Groupe De Divertissement Superclub Inactive

Filed: 18 Jan 05, 12:00am

As filed with the Securities and Exchange Commission on January 14, 2005

Registration No. 333-121032

SECURITIES AND EXCHANGE COMMISSION

Washington D.C. 20549

AMENDMENT NO. 1

TO

Form F-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

VIDÉOTRON LTÉE

AND THE GUARANTORS LISTED ON THE TABLE OF ADDITIONAL REGISTRANTS*

(Exact name of Registrant as specified in its charter)

| Province of Quebec (State or other jurisdiction of incorporation or organization) | 4841 (Primary Standard Industrial Classification Code Number) | Not applicable (I.R.S. Employer Identification No.) | ||

Vidéotron Ltée 300 Viger Avenue East Montreal, Quebec H2X 3W4 Canada (514) 281-1232 (Address, including zip code, and telephone number, including area code, of registrant's principal executive offices) | ||||

| CT Corporation System 111 Eighth Avenue New York, New York 10011 (212) 894-8600 (Name, address, including zip code, and telephone number, including area code, of agent for service) |

| Copies to: | ||

| John A. Willett, Esq. Christine D. Rogers, Esq. Arnold & Porter LLP 399 Park Avenue New York, New York 10022-4690 (212) 715-1000 | Marc Lacourcière, Esq. Ogilvy Renault 1981 McGill College Avenue, Suite 1100 Montreal, Québec H3A 3C1 Canada (514) 847-4747 | |

Approximate date of commencement of proposed sale of the securities to the public: As soon as practicable following the effectiveness of this registration statement.

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.o

CALCULATION OF REGISTRATION FEE

| Title of each class of securities to be registered | Amount to be registered | Proposed maximum offering price per unit(1) | Proposed maximum aggregate offering price(1) | Amount of registration fee(1) | ||||

|---|---|---|---|---|---|---|---|---|

| 67/8% Senior Notes due January 15, 2014 | $315,000,000 | 100% | $315,000,000 | $39,910.50(3) | ||||

| Guarantees of 67/8% Senior Notes due January 15, 2014(2) | — | — | — | — | ||||

The co-registrants hereby amend this registration statement on such date or dates as may be necessary to delay its effective date until the co-registrants shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

TABLE OF ADDITIONAL REGISTRANTS

The following subsidiaries of Vidéotron Ltée have fully and unconditionally guaranteed the 67/8% Senior Notes due January 15, 2014 of Vidéotron Ltée and are additional registrants under this Registration Statement.

| Exact Name of Additional Registrant as Specified in its Charter* | State or Other Jurisdiction of Incorporation or Organization | Primary Standard Industrial Classification Code Number | I.R.S. Employer Identification Number | |||

|---|---|---|---|---|---|---|

| Vidéotron TVN inc. | Province of Québec | 4841 | N/A | |||

| Le SuperClub Vidéotron ltée | Province of Québec | 7841 | N/A | |||

| Vidéotron (1998) ltée | Province of Québec | 4841 | N/A | |||

| Groupe de Divertissement SuperClub Inc. | Province of Québec | 7841 | N/A | |||

| SuperClub Vidéotron Canada inc. | Province of Québec | 7841 | N/A | |||

| Les Propriétés SuperClub inc. | Province of Québec | 7841 | N/A |

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to completion, dated January 14, 2005

| PROSPECTUS |

US$315,000,000

Vidéotron Ltée

Offer to Exchange All Outstanding US$315,000,000 Principal Amount of

67/8% Senior Notes due January 15, 2014

Issued on November 19, 2004

for US$315,000,000 Principal Amount of

67/8% Senior Notes due January 15, 2014

That Have Been Registered Under the Securities Act of 1933

The Exchange Offer:

The New Notes:

This investment involves risks. See "Risk Factors" beginning on page 15.

Neither the Securities and Exchange Commission nor any state securities commission has

approved or disapproved of these securities or determined if this prospectus is truthful or complete.

Any representation to the contrary is a criminal offense.

The date of this prospectus is January , 2005

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with different information. We are not making an offer of these securities in any state or other jurisdiction where the offer is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than the date on the front of this prospectus.

| | Page | |

|---|---|---|

| Industry and Market Data | ii | |

| Enforceability of Civil Liabilities | ii | |

| Forward-Looking Statements | ii | |

| Presentation of Financial Information | iii | |

| Exchange Rates | iii | |

| Summary | 1 | |

| Risk Factors | 15 | |

| Use of Proceeds | 25 | |

| Capitalization | 26 | |

| Selected Consolidated Financial and Operating Data | 27 | |

| Management's Discussion and Analysis of Financial Condition and Results of Operations | 33 | |

| Business | 50 | |

| Management | 72 | |

| Our Shareholder | 78 | |

| Certain Relationships and Related Transactions | 78 | |

| Description of Certain Indebtedness | 82 | |

| The Exchange Offer | 85 | |

| Description of the Notes | 95 | |

| Certain Tax Considerations | 140 | |

| Notice to Canadian Investors | 144 | |

| Plan of Distribution | 146 | |

| Legal Matters | 146 | |

| Independent Auditors | 146 | |

| Where You Can Find More Information | 147 | |

| Index to Financial Statements | F-1 |

This prospectus incorporates by reference documents that contain important business and financial information about Vidéotron that is not included in or delivered with this prospectus. These documents are available without charge to security holders upon written or oral request to: Vidéotron Ltée, 300 Viger Avenue East, Montreal, Québec, Canada H2X 3W4, Attention: Corporate Secretary, telephone number (514) 281-1232. To obtain timely delivery, holders of the old notes must request these documents no later than five business days before the expiration date. Unless extended, the expiration date is February , 2005.

i

Market data and certain industry statistics used throughout this prospectus were obtained from internal surveys, market research, publicly available information and industry publications. Industry publications generally state that the information contained therein has been obtained from sources believed to be reliable, but that the accuracy and completeness of such information is not guaranteed. Similarly, internal surveys and industry and market data, while believed to be reliable, have not been independently verified, and we make no representation as to the accuracy or completeness of such information.

ENFORCEABILITY OF CIVIL LIABILITIES

We are incorporated under the laws of the Province of Québec. Substantially all our directors, controlling persons and officers, as well as certain of the experts named in this prospectus, are residents of Canada, and all or a substantial portion of their assets and all of our assets are located outside the United States. We have agreed, in accordance with the terms of the indenture under which the new notes will be issued, to accept service of process in any suit, action or proceeding with respect to the indenture or the new notes brought in any federal or state court located in New York City by an agent designated for such purpose, and to submit to the jurisdiction of such courts in connection with such suits, actions or proceedings. However, it may be difficult for holders of the new notes to effect service within the United States upon directors, officers and experts who are not residents of the United States or to realize in the United States upon judgments of courts of the United States predicated upon civil liability under U.S. federal or state securities laws. We have been advised by Ogilvy Renault, our Canadian counsel, that there is doubt as to the enforceability in Canada against us or against our directors, officers and experts who are not residents of the United States, in original actions or in actions for enforcement of judgments of courts of the United States, of liabilities predicated solely upon U.S. federal or state securities laws.

