Filed by VeriFone Holdings, Inc.

Pursuant to Rule 425 under the Securities Act of 1933

and deemed filed pursuant to Rule 14a-12

of the Securities Exchange Act of 1934

Subject Company: Lipman Electronic Engineering Ltd.

Commission File No.: 000-50544

Searchable text section of graphics shown above

Management Participants

Doug Bergeron

Chairman & Chief Executive Officer – VeriFone

Barry Zwarenstein

Chief Financial Officer – VeriFone

Isaac Angel

Chief Executive Officer - Lipman

2

Safe Harbor

We have included or incorporated by reference in this document financial estimates and other forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These estimates and statements are subject to risks and uncertainties, and actual results might differ materially from these estimates and statements. Such estimates and statements include, but are not limited to, statements about the benefits of the acquisition, including future financial and operating results, VeriFone’s plans, objectives, expectations and intentions, the markets for products, and other statements that are not historical facts. Such statements are based upon the current beliefs and expectations of the management of VeriFone Holdings, Inc. and Lipman Electronic Engineering Inc. and are subject to significant risks and uncertainties outside of their control. There is no assurance the transaction contemplated in this release will be completed at all, or completed upon the same terms and conditions described.

The following factors, among others, could cause actual results to differ from those described in the forward-looking statements in this document: the ability to obtain governmental approvals of the merger on the proposed terms and schedule; the failure of VeriFone stockholders to approve the issuance of VeriFone common shares or the failure of Lipman shareholders to approve the merger; the risk that the businesses of VeriFone and Lipman will not be integrated successfully or as quickly as expected; the risk that the cost savings and any other synergies from the merger may not be fully realized or may take longer to realize than expected; disruption from the merger making it more difficult to maintain relationships with customers, employees or suppliers. Additional factors that may affect future results are contained in VeriFone’s and Lipman’s filings with the Securities and Exchange Commission (“SEC”), which are available at the SEC’s Web site (http://www.sec.gov). Neither VeriFone nor Lipman is under any obligation, and expressly disclaim any obligation, to update, alter or otherwise revise any forward-looking statement, whether written or oral, that may be made from time to time, whether as a result of new information, future events or otherwise.

3

Disclosures

In connection with the proposed transaction, VeriFone intends to file a registration statement on Form S-4, including a proxy statement for VeriFone, with the Securities and Exchange Commission (the “SEC”). Investors and security holders are urged to read the registration statement, including the proxy statement (and all amendments and supplements to it) and other materials that VeriFone may file with the SEC when they become available, because they contain important information. Investors and security holders will be able to obtain free copies of the registration statement, including the joint proxy statement/prospectus, as well as VeriFone’s other filings, at the SEC’s web site (www.sec.gov) when they become available. Free copies of VeriFone’s filings with the SEC may also be obtained at VeriFone’s web site (www.VeriFone.com) or by directing a request to: VeriFone Holdings Inc., 2099 Gateway Place, Suite 600, San Jose, CA 95110 (Tel: +1-408-232-7800, Attention: Director, Corporate Development & IR).

VeriFone, Lipman and their respective directors and executive officers and certain other members of management and employees may be deemed to be participants in the solicitation of proxies from VeriFone stockholders in respect of the proposed transaction. Information regarding VeriFone’s’ directors and executive officers is available in its Annual Report on Form 10-K for the year ended October 31, 2004, filed with the SEC on December 20, 2005 and its proxy statement for its 2006 annual meeting of stockholders, filed with the SEC on February 17, 2006. Information regarding Lipman’s directors and executive officers is available in Lipman’s 2005 Annual Report on Form 20-F filed with the SEC on March 9, 2006. Additional information regarding the interests of such potential participants will be included in the registration statement and proxy statement/prospectus, and the other relevant documents filed with the SEC when they become available.

