UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-21437 | |||||||

| ||||||||

Cohen & Steers REIT and Utility Income Fund, Inc. | ||||||||

(Exact name of registrant as specified in charter) | ||||||||

| ||||||||

280 Park Avenue, 10th Floor, New York, NY |

| 10017 | ||||||

(Address of principal executive offices) |

| (Zip code) | ||||||

| ||||||||

Adam M. Derechin | ||||||||

(Name and address of agent for service) | ||||||||

| ||||||||

Registrant’s telephone number, including area code: | (212) 832-3232 |

| ||||||

| ||||||||

Date of fiscal year end: | December 31 |

| ||||||

| ||||||||

Date of reporting period: | December 31, 2007 |

| ||||||

Item 1. Reports to Stockholders.

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

February 8, 2008

To Our Shareholders:

We are pleased to submit to you our report for the year ended December 31, 2007. The net asset value at that date was $22.13 per common share. The fund's common stock is traded on the New York Stock Exchange (NYSE) and its share price can differ from its net asset value; at year end, the fund's closing price on the NYSE was $20.11. The total return, including income, for the fund and the comparative benchmarks were:

| Six Months Ended December 31, 2007 | Year Ended December 31, 2007 | ||||||||||

| Cohen & Steers REIT and Utility Income Fund at Market Valuea | 0.46 | % | –1.24 | % | |||||||

| Cohen & Steers REIT and Utility Income Fund at Net Asset Valuea | –3.53 | % | –3.69 | % | |||||||

| FTSE NAREIT Equity REIT Indexb | –10.42 | % | –15.69 | % | |||||||

| S&P 500 Indexb | –1.37 | % | 5.49 | % | |||||||

| S&P 1500 Utilities Indexb | 8.33 | % | 16.46 | % | |||||||

| Blended Benchmark—40% FTSE NAREIT Equity REIT Index, 40% S&P 1500 Utilities Index, 20% Merrill Lynch Fixed Rate Preferred Indexb | –3.32 | % | –2.63 | % | |||||||

The performance data quoted represent past performance. Past performance is no guarantee of future results. The investment return and the principal value of an investment will fluctuate and shares, if sold, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance results reflect the effects of leverage, resulting from the issuance of preferred shares.

A long-term capital gain distribution of $0.45 per share was declared for shareholders of record on December 26, 2007 and was paid on December 31, 2007.

Three monthly dividends of $0.1375 per common share were declared and will be paid to common shareholders on January 31, 2008, February 29, 2008 and March 31, 2008c.

a As a closed-end investment company, the price of the fund's New York Stock Exchange-traded shares will be set by market forces and at times may deviate from the net asset value per share of the fund.

b The FTSE NAREIT Equity REIT Index is an unmanaged, market capitalization weighted index of all publicly traded REITs that invest predominantly in the equity ownership of real estate. The index is designed to reflect the performance of all publicly traded equity REITs as a whole. The S&P 500 Index is an unmanaged index of common stocks that is frequently used as a general measure of stock market performance. The S&P 1500 Utilities Index is an unmanaged market capitalization weighted index of 75 companies whose primary business involves the generation, transmission and/or distribution of electricity and/or natural gas. The Merrill Lynch Fixed Rate Preferred Index is an unmanaged index of preferred securities.

c Please note that distributions paid by the fund to shareholders are subject to recharacterization for tax purposes. The final tax treatment of these distributions is reported to shareholders after the close of the calendar year.

1

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

Investment Review

The year was a turbulent one for REITs, which suffered a decline after four straight years of double-digit gains and seven years of positive total returns. As the year began, real estate securities continued to be buoyed by a number of factors. The economy was strong, driving growth in demand for commercial real estate. New supply of competitive commercial real estate product was relatively muted, despite real estate being in a mature stage of its cycle. Debt markets were highly liquid and accommodative of real estate M&A activity, including leveraged buyouts (LBOs). This was highlighted in January by a bidding contest for Equity Office Properties, which was acquired by The Blackstone Group in a $41 billion transaction, at a 24% premium to the market price when the offer was first made.

REITs disproportionately hit by credit woes

While real estate fundamentals did stay generally healthy through the year, concerns over subprime mortgages began to mount, resulting in a general re-pricing of risk and a dramatic widening of credit spreads in July. Commercial banks, seeking to preserve capital to offset losses from a variety of financial instruments, became reluctant to lend. Loans to finance LBOs stopped abruptly, removing a positive catalyst for the REIT market (REITs had been a prime target of private equity investors). In addition, the credit crunch increased the possibility of a U.S. economic recession, fueling worries over underlying fundamentals for real estate.

Real estate securities, which had reached an all-time high in February 2007, declined more than 20% from that peak by August. REITs were volatile over the remainder of the year, as investors reacted to monetary news (the Federal Reserve reduced interest rates from 5.25% to 4.25% between September and the end of the year) and the latest unsettling credit news.

Another strong year for utility stocks

Utilities outperformed the broad U.S. stock market by a wide margin in 2007, registering their fifth consecutive year of double-digit returns as measured by the S&P 1500 Utilities Index. Utilities securities continued to benefit from strong fundamentals—robust demand and tight supply have resulted in high power prices across the country. This has helped the group's earnings growth stay well above its historical average, given that retail demand for electricity and natural gas is relatively inelastic.

Utilities also benefited from their relatively defensive nature. Many segments of the industry operate with regulated pricing, supporting relatively stable revenues and cash flows. This proved to be an attractive feature amid tightening credit markets and concerns over the economy.

Securities of non-regulated utilities performed well as a group. These companies benefit from the opportunity to sell electricity at market prices. While their stocks can be more volatile than regulated utilities, they have been a significant beneficiary of strong energy fundamentals and high wholesale commodity prices over the past few years.

2

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

Preferred securities suffer their worst year ever

The Merrill Lynch Fixed Rate Preferred Index had a total return of –11.3% in 2007. This represented preferreds' poorest yearly performance on record and reflected a surge in issuance. Faced with diminished capital and increased balance-sheet risk, numerous financial institutions sought to recapitalize themselves in the preferred market (driving yields up and prices down) instead of the equity market, where financial shares were trading at several-year lows. At year-end, yields on corporate and REIT preferreds —which together accounted for roughly 20% of the fund—were 7.4% and 8.5%, respectively. By comparison, the 10-year Treasury and corporate bonds, as represented by the Merrill Lynch Corporate Master Index, offered yields of 4.0% and 5.8%, respectively.

REITs weakness offsets strong utility performance

The fund had a decline in the period, as strength in utilities was more than offset by weakness in the REIT and preferred areas. Factors that hindered performance included REIT stock selection in the industrial, office, shopping center and self storage sectors; our stock selection in the hotel sector and overweight and stock selection in the health care sector (the best performing property sector in the NAREIT index in the period) aided relative return.

In the utilities portion of the fund, our non-U.S. holdings contributed positively to performance, benefiting from higher power prices in Europe. The fund's preferred securities had a collective decline, but outperformed the preferred security market broadly, which we attribute to our emphasis on higher-quality issues.

Investment Outlook

Real estate securities, which had factored in a good deal of positive news at the start of the year, ended 2007 with considerable pessimism priced into their shares. Overall, REITs were trading at an 18% discount to their underlying net asset value as of December 31, 2007, compared with a premium of 13% at the end of 2006, and compared with a historical average premium of 5%. The size of this discount suggests to us that the market is expecting at least a mild recession and perhaps a meaningful decline in property values. Our view is that the economy will slow, with some possibility of it dipping into a shallow recession, before reaccelerating as monetary actions take hold. We have already factored modest declines into property asset values due to higher cap rates, particularly for class B properties and secondary markets; but we do not expect a dramatic downturn due to strength in cash flows and fundamentals.

We believe that modest levels of employment growth stand to support demand for sectors such as offices, apartments and hotels, yet new supply is likely to be quite restrained due to the lack of credit for construction loans, which are, by their nature, more risky. Of course, ongoing credit woes could continue to hamper REITs and stocks broadly, but we believe REITs are positioned to perform well once investors sense that the worst of the credit news is behind us. In this environment, where investment opportunities are increasing due to the credit crunch, we remain highly focused on companies with strong managements, compelling long-term business models and properties in the most desirable locations.

3

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

Supportive trends for utilities

In addition to potentially benefiting from their defensive characteristics within a slowing economy (utilities have often outperformed the broader market during periods of economic weakness), utilities in our view could continue to draw support from existing trends. Earnings growth is expected to remain at historically high levels—about three times the group's longtime average. This forecast is supported by higher prices for electricity and natural gas, amid continued strong demand, and more importantly, limited supply growth.

We believe that earnings growth will also benefit from new infrastructure investment, as utilities look to replace aging assets and expand existing networks. Regulated utilities, which account for a significant portion of the fund's holdings, earn a defined rate of rate of return on these investments. We believe that two of the most significant infrastructure opportunities are in electricity transmission and natural gas pipelines.

Regarding valuations, we believe that utility stocks remain attractive, given their strong projected earnings growth and reasonable valuations—modestly above the historical average. While we expect overall market volatility to remain high, we believe utilities offer the potential for attractive total returns over time.

Yields and diversification

We believe that the fund offers an attractive combination of diversification and income potential. Real estate and utilities securities represent two of the higher income-producing sectors of the equity market, yet have relatively low historical correlation with each other. Preferred securities, which in our view currently offer compelling yields, typically help mitigate overall volatility.

4

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

Sincerely,

|  | ||||||

| MARTIN COHEN | ROBERT H. STEERS | ||||||

| Co-chairman | Co-chairman | ||||||

|  | ||||||

| ROBERT S. BECKER | WILLIAM F. SCAPELL | ||||||

| Portfolio Manager | Portfolio Manager | ||||||

|  | ||||||

| JOSEPH M. HARVEY | THOMAS N. BOHJALIAN | ||||||

| Portfolio Manager | Portfolio Manager | ||||||

The views and opinions in the preceding commentary are as of the date stated and are subject to change. This material represents an assessment of the market environment at a specific point in time, should not be relied upon as investment advice and is not intended to predict or depict performance of any investment.

