Exhibit 99.1

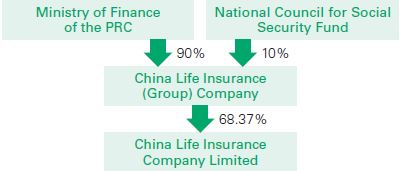

The Company is a life insurance company established in Beijing, China on 30 June 2003 according to the Company Law and the Insurance Law of the People’s Republic of China. The Company was successfully listed on the New York Stock Exchange, the Hong Kong Stock Exchange and the Shanghai Stock Exchange on 17 and 18 December 2003, and 9 January 2007, respectively. The Company’s registered capital is RMB28,264,705,000.

The Company is a leading life insurance company in China and possesses an extensive distribution network comprising exclusive agents, direct sales representatives, and dedicated and non-dedicated agencies. The Company is one of the largest institutional investors in China, and becomes one of the largest insurance asset management companies in China through its controlling shareholding in China Life Asset Management Company Limited. The Company also has controlling shareholding in China Life Pension Company Limited.

Our products and services include individual life insurance, group life insurance, and accident and health insurance. The Company is a leading provider of individual and group life insurance, annuity products and accident and health insurance in China. As at 31 December 2019, the Company had approximately 303 million long-term individual and group life insurance policies, annuity contracts, and long-term health insurance policies in force. We also provide both individual and group accident and short-term health insurance policies and services.

CONTENTS

| 01 PRELUDE | ||||

Core Competitiveness | 4 | |||

Honors and Awards | 5 | |||

Business Highlights | 7 | |||

Financial Summary | 8 | |||

| 02 CHAIRMAN’S STATEMENT | ||||

Chairman’s Statement | 12 | |||

| 03 MANAGEMENT DISCUSSION AND ANALYSIS |

| |||

Review of Business Operations in 2019 | 18 | |||

Business Analysis | 21 | |||

Analysis of Specific Items | 29 | |||

Technological Empowerment and Operations and Services | 32 | |||

Performance of the Corporate Social Responsibility | 34 | |||

Future Prospect | 34 | |||

| 04 EMBEDDED VALUE |

| |||

Embedded Value | 35 | |||

| 05 SIGNIFICANT EVENTS |

| |||

Material Litigations or Arbitrations | 41 | |||

Major Connected Transactions | 41 | |||

Material Contracts and Their Performance | 52 | |||

Undertakings | 53 | |||

Restriction on Major Assets | 53 | |||

Targeted Poverty Alleviation | 53 | |||

Others | 53 | |||

| 06 CORPORATE GOVERNANCE |

| |||

Report of the Board of Directors | 56 | |||

Report of the Board of Supervisors | 64 | |||

Changes in Ordinary Shares and Shareholders Information | 67 | |||

Directors, Supervisors, Senior Management and Employees | 71 | |||

Report of Corporate Governance | 86 | |||

| 07 FINANCIAL REPORT |

| |||

Independent Auditor’s Report | 120 | |||

Consolidated Statement of Financial Position | 127 | |||

Consolidated Statement of Comprehensive Income | 129 | |||

Consolidated Statement of Changes in Equity | 131 | |||

Consolidated Statement of Cash Flows | 132 | |||

Notes to the Consolidated Financial Statements | 134 | |||

| 08 OTHER INFORMATION |

| |||

Basic Information of the Company | 258 | |||

Index of Information Disclosure Announcements | 261 | |||

Definitions and Material Risk Alert | 264 | |||

1

2

3

China Life Insurance Company Limited Annual Report 2019

Prelude

Core Competitiveness

Long history and excellent brand | The predecessor of the Company, one of the first batch of enterprises to underwrite insurance business in China, was approved by the Chinese Government for establishment in October 1949, when the People’s Republic of China was founded. After the restructuring and reorganization, the Company was successively listed home and abroad, becoming the first financial insurance enterprise in China triple-listed on the Shanghai Stock Exchange, the Hong Kong Stock Exchange and the New York Stock Exchange. Since its establishment, the Company has played the role of an explorer and pioneer in China’s life insurance industry, and has committed to creating a world-class financial insurance brand. Through long-term and continuous brand building, China Life has become one of the famous and strong brands in the world with growing brand value and influence. As at the end of 2019, the brand of China Life has been selected as one of the “World’s 500 Most Influential Brands” published by World Brand Lab for thirteen consecutive years, ranking 132nd in 2019, and was again ranked 5th on the 2019 (the 16th session) “China’s 500 Most Valuable Brands” list published by World Brand Lab. | |||||||

| ||||||||

Prominent principal business and sound financial strength | The Company sticks to its principal business, further explores the huge potentials of the life insurance market, and maintains its leading position in China’s life insurance market. In 2017, the Company’s gross written premiums exceeded RMB500,000 million, achieving a new record high. Through the long-term development and accumulation, China Life has solid financial strength comparable to world-class enterprises in the world. As at 31 December 2019, the Company’s total assets amounted to RMB3,726,734 million, leading the life insurance industry in China. As one of the largest institutional investors in China, the Company becomes one of the largest insurance asset management companies in China through its controlling shareholding in China Life Asset Management Company Limited. As at the end of 2019, the total market capitalization of the Company was USD124,913 million. | |||||||

| �� | ||||||||

Well- established network and leading technologies | The Company has a sound institutional and services network, with its business outlets and services counters covering both urban and rural areas. As at the end of the Reporting Period, the number of sales force from all channels of the Company was 1.848 million, which forms a unique and powerful distribution and services network in China and through which, the Company becomes the life insurance service provider within the reach of customers. Moreover, the Company implemented the “Technology- driven China Life” development strategy in great depth by adhering to the leading concept of technological innovation, so as to cultivate its first-class operational management, risk control and customer services. The Company strives to establish a customer services system equipped with mobile, intelligent and social features, and leverages technologies to provide convenient insurance services to the public. | |||||||

Profound and extensive customer base

| The Company has an extensive customer base. As at 31 December 2019, the Company had approximately 303 million long-term individual and group life insurance policies, annuity contracts and long-term health insurance policies in force, offering insurance services for more than 500 million customers. | |||||||

Professional and stable core team | During the long course of its development, the Company has accumulated a wealth of experience in operation and management and has a stable and professional management team that is well versed in the art of management in China’s life insurance market. The Company’s core management team and key personnel comprise those who havein-depth knowledge and understanding of the life insurance market in China, including members of the Company’s senior management, experienced underwriting personnel, insurance actuaries and investment managers. During the Reporting Period, there was no movement of these personnel which might have a material impact on the Company. | |||||||

4

China Life Insurance Company Limited Annual Report 2019

Prelude

Forbes

“2019 Forbes Global 2000”, ranking 105th

21st Century Business Herald

“Assessment and Selection of

the Competitiveness of Asian

Financial Enterprises in the

21stCentury”

“2019 Best Life Insurance Company in Asia”

Financial Times

“Gold Medal List of Chinese

Financial Institution”

“Golden Dragon Award – 2019 Best Listed Insurance Company”

National Business Daily

“2019 Assessment and

Selection of Golden Tripod

Award in China”

“Golden Tripod Award in China – 2019 Excellent Life Insurance Company”

Securities Times

“Ark Prize for Insurance Company with High-quality Development in 2019”

“Ark Prize for Targeted Poverty Alleviation of the PRC Insurance Industry in 2019”

Sina Finance

“2019 Assessment and

Selection by Sina Gold Kirin of

the Insurance Industry”

“Best Brand Personal Insurance Company of the Year”

5

China Life Insurance Company Limited Annual Report 2019

Prelude

Shanghai Securities News “‘Golden Wealth Management’ for the Year of 2019”

“Annual Insurance Protection Brand Top Award of Golden Wealth Management in 2019”

People’s Daily Online “2019 Assessment and Selection of Craftsmanship Award of the People’s Choice”

“2019 People’s Craftsmanship Service Award”

Jointly published by China.org.cn and Insurance Today “2019 Assessment and Selection of ‘China Tripod’ in the Insurance Industry”

“Annual Best Insurance Brand”

Hexun.com The “17thFinancial Annual Champion Awards”

“Influential Insurance Company of the Year”

Data Center Dynamics “Asia Pacific Award”

China Life Hybrid Cloud being awarded by Data Center Dynamics (DCD) the “Annual Hybrid IT Project Award” for the Asia Pacific Region in 2019

being awarded by Data Center Dynamics (DCD) the “Annual Hybrid IT Project Award” for the Asia Pacific Region in 2019

Association for Talent Development (ATD) “Excellence in Practice Award”

