UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934 (Amendment No. )

the Securities Exchange Act of 1934 (Amendment No. )

Filed by the Registrant ý | |||||

Filed by a Party other than the Registrant ¨ | |||||

| Check the appropriate box: | |||||

| ¨ | Preliminary Proxy Statement | ||||

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | ||||

| ý | Definitive Proxy Statement | ||||

| ¨ | Definitive Additional Materials | ||||

| ¨ | Soliciting Material under §240.14a-12 | ||||

| NORTHSTAR REALTY FINANCE CORP. | |||||

(Name of Registrant as Specified In Its Charter) | |||||

(Name of Person(s) Filing Proxy Statement, if other than the Registrant) | |||||

| Payment of Filing Fee (Check the appropriate box): | |||||

| ý | No fee required. | ||||

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | ||||

| (1) Title of each class of securities to which transaction applies: | |||||

| (2) Aggregate number of securities to which transaction applies: | |||||

| (3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): | |||||

| (4) Proposed maximum aggregate value of transaction: | |||||

| (5) Total fee paid: | |||||

| ¨ | Fee paid previously with preliminary materials. | ||||

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | ||||

| (1) Amount Previously Paid: | |||||

| (2) Form, Schedule or Registration Statement No.: | |||||

| (3) Filing Party: | |||||

| (4) Date Filed: | |||||

To the Stockholders of NorthStar Realty Finance Corp.:

It is my pleasure to invite you to the 2014 annual meeting of stockholders of NorthStar Realty Finance Corp., a Maryland corporation. The annual meeting will be held at The New York Palace Hotel at 455 Madison Avenue, 4th Floor, Apartment South, New York, New York 10022 on September 5, 2014, beginning at 10:00 a.m., Eastern Time.

The enclosed materials include a notice of meeting, proxy statement, proxy card, self-addressed envelope and Annual Report to Stockholders for the fiscal year ended December 31, 2013.

It is important that your shares be represented at the annual meeting regardless of the size of your securities holdings. Whether or not you plan to attend the annual meeting in person, please authorize a proxy to vote your shares as soon as possible. You may authorize a proxy to vote your shares by mail, telephone or Internet. The proxy card materials provide you with details on how to authorize a proxy to vote by these three methods. If you determine to mail us your proxy, please complete, date and sign the proxy card and return it promptly in the envelope provided, which requires no postage if mailed in the United States. If you are the record holder of your shares and you attend the annual meeting, you may withdraw your proxy and vote in person, if you so choose.

We look forward to receiving your proxy and seeing you at the meeting.

| Sincerely, | ||

| ||

| DAVID T. HAMAMOTO | ||

| Chairman and Chief Executive Officer | ||

August 7, 2014

New York, New York

New York, New York

NOTICE OF ANNUAL MEETING OF STOCKHOLDERS

To Be Held on September 5, 2014

To Be Held on September 5, 2014

To the Stockholders of NorthStar Realty Finance Corp.:

The 2014 annual meeting of stockholders of NorthStar Realty Finance Corp., a Maryland corporation, or the Company, will be held at The New York Palace Hotel at 455 Madison Avenue, 4th Floor, Apartment South, New York, New York 10022 on September 5, 2014, beginning at 10:00 a.m., Eastern Time. The matters to be considered and voted upon by stockholders at the annual meeting, which are described in detail in the accompanying proxy statement, are:

| 1) | a proposal to elect as directors the five individuals nominated by our Board of Directors as set forth in the accompanying proxy statement, each to serve until the 2015 annual meeting of stockholders and until his or her successor is duly elected and qualified; |

| 2) | a proposal to adopt a resolution approving, on a non-binding, advisory basis, named executive officer compensation as disclosed in the accompanying proxy statement; |

| 3) | a proposal to ratify the appointment of Grant Thornton LLP as our independent registered public accounting firm for the fiscal year ending December 31, 2014; and |

| 4) | the transaction of any other business that may properly come before the annual meeting or any postponement or adjournment of the annual meeting. |

This notice is accompanied by the Company’s proxy statement, a proxy card, a self-addressed envelope and the Company’s Annual Report to Stockholders for the fiscal year ended December 31, 2013.

Stockholders of record at the close of business on August 6, 2014 will be entitled to notice of and to vote at the annual meeting. Whether or not you plan to attend the annual meeting in person, please authorize a proxy to vote your shares as soon as possible. If you are the record holder of your shares and you attend the annual meeting, you may withdraw your proxy and vote in person, if you so choose.

| By Order of the Board of Directors | ||

| ||

| RONALD J. LIEBERMAN | ||

| Executive Vice President, General Counsel and Secretary | ||

August 7, 2014

New York, New York

New York, New York

OUR BOARD OF DIRECTORS URGES YOU TO AUTHORIZE A PROXY TO VOTE YOUR SHARES BY ANY OF THE THREE AVAILABLE METHODS—BY MAIL, BY TELEPHONE OR BY INTERNET. IF YOU AUTHORIZE A PROXY TO VOTE YOUR SHARES BY MAIL, PLEASE COMPLETE, SIGN, DATE AND RETURN THE PROXY CARD. YOUR VOTE IS IMPORTANT!

Stockholders are invited to visit the Corporate Governance section of our website at www.nrfc.com.

____________________________

NorthStar Realty Finance Corp.

399 Park Avenue, 18th Floor

New York, New York 10022

(212) 547-2600

____________________________

PROXY STATEMENT

____________________________

FOR THE 2014 ANNUAL MEETING OF STOCKHOLDERS

To Be Held on September 5, 2014

____________________________

TABLE OF CONTENTS

| Page | |

- i -

GENERAL INFORMATION CONCERNING SOLICITATION AND VOTING

This proxy statement, the accompanying proxy card and the notice of annual meeting are provided in connection with the solicitation of proxies by and on behalf of the board of directors, or our Board, of NorthStar Realty Finance Corp., a Maryland corporation, or the Company, for use at the 2014 annual meeting of stockholders to be held at The New York Palace Hotel at 455 Madison Avenue, 4th Floor, Apartment South, New York, New York 10022 on September 5, 2014, at 10:00 a.m. Eastern Time, and any postponements or adjournments thereof.

We are a diversified commercial real estate investment company. We invest in multiple asset classes across commercial real estate, or CRE, that we expect will generate attractive risk-adjusted returns and may take the form of acquiring real estate, originating or acquiring senior or subordinate loans, as well as pursuing opportunistic CRE investments, both in the United States and internationally. We seek to generate stable cash flow for distribution to our stockholders through our diversified portfolio of commercial real estate assets and in turn build long-term franchise value. Effective June 30, 2014, we are externally managed and advised by an affiliate of NorthStar Asset Management Group Inc. (NYSE: NSAM), or NSAM. We are a Maryland corporation and completed our initial public offering in October 2004. We conduct our operations so as to continue to qualify as a real estate investment trust, or REIT, for U.S. federal income tax purposes.

On June 30, 2014, we completed the previously announced spin-off of our asset management business into a separate publicly-traded company, NSAM, in the form of a tax-free distribution, or the Distribution. In connection with the Distribution, each of our common stockholders received shares of NSAM’s common stock on a one-for-one basis, after giving effect to a one-for-two reverse stock split of our common stock. As of the completion of the spin-off, our former asset management business is owned and operated by NSAM and we are externally managed by an affiliate of NSAM through a management contract with an initial term of 20 years. Subsequent to the spin-off, we continue to operate our commercial real estate debt origination business. Most of our employees at the time of the spin-off became employees of NSAM. Our executive officers, employees engaged in our existing loan origination business and certain other employees became co-employees of both us and NSAM. Affiliates of NSAM also manage our previously sponsored non-traded REITs: NorthStar Real Estate Income Trust, Inc., or NorthStar Income, NorthStar Healthcare Income, Inc., or NorthStar Healthcare, and NorthStar Real Estate Income II, Inc. or NorthStar Income II. In addition, NSAM owns NorthStar Realty Securities, LLC, or NorthStar Securities, our previously owned captive broker-dealer platform, and performs other asset management-related services.

Prior to the Distribution, we completed an internal corporate reorganization whereby we collapsed our three-tier holding company structure into a single tier with former NorthStar Realty Finance Corp., a Maryland corporation, merging into the Company (formerly known as NRFC Sub-REIT Corp.) and the Company being re-named NorthStar Realty Finance Corp. Unless the context requires otherwise, references in this proxy statement to “the Company,” “we,” “us” or similar terms include our predecessor that merged into us as part of our internal corporate reorganization and all share and per share amounts have been retrospectively adjusted to reflect the one-for-two reverse stock split of our common stock.

The mailing address of our executive office is 399 Park Avenue, 18th Floor, New York, New York 10022. This proxy statement, the accompanying proxy card and the notice of annual meeting are first being mailed to holders of our common stock, par value $0.01 per share, on or about August 13, 2014. Our common stock is the only security entitled to vote at the annual meeting and we refer to our common stock in this proxy statement as our voting securities. Along with this proxy statement, we are also sending our Annual Report to Stockholders for the fiscal year ended December 31, 2013.

A proxy may confer discretionary authority to vote with respect to any matter presented at the annual meeting. As of the date of this proxy statement, management has no knowledge of any business that will be presented for consideration at the annual meeting and that would be required to be set forth in this proxy statement or the related proxy card other than the matters set forth in the accompanying notice of annual meeting of stockholders. If any other matter is properly presented at the annual meeting for consideration, it is intended that the persons named in the enclosed proxy card and acting thereunder will vote in accordance with their discretion on any such matter.

Grant Thornton LLP, an independent registered public accounting firm, has provided services to us during the past fiscal year, which included the examination of our Annual Report on Form 10-K, review of our quarterly reports on Form 10-Q and review of registration statements and other filings with the United States Securities and Exchange Commission, or the SEC. A representative of Grant Thornton LLP is expected to be present at the annual meeting, will be available to respond to appropriate questions from our stockholders and will be given an opportunity to make a statement if he or she desires to do so.

1

Matters to be Considered and Voted Upon at the Annual Meeting

At the annual meeting, our stockholders will consider and vote upon:

| 1) | a proposal to elect as directors the five individuals nominated by our Board as set forth in the accompanying proxy statement, each to serve until the 2015 annual meeting of stockholders and until his or her successor is duly elected and qualified; |

| 2) | a proposal to adopt a resolution approving, on a non-binding, advisory basis, named executive officer compensation as disclosed in this proxy statement; |

| 3) | a proposal to ratify the appointment of Grant Thornton LLP as our independent registered public accounting firm for the fiscal year ending December 31, 2014; and |

| 4) | the transaction of any other business that may properly come before the annual meeting or any postponement or adjournment of the annual meeting. |

Solicitation of Proxies

Your proxy is being solicited by and on behalf of our Board. The expense of preparing, printing and mailing this proxy statement and the proxies solicited hereby will be borne by us. In addition to the use of the mail, proxies may be solicited by officers and directors, without additional remuneration, by personal interview, telephone, electronic communications or otherwise. We will also request brokerage firms, nominees, custodians and fiduciaries to forward proxy materials to the beneficial owners of shares of common stock held of record as of the close of business on August 6, 2014 and will provide reimbursement for the cost of forwarding the materials.

In addition, we engaged McKenzie Partners to assist in soliciting proxies from brokers, banks and other nominee holders of our shares of common stock at a cost of $5,000, plus reasonable out-of-pocket expenses.

Stockholders Entitled To Vote

As of the close of business on August 6, 2014, there were 197,862,409 shares of our common stock outstanding and entitled to vote. Each share of our common stock entitles the holder to one vote. Common stockholders of record at the close of business on August 6, 2014 are entitled to vote at the annual meeting or any postponement or adjournment thereof.

Abstentions and Broker Non-Votes

If you hold your shares in street name and do not provide voting instructions to your bank, broker or other nominee, your shares will not be voted on any proposal on which your broker or other nominee does not have discretionary authority to vote under the rules of the New York Stock Exchange, or the NYSE, and therefore will be considered to be “broker non-votes.” Abstentions and broker non-votes, if any, will be counted as present at the meeting for the purpose of determining a quorum. Your bank, broker or other nominee does not have discretionary authority to vote your shares on the election of directors or the adoption of a resolution approving, on a non-binding, advisory basis, named executive officer compensation if your bank, broker or other nominee does not receive voting instructions from you.

Required Quorum/Vote

A quorum will be present if stockholders entitled to cast a majority of all the votes entitled to be cast at the annual meeting are present, in person or by proxy. If you hold your shares in your own name as holder of record and return a valid proxy, authorize your proxy by phone or internet or attend the annual meeting in person, your shares will be counted for the purpose of determining whether there is a quorum. If a quorum is not present, the annual meeting may be adjourned by the chairman of the meeting to a time and date not more than 120 days after the original record date without notice other than announcement at the meeting.

Election of the director nominees named in Proposal No. 1 requires the affirmative vote of a plurality of all the votes cast in the election of directors at the annual meeting by holders of our voting securities. The candidates receiving the highest number of affirmative votes will be elected directors. Shares represented by executed proxies will be voted, if authority to do so is not withheld,

2

for the election of each of our Board’s nominees named in Proposal No. 1. Votes may be cast in favor of or withheld with respect to all of the director nominees or any one or more of them. Votes “withheld” and broker non-votes, if any, will not be counted as votes cast and will have no effect on the outcome of the vote on the election of directors. Stockholders may not cumulate votes in the election of directors.

Approval, on a non-binding and advisory basis, of the compensation of our named executive officers, as specified in Proposal No. 2, requires the affirmative vote of a majority of the votes cast on the proposal at the annual meeting by holders of our voting securities. Abstentions and broker non-votes, if any, will not be counted as votes cast and will have no effect on the outcome of the vote on this proposal.

Ratification of the selection of Grant Thornton LLP as our independent registered public accounting firm for fiscal year 2014, as specified in Proposal No. 3, requires the affirmative vote of a majority of the votes cast on the proposal at the annual meeting by holders of our voting securities. Abstentions, if any, will not be counted as votes cast and will have no effect on the outcome of the vote on this proposal. Broker non-votes will not arise in connection with, and will have no effect on the outcome of, this proposal because brokers may vote in their discretion on behalf of clients who have not furnished voting instructions. If this selection is not ratified by holders of our voting securities, the Audit Committee of the Board, or the Audit Committee, may, but need not, reconsider its appointment and endorsement, respectively. Even if the selection is ratified, the Audit Committee in its discretion may direct the appointment of a different independent registered public accounting firm at any time during the year if it determines that such a change would be in the best interest of the Company.

If the enclosed proxy is properly executed and returned to us in time to cast the votes represented by such shares at the annual meeting, it will be voted as specified on the proxy unless it is properly revoked prior thereto. If no specification is made on the proxy as to any one or more of the proposals, the shares of our voting securities represented by the proxy will be voted as follows:

| 1) | FOR the election of all five nominees for director nominated by our Board; |

| 2) | FOR the adoption of a resolution approving, on a non-binding, advisory basis, named executive officer compensation, as disclosed in this proxy statement; |

| 3) | FOR the ratification of the appointment of Grant Thornton LLP as our independent registered public accounting firm for the fiscal year ending December 31, 2014; and |

| 4) | in the discretion of the proxy holder on the transaction of any other business that properly comes before the annual meeting or any postponement or adjournment thereof. |

As of the date of this proxy statement, we are not aware of any other matter to be raised at the annual meeting.

Voting

If you hold your shares of our voting securities in your own name as a holder of record, you may instruct the proxies to vote your shares as follows:

| • | Telephone—you can authorize your proxy by telephone by calling 1-(800)-proxies (1-800-776-9437) and following the instructions on the proxy card if you are located in the United States. The authorization of your proxy by telephone is available 24 hours a day. To be valid, an authorization by telephone must be received by 11:59 p.m. (Eastern Time) on September 4, 2014; |

| • | Internet—you can authorize your proxy over the Internet at www.voteproxy.com by following the instructions on the proxy card. To be valid, authorization via the Internet must be received by 11:59 p.m. (Eastern Time) on September 4, 2014; or |

| • | Mail—you can authorize your proxy by mail by signing, dating and mailing the enclosed proxy card. To be valid, authorization by mail must be received by 5:00 p.m. (Eastern Time) on September 4, 2014. |

In addition, if you are a stockholder of record, you may vote your shares of our voting securities in person at the annual meeting.

3

If your shares of our voting securities are held on your behalf by a broker, bank or other nominee, you will receive instructions from such individual or entity that you must follow in order to have your shares voted at the annual meeting. Telephone and Internet voting also will be offered to stockholders owning shares through certain banks and brokers. If your shares are not registered in your own name and you plan to vote your shares in person at the annual meeting, you should contact your broker or agent to obtain a legal proxy or broker’s proxy card and bring it to the meeting in order to vote.

Right to Revoke Proxy

If you hold shares of our voting securities in your own name as a holder of record, you may revoke your proxy instructions through any of the following methods:

| • | authorize a new proxy via telephone or Internet that is received by 11:59 p.m. (Eastern Time) on September 4, 2014; |

| • | send written notice of revocation to our General Counsel at 399 Park Avenue, 18th Floor, New York, New York 10022, which notice must be received by 5:00 p.m. (Eastern Time) on September 4, 2014; |

| • | sign and mail a new, later-dated proxy card to our General Counsel at the address specified above, which proxy card must be received by 5:00 p.m. (Eastern Time) on September 4, 2014; or |

| • | attend the annual meeting and vote your shares in person. |

Only the most recent proxy will be counted and all others will be disregarded regardless of the method by which the proxy was authorized. If shares of our voting securities are held on your behalf by a broker, bank or other nominee, you must contact it to receive instructions as to how you may revoke your proxy instructions.

Copies of Annual Report to Stockholders

A copy of our Annual Report to Stockholders for the fiscal year ended December 31, 2013 is being mailed with these proxy materials to stockholders entitled to vote at the annual meeting and is also available without charge to stockholders upon written request to: NorthStar Realty Finance Corp., 399 Park Avenue, 18th Floor, New York, New York 10022, Attn: General Counsel.

Annual Report and Quarterly Reports

We make available free of charge through our website at www.nrfc.com under the heading “Investor Relations-SEC Filings” our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and all amendments to those reports as soon as reasonably practicable after such material is electronically filed with or furnished to the SEC. Further, we will provide, without charge to each stockholder upon written request, a copy of our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and all amendments to those reports. Requests for copies should be addressed to: NorthStar Realty Finance Corp., 399 Park Avenue, 18th Floor, New York, New York 10022, Attn: General Counsel. Copies may also be accessed electronically by means of the SEC home page on the Internet, at www.sec.gov. Neither our Annual Report on Form 10-K, nor our Annual Report to Stockholders, for the fiscal year ended December 31, 2013, is part of these proxy solicitation materials.

Householding Information

We have adopted a procedure approved by the SEC called “householding.” Under this procedure, stockholders of record who have received 60-days’ prior notice from us or their broker and have the same last name and address will receive only one copy of our Annual Report to Stockholders for the fiscal year ended December 31, 2013, unless one or more of these stockholders notifies us that they wish to continue receiving individual copies. This procedure will reduce our printing costs and postage fees. Also, householding will not in any way affect dividend check mailings.

If you participate in householding and wish to receive a separate copy of our Annual Report to Stockholders for the fiscal year ended December 31, 2013, please request a copy in writing from NorthStar Realty Finance Corp., 399 Park Avenue, 18th Floor, New York, New York 10022, Attn: General Counsel or by phone by calling (212) 547-2600, and a copy will be provided to you promptly.

If you do not wish to continue participating in householding and prefer to receive separate copies of future annual reports to stockholders and other stockholder communications or you have the same last name and address as another stockholder and do not

4

participate in householding, but wish to do so, notify our General Counsel in writing at the following address: NorthStar Realty Finance Corp., 399 Park Avenue, 18th Floor, New York, New York 10022.

Voting Results

American Stock Transfer & Trust Company, LLC will have a representative present at the annual meeting to count the votes and act as the Inspector of Election. We will publish the voting results in a Current Report on Form 8-K, which we plan to file with the SEC within four business days of the annual meeting.

Confidentiality of Voting

We will keep all proxies, ballots and voting tabulations confidential. We will permit only our Inspector of Election, American Stock Transfer & Trust Company, LLC, to examine these documents, except as necessary to meet applicable legal requirements.

Recommendations of our Board

Our Board recommends a vote:

| 1) | FOR the election of all five nominees for director nominated by our Board; |

| 2) | FOR the adoption of a resolution approving, on a non-binding, advisory basis, named executive officer compensation as disclosed in this proxy statement; |

| 3) | FOR the ratification of the appointment of Grant Thornton LLP as our independent registered public accounting firm for the fiscal year ending December 31, 2014; and |

| 4) | in the discretion of the proxy holder on the transaction of any other business that properly comes before the annual meeting or any postponement or adjournment thereof. |

Important Notice Regarding the Availability of Proxy Materials for the 2014 Annual Meeting of Stockholders to be Held on September 5, 2014.

The Company’s Proxy Statement for the 2014 Annual Meeting of Stockholders and the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2013 are available at www.nrfcproxy.com.

BOARD OF DIRECTORS

General

Effective June 30, 2014, after the completion of our internal corporate reorganization and in connection with the spin-off of our asset management business to NSAM, Stephen E. Cummings, Oscar Junquera and Sridhar Sambamurthy resigned from our Board. Messrs. Cummings and Junquera joined the board of directors of NSAM. In addition, on June 30, 2014, Charles W. Schoenherr was appointed as a member of the Board, chairman of the compensation committee of the Board and as a member of each of the audit committee and the nominating and corporate governance committee of the Board. Consequently, our Board presently consists of six members, five of whom are being nominated for re-election.

Having reached the retirement age set forth in the Company’s Corporate Governance Guidelines, C. Preston Butcher will not be nominated for re-election at the 2014 annual meeting, and accordingly, will no longer serve on the Board following the 2014 annual meeting. Mr. Butcher has been one of our directors since our initial public offering in 2004 and has been invaluable to the leadership of our Company during his tenure. Through multiple market cycles and changing market conditions, Mr. Butcher has provided our Board a unique perspective and informed advice on matters central to the Company’s business and on matters pertaining to the real estate industry in general. Mr. Butcher’s knowledge of the commercial real estate markets and extensive leadership and expertise have been instrumental to the growth and success of our Company over time. In connection with Mr. Butcher not being nominated for re-election at the 2014 annual meeting, the Board will reduce its size to five members effective as of the 2014 annual meeting.

5

At the annual meeting, stockholders will vote on the election of Messrs. David T. Hamamoto, Wesley D. Minami, Louis J. Paglia and Charles W. Schoenherr and Ms. Judith A. Hannaway, for a term ending at the 2015 annual meeting of stockholders and until their successors are duly elected and qualified.

The director nominees listed below are leaders in business as well as in the real estate and financial communities because of their intellectual acumen and analytic skills, strategic vision and their records of outstanding accomplishments over a period of decades. Each has been chosen to stand for re-election in part because of his or her ability and willingness to understand our unique position and evaluate and implement our strategies.

Set forth below is each director nominee’s name and age as of the date of this proxy statement and his or her principal occupation, business history and public company directorships held during the past five years. Also set forth below are the specific experience, qualifications, attributes and skills of the director nominees that led our Board to conclude that each such person should serve as a director of the Company. Each of our director nominees currently serves on our Board and, except for Mr. Schoenherr, was elected by the stockholders at the 2013 annual meeting of stockholders.

Current Directors Who are Nominees for Election or Re-election

| Name | Age | |

| David T. Hamamoto | 54 | |

| Judith A. Hannaway | 62 | |

| Wesley D. Minami | 57 | |

| Louis J. Paglia | 56 | |

| Charles W. Schoenherr | 54 | |

David T. Hamamoto. Mr. Hamamoto has been our Chairman since October 2007 and has served as one of our directors since October 2003. Mr. Hamamoto has been our Chief Executive Officer since October 2004 and was our President from October 2004 to April 2011. Mr. Hamamoto also serves as Chairman and Chief Executive Officer of NSAM, a position he has held since January 2014. Mr. Hamamoto has also served as Chairman of NorthStar Income, the first public non-traded REIT originally sponsored by us, since February 2009 and served as its Chief Executive Officer from February 2009 until January 2013. Mr. Hamamoto has also served as Chairman of NorthStar Healthcare, the second public non-traded REIT originally sponsored by us, from January 2013 until January 2014. Mr. Hamamoto has further served as Chairman of NorthStar Income II, the third public non-traded REIT originally sponsored by us, since December 2012. In July 1997, Mr. Hamamoto co-founded NorthStar Capital Investment Corp., the predecessor to the Company, for which he served as Co-Chief Executive Officer until October 2004. From 1983 to 1997, Mr. Hamamoto worked for Goldman, Sachs & Co. where he was co-head of the Real Estate Principal Investment Area and general partner of the firm between 1994 and 1997. During Mr. Hamamoto’s tenure at Goldman, Sachs & Co., he initiated the firm’s effort to build a real estate principal investment business under the auspices of the Whitehall Funds. Additionally, Mr. Hamamoto has served as a member of the advisory committee of RXR Realty, LLC, or RXR Realty, a leading real estate operating and investment management company focused on high-quality real estate investments in the New York Tri-State area, since December 2013. Mr. Hamamoto served as Executive Chairman from March 2011 until November 2012, and as Chairman, from February 2006 until March 2011, of the board of directors of Morgans Hotel Group Co. (NASDAQ: MHGC). Mr. Hamamoto holds a Bachelor of Science from Stanford University in Palo Alto, California and a Master of Business Administration from the Wharton School of Business at the University of Pennsylvania in Philadelphia, Pennsylvania.

Consideration for Recommendation: As a founder of the Company, Mr. Hamamoto offers our Board an intuitive perspective of the business and operations of the Company as a whole. Mr. Hamamoto also has significant experience in all aspects of the commercial real estate markets, which he gained initially as co-head of the Real Estate Principal Investment Area at Goldman, Sachs & Co. Mr. Hamamoto is able to draw on his extensive knowledge to develop and articulate sustainable initiatives, operational risk management and strategic planning, which qualify him to serve as a director of the Company.

Judith A. Hannaway. Ms. Hannaway has been one of our directors since September 2004. Ms. Hannaway also serves as a director of NSAM, a position she has held since June 2014. Currently, and during the past five years, Ms. Hannaway has acted as a

6

consultant to various financial institutions. Prior to acting as a consultant, Ms. Hannaway was previously employed by Scudder Investments, a wholly-owned subsidiary of Deutsche Bank Asset Management, as a Managing Director. Ms. Hannaway joined Scudder Investments in 1994 and was responsible for Special Product Development including closed-end funds, off shore funds and REIT funds. Prior to joining Scudder Investments, Ms. Hannaway was employed by Kidder Peabody as a Senior Vice President in Alternative Investment Product Development. She joined Kidder Peabody in 1980 as a Real-Estate Product Manager. Ms. Hannaway holds a Bachelor of Arts from Newton College of the Sacred Heart and a Master of Business Administration from Simmons College Graduate Program in Management.

Consideration for Recommendation: Ms. Hannaway has had significant experience at major financial institutions and has broad ranging financial services expertise and experience in the areas of financial reporting, risk management and alternative investment products. Ms. Hannaway’s financial-related experience qualifies her to serve as a director of the Company.

Wesley D. Minami. Mr. Minami has been one of our directors since September 2004. Mr. Minami also serves as a director of NSAM, a position he has held since June 2014. Mr. Minami served as President of Billy Casper Golf LLC from 2003 until March 2012, at which time he ceased acting as President and began serving as Principal. From 2001 to 2002, he served as President of Charles E. Smith Residential Realty, Inc., a REIT that was listed on the NYSE. In this capacity, Mr. Minami was responsible for the development, construction, acquisition and property management of over 22,000 high-rise apartments in five major U.S. markets. He resigned from this position after completing the transition and integration of Charles E. Smith Residential Realty, Inc. from an independent public company to a division of Archstone-Smith Trust, an apartment company that was listed on the NYSE. From 1997 to 2001, Mr. Minami worked as Chief Financial Officer and then Chief Operating Officer of Charles E. Smith Residential Realty, Inc. Prior to 1997, Mr. Minami served in various financial service capacities for numerous entities, including Ascent Entertainment Group, Comsat Corporation, Oxford Realty Services Corporation and Satellite Business Systems. Mr. Minami holds a Bachelor of Arts in Economics, with honors, from Grinnell College and a Master of Business Administration in Finance from the University of Chicago.

Consideration for Recommendation: Mr. Minami, who has served as President of a publicly-traded REIT, chief financial officer and chief operating officer of a real estate company and in various financial service capacities, brings corporate finance, operations, public company and executive leadership expertise to our Board. Mr. Minami’s diverse experience, real estate background and understanding of financial statements qualify him to serve as a director of the Company.

Louis J. Paglia. Mr. Paglia has been one of our directors since February 2006. Mr. Paglia also serves as a director of NSAM, a position he has held since June 2014, and Arch Capital Group Ltd. (NASDAQ: ACGL), a position he has held since July 2014. Mr. Paglia founded Customer Choice LLC in April 2010, a data analytics company serving the electric utility industry. From April 2002 to March 2006, Mr. Paglia was the Executive Vice President of UIL Holdings Corporation, an electric utility, contracting and energy infrastructure company. Mr. Paglia was also President of UIL Holdings’ investment subsidiaries. From July 2002 through April 2005, Mr. Paglia also served as UIL Holdings’ Chief Financial Officer. From 1999 to 2001, Mr. Paglia was Executive Vice President and Chief Financial Officer of eCredit.com, a credit evaluation software company. Prior to 1999, Mr. Paglia served as the Chief Financial Officer for TIG Holdings Inc. and Emisphere Technologies, Inc. Mr. Paglia received a Bachelor of Science from Massachusetts Institute of Technology and a Master of Business Administration from the Wharton School of Business at the University of Pennsylvania.

Consideration for Recommendation: Mr. Paglia brings a career of broad ranging financial expertise, having held several chief financial officer positions, including at three public companies. Mr. Paglia’s extensive accounting, finance and risk management expertise qualify him to serve as a director of the Company.

Charles W. Schoenherr. Mr. Schoenherr has been one of our directors since June 2014. Mr. Schoenherr serves as Managing Director of Waypoint Residential, LLC which invests in multifamily properties in the Sunbelt. He has served in this capacity since October 2011 and is responsible for sourcing acquisition opportunities and raising capital. Mr. Schoenherr is also an independent director and a member of the audit committee of each of NorthStar Income and NorthStar Income II, positions he has held since January 2010 and December 2012, respectively. From January 2011 through December 2013, Mr. Schoenherr served as Chief Investment Officer of Broadway Partners Fund Manager, LLC, a private real estate investment and management firm that invests in office buildings across the United States. From June 2009 until January 2011, Mr. Schoenherr served as President of Scout Real Estate Capital, LLC, a full service real estate firm that focuses on acquiring, developing and operating hospitality assets, where he was responsible for managing the company’s properties and originating new acquisition and asset management opportunities. Prior to joining Scout Real Estate Capital, LLC, Mr. Schoenherr was the managing partner of Elevation Capital, LLC, where he advised real estate clients on debt and equity restructuring and performed due diligence and valuation analysis on new acquisitions between

7

November 2008 and June 2009. Between September 1997 and October 2008, Mr. Schoenherr served as Senior Vice President and Managing Director of Lehman Brothers’ Global Real Estate Group, where he was responsible for originating debt, mezzanine and equity transactions on all major property types throughout the United States. During his career he has also held senior management positions with GE Capital Corporation, GE Investments, Inc. and KPMG LLP, where he also practiced as a certified public accountant. Mr. Schoenherr currently serves on the Board of Trustees of Iona College and is on its Real Estate and Investment Committees. Mr. Schoenherr holds a Bachelor of Business Administration in Accounting from Iona College and a Master of Business Administration in Finance from the University of Connecticut.

Consideration for Recommendation: Mr. Schoenherr’s knowledge of the real estate investment and finance industries, including extensive experience originating debt, mezzanine and equity transactions, qualify him to serve as a director of the Company.

Corporate Governance Profile

We are committed to good corporate governance practices and, as such, we have adopted the corporate governance guidelines and codes of ethics discussed below to enhance our effectiveness.

Code of Ethics for Senior Financial Officers

We adopted a code of ethics for senior financial officers applicable to our chief executive officer, chief financial officer and all other senior financial officers of the Company. The code is available on our website at www.nrfc.com under the heading “Investor Relations—Corporate Governance.” Amendments to, and waivers from, the code of ethics for senior financial officers will be disclosed on our website at www.nrfc.com under the heading “Investor Relations—Corporate Governance.”

Code of Business Conduct and Ethics

We adopted a code of business conduct and ethics relating to the conduct of our business by our employees, officers and directors. We intend to maintain high standards of ethical business practices and compliance with all laws and regulations applicable to our business, including those relating to doing business outside the United States. Specifically, among other things, our code of business conduct and ethics prohibits employees from providing gifts, meals or anything of value to government officials or employees or members of their families without prior written approval from the Company’s General Counsel. The code is available on our website at www.nrfc.com under the heading “Investor Relations—Corporate Governance” and is also available without charge to stockholders upon written request to: NorthStar Realty Finance Corp., 399 Park Avenue, 18th Floor, New York, New York 10022, Attn: General Counsel.

Corporate Governance Guidelines

We adopted corporate governance guidelines to assist our Board in the exercise of its responsibilities. The corporate governance guidelines govern, among other things, Board composition, Board member qualifications, responsibilities and education, management succession and self-evaluation. A copy of our corporate governance guidelines may be found on our website at www.nrfc.com under the heading “Investor Relations—Corporate Governance” and are also available without charge to stockholders upon written request to: NorthStar Realty Finance Corp., 399 Park Avenue, 18th Floor, New York, New York 10022, Attn: General Counsel.

Board Committees

Our Board has appointed an Audit Committee, a Compensation Committee and a Nominating and Corporate Governance Committee and each of these standing committees has adopted a committee charter. Each of these committees is composed exclusively of independent directors, as defined by the listing standards of the NYSE. Moreover, the Compensation Committee is composed exclusively of individuals referred to as “non-employee directors” in Rule 16b-3 of the Securities Exchange Act of 1934, as amended, or the Exchange Act, and “outside directors” in Section 162(m) of the Internal Revenue Code of 1986, as amended, or the Internal Revenue Code.

During the year ended December 31, 2013, our Board met on thirteen occasions. Each director then serving attended at least 75% of the aggregate number of meetings of our Board and all committees on which he or she served.

8

The following table shows the current membership of the various committees:

| Audit | Compensation | Nominating and Corporate Governance | ||

Louis J. Paglia^* Wesley D. Minami^ Charles W. Schoenherr | Charles W. Schoenherr* Judith A. Hannaway Louis J. Paglia | Wesley D. Minami* Judith A. Hannaway Charles W. Schoenherr | ||

____________

| * | Denotes Chairperson |

| ^ | Denotes Audit Committee Financial Expert |

Audit Committee

The Audit Committee held eight meetings in 2013. Its report is included later within this proxy statement. Our Board has determined that all three members of the Audit Committee are independent and financially literate under the rules of the NYSE and that at least two members, Mr. Paglia, who chairs the Audit Committee, and Mr. Minami, are “audit committee financial experts,” as that term is defined by the SEC. The Audit Committee is responsible for, among other things, engaging an independent registered public accounting firm, reviewing with the independent registered public accounting firm the plans and results of the audit engagement, approving professional services provided by the independent registered public accounting firm, reviewing the independence of the independent registered public accounting firm, considering the range of audit and non-audit fees and assisting our Board in its oversight of our internal controls over financial reporting.

A copy of the Audit Committee charter is available on our website at www.nrfc.com under the heading “Investor Relations—Corporate Governance” and is also available without charge to stockholders upon written request to: NorthStar Realty Finance Corp., 399 Park Avenue, 18th Floor, New York, New York 10022, Attn: General Counsel.

Compensation Committee

The Compensation Committee held three formal meetings as well as numerous informal meetings in 2013. Its report is included later within this proxy statement. Our Board has determined that all members of the Compensation Committee are independent under the rules of the NYSE. Mr. Schoenherr chairs the Compensation Committee.

The Compensation Committee is responsible for, among other things, determining compensation for our executive officers, administering and monitoring our equity compensation plans, evaluating the performance of our executive officers and producing an annual report on executive compensation for inclusion in our annual meeting proxy statement. The Compensation Committee may delegate some or all of its duties to a subcommittee comprising one or more members of the Compensation Committee.

A copy of the Compensation Committee charter is available on our website at www.nrfc.com under the heading “Investor Relations—Corporate Governance” and is also available without charge to stockholders upon written request to: NorthStar Realty Finance Corp., 399 Park Avenue, 18th Floor, New York, New York 10022, Attn: General Counsel.

Nominating and Corporate Governance Committee

The Nominating and Corporate Governance Committee held three meetings in 2013. Our Board has determined that all members of the Nominating and Corporate Governance Committee are independent under the rules of the NYSE. Mr. Minami chairs the Nominating and Corporate Governance Committee. The Nominating and Corporate Governance Committee is responsible for, among other things, seeking, considering and recommending to our Board qualified candidates for election as directors and recommending a slate of nominees for election as directors at the annual meeting. It also periodically prepares and submits to our Board for adoption the Nominating and Corporate Governance Committee’s selection criteria for director nominees. It reviews and makes recommendations on matters involving the general operation of our Board and our corporate governance, and annually recommends to our Board nominees for each committee of our Board. In addition, the Nominating and Corporate Governance Committee annually facilitates the assessment of our Board’s performance as a whole and of the individual directors and reports thereon to our Board.

9

A copy of the Nominating and Corporate Governance Committee charter is available on our website at www.nrfc.com under the heading “Investor Relations—Corporate Governance” and is also available without charge to stockholders upon written request to: NorthStar Realty Finance Corp., 399 Park Avenue, 18th Floor, New York, New York 10022, Attn: General Counsel.

Compensation Committee Interlocks and Insider Participation

There are no Compensation Committee interlocks or employee participation on the Compensation Committee.

Director Independence

Of our five directors being nominated for re-election, four have been determined by our Board to be independent for purposes of the NYSE listing standards. In determining director independence, our Board reviewed, among other things, any transactions or relationships that exist currently or that have existed since our incorporation, between each director and the Company and its subsidiaries, affiliates and equity investors or independent auditors. In particular, our Board reviewed current or recent business transactions or relationships or other personal relationships between each director and the Company, including such director’s immediate family and companies owned or controlled by the director or with which the director was affiliated. The purpose of this review was to determine whether any such transactions or relationships failed to meet any of the objective tests promulgated by the NYSE for determining independence or were otherwise sufficiently material as to be inconsistent with a determination that the director is independent. Our Board also examined whether there were any transactions or relationships between each director and members of our senior management or our affiliates.

As a result of its review, our Board affirmatively determined that Messrs. Minami, Paglia and Schoenherr and Ms. Hannaway are independent under the NYSE listing standards.

Board Leadership Structure; Meetings of Independent Directors

Our Board believes it is important to select its chairman and the Company’s chief executive officer in the manner it considers to be in the best interests of the Company at any given point in time. The members of our Board possess considerable business experience and in-depth knowledge of the issues the Company faces, and are therefore in the best position to evaluate the needs of the Company and how best to organize the Company’s leadership structure to meet those needs. Accordingly, the chairman and chief executive officer positions may be filled by one individual or by two different individuals. After careful consideration, our Board believes that the most effective leadership structure for the Company at this time is for Mr. Hamamoto to serve as both our chairman and chief executive officer. Mr. Hamamoto’s combined role as chairman and chief executive officer creates a firm link between management and our Board and provides unified leadership for carrying out the Company’s strategic initiatives and business plans. Our Board continually evaluates the Company’s leadership structure and could in the future decide not to combine the chairman and chief executive officer positions if it believes that doing so would serve the best interests of the Company.

To promote the independence of our Board and appropriate oversight of management, the independent directors select a Lead Non-Management Director, currently Mr. Minami, to facilitate free and open discussion and communication among the independent directors of our Board and management. The Lead Non-Management Director presides at all executive sessions at which only non-management directors are present. These meetings are held in conjunction with the regularly scheduled quarterly meetings of our Board, but may be called at any time by our Lead Non-Management Director or any of our other independent directors. In 2013, our independent directors met six times in executive session without management present following Board meetings and met outside of regularly scheduled Board meetings on a number of occasions. Our Lead Non-Management Director sets the agenda for these meetings and discusses issues that arise during those meetings with our chairman. Our Lead Non-Management Director also discusses with our chairman and secretary Board meeting agendas and may request the inclusion of additional agenda items for meetings of our Board. It is expected, as provided in our corporate governance guidelines, that the individual who serves as the Lead Non-Management Director shall rotate every two years.

Communications with Directors

Our Board has established a process to receive communications from interested parties, including stockholders. Interested parties may contact the Lead Non-Management Director, any member or all members of our Board by mail. To communicate with our Board, any individual director or any group or committee of directors, correspondence should be addressed to our Board or any such

10

individual director or group or committee of directors by either name or title. All such correspondence should be sent in care of our General Counsel at NorthStar Realty Finance Corp., 399 Park Avenue, 18th Floor, New York, New York 10022.

All communications received as set forth in the preceding paragraph will be opened by the office of our General Counsel for the sole purpose of determining whether the contents represent a message to our directors. Any contents that are not in the nature of advertising, promotions of a product or service or patently offensive material will be forwarded promptly to the addressee. In the case of communications to our Board or any group or committee of directors, the office of the General Counsel will make sufficient copies of the contents to send to each director who is a member of the group or committee to which the envelope is addressed.

Section 16(a) Beneficial Ownership Reporting Compliance

Section 16(a) of the Exchange Act requires our executive officers, directors and persons who own more than 10% of a registered class of our equity securities to file reports of beneficial ownership of such securities on Forms 3, 4 and 5 with the SEC. Officers, directors and persons who own more than 10% of a registered class of our equity securities are required to furnish us with copies of all Forms 3, 4 and 5 that they file. Based solely on our review of the copies of such forms we received or written representations from certain reporting persons that no filings on such forms were required for those persons, we believe that all such filings required to be made during and with respect to the fiscal year ended December 31, 2013 by Section 16(a) of the Exchange Act were timely made.

Director Nomination Procedures

The Nominating and Corporate Governance Committee generally believes that, at a minimum, candidates for membership on our Board should have demonstrated an ability to make a meaningful contribution to our Board’s oversight of our business and affairs and have a record and reputation for honest and ethical conduct. The Nominating and Corporate Governance Committee recommends director nominees to our Board based on, among other things, its evaluation of a candidate’s experience and skills, relevant industry background and knowledge, integrity, ability to make independent analytical inquiries and a willingness to devote adequate time and effort to Board responsibilities. In addition to the criteria set forth above, when identifying and selecting nominees for our Board, the Nominating and Corporate Governance Committee does not have a specific diversity policy with respect to the director nomination process, but strives to create diversity in perspective, background and experience in our Board as a whole and seeks to have our Board nominate candidates who have such diverse perspectives, backgrounds and experiences.

In the future, the Nominating and Corporate Governance Committee intends to identify potential nominees by asking current directors and executive officers to notify the committee if they become aware of persons who meet the criteria described above. The Nominating and Corporate Governance Committee also, from time-to-time, may engage firms, at our expense, that specialize in identifying director candidates. As described below, the Nominating and Corporate Governance Committee will also consider candidates recommended by stockholders.

The Nominating and Corporate Governance Committee anticipates that once a person has been identified as a potential candidate, the Nominating and Corporate Governance Committee will collect and review publicly-available information regarding such person to assess whether the person should be considered further. If the Nominating and Corporate Governance Committee determines that the candidate warrants further consideration, the chairman or another member of the Nominating and Corporate Governance Committee will contact the person. If the person expresses a willingness to be considered and to serve on our Board, the Nominating and Corporate Governance Committee will request information from the candidate, review the person’s accomplishments and qualifications, including in light of any other candidates that the Nominating and Corporate Governance Committee might be considering and conduct one or more interviews with the candidate. In certain instances, members of the Nominating and Corporate Governance Committee may contact one or more references provided by the candidate or may contact other members of the business community or other persons that may have greater first-hand knowledge of the candidate’s accomplishments.

The Nominating and Corporate Governance Committee will consider written recommendations from stockholders of potential director candidates that have followed the procedures for nominating directors set forth in our Amended and Restated Bylaws, or our bylaws. Such recommendations should be submitted to the Nominating and Corporate Governance Committee in care of our General Counsel at NorthStar Realty Finance Corp., 399 Park Avenue, 18th Floor, New York, New York 10022. Director recommendations submitted by stockholders must comply with the procedures set forth in our bylaws, as such may be amended from time-to-time, including providing the following:

| • | the name, age and business address of the individual(s) recommended for nomination; |

11

| • | the class, series and number of any shares of our stock that are beneficially owned by the individual(s) recommended for nomination; |

| • | the date such shares of our stock were acquired by the individual(s) recommended for nomination and the investment intent of such acquisition; |

| • | whether and the extent to which the individual(s) recommended for nomination or the nominating stockholder(s) have engaged in any hedging, derivative or similar transactions involving our securities, including our common stock, since our last annual meeting; and |

| • | all other information relating to such candidate that would be required to be disclosed pursuant to Regulation 14A under the Exchange Act, including such person’s written consent to being named in the proxy statement as a nominee and to serving as a director if elected. |

The foregoing is a summary only and you should refer to our bylaws for a full description of the procedures required to nominate a director. The Nominating and Corporate Governance Committee expects to use a similar process to evaluate candidates to our Board recommended by stockholders as the one it uses to evaluate candidates otherwise identified by the Committee.

Risk Oversight

Risk is inherent with every business and how well a business manages risk can ultimately determine its success. Our management team is responsible for our risk exposures on a day-to-day basis by identifying the material risks we face, implementing appropriate risk management strategies that are responsive to our risk profile, integrating consideration of risk and risk management into our decision-making process and, if necessary, promulgating policies and procedures to ensure that information with respect to material risks is transmitted to our Board. Our Board, as a whole and through its committees, has the responsibility to oversee and monitor these risk management processes by informing itself of material risks and evaluating whether management has reasonable controls in place to address the material risks; our Board is not responsible, however, for defining or managing our various risks. Our Board is regularly informed by management of potential material risks and activities related to those risks at Board meetings. Members of our management team generally attend all Board meetings and management is readily available to our Board to address any questions or concerns raised by our Board on risk management and any other matters.

Director Attendance at Annual Meeting

We do not currently maintain a policy requiring our directors to attend the annual meeting of stockholders. Messrs. Hamamoto and Paglia as well as Ms. Hannaway each attended the 2013 annual meeting of stockholders.

Directors Offer of Resignation Policy

Whenever a member of our Board: (i) accepts a position with a company that is competitive to the business(es) then engaged in by the Company; or (ii) violates our code of business conduct and ethics, corporate governance guidelines or any other Company policy applicable to members of our Board, pursuant to our resignation policy, he or she is to offer his or her resignation to the Nominating and Corporate Governance Committee for its consideration. The Nominating and Corporate Governance Committee will consider the resignation offer, giving due consideration to all relevant factors that the Nominating and Corporate Governance Committee deems appropriate under the circumstances, including, without limitation, any requirement of the NYSE or any rule or regulation promulgated under the Exchange Act, and will recommend to our Board the action to be taken with respect to any resignation offer.

Chief Executive Officer Succession Plan

Our Board has adopted a succession plan, which it intends to review periodically, with respect to selecting a successor to our chief executive officer.

EXECUTIVE OFFICERS

Our executive officers are appointed annually by our Board and serve at the discretion of our Board. Set forth below is information, as of the date of this proxy statement, regarding our current executive officers:

12

| Name | Age | Position | |

| David T. Hamamoto | 54 | Chairman and Chief Executive Officer | |

| Albert Tylis | 40 | President | |

| Daniel R. Gilbert | 44 | Chief Investment and Operating Officer | |

| Debra A. Hess | 50 | Chief Financial Officer | |

| Ronald J. Lieberman | 44 | Executive Vice President, General Counsel and Secretary | |

Set forth below is biographical information regarding each of our current executive officers, other than Mr. Hamamoto, whose biographical information is provided above under “Board of Directors.”

Albert Tylis. Mr. Tylis has served as our President since January 2013. Prior to his current position, Mr. Tylis served as our Co-President from April 2011 until January 2013, our Chief Operating Officer from January 2010 until January 2013, our Secretary from April 2006 until January 2013, an Executive Vice President from April 2006 until April 2011 and our General Counsel from April 2006 to April 2011. Mr. Tylis also serves as President of NSAM, a position he has held since January 2014. Mr. Tylis also served as Chief Operating Officer of NorthStar Income from October 2010 until January 2013 and as General Counsel and Secretary of NorthStar Income from October 2010 until April 2011. He has further served as Chairman of the board of directors of NorthStar Healthcare from April 2011 until January 2013 and as General Counsel and Secretary of NorthStar Healthcare from October 2010 until April 2011. Prior to joining the Company in August 2005, Mr. Tylis was the Director of Corporate Finance and General Counsel of ASA Institute and from September 1999 through February 2005, Mr. Tylis was a senior attorney at the law firm of Bryan Cave LLP, where he was a member of the Corporate Finance and Securities Group, the Transactions Group, the Banking, Business and Public Finance Group and supported the firm’s Real Estate Group. Additionally, Mr. Tylis has served as a member of the advisory committee of RXR Realty since December 2013. Mr. Tylis holds a Bachelor of Science from the University of Massachusetts at Amherst and a Juris Doctor from Suffolk University Law School.

Daniel R. Gilbert. Mr. Gilbert has served as our Chief Investment and Operating Officer since January 2013. Mr. Gilbert served as Co-President of the Company from April 2011 until January 2013 and in various other senior management positions since our initial public offering in October 2004. Mr. Gilbert also serves as Chief Investment and Operating Officer of NorthStar Asset Management Group, Ltd, a wholly-owned subsidiary of NSAM, a position he has held since June 2014. Mr. Gilbert also serves as the Chief Executive Officer and President of NorthStar Income and NorthStar Income II, as well as executive chairman of NorthStar Healthcare since January 2014 (having previously served as NorthStar Healthcare’s Chief Executive Officer and President from August 2012 to January 2014). Mr. Gilbert began serving as an executive officer of each of NorthStar Income, NorthStar Healthcare and NorthStar Income II from their inceptions, in January 2009, October 2010 and December 2012, respectively. Mr. Gilbert served as an Executive Vice President and Managing Director of Mezzanine Lending of NorthStar Capital Investment Corp. a predecessor company. Prior to that role, Mr. Gilbert was with Merrill Lynch & Co. in its Global Principal Investments and Commercial Real Estate Department and prior to joining Merrill Lynch, held accounting and legal-related positions at Prudential Securities Incorporated. Mr. Gilbert holds a Bachelor of Arts degree from Union College in Schenectady, New York.

Debra A. Hess. Ms. Hess currently serves as our Chief Financial Officer, a position she has held since July 2011. Ms. Hess has also served as Chief Financial Officer and Treasurer of NorthStar Income since October 2011 and as Chief Financial Officer and Treasurer of NorthStar Healthcare since March 2012. Ms. Hess also serves as Chief Financial Officer of NSAM, a position she has held since January 2014. Ms. Hess has further served as Chief Financial Officer and Treasurer of NorthStar Income II since December 2012. Ms. Hess has significant financial, accounting and compliance experience at public companies. Ms. Hess most recently served as Chief Financial Officer and Compliance Officer of H/2 Capital Partners, where she was employed from August 2008 to June 2011. From March 2003 to July 2008, Ms. Hess was a managing director at Fortress Investment Group, where she also served as Chief Financial Officer of Newcastle Investment Corp., a Fortress portfolio company and a NYSE-listed alternative investment manager. From 1993 to 2003, Ms. Hess served in various positions at Goldman, Sachs & Co., including as Vice President in Goldman Sachs’s Principal Finance Group and as a Manager of Financial Reporting in Goldman Sachs’ Finance Division. Prior to 1993, Ms. Hess was employed by Chemical Banking Corporation in the corporate credit policy group and by Arthur Andersen & Company as a supervisory senior auditor. Ms. Hess holds a Bachelor of Science in Accounting from the University of Connecticut in Storrs, Connecticut and a Master of Business Administration in Finance from New York University in New York, New York.

13

Ronald J. Lieberman. Mr. Lieberman currently serves as our Executive Vice President, General Counsel and Secretary. Mr. Lieberman has served as our General Counsel since April 2011, an Executive Vice President since April 2012 and as Assistant Secretary from April 2011 until January 2013. Mr. Lieberman also serves as Executive Vice President, General Counsel and Secretary of NSAM, a position he has held since January 2014. Mr. Lieberman has also served as General Counsel and Secretary of NorthStar Income and NorthStar Healthcare since October 2011 and April 2011, respectively, and as an Executive Vice President of each of those companies since January 2013. Mr. Lieberman has further served as General Counsel and Secretary of NorthStar Income II since December 2012 and as Executive Vice President of that company since March 2013. Prior to joining the Company, Mr. Lieberman was a partner in the Real Estate Capital Markets practice at the law firm of Hunton & Williams LLP. Mr. Lieberman practiced at Hunton & Williams from September 2000 until March 2011 where he advised numerous REITs, including mortgage REITs and specialized in capital markets transactions, mergers and acquisitions, securities law compliance, corporate governance and other board advisory matters. Prior to joining Hunton & Williams, Mr. Lieberman was the associate general counsel at Entrade, Inc., during which time Entrade was a public company listed on the NYSE. Mr. Lieberman began his legal career at Skadden, Arps, Slate, Meagher and Flom LLP. Mr. Lieberman holds a Bachelor of Arts, Master of Business Administration and Juris Doctor, each from the University of Michigan in Ann Arbor, Michigan.

EXECUTIVE COMPENSATION AND OTHER INFORMATION

Compensation Discussion and Analysis

General

This section describes the process that the Compensation Committee undertakes and the factors it considers in determining the appropriate compensation for our executive officers. The Compensation Committee is responsible for establishing and monitoring compensation programs and for evaluating the performance of our executive officers. The Compensation Committee reviews and approves individual executive officer salaries, bonuses and other equity-based awards.

Liquidity and capital started to become more available in the commercial real estate markets to stronger sponsors beginning in 2012 and Wall Street and commercial banks began to more actively provide credit to real estate borrowers, accelerating the pace of investment in real estate. Partly as a result of governmental stimulus, the commercial real estate markets have improved, with valuations approaching, and in some cases exceeding, 2007 levels. However, a range of economic and political headwinds remain, including a moderate labor market recovery, legislative gridlock, potential conflict over budget deficits and the debt ceiling, the impact of the Affordable Care Act, uncertain U.S. Federal Reserve policy, concern with emerging market economies and Eastern European strife, among other matters. We expect that this dynamic, along with global market instability and the risk of maturing commercial real estate debt that may have difficulties being refinanced, will continue to cause periodic volatility in the CRE market for some time.