Visit Cohen & Steers online at cohenandsteers.com

For more information about any of our funds, visit cohenandsteers.com, where you'll find daily net asset values, fund fact sheets and portfolio highlights. You can also access newsletters, education tools and market updates covering REIT, utility and preferred securities sectors.

In addition, our Web site contains comprehensive information about our firm, including our most recent press releases, profiles of our senior investment professionals, and an overview of our investment approach.

5

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

Our Leverage Strategy

(Unaudited)

While we do not attempt to predict what future interest rates will be, it has been our philosophy to utilize interest rate swap transactions to seek to reduce the interest rate risk inherent in our utilization of leverage. Our leverage strategy involves issuing auction market preferred shares (AMPS) to raise additional capital for the fund, with an objective of increasing the net income available for shareholders. As of December 31, 2007, AMPS represented 38% of the fund's managed assets. Considering that AMPS have variable dividend rates, we seek to lock in the rate on a significant portion of this additional capital through interest rate swap agreements (where we effectively convert our variable rate obligation to a fixed rate obligation for the term of the swap agreements). Specifically, we have fixed the rate on 43% of our borrowings at an average interest rate of 3.5% for an average remaining period of 1.3 years (when we first entered i nto the swaps, the average term was 5.0 years). By locking in a significant portion or our leveraging costs, we have endeavored to adequately protect the dividend-paying ability of the fund. The use of leverage increases the volatility of the fund's net asset value in both up and down markets. However, we believe that locking in a portion of the fund's leveraging costs for the term of the swap agreements partially protects the fund from any impact that an increase in short-term interest rates may have as a result of the use of leverage.

Leverage Factsa

| Leverage (as a % of managed assets) | 38 | % | |||||

| % Fixed Rate | 43 | % | |||||

| % Variable Rate | 57 | % | |||||

| Weighted Average Rate on Swaps | 3.5 | % | |||||

| Weighted Average Term on Swaps | 1.3 years | ||||||

| Current Rate on AMPSb | 5.9 | % | |||||

a Data as of December 31, 2007. Information subject to change.

b See Note 5 in Notes to Financial Statements.

6

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

DECEMBER 31, 2007

Top Ten Holdingsa

(Unaudited)

| Security | Market Value | % of Managed Assets | |||||||||

| Duke Energy Corp. | $ | 84,373,934 | 4.0 | % | |||||||

| Public Service Enterprise Group | 74,711,520 | 3.6 | |||||||||

| Progress Energy | 67,748,727 | 3.2 | |||||||||

| Southern Co. | 66,735,250 | 3.2 | |||||||||

| Exelon Corp. | 63,385,296 | 3.0 | |||||||||

| Nationwide Health Properties | 63,100,755 | 3.0 | |||||||||

| Consolidated Edison | 57,862,825 | 2.8 | |||||||||

| Entergy Corp. | 55,624,608 | 2.7 | |||||||||

| Spectra Energy Corp. | 52,008,452 | 2.5 | |||||||||

| Ameren Corp. | 47,314,488 | 2.3 | |||||||||

a Top ten holdings are determined on the basis of the market value of individual securities held. The fund may also hold positions in other types of securities issued by the companies listed above. See the Schedule of Investments for additional details on such other positions.

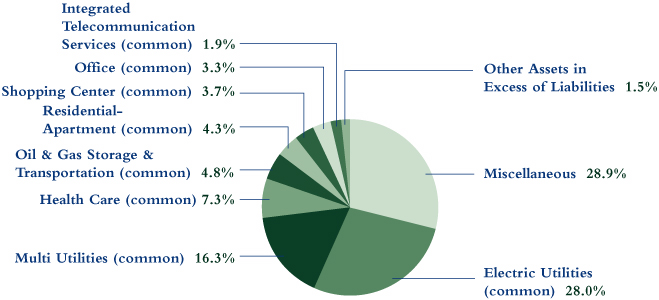

Sector Breakdown

(Based on Managed Assets)

(Unaudited)

7

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

SCHEDULE OF INVESTMENTS

December 31, 2007

| Number of Shares | Value | ||||||||||||||

| COMMON STOCK | 126.6 | % | |||||||||||||

| ENERGY | 8.8 | % | |||||||||||||

| INTEGRATED OIL & GAS | 0.5 | % | |||||||||||||

| Duncan Energy Partners LP | 81,000 | $ | 1,768,230 | ||||||||||||

| Targa Resources Partners LP | 147,000 | 4,354,140 | |||||||||||||

| 6,122,370 | |||||||||||||||

| OIL & GAS EQUIPMENT & SERVICES | 0.2 | % | |||||||||||||

| Exterran Partners LP | 88,500 | 2,839,965 | |||||||||||||

| OIL & GAS REFINING & MARKETING | 0.4 | % | |||||||||||||

| Spectra Energy Income Fund (Canada) | 172,600 | 1,573,940 | |||||||||||||

| Spectra Energy Income Fund, 144Aa (Canada) | 475,000 | 4,331,526 | |||||||||||||

| 5,905,466 | |||||||||||||||

| OIL & GAS STORAGE & TRANSPORATION | 7.7 | % | |||||||||||||

| DCP Midstream Partners LP | 142,000 | 6,524,900 | |||||||||||||

| Energy Transfer Partners LP | 95,600 | 5,150,928 | |||||||||||||

| Enterprise Products Partners LP | 202,200 | 6,446,136 | |||||||||||||

| Kinder Morgan Energy Partners LP | 123,192 | 6,651,136 | |||||||||||||

| Magellan Midstream Partners LP | 97,900 | 4,244,944 | |||||||||||||

| SemGroup Energy Partners LP | 61,200 | 1,764,396 | |||||||||||||

| Spectra Energy Corp. | 2,014,270 | 52,008,452 | |||||||||||||

| Teekay LNG Partners LP | 69,300 | 2,056,131 | |||||||||||||

| Teekay Offshore Partners LP | 78,900 | 1,995,381 | |||||||||||||

| Williams Partners LP | 336,900 | 13,206,480 | |||||||||||||

| 100,048,884 | |||||||||||||||

| TOTAL ENERGY | 114,916,685 | ||||||||||||||

| INTEGRATED TELECOMMUNICATION SERVICES | 3.0 | % | |||||||||||||

| AT&T | 267,000 | 11,096,520 | |||||||||||||

| Citizens Communications Co. | 361,100 | 4,596,803 | |||||||||||||

| Fairpoint Communications | 731,315 | 9,521,721 | |||||||||||||

| Verizon Communications | 253,118 | 11,058,726 | |||||||||||||

| Windstream Corp. | 200,000 | 2,604,000 | |||||||||||||

| 38,877,770 | |||||||||||||||

See accompanying notes to financial statements.

8

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

December 31, 2007

| Number of Shares | Value | ||||||||||||||

| REAL ESTATE | 41.6 | % | |||||||||||||

| DIVERSIFIED | 2.3 | % | |||||||||||||

| Colonial Properties Trust | 253,747 | $ | 5,742,295 | ||||||||||||

| iStar Financial | 382,300 | 9,958,915 | |||||||||||||

| Land Securities Group PLC (United Kingdom) | 100,300 | 3,006,838 | |||||||||||||

| Vornado Realty Trust | 136,950 | 12,044,752 | |||||||||||||

| 30,752,800 | |||||||||||||||

| HEALTH CARE | 11.8 | % | |||||||||||||

| HCP | 848,100 | 29,496,918 | |||||||||||||

| Health Care REIT | 467,500 | 20,892,575 | |||||||||||||

| Nationwide Health Properties | 2,011,500 | 63,100,755 | |||||||||||||

| Omega Healthcare Investors | 343,900 | 5,519,595 | |||||||||||||

| Senior Housing Properties Trust | 702,382 | 15,930,024 | |||||||||||||

| Ventas | 400,000 | 18,100,000 | |||||||||||||

| 153,039,867 | |||||||||||||||

| HOTEL | 2.6 | % | |||||||||||||

| DiamondRock Hospitality Co. | 940,100 | 14,082,698 | |||||||||||||

| Hospitality Properties Trust | 342,800 | 11,045,016 | |||||||||||||

| Strategic Hotels & Resorts | 547,800 | 9,164,694 | |||||||||||||

| 34,292,408 | |||||||||||||||

| INDUSTRIAL | 2.4 | % | |||||||||||||

| DCT Industrial Trust | 777,186 | 7,235,602 | |||||||||||||

| EastGroup Properties | 114,000 | 4,770,900 | |||||||||||||

| First Industrial Realty Trust | 141,700 | 4,902,820 | |||||||||||||

| ING Industrial Fund (Australia) | 4,600,335 | 10,259,886 | |||||||||||||

| Segro PLC (United Kingdom) | 434,980 | 4,069,595 | |||||||||||||

| 31,238,803 | |||||||||||||||

| MORTGAGE | 0.5 | % | |||||||||||||

| Annaly Capital Management | 324,842 | 5,905,628 | |||||||||||||

| OFFICE | 5.3 | % | |||||||||||||

| BioMed Realty Trust | 210,453 | 4,876,196 | |||||||||||||

| Boston Properties | 16,000 | 1,468,960 | |||||||||||||

See accompanying notes to financial statements.

