Searchable text section of graphics shown above

Review of Business Strategy and Results

1st Quarter 2005

[LOGO] |

| www.FieldstoneInvestment.com |

|

|

|

As of May 4, 2005 |

|

|

Business Summary |

| [LOGO] |

• Fieldstone Investment Corporation: (NASDAQ: FICC): REIT

• Building a portfolio of non-conforming loans on-balance sheet:

• $5.1 billion at March 31, 2005 with an average FICO of 651

• Issued $5.0 billion of MBS to match-fund portfolio for life of loans

• Paid $1.09 of pre-tax dividends to shareholders for 2004

• Paid 1st Quarter 2005 dividend of $0.47

• Fieldstone Mortgage Company: Taxable REIT Subsidiary

• Performs loan origination and underwriting

• $6.2 billion of non-conforming loans in 2004

• $1.3 billion of conforming loans in 2004

• Opened 4 regional non-conforming operation centers in 2004

• Manage the quality of loans for REIT portfolio

• Sell non-conforming fixed rate, 2nds and certain hybrid loans, and all conforming loans

• Interim servicer for loans held for sale

• Can retain any after-tax earnings from loan sales to generate capital internally

*As of May 4, 2005*

2

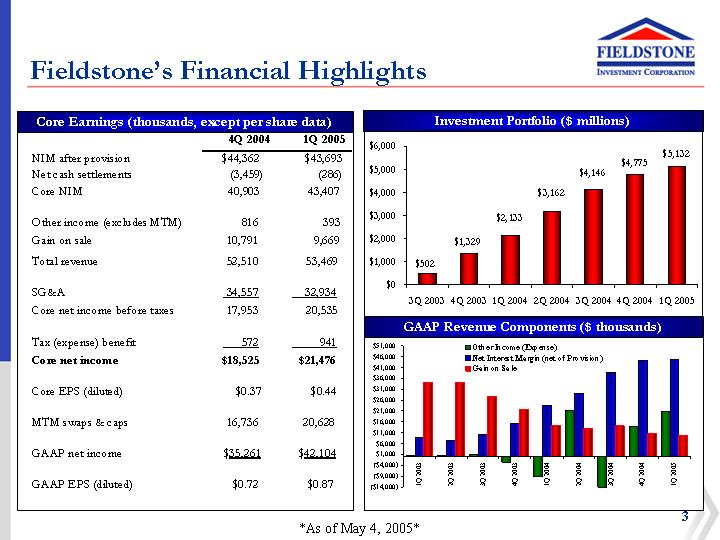

Fieldstone’s Financial Highlights

Core Earnings (thousands, except per share data)

|

| 4Q 2004 |

| 1Q 2005 |

| ||

NIM after provision |

| $ | 44,362 |

| $ | 43,693 |

|

Net cash settlements |

| (3,459 | ) | (286 | ) | ||

Core NIM |

| 40,903 |

| 43,407 |

| ||

|

|

|

|

|

| ||

Other income (excludes MTM) |

| 816 |

| 393 |

| ||

Gain on sale |

| 10,791 |

| 9,669 |

| ||

Total revenue |

| 52,510 |

| 53,469 |

| ||

|

|

|

|

|

| ||

SG&A |

| 34,557 |

| 32,934 |

| ||

Core net income before taxes |

| 17,953 |

| 20,535 |

| ||

|

|

|

|

|

| ||

Tax (expense) benefit |

| 572 |

| 941 |

| ||

Core net income |

| $ | 18,525 |

| $ | 21,476 |

|

|

|

|

|

|

| ||

Core EPS (diluted) |

| $ | 0.37 |

| $ | 0.44 |

|

|

|

|

|

|

| ||

MTM swaps & caps |

| 16,736 |

| 20,628 |

| ||

|

|

|

|

|

| ||

GAAP net income |

| $ | 35,261 |

| $ | 42,104 |

|

|

|

|

|

|

| ||

GAAP EPS (diluted) |

| $ | 0.72 |

| $ | 0.87 |

|

Investment Portfolio ($ millions)

[CHART]

GAAP Revenue Components ($ thousands)

[CHART]

