Exhibit 99.2

Management’s Discussion and Analysis Third Quarter Ended September 30, 2022 (Expressed in United States dollars, except per share amounts and where otherwise noted) |

November 8, 2022

This Management’s Discussion and Analysis ("MD&A") should be read in conjunction with the condensed consolidated interim financial statements for the period ended September 30, 2022 and related notes thereto which have been prepared in accordance with IFRS 34, Interim Financial Reporting of the International Financial Reporting Standards ("IFRS") as issued by the International Accounting Standards Board, as well as the annual audited consolidated financial statements for the year ended December 31, 2021, which are in accordance with IFRS, and the related MD&A. References to "Entrée" and the "Company" are to Entrée Resources Ltd. and/or one or more of its wholly-owned subsidiaries. For further information on the Company, reference should be made to its continuous disclosure (including its most recently filed annual information form ("AIF")), which is available on SEDAR at www.sedar.com. Information is also available on the Company’s website at www.EntreeResourcesLtd.com. Information on risks associated with investing in the Company’s securities is contained in the Company’s most recently filed AIF. Technical and scientific information under National Instrument 43-101 - Standards of Disclosure for Mineral Projects ("NI 43-101") concerning the Company’s material property, including information about mineral resources and reserves, is contained in the Company’s most recently filed AIF and in its technical report titled "Entrée/Oyu Tolgoi Joint Venture Project, Mongolia, NI 43-101 Technical Report" with an effective date of October 8, 2021 prepared by Wood Canada Limited ("Wood").

Q3 2022 HIGHLIGHTS

Oyu Tolgoi Underground Development Update

The Oyu Tolgoi project in Mongolia includes two separate land holdings: the Oyu Tolgoi mining licence, which is held by Entrée’s joint venture partner Oyu Tolgoi LLC ("OTLLC") and the Entrée/Oyu Tolgoi JV Property, which is a partnership between Entrée and OTLLC (see "Overview of Business" below). On October 17, 2022, OTLLC’s 66% shareholder Turquoise Hill Resources Ltd. ("Turquoise Hill") provided an update on Oyu Tolgoi underground development:

| • | Safety continues to be OTLLC’s top priority and COVID-19 controls remain in place at site to protect OTLLC’s work force. COVID-19 cases identified at Oyu Tolgoi continued at low levels in the third quarter 2022 and the testing regime has been eased. Following the recent relaxation of COVID-19 government-initiated restrictions in Mongolia, OTLLC has progressively restarted work on project facilities with workforce numbers now at full capacity. |

| • | Construction of the final major stage of materials handling infrastructure continues, including civil and underground works for the conveyor to surface. Undercut blasting and on-footprint construction work continued to progress during the third quarter 2022. Commissioning of the second truck chute has commenced, and the 8th draw bell was fired on October 13, 2022, both ahead of schedule. Sustainable production from Panel 0 on the Oyu Tolgoi mining licence is now anticipated in the first quarter 2023. |

| • | The Shaft 3 headframe was commissioned and sinking commenced on March 31, 2022, with the cumulative sinking level at 298 metres below ground level as at October 2, 2022. Shaft 4 advancement was 418 metres below ground level as at October 2, 2022. The rate of progress in shafts improved during the quarter due to the optimization work program to maximize the productivity of their development. Continued progress on the program is necessary to remain aligned with the 2022 cost and schedule update, which identified an approximate 15-month delay in the commissioning of Shafts 3 and 4 from the schedule in the Definitive Estimate. As previously disclosed, Turquoise Hill now expects Shafts 3 and 4 to be commissioned in the first half 2024, and progress continues to be closely monitored. Shafts 3 and 4 are required to provide ventilation to support production from Panels 1 and 2 during ramp up to 95,000 tonnes per day ("tpd"). Turquoise Hill currently expects the first Panel 1 draw bell in the first half 2027. The Hugo North Extension deposit on the Entrée/Oyu Tolgoi JV Property is located in the northern portion of Panel 1. |

| • | Design optimization work for Lift 1 on the Oyu Tolgoi mining licence and the Entrée/Oyu Tolgoi JV Property continues with the aim of minimizing risk and maximizing productivity. The Lift 1 Panel 1 design optimization study remains on track for completion in the first half 2023. |

Q3 2022 MD&A (table amounts expressed in thousands of US Dollars, except per share amounts and where otherwise noted)

| • | On September 5, 2022, Turquoise Hill announced it has entered into an arrangement agreement with Rio Tinto plc and Rio Tinto International Holdings Limited ("Rio Tinto") pursuant to which Rio Tinto will acquire the approximately 49% of the issued and outstanding shares of Turquoise Hill that Rio Tinto does not currently own for C$43.00 in cash per share, subject to approval by Turquoise Hill minority shareholders and other customary closing conditions. The special meeting of Turquoise Hill shareholders to consider and approve the statutory plan of arrangement is currently scheduled for November 15, 2022. Rio Tinto’s stated purpose for the acquisition is to strengthen its copper portfolio and create a more efficient ownership and governance structure for the Oyu Tolgoi project. If the transaction is successfully completed, Rio Tinto will have a 66% interest in deposits on the Oyu Tolgoi mining licence and a 52.8% interest in the Hugo North Extension and Heruga deposits on the Entrée/Oyu Tolgoi JV Property. |

Entrée/Oyu Tolgoi JV Property Update

| • | For Panel 1 drilling on the Entrée/Oyu Tolgoi JV Property, the Entrée/Oyu Tolgoi joint venture (the "Entrée/Oyu Tolgoi JV") has approved a 2022 budget with diamond drill holes targeting Hugo North Extension Lifts 1 and 2. The holes are collared from underground drill stations along the eastern boundary of the porphyry mineralized footprint on the Oyu Tolgoi mining licence crossing onto the Entrée/Oyu Tolgoi JV Property. As at the end of October 2022, 14 underground holes have been drilled on the Entrée/Oyu Tolgoi JV Property totalling 6,083.3 metres. In addition, two surface diamond drill holes totalling ~3,550 metres are in progress, with hole EGD173 currently at a depth of 1,698 meters (planned depth 1,800 metres) and hole EGD161 currently at a depth of 364 metres (planned depth 1,750 metres). The two surface holes will be entirely on the Entrée/Oyu Tolgoi JV Property and will target the northern portion of the Hugo North Extension deposit. The Lift 1 Panel 1 geological model is expected to be finalized in the first quarter 2023, following which a decision will be made as to whether more Lift 1 drilling will be required. The Company has received preliminary results from a portion of the underground holes and is in the process of collating and modelling the data. |

| • | With the relaxation of COVID-19 related restrictions in Mongolia, exploration drilling programs resumed in 2022. On the Shivee Tolgoi mining licence, six reverse circulation ("RC") holes totalling 1,500 metres and one 800 metre diamond drill hole have been completed at the Ulaan Khud target. In addition, three diamond drill holes totalling 2,200 metres have been completed at the Airstrip target. Analytical results are pending. On the Javhlant mining licence, five RC holes totalling 1,500 metres were planned for each of the Bumbat Ulaan and West Mag targets in 2022. Two RC holes totalling 600 metres were completed at the West Mag target; the remaining three holes were cancelled following engagement with one of the local herders. The five RC holes planned for the Bumbat Ulaan target were not completed due to the recent commissioning of the Tavan Tolgoi-Gashuunsukhait railway. |

| • | The Company continues to monitor the situation in Mongolia including with respect to possible delays to commencement of Panel 1. The Company will assess the potential impact of any delays as it becomes aware of them and will update the market accordingly. |

| • | On May 26, 2022, the Company announced it has commenced binding arbitration proceedings to seek declarations and orders for specific performance relating to certain provisions of the Equity Participation and Earn-in Agreement (the "Earn-in Agreement") with Turquoise Hill dated October 15, 2004, as amended and subsequently assigned to OTLLC and the Joint Venture Agreement appended to the Earn-in Agreement (the "Entrée/Oyu Tolgoi JVA"). The parties have been operating under the terms of the Entrée/Oyu Tolgoi JVA since OTLLC completed its earn-in obligations on the Entrée/Oyu Tolgoi JV Property in 2008. The Company will provide updates on the arbitration as developments warrant. |

Corporate

| • | Operating loss was $0.5 million and $1.8 million for the three and nine month periods of 2022, respectively, compared to $0.5 million and $1.6 million in the comparative periods of 2021. |

| • | Operating cash outflow before changes in non-cash working capital items was $0.5 million and $1.7 million for the three and nine month periods of 2022, respectively, compared to $0.5 million and $1.5 million in the comparative periods of 2021. |

| • | As at September 30, 2022, the cash balance was $7.1 million and the working capital balance was $7.1 million. |

Page 2

Q3 2022 MD&A (table amounts expressed in thousands of US Dollars, except per share amounts and where otherwise noted)

OVERVIEW OF BUSINESS

Entrée is a mineral resource company with interests in development and exploration properties in Mongolia, Peru and Australia.

The Company’s principal asset is its interest in the Entrée/Oyu Tolgoi joint venture property (the "Entrée/Oyu Tolgoi JV Property") - a carried 20% participating interest in two of the Oyu Tolgoi project deposits, and a carried 20% or 30% interest (depending on the depth of mineralization) in the surrounding large, underexplored, highly prospective land package located in the South Gobi region of Mongolia. Entrée’s joint venture partner, OTLLC, holds the remaining interest.

The Oyu Tolgoi project includes two separate land holdings: the Oyu Tolgoi mining licence, which is held by OTLLC (66% Turquoise Hill and 34% the Government of Mongolia), and the Entrée/Oyu Tolgoi JV Property, which is a partnership between Entrée and OTLLC. The Entrée/Oyu Tolgoi JV Property comprises the eastern portion of the Shivee Tolgoi mining licence, and all of the Javhlant mining licence, which mostly surround the Oyu Tolgoi mining licence (see Figure 1 below). Both the Shivee Tolgoi and Javhlant mining licences are held by Entrée. The terms of the Entrée/Oyu Tolgoi JV state that Entrée has a 20% participating interest with respect to mineralization extracted from deeper than 560 metres below surface and a 30% participating interest with respect to mineralization extracted from above 560 metres depth.