9

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

December 31, 2007

| Number of Shares | Value | ||||||||||||||

| Brandywine Realty Trust | 763,937 | $ | 13,697,391 | ||||||||||||

| Highwoods Properties | 382,200 | 11,229,036 | |||||||||||||

| HRPT Properties Trust | 702,295 | 5,428,740 | |||||||||||||

| ING Office Fund (Australia) | 3,472,712 | 4,939,729 | |||||||||||||

| Mack-Cali Realty Corp. | 453,400 | 15,415,600 | |||||||||||||

| Parkway Properties | 126,200 | 4,666,876 | |||||||||||||

| SL Green Realty Corp. | 80,204 | 7,495,866 | |||||||||||||

| 69,218,394 | |||||||||||||||

| OFFICE/INDUSTRIAL | 1.9 | % | |||||||||||||

| First Potomac Realty Trust | 195,867 | 3,386,540 | |||||||||||||

| Liberty Property Trust | 729,895 | 21,028,275 | |||||||||||||

| 24,414,815 | |||||||||||||||

| RESIDENTIAL—APARTMENT | 6.9 | % | |||||||||||||

| American Campus Communities | 299,300 | 8,036,205 | |||||||||||||

| Apartment Investment & Management Co.b | 522,900 | 18,160,317 | |||||||||||||

| Education Realty Trust | 467,800 | 5,258,072 | |||||||||||||

| GMH Communities Trust | 392,100 | 2,164,392 | |||||||||||||

| Home Properties | 786,387 | 35,269,457 | |||||||||||||

| Mid-America Apartment Communities | 201,600 | 8,618,400 | |||||||||||||

| UDR | 632,100 | 12,547,185 | |||||||||||||

| 90,054,028 | |||||||||||||||

| SELF STORAGE | 1.3 | % | |||||||||||||

| Extra Space Storage | 628,500 | 8,981,265 | |||||||||||||

| Sovran Self Storage | 218,600 | 8,765,860 | |||||||||||||

| 17,747,125 | |||||||||||||||

| SHOPPING CENTER | 6.0 | % | |||||||||||||

| COMMUNITY CENTER | 3.4 | % | |||||||||||||

| Cedar Shopping Centers | 571,300 | 5,844,399 | |||||||||||||

| Developers Diversified Realty Corp. | 509,200 | 19,497,268 | |||||||||||||

| Inland Real Estate Corp. | 753,500 | 10,669,560 | |||||||||||||

| Urstadt Biddle Properties—Class A | 517,500 | 8,021,250 | |||||||||||||

| 44,032,477 | |||||||||||||||

See accompanying notes to financial statements.

10

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

December 31, 2007

| Number of Shares | Value | ||||||||||||||

| FREE STANDING | 1.7 | % | |||||||||||||

| National Retail Properties | 934,200 | $ | 21,841,596 | ||||||||||||

| REGIONAL MALL | 0.9 | % | |||||||||||||

| General Growth Properties | 210,479 | 8,667,525 | |||||||||||||

| Glimcher Realty Trust | 249,500 | 3,565,355 | |||||||||||||

| 12,232,880 | |||||||||||||||

| TOTAL SHOPPING CENTER | 78,106,953 | ||||||||||||||

| SPECIALTY | 0.6 | % | |||||||||||||

| Entertainment Properties Trust | 161,300 | 7,581,100 | |||||||||||||

| TOTAL REAL ESTATE | 542,351,921 | ||||||||||||||

| UTILITIES | 73.2 | % | |||||||||||||

| ELECTRIC UTILITIES | 45.1 | % | |||||||||||||

| American Electric Power Co. | 186,400 | 8,678,784 | |||||||||||||

| Cleco Corp. | 243,500 | 6,769,300 | |||||||||||||

| DPL | 112,900 | 3,347,485 | |||||||||||||

| Duke Energy Corp. | 4,183,140 | 84,373,934 | |||||||||||||

| E.ON AG (ADR) (Germany) | 308,096 | 21,628,339 | |||||||||||||

| Edison International | 352,000 | 18,786,240 | |||||||||||||

| Electricite de France (France) | 172,600 | 20,561,468 | |||||||||||||

| Entergy Corp. | 465,400 | 55,624,608 | |||||||||||||

| Exelon Corp. | 776,400 | 63,385,296 | |||||||||||||

| FirstEnergy Corp. | 533,000 | 38,557,220 | |||||||||||||

| Fortum Oyj (Finland) | 139,000 | 6,261,362 | |||||||||||||

| FPL Group | 346,497 | 23,485,567 | |||||||||||||

| ITC Holdings Corp. | 195,800 | 11,047,036 | |||||||||||||

| Mirant Corp.c | 91,000 | 3,547,180 | |||||||||||||

| Northeast Utilities | 234,000 | 7,326,540 | |||||||||||||

| Pepco Holdings | 990,800 | 29,060,164 | |||||||||||||

| Pinnacle West Capital Corp. | 397,500 | 16,857,975 | |||||||||||||

| PPL Corp. | 447,000 | 23,284,230 | |||||||||||||

| Progress Energy | 1,398,900 | 67,748,727 | |||||||||||||

| Scottish and Southern Energy PLC (United Kingdom) | 308,328 | 10,053,353 | |||||||||||||

| Southern Co. | 1,722,200 | 66,735,250 | |||||||||||||

| 587,120,058 | |||||||||||||||

See accompanying notes to financial statements.

11

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

December 31, 2007

| Number of Shares | Value | ||||||||||||||

| INDEPENDENT POWER PRODUCERS & ENERGY TRADERS | 1.9 | % | |||||||||||||

| Constellation Energy Group | 162,000 | $ | 16,609,860 | ||||||||||||

| Dynegy Class Ac | 59,500 | 424,830 | |||||||||||||

| NRG Energyc | 172,000 | 7,454,480 | |||||||||||||

| 24,489,170 | |||||||||||||||

| MULTI UTILITIES | 26.2 | % | |||||||||||||

| Ameren Corp. | 872,800 | 47,314,488 | |||||||||||||

| Consolidated Edisond | 1,184,500 | 57,862,825 | |||||||||||||

| Dominion Resources | 469,400 | 22,273,030 | |||||||||||||

| DTE Energy Co. | 1,041,200 | 45,771,152 | |||||||||||||

| Integrys Energy Group | 58,300 | 3,013,527 | |||||||||||||

| NSTAR | 311,374 | 11,277,966 | |||||||||||||

| PG&E Corp. | 749,000 | 32,274,410 | |||||||||||||

| Public Service Enterprise Group | 760,500 | 74,711,520 | |||||||||||||

| RWE AG (Germany) | 50,483 | 7,085,634 | |||||||||||||

| Sempra Energy | 27,983 | 1,731,588 | |||||||||||||

| TECO Energy | 291,100 | 5,009,831 | |||||||||||||

| United Utilities PLC (United Kingdom) | 92,301 | 1,389,032 | |||||||||||||

| Vectren Corp. | 281,100 | 8,154,711 | |||||||||||||

| Xcel Energy | 1,051,200 | 23,725,584 | |||||||||||||

| 341,595,298 | |||||||||||||||

| TOTAL UTILITIES | 953,204,526 | ||||||||||||||

| TOTAL COMMON STOCK (Identified cost—$1,334,243,487) | 1,649,350,902 | ||||||||||||||

| PREFERRED SECURITIES—$25 PAR VALUE | 15.8 | % | |||||||||||||

| BANK | 0.6 | % | |||||||||||||

| BAC Capital Trust III, 7.00%, due 8/15/32, Series X | 90,000 | 2,079,000 | |||||||||||||

| Colonial Capital Trust IV, 7.875%, due 10/1/33 | 74,100 | 1,659,840 | |||||||||||||

| U.S. Bancorp, 5.843%, Series B (FRN) | 99,952 | 2,171,957 | |||||||||||||

| Wachovia Corp., 8.00% | 97,000 | 2,454,100 | |||||||||||||

| 8,364,897 | |||||||||||||||

See accompanying notes to financial statements.

12

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

December 31, 2007

| Number of Shares | Value | ||||||||||||||

| BANK—FOREIGN | 1.1 | % | |||||||||||||

| Santander Finance Preferred, 6.80% | 300,000 | $ | 6,615,000 | ||||||||||||

| Santander Finance Preferred, 6.50%, 144Aa | 80,000 | 1,670,000 | |||||||||||||

| Santander Finance Preferred, 5.661%, Series 6 (FRN) | 280,000 | 5,292,000 | |||||||||||||

| 13,577,000 | |||||||||||||||

| ELECTRIC—INTEGRATED | 0.2 | % | |||||||||||||

| FPL Group Capital, 7.45%, due 9/1/67, Series E | 120,000 | 3,120,000 | |||||||||||||

| FINANCE—INVESTMENT BANKER/BROKER | 0.4 | % | |||||||||||||

| JP Morgan Chase Capital X, 7.00% | 100,000 | 2,360,000 | |||||||||||||

| Merrill Lynch & Co., 5.482%, Series 5 (FRN) | 155,133 | 2,714,827 | |||||||||||||

| 5,074,827 | |||||||||||||||

| INSURANCE | 1.7 | % | |||||||||||||

| LIFE/HEALTH INSURANCE | 0.2 | % | |||||||||||||

| Delphi Financial Group, 7.376%, due 5/15/37 | 129,000 | 2,379,405 | |||||||||||||

| MULTI-LINE—FOREIGN | 0.4 | % | |||||||||||||

| ING Groep N.V., 6.375% | 62,893 | 1,266,036 | |||||||||||||

| ING Groep N.V., 7.375% | 142,000 | 3,378,180 | |||||||||||||

| 4,644,216 | |||||||||||||||

| PROPERTY CASUALTY | 0.4 | % | |||||||||||||

| Berkley W R Capital Trust II, 6.75%, due 7/26/45 | 47,100 | 987,687 | |||||||||||||

| Markel Corp., 7.50%, due 8/22/46 | 200,000 | 4,822,000 | |||||||||||||

| 5,809,687 | |||||||||||||||

| PROPERTY CASUALTY—FOREIGN | 0.5 | % | |||||||||||||

| ACE Ltd., 7.80%, Series C | 140,000 | 3,346,000 | |||||||||||||

| Arch Capital Group Ltd., 8.00% | 125,000 | 3,123,750 | |||||||||||||

| 6,469,750 | |||||||||||||||

| REINSURANCE—FOREIGN | 0.2 | % | |||||||||||||

| Aspen Insurance Holdings Ltd., 7.401%, Series A | 150,000 | 3,277,500 | |||||||||||||

| TOTAL INSURANCE | 22,580,558 | ||||||||||||||

See accompanying notes to financial statements.