This prospectus includes "forward-looking statements" within the meaning of Section 27A of the Securities Act and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act. All statements other than statements of historical facts included in this prospectus, including, without limitation, statements under the captions "Summary," "Risk Factors," "Use of Proceeds," "Capitalization," "Management's Discussion and Analysis of Financial Condition and Results of Operations" and "Business" as well as statements located elsewhere in this prospectus regarding the prospects of our industry and our prospects, plans, financial position and business strategy, may constitute forward-looking statements. In addition, forward-looking statements generally can be identified by the use of forward-looking terminology such as "may," "will," "expect," "intend," "estimate," "anticipate," "plan," "foresee," "believe" or "continue" or the negatives of these terms or variations of them or similar terminology. Although we believe that the expectations reflected in these forward-looking statements are reasonable, we can give no assurance that these expectations will prove to have been correct. While the below list of cautionary statements is not exhaustive, some important factors that could affect future operating results, financial position and cash flows and could cause actual results to differ materially from those expressed in these forward-looking statements are:

These and other factors could cause actual results to differ materially from our expectations expressed in the forward-looking statements included in this prospectus, and further details and descriptions of these and other factors are disclosed in this prospectus, including under the section "Risk Factors." Each of these forward-looking statements speak only as of the date of this prospectus. We will not update these statements unless the securities laws require us to do so.

ii

PRESENTATION OF FINANCIAL INFORMATION

Our consolidated financial statements, the financial statements of Videotron Telecom Ltd. and our unaudited pro forma combined financial information included in this prospectus have been prepared in accordance with accounting principles generally accepted in Canada, or Canadian GAAP. For a discussion of the principal differences between Canadian GAAP and accounting principles generally accepted in the United States, or U.S. GAAP, see note 22 to our audited consolidated financial statements for the years ended December 31, 2001, 2002 and 2003, note 8 to our unaudited interim consolidated financial statements for the nine months ended September 30, 2003 and 2004, note 19 to the audited financial statements of Videotron Telecom Ltd. for the years ended December 31, 2002 and 2003, note 7 to the unaudited interim financial statements of Videotron Telecom Ltd. for the nine months ended September 30, 2003 and 2004 and note (b) to our unaudited pro forma combined financial information, all of which are included in this prospectus.

Both we and Videotron Telecom Ltd. state our financial statements in Canadian dollars. In this prospectus, references to Canadian dollars, Cdn$ or $ are to the currency of Canada and references to U.S. dollars or US$ are to the currency of the United States.

We use in this prospectus certain financial measures that are not calculated in accordance with Canadian or U.S. GAAP to assess our financial performance and Videotron Telecom's financial performance. For example, we use EBITDA (and related ratios), cash interest expense and long-term debt, excluding QMI subordinated loans, in this prospectus. We provide the calculation of these non-GAAP financial measures and a reconciliation to the most directly comparable GAAP financial measures in notes 6, 7 and 9 under "Selected Consolidated Financial and Operating Data."

The following table sets forth, for the periods indicated, the average, high, low and end of period noon buying rates in the City of New York for cable transfers in foreign currencies as certified for customs purposes by the Federal Reserve Bank of New York, or the noon buying rate. Such rates are set forth as US dollars per Cdn$1.00 and are the inverse of rates quoted by the Federal Reserve Bank of New York for Canadian dollars per US$1.00. On January 13, 2005, the inverse of the noon buying rate was Cdn$1.00 equals US$0.8330.

| Year Ended | Average(1) | High | Low | Period End | ||||

|---|---|---|---|---|---|---|---|---|

| December 31, 2004 | 0.7719 | 0.8493 | 0.7158 | 0.8310 | ||||

| December 31, 2003 | 0.7136 | 0.7738 | 0.6349 | 0.7738 | ||||

| December 31, 2002 | 0.6370 | 0.6619 | 0.6200 | 0.6329 | ||||

| December 31, 2001 | 0.6446 | 0.6697 | 0.6241 | 0.6279 | ||||

| December 31, 2000 | 0.6727 | 0.6969 | 0.6410 | 0.6669 | ||||

| December 31, 1999 | 0.6746 | 0.6925 | 0.6535 | 0.6925 |

| Nine Months Ended | Average(1) | High | Low | Period End | ||||

|---|---|---|---|---|---|---|---|---|

| September 30, 2004 | 0.7525 | 0.7906 | 0.7243 | 0.7906 | ||||

| September 30, 2003 | 0.7000 | 0.7492 | 0.6349 | 0.7404 |

| Month Ended | Average(2) | High | Low | Period End | ||||

|---|---|---|---|---|---|---|---|---|

| December 31, 2004 | 0.8204 | 0.8435 | 0.8064 | 0.8310 | ||||

| November 30, 2004 | 0.8357 | 0.8493 | 0.8155 | 0.8402 | ||||

| October 31, 2004 | 0.8020 | 0.8201 | 0.7850 | 0.8191 | ||||

| September 30, 2004 | 0.7763 | 0.7906 | 0.7651 | 0.7906 | ||||

| August 30, 2004 | 0.7618 | 0.7714 | 0.7506 | 0.7595 | ||||

| July 31, 2004 | 0.7561 | 0.7644 | 0.7489 | 0.7521 |

iii

Canada has no system of exchange controls. There are no Canadian restrictions on the repatriation of capital or earnings of a Canadian company to non-resident investors. There are no laws of Canada or exchange restrictions affecting the remittance of dividends, interest, royalties or similar payments to non-resident holders of our securities, except as described under "Certain Tax Considerations — Canadian Material Federal Income Tax Considerations for Non-Residents of Canada."

iv

The following summary highlights selected information included in this prospectus to help you understand Vidéotron Ltée, the exchange offer and the new notes. For a more complete understanding of Vidéotron Ltée, the exchange offer and the new notes, we encourage you to read this entire prospectus carefully. Unless the context indicates or otherwise requires, the terms "Vidéotron," "our company," "we," "us" and "our" as used in this prospectus refer to Vidéotron Ltée and its consolidated subsidiaries.

We are the largest distributor of pay-television services in the Province of Québec and the third largest cable operator in Canada based on the number of cable customers. We hold cable licenses that cover approximately 80% of Québec's 3.0 million homes passed by cable, which includes residential and commercial premises. Our cable licenses include licenses for the greater Montréal area, the second largest urban area in Canada. The greater Montréal area represents one of the largest contiguous clusters in Canada and is among the largest in North America as measured by the number of cable customers. This concentration provides us with improved operating efficiencies and is a key element in the development and launch of our bundled service offerings. In 2001, we substantially completed our network modernization program, which has provided us with one of the largest bi-directional hybrid fiber coaxial (HFC) networks in North America, with approximately 97% of our systems upgraded to two-way capability and 74% of our customers served by systems upgraded to 750 MHz.

In July 2004, we announced our intention to launch a telephony service using Voice over IP technology in Québec. This project is being conducted with another wholly owned subsidiary of Quebecor Media, Videotron Telecom Ltd., or Videotron Telecom, which holds a license as a competitive local exchange carrier and will initially provide the circuit switches and local network interconnection services. We are currently conducting technical field tests for this telephony service, and we anticipate launching this service progressively among our residential and commercial customers in the first half of 2005. Our new telephony service will include local and long-distance calling and permit our customers to access a host of other telephony services, such as enhanced 911 Emergency service, name and number caller ID and automatic call forwarding.

Through SuperClub Vidéotron, we also own the largest chain of video and game rental stores in Québec and among the largest of such chains in Canada, with a total of 288 retail locations (of which 241 are franchised) and more than 1.65 million video club rental members. With approximately 145 retail locations located in our markets, SuperClub Vidéotron is both a showcase and a valuable and cost-effective distribution network for our growing array of advanced products and services, such as high-speed Internet access and digital television.

We are a wholly owned subsidiary of Quebecor Media. Quebecor Media is a leading Canadian-based media company with interests in newspaper publishing operations, television broadcasting, business telecommunications, book and magazine publishing and new media services, as well as our cable operations. Through these interests, Quebecor Media holds leading positions in the creation, promotion and distribution of news, entertainment and Internet-related services that are designed to appeal to audiences in every demographic category.

Quebecor Media is 54.7% owned by Quebecor Inc., a communications holding company, and 45.3% owned by CDP Capital-Communications. Quebecor Inc.'s primary assets are its interests in Quebecor Media and Quebecor World Inc., one of the world's largest commercial printers. CDP Capital-Communications is a wholly owned subsidiary of Caisse de dépôt et placement du Québec, Canada's largest pension fund with over $140 billion in assets under management.

Quebecor Media is neither an obligor nor a guarantor of our obligations under the notes.

1

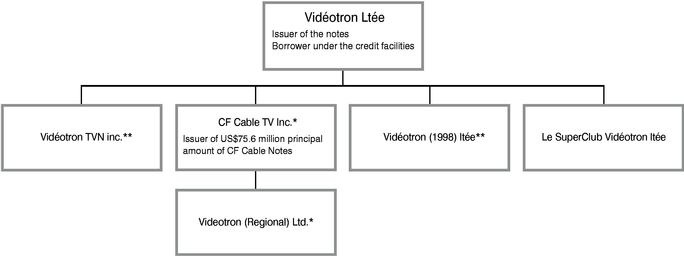

Our current corporate structure is (certain immaterial subsidiaries have been omitted):

All of the subsidiaries in the above corporate chart are wholly owned and, with the exception of CF Cable TV Inc., or CF Cable, and Videotron (Regional) Ltd., or Videotron Regional, will guarantee the new notes. CF Cable and Videotron Regional have undertaken to become guarantors of the notes at such time when CF Cable's 9.125% Senior Secured First Priority Notes due 2007, or the CF Cable notes, are no longer outstanding.