The Entrée/Oyu Tolgoi JV Property includes the Hugo North Extension copper-gold deposit (also referred to as "HNE") and the majority of the Heruga copper-gold-molybdenum deposit. The resources at Hugo North Extension include a Probable reserve, which is part of the first lift ("Lift 1") of the Oyu Tolgoi underground block cave mining operation. Lift 1 is in development by project operator Rio Tinto. When the Lift 1 underground reaches peak production, Oyu Tolgoi is expected to be the fourth largest copper mine in the world.

In addition to the Hugo North Extension copper-gold deposit, the Entrée/Oyu Tolgoi JV Property includes approximately 93% of the mineral resource tonnes outlined at the Heruga copper-gold-molybdenum deposit and a large exploration land package, which together form a significant component of the overall Oyu Tolgoi project.

The Company’s corporate headquarters are located in Vancouver, British Columbia, Canada. Field operations are conducted out of local offices in Mongolia.

As at September 30, 2022 and the date of this MD&A, Rio Tinto beneficially owns 31,981,129 common shares (including 14,539,333 common shares held by Turquoise Hill), or 16.2% of the outstanding shares of the Company. As at September 30, 2022 and the date of this MD&A, Horizon Copper Corp. (formerly Royalty North Partners Ltd. ("Horizon")) indirectly owns 49,672,515 common shares, or 25.1% of the outstanding shares of the Company.

On February 17, 2022, Sandstorm Gold Ltd. ("Sandstorm") announced it had signed a letter of intent with Horizon whereby Horizon will acquire certain non-royalty and non-stream assets from Sandstorm, including Sandstorm’s shares of the Company. The transaction is structured as a reverse take-over of Horizon. The first part of the transaction closed on August 31, 2022. Subject to the completion of a proposed concurrent financing of a minimum of US$20 million payable to Sandstorm, the second part of the transaction is expected to close in the second half 2022. Upon completion of the transaction, Horizon will continue to be listed on the TSX Venture Exchange as a Tier 1 Mining Issuer under the anticipated trading symbol "HCU". Sandstorm will retain an approximately 34% equity interest in Horizon.

On June 1, 2022, Horizon announced that pursuant to a share purchase agreement, Horizon’s wholly owned subsidiary 1363013 B.C. Ltd. had acquired Sandstorm’s shares of the Company in consideration for a promissory note in the principal amount of C$43.2 million. Horizon subsequently acquired the promissory note from Sandstorm and Horizon’s liabilities associated with the promissory note were eliminated.

On September 5, 2022, Turquoise Hill announced it has entered into an arrangement agreement with Rio Tinto pursuant to which Rio Tinto will acquire the approximately 49% of the issued and outstanding shares of Turquoise Hill that Rio Tinto does not currently own for C$43.00 in cash per share, subject to approval by Turquoise Hill minority shareholders and other customary closing conditions. The special meeting of Turquoise Hill shareholders to consider and approve the statutory plan of arrangement is currently scheduled for November 15, 2022. Rio Tinto’s stated purpose for the acquisition is to strengthen its copper portfolio and create a more efficient ownership and governance structure for the Oyu Tolgoi project. If the transaction is successfully completed, Rio Tinto will have a 66% interest in deposits on the Oyu Tolgoi mining licence and a 52.8% interest in the Hugo North Extension and Heruga deposits on the Entrée/Oyu Tolgoi JV Property.

Effective October 1, 2019, the Company voluntarily withdrew its common shares from listing on NYSE American and its common shares commenced trading on the OTCQB under the trading symbol "ERLFF". On April 24, 2006, the Company’s common shares began trading on the Toronto Stock Exchange ("TSX") and discontinued trading on the TSX Venture Exchange. The trading symbol remained "ETG".

Page 3

Q3 2022 MD&A (table amounts expressed in thousands of US Dollars, except per share amounts and where otherwise noted)

OUTLOOK AND STRATEGY

Entrée’s primary objective for the 2022 year is to confirm the transfer of the Shivee Tolgoi and Javhlant mining licences to OTLLC as manager of the Entrée/Oyu Tolgoi JV either in conjunction with finalization and execution of amendments to the Entrée/Oyu Tolgoi JVA, or enforcement of certain provisions of the Earn-in Agreement and Entrée/Oyu Tolgoi JVA pursuant to binding arbitration proceedings. The Company is also advancing discussions with Erdenes Oyu Tolgoi LLC regarding a potential acquisition by the Government of Mongolia of 34% of the Company’s economic interest in the Entrée/Oyu Tolgoi JV Property in connection with the transfer of the licences. The Company currently is registered in Mongolia as the 100% ultimate holder of the Shivee Tolgoi and Javhlant mining licences.

As previously disclosed by the Company, the contract area defined in the 2009 Oyu Tolgoi Investment Agreement among the Government of Mongolia, OTLLC, Rio Tinto and Turquoise Hill (the "Oyu Tolgoi Investment Agreement") includes the Javhlant and Shivee Tolgoi mining licences. However, at the time of negotiation of the Oyu Tolgoi Investment Agreement, the Company was not made a party to the Oyu Tolgoi Investment Agreement, and as such does not have any direct rights or benefits under the Oyu Tolgoi Investment Agreement.

Entrée has been engaged in discussions with stakeholders of the Oyu Tolgoi project, including the Government of Mongolia, OTLLC, Erdenes Oyu Tolgoi LLC, Turquoise Hill and Rio Tinto, since February 2013. The discussions to date have focused on issues arising from Entrée’s exclusion from the Oyu Tolgoi Investment Agreement, including the fact that the Government of Mongolia does not have a full 34% interest in the Entrée/Oyu Tolgoi JV Property; the fact that the mining licences integral to future underground operations are held by more than one corporate entity; and the fact that Entrée does not benefit from the stability that it would otherwise have if it were a party to the Oyu Tolgoi Investment Agreement. In order to receive the benefits of the Oyu Tolgoi Investment Agreement, the Government of Mongolia may require the Company to agree to certain concessions, including with respect to Entrée’s economic interest in the Entrée/Oyu Tolgoi JV Property.

The Company believes that amending the Entrée/Oyu Tolgoi JVA to align the interests of all stakeholders as they are now understood, transferring the licences to OTLLC as manager of the Entrée/Oyu Tolgoi JV, and resolving outstanding issues arising from Entrée’s exclusion from the Oyu Tolgoi Investment Agreement would be in the best interests of all stakeholders, provided there is no material net erosion of value to Entrée. No agreements have been finalized and there are no assurances agreements may be finalized in the future.

ENTRÉE/OYU TOLGOI JV PROPERTY AND SHIVEE WEST PROPERTY - MONGOLIA

2021 Technical Report Highlights

On October 21, 2021, the Company filed an amended Technical Report ("2021 Technical Report") for its interest in the Entrée/Oyu Tolgoi JV Property. The 2021 Technical Report has an original effective date of May 17, 2021, and an amended effective date of October 8, 2021.

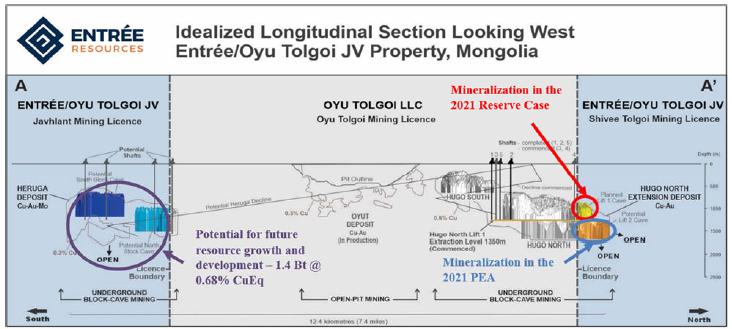

The 2021 Technical Report discusses a reserve case (the "2021 Reserve Case") based on mineral reserves attributable to the Entrée/Oyu Tolgoi JV Lift 1 of the Hugo North Extension deposit.

The 2021 Technical Report also discusses a Preliminary Economic Assessment on a conceptual second lift ("Lift 2") of the Hugo North Extension deposit (the "2021 PEA"). The 2021 PEA is based on Indicated and Inferred mineral resources from Lift 2, as the second potential phase of development and mining on the Hugo North Extension deposit. Lift 2 is directly below Lift 1 and continues further to the north (see Figure 2 below). There is no overlap in the mineral reserves from the 2021 Reserve Case and the mineral resources from the 2021 PEA. Development and capital decisions will be required for the eventual development of Lift 2 once production commences at Hugo North Extension Lift 1.

Both the 2021 Reserve Case and the 2021 PEA are based on information supplied by OTLLC or reported within its 2020 Oyu Tolgoi Mongolian Statutory Study ("OTMSS20"). OTMSS20 was completed by OTLLC in July 2020 and discusses the mine plan for Lift 1 of the Hugo North/Hugo North Extension underground block cave on the Oyu Tolgoi mining licence and the Entrée/Oyu Tolgoi JV Property. The Lift 1 mine plan incorporates the development of three panels, and in order to reach the full sustainable production rate of 95,000 tpd from the underground operations all three panels need to be in production. The Hugo North Extension deposit on the Entrée/Oyu Tolgoi JV Property is located at the northern portion of Panel 1.