3

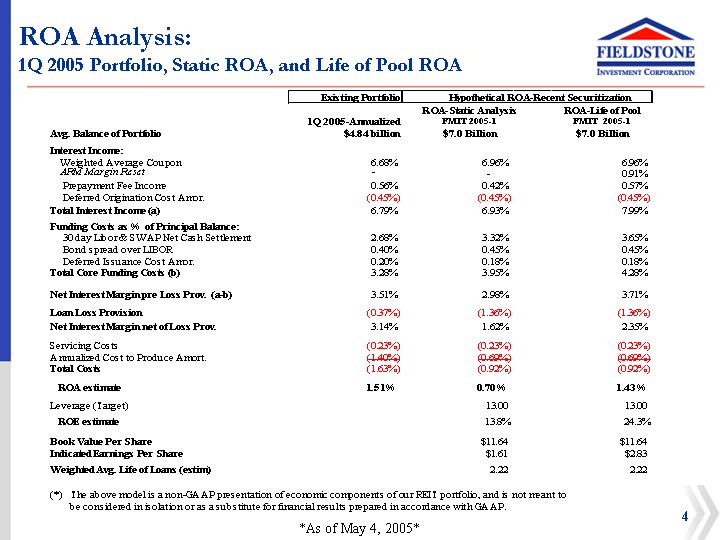

ROA Analysis:

1Q 2005 Portfolio, Static ROA, and Life of Pool ROA

|

|

|

| Hypothetical ROA-Recent Securitization |

| |||||

|

| Existing Portfolio |

| ROA-Static Analysis |

| ROA-Life of Pool |

| |||

|

| 1Q 2005-Annualized |

| FMIT 2005-1 |

| FMIT 2005-1 |

| |||

Avg. Balance of Portfolio |

| $ | 4.84 billion |

| $ | 7.0 Billion |

| $ | 7.0 Billion |

|

Interest Income: |

|

|

|

|

|

|

| |||

Weighted Average Coupon |

| 6.68 | % | 6.96 | % | 6.96 | % | |||

ARM Margin Reset |

| — |

| — |

| 0.91 | % | |||

Prepayment Fee Income |

| 0.56 | % | 0.42 | % | 0.57 | % | |||

Deferred Origination Cost Amor. |

| (0.45 | )% | (0.45 | )% | (0.45 | )% | |||

Total Interest Income (a) |

| 6.79 | % | 6.93 | % | 7.99 | % | |||

|

|

|

|

|

|

|

| |||

Funding Costs as% of Principal Balance: |

|

|

|

|

|

|

| |||

30 day Libor & SWAP Net Cash Settlement |

| 2.68 | % | 3.32 | % | 3.65 | % | |||

Bond spread over LIBOR |

| 0.40 | % | 0.45 | % | 0.45 | % | |||

Deferred Issuance Cost Amor. |

| 0.20 | % | 0.18 | % | 0.18 | % | |||

Total Core Funding Costs (b) |

| 3.28 | % | 3.95 | % | 4.28 | % | |||

|

|

|

|

|

|

|

| |||

Net Interest Margin pre Loss Prov. (a-b) |

| 3.51 | % | 2.98 | % | 3.71 | % | |||

|

|

|

|

|

|

|

| |||

Loan Loss Provision |

| (0.37 | )% | (1.36 | )% | (1.36 | )% | |||

Net Interest Margin net of Loss Prov. |

| 3.14 | % | 1.62 | % | 2.35 | % | |||

|

|

|

|

|

|

|

| |||

Servicing Costs |

| (0.23 | )% | (0.23 | )% | (0.23 | )% | |||

Annualized Cost to Produce Amort. |

| (1.40 | )% | (0.69 | )% | (0.69 | )% | |||

Total Costs |

| (1.63 | )% | (0.92 | )% | (0.92 | )% | |||

|

|

|

|

|

|

|

| |||

ROA estimate |

| 1.51 | % | 0.70 | % | 1.43 | % | |||

|

|

|

|

|

|

|

| |||

Leverage (Target) |

|

|

| 13.00 |

| 13.00 |

| |||

|

|

|

|

|

|

|

| |||

ROE estimate |

|

|

| 13.8 | % | 24.3 | % | |||

|

|

|

|

|

|

|

| |||

Book Value Per Share |

|

|

| $ | 11.64 |

| $ | 11.64 |

| |

Indicated Earnings Per Share |

|

|

| $ | 1.61 |

| $ | 2.83 |

| |

|

|

|

|

|

|

|

| |||

Weighted Avg. Life of Loans (estim) |

|

|

| 2.22 |

| 2.22 |

| |||

(*) The above model is a non-GAAP presentation of economic components of our REIT portfolio, and is not meant to be considered in isolation or as a substitute for financial results prepared in accordance with GAAP.

