Table of Contents

As filed with the Securities and Exchange Commission on July 1, 2004

Registration No. 333-112764

SECURITIES AND EXCHANGE COMMISSION

Washington D.C. 20549

Amendment NO. 3

to

FORM F-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

| Stratus Technologies, Inc. | Stratus Technologies International, S.à r.l. | |

| (Exact Name of Registrant as Specified in its Charter) | (Exact Name of Registrant as Specified in its Charter) |

| Delaware | 04-3453241 | 3571 | Luxembourg | 98-0359581 | 3571 | |||||

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | (Primary Standard Industrial Classification Code Number) | (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | (Primary Standard Industrial Classification Code Number) | |||||

111 Powdermill Road Maynard, Massachusetts 01754 (978) 461-7000 | 123, Avenue de X Septembre L-2551 Luxembourg 352 4242 69 10 | |

(Address and telephone number of Registrant’s principal executive offices) | (Address and telephone number of Registrant’s principal executive offices) | |

CSC Corporation Service Company 1133 Avenue of the Americas, Suite 3100 New York, New York 10036 (800) 221-0770 | National Registered Agents, Inc. 875 Avenue of the Americas, Suite 501 New York, New York 10001 (800) 767-1553 | |

(Name, address and telephone number of agent for service) | (Name, address and telephone number of agent for service) | |

See Table of Additional Registrants Below

copies to:

Steven Shoemate, Esq.

Joerg Esdorn, Esq.

Gibson, Dunn & Crutcher LLP

200 Park Avenue

New York, New York 10166

(212) 351-4000

APPROXIMATE DATE OF COMMENCEMENT OF PROPOSED SALE TO THE PUBLIC: As promptly as practicable after the effective date of this Registration Statement.

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number for the same offering.

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.

Table of Contents

Calculation of Registration Fee

| Title of each class of securities to be registered | Amount to be registered | Proposed maximum offering price per unit | Proposed maximum aggregate offering price (1) | Amount of registration fee | |||||||||

10.375% Senior Notes due 2008 | $ | 170,000,000 | 100 | % | $ | 170,000,000 | $ | 21,539 | |||||

Guarantees of 10.375% Senior Notes due 2008 | $ | 170,000,000 | — | — | (2 | ) | |||||||

| (1) | Estimated pursuant to Rule 457(f) under the Securities Act of 1933, as amended, solely for the purpose of calculating the registration fee. |

| (2) | Pursuant to Rule 457(n) under the Securities Act of 1933, as amended, no registration fee is required with respect to the Guarantees. |

The Registrants hereby amend this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Additional Registrants

Exact name of Additional Registrants ** | Jurisdiction of Incorporation | I.R.S. Employer Identification No. | Address and telephone number | |||

Stratus Equity S.à r.l. | Luxembourg | None | 123, Avenue de X Septembre L-2551 Luxembourg +35 242 45 6910 | |||

Stratus Technologies Bermuda Ltd. | Bermuda | 98-0412966 | Reid Hall, 3 Reid Street Hamilton HM 11, Bermuda (441) 295-2208 | |||

Stratus Technologies Ireland Limited | Ireland | 98-0368193 | College Business & Technology Park Blanchardstown Road North Blanchardstown, Dublin 15, Ireland +353 1811 6600 | |||

Stratus Research and Development Limited | Ireland | None | College Business & Technology Park Blanchardstown Road North Blanchardstown, Dublin 15, Ireland +353 1811 6600 | |||

SRA Technologies Cyprus Limited | Cyprus | None | Vyronos Avenue 36, Nicosia, Cyprus +357 25 36 25 80 | |||

Cemprus Technologies, Inc. | Delaware | 57-1146987 | 111 Powdermill Road Maynard, MA 01754 (978) 461-7000 | |||

Cemprus, LLC | Delaware | 95-4891291 | 111 Powdermill Road Maynard, MA 01754 (978) 461-7000 |

| ** | The address for service for Stratus Equity S.à r.l., Stratus Technologies Bermuda Ltd., Stratus Technologies Ireland Limited, Stratus Research and Development Limited and SRA Technologies Cyprus Limited is National Registered Agents, Inc., 875 Avenue of the Americas, Suite 501, New York, New York 10001. The address for service of Cemprus Technologies, Inc. and Cemprus, LLC is CSC Corporation Service Company, 1133 Avenue of the Americas, Suite 3100, New York, New York 10036. The primary standard industrial classification code number for each of the additional registrants is 3571. |

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities nor a solicitation of an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JULY 1, 2004

PRELIMINARY PROSPECTUS

Stratus Technologies, Inc.

OFFER TO EXCHANGE

All Outstanding $170,000,000 in 10.375% Senior Notes due 2008

for

New 10.375% Senior Notes due 2008

Which Have Been Registered Under the Securities Act of 1933

Fully and Unconditionally Guaranteed as to payment of principal and interest by

Stratus Technologies International, S.à r.l.

Stratus Equity S.à r.l.

Stratus Technologies Bermuda Ltd.

Stratus Technologies Ireland Limited

Stratus Research and Development Limited

SRA Technologies Cyprus Limited

Cemprus Technologies, Inc.

Cemprus, LLC

This Exchange Offer will expire at 5:00 p.m., New York City time, on [ ], 2004, unless extended.

Terms of the Exchange Offer:

| • | We will exchange all Outstanding Notes that are validly tendered and not withdrawn prior to the expiration of the Exchange Offer. |

| • | You may withdraw tendered Outstanding Notes at any time prior to the expiration of the Exchange Offer. |

| • | The exchange of Outstanding Notes for New Notes will not be a taxable exchange for United States federal income tax purposes. |

| • | The terms of the New Notes to be issued are substantially identical to the terms of the Outstanding Notes, except that transfer restrictions, registration rights and additional interest provisions relating to the Outstanding Notes do not apply. |

| • | Outstanding Notes tendered in the Exchange Offer must be in denominations of the principal amount of $1,000 and any integral multiple of $1,000. |

| • | Each broker-dealer that receives New Notes for its own account pursuant to the Exchange Offer must acknowledge that it will deliver a prospectus in connection with any resale of such New Notes. We will make the prospectus available to any broker-dealer for use in connection with any resale for a period of 90 days after the expiration date of the Exchange Offer. The letter of transmittal states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an “underwriter” within the meaning of the Securities Act of 1933, as amended. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of New Notes received in exchange for Outstanding Notes where such Outstanding Notes were acquired by such broker-dealer as a result of market-making activities or other trading activities. See “Plan of Distribution”. |

| • | There is no existing market for the New Notes to be issued, and we do not intend to apply for their listing on any securities exchange. |

| • | As of April 25, 2004, the New Notes would have ranked equal in right of payment to $9.5 million of unsecured senior indebtedness. |

| • | We have the option to redeem all or a portion of the New Notes at any time on or after December 1, 2006 at the redemption prices set forth in this prospectus. Before December 1, 2006, we have the option to redeem up to 35% of the aggregate principal amount of the New Notes at the redemption prices set forth in this prospectus with the proceeds of certain equity offerings. Before December 1, 2006, we also have the option to redeem all and not less than all of the New Notes in connection with a change in control. We may redeem the New Notes in the event of certain developments affecting taxation. See the section entitled “Description of New Notes—Optional Redemption” beginning on page 95 for more information on the redemption provisions applicable to the New Notes. If we undergo certain changes of control, you may require us to repurchase all or a part of the New Notes at a redemption price equal to 101% of their principal amount plus accrued and unpaid interest to the repurchase date. See the section entitled “Description of New Notes—Repurchase at the Option of Holders” beginning on page 96 for more information on the repurchase provisions applicable to the New Notes. |

| • | Pursuant to the terms of the indenture, we may issue additional notes. |

See the “Description of New Notes” section beginning on page 92 for more information about the New Notes to be issued in this Exchange Offer.

This investment involves risks. See the section entitled “Risk Factors” beginning on page 17 for a discussion of the risks that you should consider prior to tendering your Outstanding Notes for exchange.