Page 4

Q3 2022 MD&A (table amounts expressed in thousands of US Dollars, except per share amounts and where otherwise noted)

Life-of-mine ("LOM") highlights of the production and financial results from the 2021 Reserve Case and the 2021 PEA are summarized as follows:

| Entrée/Oyu Tolgoi JV Property | Units | 2021 Reserve Case (Lift 1) | 2021 PEA (Lift 2) |

| Attributable Financial Results | |||

| Cash Flow, pre-tax | US$M | 449 | 1,982 |

| NPV(5%), after-tax | US$M | 185 | 541 |

| NPV(8%), after-tax | US$M | 131 | 306 |

| NPV(10%), after-tax | US$M | 104 | 213 |

| LOM Recovered Metal | |||

| Copper Recovered | Mlb | 1,249 | 4,564 |

| Gold Recovered | koz | 549 | 2,025 |

| Silver Recovered | koz | 3,836 | 15,067 |

| LOM Processed Material | |||

| Probable Reserve Feed | 40 Mt @ 1.54% Cu, 0.53 g/t Au, 3.63 g/t Ag | - - | |

| Indicated Resource Feed | - - | 77.9 Mt @ 1.35% Cu, 0.49 g/t Au, 3.6 g/t Ag (1.64% CuEq) | |

| Inferred Resource Feed | - - | 87.8 Mt @ 1.35% Cu, 0.49 g/t Au, 3.6 g/t Ag (1.64% CuEq) |

Notes:

| 1. | Long term metal prices used in the NPV economic analyses for the 2021 Reserve Case and the 2021 PEA are: copper $3.25/lb, gold $1,591.00/oz, silver $21.08/oz. |

| 2. | Mineral reserves in the 2021 Reserve Case, and mineral resources in the 2021 PEA mine plan are reported on a 100% basis. |

| 3. | Entrée has a 20% interest in the above processed material and recovered metal. |

| 4. | The Mineral reserves that form the basis of the 2021 Reserve Case are from a separate portion of the Hugo North Extension deposit than the mineral resources in the 2021 PEA. |

| 5. | Copper equivalent ("CuEq") is calculated as shown in the notes to the Entrée/Oyu Tolgoi JV Property Mineral Resources table below. |

| 6. | 2021 Reserve Case cash flows are discounted to the beginning of 2021. |

| 7. | 2021 PEA cash flows are discounted to the beginning of 2027, the assumed beginning of Hugo North Lift 2 development. Attributable Entrée/Oyu Tolgoi JV production is assumed to begin in 2031 and ramps up to stable production in 2043. Final Entrée/Oyu Tolgoi JV attributable production is assumed to conclude in 2056. |

| 8. | The 2021 Reserve Case and 2021 PEA are exclusive of each other. |

| 9. | Indicated and Inferred resource average expected run-of-mine feed grade of 1.35% copper, 0.49 g/t gold, and 3.6 g/t silver (1.64% CuEq) includes dilution and mine losses. |

The economic analysis in the 2021 PEA is based on a conceptual mine plan and does not have as high a level of certainty as the 2021 Reserve Case. The 2021 PEA is preliminary in nature and includes Inferred mineral resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves, and there is no certainty that the 2021 PEA will be realized. Mineral resources are not mineral reserves and do not have demonstrated economic viability.

In both the 2021 Reserve Case and the 2021 PEA, Entrée is only reporting the production and cash flows attributable to the Entrée/Oyu Tolgoi JV Property, not production and cash flows for other Oyu Tolgoi project areas owned 100% by OTLLC. The production and cash flows from the 2021 Reserve Case and the 2021 PEA are from separate parts of the Hugo North Extension deposit and there is no overlap of the mineralization.

Page 5

Q3 2022 MD&A (table amounts expressed in thousands of US Dollars, except per share amounts and where otherwise noted)

Below are some of the key financial assumptions and outputs from the 2021 Reserve Case and the 2021 PEA. All figures shown for both cases are reported on a 100% Entrée/Oyu Tolgoi JV basis, unless otherwise noted. Both cases assume long term metal prices of $3.25/lb copper, $1,591.00/oz gold and $21.08/oz silver.

Key items per the 2021 Reserve Case outputs are as follows:

| • | Assumes Entrée/Oyu Tolgoi JV Property development production from Hugo North Extension Lift 1 will start in H2 2022 with the first draw bell in 2026, peak production in 2034, and final production in 2038. |

| • | 17-year Lift 1 LOM production (includes 4-years development production followed by 13-years block cave production). |

| • | Maximum production rate of approximately 25,000 tpd, which is blended with production from OTLLC’s Oyut open pit deposit and Hugo North deposit to supply a maximum mill throughput rate of 125,000 tpd. |

| • | Total recovered metal over the LOM of Hugo North Extension Lift 1: 1,249,000 lbs copper, 549,000 oz gold, 3,836,000 oz silver. |

| • | Total direct development and sustaining capital expenditures of approximately $275.7 million ($55.1 million attributable to Entrée). |

| • | Entrée LOM average cash cost before credits $1.57/lb payable copper. |

| • | Entrée LOM average cash costs after credits ("C1")* $0.79/lb payable copper. |

| • | Entrée LOM average all-in sustaining costs ("AISC")* $1.26/lb payable copper. |

Key items per the 2021 PEA outputs are as follows:

| • | Assumes Entrée/Oyu Tolgoi JV Property development production from Hugo North Extension Lift 2 to start in approximately 2034 with the first draw bell in 2038, peak production in 2047 and final production in 2055. |

| • | 22-year Lift 2 mine life (4-years development production and 18-years block cave production). |

| • | Maximum production rate of approximately 40,500 tpd, which is blended with production from OTLLC’s Oyut open pit deposit and Hugo North deposit to supply a maximum mill throughput rate of 125,000 tpd. |

| • | Total metal production over the LOM of Hugo North Extension Lift 2: 4,564,000 lbs copper, 2,025,000 oz gold, 15,067,000 oz silver. |

| • | Total direct development and sustaining capital expenditures of approximately $1,589.6 million ($319.7 million attributable to Entrée). |

| • | Entrée LOM average cash cost before credits $1.10/lb payable copper. |

| • | Entrée LOM average C1* $0.30/lb payable copper. |

| • | Entrée LOM average AISC* $0.92/lb payable copper. |

*"Cash costs after credits" (C1) and all-in sustaining cost (ASIC) are non-IFRS performance measurements. See "Non-IFRS Performance Measurements" below for further information.

The 2021 Reserve Case and the 2021 PEA are mutually exclusive. If the 2021 Reserve Case is developed and brought into production, the mineralization from Hugo North Extension Lift 2 is not sterilized or reduced in tonnage or grades. In addition, the Heruga deposit, which is not included in either the 2021 Reserve Case or the 2021 PEA, provides a great deal of future potential and with further exploration and development could become a completely standalone underground operation, independent of other Oyu Tolgoi project underground development, and provide considerable flexibility for mine planning and development.

On December 18, 2020, Turquoise Hill announced that a definitive estimate of project cost and schedule (the "Definitive Estimate") that refines the analysis in OTMSS20 and broadly confirms the economics and assumptions presented therein had been completed and delivered to OTLLC by Rio Tinto. The Company has not received a copy of the Definitive Estimate and it was not reviewed or relied upon in the preparation of the 2021 Reserve Case or the 2021 PEA. On August 4, 2022, Turquoise Hill reported it had completed its review of a 2022 cost and schedule update for the underground project, resulting in an increase in the total expected underground development capital of the Definitive Estimate from $6.75 billion to $7.06 billion. The $7.06 billion incorporates known and future incremental COVID-19 costs of $227 million, escalation of $72 million, associated taxes, and minor impacts of changes in labor laws. The 2022 cost and schedule update assumes there are no new COVID-19 related impacts beyond the end of the second quarter 2022.

Page 6

Q3 2022 MD&A (table amounts expressed in thousands of US Dollars, except per share amounts and where otherwise noted)

Neither OTMSS20 nor the results of the 2021 Reserve Case and 2021 PEA reflect the impacts of the COVID-19 pandemic or other known delays. In particular, the first Lift 1 Panel 1 draw bell is currently expected in H1 2027 rather than H2 2026 due to later than planned commencement of the Panel 0 undercut on the Oyu Tolgoi mining licence, lateral development scope changes, impacts of COVID-19 on development progression and delays to the forecast completion dates for Shafts 3 and 4. The 2022 cost and schedule update identified an approximate 15-month delay in the commissioning of Shafts 3 and 4 from the schedule in the Definitive Estimate. OTLLC currently expects Shafts 3 and 4 to be commissioned in the first half 2024 and it continues to closely monitor progress against the 2022 schedule update. Shafts 3 and 4 are required to provide ventilation to support production from Panels 1 and 2 during ramp up to 95,000 tpd.

The Company continues to monitor the situation in Mongolia including with respect to possible delays to commencement of Panel 1. The Company will assess the potential impact of any delays as it becomes aware of them and will update the market accordingly.

The 2021 Technical Report has been filed on SEDAR and is available for review under the Company’s profile on SEDAR (www.sedar.com) or on www.EntreeResourcesLtd.com.

