TRUE0001267395F-1/A4,330.04,131.31,527.01,576.765.71.65.114.7—494.9537.70.0102.97.73.73.721.025.0112.444.823.925.315.912.7323.2232.12.14.51.21.314.9—129.8—19.63.1—9.44.95.85.05.05.08.70.4—P3YP3Yhttp://fasb.org/us-gaap/2023#AccumulatedOtherComprehensiveIncomeLossNetOfTax

As filed with the Securities and Exchange Commission on April 5, 2024.

Registration No. 333-276163

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 2

to

Form F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

ASPEN INSURANCE HOLDINGS LIMITED

(Exact Name of Registrant as Specified in its Charter)

| | | | | | | | |

| Bermuda | 6331 | 98-0501000 |

(State or Other Jurisdiction

of Incorporation or Organization) | (Primary Standard Industrial

Classification Code Number) | (I.R.S. Employer Identification Number) |

141 Front Street

Hamilton, HM19

Bermuda

Telephone: (441) 295-8201

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

Cogency Global Inc.

122 East 42nd Street, 18th Floor

New York, New York 10168

Telephone: (212) 947-7200

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code,

of Agent For Service)

Copies to:

| | | | | | | | |

Samir A. Gandhi

Robert A. Ryan

Adam M. Gross

Sidley Austin LLP

787 Seventh Avenue

New York, New York 10019

(212) 839-5300 | Sarah Demerling

Natalie Neto

Rachel Nightingale

Walkers (Bermuda) Limited

Park Place

55 Par La Ville Road, Third Floor

Hamilton HM11

Bermuda

(441) 242-1500 | Marc D. Jaffe

Erika L. Weinberg

Latham & Watkins LLP

1271 Avenue of the Americas

New York, New York 10020

(212) 906-1200 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, please check the following box. ☐

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earliest effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company ☐

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

†The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. The selling shareholders may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion, Dated April 5, 2024

Preliminary Prospectus

Ordinary Shares

Aspen Insurance Holdings Limited

This is the initial public offering of the ordinary shares, par value $0.01 per share, of Aspen Insurance Holdings Limited (the “ordinary shares”). The selling shareholders identified in this prospectus are offering ordinary shares. We are not selling any ordinary shares under this prospectus and we will not receive any of the proceeds from the sale of ordinary shares by the selling shareholders.

Immediately prior to this offering, there has been no public market for our ordinary shares. It is currently estimated that the initial public offering price will be between $ and $ per ordinary share. We intend to apply to list our ordinary shares on the New York Stock Exchange (the “NYSE”) under the symbol “AHL.”

Following the completion of this offering, we will continue to have one class of authorized and outstanding ordinary shares and one class of authorized and outstanding preference shares, consisting of three series, which are our Fixed-Floating Rate Perpetual Non-Cumulative Preference Shares (“AHL PRC Shares”), our 5.625% Perpetual Non-Cumulative Preference Shares (“AHL PRD Shares”) and our 5.625% Perpetual Non-Cumulative Preference Shares (“AHL PRE Shares” and, together with our AHL PRC Shares and our AHL PRD Shares, the “Preference Shares”). The AHL PRE Shares are represented by depositary shares, each representing a 1/1000th interest in an AHL PRE Share (“Depositary Shares”). For a more detailed description of our ordinary shares and Preference Shares, see “Description of Share Capital.”

We are a “foreign private issuer” as defined under the U.S. federal securities laws and, as such, will be subject to reduced public company reporting and stock exchange governance requirements. See “Management and Corporate Governance—Foreign Private Issuer Exemption” for additional information.

AP Highlands Co-Invest, L.P., a Cayman exempted limited partnership (“AP Highlands Co-Invest”), and AP Highlands Holdings, L.P., a Cayman exempted limited partnership (“AP Highlands Holdings” and, together with AP Highlands Co-Invest, the “Apollo Shareholders”), each an affiliate of certain investment funds managed by affiliates of Apollo Global Management, Inc. (collectively with its subsidiaries, “Apollo”), are the selling shareholders in this offering (the “selling shareholders”). Following this offering, the Apollo Shareholders will collectively beneficially own approximately % of our ordinary shares (or % if the underwriters exercise in full their option to purchase additional ordinary shares from the selling shareholders). As a result, we will be a “controlled company” under the corporate governance rules of the NYSE applicable to listed companies, and therefore are permitted to elect not to comply with certain corporate governance requirements thereunder.

Investing in our ordinary shares involves a high degree of risk. Before investing in our ordinary shares, you should carefully read the “Risk Factors” beginning on page 31 of this prospectus. Neither the Securities and Exchange Commission (the “SEC”) nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| | | | | | | | | | | |

| Per ordinary share | | Total |

| Initial public offering price | $ | | | | $ | | |

Underwriting discount(1) | $ | | | | $ | | |

| Proceeds, before expenses, to the selling shareholders | $ | | | | $ | | |

__________________

(1)Please see “Underwriting (Conflicts of Interest)” for a description of all compensation payable to the underwriters.

The underwriters have an option to purchase up to an additional ordinary shares from the selling shareholders at the initial public offering price less the underwriting discount for 30 days from the date of this prospectus.

The underwriters expect to deliver the ordinary shares against payment in New York, New York on or about , 2024.

| | | | | | | | |

| Goldman Sachs & Co. LLC | Citigroup | Jefferies |

Prospectus dated , 2024.

TABLE OF CONTENTS

ABOUT THIS PROSPECTUS

About This Prospectus

We, the selling shareholders and the underwriters have not authorized anyone to provide any information different from that contained in this prospectus or in any free writing prospectuses prepared by us or on our behalf or to which we have referred prospective investors. We, the selling shareholders and the underwriters take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give prospective investors. This prospectus is an offer to sell only the ordinary shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is accurate only at the date on the front cover of this prospectus, regardless of the time of delivery of this prospectus or any sale of our ordinary shares.

We further note that the representations, warranties and covenants made by us in any agreement that is filed as an exhibit to the registration statement of which this prospectus is a part were made solely for the benefit of the parties to such agreement, including, in some cases, for the purpose of allocating risk among the parties to such agreement, and should not be deemed to be a representation, warranty or covenant made to prospective investors or for the benefit of prospective investors. Moreover, such representations, warranties or covenants were accurate only at the date they were made. Accordingly, such representations, warranties and covenants should not be relied on as accurately representing the current state of our affairs.

Certain Defined Terms

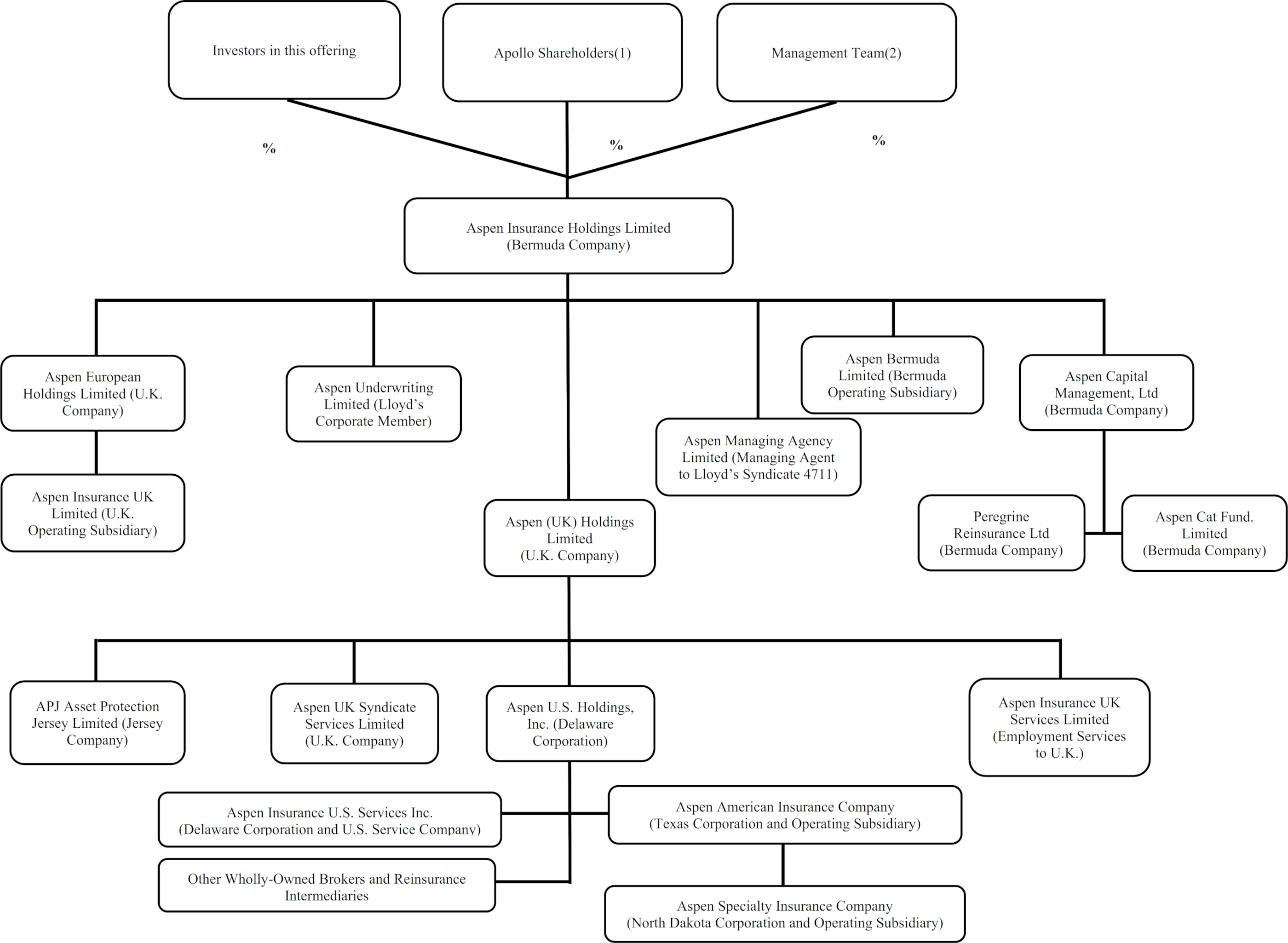

References in this prospectus to the “Company,” “Aspen,” the “Aspen Group,” “Group,” “we,” “us” or “our” refer to Aspen Insurance Holdings Limited (“Aspen Holdings”) or Aspen Holdings and its consolidated subsidiaries, as the context requires, including after giving effect to the Pre-IPO Merger Transaction (as defined below) pursuant to which Highlands Bermuda Holdco, Ltd., a holding company affiliate of certain investment funds managed by affiliates of Apollo whose sole asset is ordinary shares of Aspen, will merge with and into the Company with the Company surviving the merger as the surviving company. See “Summary—Our Corporate Structure and the Pre-IPO Merger Transaction” for more information. Our principal operating subsidiaries are: Aspen Bermuda Limited (“Aspen Bermuda”), Aspen Specialty Insurance Company (“Aspen Specialty”), Aspen American Insurance Company (“AAIC”), Aspen Insurance UK Limited (“Aspen UK”) and Aspen Underwriting Limited (“AUL”) (as corporate member of our Lloyd’s operations, Lloyd’s Syndicate 4711 (“Syndicate 4711”), which are managed by Aspen Managing Agency Limited (“AMAL”) (together, “Aspen Lloyd’s”)), each referred to herein as an “Operating Subsidiary” and collectively referred to as the “Operating Subsidiaries.” References to “Aspen Capital Markets” or “ACM” means business conducted by our subsidiaries that participate in alternative reinsurance markets, including through Peregrine Reinsurance Ltd (“Peregrine”) and related management entities, including Aspen Capital Management, Ltd. (“ACML”). ACM forms part of the Aspen Capital Partners platform, in recognition of the synergies between ACM and the Company’s outwards reinsurance teams.

