INVESTOR PRESENTATION THIRD QUARTER 2012 Aspen Insurance Holdings Limited Exhibit 99.1 |

AHL: NYSE 2 This slide presentation is for information purposes only. It should be read in conjunction with our financial supplement posted on our website on the Investor Relations page and with other documents filed or to be filed shortly by Aspen Insurance Holdings Limited (the “Company” or “Aspen”) with the US Securities and Exchange Commission. Non-GAAP Financial Measures In presenting Aspen's results, management has included and discussed certain "non-GAAP financial measures", as such term is defined in Regulation G. Management believes that these non-GAAP financial measures, which may be defined differently by other companies, better explain Aspen's results of operations in a manner that allows for a more complete understanding of the underlying trends in Aspen's business. However, these measures should not be viewed as a substitute for those determined in accordance with GAAP. The reconciliation of such non-GAAP financial measures to their respective most directly comparable GAAP financial measures in accordance with Regulation G is included herein or in the financial supplement, as applicable, which can be obtained from the Investor Relations section of Aspen's website at www.aspen.co. Application of the Safe Harbor of the Private Securities Litigation Reform Act of 1995: This presentation contains, written or oral "forward-looking statements" within the meaning of the US federal securities laws. These statements are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements include all statements that do not relate solely to historical or current facts, and can be identified by the use of words such as "expect," "intend," "plan," "believe," “do not believe,” “aim,” "project," "anticipate," "seek," "will," "estimate," "may," "continue," “guidance,” and similar expressions of a future or forward-looking nature. All forward-looking statements address matters that involve risks and uncertainties. Accordingly, there are or will be important factors that could cause actual results to differ materially from those indicated in these statements. Aspen believes these factors include, but are not limited to: the possibility of greater frequency or severity of claims and loss activity, including as a result of natural or man-made (including economic and political risks) catastrophic or material loss events, than our underwriting, reserving, reinsurance purchasing or investment practices have anticipated; the reliability of, and changes in assumptions to, natural and man-made catastrophe pricing, accumulation and estimated loss models; evolving issues with respect to interpretation of coverage after major loss events and any intervening legislative or governmental action and changing judicial interpretation and judgments on insurers’ liability to various risks; the effectiveness of our loss limitation methods; changes in the total industry losses, or our share of total industry losses, resulting from past events and,with respect to such events, our reliance on loss reports received from cedants and loss adjustors, our reliance on industry loss estimates and those generated by modeling techniques, changes in rulings on flood damage or other exclusions as a result of prevailing lawsuits and case law; the impact of acts of terrorism and acts of war and related legislation; decreased demand for our insurance or reinsurance products and cyclical changes in the insurance and reinsurance sectors; any changes in our reinsurers’ credit quality and the amount and timing of reinsurance recoverables; changes in the availability, cost or quality of reinsurance or retrocessional coverage; the continuing and uncertain impact of the current depressed economic environment in many of the countries in which we operate; the persistence of the global financial crisis and the Eurozone debt crisis; the level of inflation in repair costs due to limited availability of labor and materials after catastrophes; changes in insurance and reinsurance market conditions; increased competition on the basis of pricing, capacity, coverage terms or other factors and the related demand and supply dynamics as contracts come up for renewal; a decline in our operating subsidiaries’ ratings with Standard & Poor’s (“S&P”), A.M. Best Company, Inc. (“A.M. Best”) or Moody’s Investor Service (“Moody’s”); our ability to execute our business plan to enter new markets, introduce new products and develop new distribution channels, including their integration into our existing operations; changes in general economic conditions, including inflation, foreign currency exchange rates, interest rates and other factors that could affect our investment portfolio; the risk of a material decline in the value or liquidity of all or parts of our investment portfolio; changes in our ability to exercise capital management initiatives or to arrange banking facilities as a result of prevailing market changes or changes in our financial position; changes in government regulations or tax laws in jurisdictions where we conduct business; Aspen Holdings or Aspen Bermuda becoming subject to income taxes in the United States or the United Kingdom; loss of key personnel; and increased counter party risk due to the credit impairment of financial institutions. For a more detailed description of these uncertainties and other factors, please see the "Risk Factors" section in Aspen's Annual Report on Form 10-K as filed with the US Securities and Exchange Commission on February 28, 2012. Aspen undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the dates on which they are made. In addition, any estimates relating to loss events involve the exercise of considerable judgment and reflect a combination of ground-up evaluations, information available to date from brokers and cedants, market intelligence, initial tentative loss reports and other sources. The actuarial range of reserves and management's best estimate represents a distribution from our internal capital model for reserving risk based on our then current state of knowledge and explicit and implicit assumptions relating to the incurred pattern of claims, the expected ultimate settlement amount, inflation and dependencies between lines of business. Due to the complexity of factors contributing to the losses and the preliminary nature of the information used to prepare these estimates, there can be no assurance that Aspen’s ultimate losses will remain within the stated amounts. SAFE HARBOR DISCLOSURE |

