Aspen Insurance Holdings Limited

May 2007

Non-Deal Roadshow

Exhibit 99.1

Safe Harbor Disclosure

This slide presentation is for information purposes only. It should be read in conjunction with our financial supplement posted on our website on the Investor Relations page and with other documents filed or to

be filed shortly by Aspen Insurance Holdings Limited (the “Company” or “Aspen”) with the U.S. Securities and Exchange Commission.

Non-GAAP Financial Measures

In presenting Aspen's results, management has included and discussed certain "non-GAAP financial measures", as such term is defined in Regulation G. Management believes that these non-GAAP measures,

which may be defined differently by other companies, better explain Aspen's results of operations in a manner that allows for a more complete understanding of the underlying trends in Aspen's business.

However, these measures should not be viewed as a substitute for those determined in accordance with GAAP. The reconciliation of such non-GAAP financial measures to their respective most directly

comparable GAAP financial measures in accordance with Regulation G is included herein or in the financial supplement, as applicable, which can be obtained from the Investor Relations section of Aspen's

website at www.aspen.bm.

Application of the Safe Harbor of the Private Securities Litigation Reform Act of 1995:

This presentation contains, and Aspen's earnings conference call may contain, written or oral "forward-looking statements" within the meaning of the U.S. federal securities laws. These statements are made

pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements include all statements that do not relate solely to historical or current facts, and can be

identified by the use of words such as "expect," "intend," "plan," "believe," "project," "anticipate," "seek," "will," "estimate," "may," "continue," and similar expressions of a future or forward-looking nature.

All forward-looking statements address matters that involve risks and uncertainties. Accordingly, there are or will be important factors that could cause actual results to differ materially from those indicated in

these statements. Aspen believes these factors include, but are not limited to: the impact that our future operating results, capital position and rating agency and other considerations have on the execution of

any capital management initiatives; the impact of any capital management activities on our financial condition; the impact of acts of terrorism and related legislation and acts of war; the possibility of greater

frequency or severity of claims and loss activity, including as a result of natural or man-made catastrophic events such as Hurricanes Katrina, Rita and Wilma, than our underwriting, reserving or investment

practices have anticipated; evolving interpretive issues with respect to coverage as a result of Hurricanes Katrina, Rita and Wilma; the level of inflation in repair costs due to limited availability of labor and

materials after catastrophes; the effectiveness of Aspen's loss limitation methods; changes in the availability, cost or quality of reinsurance or retrocessional coverage, which may affect our decision to purchase

such coverage; the reliability of, and changes in assumptions to, catastrophe pricing, accumulation and estimated loss models; loss of key personnel; a decline in our operating subsidiaries' ratings with

Standard & Poor's, A.M. Best Company or Moody's Investors Service; changes in general economic conditions including inflation, foreign currency exchange rates, interest rates and other factors that could

affect our investment portfolio; the number and type of insurance and reinsurance contracts that we wrote at the January 1st and other renewal periods in 2007 and the premium rates available at the time of

such renewals within our targeted business lines; increased competition on the basis of pricing, capacity, coverage terms or other factors; decreased demand for Aspen’s insurance or reinsurance products and

cyclical downturn of the industry; changes in governmental regulations, interpretations or tax laws in jurisdictions where Aspen conducts business; proposed and future changes to insurance laws and

regulations, including with respect to U.S. state- and other government-sponsored reinsurance funds and primary insurers; Aspen or its Bermudian subsidiary becoming subject to income taxes in the United

States or the United Kingdom; the effect on insurance markets, business practices and relationships of ongoing litigation, investigations and regulatory activity by the New York State Attorney General's office

and other authorities concerning contingent commission arrangements with brokers and bid solicitation activities; the total industry losses resulting from Hurricanes Katrina, Rita and Wilma and the actual

number of Aspen's insureds incurring losses from these storms; and with respect to Hurricanes Katrina, Rita and Wilma, Aspen’s continued reliance on loss reports received from cedants and loss adjustors,

Aspen's reliance on industry loss estimates and those generated by modeling techniques, the impact of these storms on Aspen's reinsurers, any changes in Aspen's reinsurers' credit quality, the amount and

timing of reinsurance recoverables and reimbursements actually received by Aspen from its reinsurers and the overall level of competition and the related demand and supply dynamics as contracts come up for

renewal. For a more detailed description of these uncertainties and other factors, please see the "Risk Factors" section in Aspen's Annual Report on Form 10-K for the fiscal year ended December 31, 2006 as

filed with the U.S. Securities and Exchange Commission on February 22, 2007. Aspen undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new

information, future events or otherwise. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the dates on which they are made.

2

Contents

Strategy and Approach

2007 Q1 Financial Performance

Key Themes

Market Conditions

Florida Legislative Changes

2007 Outlook

3

Strategy: Key Components

Our strategy has 3 key components

1.