We manage our underwriting operations as two distinct business segments, insurance and reinsurance. References in this prospectus to our “Insurance segment” or “Aspen Insurance” refer to our insurance segment and references to the “Reinsurance segment” or “Aspen Re” refer to our reinsurance segment.

Under Bermuda law there is no concept of “outstanding” share capital. However, for purposes of this prospectus, to align with U.S. share capital terminology and for the avoidance of doubt, references to “outstanding” with respect to our share capital refer to our “issued” share capital under Bermuda law.

Exchange Control

Ordinary shares may be offered or sold in Bermuda only in compliance with the provisions of the Investment Business Act of 2003, as amended, the Bermuda Companies Act 1981, as amended (the “Companies Act”), and the Exchange Control Act 1972, as amended (the “Exchange Control Act”), and related regulations of Bermuda that regulate the sale of securities in Bermuda. In addition, specific permission is required from the Bermuda Monetary Authority (the “BMA”), pursuant to the provisions of the Exchange Control Act and related regulations, for all issuances and transfers of securities of Bermuda companies, other than in cases where the BMA has granted a

general permission. The BMA in its policy dated June 1, 2005 provides that where any equity securities of a Bermuda company are listed on an appointed stock exchange (the NYSE is such an exchange), general permission is given for the issue and subsequent transfer of any securities of the company (which includes the ordinary shares described herein) from and/or to a non-resident of Bermuda, for as long as any equity securities of the company remain so listed.

Service of Process and Enforcement of Civil Liberties

We are a Bermuda exempted company. As a result, the rights of holders of our ordinary shares will be governed by Bermuda law and our memorandum of association (our “memorandum of association”) and our amended and restated bye-laws (our “bye-laws”). The rights of shareholders under Bermuda law may differ from the rights of shareholders of companies incorporated in other jurisdictions. In addition, certain of our directors and officers reside outside the United States (“U.S.”), and a substantial portion of our assets and the assets of such persons are located in jurisdictions outside the United States. As such, it may be difficult or impossible to effect service of process upon us or those persons in the United States or to recover against us or them on judgments of U.S. courts, including judgments predicated upon civil liability provisions of the U.S. federal securities laws. It is doubtful whether courts in Bermuda will enforce judgments obtained in other jurisdictions, including the United States, against us or our directors or officers under the securities laws of those jurisdictions or entertain actions in Bermuda against us or our directors or officers under the securities laws of other jurisdictions.

Investors Outside the United States

Neither we nor the selling shareholders have done anything that would permit the possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of our ordinary shares and the distribution of this prospectus outside of the United States.

Registered Trademarks and Trademark Applications

We own or have rights to use trademarks, service marks or trade names that we use in connection with the operation of our business. Other trademarks, service marks and trade names appearing in this prospectus are the property of their respective owners. Solely for convenience, the trademarks, service marks, trade names and copyrights referred to in this prospectus are listed without the ©, ® and ™ symbols, but we will assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensors to these trademarks, service marks, trade names and copyrights.

Market & Industry Data and Forecasts

Certain market and industry data and forecasts included in this prospectus were obtained from independent market research, industry publications and surveys, governmental agencies and publicly available information. Industry surveys, publications and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable, but that the accuracy and completeness of such information is not guaranteed. We have not independently verified any of the data from third-party sources, nor have we ascertained the underlying assumptions relied upon therein. Similarly, independent market research and industry forecasts, which we believe to be reliable based upon our management’s knowledge of the industry, have not been independently verified. While we are not aware of any material misstatements regarding the market or industry data presented herein, our estimates involve risks and uncertainties and are subject to change based on various factors, including those discussed under the heading “Risk Factors.”

Basis of Presentation

The financial information included herein has been derived from the financial statements and accounting records of the Company and has been prepared in accordance with generally accepted accounting principles in the United States (“GAAP”). Amounts in this prospectus and the financial statements included in this prospectus are

presented in U.S. dollars, unless otherwise noted. Certain amounts presented in tables are subject to rounding adjustments and, as a result, the totals in such tables may not sum.

Key Performance Measures and Non-GAAP Financial Measures

In presenting Aspen’s results, management has included key performance measures and discussed certain measurements that are considered “non-GAAP financial measures” under SEC rules and regulations. Management believes that these non-GAAP financial measures, which may be defined differently by other companies, help explain and enhance the understanding of Aspen’s results of operations. However, these measures should not be viewed as a substitute for those determined in accordance with GAAP.

Gross written premiums represents the total insurance premium for policies written or assumed during a specific period of time before the reduction for policy acquisition costs or other deductions. Gross written premiums is a volume measure commonly used in the insurance industry to compare sales performance by period.

Net written premiums are gross written premiums less ceded written premiums. Ceded written premiums are the amounts recognized for the purchases of reinsurance or retrocessional coverage, and are accounted for using the same methodology as gross written premiums.

Net earned premiums are the earned portion of an insurance contract. Net written premium is earned/recognized proportionately over the coverage period and associated risk patterns. Premiums written which are not yet recognized as earned are recorded on the balance sheet as unearned premiums.

Losses and loss adjustment expenses represents the amount paid or expected to be paid to claimants, including the cost of investigating, resolving and processing these claims, net of recoveries under the reinsurance and retrocession agreements. This can be broken out into the following categories:

•Current accident year losses, excluding catastrophe losses, represents the losses arising in the current financial period, excluding any prior year reserve development and catastrophe losses; and

•Catastrophe losses are losses that arise from various unpredictable events, including, but not limited to, weather-related natural catastrophes, pandemic or contagious disease and man-made events such as acts of war and terrorism.

Prior year adverse/(favorable) reserve development - post LPT years:

Prior year adverse/(favorable) reserve development represents the strengthening/(releases) in net ultimate loss reserves and claim adjustment expense reserves at each reporting date for claims which occurred in previous calendar years/periods.

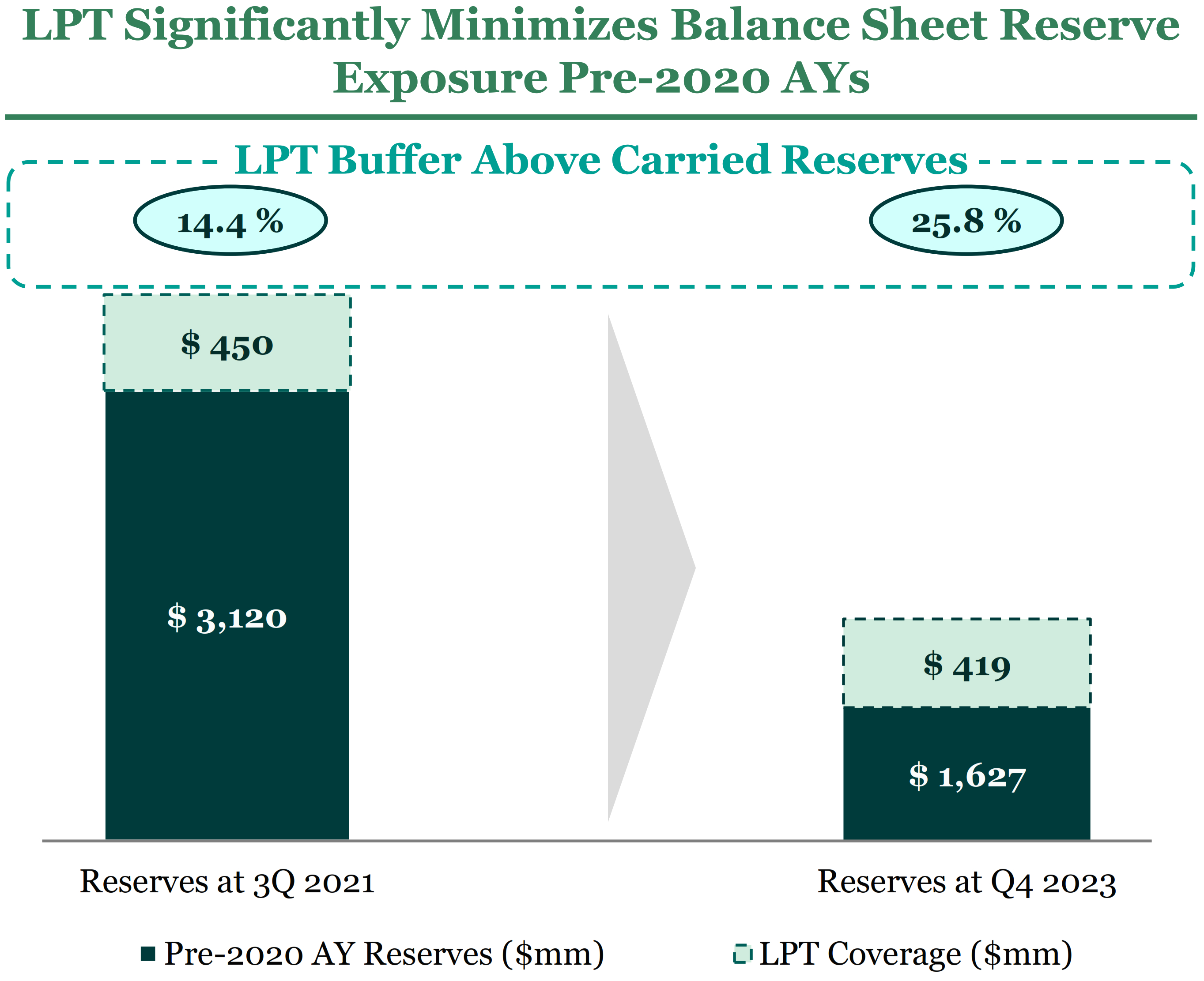

Aspen entered into a loss portfolio transfer (the “LPT”) with a subsidiary of Enstar Group Limited (“Enstar”). Under the terms of the LPT, Enstar’s subsidiary will reinsure net losses incurred on or prior to December 31, 2019 on all of Aspen’s net loss reserves of $3.12 billion as of September 30, 2021. The LPT provides a limit of $3.57 billion for 2019 and prior accident year loss development.

Prior year reserve development post LPT years represents the performance of our business for accident years 2020 onwards, reflecting the underlying underwriting performance of the ongoing business.

Adjusted losses and loss adjustment expenses is a non-GAAP financial measure. It is the sum of current accident year losses, catastrophe losses and prior year reserve strengthening/(releases) post LPT years. Adjusted losses and loss adjustment expenses excludes the change in the deferred gain on retroactive reinsurance contracts and represents the performance of our business for accident years 2020 onwards, which management believes reflects the underlying underwriting performance of the ongoing business.