4

The VeriFone Story

• Operational excellence

• Highly disciplined and experienced management team

• Industry leading revenue growth and profitability

• Consistent overachievement across all financial metrics

• Globally trusted brand developed over 25 years

• Integrated into the world’s largest payment networks

• Unparalleled customer loyalty

• Largest installed base

• Scale permits significant investment in R&D

• Geographical and product diversification

6

Our Leading Growth Drivers

Emerging | • Less than 5% of United States penetration rates |

Markets | • Government VAT mandates |

| • Development of consumer economies |

| • Foreign investment in emerging market banks |

|

|

Wireless | • 25% of international revenue now wireless; fastest growing product line |

Solutions | • Wireless solutions attract premium margins |

| • Many international markets lack reliable land line infrastructure |

| • Banks need to “capture” cash transactions (40% of total in US) |

|

|

Proliferation | • Demand for faster, advanced IP-enabled payment solutions |

of IP | • Powerful phenomenon driving US reterminalization |

7

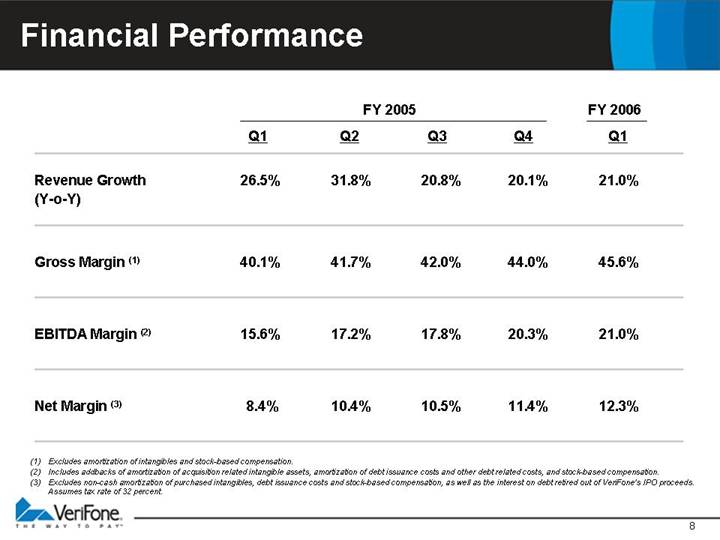

Financial Performance

|

| FY 2005 |

| FY 2006 |

| ||||||

|

| Q1 |

| Q2 |

| Q3 |

| Q4 |

| Q1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Revenue Growth (Y-o-Y) |

| 26.5 | % | 31.8 | % | 20.8 | % | 20.1 | % | 21.0 | % |

|

|

|

|

|

|

|

|

|

|

|

|

Gross Margin (1) |

| 40.1 | % | 41.7 | % | 42.0 | % | 44.0 | % | 45.6 | % |

|

|

|

|

|

|

|

|

|

|

|

|

EBITDA Margin (2) |

| 15.6 | % | 17.2 | % | 17.8 | % | 20.3 | % | 21.0 | % |

|

|

|

|

|

|

|

|

|

|

|

|

Net Margin (3) |

| 8.4 | % | 10.4 | % | 10.5 | % | 11.4 | % | 12.3 | % |

(1) Excludes amortization of intangibles and stock-based compensation.

(2) Includes addbacks of amortization of acquisition related intangible assets, amortization of debt issuance costs and other debt related costs, and stock-based compensation.

(3) Excludes non-cash amortization of purchased intangibles, debt issuance costs and stock-based compensation, as well as the interest on debt retired out of VeriFone’s IPO proceeds. Assumes tax rate of 32 percent.

8

Introduction to Lipman

• Long history of innovation

• Founded in 1974

• Public in Tel Aviv since 1993 and on NASDAQ since 2004

• Consistently first to market with new technologies

• Leading wireless portfolio

• Focus on emerging markets and wireless solutions

• China, India, Brazil, Turkey

• Leading share of US wireless installed base

• Attractive financial profile

• History of 20%+ revenue growth and 40%+ gross margins

• Highly efficient business model

• Substantial cash balance and zero debt

• Well managed and well positioned to continue growth

• Not a “turn-around” story

• Strong management team led by Isaac Angel – 27 years experience at Lipman

10

• Strong financial performance + strong financial performance = stronger financial performance and immediate accretion

• Complementary geographic coverage

• Cements leading position in North America

• Creates #1 position across emerging markets

• Creates #1 or #2 position in most other major markets worldwide

• Ability to deploy Lipman’s advanced wireless portfolio across VeriFone’s worldwide distribution platform

