Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| | |

| (Mark One) | | |

ý |

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2011 |

or |

o |

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

|

Commission File Number: 001-32330

NorthStar Realty Finance Corp.

(Exact Name of Registrant as Specified in its Charter)

| | |

Maryland

(State or Other Jurisdiction of

Incorporation or Organization) | | 11-3707493

(IRS Employer

Identification No.) |

399 Park Avenue, 18th Floor New York, NY 10022

(Address of Principal Executive Offices, Including Zip Code) |

(212) 547-2600

(Registrant's Telephone Number, Including Area Code)

|

Securities registered pursuant to Section 12(b) of the Act:

| | |

| Title of Class | | Name of Each Exchange on Which Registered |

|---|

| Common Stock, $0.01 par value | | New York Stock Exchange |

| Preferred Stock, 8.75% Series A Cumulative Redeemable, $0.01 par value | | New York Stock Exchange |

| Preferred Stock, 8.25% Series B Cumulative Redeemable, $0.01 par value | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definition of "large accelerated filer," "accelerate filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| | | | | | |

| Large accelerated filero | | Accelerated filerý | | Non-accelerated filero

(Do not check if a

smaller reporting company) | | Smaller reporting companyo |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

The aggregate market value of the registrant's voting and non-voting common equity held by non-affiliates of the registrant as of June 30, 2011, was $385,112,245. As of February 14, 2012, the registrant had issued and outstanding 96,083,488 shares of common stock, par value $0.01 per share.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive proxy statement for the registrant's 2012 Annual Meeting of Stockholders to be filed within 120 days after the end of the registrant's fiscal year ending December 31, 2011, are incorporated by reference into this Annual Report on Form 10-K in response to Part III, Items 10, 11, 12, 13 and 14.

INDEX

| | | | |

| |

| | Page |

|---|

PART I |

Item 1. | | Business | | 5 |

Item 1A. | | Risk Factors | | 18 |

Item 1B. | | Unresolved Staff Comments | | 65 |

Item 2. | | Properties | | 66 |

Item 3. | | Legal Proceedings | | 68 |

PART II |

Item 4. | | Mine Safety Disclosures | | 69 |

Item 5. | | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | | 69 |

Item 6. | | Selected Financial Data | | 70 |

Item 7. | | Management's Discussion and Analysis of Financial Condition and Results of Operations | | 73 |

Item 7A. | | Quantitative and Qualitative Disclosures About Market Risk | | 99 |

Item 8. | | Financial Statements and Supplementary Data | | 103 |

Item 9. | | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | | 182 |

Item 9A. | | Controls and Procedures | | 182 |

Item 9B. | | Other Information | | 183 |

PART III |

Item 10. | | Directors, Executive Officers and Corporate Governance | | 184 |

Item 11. | | Executive Compensation | | 184 |

Item 12. | | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | | 184 |

Item 13. | | Certain Relationships and Related Transactions and Directors Independence | | 184 |

Item 14. | | Principal Accountant Fees and Services | | 184 |

PART IV |

Item 15. | | Exhibits and Financial Statement Schedules | | 185 |

2

Table of Contents

FORWARD LOOKING STATEMENTS

This Annual Report on Form 10-K contains certain "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, or Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or Exchange Act. Forward-looking statements are generally identifiable by use of forward-looking terminology such as "may," "will," "should," "potential," "intend," "expect," "seek," "anticipate," "estimate," "believe," "could," "project," "predict," "continue," "future" or other similar words or expressions. Forward-looking statements are not guarantees of performance and are based on certain assumptions, discuss future expectations, describe plans and strategies, contain projections of results of operations or of financial condition or state other forward-looking information. Such statements include, but are not limited to, those relating to the operating performance of our investments, our financing needs, the effects of our current strategies, loan and securities activities, our ability to manage our collateralized debt obligations, or CDOs, and our ability to raise capital. Our ability to predict results or the actual effect of plans or strategies is inherently uncertain, particularly given the economic environment. Although we believe that the expectations reflected in such forward-looking statements are based on reasonable assumptions, our actual results and performance could differ materially from those set forth in the forward-looking statements and you should not unduly rely on these statements. These forward-looking statements involve risks, uncertainties and other factors that may cause our actual results in future periods to differ materially from those forward looking statements. These factors include, but are not limited to:

- •

- adverse economic conditions and the impact on the commercial real estate finance industry;

- •

- access to debt and equity capital and our liquidity;

- •

- our use of leverage;

- •

- our ability to meet various coverage tests with respect to our CDOs;

- •

- our ability to obtain mortgage financing on our net lease properties;

- •

- the affect of economic conditions on the valuations of our investments;

- •

- the impact of economic conditions on the borrowers of the commercial real estate debt we originate and the commercial mortgage loans underlying the commercial mortgage backed securities in which we invest;

- •

- any failure in our due diligence to identify all relevant facts in our underwriting process or otherwise;

- •

- credit rating downgrades;

- •

- tenant or borrower defaults or bankruptcy;

- •

- illiquidity of properties in our portfolio;

- •

- environmental compliance costs and liabilities;

- •

- effect of regulatory actions, litigation and contractual claims against us and our affiliates, including the potential settlement and litigation of such claims;

- •

- competition for investment opportunities;

- •

- regulatory requirements with respect to our business and the related cost of compliance;

- •

- the impact of any conflicts arising from our asset management business;

- •

- the ability to raise capital for the non-listed real estate investment trusts, or REITs, we sponsor;

3

Table of Contents

- •

- changes in laws or regulations governing various aspects of our business;

- •

- the loss of our exemption from the definition of "investment company" under the Investment Company Act of 1940, as amended;

- •

- competition for qualified personnel and our ability to retain key personnel;

- •

- the effectiveness of our risk management systems;

- •

- failure to maintain effective internal controls;

- •

- compliance with the rules governing REITs; and

- •

- the factors described in Item 1A. of this Annual Report on Form 10-K under the heading "Risk Factors."

The foregoing list of factors is not exhaustive. All forward-looking statements included in this Annual Report on Form 10-K are based upon information available to us on the date hereof and we are under no duty to update any of the forward-looking statements after the date of this report to conform these statements to actual results.

Factors that could have a material adverse effect on our operations and future prospects are set forth in "Risk Factors" in this Annual Report on Form 10-K beginning on page 18. The factors set forth in the Risk Factors section could cause our actual results to differ significantly from those contained in any forward-looking statement contained in this report.

4

Table of Contents

PART I

Item 1. Business

References to "we," "us" or "our" refer to NorthStar Realty Finance Corp. and its subsidiaries unless context specifically requires otherwise.

Overview

We are an internally managed real estate finance company formed in October 2003 that originates, acquires and manages portfolios of commercial real estate debt, commercial real estate securities and net lease properties. In addition, we engage in asset management and other activities related to real estate and real estate finance.

Our primary business objectives are to make real estate-related investments in order to produce attractive risk-adjusted returns, generate stable cash flows for distribution to our stockholders and build long-term franchise value. We believe that the combination of our commercial real estate, or CRE, credit underwriting and capital markets expertise provides us with a competitive advantage in the marketplace. Our businesses are complementary to each other due to their overlapping sources of investment opportunities, common reliance on CRE fundamentals and application of similar asset management skills to maximize value and to protect capital.

We use asset-level financing as part of our strategy and we seek to match-fund our assets and liabilities by having similar maturities and like-kind interest rate benchmarks (fixed or floating) to manage refinancing and interest rate risk. Our CRE debt and securities portfolios are predominantly financed through long-term, non-recourse collateralized debt obligations, or CDOs, while our net lease properties are predominantly financed with non-recourse mortgage notes.

