As filed with the Securities and Exchange Commission on March 31, 2008

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Pinnacle Entertainment, Inc.

and Additional Subsidiary Guarantor Registrants

(See Table of Other Registrants Below)

(Exact Name of Registrant as Specified in Its Charter)

| | | | |

| Delaware | | 7990 | | 95-3667491 |

(State or other jurisdiction of incorporation or organization) | | (Primary Standard Industrial Classification Code Number) | | (I.R.S. Employer Identification Number) |

3800 Howard Hughes Parkway

Las Vegas, Nevada 89169

(702) 784-7777

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

John A. Godfrey, Esq.

Executive Vice President, General Counsel and Secretary

Pinnacle Entertainment, Inc.

3800 Howard Hughes Parkway

Las Vegas, Nevada 89169

(702) 784-7777

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Alvin G. Segel, Esq.

Ashok W. Mukhey, Esq.

Irell & Manella LLP

1800 Avenue of the Stars, Suite 900

Los Angeles, California 90067

(310) 277-1010

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a small reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| | |

| Large accelerated filer x | | Accelerated filer ¨ |

| Non-accelerated filer ¨ (Do not check if a smaller reporting company) | | Smaller reporting company ¨ |

CALCULATION OF REGISTRATION FEE

| | | | | | | | |

| |

Title of each class of securities to be registered | | Amount to be

registered | | Proposed maximum offering price per note (1) | | Proposed maximum aggregate offering price (1) | | Amount of registration fee |

7 1/2% Senior Subordinated Notes due 2015 | | $385,000,000 | | 100% | | $385,000,000 | | $15,131 (1) |

Guarantees of 7 1/2% Senior Subordinated Notes due 2015 (2) | | — (2) | | — (2) | | — (2) | | — (3) |

| |

| |

| (1) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(f) under the Securities Act of 1933, as amended. |

| (2) | No separate consideration will be received for the guarantees. |

| (3) | Pursuant to Rule 457(n) under the Securities Act of 1933, no separate fee is payable for the guarantees. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

OTHER REGISTRANTS

| | | | | | |

Exact Name of Registrant as Specified in its Charter | | State or Other Jurisdiction of Incorporation or Organization | | I.R.S.

Employer

Identification

Number | | Address, including Zip

Code, and Telephone

Number, including

Area Code, of

Registrant’s Principal

Executive Offices |

ACE Gaming, LLC | | New Jersey | | 54-2131351 | | * |

AREH MLK LLC | | Delaware | | — | | * |

AREP Boardwalk Properties LLC | | Delaware | | — | | * |

Belterra Resort Indiana, LLC | | Nevada | | 93-1199012 | | * |

Biloxi Casino Corp. | | Mississippi | | 64-0814408 | | * |

Boomtown, LLC | | Delaware | | 94-3044204 | | * |

Casino Magic Corp. | | Minnesota | | 64-0817483 | | * |

Casino One Corporation | | Mississippi | | 64-0814345 | | * |

Louisiana-I Gaming, a Louisiana Partnership in Commendam | |

Louisiana | | 72-1238179 | | * |

Mitre Associates LLC | | Delaware | | — | | * |

OGLE HAUS, LLC | | Indiana | | 31-1672109 | | * |

PNK (Baton Rouge) PARTNERSHIP | | Louisiana | | 72-1246016 | | * |

PNK (Bossier City), Inc. | | Louisiana | | 64-0878110 | | * |

PNK (CHILE 1), LLC | | Delaware | | 51-0553578 | | * |

PNK (CHILE 2), LLC | | Delaware | | 51-0553581 | | * |

PNK Development 7, LLC | | Delaware | | 20-4328580 | | * |

PNK Development 8, LLC | | Delaware | | 20-4486902 | | * |

PNK Development 9, LLC | | Delaware | | 20-4328766 | | * |

PNK Development 13, LLC | | New Jersey | | 20-4330677 | | * |

PNK (ES), LLC | | Delaware | | 51-0534293 | | * |

PNK (LAKE CHARLES), L.L.C. | | Louisiana | | 02-0614452 | | * |

PNK (Reno), LLC | | Nevada | | 88-0101849 | | * |

PNK (SCB), L.L.C. | | Louisiana | | 72-1233908 | | * |

PNK (ST. LOUIS RE), LLC | | Delaware | | 51-0553585 | | * |

PNK (STLH), LLC | | Delaware | | 51-0553583 | | * |

PSW PROPERTIES LLC | | Delaware | | — | | * |

St. Louis Casino Corp. | | Missouri | | 64-0836600 | | * |

Yankton Investments, LLC | | Nevada | | 83-0445853 | | * |

| * | c/o Pinnacle Entertainment, Inc., 3800 Howard Hughes Parkway, Las Vegas, Nevada 89169, (702) 784-7777. |

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion, dated March 31, 2008

PROSPECTUS

$385,000,000

Offer to Exchange

7 1/2% Senior Subordinated Notes due 2015,

Which Have Been Registered Under the Securities Act of 1933,

for any and all Outstanding 7 1/2% Senior Subordinated Notes Due 2015

The Exchange Offer:

| | • | | Pinnacle Entertainment, Inc. will exchange all outstanding 7 1/2% senior subordinated notes due 2015, referred to as the original notes, that are validly tendered and not validly withdrawn for an equal principal amount of 7 1/2% senior subordinated notes due 2015, referred to as the exchange notes, that are, subject to specified conditions, freely tradable. |

| | • | | You may withdraw tenders of outstanding notes at any time prior to the expiration date of the exchange offer. |

| | • | | The exchange offer expires at 5:00 p.m., New York City time, on , 2008, unless extended. We do not currently intend to extend the expiration date. |

| | • | | We will not receive any cash proceeds from the exchange offer. |

The Exchange Notes:

| | • | | We are offering exchange notes to satisfy certain of our obligations under the registration rights agreement entered into in connection with the private offering of the original notes. |

| | • | | The terms of the exchange notes are substantially identical to the original notes, except that the exchange notes, subject to specified conditions, will be freely tradable. |

| | • | | The exchange notes will be guaranteed on a senior subordinated basis by certain of our current and future domestic restricted subsidiaries. |

| | • | | We do not plan to list the exchange notes on a national securities exchange or automated quotation system. |

Please see “Risk Factors” beginning on page 21 of this prospectus for a discussion of certain factors that you should consider before participating in this exchange offer.

Each broker-dealer that receives exchange notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of such exchange notes. The letter of transmittal states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an “underwriter” within the meaning of the Securities Act.

This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of exchange notes received in exchange for original notes where such original notes were acquired by such broker-dealer as a result of market-making activities or other trading activities. We have agreed that, for a period of 180 days (which period may be extended in specified circumstances) from the thirtieth business day after the effective date of the registration statement of which this prospectus is a part or such shorter period as will terminate when any broker-dealer has sold all exchange notes held by it, we will make this prospectus available to such broker-dealer for use in connection with any such resale. See “Plan of Distribution.”

None of the Securities and Exchange Commission, the Louisiana Gaming Control Board, the Indiana Gaming Commission, the Missouri Gaming Commission, the Nevada Gaming Commission, the Nevada State Gaming Control Board, the City of Reno, Nevada gaming authorities, the New Jersey Casino Control Commission, the Gaming Board for the Commonwealth of The Bahamas, or any state securities commission or any other gaming authority or other regulatory agency, has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2008

TABLE OF CONTENTS

We have not authorized any dealer, salesperson or other person to give any information or represent anything to you other than the information contained in this prospectus. You must not rely on unauthorized information or representations.

This prospectus does not offer to sell nor ask for offers to buy any of the securities in any jurisdiction where it is unlawful, where the person making the offer is not qualified to do so, or to any person who cannot legally be offered the securities. The information in this prospectus is current only as of the date on its cover and may change after that date.

This prospectus incorporates important business and financial information about us that is not included in or delivered with this document. You may obtain information incorporated by reference, at no cost, by writing or telephoning us at the following address:

Pinnacle Entertainment, Inc.