• Strong customer relationships

• Complementary efficient manufacturing models

12

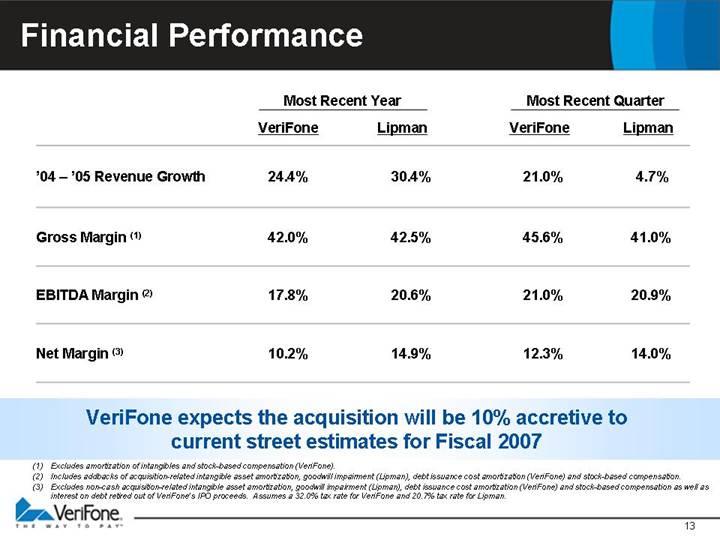

Financial Performance

|

| Most Recent Year |

| Most Recent Quarter |

| ||||

|

| VeriFone |

| Lipman |

| VeriFone |

| Lipman |

|

|

|

|

|

|

|

|

|

|

|

’04 – ’05 Revenue Growth |

| 24.4 | % | 30.4 | % | 21.0 | % | 4.7 | % |

|

|

|

|

|

|

|

|

|

|

Gross Margin (1) |

| 42.0 | % | 42.5 | % | 45.6 | % | 41.0 | % |

|

|

|

|

|

|

|

|

|

|

EBITDA Margin (2) |

| 17.8 | % | 20.6 | % | 21.0 | % | 20.9 | % |

|

|

|

|

|

|

|

|

|

|

Net Margin (3) |

| 10.2 | % | 14.9 | % | 12.3 | % | 14.0 | % |

VeriFone expects the acquisition will be 10% accretive to

current street estimates for Fiscal 2007

(1) Excludes amortization of intangibles and stock-based compensation (VeriFone).

(2) Includes addbacks of acquisition-related intangible asset amortization, goodwill impairment (Lipman), debt issuance cost amortization (VeriFone) and stock-based compensation.

(3) Excludes non-cash acquisition-related intangible asset amortization, goodwill impairment (Lipman), debt issuance cost amortization (VeriFone) and stock-based compensation as well as interest on debt retired out of VeriFone’s IPO proceeds. Assumes a 32.0% tax rate for VeriFone and 20.7% tax rate for Lipman.

