Table of Contents

As filed with the Securities and Exchange Commission on December 19, 2003

Registration No. 333-

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Forms F-4* and S-4*

REGISTRATION STATEMENT

Under

THE SECURITIES ACT OF 1933

North American Energy Partners Inc.

(Exact name of registrant as specified in its charter)

| Canada | 1629 | Not Applicable | ||

| (State or Other Jurisdiction of Incorporation or Organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

Acheson Industrial Park #2 53016—Highway 60 Spruce Grove, Alberta T7X 3G7 (780) 960-7171 | Vincent J. Gallant Acheson Industrial Park #2 53016—Highway 60 Spruce Grove, Alberta T7X 3G7 (780) 960-7171 | |

| (Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices) | (Name, address, including zip code, and telephone number, including area code, of agent for service) |

Copies to:

Gary W. Orloff, Esq.

Bracewell & Patterson, L.L.P.

711 Louisiana Street, Suite 2900

Houston, Texas 77002-2781

Phone: (713) 221-1306

Fax: (713) 221-2166

Approximate date of commencement of proposed sale of the securities to the public: As soon as practicable after this registration statement becomes effective.

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered | Amount to be Registered | Proposed Maximum Offering Price per Note | Proposed Maximum Aggregate Offering Price(1) | Amount of Registration Fee | ||||

8 3/4% Exchange Senior Notes due 2011 | $200,000,000 | 100% | $200,000,000 | $16,180 | ||||

Guarantees of 8 3/4% Exchange Senior Notes due 2011(2) | (3) | (3) | $0 | None(3) | ||||

| (1) | Estimated solely for purposes of calculating the registration fee pursuant to Rule 457(f)(2) under the Securities Act. |

| (2) | See the Table of Additional Registrants on the next page for a list of the additional registrant guarantors. |

| (3) | Pursuant to Rule 457(n) under the Securities Act, no separate registration fee is required with respect to the guarantees. |

The registrants hereby amend this registration statement on such date or dates as may be necessary to delay its effective date until the registrants shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

TABLE OF ADDITIONAL REGISTRANTS

Exact Name of Registrant as Specified in its Charter(1) | State or Other Jurisdiction of | I.R.S. Employer | ||

North American Construction Group Inc. | Canada | Not applicable | ||

North American Caisson Ltd. | Alberta, Canada | Not applicable | ||

North American Construction Ltd. | Canada | Not applicable | ||

North American Engineering Inc. | Alberta, Canada | Not applicable | ||

North American Enterprises Ltd. | Alberta, Canada | Not applicable | ||

North American Industries Inc. | Alberta, Canada | Not applicable | ||

North American Maintenance Ltd. | Alberta, Canada | Not applicable | ||

North American Mining Inc. | Alberta, Canada | Not applicable | ||

North American Pipeline Inc. | Alberta, Canada | Not applicable | ||

North American Road Inc. | Alberta, Canada | Not applicable | ||

North American Services Inc. | Alberta, Canada | Not applicable | ||

North American Site Development Ltd. | Alberta, Canada | Not applicable | ||

North American Site Services Inc. | Alberta, Canada | Not applicable | ||

Griffiths Pile Driving Inc. | Alberta, Canada | Not applicable | ||

NACG Finance LLC | Delaware | 74-3107147 |

| (1) | The address, including zip code, and telephone number, including area code, of each of the additional registrant’s principal executive offices is c/o North American Energy Partners Inc., Acheson Industrial Park #2, 53016-Highway 60, Spruce Grove, Alberta T7X 3G7, (780) 960-7171, except for NACG Finance LLC which is 28 Lawton Blvd., Toronto, Ontario M4V 1Z5. |

| * | Explanatory Note—This registration statement comprises a filing on Form F-4 with respect to the securities of the non-U.S. registrants and a filing on Form S-4 with respect to the security of the U.S. registrant. |

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statements filed with the Securities and Exchange Commission are effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to completion, dated December 19, 2003

US$200,000,000

NORTH AMERICAN ENERGY PARTNERS INC.

Offer to Exchange

8 3/4% Exchange Senior Notes due 2011

for any and all outstanding 8 3/4% Senior Notes due 2011

This prospectus, and accompanying letter of transmittal, relate to our proposed exchange offer. We are offering to exchange up to US$200,000,000 aggregate principal amount of new 8 3/4% exchange senior notes due 2011, which we call the exchange notes and which will be freely transferable, for any and all outstanding 8 3/4% senior notes due 2011, which we call the original notes, previously issued in a private offering and which have various transfer restrictions because they were not issued pursuant to a registration statement.

In this prospectus we sometimes refer to the exchange notes and the original notes collectively as the notes.

| • | The exchange offer expires at 5:00 p.m., New York City time, on , 2004, unless extended. |

| • | The terms of the exchange notes are substantially identical to the terms of the original notes, except that the exchange notes will be freely transferable and issued free of any covenants regarding exchange and registration rights. |

| • | All original notes that are validly tendered and not validly withdrawn will be exchanged. |

| • | Tenders of original notes may be withdrawn at any time prior to expiration of the exchange offer. |

| • | We will not receive any proceeds from the exchange offer. |

| • | The exchange of original notes for exchange notes will not be a taxable event for United States federal income tax purposes. |

| • | Holders of original notes do not have any appraisal or dissenters’ rights in connection with the exchange offer. |

| • | Original notes not exchanged in the exchange offer will remain outstanding and be entitled to the benefits of the indenture, but except under limited circumstances, will have no further exchange or registration rights under the registration rights agreement discussed in this prospectus. |

Please see “Risk Factors” beginning on page 10 for a discussion of factors you should consider in connection with the exchange offer.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the exchange notes or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

We may amend or supplement this prospectus from time to time by filing amendments or supplements as required. You should read this entire prospectus, the accompanying letter of transmittal and related documents and any amendments or supplements to this prospectus carefully before making your investment decision.

The date of this prospectus is , 2004.

Table of Contents

| Page | ||

| 1 | ||

| 10 | ||

| 20 | ||

| 34 | ||

| 35 | ||

| 36 | ||

| 37 | ||

| 39 | ||

Management’s Discussion and Analysis of Financial Condition and | 48 | |

| 61 | ||

| 79 | ||

| 85 | ||

| 90 | ||

| 92 | ||

| 95 | ||

| 134 | ||

| 137 | ||

| 139 | ||

| 139 | ||

| 139 | ||

| 139 | ||

| 140 | ||

| F-1 | ||

| Annex A |

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with different information. This prospectus may only be used where it is legal to sell the notes. You should not assume that the information contained in this prospectus is accurate as of any date other than the date on the front cover of the prospectus. Our business, financial condition, results of operations and prospects may have changed since that date.

The exchange notes have not been and will not be qualified for public distribution under the securities laws of any province or territory of Canada. The exchange notes are not being offered for sale and may not be offered or sold, directly or indirectly, in Canada or to any resident thereof except in accordance with the securities laws of the provinces and territories of Canada. The notes have been issued pursuant to the exemption from the prospectus requirements of the applicable Canadian provincial and territorial securities laws and may be sold in Canada only pursuant to an exemption therefrom.

