SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

Filed by the Registrantx Filed by a Party other than the Registrant¨

Check the appropriate box:

¨ Preliminary Proxy Statement

¨ Confidential, For Use of the Commission Only (as permitted by Rule 14a-6(e)(2))

¨ Definitive Proxy Statement

x Definitive Additional Materials

¨ Soliciting Material Under Rule 14a-12

Cohen & Steers REIT and Utility Income Fund, Inc.

(Name of Registrant as Specified in Its Charter)

(Name of Person(s) Filing Proxy Statement, if Other Than the Registrant)

Payment of Filing Fee (Check the appropriate box): | ||

x | No fee required. | |

¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(4) and 0-11. | |

| (1) Title of each class of securities to which transaction applies: | ||

(2) Aggregate number of securities to which transaction applies:

| ||

(3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| ||

(4) Proposed maximum aggregate value of transaction:

| ||

(5) Total fee paid:

| ||

¨ | Fee paid previously with preliminary materials. | |

¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing.

| |

| (1) Amount Previously Paid: | ||

| (2) Form, Schedule or Registration Statement No.: | ||

| (3) Filing Party: | ||

| (4) Date Filed: | ||

Cohen & Steers Select Utility Fund, Inc. (UTF) Cohen & Steers REIT and Utility Income Fund, Inc. (RTU) Annual Meeting of Stockholders |

2 CPRET8164 Table of Contents Auction Market Preferred Shares VI. Shareholder Proposal V. Election of Directors IV. RTU III. UTF II. Overview I. |

Overview |

4 CPRET8164 About Cohen & Steers Leading manager of high-income equity portfolios with a focus on: — Global real estate securities — Preferred stocks — Utilities — Large cap value equities Global presence through offices in New York, Seattle, Brussels and Hong Kong $29.8 billion in assets under management as of December 31, 2007 Advises 11 open-end funds and 11 closed-end funds Record of 32 dividend increases (never missing or reducing distributions on any existing Cohen & Steers closed-end funds) First closed-end fund launched September 1988 |

5 CPRET8164 Matters for the 2008 Annual Meeting Elect three directors, each for a three-year term — Two directors elected by common and preferred voting together — One director elected by preferred shareholders voting separately Actions of Western Investment LLC, controlled by Arthur Lipson — Soliciting for an alternate slate of three directors — Activist stockholder proposal by Bulldog Investors advocating for an extensive and continuous partial tender offer policy (UTF only) |

6 CPRET8164 Summary Cohen & Steers Our Fund board is independent and engaged. The Directors have: — Overseen outstanding performance for the life of the Funds — Delivered substantial shareholder value and met the Funds’ investment objectives — Taken actions to enhance the net asset value (NAV) and narrow the Funds’ discounts Dissident Shareholder Lipson is self-motivated—his interests are not aligned with all shareholders — Short-term hedge fund speculator looking for a quick profit — Told us directly that the long-term interests of the shareholders is “the directors’ problem”—not his! — Only recently acquired large positions in the Funds (at a discount), augmented by swaps that expire in May Lipson’s approach will have an adverse impact on all long-term shareholders |

UTF |

8 CPRET8164 UTF Performance—Strong and Improving Investment Objective: The Fund’s investment objective is to seek a high level of after-tax total return through investment in utility securities with an emphasis on current income Invests primarily in common stocks, preferred stocks and other equity securities issued by utility companies Strong market performance benefiting all shareholders Outperformed the S&P 1500 Utilities Index and the S&P 500 Index for the one- and three-year periods ended December 31, 2007 Overall Morningstar Rating The overall Morningstar Rating is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year Morningstar Rating metrics, as applicable. For each fund with at least a three-year history, Morningstar calculates its ratings based on a risk-adjusted return measure that accounts for variation in a fund’s monthly performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of funds in each category receive five stars, the next 22.5% receive four stars, the next 35% receive three stars, the next 22.5% receive two stars and the bottom 10% receive one star. Cohen & Steers Select Utility Fund received three stars in the three year category out of 8 funds. ©2008 Morningstar, Inc. All Rights Reserved. Morningstar and/or its content providers are the proprietors of this information; do not permit its unauthorized copying or distribution; do not warrant it to be accurate, complete or timely; and are not responsible for damages or losses arising from its use. |

