Exhibit 99.2

Briefing on IFRS17 & IFRS9 Updates 9 May 2023 Beijing

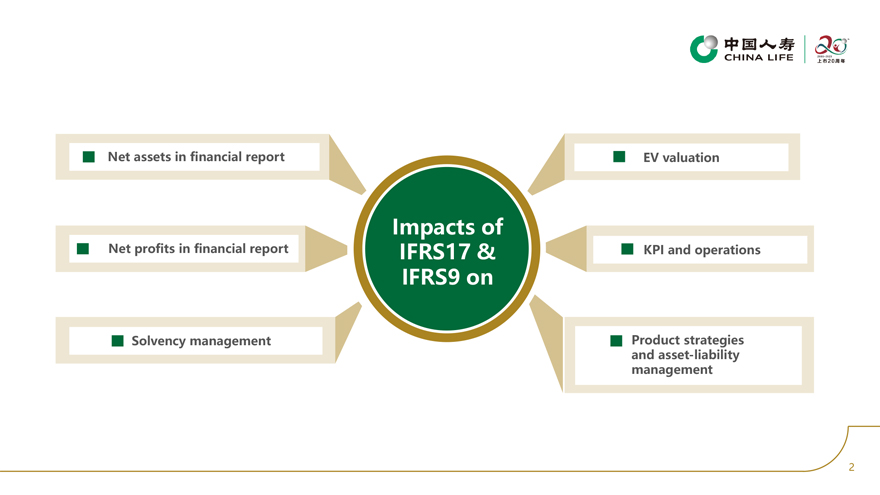

Net assets in financial report EV valuation Impacts of Net profits in financial report IFRS17 & KPI and operations IFRS9 on Solvency management Product strategies and asset-liability management 2

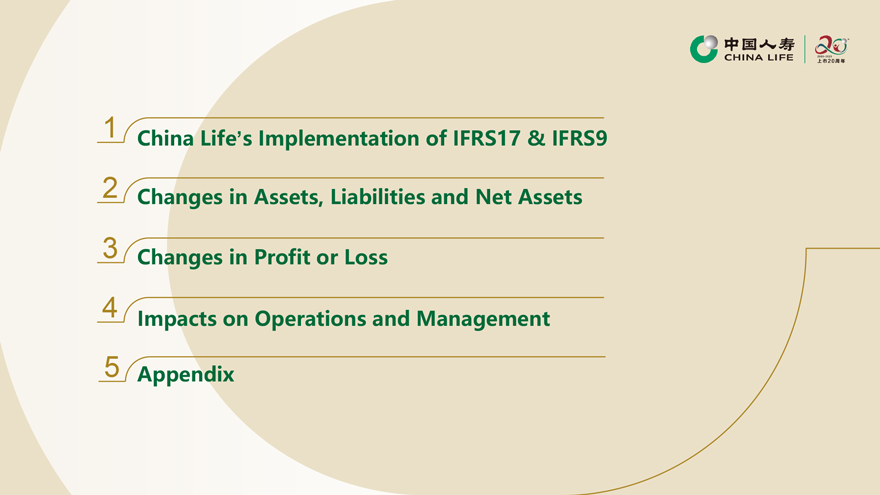

1 China Life’s Implementation of IFRS17 & IFRS9 2 Changes in Assets, Liabilities and Net Assets 3 Changes in Profit or Loss 4 Impacts on Operations and Management 5 Appendix

China Life’s Implementation of IFRS17 & IFRS9

China Life’s Implementation of IFRS 17 & IFRS 9 As the largest life insurance company in China, China Life has the most extensive 01 product offerings and the largest amount of business data. Despite a shortage of references, the Company was among the first insurance companies that have successfully implemented the new accounting standards, achieving many outstanding outcomes 01. Industry-leading data management capabilities The Company has built up full-coverage enterprise level data management system. It has deepened data governance, optimized mechanism and strengthened data empowerment. The Company received the Level 5 certification (the highest level) of DCMM (Data management Capability Maturity Model) for its data management capability, becoming the first insurance company to obtain the certification 5 5

China Life’s Implementation of IFRS 17 & IFRS 9 (cont’d) 02. Automating the entire workflows Successfully constructed the new proprietary data foundation. Based on trillion-level data processing capabilities, achieved timely, accurate and automatic issuance of financial statements under the new accounting standards and disclosed financial information based on the new standards on April 27, 2023 03. Reconstructing the accounting and actuarial system Reconstructed accounting and actuarial system with more accurate valuation, more refined model and more efficient workflows, which guarantees the systematicness completeness and accuracy of the implementation 6 6

Changes in Assets, Liabilities and Net Assets

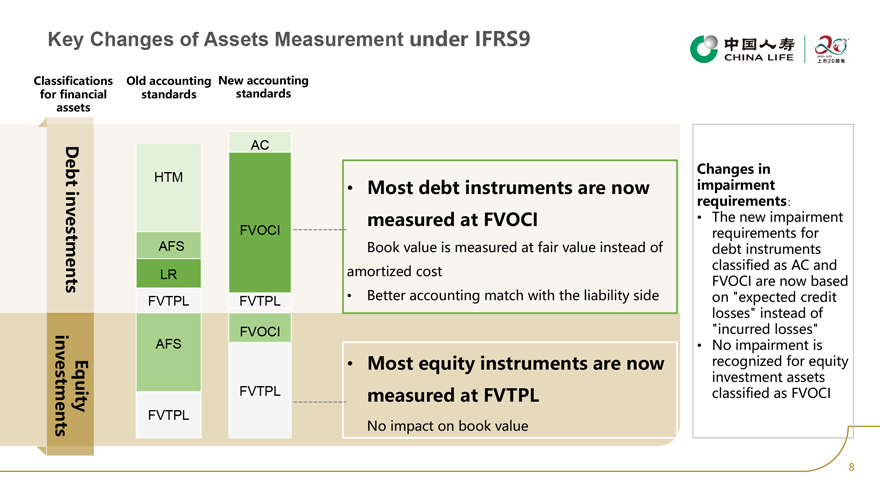

Key Changes of Assets Measurement under IFRS9 Classifications Old accounting New accounting for financial standards standards assets AC Changes in Debt HTM impairment Most debt instruments are now requirements measured at FVOCI The new impairment FVOCI requirements for AFS Book value is measured at fair value instead of debt instruments amortized cost classified as AC and investments LR FVOCI are now based FVTPL FVTPL Better accounting match with the liability side on expected credit losses instead of FVOCI incurred losses AFS No impairment is Most equity instruments are now recognized for equity investment assets Equity FVTPL measured at FVTPL classified as FVOCI investment FVTPL No impact on book value s 8

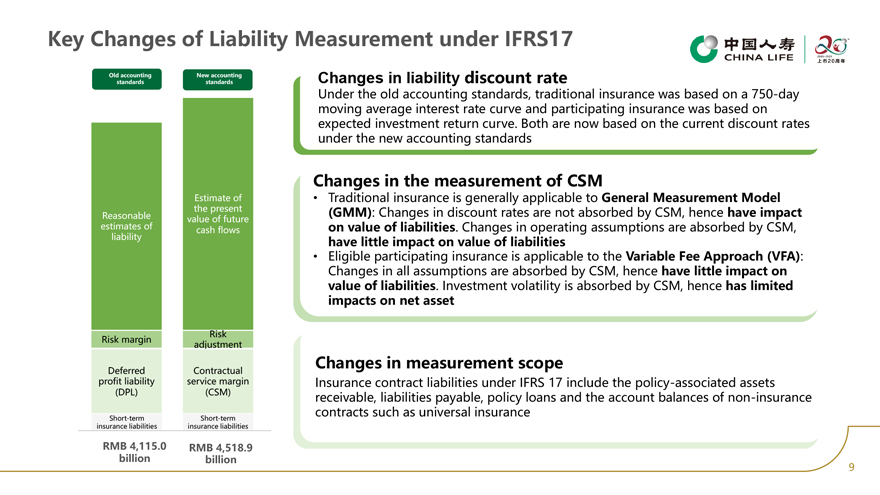

Key Changes of Liability Measurement under IFRS17 Old accounting New accounting Changes in liability discount rate standards standards Under the old accounting standards, traditional insurance was based on a 750-day moving average interest rate curve and participating insurance was based on expected investment return curve. Both are now based on the current discount rates under the new accounting standards Changes in the measurement of CSM Estimate of Traditional insurance is generally applicable to General Measurement Model the present (GMM): Changes in discount rates are not absorbed by CSM, hence have impact Reasonable value of future estimates of cash flows on value of liabilities. Changes in operating assumptions are absorbed by CSM, liability have little impact on value of liabilities Eligible participating insurance is applicable to the Variable Fee Approach (VFA): Changes in all assumptions are absorbed by CSM, hence have little impact on value of liabilities. Investment volatility is absorbed by CSM, hence has limited impacts on net asset Risk Risk margin adjustment Changes in measurement scope Deferred Contractual profit liability service margin Insurance contract liabilities under IFRS 17 include the policy-associated assets (DPL) (CSM) receivable, liabilities payable, policy loans and the account balances of non-insurance contracts such as universal insurance Short-term Short-term insurance liabilities insurance liabilities RMB 4,115.0 RMB 4,518.9 billion billion 9

Changes in Net Assets under New Accounting Standards Old standards IAS39) New standards IFRS9) Financial instruments accounting standard 2022 corresponding 2023 financial period Insurance contracts New standards IFRS17) New standards IFRS17) accounting standard Changes in net assets on December 31, 2022 under the old Changes in net assets on March 31, 2023 under the old and new accounting standards and new accounting standards RMB bn 445.1 RMB bn 505.9 375.0 470.3 Net assets at the end of Impact of present value Impact of contractual Other impacts Net assets at the end of Net assets at the Impact of IFRS9 Impact of present Impact of contractual Other impacts Net assets at the the period under the old of future cash flows service margins the period under new end of the period value of future cash service margins end of the period accounting standards accounting standards under the old flows under new accounting accounting Key reasons for the lower net assets on December 31, 2022 standards standards Under the new accounting standards, liabilities are evaluated based on the Key reasons for the higher net assets on March 31, 2023 current market interest rate, which is lower than the liability evaluation More debt investment assets are measured at fair value, which is rate under the old standards, which is based on the 750-day moving higher than amortized cost average curve and expected investment return curve The participating insurance liabilities etc. measured at VFA mirrors the fair value of debt investment assets, which is higher than the liabilities under the old standards, while debt investment assets are still measured at the old standards 10

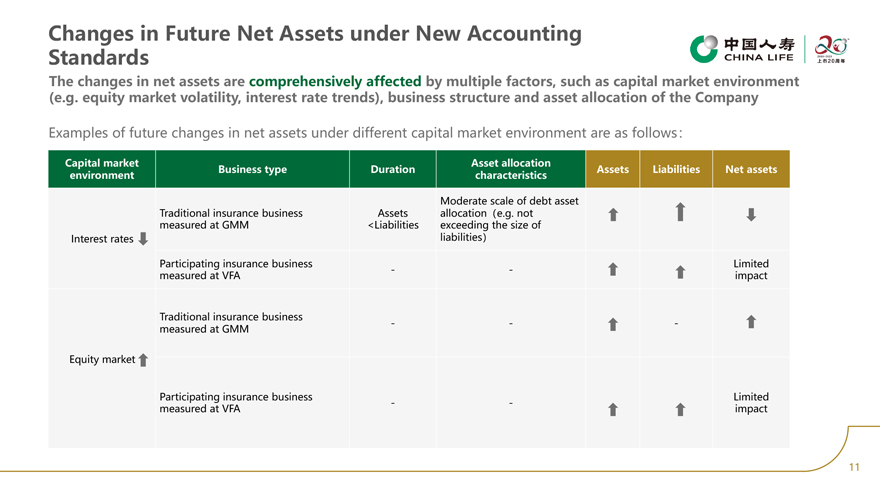

Changes in Future Net Assets under New Accounting Standards The changes in net assets are comprehensively affected by multiple factors, such as capital market environment (e.g. equity market volatility, interest rate trends), business structure and asset allocation of the Company Examples of future changes in net assets under different capital market environment are as follows Capital market Asset allocation Business type Duration Assets Liabilities Net assets environment characteristics Moderate scale of debt asset Traditional insurance business Assets allocation e.g. not measured at GMM <Liabilities exceeding the size of Interest rates liabilities Participating insurance business Limited —measured at VFA impact Traditional insurance business — -measured at GMM Equity market Participating insurance business Limited —measured at VFA impact 11

Changes in Profit or Loss

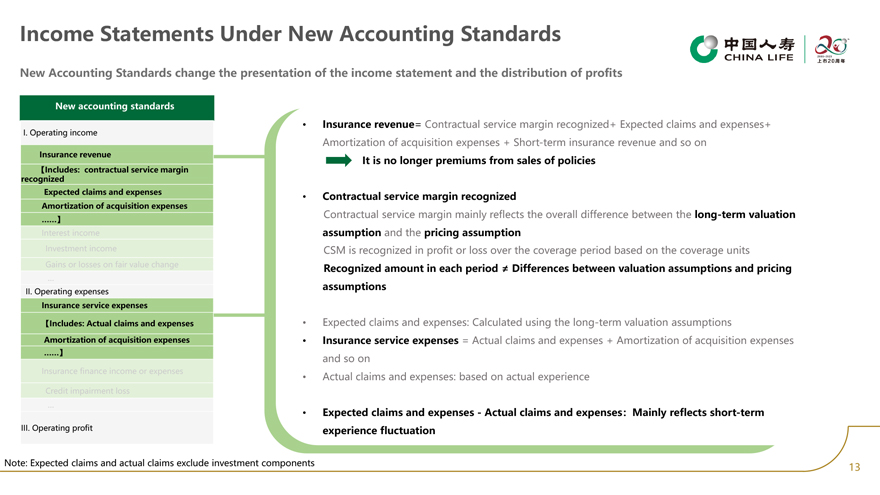

Income Statements Under New Accounting Standards New Accounting Standards change the presentation of the income statement and the distribution of profits New accounting standards Insurance revenue= Contractual service margin recognized+ Expected claims and expenses+ I. Operating income Amortization of acquisition expenses + Short-term insurance revenue and so on Insurance revenue It is no longer premiums from sales of policies Includes: contractual service margin recognized Expected claims and expenses Contractual service margin recognized Amortization of acquisition expenses Contractual service margin mainly reflects the overall difference between the long-term valuation …… Interest income assumption and the pricing assumption Investment income CSM is recognized in profit or loss over the coverage period based on the coverage units Gains or losses on fair value change Recognized amount in each period ≠Differences between valuation assumptions and pricing assumptions II. Operating expenses Insurance service expenses Includes: Actual claims and expenses Expected claims and expenses: Calculated using the long-term valuation assumptions Amortization of acquisition expenses Insurance service expenses = Actual claims and expenses + Amortization of acquisition expenses … and so on Insurance finance income or expenses experience Actual claims and expenses: based on actual Credit impairment loss … Expected claims and expenses—Actual claims and expenses Mainly reflects short-term III. Operating profit experience fluctuation Note: Expected claims and actual claims exclude investment components 13

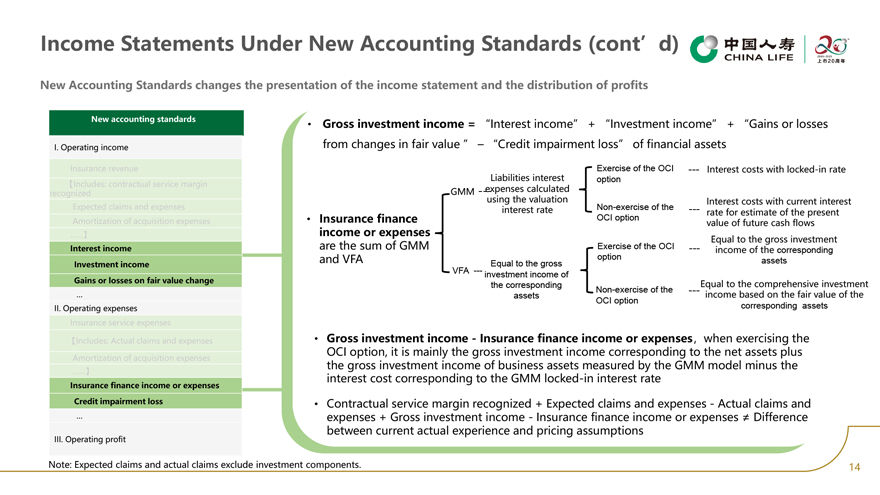

Income Statements Under New Accounting Standards (cont’d) New Accounting Standards changes the presentation of the income statement and the distribution of profits New accounting standards Gross income = investment Interest income + Investment income + Gains or losses I. Operating income from changes in fair value – Credit impairment loss of financial assets Insurance revenue Exercise of the OCI —- Interest costs with locked-in rate Liabilities interest option Includes: contractual service margin expenses calculated recognized GMM —-using the valuation Interest costs with current interest Expected claims and expenses interest rate Non-exercise of the —-rate for estimate of the present Amortization of acquisition expenses Insurance finance OCI option value of future cash flows income or expenses Equal to the gross investment Interest income are the sum of GMM Exercise of the OCI —-income of the corresponding and VFA option Investment income Equal to the gross assets VFA —- investment income of Gains or losses on fair value change Equal to the comprehensive investment the corresponding Non-exercise of the —- assets income based on the fair value of the OCI option II. Operating expenses corresponding assets Insurance service expenses Includes: Actual claims and expenses Gross investment income—Insurance finance income or expenses when exercising the OCI option, it is mainly the gross investment income corresponding to the net assets plus Amortization of acquisition expenses the gross investment income of business assets measured by the GMM model minus the interest cost corresponding to the GMM locked-in interest rate Insurance finance income or expenses Credit impairment loss Contractual service margin recognized + Expected claims and expenses—Actual claims and expenses + Gross investment income—Insurance finance income or expenses ‰ Difference between current actual experience and pricing assumptions III. Operating profit Note: Expected claims and actual claims exclude investment components. 14

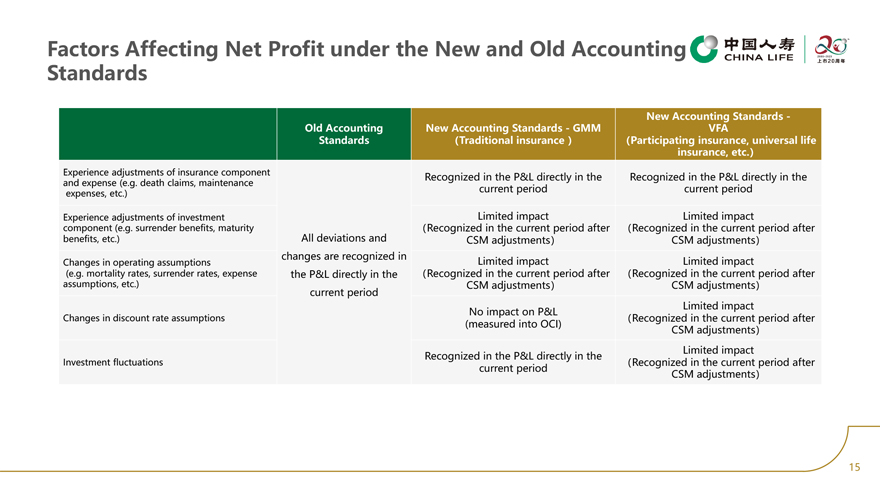

Factors Affecting Net Profit under the New and Old Accounting Standards New Accounting Standards -Old Accounting New Accounting Standards—GMM VFA Standards Traditional insurance Participating insurance, universal life insurance, etc. Experience adjustments of insurance component Recognized in the P&L directly in the Recognized in the P&L directly in the and expense (e.g. death claims, maintenance expenses, etc.) current period current period Experience adjustments of investment Limited impact Limited impact component (e.g. surrender benefits, maturity All deviations and Recognized in the current period after Recognized in the current period after benefits, etc.) CSM adjustments CSM adjustments changes are recognized in Limited impact Limited impact Changes in operating assumptions (e.g. mortality rates, surrender rates, expense the P&L directly in the Recognized in the current period after Recognized in the current period after assumptions, etc.) CSM adjustments CSM adjustments current period Limited impact No impact on P&L Changes in discount rate assumptions Recognized in the current period after (measured into OCI) CSM adjustments Limited impact Recognized in the P&L directly in the Investment fluctuations Recognized in the current period after current period CSM adjustments 15

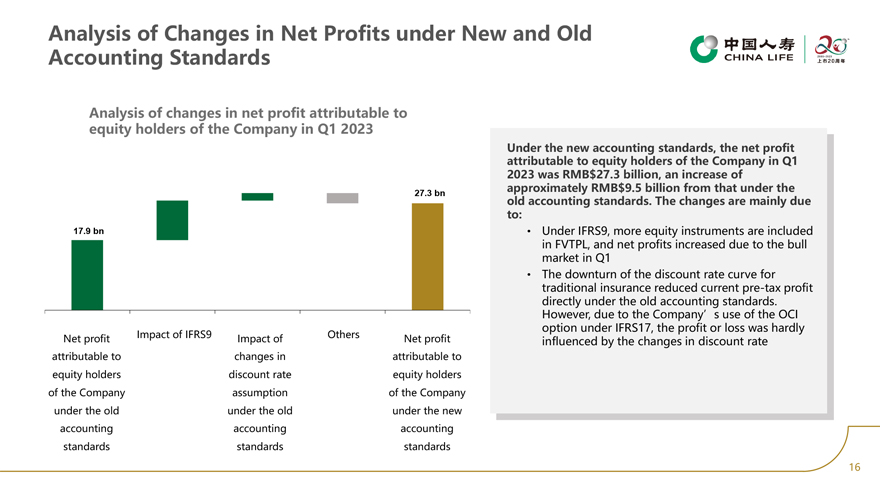

Analysis of Changes in Net Profits under New and Old Accounting Standards Analysis of changes in net profit attributable to equity holders of the Company in Q1 2023 Under the new accounting standards, the net profit attributable to equity holders of the Company in Q1 2023 was RMB$27.3 billion, an increase of approximately RMB$9.5 billion from that under the 27.3 bn old accounting standards. The changes are mainly due to: 17.9 bn Under IFRS9, more equity instruments are included in FVTPL, and net profits increased due to the bull market in Q1 The downturn of the discount rate curve for traditional insurance reduced current pre-tax profit directly under the old accounting standards. However, due to the Company’s use of the OCI option under IFRS17, the profit or loss was hardly Net profit Impact of IFRS9 Impact of Others Net profit influenced by the changes in discount rate attributable to changes in attributable to equity holders discount rate equity holders of the Company assumption of the Company under the old under the old under the new accounting accounting accounting standards standards standards 16

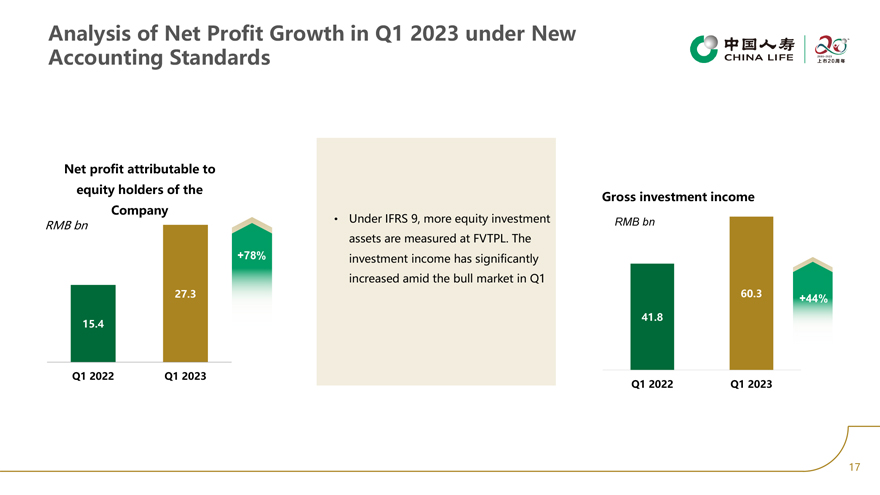

Analysis of Net Profit Growth in Q1 2023 under New Accounting Standards Net profit attributable to equity holders of the Gross investment income Company Under IFRS 9, more equity investment RMB bn RMB bn assets are measured at FVTPL. The +78% investment income has significantly increased amid the bull market in Q1 27.3 60.3 +44% 41.8 15.4 Q1 2022 Q1 2023 Q1 2022 Q1 2023 17

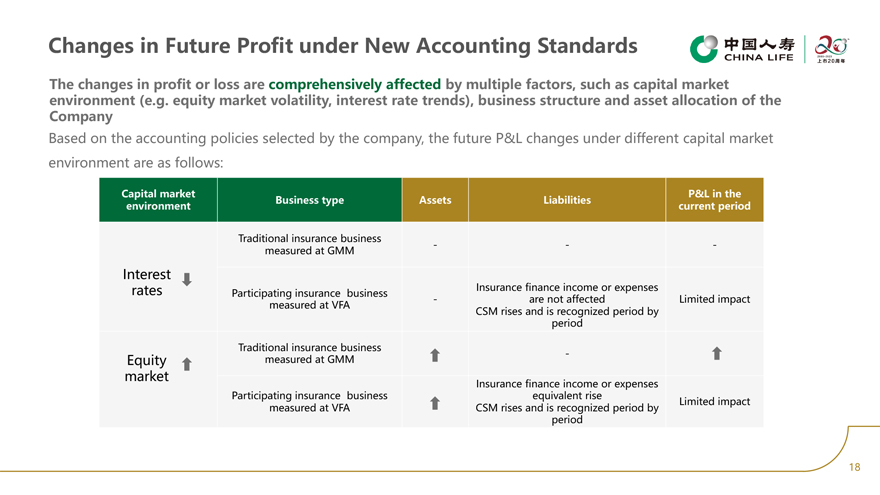

Changes in Future Profit under New Accounting Standards The changes in profit or loss are comprehensively affected by multiple factors, such as capital market environment (e.g. equity market volatility, interest rate trends), business structure and asset allocation of the Company Based on the accounting policies selected by the company, the future P&L changes under different capital market environment are as follows: Capital market P&L in the Business type Assets Liabilities environment current period Traditional insurance business — -measured at GMM Interest rates Insurance finance income or expenses Participating insurance business—are not affected Limited impact measured at VFA CSM rises and is recognized period by period Traditional insurance business -Equity measured at GMM market Insurance finance income or expenses Participating insurance business equivalent rise Limited impact measured at VFA CSM rises and is recognized period by period 18

Impacts on Operations and Management

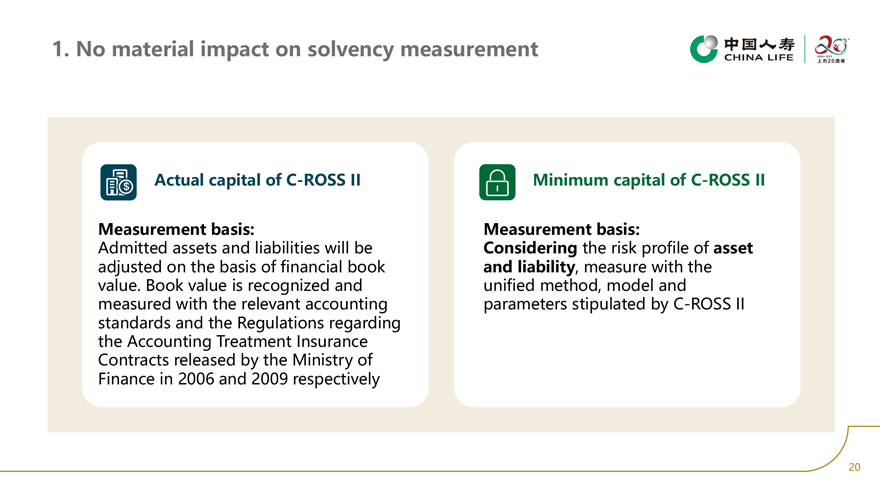

Measurement basis: Considering the risk profile of asset and liability, measure with the unified method, model and parameters stipulated by C-ROSS II Minimum capital of C-ROSS II Actual capital of C-ROSS II Measurement basis: Admitted assets and liabilities will be adjusted on the basis of financial book value. Book value is recognized and measured with the relevant accounting standards and the Regulations regarding the Accounting Treatment Insurance Contractsreleased by the Ministry of Finance in 2006 and 2009 respectively 1. No material impact on solvency measurement

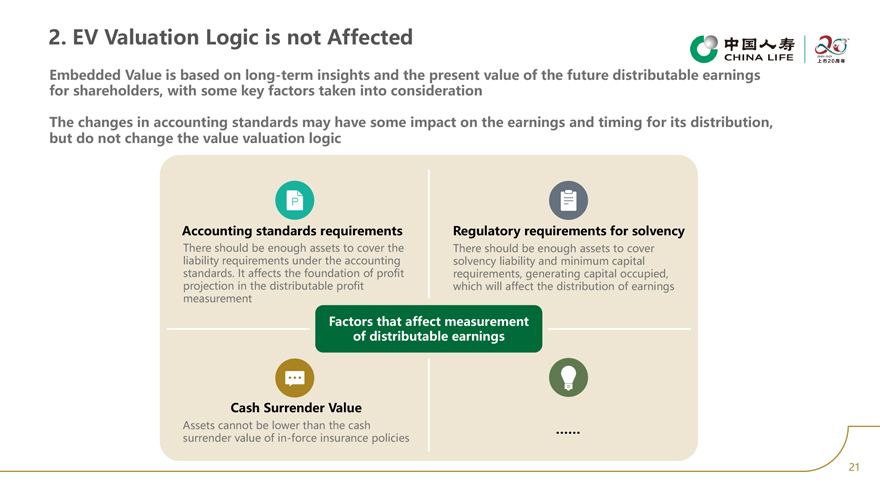

2. EV Valuation Logic is not Affected Embedded Value is based on long-term insights and the present value of the future distributable earnings for shareholders, with some key factors taken into consideration The changes in accounting standards may have some impact on the earnings and timing for its distribution, but do not change the value valuation logic Accounting standards requirements Regulatory requirements for solvency There should be enough assets to cover the There should be enough assets to cover liability requirements under the accounting solvency liability and minimum capital standards. It affects the foundation of profit requirements, generating capital occupied, projection in the distributable profit which will affect the distribution of earnings measurement Factors that affect measurement of distributable earnings Cash Surrender Value Assets cannot be lower than the cash …… surrender value of in-force insurance policies 21

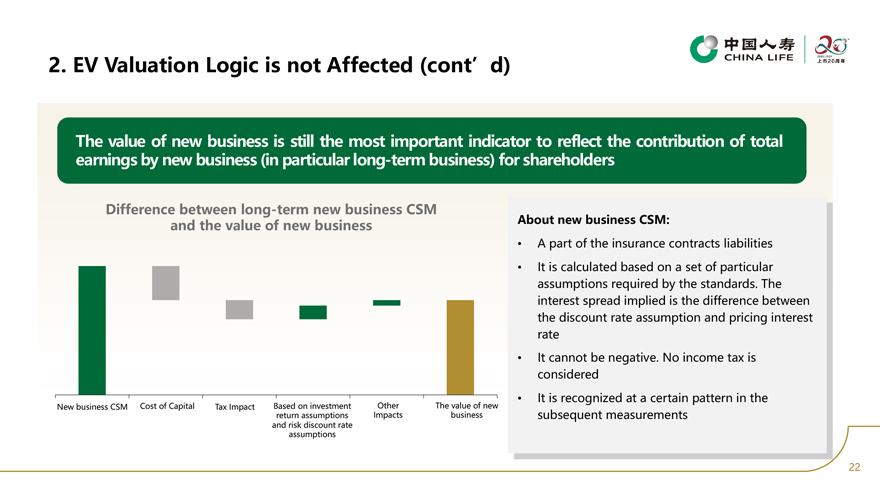

2. EV Valuation Logic is not Affected (cont’d) The value of new business is still the most important indicator to reflect the contribution of total earnings by new business (in particular long-term business) for shareholders Difference between long-term new business CSM and the value of new business About new business CSM: A part of the insurance contracts liabilities It is calculated based on a set of particular assumptions required by the standards. The interest spread implied is the difference between the discount rate assumption and pricing interest rate It cannot be negative. No income tax is considered It is recognized at a certain pattern in the New business CSM Cost of Capital Tax Impact Based on investment Other The value of new return assumptions Impacts business subsequent measurements and risk discount rate assumptions 22

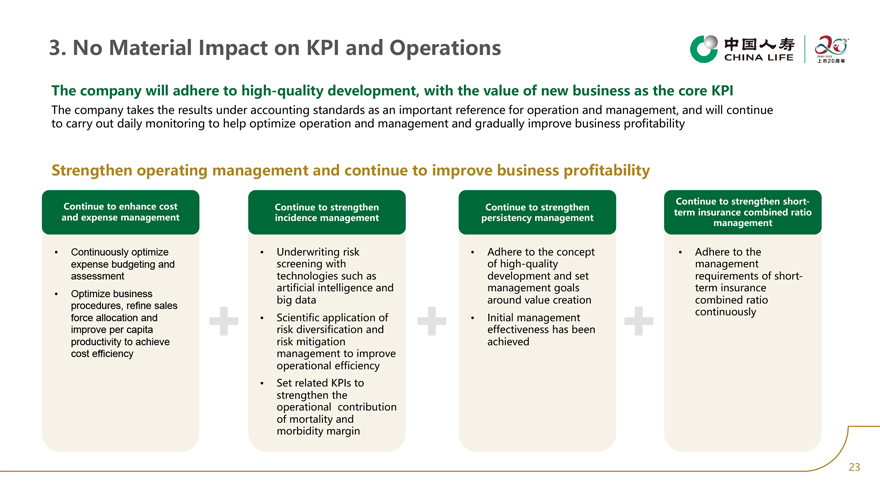

3. No Material Impact on KPI and Operations The company will adhere to high-quality development, with the value of new business as the core KPI The company takes the results under accounting standards as an important reference for operation and management, and will continue to carry out daily monitoring to help optimize operation and management and gradually improve business profitability Strengthen operating management and continue to improve business profitability Continue to strengthen short-Continue to enhance cost Continue to strengthen Continue to strengthen term insurance combined ratio and expense management incidence management persistency management management Continuously optimize Underwriting risk Adhere to the concept Adhere to the expense budgeting and screening with of high-quality management assessment technologies such as development and set requirements of short-artificial intelligence and management goals term insurance Optimize business big data around value creation combined ratio procedures, refine sales continuously force allocation and Scientific application of Initial management improve per capita risk diversification and effectiveness has been productivity to achieve risk mitigation achieved cost efficiency management to improve operational efficiency Set related KPIs to strengthen the operational contribution of mortality and morbidity margin 23

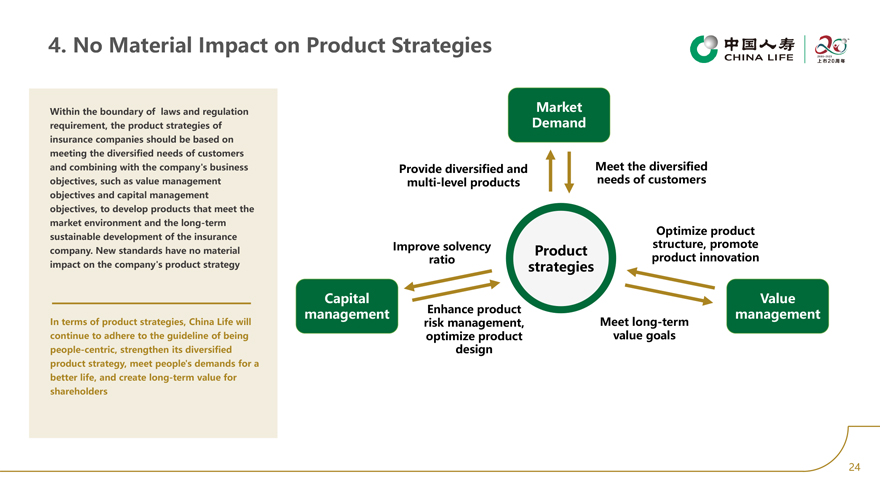

4. No Material Impact on Product Strategies Within the boundary of laws and regulation Market requirement, the product strategies of Demand insurance companies should be based on meeting the diversified needs of customers and combining with the company’s business Provide diversified and Meet the diversified objectives, such as value management multi-level products needs of customers objectives and capital management objectives, to develop products that meet the market environment and the long-term Optimize product sustainable development of the insurance Improve solvency structure, promote company. New standards have no material Product ratio product innovation impact on the company’s product strategy strategies Capital Value management Enhance product management In terms of product strategies, China Life will risk management, Meet long-term continue to adhere to the guideline of being optimize product value goals people-centric, strengthen its diversified design product strategy, meet people’s demands for a better life, and create long-term value for shareholders 24

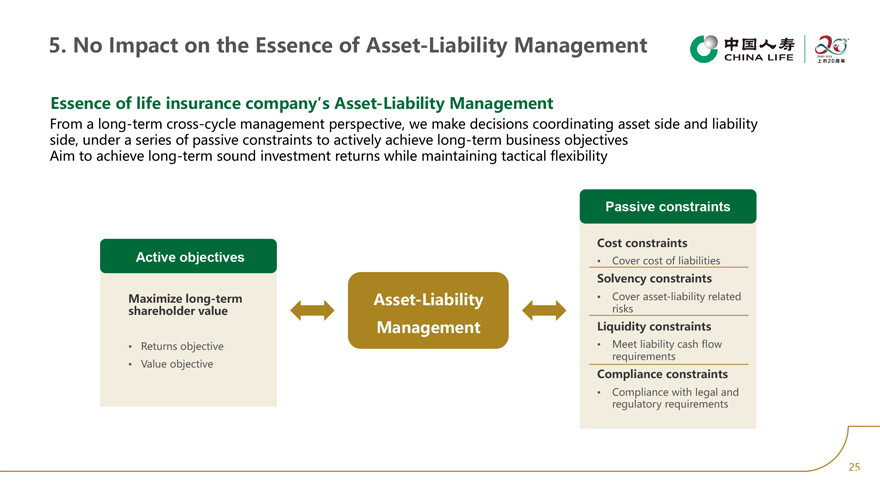

5. No Impact on the Essence of Asset-Liability Management Essence of life insurance company’s Asset-Liability Management From a long-term cross-cycle management perspective, we make decisions coordinating asset side and liability side, under a series of passive constraints to actively achieve long-term business objectives Aim to achieve long-term sound investment returns while maintaining tactical flexibility Passive constraints Cost constraints Active objectives Cover cost of liabilities Solvency constraints Maximize long-term Asset-Liability Cover asset-liability related shareholder value risks Management Liquidity constraints Returns objective Meet liability cash flow requirements Value objective Compliance constraints Compliance with legal and regulatory requirements 25 25

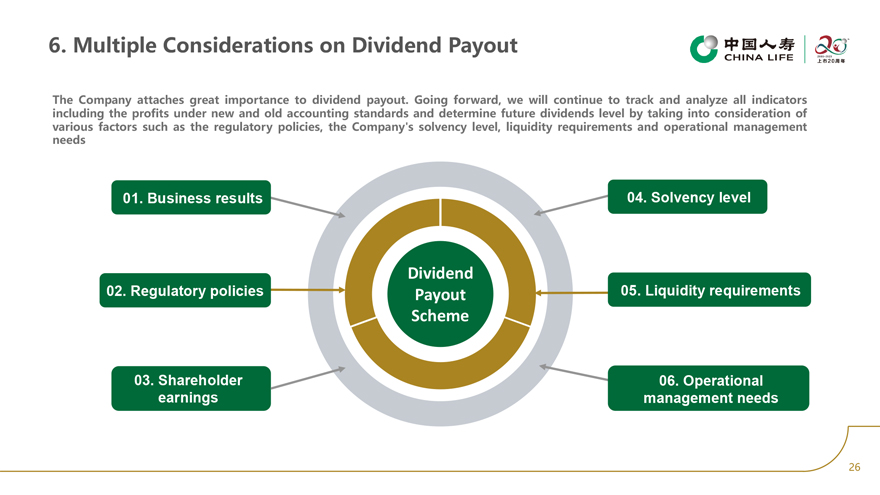

6. Multiple Considerations on Dividend Payout The Company attaches great importance to dividend payout. Going forward, we will continue to track and analyze all indicators including the profits under new and old accounting standards and determine future dividends level by taking into consideration of various factors such as the regulatory policies, the Company’s solvency level, liquidity requirements and operational management needs 01. Business results 04. Solvency level Dividend 02. Regulatory policies Payout 05. Liquidity requirements Scheme 03. Shareholder 06. Operational earnings management needs 26

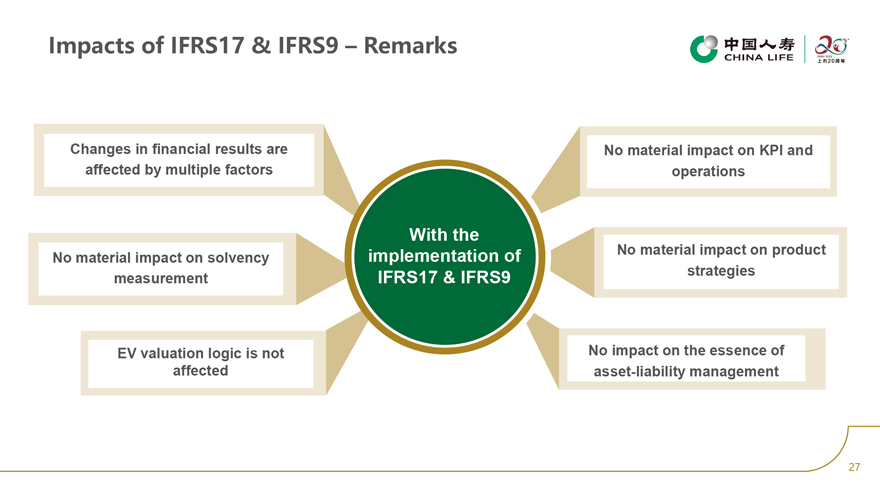

Impacts of IFRS17 & IFRS9 – Remarks Changes in financial results are No material impact on KPI and affected by multiple factors operations With the implementation of No material impact on product No material impact on solvency strategies measurement IFRS17 & IFRS9 EV valuation logic is not No impact on the essence of affected asset-liability management 27

Q&A

Appendix

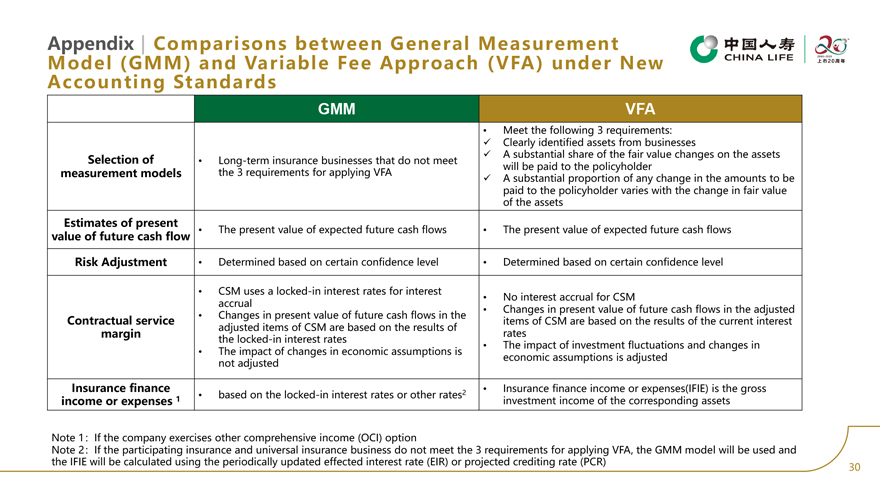

Appendix Comparisons between General Measurement Model (GMM) and Variable Fee Approach (VFA) under New Accounting Standards GMM VFA Meet the following 3 requirements: Clearly identified assets from businesses Selection of A substantial share of the fair value changes on the assets Long-term insurance businesses that do not meet will be paid to the policyholder measurement models the 3 requirements for applying VFA A substantial proportion of any change in the amounts to be paid to the policyholder varies with the change in fair value of the assets Estimates of present value of future cash flow The present value of expected future cash flows The present value of expected future cash flows Risk Adjustment Determined based on certain confidence level Determined based on certain confidence level CSM uses a locked-in interest rates for interest accrual No interest accrual for CSM Changes in present value of future cash flows in the Changes in present value of future cash flows in the adjusted Contractual service items of CSM are based on the results of the current interest adjusted items of CSM are based on the results of margin rates the locked-in interest rates The impact of investment fluctuations and changes in The impact of changes in economic assumptions is economic assumptions is adjusted not adjusted Insurance finance 2 Insurance finance income or expenses(IFIE) is the gross 1 based on the locked-in interest rates or other rates income or expenses investment income of the corresponding assets Note 1 If the company exercises other comprehensive income (OCI) option Note 2 If the participating insurance and universal insurance business do not meet the 3 requirements for applying VFA, the GMM model will be used and the IFIE will be calculated using the periodically updated effected interest rate (EIR) or projected crediting rate (PCR) 30

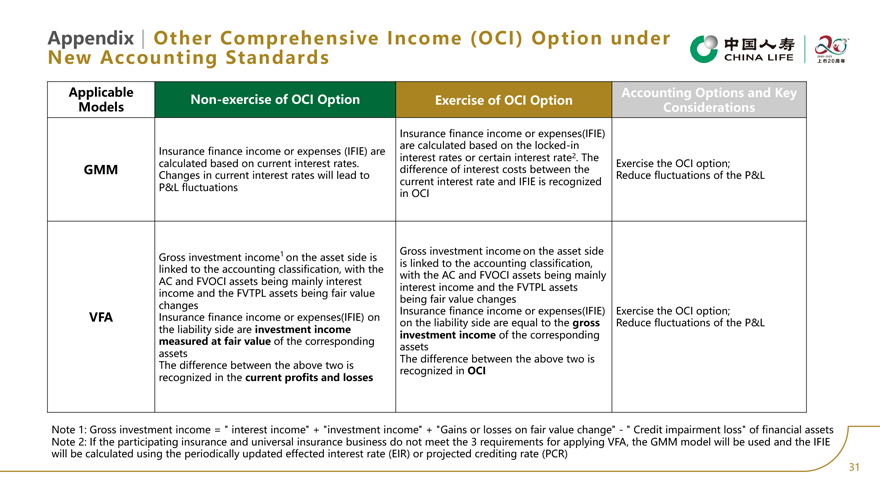

Appendix Other Comprehensive Income (OCI) Option under New Accounting Standards Applicable Accounting Options and Key Non-exercise of OCI Option Exercise of OCI Option Models Considerations Insurance finance income or expenses(IFIE) are calculated based on the locked-in Insurance finance income or expenses (IFIE) are 2 interest rates or certain interest rate . The calculated based on current interest rates. Exercise the OCI option; GMM difference of interest costs between the Changes in current interest rates will lead to Reduce fluctuations of the P&L current interest rate and IFIE is recognized P&L fluctuations in OCI 1 Gross investment income on the asset side Gross investment income on the asset side is is linked to the accounting classification, linked to the accounting classification, with the with the AC and FVOCI assets being mainly AC and FVOCI assets being mainly interest interest income and the FVTPL assets income and the FVTPL assets being fair value being fair value changes changes Insurance finance income or expenses(IFIE) Exercise the OCI option; VFA Insurance finance income or expenses(IFIE) on on the liability side are equal to the gross Reduce fluctuations of the P&L the liability side are investment income investment income of the corresponding measured at fair value of the corresponding assets assets The difference between the above two is The difference between the above two is recognized in OCI recognized in the current profits and losses Note 1: Gross investment income = interest income + investment income + Gains or losses on fair value change — Credit impairment loss of financial assets Note 2: If the participating insurance and universal insurance business do not meet the 3 requirements for applying VFA, the GMM model will be used and the IFIE will be calculated using the periodically updated effected interest rate (EIR) or projected crediting rate (PCR) 31

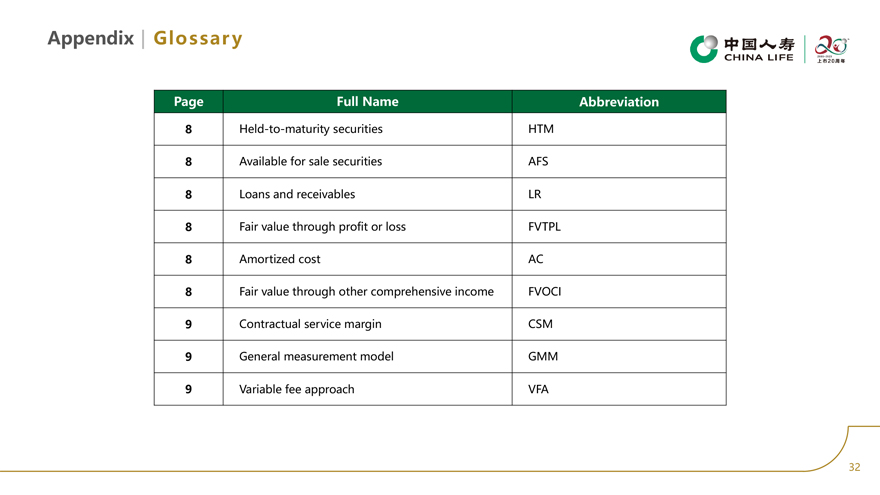

Appendix Glossar y Page Full Name Abbreviation 8 Held-to-maturity securities HTM 8 Available for sale securities AFS 8 Loans and receivables LR 8 Fair value through profit or loss FVTPL 8 Amortized cost AC 8 Fair value through other comprehensive income FVOCI 9 Contractual service margin CSM 9 General measurement model GMM 9 Variable fee approach VFA 32