A number of terms commonly used in the oil sands industry and this prospectus are defined in the glossary section of this prospectus.

i

Table of Contents

INFORMATION REGARDING FORWARD-LOOKING STATEMENTS

This document contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These statements are subject to risks and uncertainties and are based on the beliefs and assumptions of management, based on information currently available to management. Forward-looking statements are those that do not relate strictly to historical or current facts, and can be identified by the use of the future tense or other forward-looking words such as “believe,” “expect,” “anticipate,” “intend,” “plan,” “estimate,” “should,” “may,” “will,” “objective,” “projection,” “forecast,” “management believes,” “continue,” “strategy,” “position” or the negative of those terms or other variations of them or by comparable terminology. In particular, statements, express or implied, concerning future operating results or the ability to generate income or cash flow are forward-looking statements. Forward-looking statements include the information concerning possible or assumed future results of our operations set forth under “Summary,” “Risk Factors,” “Capitalization,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Business” and “Unaudited Pro Forma Financial Information.”

Forward-looking statements are not guarantees of performance. They involve risks, uncertainties and assumptions. Future actions, conditions or events and future results of operations may differ materially from those expressed in these forward-looking statements. Many of the factors that will determine these results are beyond management’s ability to control or predict. Specific factors that could cause actual results to vary from those in the forward-looking statements include:

| • | changes in oil and gas prices; |

| • | decreases in outsourcing work by our customers; |

| • | shut-downs or cutbacks at major businesses that use our services; |

| • | changes in laws or regulations, third party relations and approvals, and decisions of courts, regulators and governmental bodies that may adversely affect our business or the business of the customers we serve; |

| • | our ability to obtain surety bonds as required by some of our customers; |

| • | our ability to retain a skilled labor force and continue to bid successfully on new projects; |

| • | provincial, regional and local economic, competitive and regulatory conditions and developments; |

| • | technological developments; |

| • | capital markets conditions; |

| • | inflation rates; |

| • | foreign currency exchange rates; |

| • | interest rates; |

| • | weather conditions; |

| • | the timing and success of business development efforts; and |

| • | our ability to successfully identify and acquire new businesses and assets and integrate them into our existing operations. |

You are cautioned not to put undue reliance on any forward-looking statements, and we undertake no obligation to update those statements.

ii

Table of Contents

EXCHANGE RATE DATA

The following table lists, for each period presented, the high and low exchange rates, the average of the exchange rates on the last day of each month during the period indicated and the exchange rates at the end of the period for one Canadian dollar, expressed in U.S. dollars, based on the inverse of the noon buying rate in New York City for cable transfers in Canadian dollars as certified for customs purposes by the Federal Reserve Bank of New York. As of November 20, 2003, the inverse of the noon Federal Reserve Bank of New York buying rate of Canadian dollars was $1.00 = US$0.7674.

| Year Ended March 31, | Six Months Ended September 30, 2003 | |||||||

| 2001 | 2002 | 2003 | ||||||

High for period | 0.6889 | 0.6622 | 0.6819 | 0.7492 | ||||

Low for period | 0.6336 | 0.6200 | 0.6252 | 0.6737 | ||||

End of period | 0.6336 | 0.6266 | 0.6805 | 0.7404 | ||||

Average for period | 0.6651 | 0.6392 | 0.6455 | 0.7200 | ||||

iii

Table of Contents

This summary highlights information contained elsewhere in this prospectus. It may not contain all of the information that is important to you. Therefore, you are encouraged to read the entire prospectus carefully, including the risks discussed in the “Risk Factors” section and the financial statements of North American Energy Partners Inc. and of Norama Ltd. and the footnotes to those statements, which are included in this prospectus. This prospectus includes the historical financial statements of Norama Ltd., the holding company for the business that we acquired on November 26, 2003, pursuant to the purchase and sale agreement dated October 31, 2003. The “pro forma” financial information gives effect to the transactions, as defined below, including (1) the offering of the notes and the other financings, (2) the impact of adjustments to account for the purchase at the closing date of substantially all of our equipment under operating leases as if the equipment had been purchased at the inception of the related lease agreements and (3) the cancellation of the management fee with the sellers at the closing date. We state our financial statements in Canadian dollars. In this prospectus, references to Canadian dollars, dollars, Cdn$, or $ are to the currency of Canada, and references to U.S. dollars or US$ are to the currency of the United States.

Our Company

We are one of the largest and most experienced providers of site preparation, mining, piling and pipeline installation services in western Canada. We provide our services primarily to the major integrated and independent oil and gas, petrochemical and other natural resources companies operating in this geographic region. In serving our customers, we operate over 400 pieces of heavy equipment and over 450 support vehicles, and we have developed particular expertise operating in the difficult working conditions created by the climate and terrain of the Alberta oil sands and other areas of western Canada. Our work on private sector oil sands and pipeline installation projects is a result of focusing our asset deployment on the more technically difficult and profitable revenue opportunities rather than traditional public sector construction activity. Our services consist of:

| • | site preparation, which includes clearing, stripping, excavating and grading for mining operations and other general construction projects, as well as underground utility installation for plant, refinery and commercial building construction; |

| • | surface mining for oil sands and other natural resources, including overburden removal, the hauling of sand and gravel, mining of the ore body and delivery of the ore to the crushing facility, supply of labor and equipment to support owners’ mining operations, construction of infrastructure associated with mining operations and reclamation activities; |

| • | piling installation, including the installation of all types of driven and drilled piles, caissons and earth retention and stabilization systems for commercial buildings, private industrial projects, such as plants and refineries, and infrastructure projects, such as bridges; and |

| • | pipeline installation, including the installation of transmission and distribution pipe made of steel, plastic and fiberglass materials in sizes up to and including 36 inches in diameter for oil and gas transmission. |

For the twelve months ended September 30, 2003, on a pro forma basis, we had revenue of $402.4 million. Our revenues grew at a compounded annual growth rate of over 26% from fiscal 1999 to 2003.

1

Table of Contents

We have long-term, stable relationships with our customers, some of whom we have been serving for over 40 years. We believe we are the principal provider of site preparation, mining and piling services in the Alberta oil sands to Syncrude Canada Ltd., our largest customer and the largest producer of bitumen in the oil sands, and other major operators in the area. We also provide pipeline installation services in British Columbia to EnCana Corporation. We estimate that over 91% of our revenues from fiscal year 2001 to 2003 was attributable to private sector oil and gas projects in Alberta and British Columbia, and for the twelve months ended September 30, 2003, we derived over 94% of our revenue from this market.

Our principal office is located at Acheson Industrial Park #2, 53016-Highway 60, Spruce Grove, Alberta, T7X 3G7. Our telephone number is (780) 960-7171.

The Transactions

On October 31, 2003, NACG Preferred Corp., our corporate parent, and NACG Acquisition Inc., our wholly-owned subsidiary, as the buyers, entered into a purchase and sale agreement with Norama Ltd. and its subsidiary North American Equipment Ltd., as the sellers, and Martin Gouin and Roger Gouin, the ultimate owners of Norama Ltd. Pursuant to the purchase and sale agreement, Norama Ltd. sold to NACG Preferred Corp. 30 shares of North American Construction Group Inc. in exchange for $35.0 million of its Series A Preferred Shares and sold the remaining 170 shares of North American Construction Group Inc. to NACG Acquisition Inc. for approximately $195 million in cash. NACG Preferred Corp. contributed the 30 shares of North American Construction Group Inc. it received to us, and we contributed these shares to NACG Acquisition Inc. Additionally, North American Equipment Ltd., a wholly-owned subsidiary of Norama Ltd., sold to NACG Acquisition Inc. substantially all of the assets of North American Equipment Ltd. in exchange for $175.0 million in cash. The total consideration paid by NACG Preferred Corp. and NACG Acquisition Inc. to the sellers was approximately $405 million, subject to post-closing adjustments. The sellers utilized a portion of the proceeds to repay existing indebtedness of Norama Ltd. and for the buyout of various existing equipment leases upon closing. The foregoing actions are collectively referred to as the “acquisition.”

