Aspen Insurance Holdings Limited

Exhibit 99.1

Chris O’Kane, Chief Executive Officer

Richard Houghton, Chief Financial Officer

Investor Presentation

August 2007

AHL: NYSE

Safe Harbor Disclosure

This slide presentation is for information purposes only. It should be read in conjunction with our financial supplement posted on our website on the Investor Relations page and with other documents filed or to be filed shortly by Aspen Insurance Holdings Limited (the “Company” or “Aspen”) with the U.S. Securities and Exchange Commission.

Non-GAAP Financial Measures

In presenting Aspen's results, management has included and discussed certain "non-GAAP financial measures", as such term is defined in Regulation G. Management believes that these non-GAAP measures, which may be defined differently by other companies, better explain Aspen's results of operations in a manner that allows for a more complete understanding of the underlying trends in Aspen's business. However, these measures should not be viewed as a substitute for those determined in accordance with GAAP. The reconciliation of such non-GAAP financial measures to their respective most directly comparable GAAP financial measures in accordance with Regulation G is included herein or in the financial supplement, as applicable, which can be obtained from the Investor Relations section of Aspen's website at www.aspen.bm.

Application of the Safe Harbor of the Private Securities Litigation Reform Act of 1995:

This presentation contains written or oral "forward-looking statements" within the meaning of the U.S. federal securities laws. These statements are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements include all statements that do not relate solely to historical or current facts, and can be identified by the use of words such as "expect," "intend," "plan," "believe," "project," "anticipate," "seek," "will," "estimate," "may," "continue," and similar expressions of a future or forward-looking nature.

In addition, any estimates relating to loss events involve the exercise of considerable judgment and reflect a combination of ground-up evaluations, information available to date from brokers and cedants, market intelligence, initial tentative loss reports and other sources. Due to the complexity of factors contributing to the losses and the preliminary nature of the information used to prepare estimates relating to the UK floods, there can be no assurance that Aspen's ultimate losses associated with these floods will remain within the stated amount.

All forward-looking statements address matters that involve risks and uncertainties. Accordingly, there are or will be important factors that could cause actual results to differ materially from those indicated in these statements. Aspen believes these factors include, but are not limited to: changes in the total industry losses resulting from the UK and Australian floods and Hurricanes Katrina, Rita and Wilma and the actual number of Aspen's insureds incurring losses from these events; with respect to the UK and Australian floods and Hurricanes Katrina, Rita and Wilma, Aspen’s reliance on loss reports received from cedants and loss adjustors, Aspen's reliance on industry loss estimates and those generated by modeling techniques, the impact of these events on Aspen's reinsurers, any changes in Aspen's reinsurers' credit quality, the amount and timing of reinsurance recoverables and reimbursements actually received by Aspen from its reinsurers and the overall level of competition and the related demand and supply dynamics as contracts come up for renewal; the impact that our future operating results, capital position and rating agency and other considerations have on the execution of any capital management initiatives; the impact of any capital management activities on our financial condition; the impact of acts of terrorism and related legislation and acts of war; the possibility of greater frequency or severity of claims and loss activity, including as a result of natural or man-made catastrophic events than our underwriting, reserving or investment practices have anticipated; evolving interpretive issues with respect to coverage as a result of Hurricanes Katrina, Rita and Wilma and any other events such as the UK floods; the level of inflation in repair costs due to limited availability of labor and materials after catastrophes; the effectiveness of Aspen's loss limitation methods; changes in the availability, cost or quality of reinsurance or retrocessional coverage, which may affect our decision to purchase such coverage; the reliability of, and changes in assumptions to, catastrophe pricing, accumulation and estimated loss models; loss of key personnel; a decline in our operating subsidiaries' ratings with Standard & Poor's, A.M. Best Company or Moody's Investors Service; changes in general economic conditions including inflation, foreign currency exchange rates, interest rates and other factors that could affect our investment portfolio; the number and type of insurance and reinsurance contracts that we wrote at the January 1st and other renewal periods in 2007 and the premium rates available at the time of such renewals within our targeted business lines; increased competition on the basis of pricing, capacity, coverage terms or other factors; decreased demand for Aspen’s insurance or reinsurance products and cyclical downturn of the industry; changes in governmental regulations, interpretations or tax laws in jurisdictions where Aspen conducts business; proposed and future changes to insurance laws and regulations, including with respect to U.S. state- and other government-sponsored reinsurance funds and primary insurers; Aspen or its Bermudian subsidiary becoming subject to income taxes in the United States or the United Kingdom; the effect on insurance markets, business practices and relationships of ongoing litigation, investigations and regulatory activity by the New York State Attorney General's office and other authorities concerning contingent commission arrangements with brokers and bid solicitation activities. For a more detailed description of these uncertainties and other factors, please see the "Risk Factors" section in Aspen's Annual Reports on Form 10-K as filed with the U.S. Securities and Exchange Commission on February 22, 2007. Aspen undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the dates on which they are made.