We seek to meet our objectives by actively managing portfolio credit to preserve capital, generating and recycling liquidity from existing assets and prudently accessing new debt and equity capital for our businesses. We also explore other opportunistic investments such as repurchasing our own CDO bonds at a discount to par.

The capital and equity markets have been negatively impacted by the liquidity and credit crisis which began with the collapse of the residential real estate sector in 2007. Despite some improvement in 2011, the U.S. economy is continuing to experience high unemployment and slow growth compared to historical periods. Additionally, disruptions in the global economy, whether as a result of the Euro-zone debt crisis or otherwise, may also have a negative impact on the CRE market domestically. We expect the commercial real estate finance markets to continue to be challenged in 2012. However, despite the difficult U.S. and global economic conditions, investor interest has been returning to commercial real estate especially in urban areas having high concentrations of institutional quality real estate, and especially in certain asset types such as apartments. In response to these conditions, beginning in 2007, most of our new investment activities were funded using proceeds from repayments and sales of investments within our portfolio. When liquidity became available in the first half of 2011, we raised $232 million including $69 million net proceeds of equity capital and $163 million of exchangeable senior notes due March 2016. Then, in the fourth quarter 2011, we, through two wholly-owned subsidiaries, entered into two new $100 million term credit facilities to finance loan originations and make investments in commercial mortgage backed securities, or CMBS, respectively.

We are also focused on building our asset management business by raising and managing capital on a fee basis from alternate sources, such as the non-listed real estate investment trust sector, which we refer to as our Sponsored REITs. Currently, we are raising capital for NorthStar Real Estate Income Trust, Inc., or NSREIT, our CRE debt-oriented Sponsored REIT. In addition, we have a healthcare debt and equity investment focused product in registration, NorthStar Senior Care Trust, Inc., or Senior Care. During 2011, our capital raising efforts in NSREIT picked up significant

5

Table of Contents

momentum and we believe that our unique investment strategy and expertise are the principal drivers of that momentum. If we can successfully raise capital for our Sponsored REITs, we believe that we could generate substantial incremental cash flows to our stockholders without any significant capital at risk. We also believe our strategy of raising and managing capital on a fee basis in the non-listed REIT sector makes us less reliant on the traditional public equity markets to grow our business.

Our stock is traded on the New York Stock Exchange under the symbol "NRF." We conduct our operations so as to qualify as a real estate investment trust, or REIT, for federal income tax purposes.

Our Investments

The following describes the major CRE asset classes in which we invest and continue to actively manage to maximize stockholder value and to preserve our capital. For financial information regarding our reportable segments, refer to Note 17, Segment Reporting, in our accompanying Consolidated Financial Statements for the year ended December 31, 2011 included in Part II, Item 8. "Financial Statements and Supplementary Data."

The following table represents our assets under management as of December 31, 2011 based on principal amount of CRE debt and security investments and the cost basis of net lease properties (amounts in thousands):

| | | | | | | |

| | Amount | | Percentage | |

|---|

CRE Debt | | | | | | | |

First mortgage loans | | $ | 1,552,066 | | | 22.1 | % |

Mezzanine loans | | | 426,709 | | | 6.1 | % |

Credit tenant and term loans | | | 216,868 | | | 3.1 | % |

Subordinate mortgage interests | | | 159,289 | | | 2.3 | % |

Other(1) | | | 298,693 | | | 4.3 | % |

| | | | | | |

Total CRE debt | | | 2,653,625 | | | 37.9 | % |

CRE Securities | | | | | | | |

CMBS | | | 2,767,828 | | | 39.5 | % |

Third-party CDO notes | | | 269,081 | | | 3.8 | % |

Other securities | | | 197,236 | | | 2.8 | % |

| | | | | | |

Total CRE securities | | | 3,234,145 | | | 46.1 | % |

Net Lease | | | | | | | |

Core net lease | | | 404,427 | | | 5.8 | % |

Healthcare net lease | | | 552,415 | | | 7.9 | % |

| | | | | | |

Total net lease | | | 956,842 | | | 13.7 | % |

| | | | | | |

Subtotal NorthStar | | | 6,844,612 | | | 97.7 | % |

| | | | | | |

Sponsored REITs | | | | | | | |

NSREIT(2) | | | 169,365 | | | 2.3 | % |

| | | | | | |

Grand total | | $ | 7,013,977 | | | 100.0 | % |

| | | | | | |

- (1)

- Primarily relates to real estate owned (either directly or through a joint venture) as a result of foreclosure, presented at the principal amount of such loan at time of foreclosure.

- (2)

- Based on consolidated total assets.

6

Table of Contents

Commercial Real Estate Debt

Overview

Our CRE debt business is focused on originating, structuring, acquiring and managing senior and subordinate debt investments secured primarily by commercial and multifamily properties, including first mortgage loans, subordinate mortgage interests, mezzanine loans, credit tenant loans and other loans, including preferred equity interests in borrowers who own such properties. The collateral underlying our CRE debt investments consists primarily of income-producing real estate assets, properties that require some capital investment to increase cash flows or assets undergoing repositionings or conversions. We generally hold these instruments for investment, however, from time-to-time, we may syndicate or sell portions of loans to maximize risk adjusted returns, manage credit exposure and generate liquidity.

We emphasize direct origination of our debt investments as this allows us a greater degree of control over how they are underwritten and structured and it provides us the opportunity to syndicate senior or subordinate interests in the loan, if desired. Further, it allows us to maintain a more direct relationship with our borrowers which helps us maintain a robust pipeline, provides an opportunity for us to earn origination and other fees and offers us an important advantage when considering any potential future modifications or restructurings. We directly underwrote and originated approximately 77% of our current CRE debt investments (excluding our CRE debt investments in the CSE RE 2006-A CDO, or CSE CDO, and CapLease 2005-1 CDO, or CapLease CDO).

We believe that the continued limited availability of debt capital for commercial real estate along with the challenging U.S. and global economic conditions present opportunities for us to obtain attractive terms for both new directly-originated loans and from pre-existing loans acquired from third-party originators, who may be motivated to sell due to liquidity needs or who are exiting the business.

We believe we have built a franchise with a reputation for providing capital to high-quality real estate owners who want a responsive and flexible balance sheet lender. Given that we are a lender who does not generally seek to sell or syndicate the full amount of the loans we originate, we are able to maintain flexibility in how we structure loans to meet the needs of our borrowers. Typical CMBS and other capital markets driven lenders generally could not provide these types of loans due to constraints within their funding structures and because of their requirement to sell the entire loan to third parties and relinquish all control. Our centralized investment organization has enabled senior management to review potential new loans early in the origination process which, unlike many large institutional lenders with several levels of approval required to commit to a loan, allows us to respond quickly and provide a high degree of certainty to our borrowers that we would close a loan on terms substantially similar to those initially proposed. We believe that this level of service has enhanced our reputation in the marketplace. In addition, we believe the early and active role of senior management in our investment and risk management process has been key to maximizing recoveries of invested capital from our investments and our ability to be responsive to changing market conditions.

