Exhibit 99.1

Aspen Insurance Holdings Limited

Chris O’Kane, Chief Executive Officer

Julian Cusack, Chief Financial Officer

February 2007

AHL: NYSE

This presentation contains non-GAAP measures and is for information purposes only. It should be read in conjunction with our financial supplement posted on our website on the Investor Relations page and with other documents filed or to be filed shortly by Aspen Insurance Holdings Limited (the “Company” or “Aspen”) with the U.S. Securities and Exchange Commission.

Non-GAAP Financial Measures

In presenting Aspen's results, management has included and discussed certain "non-GAAP financial measures", as such term is defined in Regulation G. Management believes that these non-GAAP measures, which may be defined differently by other companies, better explain Aspen's results of operations in a manner that allows for a more complete understanding of the underlying trends in Aspen's business. However, these measures should not be viewed as a substitute for those determined in accordance with GAAP. The reconciliation of such non-GAAP financial measures to their respective most directly comparable GAAP financial measures in accordance with Regulation G is included herein or in the financial supplement, as applicable, which can be obtained from the Investor Relations section of Aspen's website atwww.aspen.bm.

Application of the Safe Harbor of the Private Securities Litigation Reform Act of 1995:

This presentation contains written or oral "forward-looking statements" within the meaning of the U.S. federal securities laws. These statements are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements include all statements that do not relate solely to historical or current facts, and can be identified by the use of words such as "expect," "intend," "plan," "believe," "project," "anticipate," "seek," "will," "estimate," "may," "continue," and similar expressions of a future or forward-looking nature.

All forward-looking statements address matters that involve risks and uncertainties. Accordingly, there are or will be important factors that could cause actual results to differ materially from those indicated in these statements. Aspen believes these factors include, but are not limited to: the impact that our future operating results, capital position and rating agency and other considerations have on the execution of any capital management initiatives; the impact of any capital management activities on our financial condition; the impact of acts of terrorism and related legislation and acts of war; the possibility of greater frequency or severity of claims and loss activity, including as a result of natural or man-made catastrophic events such as Hurricanes Katrina, Rita and Wilma, than our underwriting, reserving or investment practices have anticipated; evolving interpretive issues with respect to coverage as a result of Hurricanes Katrina, Rita and Wilma; the level of inflation in repair costs due to limited availability of labor and materials after catastrophes; the effectiveness of Aspen's loss limitation methods; changes in the availability, cost or quality of reinsurance or retrocessional coverage, which may affect our decision to purchase such coverage; the reliability of, and changes in assumptions to, catastrophe pricing, accumulation and estimated loss models; loss of key personnel; a decline in our operating subsidiaries' ratings with Standard & Poor's, A.M. Best Company or Moody's Investors Service; changes in general economic conditions including inflation, foreign currency exchange rates, interest rates and other factors that could affect our investment portfolio; the number and type of insurance and reinsurance contracts that we wrote at the January 1st and other renewal periods in 2007 and the premium rates available at the time of such renewals within our targeted business lines; increased competition on the basis of pricing, capacity, coverage terms or other factors; decreased demand for Aspen’s insurance or reinsurance products and cyclical downturn of the industry; changes in governmental regulations, interpretations or tax laws in jurisdictions where Aspen conducts business; proposed and future changes to insurance laws and regulations, including with respect to U.S. state- and other government-sponsored reinsurance funds and primary insurers; Aspen or its Bermudian subsidiary becoming subject to income taxes in the United States or the United Kingdom; the effect on insurance markets, business practices and relationships of ongoing litigation, investigations and regulatory activity by the New York State Attorney General's office and other authorities concerning contingent commission arrangements with brokers and bid solicitation activities; the total industry losses resulting from Hurricanes Katrina, Rita and Wilma and the actual number of Aspen's insureds incurring losses from these storms; and with respect to Hurricanes Katrina, Rita and Wilma, Aspen’s continued reliance on loss reports received from cedants and loss adjustors, Aspen's reliance on industry loss estimates and those generated by modeling techniques, the impact of these storms on Aspen's reinsurers, any changes in Aspen's reinsurers' credit quality, the amount and timing of reinsurance recoverables and reimbursements actually received by Aspen from its reinsurers and the overall level of competition and the related demand and supply dynamics as contracts come up for renewal. For a more detailed description of these uncertainties and other factors, please see the "Risk Factors" section in Aspen's Annual Reports on Form 10-K as filed with the U.S. Securities and Exchange Commission. Aspen undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the dates on which they are made.