Investor Relations

3800 Howard Hughes Parkway

Las Vegas, Nevada 89169

(702) 784-7777

To obtain timely delivery, you must request this information no later than five business days before the date you must make your investment decision. Therefore, we must receive your request for this information no later five (5) business days prior to the expiration of the exchange offer.

WHERE YOU CAN FIND MORE INFORMATION; INCORPORATION OF CERTAIN DOCUMENTS BY REFERENCE

We file annual, quarterly and special reports, proxy statements and other information with the United States Securities and Exchange Commission, or the SEC. You may read and copy any document we file with the SEC at the SEC’s public reference room at 100 F Street, N.E., Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 for further information on the public reference room and its copy charges. Our SEC filings are also available to the public on the SEC’s website atwww.sec.gov. Our common stock is listed on the New York Stock Exchange, or NYSE, under the symbol “PNK” and all reports, proxy statements and other information filed by us with the NYSE may be inspected at the NYSE’s offices at 20 Broad Street, New York, New York 10005. We maintain a website at http://www.pnkinc.com with information about our company. Our website and information contained on, or that can be accessed through, our web site are not incorporated into this prospectus and do not constitute a part of this prospectus. Our website address referenced above is intended to be an inactive textual reference only and not an active hyperlink to our website.

We have filed with the SEC a registration statement on Form S-4 under the Securities Act with respect to the exchange offer. This prospectus does not contain all of the information contained in the registration statement and the exhibits to the registration statement. Copies of our SEC filings, including the exhibits to the registration statement, are available through us or from the SEC through the SEC’s website or at its facilities described above.

In this prospectus, we “incorporate by reference” the information we file with the SEC (other than, in each case, documents or information deemed to have been furnished and not filed in accordance with the SEC rules), which means that we can disclose important information to you by referring to that information. The information incorporated by reference is considered to be an important part of this prospectus. Any statement in a document incorporated by reference in this prospectus will be deemed to be modified or superseded to the extent a statement contained in this prospectus or any other subsequently filed document that is incorporated by reference in this prospectus modifies or supersedes such statement. In addition, information contained in this prospectus shall be modified or superseded by information in any such subsequently filed documents which are incorporated by reference in this prospectus. We incorporate by reference in this prospectus the following documents filed with the SEC pursuant to the Securities Exchange Act of 1934, as amended, or the Exchange Act:

1. Our annual report on Form 10-K for the year ended December 31, 2007 (including without limitation Exhibit 99.1 thereto dealing with gaming regulations); and

2. Our current reports on Form 8-K filed on January 7, 2008, January 16, 2008, and February 26, 2008 (with respect to Item 1.01 and Exhibit 10.1 only).

We also incorporate by reference any future filings made by us with the SEC (other than information furnished pursuant to Item 2.02 or Item 7.01 of Form 8-K or as otherwise permitted by the SEC’s rules) under Sections 13(a), 13(c), 14, or 15(d) of the Exchange Act on or after the date of this prospectus and prior to the termination of the offering, and any reoffering, of the securities offered hereby.

You may request a copy of these filings, at no cost, by writing or telephoning us at the address on the previous page of this prospectus. Exhibits to the filings will not be sent, however, unless those exhibits have been specifically incorporated by reference in this prospectus.

i

MARKET DATA

We use market and industry data throughout this prospectus and the documents incorporated by reference herein that we have obtained from market research, publicly available information and industry publications. These sources generally state that the information that they provide has been obtained from sources believed to be reliable, but that the accuracy and completeness of such information is not guaranteed. The market and industry data is often based on industry surveys and the preparers’ experience in the industry. Similarly, although we believe that the surveys and market research that others have performed are reliable, we have not independently verified this information.

ii

PROSPECTUS SUMMARY

This is only a summary of the prospectus. You should read the entire prospectus, including “Risk Factors” and our consolidated financial statements and related notes, as well as the documents incorporated by reference in this prospectus, before making an investment decision. Unless the context indicates otherwise, all references to “Pinnacle,” “the Company,” “we,” “our,” “ours” and “us” refer to Pinnacle Entertainment, Inc. and its consolidated subsidiaries.

Our Company

We are a leading developer, owner and operator of casinos and related hospitality and entertainment facilities. Domestically, we currently operate six casino destinations, we have four other casino developments in various stages of planning and construction, and we are pursuing two other casino development opportunities. In addition, we have several small casino facilities in foreign markets.

Our long-term strategy is to maintain and improve each of our existing casinos; to build new resorts that produce returns above our cost of capital; and to develop the systems to tie all of our casinos together into a national gaming network. Hence, we are developing new, high-quality gaming properties in attractive gaming markets; we are maintaining and improving our existing properties with disciplined capital expenditures; we are developing a customer loyalty program designed to motivate customers to continue to patronize our casinos; and we may make strategic acquisitions at reasonable valuations, when and if available.

Our largest casino resort isL’Auberge du Lac in Lake Charles, Louisiana. Lake Charles offers the closest full-scale casino-hotel facilities to Houston (the seventh-largest metropolitan statistical area in the United States), as well as the Austin and San Antonio metropolitan areas. Lake Charles is approximately 145 miles from Houston and approximately 300 miles and 335 miles from Austin and San Antonio, respectively. L’Auberge du Lac offers approximately 995 guestrooms and suites, inclusive of our recent expansion. We recently completed an expansion project, in which we invested approximately $67 million as of the year ended December 31, 2007, and which includes 252 additional guestrooms (10 of which are new private garden villas), additional retail shops, an expanded pool area and other amenities.

OurBoomtown New Orleanscasino is the only casino in the West Bank neighborhood, across the Mississippi River from downtown New Orleans. The West Bank generally did not flood as a result of the levee breaches that occurred in connection with the hurricanes in 2005 and has experienced substantial growth during the regional reconstruction. Responding to the growth within our community, we have been designing a 200-guestroom upscale hotel, the first guestrooms at this property, and other upgrades. We also plan to replace the three-level casino riverboat with a large single-deck casino boat, similar to the casino at L’Auberge du Lac. These projects are estimated to involve an investment of approximately $150 million.

Our southern Indiana property,Belterra Casino Resort, opened in October 2000, and is located along the Ohio River near Vevay, Indiana, approximately one hour from downtown Cincinnati, Ohio and 80 minutes from Louisville, Kentucky. Belterra is approximately two hours from Indianapolis, which is the third-largest market for Belterra. Management estimates that residents of the Indianapolis metropolitan area account for approximately 10% of Belterra’s casino revenues and approximately 11% of the guests staying at Belterra’s 608-guestroom hotel. The total population within 300 miles of Belterra is approximately 48 million. Belterra attracts customers by offering amenities that are generally superior to those at competing regional properties, several of which are closer to the population centers than Belterra. In August 2007, we added five retail shops. In December 2007, we completed the refurbishment of 11 of the high-end suites at Belterra. In light of the approval in May 2007 of legislation allowing two large slot machine casinos at racetracks in Indianapolis, we postponed indefinitely our planned construction of a 250-guestroom addition at the property.

1

OurBoomtown Bossier City property in Bossier City, Louisiana, features a regional hotel built around a dockside riverboat casino. The property is located on a site directly adjacent to, and easily visible from, Interstate 20. The Bossier City/Shreveport region is a three-hour drive from the Dallas/Fort Worth metropolitan area along Interstate 20. In 2006, we acquired a barge that we intend to convert to an arrival facility for guests of our riverboat casino. The arrival facility will adjoin our casino and offer escalators, making it easier for customers to travel among the three levels of our riverboat casino.