Impact of the LPT represents the deferral of a portion of loss recoveries on 2019 and prior accident year loss development as per accounting requirements for retroactive reinsurance under GAAP. The LPT contract with Enstar is a retroactive reinsurance contract.

Underwriting result or income/ loss is a non-GAAP financial measure. Income or loss for each of the business segments is measured by underwriting income or loss. Underwriting income or loss is the excess of net earned premiums over the underwriting expenses. Underwriting expenses are the sum of losses and loss adjustment expenses, acquisition costs and general and administrative expenses. Underwriting income or loss provides a basis for management to evaluate the segment’s underwriting performance.

Adjusted underwriting income or loss is a non-GAAP financial measure. It is the underwriting profit or loss adjusted for the change in deferred gain on retroactive reinsurance contracts in order to economically match the loss recoveries under the adverse development cover (“ADC”)/LPT contracts with the underlying loss development of the assumed net loss reserves for the subject business of 2019 and prior accident years. Adjusted underwriting income or loss also excludes certain costs related to the LPT contract with Enstar that closed in the second quarter of 2022. Adjusted underwriting income represents the performance of our business for accident years 2020 onwards, which management believes reflects the underlying underwriting performance of the ongoing portfolio.

Loss ratio is the sum of current year net losses, catastrophe losses, prior year reserve strengthening/(releases), and the impact of the LPT as a percentage of net earned premiums.

Adjusted loss ratio is a non-GAAP financial measure. It is the sum of current year net losses, catastrophe losses and prior year reserve strengthening/(releases) post LPT years, as a percentage of net earned premiums. Adjusted loss ratio excludes the change in the deferred gain on retroactive reinsurance contracts and represents the performance of our business for accident years 2020 onwards, which management believes reflects the underlying underwriting performance of the ongoing business.

Along with most property and casualty insurance companies, we use the loss ratio, the expense ratio and the combined ratio as measures of underwriting performance. These ratios are relative measurements that describe, for every $100 of net earned premiums, the amount of losses and loss adjustment expenses, and the amount of other underwriting expenses that would be incurred. A combined ratio of less than 100 indicates an underwriting profit and a combined ratio of over 100 indicates an underwriting loss.

Combined ratio is the sum of the loss ratio and expense ratio. The loss ratio is calculated by dividing losses and loss adjustment expenses by net earned premiums. The expense ratio is calculated by dividing the sum of acquisition costs and general and administrative expenses, by net earned premiums.

Adjusted combined ratio is a non-GAAP financial measure. It is the sum of the adjusted loss ratio and the expense ratio. The adjusted loss ratio is calculated by dividing the adjusted losses and loss adjustment expenses by net earned premiums. The expense ratio is calculated by dividing the sum of acquisition costs and general and administrative expenses, by net earned premium.

Operating income is a non-GAAP financial measure. Operating income is an internal performance measure used by Aspen in the management of its operations and represents after-tax operating results. Operating income includes an adjustment for the change in deferred gain on retroactive reinsurance contracts in order to economically match the loss recoveries under the ADC/LPT contracts with the underlying loss development of the assumed net loss reserves for the subject business of 2019 and prior accident years. Operating income also excludes certain costs related to the LPT contract with Enstar that closed in the second quarter of 2022, net foreign exchange gains or losses, including net realized and unrealized gains and losses from foreign exchange contracts, net realized and unrealized gains or losses on investments and non-operating expenses and income.

Average equity is a non-GAAP financial measure and is used in calculating ordinary shareholders return on average equity. Average equity is calculated by taking the arithmetic average of total shareholders’ equity on a quarterly basis for the stated periods excluding the average value of Preference Shares (as defined below) less issue expenses.

Ratio of debt and hybrids to total capital is calculated by adding Preference Shares (aggregate liquidation preference net of issuance costs) and the aggregate principal amount of short-term and long-term debt and dividing by total capital. Total capital is defined as shareholders’ equity plus outstanding debt.

Total return on average cash and investments, pre-tax represents total pre-tax return/(loss) on investments as a percentage of average beginning and ending total cash and investments during the period.

Compound annual growth rate (“CAGR”) represents the annualized average rate of growth over a certain time period.

SUMMARY

Who We Are

We are a leading specialty (re)insurer focused on total value creation for all of our stakeholders. With $3,968 million of gross written premiums in 2023, we are a scaled multinational business with a diverse product mix balanced across our primary specialty insurance and opportunistic reinsurance franchises, which are both supported by our fee generating capital markets capabilities. We go to market with a single view of risk through our ‘One Aspen’ approach, which is designed to cater to complex, bespoke solutions that bring together our expertise spanning different lines of business, segments and platforms, enabling us to develop enhanced and differentiated offerings for our distribution partners and customers. We are focused on underwriting excellence and profitable growth to consistently deliver top quartile results, targeting mid-teen operating return on equity across market cycles. This is demonstrated by our combined ratio of 87.5% (adjusted combined ratio of 86.4%), return on average equity adjusted for Preference Share dividends of 26.7% and operating return on average equity (“Op. ROE”) of 20.2% for the twelve months ended December 31, 2023.

Our primary specialty insurance product set is centered around niche specialty lines, such as professional liability, credit and political risk, cyber and environmental, where we can apply our extensive underwriting and industry expertise. Our opportunistic reinsurance business is centered around both specialty and traditional reinsurance lines where we apply risk selection criteria to create unique risk profiles rather than an index of the market as other larger peers may do. Our size presents a distinct advantage, providing us with enough scale to be relevant while still maintaining the ability to be nimble and decisive, which enables us to enter, exit or change the nature of our underwriting positions faster and with greater precision.

Through our ‘One Aspen’ approach, we actively manage our insurance and reinsurance portfolios across market cycles and identify the most attractive risk versus return opportunities to allocate capital. We adopt a dynamic capital allocation approach, utilizing our strong balance sheet and our multiple platforms across the United States, the United Kingdom (“U.K.”), Lloyd’s of London (“Lloyd’s”) and Bermuda to match risk with the most appropriate source of capital, and to drive efficiencies and optimal outcomes for our customers. Our ability to offer our broker and client partners holistic and customized solutions across our entire platform provides us the opportunity to execute larger, more complex deals which frequently result in more attractive terms and conditions.

For the twelve months ended December 31, 2023, we wrote $3,968 million in gross written premiums across our Insurance and Reinsurance segments, at a combined ratio of 87.5%. Our shareholders’ equity, excluding accumulated other comprehensive income/(loss) (“AOCI”) of $(400) million and Preference Shares, net of issuance costs, with a total value of $754 million, was $2,555 million as of December 31, 2023. For the twelve months ended December 31, 2023, we generated $535 million of net income, representing a 26.7% return on average equity adjusted for Preference Share dividends and $368 million of operating income, representing a 20.2% Op. ROE.

Our Transformation

We have undertaken a comprehensive transformation of the business since our acquisition by Apollo in February 2019, centered around a clear strategic vision that has four core tenets: (1) focused underwriting; (2) reduced volatility; (3) improved operational efficiency; and (4) culture.

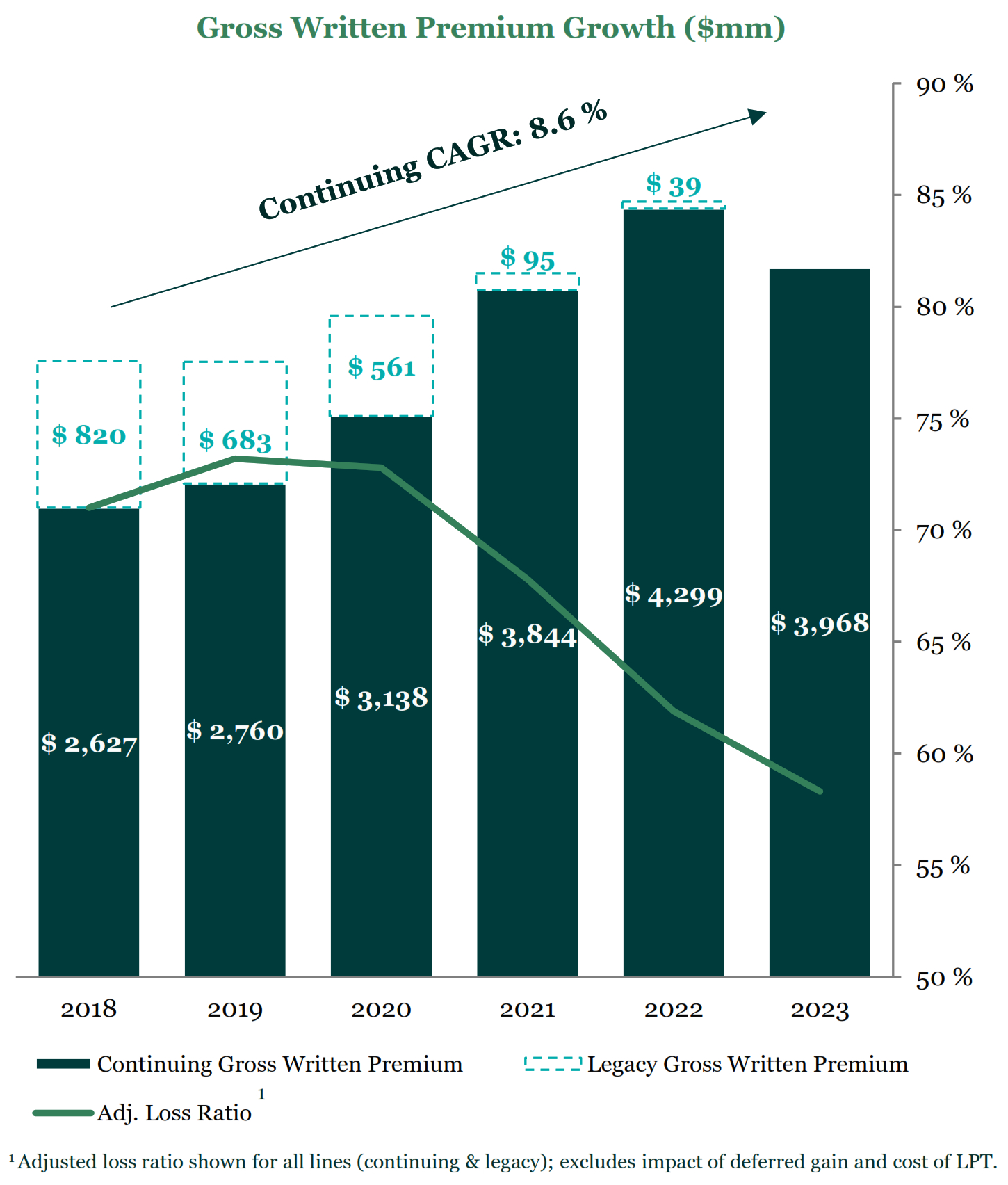

•Focused Underwriting: We have significantly reduced the breadth of our Insurance and Reinsurance product offerings to focus on core lines of business where we have a distinct relevance and leading market positions and believe we can achieve superior underwriting results with successful long-term track records. Since our acquisition by Apollo in 2019, we have exited twelve Insurance and five Reinsurance lines of business as part of the strategic repositioning of our underwriting portfolio, which accounted for approximately $911 million of gross written premiums for the twelve months ended December 31, 2018. We have classified $820 million of this as “Legacy” (as defined in “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Key Performance Measures and Non-GAAP Financial Measures—Summary of Continuing and Legacy Business”) business for purposes of reporting on historical legacy underwriting results as these lines of business were exited during the main underwriting remediation period from 2018 to 2021. There were additional exits of two Reinsurance lines of business in

2022, which were part of further refinements to our underwriting strategy, but not classified as part of Legacy underwriting results. We have delivered significant growth in our continuing lines of business, with gross written premiums of $3,968 million in 2023, having grown at a CAGR of 8.6% from 2018 to 2023 (with annual growth rates of 5.1%, 13.7%, 22.5%, 11.8% and (7.7)% for 2019, 2020, 2021, 2022 and 2023, respectively). There can be no assurance that such growth trends will continue. At the same time, we improved our underwriting performance, as illustrated by our adjusted loss ratio and combined ratio decreasing by 12.7 and 16.5 percentage points respectively, over the same period.