E-learning Center being awarded by the Association for Talent Development (ATD) the “Excellence in Practice Award”

being awarded by the Association for Talent Development (ATD) the “Excellence in Practice Award”

6

China Life Insurance Company Limited Annual Report 2019

Prelude

7

China Life Insurance Company Limited Annual Report 2019

Prelude

FINANCIAL SUMMARY

MAJOR FINANCIAL DATA AND INDICATORS FOR THE PAST FIVE YEARS

| RMB million | ||||||||||||||||||||||||

| Under International Financial Reporting Standards (IFRS) | ||||||||||||||||||||||||

Major Financial Data1 | 2019 | 2018 | Change | 2017 | 2016 | 2015 | ||||||||||||||||||

For the year ended | ||||||||||||||||||||||||

Total revenues | 729,474 | 627,419 | 16.3% | 643,355 | 540,781 | 507,449 | ||||||||||||||||||

Net premiums earned | 560,278 | 532,023 | 5.3% | 506,910 | 426,230 | 362,301 | ||||||||||||||||||

Benefits, claims and expenses | 677,690 | 621,243 | 9.1% | 608,827 | 522,794 | 463,492 | ||||||||||||||||||

Insurance benefits and claims expenses | 509,467 | 479,219 | 6.3% | 466,043 | 407,045 | 352,219 | ||||||||||||||||||

Profit before income tax | 59,795 | 13,921 | 329.5% | 41,671 | 23,842 | 45,931 | ||||||||||||||||||

Net profit attributable to equity holders of the Company | 58,287 | 11,395 | 411.5% | 32,253 | 19,127 | 34,699 | ||||||||||||||||||

Net profit attributable to ordinary share holders of the Company | 57,893 | 11,011 | 425.8% | 31,873 | 18,741 | 34,514 | ||||||||||||||||||

Net cash inflow/(outflow) from operating activities | 286,032 | 147,552 | 93.9% | 200,990 | 89,098 | (18,811 | ) | |||||||||||||||||

As at 31 December | ||||||||||||||||||||||||

Total assets | 3,726,734 | 3,254,403 | 14.5% | 2,897,591 | 2,696,951 | 2,448,315 | ||||||||||||||||||

Investment assets2 | 3,573,154 | 3,104,014 | 15.1% | 2,753,124 | 2,573,049 | 2,334,814 | ||||||||||||||||||

Total liabilities | 3,317,392 | 2,931,113 | 13.2% | 2,572,281 | 2,389,303 | 2,122,101 | ||||||||||||||||||

Total equity holders’ equity | 403,764 | 318,371 | 26.8% | 320,933 | 303,621 | 322,492 | ||||||||||||||||||

Per share (RMB) | ||||||||||||||||||||||||

Earnings per share (basic and diluted)3 | 2.05 | 0.39 | 425.8% | 1.13 | 0.66 | 1.22 | ||||||||||||||||||

Equity holders’ equity per share3 | 14.28 | 11.26 | 26.8% | 11.35 | 10.74 | 11.41 | ||||||||||||||||||

Ordinary share holders’ equity per share3 | 14.01 | 10.99 | 27.5% | 11.08 | 10.47 | 11.13 | ||||||||||||||||||

Net cash inflow/(outflow) from operating activities per share3 | 10.12 | 5.22 | 93.9% | 7.11 | 3.15 | (0.67 | ) | |||||||||||||||||

Major financial ratios | ||||||||||||||||||||||||

Weighted average ROE (%) | 16.47 | 3.54 | | increase of 12.93 percentage points | | 10.49 | 6.16 | 11.56 | ||||||||||||||||

Ratio of assets and liabilities4(%) | 89.02 | 90.07 | | decrease of 1.05 percentage points | | 88.77 | 88.59 | 86.68 | ||||||||||||||||

Gross investment yield5(%) | 5.24 | 3.29 | | increase of 1.95 percentage points | | 5.16 | 4.69 | 6.42 | ||||||||||||||||

8

China Life Insurance Company Limited Annual Report 2019

Prelude

Notes:

| 1. | Net profit refers to net profit attributable to equity holders of the Company, while equity holders’ equity refers to equity attributable to equity holders of the Company. |

| 2. | Investment assets = Cash and cash equivalents + Securities at fair value through profit or loss +Available-for-sale securities +Held-to-maturity securities + Term deposits + Derivative Financial Assets + Securities purchased under agreements to resell + Loans + Statutory deposits-restricted + Investment properties + Investments in associates and joint ventures |

| 3. | In calculating the percentage change of the “Earnings per share (basic and diluted)”, “Equity holders’ equity per share”, “Ordinary share holders’ equity per share” and “Net cash inflow/(outflow) from operating activities per share”, the tail differences of the basic figures have been taken into account. |

| 4. | Ratio of assets and liabilities = Total liabilities/Total assets |

| 5. | Gross investment yield = (Gross investment income – Interest paid for securities sold under agreements to repurchase)/((Investment assets at the end of the previous year – Securities sold under agreements to repurchase at the end of the previous year – Derivative financial liabilities at the end of the previous year + Investment assets at the end of the period – Securities sold under agreements to repurchase at the end of the period – Derivative financial liabilities at the end of the period)/2) |

9

China Life Insurance Company Limited Annual Report 2019

Prelude

MAJOR ITEMS OF THE CONSOLIDATED FINANCIAL STATEMENTS AND THE REASONS FOR CHANGE

| RMB million | ||||||||||||||

Major Items of the Consolidated Statement of | As at 31 December 2019 | As at 31 December 2018 | Change | Main Reasons for Change | ||||||||||

Term deposits | 535,260 | 559,341 | -4.3 | % | Due to the maturity of term deposits | |||||||||

Held-to-maturity securities | 928,751 | 806,717 | 15.1 | % | An increase in the allocation of government bonds | |||||||||

Available-for-sale securities | 1,058,957 | 870,533 | 21.6 | % | An increase in the allocation of stocks inavailable-for-sale securities | |||||||||

Securities at fair value through profit or loss | 141,608 | 138,717 | 2.1 | % | An increase in the fair value of stocks in securities at fair value through profit or loss | |||||||||

Securities purchased under agreements to resell | 4,467 | 9,905 | -54.9 | % | The needs for liquidity management | |||||||||

Cash and cash equivalents | 53,306 | 50,809 | 4.9 | % | The needs for liquidity management | |||||||||

Loans | 608,920 | 450,251 | 35.2 | % | An increase in policy loans and certificates of deposit | |||||||||

Investment properties | 12,141 | 9,747 | 24.6 | % | New investments in investment properties | |||||||||

Investments in associates and joint ventures | 222,983 | 201,661 | 10.6 | % | An increase in investments in associates and joint ventures | |||||||||

Deferred tax assets | 128 | 1,257 | -89.8 | % | Affected by an increase in the fair value ofavailable-for-sale securities | |||||||||

Insurance contracts | 2,552,736 | 2,216,031 | 15.2 | % | The accumulation of insurance liabilities from new policies and renewals | |||||||||

Investment contracts | 267,804 | 255,434 | 4.8 | % | An increase in the scale of universal insurance accounts | |||||||||

Securities sold under agreements to repurchase | 118,088 | 192,141 | -38.5 | % | The needs for liquidity management | |||||||||

Annuity and other insurance balances payable | 51,019 | 49,465 | 3.1 | % | — | |||||||||

Interest-bearing loans and other borrowingsNote | 20,045 | 20,150 | -0.5 | % | — | |||||||||

Bonds payable | 34,990 | — | N/A | Issuance of capital supplemental bonds during the Reporting Period | ||||||||||

Deferred tax liabilities | 10,330 | — | N/A | Affected by an increase in the fair value ofavailable-for-sale securities | ||||||||||

Equity holders’ equity | 403,764 | 318,371 | 26.8 | % | Due to the combined impact of total comprehensive income and profit distribution during the Reporting Period | |||||||||

| Note: | Interest-bearing loans and other borrowings include athree-year bank loan of EUR67 million with a maturity date on 18 January 2021, afive-year bank loan of GBP275 million with a maturity date on 25 June 2024, afive-year bank loan of USD860 million with a maturity date on 16 September 2024, and asix-month bank loan of EUR127 million with a maturity date on 11 January 2020 which is automatically renewed upon maturity pursuant to the terms of the agreement. All the above are fixed rate loans. Afive-year bank loan of USD970 million with a maturity date on 27 September 2024, athree-year loan of EUR400 million with a maturity date on 6 December 2020, and aone-year bank loan of USD18 million with a maturity date on 6 November 2020, which are floating rate loans. |