Lumière Place-St. Louis includes our new Lumière Place Casino and The Admiral Riverboat Casino, which we used to refer to as The President Riverboat Casino. Lumière Place, which is located in downtown St. Louis, Missouri, offers a 75,000-square-foot casino, a luxury Four Seasons Hotel St. Louis, the all-suites HoteLumière (formerly the Embassy Suites Hotel, which we have extensively refurbished), restaurants, banquet facilities, retail shops and convention/meeting space, including a ballroom. The Admiral Riverboat Casino offers approximately 845 slot machines and 30 table games. We own all of the facilities and have entered into a long-term agreement with Four Seasons Hotels Limited to manage our Four Seasons Hotel St. Louis. A group led by famed chef Hubert Keller manages two of our restaurants. Lumière Place is located across from the Edward Jones domed stadium and America’s Center Convention Center and just north of the famous Gateway Arch. A pedestrian tunnel to the America’s Center convention center, the Edward Jones domed stadium and the city’s central business district is expected to open in April 2008. We are currently using approximately nine of the 18 acres that we own in downtown St. Louis for the Lumière Place Casino and Hotels.

Boomtown Reno is a land-based casino-hotel located approximately 11 miles west of downtown Reno, Nevada, near the California border along Interstate 80. This interstate is the primary east-west interstate highway serving northern California. In the second quarter of 2007, we closed Boomtown Reno’s truck stop to accommodate the construction of a Cabela’s Inc. branded outdoor sporting goods store, which opened in November 2007. We sold approximately 28 acres of land to Cabela’s Inc. in 2006. We have entitlements to construct a new satellite casino and travel plaza on approximately 23 acres at a different location on the property’s 490 acres of available land. We continue to evaluate other opportunities to develop, sell or otherwise monetize our remaining excess available land.

Casino Magic Argentina, which is owned by an unrestricted subsidiary, consists of one large and several small casinos in the Patagonia region of Argentina. Casino Magic Argentina is constructing a 32-guestroom hotel, consisting of 15 large guestrooms and 17 suites, adjoining our casino. Casino Magic Argentina anticipates investing approximately US$13 million in the hotel project, which is being funded through the property’s existing cash balances and operating cash flows. We have certain exclusive rights to operate casinos in the principal cities of the Province of Neuquén. Our exclusivity rights in Neuquén should be extended from 2016 to 2021 upon the opening of our new hotel and inspection and approval of the hotel by the local gaming commission.

The Casino at Emerald Bay is a boutique casino adjoining the Four Seasons Resort at Emerald Bay on the picturesque island of Great Exuma in The Bahamas. Our casino opened in May 2006 and is the first and only casino on the island.

We are building a casino-hotel calledRiver City in St. Louis County, Missouri, which we expect to open in mid-2009. River City is located just south of the confluence of the Mississippi River and the River des Peres in the community of Lemay, one of the most densely populated areas in the St. Louis region. The first phase of the River City project is planned to include a gaming and multi-use facility and several restaurants at an estimated cost of $375 million. The second phase for the River City project is expected to include a hotel with a minimum of 100 guestrooms, as well as other amenities to be determined at a later time, at an estimated cost of $75 million. The River City casino-hotel is located on approximately 56 acres of land we control under a long-term lease from St. Louis County. The opening of River City is subject to approval of the Missouri Gaming Commission (the “MGC”).

2

In June 2007, the Louisiana Gaming Control Board (the “LGCB”) approved the architectural plans for our proposedSugarcane Bay casino resort to be built adjacent to our L’Auberge du Lac facility, which site was approved by voters of Lake Charles, Louisiana in November 2006. The project will utilize one of the two gaming entities we acquired from Harrah’s Entertainment, Inc. (“Harrah’s”) in 2006. One of the conditions to our license requires a minimum project investment of $350 million. Our plans for Sugarcane Bay include a floating, single-level dockside casino similar to that of L’Auberge du Lac and a 400-guestroom hotel, to be built on approximately 234 acres of land being leased from the Lake Charles Harbor and Terminal District. Included in the 234 acres of land we leased in January 2008 are 50 acres that we purchased for $5.0 million, though we have not selected the particular location of the acreage purchased. We will designate the location of those 50 acres in connection with the opening of Sugarcane Bay. Our Sugarcane Bay project is subject to various zoning and permitting requirements and approval of the LGCB. In addition, we have acquired approximately 56 acres of land adjacent to our Sugarcane Bay and L’Auberge du Lac properties for possible future development. We are required to complete specific milestones within certain timeframes and complete construction within 18 months of commencing excavating and grading work for the foundations, subject to certain approvals by the LGCB.

On September 18, 2007, the LGCB approved our planned $250 million casino-hotel resort namedRivière in Baton Rouge, Louisiana. Rivière will use the other gaming entity acquired from Harrah’s. We own approximately 517 acres of land and we are a majority co-owner of an additional 58 acres of land, approximately 10 miles south of downtown Baton Rouge, Louisiana. We are actively seeking the partition of such co-owned acreage with the third-party minority owner. On February 9, 2008, the voters of East Baton Rouge Parish approved this location for a casino as required under state law. The project is subject to certain conditions and various other approvals. Baton Rouge is currently believed to rival New Orleans as the largest city in Louisiana and has experienced significant growth in recent years, both before and particularly after the effects of the 2005 Hurricane Katrina on the nearby New Orleans region. We are currently in the design phase of this project. Similar to Sugarcane Bay, we are required to complete specific milestones within certain timeframes and complete construction of the first phase within 18 months of commencing excavating and grading work for the foundations, subject to certain approvals by the LGCB.

In November 2006, we purchased entities that owned a former casino site and an adjoining parcel inAtlantic City, New Jersey, which included the former Sands Casino Hotel. The aggregate purchase price paid at closing for the former casino site and additional property, other assets, tax benefits and working capital items of the entities was approximately $275 million. We paid an additional $10.1 million in the first quarter of 2007, following the settlement of a property tax matter that resulted in a like amount of property tax credits being available to us in future years. In early 2008, we acquired or agreed to purchase an additional four acres. In the aggregate, the Atlantic City site comprises approximately 22 contiguous acres at the heart of Atlantic City, with extensive frontage along The Boardwalk, Pacific Avenue and Brighton Park. We began site preparation work in 2007, including the implosion of the former Sands Casino Hotel and other structures on the site. We continue to plan and design our Atlantic City project, which for a resort of this size is expected to take at least two to three years from the date of our acquisition of the site in November 2006. The construction will then require approximately three to four additional years to complete with an anticipated opening date no earlier than 2012, subject to various regulatory approvals. This casino project is intended to be among the largest and most spectacular resorts in the region. While we have not yet determined the final scope or overall design of the new project, we estimate that its size and our investment will be substantially larger than those at any of our other facilities.

In December 2007, theUnified Government of Wyandotte County/Kansas City, Kansas (the “Unified Government”) endorsed our plan as one of three proposals sent on to state officials for consideration for selection to build and operate the one free-standing casino to be permitted in the county under legislation passed in 2004. Besides these three, there are other competing proposals under consideration for the same license. On December 31, 2007, our subsidiary signed a development agreement with the Unified Government outlining our obligations if we are selected by the State. We believe that the other two proposals endorsed by the Unified Government signed

3

similar development agreements. If we are chosen as the licensee, we intend to invest $650 million in the project, which, at a minimum, will include the construction of (a) a gaming and multi-use facility; (b) a 500-guestroom hotel; (c) a combination retail, commercial and/or entertainment facility; (d) a convention center; and (e) a central water feature connecting the gaming facility with the Schlitterbahn Vacation Village resort and water park now under construction. The project is anticipated to be substantially completed approximately 36 months after the occurrence of the latter of (i) the Lottery Gaming Facility Management Contract becoming effective or (ii) the resolution of the pending lawsuit relating to the constitutionality of the Kansas Expanded Lottery Act. The State of Kansas is expected to choose the licensee during 2008.

In August 2006, we purchased approximately one and one-half acres of gaming-zoned land inCentral City, Colorado, which is approximately 40 miles from Denver, Colorado. We have an option to purchase an additional six acres of adjoining, non-gaming zoned land. We believe our Central City land is the most conveniently located gaming-zoned site for Denver customers.