9 CPRET8164 UTF Performance—Strong and Improving (continued) Original distribution rate $1.02; current distribution rate is $2.22 per share; a 118% increase NYSE traded; market cap $1.0 billion as of March 13, 2008 Leveraged fund triple AAA rated with auction market preferred shares (AMPS) — Aggregate liquidation preference $652 million as of March 13, 2008 Cohen & Steers has managed UTF since its inception in 2004 The portfolio managers, Robert S. Becker and William F. Scapell, have been with Cohen & Steers since inception of the Fund |

10 CPRET8164 UTF Performance—Strong and Improving (continued) 9.32% 8.63% 5.49% S&P 500 18.90% 17.68% 16.46% S&P 1500 Utilities 17.02% 20.62% 25.34% UTF Since Inception (3/30/2004) 3 Years 1 Year Total returns as of December 31, 2007, based on market price. The performance data quoted represent past performance. Past performance is no guarantee of future results. The investment return will vary and the market value of an investment will fluctuate and shares may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. |

RTU |

12 CPRET8164 RTU Performance—Strong and Improving Investment Objective: The Fund’s primary investment objective is to seek high current income Invests primarily in securities issued by real estate companies, such as real estate investment trusts, or “REITs”, and companies engaged in the utilities industry Strong market performance benefiting all shareholders Outperformed the FTSE NAREIT Equity Index and the Fund’s blended index for the one- and three-year periods ended December 31, 2007 The overall Morningstar Rating is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year Morningstar Rating metrics, as applicable. For each fund with at least a three-year history, Morningstar calculates its ratings based on a risk-adjusted return measure that accounts for variation in a fund’s monthly performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of funds in each category receive five stars, the next 22.5% receive four stars, the next 35% receive three stars, the next 22.5% receive two stars and the bottom 10% receive one star. Cohen & Steers Select REIT and Utility Income Fund received four stars in the three year category out of 8 funds. ©2008 Morningstar, Inc. All Rights Reserved. Morningstar and/or its content providers are the proprietors of this information; do not permit its unauthorized copying or distribution; do not warrant it to be accurate, complete or timely; and are not responsible for damages or losses arising from its use. Overall Morningstar Rating |

13 CPRET8164 RTU Performance—Strong and Improving (continued) Original distribution rate $1.26; current distribution rate is $1.65 per share, a 31% increase NYSE traded; market cap approximately $1.02 billion as of March 13, 2008 Leveraged fund triple AAA rated with AMPS — Aggregate liquidation preference $795 million as of March 13, 2008 Cohen & Steers has managed RTU since its inception in 2004 The portfolio management team consisting of Martin Cohen, Joseph M. Harvey, Robert S. Becker, Thomas N. Bohjalian, Robert H. Steers and William F. Scapell, has been with Cohen & Steers since inception of the Fund |

14 CPRET8164 RTU Performance—Strong and Improving (continued) 12.92% 10.40% -2.63% Blended Index (1) 12.95% 8.50% -15.69% FTSE NAREIT Equity Index 9.48% 12.75% -1.24% RTU Since Inception (1/30/2004) 3 Years 1 Year (1) Blended Index consists of 40% NAREIT Equity REIT Index, 40% S&P 1500 Utilities and 20% Merrill Lynch Fixed Rate Preferred Index. Total returns as of December 31, 2007, based on market price. The performance data quoted represent past performance. Past performance is no guarantee of future results. The investment return will vary and the market value of an investment will fluctuate and shares may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. |