AHL: NYSE 3 • Who We Are & What We Do • The Aspen Approach • Aspen’s Natural Catastrophe Exposures: Major Peril Zones • Delivering Strong Investment Returns • Proactive Management of Capital • Financial Highlights 3Q 2012 and YTD 2012 • Appendix • Hurricane Sandy Industry Loss Estimates • Aspen’s Market Share of Industry Insured Losses, Net • Investment Portfolio by Asset Type • European Investment Exposure • Reserve Position CONTENTS |

STRONG BALANCE SHEET MULTI-PLATFORM APPROACH WELL DIVERSIFIED PORTFOLIO • $3.6bn of shareholders’ equity as at September 30, 2012 • Ratings of A/Stable (S&P), A2/Stable (Moody’s) and A/Stable (A.M. Best) • Diluted BVPS CAGR of 10.1% over five years to September 30, 2012 • $1.3bn ordinary capital returned to shareholders 2003 – 3Q 2012 • 3 main underwriting locations: London, Bermuda and US • Branch offices: Paris, Zurich, Cologne, Singapore, Dublin and US • More than 800 employees in 30 offices across eight countries • Specialized in providing customized underwriting solutions to clients and brokers across an array of geographies, products and perils • 49% Reinsurance, 51% Insurance (3) • 55% Property, 45% Casualty (3) AHL: NYSE 4 • Bermudian domiciled Specialty Insurer and Reinsurer • Founded 2002; IPO 2003; current market capital of $2.3bn (1) • $2.2bn GWP in 2011; $2.4bn ± 5% GWP in 2012 (2) (1) As at October 31, 2012 (2) Expected full year 2012 as at October 24, 2012 (3) Last twelve months through September 30, 2012 WHO WE ARE ASPEN GROUP |

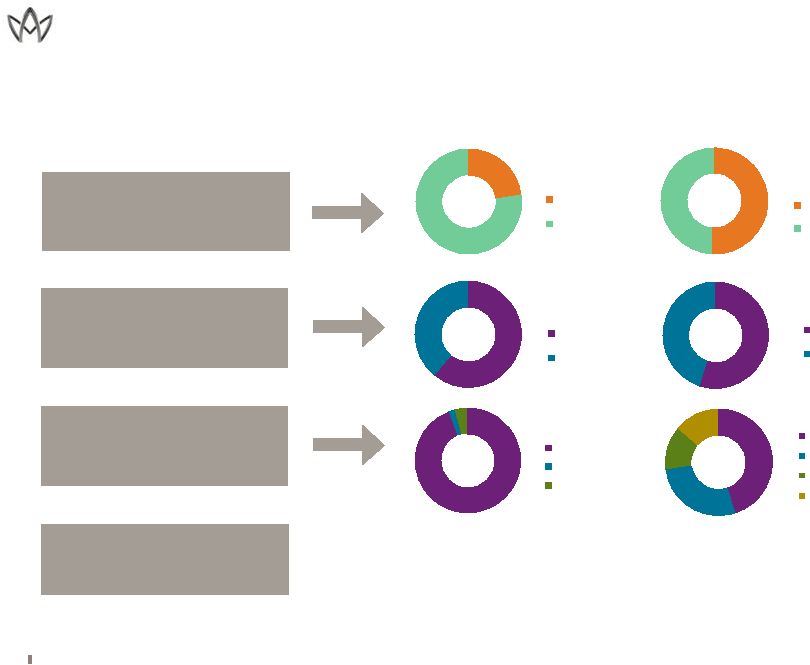

AHL: NYSE 5 INSURANCE VS. REINSURANCE (1) PROPERTY VS. CASUALTY (1) GWP BY “CORE” PLATFORM (1) GLOBAL FOOTPRINT • 176 employees • 4 offices, 3 countries • 800+ employees • 30 offices, 8 countries 2003 September 30, 2012 (1) By Gross Written Premium last twelve months through September 30, 2012 23% 77% Insurance Reinsurance 61% 39% Property Casualty 94% UK US Bermuda 51% 49% Insurance Reinsurance 55% 45% Property Casualty 45% 28% 13% 14% UK US Other Bermuda WHAT WE DO ASPEN GROUP |