Safe Harbor Disclosure

2

AHL: NYSE

Key Topics

2006 Performance

Current Market Conditions, 2007 Outlook

Florida: risks and opportunities

Capital Management

2007 Guidance

3

AHL: NYSE

Performance Highlights

Diversified Operating platform delivering results

Improving Absolute Returns

2003 ROAE* 15.9% 2006 ROAE* 18.5%

Focus on Book Value growth not top line

2004 BV $19.30 2006 BV $ 22.35

Increasing contribution from Investment Income and Capital

Management

ERM core enabler reducing volatility and risk tolerance

17.5% at 1:100; 25% at 1:250

$1,663.6 m

$378.1 m

82.4%

2006

$278 m

$119.5 m

76.8%

4Q ‘06

NWP

Net Income

Combined Ratio

4

* Reconciliation of Average Equity to closing shareholders’ equity is provided in our quarterly financial supplements available in the Financial Results section of the

Investor Relations page of Aspen website at www.aspen.bm

AHL: NYSE

Strategy: Key Components

Our strategy has 4 key components

1.

‘Specialty’ insurer and reinsurer

2.

Diversified operating platform

3.

Focus on book value growth per share,not top line

4.

Enterprise Risk Management is our core strategic enabler

A Robust and Sustainable Business Model to Deliver Consistent ROE

5

AHL: NYSE

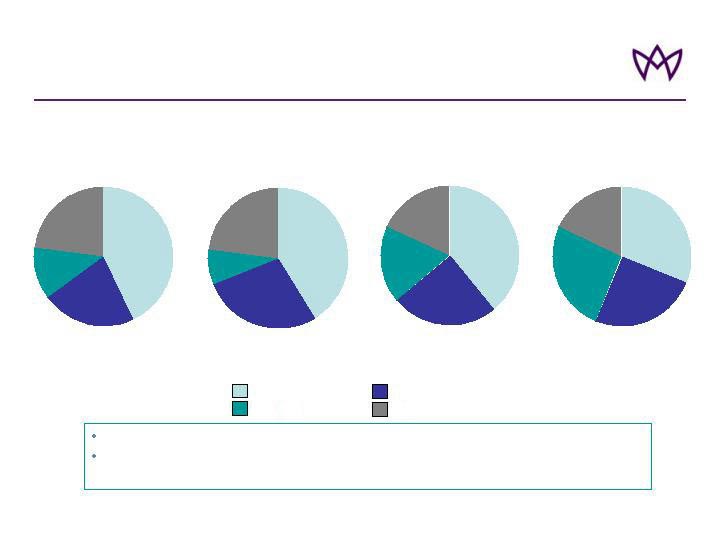

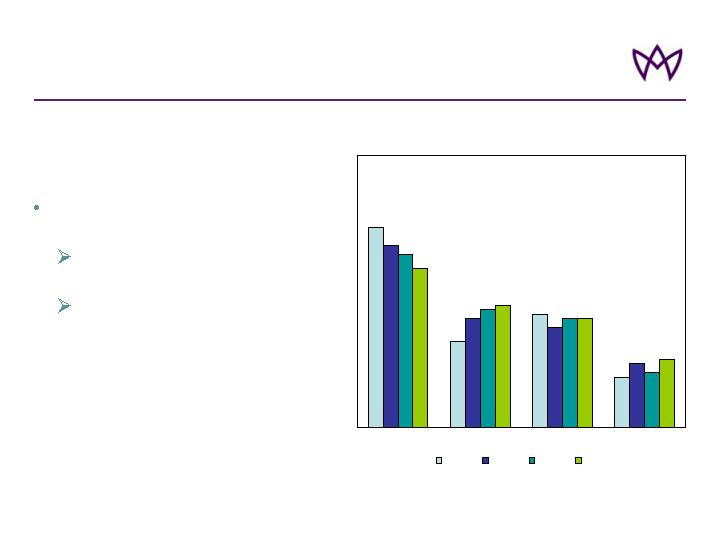

Increased Diversification

* 2003 Specialty lines excludes QQS of Wellington Syndicate 2020

Improved Spread of Risk

Specialty insurance and reinsurance has grown from 7.9% of GWP in

2004 to 26.3% in 2006

43%

12%

23%

22%

*

2005

Property Reinsurance Casualty Reinsurance

Specialty Lines Insurance

100% = $1.3bn

41%

8%

23%

28%

39%

18%

18%

25%

31%

26%

18%

25%

2004

2003

2006

100% = $1.6bn

100% = $2.1bn

100% = $1.9bn

Gross Written Premiums

6

AHL: NYSE

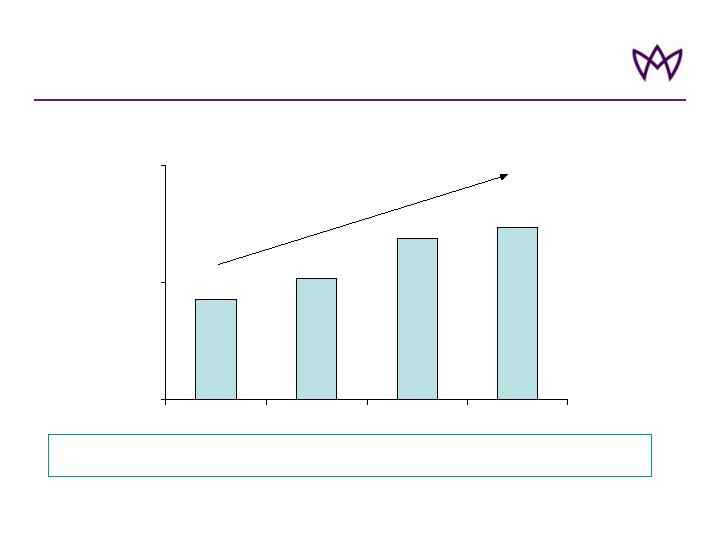

Book value per share at end of period in US$

Book Value per Share

$19.3

$20.2

$21.9

$22.4

$15

$20

$25

2005 Q4