4

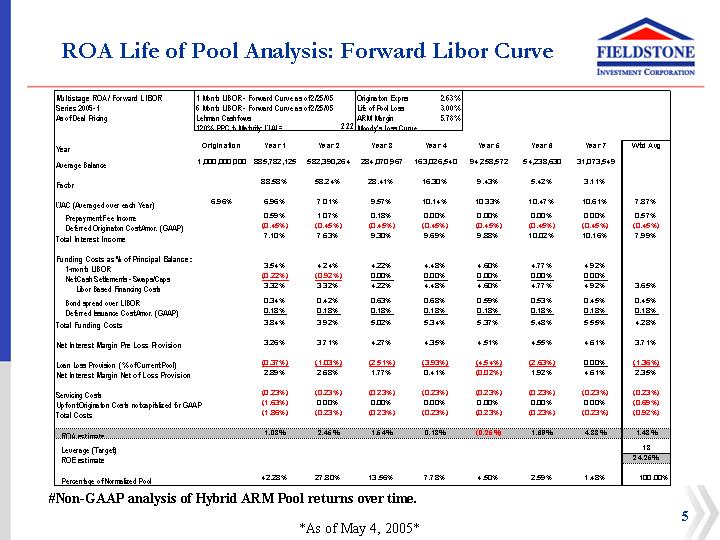

ROA Life of Pool Analysis: Forward Libor Curve

Multistage ROA / Forward LIBOR |

| 1 Month LIBOR - Forward Curve as of 2/25/05 |

| Origination Expns |

| 2.63 | % | 1.18 | % |

Series 2005-1 |

| 6 Month LIBOR - Forward Curve as of 2/25/05 |

| Life of Pool Loss |

| 3.00 | % | 1.35 | % |

As of Deal Pricing |

| Lehman Cashflows |

| ARM Margin |

| 5.78 | % |

|

|

|

| 120% PPC to Maturity: WAL= | 2.22 | Moody’s Loss Curve |

|

|

|

|

|

Year |

| Origination |

| Year 1 |

| Year 2 |

| Year 3 |

| Year 4 |

| Year 5 |

| Year 6 |

| Year 7 |

| Wtd Avg |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Average Balance |

| 1,000,000,000 |

| 885,782,125 |

| 582,390,264 |

| 284,070,967 |

| 163,026,540 |

| 94,258,572 |

| 54,238,630 |

| 31,073,549 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Factor |

|

|

| 88.58 | % | 58.24 | % | 28.41 | % | 16.30 | % | 9.43 | % | 5.42 | % | 3.11 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

WAC (Averaged over each Year) |

| 6.96 | % | 6.96 | % | 7.01 | % | 9.57 | % | 10.14 | % | 10.33 | % | 10.47 | % | 10.61 | % | 7.87 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Prepayment Fee Income |

|

|

| 0.59 | % | 1.07 | % | 0.18 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.57 | % |

Deferred Origination Cost Amor. (GAAP) |

|

|

| (0.45 | )% | (0.45 | )% | (0.45 | )% | (0.45 | )% | (0.45 | )% | (0.45 | )% | (0.45 | )% | (0.45 | )% |

Total Interest Income |

|

|

| 7.10 | % | 7.63 | % | 9.30 | % | 9.69 | % | 9.88 | % | 10.02 | % | 10.16 | % | 7.99 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Funding Costs as % of Principal Balance: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1-month LIBOR |

|

|

| 3.54 | % | 4.24 | % | 4.22 | % | 4.48 | % | 4.60 | % | 4.77 | % | 4.92 | % |

|

|

Net Cash Settlements - Swaps/Caps |

|

|

| (0.22 | )% | (0.92 | )% | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % |

|

|

Libor Based Financing Costs |

|

|

| 3.32 | % | 3.32 | % | 4.22 | % | 4.48 | % | 4.60 | % | 4.77 | % | 4.92 | % | 3.65 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Bond spread over LIBOR |

|

|

| 0.34 | % | 0.42 | % | 0.63 | % | 0.68 | % | 0.59 | % | 0.53 | % | 0.45 | % | 0.45 | % |

Deferred Issuance Cost Amor. (GAAP) |

|

|

| 0.18 | % | 0.18 | % | 0.18 | % | 0.18 | % | 0.18 | % | 0.18 | % | 0.18 | % | 0.18 | % |

Total Funding Costs |

|

|

| 3.84 | % | 3.92 | % | 5.02 | % | 5.34 | % | 5.37 | % | 5.48 | % | 5.55 | % | 4.28 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Interest Margin Pre Loss Provision |

|

|

| 3.26 | % | 3.71 | % | 4.27 | % | 4.35 | % | 4.51 | % | 4.55 | % | 4.61 | % | 3.71 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Loan Loss Provision (% of Current Pool) |

|

|

| (0.37 | )% | (1.03 | )% | (2.51 | )% | (3.93 | )% | (4.54 | )% | (2.63 | )% | 0.00 | % | (1.36 | )% |