Election of Directors |

16 CPRET8164 Independent and Engaged Board Meeting the Fund’s investment objectives for shareholders Approved additional investment strategies designed to increase income return of the Fund Fully supported Management’s build-out of a dedicated team — Responsible for implementing a covered call writing strategy designed to further enhance the Fund’s investment objectives and help meet the firm’s goal of increasing the distribution rate The Board has increased UTF’s distribution level three times in the past 12 months and a total of five times since the Fund was launched in March 2004 The distribution level has increased 80% in the past 12 months and 118% since inception UTF’s annual distribution rate is now equal to $2.22 per share, a 8.9% annualized rate (1) The Board has a solid history of taking steps to increase shareholder value and narrow the discount to NAV UTF (1) Based upon NYSE closing price on February 25, 2008. |

17 CPRET8164 Independent and Engaged Board (continued) A $10,000 investment in UTF at the Fund’s inception in 2004 would have been worth $17,092 as of December 31, 2007 (1) As of March 13, 2008, UTF’s discount to NAV was 8.98%, down from 13.95% on December 29, 2006. The discount was 6.97% on December 31, 2007, 5.32% on January 31, 2008 and 5.09% on February 29, 2008 — The Directors’ actions have improved the Fund’s discount and management believes any recent increase in the discount is a result of industry-wide issues affecting all leveraged closed- end funds The Board has a solid history of taking steps to increase shareholder value and narrow the discount to NAV UTF (1) Includes the reinvestment of distributions, which are generally reinvested at NAV if the shares are trading at a discount. Does not include brokerage costs. |

