Aspen Insurance Holdings Limited

Chris O’Kane, Chief Executive Officer

Julian Cusack, Chief Financial Officer

May 2006

Safe Harbor Disclosure

Application of the Safe Harbor of the Private Securities Litigation Reform Act of 1995:

This presentation contains written or oral “forward-looking statements” within the meaning of the U.S. federal securities laws. These statements are made

pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements include all statements that do not

relate solely to historical or current facts, and can be identified by the use of words such as “expect,” “intend,” “plan,” “believe,” “project,” “anticipate,” “seek,”

“will,” “estimate,” “may,” “continue,” and similar expressions of a future or forward-looking nature.

All forward-looking statements address matters that involve risks and uncertainties. Accordingly, there are or will be important factors that could cause actual

results to differ materially from those indicated in these statements. The Company believes these factors include, but are not limited to: the impact of acts of

terrorism and related legislation and acts of war; the possibility of greater frequency or severity of claims and loss activity, including as a result of natural or

man-made catastrophic events such as Hurricanes Katrina, Rita and Wilma, than our underwriting, reserving or investment practices have anticipated; evolving

interpretive issues with respect to coverage as a result of Hurricanes Katrina, Rita and Wilma; the level of inflation in repair costs due to limited availability of

labor and materials after catastrophes; the effectiveness of the Company's loss limitation methods; changes in the availability, cost or quality of reinsurance or

retrocessional coverage; the reliability of, and changes in assumptions to, catastrophe pricing, accumulation and estimated loss models; loss of key personnel;

a decline in our operating subsidiaries' ratings with Standard & Poor's, A.M. Best Company or Moody's Investors Service; changes in general economic

conditions including inflation, foreign currency exchange rates, interest rates and other factors that could affect our investment portfolio; increased competition

on the basis of pricing, capacity, coverage terms or other factors; decreased demand for the Company's insurance or reinsurance products and cyclical

downturn of the industry; changes in governmental regulations or tax laws in jurisdictions where the Company conducts business; Aspen or its Bermudian

subsidiary becoming subject to income taxes in the United States or the United Kingdom; the effect on insurance markets, business practices and relationships

of ongoing litigation, investigations and regulatory activity by the New York State Attorney General's office and other authorities concerning contingent

commission arrangements with brokers and bid solicitation activities; the total industry losses resulting from Hurricanes Katrina, Rita and Wilma and the actual

number of the Company's insureds incurring losses from these storms; and with respect to Hurricanes Katrina, Rita and Wilma, the limited actual loss reports

received from the Company's insureds to date, the preliminary nature of possible loss information received by brokers to date on behalf of cedants, the

Company's reliance on industry loss estimates and those generated by modeling techniques, the impact of these storms on the Company's reinsurers, any

changes in the Company's reinsurers' credit quality, the amount and timing of reinsurance recoverables and reimbursements actually received by the Company

from its reinsurers and the overall level of competition and the related demand and supply dynamics as contracts come up for renewal. For a more detailed

description of these uncertainties and other factors, please see the "Risk Factors" section in Aspen's Annual Report on Form 10-K for the year ended

December 31, 2005, filed with the U.S. Securities and Exchange Commission on March 6, 2006. Aspen undertakes no obligation to publicly update or revise

any forward-looking statements, whether as a result of new information, future events or otherwise. Readers are cautioned not to place undue reliance on

these forward-looking statements, which speak only as of the dates on which they are made.

