Municipal Purpose Loan, 3.125%, 2/1/36 | $ 1,457,984 |

| 1,150,000(d) | Town of Lexington, Municipal Purpose Loan, 3.125%, 2/1/37 | 1,028,893 |

| 1,635,000(d) | Town of Lexington, Municipal Purpose Loan, 3.25%, 2/1/38 | 1,459,957 |

| 5,000,000(d) | Town of Natick, Municipal Purpose Loan, 4.00%, 7/15/37 | 5,078,250 |

| 1,955,000(d) | Town of Norwood, Municipal Purpose Loan, 2.125%, 7/15/30 | 1,779,519 |

| 2,000,000(d) | Town of Plymouth, Municipal Purpose Loan, 3.00%, 5/1/31 | 1,955,220 |

| 1,535,000(d) | Town of Plymouth, Municipal Purpose Loan, 3.375%, 5/1/32 | 1,529,505 |

| 1,265,000(d) | Town of Plymouth, Municipal Purpose Loan, 3.50%, 5/1/35 | 1,238,410 |

| 3,500,000(d) | Town of Plymouth, Municipal Purpose Loan, 3.50%, 5/1/44 | 3,009,195 |

| 4,160,000(d) | Town of Stoughton, Municipal Purpose Loan, 3.00%, 10/15/37 | 3,740,131 |

| 1,000,000(d) | Town of Wellesley, Municipal Purpose Loan, 4.00%, 6/1/41 | 936,770 |

| 4,000,000(d) | Town of Wellesley, Municipal Purpose Loan, 4.00%, 6/1/45 | 3,649,800 |

| 2,370,000(d) | Town of Weymouth, 2.00%, 8/15/41 | 1,603,305 |

| | Total Massachusetts | $ 197,875,474 |

| | Michigan — 0.7% | |

| 10,000,000 | Michigan State Building Authority, Series I, 3.00%, 10/15/45 | $ 7,908,200 |

| | Total Michigan | $ 7,908,200 |

| | Minnesota — 1.3% | |

| 5,000,000 | City of Rochester, Health Care Facilities, Mayo Clinic, 4.00%, 11/15/48 | $ 4,775,250 |

| 5,350,000 | City of Rochester, Mayo Clinic, Series B, 5.00%, 11/15/36 | 6,328,836 |

| 2,000,000 | Minneapolis-St Paul Metropolitan Airports Commission, Series A, 4.25%, 1/1/52 | 1,908,680 |

| 1,800,000(d) | State of Minnesota, Series B, 2.00%, 8/1/34 | 1,531,818 |

| | Total Minnesota | $ 14,544,584 |

The accompanying notes are an integral part of these financial statements.

Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/2223

Schedule of Investments | 12/31/22 (continued)

Principal

Amount

USD ($) | | | | | | Value |

| | Missouri — 0.3% | |

| 4,000,000 | Health & Educational Facilities Authority of the State of Missouri, Mercy Health, Series F, 4.00%, 11/15/45 | $ 3,662,800 |

| | Total Missouri | $ 3,662,800 |

| | Nevada — 0.6% | |

| 3,500,000(d) | Las Vegas Valley Water District, Series A, 4.00%, 6/1/43 | $ 3,375,400 |

| 5,000,000(d) | State of Nevada, Series A, 2.00%, 5/1/41 | 3,317,000 |

| | Total Nevada | $ 6,692,400 |

| | New Hampshire — 1.2% | |

| 2,000,000(d) | City of Manchester, Series A, 2.00%, 6/15/33 | $ 1,687,660 |

| 5,000,000 | New Hampshire Health and Education Facilities Authority Act, Series A, 5.00%, 8/1/59 | 4,963,900 |

| 4,000,000 | New Hampshire Health and Education Facilities Authority Act, Catholic Medical Centre, 3.75%, 7/1/40 | 3,386,800 |

| 1,185,000 | New Hampshire Municipal Bond Bank, Series A, 2.50%, 2/15/47 | 769,882 |

| 3,815,000 | New Hampshire Municipal Bond Bank, Series A, 2.50%, 2/15/51 | 2,336,001 |

| | Total New Hampshire | $ 13,144,243 |

| | New Jersey — 1.7% | |

| 4,000,000 | New Jersey Educational Facilities Authority, Series C, 2.00%, 3/1/38 | $ 2,837,680 |

| 16,000,000 | New Jersey Health Care Facilities Financing Authority, 4.00%, 7/1/51 | 14,712,160 |

| 2,100,000 | New Jersey Turnpike Authority, Series B, 4.50%, 1/1/48 | 2,136,351 |