At the closing of the transactions contemplated by the purchase and sale agreement, an investor group including investment entities controlled by The Sterling Group, L.P., Genstar Capital, L.P., Perry Strategic Capital Inc., and Stephens Group, Inc., which we refer to collectively as the “sponsors,” along with Paribas North America, Inc., an affiliate of BNP Paribas Securities Corp., our management and our employees, which we refer to collectively with the sponsors as “our investor group,” purchased for cash, $92.5 million of the common shares of NACG Holdings Inc., our ultimate parent company. The $92.5 million of cash proceeds were ultimately contributed to NACG Acquisition Inc. The proceeds of the equity offering and the offering of the notes and drawings under our new credit facility were used to make the cash payments to the sellers for the acquisition and to pay related transaction fees and expenses.

The offering of the original notes, together with the execution of and initial borrowings under the new bank credit agreement, the equity investment and the preferred shares issuance are collectively referred to in this prospectus as the “financings.” We refer to the acquisition and the financings as the “transactions.”

2

Table of Contents

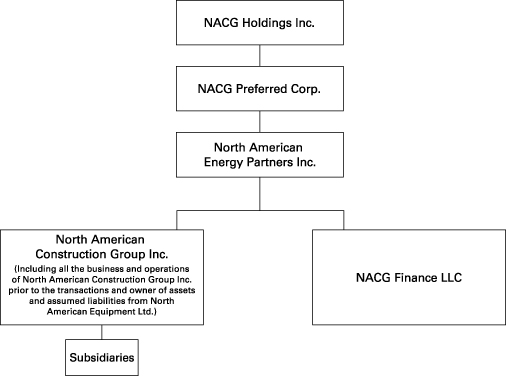

Corporate Structure

We are a wholly-owned subsidiary of NACG Preferred Corp., a company without any business operations. NACG Preferred Corp. is a wholly-owned subsidiary of NACG Holdings Inc., our ultimate parent. NACG Holdings Inc., was formed in connection with the acquisition and has no business operations. All of our restricted subsidiaries guarantee the notes. The following chart depicts our organizational structure.

3

Table of Contents

The Exchange Offer

Registration Rights Agreement | We sold US$200 million in aggregate principal amount of original notes to qualified institutional buyers as defined in Rule 144A under the Securities Act and outside the United States in accordance with Regulation S under the Securities Act through BNP Paribas Securities Corp. and RBC Dominion Securities Corporation, as initial purchasers. We entered into a registration rights agreement with the initial purchasers which grants the holders of the original notes limited exchange and registration rights. The exchange offer made pursuant to this prospectus is intended to satisfy such exchange rights. |

The Exchange Offer | $1,000 principal amount of exchange notes in exchange for each $1,000 principal amount of original notes. As of the date hereof, US$200 million aggregate principal amount of the original notes are outstanding. We will issue exchange notes to holders on the earliest practicable date following the Expiration Date. |

Resales of the Exchange Notes | Based on an interpretation by the staff of the SEC set forth in no-action letters issued to third parties, we believe that, except as described below, the exchange notes issued pursuant to the exchange offer may be offered for resale, resold and otherwise transferred by a holder thereof, other than any such holder that is an “affiliate” of ours within the meaning of Rule 405 under the Securities Act, without compliance with the registration and prospectus delivery provisions of the Securities Act, provided that such exchange notes are acquired in the ordinary course of such holder’s business and that such holder has no arrangement or understanding with any person to participate in the distribution of such exchange notes. |

Each broker-dealer that receives exchange notes pursuant to the exchange offer in exchange for original notes that such broker-dealer acquired for its own account as a result of market-making activities or other trading activities, other than original notes acquired directly from us or our affiliates, must acknowledge that it will deliver a prospectus in connection with any resale of such exchange notes. The letter of transmittal states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an “underwriter” within the meaning of the Securities Act. |

If we receive certain notices in the letter of transmittal, this prospectus, as it may be amended or supplemented from time to time, may be used for the appropriate time period |

4

Table of Contents

by a broker-dealer in connection with resales of exchange notes received in exchange for original notes where such original notes were acquired by such broker-dealer as a result of market-making activities or other trading activities and not acquired directly from us. We have agreed that, if we receive the notices in the letter of transmittal, we will make this prospectus available to any such broker-dealer for use in connection with any such resale. |

The letter of transmittal requires broker-dealers tendering original notes in the exchange offer to indicate whether the broker-dealer acquired the original notes for its own account as a result of market-making activities or other trading activities, other than original notes acquired directly from us or any of our affiliates. If no broker-dealer indicates that the original notes were so acquired, we have no obligation under the registration rights agreement to maintain the effectiveness of the registration statement past the consummation of the exchange offer or to allow the use of this prospectus for such resales. See “The Exchange Offer—Registration Rights” and “—Resale of the Exchange Notes; Plan of Distribution.” |

Expiration Date | The exchange offer expires at 5:00 p.m., New York City time, on , 2004, unless we extend the exchange offer in our sole discretion, in which case the term “Expiration Date” means the latest date and time to which the exchange offer is extended. |

Conditions to the Exchange Offer | The exchange offer is subject to certain conditions which we may waive. See “The Exchange Offer—Conditions to the Exchange Offer.” |

Procedures for Tendering the Original Notes | Each holder of original notes wishing to accept the exchange offer must complete, sign and date the accompanying letter of transmittal in accordance with the instructions contained in this prospectus and in the letter of transmittal, and mail or otherwise deliver such letter of transmittal together with the original notes and any other required documentation to the exchange agent identified below under “Exchange Agent” at the address set forth in this prospectus. By executing the letter of transmittal, a holder will make a number of representations to us. See “The Exchange Offer—Registration Rights” and “—Procedures for Tendering Original Notes.” |

Special Procedures for Beneficial Owners | Any beneficial owner whose original notes are registered in the name of a broker, dealer, commercial bank, trust |

5

Table of Contents

company or other nominee and who wishes to tender should contact the registered holder promptly and instruct the registered holder to tender on such beneficial owner’s behalf. See “The Exchange Offer—Procedures for Tendering Original Notes.” |

Guaranteed Delivery Procedures | Holders of original notes who wish to tender their original notes when those securities are not immediately available or who cannot deliver their original notes, the letter of transmittal or any other documents required by the letter of transmittal to the exchange agent prior to the Expiration Date must tender their original notes according to the guaranteed delivery procedures set forth in “The Exchange Offer—Procedures for Tendering Original Notes—Guaranteed Delivery.” |

Withdrawal Rights | Tenders of original notes pursuant to the exchange offer may be withdrawn at any time prior to the Expiration Date. |

Acceptance of Original Notes and Delivery of Exchange Notes | We will accept for exchange any and all original notes that are properly tendered in the exchange offer, and not withdrawn, prior to the exchange offer’s Expiration Date. The exchange notes issued pursuant to the exchange offer will be issued on the earliest practicable date following our acceptance for exchange of original notes. See “The Exchange Offer—Terms of the Exchange Offer.” |

Exchange Agent | Wells Fargo Bank, N.A. is serving as exchange agent in connection with the exchange offer. |

U.S. Federal Income Tax Considerations | The exchange of original notes for exchange notes pursuant to the exchange offer will not be treated as a taxable exchange for federal income tax purposes. See “Income Tax Considerations.” |

6

Table of Contents

Summary Historical and Pro Forma Financial Information

The summary historical consolidated financial information presented below as of and for each of the fiscal years ended March 31, 2001, 2002 and 2003 is derived from the audited consolidated financial statements of our predecessor company, Norama Ltd. The summary historical consolidated financial information presented below as of and for each of the six months ended September 30, 2002 and 2003 is derived from the historical unaudited financial statements of Norama Ltd. In the opinion of our management, the unaudited historical consolidated financial statements include all adjustments necessary for a fair presentation of our financial position and results of operations for such periods.