Neither the Securities and Exchange Commission nor any state securities and exchange commission has approved or disapproved these securities or passed upon the adequacy or the accuracy of this prospectus. Any representation to the contrary is a criminal offense.

Prospectus dated [ , ].

Table of Contents

| Page | ||

| 1 | ||

| 17 | ||

| 34 | ||

| 35 | ||

| 35 | ||

| 45 | ||

| 46 | ||

| 47 | ||

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 48 | |

| 69 | ||

| 79 | ||

| 85 | ||

| 87 | ||

| 89 | ||

| 91 | ||

| 92 | ||

Material United States Federal Income and Estate Tax Considerations | 136 | |

| 141 | ||

| 142 | ||

| 146 | ||

| 146 | ||

| 146 | ||

| F-1 |

This prospectus incorporates important business and financial information about us that is not included in or delivered with the document. This information is available to you without charge at your oral or written request to Stratus Technologies, Inc., 111 Powdermill Road, Maynard, Massachusetts 01754. Our telephone number at that address is (978) 461-7000.To obtain timely delivery, you must request this information no later than [ ], 2004, which is five business days before the date you must make your investment decision.

i

Table of Contents

The following summary contains material information about us and this Exchange Offer, but may not contain all the information that is important to you. We encourage you to read this entire prospectus.

Stratus Technologies Group, S.A., which we refer to as “Holdings,” is a company formed under the laws of Luxembourg. Holdings is neither an issuer nor a guarantor of the New Notes described in this prospectus.

Stratus Technologies International, S.à r.l., the parent guarantor of the New Notes, is a company formed under the laws of Luxembourg and is a wholly-owned subsidiary of Holdings. Stratus Technologies, Inc., the issuer of the New Notes, is a Delaware corporation and a wholly-owned subsidiary of Stratus Technologies International, S.à r.l. Except as otherwise expressly set forth in this prospectus, the terms “we,” “us,” “our” and “Stratus” refer to Stratus Technologies International, S.à r.l., its subsidiaries (including Stratus Technologies, Inc.) and our predecessor company, Stratus Computer, Inc. References in this prospectus to our fiscal years are to the twelve months ended February 25, 2001, February 24, 2002, February 23, 2003 and February 29, 2004.

Our Company

We are a global provider of fault-tolerant computer servers, technologies and services, with more than 20 years of experience focused in the fault-tolerant server market. Our servers provide high levels of reliability relative to the server industry, delivering 99.999% uptime or better (equivalent to less than 5 minutes of downtime annually in continuous operation). Our customers, who include some of the most recognizable companies in the world, purchase Stratus® servers and support services for their critical computer-based operations that are required to be continuously available for the proper functioning of their businesses. With our latest server line introduced in June 2001, we are broadening our customer base considerably in the high-availability server market, which is expected to grow rapidly, by offering the superior performance of continuous availability combined with operational simplicity at cost-effective prices.

We provide our products and services through subsidiaries, distributors, value-added resellers and systems integrators around the world, with approximately half of our revenue in each of the last three fiscal years generated by sales outside the United States. As of April 25, 2004, we employed approximately 900 people globally.

We currently provide two lines of fault-tolerant servers, the Continuum® system family and the ftServer® system family, each of which is supported by a technologically advanced worldwide service offering.

| • | Continuum System Family: The Continuum family of products, introduced in 1995, represents a successful history of delivering fault tolerance and continuous availability. The family is composed of mid-range and high-end fault-tolerant servers that run our proprietary VOS and FTX® operating systems and the Stratus-modified Hewlett-Packard UNIX® (HP-UX®) operating system. Approximately 1,800 Continuum servers are deployed throughout the world at over 600 customer sites, supporting mission-critical applications in the securities, banking, credit card, transportation, gaming and other industries, and in government. Examples of these applications include telecommunications control, funds transfer, securities trading, bank ATMs, enhanced 9-1-1 computer-aided dispatch and other interactive applications where systems availability and data integrity are critical requirements. List prices of Continuum servers currently range from approximately $125,000 to $1,200,000. |

| • | ftServer System Family: First introduced in June 2001, the ftServer family established a new category of server product: Intel® processor-based hardware fault-tolerant servers for Microsoft® Windows® computing environments. The ftServer system family represents a new, simplified and cost-effective implementation of our fault-tolerant technology that now targets the rapidly-growing high-availability |

1

Table of Contents

Windows- and Linux®-based server markets. Since the beginning of fiscal 2000, we have invested $264.2 million in research and development, primarily related to the development and enhancement of our ftServer systems. As a result, we hold a highly differentiated technology and product position in this segment of the server market. We currently are the only server manufacturer with hardware fault-tolerant server technology for Windows- and Linux-based operating environments. Since June 2001, approximately 1,000 customers have purchased ftServer systems, over 50% of whom were first-time Stratus customers. List prices of ftServer systems currently range from approximately $15,000 to $150,000. |

| • | Worldwide Service: Our service offering provides for remote monitoring, problem diagnosis and product repair, and is integral to the Stratus value proposition. Given the critical nature of the applications our servers support, the majority of our customers purchase service contracts with our server products. In fiscal 2004, over 98% of Continuum server sales and 78% of ftServer system sales included service contracts. In addition, service contract retention rates over the past three fiscal years have exceeded 90%. As a result of these high attach and retention rates and the evergreen nature of the service contracts, the revenue generated by our service business has historically been predictable and stable. As of February 29, 2004, our 877 service customers around the world had approximately 3,200 servers under service contract. |

We are currently a privately-held company, the result of the acquisition of the enterprise computing business of Stratus Computer, Inc. from Ascend Technologies, Inc. in February, 1999. Our principal shareholders consist of affiliates of Investcorp; an affiliate of MidOcean Partners LP; affiliates of Intel Corporation; and our management and employees. Our website address iswww.stratus.com. Information on our website does not constitute part of this prospectus.

Industry Overview

Our fault-tolerant systems compete in the high-availability server market, a rapidly-growing category of the estimated $51.4 billion global server market in 2004. The high-availability server market is expected to represent an estimated $6.5 billion share of the global server market in 2004, and is projected to grow at a 15.7% compound annual growth rate, or CAGR, through 2007 compared with a 4.2% CAGR for the market as a whole. The high-availability server market includes segments for servers that run Windows, Linux, UNIX and a number of other proprietary operating systems. Our ftServer product line targets the fastest growing segments, Windows and Linux, the combination of which we project, based on our market and industry research, to grow from $1.4 billion in 2004 to $4.5 billion in 2007, representing a 46.2% CAGR.

Our Competitive Strengths

Loyal and Diversified Customer Base. As the basis for our historically stable and recurring service revenue, our loyal customer base is one of our greatest assets. Our customer base is well-diversified, with no customer accounting for more than 8.3% of service revenue or more than 6.2% of product revenue for the fiscal year ended February 29, 2004. As of February 29, 2004, our customers had approximately 3,200 Stratus servers under our maintenance contracts, with the average Continuum server service contract having been in place for 6.1 years. Over the last three fiscal years, we have had approximately 94% service contract retention rate for our Continuum systems. We believe both the high retention rate for our service contracts and the low levels of attrition in our installed base are strong testaments to the loyalty of our customers and the high value of our services.

Compelling Value Proposition. We track and disclose the availability levels delivered by our Continuum and ftServer products under service contract and are currently achieving over 99.999% uptime for all such

2

Table of Contents

servers. This level of uptime can provide substantial cost savings to our customers. Through the introduction of the ftServer system, we have made 99.999% uptime accessible to a much broader range of customers. Out of the box, an ftServer model will run Windows 2000 Server applications unmodified, integrate quickly into the user’s IT infrastructure, and require little or no incremental IT staff support for ongoing operation, system management or service. As a result, we believe the ftServer system family offers a compelling value proposition by providing extremely high levels of reliability combined with operational simplicity in a cost-effective manner.

Proactive and Highly Automated Service. Our service technology allows us to remotely detect and resolve problems before they cause system downtime. We believe that the integrated “call home” remote support feature of our architecture allows us to run our service operations with significantly fewer technical field representatives than are used by our competitors. In addition, this proactive model helps our customers run our products with little or no incremental IT staff support. Our service offering is an integral part of our value proposition.