We currently expect that the operations of Videotron Telecom, which is a wholly owned subsidiary of Quebecor Media, will be integrated within our own operations in 2005, subject to the approval of the CRTC and our lenders, as well as the satisfactory completion of discussions with our labor unions. Combining Videotron Telecom's telecommunication network and expertise with our commercial customer base will, we believe, enable us to offer additional bundled services to those customers, which we expect will result in new business opportunities. In addition, this reorganization is a continuation of the collaboration between Videotron Telecom and our company in the Voice over IP project and fiber network development.

Videotron Telecom is a provider of a full range of business telecommunications services, including local service, long distance, high speed data transmission, Internet connectivity and Internet hosting, to customers that include businesses and governmental end users and other telecommunications service providers in Canada. Videotron Telecom's regional network has over 9,000 km of fiber optic cable in Québec and 2,000 km in Ontario and reaches more than 80% of business located in the metropolitan areas of Québec and most of the businesses located in the major metropolitan areas of Ontario. Videotron Telecom's extensive network supports direct connectivity with networks in Ontario, eastern Québec, the Maritimes and the United States. In addition, approximately 33% of Videotron Telecom's revenue in 2003 came from services provided to Quebecor Inc. and Quebecor Media and its subsidiaries.

For the year ended December 31, 2003, Videotron Telecom generated revenues of $75.6 million (including $19.9 million of revenues from Vidéotron and its subsidiaries) and EBITDA of $14.8 million. For the nine-month period ended September 30, 2004, Videotron Telecom's revenues were $56.1 million (including $9.3 million of revenues from Vidéotron and its subsidiaries) and EBITDA was $9.7 million. See the reconciliation of Videotron Telecom's EBITDA to its net loss in note 7 under "Selected Consolidated Financial and Operating Data."

2

Amendments to Our Credit Facilities

Concurrently with the completion of the private placement offering of the old notes on November 19, 2004, we used the net proceeds from the offering of the old notes to, among other things, repay in full the current outstanding indebtedness under the $318.1 million Term C loan under our credit facilities and amended the terms of our credit agreement to, among other things, increase our revolving credit facility from $100.0 million to $450.0 million and extend its maturity to November 2009.

These amendments create additional financial flexibility to allow us to redeem the CF Cable notes, which are callable at par in July 2005, and to finance future distributions to Quebecor Media, our parent company.

See "Description of Certain Indebtedness — Credit Facilities — General."

Our Principal Executive Office

Our principal executive office is located at 300 Viger Avenue East, Montréal, Province of Québec, Canada H2X 3W4. Our telephone number is (514) 281-1232.

3

On November 19, 2004, we sold our 67/8% Senior Notes due January 15, 2014 in a private placement exempt from the registration requirements of the Securities Act, and the initial purchasers of these old notes then resold them in reliance on other exemptions from the registration requirements of the Securities Act. We and the subsidiary guarantors of the old notes entered into a registration rights agreement with the initial purchasers. Under the registration rights agreement, we agreed, among other things, to deliver to you this prospectus and to keep the exchange offer open for not less than 30 days after the date notice of the exchange offer is mailed to the holders of the old notes. In addition, we agreed that if the exchange offer is not completed by May 18, 2005, we will file, and use our best efforts to cause to become effective, a shelf registration statement covering the resale of the old notes. You are entitled to exchange in the exchange offer your old notes for new notes, which are identical in all material respects to the old notes except that:

The terms of the new notes to be issued in the exchange offer will be identical to the terms of the US$335.0 million principal amount of our existing 67/8% Senior Notes due January 15, 2014, which were issued on October 8, 2003 and have been registered under the Securities Act.

The Exchange Offer | We are offering to exchange up to US$315.0 million aggregate principal amount of our new 67/8% Senior Notes due January 15, 2014, which have been registered under the Securities Act, for up to US$315.0 million aggregate principal amount of our old 67/8% Senior Notes due January 15, 2014, which were issued on November 19, 2004 pursuant to a private placement offering. Old notes may be exchanged only in integral multiples of US$1,000. | |

Resale of the New Notes | Based on interpretations by the staff of the SEC set forth in no-action letters issued to third parties, we believe that the new notes issued in the exchange offer may be offered for resale, resold and otherwise transferred by you (unless you are our "affiliate" within the meaning of Rule 405 under the Securities Act) without compliance with the registration and prospectus delivery requirements of the Securities Act,provided that you are: | |

• acquiring the new notes in the ordinary course of business; | ||

• not participating, do not intend to participate, and have no arrangement or understanding with any person to participate in the distribution of the new notes; and | ||

• not a broker-dealer who purchased your old notes directly from us for resale pursuant to Rule 144A or any other available exemption under the Securities Act. | ||

We do not intend to seek our own no-action letter, and there is no assurance that the SEC staff would make a similar determination with respect to the new notes. If this interpretation is inapplicable and you transfer any new notes issued to you in the exchange offer without delivering a prospectus or without an exemption under the Securities Act, you may incur liability under the Securities Act. We do not assume or indemnify you against this liability. | ||

4

Each broker-dealer that receives new notes for its own account in exchange for the old notes that were acquired by this broker-dealer as a result of market-making activities or other trading activities must acknowledge that it will deliver a prospectus in connection with any resale of those new notes. See "Plan of Distribution." | ||

Any holder of old notes who: | ||

• is our "affiliate" as defined in Rule 405 under the Securities Act; | ||

• does not acquire the new notes in the ordinary course of its business; | ||

• tenders in the exchange offer with the intention to participate, or for the purpose of participating, in a distribution of the new notes; or | ||

• is a broker-dealer that purchased old notes from us to resell them pursuant to Rule 144A or any other available exemption under the Securities Act, | ||

cannot rely on the position of the SEC staff expressed in the no-action letters described above and, in the absence of an exemption, must comply with the registration and prospectus delivery requirements of the Securities Act in connection with the resale of the new notes. | ||

Expiration of Exchange Offer | The exchange offer will expire at 5:00 p.m., New York City time, on February , 2005, unless we decide to extend the expiration date. | |

Withdrawal Rights | You may withdraw the tender of your old notes at any time prior to 5:00 p.m., New York City time, on the expiration date. | |

Accrued Interest on the New Notes and the Old Notes | The old note and the new notes will bear interest from July 15, 2004. | |

Conditions to the Exchange Offer | The exchange offer is subject to customary conditions, some of which we may waive. See "The Exchange Offer — Conditions to the Exchange Offer." | |

Procedures for Tendering Old Notes | If you wish to exchange your old notes for new notes pursuant to the exchange offer, you must complete, sign and date the letter of transmittal according to the instructions contained in this prospectus and the letter of transmittal. You must also mail or otherwise deliver the letter of transmittal, together with your old notes and any other required documents, to the exchange agent at the address set forth on the cover of the letter of transmittal. If you hold old notes through the Depository Trust Company, or DTC, and wish to participate in the exchange offer, you must comply with the Automated Tender Offer Program procedures of DTC, by which you will agree to be bound by the letter of transmittal. | |

By signing or agreeing to be bound by the letter of transmittal, you will represent to us that, among other things: | ||

• you are acquiring the new notes in the ordinary course of business; | ||

5

• you have no arrangement or understanding with any person to participate in the distribution of the new notes; | ||

• if you are a broker-dealer that will receive new notes for your own account in exchange for old notes that were acquired as a result of market-making or other trading activities, you will deliver a prospectus, as required by law, in connection with any resale of the new notes; and | ||

• you are not our "affiliate" as defined in Rule 405 under the Securities Act. | ||