Summary and Location of Project

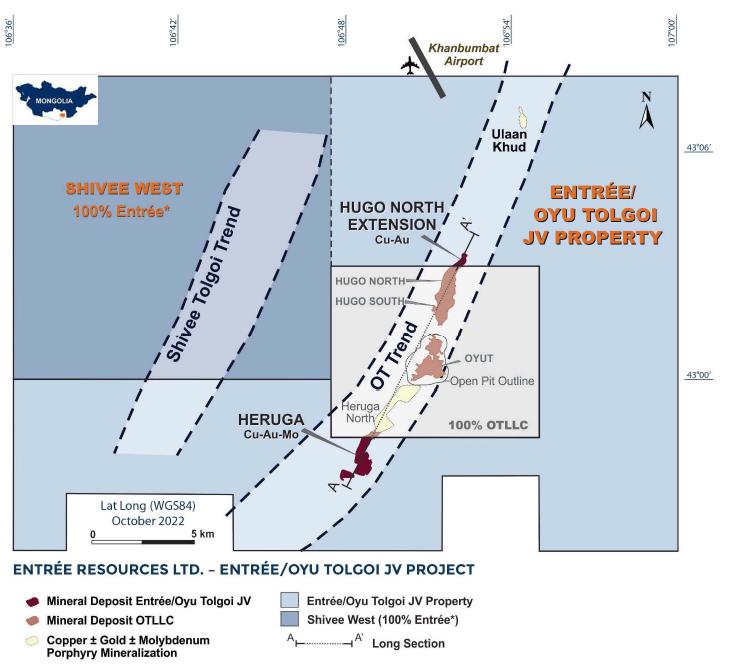

The "Entrée/Oyu Tolgoi JV Project" (shown on Figure 1 below) comprises the Entrée/Oyu Tolgoi JV Property and the Shivee West Property (see "Shivee West Property Summary" below). The Entrée/Oyu Tolgoi JV Project completely surrounds OTLLC’s Oyu Tolgoi mining licence and forms a significant portion of the overall Oyu Tolgoi project area. Figure 1 also shows the main mineral deposits that form the Oyu Tolgoi trend of porphyry deposits.

The Entrée/Oyu Tolgoi JV Project is located within the Aimag (province) of Ömnögovi in the South Gobi region of Mongolia, about 570 kilometres ("km") south of the capital city of Ulaanbaatar and 80 km north of the border with China.

The Entrée/Oyu Tolgoi JV Property comprises the eastern portion of the Shivee Tolgoi mining licence and all of the Javhlant mining licence, and hosts:

| • | The Hugo North Extension copper-gold porphyry deposit (Lift 1 and Lift 2): |

| - | Lift 1 is the upper portion of the Hugo North Extension copper-gold porphyry deposit and forms the basis of the 2021 Reserve Case. It is the northern portion of the Hugo North Lift 1 underground block cave mine plan that is currently in development on the Oyu Tolgoi mining licence. The 2021 Reserve Case assumes initial development production will start on the Entrée/Oyu Tolgoi JV Property in H2 2022. Hugo North Extension Lift 1 Probable reserves include 40 million tonnes ("Mt") grading 1.54% copper, 0.53 grams per tonne ("g/t") gold, and 3.63 g/t silver. |

| - | Lift 2 is directly below and extends north beyond Lift 1 and is the next potential phase of underground mining on the Entrée/Oyu Tolgoi JV Property, once Lift 1 mining is complete. Mineral resources from Lift 2 form the basis of the 2021 PEA mine plan, which include 78 Mt (Indicated) and 88 Mt (Inferred). The average expected run-of-mine feed grade of 1.35% copper, 0.49 g/t gold, and 3.6 g/t silver (1.64% CuEq; see the notes to the Entrée/Oyu Tolgoi JV Property Mineral Resources table below) includes dilution and mine loss. |

| • | The Heruga copper-gold-molybdenum porphyry deposit is at the south end of the Oyu Tolgoi trend of porphyry deposits. Approximately 93% of the Heruga deposit occurs on the Entrée/Oyu Tolgoi JV Property where Inferred mineral resources include: 1,400 Mt grading 0.41% copper, 0.40 g/t gold, 1.5 g/t silver and 120 parts per million ("ppm") molybdenum (0.68% CuEq; see the notes to the Entrée/Oyu Tolgoi JV Property Mineral Resources table below). While Heruga is not included in the 2021 PEA, it provides opportunity for future exploration and potential development. |

| • | A large prospective land package. |

Page 7

Q3 2022 MD&A (table amounts expressed in thousands of US Dollars, except per share amounts and where otherwise noted)

Entrée has a 20% or 30% (depending on the depth of mineralization) participating interest in the Entrée/Oyu Tolgoi JV with OTLLC holding the remaining 80% (or 70%) interest. OTLLC has a 100% interest in other Oyu Tolgoi project areas, including the Oyut open pit, which is currently in production, and the Hugo North and Hugo South deposits on the Oyu Tolgoi mining licence.

Figure 1 - Entrée/Oyu Tolgoi JV Project

Notes:

| 1. | *The Shivee West Property is subject to a License Fees Agreement between Entrée and OTLLC and may ultimately be included in the Entrée/Oyu Tolgoi JV Property. |

| 2. | Outline of copper ± gold ± molybdenum porphyry mineralization is projected to surface. |

| 3. | Entrée has a 20% participating interest in the Hugo North Extension and Heruga deposits. |

Figure 1 shows the location of a north-northeast oriented, west-looking longitudinal section (A-A’) through the 12.4 km-long trend of porphyry deposits that comprise the Oyu Tolgoi project. The longitudinal section is shown on Figure 2 with the Entrée/Oyu Tolgoi JV Property to the right (north) and left (south) of the central portion, the Oyu Tolgoi mining licence, held 100% by OTLLC.

Page 8

Q3 2022 MD&A (table amounts expressed in thousands of US Dollars, except per share amounts and where otherwise noted)

Figure 2 - Section Through the Oyu Tolgoi Trend of Porphyry Deposits

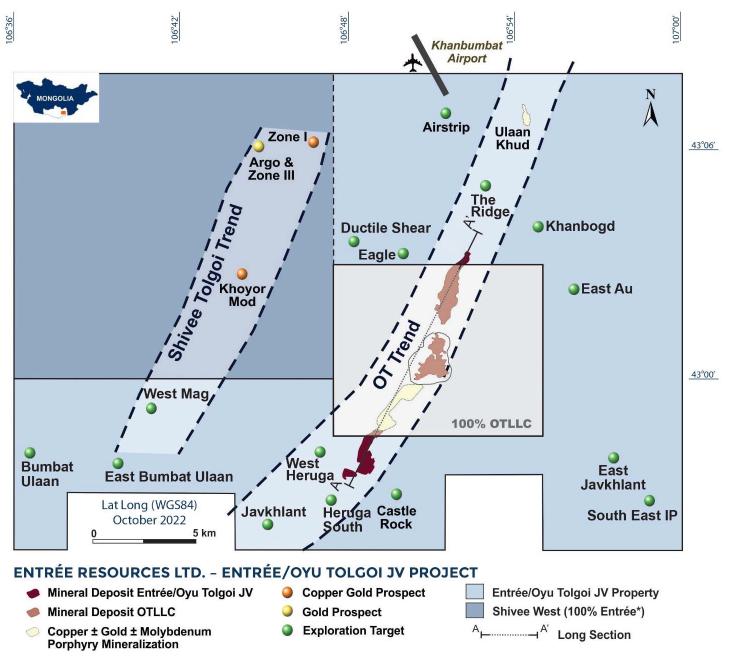

Figure 3 below shows priority exploration targets on the Entrée/Oyu Tolgoi JV Property, including Ulaan Khud, Airstrip, West Mag, Bumbat Ulaan, Ductile Shear, East Au, East Javkhlant, South East IP, Castle Rock, Javkhlant, and East Bumbat Ulaan. Additional targets exist on the Shivee West Property that remain to be further explored.

The 2021 Technical Report forms the basis for the scientific and technical information in this MD&A regarding the Entrée/Oyu Tolgoi JV Project. Portions of the information are based on assumptions, qualifications and procedures which are not fully described herein. Reference should be made to the Company’s AIF dated March 25, 2022 and to the full text of the 2021 Technical Report, which are available on the Company’s website (www.EntreeResourcesLtd.com) or on SEDAR (www.sedar.com).

Capital and Operating Costs

Under the terms of the Entrée/Oyu Tolgoi JV, OTLLC is responsible for 80% of all costs incurred on the Entrée/Oyu Tolgoi JV Property for the benefit of the Entrée/Oyu Tolgoi JV, including capital expenditures, and Entrée is responsible for the remaining 20%. In accordance with the terms of the Entrée/Oyu Tolgoi JVA, Entrée has elected to have OTLLC debt finance Entrée’s share of costs for approved programs and budgets, with interest accruing at OTLLC’s actual cost of capital or prime +2%, whichever is less, at the date of the advance. Debt repayment may be made in whole or in part from (and only from) 90% of monthly available cash flow arising from the sale of Entrée’s share of products. Available cash flow means all net proceeds of sale of Entrée’s share of products in a month less Entrée’s share of costs of Entrée/Oyu Tolgoi JV activities for the month that are operating costs under Canadian generally-accepted accounting principles.

The following is a description of how Entrée recognizes its share of Oyu Tolgoi project capital costs, specifically, the timing of recognition under the terms of the Entrée/Oyu Tolgoi JVA and generally accepted accounting principles.

Under the terms of the Entrée/Oyu Tolgoi JVA, any mill, smelter and other processing facilities and related infrastructure will be owned exclusively by OTLLC and not by Entrée. Mill feed from the Entrée/Oyu Tolgoi JV Property will be transported to the concentrator and processed at cost (using industry standards for calculation of cost including an amortization of capital costs). Underground infrastructure on the Oyu Tolgoi mining licence is also owned exclusively by OTLLC, although the Entrée/Oyu Tolgoi JV will eventually share usage once underground development crosses onto the Entrée/Oyu Tolgoi JV Property. As a result of this, Entrée recognizes those capital costs incurred by OTLLC on the Oyu Tolgoi mining licence as an amortization charge for capital costs that will be calculated in accordance with Canadian generally accepted accounting principles determined yearly based on the estimated tonnes of concentrate produced for Entrée’s account during that year relative to the estimated total life-of-mine concentrate to be produced (for processing facilities and related infrastructure), or the estimated total life-of-mine tonnes to be milled from the relevant deposit(s) (in the case of underground infrastructure). The charge is made to Entrée’s operating account when the Entrée/Oyu Tolgoi JV mine production is actually milled.