10

China Life Insurance Company Limited Annual Report 2019

Prelude

| For the year ended 31 December | RMB million | |||||||||||

Major Items of the Consolidated | 2019 | 2018 | Change | Main Reasons for Change | ||||||||

Net premiums earned | 560,278 | 532,023 | 5.3% | — | ||||||||

Life insurance business | 445,719 | 436,863 | 2.0% | Due to the steady growth of life insurance business | ||||||||

Health insurance business | 99,575 | 80,279 | 24.0% | The expansion of health insurance business by the Company | ||||||||

Accident insurance business | 14,984 | 14,881 | 0.7% | — | ||||||||

Investment income | 139,919 | 125,167 | 11.8% | An increase in interest income from fixed-maturity investments and dividends from stocks | ||||||||

Net realised gains on financial assets | 1,831 | (19,591 | ) | N/A | An increase in spread income of stocks and funds inavailable-for-sale securities | |||||||

Net fair value gains through profit or loss | 19,251 | (18,278 | ) | N/A | An increase in spread income and fair value of stocks in securities at fair value through profit or loss | |||||||

Share of net profit of associates and joint ventures | 8,011 | 7,745 | 3.4% | An increase in profits of certain associates | ||||||||

Other income | 8,195 | 8,098 | 1.2% | — | ||||||||

Insurance benefits and claims expenses | 509,467 | 479,219 | 6.3% | Due to a combined impact of the growth of insurance business and a decrease in maturities payments and surrender payments | ||||||||

Investment contract benefits | 9,157 | 9,332 | -1.9% | — | ||||||||

Policyholder dividends resulting from participation in profits | 22,375 | 19,646 | 13.9% | An increase in investment yield from the participating accounts | ||||||||

Underwriting and policy acquisition costs | 81,396 | 62,705 | 29.8% | An increase in commissions of regular business due to the growth of the Company’s business and the optimization of its business structure | ||||||||

Finance costs | 4,255 | 4,116 | 3.4% | An increase in interest paid for bonds payables | ||||||||

Administrative expenses | 40,275 | 37,486 | 7.4% | The growth of business | ||||||||

Income tax | 781 | 1,985 | -60.7% | The impact from the new policy onpre-tax deduction of underwriting and policy acquisition costs | ||||||||

Net profit attributable to equity holders of the Company | 58,287 | 11,395 | 411.5% | Due to an increase in gross investment income and the impact from the new policy onpre-tax deduction of underwriting and policy acquisition costs | ||||||||

11

China Life Insurance Company Limited Annual Report 2019

Chairman’s Statement

CHAIRMAN’S STATEMENT

The year of 2019 marked the 70th anniversary1 of the founding of China Life, and also the beginning of “China Life Revitalization”. In this inspiring springtime, I, on behalf of the Company’s board of directors (the “Board”), hereby report to shareholders and the public on the Company’s operating results for the year of 2019. 2019 was a truly remarkable year for us, when the external environment was complicated and ever-changing, and the insurance industry saw accelerated transformation. In the face of new development and consumption trends, the Company has always kept pace with the development of the times as well as demands from customers. With new development philosophy guiding new practices, we have embarked on the journey of “China Life Revitalization” and pursued high-quality development with concerted efforts.

| In the year of 2019, net profit attributable to equity holders of the Company amounted to RMB58,287 million, an increase of 411.5% year on year. Value of one year’s sales of the Company reached RMB58,698 million, an increase of 18.6% year on year, significantly leading the market. The core solvency ratio and comprehensive solvency ratio were 266.71% and 276.53%, respectively. The Company has been listed on the “Forbes Global 2000” for 16 consecutive years, ranking 105th in 2019. Based on the Company’s sound operating performance, the Board has proposed to distribute a final cash dividend of RMB0.73 per share (inclusive of tax) and such proposal will be submitted to the 2019 Annual General Meeting for review and discussion.

All these achievements embodied devotion, dedication and hard work of all the staff and sales teams of the Company, and demonstrated the precious splendor, spirit and strength of China Life. Over the past year, we adhered to the operational guideline of “prioritizing business value, strengthening sales force, achieving stable growth, upgrading technology, optimizing services and guarding against risks” and took “Dual Centers and Dual Focuses” as our strategic core, making new strides in shouldering corporate social responsibility, quality development, technology empowerment, reform and transformation, and risk prevention and control.

1 The predecessor of the Company, one of the first batch of enterprises to underwrite insurance business in China, was approved by the Chinese Government for establishment in October 1949, when the People’s Republic of China was founded. In 1996, in compliance with the separate operation regulation, Zhong Bao Life Insurance Company was established to focus on life insurance business. In 1999, Zhong Bao Life Insurance Company was renamed as China Life Insurance Company. In 2003, China Life Insurance Company accelerated its reform and development and was restructured into China Life Insurance (Group) Company, which founded the Company as a sole promoter. |

12

China Life Insurance Company Limited Annual Report 2019

Chairman’s Statement

We firmly committed to serving the society and shouldering social responsibilities for the interest of the public. The Company gave full play to the functions of insurance as an economic “shock absorber” and social “stabilizer”, and underwrote an insured sum of RMB397 trillion for the public on a cumulative basis, with the total claims payment of more than RMB120 billion. It actively carried out policy-oriented businesses such as supplementary major medical expenses insurance and medical insurance administration projects, which helped improve basic social medical insurance protection and service level and significantly alleviated the illness-related poverty. The Company targeted to the specific insurance needs of poverty-stricken people, and made claims payment of nearly RMB3 billion to poverty-stricken people in relation to supplementary major medical expenses insurance protection. In 2019, the Company gave support to the targeted poverty alleviation work, helping nearly 87,000 poverty-stricken people be lifted from poverty. The Company proactively aligned its needs for development with national strategies. Leveraging on the leading role and demonstration effect of insurance funds, it actively participated in the country’s major development strategies including those for the coordinated development of the Beijing-Tianjin-Hebei Region, the construction of the Xiong’an New Area, the integrated development along the Yangtze River Delta, and the building of the Guangdong-Hong Kong-Macao Greater Bay Area, and took multiple measures to promote the coordinated development of regional economies. The Company also led the investment in the hydropower development project in the upper reaches of the Yellow River in Qinghai Province, participated in the mixed ownership reform of state-owned enterprises, and promoted the sustainable and healthy development of green industries.

We adhered to the concept of value-oriented development and realised consistent improvement in our development quality. We strengthened the asset-liability management and further promoted the synergy between assets and liabilities. The Company continuously consolidated the development foundation, took active measures to increase the volume of value-oriented business while enhancing the profitability of scale business. The Company’s gross written premiums exceeded RMB560 billion, maintaining a leading position in the market, and the growth of value of one year’s sales was substantially higher than that of its peers, representing the coordinated growth of business value and scale. By sticking to the protection role of insurance, the Company further optimized its business structure, with its long-term regular premiums growing over 40% year on year, and the percentage of premiums from designated protection-oriented products in the first-year regular premiums rising by 8.6 percentage points year on year. The Company allocated to yield seeking assets with long duration while grasping the short-term opportunities of the market, the gross investment income registered RMB169,043 million, representing a significant increase year on year, and the gross investment yield was 5.24%. The comprehensive investment yield2 was 7.28%, representing an increase of 418 BPs from 2018. Besides, the total number of the Company’s sales force amounted to 1.848 million, and the size of the sales force was expanded with improved quality. The monthly average productive agents increased by 34.9% year on year. Both the quality and size of the Company’s sales force improved against the downward trend, and anew-type sales team was established.