The summary pro forma financial information presented below for the fiscal year ended March 31, 2003, the six months ended September 30, 2003 and the twelve months ended September 30, 2003 is derived from the unaudited pro forma financial statements of North American Energy Partners Inc. included in this prospectus. The summary unaudited pro forma balance sheet information as of September 30, 2003 gives effect to the transactions as if they had occurred on September 30, 2003. The summary pro forma consolidated statements of operations for the fiscal year ended March 31, 2003, the six months ended September 30, 2003 and the twelve months ended September 30, 2003 give effect to the transactions as if they had occurred on April 1, 2002.

The summary historical consolidated financial information for the six months ended September 30, 2003 and the unaudited pro forma financial information as of and for the six months ended September 30, 2003 and the twelve months ended September 30, 2003 are not necessarily indicative of the results that may be expected for the full fiscal year ending March 31, 2004.

The information presented below should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” the consolidated financial statements of Norama Ltd. and the related notes to those financial statements, and the Unaudited Pro Forma Financial Information for North American Energy Partners Inc. and related notes included elsewhere in this prospectus. All of the financial information presented below has been prepared in accordance with Canadian GAAP. We are not aware of any material differences in the measurement of operations or the recognition of assets and liabilities under U.S. GAAP. For a discussion of the principal differences between Canadian GAAP and U.S. GAAP as they pertain to us, see note 18 to the Norama Ltd. consolidated financial statements included elsewhere in this prospectus.

7

Table of Contents

| Historical | Pro Forma | |||||||||||||||||||||||||||||||

| Year Ended March 31, | Six Months Ended September 30, | Year Ended March 31, | Six Months Ended September 30, | Twelve Months Ended September 30, | ||||||||||||||||||||||||||||

| 2001 | 2002 | 2003 | 2002 | 2003 | 2003 | 2003 | 2003 | |||||||||||||||||||||||||

| (dollars in thousands) | ||||||||||||||||||||||||||||||||

Statement of Operations Data: | ||||||||||||||||||||||||||||||||

Revenue | $ | 247,267 | $ | 249,351 | $ | 344,186 | $ | 138,059 | $ | 196,259 | $ | 344,186 | $ | 196,259 | $ | 402,386 | ||||||||||||||||

Job costs | 128,085 | 123,893 | 220,855 | 91,245 | 116,941 | 220,706 | 116,926 | 246,461 | ||||||||||||||||||||||||

Parts, shop labor and overhead | 33,810 | 49,989 | 44,050 | 18,583 | 28,428 | 44,050 | 28,428 | 53,895 | ||||||||||||||||||||||||

Equipment leases and rentals | 30,339 | 31,091 | 26,904 | 13,301 | 15,641 | 13,110 | 5,844 | 11,534 | ||||||||||||||||||||||||

Depreciation | 10,409 | 11,299 | 10,974 | 4,409 | 5,389 | 23,601 | 12,725 | 26,563 | ||||||||||||||||||||||||

Gross margin | 44,624 | 33,079 | 41,403 | 10,521 | 29,860 | 42,719 | 32,336 | 63,933 | ||||||||||||||||||||||||

General and administrative | 9,594 | 13,089 | 12,397 | 5,099 | 5,867 | 12,397 | 5,867 | 13,165 | ||||||||||||||||||||||||

Management fees (a) | 36,550 | 14,400 | 8,000 | 6,600 | �� | 23,200 | — | — | — | |||||||||||||||||||||||

Advisory fee (b) | — | — | — | — | — | 900 | 450 | 900 | ||||||||||||||||||||||||

Interest expense, net | 3,034 | 3,510 | 4,162 | 1,492 | 1,926 | 28,564 | 14,119 | 28,401 | ||||||||||||||||||||||||

Amortization (c) | — | — | — | — | — | 9,233 | 4,617 | 9,233 | ||||||||||||||||||||||||

Gain on sale of capital assets | (979 | ) | (218 | ) | (2,265 | ) | (1,480 | ) | (49 | ) | (2,265 | ) | (49 | ) | (834 | ) | ||||||||||||||||

Income (loss) before income taxes | (3,575 | ) | 2,298 | 19,109 | (1,190 | ) | (1,084 | ) | (6,110 | ) | 7,332 | 13,068 | ||||||||||||||||||||

Income taxes | (3,667 | ) | 689 | 6,620 | (421 | ) | (460 | ) | (2,236 | ) | 2,580 | 4,343 | ||||||||||||||||||||

Net earnings (loss) | $ | 92 | $ | 1,609 | $ | 12,489 | $ | (769 | ) | $ | (624 | ) | $ | (3,874 | ) | $ | 4,752 | $ | 8,725 | |||||||||||||

Other Financial Data: | ||||||||||||||||||||||||||||||||

EBITDA (d) | $ | 9,868 | $ | 17,107 | $ | 34,245 | $ | 4,711 | $ | 6,231 | $ | 55,288 | $ | 38,793 | $ | 77,265 | ||||||||||||||||

Capital expenditures | 18,547 | 8,668 | 22,932 | 12,566 | 4,946 | 51,006 | 5,056 | 36,345 | ||||||||||||||||||||||||

Balance Sheet Data (end of period): | ||||||||||||||||||||||||||||||||

Cash | $ | 11,247 | $ | 436 | $ | 651 | $ | 6 | $ | 7,678 | $ | 10,380 | $ | 10,380 | $ | 10,380 | ||||||||||||||||

Total assets | 129,527 | 120,431 | 158,584 | 118,787 | 136,939 | 481,154 | 481,154 | 481,154 | ||||||||||||||||||||||||

Total debt | 54,678 | 50,137 | 63,401 | 62,340 | 60,254 | 311,380 | 311,380 | 311,380 | ||||||||||||||||||||||||

Total shareholder’s equity | 16,770 | 17,379 | 29,818 | 16,855 | 29,194 | 127,500 | 127,500 | 127,500 | ||||||||||||||||||||||||

Operating Data: | ||||||||||||||||||||||||||||||||

Equipment hours | 644,087 | 583,071 | 673,811 | 273,944 | 377,335 | 673,811 | 377,335 | 777,202 | ||||||||||||||||||||||||

| (a) | The management fees represent a distribution of the taxable income of Norama Ltd., our predecessor company, to its corporate shareholder. |

| (b) | Reflects the addition of a new board of directors and the sponsors’ management fee in connection with the transactions. |

| (c) | Intangible assets are being amortized over the useful lives of the related customer contracts, trade names and customer relationships. |

| (d) | EBITDA is defined as earnings before interest expense, income taxes and depreciation and amortization. EBITDA is not a measure of performance under Canadian GAAP or U.S. GAAP. We believe that EBITDA is a meaningful measure of the performance of our business. However, EBITDA does not represent, and should not be used as a substitute for, net income or cash flows from operations as determined in accordance with Canadian GAAP or U.S. GAAP, and EBITDA is not necessarily an indication of whether cash flow will be sufficient to fund our cash requirements. In addition, our definition of EBITDA may differ from that of other companies. EBITDA for the historical periods has been reduced by management fees and equipment leases and rentals as reflected in the statement of operations data above. In connection with the acquisition, these management fees will be terminated upon closing and a substantial portion of our equipment leases and rentals expense also will be terminated as a result of the purchase of the related equipment at closing. |

(footnote continued on next page)