2

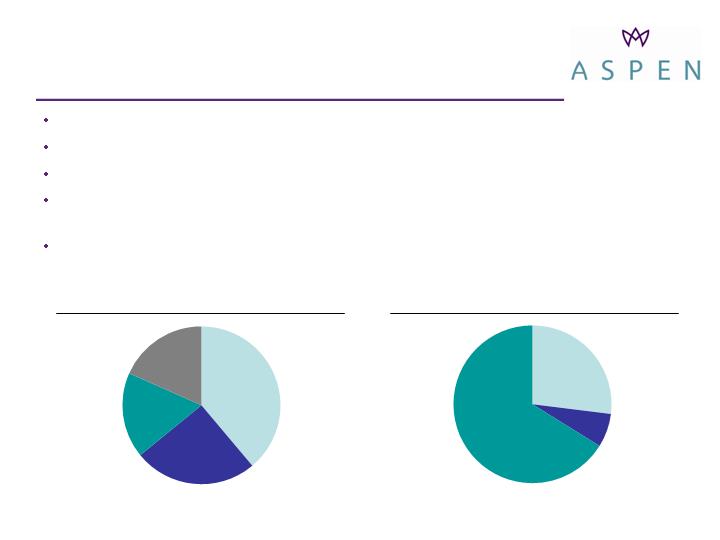

Who We Are

Property

Reinsurance

39%

Casualty

Reinsurance

25%

Specialty

18%

Insurance

18%

2005 Underwriting by Segment (GWP)

2005 Underwriting by Subsidiary (GWP)

* Shareholders’ equity (including preference shares, ex-AOCI) plus long-term debt

** Bermuda balance excludes premiums received from Aspen UK and Aspen Specialty under group quota share

UK

66%

Bermuda**

27%

US

7%

$2.3bn market cap

$1.9bn common equity (ex-AOCI) and $2.4bn total capital* as of 31-Mar-2006

~370 employees in Bermuda, London and US (as of 31-Mar-2006)

Ratings of A (S&P), A2 (Moody’s) and A / A- (AM Best, for Aspen UK and Aspen

Bermuda)

$2.1bn Gross Written Premium (GWP) in 2005; 27% GWP Compound Annual

Growth Rate since 2003

100% = $2.1bn

100% = $2.1bn

3

Investment Highlights

Leading specialty reinsurer and insurer

Diverse underwriting skills

Growing breadth of product and market presence

Proven ability and willingness to allocate capital based on market

opportunities

Meaningful exposure to hardening property pricing cycle

Material reduction in risk profile in 2006 and upgraded modeling

capabilities

Expected to result in reduced earnings volatility

Continued earnings momentum

Continued diversification of underwriting

Opportunity to increase investment yield

Capital flexibility

4

Strategic Vision

Offer specialized insurance and reinsurance to clients where price is not

the key determinant

Niche based products with a bias towards the more complex risks

Products where experience and judgment are critical to success

Products where Aspen will be compensated for its expertise and

service

Core differentiators: Underwriting, service & talent management

Maintain flexibility to opportunistically expand into new markets

Anticipate and respond quickly to events and new information

Rigorous soft cycle and portfolio management

Compete in commodity type products only when Aspen has better

knowledge and execution than the competition, or if market conditions

provide attractive returns

5

Selective Business

Line Expansion

Progressive diversification of strategic footprint through incremental expansion into

adjacent business lines*

Key enabling factors:

Consistency with Aspen’s core competencies

Appropriate timing

Availability of proven, successful underwriting teams

2003

2004

2005

2006 +

Specialty

Reinsurance

Aviation

Marine

US Casualty

US Surplus

lines

Aviation

Insurance

Marine

Insurance

Energy

Insurance

Continuing

diversification

Decrease of Property

Reinsurance

contribution to overall

portfolio

Increased emphasis

on Specialty lines

* Businesses shown for first year of meaningful premium contribution

6

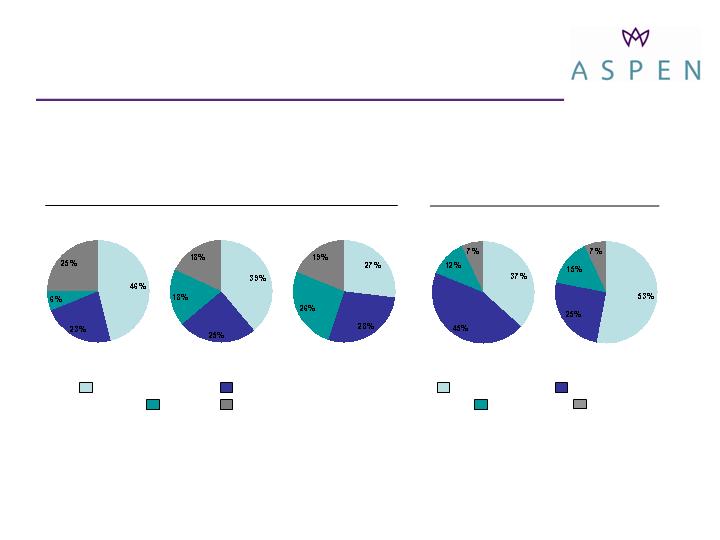

Business Mix

By Segment

By Geography

* 2003 Specialty lines excludes QQS of Wellington Syndicate 2020

** Worldwide includes policies where risks are across the world; includes policies both specifically including and excluding the United States

