Aspen Insurance Holdings Limited

July 27, 2006

July 27, 2006

Safe Harbor Disclosure

This presentation is given in the context of the quarterly earnings conference call and contains non-GAAP measures.

This presentation is given in the context of the quarterly earnings conference call and contains non-GAAP measures.

Non-GAAP Financial Measures

In presenting Aspen’s results, management has included and discussed certain "non-GAAP financial measures", as such term is defined in Regulation G. Management believes that these non-GAAP measures, which may be defined differently by other companies, better explain Aspen’s results of operations in a manner that allows for a more complete understanding of the underlying trends in Aspen’s business. However, these measures should not be viewed as a substitute for those determined in accordance with GAAP. The reconciliation of such non-GAAP financial measures to their respective most directly comparable GAAP financial measures in accordance with Regulation G is included in the financial supplement, which can be obtained from the Investor Relations section of Aspen’s website at www.aspen.bm.

Application of the Safe Harbor of the Private Securities Litigation Reform Act of 1995:

This presentation contains written or oral “forward-looking statements” within the meaning of the U.S. federal securities laws. These statements are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements include all statements that do not relate solely to historical or current facts, and can be identified by the use of words such as “expect,” “intend,” “plan,” “believe,” “project,” “anticipate,” “seek,” “will,” “estimate,” “may,” “continue,” and similar expressions of a future or forward-looking nature.

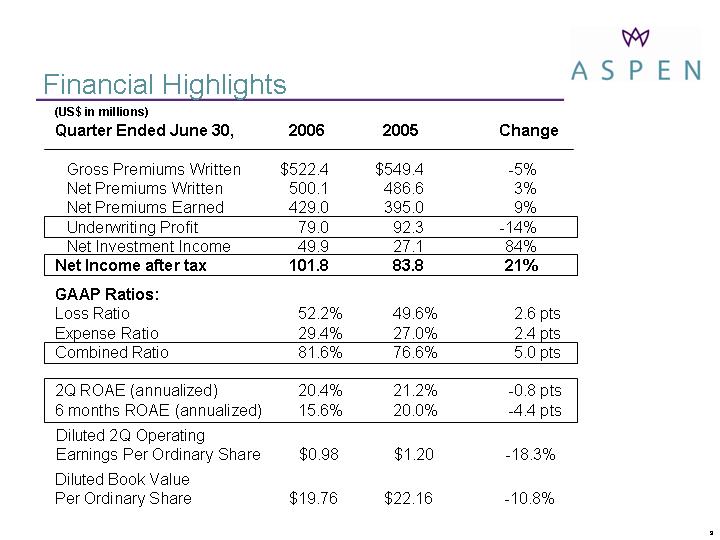

Financial Highlights

(US$ in millions)

(US$ in millions)

Gross Premiums Written $522.4 $549.4 -5%

Gross Premiums Written $522.4 $549.4 -5%

Net Premiums Written 500.1 486.6 3%

Net Premiums Earned 429.0 395.0 9%

Underwriting Profit 79.0 92.3 -14%

Net Investment Income 49.9 27.1 84%

Net Income after tax 101.8 83.8 21%

GAAP Ratios:

Loss Ratio 52.2% 49.6% 2.6 pts

Expense Ratio 29.4% 27.0% 2.4 pts

Combined Ratio 81.6% 76.6% 5.0 pts

2Q ROAE (annualized) 20.4% 21.2% -0.8 pts

Diluted Book Value

Diluted Book Value

Diluted 2Q Operating

Diluted 2Q Operating

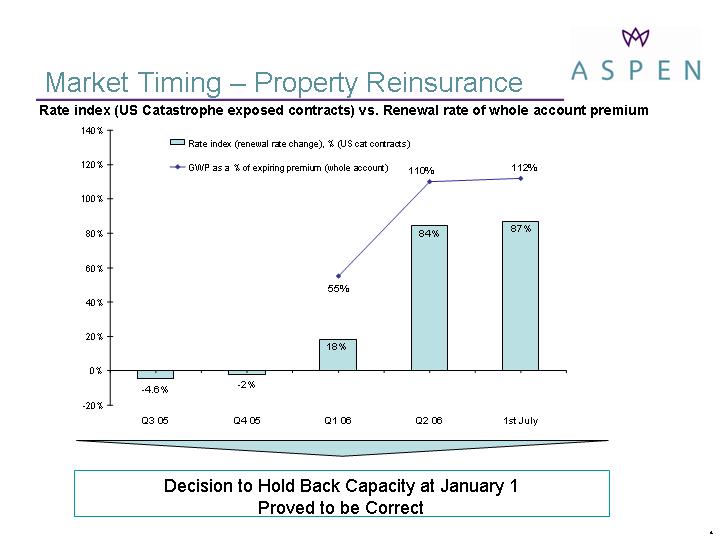

Market Timing – Property Reinsurance

Decision to Hold Back Capacity at January 1

Decision to Hold Back Capacity at January 1

Rate index (US Catastrophe exposed contracts) vs. Renewal rate of whole account premium

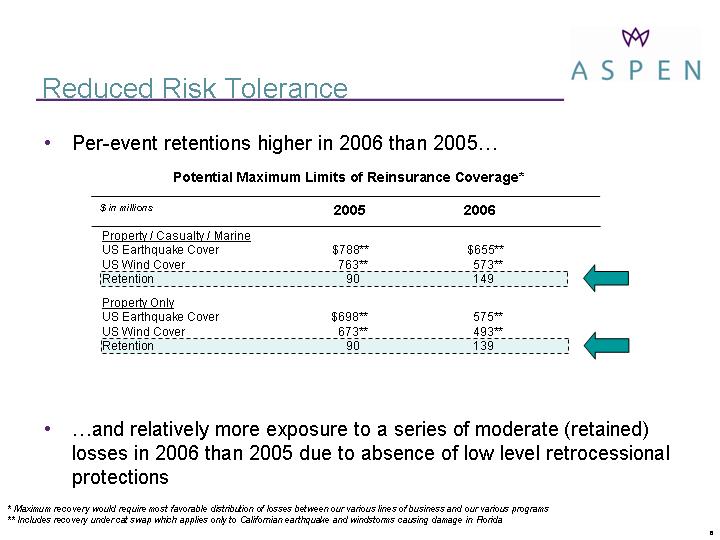

Reduced Risk Tolerance

Significant reduction in gross exposures consistent with reduced risk tolerances

$ in millions

$1,100

- -43%

- -56%

$1,726

$1,400

- -71%

Projected

Projected

* Pre-tax and reinstatement premiums

- -51%

$1,726

Property / Casualty / Marine

Property / Casualty / Marine

US Earthquake Cover $788** $655**

US Wind Cover 763** 573**

Retention 90 149

Property Only

US Earthquake Cover $698** 575**

US Wind Cover 673** 493**

Reduced Risk Tolerance

Per-event retentions higher in 2006 than 2005?

* Maximum recovery would require most favorable distribution of losses between our various lines of business and our various programs

* Maximum recovery would require most favorable distribution of losses between our various lines of business and our various programs

2005 2006

Potential Maximum Limits of Reinsurance Coverage*

$ in millions

?and relatively more exposure to a series of moderate (retained) losses in 2006 than 2005 due to absence of low level retrocessional protections

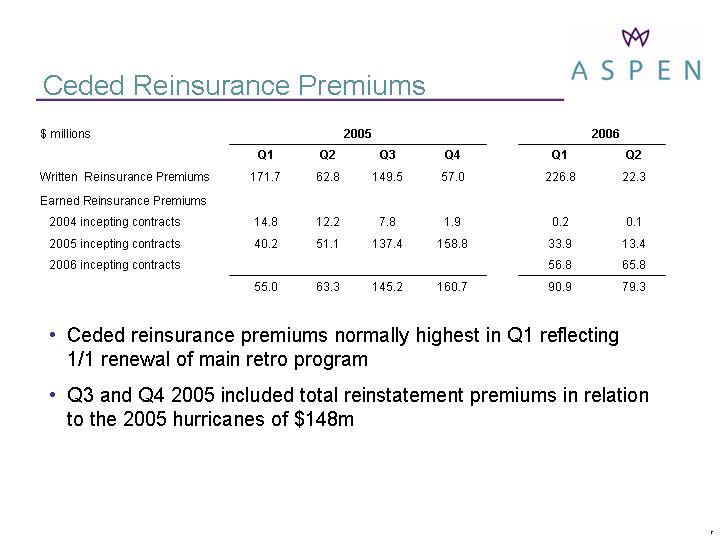

Ceded reinsurance premiums normally highest in Q1 reflecting 1/1 renewal of main retro program