Differentiating Technology. Every Stratus system includes Continuous Processing® features that aim to prevent, rather than simply recover from, unplanned downtime. Preventing downtime differentiates our systems from traditional servers and high-availability clusters (which use multiple servers to recover after one of the servers in the cluster has failed).

Extensive Experience and Expertise. We have more than two decades of field-proven experience in supplying continuously available fault-tolerant systems and services. We believe our focus and expertise in fault tolerance has helped position us to succeed in the continuous availability and high-availability server markets. Our top six senior managers have an average of over twenty-five years of experience in the high technology industry.

Efficient Cost Structure. We are focused on controlling costs to maximize the profitability and scalability of our business. We seek to minimize our fixed manufacturing costs, while achieving superior quality, by outsourcing nearly all manufacturing of new Continuum and ftServer systems. Outsourcing also affords us a high degree of scalability, in that we can quickly ramp up production when necessary without requiring significant additional capital investment. Furthermore, by partnering with resellers, we believe that our sales channels are also highly scalable.

Our Business Strategy

Our strategy is to expand our market share beyond our historical base of our proprietary servers into the faster-growing Windows- and Linux-based server market, while maintaining the historically high attach and retention rates of our service programs. We have developed the ftServer product family that delivers very high reliability at competitive prices, enabling us to offer AL4 fault-tolerant servers at AL2-AL3 prices. As we grow the ftServer system business, we also intend to offer upgrades to our Continuum system customers, and begin to upgrade them over time to an Intel-based platform.

2004 Recapitalization

On November 18, 2003, we sold $170 million aggregate principal amount of the Outstanding Notes as part of a recapitalization involving Stratus, Holdings and certain of our affiliates. In connection with the recapitalization, which we refer to as the 2004 Recapitalization, we completed the following transactions:

Note Offering. We sold $170.0 million aggregate principal amount of Outstanding Notes.

3

Table of Contents

Closing of New Credit Facility. We entered into a new $30.0 million senior secured revolving credit facility, which we refer to as the New Credit Facility. See “Description of Other Indebtedness—New Credit Facility”.

Repayment of Existing Indebtedness. We repaid approximately $96.2 million of outstanding senior indebtedness and related fees under our senior secured credit agreement with JPMorgan Chase Bank as a lender and as the administrative agent for the other lenders, which credit agreement we refer to as the Former Credit Facility.

Purchase of Holdings Preference Shares. Stratus Technologies Bermuda Ltd. purchased 4,937,835 outstanding Series A Preference Shares of Holdings from Investcorp Stratus Limited Partnership, MidOcean Capital Partners Europe, L.P. and Intel Atlantic, Inc. (collectively the “Selling Preferred Holders”), at a price per share of $11.89, for an aggregate purchase price of $58.7 million.

Purchase of Holdings Ordinary Shares. Stratus Technologies Bermuda Ltd. purchased 430,634 outstanding ordinary shares of Holdings from current holders of ordinary shares, including members of Holdings’ senior management, other current employees and other shareholders, at a price per share of $5.48, for an aggregate purchase price of $2.4 million. Each holder of ordinary shares had the right to sell 15.4% of its ordinary shares in Holdings. As a result, management and other current employees had the right to sell ordinary shares for an aggregate of $1.2 million. The members of the Investcorp Group determined not to exercise this right with respect to their ordinary shares. We believe that payment of $5.48 per ordinary share represented a premium over the estimated fair value of the ordinary shares as of November 19, 2003, the date the offer to sell ordinary shares was made to holders. The offer to sell ordinary shares expired on December 17, 2003, and the cash settlement to those participating was made in December 2003. We believe that it was in our best interest to make this offer in order to assure that holders of our ordinary shares were treated fairly, given the fact that the Selling Preferred Holders were given the opportunity to collectively sell 15.4% of their holdings of ordinary share equivalents at $5.48 per ordinary share equivalent.

Cancellation of Options to Purchase Ordinary Shares. We cancelled vested stock options to purchase ordinary shares of Holdings held by our current employees, in exchange for an amount per option equal to the difference between $5.48 and the exercise price of the option, for an aggregate of $3.7 million. Each employee who owned vested stock options as of October 24, 2003 and who remained an employee through December 17, 2003 (the end of the option cancellation offer period) had the right to exchange 15.4% of his or her vested options, provided that the aggregate amount we agreed to spend for the cancellation of vested stock options would not exceed $3.8 million. The cash settlement of options to purchase ordinary shares was made in December 2003.

For additional information about the 2004 Recapitalization, see “Use of Proceeds.”

New Credit Facility

On November 18, 2003, we entered into the New Credit Facility with a syndicate of lenders, which provides Stratus Technologies, Inc. with up to $30.0 million of revolving credit commitments, subject to borrowing base limitations. For a summary of the terms of the New Credit Facility, see “Description of Other Indebtedness—New Credit Facility.”

Principal Stockholders

As of April 25, 2004, Investcorp Stratus Limited Partnership, Stratus Holdings Limited and New Stratus Investments Limited (collectively referred to in this prospectus as the “Investcorp Group”) collectively beneficially owned 44.2% of the ordinary shares (on an as-converted basis), 2.4% of the outstanding Series A Preference Shares, 88.4% of the outstanding Series B Preference Shares, 54.1% of the total voting power and

4

Table of Contents

37.3% of the fully-diluted common equity of Holdings. Investcorp Stratus Limited Partnership, Stratus Holdings Limited and New Stratus Investments Limited are controlled, directly or indirectly, by affiliates of the international investment firm Investcorp Bank B.S.C., referred to herein as “Investcorp”. Six of the directors of Holdings, Messrs. Egan, Stadler, Marquis, Haegg, Tully and McGregor-Smith, are employees of Investcorp or one or more of its wholly-owned subsidiaries. As a result of these relationships, Investcorp may be deemed to substantially control our management and policies, although such control is not exercised on a day-to-day basis. See “Certain Transactions” and “Equity Ownership.”

As of April 25, 2004, MidOcean Capital Partners Europe, L.P., referred to in this prospectus as “MidOcean Partners,” beneficially owned 23.5% of the ordinary shares (on an as-converted basis), 69.2% of the outstanding Series A Preference Shares, 8.0% of the outstanding Series B Preference Shares, 28.8% of the total voting power and 19.9% of the fully-diluted common equity of Holdings. Two of the directors of Holdings, Messrs. Sharp and Billings, are employees of MidOcean Partners. As a result of these relationships, MidOcean Partners has consent rights over certain of our actions and policies. See “Equity Ownership,” “Certain Transactions” and “Description of Preference Shares.”

As of April 25, 2004, Intel Capital Corp. and Intel Atlantic, Inc. collectively beneficially owned 9.7% of the ordinary shares (on an as-converted basis), 28.4% of the outstanding Series A Preference Shares, 3.6% of the outstanding Series B Preference Shares, 11.9% of the total voting power of Holdings and 8.2% of the fully-diluted common equity of Holdings. As a result of this ownership, Intel Capital Corp. and Intel Atlantic, Inc have consent rights over certain of our actions and policies. See “Equity Ownership,” “Certain Transactions” and “Description of Preference Shares.”

5

Table of Contents

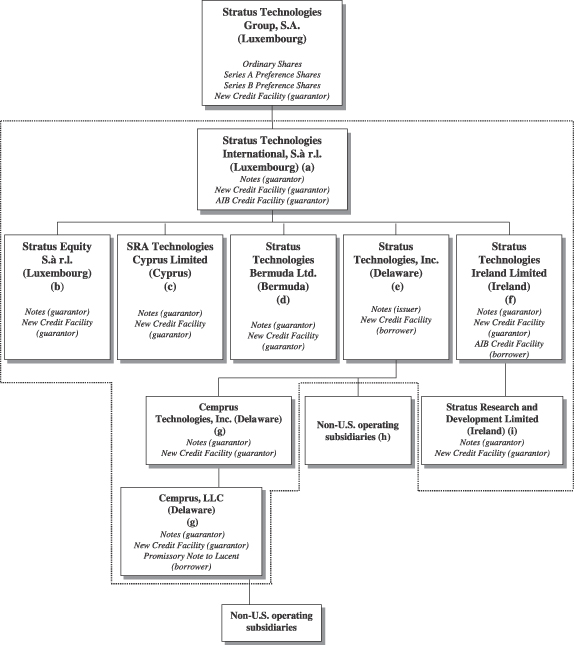

Our Structure

Holdings is the parent company of a group of consolidated companies. The diagram below contains a general depiction of the organizational structure of Holdings and its subsidiaries. It does not present a complete representation of our organizational structure. The issuer and the guarantors of the New Notes are shown within the dotted line.