ASPEN APPROACH: • Established market leader • Presence in major market hubs enables close proximity to customers • Deep expertise and understanding of client needs and risks • Focus on smaller, specialized companies and risks to maintain portfolio diversity • Focus on clients where reinsurance and reinsurance relationships are a vital part of their business needs AHL: NYSE 6 OTHER PROPERTY REINSURANCE CASUALTY REINSURANCE SPECIALTY REINSURANCE • Treaty Catastrophe • Treaty Risk Excess • Treaty Pro Rata • Global Property Facultative • US Casualty Treaty • International Casualty Treaty • Global Casualty Facultative • Credit & Surety • Agriculture • Other Specialty including Aviation, Energy and Marine ANALYSIS OF GWP BY BUSINESS LINE (1) (1) Gross Written Premium for the last twelve months through September 30, 2012 PROPERTY CATASTROPHE REINSURANCE WHAT WE DO REINSURANCE: OVERVIEW AND STRATEGY 24% 26% 27% 23% Property Catastrophe Reinsurance Other Property Reinsurance Casualty Reinsurance Specialty Reinsurance |

ASPEN APPROACH: • Innovative specialist ‘E&S’ type approach to underwriting within insurance operations • Strong emphasis on complex risks • Portfolio of highly differentiated insurance risks • Divisional focus complements in-house underwriting expertise AHL: NYSE 7 MARINE, ENERGY, AVIATION AND TRANSPORTATION FINANCIAL AND PROFESSIONAL LINES PROPERTY INSURANCE CASUALTY INSURANCE • Marine, Energy, and Construction Liability • Energy Property • Marine Hull • Specie • Aviation • US Marine • Financial Institutions • Credit, Political & Terrorism • Kidnap & Ransom • UK Professional Indemnity • UK Management Liability • Technology Liability • US Professional Liability • US Management Liability • Surety • US Property • US Programs • UK Property • UK Regional Property • Global Casualty • UK Liability • UK Regional Liability • Environmental Liability • US Primary Casualty • US Excess Casualty ANALYSIS OF GWP BY BUSINESS LINE (1) (1) Gross Written Premium for the last twelve months through September 30, 2012 40% 19% 26% 15% Marine, Energy and Transportation Financial and Professional Lines Property Insurance Casualty Insurance WHAT WE DO INSURANCE: OVERVIEW AND STRATEGY |

AHL: NYSE 8 • Continue diversification strategy by product and geography, with a focus on more pronounced growth markets • Further development of local market strategy with dedicated teams in: • Continental Europe (Zurich), Asia (Singapore), Latin America (Miami) and Middle East (London) • Implementation of cross-selling strategy to drive synergies across Property, Casualty and Specialty Lines • Improving the Market • Provide our underwriters with data and facts to support the argument for improved prices • Development of specific actions, by product and territory, to achieve more adequate rates Selective Growth in Exposures We Know and Understand, Subject to Market Conditions Business Key Elements THE ASPEN APPROACH REINSURANCE: 2012 AND BEYOND |

• Strong leadership • Established teams – Property, Professional Liability, Management Liability, Marine, Primary Casualty, Surety, Excess Casualty, Environmental Liability and Programs • Building momentum – teams executing on strategies with all licenses in place AHL: NYSE 9 • Round out ‘London Market’ portfolio • Further development of UK regional platform • Established a foothold in the Swiss insurance market • Strong demand for Marine, Energy, Political Risk and Kidnap & Ransom Selective Growth in Exposures We Know and Understand, Subject to Market Conditions Platform Key Elements THE ASPEN APPROACH INSURANCE: 2012 AND BEYOND |