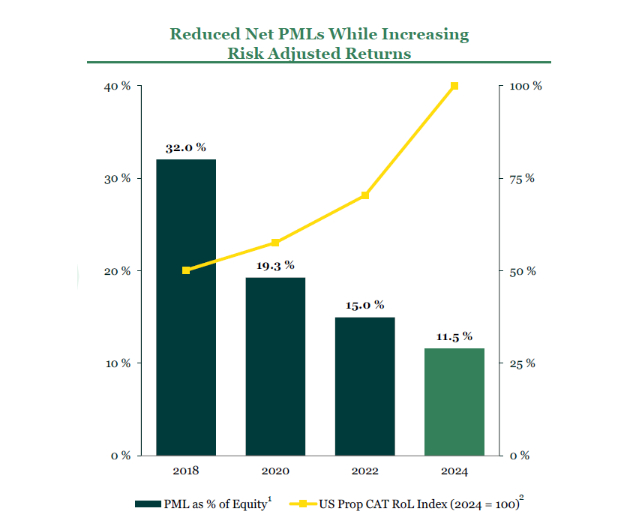

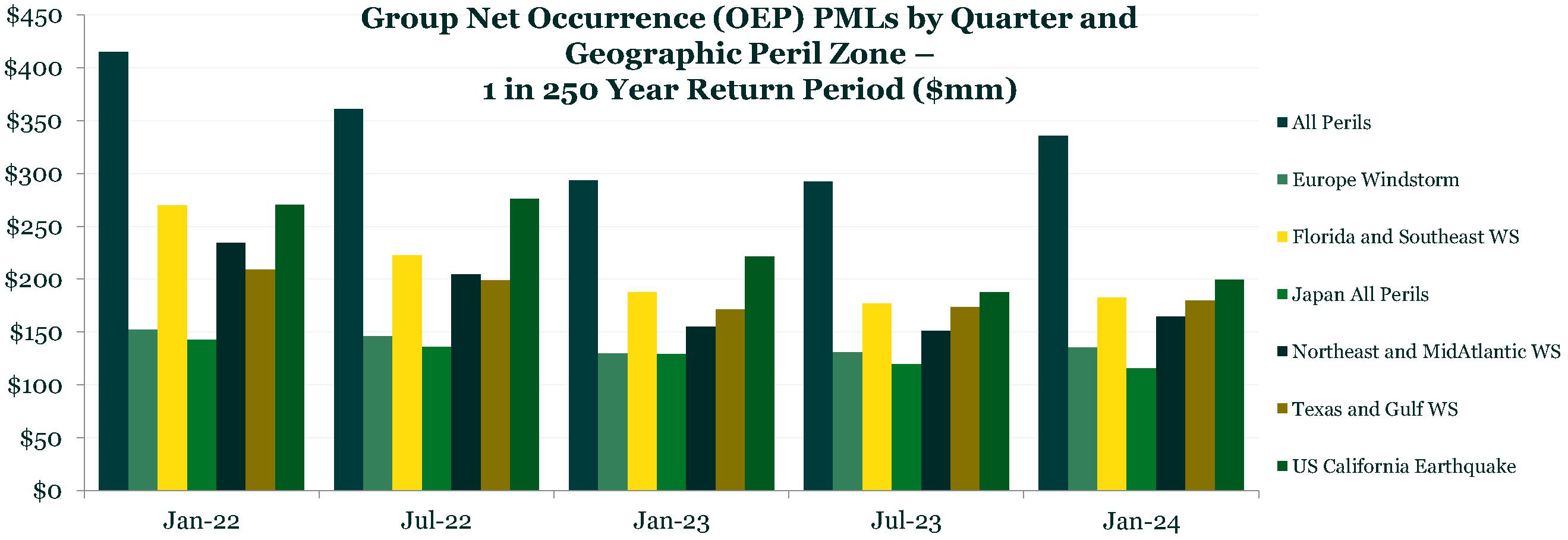

•Reduced Volatility: We have taken extensive action to reduce volatility within both our existing in-force and go-forward businesses. We have dramatically decreased our property catastrophe exposure, with January 1, 2024 net 250-year probable maximum loss (“PML”) exposure of $336 million, which has declined by approximately 64% relative to the start of 2018. This allowed us to generate a 20.2% Op. ROE for the twelve months ended December 31, 2023, despite worldwide insured losses of $95 billion, according to Munich Re. We also entered into the LPT with Enstar in May 2022 to limit our exposure to adverse development on the carried reserves for the accident years prior to 2020. This provides substantial ongoing protection against both social and economic inflation, while freeing up capital for our underwriters to deploy into the current attractive pricing environment and allowing our management team to focus on delivering profitable growth from within our continuing lines of business. Our use of ACM is also highly strategic to our business as a tool to manage net line size and overall volatility, while generating more

stable fee income. Over 90% of our fee income is derived from continuous investor relationships of 4+ years or investment structures with multi-year commitments.

_______________

(1)Represents Occurrence Exceedance Probability PML (1-in-250) for all perils worldwide as of January 1.

(2)Guy Carpenter U.S. Property CAT Rate-On-Line Index.

•Improved Operational Efficiency: We have significantly rationalized our operating footprint, reducing our office locations from 43 to 18, while growing our gross written premiums per employee by 25.8% from 2018 to 2023, and driving a reduction in our expense ratio from 32.9% in 2018 to 28.1% in 2023. We continue to invest in operational efficiencies, which we believe will bring meaningful cost benefits in the medium term through traditional operational expense reductions, as well as improvements to our loss ratio achieved through enhanced underwriting systems and data analytics.

•Culture: We have undertaken a transformation so that we can execute our go-forward strategy in adherence with our values. Since Apollo’s acquisition in 2019, to align with our culture and mission, each member of Aspen’s executive team has been newly appointed, through either internal promotions or new external hires. Our culture is defined by our core values to be open minded, to do the right thing, to be in it together, to own it, and to innovate. We empower our decision makers, who bring to bear their expertise for clients, and build our reputation as thought leaders in our market spaces. Our employees are challenged to be not just risk allocators, but considered risk managers who demonstrate underwriting judgment, exercising restraint in soft markets and pursuing growth in favorable market conditions.

The result of this transformation has been a significant shift in our culture, and a strategic repositioning of the underwriting portfolio that is now being reflected in our financial results, providing a dynamic platform on which to execute our go-forward strategy of growing our core lines of business.

Our Business

We manage our underwriting operations as two distinct business segments: Insurance and Reinsurance. We have a diversified yet complementary portfolio across these segments, constructed through the lens of our ‘One Aspen’ approach, where we balance risk on an aggregate basis and tactically deploy capital to the lines of business and platforms that we believe will generate the best returns for the Aspen Group. Our Insurance and Reinsurance segments both leverage third-party capital through ACM, which utilizes our capabilities in the third-party capital space (namely, the Insurance Linked Securities markets) to provide our core Insurance and Reinsurance segments with enhanced capital flexibility and operating leverage.

Our size provides an advantage relative to our larger peers, allowing us to be nimble and decisive; entering, exiting or changing the nature of our underwriting positions faster and with greater precision. For instance, as part of our active portfolio management process for the 2023 planning year, we made the decision to step back from the aviation, space and bloodstock reinsurance markets as we did not see medium-term returns meeting our targets, while also reducing our risk appetite for mortgage reinsurance. In addition, in the Insurance segment we actively managed down from our original 2023 planned growth within selected U.S. management liability and professional liability lines of business, where we have observed a softening rate environment.

The strength of our Insurance and Reinsurance businesses is evidenced by our numerous nominations for industry awards in 2023, including being shortlisted for Insurance Insider’s (Re)insurer of the Year, shortlisted for Insider Honours’ Diversity & Inclusion and Carrier of the Year, and our CEO and Executive Chair, Mark Cloutier, being awarded Inside P&C’s CEO of the Year.

Insurance: Our Insurance segment underwrites primary specialty risks across a diversified set of property and casualty lines of business. We focus on market segments with high barriers to entry that require bespoke underwriting and industry expertise and customized solutions to address client needs. We have long-standing relationships with key distribution partners, primarily comprised of a diversified group of leading retail brokers and wholesale brokers, along with a select number of managing general agents (“MGAs”). We believe our experience in these niche markets has cemented our role as a partner of choice for many of our distributors, as we are able to leverage our capabilities to develop one-stop custom solutions across multiple lines of business, platforms and geographies.

We have niche underwriting capabilities across multiple platforms, including: U.S. admitted lines; U.S. excess and surplus (“E&S”) lines; Lloyd’s; the U.K. Company Market and Bermuda. The breadth of our capabilities across these platforms allows for solutions that can be tailored to our clients’ needs while also allowing us to optimize returns based upon prevailing market conditions.

Specialty is at the heart of our capabilities and product offerings. We define our specialty orientation to include the following:

•Product spaces which are non-commoditized where bespoke underwriting expertise and innate sector knowledge is required and serves as a true differentiator;

•Clients that have complex business challenges requiring customized insurance solutions to fit their specific risk transfer needs; and

•Risks that are underwritten on an individual basis, frequently requiring advanced analysis and modeling as well as specialized active claims management.

