QuickLinks -- Click here to rapidly navigate through this document

As filed with the staff of the Securities and Exchange Commission on June 18, 2004

Registration Statement No. 333-112242

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Amendment No. 3 to

FORM F-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

GRUPO TMM, S.A.

(Exact name of registrant as specified in its charter)

TMM Group

(Translation of Registrant's name into English)

United Mexican States

(State or other jurisdiction of incorporation or organization)

4013

(Primary Standard Industrial Classification Code Number)

Not applicable

(I.R.S. Employer Identification Number)

Avenida de la Cúspide, No. 4755

Colonia Parques del Pedregal,

14010 Mexico, D.F.

(Address of principal executive offices)

CT Corporation System

111 Eighth Avenue

New York, New York 10011

(212) 894-8700

(Name, address, including zip code, and telephone number,

including area code, of agent for service of process)

THE SUBSIDIARY GUARANTORS LISTED ON SCHEDULE A HERETO

with copies to:

Thomas C. Janson, Jr.

Milbank, Tweed, Hadley & McCloy LLP

1 Chase Manhattan Plaza

New York, New York 10005

(212) 530-5921

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective and all other conditions to the exchange offer described in the accompanying prospectus and solicitation statement have been satisfied or waived.

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

SCHEDULE A

OTHER REGISTRANTS—SUBSIDIARY GUARANTORS

| Name of Registrant | State or Other Jurisdiction of Incorporation or Organization | IRS Employer Identification Number | ||

|---|---|---|---|---|

| TMM Holdings, S.A. de C.V. | United Mexican States | N/A | ||

| Operadora de Apoyo Logístico, S.A. de C.V | United Mexican States | N/A | ||

| Compañía Arrendadora TMM, S.A. de C.V. | United Mexican States | N/A | ||

| Transportes Marítimos México, S.A. | United Mexican States | N/A | ||

| División de Negocios Especializados, S.A. | United Mexican States | N/A | ||

| Inmobiliaria TMM, S.A. de C.V. | United Mexican States | N/A | ||

| Lacto Comercial Organizada, S.A. de C.V. | United Mexican States | N/A | ||

| Línea Mexicana TMM, S.A. de C.V. | United Mexican States | N/A | ||

| Naviera del Pacifico, S.A de C.V. | United Mexican States | N/A | ||

| Operadora Marítima TMM, S.A. de C.V. | United Mexican States | N/A | ||

| Operadora Portuaria de Tuxpan, S.A. de C.V. | United Mexican States | N/A | ||

| Personal Marítimo, S.A. de C.V. | United Mexican States | N/A | ||

| Servicios Administrativos de Transportación, S.A. de C.V. | United Mexican States | N/A | ||

| Servicios de Logística de México, S.A. de C.V. | United Mexican States | N/A | ||

| Servicios en Operaciones Logísticas, S.A. de C.V. | United Mexican States | N/A | ||

| Servicios en Puertos y Terminales, S.A. de C.V. | United Mexican States | N/A | ||

| Terminal Marítima de Tuxpan, S.A. de C.V. | United Mexican States | N/A | ||

| TMG Overseas S.A. | Republic of Panama | N/A | ||

| TMM Agencias, S.A. de C.V. | United Mexican States | N/A | ||

| TMM Logistics, S.A. de C.V. | United Mexican States | N/A | ||

| Transportación Portuaria Terrestre, S.A. de C.V. | United Mexican States | N/A |

The address, including zip code and area code, of each of the principal executive offices of the registrants listed above is Avenida de la Cúspide, No. 4755, Colonia Parques del Pedregal, 14010 Mexico, D.F. The name and address, including zip code, telephone number, and area code, of the above listed registrants' agent for service of process is CT Corporation System, 111 Eighth Avenue, New York, NY 10011, (212) 894-8700. I.R.S. Employer Identification Number is not applicable for the above listed registrants.

The information in this prospectus and solicitation statement is not complete and may be changed. We may not sell these securities until our registration statement filed with the Securities and Exchange Commission is effective. This prospectus and solicitation statement is not an offer to sell these securities and we are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

PROSPECTUS AND SOLICITATION STATEMENT

Offer to Exchange

For each $1,000 principal amount of outstanding 91/2% Notes due 2003 and 101/4% Senior Notes due 2006

of Grupo TMM, S.A., $1,000 principal amount of Senior Secured Notes due 2007 of Grupo TMM, S.A.

plus additional Senior Secured Notes due 2007 with a face amount equal to accrued and unpaid interest;

and

Solicitation of Consents to Amend the Indenture governing the 101/4% Senior Notes due 2006;

and

Solicitation of Acceptances to a U.S. Prepackaged Plan of Reorganization.