100% = $1.3bn

Gross Written Premiums

*

100% = $2.1bn

100% = $1.3bn

100% = $2.1bn

2003

2005

2006E

2003

2005

Property Reinsurance Casualty Reinsurance

Specialty Insurance

US and Canada UK and Europe

Worldwide** Other

7

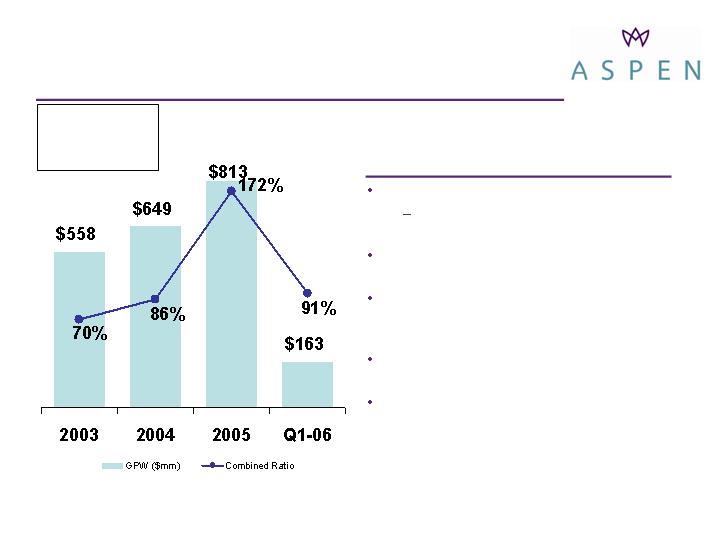

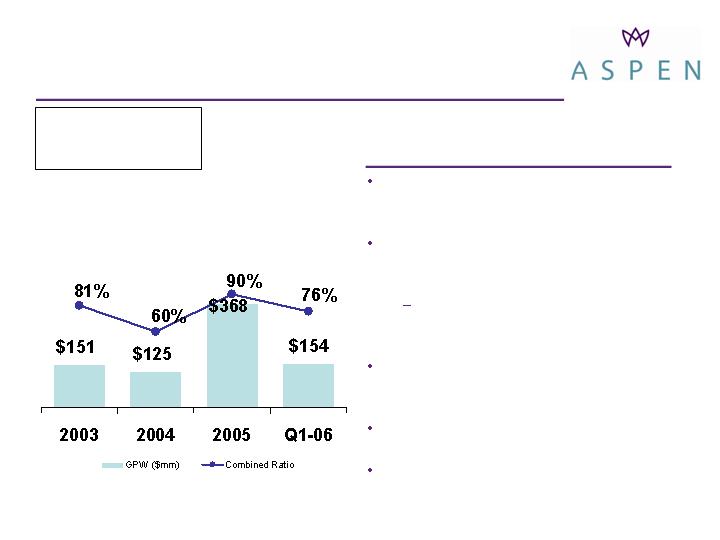

Property Reinsurance

Comments

Broad re-underwriting in 2006

Sharply reduced aggregate exposure

limits in Florida, California, Europe

US seeing better increases than the

international account

Low production in Q1-06 reflects relatively

modest pricing improvement at January

renewals

Observed much more attractive

conditions in April renewal season

Expect further hardening as year

advances

* Includes 39 points from hurricane and windstorm related losses

** Includes 104 points from hurricane and windstorm related losses

*

**

8

GWP Breakdown – 2005

Catastrophe

46 %

Risk Excess

32

Pro Rata

21

Facultative

1

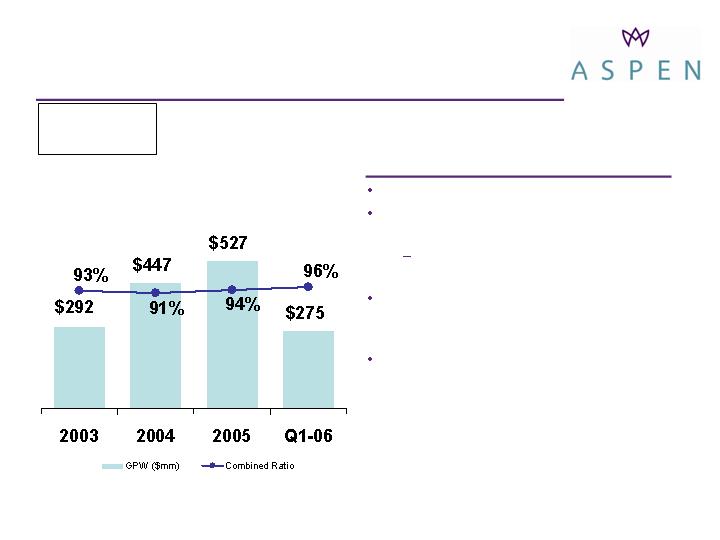

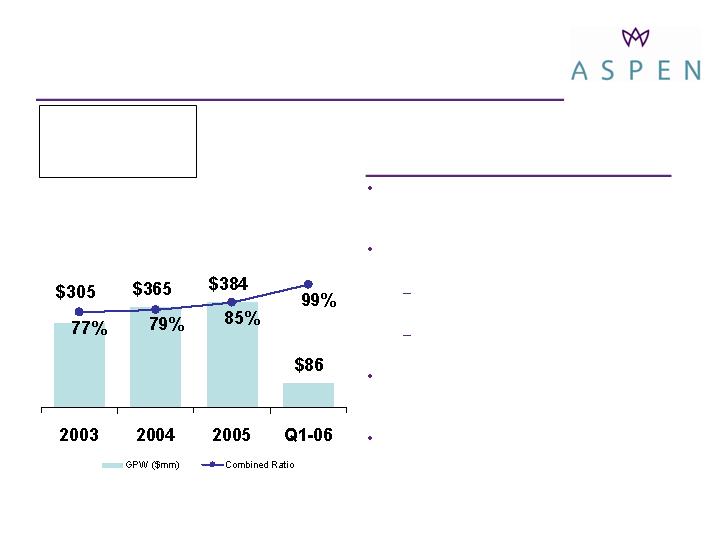

Casualty Reinsurance

Comments

Rates remain adequate but have been flat

US Casualty experienced nominal rate

increases across the portfolio

Partially offset by Casualty claims

inflation

Primary rates on Medical Malpractice and

Workers’ Compensation catastrophe

experienced little change in rates