6

Table of Contents

For more information on the Series A Preference Shares and Series B Preference Shares of Stratus Technologies Group, S.A., see “Description of Preference Shares.” For more information on the New Notes, see “Description of New Notes.” For more information on the $30.0 million New Credit Facility, the €7.6 million (approximately $9.6 million) AIB Credit Facility and the $9.5 million Promissory Note to Lucent, see “Description of Other Indebtedness.”

Notes to Organizational Diagram:

| (a) | Stratus Technologies International, S.à r.l., is a Luxembourg entity with a Swiss branch that previously provided financing to Stratus entities via intercompany loans some of which remain outstanding. |

| (b) | Stratus Equity S.à r.l. holds capital stock in Stratus Technologies Group, S.A., as treasury shares. |

| (c) | SRA Technologies Cyprus Limited licenses product and customer service intellectual property from Stratus Technologies Bermuda Ltd. and then sub-licenses the intellectual property to Stratus Technologies Ireland Limited. |

| (d) | Stratus Technologies Bermuda Ltd. owns all Stratus product and customer service intellectual property and licenses such intellectual property to SRA Technologies Cyprus Limited and unrelated third parties. |

| (e) | Stratus Technologies, Inc. sells the Stratus products it purchases from Stratus Technologies Ireland Limited to customers in the U.S. Stratus Technologies, Inc. also provides marketing and administrative support to affiliates, provides customer service support on behalf of Stratus Technologies Ireland Limited and performs research and development on behalf of Stratus Technologies Bermuda Ltd. |

| (f) | Stratus Technologies Ireland Limited sells Stratus customer service contracts directly to third parties and sells Stratus products to affiliates and third-party distributors. Stratus Technologies Ireland Limited also pays royalties to SRA Technologies Cyprus Limited for the use of Stratus customer service and product intellectual property and performs research and development on behalf of Stratus Technologies Bermuda Ltd. |

| (g) | Cemprus Technologies, Inc. owns the membership interests in Cemprus, LLC, which holds strategic licenses for the telecommunications business. |

| (h) | Stratus Technologies Japan, Inc., a non-U.S. operating subsidiary of Stratus Technologies, Inc., has an overdraft facility of ¥350.0 million (approximately $3.2 million). There were no borrowings outstanding under this facility as of February 29, 2004. See “Description of Other Indebtedness.” |

| (i) | Stratus Research and Development Limited holds certain intellectual property and licenses rights in this intellectual property in return for royalties. |

At February 29, 2004, the total amount of assets of Holdings (on a stand-alone basis) was approximately $164,000 (exclusive of stock of subsidiaries and intercompany receivables). For the fiscal year ended February 29, 2004, Holdings (on a stand-alone basis) generated no revenue.

The non-Guarantor subsidiaries are organized in Australia, Canada, France, Germany, Hong Kong, Italy, Japan, Korea, Mexico, the Netherlands, New Zealand, Singapore, South Africa, Spain and the United Kingdom. Their primary operations involve the distribution of Stratus products sold by Stratus Technologies Ireland Limited and Stratus Technologies, Inc., both in direct sales to end users and to third party resellers. The non-Guarantor subsidiaries also provide related customer service support to end users and resellers, such as installation services and remedial and preventative maintenance. Each non-Guarantor subsidiary focuses its operations in its respective country of organization and, in some cases, in neighboring countries not otherwise served by a Stratus entity or third party reseller. At February 29, 2004, the non-Guarantor subsidiaries held an aggregate of $46.9 million in assets, the main categories of which were cash (11.9%), accounts receivable (45.8%), inventory (11.0%) and property and equipment (11.6%). For the fiscal year ended February 29, 2004, the non-Guarantor subsidiaries generated total revenue of $98.0 million and gross profit of $23.8 million. At February 29, 2004, the non-Guarantor subsidiaries had no short-term indebtedness outstanding.

For certain financial information relating to Stratus Technologies, Inc. and the Guarantors of the New Notes, see note 18 to the consolidated financial statements of Stratus Technologies International, S.à r.l. appearing elsewhere in this prospectus.

7

Table of Contents

Summary of the Exchange Offer

The following is a brief summary of the terms of the Exchange Offer. For a more complete description of the Exchange Offer, see “The Exchange Offer”.

New Notes Offered | $170.0 million aggregate principal amount of 10.375% Senior Notes Due 2008, which have been registered under the Securities Act of 1933, as amended (the “Securities Act”). The terms of the New Notes offered in the Exchange Offer are substantially identical to those of the Outstanding Notes, except that certain transfer restrictions, registration rights and additional interest provisions relating to the Outstanding Notes do not apply to the registered New Notes. See “The Exchange Offer—Purpose of the Exchange Offer” and “Description of New Notes.” | |

Outstanding Notes | $170.0 million aggregate principal amount of 10.375% Senior Notes Due 2008, which were issued on November 18, 2003, in reliance on the exemption from registration set forth in Section 4(2) of the Securities Act. | |

The Exchange Offer | We are offering to issue registered New Notes in exchange for a like principal amount and like denomination of our Outstanding Notes. We are offering to issue these registered New Notes to satisfy our obligations under a registration rights agreement that we entered into with the initial purchasers of the Outstanding Notes when we sold them in a transaction that was exempt from the registration requirements of the Securities Act. You may tender your Outstanding Notes for exchange by following the procedures described under the caption “The Exchange Offer.” | |

Tenders; Expiration Date; Withdrawal | The Exchange Offer will expire at 5:00 p.m., New York City time, on[ ], 2004 unless we extend it. If you decide to exchange your Outstanding Notes for New Notes, you must acknowledge that you are not engaging in, and do not intend to engage in, a distribution of the New Notes. You may withdraw any Outstanding Notes that you tender for exchange at any time prior to[ ], 2004. If we decide for any reason not to accept any Outstanding Notes you have tendered for exchange, those Outstanding Notes will be returned to you without cost promptly after the expiration or termination of the Exchange Offer. Among other reasons, we may decide not to accept Outstanding Notes tendered for exchange if acceptance may be deemed unlawful; there are questions as to the validity of such Outstanding Notes; such Outstanding Notes are not tendered with a properly completed letter of transmittal or agent’s message, are not properly endorsed or otherwise fail to include evidence of authority of the signatory; or such Outstanding Notes are tendered after the expiration of the Exchange Offer. See “The Exchange Offer—Terms of the Exchange Offer” and “The Exchange Offer—Exchange Offer Procedures” for a more complete description of the tender and withdrawal provisions. | |

8

Table of Contents

Conditions to the Exchange Offer | The Exchange Offer is subject to customary conditions, including: | |

Ÿ any federal law, statute, rule or regulation is adopted or enacted which, in our judgment, would reasonably be expected to impair our ability to proceed with the Exchange Offer;

Ÿ any stop order is threatened or in effect with respect to the registration statement of which this prospectus constitutes a part or the qualification of the indenture under the Trust Indenture Act of 1939, as amended;

Ÿ there is a change in the current interpretation by staff of the SEC which permits, subject to certain exceptions, the New Notes issued in the Exchange Offer to be offered for resale, resold and otherwise transferred by holders without compliance with the registration and prospectus delivery provisions of the Securities Act;

Ÿ there is a general suspension of or general limitation on prices for, or trading in, securities on any national exchange or in the over-the-counter market;

Ÿ any governmental agency creates limits that adversely affect our ability to complete the Exchange Offer;