2

AHL: NYSE

Contents

Aspen at a Glance

Key Investment Considerations

Strategy and Approach

Financial Performance

Enhancing Returns

Cycle Management

UK Flood Losses

Market Conditions

2007 Guidance

Appendix

3

AHL: NYSE

Contents

Aspen at a Glance

Key Investment Considerations

Strategy and Approach

Financial Performance

Enhancing Returns

Cycle Management

UK Flood Losses

Market Conditions

2007 Guidance

Appendix

4

AHL: NYSE

3%

3%

11%

51%

1%

25%

6%

Asia & Australia

Europe

UK

US & Canada

Worldwide Ex US

Worldwide inc US

Other

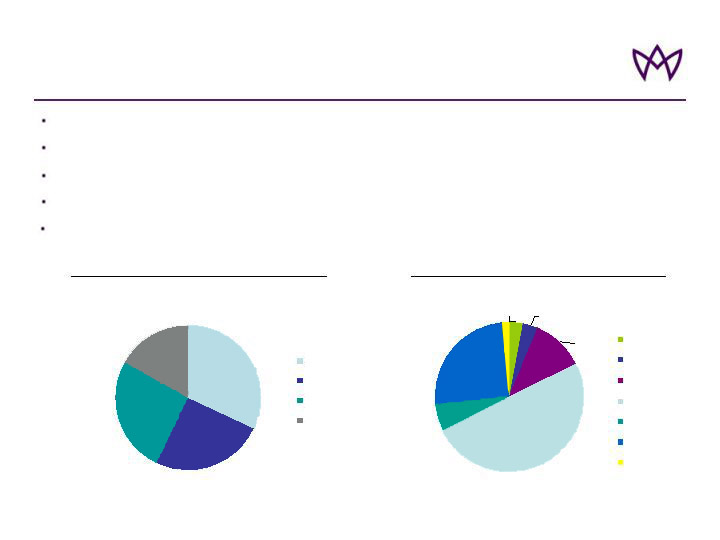

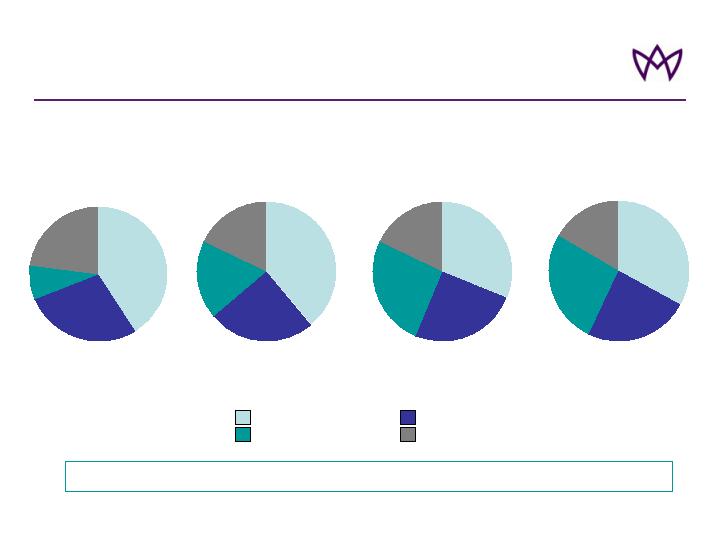

Aspen at a Glance

24%

26%

17%

33%

Prop Re

Casualty Re

Specialty Lines

Insurance

Underwriting Segment (GWP)

Geographical split of GWP

* Shareholders’ equity plus long-term debt

$2.25bn market cap (July 30, 2007)

$2.2bn common equity and $2.8bn total capital* (June 30, 2007)

Over 450 employees in Bermuda, UK, US, France and Switzerland

Ratings of A (S&P), A2 (Moody’s) and A / A- (AM Best, for Aspen UK and Aspen Bermuda)

$1.9bn Gross Written Premium (GWP) in 2006

100% = $1.8bn

5

100% = $1.8bn

12 months: July 1, 2006 – June 30, 2007

12 months: July 1, 2006 – June 30, 2007

[by location of cedant]

AHL: NYSE

Contents

Aspen at a Glance

Key Investment Considerations

Strategy and Approach

Financial Performance

Enhancing Returns

Cycle Management

UK Flood Losses

Market Conditions

2007 Guidance

Appendix

6

AHL: NYSE

Key Investment Considerations

Solid balance sheet

Diversified book of business

Strong underwriting results augmented by investment income growth

Tax rate reducing

Active capital management program

Established platforms from which we can grow; proven ability to add new

teams/lines

7

AHL: NYSE

Contents

Aspen at a Glance

Key Investment Considerations

Strategy and Approach

Financial Performance

Enhancing Returns

Cycle Management

UK Flood Losses

Market Conditions

2007 Guidance

Appendix

8

AHL: NYSE

Strategy: Key Components

Our strategy has 4 key components

1.

‘Specialty’ insurer and reinsurer

2.

Diversified operating platform: US, Bermuda, UK, France and Switzerland

3.

Enterprise Risk Management is our core strategic enabler

4.

Focus on book value growth per share, not top line

BVPS growth of 58.7% since Q4 2002, BVPS growth of 26.6% since

Jan 1, 2006

Objective: Deliver Consistent Above Average ROEs

9

AHL: NYSE

‘Specialty’ Insurer and Reinsurer

Selection of well chosen lines that match our core competencies

Mix of broad-based commercial and specialty lines

Choose businesses that reward us for specialized knowledge, not for scale

Future growth focused on specialty lines and more complex risks

Proven skill with lines that are complex, unpopular or have high barriers to entry

Effective differentiated risk management

Awarded ERM rating of “Strong”, 2nd highest level by S&P, placing Aspen in

top 14% in Europe

Well-chosen Businesses, Well-managed

10

AHL: NYSE

Well-managed Diversification

* 2003 Specialty lines includes QQS of Wellington Syndicate 2020

Targeted Growth in Specialty Lines And Improved Spread of Risk

Gross Written Premiums

11

FY 2005

Property Reinsurance

Casualty Reinsurance

Specialty Lines

Insurance

100% = $1.6bn

41%

8%

23%

28%

FY 2004

FY 2006

100% = $2.1bn

100% = $1.9bn

39%

18%

18%

25%

31%

26%

18%

25%

24%

26%

17%

33%

100% = $1.8bn

12 months: July 1, 2006 –

June 30, 2007

AHL: NYSE

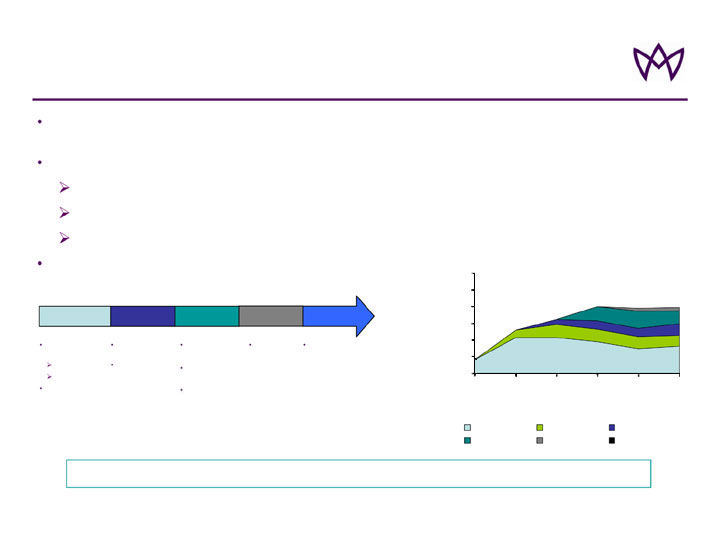

Profitable Expansion into New / Adjacent Lines

Progressive diversification of strategic footprint through incremental expansion into

adjacent business lines*

Key enablers:

Consistent with core competencies

Timing

Availability of proven, successful underwriting teams

Focus on non-correlating lines

2003

2004

2005

2007

Specialty

Reinsurance

Aviation

Marine

US Casualty Re

US Excess &

Surplus lines

Aspen Re

America

Aviation

Insurance

Marine

Insurance

Energy

Insurance

International

Property

Facultative

* Businesses shown for first year of meaningful premium contribution

** Projected for 2007

*** Underwriting commences 09/07

Diversification has Added over $1,070m** GWP in New Lines Since 2004

Development of Aspen’s GWP

0

500

1000

1500

GWP $m

2000

2500

3000

2002

2003

2004

2005

2006

2007

Year

Original Lines

2003 Lines

2004 Lines

2005 Lines

2006 Line

2007 Lines **

2006

Professional

Indemnity***

12

AHL: NYSE

Focus is on Growth in Book Value Per Share, Not Top Line

Core Beliefs about Growth

GWP and / or capital may shrink before we grow, according to market

conditions

Growth must be profitable and increase book value per share

Growth in new lines should meet two overarching sets of criteria

Underwriting fit

Operational fit

13

AHL: NYSE

UK

Commercial

Auto

War and

Terrorism

Cargo and

Specie

Excess

Casualty

US Retailer

Property

Accident &

Health/ Medical

Expenses

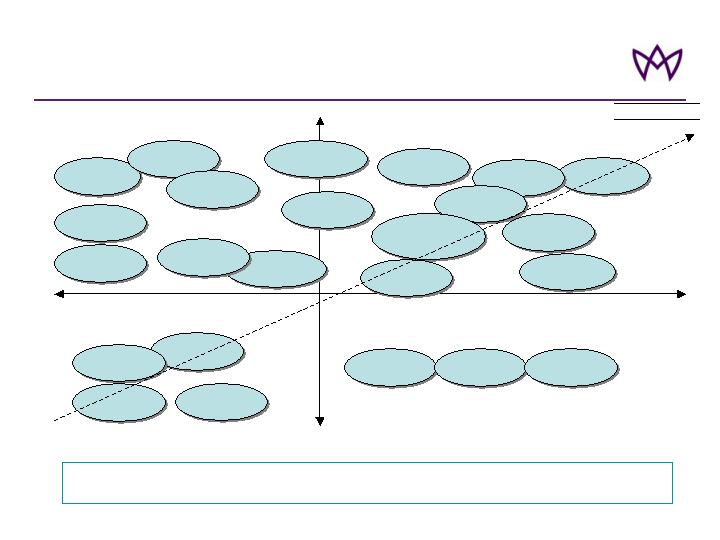

Approach to Growth - ‘Palette’

(lines we do not currently write)

Financial

Institutions

UK D&O

Operational fit

Underwriting fit

Bloodstock

Credit and

surety

Homeowners

Standard

Auto

US D&O

in US

High Net

Worths

Agriculture

US Airlines

Binder

Business

UK SMEs

Primary

Japanese

Property

HIGH

LOW

14

ILLUSTRATIVE

Political

risk

Nuclear

Contingency

US Onshore

Technical

Risk

Construction

/Engineering

Focus on Opportunities which Offer Best Fit with Our Underwriting and Operational

Capabilities

AHL: NYSE

Contents

Aspen at a Glance

Key Investment Considerations

Strategy and Approach

Financial Performance

Enhancing Returns

Cycle Management

UK Flood Losses

Market Conditions

2007 Guidance

Appendix

15

AHL: NYSE

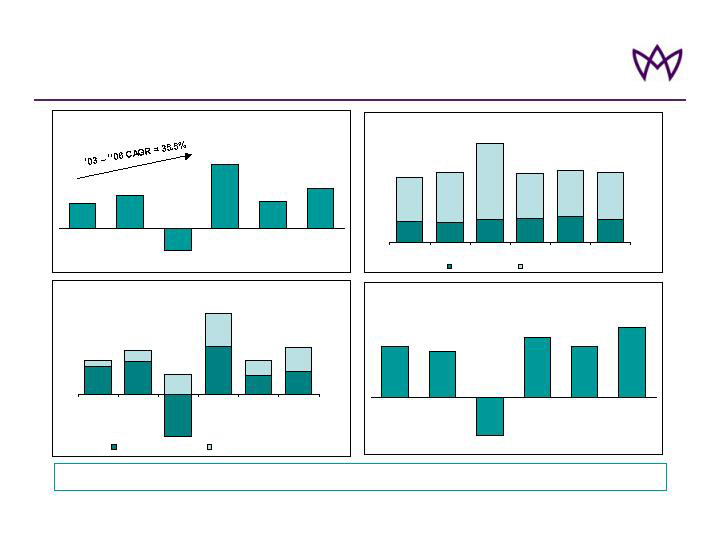

As well as increasing investment income

contribution...

$178

$204

-$259

$296

$118

$143

$68

$121

$94

$30

$204

$146

2003

2004

2005

2006

1H 2006

1H 2007

Underwriting Income

Investment Income

Financial Performance

Resulting in Improved ROAE

15.9%

14.0%

18.5%

15.6%

21.7%

-11.7%

2003

2004

2005

2006

1H 2006

1H 2007

Profitability increased substantially...

$152

$195

$378

$164

$237

($178)

2003

2004

2005

2006

1H 2006

1H 2007

Due to strong underwriting...

25%

25%

27%

29%

31%

28%

53%

59%

90%

55%

53%

56%

2003

2004

2005

2006

1H 2006

1H 2007

Expense Ratio

Loss Ratio

($ in millions)

16

Delivering Results

($ in millions – Net Income)

Note: Reconciliation of average equity to closing shareholders’ equity is provided in our quarterly financial supplements available in the Financial Results

section of the Investor Relations page of Aspen’s website, www.aspen.bm

AHL: NYSE

Financial Performance

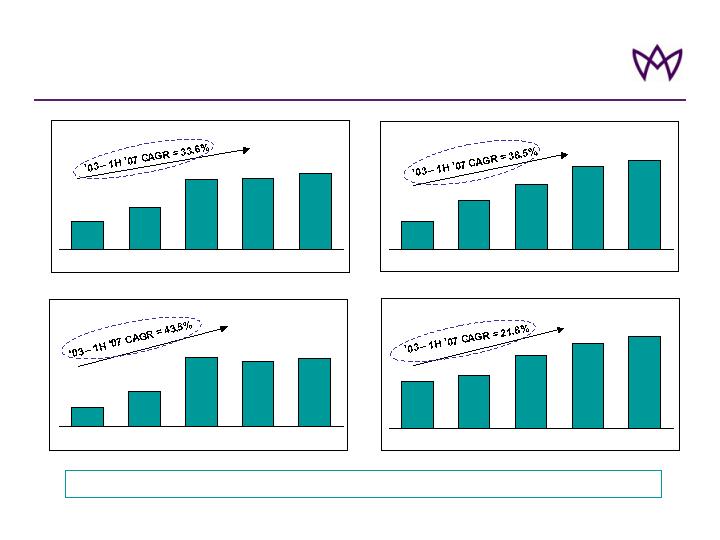

Total Assets are increasing...