‘Specialty’ insurer and reinsurer

2.

Diversified operating platform

3.

Focus on book value growth per share, not top line

Robust and Sustainable Business Model to Deliver Consistent ROEs

4

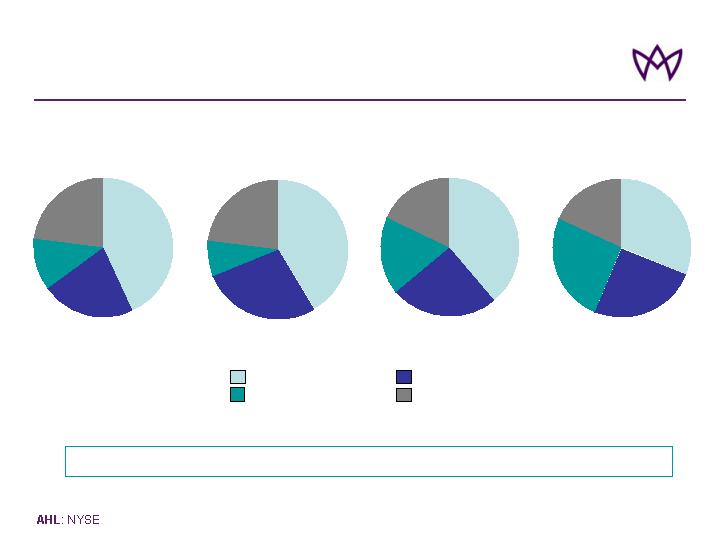

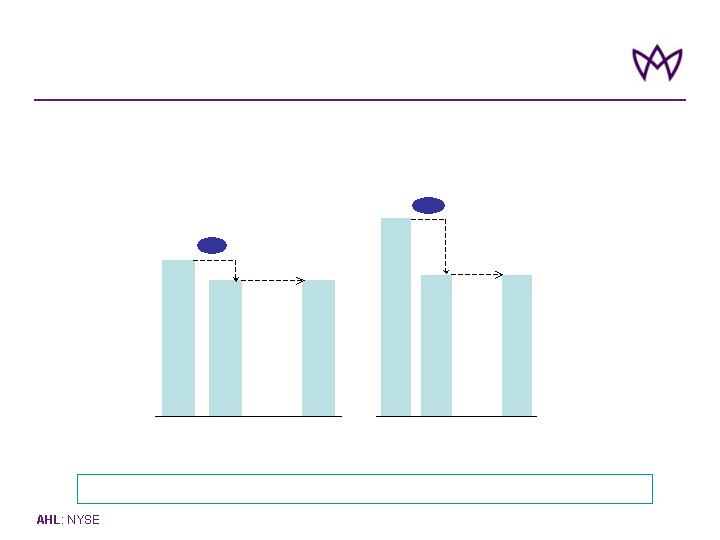

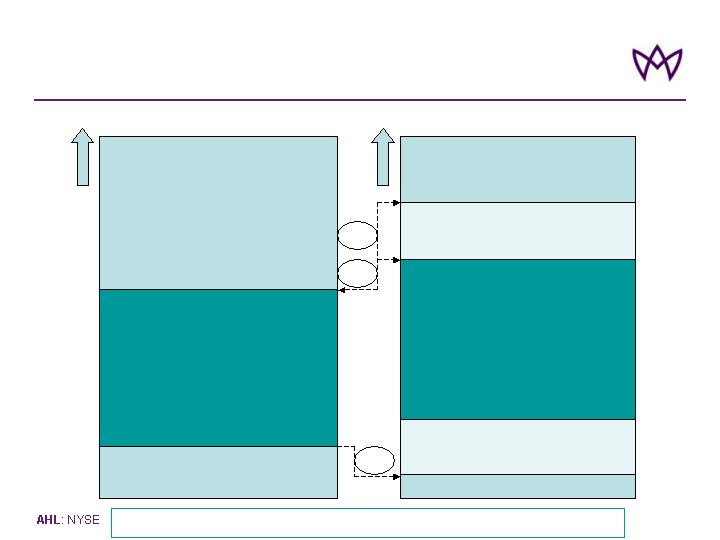

Increased Diversification

* 2003 Specialty lines includes QQS of Wellington Syndicate 2020

Significant Growth in Specialty Lines And Improved Spread of Risk

*

2005

Property Reinsurance Casualty Reinsurance

Specialty Lines Insurance

100% = $1.3bn

2004

2003

2006

100% = $1.6bn

100% = $2.1bn

100% = $1.9bn

Gross Written Premiums

5

31%

26%

18%

25%

39%

18%

18%

25%

41%

8%

23%

28%

43%

12%

23%

22%

Focus is on Growth in Book Value Per Share, Not Top Line

Core Beliefs about Growth

GWP and / or capital may shrink before we grow, according to market

conditions

Growth must be profitable and increase book value per share

Growth in new lines should meet two overarching sets of criteria