Our intention is to utilize existing cash resources, cash flows from operations, funds available under our credit facility and anticipated Biloxi and New Orleans insurance proceeds to fund operations, maintain existing properties, make necessary debt service payments and fund the development of some of our capital projects. The capital required for most of our development and expansion projects exceeds our available resources. Accordingly, construction of most of our projects would require us to access the capital markets. We expect that a substantial portion, and perhaps all, of the capital that we intend to invest in future years will be indebtedness and that our financial leverage will increase. As a result of the turmoil in the capital markets, the availability of financing in the credit markets is constrained, expensive and perhaps unavailable. We can give no assurance as to when financing would be available on more favorable terms. Various projects may have to be postponed or may not make economic sense, or may not be possible to finance, if capital markets do not improve.

4

Summary of Our Properties as of December 31, 2007

| | | | | | | | | |

| | | | | Approximate Number of | |

Locations | | Principal Markets | | Slot

Machines | | Table

Games | | Hotel

Rooms | |

Operating Properties: | | | | | | | | | |

Domestic | | | | | | | | | |

L’Auberge du Lac, LA(a) | | Houston, Beaumont, San Antonio, Austin, Southwest Louisiana and local patrons | | 1,600 | | 60 | | 995 | (a) |

Belterra Casino Resort, IN | | Cincinnati and Louisville | | 1,705 | | 55 | | 608 | |

Boomtown New Orleans, LA(b) | | Local patrons | | 1,435 | | 40 | | — | |

Boomtown Bossier City, LA | | Dallas/Ft. Worth and local patrons | | 1,115 | | 30 | | 188 | |

Lumière Place-St. Louis, MO | | | | | | | | | |

Lumière Place Casino and Hotels(c) | | Local patrons and regional tourists | | 2,000 | | 60 | | 495 | (c) |

The Admiral Riverboat Casino | | Local patrons and regional tourists | | 845 | | 30 | | — | |

Boomtown Reno, NV(d) | | Northern California, I-80 travelers and local patrons | | 945 | | 25 | | 318 | |

International | | | | | | | | | |

Casino Magic Argentina(e) | | Local patrons and regional tourists | | 985 | | 50 | | 30 | (e) |

The Casino at Emerald Bay, The Bahamas | | International tourists | | 65 | | 10 | | — | |

| | | | | | | | | |

Operating Property Total | | | | 10,695 | | 360 | | 2,634 | |

| | | | | | | | | |

New Properties Under Development and/or Construction: | | | | | | | |

River City, St. Louis, MO(f) | | Local patrons and regional tourists | | 2,300 | | 60 | | 100 | |

Sugarcane Bay, Lake Charles, LA(g) | | Houston, Beaumont, San Antonio, Austin, Southwest Louisiana and local patrons | | 1,500 | | 50 | | 400 | |

Rivière, Baton Rouge, LA(h) | | Local patrons and regional tourists | | 1,500 | | 50 | | 100 | |

Atlantic City, NJ | | New York City, Philadelphia, Baltimore, Washington, D.C., Boston and Buffalo | | Not Yet Determined(i) | |

Potential Future Development Sites: | | | | | | | | | |

Kansas City, KS(j) | | Local patrons and regional tourists | | Not Yet Determined | |

Central City, CO(k) | | Denver | | Not Yet Determined | |

| (a) | We opened 208 of the 252 new guestrooms at L’Auberge du Lac in December 2007. All of the guestrooms were available by the end of January 2008, bringing the total number of guestrooms to approximately 995. |

| (b) | We have announced plans to build a hotel and replace our casino barge at Boomtown New Orleans, and are currently in the design phase of the process. |

| (c) | We opened the Lumière Place Casino in December 2007. We opened the 200-guestroom Four Seasons Hotel St. Louis and the 294-guestroom HoteLumière (formerly the Embassy Suites Hotel, which has been extensively renovated) in early 2008. |

| (d) | As of February 2008, we have reduced the number of slot machines at our Boomtown Reno property to approximately 650 slot machines. |

| (e) | The data in the table represent the combined operations of the several casinos we operate in Argentina. We are in the process of constructing a 32-guestroom hotel that adjoins our casino in the city of Neuquén. Sixteen of the guestrooms were completed and became available in March 2008 and we anticipate completing the other 16 in mid-2008. For the year ended December 31, 2007, the Neuquén casino comprised approximately 87.9% of revenues of our Argentine operations. |

5

| (f) | We expect River City to open in mid-2009, subject to, among other things, final approval of the MGC. |

| (g) | We are underway with site preparation for our Sugarcane Bay casino-hotel. The project is subject to certain conditions and various approvals. |

| (h) | On February 9, 2008, the voters of East Baton Rouge Parish approved our casino-resort to be built on real estate that we own or control. The project is subject to certain conditions and various other approvals. |

| (i) | The specific attributes of our Atlantic City project have not yet been determined, but considering the size of the market and the site, location and cost of our site, this is expected to be significantly larger than any of our existing facilities. |

| (j) | We are seeking a license for a new gaming entertainment complex to be located on land we have optioned in Kansas City, Kansas. We have one of several proposals for the one license expected to be issued in this jurisdiction. |

| (k) | We own land and have an option to purchase additional land in Central City, Colorado. |

6

Our Principal Operating Properties and Unrestricted Subsidiaries

L’Auberge du Lac is a major casino resort in Lake Charles, Louisiana that opened in May 2005. Located on 242 acres of land, L’Auberge du Lac currently offers approximately 995 guestrooms, several restaurants, approximately 28,000 square feet of meeting space, a championship golf course designed by Tom Fazio, retail shops and a full-service spa. Unlike most other riverboat casinos, all of the public areas at L’Auberge du Lac (except the parking garage), and in particular the casino, are situated entirely on one level. The casino is surrounded on three sides by the hotel tower and other guest amenities. The hotel at L’Auberge du Lac is the largest in Louisiana outside of New Orleans.

Boomtown New Orleans is a dockside riverboat casino. It currently features a casino, two restaurants, a delicatessen, a 350-seat nightclub, 4,600 square feet of meeting space, an arcade and approximately 1,700 parking spaces. The property opened in 1994 and is located on 54 acres in Harvey, Louisiana, approximately 10 miles from downtown New Orleans and across the Mississippi River in the “West Bank” suburban area.

Belterra Casino Resort is a regional resort with an adjoining dockside riverboat casino. It opened in October 2000 and is located on 315 acres of land along the Ohio River near Vevay, Indiana, approximately one hour from downtown Cincinnati, Ohio, and 80 minutes from Louisville, Kentucky. In the fourth quarter of 2006, a new road opened that provides a more direct route for our guests coming from Cincinnati and Louisville. Belterra features a large casino and a 608-guestroom hotel, six restaurants, 33,000 square feet of meeting and conference space, a 1,750-seat entertainment showroom, retail shops, a swimming pool, a championship golf course designed by Tom Fazio and a full-service spa. The resort provides approximately 2,000 parking spaces, most of which are in a multi-level parking structure.

Boomtown Bossier City is a regional hotel property built around a dockside riverboat casino. The property opened in October 1996 on a site directly adjacent to, and easily visible from, Interstate 20. The Bossier City/Shreveport region is a three-hour drive from the Dallas/Fort Worth metropolitan area along Interstate 20. The property includes 188 guestrooms, including four master suites and 88 junior suites, four restaurants and approximately 1,860 parking spaces.

Lumière Place-St. Louis includes our new Lumière Place Casino and The Admiral Riverboat Casino. Lumière Place, which is located in downtown St. Louis, Missouri, offers a 75,000-square-foot casino, a 200-guestroom luxury Four Seasons Hotel St. Louis, the 294 all-suites HoteLumière (formerly the Embassy Suites Hotel, which we have extensively refurbished), seven restaurants, banquet facilities, retail shops and more than 22,000 square feet of convention/meeting space, including a 7,300-square-foot ballroom. The Admiral Riverboat Casino offers approximately 845 slot machines and 30 table games. We are currently using approximately nine of the 18 acres that we own in downtown St. Louis for the Lumière Place Casino and Hotels.