13

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

December 31, 2007

| Number of Shares | Value | ||||||||||||||

| INTEGRATED TELECOMMUNICATION SERVICES | 0.4 | % | |||||||||||||

| Telephone & Data Systems, 7.60%, due 12/1/41, Series A | 230,500 | $ | 4,799,010 | ||||||||||||

| United States Cellular Corp., 7.50%, due 6/15/34 | 39,700 | 833,700 | |||||||||||||

| 5,632,710 | |||||||||||||||

| MEDIA—DIVERSIFIED SERVICES | 1.1 | % | |||||||||||||

| Comcast Corp., 6.625%, due 5/15/56 | 122,037 | 2,512,742 | |||||||||||||

| Comcast Corp., 7.00%, due 9/15/55, Series B | 451,000 | 10,120,440 | |||||||||||||

| Liberty Media Corp., 8.75%, due 2/1/30 (PPLUS) | 54,000 | 1,242,000 | |||||||||||||

| 13,875,182 | |||||||||||||||

| OIL—EXPLORATION AND PRODUCTION | 0.1 | % | |||||||||||||

| Nexen, 7.35%, due 11/1/43, Series B | 29,111 | 675,084 | |||||||||||||

| REAL ESTATE | 10.1 | % | |||||||||||||

| DIVERSIFIED | 1.8 | % | |||||||||||||

| Forest City Enterprises, 7.375%, Class A | 519,000 | 11,724,210 | |||||||||||||

| iStar Financial, 7.875%, Series E | 249,300 | 4,921,182 | |||||||||||||

| iStar Financial, 7.65%, Series G | 88,300 | 1,624,720 | |||||||||||||

| iStar Financial, 7.50%, Series I | 250,000 | 4,600,000 | |||||||||||||

| Lexington Corporate Properties Trust, 8.05%, Series B | 34,400 | 717,240 | |||||||||||||

| 23,587,352 | |||||||||||||||

| HEALTH CARE | 2.8 | % | |||||||||||||

| Health Care REIT, 7.875%, Series D | 153,536 | 3,575,854 | |||||||||||||

| Health Care REIT, 7.625%, Series F | 305,600 | 6,756,816 | |||||||||||||

| LTC Properties, 8.00%, Series F | 600,000 | 13,266,000 | |||||||||||||

| Omega Healthcare Investors, 8.375%, Series D | 500,000 | 12,385,000 | |||||||||||||

| 35,983,670 | |||||||||||||||

| HOTEL | 0.6 | % | |||||||||||||

| Ashford Hospitality Trust, 8.55%, Series A | 29,633 | 555,619 | |||||||||||||

| Equity Inns, 8.00%, Series Ce | 71,225 | 961,537 | |||||||||||||

| Host Hotels & Resorts, 8.875%, Series E | 80,000 | 2,008,000 | |||||||||||||

| LaSalle Hotel Properties, 8.00%, Series E | 170,000 | 3,247,000 | |||||||||||||

| Strategic Hotels & Resorts, 8.25%, Series B | 90,800 | 1,747,900 | |||||||||||||

| 8,520,056 | |||||||||||||||

See accompanying notes to financial statements.

14

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

December 31, 2007

| Number of Shares | Value | ||||||||||||||

| OFFICE | 2.6 | % | |||||||||||||

| Alexandria Real Estate Equities, 8.375%, Series C | 374,250 | $ | 9,824,062 | ||||||||||||

| Brandywine Realty Trust, 7.50%, Series C | 177,410 | 3,626,260 | |||||||||||||

| Kilroy Realty Corp., 7.80%, Series E | 99,500 | 2,238,750 | |||||||||||||

| Maguire Properties, 7.625%, Series A | 196,240 | 2,735,586 | |||||||||||||

| SL Green Realty Corp., 7.625%, Series C | 424,500 | 9,653,130 | |||||||||||||

| SL Green Realty Corp., 7.875%, Series D | 227,650 | 5,201,803 | |||||||||||||

| 33,279,591 | |||||||||||||||

| OFFICE/INDUSTRIAL | 0.6 | % | |||||||||||||

| PS Business Parks, 7.00%, Series H | 55,959 | 1,096,796 | |||||||||||||

| PS Business Parks, 6.875%, Series I | 245,000 | 4,704,000 | |||||||||||||

| PS Business Parks, 7.95%, Series K | 65,000 | 1,430,650 | |||||||||||||

| 7,231,446 | |||||||||||||||

| RESIDENTIAL—APARTMENT | 0.4 | % | |||||||||||||

| Apartment Investment & Management Co., 9.375%, Series G | 35,000 | 854,000 | |||||||||||||

| Apartment Investment & Management Co., 8.00%, Series T | 138,400 | 2,884,256 | |||||||||||||

| Apartment Investment & Management Co., 8.00%, Series V | 47,200 | 969,016 | |||||||||||||

| Apartment Investment & Management Co., 7.875%, Series Y | 34,000 | 681,020 | |||||||||||||

| 5,388,292 | |||||||||||||||

| SHOPPING CENTER | 1.3 | % | |||||||||||||

| COMMUNITY CENTER | 1.0 | % | |||||||||||||

| Cedar Shopping Centers, 8.875%, Series A | 137,500 | 3,231,250 | |||||||||||||

| Developers Diversified Realty Corp., 7.50%, Series I | 300,700 | 6,236,518 | |||||||||||||

| Kimco Realty Corp., 7.75%, Series G | 88,700 | 2,027,682 | |||||||||||||

| Saul Centers, 8.00%, Series A | 96,300 | 2,378,610 | |||||||||||||

| 13,874,060 | |||||||||||||||

| REGIONAL MALL | 0.3 | % | |||||||||||||

| CBL & Associates Properties, 7.75%, Series C | 114,710 | 2,523,620 | |||||||||||||

| CBL & Associates Properties, 7.375%, Series D | 60,000 | 1,176,000 | |||||||||||||

| 3,699,620 | |||||||||||||||

| TOTAL SHOPPING CENTER | 17,573,680 | ||||||||||||||

| TOTAL REAL ESTATE | 131,564,087 | ||||||||||||||

See accompanying notes to financial statements.

15

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

December 31, 2007

| Number of Shares | Value | ||||||||||||||

| UTILITIES—ELECTRIC UTILITIES | 0.1 | % | |||||||||||||

| Entergy Corp., 7.625% ($50 par value) | 24,800 | $ | 1,779,400 | ||||||||||||

| TOTAL PREFERRED SECURITIES—$25 PAR VALUE (Identified cost—$233,978,086) | 206,243,745 | ||||||||||||||

| PREFERRED SECURITIES—CAPITAL SECURITIES | 11.3 | % | |||||||||||||

| AUTO—FOREIGN | 0.6 | % | |||||||||||||

| Porsche International Finance PLC, 7.20%, due 2/28/49 | 8,000,000 | 7,998,000 | |||||||||||||

| BANK | 1.1 | % | |||||||||||||

| Astoria Capital Trust I, 9.75%, due 11/1/29, Series B | 3,000,000 | 3,127,785 | |||||||||||||

| CBG Florida REIT Corp., 7.114%, due 2/15/49, 144Aa | 3,000,000 | 2,792,169 | |||||||||||||

| Sovereign Capital Trust VI, 7.908%, due 6/13/36 | 6,415,000 | 6,218,181 | |||||||||||||

| Washington Mutual Preferred Funding Cayman, 7.25%, due 3/29/49, Series A-1, 144Aa | 3,000,000 | 1,973,502 | |||||||||||||

| 14,111,637 | |||||||||||||||

| BANK—FOREIGN | 0.5 | % | |||||||||||||

| Credit Agricole SA/London, 6.637%, due 12/31/49, 144Aa | 2,000,000 | 1,858,650 | |||||||||||||

| Royal Bank of Scotland Group PLC, 6.99%, due 10/29/49, 144Aa | 2,000,000 | 1,997,468 | |||||||||||||

| Standard Chartered PLC, 7.014%, due 12/30/49, 144Aa | 2,500,000 | 2,374,198 | |||||||||||||

| 6,230,316 | |||||||||||||||

| ELECTRIC | 1.1 | % | |||||||||||||

| MULTI UTILITIES | 0.7 | % | |||||||||||||

| Dominion Resources, 7.50%, due 6/30/66, Series A | 5,440,000 | 5,386,650 | |||||||||||||

| Dominion Resources Capital Trust I, 7.83%, due 12/1/27 | 2,000,000 | 2,091,428 | |||||||||||||

| Puget Sound Energy, 6.974%, due 6/1/67, Series Ae | 2,000,000 | 1,844,230 | |||||||||||||

| 9,322,308 | |||||||||||||||

| UTILITIES | 0.4 | % | |||||||||||||

| DPL Capital Trust II, 8.125%, due 9/1/31 | 4,000,000 | 4,684,876 | |||||||||||||

| TOTAL ELECTRIC | 14,007,184 | ||||||||||||||

| FINANCE | 2.1 | % | |||||||||||||

| CREDIT CARD | 0.3 | % | |||||||||||||

| Capital One Capital III, 7.686%, due 8/15/36 | 4,500,000 | 3,668,395 | |||||||||||||

See accompanying notes to financial statements.