8

Table of Contents

| A reconciliation of EBITDA to net earnings (loss) as set forth in our consolidated statements of operations is as follows: |

| Historical | Pro Forma | |||||||||||||||||||||||||||

| Year Ended March 31, | Six Months Ended September 30, | Year Ended March 31, | Six Months Ended September 30, | Twelve Months Ended September 30, | ||||||||||||||||||||||||

| 2001 | 2002 | 2003 | 2002 | 2003 | 2003 | 2003 | 2003 | |||||||||||||||||||||

| (dollars in thousands) | ||||||||||||||||||||||||||||

Net earnings (loss) | $ | 92 | $ | 1,609 | $ | 12,489 | $ | (769 | ) | $ | (624 | ) | $ | (3,874 | ) | $ | 4,752 | $ | 8,725 | |||||||||

Adjustments: | ||||||||||||||||||||||||||||

Depreciation | 10,409 | 11,299 | 10,974 | 4,409 | 5,389 | 23,601 | 12,725 | 26,563 | ||||||||||||||||||||

Amortization | — | — | — | — | — | 9,233 | 4,617 | 9,233 | ||||||||||||||||||||

Interest expense, net | 3,034 | 3,510 | 4,162 | 1,492 | 1,926 | 28,564 | 14,119 | 28,401 | ||||||||||||||||||||

Income taxes | (3,667 | ) | 689 | 6,620 | (421 | ) | (460 | ) | (2,236 | ) | 2,580 | 4,343 | ||||||||||||||||

EBITDA | $ | 9,868 | $ | 17,107 | $ | 34,245 | $ | 4,711 | $ | 6,231 | $ | 55,288 | $ | 38,793 | $ | 77,265 | ||||||||||||

9

Table of Contents

An investment in the notes entails a high degree of risk. You should carefully consider the following risk factors and other information presented in this prospectus before deciding to purchase the notes.

Risks Related to the Notes and Our Other Indebtedness

Our substantial debt could adversely affect our financial health, make us more vulnerable to adverse economic conditions and prevent us from fulfilling our obligations under the notes or our new credit facility.

We have a significant amount of debt outstanding and significant debt service requirements. As of September 30, 2003, on a pro forma basis, we would have had outstanding $311.4 million of consolidated debt, of which $50 million would have been secured debt. As of the closing of the transactions, we had approximately $60 million of available borrowings under our new credit facility, after giving effect to our approximate $10 million letter of credit. We may, subject to covenants in our existing and future debt agreements, incur additional debt in the future.

Our high level of debt could have important consequences to holders of notes, such as:

| • | limiting our ability to obtain additional financing to fund our working capital, capital expenditures, debt service requirements, potential growth or other purposes; |

| • | limiting our ability to use operating cash flow in other areas of our business because we must dedicate a substantial portion of these funds to make payments on our debt; |

| • | limiting our ability to obtain bonding which is required by some of our customers; |

| • | placing us at a competitive disadvantage compared to competitors with less debt; |

| • | increasing our vulnerability to adverse economic and industry conditions; and |

| • | increasing our vulnerability to increases in interest rates because borrowings under our new credit facility are subject to variable interest rates. |

Our ability to pay interest on the notes and to satisfy our other debt obligations will depend upon, among other things, our future operating performance and our ability to refinance debt when necessary. Each of these factors is to a large extent dependent on economic, financial, competitive and other factors beyond our control. If, in the future, we cannot generate sufficient cash from operations to make scheduled payments on the notes or to meet our other obligations, we will need to refinance some or all of our debt, obtain additional financing or sell assets. We cannot assure you that our business will generate cash flow, or that we will be able to obtain funding, sufficient to satisfy our debt service requirements.

Restrictive covenants in our debt agreements may restrict the manner in which we can operate our business.

Our new credit facility and the indenture governing the notes limit, among other things, our ability and the ability of our restricted subsidiaries to:

| • | incur indebtedness; |

| • | pay dividends, redeem capital stock or make other restricted payments; |

10

Table of Contents

| • | incur liens to secure indebtedness; |

| • | make certain investments; |

| • | sell certain assets; |

| • | enter into transactions with our affiliates; or |

| • | merge with another person or sell substantially all of our assets. |

If we fail to comply with these covenants, we would be in default under our new credit facility and the indenture, and the principal and accrued interest on the notes and our other outstanding indebtedness may become due and payable. See “Description of Bank Credit Agreement” and “Description of Notes—Certain Covenants.” In addition, our new credit facility contains, and our future indebtedness agreements may contain, additional affirmative and negative covenants that are generally more restrictive than those contained in the indenture.

As a result of these covenants, our ability to respond to changes in business and economic conditions and to obtain additional financing, if needed, may be significantly restricted, and we may be prevented from engaging in transactions that might otherwise be considered beneficial to us. Our new credit facility also requires us, and our future credit facilities may require us, to maintain specified financial ratios and satisfy specified financial tests. Our ability to meet these financial ratios and tests can be affected by events beyond our control, and we cannot assure you that we will meet those tests. The breach of any of these covenants could result in a default under our new credit facility. Upon the occurrence of an event of default under our current or future credit facilities, the lenders could elect to declare all amounts outstanding under such credit facilities, including accrued interest or other obligations, to be immediately due and payable. If amounts outstanding under such credit facilities were to be accelerated, our assets may not be sufficient to repay in full that indebtedness and our other indebtedness, including the notes.

The notes and the guarantees are unsecured and effectively subordinated to our and our subsidiary guarantors’ secured indebtedness.

The notes and the related subsidiary guarantees are not secured by any of our assets. As of September 30, 2003, on a pro forma basis, we and our subsidiary guarantors would have had $50.0 million of secured debt outstanding. In addition, the indenture governing the notes permits the incurrence of additional debt, some of which may be secured debt. The notes are effectively subordinated to all secured debt to the extent of the value of the assets securing such debt.

If we become insolvent or are liquidated, or if payment under any secured debt is accelerated, the lenders thereunder would be entitled to exercise the remedies available to a secured lender. Accordingly, the lender will have priority over any claim for payment under the notes or the guarantees to the extent of the assets that constitute its collateral. If this were to occur, it is possible that there would be no assets remaining from which claims of the holders of the notes could be satisfied. Further, if any assets did remain after payments to these lenders, the remaining assets might be insufficient to satisfy the claims of the holders of the notes and holders of other unsecured debt that is deemed the same class as the notes, and potentially all other general creditors who would participate ratably with holders of the notes.

We may be prevented from financing, or may not have the ability to raise funds necessary to finance, the change of control offer required by the indenture.

Upon the occurrence of a change of control, each holder of notes outstanding under the indenture may require us to purchase all or a portion of the notes at a purchase price equal to

11

Table of Contents

101% of the principal amount thereof, plus accrued and unpaid interest. Our ability to purchase the notes upon a change of control event is prohibited by the terms of our new credit facility. Future agreements may contain a similar provision. Upon a change of control event, we may be required to repay immediately the outstanding principal, any accrued interest on and any other amounts owed by us under our new credit facility. We cannot assure you that we would be able to repay amounts outstanding under our new credit facility. Upon a change of control, we may not have sufficient funds available to purchase all of the notes tendered to us. Any requirement to offer to purchase any outstanding notes may result in us having to refinance our outstanding debt or obtain necessary consents under our other debt agreements to repurchase the notes, which we may not be able to do. In such case, our failure to purchase notes following a change of control would constitute an event of default under the indenture, which would, in turn, constitute a default under our new credit facility.

We rely on our subsidiaries for our operating funds, and our subsidiaries have no obligation to supply us with any funds.