Boomtown Reno is a land-based casino-hotel that has been operating for more than 40 years and is located on a portion of approximately 550 acres approximately 11 miles west of downtown Reno, Nevada. The property offers 318 guestrooms, which we are planning to refurbish. In addition, the property has three restaurants, a 30,000-square-foot amusement center and approximately 1,300 parking spaces. In addition to the main casino-hotel, the property has a gas station and mini-mart and a 197-space recreational vehicle park. The property also contains a large Cabela’s branded sporting goods store.

The Casino at Emerald Bay is a boutique casino adjoining the Four Seasons Resort Great Exuma at Emerald Bay on the picturesque island of Great Exuma in The Bahamas. The casino, which opened in May 2006, is the first and only casino on the island.

7

Unrestricted Subsidiaries. We have three principal unrestricted subsidiaries described below. Unrestricted subsidiaries will not be subject to the covenants under the indenture. Unrestricted subsidiaries may enter into financing arrangements that limit their ability to make loans or other payments to fund payments in respect of the notes. Accordingly, we may not be able to rely on the cash flow or assets of unrestricted subsidiaries to pay any of our indebtedness, including the notes.

Casino Magic Neuquén S.A., owner of Casino Magic Argentina, is one of our principal unrestricted subsidiaries. Casino Magic Argentina consists of one large and several small casinos in the Patagonia region of Argentina. The principal Casino Magic Argentina property, in the city of Neuquén, opened in July 2005 and replaced a leased facility that had operated for over 20 years. Casino Magic Neuquén includes a large, first-class casino, a restaurant, several bars and an entertainment venue on approximately 20 acres of land. We are constructing a 32-guestroom hotel, consisting of 15 large guestrooms and 17 suites, adjoining our casino. We anticipate investing approximately US$13 million in the hotel project, which is being funded through the property’s existing cash balances and operating cash flows. We have certain exclusive rights to operate casinos in the principal cities of the Province of Neuquén. Our exclusivity rights in Neuquén should be extended from 2016 to 2021 upon the opening of our new hotel and inspection and approval of the hotel by the local gaming commission. Casino Magic Neuquén has entered into agreements with us relating to slot machine leases, technical assistance services and the non-exclusive use of the of the trade name “Casino Magic,” which may be amended in future. In addition, we have made a $4 million loan to Casino Magic Neuquén.

PNK Development 10, LLC, or PNK 10, an unrestricted subsidiary, owns a corporate airplane, a Falcon 2000 aircraft, built in 2000 and acquired in April 2007. PNK 10 leases the Falcon to Pinnacle until December 31, 2008, with three remaining automatic one-year renewal terms, for monthly rental payments of $200,000. PNK 10 also held cash of approximately $852,000 at December 31, 2007.

As of December 31, 2007, PNK Development 11, LLC, or PNK 11, an unrestricted subsidiary, held approximately $72.9 million in cash and marketable securities as of such date.

In 2005, Landing Condominium LLC, or Landing Condominium, entered into a joint venture with local developers to develop a 10-story luxury condominium project in Laclede’s Landing, near Lumière Place. Port St. Louis Condominium, LLC, or Port St. Louis, which is 50% owned by Landing Condominium and 50% owned by a third party, then designed the building, arranged a $19.0 million financing commitment and solicited bids for the building’s construction. The estimated costs of construction turned out to be higher than was originally estimated, while the overall market for residential housing has deteriorated in the interim. As a result, the partners determined that the project would not achieve sufficient returns and Port St. Louis has terminated the project. Through Port St. Louis, we have contributed approximately $1.3 million in expenses and our partner has contributed a portion of the project real property. Landing Condominium is currently in discussions with the partner and a construction lender regarding dissolving Port St. Louis and the potential transfer of the property to the partner, for reimbursement of $500,000 of the expenses plus the entire purchase price paid by the partnership for the remaining portion of the project real property.

8

Recent Developments

On February 22, 2008, we and Arch Specialty Insurance Company entered into a settlement agreement to settle our suit against Arch in connection with the hurricane-related damage to our former casino in Biloxi, Mississippi and its Boomtown New Orleans casino in Harvey, Louisiana. Pursuant to the settlement agreement, Arch has paid us approximately $36.8 million in exchange for a full and final release of all claims and a dismissal with prejudice of our lawsuit against Arch. Arch’s payment came from its $50 million policy participation in the $100 million layer of coverage in excess of $150 million. We continue to pursue our claims against the two remaining defendant insurance carriers for their respective shares of our total hurricane-related damage and consequential loss, which we value at least at $297 million. One of those carriers, Allianz Global Risks US Insurance Company, insured the layer of loss between $100 million and $150 million and has previously advanced $5 million, subject to a reservation of rights. The other carrier, RSUI Indemnity Company, provided pari passu coverage with Arch for the $100 million layer and is the sole carrier for the layer of coverage between $250 million and $400 million. As of March 15, 2008, we have received payments totaling approximately $141.8 million from our insurers relative to these claims, including the settlement payment received from Arch.

9

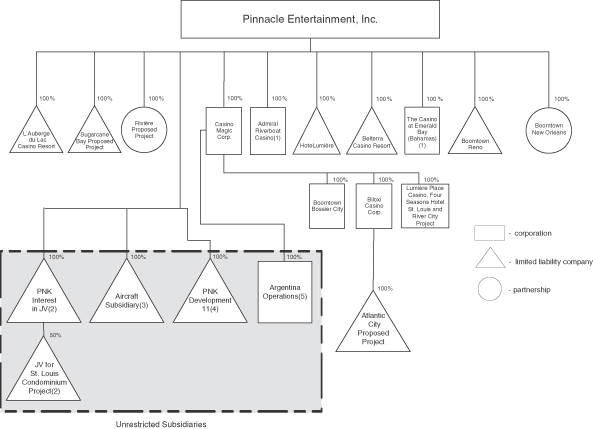

Corporate Structure

The following chart illustrates the organizational structure of our principal operations. It is designed to depict generally how our various operations and major properties relate to one another and our ownership interest in them. It does not contain all of our subsidiaries and, in some cases for presentation purposes, we have combined separate entities to indicate operational relationships. We have also indicated the principal subsidiaries that are currently unrestricted subsidiaries under the indenture governing the exchange notes offered hereby, i.e., the subsidiaries that will not be guarantors and will not be subject to the indenture covenants.

| (1) | President Riverboat Casino—Missouri, Inc., the entity that owns The Admiral Riverboat Casino, and PNK (Exuma) Limited, the entity that owns The Casino at Emerald Bay, are restricted subsidiaries but are not guarantors under the indentures governing our senior subordinated notes, including the exchange notes. |

| (2) | The unrestricted subsidiaries are Landing Condominium LLC (100% owned by Pinnacle) and Port St. Louis Condominium, LLC (50% owned by Landing Condominium LLC and 50% owned by a third party). Landing Condominium, the third-party partner and a construction lender are in discussions about dissolving Port St. Louis Condominium, LLC. |

| (3) | The unrestricted subsidiary is PNK Development 10, LLC and owns an airplane and as of December 31, 2007 held approximately $852,000 in cash. |

| (4) | The unrestricted subsidiary is PNK Development 11, LLC, which, as of December 31, 2007, held miscellaneous assets including $72.9 million in cash and marketable securities as of such date. |

| (5) | The unrestricted subsidiary is Casino Magic Neuquén, S.A. |

10

The Exchange Offer

The following summary contains basic information about the exchange offer and the exchange notes. It does not contain all the information that is important to you. For a more complete understanding of the exchange notes, please refer to the sections of this prospectus entitled “The Exchange Offer” and “Description of Exchange Notes.”

The Exchange Offer | We are offering to exchange an aggregate of $385 million principal amount of our exchange notes for $385 million principal amount of our original notes. Original notes may be exchanged in integral multiples of $1,000 principal amount. To be exchanged, an original note must be properly tendered and accepted. All outstanding original notes that are validly tendered and not validly withdrawn will be exchanged for an equal principal amount of exchange notes issued on or promptly after the expiration date of the exchange offer. Currently, there is $385 million aggregate principal amount of the original notes outstanding and there are no exchange notes outstanding. |

The form and terms of the exchange notes will be substantially identical to those of the original notes except that the exchange notes will have been registered under the Securities Act. Therefore, the exchange notes will not be subject to certain contractual transfer restrictions, registration rights and certain additional interest provisions applicable to the original notes prior to consummation of the exchange offer.