See "The Exchange Offer — Procedures for Tendering Old Notes." | ||

Special Procedures for Beneficial Owners | If you own a beneficial interest in old notes that are registered in the name of a broker, dealer, commercial bank, trust company or other nominee or custodian, and you wish to tender your old notes in the exchange offer, you should contact the registered holder as soon as possible and instruct the registered holder to tender on your behalf. | |

Guaranteed Delivery Procedures | If you wish to tender your old notes and your old notes are not immediately available or you cannot deliver your old notes, the letter of transmittal or any other documents required by the letter of transmittal to the exchange agent or comply with the applicable procedures under DTC's Automated Tender Offer Program by the expiration date, you must tender your old notes pursuant to the guaranteed delivery procedures described in this prospectus under the heading "The Exchange Offer — Procedures for Tendering Old Notes — Guaranteed Delivery Procedures." | |

Consequences of Failure to Exchange the Old Notes for the New Notes | All unexchanged old notes will continue to be subject to transfer restrictions. In general, the old notes may not be offered or sold unless registered under the Securities Act or pursuant to an exemption from registration under the Securities Act and applicable state securities laws. Therefore, the market for secondary resales of any unexchanged old notes is likely to be minimal. Other than in connection with the exchange offer, we do not currently anticipate that we will register the old notes under the Securities Act. | |

Federal Income Tax Consequences | The exchange of the old notes for the new notes will generally not be a taxable event for U.S. federal income tax purposes. See "Certain Tax Considerations — Certain U.S. Federal Income Tax Considerations." | |

Use of Proceeds | We will not receive any cash proceeds from the issuance of the new notes in the exchange offer. We will pay all expenses incident to the exchange offer. See "Use of Proceeds" and "The Exchange Offer — Fees and Expenses." | |

Exchange Agent for Notes | Wells Fargo Bank, National Association is the exchange agent for the exchange offer. |

6

The summary below describes the principal terms of the new notes. Some of the terms and conditions described below are subject to important limitations and exceptions. The "Description of the Notes" section of this prospectus contains a more detailed description of the terms and conditions of the notes.

Issuer | Vidéotron Ltée. | |||

Securities | US$315,000,000 in principal amount of senior unsecured notes due January 15, 2014. The new notes will be issued under an indenture dated as of October 8, 2003, as supplemented, pursuant to which we previously issued US$335,000,000 aggregate principal amount of our existing 67/8% Senior Notes due January 15, 2014 that had been registered under the Securities Act. The new notes will rank equally and form part of a single series with these existing notes and will have the same terms as these existing notes. | |||

Maturity | January 15, 2014. | |||

Interest | Annual rate: 67/8%. | |||

Payment frequency: every six months on January 15 and July 15. | ||||

First payment: January 15, 2005. | ||||

Ranking | The existing notes and the old notes are, and the new notes will be, senior unsecured obligations of Vidéotron Ltée. Accordingly, the existing notes and the old notes rank, and the new notes will rank: | |||

• | equally with all of our existing and future unsecured unsubordinated indebtedness; | |||

• | senior to all of our existing and future subordinated indebtedness; | |||

• | effectively subordinated to all of our existing and future secured indebtedness, to the extent of the assets securing such indebtedness; and | |||

• | structurally subordinated to all of the existing and future liabilities, including trade payables, of our subsidiaries that are not guarantors. | |||

After giving effect to the completion of the offering of the old notes and the application of the net proceeds as described under "Use of Proceeds," as of September 30, 2004, we would have had $2,184.7 million of indebtedness, or $934.7 million of indebtedness excluding the QMI subordinated loans, of which $97.1 million would have been senior secured debt of subsidiaries that are not guarantors. These non-guarantor subsidiaries would have had no additional indebtedness to third parties and an additional $83.2 million of total liabilities (excluding inter-company liabilities). See "Capitalization." | ||||

Guarantees | The existing notes and the old notes are, and the new notes will be, guaranteed by certain of our existing and future subsidiaries on a senior unsecured basis. | |||

The guarantees will be general unsecured senior obligations of the guarantors. Accordingly, they will rank equally with all unsecured unsubordinated indebtedness of the guarantors, effectively subordinated to all secured indebtedness of the guarantors, to the extent of the assets securing such indebtedness, and senior to all future subordinated indebtedness of the guarantors. | ||||

7

Optional Redemption | We may redeem the notes, in whole or in part, at any time on or after January 15, 2009 at the redemption prices described in the section "Description of the Notes — Optional Redemption" plus accrued and unpaid interest. | |||

In addition, on or before January 15, 2007, we may redeem up to 35% of the principal amount of the notes with the net cash proceeds from certain equity offerings at the redemption price listed in the section "Description of the Notes — Optional Redemption." | ||||

Tax Redemption | We may also redeem the notes, in whole but not in part, at any time at 100% of the principal amount of the notes plus accrued and unpaid interest, if any, to the date of redemption in the event of changes affecting Canadian withholding taxes that would require us to pay "additional amounts" to holders of the notes. See "Description of the Notes — Redemption for Changes in Withholding Taxes" and "— Payment of Additional Amounts." | |||

Change of Control | If we experience a change in control, we must offer to purchase the notes at 101% of the principal amount plus accrued and unpaid interest, if any, to the date of purchase. | |||

Certain Covenants | The indenture governing the notes limits our ability and the ability of our restricted subsidiaries to: | |||

• | borrow money or sell preferred stock; | |||

• | create liens; | |||

• | pay dividends on or redeem or repurchase our stock; | |||

• | make certain types of investments; | |||

• | sell stock in our restricted subsidiaries; | |||

• | restrict dividends or other payments from restricted subsidiaries; | |||

• | enter into transactions with affiliates; | |||

• | issue guarantees of debt; and | |||

• | sell assets or merge with other companies. | |||

These covenants contain important exceptions, limitations and qualifications. See "Description of the Notes." | ||||

Additional Amounts | Any payments made by us with respect to the notes will be made without withholding or deduction for Canadian taxes unless required by law. If we are required by law to withhold or deduct for Canadian taxes with respect to a payment to the holders of notes, we will pay the additional amount necessary so that the net amount received by the holders of notes after the withholding is not less than the amount that they would have received in the absence of the withholding. See "Description of the Notes — Payment of Additional Amounts." | |||

Tax Consequences | For a discussion of the possible U.S. and Canadian federal income tax consequences of an investment in the new notes, see "Certain Tax Considerations." You should consult your own tax advisor to determine the federal, state, provincial, local and other tax consequences of an investment in the new notes. | |||

8

Use of Proceeds | We will not receive any cash proceeds from the issuance of the new notes in the exchange offer. See "Use of Proceeds." | |||

Absence of an Active Public Market for the New Notes | The old notes are presently eligible for trading in the PORTAL market. We do not intend to apply for the new notes to be listed on any securities exchange or to arrange for any quotation system to quote them. The initial purchasers have advised us that they intend to make a market for the new notes, but they are not obligated to do so. The initial purchasers may discontinue any market making in the new notes at any time in their sole discretion. Accordingly, we cannot assure you that a liquid market for the new notes will develop or be maintained. | |||

You should refer to "Risk Factors" for an explanation of certain risks of investing in the new notes.