Page 9

Q3 2022 MD&A (table amounts expressed in thousands of US Dollars, except per share amounts and where otherwise noted)

For direct capital cost expenditures on the Entrée/Oyu Tolgoi JV Property, Entrée will recognize its proportionate share of costs at the time of actual expenditure.

The capital and operating costs in the 2021 Reserve Case are based on estimates prepared for OTMSS20 or information provided by OTLLC. Capital cost and sustaining cost estimates in the 2021 PEA were prepared as separate and independent estimates by OTLLC. Wood reviewed the estimates and accepts them as reasonable.

The cash flows in the 2021 Reserve Case and 2021 PEA are based on information provided by OTLLC, including mining schedules and annual capital and operating cost estimates, as well as Entrée’s interpretation of the commercial terms applicable to the Entrée/Oyu Tolgoi JV, and certain assumptions regarding taxes and royalties. The cash flows have not been reviewed or endorsed by OTLLC. There can be no assurance that OTLLC or its shareholders will not interpret certain terms or conditions or attempt to renegotiate some or all of the material terms governing the joint venture relationship, in a manner which could have an adverse effect on Entrée’s future cash flow and financial condition.

The cash flows also assume that Entrée will ultimately have the benefit of the standard royalty rate of 5% of sales value, payable by OTLLC under the Oyu Tolgoi Investment Agreement. Unless and until Entrée finalizes agreements with the Government of Mongolia or other Oyu Tolgoi stakeholders or enforces certain provisions of the Earn-in Agreement and Entrée/Oyu Tolgoi JVA pursuant to binding arbitration proceedings, there can be no assurance that the Entrée/Oyu Tolgoi JV will not be subject to additional taxes and royalties, such as the surtax royalty which came into effect in Mongolia on January 1, 2011, which could have an adverse effect on Entrée’s future cash flow and financial condition. In the course of finalizing such agreements or enforcing such provisions, Entrée may have to make certain concessions, including with respect to the economic benefit of Entrée’s interest in the Entrée/Oyu Tolgoi JV Property, Entrée’s direct or indirect participating interest in the Entrée/Oyu Tolgoi JV or the application of a special royalty (not to exceed 5%) to Entrée’s share of the Entrée/Oyu Tolgoi JV Property mineralization or otherwise.

Mineral Resources and Mineral Reserves - Entrée/Oyu Tolgoi JV Property

The following Entrée/Oyu Tolgoi JV Property mineral resource estimates reported in the 2021 Technical Report for the Hugo North Extension and Heruga deposits have an effective date of March 31, 2021. Mineral resources for the Hugo North Extension deposit are reported inclusive of those mineral resources that were converted to mineral reserves. Mineral resources that are not mineral reserves do not have demonstrated economic viability.

| Entrée/Oyu Tolgoi JV Property - Mineral Resources | ||||||||||

| Classification | Tonnage (Mt) | Cu (%) | Au (g/t) | Ag (g/t) | Mo (ppm) | CuEq (%) | Contained Metal | |||

Cu (Mlb) | Au (Koz) | Ag (Koz) | Mo (Mlb) | |||||||

| Hugo North Extension (>0.41% CuEq Cut-Off) | ||||||||||

| Indicated | 120 | 1.70 | 0.58 | 4.3 | n/a | 2.04 | 4,500 | 2,200 | 16,000 | n/a |

| Inferred | 167 | 1.02 | 0.36 | 2.8 | n/a | 1.23 | 3,800 | 1,900 | 15,000 | n/a |

| Heruga (>0.41% CuEq Cut-Off) | ||||||||||

| Inferred | 1,400 | 0.41 | 0.40 | 1.5 | 120 | 0.68 | 13,000 | 18,000 | 66,000 | 370 |

Notes:

| 1. | Mineral resources have an effective date of March 31, 2021. |

| 2. | Metal prices used for CuEq and cut-off grade calculation for both Hugo North Extension and Heruga are: $3.08/lb copper, $1,292.00/oz gold, $19.00/oz silver and $10.00/lb molybdenum (Heruga only). Metallurgical recoveries used for CuEq and cut-off grade calculation at Hugo North Extension are 93% for copper, 80% for gold and 81% for silver. Metallurgical recoveries used for CuEq and cut-off grade calculation at Heruga are 82% for copper, 73% for gold, 78% for silver and 60% for molybdenum. |

| 3. | Mineral resources at Hugo North Extension are constrained within a conceptual mining shape constructed at a nominal 0.50% CuEq grade and above a CuEq grade of 0.41% CuEq. The CuEq formula is CuEq = Cu + ((Au * 35.7175) + (Ag * 0.5773)) / 67.9023 taking into account differentials between metallurgical performance and price for copper, gold and silver. |

| 4. | The overall geometry and depth of the Heruga deposit make it amenable to underground mass mining methods. Mineral resources are stated above a CuEq grade. The CuEq formula is CuEq = Cu + ((Au * 37.0952) + (Ag * 0.5810) + (Mo * 0.0161)) / 67.9023 taking into account differentials between metallurgical performance and price for copper, gold, silver and molybdenum. |

| 5. | A CuEq break-even cut-off grade of 0.41% CuEq for Hugo North Extension mineralization and covers mining, processing and G&A operating cost and the cost of primary and secondary block cave mine development. |

| 6. | A CuEq break-even cut-off grade of 0.41% CuEq is used for the Heruga mineralization and covers mining, processing and G&A operating cost and the cost of primary and secondary block cave mine development. |

| 7. | Mineral resources are stated as in situ with no consideration for planned or unplanned external mining dilution. |

| 8. | Mineral resources are reported on a 100% basis. OTLLC has a participating interest of 80%, and Entrée has a participating interest of 20%. Notwithstanding the foregoing, in respect of products extracted from the Entrée/Oyu Tolgoi JV Property pursuant to mining carried out at depths from surface to 560 metres below surface, the participating interest of OTLLC is 70% and the participating interest of Entrée is 30%. |

Page 10

Q3 2022 MD&A (table amounts expressed in thousands of US Dollars, except per share amounts and where otherwise noted)

| 9. | Numbers have been rounded as required by reporting guidelines and may result in apparent summation differences. |

Entrée/Oyu Tolgoi Mineral Reserves

Entrée/Oyu Tolgoi JV Property mineral reserves are contained within the Hugo North Extension Lift 1 block cave mining plan. The mine design work on Hugo North Lift 1, including the Hugo North Extension, was prepared by OTLLC and was used as the basis for OTMSS20. The mineral reserve estimate is based on what is deemed minable when considering factors such as the footprint cut-off grade, the draw column shut-off grade, maximum height of draw, consideration of planned dilution and internal waste rock.

The mineral reserve estimate only considers mineral resources in the Indicated category and engineering that has been carried out to a Feasibility level or better to state the underground mineral reserve. There is no Measured mineral resource currently estimated within the Hugo North Extension deposit. Copper and gold grades for the Inferred mineral resources within the block cave shell were set to zero and such material was assumed to be dilution. The block cave shell was defined by a $17.84/t NSR. Future mine planning studies may examine lower shut-offs.

The following Entrée/Oyu Tolgoi JV Property Hugo North Extension Lift 1 mineral reserve estimate has an effective date of May 15, 2021:

Entrée/Oyu Tolgoi JV Property - Mineral Reserve Hugo North Extension Lift 1 | ||||||||

| Classification | Tonnage | NSR | Cu | Au | Ag | Contained Metal | ||

| (Mt) | ($/t) | (%) | (g/t) | (g/t) | Cu (Mlb) | Au (Koz) | Ag (Koz) | |

| Probable | 40 | 97.52 | 1.5 | 0.53 | 3.63 | 1,340 | 676 | 4,613 |

Notes:

| 1. | Mineral reserves have an effective date of May 15, 2021. |

| 2. | For the underground block cave, all Indicated mineral resources within the cave outline were converted to Probable mineral reserves. No Proven mineral reserves have been estimated. The estimation includes low-grade Indicated mineral resources and Inferred mineral resource assigned zero grade that is treated as dilution. |

| 3. | A column height shut-off NSR of $17.84/t was used to define the footprint and column heights. The NSR calculation assumed metal prices of $3.08/lb Cu, $1,292.00/oz Au, and $19.00/oz Ag. The NSR was calculated with assumptions for smelter refining and treatment charges, deductions and payment terms, concentrate transport, metallurgical recoveries, and royalties using OTLLC’s Base Data Template 38. |

| 4. | Mineral reserves are reported on a 100% basis. OTLLC has a participating interest of 80%, and Entrée has a participating interest of 20%. Notwithstanding the foregoing, in respect of products extracted from the Entrée/Oyu Tolgoi JV Property pursuant to mining carried out at depths from surface to 560 metres below surface, the participating interest of OTLLC is 70% and the participating interest of Entrée is 30%. |

| 5. | Numbers have been rounded as required by reporting guidelines and may result in apparent summation differences. |

Shivee West Property Summary

The Shivee West Property comprises the northwest portion of the Entrée/Oyu Tolgoi JV Project and adjoins the Entrée/Oyu Tolgoi JV Property and OTLLC’s Oyu Tolgoi mining licence (see Figure 1 above).