AHL: NYSE 10 (1) 1 in 100 year tolerance: 17.5% of total shareholders’ equity 250 year return period as % of total Shareholders’ Equity 100 year return period as % of total Shareholders’ Equity 14.7% 8.8% 8.1% 8.1% 3.4% 1.7% 0% 5% 10% 15% 20% U.S. All Wind California EQ European Wind Japan All Perils U.S. Pacific NW EQ U.S. Eastern EQ 100 year return period as % of Total Shareholders' Equity ASPEN’S NATURAL CATASTROPHE EXPOSURES: MAJOR PERIL ZONES 1 in 250 year tolerance: 25.0% of total shareholders’ equity 20.7% 11.5% 10.7% 10.6% 6.2% 6.8% 0% 5% 10% 15% 20% 25% 250 year return period as % of Total Shareholders' Equity U.S. All Wind California EQ European Wind Japan All Perils U.S. Pacific NW EQ U.S. Eastern EQ Based on Shareholders' equity of $3,554.2 million at September 30, 2012. The estimates reflect Aspen's own view of the modelled maximum losses at the return periods shown which include input from various third party vendor models and our own proprietary adjustments to these models. Catastrophe loss experience may materially differ from the modelled PML’s due to limitations in one or more of the models or uncertainties in the application of policy terms and limits. |

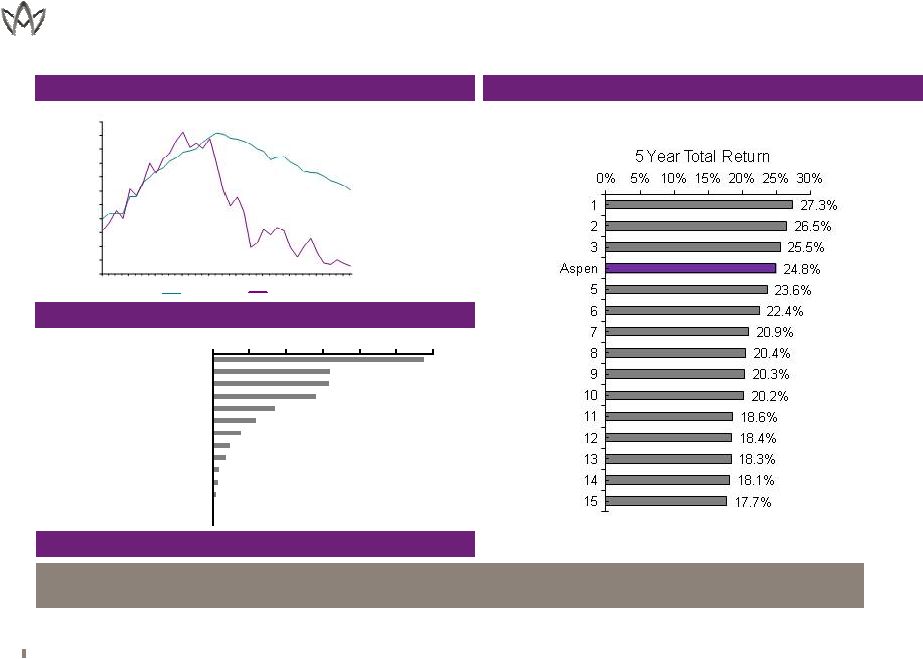

0% 5% 10% 15% 20% 25% 30% Corporate bonds Agency MBS Cash and cash equivalents US government Foreign government Short-term Agency debentures Equity Bonds backed by foreign government CMBS ABS Munis High Yield FDIC guaranteed AHL: NYSE DELIVERING STRONG INVESTMENT RETURNS 11 (1) (1) INVESTMENT PORTFOLIO ASSET CLASS AND SECTOR ALLOCATIONS $8.1 BILLION AS AT SEPTEMBER 30, 2012 Outperformance vs. Peers; Aspen Ranked #4 for 5 Year Total Return 5 YEAR TOTAL RETURN (1) VS. PEERS (2) ASPEN’S FIXED INCOME BOOK YIELD vs. 3 YR TREASURY YIELD SINCE 2003 (1) 5 year cumulative performance as at June 30, 2012 (2) Peers include ACGL, ALTE, AWH, AXS, ENH, MRH, PRE, PTP, RE, RNR, TRH, XL – VR data not available for 5 years 3.0% 0.3% 0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5% 4.0% 4.5% 5.0% 5.5% 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 Aspen FI Book Yield 3YR Treas Mkt Yield |