Net Interest Margin Net of Loss Provision |

|

|

| 2.89 | % | 2.68 | % | 1.77 | % | 0.41 | % | (0.02 | )% | 1.92 | % | 4.61 | % | 2.35 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Servicing Costs |

|

|

| (0.23 | )% | (0.23 | )% | (0.23 | )% | (0.23 | )% | (0.23 | )% | (0.23 | )% | (0.23 | )% | (0.23 | )% |

Upfront Origination Costs not capitalized for GAAP |

|

|

| (1.63 | )% | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | (0.69 | )% |

Total Costs |

|

|

| (1.86 | )% | (0.23 | )% | (0.23 | )% | (0.23 | )% | (0.23 | )% | (0.23 | )% | (0.23 | )% | (0.92 | )% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ROA estimate |

|

|

| 1.03 | % | 2.45 | % | 1.54 | % | 0.18 | % | (0.25 | )% | 1.69 | % | 4.38 | % | 1.43 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Leverage (Target) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| 13 |

|

ROE estimate |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| 24.25 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Percentage of Normalized Pool |

|

|

| 42.28 | % | 27.80 | % | 13.56 | % | 7.78 | % | 4.50 | % | 2.59 | % | 1.48 | % | 100.00 | % |

#Non-GAAP analysis of Hybrid ARM Pool returns over time.

5

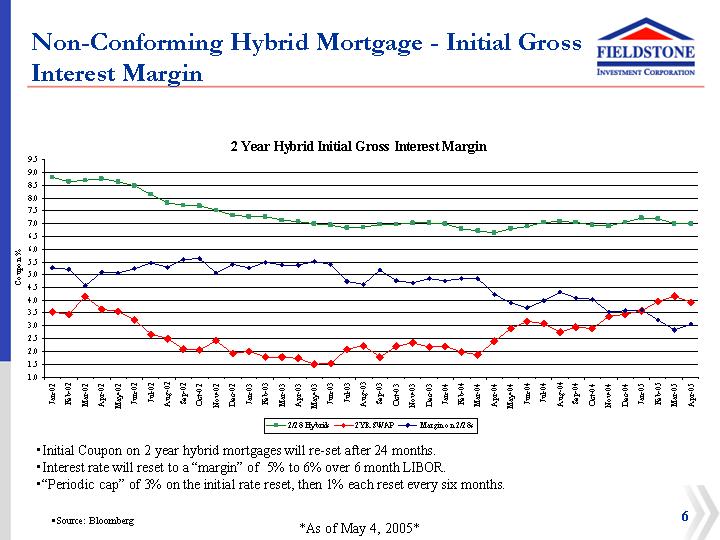

Non-Conforming Hybrid Mortgage - Initial Gross Interest Margin

2 Year Hybrid Initial Gross Interest Margin

[CHART]

• Initial Coupon on 2 year hybrid mortgages will re-set after 24 months.

• Interest rate will reset to a “margin” of 5% to 6% over 6 month LIBOR.

• “Periodic cap” of 3% on the initial rate reset, then 1% each reset every six months. .

• Source: Bloomberg

6

Hybrid Loans Funded with LIBOR Based Debt

Fieldstone Portfolio Hedging Program

Portfolio Weighted Average Swap Rate vs. Forward LIBOR Curve

[CHART]