13

Complementary Geographic Coverage

VeriFone’s Important Markets |

| Lipman’s Important Markets |

|

|

|

• United States |

| • United States |

• Banks, processors, oil companies, retail |

| • ISO channel |

• Recent focus on ISOs and wireless |

| • Leading wireless provider |

|

|

|

• Europe |

| • Europe |

• Eastern Europe |

| • UK, Spain, Italy |

• Investing for future growth in Continental Europe |

|

|

|

|

|

• Emerging markets |

| • Emerging markets |

• Mexico, Caribbean, South East Asia |

| • China, India, Brazil, Turkey |

VeriFone will be #1 or #2 in most major markets worldwide

14

The China and India Opportunity

|

| [GRAPHIC] |

| [GRAPHIC] |

| [GRAPHIC] |

|

|

|

|

|

|

|

|

| US |

| China |

| India |

|

|

|

|

|

|

|

• Population |

| • 296 million |

| • 1,306 million |

| • 1,080 million |

|

|

|

|

|

|

|

• Annual Electronic Transactions per Person (1) |

| • 155.0 |

| • 1.0 |

| • 1.0 |

|

|

|

|

|

|

|

• Financial Card Transaction CAGR (1) |

| • 11.0% |

| • 30.0% |

| • 99.0% |

|

|

|

|

|

|

|

• Solutions / 1,000 people (2) |

| • 9.8 |

| • 0.5 |

| • 0.1 |

|

|

|

|

|

|

|

• Key Trends |

| • Wireless |

| • Foreign bank ownership |

| • Foreign bank ownership |

|

|

|

|

|

|

|

|

| • IP |

| • VAT collection |

| • Strong economic growth |

|

|

|

|

|

|

|

|

| • PIN-Debit |

| • Modernization |

| • VAT collection |

|

|

|

|

|

|

|

|

|

|

| • Olympics |

| • Expanding wireless networks |

15

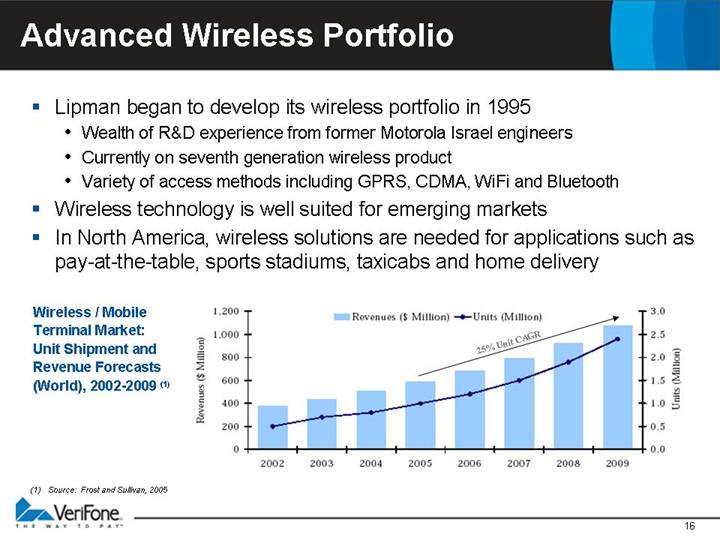

Advanced Wireless Portfolio

• Lipman began to develop its wireless portfolio in 1995

• Wealth of R&D experience from former Motorola Israel engineers

• Currently on seventh generation wireless product

• Variety of access methods including GPRS, CDMA, WiFi and Bluetooth

• Wireless technology is well suited for emerging markets

• In North America, wireless solutions are needed for applications such as pay-at-the-table, sports stadiums, taxicabs and home delivery

Wireless / Mobile Terminal Market: Unit Shipment and Revenue Forecasts (World), 2002-2009 (1)

[CHART]

(1) Source: Frost and Sullivan, 2005

16

Strong Customer Relationships

Lipman has strong customer relationships

• Customers diversified geographically

• Never lost a material customer

• Many customers purchase a range of Lipman products

Key Customers

[LOGO]

17

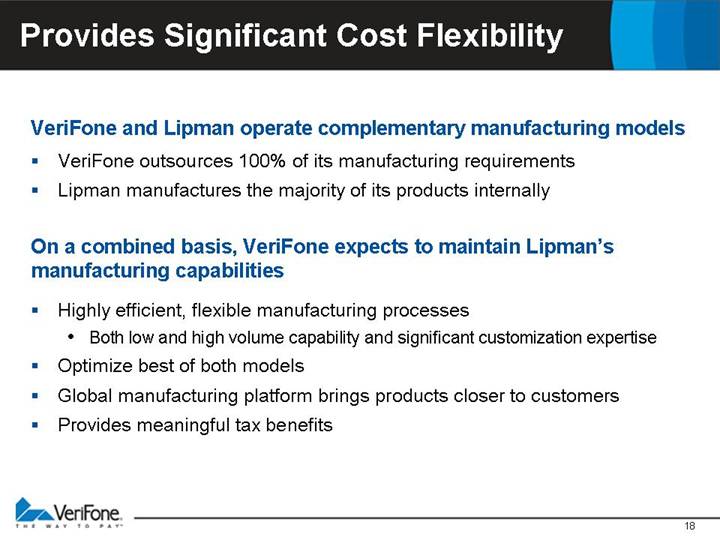

Provides Significant Cost Flexibility

VeriFone and Lipman operate complementary manufacturing models

• VeriFone outsources 100% of its manufacturing requirements

• Lipman manufactures the majority of its products internally

On a combined basis, VeriFone expects to maintain Lipman’s manufacturing capabilities