AHL: NYSE 12 CAPITAL MANAGEMENT STRATEGY • Maintain capital at levels that satisfy all regulatory and rating agency requirements as well as internal metrics • Optimize capital structure; conservatively leverage the balance sheet using high equity content preferred shares • Issued $160 million 7.250% Perpetual Non-Cumulative Preference Shares in April 2012 • Competitive dividend yield; quarterly dividend increased 13% in 1Q 2012 • Return capital to shareholders • Continue to monitor trading activity to repurchase shares at attractive levels • Repurchased $50 million of ordinary shares in the open market under the share repurchase program in the year to September 30, 2012 • Remaining $142 million share repurchase authorization at September 30, 2012; replaced with a new share repurchase authorization of $400 million in October 2012 September 30, 2012 Debt/total capital 12.3% Debt and preferred/total capital 24.8% (1) Capital Requirement Based On Disciplined Risk Management Approach PROACTIVE MANAGEMENT OF CAPITAL |

AHL: NYSE 13 QUARTER ENDED SEPTEMBER 30 2012 2011 CHANGE Gross written premiums 558.4 495.6 12.7% Net written premiums 507.1 462.6 9.6% Net earned premiums 516.2 486.9 6.0% Underwriting income including corporate expenses 67.4 15.3 340.5% Net investment income 48.6 57.3 (15.2%) Net income after tax 115.1 21.2 442.9% FINANCIAL RATIOS Loss ratio 49.4% 62.9% Policy acquisition expense ratio 20.0% 19.2% General, administrative and corporate expense ratio 17.6% 14.8% Combined ratio 87.0% 96.9% Annualized operating ROE (2) 13.2% 7.2% Diluted operating EPS (1) 1.34 0.68 Diluted book value per share 41.53 38.07 9.1% FINANCIAL HIGHLIGHTS: 3Q 2012 Note: See Aspen's quarterly financial supplement for a reconciliation of operating income to net income, average equity to closing shareholders’ equity, diluted book value per share to basic book value per share in the Investor Relations section of Aspen's website at www.aspen.co. NM: Not meaningful (1) ( $ millions, except per share data) |

AHL: NYSE 14 NINE MONTHS ENDED SEPTEMBER 30 2012 2011 CHANGE Gross written premiums 2,007.1 1,749.1 14.8% Net written premiums 1,722.5 1,497.9 15.0% Net earned premiums 1,525.0 1399.1 9.0% Underwriting income / (loss) including corporate expenses 163.7 (229.1) NM Net investment income 153.8 171.4 (10.3%) Net income / (loss) after tax 278.4 (122.5) NM FINANCIAL RATIOS Loss ratio 52.5% 83.0% Policy acquisition expense ratio 19.8% 18.7% General, administrative and corporate expense ratio 17.0% 14.7% Combined ratio 89.3% 116.4% Annualized operating ROE (2) 12.0% (4.4%) Diluted operating EPS (1) 3.53 (1.32) Diluted book value per share 41.53 38.07 9.1% FINANCIAL HIGHLIGHTS: YTD 2012 ( $ millions, except per share data) NM: Not meaningful (1) Note: See Aspen's quarterly financial supplement for a reconciliation of operating income to net income, average equity to closing shareholders’ equity, diluted book value per share to basic book value per share in the Investor Relations section of Aspen's website at www.aspen.co. |

APPENDIX |

AHL: NYSE 16 LOSS ESTIMATES: ECONOMIC AND INSURED • Moody’s • As of 11/1, estimated the total economic losses from Sandy at $50bn • The $50bn estimate is the sum of “Lost output” estimated at $19.9bn and “Damages” of $30bn • EQECAT • As of 11/1, estimated insured losses of $10-$20bn with total economic losses of $30 - $50bn • AIR • As of 10/30, estimated insured losses ranging from $7bn to $15bn, to include: • Insured physical damage to property both structures and contents • Additional living expenses for residential claims • For residential lines AIR believe insurers will ultimately pay 10% of modeled storm surge damage as wind losses • For commercial lines insured physical damage to structures and contents and business interruption directly caused by storm surge; assumes a 10% take-up rate for commercial flood policies; business interruption losses include direct and indirect losses for insured risks that experience physical loss • RMS • An 11/2 press release indicated it was too early to calculate reliable loss • “The event is still live and several variables are yet to play out, consequently, it remains too early to provide a reliable estimate of the total insured losses. In particular the speed of restoration of power, and pumping out of floodwaters from towns and transport systems remain major unknowns. Our experience shows that these key variables will play a significant part in the ultimate loss.” • A significant source of the damage from Sandy may arise from flood rather than wind. Thus a wind PML is not a reliable benchmark to gauge exposure. (1) It is too early for Aspen to provide a reliable estimate of losses related to Sandy HURRICANE SANDY INDUSTRY LOSS ESTIMATES |