7

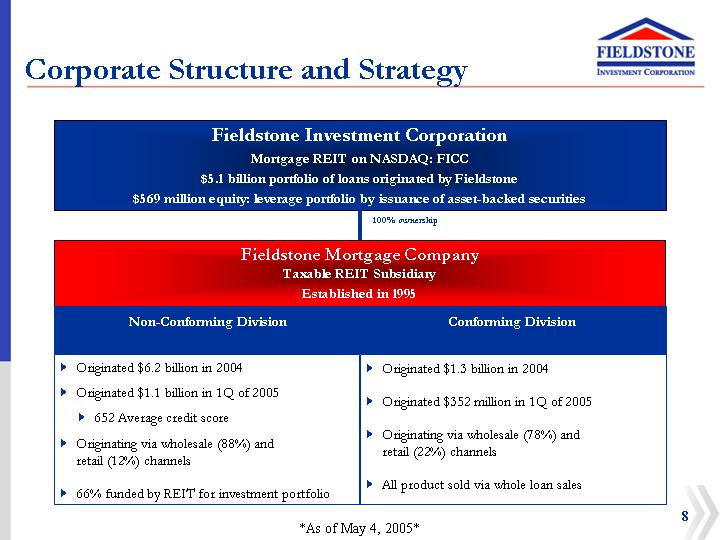

Corporate Structure and Strategy

Fieldstone Investment Corporation

Mortgage REIT on NASDAQ: FICC

$5.1 billion portfolio of loans originated by Fieldstone

$569 million equity: leverage portfolio by issuance of asset-backed securities

| 100% ownership |

Fieldstone Mortgage Company

Taxable REIT Subsidiary

Established in 1995

Non-Conforming Division |

| Conforming Division |

|

|

|

• Originated $6.2 billion in 2004 |

| • Originated $1.3 billion in 2004 |

|

|

|

• Originated $1.1 billion in 1Q of 2005 |

| • Originated $352 million in 1Q of 2005 |

|

|

|

• 652 Average credit score |

| • Originating via wholesale (78%) and retail (22%) channels |

• Originating via wholesale (88%) and retail (12%) channels |

|

|

|

| • All product sold via whole loan sales |

• 66% funded by REIT for investment portfolio |

|

|

8

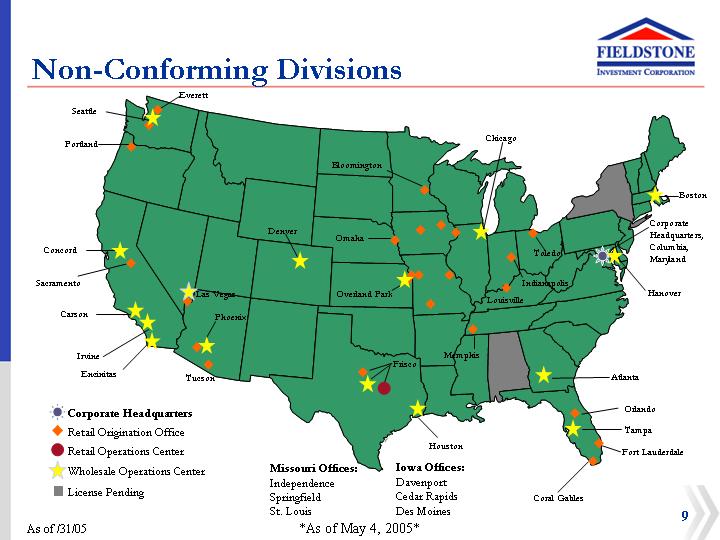

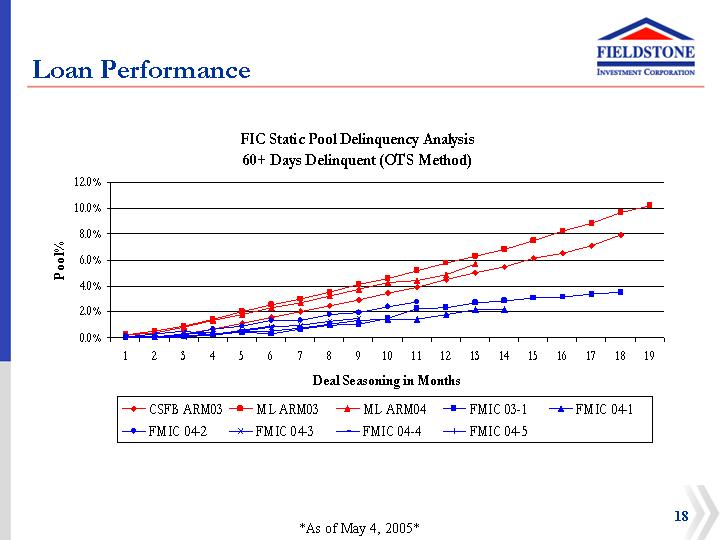

Non-Conforming Divisions

[GRAPHIC]