9

Summary Consolidated Financial and Operating Data and

Pro Forma Combined Financial Information

The following tables present financial information derived from our consolidated financial statements. Our consolidated financial statements included in this prospectus are comprised of balance sheets as at December 31, 2002 and 2003 and the statements of operations, shareholder's equity and cash flows for each of the years in the three-year period ended December 31, 2003 and have been audited by KPMG LLP, independent chartered accountants. KPMG LLP's report on these audited consolidated financial statements is included in this prospectus. The consolidated balance sheet data as at December 31, 2001 have been derived from the audited consolidated balance sheet not included in this prospectus. The financial information for the nine months ended September 30, 2003 and 2004 are derived from our unaudited interim consolidated financial statements for such periods included in this prospectus. In the opinion of management, our unaudited interim consolidated financial statements for the nine months ended September 30, 2003 and 2004 include all adjustments (consisting solely of normal recurring adjustments) necessary to present fairly the financial results for such periods. Interim results are not necessarily indicative of the results, which may be expected for any other interim period or for a full year. Our unaudited pro forma combined financial data presented below are derived from our unaudited pro forma combined financial statements included elsewhere in this prospectus. Our unaudited pro forma combined statements of operations included in this prospectus give effect to the reorganization described under "Summary — Reorganization" as if it had occurred on January 1, 2001, and our unaudited pro forma combined balance sheet included in this prospectus gives effect to this reorganization as if it had occurred on September 30, 2004. Our unaudited pro forma combined financial statements are based on our historical consolidated financial statements included in this prospectus and the historical financial statements of Videotron Telecom; Videotron Telecom's audited financial statements for the years ended December 31, 2002 and 2003 and unaudited interim financial statements as at and for the nine months ended September 30, 2003 and 2004 are included in this prospectus. Our unaudited pro forma combined financial statements purport neither to represent what our results of operations or financial position would have been had this reorganization in fact occurred on January 1, 2001 or September 30, 2004 nor to project our results of operations or financial position for any future period or date. The pro forma adjustments eliminate significant transactions and balances between us and Videotron Telecom. The information presented below the caption "Operating Data" is not derived from our consolidated financial statements. The information presented below the captions "Other Financial Data and Ratios" and "Other Financial Data and Ratio" is unaudited except for cash flows and capital expenditures for the years ended December 31, 2001, 2002 and 2003. All information contained in the following tables should be read in conjunction with, and is qualified in its entirety by reference to, all our consolidated financial statements and the related notes included in this prospectus and the section entitled "Management's Discussion and Analysis of Financial Condition and Results of Operations." Our financial statements and our unaudited pro forma combined financial information have been prepared in accordance with Canadian GAAP. For a discussion of the principal differences between Canadian GAAP and U.S. GAAP, see note 22 to our audited consolidated financial statements for the years ended December 31, 2001, 2002 and 2003, note 8 to our unaudited consolidated financial statements for the nine months ended September 30, 2003 and 2004 and note (b) to our unaudited pro forma combined financial information included in this prospectus.

10

| | | | | Pro Forma Combined(17) | | | Pro Forma Combined(17) | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | | | Nine Months Ended September 30, | ||||||||||||||||||||

| | Year Ended December 31, | |||||||||||||||||||||||

| | Year Ended December 31, 2003 | Nine Months Ended September 30, 2004 | ||||||||||||||||||||||

| | 2001 | 2002 | 2003 | 2003 | 2004 | |||||||||||||||||||

| | (restated)(1) | (restated)(1) | | | (restated)(1) | | | |||||||||||||||||

| | | | | (unaudited) | (unaudited) | (unaudited) | ||||||||||||||||||

| | (dollars in thousands, except for ARPU) | |||||||||||||||||||||||

| Statement of Operations Data: | ||||||||||||||||||||||||

| Operating revenues: | ||||||||||||||||||||||||

| Cable television | $ | 607,942 | $ | 579,200 | $ | 558,887 | $ | 558,887 | $ | 418,383 | $ | 428,542 | $ | 428,542 | ||||||||||

| Internet access | 99,629 | 135,514 | 183,268 | 183,268 | 133,033 | 162,603 | 162,603 | |||||||||||||||||

| Telecommunications | — | — | — | 55,663 | — | — | 46,765 | |||||||||||||||||

| Video stores | 35,155 | 35,344 | 38,450 | 38,450 | 28,267 | 32,590 | 32,590 | |||||||||||||||||

| Other(1) | 22,728 | 30,982 | 24,396 | 24,396 | 16,123 | 16,652 | 16,652 | |||||||||||||||||

| Total operating revenues | 765,454 | 781,040 | 805,001 | 860,664 | 595,806 | 640,387 | 687,152 | |||||||||||||||||

| Direct cost(1) | 227,322 | 259,686 | 245,967 | 244,715 | 182,847 | 182,651 | 185,569 | |||||||||||||||||

| Operating, general and administrative expenses(1) | 274,202 | 285,816 | 283,784 | 323,378 | 212,679 | 204,235 | 236,674 | |||||||||||||||||

| Depreciation and amortization(1) | 116,692 | 120,016 | 122,958 | 158,824 | 87,326 | 94,797 | 119,981 | |||||||||||||||||

| Financial expenses | 101,307 | 76,188 | 64,602 | 63,179 | 34,361 | 133,339 | 133,299 | |||||||||||||||||

| Dividend income from parent company | — | — | — | — | (85,626 | ) | (85,626 | ) | ||||||||||||||||

| Other items(2) | 95,570 | 25,000 | (2,500 | ) | (8 | ) | (2,500 | ) | — | 1,700 | ||||||||||||||

| Income taxes(1) | (10,076 | ) | 2,663 | 26,830 | 21,388 | 24,156 | 10,211 | 5,735 | ||||||||||||||||

| Non-controlling interest in a subsidiary | 145 | 188 | 49 | 49 | 46 | 79 | 79 | |||||||||||||||||

| Amortization of goodwill(3) | 13,331 | — | — | — | — | — | — | |||||||||||||||||

| Net income (loss)(1)(3) | $ | (53,039 | ) | $ | 11,483 | $ | 63,311 | $ | 49,139 | $ | 56,891 | $ | 100,701 | $ | 89,741 | |||||||||

| Balance Sheet Data (at period end): | ||||||||||||||||||||||||

| Cash and cash equivalents | $ | 80,935 | $ | 16,041 | $ | 28,329 | $ | 816 | $ | 25,747 | $ | 25,913 | ||||||||||||

| Total assets(1)(5) | 1,728,715 | 1,570,463 | 1,525,605 | 1,490,167 | 2,608,272 | 2,881,779 | ||||||||||||||||||

| Long-term debt, excluding QMI subordinated loans(4)(5) | 1,310,179 | 1,119,625 | 886,677 | 884,108 | 834,368 | 934,700 | (10) | |||||||||||||||||

| QMI subordinated loans(5) | — | — | 150,000 | 150,000 | 1,250,000 | 1,250,000 | ||||||||||||||||||

| Common shares(4) | 1 | 1 | 173,326 | 31,311 | 173,236 | 333,593 | ||||||||||||||||||

| Shareholder's equity(4) | (328,673 | ) | (345,189 | ) | 70,817 | 44,182 | 89,767 | 332,361 | ||||||||||||||||

Other Financial Data and Ratios: | ||||||||||||||||||||||||

| EBITDA(1)(6) | $ | 168,215 | $ | 210,350 | $ | 277,701 | $ | 292,530 | $ | 202,734 | $ | 339,048 | $ | 348,756 | ||||||||||

| EBITDA margin(1)(6) | 22.0 | % | 26.9 | % | 34.5 | % | 34.0 | % | 34.0 | % | 52.9 | % | 50.8 | % | ||||||||||

| Cash flows from operating activities | $ | 208,005 | $ | 195,934 | $ | 194,078 | $ | 64,858 | $ | 189,565 | ||||||||||||||

| Cash flows used in investing activities | (135,305 | ) | (91,878 | ) | (110,802 | ) | (53,922 | ) | (1,179,785 | ) | ||||||||||||||

| Cash flows from (used in) financing activities | 5,327 | (159,372 | ) | (72,094 | ) | (31,870 | ) | 977,620 | ||||||||||||||||

| Capital expenditures(7) | 133,319 | 93,041 | 90,284 | 55,398 | 96,434 | |||||||||||||||||||

| Cash interest expense(8) | 85,529 | 76,416 | 65,098 | 49,137 | 44,061 | |||||||||||||||||||

| Ratio of long-term debt, excluding QMI subordinated loans, to EBITDA(1)(4)(5)(6)(9) | 7.8x | 5.3x | 3.2x | 3.3x | 1.8x | 2.0x | (10) | |||||||||||||||||

| Ratio of EBITDA to cash interest expense(1)(6)(8) | 2.0x | 2.8x | 4.3x | 4.1x | 7.7x | |||||||||||||||||||

| Ratio of earnings to fixed charges(11) | 0.3x | 1.2x | 2.0x | 2.4x | 3.4x | |||||||||||||||||||