Underwriting fit

Operational fit

6

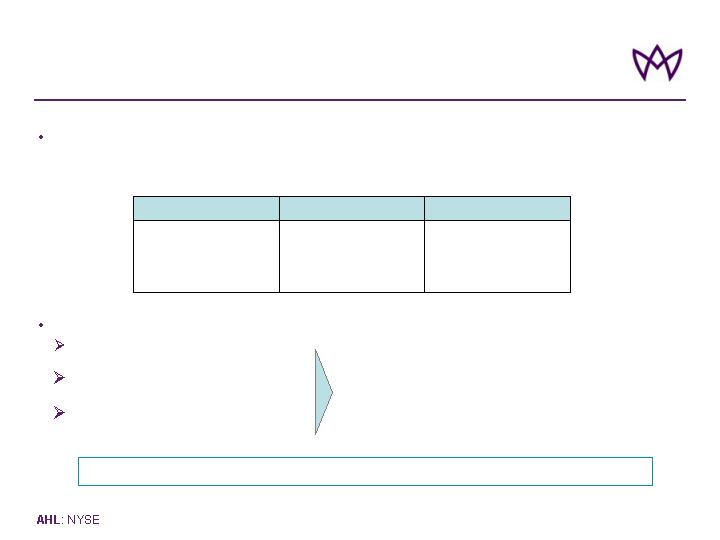

Approach to Growth - ‘Palette’

(lines we do not currently write)

Focus on Opportunities which Offer Best Fit with Our Underwriting and Operational

Capabilities

Financial

Institutions

Personal

Accident

UK D&O

UK PI

Operational fit

Underwriting fit

Medical

Expenses

Excess

Casualty

Bloodstock

Cargo and

Specie

Credit and

surety

Homeowners

Standard

Auto

US D&O

in US

High Net

Worths

Agriculture

Political

risk

US Airlines

Binder

Business

US

Products

Liability

War and

Terrorism

UK SMEs

Primary

Japanese

Property

HIGH

LOW

7

ILLUSTRATIVE

Construction

Liability

General

Liability

Contents

Strategy and Approach

2007 Q1 Financial Performance

Key Themes

Market Conditions

Florida Legislative Changes

2007 Outlook

8

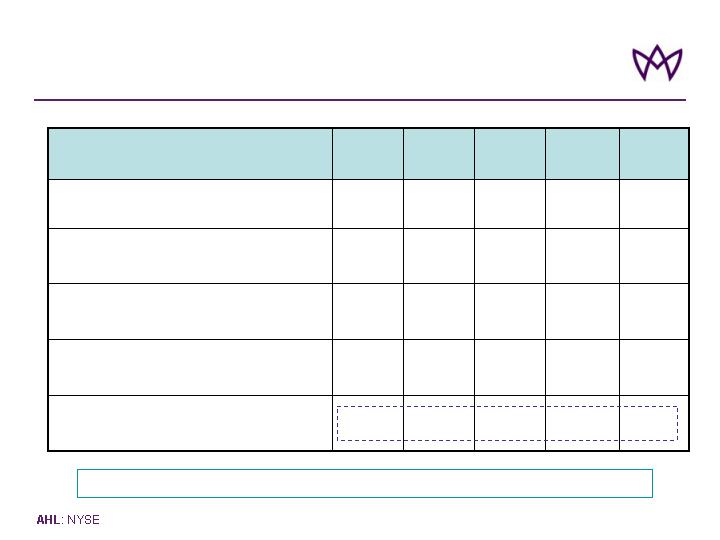

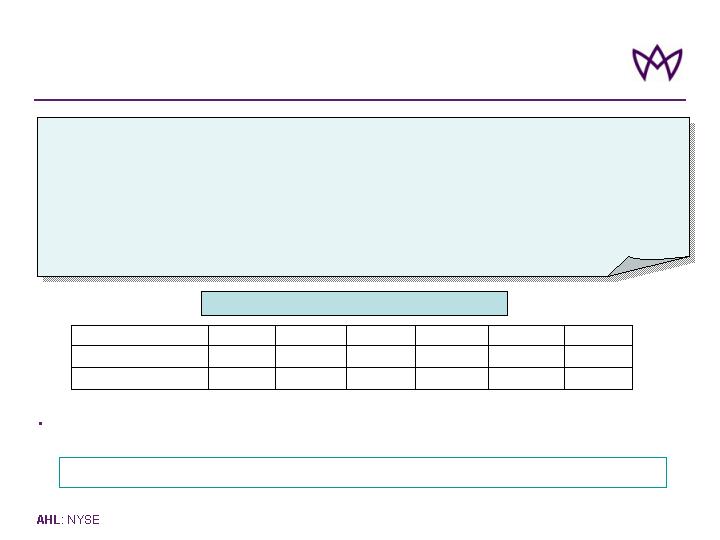

Financial Highlights - Q1 2007

(US$ in millions, except per share data)