16

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

December 31, 2007

| Number of Shares | Value | ||||||||||||||

| DIVERSIFIED FINANCIAL SERVICES | 1.5 | % | |||||||||||||

| Citigroup Capital XXI, 8.30%, due 12/21/57 | 2,500,000 | $ | 2,617,885 | ||||||||||||

| Old Mutual Capital Funding, 8.00%, (Eurobond) | 15,450,000 | 15,493,260 | |||||||||||||

| Webster Capital Trust IV, 7.65%, due 6/15/37 | 2,000,000 | 1,695,272 | |||||||||||||

| 19,806,417 | |||||||||||||||

| INVESTMENT BANKER/BROKER | 0.3 | % | |||||||||||||

| JP Morgan Chase Capital XVIII, 6.95%, due 8/17/36, Series R | 2,000,000 | 1,905,406 | |||||||||||||

| JP Morgan Chase Capital XXV, 6.80%, due 10/1/37, Series Y | 2,000,000 | 1,928,918 | |||||||||||||

| 3,834,324 | |||||||||||||||

| TOTAL FINANCE | 27,309,136 | ||||||||||||||

| FOOD | 0.6 | % | |||||||||||||

| Dairy Farmers of America, 7.875%, 144Aa,e,f | 42,500 | 3,792,700 | |||||||||||||

| Gruma S.A., 7.75%, due 12/29/49, 144Aa | 3,500,000 | 3,403,750 | |||||||||||||

| 7,196,450 | |||||||||||||||

| GAS UTILITIES | 0.7 | % | |||||||||||||

| Southern Union Co., 7.20%, due 11/1/66 | 9,800,000 | 9,688,084 | |||||||||||||

| INSURANCE | 3.1 | % | |||||||||||||

| FINANCIAL GUARANTEE | 0.1 | % | |||||||||||||

| Security Capital Assurance Ltd., 6.88%, due 6/30/49, Series Af | 3,700,000 | 1,554,000 | |||||||||||||

| LIFE/HEALTH INSURANCE | 1.3 | % | |||||||||||||

| Liberty Mutual Group, 7.00%, due 3/15/37, 144Aa | 2,000,000 | 1,816,012 | |||||||||||||

| Liberty Mutual Group, 7.50%, due 8/15/36, 144Aa | 1,750,000 | 1,712,524 | |||||||||||||

| Liberty Mutual Group, 7.80%, due 3/15/37, 144Aa | 8,000,000 | 7,135,000 | |||||||||||||

| Liberty Mutual Insurance, 7.697%, due 10/15/97, 144Aa | 7,000,000 | 6,581,631 | |||||||||||||

| 17,245,167 | |||||||||||||||

| MULTI-LINE | 1.3 | % | |||||||||||||

| AFC Capital Trust I, 8.207%, due 2/3/27, Series Be | 9,000,000 | 8,624,745 | |||||||||||||

| Catlin Insurance Co., 7.249%, due 12/1/49, 144Aa | 4,000,000 | 3,663,056 | |||||||||||||

| Metlife Capital Trust IV, 7.875%, due 12/15/37, 144Aa | 4,000,000 | 4,087,328 | |||||||||||||

| 16,375,129 | |||||||||||||||

See accompanying notes to financial statements.

17

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

December 31, 2007

| Number of Shares | Value | ||||||||||||||

| PROPERTY CASUALTY | 0.3 | % | |||||||||||||

| Progressive Corp. (The), 6.70%, due 6/15/37 | 3,000,000 | $ | 2,789,835 | ||||||||||||

| White Mountains Re Group Ltd., 7.506%, due 5/29/49, 144Aa | 2,000,000 | 1,794,608 | |||||||||||||

| 4,584,443 | |||||||||||||||

| REINSURANCE | 0.1 | % | |||||||||||||

| PartnerRe Finance II, 6.44%, due 12/1/66 | 2,000,000 | 1,762,034 | |||||||||||||

| TOTAL INSURANCE | 41,520,773 | ||||||||||||||

| OIL & GAS STORAGE & TRANSPORTATION | 0.6 | % | |||||||||||||

| Enterprise Products Operating LP, 8.375%, due 8/1/66 | 3,500,000 | 3,588,890 | |||||||||||||

| PPL Capital Funding, 6.70%, due 3/30/67, Series A | 5,000,000 | 4,608,160 | |||||||||||||

| 8,197,050 | |||||||||||||||

| OIL—EXPLORATION AND PRODUCTION | 0.9 | % | |||||||||||||

| Pemex Project Funding Master Trust, 7.75%, due 9/28/49 | 11,500,000 | 11,629,375 | |||||||||||||

| TOTAL PREFERRED SECURITIES—CAPITAL SECURITIES (Identified cost—$157,356,183) | 147,888,005 | ||||||||||||||

| Principal Amount | |||||||||||||||

| CORPORATE BONDS | 4.8 | % | |||||||||||||

| INDEPENDENT POWER PRODUCER | 0.1 | % | |||||||||||||

| NRG Energy, 7.375%, due 1/15/17 | $ | 2,000,000 | 1,955,000 | ||||||||||||

| INTEGRATED TELECOMMUNICATION SERVICES | 1.9 | % | |||||||||||||

| Citizens Communications Co., 7.875%, due 1/15/27 | 2,000,000 | 1,915,000 | |||||||||||||

| Citizens Communications Co., 9.00%, due 8/15/31 | 14,500,000 | 14,536,250 | |||||||||||||

| Embarq Corp., 7.995%, due 6/1/36 | 8,000,000 | 8,455,072 | |||||||||||||

| 24,906,322 | |||||||||||||||

| MEDIA | 1.4 | % | |||||||||||||

| Cablevision Systems Corp., 8.00%, due 4/15/12 | 4,150,000 | 4,046,250 | |||||||||||||

| CSC Holdings, 7.625%, due 7/15/18 | 1,000,000 | 923,750 | |||||||||||||

| Rogers Cable, 8.75%, due 5/1/32 | 10,430,000 | 13,145,315 | |||||||||||||

| 18,115,315 | |||||||||||||||

| OIL & GAS EXPLORATION & PRODUCTION | 0.5 | % | |||||||||||||

| Kerr-McGee Corp., 7.875%, due 9/15/31 | 6,000,000 | 7,175,184 | |||||||||||||

See accompanying notes to financial statements.

18

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

December 31, 2007

| Principal Amount | Value | ||||||||||||||

| OIL & GAS STORAGE & TRANSPORTATION | 0.3 | % | |||||||||||||

| Williams Cos. (The), 7.75%, due 6/15/31 | $ | 3,000,000 | 3,300,000 | ||||||||||||

| PIPELINES | 0.2 | % | |||||||||||||

| Enbridge Energy Partners LP, 8.05%, due 10/1/37 | 2,000,000 | 1,978,550 | |||||||||||||

| REAL ESTATE | 0.4 | % | |||||||||||||

| BF Saul REIT, 7.50%, due 3/1/14 | 5,000,000 | 4,625,000 | |||||||||||||

| TOTAL CORPORATE BONDS (Identified cost—$60,504,383) | 62,055,371 | ||||||||||||||

| COMMERCIAL PAPER | 2.9 | % | |||||||||||||

| State Street Boston, 2.00%, due 1/2/08 (Identified cost—$37,222,932) | 37,225,000 | 37,222,932 | |||||||||||||

| TOTAL INVESTMENTS (Identified cost—$1,823,305,071) | 161.4 | % | 2,102,760,955 | ||||||||||||

| LIABILITIES IN EXCESS OF OTHER ASSETS | (0.4 | )% | (5,281,410 | ) | |||||||||||

| LIQUIDATION VALUE OF PREFERRED SHARES | (61.0 | )% | (795,000,000 | ) | |||||||||||

| NET ASSETS APPLICABLE TO COMMON SHARES (Equivalent to $22.13 per share based on 58,858,135 shares of common stock outstanding) | 100.0 | % | $ | 1,302,479,545 | |||||||||||

See accompanying notes to financial statements.

19

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

December 31, 2007

Glossary of Portfolio Abbreviations

ADR American Depositary Receipt

FRN Floating Rate Note

PPLUS Preferred Plus Trust

REIT Real Estate Investment Trust

Note: Percentages indicated are based on the net assets applicable to common shares of the fund.

a Resale is restricted to qualified institutional investors. Aggregate holdings equal 3.9% of net assets applicable to common shares.

b 34,900 shares segregated as collateral for interest rate swap transactions.

c Non-income producing security.

d 110,000 shares segregated as collateral for interest rate swap transactions.

e Illiquid security. Aggregate holdings equal 1.2% of net assets applicable to common shares.

f Fair valued security. Aggregate holdings equal 0.4% of net assets applicable to common shares.

See accompanying notes to financial statements.

20

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

December 31, 2007

Interest rate swaps outstanding at December 31, 2007 are as follows:

| Counterparty | Notional Amount | Fixed Rate Payable | Floating Ratea (reset monthly) Receivable | Termination Date | Unrealized Appreciation/ (Depreciation) | ||||||||||||||||||

| Merrill Lynch Derivative Products AG | $ | 46,000,000 | 3.228 | % | 4.845 | % | March 29, 2008 | $ | 164,400 | ||||||||||||||

| Merrill Lynch Derivative Products AG | $ | 34,000,000 | 3.535 | % | 4.896 | % | April 23, 2008 | 126,225 | |||||||||||||||

| Merrill Lynch Derivative Products AG | $ | 46,000,000 | 3.415 | % | 4.845 | % | March 29, 2009 | 254,321 | |||||||||||||||

| Merrill Lynch Derivative Products AG | $ | 46,000,000 | 3.461 | % | 4.845 | % | March 29, 2010 | 283,702 | |||||||||||||||

| Royal Bank of Canada | $ | 68,000,000 | 2.990 | % | 4.865 | % | March 26, 2009 | 740,548 | |||||||||||||||

| UBS AG | $ | 34,000,000 | 3.440 | % | 4.965 | % | April 19, 2008 | 142,484 | |||||||||||||||

| UBS AG | $ | 34,000,000 | 4.060 | % | 4.965 | % | April 19, 2010 | (222,809 | ) | ||||||||||||||

| UBS AG | $ | 34,000,000 | 4.173 | % | 4.855 | % | April 28, 2010 | (317,361 | ) | ||||||||||||||

| $ | 1,171,510 | ||||||||||||||||||||||

a Based on LIBOR (London Interbank Offered Rate). Represents rates in effect at December 31, 2007.