We conduct our operations through subsidiaries and are dependent upon our subsidiaries for the funds we need to operate. We are dependent on the transfer of funds from our subsidiaries to make the payments due under the notes. Although our restricted subsidiaries guarantee the notes, each of our subsidiaries is a distinct legal entity and has no obligation, other than the guarantees, to transfer funds to us. Our ability to pay the notes, and the ability of our subsidiaries to transfer funds to us, could be restricted by the terms of subsequent financings. The payment of dividends to us by our subsidiaries is subject to various business considerations as well as contractual provisions which may restrict the payment of dividends and distributions and the transfer of assets to us.

Your ability to transfer the notes may be limited by the absence of an active trading market, and there is no assurance that any active trading market will develop for the notes.

The notes are a new issue of securities for which there is no established trading market. We do not intend to have the notes listed on a national securities exchange or quoted on the National Association of Securities Dealers Automated Quotation System, although the original notes are eligible for trading in the PORTAL MarketSM. At the time of the private placement of the original notes, the initial purchasers advised us that they intend to make a market in the original notes, and, if issued, the exchange notes, as permitted by applicable law; however, the initial purchasers are not obligated to make a market in the original notes or the exchange notes, and they may discontinue their market-making activities at any time without notice. Therefore, we cannot assure you that an active market for the original notes or the exchange notes will develop or, if developed, that it will continue. Historically, the market for non-investment grade debt has been subject to disruptions that have caused substantial volatility in the prices of securities similar to the notes. We cannot assure you that the market, if any, for the original notes or the exchange notes will be free from similar disruptions or that any such disruptions will not adversely affect the prices at which you may sell your notes. In addition, subsequent to their initial issuance, the original notes or the exchange notes may trade at a discount from their initial offering price depending on prevailing interest rates, the market for similar notes, our performance and other factors.

Currency exchange rate fluctuations could adversely affect our ability to repay the notes.

Substantially all of our revenues and costs are incurred in Canadian dollars. However, the obligations represented by the notes are denominated in U.S. dollars. If the Canadian dollar loses value against the U.S. dollar while other factors remain constant, our ability to pay interest and principal on the notes will be diminished.

12

Table of Contents

You may be unable to enforce your rights under U.S. bankruptcy law, and Canadian bankruptcy and insolvency laws may impair the trustee’s ability to enforce remedies under the notes.

We are incorporated under the laws of Canada and our principal operating assets are located outside of the United States. Under bankruptcy laws in the United States, courts typically take jurisdiction over a debtor’s property, wherever located, including property situated in other countries. However, courts outside of the United States may not recognize the U.S. bankruptcy court’s jurisdiction. Accordingly, difficulties may arise in administering a U.S. bankruptcy case involving a Canadian debtor with property located outside the United States, and any orders or judgments of a bankruptcy court in the United States may not be enforceable against such property.

The rights of the indenture trustee and holders of the notes to enforce remedies under the indenture could be delayed by the restructuring provisions of applicable Canadian federal bankruptcy, insolvency and other restructuring legislation if the benefit of such legislation is sought with respect to us. The Canadian Bankruptcy and Insolvency Act provides an “insolvent person” with automatic protection, and the Canadian Companies’ Creditors Arrangement Act allows an “insolvent person” to apply to court for an order granting it protection that could prevent its creditors and others from initiating or continuing proceedings against it while it prepares a proposal or plan of arrangement for approval by those creditors who will be affected by the proposal or plan of arrangement. Such a restructuring plan or proposal, if accepted by the requisite majorities of each affected class of the insolvent person’s creditors and approved by the supervising court, would be binding on the minorities in any such class who vote against the plan or proposal. This restructuring legislation generally permits the insolvent debtor to retain possession and administration of its property, even though it may be in default under the applicable debt instrument during the period that the protection against proceedings remains in force.

During the stay period, the indenture trustee and holders of the notes are likely to be restrained from enforcing remedies under the indenture and payments under the notes are unlikely to be made. It is equally unlikely that holders of the notes would be compensated for any delay in payment, if any, of principal or interest other than a right to claim accrued and unpaid interest on the amounts owing under the notes and the indenture, unless the right is itself compromised under any restructuring plan or proposal approved by creditors and the court.

The market value of your original notes may be lower if you do not exchange your original notes or fail to properly tender your original notes for exchange.

To the extent that original notes are tendered and accepted for exchange pursuant to the exchange offer, the trading market for original notes that remain outstanding may be significantly more limited, which might adversely affect the liquidity of the original notes not tendered for exchange. The extent of the market and the availability of price quotations for original notes will depend upon a number of factors, including the number of holders of original notes remaining at such time and the interest in maintaining a market in such original notes on the part of securities firms. An issue of securities with a smaller outstanding market value available for trading, called the “float,” may command a lower price than would a comparable issue of securities with a greater float. Therefore, the market price for original notes that are not exchanged in the exchange offer may be affected adversely to the extent that the amount of original notes exchanged pursuant to the exchange offer reduces the float. The reduced float also may tend to make the trading price of the original notes that are not exchanged more volatile.

13

Table of Contents

Issuance of the exchange notes in exchange for the original notes pursuant to the exchange offer will be made following the prior satisfaction, or waiver, of the conditions set forth in “The Exchange Offer—Conditions to the Exchange Offer” and only after timely receipt by the exchange agent of such original notes, a properly completed and duly executed letter of transmittal and all other required documents. Therefore, holders of original notes desiring to tender such original notes in exchange for exchange notes should allow sufficient time to ensure timely delivery of all required documentation. Neither we, the exchange agent nor any other person is under any duty to give notification of defects or irregularities with respect to the tenders of original notes for exchange. Original notes that may be tendered in the exchange offer but which are not validly tendered will, following the consummation of the exchange offer, remain outstanding and will continue to be subject to the same transfer restrictions currently applicable to such original notes.

Risks Related to Our Business

We rely on a small number of customers from whom we receive a significant amount of our revenues.

We provide our services primarily to a small number of major integrated and independent oil and gas and other natural resources companies operating in western Canada. Revenue from our four largest customers represented approximately 94% of our total revenue for the twelve months ended September 30, 2003 and those customers are expected to continue to provide a significant percentage of our revenues in the future. Each year any one of our customers may constitute a significant portion of our revenue. For example, for the twelve months ended September 30, 2003, revenue generated from work for Syncrude constituted approximately 65% of our total revenue primarily due to several large projects with Syncrude and our status as one of their preferred contractors. We may not be able to replace the work generated by these projects with work from other customers. Our services to our customers are typically provided under contracts with terms ranging from six months to five years, some of which have terms allowing for automatic or optional renewals of the contract. However, a significant number of our contracts terminate upon completion of the project without having a definite termination date, and the contracts typically allow the customer to reduce or eliminate the work which we are to perform. In addition, the customers may choose not to extend the existing contracts or enter into new contracts. The loss of or significant reduction in business with one or more of these customers could have a material adverse effect on our business.

A significant amount of our revenues are generated by providing non-recurring services.

Approximately 60% of our revenue for the fiscal year ended March 31, 2003 was derived from projects which we consider to be non-recurring. This revenue primarily relates to site preparation and piling services provided for the construction of extraction, upgrading and other oil sands mining infrastructure projects. Future revenues from these types of services will depend upon customers expanding existing mines and developing new projects.

We are dependent upon continued outsourcing by our customers of site preparation and mining services.

Outsourced site preparation and mining services constitute a large portion of the work we perform for our customers. For example, our mining project revenues constituted approximately 29%, 52% and 33% of our revenues in the fiscal years ended March 31, 2003, 2002 and 2001, respectively. The election by one or more of our customers to perform some or all of these services themselves, rather than outsourcing the work to us, could have a material adverse impact on our business.