Period Ended March 31

2007

2006

o Gross Written Premiums

$636.5

$678.7

o Net Written Premiums

555.1

451.9

o Net Earned Premiums

439.0

402.6

o Underwriting Income

90.5

38.7

o Net Investment Income

67.5

44.5

Net Income after tax

121.9

61.8

GAAP Ratios:

Loss Ratio

51.4%

57.7%

Expense Ratio

28.0%

32.7%

Combined Ratio

79.4%

90.4%

Full Year ROAE ¹

22.9%*

12.5%*

Diluted Operating

Earnings Per Ordinary Share

$1.26

$0.59

97% Increase in NI and Annualised ROAE of 22.9%

•Annualised

¹ Reconciliation of Average Equity to closing shareholders’ equity is provided in our quarterly financial supplements available in the Financial Results section

of the Investor Relations page of Aspen’s website at www.aspen.bm

9

Results by Business Line – Q1 2007

Strong Performance From Each Product Segment and Significant

Contribution from Investments

10

Income Contribution

68

90

0

40

80

Net Investment Income

Underwriting Profit

Underwriting Profit

44

16

20

10

0

20

40

Property Re

Casualty Re

Specialty

Lines

Insurance

NWP

176

217

127

35

0

40

80

120

160

200

240

Property Re

Casualty Re

Specialty

Lines

Insurance

GWP

187

223

156

70

0

40

80

120

160

200

240

$ms

$ms

$ms

$ms

Property Re

Casualty Re

Specialty

Lines

Insurance

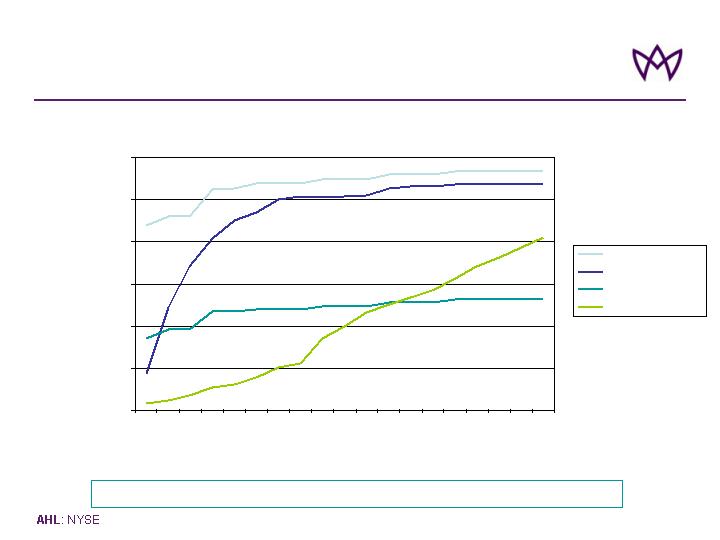

Katrina Loss Development

(in $ millions)