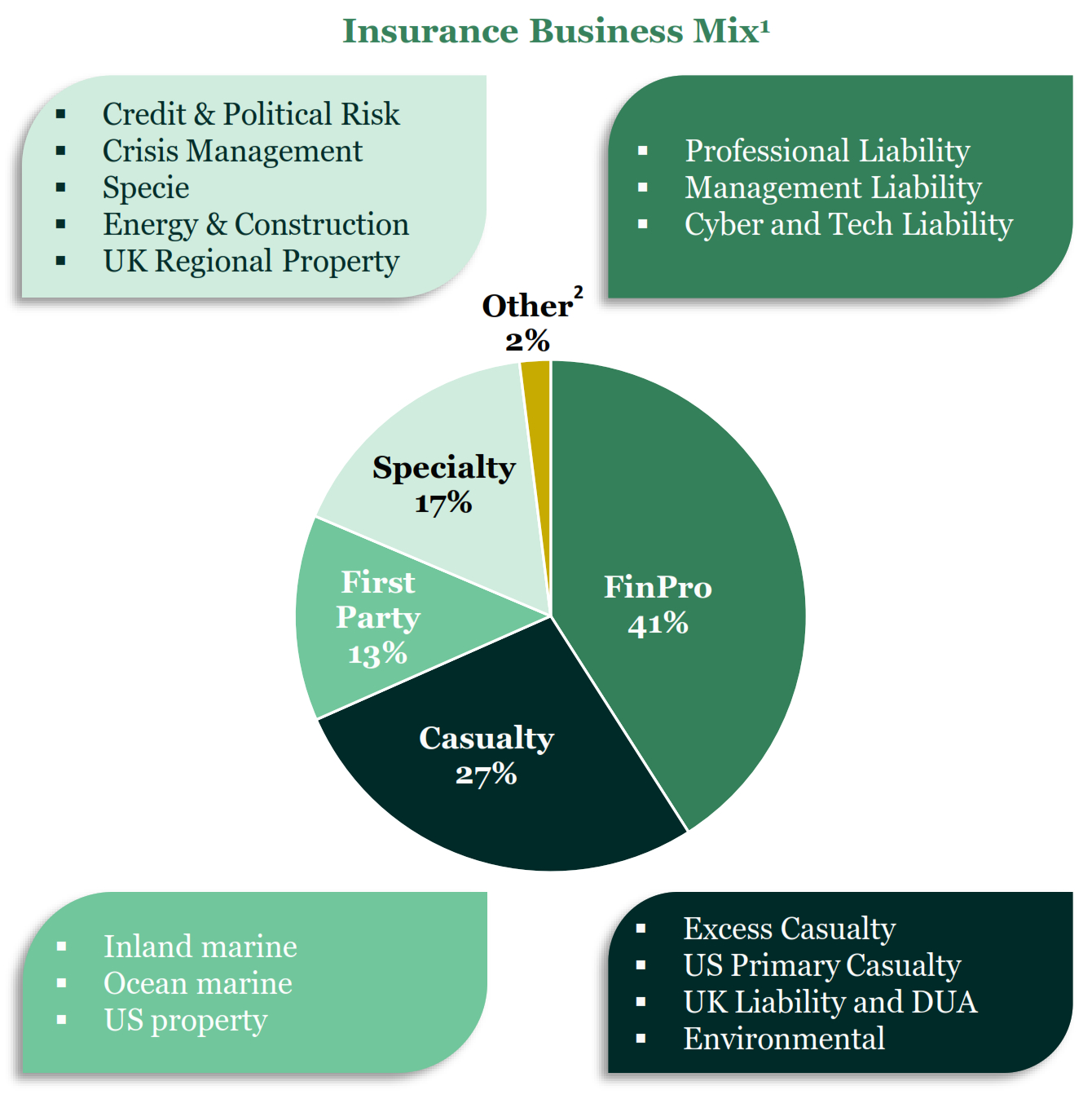

Our Insurance segment is organized into four primary portfolios of business: (1) financial and professional lines; (2) casualty and liability lines; (3) first party lines; and (4) specialty lines. Each portfolio has multiple product offerings which are overseen by experienced teams of underwriters who are experts in their given niche. The

composition of our Insurance product offering is included below with percentages based on gross written premiums for the twelve months ended December 31, 2023.

________________

(1)Percentages represent 2023 gross written premium as a percent of total Insurance gross written premium.

(2)Primarily consists of Carbon Syndicate.

Specific examples of our expertise and differentiated approach across product lines include:

•Specialized Expert Underwriters. We employ underwriters who are experts in their respective fields, with the requisite sector knowledge to best assess, select and price risk. For example, the team that handles our ocean marine product line includes former members of the Merchant Marines; our credit and political risk business is led by former bankers who understand the nuanced complexity associated with credit risk, while our cyber and tech liability teams are trained to field-recognized designations that would traditionally sit outside the insurance industry.

•Customized Product Offering. We have significantly narrowed our focus to concentrate on niche offerings, seeking to underwrite beyond the traditional lines of business that would result in a portfolio that stands and performs as just an index of the market. Examples of some of our specific product offerings include:

◦Credit and Political Risk: Bespoke contracts for complex credit and project finance deals underwritten by an experienced team of underwriters, supported by dedicated in-house credit analysts, offering one of the widest product suites in the market;

◦Cyber and Tech Liability: A team of global underwriters providing robust risk selection capabilities, who are all required to pass a credentialed network security exam (Certified Information Privacy Professional or Certified Information Privacy Technologist) to ensure consistent risk assessment expertise across the team;

◦Environmental: Specialist liability products to mitigate the financial impacts of environmental financial claims with a team of over 25 underwriters with experience across law, engineering,

consulting and risk management, that provide global capabilities from eight cities around the world;

◦Inland Marine: Within this business line, we underwrite both fine arts and construction. Fine arts is underwritten by a dedicated underwriting team with members having over ten years of experience on average. Our construction team has industry relationships with Engineering News Record Top 25 General Contractors, supported by an on-staff engineer, who provides clients access to risk control review, industry recommendations and best practice health checks;

◦U.K. Property & Construction: Structured as three underwriting teams across property investors, business & public sector, and construction, our U.K. property & construction team excels at unusual and special circumstances. We work in collaboration with our U.K. & international casualty underwriters to provide cross-class solutions for our clients and broker partners; and

◦U.S. Management Liability: A portfolio tactically balanced between open market writings (with greater exposure to fluctuations in market conditions) and delegated underwriting authority business in the small and midsize enterprise space (which is more stable and less price sensitive). As a subset of our management liability portfolio, transactional liability is a true specialty class where we have long-standing partnerships with two of the most respected underwriting facilities in the market, Ambridge Partners and Euclid Transactional.

•Tailored Portfolio Solutions. We have designed bespoke portfolio solutions across multiple lines of business for a number of our long-term trading partners. We continue to leverage our multiple operating platforms, bringing the ‘One Aspen’ approach to market, where our Reinsurance and ACM capabilities facilitate support of and alignment with our Insurance offerings. An example of this is a binder agreement we have with a leading wholesaler, whereby we provide underwriting capacity to multiple specialty programs across both the United States and Europe, utilizing our multiple operating platforms.

This approach has been the foundation for establishing a long-term track record of underwriting profitability across numerous lines of business. Aspen’s insurance segment includes a number of highly specialized lines of business that have returned favorable combined ratios across the cycle, highlighting the strength and niche nature of this business. We strive to maintain this caliber of underwriting performance in these lines, while building our track record within our other primary insurance lines of business.

For the twelve months ended December 31, 2023, our Insurance segment had $2,447 million of gross written premiums, generated $113 million of underwriting income and had a combined ratio of 92.3%. For the five-year period 2018 to 2023, continuing lines gross written premiums within our Insurance segment grew at a CAGR of 9.5% (with annual growth rates of 8.0%, 9.7%, 22.7%, 11.0% and (2.3)% for 2019, 2020, 2021, 2022 and 2023, respectively). There can be no assurance that such growth trends will continue.

Reinsurance: Within this segment, we offer expertise in a variety of global reinsurance lines including property catastrophe reinsurance, other property reinsurance, casualty reinsurance, and specialty reinsurance. We implement a simple, yet effective, distribution model targeting long-term relationships and product spaces that have demonstrated strong underwriting returns through market cycles. Our focus goes beyond traditional reinsurance, as we seek to provide our clients with innovative solutions, through both traditional retrocession, and the utilization of third-party capital through ACM alongside our own Aspen balance sheet capital. We are opportunistic yet disciplined in our approach, positioned to benefit from market dislocations and underwriting modest lines to reduce volatility from loss events with the aim of generating highly attractive risk-adjusted returns, as opposed to returns that just track the market index.

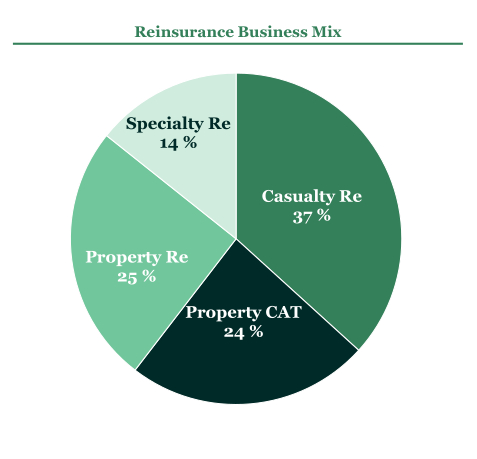

Our Reinsurance segment is organized into four portfolios: (1) property catastrophe reinsurance; (2) other property reinsurance; (3) casualty reinsurance; and (4) specialty reinsurance.

•Property Catastrophe Reinsurance: Our success in the property catastrophe market is based on strong risk controls and deep, embedded relationships with our clients, giving us differentiated insights to manage exposures. We utilize advanced models, analytical tools and our experienced global underwriting teams to

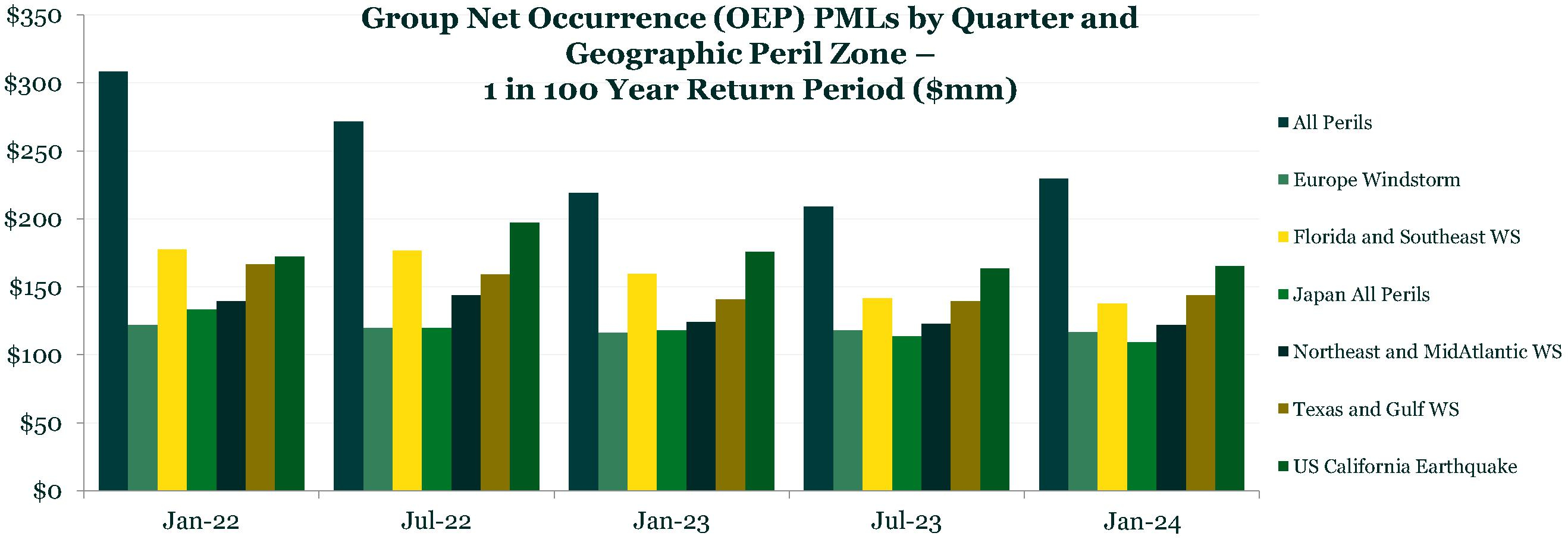

set terms and deliver timely capacity. Our opportunistic strategy in this line has allowed us to take advantage of a hard market cycle, using price increases, improvement in terms and ACM to enhance our underwriting margins and reshape our exposures. Importantly, we have used the hard market conditions not just for premium growth, but to reduce volatility, as evidenced by a significant reduction in PMLs from 2018 to 2023.