Grupo TMM, S.A., a Mexicansociedad anónima ("Grupo TMM" or the "Company"), proposes a financial restructuring through one of the following two alternatives:

- 1.

- an out-of-court restructuring, or "recapitalization plan," which consists of:

- •

- an offer to exchange all of our outstanding 91/2% Notes due 2003, which we refer to as the "2003 notes," and 101/4% Senior Notes due 2006, which we refer to as the "2006 notes," and together with the 2003 notes, the "existing notes," for newly issued Senior Secured Notes due 2007, which we refer to as the "new notes." The new notes will be guaranteed by our direct and indirect wholly owned subsidiaries (which we refer to as the "guarantors") and secured by a pledge of certain assets of the Company and the guarantors; and

- •

- a consent solicitation (which we refer to as the "consent solicitation") to remove substantially all the restrictive covenants and certain events of default in the indenture governing any of the 2006 notes that remain outstanding at the completion of the exchange offer,

or

- 2.

- an in-court restructuring through the solicitation of acceptances under Chapter 11 of the United States Bankruptcy Code (the "U.S. prepackaged plan") on substantially the same terms as the recapitalization plan. In the event that we do not receive sufficient acceptances to complete the U.S. prepackaged plan, we intend to pursue a prearranged plan under theLey de Concursos Mercantiles, or bankruptcy laws, of Mexico (the "prearrangedconcurso mercantil"). The recapitalization plan, the U.S. prepackaged plan and the prearrangedconcurso mercantil together are referred to herein as the "restructuring."We have entered into agreements with sufficient creditors pursuant to which they have agreed to consent to, and not oppose, the restructuring, which we believe should permit us to accomplish either the U.S. prepackaged plan, or, in the alternative, a prearrangedconcurso mercantil,on substantially the same terms as the recapitalization plan without having to secure the consent of any other holder of existing notes or other creditors, although we cannot assure you that that is the case.

Each holder whose 2003 notes or 2006 notes are validly tendered and accepted in the exchange offer will be issued new notes with a face amount equal to the face amount of the existing notes plus the dollar amount of accrued and unpaid interest on such existing notes to the settlement date at the rates set forth in this prospectus and solicitation statement. In addition, each holder whose consent is received by [ ], 2004 (the "consent deadline") will receive a pro rata portion of $21,094,605 principal amount of new notes (the "consent fee"). We have entered into voting agreements with holders of approximately 72% of the aggregate principal amount of the existing notes pursuant to which they have agreed to support the restructuring. Under existing interpretations of the Securities and Exchange Commission, ("SEC"), the execution of the voting agreements constituted private offerings of the securities to be issued in the exchange offer and, accordingly, such securities are not included in this registration statement. Consummation of the exchanges in both the private offering to holders who entered into the voting agreements (which we refer to as the "private exchange offer") and in the exchange offer under this registration statement (which we refer to as the "public exchange offer") will occur simultaneously. The new notes to be issued in the private exchange offer will be restricted securities under the Securities Act of 1933 and will contain a legend to that effect. We have agreed to register these securities under the Securities Act of 1933 as soon as practicable after the completion of the exchange offer. This prospectus and solicitation statement relates to the public exchange offer that we are making to the holders of the existing notes who did not execute voting agreements. We refer to the public exchange offer pursuant to this prospectus and solicitation statement and the private exchange offer pursuant to the voting agreements collectively as the "exchange offer."

The exchange offer will expire at 11:59 p.m., New York City time, on [ ], [ ], 2004, and the ballots for the U.S. prepackaged plan must be received by 11:59 p.m., New York City time, on [ ], [ ], 2004, unless extended by us. The exchange offer and the consent solicitation are conditioned, among other things, on the receipt of tenders of at least 98% of the aggregate principal amount of 2003 notes outstanding and 95% of the aggregate principal amount of 2006 notes outstanding. You may not withdraw any existing notes once they have been tendered, except under certain circumstances as set forth herein.

You should consider carefully the "Risk Factors" beginning on page 40 of this prospectus and solicitation statement before you make a decision as to whether to tender your existing notes and consent to the proposed amendment to the indenture governing the 2006 notes and how to vote on the U.S. prepackaged plan.