Underwriting Process

We use a rigorous investment and underwriting process that has been developed and utilized by our senior management team leveraging their extensive commercial real estate expertise over many years and focuses on the following factors designed to ensure each investment is being evaluated appropriately: (i) macroeconomic conditions that may influence operating performance; (ii) fundamental analysis of the underlying real estate collateral, including tenant rosters, lease terms, zoning, operating costs and the asset's overall competitive position in its market; (iii) real estate market factors that may influence the economic performance of the collateral including leasing conditions; (iv) the operating expertise and financial strength of the sponsor or borrower; (v) the cash flow in place and projected to be in place over the term of the loan; (vi) the appropriateness of estimated costs

7

Table of Contents

associated with rehabilitation; (vii) a valuation of the property, our investment basis relative to its value and the ability to liquidate an investment through a sale or refinancing of the underlying asset; (viii) review of third-party reports including appraisals, engineering and environmental reports; (ix) physical inspections of properties and markets; (x) the overall legal structure of the investment, contractual implications and the lenders' rights; and (xi) the tax and accounting impact.

Our Portfolio

As of December 31, 2011, $2.7 billion, or 37.9%, of our assets under management were invested in CRE debt, which includes $299 million principal amount of loans related to certain investments accounted for as joint ventures and real estate owned. Our CRE debt portfolio, excluding amounts related to joint ventures and real estate owned, was comprised of the following (amounts in thousands):

| | | | | | | | | | | | | | | | | | | | | | |

| |

| |

| |

| |

| | Weighted Average | |

|---|

Asset Type: | | Number | | Principal

Amount | | Carrying

Value(1) | | Allocation by

Investment

Type(2) | | Fixed Rate | | Spread

Over | | Spread

Over Prime | |

|---|

First mortgage loans | | | 75 | | $ | 1,552,066 | | $ | 1,094,957 | | | 65.9 | % | | 4.77 | % | | 2.72 | % | | 3.30 | % |

Mezzanine loans | | | 17 | | | 426,709 | | | 334,317 | | | 18.1 | % | | 6.43 | % | | 2.21 | % | | — | |

Subordinate mortgage interests | | | 9 | | | 159,289 | | | 96,565 | | | 6.8 | % | | 6.40 | % | | 3.51 | % | | — | |

Credit tenant loans | | | 55 | | | 147,426 | | | 140,342 | | | 6.3 | % | | 6.49 | % | | — | | | — | |

Term loans | | | 6 | | | 69,442 | | | 44,401 | | | 2.9 | % | | 7.75 | % | | 3.50 | % | | — | |

| | | | | | | | | | | | | | | | |

Total/Weighted average | | | 162 | | $ | 2,354,932 | | $ | 1,710,582 | | | 100.0 | % | | 6.21 | % | | 2.70 | % | | 3.30 | % |

| | | | | | | | | | | | | | | | |

- (1)

- $1.6 billion in carrying value served as collateral for our consolidated CDO financing transactions and the remainder is unleveraged.

- (2)

- Based on principal amount.

As of December 31, 2011, our $2.4 billion CRE debt portfolio consisted of 162 investments with an average investment size of $14 million.

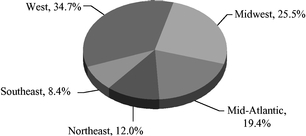

The portfolio's diversity across property type and geographic location is summarized as follows, based on outstanding principal amount:

| | |

| |

|

|---|

Loan Portfolio by Property Type | | Loan Portfolio by Geographic Location |

| |

|

Commercial Real Estate Securities

Overview

Our CRE securities business is focused on investing in and managing a wide range of CRE securities, including CMBS, unsecured REIT debt and CDO notes backed primarily by CRE securities and debt. Substantially all of our securities have explicit credit ratings assigned by at least one of the

8

Table of Contents

major rating agencies (Moody's Investors Services, Standard & Poor's, Fitch Ratings, Morningstar, DBRS and Kroll, generally referred to as rating agencies) and were typically originally rated investment grade.

We seek to mitigate credit risk through fundamental CRE credit analysis, subordination and diversification. CMBS investments financed with our credit facility are AAA-rated while most of our other CMBS investments are generally junior in right of payment of interest and principal to one or more senior classes but benefit from the support of one or more subordinate classes of securities or other forms of credit support within a securitization transaction. Further, to the extent we become controlling classholder in the future for a CMBS investment, we may appoint ourselves special servicer which would enable us more control over restructurings and fees. The senior unsecured REIT debt we invest in carry similar credit ratings and reflect comparable credit risk. While the expected yield on our securities is sensitive to the performance of the underlying assets, the more subordinated securities, in the case of CMBS, and the REIT issuer's underlying equity, in the case of REIT debt, are designed to bear the first risk of default and loss. In addition to diversification by issuer and security within our CRE securities portfolio, the underlying real estate portfolio represented by each such security are further diversified by number of properties, property type, geographic location and tenant composition.

A summary of the various types of CRE securities we invest in is as follows.

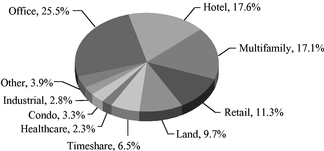

CMBS: CMBS are commercial mortgages pooled in a trust and are principally secured by real property or interests therein having a multifamily or commercial use and located in the United States. Underlying property types include regional malls, neighborhood shopping centers, office buildings, industrial or warehouse properties, hotels, multifamily, self-storage and healthcare facilities.

Unsecured REIT Debt: Substantially all of our unsecured REIT debt consists of non-amortizing senior unsecured notes issued by equity REITs. REITs own a variety of property types with a large number of companies focused on the office, retail, multifamily, industrial, healthcare and hotel sectors. Unsecured REIT debt typically incorporates protective financial covenants and has credit ratings issued by one or more rating agencies. We may also invest in junior unsecured debt or preferred equity of REITs.

CDO Notes: CDO notes are typically collateralized by a combination of CMBS and unsecured REIT debt and may also include CRE first mortgage loans, subordinate mortgage interests and other asset-backed securities as part of their underlying collateral. These assets are held within a special-purpose vehicle that issues rated securities and equity in private securities offerings.

Underwriting Process

Our underwriting process for CRE securities is focused on evaluating both the real estate risk of the underlying assets and the structural protections available to the particular class of securities in which we are investing. We believe that even when a security such as CMBS or REIT debt is backed by a diverse pool of properties, risk cannot be evaluated purely by statistical or quantitative means but must include a fundamental real estate analysis as well. Properties backing loans with identical debt service coverage ratios or loan-to-value ratios can have very different risk characteristics depending on their age, location, lease structure, physical condition and other factors. Our underwriting process seeks to identify those factors that may lead to an increase or decrease in credit quality over time.

When evaluating a CMBS backed by a large number of loans, we combine real estate analysis on individual loans with stress testing of the portfolio under various sets of default and loss assumptions. Unsecured REIT debt is generally evaluated based on the quality, type and location of the property portfolio, the capital structure, debt covenants, financial ratios of the company and management's track record, operating expertise and strategy. Our investment decisions are based on the REIT's ability to withstand financial stress, as well as more subjective criteria related to the quality of management and

9

Table of Contents

of the property portfolio. We use a consistent methodology to evaluate the underlying collateral in a CDO note investment.