Ceded reinsurance premiums normally highest in Q1 reflecting 1/1 renewal of main retro program

Ceded Reinsurance Premiums

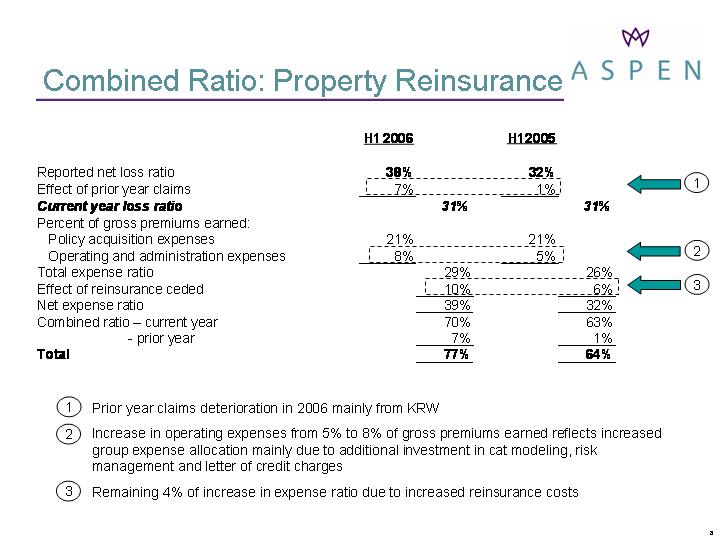

Combined Ratio: Property Reinsurance

Prior year claims deterioration in 2006 mainly from KRW

Prior year claims deterioration in 2006 mainly from KRW

Increase in operating expenses from 5% to 8% of gross premiums earned reflects increased group expense allocation mainly due to additional investment in cat modeling, risk management and letter of credit charges

1

2

3

1

2

3

H1

H1

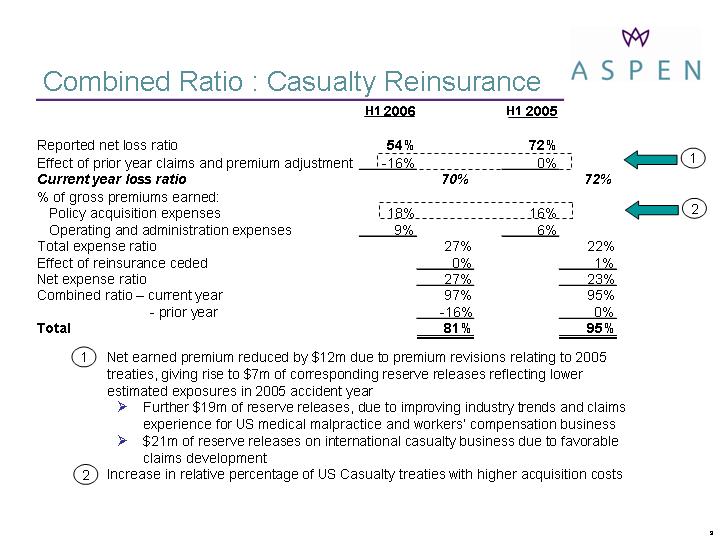

Combined Ratio : Casualty Reinsurance

Net earned premium reduced by $12m due to premium revisions relating to 2005 treaties, giving rise to $7m of corresponding reserve releases reflecting lower estimated exposures in 2005 accident year

Net earned premium reduced by $12m due to premium revisions relating to 2005 treaties, giving rise to $7m of corresponding reserve releases reflecting lower estimated exposures in 2005 accident year

Further $19m of reserve releases, due to improving industry trends and claims experience for US medical malpractice and workers’ compensation business

$21m of reserve releases on international casualty business due to favorable claims development