2006 Q2

2006 Q3

2006 Q4

16%

Focus on Growing Book Value

7

AHL: NYSE

Book Value Growth Drivers

Disciplined approach to underwriting opportunities

margin stability, selective margin expansion

Capital management

Tax efficiency

ERM, no surprises

8

AHL: NYSE

Market Conditions 2007 Outlook:

Property and Specialty Lines

Risk Excess

Treaty

Pro Rata

Catastrophe

Treaty

Trend

Outlook ’07

Line

Specialty

Reinsurance

Marine & Energy

Liability

Offshore Energy

Physical Damage

Marine Hull

Aviation

Trend

Outlook ’07

Line

International

Property Fac.

E&S Property

UK Property

Trend

Outlook ’07

Line

Property Reinsurance

Specialty lines

Insurance

= Absolute rate levels attractive

= Absolute rate levels mixed

= Absolute rate levels very challenging

= 12 month rate trend positive

= 12 month rate trend neutral

= 12 month rate trend slightly downwards

= 12 month rate trend downwards

9

AHL: NYSE

Market Conditions 2007 Outlook:

Casualty Lines

Casualty

Facultative

US Casualty

International

Casualty

Trend

Outlook ’07

Line

E&S Casualty

UK Liability

Trend

Outlook ’07

Line

Casualty Reinsurance

Insurance

Pricing Under Pressure but still Adequate

= Absolute rate levels attractive

= Absolute rate levels mixed

= Absolute rate levels very challenging

= 12 month rate trend positive

= 12 month rate trend neutral

= 12 month rate trend downwards

10

AHL: NYSE

80%

Target Combined Ratios:

Across Cycles, 2007 Outlook

E2007

E2007

95%

100%

105%

90%

85%

75%

95%

100%

105%

90%

85%

80%

75%

95%

100%

105%

90%

85%

80%

75%

78%-82%

81%-

85%

Cycle

Range

83%-88%

92%-

97%

Cycle

Range

Property and

Specialty Lines

Casualty Lines

Overall

E2007

92%-97%

85%-

92%

Cycle

Range

Expected Market Conditions in 2007 Supportive of Continuing

Strong Underwriting Performance

Note: Assuming no major losses or prior year reserve movements

11

AHL: NYSE

Strengthening Risk Management:

Managing Volatility of Results

Group / regulatory / reputational

Operational

Liquidity

Minimize risk

Non – core risks

Credit

Strategic

Investment

Optimize risk- return

Core risks

Underwriting

Risk Type

Risk management policy

Risk Type

12

AHL: NYSE

Reduce Volatility, Lower Risk Tolerance

1-in-100 Tolerance

(% of Surplus)

2005

1-in-250 Tolerance

(% of Surplus)

25%

35%

2005

-1000bp

20.0%

17.5%

2007

2007

-250bp

Significant Reduction in Risk Tolerances

Single Zone Risk Tolerance Per Peril Net of Reinsurance, Post Tax

13

AHL: NYSE

Focus is on Growth in Book Value Per Share,Not Top Line

Core Beliefs about Growth

GWP and / or capital may shrink before we grow,

according to market conditions

Growth must be profitable and increase book value per

share

Growth in new lines should meet two overarching sets of

criteria

Underwriting fit

Operational fit

14

AHL: NYSE

Approach to Growth - ‘Palette’

(lines we do not currently write)

Focus on Opportunities which Offer Best Fit with Our Underwriting

and Operational Capabilities

Financial

Institutions

Personal

Accident

UK D&O

UK PI

Operational fit

Underwriting fit

Medical

Expenses

Property

fac

Bloodstock

Cargo and

Specie

Credit and

surety

Homeowners

Standard

Auto

US D&O

in US

High Net

Worths

Agriculture

Political

risk

US Airlines

Binder

Business

US

Products

Liability

War and

Terrorism

UK SMEs

Primary

Japanese

Property

HIGH

LOW

15

AHL: NYSE

2007 Impact of Florida Legislation

Aspen direct exposure

to Florida

$3 million estimated 2007 premium loss from

Florida domiciled clients (maximum)

Aspen indirect exposure

to Florida

$10 million estimated premium loss

from non-Florida domiciled business

Other indirect Impact

Estimated 2.5% reduction in worldwide property

reinsurance premium due to increased competition

16

AHL: NYSE

Financial Highlights – Full Year

Year Ended December 31

2006

2005

Change

(US$ in millions, except per share data)

(*) = Percentage ratio not meaningful comparison

17

AHL: NYSE

Gross Premiums Written

$1,945.5

$2,092.5

(7.0%)

Net Premiums Written

1,663.6

1,651.6

0.7%

Net Premiums Earned

1,676.2

1,508.4

11.1%

Underwriting Income

295.6

(259.2)

NM*

Net Investment Income

204.4

121.3

68.5%

Net Income after tax

378.1

(177.8)

NM*

GAAP Ratios:

Loss Ratio

53.1%

90.1%

(37.0%) pts

Expense Ratio

29.3%

27.1%

2.2% pts

Combined Ratio

82.4%

117.2%

(34.8%) pts

Full Year ROAE

18.5%

(11.7%)

NM*

Diluted Operating

Earnings Per Ordinary Share

$3.72

($2.11)

NM*

2006 Performance

Good performance in ongoing

business

GWP $158 million

Attritional losses from non-renewed

Risk Excess

XOL Treaty

Disappointing performance in

Bermuda book

Good performance in Japan and

Aspen Re America portfolios

GWP $119 million

Pro Rata

Strong performance

GWP $315 million

Catastrophe

Treaty

Comment

Result

Line

Good results

GWP $82 million

E&S

Casualty

Loss making in 2006

Taking steps to rectify

difficulties

GWP $72 million

E&S Property

Strong performance

GWP $125 million

UK Liability

Strong performance

GWP $51 million

UK Property

Comment

Result

Line

/

Property Reinsurance

Retro cost in '06 not necessary in '07

Property & Casualty Insurance

x

x

18

AHL: NYSE

GWP Underwriting Pattern

44

19

25

11

40

24

22

14

38

26

24

12

35

27

24

15

Q1

Q2

Q3

Q4

2003

2004

2005

2006

Production pattern shifted from

44% in Q1 2003 to 35% in 2006

Diversification strategy

results coming through

Reflects changing business

mix as additional lines of

business have been added

GWP by Quarter (% of annual total)