We continued to deepen technological empowerment, which comprehensively enhanced our sales and services. The Company kicked off the three-year action plan for the “Technology-driven China Life” initiative, actively applying technologies, such as AI, Big Data and Internet of Things, to empower the whole insurance value chain, pushed forward the upgrade of customer-oriented sales model, and stepped up efforts in providingone-stop integrated financial and insurance services for customers. The Company improved the whole chain of services, accelerated the building of the “One Customer, One China Life” platform, further transformed and upgraded its operations and services by promoting integrated, intelligent and ecological operations and services, and built up an “Insurance Plus” ecosystem. The Company further improved the customer experience and introduced intelligent underwriting and intelligent customer service systems. The paperless policy application rate for individual customers reached 97.8%, and the number of claims settled automatically in the whole process exceeded 10 million. The Company’s service efficiency was increased significantly with the digitalized service supply system being further optimized.

| 2 | Comprehensive investment yield = (Gross investment income – Interest paid for securities sold under agreements to repurchase + Current net fair value changes ofavailable-for-sale securities recognised in other comprehensive income)/((Investment assets at the end of the previous year – Securities sold under agreements to repurchase at the end of the previous year – Derivative financial liabilities at the end of the previous year + Investment assets at the end of the period – Securities sold under agreements to repurchase at the end of the period – Derivative financial liabilities at the end of the period)/2) |

13

China Life Insurance Company Limited Annual Report 2019

Chairman’s Statement

We continued to reform and innovate, which boosted vigorous driving forces for our development. The Company steadily carried out the “Dingxin Project”, upheld the concept of a “strong headquarters, streamlined provincial branches, optimized city branches and invigorated field offices”, and a development system of “Yi Ti Duo Yuan” was initially formed, featuring a strengthened individual agent channel with an emphasis on its core role of value creation in coordination with the development of group insurance, bancassurance and health insurance. By focusing on the value chain, the Company reconstructed a market-oriented and professional investment management system. It sped up the integration of front, middle and back offices and initially built an integrated intelligent operational system and a precise financial resource allocation system. It also optimized and improved the assessment and evaluation of management personnel, adopting market-oriented mechanism in talent selection and recruitment. Keeping in step with the national and regional development strategies, the Company vigorously pushed forward business revitalization in key cities, and built the new organizations, new mechanisms, new teams and new systems to cater to the urban market. The Company also implemented the “Gorgeous Counties, Happy Villages” project to consolidate its competitive strengths in rural markets of strategic importance, and generated more sources of growth from the grassroots branches of the Company.

We continued to strengthen our capability in risk control and prevention, and firmly held onto the bottom line of risks. The Company constantly improved thetop-level design for risk management and control, improved the risk management system and the risk preference transmission mechanism, completed a closed loop of risk management and control covering all links of its value chain and all aspects of operation and management, and established a comprehensive risk control model with full staff participation and whole process management. The Company carried outin-depth risk inspections, comprehensively prevented and controlled key risks, strengthened the technology empowerment in risk management and control, continued to build the intelligent risk control system, and achieved more accurate prevention and control of fraud risks and money laundering risks.

After the outbreak ofCOVID-19 in early 2020, the Company took immediate actions in providing insurance protection, donating epidemic prevention supplies, and offering health-related insurance services, etc. The Company expanded the scope of insurance coverage of its current products, upgraded claims settlement services, and improved online services. It provided complimentary insurance protection for over 2.48 million people fighting on the front line of the epidemic. While serving the national battle against the outbreak, the Company leveraged on the achievements of “Technology-driven China Life” to enrich a variety of insurance products sold online, innovate online sales team management model, conduct sales online, and strengthen remote service capabilities, so as to secure the sales force management and business operation in an orderly manner, and provide comprehensive protection for the customers’ rights.

14

China Life Insurance Company Limited Annual Report 2019

Chairman’s Statement

Looking ahead, we firmly believe that the Chinese economy will maintain its long-term sound development and its high-quality growth fundamentals remain unchanged, and that the domestic insurance industry is still at an important stage full of strategic opportunities. In 2020, we will continue to pursue high-quality development, stick to value creation during the whole process of the Company’s reform and development, and make concrete progress with “China Life Revitalization”. We will vigorously push forward the market-oriented reforms, accelerate the implementation of the “Dingxin Project”, speed up the digitalization process in business operation, enhance the application of digital technologies in sales, services and management, and strengthen the application of technological empowerment in sales, services and business operation. We will speed up the integration of service platforms, and shape the Company’s operation and services to be more integrated, intelligent and ecological. We will also strengthen risk management and control, strive to prevent major risks, enhance asset-liability management, implement “Environmental, Social and Governance (ESG)” concept, and advance our corporate governance.

“Many a little makes a mickle.” The Company will continue to uphold its original aspiration of “Protecting People’s Good Life”, revitalize China Life, forge ahead with the reform initiatives, and strive to create value for our shareholders, customers and society, making unremitting efforts to promote the high-quality development of the Chinese insurance industry, build a moderately prosperous society in all respects, and realise the first centenary goal of the country.

By Order of the Board

Wang Bin Chairman |

Beijing, China 25 March 2020 |

15

China Life Insurance Company Limited Annual Report 2019

Chairman’s Statement

CHINA LIFE REVITALIZATION

DINGXIN PROJECT

Principles

Strong headquarters, streamlined provincial branches, optimized city branches and invigorated field offices

One Goal

Build a vibrant organizational structure to achieve the goal of revitalizing China Life

Two Focuses

Create a strengthened individual agent channel in coordination with other channels (Yi Ti Duo Yuan) and a market-oriented investment management system

“Yi Ti” refers to the strengthened individual agent channel by upgrading the general team and consolidating the upsales, insurance planners and tele-sales teams for enhanced value creation; “Duo Yuan” refers to the operation of business through bancassurance, group and health insurance channels so as to form effective synergy with individual agent channel, and consolidate market leading position.

Two Engines

Establish market-oriented incentive and talent development mechanisms and optimize the models of technological development

Two Supports

Integrated intelligent operational system and precise financial resource allocation system

16

17

China Life Insurance Company Limited Annual Report 2019

Management Discussion and Analysis

MANAGEMENT DISCUSSION AND ANALYSIS

REVIEW OF BUSINESS OPERATIONS IN 2019

In 2019, despite the complicated situation of increased risks and challenges at home and abroad, the Company concentrated on the strategic goal of “China Life Revitalization” with “Dual Centers and Dual Focuses” as its strategic core, adhered to the overall keynote of making steady progress, and upheld the operational guideline of “prioritizing business value, strengthening sales force, achieving stable growth, upgrading technology, optimizing services, and guarding against risks”. The Company accelerated the establishment of a development system of “Yi Ti Duo Yuan” with strengthened individual agent channel in coordination with other channels as well as a market-oriented investment management system, strengthened technological empowerment, focused on the transformation of sales and the development of protection-oriented business, reformed its sales models, investment and services systems, constantly improved the efficiency of risk prevention and control, and achieved the coordinated growth of business scale and value.

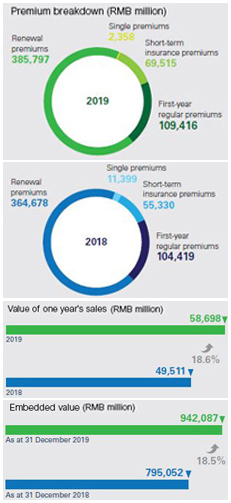

During the Reporting Period, the Company’s gross written premiums amounted to RMB567,086 million, an increase of 5.8% year on year, maintaining its industry leadership position. As at 31 December 2019, embedded value of the Company reached RMB942,087 million, an increase of 18.5% from the end of 2018. Value of one year’s sales was RMB58,698 million, an increase of 18.6% year on year. During the Reporting Period, the Company continued to enhance the asset-liability management, and its gross investment income reached RMB169,043 million, a significant increase of 77.7% from 2018. Due to an increase in gross investment income and the impact from the new policy onpre-tax deduction of underwriting and policy acquisition costs, net profit attributable to equity holders of the Company was RMB58,287 million, an increase of 411.5% year on year. As at the end of the Reporting Period, the core solvency ratio and the comprehensive solvency ratio were 266.71% and 276.53%, respectively.

18

China Life Insurance Company Limited Annual Report 2019

Management Discussion and Analysis

Key Performance Indicators of 2019

| RMB million | ||||||||

| 2019 | 2018 | |||||||

Gross written premiums | 567,086 | 535,826 | ||||||

Premiums from new policies | 181,289 | 171,148 | ||||||

Including: First-year regular premiums | 109,416 | 104,419 | ||||||

First-year regular premiums with a payment duration of ten years or longer | 59,168 | 41,635 | ||||||

Renewal premiums | 385,797 | 364,678 | ||||||

Gross investment income | 169,043 | 95,148 | ||||||

Net profit attributable to equity holders of the Company | 58,287 | 11,395 | ||||||

Value of one year’s sales1 | 58,698 | 49,511 | ||||||

Including: Exclusive individual agent channel | 52,189 | 42,839 | ||||||

Bancassurance channel | 6,288 | 6,357 | ||||||

Group insurance channel | 221 | 314 | ||||||

Policy Persistency Rate (14 months) 2(%) | 86.80 | 91.10 | ||||||

Policy Persistency Rate (26 months) 2(%) | 85.90 | 86.00 | ||||||

| As at | As at | |||||||

| 31 December 2019 | 31 December 2018 | |||||||

Embedded value | 942,087 | 795,052 | ||||||

Number of long-termin-force policies (hundred million) | 3.03 | 2.85 | ||||||

Notes:

| 1. | Numbers may not be additive due to rounding. |

| 2. | The Persistency Rate forlong-term individual life insurance policy is an important operating performance indicator for life insurance companies. It measures the ratio ofin-force policies in a pool of policies after a certain period of time. It refers to the proportion of policies that are still effective during the designated month in the pool of policies whose issue date was 14 or 26 months ago. |

19

China Life Insurance Company Limited Annual Report 2019

Management Discussion and Analysis

During the Reporting Period, with a commitment to high-quality development, the Company achieved a rapid growth in its business value. Value of one year’s sales of the Company was RMB58,698 million, an increase of 18.6% year on year. The new business margin of one year’s sales of the exclusive individual agent channel and the bancassurance channel increased by 3.2 and 5.1 percentage points year on year, respectively. As at 31 December 2019, embedded value of the Company reached RMB942,087 million, increasing by 18.5% from the end of 2018. The surrender rate3 was 1.89%, a decrease of 2.80 percentage points year on year.