| | Total New Jersey | $ 19,686,191 |

| | New York — 6.0% | |

| 1,745,000(d) | Massapequa Union Free School District, 2.00%, 10/1/32 (ST AID WITHHLDG Insured) | $ 1,506,389 |

| 1,785,000(d) | Massapequa Union Free School District, 2.00%, 10/1/33 (ST AID WITHHLDG Insured) | 1,497,026 |

| 5,000,000 | New York City Housing Development Corp., 3.05%, 5/1/50 | 3,531,500 |

| 3,000,000 | New York City Housing Development Corp., Series 1, 4.90%, 11/1/57 | 3,063,780 |

| 5,000,000 | New York City Housing Development Corp., Series C, 2.75%, 2/1/51 | 3,316,950 |

| 40,000,000(b) | New York Counties Tobacco Trust, Series F, 6/1/60 | 1,868,000 |

| 10,000,000 | New York State Dormitory Authority, Series A, 3.00%, 3/15/42 | 8,120,000 |

The accompanying notes are an integral part of these financial statements.

24Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/22

Principal

Amount

USD ($) | | | | | | Value |

| | New York — (continued) | |

| 1,000,000 | New York State Dormitory Authority, Series A, 4.00%, 7/1/35 | $ 1,017,930 |

| 6,885,000 | New York State Dormitory Authority, Columbia University, Series A, 5.00%, 10/1/50 | 7,906,390 |

| 10,000,000 | New York State Dormitory Authority, Columbia University, Series A2, 5.00%, 10/1/46 | 11,328,200 |

| 5,515,000 | New York State Dormitory Authority, Insured-FIT Student Housing Corp., 5.25%, 7/1/24 (NATL Insured) | 5,567,723 |

| 4,500,000 | New York State Dormitory Authority, New York University, Series A, 4.00%, 7/1/36 | 4,527,000 |

| 3,250,000 | New York State Dormitory Authority, Trustees of Columbia University, 5.00%, 10/1/45 | 3,711,890 |

| 1,804,085 | New York State Housing Finance Agency, Series 2020-A, 1.65%, 5/15/39 (FNMA Insured) | 1,248,156 |

| 1,000,000 | New York State Housing Finance Agency, Series A-1, 3.95%, 11/1/60 (SONYMA Insured) | 789,380 |

| 5,000,000 | New York State Urban Development Corp., Group 3, Series A, 3.00%, 3/15/49 | 3,699,100 |

| 1,500,000 | Port Authority of New York & New Jersey, Consolidated Ninety-Third Series, 6.125%, 6/1/94 | 1,527,360 |

| 4,935,000(d) | Port Chester-Rye Union Free School District, 2.00%, 6/1/36 (ST AID WITHHLDG Insured) | 3,610,989 |

| | Total New York | $ 67,837,763 |

| | North Carolina — 1.4% | |

| 2,000,000 | City of Charlotte Airport Revenue, Charlotte Douglas International Airport Revenue, Series A, 4.00%, 7/1/47 | $ 1,854,680 |

| 1,000,000 | City of Charlotte Airport Revenue, Charlotte Douglas International Airport Revenue, Series A, 4.00%, 7/1/52 | 911,320 |

| 3,000,000 | City of Charlotte Storm Water Revenue, 4.00%, 12/1/43 | 3,034,170 |

| 3,250,000 | City of Charlotte Water & Sewer System Revenue, 2.25%, 7/1/50 | 2,065,538 |

| 5,920,000 | County of Union, Enterprise System Revenue, 3.00%, 6/1/51 | 4,315,088 |

| 4,615,000(d) | State of North Carolina, Series A, 3.00%, 6/1/35 | 4,339,715 |

| | Total North Carolina | $ 16,520,511 |

| | Ohio — 2.1% | |

| 8,000,000 | Buckeye Tobacco Settlement Financing Authority, Senior Class 2, Series B-2, 5.00%, 6/1/55 | $ 6,892,800 |

The accompanying notes are an integral part of these financial statements.

Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/2225

Schedule of Investments | 12/31/22 (continued)

Principal

Amount

USD ($) | | | | | | Value |

| | Ohio — (continued) | |

| 2,500,000 | Ohio State University, Series A, 4.00%, 12/1/48 | $ 2,387,050 |

| 16,780,000 | State of Ohio, Series A, 4.00%, 1/15/50 | 14,289,848 |

| | Total Ohio | $ 23,569,698 |

| | Oklahoma — 0.1% | |

| 720,000 | McGee Creek Authority, 6.00%, 1/1/23 (NATL Insured) | $ 720,000 |

| | Total Oklahoma | $ 720,000 |

| | Oregon — 2.8% | |

| 1,800,000 | City of Portland, Sewer System Revenue, First Lien, Series A, 2.00%, 6/15/29 | $ 1,626,822 |