Expiration Date | The exchange offer will expire at 5:00 p.m., New York City time on , 2008, unless extended, in which case the term “expiration date” shall mean the latest date and time to which the exchange offer is extended. We do not currently intend to extend the expiration date of the exchange offer. |

Withdrawal | You may withdraw the tender of your original notes at any time prior to the expiration date of the exchange offer. See “The Exchange Offer—Withdrawal Rights.” |

Conditions to the Exchange Offer | The exchange offer is subject to customary conditions which we may assert or waive. The exchange offer is not conditioned upon any minimum principal amount of original notes being tendered for exchange. See “The Exchange Offer—Conditions to the Exchange Offer.” |

Procedures for Tendering Original Notes | If you are a holder of original notes who wishes to accept the exchange offer, you must: |

| | • | | properly complete, sign and date the accompanying letter of transmittal (including any documents required by the letter of transmittal), or a facsimile of the letter of transmittal, according to the instructions contained in this prospectus and the letter of transmittal, and mail or otherwise deliver the letter of transmittal, |

11

| | together with the certificates for your original notes, to the exchange agent at the address set forth under “The Exchange Offer—Exchange Agent;” or |

| | • | | tender your original notes by using the book-entry transfer procedures described below and transmitting a properly completed and duly executed letter of transmittal, or an agent’s message instead of the letter of transmittal, to the exchange agent. For a book-entry transfer to constitute a valid tender of your original notes in the exchange offer, Bank of New York Trust Company, N.A., as exchange agent, must receive a confirmation of book-entry transfer of your original notes into the exchange agent’s account at The Depositary Trust Company, or DTC, prior to the expiration or termination of the exchange offer. For more information regarding the use of book-entry transfer procedures, including a description of the required agent’s message, see the discussion below under the caption “The Exchange Offer—Procedures for Tendering Original Notes.” As used in this prospectus, the term “agent’s message” means a message, transmitted by DTC to and received by the exchange agent and forming a part of a book-entry transfer, which states that DTC has received an express acknowledgment from the tendering participant stating that such participant has received and agrees to be bound by the letter of transmittal and that we may enforce such letter of transmittal against such participant. |

| | By tendering your original notes in either manner, you will be representing, among other things, that: |

| | • | | you are acquiring the exchange notes issued to you in the exchange offer in the ordinary course of your business; |

| | • | | you are not engaged in, and do not intend to engage in, and have no arrangement or understanding with any person to participate in, a distribution of the exchange notes issued to you in the exchange offer; and |

| | • | | you are not an “affiliate” of ours within the meaning of Rule 405 under the Securities Act. |

| | See “The Exchange Offer—Procedures for Tendering Original Notes.” |

Special Procedures for Beneficial Owners | If you beneficially own original notes registered in the name of a broker, dealer, commercial bank, trust company or other nominee and wish to tender your beneficially owned original notes in the exchange offer, you should contact the registered holder promptly and instruct it to tender the original notes on your behalf. If you wish to tender on your own behalf, you must, prior to completing and executing the letter of transmittal and delivering your outstanding notes, either |

12

| | make appropriate arrangements to register ownership of the outstanding notes in your name or obtain a properly completed bond power from the registered holder. The transfer of registered ownership may take considerable time and may not be able to be completed prior to the expiration date. See “The Exchange Offer—Procedures for Tendering Original Notes.” |

Guaranteed Delivery Procedures | If you wish to tender your original notes, but: |

| | • | | your original notes are not immediately available; or |

| | • | | you cannot deliver your original notes, the letter of transmittal or any other documents required by the letter of transmittal to the exchange agent prior to the expiration date; or |

| | • | | the procedures for book-entry transfer of your original notes cannot be completed prior to the expiration date, |

| | you may tender your original notes pursuant to the guaranteed delivery procedures set forth in this prospectus and the letter of transmittal. See “The Exchange Offer—Guaranteed Delivery Procedures.” |

Acceptance of Original Notes for Exchange and Delivery of Exchange Notes | Upon satisfaction or waiver of all the conditions to the exchange offer, we will accept any and all original notes that are properly tendered in the exchange offer prior to 5:00 p.m., New York City time, on the expiration date. The exchange notes issued pursuant to the exchange offer will be delivered promptly following the expiration date. See “The Exchange Offer—Acceptance of Original Notes for Exchange and Delivery of Exchange Notes.” |

Material United States Federal Income Tax Considerations | The exchange of exchange notes for original notes in the exchange offer should not be a taxable exchange for U.S. federal income tax purposes. See “Summary of Material United States Federal Income Tax Considerations.” |

Use of Proceeds | We will not receive any cash proceeds from the issuance of exchange notes pursuant to the exchange offer. |

Fees and Expenses | We will pay all expenses incident to the consummation of the exchange offer and compliance with the registration rights agreement. We will also pay certain transfer taxes applicable to the exchange offer, if any. See “The Exchange Offer—Fees and Expenses.” |

Termination of Certain Rights | The original notes were issued and sold in a private offering to Lehman Brothers Inc., Bear, Stearns & Co. Inc., Banc of America Securities LLC, Deutsche Bank Securities Inc., SG Americas Securities LLC, Wells Fargo Securities, LLC, Barclays Capital Inc., Wachovia Capital Markets, LLC, Calyon Securities (USA) Inc., |

13

| | Commerzbank Capital Markets Corp., Capital One Southcoast, Inc., Merrill Lynch, Pierce, Fenner & Smith Incorporated and Morgan Stanley & Co. Incorporated, as the initial purchasers, on June 8, 2007. In connection with that sale, we executed and delivered a registration rights agreement for the benefit of the noteholders. |

| | Pursuant to the registration rights agreement, holders of original notes: (i) have rights to receive additional interest in certain instances; and (ii) have certain rights intended for the holders of unregistered securities. Holders of exchange notes will not be, and upon consummation of the exchange offer, holders of original notes will no longer be, entitled to the right to receive additional interest in certain instances, as well as certain other rights under the registration rights agreement for holders of unregistered securities. If you do not tender your original notes in the exchange offer, after consummation of the exchange offer we will have no further obligation to you to register original notes under the registration rights agreement. See “The Exchange Offer.” |

Resale of Exchange Notes | We believe, based on an interpretation by the staff of the SEC contained in no-action letters issued to third parties in other transactions, that you may offer to sell, sell or otherwise transfer the exchange notes issued to you in this exchange offer without complying with the registration and prospectus delivery requirements of the Securities Act, provided that: |

| | • | | you are acquiring the exchange notes issued to you in the exchange offer in the ordinary course of your business; |

| | • | | you are not engaged in, and do not intend to engage in, and have no arrangement or understanding with any person to participate in, a distribution of the exchange notes issued to you in the exchange offer; and |

| | • | | you are not an “affiliate” of ours within the meaning of Rule 405 under the Securities Act. |

| | If you are not acquiring the exchange notes in the ordinary course of your business, or if you are engaging in, intend to engage in, or have any arrangement or understanding with any person to participate in, a distribution of the exchange notes, or if you are an affiliate of Pinnacle or any of our subsidiaries, then: |

| | • | | you cannot rely on the position of the staff of the SEC enunciated in Morgan Stanley & Co., Inc. (available June 5, 1991), Exxon Capital Holdings Corporation (available May 13, 1988), as interpreted in the SEC’s letter to Shearman & Sterling dated July 2, 1993, or similar no-action letters; |

| | • | | you will not be entitled to tender your original notes in the exchange offer; and |

14

| | • | | in the absence of an exception from the position of the SEC stated in the bullet point above, you must comply with the registration and prospectus delivery requirements of the Securities Act in connection with any resale transaction; |

| | Furthermore, any broker-dealer that acquired any of its original notes directly from us: |

| | • | | may not rely on the position of the staff of the SEC described above; and |

| | • | | must also be named as a selling noteholder in connection with the registration and prospectus delivery requirements of the Securities Act relating to any resale transaction. |