•Other Property Reinsurance: We provide tailored solutions for a broad spectrum of property risks worldwide through our dual distribution approach, writing business both directly to ceding firms and through brokers.

•Casualty Reinsurance: Our casualty treaty team operates on a global basis, and our analysis of market-wide trends in key territories, supported by close coordination with our claims, legal and actuarial teams, gives us insights that we believe will enable us to succeed in the changing liability landscape.

•Specialty Reinsurance: We target niche or unusual risks and are focused on offering tailor-made risk transfer solutions for several specialty lines. We believe our global expertise is well recognized and our team of underwriters across London, Singapore, Zurich and the United States give us valuable regional and global expertise to support our clients.

The composition of our Reinsurance business mix based on gross written premiums for the twelve months ended December 31, 2023 is included in the following chart:

For the twelve months ended December 31, 2023, our Reinsurance segment had $1,521 million of gross written premiums, generated $214 million of underwriting income and had a combined ratio of 81.4%. For the five-year period 2018 to 2023, continuing lines gross written premiums within our Reinsurance segment grew at a CAGR of 7.2% (with annual growth rates of 0.9%, 19.9%, 22.3%, 13.0% and (15.3)% for 2019, 2020, 2021, 2022 and 2023, respectively). There can be no assurance that such growth trends will continue.

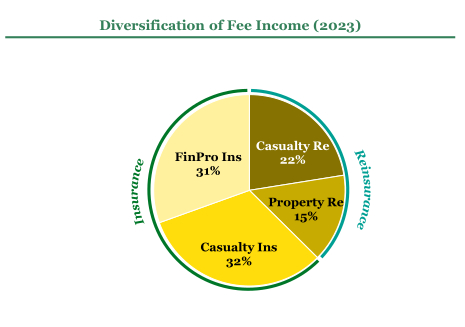

ACM: We participate in the alternative reinsurance market through ACM, which acts as a conduit between Aspen’s balance sheet and third-party investors and supports each of our Insurance and Reinsurance segments. Through reinsurance sidecar investments, ACM provides investors direct access to our underwriting expertise and earns underwriting, management and performance fees for Aspen from other third-party investors primarily through the placement and management of sidecars, insurance linked securities (“ILS”) funds and other offerings. ACM is highly strategic to our business, providing a unique set of capabilities and tactical optionality to manage risk and improve our returns. Unlike other offerings in the market that are predominantly property catastrophe reinsurance focused, ACM offers investors a broader product suite that provides direct, fully aligned participation to risk

underwritten by Aspen’s primary specialty insurance and reinsurance portfolios, including actively managed fund products and sidecars. Notably, ACM’s capabilities in longer-tail lines of business bring greater stability to our fee income, and thus our underwriting results, as this fee income is associated with “stickier” third-party capital structured over multiple years. As of December 31, 2023, approximately 55% of third-party capital within ACM supported longer-tail products.

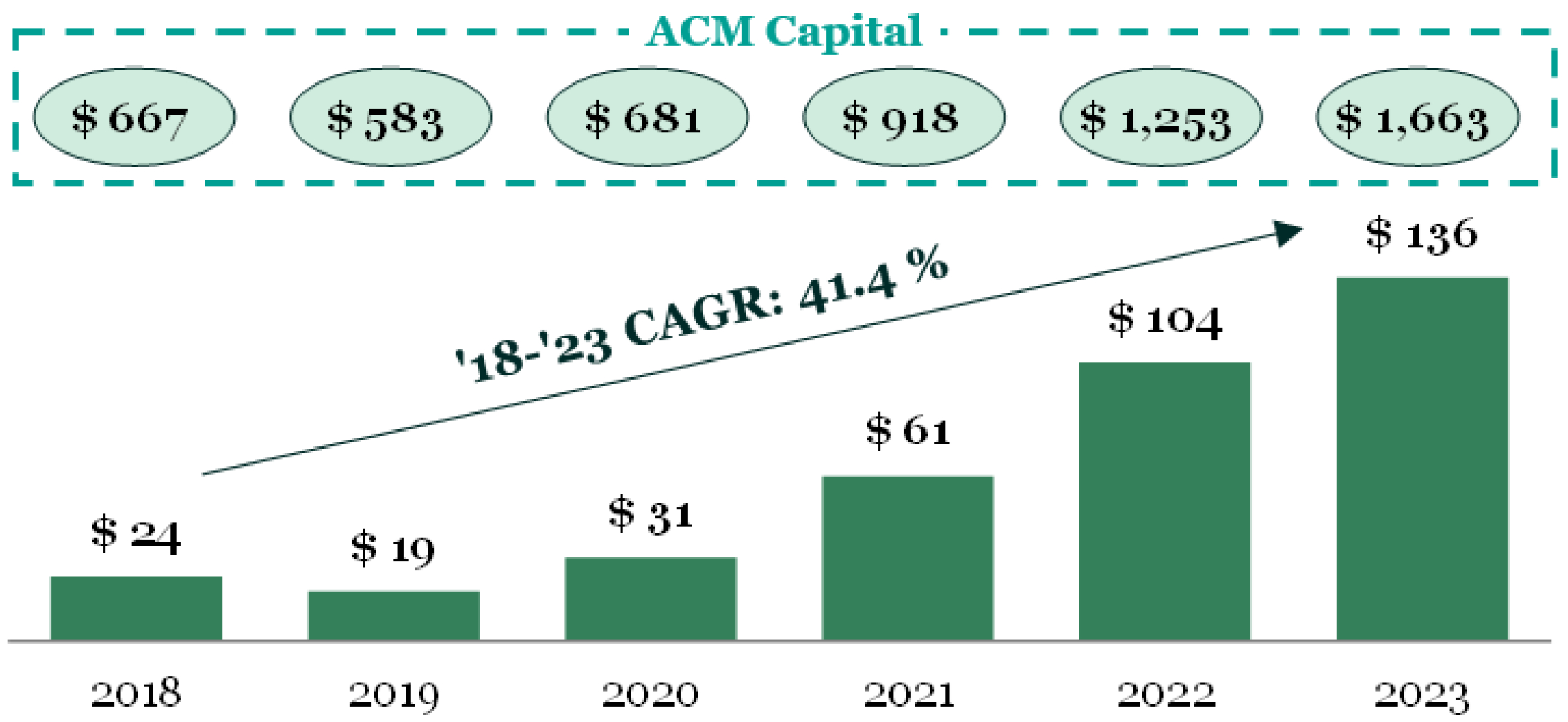

ACM is a core differentiator for Aspen, bringing our expertise in capital markets alongside that of our traditional outwards reinsurance capabilities, providing us with increased optionality across cycles in terms of access to capital, complementing our dynamic capital allocation approach. The ACM portfolio generally mirrors our own through collateralized quota share arrangements that provide third-party investors with aligned participation to our Insurance and Reinsurance underwriting. ACM is recognized as an innovator across both catastrophe and non-catastrophe risks and was one of the leaders in developing ILS capabilities for cyber risk. Our strong relationships and reputation in the market have enabled ACM to achieve significant growth since 2018, including in recent years where many insurance capital markets players reduced capacity. The following charts reflect the fee income generated by ACM for each of the twelve months ended December 31, 2018 through December 31, 2023, and the diversification of ACM’s fee income for the twelve months ended December 31, 2023.

ACM generated $135.5 million in fee income for the twelve months ended December 31, 2023. For the five-year period from 2018 to 2023, fee income grew at a CAGR of 41.4% (with annual growth rates of (22.9)%, 67.6%, 98.1%, 69.2%, and 30.4% for 2019, 2020, 2021, 2022 and 2023, respectively). There can be no assurance that such growth trends will continue. This fee income is primarily reflected as an offset to our acquisition costs and is therefore embedded in our underwriting results. For the five-year period from 2018 to 2023, third-party capital grew at a CAGR of 20.0% (with annual growth rates of (12.6)%, 16.8%, 34.8%, 36.5% and 32.7% for 2019, 2020, 2021, 2022 and 2023, respectively). There can be no assurance that such growth trends will continue.

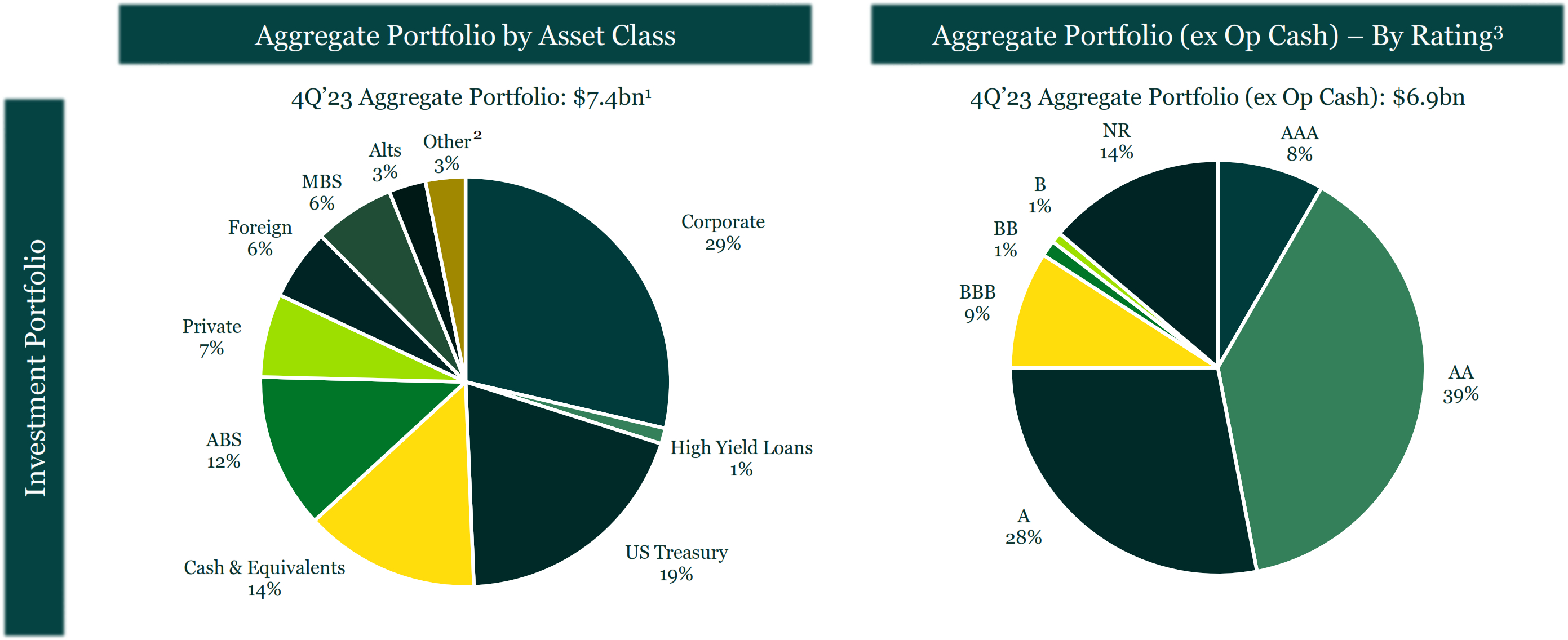

Investments: Our investment strategy is focused on delivering stable investment income and total return through all market cycles, while maintaining high credit quality and portfolio liquidity. We manage a conservative investment portfolio that is appropriately balanced between our liquidity needs and investment returns, with an average credit rating of AA- and duration of 2.6 years of fixed income securities within our portfolio, as of December 31, 2023. We have access to world-class investment managers and execute this strategy through thoughtful allocations of investment assets to our key investment management partners.