Our Portfolio

As of December 31, 2011, $3.2 billion, or 46.1%, of our assets under management were invested in a portfolio of CRE securities. Our CRE securities portfolio consisted of 693 investments with an average investment size of $5 million. As of December 31, 2011, we held the following CRE security investments (amounts in thousands):

| | | | | | | | | | | | | | | | | | | |

Asset Type: | | Number | | Principal

Amount | | Amortized

Cost | | Fair

Value(1) | | Allocation by

Type(2) | | Weighted

Average

Coupon | |

|---|

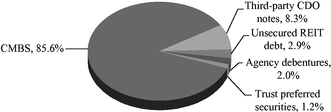

CMBS | | | 618 | | $ | 2,767,828 | | $ | 1,964,843 | | $ | 1,272,736 | | | 85.6 | % | | 4.42 | % |

Third-party CDO notes | | | 44 | | | 269,081 | | | 210,080 | | | 63,567 | | | 8.3 | % | | 0.86 | % |

Unsecured REIT debt | | | 22 | | | 94,236 | | | 88,870 | | | 94,298 | | | 2.9 | % | | 5.99 | % |

Trust preferred securities | | | 5 | | | 40,000 | | | 35,105 | | | 19,145 | | | 1.2 | % | | 2.47 | % |

Agency debentures | | | 4 | | | 63,000 | | | 16,659 | | | 23,559 | | | 2.0 | % | | NA | |

| | | | | | | | | | | | | | |

Total | | | 693 | | $ | 3,234,145 | | $ | 2,315,557 | | $ | 1,473,305 | | | 100.0 | % | | 4.06 | % |

| | | | | | | | | | | | | | |

- (1)

- $1,358 million in fair value served as collateral for our consolidated CDO financing transactions and $73 million served as collateral for our credit facility as of December 31, 2011. The remainder is either financed under other borrowing facilities or unleveraged.

- (2)

- Based on principal amount.

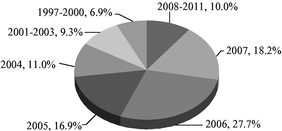

CMBS represents $2.8 billion, or 85.6%, of our CRE securities portfolio. The CMBS portfolio had an average credit rating of B-/B3.

The following charts display our CRE securities by type and CMBS by vintage, based on outstanding principal amount:

| | |

| |

|

|---|

Securities by Type | | CMBS by Vintage |

| |

|

Net Lease Properties

Overview

Our net lease property strategy involves investing primarily in office, industrial, retail and healthcare-related properties across the United States that are net leased to corporate tenants and healthcare operators. Net lease properties are typically leased to a single tenant who agrees to pay basic rent, plus all taxes, insurance, capital and operating expenses arising from the use of the leased property generally leaving us, as owner, with minimal ongoing operational or expense obligations. We may also invest in properties that are leased to tenants for which we are responsible for some of the operating expenses and capital costs. At the end of the lease term, the tenant typically has a right to

10

Table of Contents

renew the lease at market rates or to vacate the property with no further ongoing obligation. Accordingly, we target properties that are located in primary or secondary markets with strong demand fundamentals and that have a property design and location that make them suitable and attractive for alternative tenants.

Underwriting Process

Our core net lease property investments are underwritten utilizing our skills in evaluating real estate market and property fundamentals, real estate residual values and tenant credit. At inception and throughout the life of our ownership, we conduct detailed tenant credit analyses to assess, among other things, the potential for credit deterioration and lease default risk. This analysis is also used to measure the adequacy of landlord protection mechanisms incorporated into the underlying lease. Our process includes sub-market and property-level due diligence in order to understand downside investment risks, including quantifying the costs associated with tenant defaults and re-leasing scenarios. We typically perform physical inspections of the properties, review the environmental reports, evaluate title and undertake other due diligence procedures. We also evaluate stress scenarios to understand refinancing risk.

Our healthcare net lease property investments are underwritten utilizing a comprehensive analysis of the profitability of a targeted business or facility, its cash flow, occupancy, patient and payer mix (public versus private), financial trends in revenues and expenses, barriers to competition, the need in the market for the type of healthcare services provided by the business or the facility, the strength of the location and the underlying value of the business or the facility, as well as the financial strength and experience of the operator of the business or the facility.

Our Portfolio

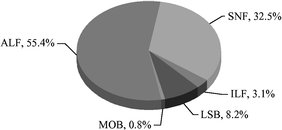

As of December 31, 2011, we held the following net lease investments (amounts in thousands):

| | | | | | | | | | | | | |

Type of Property | | Number | | Cost

Basis(1)(2) | | % of Cost | | Rental

Cash Flow(3) | |

|---|

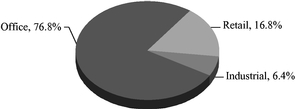

Core net lease(4) | | | | | | | | | | | | | |

Office | | | 12 | | $ | 310,620 | | | 76.8 | % | $ | 23,388 | |

Retail | | | 11 | | | 67,794 | | | 16.8 | % | | 6,212 | |

Industrial | | | 1 | | | 26,013 | | | 6.4 | % | | 868 | |

| | | | | | | | | | |

Subtotal | | | 24 | | | 404,427 | | | 100.0 | % | | 30,468 | |

Healthcare net lease | | | | | | | | | | | | | |

Assisted living facilities (ALF) | | | 42 | | | 305,522 | | | 55.3 | % | | 21,325 | |

Skilled nursing facilities (SNF) | | | 31 | | | 179,680 | | | 32.5 | % | | 17,393 | |

Life science buildings (LSB) | | | 3 | | | 45,475 | | | 8.2 | % | | 3,708 | |

Independent living facilities (ILF) | | | 5 | | | 16,955 | | | 3.1 | % | | 3,164 | |

Medical office building (MOB) | | | 1 | | | 4,783 | | | 0.9 | % | | 192 | |

| | | | | | | | | | |

Subtotal | | | 82 | | | 552,415 | | | 100.0 | % | | 45,782 | |

| | | | | | | | | | | |

Total | | | 106 | | $ | 956,842 | | | | | $ | 76,250 | |

| | | | | | | | | | | |

- (1)

- Represents our cost basis, including net purchase price allocations of $42 million related to intangible assets.

- (2)

- Excludes certain real estate owned of $320 million as the result of foreclosure, of which the principal amount of such loans at the time of foreclosure was $119 million.

- (3)

- Represents contractual base rent, excluding the effects of straight-line rent annualized based on fourth quarter 2011 amounts.

- (4)

- Includes a $28 million property owned through a joint venture investment.

11

Table of Contents

Core Net Lease Properties

As of December 31, 2011, $404 million, or 5.8%, of our total assets under management were invested in our core net lease properties, consisting of a portfolio of office, retail and industrial facilities totaling 3.2 million square feet. As of December 31, 2011, our core net lease properties had a weighted average remaining lease term of 6.4 years and were 94% leased. The following summarizes our core net lease portfolio's diversity across property type and geographic location as of December 31, 2011, based on purchase price, or cost.

| | |

| |

|

|---|

Core Net Lease by Property Type | | Core Net Lease by Geographic Location |

| |

|

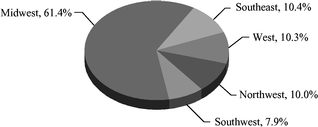

Healthcare Net Lease Properties

As of December 31, 2011, $552 million, or 7.9%, of our assets under management were invested in our healthcare net lease properties, with a focus on the senior housing sector which includes assisted living, skilled nursing and independent living facilities. Our portfolio was comprised of 42 assisted living facilities (ALF), 31 skilled nursing facilities (SNF), three life science buildings (LSB), five independent living facilities (ILF) and one medical office building (MOB). As of December 31, 2011, 100% of our net lease healthcare portfolio was leased to third-party operators with weighted average lease coverage of 1.4x and a 7.7 year weighted average remaining lease term. The following summarizes our healthcare portfolio by property type and geographic location as of December 31, 2011, based on purchase price.

| | |

| |

|

|---|

Healthcare Net Lease by Property Type | | Healthcare Net Lease by Geographic Location |

| |

|

Asset Management and Other

Our asset management and other activities are focused on:

- •

- Managing CDO financing transactions on a fee basis.