During the Reporting Period, the Company vigorously developed its long-term regular business and its business structure was further optimized. First-year regular premiums amounted to RMB109,416 million, which accounted for 97.89% of long-term first-year premiums, increasing by 7.73 percentage points year on year. In particular, first-year regular premiums with a payment duration of ten years or longer were RMB59,168 million (ayear-on-year increase of 42.1%), which accounted for 54.08% of the first-year regular premiums (ayear-on-year increase of 14.21 percentage points). Renewal premiums amounted to RMB385,797 million (ayear-on-year increase of 5.8%), which accounted for 68.03% of the gross written premiums.

During the Reporting Period, the Company emphasized its due role of insurance protection, and made great efforts to develop protection-oriented business. The Company accelerated the development of protection-oriented businesses and further diversified its product mix. Out of the top ten insurance products by first-year regular premiums, six were protection-oriented products. The percentage of premiums from designated protection-oriented insurance business in the first-year regular premiums rose by 8.6 percentage points year on year, with an increase in both the number of protection-oriented insurance policies and average premiums per policy.

During the Reporting Period, the Company achieved significant increase in investment income by constantly enhancing the asset-liability management and optimizing its asset allocation strategies. The Company recorded a gross investment income of RMB169,043 million, ayear-on-year increase of 77.7% from 2018.

In 2019, the Company kicked off the “Dingxin Project” under the guidance of “China Life Revitalization” strategy with “Dual Centers and Dual Focuses” as its strategic core. As at the end of the Reporting Period, the Company completed the optimization of its organizational structure

3 Surrender Rate = Surrender payment/(Liability of long-term insurance contracts at the beginning of the period + Premiums of long-term insurance contracts) |  |

20

China Life Insurance Company Limited Annual Report 2019

Management Discussion and Analysis

and personnel adjustments and actively explored and established an organizational model and mechanism in line with the Company’s strategy.In terms of salesfunction, a development system of “Yi Ti Duo Yuan” was initially formed, which featured a strengthened individual agent channel at the core of value creation. The Company integrated all sales resources for individual insurance business and consolidated the bancassurance channel’s insurance planners, tele-sales and agent channel’s upsales teams. By separately managing and operating the general agent team and the new upsales team, which were both supported by the four functions of individual insurance planning, individual insurance operation, training and integrated finance functions, the Company deepened the transformation and upgrade of individual insurance business. In the development of the diversification (“Duo Yuan”) system, the Company reinforced and improved the existing advantages of the other channels. The group insurance channel focused on the development of its professional operation capacity. The bancassurance channel would generate business through bank outlets, properly coordinate growth in business scale and value, and optimize its business structure. The health insurance channel focused on professional development.In terms of the investment function, the Company further improved itstop-down investment management system in line with the investment value creation chain, including strategic asset allocation, tactical asset allocation, investment management, strengthened risk management in all aspects and investment operation support.In terms of operations, the Company accelerated the integration of front, middle, and back offices, gradually established an integrated intelligent operational system and a precise financial resource allocation system, and started to set up an operation and financial sharing service center. Based on the completion of its organizational restructuring in 2019, the Company will continue to push forward the “Dingxin Project” reforms, further improve its operational and management capabilities, and further promote reform and transformation in sales, investment, product, operations, technology, and human resources.

BUSINESS ANALYSIS

Insurance Business

Gross written premiums categorized by business

For the year ended 31 December | RMB million | |||||||||||

| 2019 | 2018 | Change | ||||||||||

Life Insurance Business | 446,562 | 437,540 | 2.1 | % | ||||||||

First-year business | 100,674 | 106,212 | -5.2 | % | ||||||||

First-year regular | 98,342 | 94,834 | 3.7 | % | ||||||||

Single | 2,332 | 11,378 | -79.5 | % | ||||||||

Renewal business | 345,888 | 331,328 | 4.4 | % | ||||||||

Health Insurance Business | 105,581 | 83,614 | 26.3 | % | ||||||||

First-year business | 66,213 | 50,705 | 30.6 | % | ||||||||

First-year regular | 11,000 | 9,430 | 16.6 | % | ||||||||

Single | 55,213 | 41,275 | 33.8 | % | ||||||||

Renewal business | 39,368 | 32,909 | 19.6 | % | ||||||||

Accident Insurance Business | 14,943 | 14,672 | 1.8 | % | ||||||||

First-year business | 14,402 | 14,231 | 1.2 | % | ||||||||

First-year regular | 74 | 155 | -52.3 | % | ||||||||

Single | 14,328 | 14,076 | 1.8 | % | ||||||||

Renewal business | 541 | 441 | 22.7 | % | ||||||||

|

|

|

|

|

| |||||||

Total | 567,086 | 535,826 | 5.8 | % | ||||||||

|

|

|

|

|

| |||||||

| Note: | Single premiums in the above table include premiums from short-term insurance business. |

During the Reporting Period, by further improving its business structure, gross written premiums from the life insurance business of the Company amounted to RMB446,562 million, rising by 2.1% year on year; gross written premiums from the health insurance business reached RMB105,581 million, rising by 26.3% year on year; and gross written premiums from the accident insurance business were RMB14,943 million, ayear-on-year increase of 1.8%.

21

China Life Insurance Company Limited Annual Report 2019

Management Discussion and Analysis

Gross written premiums categorized by channel

For the year ended 31 December | 2019 | RMB million 2018 | ||||||

Exclusive Individual Agent Channel | 436,621 | 408,278 | ||||||

First-year business of long-term insurance | 84,142 | 79,513 | ||||||

First-year regular | 83,865 | 79,241 | ||||||

Single | 277 | 272 | ||||||

Renewal business | 336,676 | 316,930 | ||||||

Short-term insurance business | 15,803 | 11,835 | ||||||

Bancassurance Channel | 70,060 | 76,841 | ||||||

First-year business of long-term insurance | 23,851 | 31,881 | ||||||

First-year regular | 23,820 | 23,239 | ||||||

Single | 31 | 8,642 | ||||||

Renewal business | 44,623 | 43,785 | ||||||

Short-term insurance business | 1,586 | 1,175 | ||||||

Group Insurance Channel | 28,846 | 26,404 | ||||||

First-year business of long-term insurance | 3,018 | 3,487 | ||||||

First-year regular | 968 | 1,004 | ||||||

Single | 2,050 | 2,483 | ||||||

Renewal business | 1,995 | 1,649 | ||||||

Short-term insurance business | 23,833 | 21,268 | ||||||

Other Channels1 | 31,559 | 24,303 | ||||||

First-year business of long-term insurance | 763 | 937 | ||||||

First-year regular | 763 | 935 | ||||||

Single | — | 2 | ||||||

Renewal business | 2,503 | 2,314 | ||||||

Short-term insurance business | 28,293 | 21,052 | ||||||

|

|

|

| |||||

Total | 567,086 | 535,826 | ||||||

|

|

|

| |||||

Notes:

| 1. | Other channels mainly include supplementary major medical expenses insurance business, tele-sales, online sales, etc. |

| 2. | The Company’s channel premium breakdown was presented based on the separate groups of sales personnel including exclusive individual agent team, group insurance sales representatives, bancassurance sales team and other distribution channels. |

In 2019, by consistently focusing on business value growth and accelerating reform and transformation, the Company’s core businesses developed at a faster speed with its value of one year’s sales rising significantly. With its sales force expanding steadily, quality of the sales force improved constantly. As at the end of 2019, the total number of the Company’s sales force reached 1.848 million.