The performance and efforts of our management team through varying economic and market conditions, including with respect to our legacy portfolio, continued to be evident in the Company’s performance in 2013. Our management team performed extremely well and generated $1.06 per share of cash available for distribution, or CAD and issued $1.9 billion of corporate capital during 2013. For a reconciliation of net income (loss) attributable to common stockholders to CAD, please refer to “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Non-GAAP Financial Measures” at pages 107 through 109 of the Company’s Annual Report on Form 10-K for the year ended December 31, 2013. In 2013, the Company committed to $3.6 billion of diversified commercial real estate investments with an expected weighted average return on equity in excess of 16%, which is accretive to the Company’s dividend. Additionally, the Company made investments of $1.3 billion on behalf of the non-traded REITs originally sponsored by the Company. As a result of the Company’s continued strong performance and operating cash flow, it increased its dividend each quarter in 2013, resulting in ten consecutive increases.

In addition, the Company raised $683 million of capital for the non-traded REITs originally sponsored by the Company resulting in $1.3 billion being raised from inception through December 31, 2013.

On June 30, 2014, we completed the previously announced spin-off of our asset management business into a separate publicly-traded company, NSAM, in the form of a tax-free distribution. In the distribution, each of our common stockholders received shares of NSAM common stock on a one-for-one basis, after giving effect to a one-for-two reverse stock split. Upon completion of the spin-off, our former asset management business became owned and operated by NSAM and we became externally managed by an affiliate of NSAM through a management contract with an initial term of 20 years. Affiliates of NSAM also manage the Company’s

14

previously sponsored non-traded REITs, NorthStar Income, NorthStar Healthcare and NorthStar Income II, and NSAM also owns NorthStar Realty Securities, LLC, formerly our captive broker-dealer platform. Notwithstanding the spin-off, we retained and we continue to operate our commercial real estate debt origination business. Employees of the Company at the time of the spin-off became employees of NSAM or one of its subsidiaries except for our executive officers, the employees engaged in our existing commercial real estate debt origination business and certain other employees that became co-employees of both the Company and NSAM or one of its subsidiaries.

Following the spin-off, the form and amount of compensation that we pay to our named executive officers will be significantly different from what it has been historically. We expect the substantial majority of the compensation that our named executive officers receive in the future for providing services to us will be determined and paid by NSAM or its subsidiaries; however, we will be obligated to pay or reimburse the subsidiary of NSAM that serves as our asset manager following the spin-off, or our asset manager, certain amounts related to the compensation or severance that NSAM or its subsidiaries determines to pay our named executive officers. Pursuant to the management agreement that we entered into in connection with the spin-off with our asset manager, we agreed to issue up to 50% of NSAM’s long-term bonus or other compensation that NSAM’s compensation committee determines shall be paid and/or settled in the form of the Company’s equity to executives, employees and service providers of our asset manager, including our named executive officers, in connection with the performance of services under the management agreement. At the discretion of NSAM’s compensation committee, the foregoing compensation may be granted in shares of our restricted stock, restricted stock units, or RSUs, long-term incentive plan units, or LTIP units, or other forms of equity compensation or stock-based awards, provided that if at any time, a sufficient number of shares of our common stock are not available for issuance under our equity compensation plan (as in effect from time-to-time), such equity compensation shall be paid in the form of RSUs, LTIP units or such other securities that may be settled by us in cash. We also agreed to reimburse our asset manager for additional costs and expenses incurred by it or its affiliated entities for an amount not to exceed the following: (i) 20% of the combined total of (a) our general and administrative expenses as reported in our consolidated financial statements excluding (1) equity-based compensation expense, (2) non-recurring items, (3) fees payable to our asset manager and its affiliated entities under the terms of the management agreement and (4) any allocation of expenses from NSAM (“NRF G&A”); and (b) our asset manager’s and its affiliated entities’ general and administrative expenses as reported in its consolidated financial statements, excluding equity-based compensation expense and adding back any costs or expenses allocated to us or any other company, fund or vehicle managed by our asset manager or certain of its affiliated entities; less (ii) the NRF G&A. In addition, we agreed to pay directly or reimburse our asset manager for the portion of any severance paid by our asset manager or NSAM or its other subsidiaries to an individual pursuant to the terms of any employment, consulting or similar service agreement that corresponds to or is attributable to (i) the equity compensation that we are required to pay directly or reimburse our asset manager, as described above, (ii) any cash and/or equity compensation paid directly by us to such individual as an employee or other service provider of our company and (iii) any amounts paid to such individual by our asset manager or NSAM or its other subsidiaries that we are obligated to reimburse our asset manager pursuant to the management agreement.

As of December 31, 2013, the Company had total equity capitalization, including common and preferred stock, of $5.0 billion. Into 2014, the Company experienced further significant growth. As of June 30, 2014, immediately prior to the spin-off of our asset management business, the Company had total equity capitalization of $7.4 billion and immediately following the spin-off, the Company had total equity capitalization of $4.2 billion.

The Company’s total stockholder return for 2013 was 107.7%. Additionally, the below chart presents a comparison of the Company’s five-year cumulative total stockholder return to the Russell 2000 and NAREIT All REIT Index.

15

________________

| (1) | The graph assumes an investment of $100 on January 1, 2009 and the reinvestment of any dividends. The stock price performance shown on this graph is not necessarily indicative of future price performance. The information in the graph and the table above was obtained from Bloomberg Finance, LP., Russell Investments and NAREIT. |

16

The CEO’s compensation, on a relative basis, has generally increased along with the Company’s performance.

The below chart presents a comparison of the CEO’s compensation and the Company’s total stockholder return for the five years ended December 31, 2013:

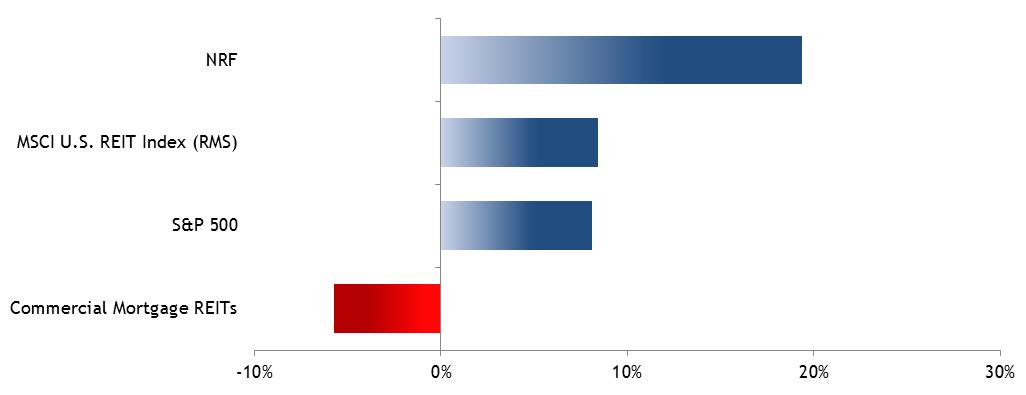

As of August 1, 2014, the Company’s compounded annual stockholder return since its initial public offering in 2004 was 19% per year, despite the severe economic recession and liquidity/credit crises which saw the failure of many of the Company’s competitors. The Compensation Committee believes that management’s strong performance last year and over the last several years has been a critical component of our success, both on an absolute basis and relative to similarly situated companies.

Compounded Annual Total Return(1)

October 2004 (IPO) through August 1, 2014

_______________

| (1) | Commercial mortgage REITs include Arbor Realty Trust, Inc., Newcastle Investment Corp., RAIT Financial Trust and iStar Financial Inc. |

17

Compensation Policies and Objectives