We manage eleven CDOs representing $6.1 billion of assets based on principal amount, nine of which were sponsored by us, or the N-Star CDOs. In addition, we have acquired the equity interests of two CDOs that have been integrated into our platform, the CSE CDO and the CapLease CDO, which we herein collectively refer to as our acquired CDOs. In the case of the CSE CDO, we were delegated the collateral management and special servicing rights and for the

12

Table of Contents

CapLease CDO, we acquired the collateral management rights. Five of the CDOs are primarily collateralized by CRE debt and six are primarily collateralized by CRE securities.

We consolidate these CDO financing transactions under accounting principles generally accepted in the United States, or U.S. GAAP. As a result, the collateral management fees we earn and receive in cash are eliminated in the consolidated statements of operations.

- •

- Sponsoring and advising on a fee basis, our Sponsored REITs.

In connection with our current Sponsored REIT, we manage the day-to-day affairs including identifying, originating, acquiring and managing investments on its behalf, and we earn advisory and other fees for these services, which vary based on the amount of assets under management, investment activity and investment performance.

In addition, NorthStar Realty Securities, LLC (formerly known as NRF Capital Markets, LLC), or NorthStar Realty Securities, our wholly-owned broker-dealer subsidiary, distributes equity for our Sponsored REITs. NorthStar Realty Securities is currently raising equity capital for NSREIT and we expect that NorthStar Realty Securities will assist us in the future in accessing diverse sources of capital for other companies that may be sponsored and managed by us.

- •

- Acting as special servicer for our owned (and potentially third-party owned) CMBS.

We are a rated special servicer by Standard & Poor's and Fitch Ratings and have been approved by Moody's Investor Services in connection with a recent transaction. We currently own over 600 CMBS investments. To the extent we become the controlling classholder in the future for our CMBS investments, we may appoint ourselves special servicer, which would, among other things, provide us more control over restructurings and special servicing fees.

Other Opportunistic Investments

We also pursue other opportunistic investments that we expect will generate attractive risk-adjusted returns, such as repurchasing our CDO bonds at a significant discount to principal amount. These CDO bonds typically have significant credit support and, when we repurchase a CDO bond, we generally expect the CDO bonds will be repaid at par.

As of December 31, 2011, we owned $555 million principal amount of our CDO bonds unleveraged, of which $376 million were repurchased with a weighted average original rating of AA/Aa3 and an average price of 31%. Because our CDO financing transactions are consolidated under U.S. GAAP, these CDO bonds are not presented as an investment but rather are eliminated in our consolidated financial statements. We will generate cash flows in future periods through the interest payable on these bonds, as well as realizing (in cash) the discount when the bonds repay. This realization of the discount will not be reported as a gain under U.S. GAAP.

Financing Strategy

We seek to access a wide range of secured and unsecured debt and public and private equity capital sources to fund our investment activities and asset growth. Since our IPO in 2004, we have completed preferred and common equity offerings raising approximately $1.0 billion of aggregate net proceeds. We have also raised $286 million of long-term, subordinated debt capital that is equity-like in nature due to its 30-year term (at the time of issuance) and relatively few covenants. In addition, we have raised $425 million of unsecured exchangeable senior notes, of which $229 million is outstanding as of December 31, 2011.

We use asset-level financing as part of our strategy and we seek to match-fund our assets and liabilities by having similar maturities and like-kind interest rate benchmarks (fixed or floating) to manage refinancing and interest rate risk. We seek access to diverse sources of short and long-term

13

Table of Contents

financing to enable us to prudently leverage our assets and deliver attractive risk-adjusted returns to our stockholders.

Our CRE debt and security portfolios are predominantly financed through long-term, non-recourse CDOs. We currently use secured term credit facilities provided by major financial institutions to fund new investments until permanent financing is available. However, we believe the terms of these facilities are flexible enough to provide sufficient term financing to match the underlying assets to the extent the securitization market remains inaccessible.

In our N-Star CDOs, rated CDO bonds are issued and backed by pools of collateral originated or acquired by us. The CDO bonds are non-recourse and the collateral is used to service the interest payments on the rated CDO bonds. After a reinvestment period, which is typically five years, principal from collateral payoffs is used to amortize the CDO bonds, so there is no maturity risk. We typically have sold all of the investment-grade rated CDO bonds and retained the non-investment grade subordinate classes and equity notes which we refer to as our retained equity interest in the CDO. CDO financings provided low-cost borrowing because the majority of the liabilities we issued were the most senior bond classes which were rated "AAA/Aaa" by the rating agencies, and therefore had the lowest cost of funds.

Our net lease properties are typically financed with non-recourse mortgages. We seek to match the term of the financing with the remaining lease term of the properties.

Given the nature of our financing arrangements, we expect to maintain our borrowings at or near our current levels for our existing investments. Borrowing levels may change for new investments depending upon the nature of the assets and the related financing. Our financing strategy for current or future investments is dependent on our ability to obtain the match-funded borrowings at rates that provide a positive net funding spread. Match-funded borrowing was difficult to obtain during the credit crisis. During that time, we focused on using our existing CDO structures to fund future investment activity when repayment or sale proceeds became available within the CDOs or we acquired investments that generated attractive returns without leverage.

We actively seek financing for our businesses of originating loans and acquiring CRE securities. As a result, in the fourth quarter of 2011, we, through two wholly-owned subsidiaries, entered into two new credit facilities with Wells Fargo Bank N.A., or Wells Fargo, a $100 million credit facility to finance the origination of CRE loans and a $100 million credit facility to finance the acquisition of AAA-rated CMBS.

Hedging Strategy

We use derivative instruments primarily to manage interest rate risk exposure. These derivatives are typically in the form of interest rate swap agreements and the primary objective is to manage the interest rate risks associated with our investing and financing activities. The counterparties to these arrangements are major financial institutions with which we may also have other financial relationships.

Creating an effective strategy for dealing with interest rate movements is complex and no strategy can completely insulate us from risks associated with such fluctuations. There can be no assurance that our hedging activities will have the intended impact on our results. A more detailed discussion of our hedging policy is provided in Item 7. "Management's Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources."

Risk Management

We use many methods to actively manage our asset base to preserve our income and capital. For CRE debt and net lease assets, frequent dialogue with borrowers/tenants and inspections of our collateral and owned properties have proven to be an effective process for identifying issues early. For

14

Table of Contents

our healthcare net lease assets, we also consider the impact of regulatory changes on operator performance and property values. Many of our debt investments also require borrowers to replenish cash reserves for items such as taxes, insurance and future debt service costs. Late replenishments of cash reserves also may be an early indicator there could be a problem with the borrower or collateral property. We also may negotiate modifications to debt terms if we believe such modification improves our ability to maximize principal recovery. Modifications may include changes to contractual interest rates, maturity dates and other borrower obligations. When we make a concession, such as reducing an interest rate or extending a maturity date, we may seek to obtain additional collateral, fees and/or upside participation in any value creation of the property in return for the modification, although in a challenging real estate market, obtaining additional collateral from struggling borrowers is difficult. As part of our risk management process, we evaluate the best alternatives for our loans which in some cases, may result in us issuing default notices and beginning foreclosure proceedings when the borrower is not complying with the debt terms where we believe taking control of the collateral as real estate owned, or REO, is the best course of action to protect our capital.

In certain circumstances, we may pursue a debt sale or payoff at a discount to our carrying value. We may agree to a discounted sale or payoff where we believe there is an economic benefit from monetizing the asset in advance of its contractual maturity date. When evaluating a sale or payoff at a discount to carrying value, we also consider the impact such transaction may have on our financing structures, corporate borrowing covenants and income.