| 5,000,000(d) | Clackamas County School District No 7J Lake Oswego, 4.00%, 6/1/43 (SCH BD GTY Insured) | 4,915,850 |

| 15,000,000 | Medford Hospital Facilities Authority, Series A, 3.00%, 8/15/50 (AGM Insured) | 11,542,650 |

| 2,000,000(b)(d) | Multnomah County School District No. 40, Deferred Interest, Series B, 6/15/30 (SCH BD GTY Insured) | 1,599,880 |

| 2,000,000(b)(d) | Multnomah County School District No. 40, Deferred Interest, Series B, 6/15/31 (SCH BD GTY Insured) | 1,535,960 |

| 1,715,000(b)(d) | Multnomah County School District No. 40, Deferred Interest, Series B, 6/15/32 (SCH BD GTY Insured) | 1,264,624 |

| 2,000,000 | Oregon Health & Science University, Series A, 5.00%, 7/1/42 | 2,103,440 |

| 5,000,000 | Oregon Health & Science University, Green Bond, Series A, 3.00%, 7/1/51 | 3,708,300 |

| 5,000,000 | University of Oregon, Series A, 3.50%, 4/1/52 | 4,016,950 |

| | Total Oregon | $ 32,314,476 |

| | Pennsylvania — 7.2% | |

| 825,000 | Chester County Industrial Development Authority, Collegium Charter School, Series A, 5.125%, 10/15/37 | $ 821,799 |

| 175,000 | Chester County Industrial Development Authority, Collegium Charter School, Series A, 5.25%, 10/15/47 | 158,235 |

| 3,725,000 | Delaware County Industrial Development Authority, Chester Charter School Arts Project, Series A, 5.125%, 6/1/46 (144A) | 3,889,757 |

| 5,385,000 | Pennsylvania Higher Educational Facilities Authority, 3.00%, 8/15/47 | 3,942,951 |

| 605,000 | Pennsylvania Higher Educational Facilities Authority, Bryn Mawr College, 4.00%, 12/1/44 | 566,885 |

| 4,750,000 | Pennsylvania Higher Educational Facilities Authority, Thomas Jefferson University, Series A, 5.00%, 9/1/39 | 4,852,458 |

| 1,000,000 | Pennsylvania Housing Finance Agency, Series 129, 3.35%, 10/1/45 | 825,670 |

The accompanying notes are an integral part of these financial statements.

26Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/22

Principal

Amount

USD ($) | | | | | | Value |

| | Pennsylvania — (continued) | |

| 2,000,000 | Pennsylvania Housing Finance Agency, Series 129, 3.40%, 10/1/49 | $ 1,638,440 |

| 2,000,000 | Pennsylvania Turnpike Commission, Series 1, 5.00%, 12/1/42 | 2,043,680 |

| 5,000,000 | Pennsylvania Turnpike Commission, Series 1, 5.00%, 12/1/47 | 5,096,200 |

| 14,890,000 | Pennsylvania Turnpike Commission, Series A, 3.00%, 12/1/51 | 10,618,506 |

| 20,000,000 | Pennsylvania Turnpike Commission, Series A, 4.00%, 12/1/51 | 18,329,000 |

| 2,500,000 | Philadelphia Authority for Industrial Development, Childrens Hospital Philadelphia, 4.00%, 7/1/35 | 2,519,075 |

| 3,750,000 | Philadelphia Authority for Industrial Development, Childrens Hospital Philadelphia, 4.00%, 7/1/36 | 3,757,125 |

| 2,500,000 | Philadelphia Authority for Industrial Development, Childrens Hospital Philadelphia, 4.00%, 7/1/37 | 2,480,575 |

| 3,000,000 | Philadelphia Authority for Industrial Development, Thomas Jefferson University, Series A, 4.00%, 9/1/42 | 2,834,430 |

| 5,015,000 | Swarthmore Borough Authority, Swarthmore College, 5.00%, 9/15/44 | 5,376,581 |

| 1,195,000 | Swarthmore Borough Authority, Swarthmore College, 5.00%, 9/15/45 | 1,279,881 |

| 4,955,000 | Swarthmore Borough Authority, Swarthmore College, Series B, 4.00%, 9/15/42 | 4,902,427 |

| 6,000,000 | Swarthmore Borough Authority, Swarthmore College, Series B, 4.00%, 9/15/49 | 5,700,360 |

| | Total Pennsylvania | $ 81,634,035 |

| | Puerto Rico — 0.2% | |

| 86,254(b)(d) | Commonwealth of Puerto Rico, Series A, 7/1/24 | $ 79,893 |

| 333,599(b)(d) | Commonwealth of Puerto Rico, Series A, 7/1/33 | 180,300 |

| 259,226(d) | Commonwealth of Puerto Rico, Series A-1, 4.00%, 7/1/33 | 224,757 |