Gross Incurred Claims Stabilized

11

0

200

400

600

800

1,000

1,200

Gross Ultimate

Gross Incurred

Net Ultimate

Gross Paid

Sep-05

Oct-05

Nov-05

Dec-05

Feb-06

Jan-06

Mar-06

Apr-06

May-06

Jun-06

Aug-06

Sep-06

Oct-06

Jul-06

Dec-06

Jan-07

Nov-06

Feb-07

Mar-07

Improvement in Expense Ratio

28.0%

2.0%

26.0%

9.6%

16.4%

Q1 2007

28.2%

4.0%

24.2%

10.3%

13.9%

Q4 2006

29.4%

4.5%

24.9%

8.5%

16.4%

Q2 2006

27.0%

4.4%

22.6%

7.2%

15.4%

Q3 2006

32.7%

Net expense ratio

6.1%

Effect of reinsurance

26.6%

Total gross expense ratio

7.7%

General and administrative expenses

18.9%

Acquisition expenses

Q1 2006

% of Gross Earned Premium

470 bps Improvement in Net Expense Ratio Q107 vs. Q106

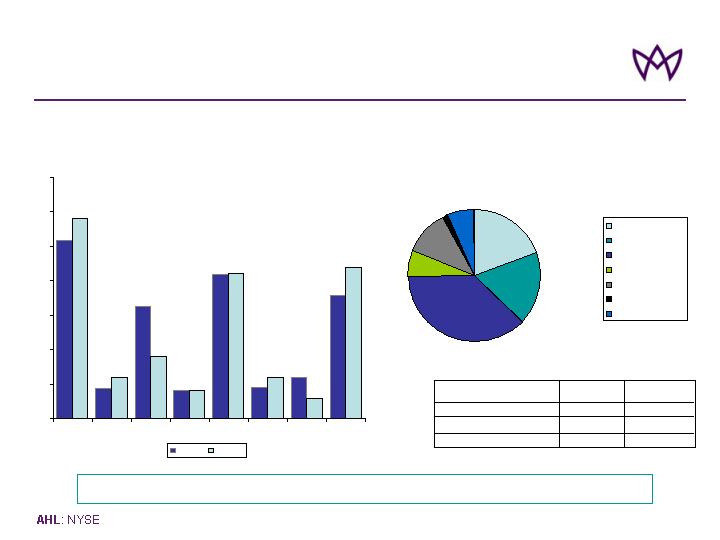

12

19%

18%

37%

7%

11%

2%

6%

Govt

Agency

AAA

AA+/AA/AA-

A+/A/A-

BBB+/BBB/BBB-

NR

Investment Portfolio

Asset Class Allocation

Portfolio Credit Ratings

(as at March 31, 2007)

AAA

AA+

Overall Fixed Income Rating

AAA

3%

Actual as at

December 31, 2006

AAA

Overall Portfolio Rating

6%

Fund of Hedge Funds

Actual as at

March 31, 2007

Indicator (S&P Ratings)

91% of Portfolio ‘A’ or Better

13

26%

4%

16%

5%

6%

18%

6%

9%

4%

21%

6%

3%

21%

4%

23%

28%

0%

5%

10%

15%

20%

25%

30%

35%

Govt

Agency

MBS

CMBS

Corp

ABS

FOHF

Cash/ST

Mar 07

Dec 06

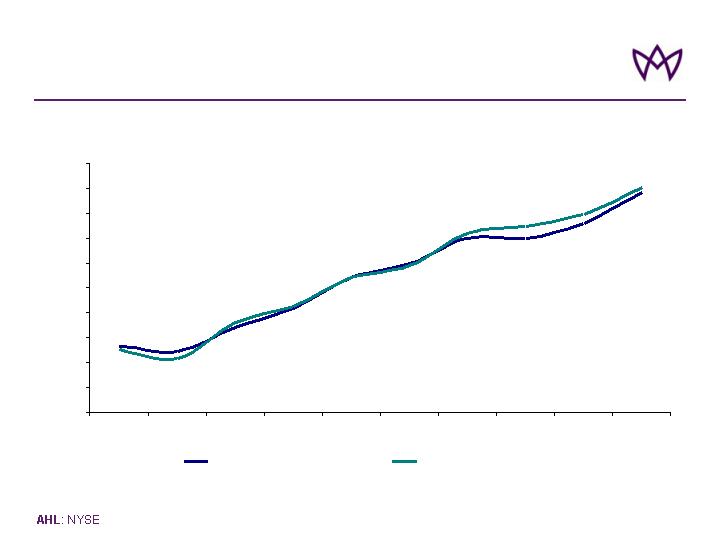

Improvement in Investment Yield

(*) including cash and cash equivalents but excluding FoHF - Initial investments in Fund of Hedge Funds were made on April 1, 2006 with

subsequent investment on February 1, 2007.

*

14

3.0%

3.2%

3.4%

3.6%

3.8%

4.0%

4.2%

4.4%

4.6%

4.8%

5.0%

Q404

Q105

Q205

Q305

Q405

Q106

Q206

Q306

Q406

Q107

Fixed Income portfolio book yield

Aggregate portfolio book yield

Contents

15

Strategy and Approach

2007 Q1 Financial Performance

Key Themes

Market Conditions

Florida Legislative Changes

2007 Outlook

Key Themes: 2006/2007

4 Key Themes in 2006 / 2007

1.

Reducing volatility

2.

Strengthening risk management

3.

Build-out of management team

4.

Improving absolute returns

16

Ongoing

2005

2006

2007

2005

2006

2007

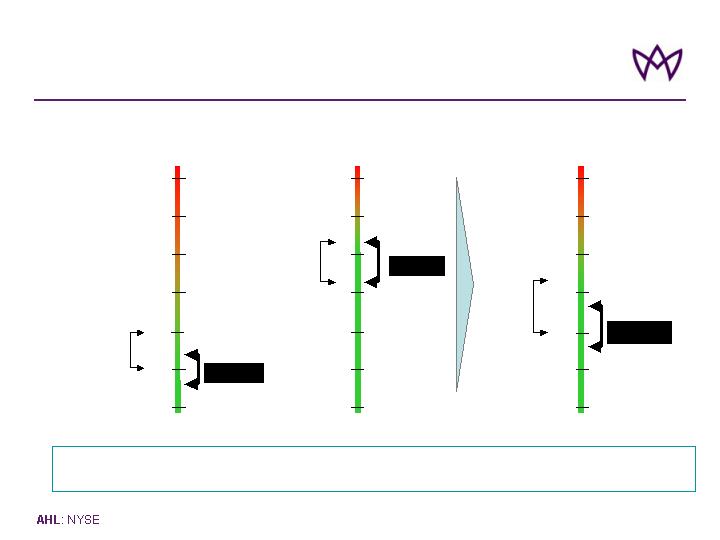

Reducing Volatility – Reduced Risk Tolerance

Significant Reduction in Risk Tolerances…

Single Zone Risk Tolerance Per Peril Net of Reinsurance, Post Tax

-1000bp

20.0%

17.5%

-250bp

17

17.5%

1-in-250 Tolerance

(% of Surplus)