See accompanying notes to financial statements.

21

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

STATEMENT OF ASSETS AND LIABILITIES

December 31, 2007

| ASSETS: | |||||||

| Investments in securities, at value (Identified cost—$1,823,305,071) | $ | 2,102,760,955 | |||||

| Cash | 204,819 | ||||||

| Dividends and interest receivable | 10,856,133 | ||||||

| Unrealized appreciation on interest rate swap transactions | 1,711,680 | ||||||

| Receivable for investment securities sold | 1,140,227 | ||||||

| Other assets | 41,876 | ||||||

| Total Assets | 2,116,715,690 | ||||||

| LIABILITIES: | |||||||

| Payable for investment securities purchased | 9,756,074 | ||||||

| Payable for dividends declared on common shares | 5,129,095 | ||||||

| Payable for dividends declared on preferred shares | 2,162,519 | ||||||

| Payable for investment management fees | 1,184,156 | ||||||

| Unrealized depreciation on interest rate swap transactions | 540,170 | ||||||

| Payable for administration fees | 78,901 | ||||||

| Payable for directors' fees | 4,099 | ||||||

| Other liabilities | 381,131 | ||||||

| Total Liabilities | 19,236,145 | ||||||

| LIQUIDATION VALUE OF PREFERRED SHARES | 795,000,000 | ||||||

| TOTAL NET ASSETS APPLICABLE TO COMMON SHARES | $ | 1,302,479,545 | |||||

| NET ASSETS APPLICABLE TO COMMON SHARES consist of: | |||||||

| Common Stock ($0.001 par value, 58,858,135 shares issued and outstanding) | $ | 1,026,146,757 | |||||

| Dividends in excess of net investment income | (4,240,392 | ) | |||||

| Accumulated net realized loss | (57,158 | ) | |||||

| Net unrealized appreciation | 280,630,338 | ||||||

| $ | 1,302,479,545 | ||||||

| NET ASSET VALUE PER COMMON SHARE: | |||||||

| ($1,302,479,545 ÷ 58,858,135 shares outstanding) | $ | 22.13 | |||||

| MARKET PRICE PER COMMON SHARE | $ | 20.11 | |||||

| MARKET PRICE DISCOUNT TO NET ASSET VALUE PER COMMON SHARE | (9.13 | )% | |||||

See accompanying notes to financial statements.

22

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

STATEMENT OF OPERATIONS

For the Year Ended December 31, 2007

| Investment Income: | |||||||

| Dividend income (net of $506,341 of foreign withholding tax) | $ | 81,667,630 | |||||

| Interest income | 15,998,293 | ||||||

| Total Income | 97,665,923 | ||||||

| Expenses: | |||||||

| Investment management fees | 19,026,873 | ||||||

| Preferred remarketing fee | 1,972,194 | ||||||

| Administration fees | 1,245,059 | ||||||

| Custodian fees and expenses | 250,958 | ||||||

| Professional fees | 238,497 | ||||||

| Shareholder reporting expenses | 227,863 | ||||||

| Directors' fees and expenses | 53,735 | ||||||

| Transfer agent fees and expenses | 26,040 | ||||||

| Miscellaneous | 179,192 | ||||||

| Total Expenses | 23,220,411 | ||||||

| Reduction of Expenses | (4,476,911 | ) | |||||

| Net Expenses | 18,743,500 | ||||||

| Net Investment Income | 78,922,423 | ||||||

| Net Realized and Unrealized Gain (Loss): | |||||||

| Net realized gain (loss) on: | |||||||

| Investments | 32,606,648 | ||||||

| Foreign currency transactions | (68,028 | ) | |||||

| Interest rate swap transactions | 6,451,659 | ||||||

| Net realized gain | 38,990,279 | ||||||

| Net change in unrealized appreciation (depreciation) on: | |||||||

| Investments | (128,786,762 | ) | |||||

| Foreign currency translations | 3,044 | ||||||

| Interest rate swap transactions | (10,018,825 | ) | |||||

| Net change in unrealized appreciation (depreciation) | (138,802,543 | ) | |||||

| Net realized and unrealized loss | (99,812,264 | ) | |||||

| Net Decrease in Net Assets Resulting from Operations | (20,889,841 | ) | |||||

| Less Dividends and Distributions to Preferred Shareholders | (42,768,598 | ) | |||||

| Net Decrease in Net Assets from Operations Applicable to Common Shares | $ | (63,658,439 | ) | ||||

See accompanying notes to financial statements.

23

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

STATEMENT OF CHANGES IN NET ASSETS

| For the Year Ended December 31, 2007 | For the Year Ended December 31, 2006 | ||||||||||

| Change in Net Assets Applicable to Common Shares: | |||||||||||

| From Operations: | |||||||||||

| Net investment income | $ | 78,922,423 | $ | 78,650,786 | |||||||

| Net realized gain | 38,990,279 | 72,444,479 | |||||||||

| Net change in unrealized appreciation (depreciation) | (138,802,543 | ) | 255,409,943 | ||||||||

| Net increase (decrease) in net assets resulting from operations | (20,889,841 | ) | 406,505,208 | ||||||||

| Less Dividends and Distributions to Preferred Shareholders from: | |||||||||||

| Net investment income | (32,007,551 | ) | (19,018,097 | ) | |||||||

| Net realized gain on investments | (10,761,047 | ) | (15,258,474 | ) | |||||||

| Total dividends and distributions to preferred shareholders | (42,768,598 | ) | (34,276,571 | ) | |||||||

| Net increase (decrease) in net assets from operations applicable to common shares | (63,658,439 | ) | 372,228,637 | ||||||||

| Less Dividends and Distributions to Common Shareholders from: | |||||||||||

| Net investment income | (58,279,954 | ) | (66,563,658 | ) | |||||||

| Net realized gain on investments | (19,130,750 | ) | (51,082,718 | ) | |||||||

| Tax return of capital | (39,569,854 | ) | (20,817,396 | ) | |||||||

| Total dividends and distributions to common shareholders | (116,980,558 | ) | (138,463,772 | ) | |||||||

| Capital Stock Transactions: | |||||||||||

| Decrease in net assets from underwriting commissions and offering expenses from issuance of preferred shares | (1,184,000 | ) | (855,487 | ) | |||||||

| Total increase (decrease) in net assets applicable to common shares | (181,822,997 | ) | 232,909,378 | ||||||||

| Net Assets Applicable to Common Shares: | |||||||||||

| Beginning of year | 1,484,302,542 | 1,251,393,164 | |||||||||

| End of yeara | $ | 1,302,479,545 | $ | 1,484,302,542 | |||||||

a Includes dividends in excess of net investment income of $4,240,392 and $2,298,808, respectively.

See accompanying notes to financial statements.

24

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

FINANCIAL HIGHLIGHTS

The following table includes selected data for a common share outstanding throughout each period and other performance information derived from the financial statements. It should be read in conjunction with the financial statements and notes thereto.

| For the Year Ended December 31, | For the Period January 30, 2004a through | ||||||||||||||||||

| Per Share Operating Performance: | 2007 | 2006 | 2005 | December 31, 2004 | |||||||||||||||

| Net asset value per common share, beginning of period | $ | 25.22 | $ | 21.26 | $ | 21.51 | $ | 19.10 | |||||||||||

| Income from investment operations: | |||||||||||||||||||

| Net investment income | 1.50 | 1.43 | 1.17 | b | 0.90 | ||||||||||||||

| Net realized and unrealized gain (loss) | (1.85 | ) | 5.47 | 0.57 | 2.97 | ||||||||||||||

| Total income (loss) from investment operations | (0.35 | ) | 6.90 | 1.74 | 3.87 | ||||||||||||||

| Less dividends and distributions to preferred shareholders from: | |||||||||||||||||||

| Net investment income | (0.55 | ) | (0.32 | ) | (0.25 | ) | (0.12 | ) | |||||||||||

| Net realized gain on investments | (0.18 | ) | (0.26 | ) | (0.12 | ) | (0.01 | ) | |||||||||||

| Total dividends and distributions to preferred shareholders | (0.73 | ) | (0.58 | ) | (0.37 | ) | (0.13 | ) | |||||||||||

| Total from investment operations applicable to common shares | (1.08 | ) | 6.32 | 1.37 | 3.74 | ||||||||||||||

| Less: Offering costs charged to paid-in capital—preferred shares | (0.02 | ) | (0.01 | ) | (0.02 | ) | (0.12 | ) | |||||||||||

| Offering costs charged to paid-in capital—common shares | — | — | — | (0.04 | ) | ||||||||||||||

| Dilutive effect of common share offering | — | — | — | (0.12 | ) | ||||||||||||||

| Preferred and common share offering cost adjustment | — | — | 0.00 | c | — | ||||||||||||||

| Total offering costs | (0.02 | ) | (0.01 | ) | (0.02 | ) | (0.28 | ) | |||||||||||

| Less dividends and distributions to common shareholders from: | |||||||||||||||||||

| Net investment income | (0.99 | ) | (1.13 | ) | (0.93 | ) | (0.79 | ) | |||||||||||

| Net realized gain on investments | (0.33 | ) | (0.87 | ) | (0.46 | ) | (0.03 | ) | |||||||||||

| Tax return of capital | (0.67 | ) | (0.35 | ) | (0.21 | ) | (0.23 | ) | |||||||||||

| Total dividends and distributions to common shareholders | (1.99 | ) | (2.35 | ) | (1.60 | ) | (1.05 | ) | |||||||||||

| Net increase (decrease) in net asset value per common share | (3.09 | ) | 3.96 | (0.25 | ) | 2.41 | |||||||||||||

| Net asset value, per common share, end of period | $ | 22.13 | $ | 25.22 | $ | 21.26 | $ | 21.51 | |||||||||||

| Market value, per common share, end of period | $ | 20.11 | $ | 22.35 | $ | 17.66 | $ | 18.76 | |||||||||||

| Net asset value total returne | –3.69 | % | 32.65 | % | 7.65 | % | 19.46 | %d | |||||||||||

| Market value returne | –1.24 | % | 41.52 | % | 2.53 | % | –0.50 | %d | |||||||||||

See accompanying notes to financial statements.