Neither the SEC nor any state securities commission has approved or disapproved these securities or passed upon the adequacy or accuracy of this prospectus and solicitation statement. Any representation to the contrary is a criminal offense.

The solicitation agent, information agent and voting agent for the exchange offer, consent solicitation and solicitation of acceptances is:

Innisfree M&A Incorporated

The date of this prospectus and solicitation statement is , 2004

The Following Statement Is Included At The Request Of The National Banking And Securities Commission (Comisión Nacional Bancaria Y De Valores) Of México For The Benefit Of Mexican Investors:

The Information Contained In This Prospectus And Solicitation Statement Is Exclusively The Responsibility Of Grupo TMM And Does Not Require Authorization By The Comisión Nacional Bancaria Y De Valores. The Registration With The Sección Especial (Special Section) Of The Registro Nacional De Valores Maintained By The Comisión Nacional Bancaria Y De Valores Does Not Imply A Certification Of The Investment Quality Of The Securities Or Our Solvency. The New Notes Have Not Been Registered With The Sección Especial (Special Section) Of The Registro Nacional De Valores And Therefore The Securities Are Not Subject To A Public Offering Or Intermediation In Mexico. The Acquisition Of The Securities By Any Investor Of Mexican Nationality Will Be Made Under Such Investor's Own Responsibility.

| | Page | |

|---|---|---|

| Summary | 1 | |

| Questions and Answers Relating To the Exchange Offer and Consent Solicitation | 33 | |

| Risk Factors | 39 | |

| Forward-Looking Information | 66 | |

| The Exchange Offer and Consent Solicitation | 67 | |

| The Proposed Amendment | 79 | |

| The U.S. Prepackaged Plan | 82 | |

| The Mexican Law of Commercial Reorganizations | 143 | |

| Financing For the Offer | 147 | |

| Presentation of Financial Information | 148 | |

| Capitalization | 149 | |

| Selected Consolidated Historical Financial Information | 150 | |

| Ratio of Earnings To Fixed Charges | 156 | |

| Unaudited Pro Forma Financial Data | 157 | |

| Operating and Financial Review and Prospects | 161 | |

| Quantitative and Qualitative Disclosures About Market Risks | 188 | |

| Exchange Rates and Exchange Controls | 190 | |

| The Company | 191 | |

| Management | 219 | |

| Major Shareholders and Related Party Transactions | 225 | |

| Legal Proceedings | 228 | |

| Description of Significant Indebtedness and Securitization Facility | 232 | |

| The Guarantors and the Security | 235 | |

| Description of the New Notes | 237 | |

| Comparison of Material Differences Among the 2003 Notes, the 2006 Notes and the New Notes | 282 | |

| Material United States Federal Income Tax Considerations | 300 | |

| Material Mexican Federal Income Tax Considerations | 312 | |

| Enforcement of Civil Liabilities Against Non-U.S. Persons | 314 | |

| Legal Matters | 315 | |

i

| Experts | 315 | |

| Where You Can Find More Information | 315 | |

| Index To Consolidated Financial Statements | F-1 | |

| Annex A Plan of Reorganization | A-1 | |

| Annex B Form of Supplemental Indenture For 101/4% Senior Notes Due 2006 | B-1 |

In connection with the exchange offer described herein, you should rely only on the information contained in this prospectus and solicitation statement or in any supplement accompanying this prospectus and solicitation statement. We have not authorized anyone to provide you with different information. We are not making an offer of these securities in any jurisdiction in which such an offer is not permitted. You should not assume that the information contained in this prospectus and solicitation statement or in any supplement accompanying this prospectus and solicitation statement is accurate as of any date other than the date on the front of this prospectus and solicitation statement.

ii

In this document, unless specified otherwise, "we," "us," "our," "Grupo TMM" and "the Company" refer to Grupo TMM, S.A. and its subsidiaries, and "you" refers to the holders of the existing notes.

References in this document to "$," "US$" or "dollars" are to United States dollars and references to "pesos" or "ps." are to Mexican pesos. This document contains translations of certain peso amounts into dollars at specified rates solely for the convenience of the reader. These translations should not be construed as representations that the peso amounts actually represent such dollar amounts or could be converted into dollars at the rates indicated or at any other rate.