Ÿ there is any declaration of war, armed hostilities or other similar international calamity directly or indirectly involving the United States, or the worsening of any such condition that existed at the time that we commence the Exchange Offer;

Ÿ there is a change or a development involving a prospective change in our and our subsidiaries’ businesses, properties, assets, liabilities, financial condition, operations or results of operations, taken as a whole, that is or may be adverse to us; or

Ÿ we become aware of facts that, in our reasonable judgment, have or may have adverse significance with respect to the value of the Outstanding Notes or the New Notes to be issued in the Exchange Offer. | ||

| We may waive one or more of these conditions (other than those pertaining to enactment of federal law, stop orders or changes in SEC interpretation) in our discretion and consummate the Exchange Offer. See “The Exchange Offer—Conditions to the Exchange Offer.” Other than federal securities laws, we are not subject to federal or state regulatory requirements in connection with the Exchange Offer. | ||

U.S. Federal Income Tax Consequences | Your exchange of Outstanding Notes for New Notes to be issued in the Exchange Offer will not result in any gain or loss to you for U.S. federal income tax purposes. | |

9

Table of Contents

Use of Proceeds | We will not receive any cash proceeds from the Exchange Offer. | |

Exchange Agent | U.S. Bank National Association | |

Consequences of Failure to Exchange Your Outstanding Notes |

Outstanding Notes that are not tendered or that are tendered but not accepted will continue to be subject to the restrictions on transfer that are described in the legend on those Outstanding Notes. In general, you may offer or sell your Outstanding Notes only if they are registered under, or offered or sold under an exemption from, the Securities Act and applicable state securities laws. We, however, will have no further obligation to register the Outstanding Notes. If you do not participate in the Exchange Offer, the liquidity of your Outstanding Notes could be adversely affected. See “The Exchange Offer—Consequences of Failure to Exchange Outstanding Notes.” | |

Consequences of Exchanging Your Outstanding Notes |

Based on interpretations of the staff of the SEC, we believe that you may offer for resale, resell or otherwise transfer the New Notes that we issue in the Exchange Offer without complying with the registration and prospectus delivery requirements of the Securities Act if you: | |||

| • | acquire the New Notes issued in the Exchange Offer in the ordinary course of your business; | |||

| • | are not participating, do not intend to participate, and have no arrangement or undertaking with anyone to participate, in the distribution of the New Notes issued to you in the Exchange Offer; and | |||

| • | are not an “affiliate” of our company as defined in Rule 405 under the Securities Act. | |||

| If any of these conditions are not satisfied and you transfer any New Notes issued to you in the Exchange Offer without delivering a proper prospectus or without qualifying for a registration exemption, you may incur liability under the Securities Act. We will not be responsible for or indemnify you against any liability you may incur. | ||||

| Any broker-dealer that acquires New Notes in the Exchange Offer for its own account in exchange for Outstanding Notes which it acquired through market-making or other trading activities, must acknowledge that it will deliver a prospectus when it resells or transfers any New Notes issued in the Exchange Offer. See “Plan of Distribution” for a description of the prospectus delivery obligations of broker-dealers in the Exchange Offer. | ||||

10

Table of Contents

Summary Description of the New Notes

The following summarized description of the New Notes is subject to a number of important qualifications and exceptions. For additional information on the terms of the New Notes, see “Description of New Notes.”

Issuer | Stratus Technologies, Inc. | |

New Notes | $170.0 million aggregate principal amount of registered 10.375% Senior Notes due 2008. | |

Maturity | December 1, 2008. | |

Interest Rate | 10.375% per year. | |

Interest Payment Dates | June 1 and December 1 of each year, commencing June 1, 2004. | |

Ranking | The New Notes will be our senior unsecured obligations and will rankpari passu in right of payment to our existing senior unsecured indebtedness ($9.5 million as of April 25, 2004) and any of our future senior unsecured indebtedness and senior in right of payment to any of our future subordinated indebtedness. However, the New Notes will be effectively subordinated to all future indebtedness of our subsidiaries that do not guarantee the New Notes. The New Notes also will be effectively junior to our secured indebtedness up to the value of the collateral securing such indebtedness or the amount of such secured indebtedness, whichever is less. As of April 25, 2004, there was approximately $2.7 million outstanding under the AIB Credit Facility (as defined below) and $1.3 million of outstanding letters of credit applied against our $30.0 million New Credit Facility (as defined below). See “Description of Other Indebtedness.” | |

Guarantees | The New Notes will be guaranteed by Stratus Technologies International, S.à r.l., which we refer to as the parent guarantor, and all of its subsidiaries other than its immaterial subsidiaries and foreign subsidiaries of Stratus Technologies, Inc. Each guarantee will rankpari passu in right of payment to all existing and future senior unsecured indebtedness of that guarantor and senior in right of payment to any future subordinated indebtedness of that guarantor. However, the guarantees will be effectively junior to all secured indebtedness of the guarantors up to the value of the collateral securing such indebtedness or the amount of such secured indebtedness, whichever is less. | |

Optional Redemption | We cannot redeem the New Notes until December 1, 2006, except as described below. After December 1, 2006, we may redeem some or all of the New Notes at the redemption prices listed in the “Description of New Notes—Optional Redemption” section of this prospectus, plus accrued interest to the date of such redemption. | |

11

Table of Contents

Optional Redemption After Equity Offerings | At any time before December 1, 2006, on one or more occasions, we may redeem up to 35% of the outstanding principal amount of the New Notes, including any additional New Notes issued in accordance with the provisions of the indenture, with the net cash proceeds of any one or more equity offerings, at a redemption price equal to 110.375% of the principal amount thereof, plus accrued and unpaid interest to the redemption date, so long as at least 65% of the aggregate principal amount of New Notes issued under the indenture, including the principal amount of any additional New Notes, remains outstanding immediately after each such redemption. | |||

Optional Redemption After Change of Control |

At any time before December 1, 2006, if a Change of Control occurs, we can redeem all, but not less than all, of the New Notes if we pay holders of the New Notes a redemption price of 100% of the face amount of the New Notes, plus accrued interest to date of such redemption and a “make-whole” premium. The term “Change of Control” is defined in the “Description of New Notes—Certain Definitions” section of this prospectus. | |||

Optional Redemption After Change in Tax Law |

Upon changes in foreign or domestic tax laws or their interpretation that would require a Guarantor to pay Additional Amounts to holders of New Notes in respect of payments made on the New Notes, we may redeem all, but not less than all, of the New Notes at a redemption price equal to the principal amount of the New Notes, plus accrued interest and additional amounts (if any). See “Description of New Notes—Redemption for Taxation Reasons” and “Description of New Notes—Additional Amounts.” | |||

Selection of New Notes Upon Optional Redemption |

If less than all of the New Notes are to be redeemed at any time, selection of New Notes for redemption will be made by the trustee in compliance with the requirements of the principal national securities exchange, if any, on which the New Notes are listed, or, if the New Notes are not so listed, on a pro rata basis (among the New Notes issued on the Issue Date and any additional notes issued under the indenture after the Issue Date, if any, as one class), by lot or by such method as the trustee shall deem fair and appropriate. | |||

Change of Control Offer | If a Change of Control occurs, we must give holders of the New Notes the opportunity to sell their New Notes to us at a purchase price of 101% of their face amount, plus accrued interest to the date of purchase. The term “Change of Control” is defined in the “Description of New Notes—Certain Definitions” section of this prospectus. | |||

12

Table of Contents

Covenants | The indenture governing the New Notes will contain covenants that limit our ability and that of our subsidiaries to: | |||

| • | incur additional debt; | |||

| • | pay dividends or distributions on, or redeem or repurchase, our capital stock; | |||

| • | make investments; | |||

| • | enter into sale and leaseback transactions; | |||

| • | engage in transactions with affiliates; | |||

| • | create liens on our assets; | |||

| • | transfer or sell assets; | |||

| • | guarantee debt; | |||

| • | restrict dividend or other payments to us; | |||

| • | consolidate, merge or transfer all or substantially all of our assets; and | |||

| • | engage in unrelated businesses. | |||

Risk Factors

Investing in the New Notes involves substantial risk. See “Risk Factors” section beginning on page 17 of this prospectus for a description of certain of the risks you should consider before investing in the New Notes.