25

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

FINANCIAL HIGHLIGHTS—(Continued)

| For the Year Ended December 31, | For the Period January 30, 2004a through | ||||||||||||||||||

| Ratios/Supplemental Data: | 2007 | 2006 | 2005 | December 31, 2004 | |||||||||||||||

| Net assets applicable to common shares, end of period (in millions) | $ | 1,302.5 | $ | 1,484.3 | $ | 1,251.4 | $ | 1,266.2 | |||||||||||

| Ratio of expenses to average daily net assets applicable to common shares (before expense reduction)g | 1.60 | % | 1.57 | % | 1.57 | % | 1.49 | %f | |||||||||||

| Ratio of expenses to average daily net assets applicable to common shares (net of expense reduction)g | 1.29 | % | 1.27 | % | 1.27 | % | 1.21 | %f | |||||||||||

| Ratio of net investment income to average daily net assets applicable to common shares (before expense reduction)g | 5.12 | % | 5.47 | % | 5.15 | % | 5.40 | %f | |||||||||||

| Ratio of net investment income to average daily net assets applicable to common shares (net of expense reduction)g | 5.42 | % | 5.77 | % | 5.45 | % | 5.68 | %f | |||||||||||

| Ratio of expenses to average daily managed assets (before expense reduction)g,h | 1.04 | % | 1.04 | % | 1.04 | % | 1.04 | %f | |||||||||||

| Ratio of expenses to average daily managed assets (net of expense reduction)g,h | 0.84 | % | 0.84 | % | 0.84 | % | 0.84 | %f | |||||||||||

| Portfolio turnover rate | 22 | % | 24 | % | 20 | % | 18 | %d | |||||||||||

| Preferred Shares: | |||||||||||||||||||

| Liquidation value, end of period (in 000's) | $ | 795,000 | $ | 700,000 | $ | 645,000 | $ | 570,000 | |||||||||||

| Total shares outstanding (in 000's) | 32 | 28 | 26 | 23 | |||||||||||||||

| Asset coverage ratio | 264 | % | 312 | % | 294 | % | 322 | % | |||||||||||

| Asset coverage per share | $ | 65,958 | $ | 78,011 | $ | 73,504 | $ | 80,534 | |||||||||||

| Liquidation preference per share | $ | 25,000 | $ | 25,000 | $ | 25,000 | $ | 25,000 | |||||||||||

| Average market value per sharei | $ | 25,000 | $ | 25,000 | $ | 25,000 | $ | 25,000 | |||||||||||

a Commencement of operations.

b Calculation based on average common shares outstanding.

c Amount is less than $0.005.

d Not annualized.

e Total market value return is computed based upon the New York Stock Exchange market price of the fund's shares and excludes the effects of brokerage commissions. Total net asset value return measures the changes in value over the period indicated, taking into account dividends as reinvested. Dividends and distributions, if any, are assumed for purposes of these calculations, to be reinvested at prices obtained under the fund's dividend reinvestment plan.

f Annualized.

g Ratios do not reflect dividend payments to preferred shareholders.

h Average daily managed assets represent net assets applicable to common shares plus liquidation preference of preferred shares.

i Based on weekly prices.

See accompanying notes to financial statements.

26

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

NOTES TO FINANCIAL STATEMENTS

Note 1. Significant Accounting Policies

Cohen & Steers REIT and Utility Income Fund, Inc. (the fund) was incorporated under the laws of the State of Maryland on October 1, 2003 and is registered under the Investment Company Act of 1940, as amended, as a nondiversified, closed-end management investment company. The fund's investment objective is high current income.

The following is a summary of significant accounting policies consistently followed by the fund in the preparation of its financial statements. The policies are in conformity with accounting principles generally accepted in the United States of America (GAAP). The preparation of the financial statements in accordance with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

Portfolio Valuation: Investments in securities that are listed on the New York Stock Exchange are valued, except as indicated below, at the last sale price reflected at the close of the New York Stock Exchange on the business day as of which such value is being determined. If there has been no sale on such day, the securities are valued at the mean of the closing bid and asked prices for the day or, if no asked price is available, at the bid price.

Securities not listed on the New York Stock Exchange but listed on other domestic or foreign securities exchanges or admitted to trading on the National Association of Securities Dealers Automated Quotations, Inc. (Nasdaq) national market system are valued in a similar manner. Securities traded on more than one securities exchange are valued at the last sale price on the business day as of which such value is being determined as reflected on the tape at the close of the exchange representing the principal market for such securities.

Readily marketable securities traded in the over-the-counter market, including listed securities whose primary market is believed by Cohen & Steers Capital Management, Inc. (the investment manager) to be over-the-counter, but excluding securities admitted to trading on the Nasdaq National List, are valued at the official closing prices as reported by Nasdaq, the National Quotation Bureau, or such other comparable sources as the Board of Directors deem appropriate to reflect their fair market value. If there has been no sale on such day, the securities are valued at the mean of the closing bid and asked prices for the day, or if no asked price is available, at the bid price. However, certain fixed-income securities may be valued on the basis of prices provided by a pricing service when such prices are believed by the Board of Directors to reflect the fair market value of such securities. Where securities are traded on more than one exchan ge and also over-the-counter, the securities will generally be valued using the quotations the Board of Directors believes most closely reflect the value of such securities.

Securities for which market prices are unavailable, or securities for which the investment manager determines that bid and/or asked price does not reflect market value, will be valued at fair value pursuant to procedures approved by the fund's Board of Directors. Circumstances in which market prices may be unavailable include, but are not limited to, when trading in a security is suspended, the exchange on which the security is traded is subject to an unscheduled close or disruption or material events occur after the close of the exchange on which the security

27

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

NOTES TO FINANCIAL STATEMENTS—(Continued)

is principally traded. In these circumstances, the fund determines fair value in a manner that fairly reflects the market value of the security on the valuation date based on consideration of any information or factors it deems appropriate. These may include recent transactions in comparable securities, information relating to the specific security and developments in the markets.

The fund's use of fair value pricing may cause the net asset value of fund shares to differ from the net asset value that would be calculated using market quotations. Fair value pricing involves subjective judgments and it is possible that the fair value determined for a security may be materially different than the value that could be realized upon the sale of that security.

Short-term debt securities, which have a maturity date of 60 days or less, are valued at amortized cost, which approximates value.

Security Transactions and Investment Income: Security transactions are recorded on trade date. Realized gains and losses on investments sold are recorded on the basis of identified cost. Interest income is recorded on the accrual basis. Discounts are accreted and premiums are amortized over the life of the respective securities. Dividend income is recorded on the ex-dividend date except for certain dividends on foreign securities, which are recorded as soon as the fund is informed after the ex-dividend date. The fund records distributions received in excess of income from underlying investments as a reduction of cost of investments and/or realized gain. Such amounts are based on estimates if actual amounts are not available, and actual amounts of income, realized gain and return of capital may differ from the estimated amounts. The fund adjusts the estimated amoun ts of the components of distributions (and consequently its net investment income) as an increase to unrealized appreciation/ (depreciation) and realized gain/(loss) on investments as necessary once the issuers provide information about the actual composition of the distributions.

Foreign Currency Translations: The books and records of the fund are maintained in U.S. dollars as follows: (1) the foreign currency market value of investment securities, other assets and liabilities and foreign currency contracts are translated at the exchange rates prevailing at the end of the period; and (2) purchases, sales, income and expenses are translated at the exchange rates prevailing on the respective dates of such transactions. The resultant exchange gains and losses are recorded as realized and unrealized gain/loss on foreign exchange transactions. Pursuant to U.S. federal income tax regulations, certain foreign exchange gains/losses included in realized and unrealized gain/loss are included in or are a reduction of ordinary income for federal income tax purposes. The fund does not isolate that portion of the results of operations arising as a resul t of changes in the foreign exchange rates from the changes in the market prices of the securities.

Foreign Securities: The fund may directly purchase securities of foreign issuers. Investing in securities of foreign issuers involves special risks not typically associated with investing in securities of U.S. issuers. The risks include possible revaluation of currencies, the ability to repatriate funds, less complete financial information about companies and possible future adverse political and economic developments. Moreover, securities of many

28

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

NOTES TO FINANCIAL STATEMENTS—(Continued)

foreign issuers and their markets may be less liquid and their prices more volatile than those of securities of comparable U.S. issuers.