| 233,010(d) | Commonwealth of Puerto Rico, Series A-1, 4.00%, 7/1/35 | 196,092 |

| 271,901(d) | Commonwealth of Puerto Rico, Series A-1, 4.00%, 7/1/41 | 212,890 |

| 144,755(d) | Commonwealth of Puerto Rico, Series A-1, 5.25%, 7/1/23 | 144,755 |

| 288,706(d) | Commonwealth of Puerto Rico, Series A-1, 5.375%, 7/1/25 | 291,888 |

| 286,091(d) | Commonwealth of Puerto Rico, Series A-1, 5.625%, 7/1/27 | 291,490 |

The accompanying notes are an integral part of these financial statements.

Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/2227

Schedule of Investments | 12/31/22 (continued)

Principal

Amount

USD ($) | | | | | | Value |

| | Puerto Rico — (continued) | |

| 281,449(d) | Commonwealth of Puerto Rico, Series A-1, 5.625%, 7/1/29 | $ 288,592 |

| 273,369(d) | Commonwealth of Puerto Rico, Series A-1, 5.75%, 7/1/31 | 282,070 |

| | Total Puerto Rico | $ 2,192,727 |

| | Rhode Island — 1.3% | |

| 5,140,000 | Rhode Island Health & Educational Building Corp., Brown University, Series A, 4.00%, 9/1/37 | $ 5,182,456 |

| 7,050,000(h) | Tender Option Bond Trust Receipts/Certificates, RIB, Series 2019-XM072, 2.165%, 9/1/47 (144A) | 6,405,419 |

| 20,000,000(b) | Tobacco Settlement Financing Corp., Asset-Backed, Series B, 6/1/52 | 3,370,200 |

| | Total Rhode Island | $ 14,958,075 |

| | South Carolina — 1.2% | |

| 5,000,000 | City of Charleston Waterworks & Sewer System Revenue, 4.00%, 1/1/49 | $ 4,691,650 |

| 5,000,000(d) | County of Charleston, Series A, 2.00%, 11/1/39 | 3,475,300 |

| 5,675,000 | South Carolina Transportation Infrastructure Bank, Series A, 3.00%, 10/1/33 | 5,351,695 |

| | Total South Carolina | $ 13,518,645 |

| | Texas — 11.0% | |

| 25,000,000 | Board of Regents of the University of Texas System, Series B, 5.00%, 8/15/49 | $ 28,499,250 |

| 3,550,000(b) | Central Texas Regional Mobility Authority, Capital Appreciation, 1/1/26 | 3,171,854 |

| 5,000,000 | Central Texas Regional Mobility Authority, Senior Lien, Series D, 3.00%, 1/1/46 | 3,485,150 |

| 6,500,000 | Central Texas Turnpike System, Series A, 3.00%, 8/15/40 | 5,041,725 |

| 5,000,000 | City of Austin Airport System Revenue, Series A, 5.00%, 11/15/49 | 5,094,850 |

| 5,360,000 | City of Austin Water & Wastewater System Revenue, Series C, 5.00%, 11/15/45 | 5,733,967 |

| 10,000,000 | City of Houston Combined Utility System Revenue, Series C, 2.50%, 11/15/40 | 7,185,300 |

| 3,790,000(d) | County of Williamson, 2.375%, 2/15/37 | 3,000,164 |

| 10,000,000 | Dallas Area Rapid Transit, Series B, 3.00%, 12/1/47 | 7,656,400 |

| 5,000,000 | Dallas Fort Worth International Airport, Series B, 4.00%, 11/1/45 | 4,682,750 |

| 80,000(d) | Eagle Mountain & Saginaw Independent School District, 3.00%, 8/15/29 (PSF-GTD Insured) | 80,015 |

| 10,000,000 | Harris County Cultural Education Facilities Finance Corp., Texas Children's Hospital, 3.00%, 10/1/51 | 7,036,700 |

The accompanying notes are an integral part of these financial statements.

28Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/22

Principal

Amount

USD ($) | | | | | | Value |

| | Texas — (continued) | |

| 1,000,000 | Harris County Cultural Education Facilities Finance Corp., YMCA Greater Houston Area, Series A, 5.00%, 6/1/28 | $ 988,160 |

| 500,000 | Harris County Cultural Education Facilities Finance Corp., YMCA Greater Houston Area, Series A, 5.00%, 6/1/33 | 458,145 |

| 5,000,000(d) | Lubbock-Cooper Independent School District, 4.00%, 2/15/49 (PSF-GTD Insured) | 5,017,250 |

| 2,000,000 | New Hope Cultural Education Facilities Finance Corp., Cardinal Bay, Inc., Village On The Park, Series B, 4.75%, 7/1/51 | 560,000 |

| 5,000,000 | North Texas Tollway Authority, First Tier, Series A, 3.00%, 1/1/38 | 4,214,600 |

| 5,000,000(d) | Port Authority of Houston of Harris County Texas, Series A, 3.00%, 10/1/39 | 4,368,050 |

| 10,000,000(d) | Tarrant County College District, 2.00%, 8/15/37 | 7,358,000 |

| 1,970,000 | Texas Department of Housing & Community Affairs, Series A, 2.45%, 7/1/46 (GNMA Insured) | 1,410,540 |

| 1,295,000 | Texas Department of Housing & Community Affairs, Series A, 3.50%, 7/1/34 (GNMA/FNMA Insured) | 1,321,185 |

| 1,625,000 | Texas Department of Housing & Community Affairs, Series A, 3.80%, 7/1/39 (GNMA/FNMA Insured) | 1,552,866 |

| 1,500,000 | Texas Water Development Board, 4.80%, 10/15/52 | 1,564,890 |

| 5,000,000 | Texas Water Development Board, St. Water Implementation Fund, 4.00%, 10/15/44 | 4,905,400 |

| 5,000,000 | Texas Water Development Board, St. Water Implementation Fund, Series A, 4.00%, 4/15/48 | 4,810,450 |

| 5,000,000 | Texas Water Development Board, St. Water Implementation Fund, Series B, 5.00%, 4/15/49 | 5,276,600 |

| | Total Texas | $ 124,474,261 |

| | Utah — 0.9% | |

| 13,110,000 | Utah State University, Series B, 3.00%, 12/1/49 | $ 10,072,544 |

| | Total Utah | $ 10,072,544 |

| | Virginia — 6.3% | |

| 5,340,000(d) | City of Alexandria, Series A, 3.00%, 7/15/46 (ST AID WITHHLDG Insured) | $ 4,200,497 |

| 2,425,000(d) | City of Lynchburg, 2.375%, 8/1/39 | 1,758,319 |

| 2,505,000(d) | City of Lynchburg, 2.375%, 8/1/40 | 1,775,294 |

| 1,170,000(d) | City of Manassas, 2.00%, 7/1/31 (ST AID WITHHLDG Insured) | 1,037,252 |

| 4,100,000 | City of Virginia Beach Storm Water Utility Revenue, Series A, 3.00%, 11/15/42 | 3,345,518 |

| 13,500,000 | Hampton Roads Transportation Accountability Commission, Series A, 4.00%, 7/1/52 | 12,508,695 |

The accompanying notes are an integral part of these financial statements.

Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/2229

Schedule of Investments | 12/31/22 (continued)

Principal

Amount

USD ($) | | | | | | Value |

| | Virginia — (continued) | |

| 2,750,000 | Hampton Roads Transportation Accountability Commission, Series A, 4.00%, 7/1/57 | $ 2,488,200 |

| 5,725,000 | Loudoun County Economic Development Authority, Series A, 2.125%, 12/1/39 | 3,782,107 |

| 5,000,000 | Loudoun County Economic Development Authority, Series A, 3.00%, 12/1/37 | 4,560,450 |

| 7,500,000 | Loudoun County Economic Development Authority, Howard Hughes Medical Institute Issue, Series A, 4.00%, 10/1/52 | 7,232,025 |

| 18,490,000 | Tobacco Settlement Financing Corp., Series B-1, 5.00%, 6/1/47 | 17,236,008 |

| 5,870,000 | Virginia Commonwealth Transportation Board, 4.00%, 5/15/44 | 5,730,411 |

| 5,000,000 | Virginia Commonwealth Transportation Board, Capital Projects, 3.00%, 5/15/37 | 4,293,700 |

| 650,000 | Virginia Housing Development Authority, Series E, 2.10%, 7/1/35 | 550,043 |

| 1,000,000 | Virginia Housing Development Authority, Series E, 2.30%, 7/1/40 | 794,680 |

| | Total Virginia | $ 71,293,199 |

| | Washington — 5.0% | |

| 3,600,000 | Central Puget Sound Regional Transit Authority, Green Bond, Series 1, 3.00%, 11/1/36 | $ 3,152,556 |

| 26,025,000 | Central Puget Sound Regional Transit Authority, Green Bond, Series S-1, 5.00%, 11/1/46 | 29,896,739 |

| 10,250,000 | City of Seattle Municipal Light & Power Revenue, Series A, 4.00%, 1/1/48 | 9,873,005 |

| 10,000,000 | King County Housing Authority, Birch Creek Apartments Project, 5.50%, 5/1/38 (CNTY GTD Insured) | 10,028,500 |

| 4,000,000 | Snohomish County Public Utility District No 1, Series A, 5.00%, 12/1/51 | 4,294,040 |

| | Total Washington | $ 57,244,840 |

| | Total Municipal Bonds

(Cost $1,284,969,668) | $1,132,496,794 |

|

|

The accompanying notes are an integral part of these financial statements.

30Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/22

| Shares | | | | | | Value |

| | Liquidating Trust — Real Estate — 0.0%†

of Net Assets# | |

| 200(i) | CMS Liquidating Trust | $ 10,000 |

| | Total Liquidating Trust — Real Estate

(Cost $204,541) | $ 10,000 |

| | TOTAL INVESTMENTS IN UNAFFILIATED ISSUERS — 99.7%

(Cost $1,285,174,209) | $1,132,506,794 |

| | OTHER ASSETS AND LIABILITIES — 0.3% | $ 3,170,376 |

| | net assets — 100.0% | $1,135,677,170 |

| | | | | | | |

| AGC | Assured Guaranty Corp. |

| AGM | Assured Guaranty Municipal Corp. |

| AMBAC | Ambac Assurance Corporation. |

| CNTY GTD | County Guaranteed. |

| FNMA | Federal National Mortgage Association. |

| GNMA | Government National Mortgage Association. |

| NATL | National Public Finance Guarantee Corp. |

| PSF-GTD | Permanent School Fund Guaranteed. |

| RIB | Residual Interest Bond is purchased in a secondary market. The interest rate is subject to change periodically and inversely based upon prevailing market rates. The interest rate shown is the rate at December 31, 2022. |

| SCH BD GTY | School Board Guaranty. |

| ST AID WITHHLDG | State Aid Withholding. |

| (144A) | Security is exempt from registration under Rule 144A of the Securities Act of 1933. Such securities may be resold normally to qualified institutional buyers in a transaction exempt from registration. At December 31, 2022, the value of these securities amounted to $12,298,956, or 1.1% of net assets. |

| (a) | Consists of Revenue Bonds unless otherwise indicated. |

| (b) | Security issued with a zero coupon. Income is recognized through accretion of discount. |

| (c) | Escrow to maturity. |

| (d) | Represents a General Obligation Bond. |

| (e) | Debt obligation initially issued at one coupon which converts to a higher coupon at a specific date. The rate shown is the rate at December 31, 2022. |

| (f) | Security is in default. |

| (g) | Pre-refunded bonds have been collateralized by U.S. Treasury or U.S. Government Agency securities which are held in escrow to pay interest and principal on the tax exempt issue and to retire the bonds in full at the earliest refunding date. |

The accompanying notes are an integral part of these financial statements.

Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/2231

Schedule of Investments | 12/31/22 (continued)

| (h) | The interest rate is subject to change periodically. The interest rate and/or reference index and spread shown at December 31, 2022. |

| (i) | Non-income producing security. |

| † | Amount rounds to less than 0.1%. |

| # | Securities are restricted as to resale. |

| Restricted Securities | Acquisition date | Cost | Value |

| CMS Liquidating Trust | 11/20/2012 | $204,541 | $10,000 |

| % of Net assets | | | 0.0% † |

| † | Amount rounds to less than 0.1%. |

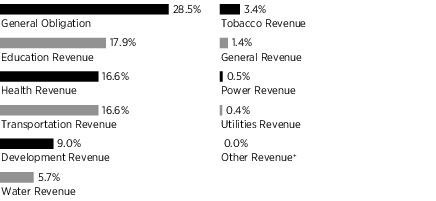

| Revenue Bonds: | |

| Education Revenue | 17.9% |

| Health Revenue | 16.6 |

| Transportation Revenue | 16.6 |

| Development Revenue | 9.0 |

| Water Revenue | 5.7 |

| Tobacco Revenue | 3.4 |

| General Revenue | 1.4 |

| Power Revenue | 0.5 |

| Utilities Revenue | 0.4 |

| | 71.5% |

| General Obligation Bonds: | 28.5% |

| | 100.0% |

Purchases and sales of securities (excluding short-term investments) for the year ended December 31, 2022, aggregated $275,005,990 and $405,739,382, respectively.

The Fund is permitted to engage in purchase and sale transactions (“cross trades”) with certain funds and accounts for which Amundi Asset Management US, Inc. (the "Adviser") serves as the Fund's investment adviser, as set forth in Rule 17a-7 under the Investment Company Act of 1940, pursuant to procedures adopted by the Board of Trustees. Under these procedures, cross trades are effected at current market prices. During the year ended December 31, 2022, the Fund engaged in purchases of $19,899,200. During the year ended December 31, 2022, the Fund did not engage in sales pursuant to these procedures.