Securities generally have a more liquid market than debt and net lease properties, but we typically have very little control over restructuring decisions when there are problems with the underlying collateral. We are a rated special servicer by Standard & Poor's and Fitch Ratings and have been approved by Moody's Investor Services in connection with a recent transaction. We may appoint ourselves as special servicer in CMBS transactions where we become the controlling class holder which will, among other things, provide us more control over restructurings. We manage risk in the securities portfolio by selling assets when we can obtain a price that is attractive relative to its risk. In certain situations, we may sell an asset because there is an opportunity to reinvest the capital into a new asset with a more attractive risk/return profile.

We maintain a comprehensive risk management process that generally includes day-to-day oversight by the portfolio management team, weekly management meetings and a quarterly credit review process. These processes are designed to enable management to evaluate and proactively manage asset-specific credit issues and identify credit trends on a portfolio-wide basis. Nevertheless, we cannot be certain that our review will identify all issues within our portfolio due to, among other things, adverse economic conditions or events adversely affecting specific assets; therefore, potential future losses may also stem from investments that are not identified by our credit reviews. During the quarterly reviews, or more frequently as necessary, investments are put on highly-monitored status and identified for possible impairment based upon several factors, including missed or late contractual payments, significant declines in collateral performance and other data which may indicate a potential issue in our ability to recover our capital from the investment.

Many of our debt investments were made to borrowers who had a business plan to improve the collateral property and who therefore needed a flexible balance sheet lender. Property cash flows are generally lower today than was projected by the borrower for many of our debt investments when they were originated. As a result, some real estate owners are having trouble refinancing their assets at maturity or selling their properties to recoup their capital. Other owners are having trouble achieving their business plans to the extent they acquired a property to reposition it or otherwise invest capital to increase the property's cash flows.

We generally required the borrowers, at the time of origination and/or as required by property performance during the loan term, to pre-fund reserves to cover interest and operating expenses until

15

Table of Contents

the property cash flows increased sufficiently to cover debt service costs. We also generally required the borrower to refill these reserves if they became deficient due to underperformance and if the borrower wanted to exercise an extension option under the loan as some of the borrowers had a recourse obligation to do so. Despite low interest rates and improving real estate fundamentals, we expect that in the future some of our borrowers may still have difficulty servicing our debt.

Each of our debt investments, while primarily backed by CRE collateral, is unique and requires customized risk management strategies for dealing with potential credit situations. The complexity of each situation depends on many factors, including the number of collateral properties, the type of property, macro and local market conditions impacting supply/demand, cash flow and collateral, and the financial condition of our borrowers and their willingness to support our collateral properties.

Our risk management process may lead us to the determination that extending and working out debt, rather than pursuing foreclosure, is the best course of action to maximize total and long-term value. Our impairment analysis often requires that we make assumptions regarding collateral value and the timing with regards to when we receive debt service payments, including principal recovery, and as a result, our analysis can be highly subjective and uncertain.

Our CRE debt and security investments are predominantly financed in CDOs. We consolidate the CDO financing transactions under U.S. GAAP regardless of whether we retained the equity interests for our sponsored CDOs or acquired the equity interests of other CDOs. When we refer to equity interests in a CDO, we are collectively referring to subordinate CDO bonds, preferred shares and equity notes. The CDOs require that we meet tests in order to receive regular cash flow distributions on our subordinate CDO bonds and equity notes. Our risk management process is also focused on actively monitoring and managing our CDO financing transactions. A more detailed discussion of our CDO financing structures are provided in Item 7. "Management's Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources."

Regulation

We are subject, in certain instances, to supervision and regulation by state and federal governmental authorities and may be subject to various laws and judicial and administrative decisions imposing various requirements and restrictions, which, among other things: (1) regulate credit granting activities; (2) require disclosures to customers; (3) govern secured transactions; and (4) set collection, foreclosure, repossession and claims-handling procedures and other trade practices. Although most states do not regulate commercial finance, certain states impose limitations on interest rates and other charges and on certain collection practices and creditor remedies and require licensing of lenders and financiers and adequate disclosure of certain contract terms. We are also required to comply with certain provisions of the Equal Credit Opportunity Act that are applicable to CRE loans.

We believe that we are not, and intend to conduct our operations so as not to become regulated as an investment company under the Investment Company Act of 1940, as amended, or the Investment Company Act. We have relied, and intend to continue to rely on current interpretations of the staff of the Securities and Exchange Commission, or the SEC, in an effort to continue to qualify for an exemption from registration under the Investment Company Act. For more information on the exemptions that we utilize refer to Item 1A. "Risk Factors—Maintenance of our Investment Company Act exemption imposes limits on our operations."

We do not believe we or our subsidiaries are required to register as an investment advisor under the Investment Advisors Act of 1940. Such registration could result in us being supervised by the SEC and require our compliance with numerous obligations, including record-keeping requirements, operational procedures and disclosure obligations.

16

Table of Contents

We have elected and expect to continue to make an election to be taxed as a REIT under Section 856 through 860 of the Internal Revenue Code of 1986, as amended, or the Code. As a REIT, we must currently distribute, at a minimum, an amount equal to 90% of our taxable income. In addition, we must distribute 100% of our taxable income to avoid paying corporate federal income taxes. REITs are also subject to a number of organizational and operational requirements in order to elect and maintain REIT status. These requirements include specific share ownership tests and assets and gross income composition tests. If we fail to qualify as a REIT in any taxable year, we will be subject to federal income tax (including any applicable alternative minimum tax) on our taxable income at regular corporate tax rates. Even if we qualify for taxation as a REIT, we may be subject to state and local income taxes and to federal income tax and excise tax on our undistributed income.

On April 20, 2010, NorthStar Realty Securities became registered with the SEC and a member of the Financial Industry Regulatory Authority, or FINRA. Much of the regulation of broker-dealers has been delegated to self-regulatory organizations, or SROs, principally FINRA, that adopt and amend rules, subject to approval by the SEC, which govern their members and conduct periodic examinations of member firms' operations. The SEC, SROs and state securities commissions may conduct administrative proceedings that can result in censure, fine, suspension or expulsion of a broker-dealer, its officers or employees. Such administrative proceedings, whether or not resulting in adverse findings, can require substantial expenditures and can have an adverse impact on the reputation of a broker-dealer.

As a registered broker-dealer, NorthStar Realty Securities is required by federal law to belong to the Securities Investor Protection Corporation, or SIPC. When the SIPC fund falls below a certain amount, members are required to pay annual assessments to replenish the reserves. Our broker-dealer subsidiary will be required to pay 0.25% of net operating revenues as a special assessment. As of December 31, 2011, we have incurred an immaterial amount of special assessment charges. The SIPC fund provides protection for securities held in customer accounts up to $500,000 per customer, with a limitation of $100,000 on claims for cash balances, although NorthStar Realty Securities does not hold any customer accounts.

In addition, as a registered broker-dealer and member of FINRA, NorthStar Realty Securities is subject to the SEC's Uniform Net Capital Rule 15c3-1, which is designed to measure the general financial integrity and liquidity of a broker-dealer and requires the maintenance of minimum net capital. Net capital is defined as the net worth of a broker-dealer subject to certain adjustments. In computing net capital, various adjustments are made to net worth that exclude assets not readily convertible into cash. Additionally, the regulations require that certain assets, such as a broker-dealer's position in securities, be valued in a conservative manner so as to avoid over-inflation of the broker-dealer's net capital. We believe the net capital requirement is immaterial.