• Highly efficient, flexible manufacturing processes

• Both low and high volume capability and significant customization expertise

• Optimize best of both models

• Global manufacturing platform brings products closer to customers

• Provides meaningful tax benefits

18

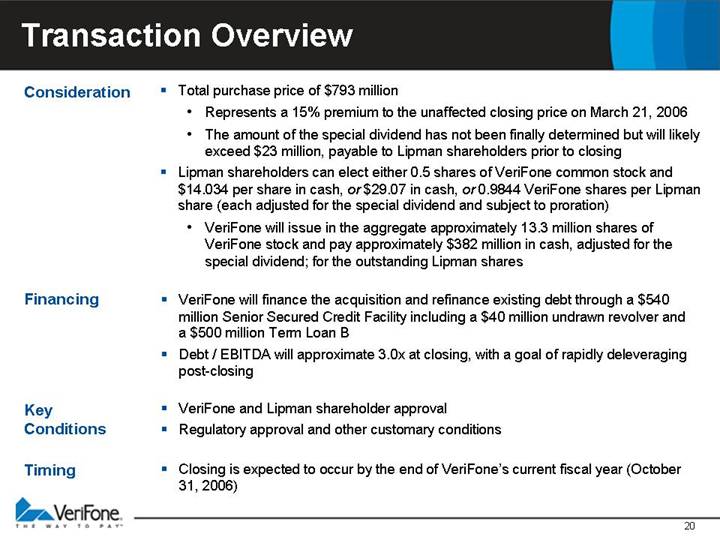

Consideration |

| • Total purchase price of $793 million |

|

|

|

|

| • Represents a 15% premium to the unaffected closing price on March 21, 2006 |

|

|

|

|

| • The amount of the special dividend has not been finally determined but will likely exceed $23 million, payable to Lipman shareholders prior to closing |

|

|

|

|

| • Lipman shareholders can elect either 0.5 shares of VeriFone common stock and $14.034 per share in cash, or $29.07 in cash, or 0.9844 VeriFone shares per Lipman share (each adjusted for the special dividend and subject to proration) |

|

|

|

|

| • VeriFone will issue in the aggregate approximately 13.3 million shares of VeriFone stock and pay approximately $382 million in cash, adjusted for the special dividend; for the outstanding Lipman shares |

|

|

|

Financing |

| • VeriFone will finance the acquisition and refinance existing debt through a $540 million Senior Secured Credit Facility including a $40 million undrawn revolver and a $500 million Term Loan B |

|

|

|

|

| • Debt / EBITDA will approximate 3.0x at closing, with a goal of rapidly deleveraging post-closing |

|

|

|

Key Conditions |

| • VeriFone and Lipman shareholder approval |

|

|

|

|

| • Regulatory approval and other customary conditions |

|

|

|

Timing |

| • Closing is expected to occur by the end of VeriFone’s current fiscal year (October 31, 2006) |

20

Why Now?

Why Now for VeriFone? |

| • Demonstrated track record in public market since IPO |

|

|

|

|

| • Outperformed expectations for 4 quarters as a public company |

|

|

|

|

| • Accelerating focus on emerging market opportunities including China and India |

|

|

|

|

| • Wireless has become a growth accelerator |

|

|

|

|

| • Vx Solutions platform transition now complete |

|

|

|

Why Now for Lipman? |

| • Breadth and scale are critically important to remain on leading edge of technology and product development |

|

|

|

|

| • Research and development spend is a differentiator |

|

|

|

|

| • VeriFone’s distribution infrastructure will accelerate sales of Lipman’s leading wireless platform |

21

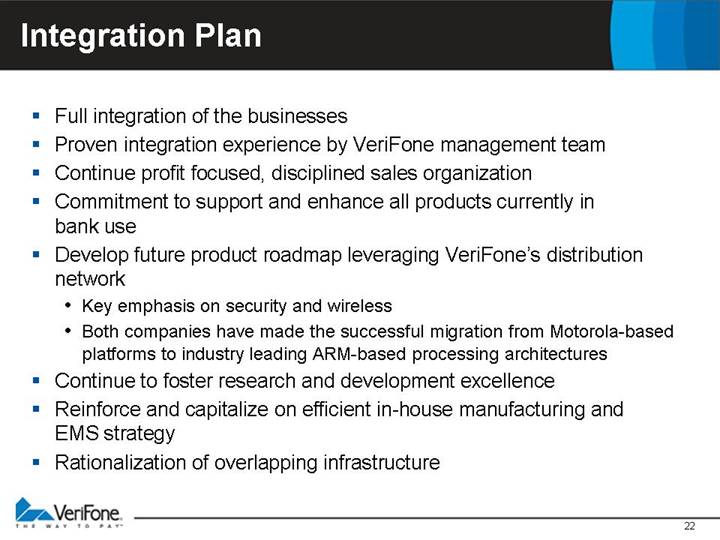

Integration Plan

• Full integration of the businesses

• Proven integration experience by VeriFone management team

• Continue profit focused, disciplined sales organization

• Commitment to support and enhance all products currently in bank use

• Develop future product roadmap leveraging VeriFone’s distribution network

• Key emphasis on security and wireless

• Both companies have made the successful migration from Motorola-based platforms to industry leading ARM-based processing architectures