| Missouri Offices: | Iowa Offices: |

| Independence | Davenport |

| Springfield | Cedar Rapids |

| St. Louis | Des Moines |

9

Portfolio Strategy

• Originate high quality non-conforming ARM loans for REIT portfolio

• 2/28 hybrid ARMs primarily

• 651 average credit score

• Interest only 2/28 ARM loans, fully amortize after five years

• Reduced documentation and higher LTV at higher average credit score

• Finance portfolio with long-term securitization debt

• On-balance sheet financing

• No “gain on sale” non-cash gains on securitization

• Committed financing with strong asset-liability management

• Retain Fieldstone loans to assure quality and minimize cost basis

• Current Target portfolio size of $6 to $7 billion

11

Fieldstone Portfolio as of March 31, 2005

Collateral Characteristics

Average Credit Score |

| 651 |

| |

|

|

|

| |

Hybrid Arms |

| 99.4 | % | |

|

|

|

| |

Average Coupon |

| 6.9 | % | |

|

|

|

| |

Gross Margin |

| 5.7 | % | |

|

|

|

| |

Prepayment Fee Coverage |

| 86.8 | % | |

|

|

|

| |

Full Income Documentation |

| 46.3 | % | |

|

|

|

| |

Interest Only Loans |

| 61.3 | % | |

|

|

|

| |

Weighted Average LTV |

| 82.1 | % | |

|

|

|

| |

-LTV>90% |

| 3.3 | % | |

|

|

|

| |

Weighted Average CLTV |

| 92.5 | % | |

|

|

|

| |

State Concentration-California |

| 45.8 | % | |

|

|

|

| |

Average Loan Size |

| $ | 193,874 |

|

|

|

|

| |

-Avg. Property Value |

| $ | 240,142 |

|

|

|

|

| |

-Avg. Property Value-CA |

| $ | 356,470 |

|

Investment Portfolio Growth ($ millions)

[CHART]

Credit Score Distribution

[CHART]

12

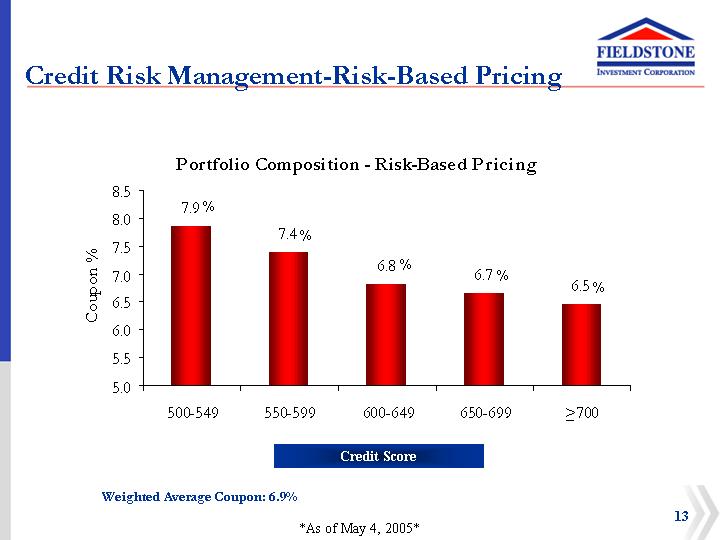

Credit Risk Management-Risk-Based Pricing

Portfolio Composition - Risk-Based Pricing

[CHART]

Weighted Average Coupon: 6.9%

13

Underwriting Philosophy

“Hardest place to deliver a bad loan”

• Rigorous appraisal review

• Detailed checklist

• AVM screening

• Reviews:

• Enhanced desk reviews

• National firm drive-by or 2nd full

• Borrower benefit analysis in writing on refinances

• Fieldscore and loan origination system edits

• Investigative underwriting in regional centers

• Quality Control department re-underwritings

• Investor and rating agency due diligence

• Results:

• Improved credit performance

• Predatory lending prevention

• Fraud deterrence due to process and reputation

14

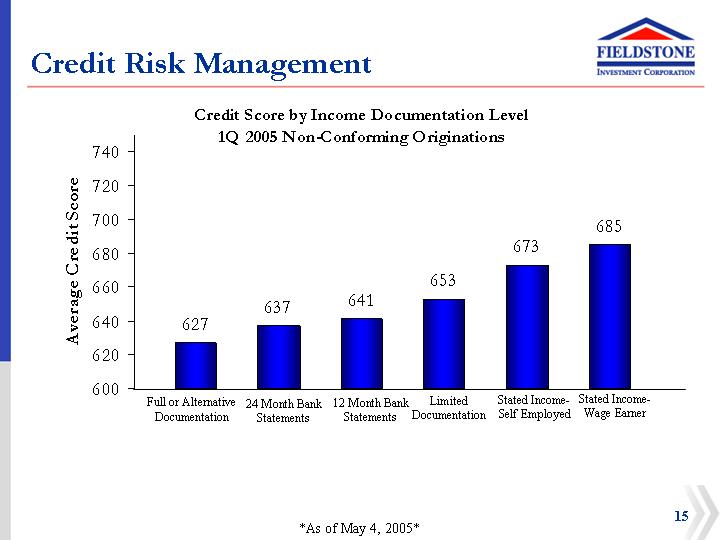

Credit Risk Management

Credit Score by Income Documentation Level

1Q 2005 Non-Conforming Originations

[CHART]

15

Servicing Strategy

• Fieldstone performs key loan set-up and initial quality control functions on all loans

• Highly rated sub-servicer: Chase Home Finance, LLC

• Fitch: RPS1- and RSS1- (primarily subprime and special servicing, respectively)

• Moody’s: SQ1 (subprime servicing)

• S&P: “STRONG” and on its select servicer list

• Wells Fargo Bank as:

• Master Servicer

• Bond Administrative Agent

• Servicer Oversight

• Ultimately, Fieldstone will look to build or acquire a significant servicing capacity

16

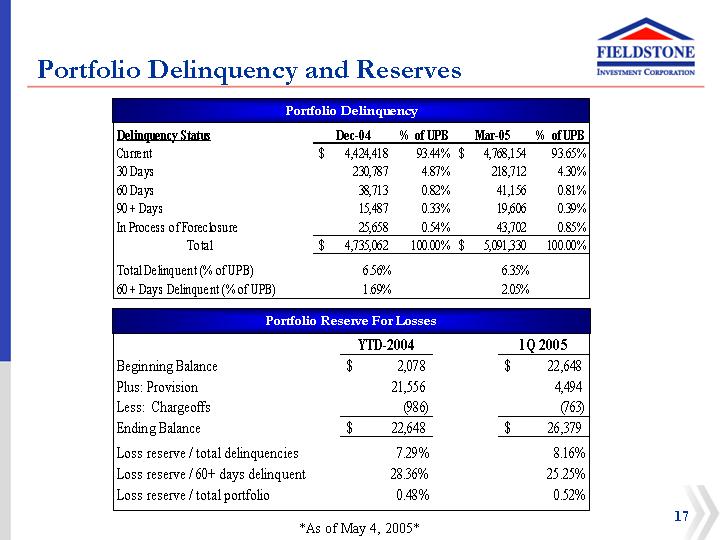

Portfolio Delinquency and Reserves

Portfolio Delinquency

Delinquency Status |

| Dec-04 |

| % of UPB |

| Mar-05 |

| % of UPB |

| ||

Current |

| $ | 4,424,418 |

| 93.44 | % | $ | 4,768,154 |

| 93.65 | % |

30 Days |

| 230,787 |

| 4.87 | % | 218,712 |

| 4.30 | % | ||

60 Days |

| 38,713 |

| 0.82 | % | 41,156 |

| 0.81 | % | ||

90 + Days |

| 15,487 |

| 0.33 | % | 19,606 |

| 0.39 | % | ||

In Process of Foreclosure |

| 25,658 |

| 0.54 | % | 43,702 |

| 0.85 | % | ||

Total |

| $ | 4,735,062 |

| 100.00 | % | $ | 5,091,330 |

| 100.00 | % |

|

|

|

|

|

|

|

|

|

| ||

Total Delinquent (% of UPB) |

| 6.56 | % |

|

| 6.35 | % |

|

| ||

60 + Days Delinquent (% of UPB) |

| 1.69 | % |

|

| 2.05 | % |

|

| ||

Portfolio Reserve For Losses

|

| YTD-2004 |

| 1Q 2005 |

| ||

Beginning Balance |

| $ | 2,078 |

| $ | 22,648 |

|

Plus: Provision |

| 21,556 |

| 4,494 |

| ||

Less: Chargeoffs |

| (986 | ) | (763 | ) | ||

Ending Balance |

| $ | 22,648 |

| $ | 26,379 |

|

|

|

|

|

|

| ||

Loss reserve / total delinquencies |

| 7.29 | % | 8.16 | % | ||

Loss reserve / 60+ days delinquent |

| 28.36 | % | 25.25 | % | ||

Loss reserve / total portfolio |

| 0.48 | % | 0.52 | % | ||

17

Liquidity Risk Management

• Finance loans prior to securitization or sale with a diverse group of Wall Street and bank lenders under $2.0 billion of committed lines

• Use mortgage-backed securities (MBS) to finance REIT portfolio

• Provides long-term financing for portfolio without margin calls

• MBS market highly liquid

• Structure securitizations to cash flow NIM from month one

• Not issuing “NIM” securities

• Focus on issuing bonds rated BBB or higher

• Not reliant upon selling low rated and less liquid (BBB- or BB) bonds

• Highly efficient - weighted average bond spread of LIBOR + 35 bps on 2005-1 (to call)

[GRAPHIC]