1-in-100 Tolerance

(% of Surplus)

35%

25%

25%

Reducing Volatility – Improved Risk Profile

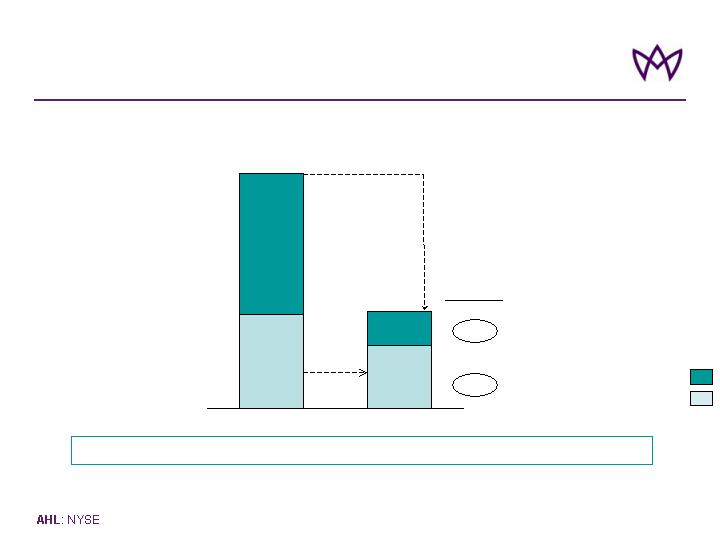

Recoveries

2005 Hurricanes*: Actual Losses vs. As if @ May’07 - Gross Loss and Net of Recoveries**

$ millions and % change

Net loss***

Notes:

(*) Katrina, Rita, Wilma

(**) Losses and recoveries: after inwards and outwards reinstatement premium, additional premium (AP) and tax

(***) Hurricane Katrina: Actual recoveries include $21m recoveries from the Cat Swap. As-if recoveries include no recoveries from the Cat Swap, but if Katrina

happened prior to August 18 , there will be an additional $9m of recoveries

$1,573m

$647m

-58%

-33%

% change

Gross

Net

…Resulting in Significant Reduction in Gross and Net Exposure

th

18

628

418

945

229

Actual

As-if@May 07

Strengthening Risk Management

Group / regulatory / reputational

Operational

Liquidity

Minimize risk

Non – core risks

Credit

Strategic

Investment

Optimize risk- return

Core risks

Underwriting

Risk Type

Risk management policy

Risk Type

Managing Volatility of Results

19

Build-out of Management Team

Announced 4 new significant appointments YTD 2007

Glyn Jones

Chairman

Nathan Warde

President of US Insurance

Matt Yeldham*

Head of International Insurance

Richard Houghton

CFO

Focus on re-positioning US E&S operation

Focus on Non-US Insurance and Specialty Lines businesses

Continued focus on strengthening / streamlining operational

infrastructure and capabilities

Management Team Build-out Completed

* Joins October 2007

Strategic evolution and enhanced performance

20

Improving Absolute Returns

* Reconciliation of Average Equity to closing shareholders’ equity is provided in our quarterly financial supplements available in the Financial Results section of the

Investor Relations page of Aspen’s website at www.aspen.bm

Annualized ROAE* of 22.9% in 1Q07

$200m share-buy back program

completed Q4 2006; authorisation for a

further $100m

Capital Management

35.0% of net income (2004) 55.4% of

net income (1Q07)

Increasing Contribution from

Investment Income

BVPS $19.30 (2005) $23.62 (1Q07)

Book Value Growth

Financial leverage ratio increased from

14.4% (2004) to 24.2% (1Q07)