To date, no economic zones of precious or base metals mineralization have been outlined on the Shivee West Property. However, zones of gold and copper mineralization have previously been identified at Zone III/Argo Zone and Khoyor Mod. There has been no drilling on the ground since 2011, and no exploration work has been completed since 2012. In 2015, in light of the ongoing requirement to pay approximately $350,000 annually in licence fees for the Shivee West Property and a determination that no further exploration work would likely be undertaken in the near future, Entrée began to examine options to reduce expenditures in Mongolia. These options included reducing the area of the mining licence, looking for a purchaser or partner for the Shivee West Property, and rolling the ground into the Entrée/Oyu Tolgoi JV. Management determined that it was in the best interests of Entrée to roll the Shivee West Property into the Entrée/Oyu Tolgoi JV, and Entrée entered into a License Fees Agreement with OTLLC on October 1, 2015. The License Fees Agreement provides the parties will use their best efforts to amend the terms of the Entrée/Oyu Tolgoi JVA to include the Shivee West Property in the definition of Entrée/Oyu Tolgoi JV Property. Entrée determined that rolling the Shivee West Property into the Entrée/Oyu Tolgoi JV would provide the joint venture partners with continued security of tenure; Entrée shareholders would continue to benefit from any exploration or development that the Entrée/Oyu Tolgoi JV management committee approves on the Shivee West Property; and Entrée would no longer have to pay licence fees, as the parties agreed that the licence fees would be for the account of each joint venture participant in proportion to their respective interests, with OTLLC contributing Entrée’s 20% share charging interest at prime plus 2%. To date, no amended Entrée/Oyu Tolgoi JVA has been entered into and Entrée retains a 100% interest in the Shivee West Property.

Page 11

Q3 2022 MD&A (table amounts expressed in thousands of US Dollars, except per share amounts and where otherwise noted)

Underground Development Progress - Oyu Tolgoi Project

On October 17, 2022, Turquoise Hill provided an update regarding the Oyu Tolgoi project.

Underground Development Update

Safety continues to be OTLLC’s top priority and COVID-19 controls remain in place at site to protect OTLLC’s work force. COVID-19 cases identified at Oyu Tolgoi continued at low levels in the third quarter 2022 and the testing regime has been eased. Following the recent relaxation of COVID-19 government-initiated restrictions in Mongolia, OTLLC has progressively restarted work on project facilities with workforce numbers now at full capacity.

Construction of the final major stage of materials handling infrastructure continues, including civil and underground works for the conveyor to surface. Undercut blasting and on-footprint construction work continued to progress during the third quarter 2022. Commissioning of the second truck chute has commenced, and the 8th draw bell was fired on October 13, 2022, both ahead of schedule. Sustainable production from Panel 0 on the Oyu Tolgoi mining licence is now anticipated in the first quarter 2023.

The Shaft 3 headframe was commissioned and sinking commenced on March 31, 2022, with the cumulative sinking level at 298 metres below ground level as at October 2, 2022. Shaft 4 advancement was 418 metres below ground level as at October 2, 2022. The rate of progress in shafts improved during the quarter due to the optimization work program to maximize the productivity of their development. Continued progress on the program is necessary to remain aligned with the 2022 cost and schedule update, which identified an approximate 15-month delay in the commissioning of Shafts 3 and 4 from the schedule in the Definitive Estimate. As previously disclosed, Turquoise Hill now expects Shafts 3 and 4 to be commissioned in the first half 2024, and progress continues to be closely monitored. Shafts 3 and 4 are required to provide ventilation to support production from Panels 1 and 2 during ramp up to 95,000 tpd. Turquoise Hill currently expects the first Panel 1 draw bell in the first half 2027. The Hugo North Extension deposit on the Entrée/Oyu Tolgoi JV Property is located in the northern portion of Panel 1.

Design optimization work for Lift 1 on the Oyu Tolgoi mining licence and the Entrée/Oyu Tolgoi JV Property continues with the aim of minimizing risk and maximizing productivity. The Lift 1 Panel 1 design optimization study remains on track for completion in the first half 2023.

Renewed Partnership with Government of Mongolia

On November 21, 2019, Resolution 92 was passed in a plenary session of the Parliament of Mongolia. Resolution 92 was published on December 6, 2019 and includes measures to improve the implementation of the Oyu Tolgoi Investment Agreement and the 2011 Amended and Restated Shareholders’ Agreement (the "Shareholders’ Agreement"), improve the 2015 Oyu Tolgoi Underground Mine Development and Financing Plan (the "Mine Plan") and explore and resolve options to have a product sharing arrangement or swap Mongolia’s 34% equity holding for a special royalty.

In the fourth quarter 2021, negotiations between Turquoise Hill, Rio Tinto and various Mongolian governmental bodies progressed towards resolution of the outstanding items necessary to enable Lift 1 Panel 0 undercut commencement including approval for registration of the resources and reserves update ("RR19") through the Minerals Council of Mongolia in the fourth quarter 2021, and submission for assessment of OTMSS20 to the Mongolian Minerals Council pursuant to Mongolian regulatory requirements.

On December 13, 2021, Rio Tinto and Turquoise Hill made a joint offer to the Government of Mongolia with the aim of resetting the relationship and allowing all parties to move forward together. On December 30, 2021, the Parliament of Mongolia passed Resolution 103 that aimed to improve the benefits to Mongolia from the Oyu Tolgoi project and set out a number of required measures to resolve the outstanding issues in relation to Resolution 92.

Page 12

Q3 2022 MD&A (table amounts expressed in thousands of US Dollars, except per share amounts and where otherwise noted)

On January 24, 2022, Turquoise Hill announced that it had successfully reached a mutual understanding for a renewed partnership with the Government of Mongolia and that the OTLLC board had unanimously approved the commencement of the undercut and the Definitive Estimate underground development budget of $6.75 billion.

The decision to approve the undercut followed resolution of many of the conditions required in Resolution 103 including:

| • | Turquoise Hill agreeing to waive in full the $2.4 billion carry account loan of Erdenes Oyu Tolgoi LLC. |

| • | Improved cooperation with Erdenes Oyu Tolgoi LLC in monitoring the Oyu Tolgoi underground development and enhancing environment, social and governance (ESG) matters. |

| • | The approval of the Electricity Supply Agreement with, amongst others, Southern Region Electricity Distribution Network to provide OTLLC with a long-term source of power from the Mongolian grid on terms fully agreed with the Government of Mongolia. |

| • | The establishment of a funding structure at OTLLC that does not incur additional loan financing prior to sustainable production for Panel 0 (expected in the first quarter 2023). |

Remaining outstanding measures of Resolution 103 include the formal termination of the Mine Plan and resolution of the outstanding OTLLC tax arbitration.

Resolution 103 imposes restrictions that limit OTLLC’s ability to obtain third party debt financing and Turquoise Hill’s ability to fund OTLLC with shareholder debt or to carry common share investments in OTLLC on behalf of Erdenes Oyu Tolgoi LLC until sustainable production from Lift 1 Panel 0 is achieved, which is currently expected in the first quarter 2023. On August 4, 2022, Turquoise Hill reported that until sustainable production from Lift 1 Panel 0 is achieved, OTLLC’s estimated funding requirements are expected to be addressed by cash on hand at OTLLC, the Re-profiling and an OTLLC board approved pre-paid copper concentrate sale arrangement between Turquoise Hill and OTLLC.

Oyu Tolgoi Funding

As reported by Turquoise Hill, as provided for in the Third Amended and Restated Heads of Agreement dated September 5, 2022 (the "Amended HoA"), Turquoise Hill and Rio Tinto have continued to advance discussions with project finance lenders under the Oyu Tolgoi project financing (the "OT Project Financing") with a view to rescheduling the principal repayments of the existing Oyu Tolgoi project debt (the "Re-profiling") so as to potentially reduce Turquoise Hill’s base case funding requirement (estimated as at August 4, 2022 to be approximately $3.6 billion) by up to approximately $1.7 billion and better align the servicing of such debt with the updated Oyu Tolgoi project mine plan and to raise up to $500 million of additional senior supplemental debt ("SSD"). Rio Tinto is responsible for leading the process and negotiations for the Re-profiling and SSD with support from and consultation with Turquoise Hill and OTLLC. To become effective, the Re-profiling requires the unanimous consent of the existing lenders under the OT Project Financing or the replacement of any lenders that withhold their consent; it will also require the approval of the OTLLC board. Turquoise Hill and Rio Tinto have been working towards completing the Re-profiling prior to the scheduled repayment of $362 million due on December 15, 2022 under the existing OT Project Financing.

Progress has been made on reaching agreement on the commercial terms and conditions of the Re-profiling, with the commercial terms and conditions now substantially agreed. Certain existing commercial bank lenders under the OT Project Financing have indicated that they are unable or unwilling to participate in the Re-profiling. Consequently, Rio Tinto and Turquoise Hill are pursuing several potential solutions, including but not limited to engaging existing lenders that are currently participating in the Re-profiling with a view to increasing their current participation levels, and engaging new potential commercial bank lenders who could replace any banks that ultimately decide to exit.

If Rio Tinto and Turquoise Hill are not successful in their efforts to secure the Re-profiling on or before December 15, 2022, Turquoise Hill would in order to address near-term liquidity needs, be required to draw on the $362 million bridge financing that Rio Tinto has committed to provide under the Amended HoA in order to fund the principal repayment of that same amount under the OT Project Financing due on December 15, 2022. The Amended HoA contemplates that the $362 million bridge facility will be made on the same terms as the $650 million "Early Advance" commitment thereunder and would be repaid through an equity raise.

If the Re-profiling and SSD funding contemplated by the Amended HoA are not wholly successful, or the principal repayment of $362 million under the OT Project Financing is required to be made on December 15, 2022, Turquoise Hill would require additional equity financing which would be incremental to estimated equity raising of $1.05 billion previously disclosed in Turquoise Hill’s second quarter 2022.

Turquoise Hill’s incremental funding requirement, and quantum and timing of any incremental equity raises, continue to be impacted by various factors, many of which are outside of its control and, as a result, their actual quantum and/or timing could be different from the estimates provided by Turquoise Hill.