Broker-Dealers | Each broker-dealer that receives exchange notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of such exchange notes. The letter of transmittal states that by so acknowledging and delivering a prospectus, a broker-dealer will not be deemed to admit that it is an “underwriter” within the meaning of the Securities Act. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of exchange notes received in exchange for original notes which were received by the broker-dealer as a result of market-making or other trading activities. Under the registration rights agreement, we have agreed that for a period of 180 days (which period may be extended in specified circumstances) following the thirtieth business day after the registration statement containing this prospectus is declared effective or such shorter period as will terminate when any broker-dealer has sold all exchange notes held by it, we will make this prospectus available to any broker-dealer for use in connection with any such resale. See “Plan of Distribution.” |

Consequences of Failure to Exchange | If you do not tender your original notes or if you tender your original notes improperly, you will continue to be subject to the restrictions on transfer of your original notes as contained in the legend on the original notes. In general, you may not sell or offer to sell the original notes, except pursuant to a registration statement under the Securities Act or any exemption from registration thereunder and in compliance with all applicable state securities laws. See “The Exchange Offer—Consequences of Failure to Exchange.” |

Exchange Agent | The Bank of New York Trust Company, N.A. is the exchange agent for the exchange offer. |

15

The Exchange Notes

The form and terms of the exchange notes will be substantially identical to those of the original notes except that the exchange notes will have been registered under the Securities Act. Therefore, the exchange notes will not be subject to certain transfer restrictions, registration rights and certain additional interest provisions applicable to the original notes prior to the consummation of the exchange offer.

Issuer | Pinnacle Entertainment, Inc. |

Total amount of exchange notes offered | Up to $385,000,000 in aggregate principal amount of 7 1/2% Senior Subordinated Notes due 2015. |

Maturity date | June 15, 2015 |

Interest payment dates | June 15 and December 15 of each year. The first interest payment date on the original notes was December 15, 2007. |

Guarantees | Our obligations under the exchange notes will be fully and unconditionally guaranteed on a senior subordinated basis, jointly and severally, by certain of our current and future domestic restricted subsidiaries. Certain of our subsidiaries, including our subsidiaries which own The Admiral Riverboat Casino in St. Louis, our Bahamian facility, our Argentine operations, our corporate aircraft and our condominium development in St. Louis, are not guarantors of the notes. As of December 31, 2007, the non-guarantor subsidiaries held approximately $183 million of our total assets of approximately $2.2 billion. |

Ranking | The exchange notes and the subsidiary guarantees will be unsecured senior subordinated indebtedness. Accordingly, they will be: |

| | • | | subordinated in right of payment to all of our and our subsidiary guarantors’ existing and future indebtedness except indebtedness that expressly provides that it ranks equal or subordinate in right of payment to the notes and the subsidiary guarantees; |

| | • | | equal in right of payment to all of our and our subsidiary guarantors’ existing and future senior subordinated indebtedness, including our 8.75% senior subordinated notes due 2013, our 8.25% senior subordinated notes due 2012 and any original notes that remain after the consummation of the exchange offer; |

| | • | | senior in right of payment to all of our and our subsidiary guarantors’ future debt that is specifically subordinated to the notes and the guarantees; |

| | • | | effectively subordinated to all of our and our subsidiaries’ secured indebtedness; and |

| | • | | structurally subordinated to all obligations of our non-guarantor subsidiaries. |

16

| | As of December 31, 2007, the exchange notes and the subsidiary guarantees would have been subordinated to (i) approximately $71 million of senior indebtedness, and (ii) approximately $554 million of unused revolving credit facilities. Of the amount of undrawn revolving credit facilities, we drew an additional $100 million between January 1, 2008 and March 15, 2008. |

Optional redemption | Prior to June 15, 2010 we may redeem up to 35% of the aggregate principal amount of the exchange notes with the proceeds of certain equity offerings. |

| | At any time prior to June 15, 2011, we may redeem some or all of the exchange notes at a redemption price equal to the principal amount of the exchange notes redeemed plus accrued and unpaid interest to the date of redemption plus an applicable premium. “Applicable premium” means with respect to any exchange note on any redemption date, the greater of (1) 1.0% of the principal amount of the exchange note; or (2) the excess of (a) the present value at such redemption date of (i) the optional redemption price of the note at June 15, 2011 plus (ii) all required interest payments due on the exchange note through June 15, 2011 (excluding accrued but unpaid interest to the redemption date), computed using a discount rate equal to the treasury rate, as defined, as of such redemption date plus 50 basis points; over (b) the principal amount of the note. See “Description of Exchange Notes—Redemption at Make-Whole Premium.” |

| | In addition, at any time on or after June 15, 2011, we may redeem some or all of the exchange notes at the redemption prices set forth under “Description of Exchange Notes—Optional Redemption.” |

Offer to purchase | If we experience specific kinds of changes of control, and, under certain circumstances, if we sell assets, we may be required to offer to purchase the notes at the prices set forth under “Description of Exchange Notes—Repurchase at the Option of Holders—Change of Control” and “—Asset Sales.” |

Redemption or other disposition based upon gaming laws | The notes are subject to redemption or disposition requirements imposed by gaming laws and regulations of gaming authorities in jurisdictions in which we conduct gaming operations. See “Description of Exchange Notes—Gaming Redemption or Other Disposition.” |

Covenants | The indenture governing the notes, among other things, limits our (and our restricted subsidiaries’) ability to: |

| | • | | incur additional indebtedness and issue preferred stock; |

| | • | | pay dividends or distributions on or purchase our equity interests; |

| | • | | make other restricted payments or investments; |

17

| | • | | use our assets as security in other transactions; |

| | • | | place restrictions on distributions and other payments from restricted subsidiaries; |

| | • | | sell certain assets or merge with or into other entities; and |

| | • | | enter into transactions with affiliates. |

| | Each of the covenants is subject to a number of important exceptions and qualifications. See “Description of Exchange Notes—Certain Covenants.” |

Use of Proceeds | We will not receive any cash proceeds from the issuance of the exchange notes. |

Risk Factors

An investment in the exchange notes involves risk. You should carefully consider the information under “Risk Factors” in this prospectus and the information in our Annual Report on Form 10-K for the year ended December 31, 2007 and all other information included or incorporated by reference in this prospectus.

Corporate Information

We were incorporated in the State of Delaware in 1981 as the successor to a business that started in 1938. Our executive offices are located at 3800 Howard Hughes Parkway, Las Vegas, Nevada 89169 and our telephone number is (702) 784-7777.

Our website address is www.pnkinc.com. Information contained in our website, including any links contained in our website, does not constitute part of this prospectus.

18

Summary Consolidated Financial Data

The following tables present our summary consolidated financial data for the years ended December 31, 2007, 2006 and 2005. This data is derived from our audited consolidated financial statements and the notes to those statements. Because the data in these tables is only a summary, you should read our consolidated financial statements, including the related notes, and the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in the Annual Report on Form 10-K that is incorporated herein by reference, as well as the other data we have incorporated by reference into this prospectus.