13

Table of Contents

Summary Consolidated Financial Data

The summary fiscal year financial data presented below has been derived from our audited financial statements for the fiscal years ended February 24, 2002, February 23, 2003 and February 29, 2004 included elsewhere herein. We have restated our consolidated financial statements for fiscal 2002 and 2003 to correct the accounting of two leases of Stratus Technologies, Inc. For additional information, see “Capitalization,” “Selected Historical Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and our audited financial statements included elsewhere in this prospectus.

| Fiscal Years Ended | ||||||||||||

February 24, (restated) | February 23, (restated) | February 29, 2004 | ||||||||||

| (dollars in millions) | ||||||||||||

Statement of Operations Data: | ||||||||||||

Revenue | ||||||||||||

Continuum products | $ | 105.1 | $ | 85.0 | $ | 69.0 | ||||||

ftServer products | 13.6 | 34.4 | 41.9 | |||||||||

Total product revenue | 118.7 | 119.4 | 110.9 | |||||||||

Total service revenue | 126.1 | 127.5 | 150.4 | |||||||||

Total revenue | 244.8 | 246.9 | 261.3 | |||||||||

Total cost of revenue | 153.7 | 128.5 | 128.0 | |||||||||

Gross profit | 91.1 | 118.4 | 133.3 | |||||||||

Total operating expenses | 124.3 | 109.5 | 118.7 | |||||||||

Profit (loss) from operations | (33.2 | ) | 8.9 | 14.6 | ||||||||

Interest income | 0.5 | 0.2 | 0.1 | |||||||||

Interest expense | (10.9 | ) | (11.6 | ) | (16.3 | ) | ||||||

Other income (expense), net | (0.4 | ) | (0.3 | ) | 3.3 | |||||||

Income (loss) before income taxes | (44.0 | ) | (2.8 | ) | 1.7 | |||||||

Provision for income taxes | 9.4 | 3.3 | 3.0 | |||||||||

Net income (loss) | $ | (53.4 | ) | $ | (6.1 | ) | $ | (1.3 | ) | |||

| As of | ||||||||||||

February 24, (restated) | February 23, (restated) | February 29, 2004 | ||||||||||

| (dollars in millions) | ||||||||||||

Balance Sheet Data: | ||||||||||||

Cash and cash equivalents | $ | 22.7 | $ | 16.4 | $ | 23.1 | ||||||

Property, plant and equipment, net | 50.8 | 45.6 | 42.2 | |||||||||

Total assets | 203.1 | 213.1 | 210.4 | |||||||||

Total debt | 146.8 | 115.3 | 182.8 | |||||||||

Total stockholder’s equity (deficit) | (35.3 | ) | (0.5 | ) | (58.9 | ) | ||||||

14

Table of Contents

| Fiscal Years Ended | ||||||||||

February 24, (restated) | February 23, (restated) | February 29, 2004 | ||||||||

| (dollars in millions) | ||||||||||

Other Financial Data: | ||||||||||

Depreciation and amortization | $ | 28.5 | $ | 23.1 | 25.1 | |||||

Capital expenditures | 17.6 | 9.7 | 14.6 | |||||||

| Fiscal Years Ended | ||||||||

February 24, (restated) | February 23, (restated) | February 29, 2004 | ||||||

| (dollars in millions) | ||||||||

Other Data: (unaudited) | ||||||||

EBITDA (1)(3) | (5.1 | ) | 31.7 | 43.0 | ||||

Ratio of earnings to fixed charges (2) | — | — | 1.1 | x | ||||

| (1) | EBITDA represents net income (loss) before interest, taxes, depreciation and amortization. We present EBITDA because we consider it an important supplemental measure of our performance and believe it is frequently used by securities analysts, investors and other interested parties in the evaluation of companies in our industry. |

| We also use EBITDA for the following purposes: Our credit agreement and our indenture use EBITDA (with additional adjustments) to measure our compliance with covenants such as interest coverage and debt incurrence. EBITDA is also used by us and others in our industry to evaluate and price potential acquisition candidates. |

| EBITDA has limitations as an analytical tool, and you should not consider it in isolation, or as a substitute for analysis of our results as reported under GAAP. Some of these limitations are: |

| • | EBITDA does not reflect our cash expenditures, or future requirements for capital expenditures, or contractual commitments; |

| • | EBITDA does not reflect changes in, or cash requirements for, our working capital needs; |

| • | EBITDA does not reflect the significant interest expense, or the cash requirements necessary to service interest or principal payments, on our debts; |

| • | Although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future, and EBITDA does not reflect any cash requirements for such replacements; |

| • | EBITDA does not reflect the impact of earnings or charges resulting from matters we consider not to be indicative of our ongoing operations; and |

| • | Other companies in our industry may calculate EBITDA differently than we do, limiting its usefulness as a comparative measure. |

Because of these limitations, EBITDA should not be considered as a measure of discretionary cash available to us to invest in the growth of our business. We compensate for these limitations by relying primarily on our GAAP results and using EBITDA only supplementally. See the Statements of Cash Flow included in our financial statements.

| (2) | The ratio of earnings to fixed charges is computed by dividing earnings by fixed charges. For this purpose, “earnings” include net income (loss) before taxes and fixed charges. “Fixed charges” include interest, whether expensed or capitalized, amortization of debt expense and the portion of rental expense that is representative of the interest factor in these rentals. For fiscal 2002 and 2003, earnings before fixed charges were insufficient to cover fixed charges by approximately $44.0 million and $2.8 million, respectively. |

15

Table of Contents

| (3) | EBITDA and the related ratios presented in this table are measures of our performance that are not required by, or presented in accordance with, GAAP. EBITDA is not a measurement of our financial performance under GAAP and should not be considered as an alternative to net income, operating income or any other performance measure derived in accordance with GAAP or as an alternative to cash flow from operating activities as a measure of our liquidity. The following is a reconciliation of EBITDA to net income (loss) for the periods indicated: |

| Fiscal Years Ended | ||||||||||||

| February 24, 2002 (restated) | February 23, 2003 (restated) | February 29, 2004 | ||||||||||

| (dollars in millions) | ||||||||||||

Net income (loss) | $ | (53.4 | ) | $ | (6.1 | ) | $ | (1.3 | ) | |||

Add (deduct): | ||||||||||||

Interest expense, net | 10.4 | 11.4 | 16.2 | |||||||||

Provision for income taxes | 9.4 | 3.3 | 3.0 | |||||||||

Depreciation and amortization | 28.5 | 23.1 | 25.1 | |||||||||

EBITDA | $ | (5.1 | ) | $ | 31.7 | $ | 43.0 | |||||

16

Table of Contents

You should carefully consider the risks described below before making an investment decision. The risks described below are the significant ones facing us that are currently known and unique to us. In such case, you may lose all or part of your original investment.

Risks Related to the Exchange Offer

After the Exchange Offer, the market for Outstanding Notes may be less liquid and you may have difficulty selling the Outstanding Notes that you do not exchange.

If you do not exchange your Outstanding Notes for the New Notes offered in this Exchange Offer, you will continue to be subject to the restrictions on the transfer of your Outstanding Notes. Those transfer restrictions are described in the indenture governing the Outstanding Notes and in the legend contained on the Outstanding Notes, and arose because we originally issued the Outstanding Notes under exemptions from, and in transactions not subject to, the registration requirements of the Securities Act.

In general, you may offer or sell your Outstanding Notes only if they are registered under the Securities Act and applicable state securities laws, or if they are offered and sold under an exemption from those requirements. We do not intend to register the Outstanding Notes under the Securities Act.

If a large number of Outstanding Notes are exchanged for New Notes issued in the Exchange Offer, we would expect the remaining market for the Outstanding Notes to be less liquid, and it may be more difficult for you to sell your Outstanding Notes. In addition, if you do not exchange your Outstanding Notes in the Exchange Offer, you will no longer be entitled to have those Outstanding Notes registered under the Securities Act.

See “The Exchange Offer—Consequences of Failure to Exchange Outstanding Notes” for a discussion of the possible consequences of failing to exchange your Outstanding Notes.