14

Table of Contents

Our operations are subject to weather-related factors that may cause delays in our completion of projects.

Because our operations are located in western Canada, we are often subject to extreme weather conditions. While our operations are not significantly affected by normal seasonal weather patterns, extreme weather, including heavy rain and snow, can cause us to delay the completion of a project, which could result in lower margins than estimated.

Changes in oil and gas prices could cause our customers to slow down or curtail their current production and future expansions which would in turn reduce our revenue from those customers.

The profitability and growth of our customers may be impacted by the prices of oil and gas. Prices for oil are subject to large fluctuations in response to relatively minor changes in the supply of and demand for oil, market uncertainty and a variety of additional factors beyond our control. Such factors include weather conditions, the condition of the Canadian and U.S. economies, the actions of the Organization of Petroleum Exporting Countries, governmental regulation, political stability in the Middle East, war or the threat of war in oil producing regions, the foreign supply of oil and the availability of fuel from alternate sources. In addition, our customers make their major expansion investment decisions based on their long-term outlook for the prices of oil and gas and their profitability based on those prices. If they believe the prices of those commodities will remain at depressed levels or that their profitability will be adversely affected by fluctuations in currency exchange rates, they may delay or curtail their current expansion plans. Such a delay or curtailment could have a material adverse impact on our financial condition and results of operations.

Insufficient pipeline and refining capacity for heavy crude products could cause our customers to slow down or curtail their current production and future expansions which would, in turn, reduce our revenue from those customers.

While current pipeline capacity is sufficient to transport existing oil sands production to market, future production growth will require increased pipeline capacity. If such increases do not materialize, our customers may be unable to efficiently deliver increased production to market. Additionally, we expect that increases in oil sands production will require added heavy crude oil refinery capacity. Similarly, if such increased capacity or alternative markets do not materialize, future growth in demand for our customers’ products could be reduced.

Penalty clauses in our customer contracts could expose us to losses if total project costs exceed original estimates or if projects are not completed by specified completion date milestones.

A portion of our revenue is derived from contracts which have performance incentives and penalties depending on the total cost of a project as compared to the original estimate. We could incur significant penalties based on cost overruns. In addition, the total project cost as defined in the contract may include not only our work, but also work performed by other contractors. As a result, we could incur penalties due to work performed by others over which we have no control. We may also incur penalties if projects are not completed by specified completion date milestones. Such penalties, if incurred, could have a significant impact on our profitability under these contracts.

15

Table of Contents

Because most of our customers are located or operate in western Canada, a downturn in the energy industry in western Canada could result in a decrease in the demand for our services by our customers.

Most of our customers are located or operate in western Canada. In the fiscal year ended March 31, 2003, we generated approximately 80% of our operating revenues from the Alberta oil sands. A downturn in the energy industry in western Canada could cause our customers to slow down or curtail their current production and future expansions which would, in turn, reduce our revenue from those customers. Such a delay or curtailment could have a material adverse impact on our financial condition and results of operations.

Shortages of skilled labor, work stoppages or other labor disruptions at our operations or those of our principal customers or service providers could have an adverse effect on our profitability and financial condition.

Our ability to provide high-quality services on a timely basis requires an adequate number of skilled workers such as engineers, trades people and equipment operators. We cannot assure you that we will be able to maintain an adequate skilled labor force or that our labor expenses will not increase. A shortage of skilled labor would require us to curtail our planned internal growth or may require us to use less skilled labor which could adversely affect our ability to perform work.

Substantially all of our hourly employees are subject to collective bargaining agreements to which we are a party or are otherwise subject because of a bargaining relationship with the particular trade union that is a party to the collective bargaining agreement. Any work stoppage resulting from a strike or lockout could have a material adverse effect on our financial condition and results of operations.

In the province of Alberta, collective bargaining in the construction industry is subject to registration. A registered employer’s organization which has been registered by the Labour Relations Board bargains with the trade unions named in the certificate on behalf of all employers who work in that part of the construction industry described in the certificate with whom the unions have a bargaining relationship. Any collective agreement entered into by the employer’s organization is binding on all such employers. The primary term of some of these collective agreements has expired, however the agreements continue in force from year to year until they are terminated by a strike or lockout. Negotiations are underway between representatives of the employers organization and the union in respect of some of these agreements. We cannot assure you that new agreements will be reached without a work stoppage or that, if reached, the terms will not significantly increase our costs. We do not have control over the terms of such agreements but will be bound by these because of registration.

In addition, our customers employ workers under the same and other collective bargaining agreements. Any work stoppage or labor disruption at our key customers could significantly reduce the amount of services that we provide.

Demand for our services may be adversely impacted by regulations affecting the energy industry.

Our principal customers are energy companies involved in the development of the Alberta oil sands and natural gas production. The operations of these companies, including the mining operations in the oil sands, are subject to or impacted by a wide array of regulations in the jurisdictions where they operate, including those directly impacting mining activities and those

16

Table of Contents

indirectly affecting their businesses, such as applicable environmental laws. As a result of changes in regulations and laws relating to the energy production industry including the operation of mines, our customers’ operations could be disrupted or curtailed by governmental authorities. The high cost of compliance with applicable regulations may induce customers to discontinue or limit their operations, and may discourage companies from continuing development activities. As a result, demand for our services could be substantially affected by regulations adversely impacting the energy industry.

Our operations expose us to potential environmental liabilities.

Our operations are subject to numerous environmental protection laws and regulations that are complex and stringent. Contracts with our customers require us to operate in compliance with these laws and regulations. We regularly perform work in and around sensitive environmental areas such as rivers, lakes and forests. Significant fines and penalties may be imposed on us or our customers for non-compliance with environmental laws and regulations, and our contracts generally require us to indemnify our customers for environmental claims suffered by them as a result of our actions. In addition, some environmental laws provide for joint and several strict liability for remediation of releases of hazardous substances, rendering a person liable for environmental damage, without regard to negligence or fault on the part of such person. In addition to potential liabilities that may be incurred in satisfying these requirements, we may be subject to claims alleging personal injury or property damage as a result of alleged exposure to hazardous substances. These laws and regulations may expose us to liability arising out of the conduct of operations or conditions caused by others, or for our acts which were in compliance with all applicable laws at the time these acts were performed.

We own, or lease, and operate several properties that have been used for a number of years for the storage and maintenance of equipment and other industrial uses upon which fuel may have been spilled, or hydrocarbons or other wastes which may have been disposed of or released. Any release of substances by us or by third parties who previously operated on these properties may be subject to laws which impose joint and several liability, without regard to fault or the legality of the original conduct, on certain classes of persons who are considered to be responsible for the release of hazardous substances into the environment. Under such laws, we could be required to remove or remediate previously disposed wastes and clean up contaminated property.

We operate in a highly competitive industry where our growth could be impeded.

Approximately 80% of the major projects that we pursue are awarded to us based on bid proposals. We may compete in the future for these projects against companies that may have substantially greater financial and other resources than we do. Some smaller competitors may have lower overhead cost structures and may be able to provide their services at lower rates than we can. Further, public sector work is often performed by governmental agencies. Our growth may be impacted to the extent that we are unable to successfully bid against these companies.

Fixed price contracts with our customers could expose us to losses if our estimates of project costs are too low or if we fail to perform within our cost estimates.