Exclusive Individual Agent Channel. In 2019, focusing on business value growth, the exclusive individual agent channel deepened transformation and upgrade in its sales management, prioritized the growth of protection-oriented business, reinforced coordinated development of business, sales force andday-to-day management, and achieved coordinated growth of business scale and value, with its new business margin of one year’s sales

22

China Life Insurance Company Limited Annual Report 2019

Management Discussion and Analysis

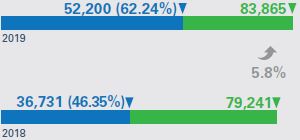

increasing significantly. During the Reporting Period, gross written premiums from the exclusive individual agent channel amounted to RMB436,621 million, an increase of 6.9% year on year. First-year regular premiums from the channel were RMB83,865 million, an increase of 5.8% year on year, which accounted for 99.67% of first-year premiums of long-term insurance. In particular, the percentage of first-year regular premiums with a payment duration of ten years or longer in first-year regular premiums was 62.24%, an increase of 15.89 percentage points year on year. Renewal premiums amounted to RMB336,676 million, an increase of 6.2% year on year. New business margin of one year’s sales of the channel reached 45.3%, ayear-on-year increase of 3.2 percentage points. In 2019, the sales force of the channel was improved in both quantity and quality, which substantially drove business growth. As at the end of 2019, the number of exclusive individual agents was 1.613 million, an increase of 12.1% from the end of 2018. The quality of the sales force was improved constantly, with the number of monthly average productive agents increasing by 34.9% year on year and the monthly average number of agents selling designated protection-oriented products increasing by 43.8% year on year. As at the end of 2019, the number of upsales agents which were included in the exclusive individual agents reached 577,000, an increase of 42.1% from the end of 2018, outpacing the growth of the exclusive individual agent force as a whole. In 2019, theday-to-day management of the channel was strengthened significantly, with variousday-to-day management indicators being improved.

First-year regular premiums from

exclusive individual agent channel(RMB million)

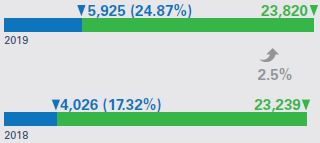

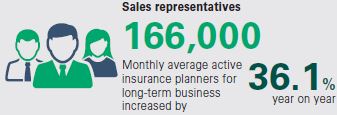

Bancassurance Channel. In 2019, with an emphasis on regular premium business, the bancassurance channel furthered its business restructuring, with its new business margin of one year’s sales of the channel rising constantly. During the Reporting Period, gross written premiums from the bancassurance channel amounted to RMB70,060 million, a decrease of 8.8% year on year. First-year regular premiums were RMB23,820 million, an increase of 2.5% year on year. In particular, first-year regular premiums with a payment duration of ten years or longer were RMB5,925 million (ayear-on-year increase of 47.2%), accounting for 24.87% of the first-year regular premiums, ayear-on-year increase of 7.55 percentage points. New business margin of one year’s sales of the channel reached 23.8%, increasing by 5.1 percentage points year on year. Renewal premiums amounted to RMB44,623 million (ayear-on-year increase of 1.9%), accounting for 63.69% of the gross written premiums from this channel, ayear-on-year increase of 6.71 percentage points. As at the end of 2019, as a result of strengthening its sales team management and improving sales force quality, the number of sales representatives of the bancassurance channel was 166,000, with the monthly average active insurance planners for long-term business increasing by 36.1% year on year.

First-year regular premiums

from bancassurance channel (RMB million)

23

China Life Insurance Company Limited Annual Report 2019

Management Discussion and Analysis

Group Insurance Channel. In 2019, the group insurance channel consistently deepened business diversification, stepped up efforts to expand key business segments, and achieved rapid development of various businesses. During the Reporting Period, gross written premiums from the group insurance channel were RMB28,846 million, an increase of 9.2% year on year. Short-term insurance premiums from the channel were RMB23,833 million, an increase of 12.1% year on year. The Company actively carried out the pilot program of tax deferred pension insurance business and consistently promoted thetax-advantaged health insurance business. With stricter performance appraisal and seeking for quality enhancement of its sales team, the number of direct sales representatives was 65,500 as at the end of 2019, among which, the number of high-performance representatives reached 45,000.

Other Channels. In 2019, gross written premiums from other channels reached RMB31,559 million, an increase of 29.9% year on year. The Company actively developed policy-oriented health insurance businesses, including supplementary major medical expenses insurance, long-term care insurance and supplementary medical insurance for social security, which consistently led the market. As at the end of the Reporting Period, the Company carried out over 230 supplementary major medical expenses insurance programs, providing services to nearly 400 million people in 31 provinces and cities. It also provided supplementary medical insurance protection for social security in 15 provinces, serving 38 million people, undertook over 600 medical insurance administration projects, covering more than 100 million people, and offered long-term care insurance protection for more than 13 million people. In 2019, the Company saw a faster growth in its online sales business. The Company emphasized product innovation, reinforced quality management and guarded against business risk. To optimize customer experience, the Company provided quick and convenient ways for online insurance application and diversified online services to insurance customers via various models, including direct sales on the Company’s official website, integration of both online and offline sales, and collaboration with platform resources.

The Company actively consolidated internal and external ecological resources, steadily pushed forward its coordinated business development with other subsidiaries of CLIC, carried out market expansion and widened customer base through the strategy of “One Customer,One-stop Service”. In 2019, premiums from property insurance cross-sold by the Company increased by 9.4% year on year, whereas new bids of enterprise annuity funds and pension security products of Pension Company cross-sold by the Company grew by 26.7% year on year. Meanwhile, the Company entrusted CGB to sell bancassurance products, with first-year regular premiums for 2019 increasing by 52.8% year on year. The number of new debit cards and credit cards jointly issued by the Company and CGB during the year exceeded one million, which demonstrated the synergy effects of platform operation, positive interaction and mutual benefits to both companies.

24

China Life Insurance Company Limited Annual Report 2019

Management Discussion and Analysis

Analysis of major insurance products

Top five insurance products in terms of gross written premium

| For the year ended 31 December | RMB million | |||||||||||||

Insurance product | Gross written premium | Standard premiums from new policies 1 | Major sales channel | Surrenders | ||||||||||

China Life Xin Fu Ying Jia Annuity Insurance | 37,024 | — | Mainly through the channel of exclusive individual agents | 586 | ||||||||||

China Life Xin Xiang Jin Sheng Annuity Insurance (Type A) | 36,345 | 10,948 | Mainly through the channel of exclusive individual agents | 140 | ||||||||||

China Life Supplementary Major Medical Expenses Insurance for Rural and Urban Citizens (Type A) | 25,757 | 25,757 | Through other channels | — | ||||||||||

China Life Hong Fu Zhi Zun Annuity Insurance (participating insurance) | 21,429 | — | Mainly through the channel of exclusive individual agents | 503 | ||||||||||

China Life Xin Ru Yi Annuity Insurance (platinum version) | 21,276 | — | Mainly through the channel of exclusive individual agents | 504 | ||||||||||

Notes:

| 1. | Standard premiums were calculated in accordance with the calculation methods set forth in the “Notice on Establishing the Industry Standard of Standard Premiums in the Life Insurance Industry” (Bao Jian Fa [2004] No. 102) and the “Supplementary Notice of the ‘Notice on Establishing the Industry Standard of Standard Premiums in the Life Insurance Industry’” (Bao Jian Fa [2005] No. 25) of the former China Insurance Regulatory Commission. |

| 2. | China Life Xin Fu Ying Jia Annuity Insurance, China Life Hong Fu Zhi Zun Annuity Insurance (participating insurance) and China Life Xin Ru Yi Annuity Insurance (platinum version) have been replaced by their upgraded products and are no longer on sale, and the gross written premiums are recorded as renewal premiums. |

Top three insurance products in terms of net increase in investment contract

| For the year ended 31 December | RMB million | |||||||||

Insurance product | Net increase in investment contract | Major sales channel | Surrender value | |||||||

China Life Xin Account Endowment Insurance (universal type) (exclusive version) | 10,107 | Mainly through the channel of exclusive individual agents | 157 | |||||||

China Life Xin Account Endowment Insurance (universal type) (diamond version) | 7,598 | Mainly through the channel of exclusive individual agents | 349 | |||||||

China Life Jin Account Endowment Insurance (universal type) | 3,385 | Mainly through the channel of exclusive individual agents | 134 | |||||||

25

China Life Insurance Company Limited Annual Report 2019

Management Discussion and Analysis

Insurance contracts

| RMB million | ||||||||||||

| As at 31 December 2019 | As at 31 December 2018 | Change | ||||||||||

Life insurance | 2,385,407 | 2,081,822 | 14.6 | % | ||||||||

Health insurance | 158,800 | 125,743 | 26.3 | % | ||||||||

Accident insurance | 8,529 | 8,466 | 0.7 | % | ||||||||

|

|

|

| |||||||||

Total of insurance contracts | 2,552,736 | 2,216,031 | 15.2 | % | ||||||||

|

|

|

| |||||||||

Including: residual marginNote | 768,280 | 684,082 | 12.3 | % | ||||||||

| Note: | The residual margin is a component of insurance contract reserve, which results in no Day 1 gain at the initial recognition of an insurance contract. The residual margin is set to zero if it is negative. The growth of residual margin arises mainly from new business. |

As at the end of the Reporting Period, the reserves of insurance contracts of the Company increased by 15.2% from the end of 2018, which is primarily due to the accumulation of insurance liabilities from new policies and renewal business. As at the date of the statement of financial position, the reserves of various insurance contracts of the Company passed the adequacy test.

Analysis of claims and policyholder benefits

| RMB million | ||||||||||||

For the year ended 31 December | 2019 | 2018 | Change | |||||||||

Insurance benefits and claims expenses | 509,467 | 479,219 | 6.3 | % | ||||||||

Life insurance business | 427,673 | 412,876 | 3.6 | % | ||||||||

Health insurance business | 75,471 | 59,689 | 26.4 | % | ||||||||

Accident insurance business | 6,323 | 6,654 | -5.0 | % | ||||||||

Investment contract benefits | 9,157 | 9,332 | -1.9 | % | ||||||||

Policyholder dividends resulting from participation in profits | 22,375 | 19,646 | 13.9 | % | ||||||||

During the Reporting Period, insurance benefits and claims expenses rose by 6.3% year on year due to an increase in reserves for insurance liabilities. In particular, health insurance business rose by 26.4% year on year due to health insurance business growth. Investment contract benefits declined by 1.9% year on year due to a decrease in the settlement interest rate of universal insurance accounts. Policyholder dividends resulting from participation in profits increased by 13.9% year on year due to an increase in investment yield from participating account.

Analysis of underwriting and policy acquisition costs and other expenses

| RMB million | ||||||||||||

For the year ended 31 December | 2019 | 2018 | Change | |||||||||

Underwriting and policy acquisition costs | 81,396 | 62,705 | 29.8 | % | ||||||||

Finance costs | 4,255 | 4,116 | 3.4 | % | ||||||||

Administrative expenses | 40,275 | 37,486 | 7.4 | % | ||||||||

Other expenses | 9,602 | 7,642 | 25.6 | % | ||||||||

Statutory insurance fund contribution | 1,163 | 1,097 | 6.0 | % | ||||||||

During the Reporting Period, underwriting and policy acquisition costs rose by 29.8% year on year due to an increase in the commissions of regular business resulting from the Company’s enhanced efforts in business restructuring. Administrative expenses increased by 7.4% year on year as a result of business growth.

26

China Life Insurance Company Limited Annual Report 2019

Management Discussion and Analysis

Investment Business

In 2019, the global economic growth slowed down synchronously, with repeated trade frictions becoming the biggest disturbance factor. The growth of domestic economy slightly slowed down but generally remained stable. The interest rate of the domestic bond market fluctuated and declined within a narrow range, and the stock market saw a significant rise compared to the beginning of 2019. The Company constantly reinforced its asset-liability management and increased the allocation in yield seeking assets and strategic assets. In respect of fixed-income investment, the Company optimized the portfolio structure and accumulated assets with long duration. While grasping opportunities to allocate to traditional fixed-income assets with long duration, it increased allocation tonon-standard financial assets and bank capital replenishment instruments, etc. As a result, the Company’s investment yields were increased while the credit risk was strictly controlled. In respect of its open market equity investment, the Company achieved satisfactory investment returns through effectively implementing tactical allocations, carrying out rebalancing as appropriate and optimizing the structure of equity holdings. As at the end of the Reporting Period, the Company’s investment assets reached RMB3,573,154 million, an increase of 15.1% from the end of 2018.

Investment portfolios

As at the end of the Reporting Period, our investment assets categorized by investment object are set out as below:

| RMB million | ||||||||||||||||

| As at 31 December 2019 | As at 31 December 2018 | |||||||||||||||

Investment category | Amount | Percentage | Amount | Percentage | ||||||||||||

Fixed-maturity financial assets | 2,674,261 | 74.85 | % | 2,407,236 | 77.55 | % | ||||||||||

Term deposits | 535,260 | 14.98 | % | 559,341 | 18.02 | % | ||||||||||

Bonds | 1,410,564 | 39.48 | % | 1,309,831 | 42.20 | % | ||||||||||

Debt-type financial products1 | 415,024 | 11.62 | % | 351,277 | 11.32 | % | ||||||||||

Other fixed-maturity investments2 | 313,413 | 8.77 | % | 186,787 | 6.01 | % | ||||||||||

Equity financial assets | 605,996 | 16.95 | % | 424,656 | 13.68 | % | ||||||||||

Common stocks | 276,604 | 7.74 | % | 178,710 | 5.76 | % | ||||||||||

Funds3 | 118,450 | 3.31 | % | 106,271 | 3.42 | % | ||||||||||

Bank wealth management products | 32,640 | 0.91 | % | 32,854 | 1.06 | % | ||||||||||

Other equity investments4 | 178,302 | 4.99 | % | 106,821 | 3.44 | % | ||||||||||

Investment properties | 12,141 | 0.34 | % | 9,747 | 0.31 | % | ||||||||||

Cash and others5 | 57,773 | 1.62 | % | 60,714 | 1.96 | % | ||||||||||

Investments in associates and joint ventures | 222,983 | 6.24 | % | 201,661 | 6.50 | % | ||||||||||

|

|

|

|

|

|

|

| |||||||||

Total | 3,573,154 | 100.00 | % | 3,104,014 | 100.00 | % | ||||||||||

|

|

|

|

|

|

|

| |||||||||

| Notes: |

| 1. | Debt-type financial products include debt investment schemes, equity investment plans, trust schemes, project asset-backed plans, credit asset-backed securities, specialized asset management plans, and asset management products, etc. |

| 2. | Other fixed-maturity investments include policy loans, statutory deposits-restricted, and interbank certificates of deposit, etc. |

| 3. | Funds include equity funds, bond funds and money market funds, etc. In particular, the balances of money market funds as at 31 December 2019 and 31 December 2018 were RMB1,829 million and RMB4,635 million, respectively. |

| 4. | Other equity investments include private equity funds, unlisted equities, preference shares, and equity investment plans, etc. |

| 5. | Cash and others include cash, cash at banks, short-term deposits and securities purchased under agreements to resell, etc. |

27

China Life Insurance Company Limited Annual Report 2019

Management Discussion and Analysis

As at the end of the Reporting Period, among the major types of investments, the percentage of investment in bonds changed to 39.48% from 42.20% as at the end of 2018, the percentage of term deposits changed to 14.98% from 18.02% as at the end of 2018, the percentage of investment in debt-type financial products increased to 11.62% from 11.32% as at the end of 2018, and the percentage of investment in stocks and funds (excluding money market funds) increased to 11.00% from 9.03% as at the end of 2018.

The Company’s debt-type financial products mainly concentrated on sectors such as transportation, public utilities and energy, and the financing entities were primarily large central-owned enterprises and state-owned enterprises. As at the end of the Reporting Period, over 99% of the debt-type financial products held by the Company had ratings of AAA or above by external rating institutions. In general, the quality of the debt-type financial products invested by the Company was in good condition and the risks were well controlled.

Investment income

For the year ended 31 December | 2019 | RMB million 2018 | ||||||

Gross investment income | 169,043 | 95,148 | ||||||

Net investment income | 149,109 | 133,017 | ||||||

Net income from fixed-maturity investments | 116,254 | 106,422 | ||||||

Net income from equity investments | 22,804 | 17,776 | ||||||

Net income from investment properties | 31 | 105 | ||||||

Investment income from cash and others | 861 | 969 | ||||||

Share of profit of associates and joint ventures | 9,159 | 7,745 | ||||||

Net realised gains on financial assets | 1,831 | (19,591 | ) | |||||

Net fair value gains through profit or loss | 19,251 | (18,278 | ) | |||||

Disposal gains and impairment loss of associates and joint ventures | (1,148 | ) | — | |||||

Net investment yield1 | 4.61 | % | 4.64 | % | ||||

Gross investment yield2 | 5.24 | % | 3.29 | % | ||||

| Notes: |

| 1. | Net investment yield = (Net investment income – Interest paid for securities sold under agreements to repurchase)/((Investment assets at the end of the previous year – Securities sold under agreements to repurchase at the end of the previous year + Investment assets at the end of the period – Securities sold under agreements to repurchase at the end of the period)/2) |

| 2. | Gross investment yield = (Gross investment income – Interest paid for securities sold under agreements to repurchase)/((Investment assets at the end of the previous year – Securities sold under agreements to repurchase at the end of the previous year – Derivatives financial liabilities at the end of the previous year + Investment assets at the end of the period – Securities sold under agreements to repurchase at the end of the period – Derivatives financial liabilities at the end of the period)/2) |

In 2019, the Company’s net investment income was RMB149,109 million, an increase of RMB16,092 million from 2018 and ayear-on-year increase of 12.1%. As the Company increased its allocation in interest-bearing assets such as bonds with long duration, stocks with high dividends andnon-standard assets in recent years, although the interest rate fluctuated and trended downwards, the Company’s net investment yield remained stable at 4.61%. In the meantime, in respect of the equity investments, the Company followed the long-term investment direction and effectively implemented tactical allocations under the established strategic asset allocation guidance, and the Company’s investment income rose significantly.

The gross investment income of the Company reached RMB169,043 million, an increase of RMB73,895 million from 2018, and the gross investment yield was 5.24%, an increase of 195 BPs from the end of 2018. The comprehensive investment yield taking into account the current net fair value changes ofavailable-for-sale securities recognised in other comprehensive income was 7.28%, an increase of 418 BPs from the end of 2018.

Major investments

During the Reporting Period, there was no material equity investment ornon-equity investment of the Company that is subject to disclosure requirements.

28

China Life Insurance Company Limited Annual Report 2019

Management Discussion and Analysis

ANALYSIS OF SPECIFIC ITEMS

Profit before Income Tax

| RMB million | ||||||||||||

For the year ended 31 December | 2019 | 2018 | Change | |||||||||

Profit before income tax | 59,795 | 13,921 | 329.5 | % | ||||||||

Life insurance business | 42,418 | 1,630 | 2,502.3 | % | ||||||||

Health insurance business | 5,875 | 4,100 | 43.3 | % | ||||||||

Accident insurance business | 489 | 495 | -1.2 | % | ||||||||

Other businesses | 11,013 | 7,696 | 43.1 | % | ||||||||

During the Reporting Period, due to an increase in gross investment income, profit before income tax from the life insurance business increased by 2,502.3% year on year, profit before income tax from the health insurance business increased by 43.3% year on year, profit before income tax from the accident insurance business basically remained flat compared to 2018, and profit before income tax from other businesses increased by 43.1% year on year.

Analysis of Cash Flows

Liquidity sources

The Company’s cash inflows mainly come from insurance premiums, income fromnon-insurance contracts, interest income, dividends and bonus, and proceeds from sale and maturity of investment assets. The primary liquidity risks with respect to these cash inflows are the risk of surrender by contract holders and policyholders, as well as the risks of default by debtors, interest rate fluctuations and other market volatilities. The Company closely monitors and manages these risks.

The Company’s cash and bank deposits can provide it with a source of liquidity to meet normal cash outflows. As at the end of the Reporting Period, the balance of cash and cash equivalents was RMB53,306 million. In addition, the vast majority of the Company’s term deposits in banks allow it to withdraw funds on deposits, subject to a penalty interest charge. As at the end of the Reporting Period, the amount of term deposits was RMB535,260 million.

The Company’s investment portfolio also provides it with a source of liquidity to meet unexpected cash outflows. The Company is also subject to market liquidity risk due to the large size of its investments in some of the markets. In some circumstances, some of its holdings of investment securities may be large enough to have an influence on the market value. These factors may adversely affect the Company’s ability to sell these investments or sell them at a fair price.

Liquidity uses

The Company’s principal cash outflows primarily relate to the payables for the liabilities associated with its various life insurance, annuity, accident insurance and health insurance products, operating expenses, income taxes and dividends that may be declared and paid to its equity holders. Cash outflows arising from its insurance activities primarily relate to benefit payments under these insurance products, as well as payments for policy surrenders, withdrawals and policy loans.

The Company believes that its sources of liquidity are sufficient to meet its current cash requirements.

29

China Life Insurance Company Limited Annual Report 2019

Management Discussion and Analysis

Consolidated cash flows

The Company has established a cash flow testing system, and conducts regular tests to monitor the cash inflows and outflows under various scenarios and adjusts the asset portfolio accordingly to ensure sufficient sources of liquidity.

| RMB million | ||||||||||||||

For the year ended 31 December | 2019 | 2018 | Change | Main Reasons for Change | ||||||||||

Net cash inflow/(outflow) from operating activities | 286,032 | 147,552 | 93.9 | % | A decrease in surrender payments and maturity payments | |||||||||

Net cash inflow/(outflow) from investing activities | (247,515 | ) | (238,373 | ) | 3.8 | % | The needs for investment management | |||||||

Net cash inflow/(outflow) from financing activities | (36,075 | ) | 92,963 | N/A | The needs for liquidity management | |||||||||

Foreign exchange gains/(losses) on cash and cash equivalents | 55 | 81 | -32.1 | % | — | |||||||||

|

|

|

| |||||||||||

Net increase/(decrease) in cash and cash equivalents | 2,497 | 2,223 | 12.3 | % | — | |||||||||

|

|

|

| |||||||||||

Solvency Ratio

An insurance company shall have the capital commensurate with its risks and business scale. According to the nature and capacity of loss absorption by capital, the capital of an insurance company is classified into the core capital and the supplementary capital. The core solvency ratio is the ratio of core capital to minimum capital, which reflects the adequacy of the core capital of an insurance company. The comprehensive solvency ratio is the ratio of the sum of core capital and supplementary capital to minimum capital, which reflects the overall capital adequacy of an insurance company. The following table shows our solvency ratios as at the end of the Reporting Period:

| RMB million | ||||||||

| As at 31 December 2019 | As at 31 December 2018 | |||||||

Core capital | 952,030 | 761,353 | ||||||

Actual capital | 987,067 | 761,367 | ||||||

Minimum capital | 356,953 | 303,872 | ||||||

Core solvency ratio | 266.71 | % | 250.55 | % | ||||

Comprehensive solvency ratio | 276.53 | % | 250.56 | % | ||||

|

|

|

| |||||

| Note: | The China Risk Oriented Solvency System was formally implemented on 1 January 2016. This table is compiled according to the rules of the system. |

As at the end of the Reporting Period, the Company’s comprehensive solvency ratio increased by 25.97 percentage points from the end of 2018, which was due to an increase in gross investment income, improvement of business structure and the issuance of capital supplemental bonds of RMB35 billion.

Sale of Material Assets and Equity

During the Reporting Period, there was no sale of material assets and equity of the Company.

30

China Life Insurance Company Limited Annual Report 2019

Management Discussion and Analysis

Major Subsidiaries and Associates of the Company

| RMB million | ||||||||||||||||||||||

Company Name | Major Business Scope | Registered Capital | Shareholding | Total Assets | Net Assets | Net Profit | ||||||||||||||||

China Life Asset Management Company Limited | Management and utilization of proprietary funds; acting as agent or trustee for asset management business; consulting business relevant to the above businesses; other asset management business permitted by applicable PRC laws and regulations | 4,000 | 60% | 11,914 | 10,354 | 1,286 | ||||||||||||||||

China Life Pension Company Limited | Group pension insurance and annuity; individual pension insurance and annuity; short-term health insurance; accident insurance; reinsurance of the above insurance businesses; business for the use of insurance funds that are permitted by applicable PRC laws and regulations; pension insurance asset management product business; management of funds in RMB or foreign currency as entrusted by entrusting parties for the retirement benefit purpose; other businesses permitted by the CBIRC | 3,400 | | 70.74% is held by the Company, and 3.53% is held by AMC | | 5,644 | 4,084 | 635 | ||||||||||||||

China Life Property and Casualty Insurance Company Limited | Property loss insurance; liability insurance; credit insurance and guarantee insurance; short-term health insurance and accident insurance; reinsurance of the above insurance businesses; business for the use of insurance funds that are permitted by applicable PRC laws and regulations; other business permitted by the CBIRC | 18,800 | 40% | 91,167 | 23,330 | 2,123 | ||||||||||||||||

China Guangfa Bank Co., Ltd. | The businesses approved by the CBIRC include commercial banking businesses such as public and private deposits, loans, payment and settlement, and capital business | 19,687 | 43.686% | 2,632,798 | 209,564 | 12,581 | ||||||||||||||||

| Note: | For details, please refer to Note 9 and Note 35 in the Notes to the Consolidated Financial Statements in this annual report. |

Structured Entities Controlled by the Company