Operating Data (unaudited): | ||||||||||||||||||||||||

| Homes passed(12) | 2,330,648 | 2,329,023 | 2,351,344 | 2,344,149 | 2,374,668 | |||||||||||||||||||

| Basic customers(13) | 1,519,172 | 1,440,184 | 1,433,260 | 1,422,965 | 1,450,547 | |||||||||||||||||||

| Basic penetration(14) | 65.2 | % | 61.8 | % | 61.0 | % | 60.7 | % | 61.1 | % | ||||||||||||||

| Digital customers | 114,634 | 171,625 | 240,863 | 214,372 | 308,954 | |||||||||||||||||||

| Digital penetration(15) | 7.5 | % | 11.9 | % | 16.8 | % | 15.1 | % | 21.3 | % | ||||||||||||||

| High-speed Internet customers | 228,328 | 305,054 | 406,277 | 378,525 | 476,182 | |||||||||||||||||||

| High-speed Internet penetration(14) | 9.8 | % | 13.1 | % | 17.3 | % | 16.1 | % | 20.1 | % | ||||||||||||||

ARPU(16) | $ | 38.33 | $ | 40.45 | $ | 43.40 | $ | 43.01 | $ | 45.73 | ||||||||||||||

11

| | Year Ended December 31, | Nine Months Ended September 30, | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2002 | 2003 | 2003 | 2004 | |||||||||||

| | (restated)(1) | | (restated)(1) | | |||||||||||

| | | | (unaudited) | ||||||||||||

| | (dollars in thousands) | ||||||||||||||

| AMOUNTS UNDER U.S. GAAP | |||||||||||||||

| Statement of Operations Data: | |||||||||||||||

| Operating revenues: | |||||||||||||||

| Cable television | $ | 579,200 | $ | 558,887 | $ | 418,383 | $ | 434,650 | |||||||

| Internet access | 135,514 | 183,268 | 133,033 | 163,950 | |||||||||||

| Video stores | 35,344 | 38,450 | 28,267 | 32,590 | |||||||||||

| Other(1) | 30,982 | 24,396 | 16,123 | 16,652 | |||||||||||

| Total operating revenues | 781,040 | 805,001 | 595,806 | 647,842 | |||||||||||

| Direct cost(1) | 259,044 | 245,967 | 182,847 | 182,651 | |||||||||||

| Operating, general and administrative expenses(1) | 285,952 | 280,804 | 210,435 | 211,849 | |||||||||||

| Depreciation and amortization(1) | 137,687 | 133,003 | 95,231 | 104,013 | |||||||||||

| Financial expenses | 72,850 | 62,424 | 24,947 | 121,965 | |||||||||||

| Dividend income from parent company | — | — | — | (85,626 | ) | ||||||||||

| Other items(2) | 606 | — | — | — | |||||||||||

| Income taxes(1) | 5,166 | 24,079 | 21,862 | 6,717 | |||||||||||

| Non-controlling interest in a subsidiary | 188 | 49 | 46 | 79 | |||||||||||

| Impairment of goodwill(3) | 2,004,000 | — | — | — | |||||||||||

| Net income (loss)(1)(3) | $ | (1,984,453 | ) | $ | 58,675 | $ | 60,438 | $ | 106,194 | ||||||

Balance Sheet Data (at period end): | |||||||||||||||

| Cash and cash equivalents | $ | 16,041 | $ | 28,329 | $ | 816 | $ | 25,747 | |||||||

| Total assets(1) | 3,956,549 | 3,899,915 | 3,883,831 | 4,965,952 | |||||||||||

| Long-term debt, excluding QMI subordinated loans(4)(5) | 1,119,625 | 888,017 | 884,108 | 830,253 | |||||||||||

| QMI subordinated loans(5) | — | 150,000 | 150,000 | 1,250,000 | |||||||||||

| Common shares(4) | 1 | 173,236 | 31,311 | 173,236 | |||||||||||

| Shareholder's equity(4) | 1,963,438 | 2,373,352 | 2,356,355 | 2,395,255 | |||||||||||

Other Financial Data and Ratio: | |||||||||||||||

| EBITDA(1)(6) | $ | 235,250 | $ | 278,181 | $ | 202,478 | $ | 338,889 | |||||||

| EBITDA margin(1)(6) | 30.1 | % | 34.6 | % | 34.0 | % | 52.3 | % | |||||||

| Cash flows from operating activities | $ | 189,617 | $ | 193,878 | $ | 64,716 | $ | 189,406 | |||||||

| Cash flows used in investing activities | (85,561 | ) | (110,602 | ) | (53,780 | ) | (1,179,626 | ) | |||||||

| Cash flows from (used in) financing activities | (159,372 | ) | (72,094 | ) | (31,870 | ) | 977,620 | ||||||||

| Capital expenditures(7) | 92,414 | 90,284 | 55,398 | 96,434 | |||||||||||

| Ratio of earnings to fixed charges(11) | — | 1.9x | 2.8x | 4.2x | |||||||||||

12

this change in accounting policy were applied to the reported combined statements of operations for the prior periods, the impact of the change, in respect of goodwill and intangible assets with indefinite useful lives not being amortized, would be as follows:

| | Year Ended December 31, | |||

|---|---|---|---|---|

| | 2001 | |||

| | (restated) | |||

| | (dollars in thousands) | |||

| Net loss | $ | (53,039 | ) | |

| Goodwill amortization | 13,331 | |||

| Net loss before goodwill amortization | $ | (39,708 | ) | |

13

expensed and capitalized, plus amortized premiums, discounts and capitalized expenses relating to indebtedness and an estimate of the interest within rental expense. For the years ended December 31, 2000 and 2001, earnings as calculated under Canadian GAAP, were inadequate to cover our fixed charges, and the coverage deficiency was $66.8 million and $63.0 million, respectively. For the year ended December 31, 2002, earnings, as calculated under U.S. GAAP, were inadequate to cover our fixed charges, and the coverage deficiency was $1,978.5 million. For the ratios of earnings to fixed charges for the year ended August 31, 1999, the four months ended December 31, 1999 and the year ended December 31, 2000, see "Selected Consolidated Financial and Operating Data."

14

An investment in the new notes involves risks. You should consider carefully the risks described below as well as the other information appearing elsewhere in this prospectus before you decide to invest in the new notes.

Risks Relating to the Notes

If you do not properly tender your old notes, you will not receive new notes in the exchange offer, and you may not be able to sell your old notes.

We registered the new notes, but not the old notes, under the Securities Act. We will only issue new notes in exchange for old notes that are timely received by the exchange agent, together with all required documents, including a properly completed and duly signed letter of transmittal. Therefore, you should allow sufficient time to ensure timely delivery of the old notes, and you should carefully follow the instructions on how to tender your old notes.

Neither we nor the exchange agent is required to tell you of any defects or irregularities with respect to your tender of the old notes. If you do not tender your old notes or if we do not accept your old notes because you did not tender your old notes properly, then, after we consummate the exchange offer, you will continue to hold old notes that are subject to the existing transfer restrictions. In general, you may not offer or sell the old notes unless they are registered under the Securities Act or offered or sold in a transaction exempt from, or not subject to, the registration requirements of the Securities Act and applicable state securities laws.

Although we may in the future seek to acquire unexchanged old notes in open market or privately negotiated transactions, through subsequent exchange offers or otherwise, we have no present plans to acquire any unexchanged old notes or to file with the SEC a shelf registration statement to permit resales of any unexchanged old notes. In addition, holders who do not tender their old notes, except for initial purchasers or holders of old notes who are prohibited by applicable law or SEC policy from participating in the exchange offer or may not resell the new notes acquired in the exchange offer without delivering a prospectus and this prospectus is not appropriate or available for such resales by such holders, will not have any further registration rights and will not have the right to receive special interest on their old notes.

The market for the old notes may be significantly more limited after the exchange offer.

Because we anticipate that most holders of old notes will elect to exchange their old notes, we expect that the liquidity of the market for any old notes remaining after the completion of the exchange offer may be substantially limited. Any old notes tendered and exchanged in the exchange offer will reduce the aggregate principal amount of the old notes outstanding. Accordingly, the liquidity of the market for any old notes could be adversely affected and you may be unable to sell them. The extent of the market for the old notes and the availability of price quotations would depend on a number of factors, including the number of holders of old notes remaining outstanding and the interest of securities firms in maintaining a market in the old notes. An issue of securities with a smaller number of units available for trading may command a lower, and more volatile, price than would a comparable issue of securities with a larger number of units available for trading. Therefore, the market price for the old notes that are not exchanged may be lower and more volatile as a result of the reduction in the aggregate principal amount of the old notes outstanding.