A portion of our revenue is derived from fixed price (lump sum) contracts. The terms of these contracts require us to guarantee the price of the services we provide and assume the risk that our costs to perform the services and provide the materials will be greater than anticipated. Our profitability in this market is therefore dependent upon our ability to accurately predict the

17

Table of Contents

costs associated with our services. These costs may be affected by a variety of factors, some of which may be beyond our control. If we are unable to accurately estimate the costs of fixed price contracts, or if we incur unrecoverable cost overruns, some projects could have lower margins than anticipated or even incur losses, which could have a material adverse effect on our business. Approximately 5% of our revenue for the twelve months ended September 30, 2003 was derived from fixed price contracts.

Our projects expose us to potential professional liability, product liability, warranty or other claims.

We install deep foundations in congested areas and provide construction management services for significant projects. Notwithstanding the fact that we will generally not accept liability for consequential damages in our contracts, any catastrophic occurrence in excess of insurance limits at projects where our structures are installed or services are performed could result in significant professional liability, product liability, warranty or other claims against us. Such liabilities could potentially exceed our current insurance coverage and the fees we derive from those services. A partially or completely uninsured claim, if successful and of a significant magnitude, could result in substantial losses.

If our access to the surety market were to be restricted in the future, our business could be impaired.

Like all businesses providing similar services, we are at times required to post bid or performance bonds issued by a financial institution known as a surety. The surety industry experiences periods of unsettled and volatile markets, usually in the aftermath of substantial loss exposures or corporate bankruptcies with significant surety exposure. Historically, these types of events have caused reinsurers and sureties to reevaluate their committed levels of underwriting and required returns. As needed in the ordinary course of business, we have been able to secure necessary bonds and we will seek opportunities to expand our surety relationships. However, if for any reason our bonding capacity becomes insufficient to satisfy our future bonding requirements, our business could be impaired.

Cost overruns by our customers on their projects may cause our customers to terminate future projects or expansions which could adversely affect the amount of work we receive from those customers.

Oil sands development projects require substantial capital expenditures. In the past, several of our customers’ projects have experienced significant cost overruns, impacting their returns. As new projects are contemplated or built, if cost overruns continue to challenge our customers, they could reassess future projects and expansions which could adversely affect the amount of work we receive from our customers, causing an adverse effect on our financial condition.

We may not be able to achieve the expected benefits from any future acquisitions, which would adversely affect our financial condition and results of operations.

We intend to pursue selective acquisitions as a method of expanding our business. If we do not successfully integrate acquisitions, we may not realize anticipated operating advantages and cost savings. The integration of companies that have previously operated separately involves a number of risks, including:

| • | demands on management related to the increase in our size after an acquisition; |

| • | the diversion of our management’s attention from the management of daily operations; |

18

Table of Contents

| • | difficulties in implementing or unanticipated costs of accounting, estimating, reporting and other systems; |

| • | difficulties in the assimilation and retention of employees; and |

| • | potential adverse effects on operating results. |

We may not be able to maintain the levels of operating efficiency that acquired companies will have achieved or might achieve separately. Successful integration of each of their operations will depend upon our ability to manage those operations and to eliminate redundant and excess costs. Because of difficulties in combining operations, we may not be able to achieve the cost savings and other size-related benefits that we hoped to achieve after these acquisitions which would harm our financial condition and results of operations.

Loss of key personnel could adversely affect our business.

Many of our senior officers and key employees are important to our management and direction. Our future success depends on our ability to retain these officers and key employees. Although we believe that we will continue to be able to attract and retain other talented personnel and replace key personnel should the need arise, competition in recruiting replacement personnel could be significant. If we are not successful in retaining our key personnel or replacing them, our business, financial condition or results of operations could be adversely affected. We do not maintain key personnel insurance.

Aboriginal peoples may make claims against our customers or their projects regarding the lands on which their projects are located.

Aboriginal peoples have claimed aboriginal title and rights to a substantial portion of western Canada. Although we are not aware of any such claims against our customers, such claims, if successful, could have an adverse effect on our customers which may, in turn, negatively impact our business.

19

Table of Contents

Registration Rights

At the closing of the offering of the original notes, we entered into the registration rights agreement with the initial purchasers pursuant to which we agreed, for the benefit of the holders of the original notes, at our cost,

| • | within 90 days after the date of the original issuance of the original notes, to file an exchange offer registration statement with the SEC with respect to the exchange offer for the exchange notes, and |

| • | to use our reasonable efforts to cause the exchange offer registration statement to be declared effective under the Securities Act within 190 days after the date of original issuance of the original notes. |

Upon the exchange offer registration statement being declared effective, we agreed to offer the exchange notes in exchange for surrender of the original notes. We agreed to keep the exchange offer open for not less than 30 days, or longer if required by applicable law.

For each original note surrendered to us pursuant to the exchange offer, the holder of such original note will receive an exchange note having a principal amount equal to that of the surrendered original note. Interest on each exchange note will accrue from the last interest payment date on which interest was paid on the original note surrendered in exchange therefor or, if no interest has been paid on such original note, from the date of its original issue. The registration rights agreement also provides an agreement to include in the prospectus for the exchange offer certain information necessary to allow a broker-dealer who holds original notes that were acquired for its own account as a result of market-making activities or other ordinary course trading activities (other than original notes acquired directly from us or one of our affiliates) to exchange such original notes pursuant to the exchange offer and to satisfy the prospectus delivery requirements in connection with resales of exchange notes received by such broker-dealer in the exchange offer. We agreed to maintain the effectiveness of the registration statement for these purposes for 180 days.

The preceding agreement is needed because any broker-dealer who acquires original notes for its own account as a result of market-making activities or other trading activities is required to deliver a prospectus meeting the requirements of the Securities Act. This prospectus covers the offer and sale of the exchange notes pursuant to the exchange offer made pursuant to this prospectus and the resale of exchange notes received in the exchange offer by any broker-dealer who held original notes acquired for its own account as a result of market-making activities or other trading activities other than original notes acquired directly from us or one of our affiliates.

Under existing interpretations of the staff of the SEC contained in several no-action letters to third parties, the exchange notes will in general be freely tradeable after the exchange offer without further registration under the Securities Act. However, any purchaser of original notes who is an “affiliate” of ours or who intends to participate in the exchange offer for the purpose of distributing the related exchange notes

| • | will not be able to rely on the interpretation of the staff of the SEC, |

| • | will not be able to tender its original notes in the exchange offer, and |

| • | must comply with the registration and prospectus delivery requirements of the Securities Act in connection with any sale or transfer of the original notes unless such sale or transfer is made pursuant to an exemption from such requirements. |

20

Table of Contents

Each holder of the original notes, other than certain specified holders, who wishes to exchange original notes for exchange notes in the exchange offer will be required to make certain representations, including that

| • | it is not an affiliate of ours, |

| • | any exchange notes to be received by it were acquired in the ordinary course of its business, and |

| • | at the time of commencement of the exchange offer, it has no arrangement with any person to participate in the distribution (within the meaning of the Securities Act) of the exchange notes. |

In the event that any changes in law or the applicable interpretations of the staff of the SEC do not permit us to effect the exchange offer, or if under various circumstances, some holders of original notes so request, or in the case of any holder that participates in the exchange offer, such holder does not receive exchange notes on the date of the exchange that may be sold without restriction under U.S. state and federal securities laws, other than due solely to the status of such holder as an affiliate of us, we will, at our cost,

| • | as promptly as practicable, file a shelf registration statement (which may be an amendment of the registration statement of which this prospectus is a part) covering resales of the original notes, |

| • | use our reasonable efforts to cause the shelf registration statement to be declared effective under the Securities Act, and |

| • | use all reasonable efforts to keep effective the shelf registration statement until the earlier of two years after the date of original issuance of the original notes, the date the notes become eligible for resale without volume restrictions under Rule 144 under the Securities Act, or until all notes covered by the shelf registration statement have been sold. |