$2,579

$3,943

$6,538

$6,640

$7,103

2003

2004

2005

2006

1H 2007

...As well as total investments

$1,616

$2,736

$3,689

$4,681

$5,058

2003

2004

2005

2006

1H 2007

Total Reserves

$1,098

$1,992

$3,910

$3,661

$3,883

2003

2004

2005

2006

1H 2007

($ in millions)

($ in millions)

($ in millions)

Shareholders’ Equity

$1,299

$1,482

$2,040

$2,389

$2,591

2003

2004

2005

2006

1H 2007

($ in millions)

Strong Balance Sheet

17

AHL: NYSE

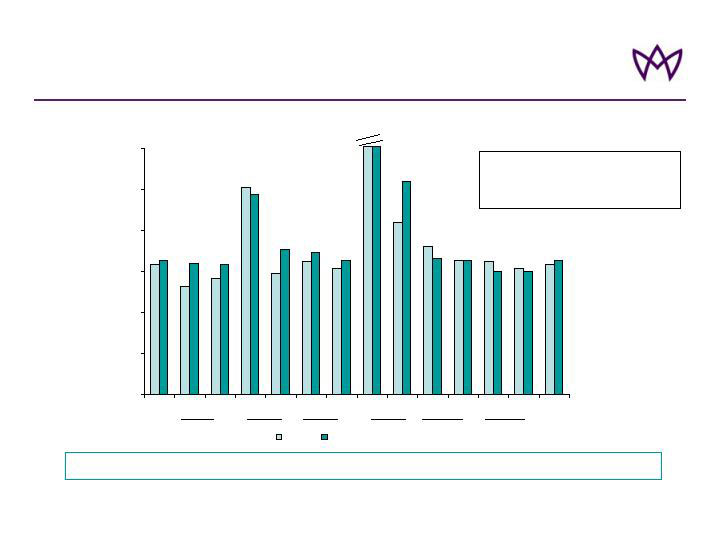

Underwriting Performance* vs. Peers

Underwriting Performance* Exceeds Industry 75% of the time

* Measured by combined ratio

** 05 Aspen -207%, 05 Peer Group average -199%

*** ACE, AWH, ACGL, AXS, ENH, RE, IPCR, MXGL, MRH, ORH, PRE, PTP, RNR, TRH, XL

0%

25%

50%

75%

Combined Ratio

100%

125%

150%

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Aspen

Peer Group Average***

Aspen average*: 92%

Peer group average*: 96%

04

03

05

06

07

**

18

AHL: NYSE

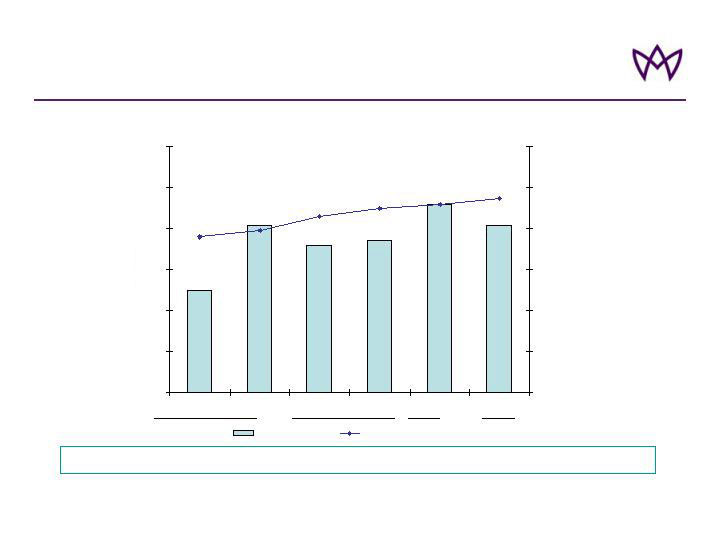

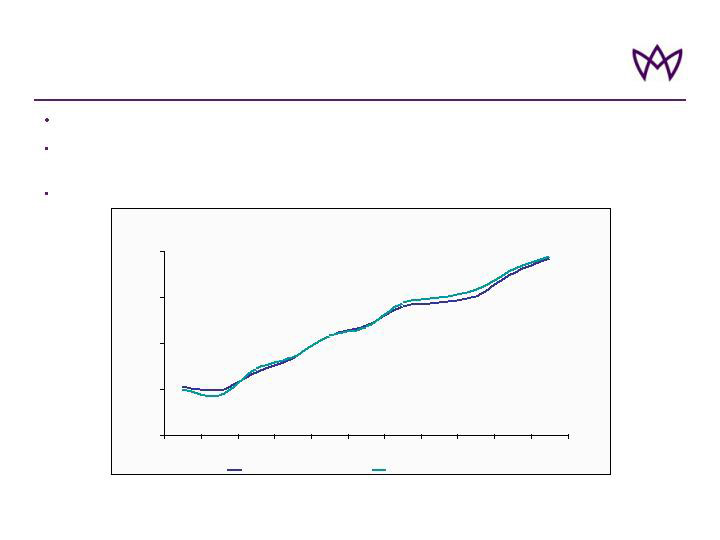

Growth in ROAE* and Book Value Per Share

12.5%

20.4%

18.0%

18.5%

22.9%

20.4%

0%

5%

10%

15%

ROAE %

20%

25%

30%

Q1

Q2

Q3

Q4

Q1

Q2

0.00

5.00

10.00

15.00

$ Diluted B/V Per Share

20.00

25.00

30.00

Annualised ROAE

Diluted BV Per Share**

06

07

Annualised ROAE >18% Over Last 6 Quarters, 26.6% Growth in BVPS

19

* Reconciliation of average equity to closing shareholders’ equity is provided in our quarterly financial supplements available in the Financial Results section of the Investor Relations

page of Aspen’s website, www.aspen.bm

** See Aspen’s quarterly financial supplement for a reconciliation of diluted book value per share to basic book value per share. Aspen’s financial supplement can be obtained from

the Investor Relations section of Aspen’s website at www.aspen.bm

AHL: NYSE

Contents

Aspen at a Glance

Key Investment Considerations

Strategy and Approach

Financial Performance

Enhancing Returns

Cycle Management

UK Flood Losses

Market Conditions

2007 Guidance

Appendix

20

AHL: NYSE

Reduced Exposure to Natural Catastrophes

Significant Reduction in Exposure to Natural Catastrophes At All Return Periods

Group Net AEP* Combined All Perils

“As-If” to RMS v6

* Aggregate Exceedance Probability (excludes inwards reinstatement premiums, includes outwards reinstatement premiums, net of tax)