The Company and the Guarantors

We offer an integrated regional network of rail and road transportation services, port management, specialized maritime operations and logistics. Our services include:

- •

- rail transport within Mexico and to and from the United States through our subsidiary, TFM, S.A. de C.V. (which we refer to as "TFM");

- •

- logistics operations, including dedicated contract trucking, and integrated logistics outsourcing services;

- •

- specialized maritime shipping, including chartering supply ships to serve offshore oil rigs, furnishing towing services for ships at the port of Manzanillo, and transporting automobiles, and refined petroleum and chemical products; and

- •

- port and terminal operations at the Mexican ports of Acapulco and Tuxpan.

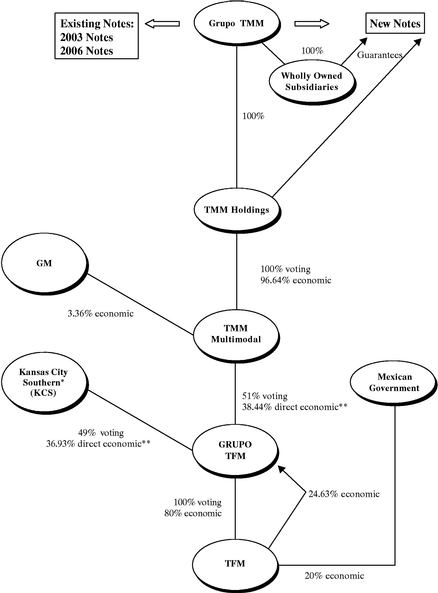

Our railroad operations are conducted through our indirect subsidiary, TFM. We hold our interest in TFM through TMM Holdings S.A. de C.V. ("TMM Holdings"), our 100% owned subsidiary which, in turn, owns an approximate 96.6% interest in TMM Multimodal, S.A. de C.V. ("TMM Multimodal"). TMM Multimodal, in turn, has a voting interest of 51% and a direct economic interest of 38.4% in Grupo Transportación Ferroviaria Mexicana, S.A. de C.V. (which we refer to as "Grupo TFM") and Grupo TFM holds an 80% direct economic interest in TFM. The remaining 20% economic interest in TFM is currently owned by the Mexican government. See "Summary—Corporate Structure."

We were formed on August 14, 1987 under the laws of Mexico as a variable capital corporation (sociedad anónima de capital variable) to serve as a holding company for investments by certain members of the Serrano Segovia family. On December 26, 2001, we completed a merger with our subsidiary, Transportación Marítima Mexicana, S.A. de C.V. ("TMM"), and we were the surviving entity. On September 13, 2002, we completed a reorganization that eliminated the variable portion of our capital stock and we became a fixed capital corporation. Consequently, our registered name changed from Grupo TMM, S.A. de C.V. to Grupo TMM, S.A.

Each of our wholly owned direct or indirect subsidiaries, including TMM Holdings, through which we hold our interest in TFM, Operadora de Apoyo Logístico, S.A. de C.V., Compañía Arrendadora TMM, S.A. de C.V., Transportes Marítimos México, S.A., División de Negocios Especializados, S.A., Inmobiliaria TMM, S.A. de C.V., Lacto Comercial Organizada, S.A. de C.V., Línea Mexicana TMM, S.A. de C.V., Naviera del Pacifico, S.A de C.V., Operadora Marítima TMM, S.A. de C.V., Operadora Portuaria de Tuxpan, S.A. de C.V., Personal Marítimo, S.A. de C.V., Servicios Administrativos de Transportación, S.A. de C.V., Servicios de Logística de México, S.A. de C.V., Servicios en Operaciones Logísticas, S.A. de C.V., Servicios en Puertos y Terminales, S.A. de C.V., Terminal Marítima de Tuxpan, S.A. de C.V., TMG Overseas S.A., TMM Agencias, S.A. de C.V., TMM Logistics, S.A. de C.V., and Transportación Portuaria Terrestre, S.A. de C.V. (collectively, the "guarantors"), will irrevocably and unconditionally guarantee our obligations under the new notes. In addition, in the event that any entity becomes a wholly owned subsidiary after the issuance of the new notes (including as a result of the purchase of additional shares by the Company or another wholly owned subsidiary), that entity will also be required to guarantee the new notes. Furthermore, we and the guarantors will also enter into security agreements, which we refer to collectively as the "security agreements," in connection with the issuance of the new notes.