Upward trend in combined ratio reflects

increasing contribution from US business

with higher acquisition costs and loss

ratios

9

GWP Breakdown – 2005

US Treaty

58 %

Non-US Treaty

37

Facultative

5

Specialty Lines

Comments

Premium growth driven by attractive rate

increases with terms and conditions

stable or improving

Marine Liability rates, terms and

conditions continuing to improve after five

years of tightening

Rate increases of approximately 26%

due partially to hurricanes and cost of

reinsurance

Offshore Energy - Physical Damage

component - is showing the highest level

of increase

Gulf of Mexico exposures may experience

capacity shortages in 2Q renewal season

Specialty Reinsurance experiencing

favorable conditions driven by supply /

demand imbalances

* Includes 3 points from hurricane and windstorm related losses

** Includes 12 points from hurricane and windstorm related losses

*

**

10

GWP Breakdown – 2005

Marine/Specialty Liability

33 %

Marine and Energy Property

30

Aviation

14

Specialty Reinsurance

23

Property & Casualty Insurance

Comments

New competitors entering the UK Liability

and Property market have put downward

pressure on pricing

Reduced top line to ensure sufficient rate

adequacy in UK business

UK liability GWP down 40% from

peak 3 years ago

Offered modest reductions of 10% for

continuing customers in UK Property

US Surplus lines rate levels continue to

be acceptable despite signs of modest

competition

Rebalancing US business by

geographically diversifying risk and

targeting non-coastal exposures

* Includes 5 points from hurricane and windstorm related losses

** Includes 9 points from hurricane and windstorm related losses

*

**

11

GWP Breakdown – 2005

UK Commercial Property

16 %

US Commercial Property

17

Worldwide Property

3

UK Commercial Liability

45

US Commercial Liability

19

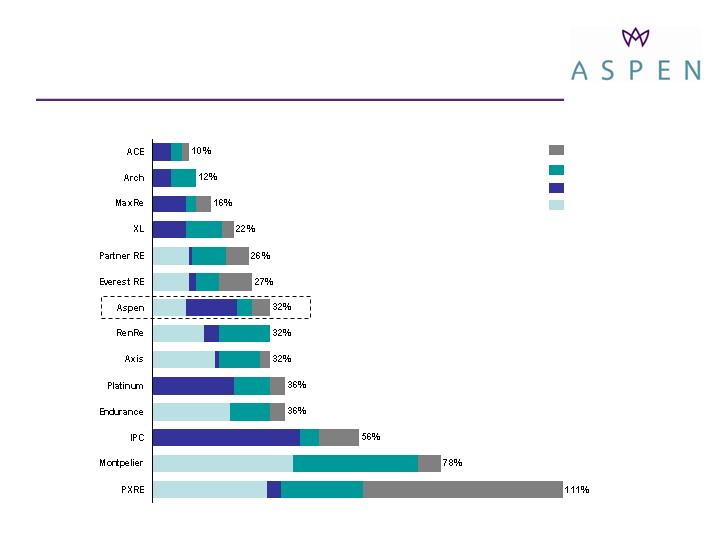

Hurricane Losses in Context

29 March 2006

24th Nov 2005

10th Oct 2005

14th Sep 2005

2005 Hurricane Losses, % of Jun-05 Equity

Source: Financial reports, press releases and Aspen analysis

12

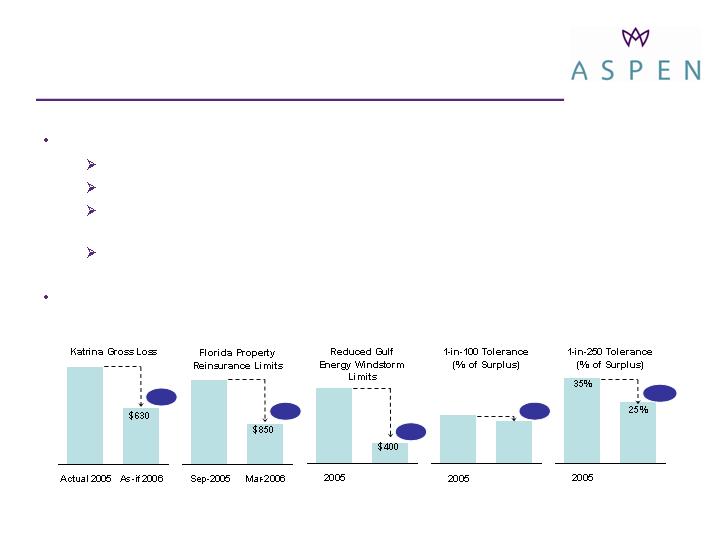

Risk Profile Reduction

Reduction in our risk tolerance overall

Modelling refinements

Reduced proportion of business exposed to risks from peak zones

Reduced business exposed to accumulating high severity catastrophe contracts

where there are too many “unknowns”

Re-underwriting: re-pricing, accumulation management and sub-limits in energy

business

Continued focus on developing non-correlated risks via our diversified underwriting

platform

($ in millions)