You may find it difficult to sell the New Notes because there is no existing trading market for the New Notes.

There is no existing trading market for the New Notes. You may find it difficult to sell your New Notes because an active trading market for the New Notes may not develop. We do not intend to apply for listing or quotation of the New Notes on any exchange. The New Notes are being offered to the holders of the Outstanding Notes. The Outstanding Notes were issued on November 18, 2003 to a small number of institutional investors. Therefore, we do not know the extent to which investor interest will lead to the development of a trading market or how liquid that market may be. Although we were informed by the initial purchasers of the Outstanding Notes that they intend to make a market in the New Notes, they are not required to do so, and they may cease market-making at any time without notice. Consequently, the market price of the New Notes issued in this Exchange Offer could be materially reduced and you may not be able to liquidate your investment readily.

Risks Related to the New Notes

We are highly leveraged and may be unable to service or refinance our debt.

As a result of the 2004 Recapitalization, we are highly leveraged, which means we have a large amount of indebtedness in relation to our equity. As of February 29, 2004, we had approximately $182.8 million of indebtedness (including $170.0 million of Outstanding Notes, $3.3 million of secured borrowing under credit facilities and $9.5 million of unsecured indebtedness) and stockholder’s deficit of $(58.9) million. Our substantial indebtedness could adversely affect our ability to repay the New Notes.

17

Table of Contents

Our high level of indebtedness could have important consequences to you, including the risks that:

| • | our ability to obtain additional financing for working capital, capital expenditures, product development efforts, strategic acquisitions, general corporate purposes or other purposes may be impaired in the future; |

| • | we may not be able to refinance our existing indebtedness on terms that are favorable or at all; |

| • | a substantial portion of our cash flows from operations must be dedicated to the payment of principal and interest on our indebtedness, decreasing the amount of cash available for other purposes; |

| • | we are substantially more leveraged and have significantly less financial resources than certain of our competitors, which could place us at a competitive disadvantage; |

| • | we may be hindered in our ability to adjust to rapidly changing market conditions; |

| • | our high degree of leverage could make us more vulnerable in the event of a downturn in general economic conditions or our business or in the event of adverse changes in the regulatory environment or other adverse circumstances applicable to us; |

| • | our level of indebtedness may prevent us from raising the funds necessary to repurchase all of the New Notes tendered to us upon the occurrence of a change of control; and |

| • | our failure to comply with the financial and other restrictive covenants in our indebtedness, which, among other things, require us to maintain certain financial ratios and limit our ability to incur debt and sell assets, could result in an event of default that, if not cured or waived, could have a material adverse effect on our business or our prospects. |

See “Description of Other Indebtedness,” “Description of New Notes—Change of Control” and “—Defaults.”

Our ability to service or refinance our debt and to operate our business will require a significant amount of cash.

Our ability to repay or refinance our debt and to fund working capital needs and planned capital expenditures depends on our successful financial and operating performance. We cannot assure you that our business strategy will succeed or that we will achieve our anticipated financial results. We cannot assure you that we will generate sufficient cash flow from operations or that we will be able to obtain sufficient funding to satisfy all of our obligations, including those under the New Notes.

We currently generate approximately $23.2 million in funds per month, offset by an average funds usage of $22.1 million per month (including principal and interest payments on outstanding indebtedness, including the Outstanding Notes). We do not anticipate a need for additional capital to fund planned operations over the next twelve months. However, if our business does not generate sufficient cash flow from operations, and sufficient future borrowings are not available to us under the New Credit Facility or from other sources of financing, we may not be able to repay the New Notes or our other indebtedness, operate our business or fund our other liquidity needs. If we cannot meet or refinance our obligations when they are due, we will be required to pursue one or more alternative strategies, such as selling assets, refinancing or restructuring our indebtedness, selling additional equity capital, reducing capital expenditures or taking other actions that could have a material adverse effect on us. However, we cannot assure you that any alternative strategies will be feasible or prove adequate. Also, certain alternative strategies would require the consent of our senior secured lenders before we engaged in such strategies. See “Description of Other Indebtedness” and “Description of New Notes.”

18

Table of Contents

The volatile nature and competitive conditions of the computer server industry, our relative high level of indebtedness and other factors beyond our control may have an adverse effect on our financial and operational performance.

Our financial and operational performance depend upon a number of factors, many of which are beyond our control. These factors include:

| • | current economic and competitive conditions in our segments of the computer server industry; |

| • | solvency of our primary suppliers; |

| • | operating difficulties, operating costs or pricing pressures we may experience; |

| • | passage of legislation or other regulatory developments that affect us adversely; and |

| • | delays in implementing any strategic projects we may have. |

If our business does not generate sufficient cash flow from operations, and sufficient future borrowings are not available to us under the New Credit Facility or from other sources of financing, we may be required to seek additional financing. We cannot assure you that we will be able to obtain additional financing, on favorable terms or at all, particularly because we pledged substantially all our assets as collateral to secure the New Credit Facility, and because of our anticipated high levels of indebtedness and the indebtedness incurrence restrictions imposed by the agreements and instruments governing our indebtedness.

We may be able to incur additional debt, which may negatively affect our capital structure and credit ratings and may amplify the risks described above.

Despite current indebtedness levels, we and our subsidiaries may still be able to incur substantially more debt. This could further exacerbate the risks described above.

The terms of the indenture governing the New Notes limit but do not prohibit us or our subsidiaries from incurring additional indebtedness. In particular, as of February 29, 2004, we had approximately $28.7 million of additional borrowing capacity under the New Credit Facility and ¥350.0 million (approximately $3.2 million) of additional borrowing capacity under the existing overdraft facility in Japan. In addition to the additional borrowing capacity that we have under the New Credit Facility, we also may incur indebtedness from other sources. If new debt is added by us or our subsidiaries, our capital structure and credit ratings may be negatively affected and the related risks that we and they now face could intensify. See “Capitalization,” “Selected Historical Financial Data,” “Description of Other Indebtedness” and “Description of New Notes.”

Since the New Notes are unsecured, your right to receive payments on the New Notes is effectively subordinated to the rights of our existing and future secured creditors. Further, the Guarantees of the New Notes are effectively subordinated to all of our Guarantors’ existing and future secured indebtedness.

If we become insolvent or are liquidated, or if our debt under the New Credit Facility or our other existing or future secured indebtedness is accelerated, then the lenders under the New Credit Facility or our other secured indebtedness, as applicable, would have claims on our assets prior to the holders of the New Notes. The New Credit Facility is secured by liens on substantially all of our assets and the assets of the Guarantors. Holders of the New Notes will participate ratably with all holders of our senior unsecured indebtedness, based upon the respective amounts owed to each creditor, in our remaining assets. In such circumstances, we cannot assure you that there will be sufficient assets to pay amounts due on the New Notes. As a result, holders of New Notes may receive less, ratably, than holders of secured indebtedness in such circumstances.

As of February 29, 2004, the aggregate amount of our secured indebtedness and the secured indebtedness of our subsidiaries was approximately $3.3 million, and approximately $28.7 million was available for additional borrowing under the New Credit Facility. We will be permitted to borrow substantial additional indebtedness, including secured debt, in the future under the terms of the indenture governing the New Notes. See “Description of Other Indebtedness—The New Credit Facility.”

19

Table of Contents

The agreements and instruments governing our debt contain restrictions and limitations that could significantly impact the holders of the New Notes and our ability to operate our business.