Our substantial indebtedness and significant interest payment requirements could adversely affect our financial condition and prevent us from fulfilling our obligations under the notes.

We have a substantial amount of indebtedness, which could have significant consequences, including the following:

15

We will need a significant amount of cash to service our debt. Our ability to generate cash depends on many factors beyond our control.

Our ability to meet our debt service requirements, including those with respect to the notes, will depend on our ability to generate cash in the future. Our ability to generate cash depends on many factors beyond our control, such as competition and general economic conditions. In addition, our ability to borrow funds in the future to make payments on our debt will depend on our satisfaction of the covenants in our credit facilities and our other debt agreements, including the indenture governing the notes, and other agreements that we may enter into in the future. We cannot assure you that we will generate sufficient cash flow from operations or that future distributions will be available to us in amounts sufficient to pay our indebtedness, including the notes, or to fund our other liquidity needs. If we are unable to generate sufficient cash flow to meet our debt service requirements, we may have to renegotiate the terms of our debt or obtain additional financing. We cannot assure you that we will be able to refinance any of our debt, including our credit facilities or the notes, or obtain additional financing on commercially reasonable terms, if at all.

Restrictive covenants in our outstanding debt instruments may reduce our operating and financial flexibility, which may prevent us from capitalizing on business opportunities.

The terms of our credit facilities and the indenture governing the notes contain a number of operating and financial covenants restricting our ability to, among other things:

In addition, our ability to comply with covenants contained in the indenture, our credit facilities and the agreements governing other debt to which we are or may become a party may be affected by events beyond our control, including prevailing economic, financial and industry conditions. Our failure to comply with these covenants could result in an event of default which, if not cured or waived, could result in an acceleration of our debt and cross-defaults under our other debt. This could require us to repay or repurchase debt prior to the date it would otherwise be due, which could adversely affect our financial condition. Acceleration of any debt outstanding under our credit facilities or any of our other debt could prevent us from making interest and principal payments on the notes. Even if we are able to comply with all applicable covenants, the restrictions on our ability to manage our business in our sole discretion could adversely affect our business by, among other things, limiting our ability to take advantage of financings, mergers, acquisitions and other corporate opportunities that we believe would be beneficial to us.

16

Although these notes are referred to as "senior notes," they will be effectively subordinated to our and the guarantors' secured indebtedness.

Like the existing notes and the old notes, and each guarantee of the existing notes and the old notes, the new notes, and each guarantee of the new notes, will be unsecured and therefore are effectively subordinated to any secured indebtedness that we, or the relevant guarantor, may incur to the extent of the assets securing such indebtedness. In the event of a bankruptcy or similar proceeding involving us or a guarantor, the assets that serve as collateral for any secured indebtedness will be available to satisfy the obligations under the secured indebtedness before any payments are made on the notes. After giving effect to the completion of the offering of the old notes and the application of the net proceeds from this offering as described under "Use of Proceeds," as of September 30, 2004, we would have had $2,184.7 million of debt outstanding, $97.1 million of which would have been senior secured debt. The existing notes and the old notes are, and the new notes will be, effectively subordinated to any borrowings under our credit facilities. See "Description of Certain Indebtedness."

Not all of our subsidiaries guarantee our obligations under the notes, and the assets of our subsidiaries that do not guarantee the notes may not be available to make payments on the notes.

The guarantors of the notes do not include all of our subsidiaries. Payments on the notes are only required to be made by us and the guarantors. As a result, no payments are required to be made from assets of subsidiaries that do not guarantee the notes, unless those assets are transferred by dividend or otherwise to us or a guarantor. Initially, neither our wholly owned subsidiary CF Cable, nor its wholly owned subsidiary, Videotron Regional, will guarantee the notes until the termination of the indenture governing the CF Cable notes. Until CF Cable and Videotron Regional guarantee the notes, the notes will rank effectively behind the liabilities of CF Cable and Videotron Regional, including the CF Cable notes. This means that CF Cable and its subsidiaries must pay their creditors, including the holders of the CF Cable notes, in full before their assets are available to us to pay you. As of September 30, 2004, the aggregate amount of liabilities (including the CF Cable notes and trade payables but excluding inter-company liabilities) of CF Cable and its subsidiaries was $179.9 million.

In the event of a bankruptcy, liquidation or reorganization of any of the subsidiaries that do not guarantee the notes, holders of their liabilities, including their trade creditors, will be entitled to payment of their claims from the assets of those subsidiaries before any assets of these subsidiaries are made available for distribution on us. As a result, the existing notes and the old notes are, and the new notes will be, effectively subordinated to all debt and other liabilities of the subsidiaries that do not guarantee the notes. As of September 30, 2004, the total liabilities of those of our subsidiaries that do not guarantee the notes, excluding inter-company liabilities, were $180.3 million.

We may still be able to incur substantially more debt, which could increase the risks described above.

The terms of our credit facilities and the indenture governing the notes do not fully prohibit us or our subsidiaries from incurring additional debt. After giving effect to the completion of the offering of the old notes and the amendment of our credit facilities and the application of the net proceeds from this offering as described under "Use of Proceeds," as of September 30, 2004, we would have had $450 million available for additional borrowings under our credit facilities. We may be able to incur substantial additional debt in the future. If we do so, the risks described above could be greater.

We depend, to a certain extent, on our subsidiaries for cash needed to service our obligations under our indebtedness, including the notes.

For the year ended December 31, 2003, our subsidiaries generated approximately 49% of our revenues (before inter-company eliminations) and held approximately 48% of our consolidated total assets. We need the cash generated by our subsidiaries from their operations and their borrowings to service our obligations, including the notes. Our subsidiaries are not obligated to make funds available to us.

Our subsidiaries' ability to make payments to us will depend upon their operating results and will also be subject to applicable laws and contractual restrictions. For example, the terms of the indenture governing the CF Cable notes contain a number of operating and financial covenants that restrict CF Cable's ability to, among other things, pay dividends and make restricted payments to us. In addition, some of our subsidiaries may, in the future, become subject to loan agreements and indentures that restrict sales of assets and prohibit or significantly restrict

17

the payment of dividends or the making of distributions, loans or advances to shareholders and partners. The indenture governing the notes permits our subsidiaries to incur debt with similar prohibitions and restrictions.

We may not be able to finance a change of control offer required by the indenture because we may not have sufficient funds at the time of the change of control or our credit facilities may not allow the repurchases.

If we were to experience a change of control (as defined under the indenture governing our notes), we would be required to make an offer to purchase all of the notes then outstanding at 101.0% of the principal mount plus accrued and unpaid interest, if any, to the date of purchase. However, we may not have sufficient funds at the time of the change of control to make the required repurchase of the notes.

In addition, under our credit facilities, a change of control would be an event of default. Any future credit agreement or other agreements relating to our senior indebtedness to which we become a party may contain similar provisions. Our failure to purchase the notes upon a change of control under the indenture would constitute an event of default under the indenture. This default would in turn constitute an event of default under our credit facilities and may constitute an event of default under future senior indebtedness, any of which may cause the related debt to be accelerated after the expiry of any applicable notice or grace periods. If debt were to be accelerated, we may not have sufficient funds to repurchase the notes and repay the debt.

Canadian bankruptcy and insolvency laws may impair the trustee's ability to enforce remedies under the notes.

The rights of the trustee who represents the holders of the notes to enforce remedies could be delayed by the restructuring provisions of applicable Canadian federal bankruptcy, insolvency and other restructuring legislation if the benefit of such legislation is sought with respect to us. For example, both theBankruptcy and Insolvency Act (Canada) and theCompanies' Creditors Arrangement Act (Canada) contain provisions enabling an insolvent person to obtain a stay of proceedings against its creditors and to file a proposal to be voted on by the various classes of its affected creditors. A restructuring proposal, if accepted by the requisite majorities of each affected class of creditors, and if approved by the relevant Canadian court, would be binding on all creditors within each affected class, including those creditors that did not vote to accept the proposal. Moreover, this legislation, in certain instances, permits the insolvent debtor to retain possession and administration of its property, subject to court oversight, even though it may be in default under the applicable debt instrument, during the period that the stay against proceedings remains in place.