We own and manage a portfolio of healthcare net lease properties, with a focus on the senior housing sector. As such, we or our operators, as the case may be, are subject to numerous federal, state and local laws and regulation that are subject to frequent and substantial changes (sometimes applied retroactively) resulting from legislation, adoption of rules and regulations and administrative and judicial interpretations of existing laws.

We are also subject to regulation with respect to certain of our loan servicing activities, such as Regulation AB.

In the judgment of management, existing statutes and regulations have not had a material adverse effect on our business. However, it is not possible to forecast the nature of future legislation, regulations, judicial decisions, orders or interpretations, nor their impact upon our future business, financial condition, results of operations or prospects.

17

Table of Contents

Competition

We have in the past been subject to significant competition in seeking real estate investments. Historically, we have competed with many third parties engaged in real estate investment activities including other REITs, specialty finance companies, savings and loan associations, banks, mortgage bankers, insurance companies, mutual funds, private institutional funds, hedge funds, private opportunity funds, investment banking firms, governmental bodies and other entities. Some of these competitors, including other REITs and private real estate companies and funds, have substantially greater financial resources than we do. They may also enjoy significant competitive advantages that result from, among other things, a lower cost of capital and enhanced operating efficiencies.

Although the current environment is less competitive compared to historical periods, future competition from new market entrants may limit the number of suitable investment opportunities offered to us. It may also result in higher prices, lower yields and a narrower spread of yields over our borrowing costs, making it more difficult for us to acquire new investments on attractive terms.

Employees

As of December 31, 2011, we had 107 employees. Management believes that a major strength of NorthStar is the quality and dedication of our people. We maintain a work environment that fosters professionalism, excellence, diversity and cooperation among our employees.

Corporate Governance and Internet Address

We emphasize the importance of professional business conduct and ethics through our corporate governance initiatives. Our board of directors consists of a majority of independent directors; the audit, nominating and corporate governance and compensation committees of our board of directors are composed exclusively of independent directors. We have adopted corporate governance guidelines and a code of business conduct and ethics, which delineate our standards for our officers, directors and employees.

Our internet address iswww.nrfc.com. The information on our website is not incorporated by reference in this Annual Report on Form 10-K. We make available, free of charge through a link on our site, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to such reports, if any, as filed or furnished with the SEC, as soon as reasonably practicable after such filing or furnishing. Our site also contains our code of business conduct and ethics, code of ethics for senior financial officers, corporate governance guidelines and the charters of our audit committee, nominating and corporate governance committee and compensation committee of our board of directors. Within the time period required by the rules of the SEC and the New York Stock Exchange, or NYSE, we will post on our website any amendment to our code of business conduct and ethics and our code of ethics for senior financial officers as defined in the code.

Item 1A. Risk Factors

The following risk factors and other information included in this Annual Report on Form 10-K should be carefully considered. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties not presently known to us or that we currently deem immaterial also may adversely impact our business. If any of the following risks occur, our business, financial condition, operating results, cash flows and liquidity could be materially adversely affected.

18

Table of Contents

Risks Related to Our Businesses

The CRE finance industry has been and may continue to be adversely affected by economic conditions in the U.S. and global financial markets generally.

Our business and operations is dependent on the CRE finance industry generally, which in turn is dependent upon broad economic conditions in the U.S. and abroad. Despite some recent improvements, the U.S. economy is continuing to experience relatively high unemployment and slow growth. A worsening of economic conditions would likely have a negative impact on the CRE finance industry generally and on our business and operations specifically. Additionally, disruptions in the global economy, whether as a result of the Euro-zone debt crisis, regional conflict or otherwise, may also have a negative impact on the CRE market domestically. Adverse conditions in the CRE finance industry could harm our business and financial condition by, among other factors, reducing the value of our existing assets, limiting our access to debt and equity capital, harming our ability to originate new CRE debt and otherwise negatively impacting our operations.

Liquidity is essential to our businesses and we rely on outside sources of capital that have been negatively impacted by U.S. and global economic conditions.

We require significant outside capital to fund and grow our businesses. A primary source of liquidity for us has been the equity and debt capital markets, including issuances of common equity, preferred equity, trust preferred securities and exchangeable senior notes. Access to the capital markets and other sources of liquidity was severely disrupted during the relatively recent credit crisis and, despite some improvements in 2011, the markets could suffer another severe downturn and another liquidity crisis could emerge. If we are unable to obtain sufficient capital on acceptable terms, our business, ability to operate and liquidity could be severely impacted. For information about our available sources of funds, refer to Part II Item 7. "Management's Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources" and the notes to the consolidated financial statements located in Part II Item 8. of this Annual Report on Form 10-K.

Our CDO bonds payable have certain coverage tests that are required to be met in order for payments to be made to our retained equity interests in the CDO. Failing coverage tests could significantly impact our cash flow and overall liquidity position.

Our CDO bonds payable generally require that the underlying collateral and cash flow generated by the collateral be in excess of ratios stipulated in the related indentures. These overcollateralization, or OC, and interest coverage, or IC, tests are used primarily to determine whether and to what extent principal and interest proceeds on the underlying collateral may be used to pay principal of, and interest on, our retained equity interests in the CDOs. Our CDOs are collateralized by CRE debt and securities, with a majority of our equity invested in our real estate debt CDOs. Uncured defaults on CRE debt and rating agency downgrades on CMBS are the primary causes for decreases in the OC and IC tests. In the event these tests are not met, cash flow that would normally be distributed to us would be used to amortize the senior CDO bonds until the CDO is back in compliance with the tests. Even if we have control because we may have originated a loan and even when we may be able to appoint ourselves as special servicer in connection with a CMBS investment, we may be unable to prevent adverse conditions that could negatively affect our cash flow and overall liquidity position.

As of December 31, 2011, all of our real estate debt CDOs were in compliance with their OC and IC tests. Four of our N-Star securities CDOs (I, II, V and VII) were out of compliance with their respective OC tests and we expect that complying with OC and IC tests will continue to be difficult. Weaker than expected economic conditions, deterioration of the CRE market and credit rating downgrades of real estate securities will make complying with OC and IC tests more difficult or even

19

Table of Contents

impossible in the future. Our failure to satisfy the coverage tests could adversely affect our operating results, liquidity and cash flows.

The reinvestment period for three of our CDOs will expire in 2012 and the reinvestment periods for our other CDOs expired prior to December 31, 2011.

During the reinvestment period of our CDOs, we are allowed to reinvest principal payments on the underlying assets into qualifying replacement collateral. The reinvestment period for two of our CDO's (CSE CDO and N-Star CDO VIII) just ended in January 2012 and February 2012, respectively, while the reinvestment period for N-Star CDO IX ends in June 2012. Because we will be unable to reinvest principal in these CDOs after the reinvestment period ends, principal repayments after the reinvestment period ends will pay down the senior bonds, which will delever the CDO and negatively impact our cash flow. Additionally, our ability to reinvest has been instrumental in maintaining OC and IC ratios under our CDOs. Following the end of the reinvestment period in our CDOs, our ability to maintain the OC and IC ratios will be negatively impacted, which could adversely affect our cash flow and results of operation.

We retain the equity interests in our CDOs, which entails certain risks, including that these interests are the most junior interests and receive distributions only if the CDO generates enough cash flow to pay all of the other senior CDO bonds.