To enhance investment returns, we tactically calibrate asset allocation and the duration of our investment portfolio, taking into account the duration of our insurance and reinsurance liabilities, as well as our view of interest rates, the yield curve, credit spreads and other general market conditions. In recent years we have diversified the range of asset classes in which we invest to include collateralized loan obligations, broadly syndicated loans, private credit, real estate equity and debt, private equity related infrastructure investments, high yield bonds and leveraged loans. We hold these investments directly or through fund vehicles. As of December 31, 2023, we allocated $1.8 billion (24%) of our investment portfolio to these asset classes. Apollo Asset Management Europe PC LLP

(“AAME”) manages $1.6 billion (22%) of these asset classes with the remainder managed by other third party managers.

As of December 31, 2023, we had $7.4 billion of total cash and investments, excluding catastrophe bonds, net receivables for securities sold and accrued interest receivable, on our balance sheet and for the twelve months ended December 31, 2023, we generated $276 million of net investment income.

________________

(1)Excludes catastrophe bonds, net receivables for securities sold and accrued interest receivable.

(2)Other includes U.S. Agency, Municipals and short-term investments.

(3)Based on the Bloomberg Barclays Rating Methodology.

For more information on our aggregate portfolio reflected in the chart above (including the characterization of our investments as available for sale and trading), please refer to “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Balance Sheet—Total cash and investments.”

Our Competitive Strengths

We believe that our competitive strengths include:

‘One Aspen’ Approach, Supported by Dynamic Capital Allocation

Through our ‘One Aspen’ approach, we can actively manage our portfolio across counter-cyclical pricing environments in the insurance and reinsurance markets, shifting capital between our two segments and being opportunistic in markets where we perceive advantageous risk versus return opportunities. The markets we serve require capabilities that are not easily replicated and we come to market in a way that allows us to bring our product offerings together and execute on large new deals across different lines of business, platforms and segments. This provides us with greater control over capital allocation and underwriting outcomes, and is a key pillar of our go-forward offering and growth strategy.

Our operating and risk allocation strategy has been carefully designed to optimize the use of both our own assets, as well as third-party capital. Business sourced is carefully analyzed and directed to the appropriate underwriting platform, taking into account client characteristics, as well as operational and efficiency considerations. We have a scaled but nimble (re)insurance presence across the most important global underwriting hubs for our lines of business, including the U.S. admitted, U.S. E&S, Bermuda, Lloyd’s and the U.K. Company Market, all leveraging our third-party capital markets capabilities (through ACM).

Niche Primary Insurance Platform

Our insurance strategy is focused on underwriting complex, highly curated, niche lines of business with high barriers to entry. Our Insurance segment generated $2,447 million in gross written premiums for the twelve months ended December 31, 2023. We only participate in lines of business in which our underwriters have deep, technical expertise and where they can be well supported by our platforms and strong capabilities, allowing us to provide innovative and coordinated solutions to clients. From 2018 to 2023, we experienced aggregate rate increases of 66.4% in our portfolio, driven by pricing improvements from our core lines of business. We adopt an efficient tactical use of outwards reinsurance, enabling us to write higher exposure policies while appropriately managing our net retained exposure.

Since being acquired by Apollo, we have exited a number of lines of business (legacy business) while also achieving strong growth in our continuing lines of business generating attractive profitability. The gross written premiums CAGR within these continuing lines of business has been 9.5% since 2018 (with annual growth rates of 8.0%, 9.7%, 22.7%, 11.0% and (2.3)% for 2019, 2020, 2021, 2022 and 2023, respectively). There can be no assurance that such growth trends will continue. The combined ratio has improved from 99.1% in 2018, to 92.3% in 2023.

Opportunistic Specialist Reinsurance Franchise

We have built a nimble reinsurance strategy focused on core lines of business within property, casualty and specialty. Our Reinsurance segment generated $1,521 million in gross written premiums for the twelve months ended December 31, 2023 and is positioned to capitalize on dislocation within a broad set of markets. Our strategy is to underwrite modest line sizes to limit exposure from large loss events, and our property catastrophe portfolio has been optimized to generate higher risk-adjusted returns and manage overall volatility. The gross written premiums CAGR within these continuing lines of business has been 7.2% since 2018 (with annual growth rates of 0.9%, 19.9%, 22.3%, 13.0% and (15.3)% for 2019, 2020, 2021, 2022 and 2023, respectively). There can be no assurance that such growth trends will continue. The combined ratio has improved from 104.7% in 2018, to 81.4% in 2023.

Our opportunistic approach has allowed us to take upside from attractive reinsurance underwriting conditions, where we have experienced strong rate increases in a hard market cycle. We have experienced cumulative rate increases of 70% from 2018 to 2023. We continued to benefit from an attractive pricing environment with a rate increase of 8.1% on 2024 renewed premium for existing policies that were renewed from January 1, 2024 through January 31, 2024. Our strength in reinsurance is bolstered through the deployment of third-party capital through ACM, which provides us with differentiated access to capital and allows us to “flex” into attractive market opportunities.

Growing and Highly Complementary Capital Markets Business

Since its inception in 2013, ACM uses our capabilities in the third-party capital markets, to increase the flexibility Aspen’s Insurance and Reinsurance underwriters have in allocating risk to the best source of capital. ACM leverages the full breadth of our expertise across distribution, underwriting, modelling, actuarial and claims, to create attractive opportunities for our investor partners. ACM has experienced significant growth, with third-party capital growing from $667 million in 2018 to $1,663 million at the end of 2023, and generating $136 million in fee income for Aspen in 2023. We believe we have driven innovation in this market and have cultivated close relationships with third-party capital investors. ACM is a differentiated capability and highly strategic to our business, allowing us to support our Insurance and Reinsurance segments with third-party capital, and serving as a mechanism for tactical de-risking as we leverage fee income from our on-balance sheet underwriting risk. This capability provides us with the ability to “flex” into attractive opportunities in accordance with underwriting cycles and enhances our go-to-market strategy.

Deep Trading Partner Relationships

We have seasoned and diversified relationships with partners across our (re)insurance segments. The distribution strategy within our Insurance segment is focused on specialized intermediaries with whom we have long-standing relationships. Our distributors are experts in their field and know our products and risk appetite well.

We have flexibility across retail brokers, wholesale brokers and MGAs to drive value and maintain deep relationships without being overly reliant on any one large partner. Our Reinsurance segment is characterized by the longevity of our relationships with cedants, with 89% of premium for underwriting year 2023 having been written with cedants who have maintained their reinsurance relationship with us since 2013. We believe we are viewed as a strong, reliable counterparty.

Strong Balance Sheet

We have an efficient capital structure and strong capitalization with $3,209 million of total capital as of December 31, 2023. Additionally, we have strong financial strength ratings from both A.M. Best Company, Inc. (“A.M. Best”) (“A”) and Standard & Poor’s Financial Services LLC (“S&P”) (“A-”) and maintain Group BMA Bermuda Solvency Capital Requirement (“BSCR”) of 237% as of December 31, 2022. We maintain our Group BMA BSCR significantly in excess of regulatory minimums.

The strength of our balance sheet and underwriting platform is supported by the LPT transaction with Enstar, which provides protection against deterioration on 2019 and prior accident year carried reserves, significantly limiting Aspen’s exposure to the risk of unfavorable development from these accident years while still retaining the scale, market relationships, and operational infrastructure to capitalize on current market conditions to continue to grow our business. The following chart shows our pre-2020 accident year carried reserves, as well as the LPT coverage above such carried reserves, as of September 30, 2021 and December 31, 2023.

Highly Experienced Management Team

Led by our CEO and Executive Chair, Mark Cloutier, we have an experienced executive leadership team from diverse backgrounds, each with a specific role and purpose to drive the transformation of our business. Since Apollo’s acquisition in 2019, to align with our corporate culture and mission, each member of Aspen’s executive team has been newly appointed, through either internal promotions or new external hires. Our team has an average of 28 years of experience across all facets of the global specialty property & casualty (re)insurance and financial services sectors, including underwriting, claims, technology, investment management, risk management, finance, brokering, actuarial, people and operations.

Our Strategy

As an institution we aim to bring “Clarity from Complexity.” We seek to transform complex risks into opportunities through efficient and innovative solutions, leveraging our multi-platform capabilities across our Insurance and Reinsurance segments, both of which are supported by ACM. We believe we are a market leader in our industry that provides our clients with confidence and the best possible outcomes. Our culture, which prioritizes collaboration, accountability and service, allows us to provide intelligent, swift solutions in the face of challenges. Whatever the challenge is, we are ‘One Aspen’.

Our vision statement is ‘to be a top quartile specialty risk (re)insurer focused on total value creation through underwriting profit and investment performance.’ Our ability to achieve this goal is based on three key pillars, which we believe create a virtuous cycle for success:

1.Sustained Profitability: This encompasses several items, including profitable growth, delivering consistent results, managing Funds at Lloyd’s (as defined below) and efficiently allocating capital, retaining agility and embedding cross functional collaboration. These goals all highlight the importance of financial success and sound risk management for Aspen.

2.Brand Strength and Market Presence: This priority relates to being a partner of choice, easy to transact with, a provider of creative solutions and outstanding service and our use of data and analytics to improve performance and service and a healthy control environment.

3.Employer of Choice: Talent development, leadership, and building a strong, engaged workforce are emphasized throughout Aspen. Improving the effectiveness of the Group Executive Committee (the “Group Executive Committee”), managing people and communication implications, and developing a sustainable model all point to the importance of investing in human capital and fostering a positive work environment.