Improved Balance Sheet

Efficiency

21

Strategy and Approach

2007 Q1 Financial Performance

Key Themes

Market Conditions

Florida Legislative Changes

2007 Outlook

Contents

22

Market Conditions

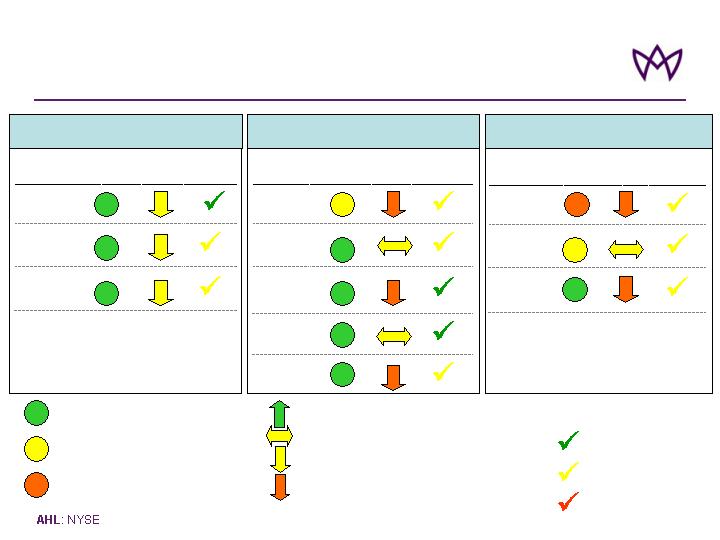

2007 Outlook: Property and Specialty Lines

Market

Trend

Risk Excess

Treaty

Pro Rata

Catastrophe

Treaty

Aspen 1Q07

Performance

Market

Conditions

Line

Market

Trend

Specialty

Reinsurance

Marine &

Energy Liability

Offshore

Energy

Physical

Damage

Marine Hull

Aviation

Aspen 1Q07

Performance

Market

Conditions

Line

Market

Trend

International

Property Fac.

E&S Property

UK Property

Aspen 1Q07

Performance

Market

Conditions

Line

Property Reinsurance

Specialty Lines

Property Insurance

= Absolute rate levels attractive

= Absolute rate levels mixed

= Absolute rate levels very challenging

= 12 month rate trend positive

= 12 month rate trend neutral

= 12 month rate trend slightly downwards

= 12 month rate trend downwards

23

Strong

Good

Improvement Required

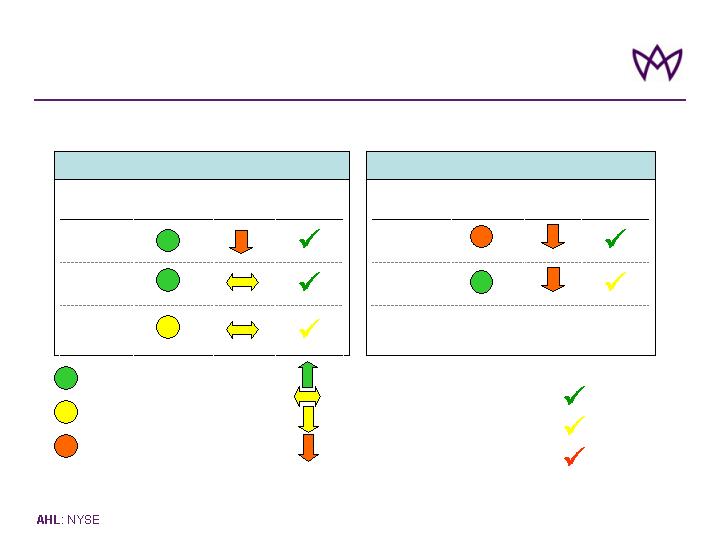

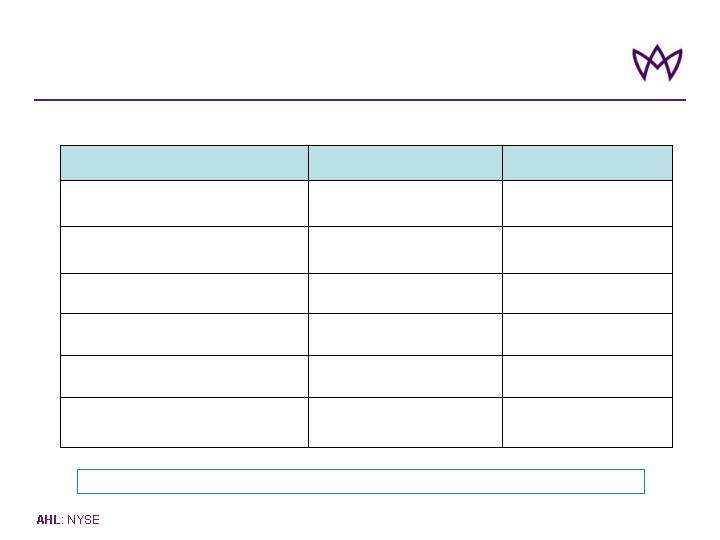

Market Conditions 2007 Outlook: Casualty Lines

Market

Trend

Casualty

Facultative

US Casualty

International

Casualty

Aspen 1Q07

Performance

Market

Conditions

Line

Market

Trend

E&S Casualty

UK Liability

Aspen 1Q07

Performance

Market

Conditions

Line

Casualty Reinsurance

Casualty Insurance

= Absolute rate levels attractive

= Absolute rate levels mixed

= Absolute rate levels very challenging

24

Strong

Good

Improvement Required

= 12 month rate trend positive

= 12 month rate trend neutral

= 12 month rate trend slightly downwards

= 12 month rate trend downwards

Strategy and Approach

2007 Q1 Financial Performance

Key Themes

Market Conditions

Florida Legislative Changes

2007 Outlook

Contents

25

Florida Hurricane Catastrophe Fund (“FHCF”):