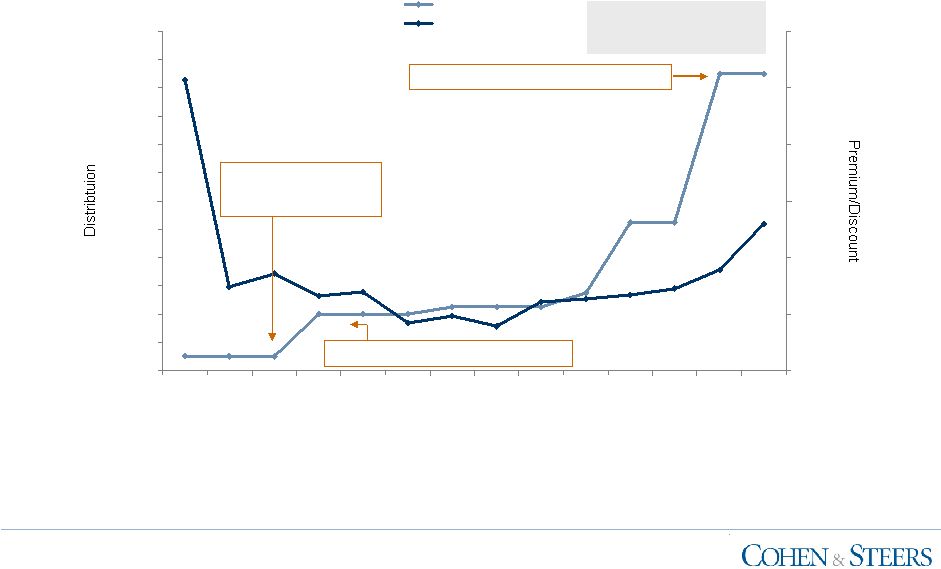

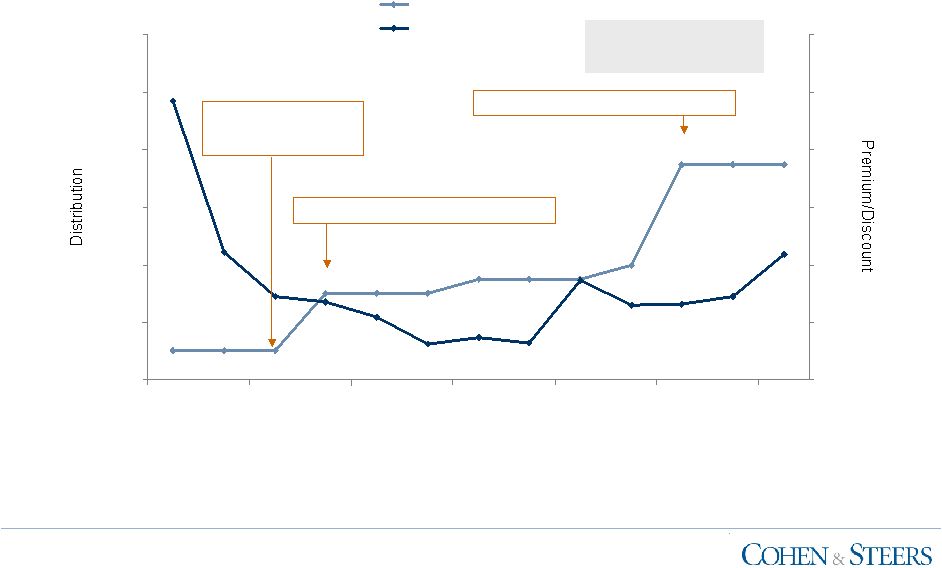

18 CPRET8164 Independent and Engaged Board (continued) UTF’s discount to NAV has declined as a result of strong performance and distribution increases UTF Distribution/Premium Discount History 0.103 0.133 0.108 0.185 0.100 0.085 $0.08 $0.09 $0.10 $0.11 $0.12 $0.13 $0.14 $0.15 $0.16 $0.17 $0.18 $0.19 $0.20 4/2004 12/2004 6/2005 3/2006 12/2006 6/2007 12/2007 -20% -15% -10% -5% 0% 5% 10% Distribution Rate Premium/Discount 12/13/07: Fifth distribution increase 2007: Amended filing for closed-end managed distribution order 2004: Filed for closed-end managed distribution order 3/8/05: First distribution increase |

19 CPRET8164 Independent and Engaged Board (continued) Meeting the Fund’s investment objectives for shareholders Approved additional investment strategies designed to increase income return of the Fund Fully supported Management’s build-out of a dedicated team — Responsible for implementing a covered call writing strategy designed to further enhance the Fund’s investment objectives and help meet the firm’s goal of increasing the distribution rate The Board has increased RTU’s distribution level each year since the fund was launched in January 2004 RTU has paid total distributions of $6.99 per share since inception RTU The Board has a solid history of taking steps to increase shareholder value and narrow the discount to NAV |

20 CPRET8164 Independent and Engaged Board (continued) A $10,000 investment in RTU at the Fund’s inception in 2004 would have been worth $14,006 as of December 31, 2007 (1) As of March 13, 2008, RTU’s discount to NAV was 10.78%, down from 11.38% on December 29, 2006. The discount was 9.13% on December 31, 2007, 7.75% on January 31, 2008 and 8.44% on February 29, 2008 — The Directors’ actions have improved the Fund’s discount and management believes any recent increase in the discount is a result of industry-wide issues affecting all leveraged closed-end funds (1) Includes the reinvestment of distributions, which are generally reinvested at NAV if the shares are trading at a discount. Does not include brokerage costs. RTU The Board has a solid history of taking steps to increase shareholder value and narrow the discount to NAV |

21 CPRET8164 0.105 0.115 0.118 0.120 0.138 $0.10 $0.11 $0.12 $0.13 $0.14 $0.15 $0.16 2/2004 12/2004 6/2005 3/2006 12/2006 6/2007 12/2007 -20% -15% -10% -5% 0% 5% 10% Distribution Rate Premium/Discount Independent and Engaged Board (continued) RTU Distribution/Premium Discount History RTU’s discount to NAV has declined as a result of strong performance and distribution increases 2007: Amended filing for closed-end managed distribution order 3/8/05: First distribution increase 6/13/07: Fourth distribution increase 2004: Filed for closed-end managed distribution order |