The following table presents our summary consolidated financial data for the years ended December 31, 2007, 2006 and 2005:

| | | | | | | | | | | | |

| | | For the years ended December 31, | |

| | | 2007(a) | | | 2006(b) | | | 2005(c) | |

Statement of Operations Data: | | | | | | | | | | | | |

Revenues | | $ | 923,711 | | | $ | 912,357 | | | $ | 668,463 | |

Income (loss) from continuing operations | | | (1,385 | ) | | | 61,887 | | | | (60 | ) |

Income (loss) from discontinued operations, net | | | (21 | ) | | | 14,999 | | | | 6,185 | |

Net income (loss) | | $ | (1,406 | ) | | | 76,886 | | | | 6,125 | |

| | | |

Net income per common share—basic: | | | | | | | | | | | | |

Income (loss) from continuing operations | | $ | (0.02 | ) | | $ | 1.30 | | | $ | 0.00 | |

Income (loss) from discontinued operations, net | | | — | | | | 0.31 | | | | 0.15 | |

| | | | | | | | | | | | |

Net income (loss) per common share—basic | | $ | (0.02 | ) | | $ | 1.61 | | | $ | 0.15 | |

| | | | | | | | | | | | |

Net income per common share—diluted: | | | | | | | | | | | | |

Income (loss) from continuing operations | | $ | (0.02 | ) | | $ | 1.26 | | | $ | 0.00 | |

Income (loss) from discontinued operations, net | | | — | | | | 0.30 | | | | 0.14 | |

| | | | | | | | | | | | |

Net income (loss) per common share—diluted | | $ | (0.02 | ) | | $ | 1.56 | | | $ | 0.14 | |

| | | | | | | | | | | | |

Other Data: | | | | | | | | | | | | |

Adjusted EBITDA(d): | | | | | | | | | | | | |

L’Auberge du Lac | | $ | 75,257 | | | $ | 72,364 | | | $ | 11,331 | |

Boomtown New Orleans | | | 54,180 | | | | 80,972 | | | | 51,442 | |

Belterra Casino Resort | | | 39,251 | | | | 37,289 | | | | 39,574 | |

Boomtown Bossier City | | | 17,861 | | | | 23,039 | | | | 19,636 | |

Lumière Place-St. Louis(a) | | | 6,125 | | | | 2,051 | | | | 726 | |

Boomtown Reno(e) | | | 3,465 | | | | 6,800 | | | | 10,356 | |

International(f) | | | 12,777 | | | | 9,176 | | | | 7,777 | |

| | | |

Capital expenditures | | $ | 545,644 | | | $ | 186,533 | | | $ | 202,774 | |

| | | |

Cash flows provided by (used in): | | | | | | | | | | | | |

Operating activities | | $ | 153,421 | | | $ | 206,527 | | | $ | 61,746 | |

Investing activities | | | (566,161 | ) | | | (459,323 | ) | | | (138,602 | ) |

Financing activities | | | 414,636 | | | | 294,128 | | | | 23,226 | |

19

| | |

| | | As of

December 31, 2007 |

Balance Sheet Data: | | |

Cash and cash equivalents | | 191,124 |

Total assets | | 2,193,544 |

Total notes payable | | 841,301 |

Stockholders’ equity | | 1,052,359 |

| (a) | The results for 2007 include Lumière Place-St. Louis, which opened on December 19, 2007, the Four Seasons Hotel St. Louis, HoteLumière (the renovated former Embassy Suites Hotel) and The Admiral Riverboat Casino. We acquired The Admiral Riverboat Casino on December 20, 2006. The former Embassy Suites Hotel was closed March 31, 2007 for refurbishment. The restaurant at the former Embassy Suites Hotel remained open throughout the majority of 2007. HoteLumière and the Four Seasons Hotel St. Louis opened in January and February 2008, respectively. |

| (b) | The results for 2006 include merger termination proceeds, net of expenses, of $44.7 million. |

| (c) | The results for 2005 include losses on the early extinguishment of debt of $3.8 million. |

| (d) | We define Adjusted EBITDA as earnings before interest income and expense, income taxes, depreciation, amortization, pre-opening and development costs, non-cash share-based compensation, merger termination proceeds, asset impairment charges, loss on early extinguishment of debt and discontinued operations. We report segment operating results in part based on Adjusted EBITDA. Such segment reporting is on a consistent basis with how we measure our business and allocate resources internally. See Note 12 to our audited Consolidated Financial Statements in our Annual Report on Form 10-K for the year ended December 31, 2007, which is incorporated herein by reference, for more information regarding our segment information. |

| (e) | We closed the truck stop at Boomtown Reno in June 2007 to facilitate construction of the neighboring Cabela’s Inc. branded sporting goods store. We have entitlements for a new satellite casino and travel plaza that could be built at a different location on the property’s 490 acres of available land. |

| (f) | Includes Casino Magic Argentina and The Casino at Emerald Bay in The Bahamas, which opened in May 2006. |

20

RISK FACTORS

Before making any decision to participate in the exchange offer, you should carefully consider the following risk factors in addition to the other information contained in this prospectus and incorporated by reference in this prospectus, including but not limited to, our Annual Report on Form 10-K for the year ended December 31, 2007 and other information which may be incorporated by reference in this prospectus as provided under “Where You Can Find More Information; Incorporation of Certain Documents by Reference.” If any of the following risks materialize, our business, financial condition and results of operations may suffer. As a result, you could lose part or all of your investment. As used herein, the term “notes” means both the exchange notes and the original notes, unless otherwise indicated.

Risks Related to our Business

Our substantial funding needs in connection with our development projects, our current expansion projects and other capital-intensive projects, to the extent such projects are undertaken, will require us to raise substantial amounts of money from outside sources. In the near term, the availability of financing may be constrained by current disruptions in the credit markets.

We are currently engaged in and have planned expansions and development projects that would require substantial amounts of capital. We are currently constructing River City, are planning to begin construction of Sugarcane Bay in 2008, construction of Rivière in 2009, and have expansion and improvement projects at several of our existing facilities, including Boomtown New Orleans, Boomtown Reno and Boomtown Bossier City. These projects have an expected aggregate investment of more than $1.2 billion, of which we have invested approximately $56.4 million through December 31, 2007. In addition, our proposed Atlantic City project is expected to require a very substantial additional investment. We have been endorsed for a new casino resort in Kansas City, Kansas by that area’s Unified Government. If we are chosen as a licensee by the Kansas Racing and Gaming Commission, we expect to invest approximately $650 million in our Kansas City project. We may also consider additional small-scale and large-scale projects as such opportunities arise. Accordingly, we expect that the total cost of our development and expansion projects over the next several years will be several billion dollars. While we will endeavor to stage development and construction of these projects over several years, our proposed projects could strain our financial resources.

In order to fund most of these projects, we will need to access the capital markets since the capital required for these projects exceeds our available financial resources. As a result of the turmoil in the credit markets, the availability of debt financing is constrained, expensive and potentially unavailable. We cannot accurately predict when or if the credit markets will return to more normalized conditions. If the current debt market environment does not improve, we may not be able to raise additional funds in a timely manner, or on acceptable terms, or at all. Inability to access the capital markets, or the necessity to access the capital markets on less than favorable terms, may force us to delay, reduce or cancel planned development and expansion projects, sell assets or obtain additional equity financing. Our current stock price, along with the stock prices of many public gaming companies, has declined sharply from the recent historical levels. We may choose to cancel or delay projects rather than issue equity at these levels. This may impair our growth and materially and adversely affect our financial condition, results of operations and cash flow and the returns of investing in our securities.

Our ability to obtain bank financing or to access the capital markets for future debt or equity offerings may also be limited by our financial condition, results of operations or other factors, such as our credit rating or outlook at the time of any such financing or offering and the covenants in our existing debt agreements, as well as by general economic conditions and contingencies and uncertainties that are beyond our control. As we seek financing for our development projects, we will be subject to the risks of rising interest rates and other factors affecting the financial markets. Moreover, if we obtain additional funds by issuing equity securities or securities convertible into equity securities, dilution to stockholders may occur. In addition, preferred stock could be issued

21

in the future without stockholder approval and the terms of the preferred stock could include dividend, liquidation, conversion, voting and other rights that are more favorable than the rights of the holders of our common stock.

Insufficient or lower-than-expected results generated from our new developments and acquired properties may negatively affect the market for our securities.

We cannot assure you that, if and once completed, the revenues generated from our new developments and acquired properties will be sufficient to pay related expenses; or, even if revenues are sufficient to pay expenses, that the new developments and acquired properties will yield an adequate or expected return on our significant investments. Our projects, if completed, may take significantly longer than we expect to generate returns, if any.

Moreover, lower-than-expected results from the opening of a new facility may negatively affect us and the market for our securities and may make it more difficult to raise capital, even as the shortfall increases the need to raise capital.