1

The Company's obligations under the new notes and the security agreements, and the guarantors' obligations under the guarantee and security agreements, will be secured by a first priority security interest in (a) the shares of the stock of our subsidiaries held by the Company and the guarantors, including the shares of TMM Multimodal owned by TMM Holdings (the "MM Shares"), subject to certain restrictions in our existing joint venture arrangements as well as certain rights of holders of certificates issued by a trust pursuant to our receivables securitization facility (the "securitization facility"), and (b) all of the Company's and the guarantors' present and future tangible and intangible assets, subject to certain prior existing security arrangements, other specific carve-outs and release and substitution provisions to permit the Company and its subsidiaries to conduct their business in the ordinary course. See "The Guarantors and the Security" for more information concerning the foregoing.

The following diagram illustrates the basic corporate structure of Grupo TMM and its subsidiaries:

- *

- Through its wholly owned subsidiaries.

- **

- Without giving effect to the additional indirect interest created by the interest in Grupo TFM held by TFM.

2

Recent Results of Operations

On April 29, 2004, we announced our first quarter financial results for 2004. On a consolidated basis, we reported revenues from consolidated operations of $218.5 million for the first quarter of 2004 compared to revenues from consolidated operations of $219.2 million for the same period in 2003. We reported a net loss of $9.1 million or $0.16 per share in the first quarter of 2004 as compared with a net loss of $27.7 million, or $0.49 per share, for the same period in 2003. Operating profit for the first quarter of 2004 was $25.7 million, representing a decrease of $1.4 million from consolidated operating profit of $27.1 million reported for the same period in 2003.

Background of the Restructuring

At September 30, 2002, Grupo TMM had $235.6 million of short-term debt, which included $176.9 million of the 2003 notes, and $202.5 million of long-term debt, including $200.0 million of the 2006 notes. In addition, as of such date, there were approximately $21.7 million of outstanding certificates issued by the trust established under the securitization facility, which were payable in April 2003.

In light of the near term maturity of the 2003 notes, in early 2002, the Company, together with our financial advisors, began to evaluate various additional alternatives for strengthening our balance sheet, meeting our capital needs and refinancing or extending the maturity of our obligations. As part of this process, we considered sales of equity securities, sales of new debt securities, asset sales and various refinancing transactions. Given our liquidity profile and the advice of our financial advisors that the capital markets would not respond favorably to a new offering of high yield debt securities by us at that time, it was determined that issuing new debt securities was not feasible. We concluded that the market undervalued our equity in light of uncertainty concerning TFM's VAT claim and that sales of equity securities would therefore be prohibitively dilutive.

In addition to these measures, we implemented a number of short-term measures in an effort to address these liquidity concerns. Key elements of our strategy, which are more fully described in "The Company-Our Business Strategy," included:

- •

- Reducing our cost structure in late 2002 and throughout 2003; and

- •

- Continuing the effort, which began in 1997, to achieve the successful resolution of TFM's value added tax ("VAT") claim.

Previous Exchange Offers

In mid-2002, we determined, in consultation with our financial advisors, that the most feasible alternative was to extend the maturity of the 2003 notes through offers made to the holders of the 2003 notes and the 2006 notes of new debt securities with a later maturity and other modified terms, including a guarantee by TMM Holdings, a new holding company formed to indirectly hold our interest in Grupo TFM.

We commenced exchange offers on December 26, 2002 seeking to exchange all of the 2003 notes and the 2006 notes for a new issue of debt securities that would mature in 2010, bear interest at 101/2% and be guaranteed by TMM Holdings.

The exchange offers were not accepted by the required percentage of holders of the 2003 notes. Based on advice from our financial advisor, on February 18, 2003, we amended the exchange offers to add, as additional consideration, warrants to purchase ADRs of the Company, reduced the percentage of 2003 notes required to be tendered and extended the expiration date of the exchange offers.

During the period in which the exchange offers were pending, we were engaged in discussions and negotiations with other parties with respect to the sale of certain of our assets as well as certain other

3

investments by third parties in the Company or our subsidiaries. The purpose of these discussions was to provide us with alternative sources of liquidity to meet our obligations in the event that the exchange offers were unsuccessful. As a result of these negotiations, we entered into (i) an agreement with Stevedoring Services of America ("SSA") to sell our interest in the ports that were jointly owned by us and SSA (other than our ports in Acapulco and Tuxpan) to an affiliate of SSA for cash (the "Port Sale") and (ii) an agreement with Kansas City Southern (which we refer to as "KCS") to sell our interest in Grupo TFM to KCS for a combination of cash and stock of KCS and an additional earnout (the "TFM Sale"). Following the execution of the agreements for the Port Sale and the TFM Sale, on April 29, 2003, we again amended the exchange offers to eliminate the warrant component of the consideration offered in the exchange offers, shorten the maturity of the notes being offered to May 2004, increase the interest rate to 12% and amend the covenants to permit the TFM Sale to be completed. The Port Sale was completed on May 13, 2003.

The exchange offers were extended several times. Ultimately, however, insufficient 2003 notes were tendered to permit the conditions to the exchange offers to be satisfied and the exchange offers were terminated on May 15, 2003. We did not have the liquidity necessary to meet the principal and interest payments due on that date for the 2003 notes or the interest payments due on that date for the 2006 notes and we defaulted on those obligations. These defaults, in turn, created cross-defaults under certain of our other obligations. See "Summary—Consequences if the Restructuring Fails."

In August 2003, our stockholders voted to reject the Acquisition Agreement and we subsequently notified KCS that we were terminating the Acquisition Agreement based on the results of the stockholder vote. KCS has challenged our right to terminate the Acquisition Agreement and alleged certain breaches of the Acquisition Agreement by the Company. Pursuant to the Acquisition Agreement, the dispute was submitted to binding arbitration. In March 2004, the arbitration panel issued a ruling solely on the issue of the termination of the agreement by the Company based on the failure of the stockholders to approve the TFM Sale at the stockholder meeting held in August 2003. The panel ruled that the termination on this basis was not effective and that the Agreement remained in effect and binding on the parties unless otherwise terminated in accordance with its terms or by law. The parties have entered into a stipulation under which further arbitration proceedings have been deferred and each party reserved its rights to pursue further proceedings at any time. See "The Company—Legal Proceedings—The Dispute with Kansas City Southern."

Proposed Exchange Offer

Following the termination of the exchange offers, we retained Miller Buckfire Lewis Ying & Co., LLC ("MBLY") and Elek, Moreno-Valley Associados ("EMVA"), as financial advisors, to advise us on alternatives. As part of this process, we again contemplated sales of new debt securities and sales of equity securities. Given our liquidity profile and the advice of our financial advisors that the capital markets likely would not respond favorably to a new offering of high yield debt securities by us at that time, it was determined that issuing new debt securities was not feasible. We concluded that the market continued to undervalue our equity at the time in light of uncertainty concerning TFM's VAT claim and that sales of equity securities would therefore be prohibitively dilutive. As a result, we elected to attempt to restructure the outstanding 2003 notes and 2006 notes either through a revised exchange offer or a prepackaged or prearranged bankruptcy proceeding in the United States or Mexico. As part of this process, we and our advisors encouraged the formation of an ad hoc committee of holders of the existing notes, which we refer to as the "Committee," and agreed to pay the fees and expenses of the legal advisors and a financial advisor to the Committee. The Committee subsequently retained Houlihan Lokey Howard & Zukin Capital as financial advisor, Akin Gump Strauss Hauer & Feld LLP as U.S. legal advisor, and Franck, Galicia y Robles, S.C. as Mexican legal advisor. During the period from July 2003 to December 2003, we engaged in extensive negotiations with the advisors to the Committee and certain members of the Committee regarding the terms of the restructuring. As a result

4

of these discussions, members of the Committee holding approximately 72% of the aggregate principal amount of existing notes have entered into voting agreements (as amended through the date hereof, the "voting agreements") pursuant to which they have agreed to tender their existing notes in the exchange offer, consent to the amendment (if they are holders of 2006 notes) and vote to accept, and not to oppose, the U.S. prepackaged plan or the prearrangedconcurso mercantil. The voting agreements originally provided that such holders could terminate the voting agreements at any time after March 31, 2004. As of March 31, 2004, Grupo TMM entered into amended voting agreements that extended the termination date and made certain other changes.

The new termination date of the voting agreements is July 22, 2004 (or, in connection with an extension of the exchange offers, such date will be August 5, 2004). However, if we have commenced the U.S. prepackaged plan or prearrangedconcurso mercantil prior to such termination date, the termination date will be September 30, 2004. For a more detailed description of the terms of the voting agreements and the termination provisions, see "The Company—Recent Developments—Negotiations with Ad Hoc Committee of Holders of Existing Notes; Voting Agreements."