Note: For net figures we have applied the current 2007 reinsurance / retro program to reflect what our previous exposure would have been versus our current structure

21

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

Annual Cat

Loss in USD 000

1,400,000

1,600,000

1,800,000

2,000,000

Mean

1 in 5

1 in 10

1 in 20

1 in 25

1 in 30

1 in 40

1 in 50

1 in 100

1 in 250

’08/2004

’02/2005

’08/2005

’02/2006

’08/2006

’02/2007

’06/2007

Event Frequency in

years

AHL: NYSE

Reduced Exposure to Natural Catastrophes

22

n/a

n/a

0.7%

0.3%

0.9%

0.8%

‘As-if’ loss (Gross)***

0.8%

0.5%

1.8%

1.5%

2.3%

1.7%

Actual loss (Gross)

Aspen Market share

3.0**

5.5**

89.6

12.9*

10.4*

66.3*

Selected market loss

June UK

Floods

Kyrill

Total KRW

Wilma

Rita

Katrina

US$ in billions

* Source: Sigma

** Reflects market estimates

*** ‘As-if’ is calculated by modelling the same event through our current portfolio

As of July 30, 2007

Reduced Share of Recent Cat Losses

Share of Recent Cat Losses

AHL: NYSE

Increasing Contribution from Investment Income

3.0%

3.5%

4.0%

4.5%

5.0%

Q404

Q105

Q205

Q305

Q405

Q106

Q206

Q306

Q406

Q107

Q207

Fixed Income portfolio book yield

Aggregate portfolio book yield*

23

* Including cash and cash equivalents but excluding Fund of Hedge Funds - Initial investments in Fund of Hedge Funds were made on April 1, 2006 with subsequent investment on February 1 and

June 1, 2007

Fixed income yield improved from 3.53% in Q4 04 to 4.94% in Q2 07

Invested 3% ($150m) in Funds of Hedge Funds in April ’06; now 8.8% ($481.6m); annualised

return of 17% in Q2 07

Investment leverage of 251% at Q2 07, up 23% from Q4 04

AHL: NYSE

22%

17%

32%

8%

10%

2%

9%

Govt

Agency

AAA

AA+/AA/AA-

A+/A/A-

BBB+/BBB/BBB-

NR

Investment Portfolio

Asset Class Allocation

25%

8%

15%

9%

16%

6%

13%

21%

6%

3%

22%

4%

23%

28%

0%

5%

10%

15%

20%

25%

30%

35%

Govt

Agency

MBS

Corp

ABS

FOHF

Cash/ST

Jun 07

Dec 06

Diversification with Performance

24

AAA

AAA

Overall Fixed Income Rating

3%

Actual as at

December 31,

2006

9%

Fund of Hedge Funds

Actual as at

June 30,

2007

Indicator (S&P Ratings)

Portfolio Credit Ratings

(as at June 30, 2007)

(As of June 30, 2007)

AHL: NYSE

Contents

Aspen at a Glance

Key Investment Considerations

Strategy and Approach

Financial Performance

Enhancing Returns

Cycle Management

UK Flood Losses

Market Conditions

2007 Guidance

Appendix

25

AHL: NYSE

Approach to Cycle Management

Growth = growth in BVPS, not top line per se

Business pricing must meet or exceed adequacy levels

Key components

Underwriting integrity

Optimizing business mix

Strong risk management

Efficient use of reinsurance / retrocession purchasing

Expense control

Improving investment contribution

Return Excess Capital to Shareholders When Appropriate

26

Profitability not volume paramount

AHL: NYSE

Managing the Underwriting Cycle

Board of Directors

CEO / Management Team

Annual planning process Target RORAC* and risk appetite

Monthly performance reviews

Underwriting quality reviews

Rate movement analysis

Technical pricing benchmarks

Peer review

Group Underwriting Committee review

Tactical level

Portfolio Level

Proactive Cycle Management

27

* RORAC = return on risk adjusted capital

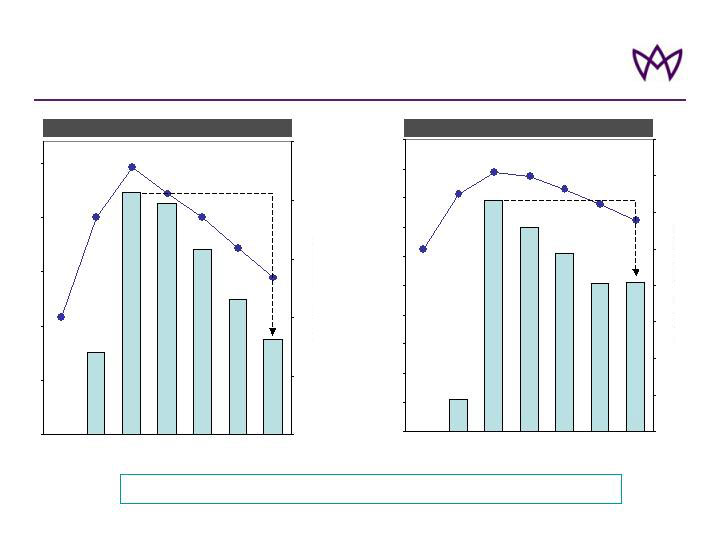

AHL: NYSE

76

223

213

171

125

88

0

50

100

150

200

GWP

$millions

250

2001

2002*

2003

2004

2005

2006

2007**

0

50

100

150

Rate Index, 2001=100%

200

250

RRV

(right scale)

GWP

(left scale)

GWP and rate index

11

79

70

61

51

51

0

10

20

30

40

50

60

70

GWP

$millions

80

90

100

2001

2002*

2003

2004

2005

2006

2007**

0

20

40

60

80

Rate Index,

2001=100%

100

120

140

160

RRV

(right scale)

GWP

(left scale)