• Continue to foster research and development excellence

• Reinforce and capitalize on efficient in-house manufacturing and EMS strategy

• Rationalization of overlapping infrastructure

22

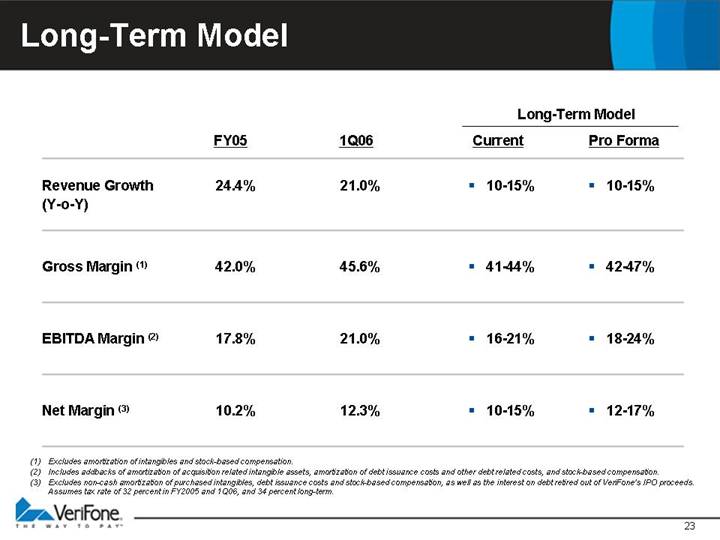

Long-Term Model

|

|

|

|

|

| Long-Term Model |

| ||||

|

| FY05 |

| 1Q06 |

| Current |

| Pro Forma |

| ||

|

|

|

|

|

|

|

|

|

| ||

Revenue Growth (Y-o-Y) |

| 24.4 | % | 21.0 | % | • | 10-15 | % | • | 10-15 | % |

|

|

|

|

|

|

|

|

|

|

|

|

Gross Margin (1) |

| 42.0 | % | 45.6 | % | • | 41-44 | % | • | 42-47 | % |

|

|

|

|

|

|

|

|

|

|

|

|

EBITDA Margin (2) |

| 17.8 | % | 21.0 | % | • | 16-21 | % | • | 18-24 | % |

|

|

|

|

|

|

|

|

|

|

|

|

Net Margin (3) |

| 10.2 | % | 12.3 | % | • | 10-15 | % | • | 12-17 | % |

(1) Excludes amortization of intangibles and stock-based compensation.

(2) Includes addbacks of amortization of acquisition related intangible assets, amortization of debt issuance costs and other debt related costs, and stock-based compensation.

(3) Excludes non-cash amortization of purchased intangibles, debt issuance costs and stock-based compensation, as well as the interest on debt retired out of VeriFone’s IPO proceeds. Assumes tax rate of 32 percent in FY2005 and 1Q06, and 34 percent long-term.

23

Capitalization

|

| As of January 31, 2006 |

| |||||||||||||

|

| VeriFone |

| Lipman |

| Combined |

| Adjust. |

| Pro Forma |

| |||||

|

|

|

|

|

|

|

|

|

|

|

| |||||

Cash (1) |

| $ | 88.2 |

| $ | 116.9 |

| $ | 205.1 |

| $ | (97.6 | ) | $ | 107.5 |

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

Debt |

| $ | 182.3 |

| — |

| $ | 182.3 |

| $ | 317.7 |

| $ | 500.0 |

| |

|

|

|

|

|

|

|

|

|

|

|

| |||||

Equity |

| $ | 42.6 |

| $ | 252.5 |

| — |

| — |

| $ | 445.5 |

| ||

|

|

|

|

|

|

|

|

|

|

|

| |||||

Total Capitalization |

| $ | 224.9 |

| $ | 252.5 |

| — |

| — |

| $ | 945.5 |

| ||

(1) Lipman cash and cash equivalents of $124.4 million as of 12/31/05 less $7.5 million in share repurchases since the end of 2005.

24