Under the U.S. Bankruptcy Code, the affirmative votes by holders of at least 662/3% in principal amount and more than one-half in number of those holders of existing notes voting on the U.S. prepackaged plan are required for confirmation of the U.S. prepackaged plan. Similarly, confirmation of a prearrangedconcurso mercantilplan would require (i) the approval of creditors, recognized by the Mexican court as holders of our unsecured debt, holding a majority of the aggregate amount of outstanding unsecured indebtedness recognized by the court (not just the holders of our existing notes) and (ii) that more than one-half in number of our recognized creditors do not vote against the plan. We have entered into voting agreements with sufficient holders of the existing notes that we believe that, if the conditions to the exchange offer are not satisfied, we should have sufficient acceptances to permit us to complete the restructuring either through the U.S. prepackaged plan or, if we determine to pursue a prearrangedconcurso mercantil,through a prearrangedconcurso mercantil,in each case without requiring the approval of any other holders of the existing notes or any of our other creditors. However, since we are not able to determine with certainty how many holders of our existing notes, by number, would vote on the U.S. prepackaged plan, or if we determine to pursue aconcurso mercantil proceeding, would be recognized as creditors or vote in a prearrangedconcurso mercantil, we cannot assure you that the vote of the holders subject to the voting agreements would be sufficient to confirm the U.S. prepackaged plan or to complete a prearrangedconcurso mercantil.

The restructuring will extend the maturity of the 2003 notes and the 2006 notes and significantly reduce the cash interest payments that the Company is required to make. We believe this will allow us to meet these obligations as they mature through refinancings, asset sales or otherwise.

Restructuring Plan

We propose to effect the restructuring through one of the following two alternatives:

- 1.

- a recapitalization plan which consists of:

- •

- an offer to exchange all of our outstanding 2003 notes and 2006 notes for new notes that will be guaranteed by our direct and indirect wholly owned subsidiaries and secured by a pledge of certain assets of the Company and the guarantors; and

- •

- a consent solicitation to remove substantially all the restrictive covenants and certain events of default in the indenture governing the 2006 notes that remain outstanding at the completion of the exchange offer,

5

or

- 2.

- the U.S. prepackaged plan, which would accomplish the restructuring on substantially the same terms as the recapitalization plan, through the solicitation of acceptances under Chapter 11 of the United States Bankruptcy Code. In the event that we do not receive sufficient acceptances to complete the U.S. prepackaged plan, we intend to pursue a prearrangedconcurso mercantilin Mexico.We have entered into voting agreements with sufficient creditors pursuant to which they have agreed to consent to, and not oppose, the restructuring, which we believe should permit us to accomplish either the U.S. prepackaged plan, or a prearrangedconcurso mercantilon substantially the same terms as the recapitalization plan without having to secure the consent of any other holders of existing notes or other creditors, but subject to satisfying all other conditions and requirements for court approval of the U.S. prepackaged plan or prearrangedconcurso mercantil,as applicable.

The principal objectives of the restructuring described in this prospectus and solicitation statement are to reduce our mandatory cash interest payments and extend the maturity dates of the existing notes.

Each holder whose 2003 notes or 2006 notes are validly tendered and accepted in the exchange offer will be issued new notes with a face amount equal to the face amount of the existing notes plus the dollar amount of accrued and unpaid interest on such existing notes to the settlement date at the rates set forth in this prospectus and solicitation statement. In addition, each holder whose consent is received by [ ], 2004 will receive the consent fee. The exchange offer will expire at 11:59 p.m., New York City time, on [ ], [ ], 2004, unless extended by us. The exchange offer and the consent solicitation are conditioned, among other things, on the receipt of tenders of at least 98% of the aggregate principal amount of 2003 notes outstanding and 95% of the aggregate principal amount of 2006 notes outstanding. You may not withdraw tenders of any existing notes once they have been tendered, except for circumstances in which we make a material amendment to the exchange offer or waive a material condition thereto or except as permitted by the voting agreements in the case of holders of existing notes who have entered into such voting agreements. See "The Exchange Offer and Consent Solicitation—No Withdrawal Rights."