The accompanying notes are an integral part of these financial statements.

32Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/22

At December 31, 2022, the net unrealized depreciation on investments based on cost for federal tax purposes of $1,283,303,612 was as follows:

| Aggregate gross unrealized appreciation for all investments in which there is an excess of value over tax cost | $ 14,857,496 |

| Aggregate gross unrealized depreciation for all investments in which there is an excess of tax cost over value | (165,654,314) |

| Net unrealized depreciation | $(150,796,818) |

Various inputs are used in determining the value of the Fund's investments. These inputs are summarized in the three broad levels below.

| Level 1 | – | unadjusted quoted prices in active markets for identical securities. |

| Level 2 | – | other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risks, etc.). See Notes to Financial Statements — Note 1A. |

| Level 3 | – | significant unobservable inputs (including the Adviser's own assumptions in determining fair value of investments). See Notes to Financial Statements — Note 1A. |

The following is a summary of the inputs used as of December 31, 2022, in valuing the Fund's investments:

| | Level 1 | Level 2 | Level 3 | Total |

| Municipal Bonds | $— | $1,132,496,794 | $— | $1,132,496,794 |

| Liquidating Trust — Real Estate | — | 10,000 | — | 10,000 |

| Total Investments in Securities | $ — | $ 1,132,506,794 | $ — | $ 1,132,506,794 |

During the year ended December 31, 2022, there were no transfers in or out of Level 3.

The accompanying notes are an integral part of these financial statements.

Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/2233

Statement of Assets and Liabilities | 12/31/22

| ASSETS: | |

| Investments in unaffiliated issuers, at value (cost $1,285,174,209) | $1,132,506,794 |

| Receivables — | |

| Fund shares sold | 16,936,428 |

| Interest | 13,726,822 |

| Due from the Adviser | 10,455 |

| Other assets | 74,220 |

| Total assets | $1,163,254,719 |

| LIABILITIES: | |

| Overdraft due to custodian | $ 9,069,695 |

| Payables — | |

| Fund shares repurchased | 16,482,043 |

| Distributions | 1,603,689 |

| Management fees | 55,777 |

| Administrative expenses | 36,902 |

| Distribution fees | 15,197 |

| Accrued expenses | 314,246 |

| Total liabilities | $ 27,577,549 |

| NET ASSETS: | |

| Paid-in capital | $1,313,667,246 |

| Distributable earnings (loss) | (177,990,076) |

| Net assets | $1,135,677,170 |

| NET ASSET VALUE PER SHARE: | |

| No par value (unlimited number of shares authorized) | |

| Class A (based on $483,373,312/38,164,450 shares) | $ 12.67 |

| Class C (based on $17,357,432/1,382,263 shares) | $ 12.56 |

| Class Y (based on $634,946,426/50,343,310 shares) | $ 12.61 |

| MAXIMUM OFFERING PRICE PER SHARE: | |

| Class A (based on $12.67 net asset value per share/100%-4.50% maximum sales charge) | $ 13.27 |

The accompanying notes are an integral part of these financial statements.

34Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/22

Statement of Operations FOR THE YEAR ENDED 12/31/22

| INVESTMENT INCOME: | | |

| Interest from unaffiliated issuers | $43,357,115 | |

| Total Investment Income | | $ 43,357,115 |

| EXPENSES: | | |

| Management fees | $ 5,801,526 | |

| Administrative expenses | 337,014 | |

| Transfer agent fees | | |

| Class A | 190,279 | |

| Class C | 13,521 | |

| Class Y | 963,832 | |

| Distribution fees | | |

| Class A | 1,385,325 | |

| Class C | 227,242 | |

| Shareowner communications expense | 114,619 | |

| Custodian fees | 12,797 | |

| Registration fees | 152,416 | |

| Professional fees | 163,898 | |

| Printing expense | 61,556 | |

| Pricing fees | 2,098 | |

| Officers' and Trustees' fees | 74,278 | |

| Insurance expense | 13,191 | |

| Miscellaneous | 142,606 | |

| Total expenses | | $ 9,656,198 |

| Less fees waived and expenses reimbursed by the Adviser | | (1,314,106) |

| Net expenses | | $ 8,342,092 |

| Net investment income | | $ 35,015,023 |

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS: | | |

| Net realized gain (loss) on: | | |

| Investments in unaffiliated issuers | | $ (31,440,441) |

| Change in net unrealized appreciation (depreciation) on: | | |

| Investments in unaffiliated issuers | | $ (274,084,357) |

| Net realized and unrealized gain (loss) on investments | | $(305,524,798) |

| Net decrease in net assets resulting from operations | | $ (270,509,775) |

The accompanying notes are an integral part of these financial statements.

Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/2235

Statements of Changes in Net Assets

| | Year

Ended

12/31/22 | Year

Ended

12/31/21 |

| FROM OPERATIONS: | | |

| Net investment income (loss) | $ 35,015,023 | $ 31,789,774 |

| Net realized gain (loss) on investments | (31,440,441) | 2,113,655 |

| Change in net unrealized appreciation (depreciation) on investments | (274,084,357) | (8,439,352) |

| Net increase (decrease) in net assets resulting from operations | $ (270,509,775) | $ 25,464,077 |

| DISTRIBUTIONS TO SHAREOWNERS: | | |

| Class A ($0.30 and $0.30 per share, respectively) | $ (12,418,459) | $ (13,381,751) |

| Class C ($0.20 and $0.18 per share, respectively) | (321,458) | (415,186) |

| Class Y ($0.34 and $0.34 per share, respectively) | (18,983,013) | (19,366,408) |

| Total distributions to shareowners | $ (31,722,930) | $ (33,163,345) |

| FROM FUND SHARE TRANSACTIONS: | | |

| Net proceeds from sales of shares | $ 614,720,285 | $ 475,934,097 |

| Reinvestment of distributions | 16,801,547 | 20,168,626 |

| Cost of shares repurchased | (883,618,920) | (421,962,197) |

| Net increase (decrease) in net assets resulting from Fund share transactions | $ (252,097,088) | $ 74,140,526 |

| Net increase (decrease) in net assets | $ (554,329,793) | $ 66,441,258 |

| NET ASSETS: | | |

| Beginning of year | $1,690,006,963 | $1,623,565,705 |

| End of year | $1,135,677,170 | $ 1,690,006,963 |

The accompanying notes are an integral part of these financial statements.

36Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/22

| | Year

Ended

12/31/22

Shares | Year

Ended

12/31/22

Amount | Year

Ended

12/31/21

Shares | Year

Ended

12/31/21

Amount |

| Class A | | | | |

| Shares sold | 4,849,886 | $ 63,996,828 | 4,450,229 | $ 69,365,275 |

| Reinvestment of distributions | 769,484 | 10,182,939 | 697,232 | 10,849,115 |

| Less shares repurchased | (11,531,321) | (153,953,838) | (8,247,801) | (128,502,248) |

| Net decrease | (5,911,951) | $ (79,774,071) | (3,100,340) | $ (48,287,858) |

| Class C | | | | |

| Shares sold | 373,144 | $ 4,783,991 | 262,794 | $ 4,066,612 |

| Reinvestment of distributions | 20,655 | 271,473 | 22,427 | 345,861 |

| Less shares repurchased | (1,160,056) | (15,411,653) | (756,924) | (11,691,931) |

| Net decrease | (766,257) | $ (10,356,189) | (471,703) | $ (7,279,458) |

| Class Y | | | | |

| Shares sold | 41,379,537 | $ 545,939,466 | 25,917,427 | $ 402,502,210 |

| Reinvestment of distributions | 475,841 | 6,347,135 | 579,098 | 8,973,650 |

| Less shares repurchased | (53,688,995) | (714,253,429) | (18,186,912) | (281,768,018) |

Net increase

(decrease) | (11,833,617) | $(161,966,828) | 8,309,613 | $ 129,707,842 |

The accompanying notes are an integral part of these financial statements.

Pioneer AMT-Free Municipal Fund | Annual Report | 12/31/2237

| | Year

Ended

12/31/22 | Year

Ended

12/31/21 | Year

Ended

12/31/20 | Year

Ended

12/31/19 | Year

Ended

12/31/18 |

| Class A | | | | | |

| Net asset value, beginning of period | $ 15.63 | $ 15.70 | $ 15.17 | $ 14.23 | $ 14.64 |

| Increase (decrease) from investment operations: | | | | | |

| Net investment income (loss) (a) | $ 0.34 | $ 0.28 | $ 0.33 | $ 0.40 | $ 0.41 |

| Net realized and unrealized gain (loss) on investments | (3.00) | (0.05) | 0.68 | 0.95 | (0.41) |

| Net increase (decrease) from investment operations | $ (2.66) | $ 0.23 | $ 1.01 | $ 1.35 | $ — |

| Distributions to shareowners: | | | | | |

| Net investment income | $ (0.30) | $ (0.28) | $ (0.34) | $ (0.41) | $ (0.40) |

| Net realized gain | — | (0.02) | (0.14) | — | (0.01) |

| Total distributions | $ (0.30) | $ (0.30) | $ (0.48) | $ (0.41) | $ (0.41) |

| Net increase (decrease) in net asset value | $ (2.96) | $ (0.07) | $ 0.53 | $ 0.94 | $ (0.41) |