Interest Rate Swaps: The fund uses interest rate swaps in connection with the sale of preferred shares. The interest rate swaps are intended to reduce the risk that an increase in short-term interest rates could have on the performance of the fund's common shares as a result of the floating rate structure of the preferred shares. In these interest rate swaps, the fund agrees to pay the other party to the interest rate swap (which is known as the counterparty) a fixed rate payment in exchange for the counterparty agreeing to pay the fund a variable rate payment that is intended to approximate the fund's variable rate payment obligation on the preferred shares. The payment obligation is based on the notional amount of the swap. Depending on the state of interest rates in general, the use of interest rate swaps could enhance or harm the overall performance of the com mon shares. The market value of interest rate swaps is based on pricing models that consider the time value of money, volatility, the current market and contractual prices of the underlying financial instrument. Unrealized appreciation is reported as an asset and unrealized depreciation is reported as a liability on the Statement of Assets and Liabilities. The change in value of swaps, including the accrual of periodic amounts of interest to be paid or received on swaps, is reported as unrealized appreciation or depreciation in the Statement of Operations. A realized gain or loss is recorded upon payment or receipt of a periodic payment or termination of swap agreements. Swap agreements involve, to varying degrees, elements of market and counterparty risk, and exposure to loss in excess of the related amounts reflected in the Statement of Assets and Liabilities.

Dividends and Distributions to Shareholders: Dividends from net investment income and capital gain distributions are determined in accordance with U.S. federal income tax regulations, which may differ from GAAP. Dividends from net investment income are declared and paid monthly. Net realized capital gains, unless offset by any available capital loss carryforward, are typically distributed to shareholders at least annually. Dividends and distributions to shareholders are recorded on the ex-dividend date and are automatically reinvested in full and fractional shares of the fund unless the shareholder has elected to have them paid in cash.

Distributions paid by the fund are subject to recharacterization for tax purposes. Based upon the results of operations for the year ended December 31, 2007, a portion of the dividends have been reclassified to return of capital and distributions of net realized capital gains.

Series M7, Series T7, Series T7-2, Series W7, Series TH7 and Series F7 preferred shares pay dividends based on a variable interest rate set at auctions, normally held every seven days. Dividends and distributions are declared and recorded for the subsequent seven day period on the auction date. In most instances, dividends are payable every seven days, on the first business day following the end of the dividend period.

Series M28, Series T28, Series W28 and Series F28 preferred shares pay dividends based on a variable interest rate set at auctions, normally held every 28 days. The dividends are declared and recorded for the subsequent 28 day

29

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

NOTES TO FINANCIAL STATEMENTS—(Continued)

period on the auction date. In most instances, dividends are payable every 28 days, on the first business day following the end of the dividend period.

Income Taxes: It is the policy of the fund to continue to qualify as a regulated investment company, if such qualification is in the best interest of the shareholders, by complying with the requirements of Subchapter M of the Internal Revenue Code applicable to regulated investment companies, and by distributing substantially all of its taxable earnings to its shareholders. Accordingly, no provision for federal income or excise tax is necessary.

Note 2. Investment Management Fees, Administration Fees and Other Transactions with Affiliates

Investment Management Fees: The investment manager serves as the fund's investment manager pursuant to an investment management agreement (the management agreement). Under the terms of the management agreement, the investment manager provides the fund with day-to-day investment decisions and generally manages the fund's investments in accordance with the stated polices of the fund, subject to the supervision of the Board of Directors.

For the services under the management agreement, the fund pays the investment manager a management fee, accrued daily and paid monthly, at an annual rate of 0.85% of the fund's average daily managed asset value. Managed asset value is the net asset value of the common shares plus the liquidation preference of the preferred shares.

The investment manager has contractually agreed to waive its investment management fee in the amount of 0.20% of average daily managed asset value for the first five years of the fund's operations, 0.15% of average daily managed asset value in year six, 0.10% of average daily managed asset value in year seven and 0.05% of average daily managed asset value in year eight. During the year ended December 31, 2007, the investment manager waived its fee at the annual rate of 0.20%.

Administration Fees: The fund has entered into an administration agreement with the investment manager under which the investment manager performs certain administrative functions for the fund and receives a fee, accrued daily and paid monthly, at the annual rate of 0.06% of the fund's average daily managed assets up to $1 billion, 0.04% of the fund's average daily managed assets in excess of $1 billion up to $1.5 billion and 0.02% of the fund's average daily managed assets in excess of $1.5 billion. For the year ended December 31, 2007, the fund incurred $947,691 in administration fees. Additionally, the fund has retained State Street Bank and Trust Company as sub-administrator under a fund accounting and administration agreement.

Directors' and Officers' Fees: Certain directors and officers of the fund are also directors, officers, and/or employees of the investment manager. The fund does not pay compensation to any affiliated directors and officers except for the Chief Compliance Officer, who received $14,770 from the fund for the year ended December 31, 2007.

30

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

NOTES TO FINANCIAL STATEMENTS—(Continued)

Note 3. Purchases and Sales of Securities

Purchases and sales of securities, excluding short-term investments, for the year ended December 31, 2007, totaled $510,286,241 and $489,800,432, respectively.

Note 4. Income Tax Information

The tax character of dividends and distributions paid was as follows:

| For the Year Ended December 31, | |||||||||||

| 2007 | 2006 | ||||||||||

| Ordinary income | $ | 90,287,505 | $ | 87,876,128 | |||||||

| Long-term capital gains | 29,891,797 | 64,046,819 | |||||||||

| Tax return of capital | 39,569,854 | 20,817,396 | |||||||||

| Total dividends and distributions | $ | 159,749,156 | $ | 172,740,343 | |||||||

As of December 31, 2007, the tax-basis components of accumulated earnings and the federal tax cost were as follows:

| Gross unrealized appreciation | $ | 733,255,578 | |||||

| Gross unrealized depreciation | (455,956,986 | ) | |||||

| Net unrealized appreciation | $ | 277,298,592 | |||||

| Cost for federal income tax purposes | $ | 1,825,462,363 | |||||

As of December 31, 2007, the fund had temporary book/tax differences primarily attributable to timing differences on dividends payable and the mark-to-market of passive foreign investment companies and permanent book/tax differences primarily attributable to differing treatment on interest rate swaps. To reflect reclassifications arising from the permanent differences, paid-in capital was charged $273,548, accumulated net realized gain was charged $9,149,950 and accumulated net investment income was credited $9,423,498.

Note 5. Capital Stock

The fund is authorized to issue 100 million shares of common stock at a par value of $0.001 per share.

During the year ended December 31, 2007 and the year ended December 31, 2006, the fund issued no shares of common stock for the reinvestment of dividends.

31

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

NOTES TO FINANCIAL STATEMENTS—(Continued)

The fund's articles of incorporation authorize the issuance of fund preferred shares, par value $0.001 per share, in one or more classes or series, with rights as determined by the Board of Directors, by action of the Board of Directors without the approval of the common shareholders.

On February 14, 2007, the fund issued 3,800 auction market preferred shares, Series T7-2 (par value $0.001). Proceeds paid to the fund amounted to $93,816,000 after deduction of underwriting commissions and offering expenses of $1,184,000. This issue has received a "AAA/Aaa" rating from Standard & Poor's and Moody's.

On February 22, 2006 the fund issued 2,200 auction market preferred shares, Series M28 (par value $0.001). Proceeds paid to the fund amounted to $54,144,513 after deduction of underwriting commissions and offering expenses of $855,487. This issue has received a "AAA/Aaa" rating from Standard & Poor's and Moody's.

Preferred shares are senior to the fund's common shares and will rank on a parity with shares of any other series of preferred shares, and with shares of any other series of preferred stock of the fund, as to the payment of dividends and the distribution of assets upon liquidation. If the fund does not timely cure a failure to (1) maintain a discounted value of its portfolio equal to the preferred shares basic maintenance amount, (2) maintain the 1940 Act preferred shares asset coverage, or (3) file a required certificate related to asset coverage on time, the preferred shares will be subject to a mandatory redemption at the redemption price of $25,000 per share plus an amount equal to accumulated but unpaid dividends thereon to the date fixed for redemption. To the extent permitted under the 1940 Act and Maryland Law, the fund at its option may without consent of the holders of preferred shares, redeem preferred shares having a dividend per iod of one year or less, in whole, or in part, on the business day after the last day of such dividend period upon not less than 15 calendar days and not more than 40 calendar days prior to notice. The optional redemption price is $25,000 per share plus an amount equal to accumulated but unpaid dividends thereon to the date fixed for redemption.

The fund's common shares and preferred shares have equal voting rights of one vote per share and vote together as a single class, except in certain circumstances regarding the election of directors. In addition, the affirmative vote of the holders of a majority, as defined in the 1940 Act, of the outstanding preferred shares shall be required to (1) approve any plan of reorganization that would adversely affect the preferred shares and (2) approve any matter that materially and adversely affects the rights, preferences, or powers of that series.

32

COHEN & STEERS REIT AND UTILITY INCOME FUND, INC.

NOTES TO FINANCIAL STATEMENTS—(Continued)

The following table reflects the preferred shares issued and outstanding as of December 31, 2007 along with the range of dividend rates paid during the year ended December 31, 2007:

| Value | Range | ||||||||||

| Auction market preferred shares, Series M7, ($25,000 liquidation value, $0.001 par value, 3,360 shares issued and outstanding) | $ | 84,000,000 | 4.80 | %-6.35% | |||||||

| Auction market preferred shares, Series M28, ($25,000 liquidation value, $0.001 par value, 2,200 shares issued and outstanding) | $ | 55,000,000 | 5.09 | %-6.25% | |||||||

| Auction market preferred shares, Series T7, ($25,000 liquidation value, $0.001 par value, 3,360 shares issued and outstanding) | $ | 84,000,000 | 4.95 | %-6.50% | |||||||

| Auction market preferred shares, Series T7-2, ($25,000 liquidation value, $0.001 par value, 3,800 shares issued and outstanding) | $ | 95,000,000 | 5.00 | %-6.50% | |||||||

| Auction market preferred shares, Series T28, ($25,000 liquidation value, $0.001 par value, 3,000 shares issued and outstanding) | $ | 75,000,000 | 5.15 | %-6.10% | |||||||

| Auction market preferred shares, Series W7, ($25,000 liquidation value, $0.001 par value, 3,360 shares issued and outstanding) | $ | 84,000,000 | 4.80 | %-6.35% | |||||||