22 CPRET8164 Independent and Engaged Board—Focused on Discount to NAV In December 2004, the Funds applied to the SEC for an exemption to permit the Funds to adopt a managed distribution plan The Funds submitted an amended application in 2007 If and when this relief is granted, Management expects to recommend to the Board that they consider additional distribution increases, further reducing the discount to NAV Since 2005, the Board has been working with UBS Investment Bank exploring additional ways to decrease the discount in a responsible manner UBS has presented to the Board on multiple occasions and was engaged well before the recent public filings by Lipson and Bulldog Investors Regular updates by Management on NAV, distribution and the discount level (if any) on all Funds Commitment to monitor a Fund’s discount level and take action when appropriate |

23 CPRET8164 Independent and Engaged Board (continued) With the help of UBS and other advisors, during the last two years, the Board has evaluated numerous alternatives for possibly reducing the discount, including the following: — Increasing the distribution rate — Self-tender offers — Converting to an interval fund — Open-ending — Liquidating — Merging with another closed-end fund — Repositioning the Funds’ focus — Instituting a share buyback program After analyzing each of the options, each time the Board concluded that increasing the distribution rate is the only proven way to reduce the discount over the long-term while continuing to serve the interests of all shareholders |

24 CPRET8164 Independent and Engaged Board (continued) Lipson wants to initiate a large self-tender aimed at exiting the Funds and unwinding a leveraged derivatives position UBS and other advisors have counseled the Board that share buybacks and self-tenders may hurt long- term shareholders by: — Decreasing the Funds’ assets as short-term investors like Lipson sell their shares back to the Funds, resulting in higher expense ratios for remaining shareholders — Increasing costs like brokerage and other trading expenses as the Funds sell securities to raise cash — Triggering substantial capital gains and taxes — Forcing the Funds’ to redeem/reduce some of their preferred shares/financing, effectively reducing the Fund’s leverage and possibly their returns While the Board may in the future consider buybacks and self-tenders, it will only do so in a responsible manner and for the benefit of ALL shareholders |

25 CPRET8164 Independent, Engaged and Experienced Directors Each of the Board’s nominees has been a director since 2004, regularly assessing, along with the rest of the Board, how best to maintain each Fund’s strong performance while increasing value for all stockholders. Cohen & Steers does not nominate or select any of the independent directors. Bonnie Cohen (1) —consultant; former Undersecretary of State, United States Department of State; Director of NASD quoted Reis, Inc., formerly Wellsford Real Property Richard E. Kroon— lead independent director; member of Investment Committee, Monmouth University; retired chairman and managing partner of the Sprout Group venture capital funds, then an affiliate of Donaldson, Lufkin & Jenrette Securities Corporation; former chairman of the National Venture Capital Association Willard H. Smith Jr.— board member of NYSE listed companies, Essex Property Trust, Inc., Realty Income Corporation and Crest Net Lease, Inc.; managing director at Merrill Lynch & Co., Equity Capital Markets Division (1983–1995) (1) Not related to Martin Cohen |

26 CPRET8164 Lipson Director Nominees Less Qualified The Board’s three nominees are better qualified to serve as closed-end fund directors than Lipson’s nominees Cohen & Steers doesn’t believe Lipson’s nominees will reliably represent all shareholders Lipson’s nominees are conflicted – will they serve the interests of the shareholders in the Funds or the investors in his hedge funds? These nominees will advocate Lipson’s short-term strategy, which is adverse to long-term holders Arthur D. Lipson— sole managing member of Western Investment. Less than one year of experience as a director of a closed-end fund. William J. Roberts— no financial markets experience (per his bio in Lipson’s proxy statement). No experience as a director of a public company or investment company. Matthew S. Crouse— employed by Lipson. No experience as a director of a public company or investment company. |

27 CPRET8164 Lipson’s Interests Are Not Aligned With All Shareholders Western Investment is a hedge fund manager controlled by Lipson with a history of closed-end fund activism In a telephone meeting on December 19, 2007, Lipson told us “I'm not interested in long-term solutions; the long-term is the directors' problem” — He clearly doesn't care about any shareholders but himself and his hedge funds — No value was placed on performance and history of distribution increases as an effective strategy — Lipson’s strategy is likely to impair the ability to maintain the current distribution rate and put further pressure on the discount Lipson’s nominees would detract from the Funds’ focus on sustainable and long-term performance — They will seek to implement proposals to allow Lipson and his hedge funds to sell their shares back to the funds and earn a profit on his expiring derivatives transaction |

28 CPRET8164 Correcting the Record Lipson claims that Cohen & Steers is unresponsive to shareholder concerns and that Cohen & Steers cancelled a meeting with him Cohen & Steers was in fact responsive to Lipson's request for a meeting — Cohen & Steers co-chairmen and CEO’s had a conference call with Lipson in December — At the December meeting, Lipson repeatedly demanded a large share tender be effected — Cohen & Steers agreed to meet with Lipson in January — While the firm was fully prepared to have a second dialogue with Lipson, at the last minute Lipson said that he planned to bring along a reporter — After Cohen & Steers indicated that it would not be constructive to invite the press and confirmed its willingness to meet privately, Lipson abruptly cancelled the meeting |

29 CPRET8164 December 2007 By-Law Amendments The Board reviewed the Funds’ corporate governance provisions at its regular December meeting to ensure that it would be in a position to act in accordance with its responsibilities under Maryland corporate law and to protect the interests of all shareholders. Lipson complains of several provisions—some of which were in place at the time of the 2004 IPOs and were fully disclosed when he acquired his positions. For example, the December changes did not affect the voting threshold percentage for the call of a special shareholder meeting. The Board adopted provisions designed to improve transparency of shareholder information and the proper conduct of meetings. For example, shareholders that make proposals are required to disclose hedging activities to determine whether they are in a similar position as all other shareholders. The Board did not adopt any “poison pills” or similar anti-takeover measures. The Board also amended the by-laws to deal with certain procedural matters. Each measure was standard in Maryland corporate law and was adopted for the purpose of permitting the Board to carry out its responsibilities in the best interests of the Funds and their shareholders. Nothing was done to impede Lipson from instituting a proxy contest or shareholders from submitting proposals, which they have proceeded to do. Corporate Governance |

Shareholder Proposal |

31 CPRET8164 Shareholder Proposal Bulldog Investors is requesting that UTF shareholders approve the following proposal — “If the Fund's shares trade at an average discount of more than 7.5% during any calendar quarter the Fund shall commence a self-tender offer within twenty days of the end of such quarter for 15% of its shares at 98% of net asset value.” Issue—the tender proposal would create an ongoing and burdensome obligation, potentially forcing the Fund into a liquidation as implementing the proposal could result in 60% of the Fund’s assets being liquidated in the fiscal year and harming shareholders who want to remain invested in the Fund Please refer to slide 24 for information about the Board’s actions and reasons for not implementing such a strategy |

Auction Market Preferred Shares |

33 CPRET8164 Auction Market Preferred Shares The Board is very sensitive to the recent lack of liquidity in the AMPS — The Board of Directors, along with management, is addressing the situation and evaluating the best long-term solution for the Funds—one that balances the interests of common and preferred shareholders Lipson, through his hedge fund owns only four AMPS of the Funds totaling $100,000 which was purchased on February 25, 2008, the record date. Together, the Funds have $1.45 billion of AMPS outstanding. Lipson’s proposal would result in the redemption of only a limited number of AMPS, leaving most AMPS outstanding, and would not address the industry-wide issues in the AMPS market Lipson’s proposal to reduce leverage would decrease the distributions to common shareholders and potentially increase the discount |

34 CPRET8164 Forward-Looking Statements Statements made in this presentation that look forward in time involve risks and uncertainties and are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Such risks and uncertainties include, without limitation, the adverse effect from a decline in the securities markets or a decline in the Funds’ performance, a general downturn in the economy, competition from other closed-end investment companies, changes in government policy or regulation, inability of the Funds’ investment adviser to attract or retain key employees, inability of the Funds to implement its investment strategy, inability of the Fund to manage unforeseen costs and other effects related to legal proceedings or investigations of governmental and self-regulatory organizations. |