The New Credit Facility contains a number of significant covenants that could adversely impact the holders of the New Notes and our business. In general, these covenants, among other things, prohibit us and our subsidiaries from:

| • | paying dividends or making other distributions on equity interests; |

| • | making investments or acquisitions, with exceptions for, among other things, |

| • | certain acquisitions of related businesses for up to $35.0 million per acquisition and no more than $60.0 million in the aggregate (provided that additional consideration up to $100.0 million in the aggregate funded with the proceeds of concurrent equity issuances is permitted); and |

| • | certain other investments in related joint ventures and other related businesses in an aggregate amount up to $25.0 million (provided that additional consideration up to $50.0 million in the aggregate funded with the proceeds of concurrent equity issuances is permitted) other than transactions on arm’s length terms in the ordinary course of business; |

| • | entering into transactions with affiliates; |

| • | disposing of assets or entering into business combinations, with exceptions for, among other things, asset sales with net proceeds in an aggregate amount up to $10.0 million and asset sales with no more than $12.0 million of unreinvested net proceeds at any time; |

| • | incurring or guaranteeing additional debt, with exceptions for, among other things, certain unsecured indebtedness in an aggregate amount up to $25.0 million, certain indebtedness in connection with acquisitions so long as certain conditions are met, certain other indebtedness of foreign subsidiaries in an amount up to $22.5 million, indebtedness under the New Notes and certain refinancings thereof, and unsecured subordinated debt of up to $10.0 million; |

| • | repurchasing or redeeming certain debt, with exceptions for, among other things, redemption of up to an aggregate amount of $50.0 million of New Notes with proceeds of an initial public offering, provided that at such time the aggregate amount of loans outstanding under the New Credit Facility is less than $5.0 million and the leverage ratio for the four preceding fiscal quarters is 2.5 to 1.0 or lower; |

| • | creating or permitting to exist certain liens; |

| • | materially amending certain debt; |

| • | making capital expenditures in excess of a given amount in any fiscal year; and |

| • | permitting consolidated EBITDA (as defined in the New Credit Facility) for a period of four consecutive fiscal quarters to be less than $35.0 million. Our consolidated EBITDA (as so defined) for the four consecutive fiscal quarters ended February 29, 2004 was $45.0 million. We do not expect to have difficulty maintaining compliance with this minimum consolidated EBITDA requirement. |

These restrictions could limit our ability to obtain future financing, make acquisitions or needed capital expenditures, withstand a future downturn in our business or the economy in general, conduct operations or otherwise take advantage of business opportunities that may arise. Furthermore, the New Credit Facility requires us to meet specified financial ratios and other tests. Our ability to comply with these provisions may be affected by events beyond our control. The breach of any of these covenants could result in a default under the New Credit Facility, which could permit the holders of that indebtedness to accelerate the maturity of such indebtedness and could cause defaults under our other indebtedness (including the New Notes) or result in our bankruptcy. An acceleration or bankruptcy resulting from a default under the New Credit Facility would result in a default on the New Notes and could delay or preclude payment of principal of or interest on the New Notes. Our ability to meet our obligations depends on our future performance, which is subject to prevailing economic conditions and to financial, business and other factors, including factors beyond our control. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources” and “Description of Other Indebtedness—New Credit Facility.”

20

Table of Contents

If we default under the New Credit Facility, we may not have the ability to make payments on the New Notes.

In the event of a default under the New Credit Facility, our lenders could elect to declare all amounts borrowed, together with accrued and unpaid interest and other fees, to be due and payable. If such an acceleration occurs, thereby causing a default under the New Notes, we may not be able to repay, or borrow money to repay, the amounts due under the New Credit Facility or the New Notes. This inability could have serious consequences to the holders of the New Notes and to our financial condition and results of operations, and could cause us to become bankrupt or insolvent.

Guarantees are subject to limitations that could affect your right to receive payments on the New Notes.

Although the Guarantees provide the holders of the New Notes with a direct claim against the assets of the Guarantors, enforcement of the Guarantees against any Guarantor could be subject to certain suretyship defenses available to guarantors generally. To the extent that the Guarantees are not enforceable, the New Notes would be effectively subordinated to all liabilities of the Guarantors, including trade payables of such Guarantors, whether or not such liabilities otherwise would constitute senior indebtedness under the indenture governing the New Notes.

Stratus Technologies, Inc. may not have access to the cash flow and other assets of its subsidiaries and sister companies that may be needed to make payment on the New Notes.

Although much of the business of Stratus Technologies, Inc., the issuer of the New Notes, is conducted through its subsidiaries and sister companies, none of these companies is obligated to make funds available to Stratus Technologies, Inc. for payment on the New Notes. Accordingly, the ability of Stratus Technologies, Inc. to make payments on the New Notes is dependent on the earnings and the distribution of funds from these companies. The terms of the New Credit Facility significantly restrict the subsidiaries of Stratus Technologies, Inc. from paying dividends and otherwise transferring assets to Stratus Technologies, Inc. Furthermore, the subsidiaries and sister companies of Stratus Technologies, Inc. are permitted under the terms of the indenture governing the New Notes to incur additional indebtedness that may severely restrict or prohibit the making of distributions, the payment of dividends or the making of loans by such companies to Stratus Technologies, Inc. We cannot assure you that the agreements governing the current and future indebtedness of the subsidiaries and sister companies of Stratus Technologies, Inc. will permit these companies to provide Stratus Technologies, Inc. with sufficient dividends, distributions or loans to fund payments on these Notes when due. See “Description of Other Indebtedness.” In addition, the payment of dividends to Stratus Technologies, Inc. by its subsidiaries is contingent upon the earnings of those subsidiaries and approval by the respective boards of directors of those subsidiaries.

Your right to receive payments on these Notes could be adversely affected if any of the non-Guarantor subsidiaries declare bankruptcy, liquidate or reorganize.

The foreign subsidiaries of Stratus Technologies, Inc., the issuer of the New Notes, are not guaranteeing the New Notes in order to avoid adverse tax consequences to us. Additionally, Holdings, our ultimate parent entity, is not guaranteeing the New Notes due to concepts of Luxembourg law that prohibit Luxembourg companies from providing security with a view to the acquisition of their shares by a third party. See “Use of Proceeds.” In the event of a bankruptcy, liquidation or reorganization of any of the non-Guarantor subsidiaries, holders of their indebtedness and their trade creditors will generally be entitled to payment of their claims from the assets of those subsidiaries before any assets are made available for distribution to us. At February 29, 2004, the non-Guarantor subsidiaries held an aggregate of $46.9 million in assets. For the fiscal year ended February 29, 2004, the non-Guarantor subsidiaries generated total revenue of $98.0 million and gross profit of $23.8 million.

21

Table of Contents

As of February 29, 2004, the New Notes were effectively junior to $21.5 million of trade payables and other liabilities of the non-Guarantor subsidiaries and $3.2 million was available to a non-Guarantor subsidiary for future borrowings. The non-Guarantor subsidiaries generated 36.1% of our consolidated revenue (excluding intercompany transactions) in the fiscal year ended February 29, 2004 and held 22.3% of our consolidated assets as of February 29, 2004. See note 18 to our audited consolidated financial statements included at the back of this prospectus.

Fraudulent conveyance laws could void our obligations under the New Notes and the Guarantees.

We will incur substantial indebtedness under the New Notes. Our incurrence of indebtedness under the New Notes and the incurrence by some of our affiliates of indebtedness under their Guarantees may be subject to review under federal and state fraudulent conveyance laws (and applicable equivalent foreign law concepts) if a bankruptcy, reorganization or rehabilitation case or a lawsuit (including circumstances in which bankruptcy is not involved) were commenced by, or on behalf of, our unpaid creditors or unpaid creditors of our Guarantors at some future date. Federal and state statutes may allow courts, under specific circumstances, to void the New Notes and the Guarantees and require noteholders to return payments received from us or the Guarantors.

An unpaid creditor or representative of creditors, such as a trustee in bankruptcy of Stratus as a debtor-in-possession in a bankruptcy proceeding, could file a lawsuit claiming that the issuances of the New Notes constituted a fraudulent conveyance. To make such a determination, a court would have to find that we did not receive fair consideration or reasonably equivalent value for the New Notes, and that, at the time the New Notes were issued, we:

| • | were insolvent; |

| • | were rendered insolvent by the issuance of the New Notes; |

| • | were engaged in a business or transaction for which our remaining assets constituted unreasonably small capital; or |

| • | intended to incur, or believed that we would incur, debts beyond our ability to repay those debts as they matured. |

If a court were to make such a finding, it could void our obligations under the New Notes, subordinate the New Notes to our other indebtedness or take other actions detrimental to you as a holder of the New Notes.