2006 vs. 2007

2006 2007

PRIVATE MARKET

LAYERS

$16.7bn xs $5.3bn

FHCF

$21bn

$5.3bn

PRIVATE MARKET

LAYERS

$12bn TICL LAYER

- OPTIONAL

$18bn xs $6bn

FHCF

$3bn xs $3bn TEACO

LAYER - OPTIONAL

$36bn

$24bn

$6bn

$3bn

PRIVATE MARKET

LAYERS

PRIVATE MARKET

LAYERS

$2.3bn

$12bn

$2.3bn

Capacity Offered by FHCF Increased by up to $16.6 bn

0

0

26

Impact of Florida Legislation

Buying requirement increased significantly due to model change = circa +$28bn

$61bn

$54bn

$22bn

RMS v5

$89bn

Combined

$70bn

Personal

$39bn

Commercial

RMS v6

Limitations on cover offered by FHCF

Sold for named hurricane only

90% of each limit provided only

No reinstatement of cover

Opportunity to offer cover ‘below, above

and behind’ FHCF

Impact Less Dramatic than First Perceived

27

Florida 100 year PMLs*

* Probable Maximum Loss

Hurricane Risk

“As we know our climate is changing, the average temperature of the earth is rising, and greenhouse

gas emissions are increasing. We also know that climate remains an extraordinary complex area of

scientific study. While our understanding of the science continues to evolve and improve, there is still

much that we do not know and cannot fully recognize in efforts to model and predict future climate

system behaviour”.

Rex W Tillerson

Chairman and CEO, Exxon Mobil Corporation, Texas

Excerpt from his Keynote Speech at CERA Week 2007 (February 13 2007)

5.0

8.9

2006

8.3

7.5

7.7

7.8

7.5

Consensus Forecast*

?

15.0

9.0

7.0

4.0

Actual

2007

2005

2004

2003

2002

Year

Threat of Hurricane Risk Remains Very Acute and Hard to Predict

* Average of CPC, CSU, WRC, AEF, TSR

¹ Accurate Environmental Forecasting

Hurricane Forecasts vs. Actual 2002 - 2006

AEF¹ estimated 52% chance of no mainland USA strikes in 2006!

28

Strategy and Approach

2007 Q1 Financial Performance

Key Themes

Market Conditions

Florida Legislative Changes

2007 Outlook

Contents

29

80%

Target Combined Ratios: Across Cycles

E2007

E2007

95%

100%

105%

90%

85%

75%

95%

100%

105%

90%

85%

80%

75%

95%

100%

105%

90%

85%

80%

75%

78%-82%

81%-

85%

Cycle

Range

83%-88%

92%-

97%

Cycle

Range

Property and

Specialty Lines

Casualty Lines

Overall

E2007

92%-97%

85%-

92%

Cycle

Range

Market Conditions in 2007 Supportive of Continuing

Strong Underwriting Performance

Note: Assuming no major losses or prior year reserve movements

30

Improving Absolute Returns

Pick-up in yield

Investment Return

$200m hybrid offering and $200m buy-back completed;

authorisation for an additional $100m share buy-back

Financial Leverage

Re-distribution of income between operating companies

will result in reduced average tax rate

Tax Rate

Increase due to growth in reserves

Investment

leverage

Market conditions expected to remain attractive in most

lines

Combined Ratio

Reduction in GWP offset by reduction in ceded premium

Operating leverage

Significant reduction in retrocession purchased; risk

tolerances unchanged

Ceded premium

Expected impact

on ROAE

Outlook 2007

Lever

Targeted Management of Underlying Levers of ROAE

31

2007 Guidance

* Assumes no major losses or prior year reserve movements

Full 2007 Year Outlook

May 3, 2007

February 9, 2007

$135 million

16% to 19%

$230 – $250 million

83% – 88%*

6% – 8% of GWP

$1.9 billion + 5%

$115 million

(remainder of year)

16% to 19%

$250 – $270 million

83% – 88%*

6% – 8% of GWP

$1.8 billion + 5%

Tax Rate

Assumed Average Cat-Load

Investment Income

Combined Ratio

% Premium Ceded

GWP

Implied ROE of 16% – 20%

32

Aspen Insurance Holdings Limited

May 2007

Non-Deal Roadshow