$1,100

-43%

-51%

$1,726

$1,400

-71%

-1000bp

20.0%

17.5%

Projected

2006

Projected

2006

Projected

2006

-250bp

13

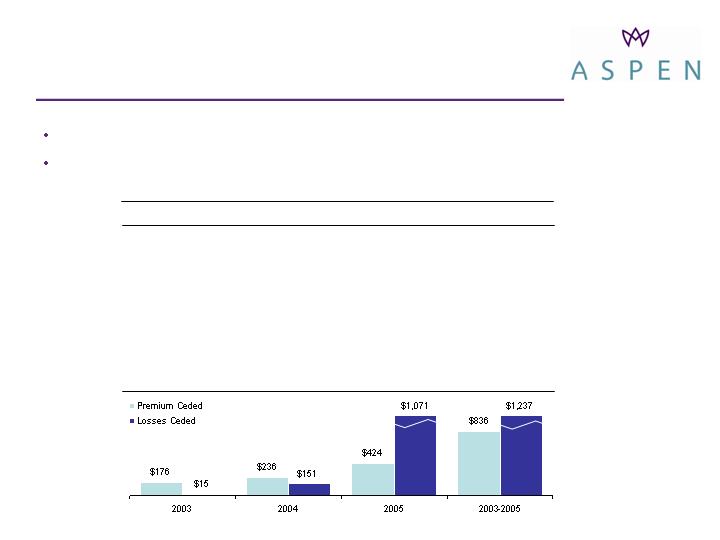

Historical Experience

Outwards Reinsurance

Mostly renewed in January

Limited exposure to further rate hardening in the retro market in 2006

($ in millions)

Review of Reinsurance Coverage

* Includes recovery under cat swap which applies only to Californian earthquake and windstorms causing damage in Florida

14

2005

2006

Property / Casualty / Marine

US Earthquake Cover

$788*

$655*

US Wind Cover

763*

573*

Retention

90

149

Property Only

US Earthquake Cover

$698*

575*

US Wind Cover

673*

493*

Retention

90

139

Portfolio designed to provide limited

book value volatility in a rising rate

environment

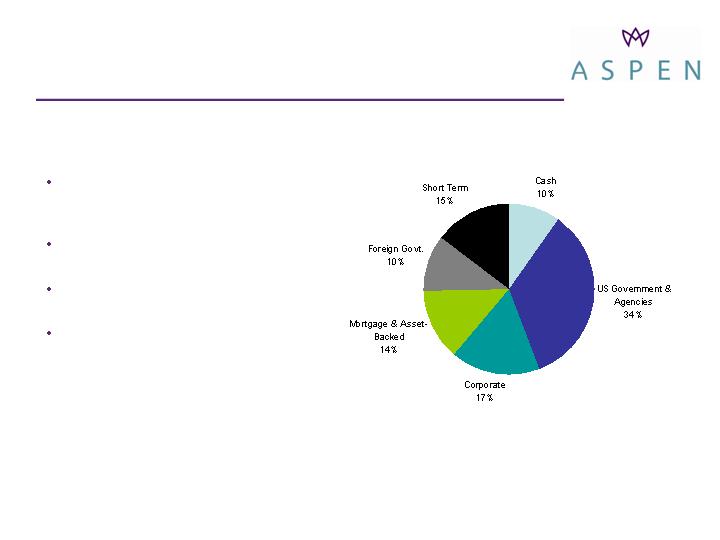

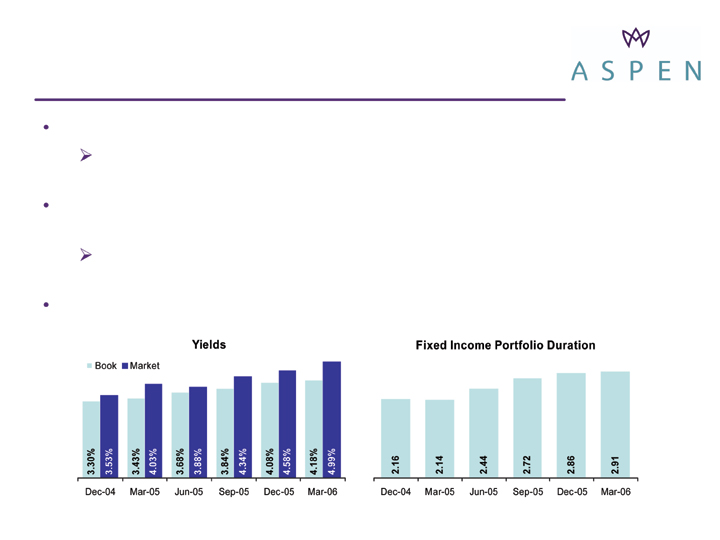

Diversified, highly-rated, liquid fixed

income portfolio. AAA rating

Strict guidelines on overall portfolio

concentration, credit and duration

Fixed Income duration of 2.91 years

and book yield of 4.18%, at Mar-

2006 (vs. 2.16 years and 3.30% at

Dec-2004)

Investment portfolio sector

allocations as of 3/31/06

$4.5 billion

Investment Strategy:

Current

15

Continued extension of asset duration in line with growing liability duration

Fixed income portfolio duration of 1.1 years in late 2003 to 2.91 years at

Mar-2006

Two-year plan to invest up to 15% of investment portfolio in non-fixed

income securities

As of 1-Apr-2006, invested $150mm (3% of portfolio) in two low-

volatility, diversified hedge fund-of-funds

Continue to monitor credit spreads to diversify credit risk when appropriate

Investment Strategy:

Growth Opportunities

16

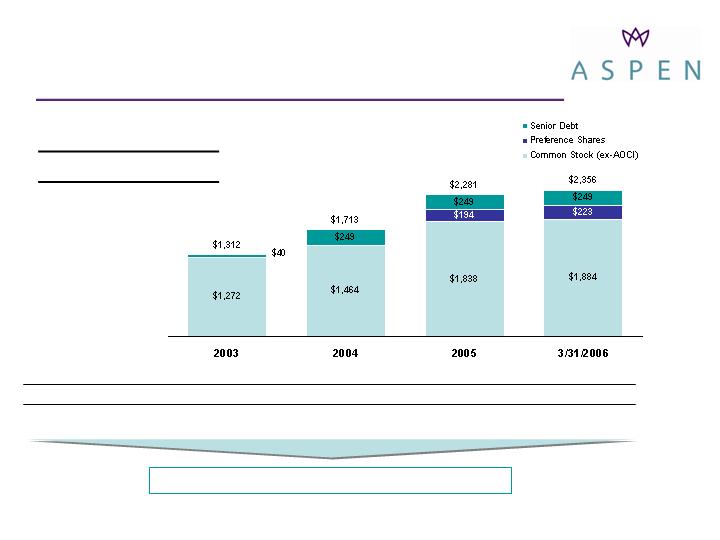

Capital Structure Overview

Ratings

* Credit ratings of Aspen Insurance UK Limited

** Common equity excludes AOCI

*** Preference shares given 50% equity credit, per Moody’s guidance; common equity excludes AOCI; end of period

($ in millions)

Opportunity for Further Financial Leverage

17

S&P

A*

BBB+

BBB-

Moody’s

A*

Baa2

BB+

Best

A2*

N/A

N/A

FSR/

Senior

Preference

Counter

Debt

Shares

Debt / Capital**

3.0

%

14.5

%

10.9

%

10.6

%

Preference Shares / Capital**

-

-

8.5

9.5

Adjusted Debt / Capital***

3.0

14.5

15.2

15.3

Breakdown of ROAE*

2004

2003

* ROAE – return on average common shareholders’ equity (see slide 26)

14.6%

4.9%

(4.9)%

14.0%

(0.7)%

Under-

writing

Investment

Income

Other

Taxes

ROAE

2005

(17.2)%

8.0%

(1.2)%

(11.8)%

(1.5)%

Under-

writing

Investment

Income

Other

Taxes

ROAE

18.7%

3.1%

(5.7)%

15.9%

(0.1)%

Under-

writing

Investment

Income

Other

Taxes

ROAE

18

Implied 2006 ROAE Based on

Previous Public Guidance

Lower Upper Comments

* Assumes no adjustments to prior year reserves

Based on growth estimates

Based on 15% premium ceding

guidance

Based on 85-95% combined ratio

and assumes NWP=NEP

Midpoint of guidance ($180-200)

Based on dividends per share

from 10-K and assumes no

change in AOCI

19

Gross Written Premiums ($mm)

$2,100

$2,200

Net Written Premiums ($mm)

1,785

1,870

Underwriting Profit ($mm)

89

281

Investment Income ($mm)

190

190

Net Income* ($mm)

$200

$353

Average Common Equity ($bn)

1.9

2.0

ROAE

10

%

18

%

ROAE Components

Underwriting

5

%

14

%

Investment Income

10

10

Interest and Preferred Dividends

(2

)

(2

)

Income Before Tax

13

22

Taxes

(3

)

(4

)

Total ROAE

10

18

Appendix

First Quarter Update

Three Months

Ended March 31,

($ in millions)