The powers of the court under theBankruptcy and Insolvency Act (Canada) and particularly under theCompanies' Creditors Arrangement Act (Canada) have been interpreted and exercised broadly so as to protect a restructuring entity from actions taken by creditors and other parties. Accordingly, we cannot predict whether payments under the notes would be made during any proceedings in bankruptcy, insolvency or other restructuring, whether or when the trustee could exercise its rights under the indenture governing the notes or whether and to what extent holders of the notes would be compensated for any delays in payment, if any, of principal, interest and costs, including the fees and disbursements of the trustee.

An active trading market for the new notes may not develop or be maintained.

The existing notes are not listed on a national securities exchange, and we do not intend to have the existing notes and the new notes listed on a national securities exchange. We have been informed by the initial purchasers that they currently intend to make a market in the new notes. However, they are under no obligation to do so, and, if they do make a market in the new notes, they may cease their market-making at any time without notice. Accordingly, we cannot assure you of the liquidity of the market for the new notes or the prices at which you may be able to sell the new notes.

In addition, the market for non-investment grade debt has historically been subject to disruptions that caused volatility in prices. It is possible that the market for the new notes will be subject to disruptions. Any such disruptions may have a negative effect on your ability to sell the new notes regardless of our prospects and financial performance.

18

Non-U.S. holders of the notes are subject to restrictions on the resale of notes.

We sold the old notes in reliance on exemptions from applicable Canadian provincial securities laws and the laws of other jurisdictions where the old notes were offered and sold, and therefore the old notes may be transferred and resold only in compliance with the laws of those jurisdictions to the extent applicable to the transaction, the transferor and/or the transferee. Although we registered the new notes under the Securities Act, we did not, and we do not intend to, qualify the new notes by prospectus in Canada, and, accordingly, the new notes will remain subject to restrictions on resale in Canada. In addition, non-U.S. holders will remain subject to restrictions imposed by the jurisdiction in which the holder is resident. See "The Exchange Offer — Resale of the New Notes" and "Notice to Canadian Investors."

Applicable statutes allow courts, under specific circumstances, to void the guarantees of the notes provided by certain of our subsidiaries.

Our creditors or the creditors of one or more guarantors of the notes could challenge the guarantees as fraudulent transfers, conveyances or preferences or on other grounds under applicable U.S. federal or state law or applicable Canadian federal or provincial law. While the relevant laws vary from one jurisdiction to another, the entering into of the guarantees by certain of our subsidiaries could be found to be a fraudulent transfer, conveyance or preference or otherwise void if a court were to determine that:

To the extent a court voids a guarantee as a fraudulent transfer, preference or conveyance or holds it unenforceable for any other reason, holders of notes would cease to have any direct claim against the guarantor that delivered a guarantee. If a court were to take this action, the guarantor's assets would be applied first to satisfy the guarantor's liabilities, including trade payables and preferred stock claims, if any, before any portion of its assets could be distributed to us to be applied to the payment of the notes. We cannot assure you that a guarantor's remaining assets would be sufficient to satisfy the claims of the holders of notes relating to any voided portions of the guarantees.

In addition, the corporate statutes governing the guarantors of the notes may also have provisions that serve to protect each guarantor's creditors from impairment of its capital from financial assistance given to its corporate insiders where there are reasonable grounds to believe that, as a consequence of this financial assistance, the guarantor would be insolvent or the book value, or in some cases the realizable value, of its assets would be less than the sum of its liabilities and its issued and paid-up share capital. While the applicable corporate laws may not prohibit financial assistance transactions and a corporation is generally permitted flexibility in its financial dealings, the applicable corporate laws may place restrictions on each guarantor's ability to give financial assistance in certain circumstances.

U.S. investors in the notes may have difficulties enforcing civil liabilities.

We are governed by the laws of the Province of Québec. Moreover, substantially all of our directors, controlling persons and officers are residents of Canada or other jurisdictions outside of the United States and a substantial portion of our assets and their assets are located outside of the United States. As a result, it may be difficult for holders of notes to effect service of process upon us or such persons within the United States or to enforce against us or them in the United States, judgments of courts of the United States predicated upon the civil liability provisions of the U.S. federal or state securities laws or other laws of the United States. In addition, there is doubt as to the enforceability in Canada of liabilities predicated solely upon U.S. federal or state securities law against us and our directors, controlling persons and officers who are not residents of the United States, in original actions or in actions for enforcement of judgments of U.S. courts.

19

Risks Relating to Our Business

We may not successfully implement our business and operating strategies.

Our business and operating strategies include maximizing customer satisfaction, launching and deploying additional value-added products and services, maintaining our advanced broadband network, reducing costs and improving operating efficiency, and further integrating our operations within the Quebecor Media group of companies. We may not be able to fully implement these strategies or realize their anticipated results. Implementation of these strategies could also be affected by a number of factors, some of which are beyond our control, such as operating difficulties, increased operating costs or capital expenditures, regulatory developments, general or local economic conditions or increased competition. Any material failure to implement our strategies could have a material adverse effect on our business, financial condition and operating results and on our ability to meet our obligations, including our ability to service our indebtedness.

We operate in highly competitive industries.

In our cable operations, we compete against direct broadcast satellite, or DBS, providers, multi-channel multipoint distribution systems, or MDS, satellite master antenna television systems and over-air television broadcasters. In addition, we will soon compete against incumbent local exchange carriers, which are in the process of securing licenses to launch video distribution services using video digital subscriber line, or VDSL, technology. We also face competition from illegal providers of cable television services and illegal access to foreign DBS and pirate systems that enable customers to access programming services from U.S. and Canadian DBS without paying any fee. In our Internet access business, we compete against other Internet service providers offering residential and commercial Internet access services. Recent decisions of the CRTC also require us to offer access to our high speed Internet system to competitive Internet service providers. Competitors in the video rental industry include other video stores, video-on-demand services, television and other alternative entertainment media. In addition, depending on the final regulatory framework set by the CRTC, our planned telephony service will have numerous competitors, including incumbent local exchange carriers, competitive local exchange carriers, wireless telephone service operators and other providers of Voice over IP telephony services, and possibly including competitors that are not facilities-based and therefore have a much lower infrastructure cost. We cannot assure you that our existing and future competitors will not pursue or be capable of achieving business strategies similar to or competitive with ours. Some of our competitors have greater financial and other resources than we do. We may not be able to compete successfully in the future against existing or potential competitors, and increased competition could have a material adverse effect on our business, financial condition or results of operations.

We compete, and will continue to compete, with alternative technologies, and we may be required to invest a significant amount of capital to address continued technological development.

The cable and Internet access industries are experiencing rapid and significant technological changes, which may result in alternative means of transmission and which could have a material adverse effect on our business, financial condition or results of operations. Further, industry regulators have authorized direct-to-home satellite (DTH), microwave services and video digital subscriber line (VDSL) services, and may authorize other alternative methods of transmitting television and other content with improved speed and quality. We may not be able to successfully compete with existing or newly developed alternative technologies or may be required to acquire, develop or integrate new technologies ourselves. The cost of the acquisition, development or implementation of new technologies could be significant and our ability to fund such implementation may be limited and could have a material adverse effect on our ability to successfully compete in the future.

We may not be able to obtain additional capital to continue the development of our business.

Our business has required substantial capital for the upgrade, expansion and maintenance of our network and the launch and expansion of new or additional services. If the demand for capacity increases, or if we decide to introduce new services, such as high definition television, or HDTV, or our new telephony service, which we intend to launch in Québec in the first half of 2005 and depending on the evolution of our product and service offerings, we may need to make unplanned additional capital expenditures. We may not be able to obtain the funds necessary to finance our capital improvement program or any additional capital requirements through internally generated

20

funds, additional borrowings or other sources. If we are unable to obtain these funds, we would not be able to implement our business strategy and our results of operations would be adversely affected.

Our financial performance will be materially adversely affected if we cannot continue to distribute a wide range of television programming on reasonable terms.