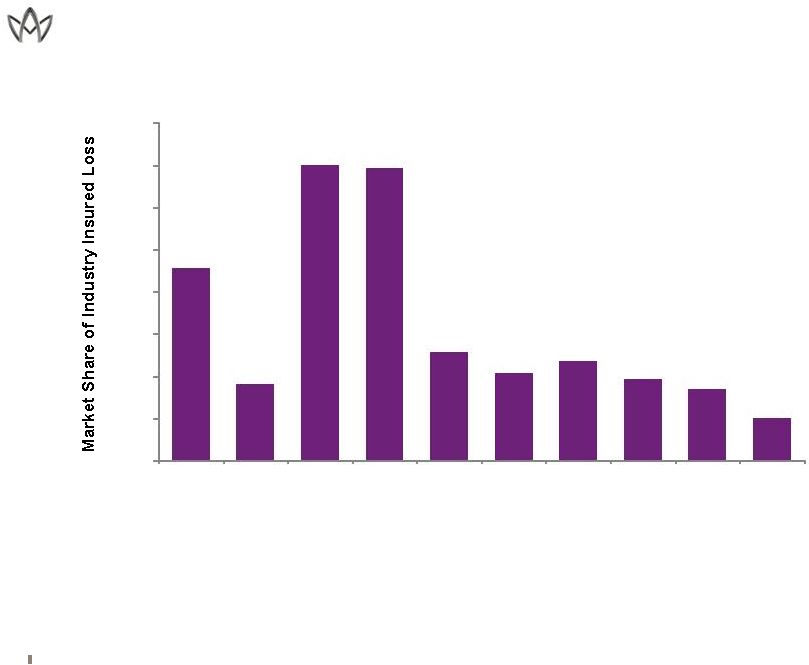

AHL: NYSE 17 (1) 0.0% 0.2% 0.4% 0.6% 0.8% 1.0% 1.2% 1.4% 1.6% Hur. Ike (2008) Hur. Gustav (2008) Chile Eq. (2010) NZ1 Darfield Eq. (2010) Tohuku (2011) US weather incl Joplin (2011) NZ2 Litteton Eq. (2011) Australian Weather (2011) Thailand Floods (2011) Hurricane Irene (2011) ASPEN’S MARKET SHARE OF INDUSTRY INSURED LOSSES, NET • Although historical loss percentages are interesting data points they are not reliable indicators for future losses • Every event is considerably different as well as the business mix of companies’ books change over time 0.9% 0.4% 1.4% 1.4% 0.5% 0.4% 0.5% 0.4% 0.3% 0.2% |