Our retained equity interests in the CDOs represent leveraged investments in the underlying assets. The senior CDO bonds participate in the cash flow in CDOs and distributions on equity interests are generally made only after payment of interest on, and principal of, the senior CDO bonds. Although generally there is no interest or principal due on the equity notes, distributions may be made to us as holders of the equity interests on each payment date only after all of the other required payments are made. There will be little or no cash flow available to our equity interests if there are defaults by the obligors under the underlying collateral and those defaults exceed a certain amount. In that event, the value of our investment in our CDOs could decrease quickly and substantially. There can be no assurance that after making required payments on the senior CDO bonds there will be any remaining funds available to pay us. Accordingly, our equity interests may not be paid in full and we may be subject to a loss of all or part of our interest in the event that payments are not made on the underlying assets or losses are incurred with respect to the underlying assets, which could have a material adverse effect on us.

A payment default on our CDO bonds could have a compounding effect on our other CDOs.

Certain of our CDOs have invested in CDO bonds issued by other CDOs that we sponsored and/or acquired. Such investments expose us to increased risk, as defaults in any particular CDO would also affect another CDO that owns bonds in the CDO that experiences defaults. Defaults across certain of our CDOs could, therefore, have a material impact on the cash flow of other CDOs that we own that may not have otherwise experienced such an impact.

We are unable to complete additional CDOs due to the decreased liquidity in the CRE finance market.

We historically accessed the securitization markets to finance our CRE debt and security investments with non-recourse, long-term liabilities which were structured as CDOs. Issuing long-term financing, such as CDO bonds, has historically been an important part of our overall business plan. Despite improvements in market liquidity, we currently believe structured CDO financing may not be available for the foreseeable future, if ever.

20

Table of Contents

The documentation governing our CDOs is complex and contains certain ambiguities that are subject to interpretation.

Each of our CDOs is governed by an indenture, collateral management agreement and other documentation. The documents are complex and collectively describe the conditions upon which we can sell assets and reinvest principal proceeds and set forth covenants and other provisions to which we and the CDOs are subject. In certain circumstances, the performance of the underlying CDO collateral has raised ambiguities in our CDO documentation. Although we have as a general matter been able to reach agreement with our CDO trustees as to how the CDO documentation should be interpreted, it is possible that we and our CDO trustees may not be able to reach agreement on important CDO documentation provisions in the future. To the extent we and our CDO trustees are unable to resolve any differences in the interpretation of CDO documentation, or if third parties, such as bondholders or other parties, do not agree with conclusions that are reached by us and/or the CDO trustees, our ability to manage the underlying collateral, and thus maintain the IC and OC ratios and otherwise optimize the performance of our CDOs, may be adversely affected. We could take a position, inadvertently or otherwise, that a court ultimately determines constitutes a breach of the underlying agreements and the results of such a determination could have a material adverse affect on our business and financial condition.

Challenging economic and financial market conditions could significantly reduce the amount of income we earn on our CRE debt investments and further reduce the values of our investments.

Challenging economic and financial market conditions have caused us to experience an increase in the number of CRE debt investments that result in delinquencies, foreclosures and non-performing assets and a decrease in the value of the property or other collateral which secures our CRE loans, all of that could adversely affect our results of operations. Loan defaults result in a decrease in interest income and may require the establishment of, or an increase in, provision for loan losses. The decrease in interest income resulting from a loan default may continue for a prolonged period of time as we seek to recover, primarily through legal proceedings, the outstanding principal amount, accrued interest and default interest due on a defaulted CRE debt investment. Legal proceedings, which may include foreclosure actions and bankruptcy proceedings, are expensive and time consuming and we may still never recover all or a portion of our principal. The decrease in interest income and the costs involved in pursuing our legal remedies will reduce the amount of cash available to meet our expenses and adversely impact our liquidity and operating results.

Real estate debt restructurings may reduce our net interest income.

Although the CRE market has exhibited signs of recovery, we may continue to need to restructure our real estate debt investments. In order to preserve long-term value, we are often required to lower the interest rate on our loans in connection with a restructuring, which will have an adverse impact on our net interest margin. We may also determine to extend the time to maturity on our real estate debt investments and make other concessions with the goal of increasing overall value but there is no assurance that the results of our restructurings will be favorable to us.

We may be unable to restructure loans in a manner that we believe maximizes value, particularly if we are one of multiple creditors in large capital structures.

In the current environment, in order to maximize value we may be more likely to extend and work out a loan, rather than pursue foreclosure. However, in situations where there are multiple creditors in large capital structures, it can be particularly difficult to assess the most likely course of action that a lender group or the borrower may take and it may also be difficult to achieve consensus among the lender group as to major decisions. Consequently, there could be a wide range of potential principal recovery outcomes, the timing of which can be unpredictable, based on the strategy pursued by a

21

Table of Contents

lender group and/or by a borrower. These multiple creditor situations tend to be associated with our larger loans. We, as one of a group of lenders, are often a lender on a subordinated basis, and may not independently control the decision making. Consequently, we may be unable to restructure a loan in a manner that we believe would maximize value. Risks associated with our largest multiple creditor loans are described in more detail in Item 7. "Management's Discussion and Analysis of Financial Condition and Results of Operations—Risk Management."

We have restructured certain CRE investments in the past in an effort to maximize the value of our investment, however, there is no assurance that our restructurings will be successful and we may still lose some or all of our investment.

Examples of CRE investments we have restructured include our:

- •

- $110 million (22%) equity interest in Meadowlands Two, LLC, which holds 100% of Meadowlands One, LLC, or Meadowlands One, which is secured by a retail/entertainment complex located in East Rutherford, New Jersey, or the NJ Property. During the third quarter 2010, Meadowlands One took effective ownership of the NJ Property. Meadowlands One is in the process of seeking to recapitalize the NJ Property. While Meadowlands One has entered into an agreement with a developer, who is covering the majority of costs of operating the asset, there is no assurance that a recapitalization will be completed or that a recapitalization will be completed on terms acceptable to us. As of December 31, 2011, our carrying value in the NJ Property is $66 million.

- •

- $89 million mezzanine loan, or the NV Loan, that is secured by the Hard Rock Hotel and Casino in Las Vegas, Nevada, or Hard Rock. We, along with certain of the other lenders, and the borrower and its affiliates under the NV Loan, have completed a long-term restructuring of the NV Loan. As part of the restructuring, Brookfield took ownership of Hard Rock and entered into a seven-year loan with the existing senior lender, subject to achieving certain tests, and we retained our $89 million mezzanine loan (or its economic equivalent), as well as an equity participation in Hard Rock. There is no assurance that the restructured NV Loan will be successful over time. As of December 31, 2011, our carrying value in the NV Loan is $45 million.

- •

- €43 million participation in a mezzanine loan that is collateralized by a German retail portfolio that is net leased to a single tenant that filed for bankruptcy in Germany, or the German Loan. The German Loan was restructured in 2010 and since restructuring, the loan has been performing. However, there can be no assurance that the German Loan will not default in the future, including at maturity which is July 2014. As of December 31, 2011, our carrying value in the €43 million participation is $56 million.

We may lose a portion or all of our restructured investments, which could have a material adverse effect on our business and operations.

Our borrowers may be unable to achieve their business plans due to the difficult U.S. and global economic conditions, which could cause incremental stress in our CRE debt portfolio.

Many of our CRE debt investments were made to borrowers who had business plans to improve occupancy and cash flows that have not been accomplished due to the challenging economic conditions. U.S. economic conditions, including high unemployment and slow growth, along with overall financial uncertainty, have resulted in lower occupancy rates and lower lease rates across many property types and created obstacles for our borrowers attempting to achieve their business plans. If our borrowers are unable to achieve their business plans, the related CRE loans could go into default and severely impact our operating results and cash flows.

22

Table of Contents

Many of our CRE debt investments are funded with interest reserves and our borrowers may be unable to replenish those interest reserves once they run out.