20

Taxable Income

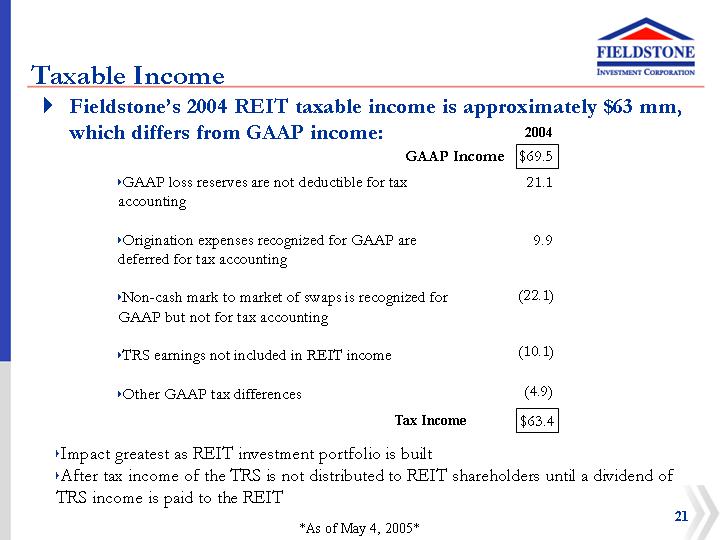

• Fieldstone’s 2004 REIT taxable income is approximately $63 mm, which differs from GAAP income:

|

| 2004 |

| |

GAAP Income |

| $ | 69.5 |

|

|

|

|

|

|

• GAAP loss reserves are not deductible for tax accounting |

| 21.1 |

| |

|

|

|

| |

• Origination expenses recognized for GAAP are deferred for tax accounting |

| 9.9 |

| |

|

|

|

| |

• Non-cash mark to market of swaps is recognized for GAAP but not for tax accounting |

| (22.1 | ) | |

|

|

|

| |

• TRS earnings not included in REIT income |

| (10.1 | ) | |

|

|

|

| |

• Other GAAP tax differences |

| (4.9 | ) | |

|

|

|

| |

Tax Income |

| $ | 63.4 |

|

• Impact greatest as REIT investment portfolio is built

• After tax income of the TRS is not distributed to REIT shareholders until a dividend of TRS income is paid to the REIT

21

REIT Dividends

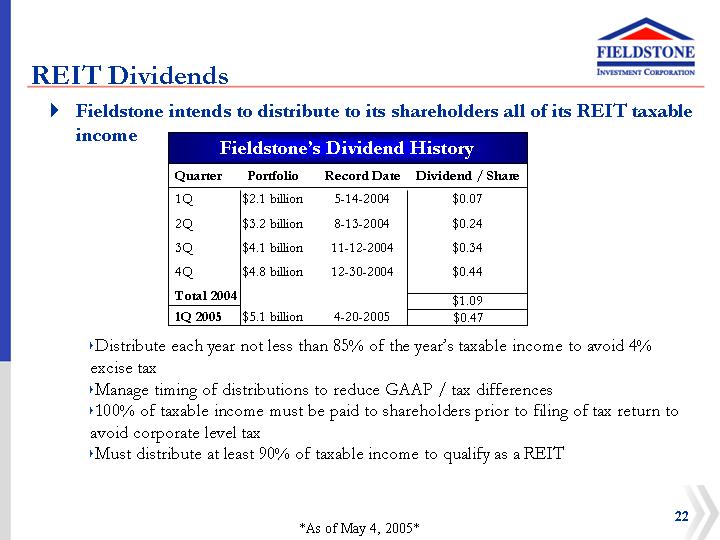

• Fieldstone intends to distribute to its shareholders all of its REIT taxable income

Fieldstone’s Dividend History

Quarter |

| Portfolio |

| Record Date |

| Dividend / Share |

| ||

1Q |

| $ | 2.1 billion |

| 5-14-2004 |

| $ | 0.07 |

|

|

|

|

|

|

|

|

|

|

|

2Q |

| $ | 3.2 billion |

| 8-13-2004 |

| $ | 0.24 |

|

|

|

|

|

|

|

|

|

|

|

3Q |

| $ | 4.1 billion |

| 11-12-2004 |

| $ | 0.34 |

|

|

|

|

|

|

|

|

|

|

|

4Q |

| $ | 4.8 billion |

| 12-30-2004 |

| $ | 0.44 |

|

|

|

|

|

|

|

|

| ||

Total 2004 |

|

|

|

|

| $ | 1.09 |

| |

1Q 2005 |

| $ | 5.1 billion |

| 4-20-2005 |

| $ | 0.47 |

|

• Distribute each year not less than 85% of the year’s taxable income to avoid 4% excise tax

• Manage timing of distributions to reduce GAAP / tax differences

• 100% of taxable income must be paid to shareholders prior to filing of tax return to avoid corporate level tax

• Must distribute at least 90% of taxable income to qualify as a REIT

22

Fieldstone’s Culture and Strategy

• Each employee takes personal accountability for the success of the Team

• Focus on long term relationships with market professionals where “value added” enables rational pricing and loan quality

• Fully integrated originator of and investor in quality mortgage loans in a tax-advantaged structure

• Experienced management team focused on:

• Quality of loans and operations

• Portfolio structured for stability in multiple rate environments

• Long-term value

23