19

AHL: NYSE

Improving Absolute Returns

Pick-up in yield

Investment Return

$200m hybrid offering and $200m buy-back completed;

authorisation for an additional $100m share buy-back

Financial Leverage

Re-distribution of income between operating companies

will result in reduced average tax rate

Tax Rate

Increase due to growth in reserves

Investment

leverage

Market conditions expected to remain attractive in most

lines

Combined Ratio

Reduction in GWP offset by reduction in ceded premium

Operating leverage

Significant reduction in retrocession purchased; risk

tolerances unchanged

Ceded premium

Expected impact

on ROAE

Outlook 2007

Lever

Targeted Management of Underlying Levers of ROE

20

AHL: NYSE

0%

5%

10%

15%

20%

25%

30%

35%

U/W Profit

Earned RI

Costs

Invest

Income

Other inc

pref divs

Tax

Total

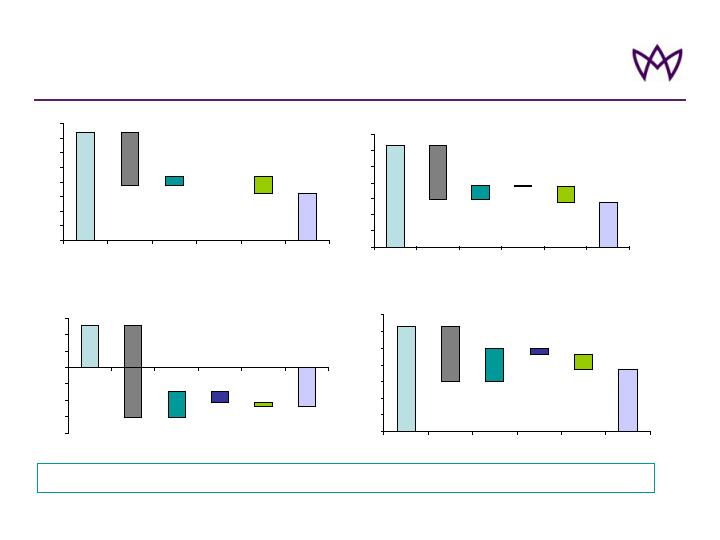

Decomposition of Historical ROAE*

Increasing Contribution from Investment Income

2004

2006

2005

0%

5%

10%

15%

20%

25%

30%

35%

U/W Profit

Earned RI

Costs

Invest

Income

Other

Tax

Total

32%

-17%

5%

-0.4%

-5%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

U/W Profit

Earned RI

Costs

Invest

Income

Other

Tax

Total

-28%

13%

8%

-1%

-11%

32%

-17%

10%

-2%

19%

2003

0%

5%

10%

15%

20%

25%

30%

35%

40%

U/W Profit

Earned RI

Costs

Invest

Income

Other

Tax

Total

37%

-18%

3%

-6%

16%

14%

-3%

-5%

21

* Reconciliation of Average Equity to closing shareholders’ equity is provided in our quarterly financial supplements available in the Financial Results section of the

Investor Relations page of Aspen website at www.aspen.bm

AHL: NYSE

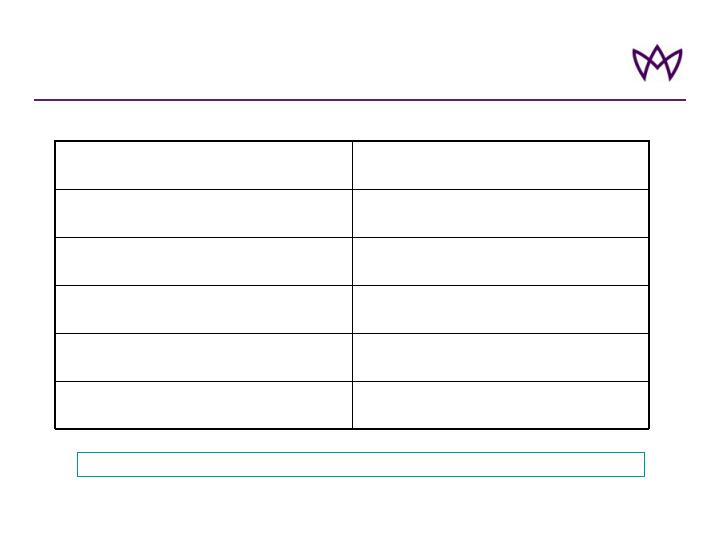

(1)

Reconciliations of Average Equity to closing shareholders’ equity and operating income to net income are provided in our 4Q06 financial supplement available on the Aspen website at www.aspen.bm

(2)

Pro forma Average Equity is reduced by $167 million from average equity assuming that our $200 million share repurchase program occurred on January 1, 2006.