2022 Planned Development and Exploration Work on the Entrée/Oyu Tolgoi JV Property

Planned Development Work

For Panel 1 drilling on the Entrée/Oyu Tolgoi JV Property, the Entrée/Oyu Tolgoi JV has approved a 2022 budget with diamond drill holes targeting Hugo North Extension Lifts 1 and 2. The holes are collared from underground drill stations along the eastern boundary of the porphyry mineralized footprint on the Oyu Tolgoi mining licence crossing onto the Entrée/Oyu Tolgoi JV Property. As at the end of October 2022, 14 underground holes have been drilled on the Entrée/Oyu Tolgoi JV Property totalling 6,083.3 metres. In addition, two surface diamond drill holes totalling ~3,550 metres are in progress, with hole EGD173 currently at a depth of 1,698 meters (planned depth 1,800 metres) and hole EGD161 currently at a depth of 364 metres (planned depth 1,750 metres). The two surface holes will be entirely on the Entrée/Oyu Tolgoi JV Property and will target the northern portion of the Hugo North Extension deposit.

Page 13

Q3 2022 MD&A (table amounts expressed in thousands of US Dollars, except per share amounts and where otherwise noted)

OTLLC has planned the Lift 1 Panel 1 underground drilling primarily for geological and geotechnical investigation and grade validation. OTLLC characterizes the main purpose of the Lift 2 Panel 1 underground drilling as geological and geotechnical investigation and resource conversion. OTLLC had scheduled all the drilling to be completed during 2022, with potential additional phases to follow in 2023 or beyond.

The Lift 1 Panel 1 geological model is expected to be finalized in the first quarter 2023, following which a decision will be made as to whether more Lift 1 drilling will be required. The Company has received preliminary results from a portion of the underground holes and is in the process of collating and modelling the data.

Panel 1 Development

The Company continues to monitor the situation in Mongolia including with respect to possible delays to commencement of Panel 1. The Company will assess the potential impact of any delays as it becomes aware of them and will update the market accordingly.

Planned Target Generation Work

OTLLC’s site technical services team undertakes all exploration work on the Entrée/Oyu Tolgoi JV Property. Turquoise Hill has reported that the current exploration strategy for the Oyu Tolgoi project, including the Entrée/Oyu Tolgoi JV Property, is focused on developing a project pipeline prioritized in areas that can impact the current development of the Oyu Tolgoi deposits, seeking low-cost development options and continuing the assessment of legacy datasets to enable future discovery.

Exploration during 2016 to 2021 on the Entrée/Oyu Tolgoi JV Property included early-stage target generation work on both the Shivee Tolgoi and Javhlant mining licences. The work included geological mapping, soil and rock geochemical sampling, geophysical surveys, small amounts of shallow core and RC drilling, and integrated geological-geophysical 3D modelling. Results of work conducted between 2016 and 2020 and detailed descriptions of the targets have been reported in the Company’s previous quarterly and annual filings, as well as the 2021 Technical Report, available on SEDAR at www.sedar.com under the Company’s profile.

During 2021, exploration programs on the Entrée/Oyu Tolgoi JV Property were very minimal and all exploration drilling and larger programs were put on hold due to COVID-19 related restrictions. With the relaxation of COVID-19 related restrictions in Mongolia, exploration drilling programs resumed in 2022. On the Shivee Tolgoi mining licence, six RC holes totalling 1,500 metres and one 800 metre diamond drill hole have been completed at the Ulaan Khud target. In addition, three diamond drill holes totalling 2,200 metres have been completed at the Airstrip target. Analytical results are pending.

On the Javhlant mining licence, five RC holes totalling 1,500 metres were planned for each of the Bumbat Ulaan and West Mag targets in 2022. Two RC holes totalling 600 metres were completed at the West Mag target and analytical results are pending; the remaining three holes were cancelled following engagement with one of the local herders. The five RC holes planned for the Bumbat Ulaan target were not completed due to the recent commissioning of the Tavan Tolgoi-Gashuunsukhait railway.

Dipole-dipole induced polarization survey work has been completed at the East Au, South East IP, West Mag, East Bumbat Ulaan, and Ductile Shear target areas. No results from the above work have been provided to Entrée. 3D modeling is also underway for several of the current target areas and a final report is expected to be completed in December 2022. Proposed mapping and rock-soil sampling programs have been cancelled due to inclement weather.

Page 14

Q3 2022 MD&A (table amounts expressed in thousands of US Dollars, except per share amounts and where otherwise noted)

Figure 3 - Entrée/Oyu Tolgoi JV Project Exploration Targets

| 1. | The Shivee West Property is subject to a License Fees Agreement between Entrée and OTLLC and may ultimately be included in the Entrée/Oyu Tolgoi JV Property. |

| 2. | Outline of copper ± gold ± molybdenum porphyry mineralization is projected to surface. |

| 3. | Entrée has a 20% or 30% participating interest depending on the depth of mineralization. |

Q3 2022 Financial Review

Entrée expenses related to Mongolian operations included expenditures of $0.3 million for strategic and administration costs in Mongolia. The Company focused its efforts on advancing potential amendments to the Entrée/Oyu Tolgoi JVA with the objective to align the interests of all stakeholders as they are now understood, which would be in the best interests of all stakeholders. Costs were related to legal and tax advisory consultants to assist in the process in the current period, which also include costs related to the arbitration. The costs in the comparative periods of 2021 include professional fees related to the 2021 Technical Report.

Page 15

Q3 2022 MD&A (table amounts expressed in thousands of US Dollars, except per share amounts and where otherwise noted)

SUMMARY OF CONSOLIDATED FINANCIAL OPERATING RESULTS

Operating Results

The Company’s operating results for the three and nine months ended September 30 were:

| (unaudited) | Three months ended September 30 | Nine months ended September 30 | ||||||||||||||

| 2022 | 2021 | 2022 | 2021 | |||||||||||||

| Expenses | ||||||||||||||||

| Project expenditures | $ | 67 | $ | 169 | $ | 318 | $ | 414 | ||||||||

| General and administrative | 348 | 310 | 1,286 | 1,093 | ||||||||||||

| Share-based compensation | 19 | – | 77 | – | ||||||||||||

| Depreciation | 30 | 30 | 95 | 87 | ||||||||||||

| Operating loss | 464 | 509 | 1,776 | 1,594 | ||||||||||||

| Foreign exchange loss | 529 | 210 | 660 | 16 | ||||||||||||

| Interest income | (36 | ) | (5 | ) | (77 | ) | (23 | ) | ||||||||

| Interest expense | 95 | 88 | 273 | 259 | ||||||||||||

| Loss from equity investee | 116 | 41 | 181 | 112 | ||||||||||||

| Finance costs | 15 | 3 | 46 | 10 | ||||||||||||

| Deferred revenue finance costs | 1,040 | 1,021 | 3,150 | 2,995 | ||||||||||||

| Other | – | 9 | – | 9 | ||||||||||||

| Loss for the period | 2,223 | 1,876 | 6,009 | 4,972 | ||||||||||||

| Other comprehensive (income) loss | ||||||||||||||||

| Foreign currency translation | (3,411 | ) | 1,497 | (4,325 | ) | (91 | ) | |||||||||

| Total comprehensive (income) loss | $ | (1,188 | ) | $ | 3,373 | $ | 1,684 | $ | 4,881 | |||||||

| Net loss per common share | ||||||||||||||||

| Basic and fully diluted | $ | (0.01 | ) | $ | (0.01 | ) | $ | (0.03 | ) | $ | (0.03 | ) | ||||

| Total assets | $ | 8,082 | $ | 7,311 | $ | 8,082 | $ | 7,311 | ||||||||

| Total non-current liabilities | $ | 62,709 | $ | 61,220 | $ | 62,709 | $ | 61,220 | ||||||||

Operating Loss:

During the three and nine month periods ended September 30, 2022, the Company’s operating loss was $0.5 million and $1.8 million, respectively, compared to an operating loss of $0.5 million and $1.6 million in the comparative periods of 2021.

Project expenditures in Q3 2022 were lower compared to Q3 2021 due to 2021 expenses relating to the 2021 Technical Report.

General and administration was higher than the 2021 periods due to increased administration expenses and inflationary cost increases.

Share-based compensation in Q3 2022 was related to vesting of share options granted to new directors in the previous quarter.

Page 16

Q3 2022 MD&A (table amounts expressed in thousands of US Dollars, except per share amounts and where otherwise noted)

Depreciation expense was consistent with the comparative periods in 2021.

Non-operating Items:

The foreign exchange loss was primarily the result of movements between the C$ and US dollar as the Company holds its cash in both currencies and the loan payable is denominated in US dollars.

Interest expense was primarily related to the loan payable to OTLLC pursuant to the Entrée/Oyu Tolgoi JVA and is subject to a variable interest rate.

The amount recognized as a loss from equity investee is related to exploration costs on the Entrée/Oyu Tolgoi JV Property.

Deferred revenue finance costs are related to recording the non-cash finance costs associated with the deferred revenue balance, specifically the Sandstorm stream.

The total assets as at September 30, 2022 were higher than at September 30, 2021 mainly due to funds received from the exercise of share purchase warrants during Q1 2022 and Q4 2021. See “Shareholder’s Deficiency” section below. Total non-current liabilities have increased since September 30, 2021 due to recording the non-cash deferred revenue finance costs each quarter.