UK Liability

UK Commercial Property

Proactive Cycle Management

% change ‘03-’07

Rates: -19%

GWP: -35%

% change ‘03-’07

Rates: -41%

GWP: -60%

Disciplined Underwriting and Cycle Management

* Since inception June 2002

** Projected year end 2007

AHL: NYSE

Contents

Aspen at a Glance

Key Investment Considerations

Strategy and Approach

Financial Performance

Enhancing Returns

Cycle Management

UK Flood Losses

Market Conditions

2007 Guidance

Appendix

29

AHL: NYSE

June/July UK Flood Losses

June 2007 UK Floods

Impacted Northern England

Q2 07 reserved $23.5 million

- $17.0 million from property reinsurance

- $6.5 million UK commercial property insurance

Estimate consistent with a market loss of GBP1.5 billion or $3 billion

July 2007 UK Floods

Impacted areas of Central and Southern England

Majority of UK flood exposures emanate from property catastrophe

reinsurance account; designed to respond to events of much greater

severity than the June floods

RMS and ABI indicate July floods will be less severe than June floods

30

AHL: NYSE

Contents

Aspen at a Glance

Key Investment Considerations

Strategy and Approach

Financial Performance

Enhancing Returns

Cycle Management

UK Flood Losses

Market Conditions

2007 Guidance

Appendix

31

AHL: NYSE

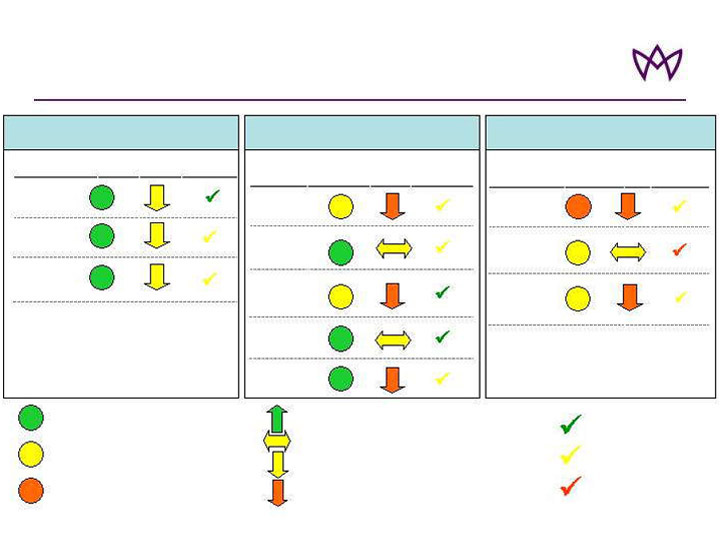

Market Conditions 2007 Outlook:

Property and Specialty Lines

Pro Rata

Market Trend

Risk Excess

Treaty

Catastrophe

Treaty

Aspen 1H07

Performance

Market Conditions

Line

Market

Trend

Specialty

Reinsurance

Marine &

Energy Liability

Offshore

Energy

Physical

Damage

Marine Hull

Aviation

Aspen 1H07

Performance

Market Conditions

Line

International

Property Fac.

E&S Property

Market Trend

UK Property

Aspen 1H07

Performance

Market

Conditions

Line

Property Reinsurance

Specialty Lines

Property Insurance

= Absolute rate levels attractive

= Absolute rate levels mixed

= Absolute rate levels very challenging

= 12 month rate trend positive

= 12 month rate trend neutral

= 12 month rate trend slightly downwards

= 12 month rate trend downwards

32

Strong

Good

Improvement Required

Updated July 27, 2007

AHL: NYSE

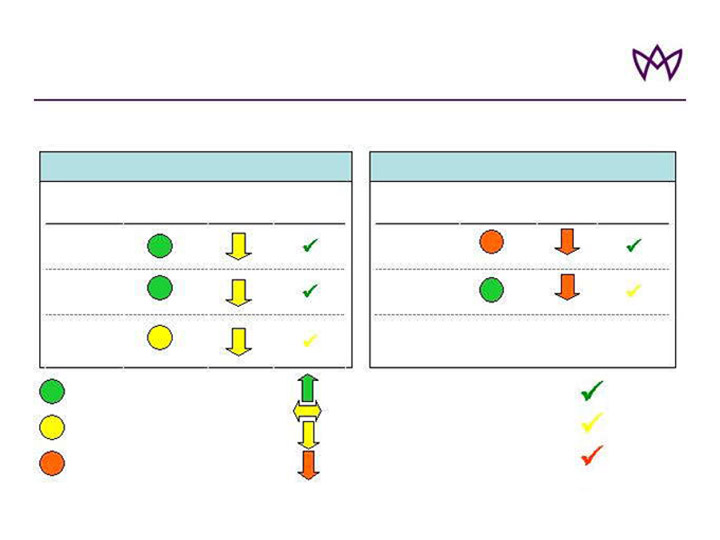

Market Conditions 2007 Outlook: Casualty Lines

Market Trend

Casualty

Facultative

US Casualty

International

Casualty

Aspen 1H07

Performance

Market Conditions

Line

Market Trend

E&S Casualty

UK Liability

Aspen 1H07

Performance

Market Conditions

Line

Casualty Reinsurance

Casualty Insurance

= Absolute rate levels attractive

= Absolute rate levels mixed

= Absolute rate levels very challenging

33

Strong

Good

Improvement Required

= 12 month rate trend positive

= 12 month rate trend neutral

= 12 month rate trend slightly downwards

= 12 month rate trend downwards

Updated July 27, 2007

AHL: NYSE

Contents

Aspen at a Glance

Key Investment Considerations

Strategy and Approach

Financial Performance

Enhancing Returns

Cycle Management

UK Flood Losses

Market Conditions

2007 Guidance

Appendix

34

AHL: NYSE

2007 Guidance

Full 2007 Year Outlook

$145 million

(full year)

16% to 19%

$250 – $270 million

83% – 88%

Approx 9% of GEP*

$1.8 billion + 5%

August 7, 2007

$145 million

(full year)

16% to 19%

$250 – $270 million

83% – 88%

6% – 8% of GWP

$1.8 billion + 5%

Q2 07 Earnings Call

Q4 06 Earnings Call

$135 million

(full year)

16% to 19%

$230 – $250 million

83% – 88%

6% – 8% of GWP

$1.9 billion + 5%

Tax Rate

Assumed Average Cat-

Load

Investment Income

Combined Ratio

% Premium Ceded

GWP

Implied ROE of 16% - 20%

35

* Metric changed from percent of GWP to percent of GEP to reflect that the company has purchased multi year retrocessional policies and believes that a comparison with earned premiums is more appropriate than written premium for guidance purposes. This change in the ceded premium metric does not impact our current ROE guidance.