(3)

Pro forma net income and operating income reduces net income and operating income by the additional preference share dividends payable assuming the $200 million share

repurchase program occurred on January 1, 2006.

Calculation of Pro Forma ROAE

AHL:NYSE

2006

FY

Average Equity reported in earnings release (1)

$1,955

Pro forma Average Equity (2)

$1,788

Net Income adjusted for preference share dividend

$363

Operating Income adjusted for preference share dividend (1)

$360

Pro forma net income adjusted for preference share dividend (3)

$351

Pro forma operating income adjusted for preference share dividend (3)

$349

ROAE: Net Income adjusted for preference share dividend

18.5%

ROAE: Operating Income adjusted for preference share dividend

18.4%

Pro forma ROAE: Net Income adjusted for preference share dividend

19.7%

Pro forma ROAE: Operating Income adjusted for preference share dividend

19.5%

AHL: NYSE

22

(US$ in millions)

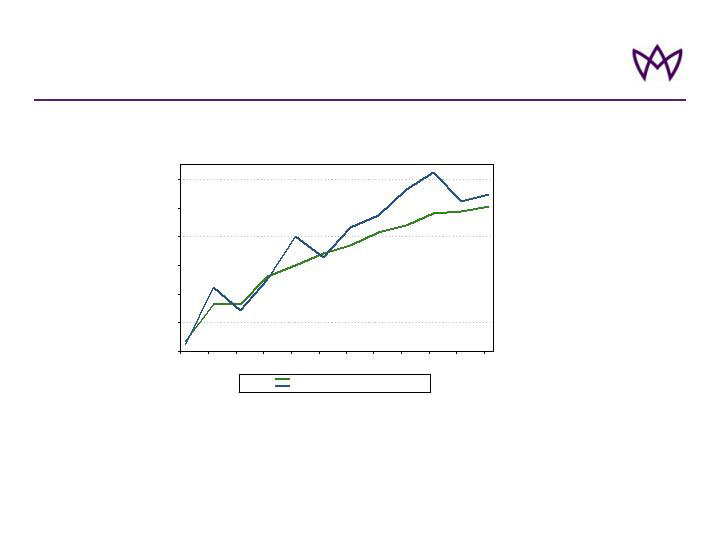

Improvement in Investment Yield

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

Mar-04

Jun-04

Sep-04

Dec-04

Mar-05

Jun-05

Sep-05

Dec-05

Mar-06

Jun-06

Sep-06

Dec-06

Aspen Book Yield

3-Year Treasury Market Yield

Fixed income management has kept the improvement in our book yield

in-line with the 3 year Treasury market yield.

In recognition that the Fed was to begin a period of increasing the Federal Funds Rate in

2004, Aspen embarked on an incremental duration extension program to capture book

yield as the Fed raised rates. Aspen also recognized the value of extending duration into

the steep yield curve during 2004. The result has been a pick up in book yield of

approximately 235 basis points.

23

AHL: NYSE

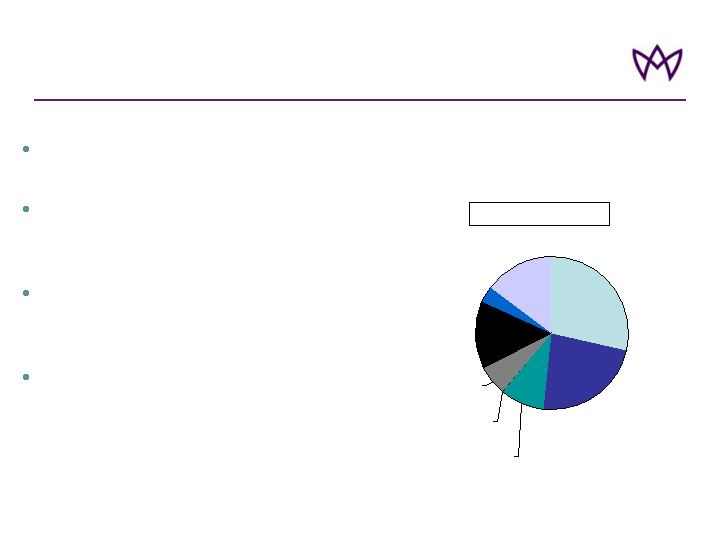

U.S. government

and agency

securities

28.7%

Corporate

securities

23.0%

Foreign

government

9.4%

Asset-backed

securities

6.2%

Mortgage-backed

securities

14.4%

Hedge funds

3.4%

Short-term

investments

14.9%

Municipals

0.03%

Portfolio investments to limit book

value volatility

Diversified, highly-rated, liquid

fixed income portfolio. AAA rating

capture yield curve opportunities

Strict guidelines on overall

portfolio concentration, credit and

duration

Fixed Income duration of 3.01

years and book yield of 4.52%, at

December 2006 (vs. 2.86 years

and 4.08% at December 2005)