Quarterly Financial Data - 2 year historic trend

| Q3 22 | Q2 22 | Q1 22 | Q4 21 | Q3 21 | Q2 21 | Q1 21 | Q4 20 | |||||||||||||||||||||||||

| Project expenditures | $ | 67 | $ | 151 | $ | 100 | $ | 88 | $ | 169 | $ | 158 | $ | 87 | $ | 41 | ||||||||||||||||

| General and administrative | 348 | 500 | 438 | 512 | 310 | 444 | 339 | 437 | ||||||||||||||||||||||||

| Share-based compensation | 19 | 58 | – | 735 | – | – | – | 538 | ||||||||||||||||||||||||

| Depreciation | 30 | 33 | 33 | 31 | 30 | 27 | 30 | 22 | ||||||||||||||||||||||||

| Operating loss | 464 | 741 | 571 | 1,366 | 509 | 629 | 456 | 1,038 | ||||||||||||||||||||||||

| Foreign exchange loss (gain) | 529 | 261 | (130 | ) | (46 | ) | 210 | (101 | ) | (93 | ) | (355 | ) | |||||||||||||||||||

| Interest expense, net | 59 | 64 | 88 | 95 | 92 | 76 | 77 | 65 | ||||||||||||||||||||||||

| Loss from equity investee | 116 | 33 | 32 | 123 | 41 | 36 | 35 | 60 | ||||||||||||||||||||||||

| Deferred revenue finance costs | 1,040 | 1,058 | 1,052 | 1,040 | 1,021 | 1,006 | 968 | 887 | ||||||||||||||||||||||||

| Finance costs | 15 | 16 | 15 | 5 | 3 | 3 | 4 | 4 | ||||||||||||||||||||||||

| Net loss | $ | 2,223 | $ | 2,173 | $ | 1,613 | $ | 2,583 | $ | 1,876 | $ | 1,649 | $ | 1,447 | $ | 1,699 | ||||||||||||||||

| Basic/diluted loss per share | $ | (0.01 | ) | $ | (0.01 | ) | $ | (0.01 | ) | $ | (0.01 | ) | $ | (0.01 | ) | $ | (0.01 | ) | $ | (0.01 | ) | $ | (0.01 | ) | ||||||||

| USD:CAD FX Rate(1) | 1.3707 | 1.2886 | 1.2496 | 1.2678 | 1.2741 | 1.2394 | 1.2575 | 1.2732 | ||||||||||||||||||||||||

| 1. | USD:CAD foreign exchange rate was the quarter ended rate per the Bank of Canada. |

Project expenditures in Q2 2022, Q3 2021 and Q2 2021 were higher compared to other quarters due to expenses relating to professional fees to advance potential amendments to the Entrée/Oyu Tolgoi JVA and due to expenses for preparation of the 2021 Technical Report.

General and administrative expenses were higher in Q2 2022 and Q4 2021 due mainly to regulatory costs and compensation costs, respectively.

Share-based compensation expenditures in Q4 2021 included deferred share unit ("DSU") grants at higher fair value compared to DSU grants in Q4 2020.

Interest expense, net, consists of accrued interest on the OTLLC loan payable net of interest income earned on invested cash.

The loss from equity investee was related to the Entrée/Oyu Tolgoi JV Property and fluctuations are due to exploration activity and foreign exchange changes.

Page 17

Q3 2022 MD&A (table amounts expressed in thousands of US Dollars, except per share amounts and where otherwise noted)

LIQUIDITY AND CAPITAL RESOURCES

| Three months ended September 30 | Nine months ended September 30 | |||||||||||||||

| 2022 | 2021 | 2022 | 2021 | |||||||||||||

| Cash flows used in operating activities | ||||||||||||||||

| - Before changes in non-cash working capital items | $ | (534 | ) | $ | (464 | ) | $ | (1,720 | ) | $ | (1,488 | ) | ||||

| - After changes in non-cash working capital items | (557 | ) | (679 | ) | (1,627 | ) | (1,447 | ) | ||||||||

| Cash flows from financing activities | 133 | 136 | 1,893 | 892 | ||||||||||||

| Cash flows used in investing activities | – | (1 | ) | – | (33 | ) | ||||||||||

| Net cash inflows (outflows) | (424 | ) | (544 | ) | 266 | (588 | ) | |||||||||

| Effect of exchange rate changes on cash | (224 | ) | (143 | ) | (306 | ) | (4 | ) | ||||||||

| Cash balance | $ | 7,050 | $ | 6,668 | $ | 7,050 | $ | 6,668 | ||||||||

Cash outflows after changes in non-cash working capital items for the three and nine month periods ended September 30, 2022 varied against than the comparative period in 2021 due to timing payments on accounts payable balances.

Cash flows from financing activities in all periods were due mainly to funds received from share option and warrant exercises.

Cash flows used in investing activities was minimal.

The Company is an exploration stage company and has not generated positive cash flows from its operations. As a result, the Company has been dependent on equity and production-based financings for additional funding. Working capital on hand at September 30, 2022 was approximately $7.1 million. Management believes it has adequate financial resources to satisfy its obligations over the next 12-month period and beyond. The Company does not currently anticipate the need for additional funding during this time.

Loan Payable to Oyu Tolgoi LLC

Under the terms of the Entrée/Oyu Tolgoi JVA, the Company has elected to have OTLLC contribute funds to approved joint venture programs and budgets on the Company’s behalf, each such contribution to be treated as a non-recourse loan. Interest on each loan advance shall accrue at an annual rate equal to OTLLC’s actual cost of capital or the prime rate of the Royal Bank of Canada, plus two percent (2%) per annum, whichever is less, as at the date of the advance. The loan will be repayable by the Company monthly from ninety percent (90%) of the Company’s share of available cash flow from the Entrée/Oyu Tolgoi JV. In the absence of available cash flow, the loan will not be repayable. The loan is not expected to be repaid within one year.

Contractual Obligations

As at September 30, 2022, the Company had the following contractual obligations outstanding:

| Total | Less than 1 year | 1 - 3 years | 3-5 years | More than 5 years | |

| Lease commitments | $ 684 | $ 128 | $ 385 | $ 171 | $ - |

SHAREHOLDERS’ DEFICIENCY

The Company’s authorized share capital consists of unlimited common shares without par value.

At the date of this MD&A, the Company had 197,964,931 shares issued and outstanding (September 30, 2022 - 197,831,429 shares).

Page 18

Q3 2022 MD&A (table amounts expressed in thousands of US Dollars, except per share amounts and where otherwise noted)

Share Purchase Warrants

During the nine months ended September 30, 2022, share purchase warrants to purchase 4,115,354 common shares with an exercise price of C$0.55 were exercised resulting in gross proceeds of C$2,263,445 being received by the Company. 586,803 share purchase warrants with an exercise price of C$0.55 expired on January 10, 2022.

The following share purchase warrants were outstanding as at the date of this report:

| Number of share purchase warrants (000’s) | Exercise price per share purchase warrant C$ | Expiry date |

| 5,139 | 0.60 | September 13, 2023 |

Stock Option Plan

As at September 30, 2022 the Company had 8,159,500 stock options outstanding of which 8,009,500 are exercisable. As at the date of this MD&A the Company had 7,849,500 stock options outstanding of which 7,699,500 are exercisable.

The following is a summary of stock options outstanding as at the date of this report:

| Number of share options (000`s) | Number of share options vested (000’s) | Exercise price per share option (C$) | Expiry date |

| 3,800 | 3,800 | 0.365 - 0.63 | Feb - Dec 2023 |

| 1,545 | 1,545 | 0.365 | Dec 2024 |

| 1,285 | 1,285 | 0.51 | Dec 2025 |

| 920 | 920 | 0.77 | Dec 2026 |

| 300 | 150 | 0.82 - 1.07 | Apr - June 2027 |

| 7,850 | 7,700 |

Deferred share units (DSU)

DSUs are granted to the Company’s directors and executives as a part of compensation under the terms of the Company’s Deferred Share Unit Plan (the "DSU Plan"). Typically, DSUs vest when certain conditions as stated in the DSU Plan are met, except in the event of an earlier change of control, in which case, the DSUs will vest fully upon such change of control.

During the nine months ended September 30, 2022, 110,000 deferred share units were redeemed for 110,000 common shares.

At September 30, 2022, the following DSUs were outstanding and fully vested:

| Number of DSUs (000’s) | |

| Outstanding - December 31, 2021 | 1,065 |

| Redeemed | (110) |

| Outstanding - September 30, 2022 | 955 |

Each vested DSU entitles the holder to receive one common share of the Company or a cash payment equivalent to the closing price of one common share of the Company on the TSX on the last trading day preceding the DSU’s redemption date.

DEFERRED REVENUE - SANDSTORM

The Company has an agreement to use future payments that it receives from its mineral property interests to purchase and deliver gold, silver and copper credits to Sandstorm (the "Sandstorm Agreement").

Under the terms of the Sandstorm Agreement, Sandstorm provided the Company with a net deposit of C$30.9 million (the "Deposit") in exchange for the future delivery of gold, silver and copper credits equivalent to:

Page 19

Q3 2022 MD&A (table amounts expressed in thousands of US Dollars, except per share amounts and where otherwise noted)

| • | 28.1% of Entrée’s share of gold and silver, and 2.1% of Entrée’s share of copper, produced from the Shivee Tolgoi mining licence (excluding the Shivee West Property); and |

| • | 21.3% of Entrée’s share of gold and silver, and 2.1% of Entrée’s share of copper, produced from the Javhlant mining licence. |

Upon the delivery of metal credits, Sandstorm will make a cash payment to the Company equal to the lesser of the prevailing market price and $220 per ounce of gold, $5 per ounce of silver and $0.50 per pound of copper (subject to inflation adjustments). After approximately 8.6 million ounces of gold, 40.3 million ounces of silver and 9.1 billion pounds of copper have been produced from the entire Entrée/Oyu Tolgoi JV Property (as currently defined) the cash payment will be increased to the lesser of the prevailing market price and $500 per ounce of gold, $10 per ounce of silver and $1.10 per pound of copper (subject to inflation adjustments). To the extent that the prevailing market price is greater than the amount of the cash payment, the difference between the two will be credited against the Deposit.

The Deposit has been accounted for as deferred revenue on the statement of financial position and is subject to foreign currency fluctuations upon conversion to US dollars at each reporting period. The Deposit contains a significant financing component and, as such, the Company recognizes a financing charge at each reporting period and grosses up the deferred revenue balance to recognize the significant financing element that is part of this contract at a discount rate of 8%.