AHL: NYSE

Contents

Aspen at a Glance

Key Investment Considerations

Strategy and Approach

Financial Performance

Enhancing Returns

Cycle Management

UK Flood Losses

Market Conditions

2007 Guidance

Appendix

36

AHL: NYSE

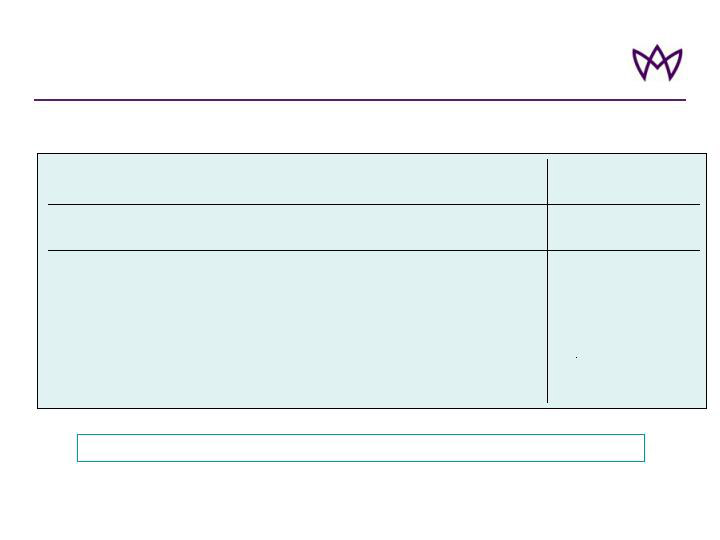

Financial Highlights – Q2 2007

37

* Annualised

¹ Reconciliation of Average Equity to closing shareholders’ equity and operating income to net income is provided in our quarterly financial supplements

available in the Financial Results section of the Investor Relations page of Aspen’s website at www.aspen.bm

Appendix

AHL: NYSE

(US$ in millions, except per share data)

Quarter Ended June 30

2007

2006

% Change

Gross Written Premiums

503.5

522.4

(3.6)

Net Written Premiums

418.5

500.1

(16.3)

Net Earned Premiums

451.2

429.0

5.2

Underwriting Income

52.4

79.0

(33.7)

Net Investment Income

78.8

49.9

57.9

Net Income after tax

$114.7

$101.8

12.7%

GAAP Ratios:

Loss Ratio

60.5%

52.2%

Expense Ratio

27.9%

29.4%

Combined Ratio

88.4%

81.6%

Full Year ROAE

20.4%*

20.4%*

Diluted Income Per Ordinary Share:

Net Income

$1.19

$1.01

17.8%

Operating Income¹

$1.14

$0.98

16.3%

Financial Highlights – Half Year 2007

(US$ in millions, except per share data)

Six Months Ended June 30 2007 2006 % Change

* Annualised

¹ Reconciliation of Average Equity to closing shareholders’ equity and operating income to net income is provided in our quarterly financial supplements

available in the Financial Results section of the Investor Relations page of Aspen’s website at www.aspen.bm

38

Appendix

AHL: NYSE

Gross Written Premiums

1,140.0

1,201.1

(5.1)

Net Written Premiums

973.6

952.0

2.3

Net Earned Premiums

890.2

831.6

7.0

Underwriting Income

142.9

117.7

21.4

Net Investment Income

146.3

94.4

55.0

Net Income after tax

$236.6

$163.6

44.6%

GAAP Ratios:

Loss Ratio

55.9%

54.8%

Expense Ratio

28.0%

31.0%

Combined Ratio

83.9%

85.8%

Full Year ROAE

21.7%*

15.6%*

Book Value Per Ordinary Share

$24.44

$20.19

21.1%

Diluted Income Per Ordinary Share:

Net Income

$2.46

$1.61

52.8%

Operating Income¹

$2.40

$1.57

52.9%

Financial Highlights – Group Summary Q2

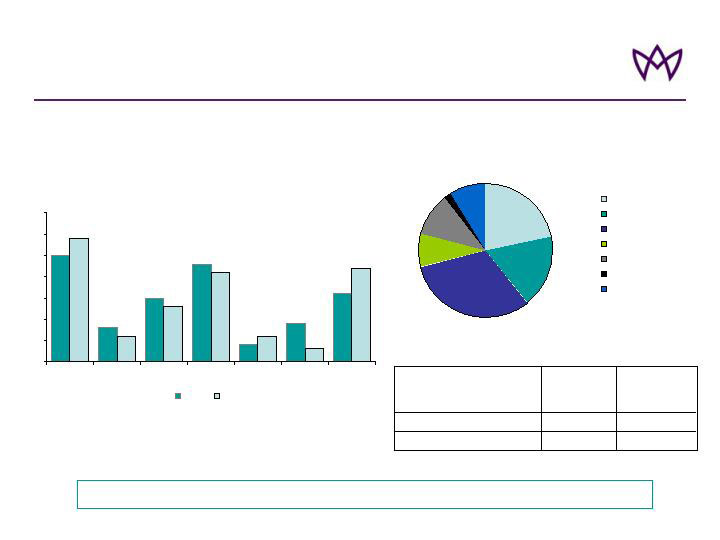

Underwriting Revenues

522

22

500

429

504

85

419

451

0

200

400

$ms

600

GWP

Premiums

Ceded

NWP

NEP

2006 Q2

2007 Q2

Income

124

127

102

84

129

131

115

95

0

40

80

120

$ms

160

200

Operating

Income

Before Tax

Income

Before Tax

Income After

Tax

Retained

Income

2006 Q2

2007 Q2

Underwriting Income

79

52

0

40

$ms

80

120

Underwriting Income

2006 Q2

2007 Q2

Underwriting Expenses

224

83

43

350

82

44

399

273

0

200

400

$ms

600

Losses &

Loss

Expenses

Acquisition

Exp

General &

Admin

Expenses

Total

Underwriting

Expenses

2006 Q2

2007 Q2

39

Appendix

AHL: NYSE

Financial Highlights – Group Summary - Half Year

Underwriting Revenues

1201

249

952

832

1140

166

974

890

0

200

400

600

800

1,000

1,200

1,400

GWP

Premiums

Ceded

NWP

NEP

2006 H1

2007 H1

Income

202

205

164

128

275

278

237

196

0

40

80

120

160

200

240

280

320

Operating

Income

Before Tax

Income

Before Tax

Income After

Tax

Retained

Income

2006 H1

2007 H1

Underwriting Income

118

143

0

40

80

$ms

$ms

$ms

$ms

120

160

Underwriting Income

2006 H1

2007 H1

Underwriting Expenses

456

177

81

714

159

90

747

498

0

200

400

600

800

1000

Losses &

Loss

Expenses

Acquisition

Exp

General &

Admin

Expenses

Total

Underwriting

Expenses

2006 H1

2007 H1

40

Appendix

AHL: NYSE

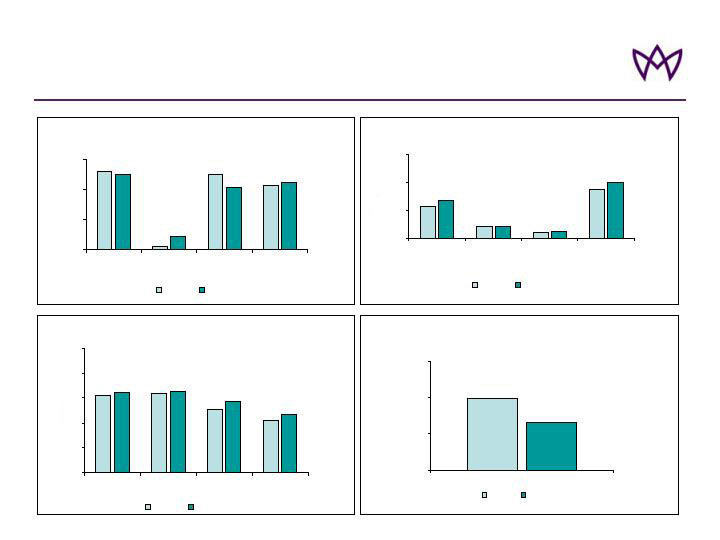

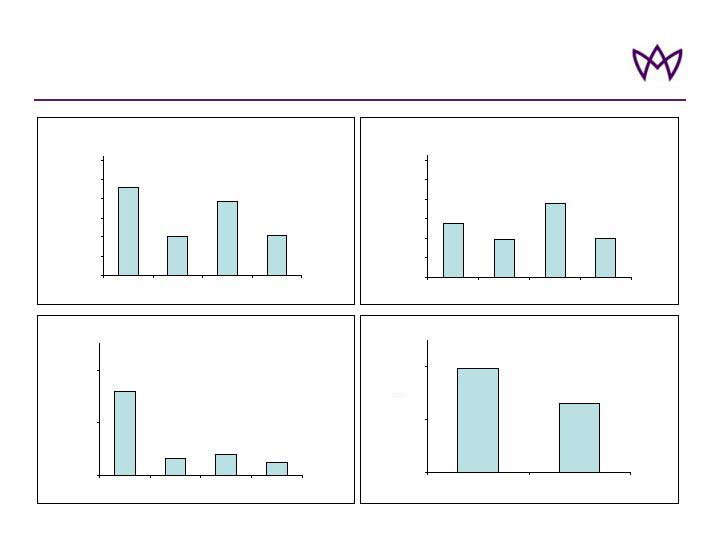

Results by Business Segment – Q2 2007

GWP

185

80

155

84

0

40

80

120

160

200

240

Property Re

Casualty Re

Specialty

Lines

P&C

Insurance

NWP

110

78

152

79

0

40

80

120

160

200

240

Property Re

Casualty Re

Specialty

Lines

P&C

Insurance

Underwriting Profit

32

7

8

5

0

20

$ms

$ms

$ms

$ms

40

Property Re

Casualty Re

Specialty

Lines

P&C

Insurance

Income Contribution

79

52

0

40

80

Net Investment Income

Underwriting Profit

41

Appendix

AHL: NYSE

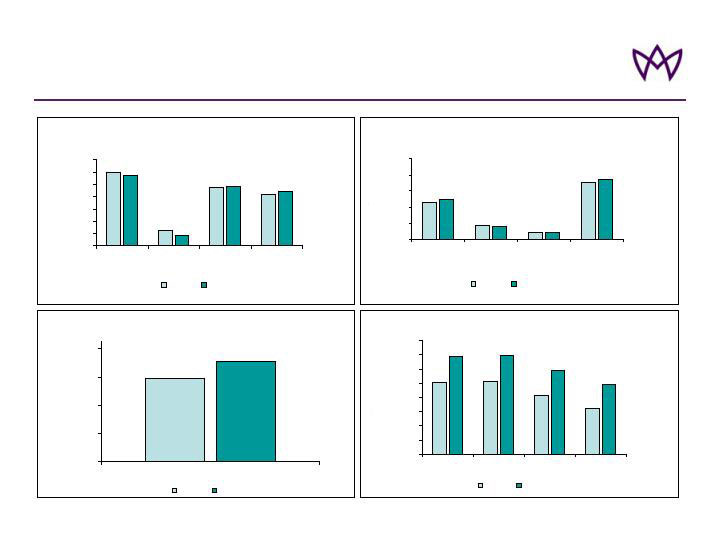

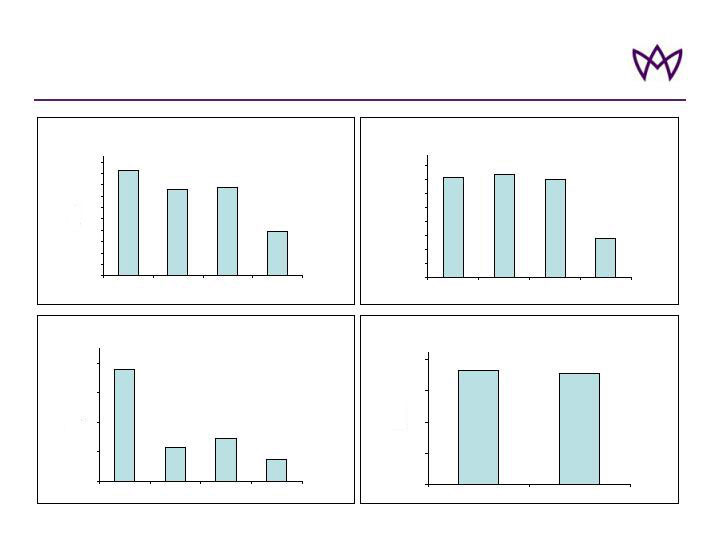

Results by Business Segment – Half Year 2007

GWP

372

303

311

154

0

40

80

120

160

200

240

280

320

360

400

Property Re

Casualty Re

Specialty

Lines

P&C

Insurance

NWP

287

295

279

113

0

40

80

120

160

200

240

280

320

Property Re

Casualty Re

Specialty

Lines

P&C

Insurance

Underwriting Profit

76

23

29

15

0

20

40

$ms

$ms

$ms

$ms

60

80

Property Re

Casualty Re

Specialty

Lines

P&C

Insurance

Income Contribution

146

143

0

40

80

120

160

Net Investment Income

Underwriting Profit

42

Appendix

AHL: NYSE