1

2

2

1

H1

H1

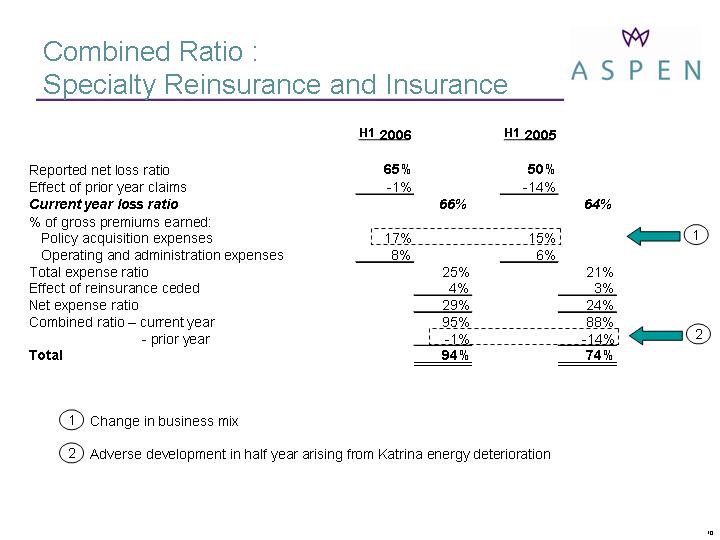

Combined Ratio : <br/>Specialty Reinsurance and Insurance

Change in business mix

Change in business mix

2

1

1

2

H1

H1

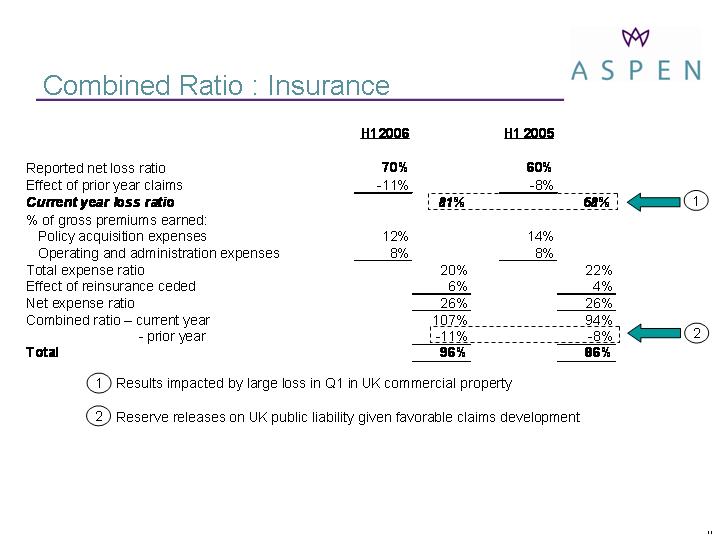

Combined Ratio : Insurance

Results impacted by large loss in Q1 in UK commercial property

Results impacted by large loss in Q1 in UK commercial property

Reserve releases on UK public liability given favorable claims development

2

1

1

2

H1

H1

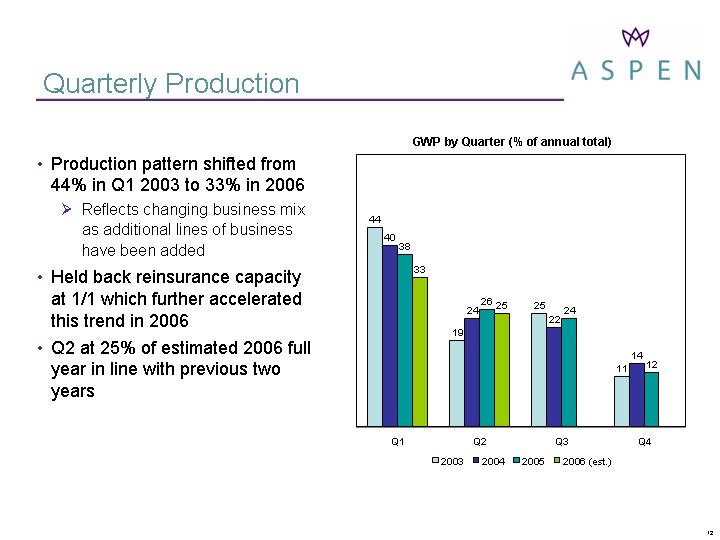

Quarterly Production

Production pattern shifted from 44% in Q1 2003 to 33% in 2006

Reflects changing business mix as additional lines of business have been added

Held back reinsurance capacity at 1/1 which further accelerated this trend in 2006

GWP by Quarter (% of annual total)