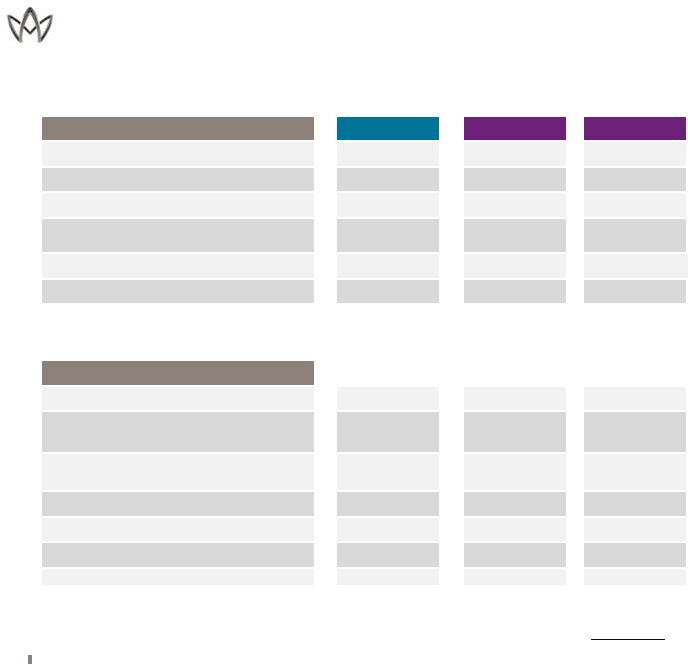

AHL: NYSE 18 CASH, SHORT-TERM SECURITIES AND EQUITY SECURITIES GOVERNMENT / AGENCY STRUCTURED SECURITIES CREDIT SECURITIES Short-term securities 505.3 US government 1,107.4 Asset-backed securities 65.1 Corporate bonds 1,842.3 Equity securities 197.1 Agency debentures 313.7 Agency rated mortgage- backed securities (GNMA, FINMA, FHLB) 1,288.2 FDIC guaranteed corporate bonds 3.0 Cash and cash equivalents 1,374.2 Foreign governments 650.3 Non-agency rated commercial mortgage- backed securities 75.6 Foreign corporates 455.6 Investment in Cartesian Iris Offshore Fund L.P. 34.8 Bonds backed by foreign government 139.1 Municipal bonds 42.8 Q3 2012 2,111.4 Q3 2012 2,071.4 Q3 2012 1,428.9 Q3 2012 2,482.8 Q2 2012 2,033.1 Q2 2012 1,943.8 Q2 2012 1,447.4 Q2 2012 2,400.0 TOTAL INVESTMENT PORTFOLIO AT MARKET VALUE ($ millions) (1) : $8,094.5 Overall Portfolio Asset Allocations Have Not Changed Significantly During 2012 (1) As at September 30, 2012, including cash and cash equivalents INVESTMENT PORTFOLIO BY ASSET TYPE |

AHL: NYSE 19 ($ in millions except for percentages) Note - Aspen takes the lower of the Moody’s and S&P ratings. • Eurozone exposures consist of sovereigns, equities, and high quality corporates with 90% having a rating of “A” or higher, with de minimis exposure to Italian and Spanish corporate bonds • Eurozone exposure is approximately 4% of Aspen’s aggregate investment portfolio • Aspen has no exposure to the sovereign debt of Greece, Ireland, Italy, Portugal or Spain COUNTRY AAA AA A BBB NR MARKET VALUE MARKET VALUE % UNREALIZED PRE-TAX Austria - 20.2 - - - 20.2 2.2% 0.1 Belgium - - 3.0 - 3.5 6.5 0.7% 1.5 Denmark 19.8 - - 0.4 - 20.2 2.2% 0.0 Finland 11.2 - - - 2.0 13.2 1.4% 0.7 France 4.5 68.8 17.7 1.6 15.5 108.1 11.7% 5.3 Germany 56.7 6.1 15.9 2.8 2.0 83.5 9.0% 4.1 Italy - - - 0.7 2.0 2.7 0.3% 0.0 Netherlands 24.4 22.5 15.6 - 4.5 67.0 7.2% 3.2 Norway 14.0 16.6 - - - 30.6 3.3% 1.8 Spain - - - 3.4 - 3.4 0.4% - Sweden - 17.8 - 1.0 8.0 26.8 2.9% 1.9 Switzerland 6.0 25.2 72.8 1.1 14.0 119.1 12.9% 10.4 United Kingdom 275.5 10.7 80.0 14.0 43.6 423.8 45.8% 22.9 European Exposures Q3 2012 412.1 187.9 205.0 25.0 95.1 925.1 100.0% 51.9 RATINGS EUROPEAN INVESTMENT EXPOSURE |

AHL: NYSE 20 AS AT SEPTEMBER 30, 2012 CASE IBNR TOTAL Reinsurance 1,371.4 1,574.7 2,946.2 Insurance 815.4 878.1 1,693.4 GROUP TOTAL 2,186.8 2,452.8 4,639.6 Note: Refer to our 2011 annual report on Form 10-K for a discussion of assumptions and uncertainties relating to the Company's reserves. Source: Aspen Company Data Incurred But Not Reported (IBNR) Represented 53% of Total Reserves at September 30, 2012 ($ in millions) RESERVE POSITION |

|