Investment portfolio sector allocations

(Excluding Cash and Cash Equivalents)

As of December 31, 2006

100% = $4.7 billion

Investment Strategy

24

AHL: NYSE

Continued extension of fixed income portfolio

duration in-line with liability duration and long-term

yield curve and interest rate outlook

Fixed income portfolio duration of 1.1 years in

late 2003 to 3.00 years at December 31, 2006

Strategy of incrementally diversifying investment

portfolio away from 100% fixed income securities

April 1, 2006 invested 3% of assets in two low-

volatility, diversified hedge funds-of-funds

February 1, 2007 invested an additional 3% of

assets in low-volatility, diversified hedge funds-

of-funds

Continue to actively monitor credit spreads and

sector allocations and effect changes when

appropriate

Fixed Income Portfolio Duration

Investment Strategy: Growth Opportunities

25

Dec-

04

Mar-

05

Jun-

05

Sep-

05

Dec-

05

Mar-

06

Jun-

06

Sep-

06

Dec-

06

Dec-

04

Mar-

05

Jun-

05

Sep-

05

Dec-

05

Mar-

06

Jun-

06

Sep-

06

Dec-

06

Yield

Book

Market

AHL: NYSE

2007 Guidance

(*) Assumes no major losses or prior year reserve movements

As provided on February 9, 2007 earnings conference call

16% to 19%

Tax Rate

$135 million

Assumed Average Cat-Load

$230 – $250 million

Investment Income

83% – 88%*

Combined Ratio

6% – 8% of GWP

% Premium Ceded

$1.9 billion+ 5%

GWP

Implied ROE of 16% – 20%

26

AHL: NYSE

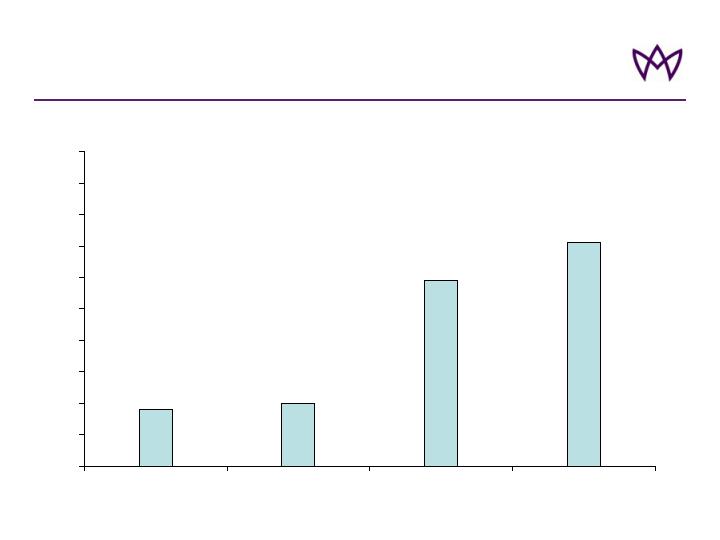

Float as a % of shares outstanding

Improved Share Trading Liquidity

18%

20%

59%

71%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

12/31/03

12/31/04

12/31/05

12/31/06

27

AHL: NYSE

Conclusions

Robust business model — enhanced returns with reduced volatility

Market conditions remain attractive in 2007

Strong risk management and ROAE

Focused management of underlying ROAE drivers to improve

returns

Selective organic growth opportunities

Enhanced Returns with Lower Volatility

28

AHL: NYSE

Standard & Poor’s on the Aspen Group

“…Aspen’s proven management team, strong ERM, strong earnings, strong competitive position, and strong capitalization… will be reflected in reduced earnings volatility prospectively.”

-- November 27, 2006

29

AHL: NYSE