Our technology strategy is underpinned by our mission to underwrite excellent business and to automate and digitize operations from ingestion to downstream functions. As part of our strategy, we amplify underwriting and claims results through the use of data and technology insights. Underlying data is key to our decision making and we have extensively invested in enterprise-wide data and analytics capabilities. We are transitioning to a single, comprehensive enterprise-wide data repository, built on over 20 years of underwriting history, which we expect will form the foundation for our reporting, business intelligence, analytics and other advanced data capabilities. We believe this agile platform will allow us to develop our real time access to analytics and provide us with an advantage in managing our risk and better claims / portfolio management. In addition, we have invested in a variety of application programming interface and cloud capabilities, which give us greater flexibility in integrating our multi-national underwriting operations and leveraging software as a service and third-party data sources to ensure a competitive advantage.

Underpinning all of this is our ability to maintain a strong balance sheet and manage our capital prudently. We have a highly efficient capital structure and our capitalization is strong, as evidenced by our strong financial strength ratings. We are constantly monitoring rating agency guidelines, changes in our regulatory environment and market opportunities to ensure that our capital structure is appropriate for our strategic ambitions. We maintain robust procedures for setting loss reserves and actively managing risk in our portfolio. Our reserve confidence was further strengthened by the previously mentioned LPT transaction executed in May 2022. In today’s attractive underwriting environment, we see ample opportunity to deploy excess capital into both our Insurance and Reinsurance segments, but through the cycle we may return capital to shareholders when opportunities are limited during soft insurance markets. See “Dividend Policy.”

We are guided by the phrase “One Aspen Team, Creating Value,” which is underpinned by our core set of values – to be open minded, to do the right thing, to be in it together, to own it, and to innovate. We have built

Aspen’s culture around these guiding principles to foster an environment that promotes innovation, collaboration, inclusiveness and accountability.

Our Markets and Opportunity

We operate within the global (re)insurance market, where we have significant opportunities to capture attractive risk-adjusted returns across the cycle through our multi-platform capabilities. The global macroeconomic and social environment continues to drive demand for increasingly complex (re)insurance solutions delivered as a joined-up offering, which is where we thrive. In recent years, rate increases have been driven by the increased frequency and severity of natural catastrophe events globally (impacted by changing weather patterns), inflation (both social and economic), increased geopolitical tensions and other risks that have grown and emerged, increasing the demand for specialty solutions. As a result, the global commercial insurance industry has seen 25 consecutive quarters of price increases according to Marsh’s Global Insurance Market Index Q4’2023.

We expect these hard market conditions will persist, as they are driven by uncorrelated and continuing macroeconomic and social dynamics. This will provide opportunities for us to deliver profitable growth as we target new business and clients at favorable rates and with improved terms and conditions, while maintaining disciplined risk selection. Furthermore, our chosen lines of business within Insurance have high barriers to entry requiring the bespoke tailoring of products and the need for specialized and experienced underwriters with tenured distribution relationships.

The higher interest rate environment provides additional tailwinds for our business. Higher returns from our fixed income portfolio complement our underwriting income with attractive investment income and contribute to our ability to generate strong risk-adjusted returns for our shareholders. With a low-risk fixed income portfolio of relatively short duration 2.6 years as of December 31, 2023, we are well placed to take advantage of attractive investment yields as we rotate and reinvest.

Global Insurance Market

Within Insurance, we operate within both the U.S. specialty and international insurance markets.

U.S. Specialty

Aspen operates within the broadly defined U.S. commercial lines market, which generated annual industry direct premiums of approximately $474 billion as for the twelve months ended December 31, 2023. The industry has experienced improved underwriting performance following the COVID-19 pandemic and wider economic uncertainty. Within commercial insurance, the excess and surplus (“E&S,” “non-admitted” or “surplus lines”) market has demonstrated strong growth, with highly attractive rate increases and improvement in terms and conditions. For the twelve months ended December 31, 2023 we wrote $879 million of gross premiums in the E&S market. A.M. Best estimates that this market segment is approaching $100 billion in annual premiums, nearly doubling since 2018. Driving this growth is the macroeconomic and social environment and challenges within the

admitted space, which continues to drive demand for specialized insurance solutions due to both increasing and more complex risks from the commercial market.

E&S carriers are generally permitted to craft insurance terms to suit the particular risk they are assuming as the underlying risks tend to have unique qualities. Consequently, in this space we are able to provide tailored contracts and limit exposure to loss by either excluding coverage or providing a sub-limit on coverage. This customized approach provides the opportunity to achieve attractive long-term profitability. E&S combined ratios have outperformed admitted combined ratios by approximately 3% on average from 2018 through 2022, according to A.M. Best.

We underwrite business in the United States through Aspen American Insurance Company and Aspen Specialty Insurance Company on an admitted and E&S basis, respectively. For the twelve months ended December 31, 2023, we generated $879 million and $863 million of gross written premiums in the U.S. E&S and admitted markets, respectively.

International Insurance

Our international insurance products are underwritten in the London Market, through both our Lloyd’s and U.K. Company Market platforms.

Lloyd’s is a competitive insurance market where individual underwriters accept risks on behalf of groups, called syndicates, of individual and corporate members whose resources provide the security behind Lloyd’s policies. Lloyd’s is the world’s largest specialty insurance marketplace, underwriting £52 billion of premiums during the twelve months ended December 31, 2023, up 12% from the same period in the prior year. The Lloyd’s global distribution network is where many of the world’s most complex risks are placed, across more than 60 specialty lines of business. Over 50 leading insurance companies participate in the market with more than 380 registered Lloyd’s brokers and a global network of over 4,000 local coverholders. We have a significant presence at Lloyd’s through our integrated Lloyd’s vehicle, comprising Syndicate 4711, managed by AMAL with fully aligned capital, which in addition to access to complex risks also provides us (re)insurance licensing access for 80 territories (and an additional 20 territories on a reinsurance only basis) across the Americas, the United Kingdom, Europe, and Asia Pacific. AUL, as the sole corporate member of Syndicate 4711, must deposit sufficient capital to support its underwriting at Lloyd’s. For the twelve months ended December 31, 2023, AUL supported capacity of £1,115 million on Syndicate 4711. Aspen is well positioned within Lloyd’s, with Syndicate 4711 having a reported combined ratio of 86.7% for 2023 and increased underwriting capacity for 2024. For the twelve months ended December 31, 2023, we wrote $1,054 million of gross premiums in the Lloyd’s market.

The U.K. Company Market is an important market for global specialty insurance, with companies and individuals worldwide turning to this market to protect against niche and hard-to-place risks, ranging from liability and professional lines, to cyber and renewable energy exposures. Gross premium written in this market stood at £44 billion in 2023 up 34% from £33 billion in 2020. While there is no standard definition of this market, there is a general agreement that the core of its activity is internationally traded non-life, commercial and specialty insurance and reinsurance business written by standalone insurers operating outside Lloyd’s, but within its wider ecosystem. This is mostly P&C (re)insurance, with an increasing emphasis on high-exposure risks. The diversity and expertise of insurers and underwriting talent, as well as the ecosystem of service providers, make this a highly attractive market to write our U.K.-centric lines of business. We write business in this market through Aspen Insurance UK Limited. For the twelve months ended December 31, 2023, we wrote $320 million of gross written premiums in this market.

Global Reinsurance Market

The global reinsurance market has approximately $670 billion of capital committed as of December 31, 2023, a decrease of 0.7% from December 31, 2021. We believe the market is witnessing an opportunity for margin expansion. There is a supply and demand imbalance in global reinsurance due to limited new capacity entering the market, retreating rated reinsurers, reduced ILS capacity for traditional property catastrophe focused managers, increased exposure from inflation, and reduced capital positions as a result of unrealized losses on fixed income portfolios. While the opportunity is currently led by property catastrophe pricing, which has seen an approximately

29% increase in rates in 2023 according to Guy Carpenter’s Global Property Rate-On-Line Index, along with significantly better terms and conditions and primary retention, there remains broader opportunity to cross sell to quality, non-retreating carriers. Our global underwriting platforms in reinsurance, and differentiated, diverse ACM capabilities provide us with an opportunity to react quickly to market conditions and benefit from the current market cycle.

Our Reinsurance business segment is underwritten through four core platforms, which include AAIC, Aspen UK, Syndicate 4711 and Aspen Bermuda, and our branch offices including our European hub in Zurich and Asia Pacific hub in Singapore. For the twelve months ended December 31, 2023, we wrote $1,521 million of gross written premiums in the reinsurance market.

Our Sustainability Principles

Our goal is to be a diverse and inclusive business, providing strong risk-adjusted returns as we work towards a goal of having a deep sense of social responsibility, whether that be supporting the local communities in which we operate or proactively managing the environmental footprint of our direct operations. Sustainability and Environmental, Social and Governance (“ESG”) are closely linked, and we expect to play our part pragmatically in the transition to net zero. Our vision is to bring “Clarity from Complexity” and this is reflected in the approach we take and how we deliver our long-term objectives in respect of sustainability. We believe our heritage of deep sector expertise, strong culture and our proven ability to apply the full breadth of our capabilities to solve problems created by new and changing risks, makes us uniquely positioned to be a relevant partner as the energy and other sectors work towards this transition. Our philosophy is centered around three pillars:

1.Environmental: We have calculated our Scope 1, Scope 2 and, in relation to certain categories, Scope 3 greenhouse gas emissions utilizing estimates, methodologies and conversion factors aligned to the Greenhouse Gas Protocol for our industry. As we work towards carbon reductions across our value chain, we also make use of offsetting projects accredited by the Verified Carbon Standard (“VCS”) and Gold Standard (“GS”) to compensate for 100% of our Scope 1 and 2 greenhouse gas emissions, along with all calculated Scope 3 categories (i.e., fuel and energy related activities, waste generated in our operations, business travel and employee commuting (including working from home)) directly relating to our employees. We plan to continue our carbon offsets program to continue addressing our overall carbon footprint. Our sustainability development and focus is enabling us to be more data-led when determining projects to fund, where we invest and how to consider clients’ sustainability in our underwriting;

2.Social: Our policies are designed to empower our staff to support their own charitable passions, with the goal of providing opportunities for future success in our global and local communities. We develop collaborative engagement with our employees and our third sector partners, instilling a sense of pride in current staff and building a platform to attract future talent. In tandem with attracting talent, we have a clear workplan that is led by people from across our business and championed by executive sponsors to foster a diverse and inclusive culture; and

3.Governance: In an age of increased risks, we employ a comprehensive risk management framework, which provides the foundation through which we evaluate and manage business opportunities and related risks in a disciplined manner across the Group. Strong governance is the bedrock of our focus on offering value to our clients, employees and communities around us and we have a clear structure in place to deliver on this.

Summary Risk Factors

Investing in our ordinary shares involves risks. Prospective investors should carefully consider the risks described in “Risk Factors” below, as well as other information contained in this prospectus before making a decision to invest in our ordinary shares. Any of the factors set forth under “Risk Factors” could materially adversely affect our business, financial condition, results of operations or cash flows and could impact any forward-looking statements. Prospective investors should note that such risks are not the only ones we face. Additional risks

and uncertainties not currently known to us or that we currently deem to be immaterial may also materially and adversely affect us in the future. Among these important risks are the following: