FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16 of

the Securities Exchange Act of 1934

For the month of June, 2006

Commission File Number: 333-132076

GAS NATURAL SDG, S.A.

(Translation of Registrant’s Name into English)

Av. Portal de L’Angel, 20-22

08002 Barcelona, Spain

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file

annual reports under cover Form 20-F or Form 40-F:

Form 20-F x Form 40-F ¨

Indicate by check mark if the registrant is submitting the Form 6-K

in paper as permitted by Regulation S-T Rule 101(b)(1):

Yes ¨ No x

Indicate by check mark if the registrant is submitting the Form 6-K

in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes ¨ No x

Indicate by check mark whether by furnishing the information

contained in this Form, the Registrant is also thereby furnishing the information to the

Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934:

Yes ¨ No x

If “Yes” is marked, indicate below the file number assigned to the registrant

in connection with Rule 12g3-2(b):N/A

Annual General Meeting Gas Natural SDG, S.A. * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * |

Disclaimer In connection with the offer by Gas Natural SDG, S.A. (Gas Natural) to acquire 100% of the share capital of Endesa, S.A. (Endesa), Gas Natural has filed with the United States Securities and Exchange Commission (SEC) a registration statement on Form F-4 (File No.: 333-132076), which includes a prospectus and related exchange offer materials to register the Gas Natural ordinary shares (including Gas Natural ordinary shares represented by Gas Natural American Depositary Shares (ADSs)) to be issued in exchange for Endesa ordinary shares held by U.S. persons and for Endesa ADSs held by holders wherever located. In addition, Gas Natural has filed a Statement on Schedule TO with the SEC in respect of the exchange offer. INVESTORS AND HOLDERS OF ENDESA SECURITIES ARE URGED TO READ THE REGISTRATION STATEMENT AND THE PROSPECTUS, THE STATEMENT ON SCHEDULE TO, AND ANY OTHER RELEVANT DOCUMENTS FILED WITH THE SEC, AS WELL AS ANY AMENDMENTS AND SUPPLEMENTS TO THOSE DOCUMENTS, BECAUSE THEY CONTAIN IMPORTANT INFORMATION. Investors and security holders may obtain free copies of the registration statement, the prospectus and related exchange offer materials and the Statement on Schedule TO, as well as other relevant documents filed with the SEC, at the SEC’s website at www.sec.gov. The prospectus and other transaction-related documents are being mailed to holders of Endesa securities eligible to participate in the U.S. offer and additional copies may be obtained for free from Georgeson Shareholder Communications, Inc., the information agent: 17 State Street, 10th Floor, New York, New York 10004, Toll Free (888) 206-0860, Banks and Brokers (212) 440-9800. This communication is not an offering document and does not constitute an offer to sell or the solicitation of an offer to buy securities or a solicitation of any vote or approval, nor shall there be any sale or exchange of securities in any jurisdiction in which such offer, solicitation or sale or exchange would be unlawful prior to the registration or qualification under the laws of such jurisdiction. The solicitation of offers to buy Gas Natural ordinary shares (including Gas Natural ordinary shares represented by Gas Natural ADSs) in the United States will only be made pursuant to a prospectus and related offering materials that will be mailed to holders of Endesa ADSs and U.S. holders of Endesa ordinary shares. Investors in ordinary shares of Endesa should not subscribe for any Gas Natural ordinary shares to be issued in the offer to be made by Gas Natural in Spain except on the basis of the final approved and published offer document in Spain that will contain information equivalent to that of a prospectus pursuant to Directive 2003/71/EC and Regulation (EC) No. 809/2004. These materials may contain forward-looking statements based on management’s current expectations or beliefs. These forward-looking statements may relate to, among other things: • management strategies; • synergies and cost savings; • integration of the businesses; • market position; • expected gas and electricity mix and volume increases; • planned asset disposals and capital expenditures; • net debt levels and EBITDA and earnings per share growth; • dividend policy; and • timing and benefits of the offer and the combined company. These forward-looking statements are subject to a number of factors and uncertainties that could cause actual results to differ materially from those described in the forwarding-looking statements, including, but not limited to, changes in regulation, the natural gas and electricity industries and economic conditions; the ability to integrate the businesses; obtaining any applicable governmental approvals and complying with any conditions related thereto; costs relating to the offer and the integration; litigation; and the effects of competition. Forward-looking statements may be identified by words such as “believes,” “expects,” “anticipates,” “projects,” “intends,” “should,” “seeks,” “estimates,” “future” or similar expressions. These statements reflect our current expectations. In light of the many risks and uncertainties surrounding these industries and the offer, you should understand that we cannot assure you that the forward-looking statements contained in these materials will be realized. You are cautioned not to put undue reliance on any forward-looking information. This communication is not for publication, release or distribution in or into or from Australia, Canada or Japan or any other jurisdiction where it would otherwise be prohibited. * * * * |

Introduction 1. State of the Energy Markets 2. Financial Year 2005 3. 2006 1 st Quarter Results 4. Tender Offer for Endesa 5. Corporate Governance and Responsibility 6. Strategic Positioning Agenda ************ * * * * |

Salvador Gabarró Chairman * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * ** * * * * |

Introduction * * * * * * * * * * * |

Rafael Villaseca Chief Executive Officer * * * * * * * * * |

State of the Energy Markets * * * * * * * |

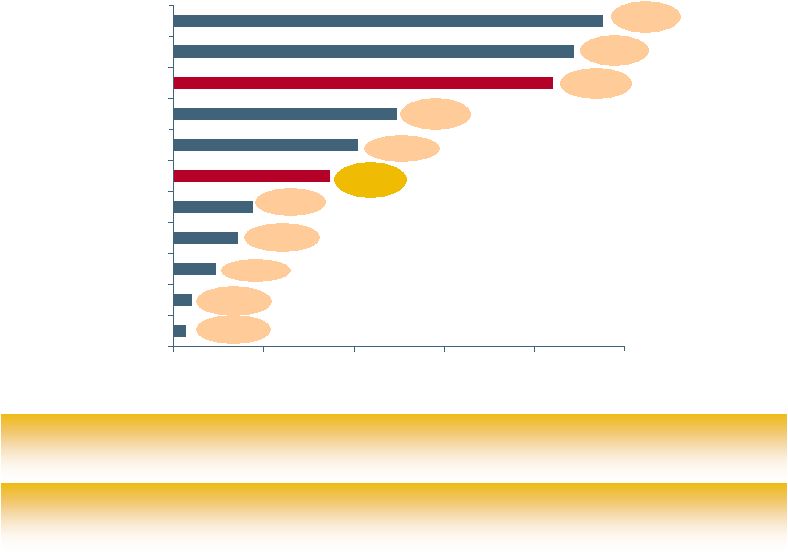

8 Gas demand in Europe has grown as a consequence of the low maturity of some markets and the introduction of CCGTs 0 20 40 60 80 100 Greece Ireland Austria Hungary Belgium Spain Holland France Italy Germany United Kingdom (Bcm) +3% +4% +5% +2% +14% +0% +3% +4% +1% (3%) +6% Gas demand in Europe Source: Eurogas Gas demand in main European countries in 2005 (2005 and annual growth versus 2000) The Spanish market has been the main growth contributor in the European gas market * * * |

9 0 50 100 150 200 250 300 350 400 2000 2001 2002 2003 2004 2005 Gas demand growth in Europe Source: CNE (Monthly bulletin on natural gas statistics) Gas demand evolution in Spain Continued growth in Spanish gas demand during the last years Spanish energy matrix (2005) Source: Quarterly bulletin on energy situation, Ministry of Industry, tourism and commerce +17.6% CAGR: +13.8% Nuclear* 11% Coal* 15% Oil 51% Hydro, Renewables & Other 4% Natural gas 20% * |

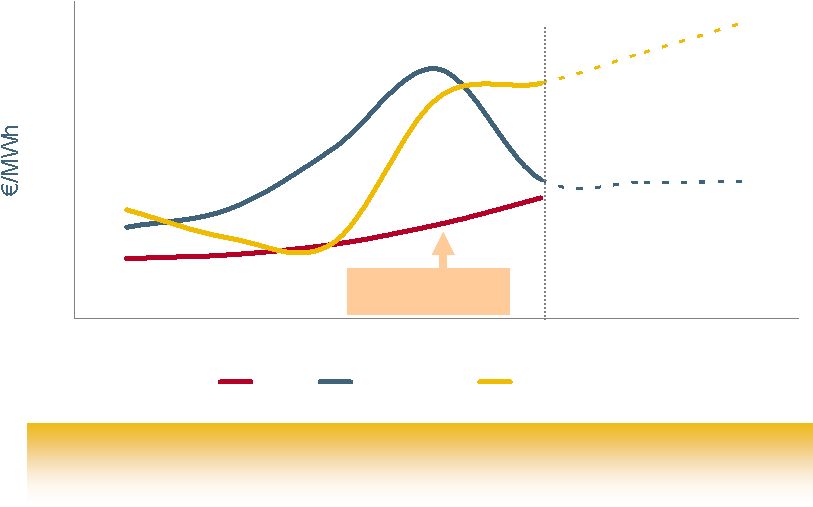

10 5 10 15 20 25 30 35 40 45 Q1 05 Q2 05 Q3 05 Q4 05 Q1 06 6m Fut CMP Henry Hub NBP Recent evolution of gas prices Source: CNE (Monthly bulletin on natural gas statistics), Bloomberg and own elaboration Divergence between CMP and international gas prices has been corrected Recognition of real cost of gas * * * |

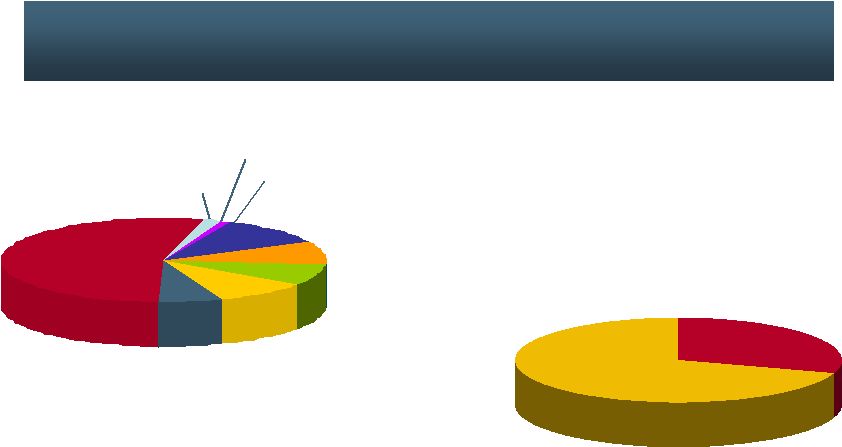

11 0 50 100 150 200 250 300 2000 2001 2002 2003 2004 2005 Electricity demand growth in Spain Source: Red Eléctrica Electricity demand has grown at over 4% annually during the last years +4.3% Electricity demand evolution in Spain Electricity production mix (2005) Source: Red Eléctrica, peninsular system, ordinary regime CAGR: +4.8% Coal 29% Nuclear 22% Fuel-Gas 4% Wind 8% Hydro 7% Other renewable 12% CCGT 18% * |

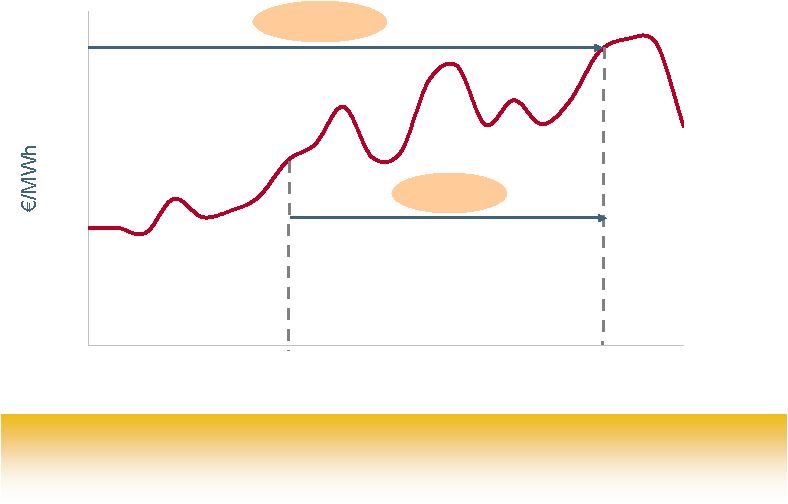

12 0 10 20 30 40 50 60 70 80 Jun-04 Sep-04 Dec-04 Mar-05 Jun-05 Sep-05 Dec-05 Mar-06 Evolution of electricity generation prices Source: OMEL, average monthly price Pool price in Spain grew by 60% during 2005 and 150% from June 2004 to December 2005 +58.9% +149.5% * * * |

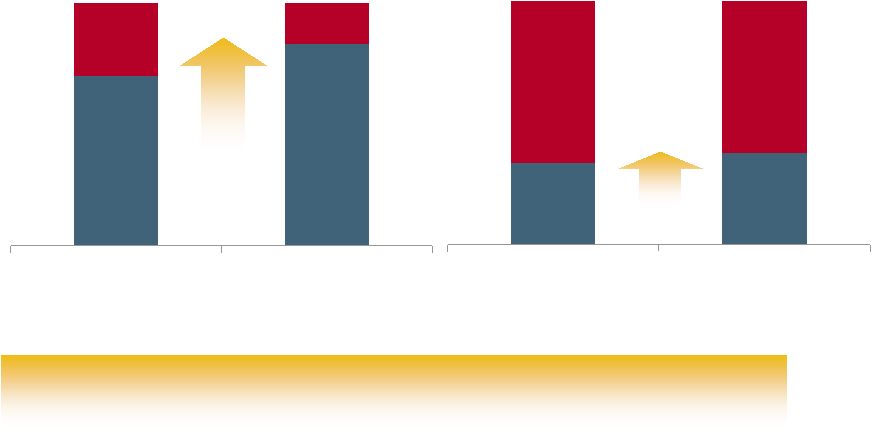

13 2004 2005 Liberalisation of the Spanish energy markets The gas market has advanced more than the electricity market in terms of real liberalisation Electricity market (volume) Source: CNE monthly bulletin Gas market (volume) Source: CNE 2005 information bulletin +13p.p. Regulated Liberalised 30% 70% 17% 83% 2004 2005 66% 34% 62% 38% +4p.p. |

14 Evolution in the liberalisation of the gas sector Regulated tariffs to disappear by 2008 Separation of distribution and regulated commercialisation Creation of the “Supplier of Last Resort” Creation of a “Supplier Switching Office” Creation of an Energy System Technical Management Oversight Committee Main measures adopted Full liberalisation in 2008 Liberalisation in the gas sector is a reality: there is no need to apply structural changes Elimination of tariffs for industrial clients 83% of volume liberalised, in line with objectives set Current situation * * * |

15 New market rules designed to eliminate tariff deficit: 42.35 €/MWh cap on sales to the regulated market Value of CO 2 emission rights awarded for free discounted Tariff methodology that does not include the real cost energy A regulated electricity tariff together with the generation market leads to a tariff deficit (€3,830 million euro in 2005) Set back in the liberalization process, with clients coming back to the regulated market Measures taken Criticisms to the generation market from the White Book and the Ministry of Industry: New legislation to solve some of the problems of the Spanish electricity sector * * * |

16 Advance in the liberalisation of the electricity sector Regulated tariffs to disappear by 2011 Legal and functional separation of distribution and regulated commercialisation Creation of the “Supplier of Last Resort” Creation of the “Supplier Switching Office” Creation of a Energy System Technical Management Oversight Committee to ensure security of supply Main measures adopted End of transitory period by 2011 Need to reorganise the generation market * * * |

17 Gas expected to play an increasingly important role to meet Europe’s energy demand Sizeable increase in gas consumption compared to other traditional sources of energy such as coal and nuclear Source: IEA, World Energy Outlook 0 200 400 600 800 1971 2002 2010 2030 Coal Fuel-oil Gas Nuclear Others * * * |

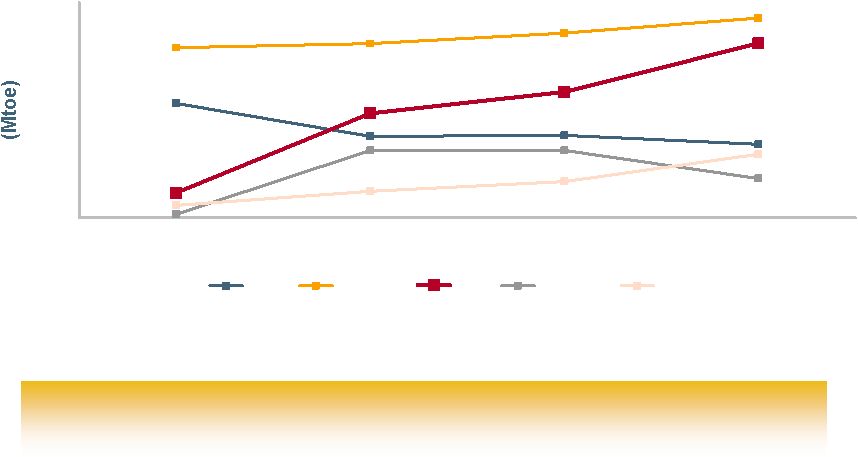

18 The electricity sector is expected to be the main gas consumer in Europe... Most of the growth in demand to come from electricity generation Source: IEA, World Energy Outlook Generation Industry Other 600 700 800 1980 1990 2000 2030 bcm 2010 2020 200 300 400 500 100 * * * |

19 Source: European Energy and Transport Trends … at the same time gas – fired generation is expected to become the main source of electricity Gas – power convergence in Europe is a reality 0% 20% 40% 60% 80% 100% 1990 2000 2010 2020 2030 Nuclear Hydro Wind Fossil Fuel CCGT Others * * * |

20 LNG is expected to be increasingly important to satisfy the growing gas demand in Europe Source: BP Statistical Review, UBS Research LNG expected to play a key role to diversify gas procurement and guarantee security of supply 0 100 200 300 400 500 600 700 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 Domestic production Russia Algeria LNG Other * * |

21 Spain is expected to be one of the main contributors to gas demand growth in Europe Gas natural consumption in Spain is expected to continue to grow at faster rates than in the rest of Europe Source: Future Natural Gas Demand in Europe. Oxford Institute for Energy Studies Expected gas demand annual growth 0% 2% 4% 6% 8% 2004-2010 2010-2015 * * |

22 Gas – power convergence can also be noticed in Spain Increasing importance of CCGTs in generation Growing gas peak demand mainly due to electricity generation Source: Review of the Plan for Electricity and Gas Sectors for 2002-2011 The Government’s recent Review of the Electricity and Gas sectors 2002 – 2011 planning increases by 28% its objective of installed CCGT capacity in 2011. A 184% increase in CCGT capacity is expected from 2005 0% 20% 40% 60% 80% 100% 2000 2005 2007 2011 Coal Nuclear Natural gas Oil Renewables 0 500 1,000 1,500 2,000 2,500 3,000 2004 2005 2006 2007 2008 2009 2010 2011 Electricity generation Conventional gas market * * |

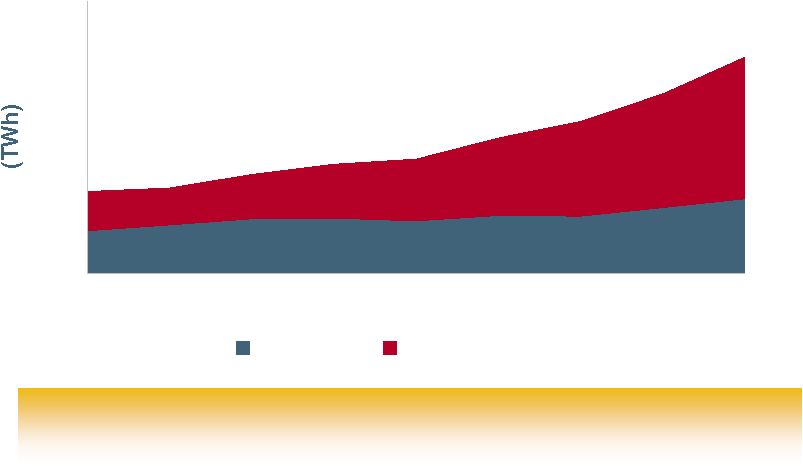

23 0 100 200 300 400 500 1997 1998 1999 2000 2001 2002 2003 2004 2005 Natural gas Liquified natural gas The Spanish gas market is even more dependent on LNG than the rest of Europe LNG represents approximately 2/3 of the gas imported in Spain Source: CNE * * * |

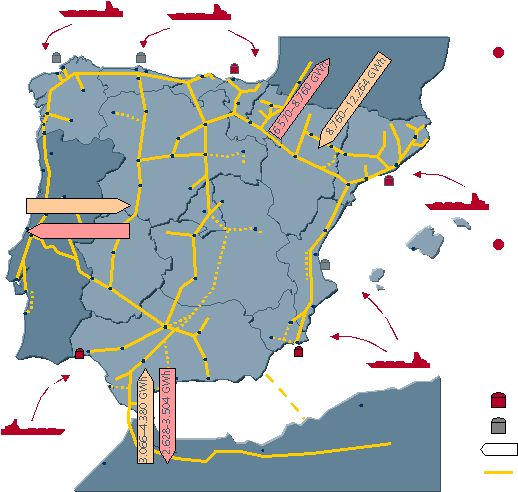

24 Guaranteeing security of supply is a priority in Spain Gas procurement through the Europe – Maghreb pipeline (~1/3 of total) and LNG tankers (~2/3) Electric interconnection with France only amounts to 3-4% of total demand in Spain 5.256-7.446 GWh 6.570-9.198 GWh Cartagena Huelva Barcelona Ferrol Bilbao Regassification plant Pipeline Import/Export electricity capacity Gijón Sagunto Regassification plant under construction * * * |

Financial Year 2005 2005 Operating Review Significant Events in 2005 2005 Financial Results Our Team Gas Natural Foundation * * * * * * |

26 1,519 million euro EBITDA 13.7% 749 million euro Net Income 16.7% Exceeding the targets set in the 2004 - 2008 Strategic Plan 2005 Operating review Main financial figures * * * |

27 2005 Operating review 317,555 GWh Gas supply 10.2% Gas distribution 9.7% 100,150 Km Distribution network 1 5.2% Main gas figures 422,912 GWh Note: 1 As of 31st December 2005 * * * |

28 2005 Operating review Main electricity figures 3,373 MW Installed capacity 10,466 GWh Electricity produced 43.9% 6,296 GWh Electricity sales in Spain 41.3% 194.6% * * * |

29 615,000 new clients 10.2 million clients in the world 1 6.4% Main client figures 2005 Operating review Note: 1 Spain, Italy and Latinamerica * * * * * |

30 Capacity of the Maghreb-Europe pipeline increased to 136 TWh / year Creation of GAS NATURAL’s Client Service Guarantee Office Approval of the Code of Conduct for employees Significant events in 2005 1 st Quarter * * * |

31 Acquisition of DERSA Strategic agreement with Repsol YPF: joint participation in upstream projects and creation of a 50/50 Joint Venture for the midstream business Change in the organisational structure to adapt to the strategic challenges implied by GAS NATURAL's growth vision Significant events in 2005 2 nd Quarter * * * |

32 Signing of the first contracts to begin gas natural sales in France Tender offer for 100% of Endesa, S.A. GAS NATURAL is included for the first time in the Dow Jones Sustainability World index (DJSI World) Significant events in 2005 3 rd Quarter * * * |

33 Segregation of regulated gas distribution and secondary gas transportation in Spain Synchronisation of the Escombreras (Cartagena) 1,200 MW CCGT Significant events in 2005 4 th Quarter * * * |

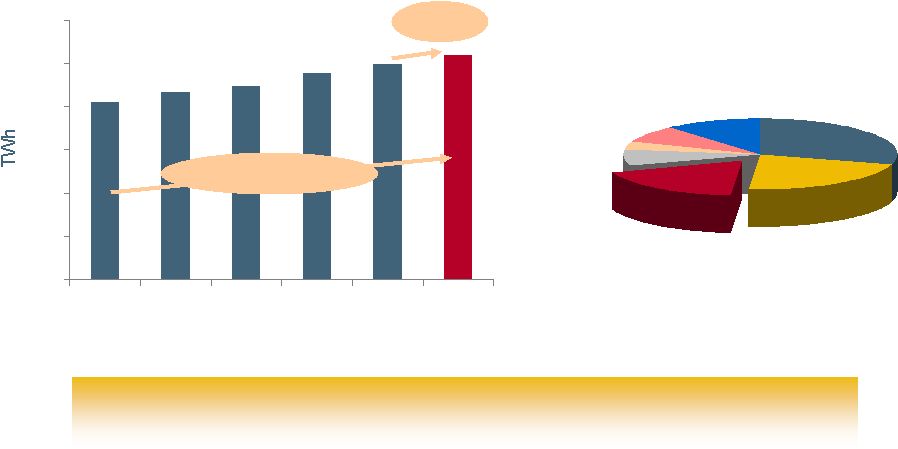

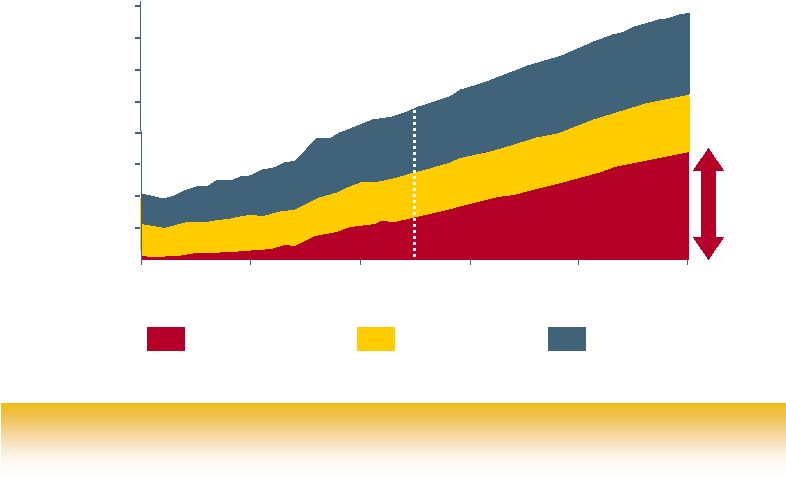

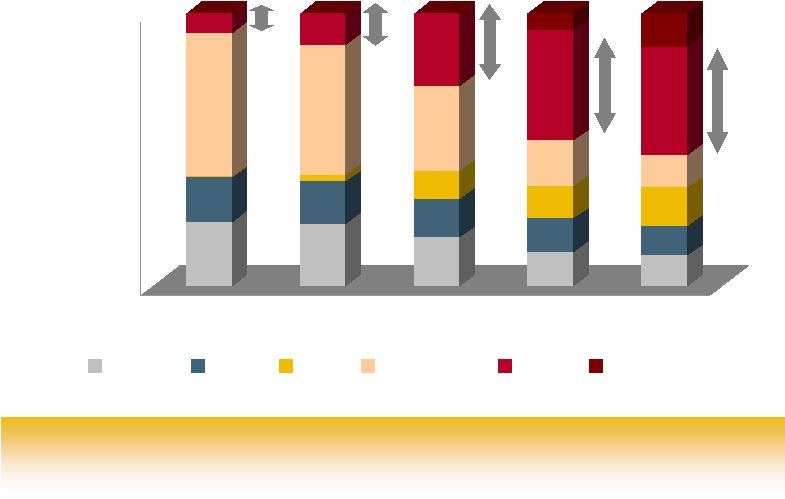

34 (€ million) 2004 974 722 228 24 98 44 54 251 144 107 12 1,335 2005 1,122 778 317 27 152 90 62 237 176 61 8 1,519 15.2 7.7 39.0 14.2 54.9 102.7 15.6 -5.8 21.6 -42.8 -31.1 13.7 % EBITDA breakdown Distribution Spain LatAm Italy Electricity Spain Puerto Rico Gas Up + Midstream Wholesale and Retail Other Total EBITDA 2005 financial results Note: Figures rounded to closest million euro * * * |

35 Distribution in Spain Regulated gas sales and TPA 254,774 GWh 39,611 Km 5.1 million 2,077 Km added to network 11.3% 325,000 new customer connections 2005 financial results GAS NATURAL is the main gas distribution company in the Iberian Peninsula, and the Spanish utility with more new clients in 2005 1 Note: 1 Regulated clients * * * |

36 2002 2003 2004 2005 Distribution in Spain Notes: 1 2002 and 2003 data as per Spanish GAAP, 2004 and 2005 under IFRS 2 Not taking into account the effect of the prior regulatory regime in the first quarter of 2002 Stable regulatory regime that allows for gas network growth and sector liberalisation 2005 financial results 660 722 778 (€ million) +7.7% +9.4% +15.9% 569 2 Spain distribution EBITDA * * * |

37 6.5% Distribution in LatAm Regulated gas sales and TPA 165,408 GWh Strong growth in Brazil and Colombia in all markets Argentina’s recovery confirmed in the second half of the year Stable EBITDA growth in Mexico despite prices linked to Southern US market 16.2% Brazil 14.9% Colombia 3.7% Argentina 0.3% Mexico 2005 financial results * * * |

38 Distribution in LatAm 253,000 new customer connections 4.8 million 56,763 Km 2,643 new network km 2005 financial results Mexico 1.1 (23%) Colombia 1.6 (34%) Argentina 1.3 (27%) Brazil 0.8 (16%) GAS NATURAL is the first non State-owned gas distribution company in LatAm, and a leader adding new clients * * |

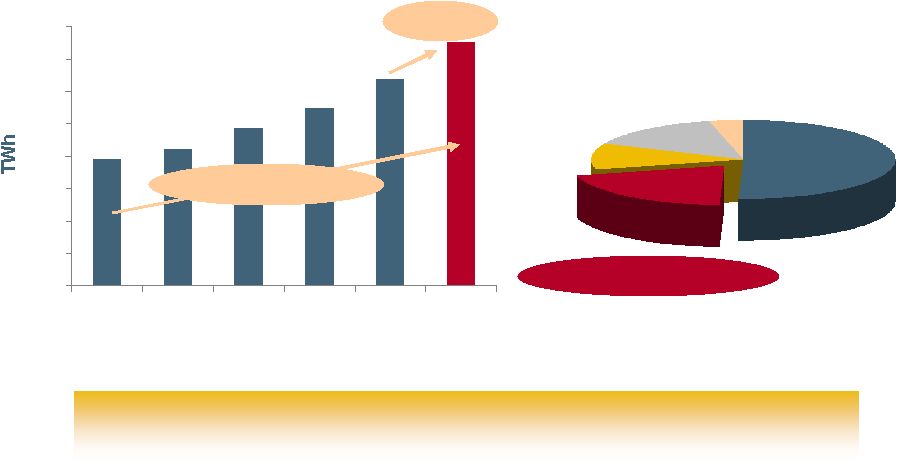

39 152 228 317 2003 2004 2005 65 73 83 97 Q1 Q2 Q3 Q4 Distribution in LatAm 2005 quarterly EBITDA EBITDA evolution 2003 - 2005 Sustained growth over the past years 2005 financial results +50.0 +39.0% Notes: 1 2003 data under Spanish GAAP, 2004 and 2005 under IFRS (€ million) (€ million 1 ) * * * |

40 Distribution in Italy Regulated gas sales and TPA 2,730 GWh 3,776 Km 288,000 7.9% network growth 101.5% 14.3% customer connections growth Organic growth sustained by our know-how €27 million EBITDA (+14.2%) 2005 financial results * * * |

41 Spain—Electricity Installed capacity 3,102 MW DERSA acquisition 2,800 MW CCGT 254.9% 302 MW Wind and cogen 2 GAS NATURAL is the Spanish utility that has increased more its market share in generation during the last five years and the Spanish utility that has installed more CCGTs in 2005 2005 financial results +1,000 MW in new projects Notes: 1 Synchronisation at the end of 2005, fully operative in the first quarter 2006 2 Attributable power EBITDA has doubled, reaching € 90 million Incorporation of Arrúbal (800 MW) and Cartagena 1 (1,200 MW) * * * |

Puerto Rico—Electricity Electricity production 1,562 GWh 50% stake in a 540MW CCGT Increased load factor 66% 70% 6.3% €62 million EBITDA (+15.6%) 2005 financial results * * * |

43 26.2% Gas—Up + Midstream 145,923 GWh Transported through EMPL Advances in the upstream agreement: Gassi Touil in development phase € 176 million EBITDA (+21.6%) 2005 financial results One of the largest tanker fleets in the Atlantic Midstream Joint Venture established with Repsol YPF in 2005 * * * |

44 10.2% Gas—Wholesale and Retail 317,555 GWh Gas sales 211,895 GWh 16.3% growth sales to the liberalised market € 61 million EBITDA 2005 financial results GAS NATURAL is the main gas purchaser in Spain and a leader in the global LNG market * * * |

45 Gas—Wholesale and Retail 2005 financial results The appropriate measures have been taken ... Reduction in 2005 EBITDA due to competitive conditions and the state of the international markets Adapting our gas portfolio to new market conditions, both in volumes and in discounts €25 million EBITDA in Q106 substantially higher (+85.9%) than Q105 ... and results are already visible * * * |

46 Multiproduct Sales network: 877 points of sale Strong and well-established brand in Spain 1,5 million eligible residential gas customers 1,4 million maintenance contracts 80% residential gas customers retained 0,5 million residential electricity customers GAS NATURAL is the leading Spanish energy company in the multiservice business 2005 financial results 1.47 contracts per customer as of December 31, 2005 * * * |

47 1,188 million euro Tangible and intangible investments 17.8% DERSA acquisition Financial investments 296 million euro Distribution 52% Other 6% Gas 4% Electricity 38% 2005 financial results * * * |

48 Net Debt and leverage 1 Notes: 1 2004 and 2005 data under IFRS 2 Defined as net debt/ (net debt + total equity) 3,677 1,627 1,869 2,650 3,615 2001 2002 2003 2004 2005 49.0% 28.0% 29.3% 35.6% 38.5% Leverage 2 2005 financial results * * * |

49 Dividend proposal 0.33 0.40 0.60 0.71 0.84 2001 2002 2003 2004 2005 (€ / share) CAGR +26.3% +18.3% Note: 1 The year represents the fiscal year against which results the dividend is declared Dividend per share 1 2005 financial results Sustained growth of shareholder remuneration through dividend increase * * * |

50 26.0 22.2 47.3 49.5 50.2 2001 2002 2003 2004 2005 (%) Payout ratio 1,2 Reaching the targets set Notes: 1 The year represents the fiscal year against which results the dividend is declared 2 2001, 2002 and 2003 under Spanish GAAP, 2004 and 2005 under IFRS 2005 financial results * * * |

51 Strong financial performance in 2005 despite a difficult market environment and operating conditions Conclusions Strong EBITDA, Net Income and Dividend, growth based on cash generation Positive trends shown in 2005 expected to materialise in 2006, boosting growth and profitability 2005 financial results We continue to exceed the targets set in our 2004-2008 Strategic Plan * * * |

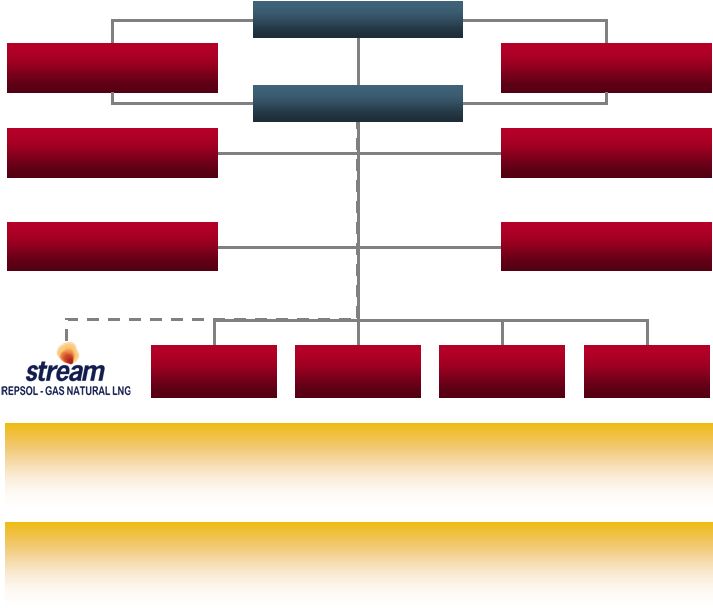

52 Chairman Communication and Chairman’s office C.E.O. C.F.O. Internal Audit Legal Services Corporate Resources Our organisation Gas Management Wholesale Retail International Organisation around markets and businesses that ensures integration through the gas value chain Strategy and Development Efficient operating structure adapted to the strategic challenges resulting from GAS NATURAL’s growth vision * * * |

53 Female 30% Male 70% Our team Number of employees in the world: 6,717 Puerto Rico 78 Mexico 629 Colombia 578 Brazil 560 Argentina 637 Italy 396 Spain 3.731 Morocco 107 France 1 * * * |

54 Professional Development Programs Increase in online learning programs (e-learning) Implementation of ECO and COMPRAS projects Training Courses 2,477 Participants 5,695 37.7% of the workforce are university graduates Hours 223,655 Hours per employee 33.30 Our team * * * |

55 Gas Natural Foundation Environment Energy Training Centre Gas History Centre International Numerous actions in different areas Commitment and contribution to the regions where GAS NATURAL is present * * * |

2006 1 st Quarter Results * * * * * * |

57 508 million euro EBITDA 29.3% 277 million euro Net Income 16.3% Exceeding the targets set in the 2004 - 2008 Strategic Plan 2006 1 st Quarter results Main financial magnitudes * * * |

58 2006 1 st Quarter results Advances in Upstream LNG agreement in Nigeria Acquisition of Petroleum Oil & Gas España New Gas conditions Improved client portfolio EBITDA +85.9% Electricity contribution Installed capacity in Spain x2 Improved client portfolio EBITDA +221.3% Distribution Continued solid growth and profitability EBITDA +13.2% Note: Growth rates calculated versus Q105 * * * |

59 Q1 06 3,107 508 358 277 290 3,397 Q1 05 51.9 29.3 29.6 16.3 12.5 29.7 Change (%) 2006 1 st Quarter results Solid financial performance, in line with the 2004-2008 Strategic Plan (€ million) 2,045 393 276 238 258 2,620 Revenues EBITDA EBIT Net Income Investments Net debt (as of 31/03) Note: Figures rounded to the closest million * * * |

60 292 211 65 17 35 22 13 57 44 14 8 393 331 218 93 21 89 71 18 80 55 25 8 508 13.2 3.3 42.7 23.8 155.3 221.3 41.4 38.9 24.4 85.9 (1.2) 29.3 Distribution Spain LatAm Italy Electricity Spain Puerto Rico Gas Up + Midstream Wholesale and Retail Other Total EBITDA 2006 1 st Quarter results Q106 Q105 Change (%) (€ million) EBITDA breakdown Note: Figures rounded to the closest million * * * |

61 The positive trends shown in 2005 are materialising in 2006, boosting growth and profitability 2006 1 st Quarter results Consolidation of GAS NATURAL’s presence in electricity generation Exceeding the targets set in the 2004 - 2008 Strategic Plan Double digit Growth in EBITDA and Net Income based on cash generation Solid and growing distribution business Advances in the development of equity gas * * * |

Tender offer for Endesa S,A, * * * * * |

63 All the regulatory and administrative steps have been taken Spanish antitrust authorities Regulated activities (Function XIV) National Energy Commission The EC confirmed jurisdiction on competition belonged to Spain European antitrust authorities Golden Share Secretary General of Energy Nov 05 Combination GAS NATURAL–Endesa approved by the Council of Ministers Feb 06 Nov 05 Dec 05 Spanish offer/prospectus approved CNMV US prospectus (F-4) declared effective SEC (USA) Feb 06 Mar 06 Note: The offer and therefore the processing of any action related to the offer, and the performance of the agreement between Gas Natural and Iberdrola are currently suspended, following the injunction granted by the Madrid Court for Business Matters Nº3. and the posting by Endesa of a €1,000m guarantee. The Supreme Court has awarded the injunction requested by Endesa consisting of the suspension of the Council of Minister decision, subject to Endesa presenting certain guarantees. GAS NATURAL has appealed both decisions. * * |

64 E.On’s offer acceptance period will have to wait due to GAS NATURAL’s offer 1 Impact of the injunctions Suspension of the Council of Ministers resolution Subject to Endesa presenting certain guarantees, being admissible to extend the ones presented to the Madrid’s Court for Business Matters GAS NATURAL has appealed the decision Court for Business Matters N O. 3 order Supreme Court order Suspension of the processing of GAS NATURAL offer and the performance of the agreement with Iberdrola Subject to Endesa presenting a €1,000 million bond, which was posted on the 5 th of April GAS NATURAL has appealed the Court’s decision As per the CNMV’s note issued on the 24th March 2006 relating to the first of the decisions: Notes: 1 CNMV has indicated that E.On´s offer request continues with the administrative process * * * |

65 Creating a leading, fully integrated, global energy group Combined management of clients and networks More flexible and competitive gas procurement More balanced and competitive generation portfolio Attractive business mix and investment profile Global integrated energy leader in high-growth markets Sizeable synergies A solid strategic, industrial and financial rationale * * * |

Salvador Gabarró Chairman * * * * * * * * * * |

Corporate Governance and Responsibility * * * * * |

68 Corporate responsibility Gas Natural Corporate Responsibility Excellent service Integrity and responsibility Environment preservation Growth and professional development Increasing value and transparency EMPLOYEES Stable relationships and objective selection ENVIRONMENT * * * |

69 Corporate responsibility 2005 Corporate Responsibility Report Fourth Corporate responsibility report published in accordance with the directives published in the “guide for the elaboration of sustainability reports 2002” and reviewed by GRI (Global Reporting Initiative) Verified by an independent external auditor * * * |

70 Entered the Dow Jones Sustainability World Index (DJSI World), and stayed for the second consecutive year in the European index DJSI STOXX Fourth consecutive year in the European index FTSE4Good, which includes companies with the best financial, social and environmental management Certification of the Corporate Responsibility Report by GRI (Global Reporting Initiative) Second position in the sector corporate reputation ranking MERCO Eighth position in the most internationally admired companies ranking prepared by PricewaterhouseCoopers and Financial Times Corporate responsibility The recognition of our efforts * * |

71 Corporate governance The Corporate Governance report contains in a detailed and complete manner information about: Capital structure Government bodies composition and functioning Decision making processes Related parties operations and risk control mechanisms Compliance with the recommendations of good corporate governance Compliance with transparency requisites in management and information * * * |

72 Corporate governance GAS NATURAL has the necessary tools for a good corporate governance of the company: Rules of the Board of Directors and the different commissions: Executive Committee Audit and Compliance Committee Hiring and Compensation Committee Investment, Strategy and Competition Committee Rules of the Shareholder Meeting Internal conduct code relating to capital markets issues Conduct code Recent creation of the Corporate Governance Unit, integrated in the Board’s Secretary office with exclusive dedication * * * |

Strategic Positioning * * * * * * |

74 A multinational leader in the energy sector operating through the whole gas value chain Gas and electricity assets Gas transport and infra- estructure Gas supply and demand Upstream Clients Advancing in the upstream business Consolidation of our leading position in the midstream business Positioned as an important player in the electricity business Maintaining the leadership and profitable growth in our gas distribution business * * |

75 A multinational leader in the energy sector that operates through the whole gas value chain Gas and electricity assets Gas transport and infra- estructure Gas supply and demand Upstream Clients Integrated LNG project in Gassi Touil (Algeria) Gas prospecting project in Gassi Chergui (Algeria) Acquisition of Petroleum Oil & Gas España MoU signed with Nigerian Government * * |

76 A multinational leader in the energy sector that operates through the whole gas value chain Gas and electricity assets Gas transport and infra- estructure Gas supply and demand Upstream Clients Maghreb-Europe pipeline expansion to c. 12 bcm/year 8 tankers (702,000 m 3 ) + 1 in 2007 (138,000 m 3 ) + 1 new tanker in 2009 (138,000 m 3 ) Regasification plant in Puerto Rico Requesting permits for the construction of two regasification plants in Italy * |

77 A multinational leader in the energy sector that operates through the whole gas value chain Gas and electricity assets Gas transport and infra- estructure Gas supply and demand Upstream Clients Main importer of gas natural and LNG in Spain through long term contracts (average residual life 15 years) Trading and energy management opportunities Gas supply 27.9 bcm: • 23.9 bcm Spain • 4 bcm International Key role for the security of supply in Spain * |

78 A multinational leader in the energy sector that operates through the whole gas value chain Gas and electricity assets Gas transport and infra- estructure Gas supply and demand Upstream Clients Electricity generation CCGT and wind capacity under construction and awaiting permits Gas distribution network: 100,150 Km: • 39,611 Km Spain • 56,763 Km LatAm • 3,776 Km Italy • 3,102 MW in Spain • 271 MW in Puerto Rico • 2,000 MW CCGT in Spain • > 1,000 MW wind and cogen. * |

79 Gas and electricity assets Gas transport and infra- estructure Gas supply and demand Upstream Clients 1 5,134,000 in Spain 4,757,000 on LatAm 288,000 in Italy 1.47 contracts per client in Spain A multinational leader in the energy sector that operates through the whole gas value chain Note: 1 Points of supply * |

80 Our commitment … which translates into growth of financial magnitudes… … and shareholder remuneration Reach operating growth potential… Note: 1 These commitments do not include the potential Endesa acquisition nor are estimates nor forecasts from Gas Natural about the future of the Gas Natural – Endesa Group performance * * |

81 13 million 10% Clients (2008) Generation share in Spain (2008) 1 Reach operating growth potential Leading position ~15% long term LNG business Equity gas position Note: 1 Ordinary regime 2 These commitments do not include the potential Endesa acquisition nor are estimates nor forecasts from Gas Natural about the future of the Gas Natural – Endesa Group performance * * |

82 ~2,500 million euro ~ 10% CAGR EBITDA (2008) Net Income (2004-2008) Financial magnitudes growth ~8,800 million euro Capex (2004-2008) Note: 1 These commitments do not include the potential Endesa acquisition nor are estimates nor forecasts from Gas Natural about the future of the Gas Natural – Endesa Group performance * * * |

83 Shareholder remuneration Pay-out Dividend (€/share) 47.3% 49.5% 52–55% 0.60 2003 2004 2008(e) 0.71 +18.3% 50.2% 2005 +18.3% 0.84 52 – 55% in 2008 Payout Notes: 1 The year represents the fiscal year against which results the dividend is declared 2 2003 data under Spanish GAAP, 2004 and 2005 under IFRS 3 These commitments do not include the potential Endesa acquisition nor are estimates nor forecasts from Gas Natural about the future of the Gas Natural – Endesa Group performance * * * |

Proposed Resolutions * * * * * * * * * * |

85 Proposed resolutions The Annual Accounts, the Management Report, both for Gas Natural SDG, S.A. and for its consolidated group, and of the management of the Board of Directors, for the fiscal year ended on December 31, 2005 The distribution of the corresponding dividend (total gross dividend of 0.84 euro per share) and the transfer of the pertinent amount from the Allowance for Free Depreciation Account to Voluntary Reserves Amendment, as appropriate, of the company’s Bylaws and Rules for the General Shareholders Meeting to take into consideration the latest update of the Corporations Act. The Board of Directors presents to the Ordinary General Shareholders Meeting and asks for the Shareholders approval of: * * * |

86 Proposed resolutions Re-election of the following Directors: Salvador Gabarró Serra (executive member) Emiliano López Achurra (independent member) Caixa d’Estalvis de Catalunya (owner’s member) Authorisation to issue fixed-income titles not convertible into shares, for up to a total of €2,000 million, as well as authorisation to make one or more purchases within eighteen months of up to 5% of the paid-in shares of the company’s corporate capital Delegation to execute the resolutions adopted in the General Shareholders Meeting The Board of Directors presents to the Ordinary General Shareholders Meeting and asks for the Shareholders approval of: * * * |

Annual General Meeting Gas Natural SDG, S.A. * * * * * * |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| GAS NATURAL SDG, S.A. | ||||||

| Date: June 8, 2006 | By: | /s/ Carlos J. Álvarez Fernández | ||||

| Name: | Carlos J. Álvarez Fernández | |||||

| Title: | Chief Financial Officer | |||||