21

Percent

Full Year

2006

2005

Change

2005

Gross Premiums Written

$678.7

$804.1

(15.6

)%

$2,092.5

Net Premiums Written

451.9

632.4

(28.5

)%

1,651.6

Net Premiums Earned

402.6

378.7

6.3

%

1,508.4

Loss Ratio

57.7

%

54.8

%

90.1

%

Expense Ratio

32.7

26.3

27.1

Combined Ratio

90.4

81.1

117.2

Underwriting Income

$38.7

$71.7

(46.0

)%

$(259.2

)

Investment Income

44.5

25.5

74.5

121.3

Other

(5.9

)

(7.3

)

(19.2)

(22.5

)

Income Before Tax

77.3

89.9

(14.0)

(160.4

)

After-Tax Income

to Common Shareholders

$57.9

$70.1

(17.4)

%

$(177.8)

Q1 Expense Ratio Detail

($ in millions)

22

2005

Q1-2005

Q1- 2006

Gross Premiums Earned

$1,932.6

$433.7

$493.5

Acquisition Expenses

283.2

70.2

93.3

G&A Expenses

125.9

29.4

38.2

Acquisition Expense / GPE

14.7

%

16.2

%

18.9

%

G&A Expense / GPE

6.5

6.8

7.7

Acquisition and G&A

Expenses / GPE

21.2

23.0

26.6

Income Statement

* Results from inception on June 22, 2002 through December 31, 2002

($ in millions)

23

2002*

2003

2004

2005

Gross Premiums Written

$375

$1,307

$1,586

$2,093

Net Premiums Written

313

1,093

1,358

1,652

Net Premiums Earned

120

812

1,233

1,508

Underwriting Profit

14

178

204

(259

)

Net Investment Income

9

30

68

121

Net Income

29

152

195

(178

)

GAAP Ratios:

Loss Ratio

64

%

53

%

59

%

90

%

Expense Ratio

25

25

25

27

Combined Ratio

89

%

78

%

84

%

117

%

ROAE

6%

16

%

14

%

NA

Effective Tax Rate

NA

26

%

26

%

NA

Balance Sheet

($ in millions)

* Reinsurance recoverables; excludes ceded unearned premiums

24

Cash and Investments

$932

$1,847

$3,021

$4,437

$4,475

Recoverables*

13

44

198

1,193

1,191

Total Assets

1,212

2,579

3,943

6,517

6,859

Long Term Debt

-

40

249

249

249

Preference Shares

-

-

-

194

223

Common Equity

(ex-AOCI)

878

1,272

1,464

1,838

1,884

Book Value Per

Ordinary Share

$15.44

$18.77

$21.37

$19.39

$19.49

2002

2003

2004

2005

2006 YTD

2.0%

1,931,874

Officers, Directors & Employees as a Group **

Shares Outstanding (3/31/06) = 95,250,401

64.2%

61,165,268

Public Float

35.8%

34,085,133

Total Founder/Management Ownership

0.5%

465,873

Others ***

4.0%

3,800,412

Wellington Investment Holdings (Jersey) Ltd. *

6.4%

6,074,493

Candover Investments plc

6.5%

6,149,417

Credit Suisse

16.4%

15,663,064

The Blackstone Group

% of Shares

Outstanding

Shares

Currently Held

Founder/Management Shareholders

* Wellington Underwriting plc transferred its shares and options to this affiliate in December 2005;

Does not include Wellington Underwriting plc's exercisable options to purchase 3,781,120 non-voting shares

** Includes exercisable vested options for Aspen’s Officers, Directors and Employees as a group as of February 15, 2006

*** Other includes Appleby Names Trust and Mourant & Co. Trustees Limited

Founder / Management Share

Ownership and Public Float

25

Reconciliation of Shareholders’

Equity to Average Common Equity*

*

Average equity is a “non-GAAP financial measure,” as such term is defined in Regulation G, which management believes

better explains the Company’s results in a manner that allows for a more complete understanding of the underlying trends

in the Company’s business. Average common shareholders’ equity is calculated as the arithmetic average of common

equity on a monthly basis for the stated periods.

26

2003

2004

2005

Closing Shareholders’ Equity

$1,298.7

$1,481.5

$2,039.8

Less: Preference Shares

0.0

0.0

193.8

Common Shareholders’ Equity

1,298.7

1,481.5

1,846.0

Less: Average Adjustment

343.0

87.0

338.0

Average Common

Shareholders’ Equity

$955.7

$1,394.5

$1,508.0