Your decision to participate in the exchange offer is completely independent of your decision to vote to accept or reject the U.S. prepackaged plan. Your acceptance of the exchange offer will not constitute acceptance or rejection of the U.S. prepackaged plan and a vote in favor of the U.S. prepackaged plan will not be deemed an acceptance of the exchange offer. We will not commence a Chapter 11 case and seek confirmation of the U.S. prepackaged plan or commence a prearrangedconcurso mercantilif all of the conditions to the exchange offer are met or waived by us. If all of the conditions to the exchange offer are not met or waived by us, principally the minimum tender condition that holders of 98% in aggregate principal amount of the 2003 notes outstanding and holders of 95% in aggregate principal amount of the 2006 notes outstanding participate in the exchange offer, but all of the conditions to the U.S. prepackaged plan are met, including the condition that we receive accepting votes from the requisite principal amount and requisite number of holders of existing notes to constitute an "accepting class" (as such term is defined in the U.S. Bankruptcy Code) and the voting agreements have not been terminated, we will be obligated under the voting agreements to commence either the U.S. prepackaged plan or the prearrangedconcurso mercantil.The determination of whether to file the U.S. prepackaged plan or the prearrangedconcurso mercantilwill be made solely by us, after consultation with the Committee.

Because the U.S. prepackaged plan can be confirmed by a U.S. bankruptcy court if we receive the affirmative votes of 662/3% in principal amount and more than one-half in number of those holders of existing notes voting, we may be able to consummate the U.S. prepackaged plan with significantly less support than that required in order to consummate the exchange offer. Similarly, confirmation of a

6

prearrangedconcurso mercantilplan requires (i) the approval of creditors, recognized by the Mexican court as holders of our unsecured debt, holding a majority of the aggregate amount of outstanding unsecured indebtedness recognized by the court and (ii) that more than one-half in number of creditors, recognized by the Mexican court as holders of our unsecured debt, holding our outstanding unsecured indebtedness recognized by the court do not veto the plan. Accordingly, we may be able to consummate a prearrangedconcurso mercantilwith significantly less support than would be required to effect either the exchange offer or the U.S. prepackaged plan.

The existing notes constitute the only claims considered to be impaired in a Chapter 11 case. Therefore, only the holders of existing notes are entitled to vote to accept or reject the U.S. prepackaged plan. Under the U.S. prepackaged plan, the holders of our existing notes will receive the same consideration in exchange for their claims as they could receive by participating in the exchange offer except that, in the U.S prepackaged plan, the consent fee will be prorated among all of the holders of existing notes, whether or not such holders voted to accept the U.S. prepackaged plan, whereas in the exchange offer the consent fee will be prorated only among the holders of existing notes who have entered into voting agreements or tendered their existing notes prior to the consent deadline, unless otherwise required by law.

Chapter 11

Chapter 11 is the principal reorganization chapter of the U.S. Bankruptcy Code. In a Chapter 11 case, the debtor is allowed to remain in possession of its business and assets as it works out its financial difficulties and attempts to reorganize its business for the benefit of all of its constituencies. The principal objective of Chapter 11 is to formulate, confirm, and consummate a plan of reorganization, which is the operative document containing the terms of the reorganization. In a typical Chapter 11 case, the plan of reorganization is negotiated with the company's constituencies after the commencement of the case, and the solicitation of acceptances to the plan is then undertaken pursuant to a disclosure statement approved by the U.S. bankruptcy court as containing adequate information within the meaning of Section 1125(a) of the U.S. Bankruptcy Code. In a prepackaged Chapter 11 case, on the other hand, the negotiation, solicitation, and voting on the plan are completed prior to the filing, so that by the time the filing occurs, the company already has the requisite acceptances in hand to confirm its plan of reorganization, subject to meeting the various confirmation standards and obtaining the U.S. bankruptcy court's approval. Because the voting on the plan occurs prior to the filing, a prepackaged Chapter 11 case is normally considerably shorter in duration than a typical reorganization case. Moreover, in a prepackaged Chapter 11 case—such as that which we may commence—all creditors (other than the holders of existing notes), as well as our shareholders, would be unaffected by the filing of the case. For a more detailed discussion of the Chapter 11 process in general, and prepackaged bankruptcies in particular, see "The U.S. Prepackaged Plan."

Concurso Mercantil

Aconcurso mercantilis the primary form of reorganization under the MexicanLey de Concursos Mercantiles(Law of Commercial Reorganizations), which we refer to as the "LCR." The LCR provides for two different proceedings: conciliation (conciliación) and bankruptcy/liquidation (quiebra). The LCR was enacted in May 2000 and is largely untested, especially for large, complex proceedings such as those involving a company like Grupo TMM, and in the context of prepackaged proceedings, for which precedents do not exist. In conciliation, the goal is for the debtor and its recognized creditors to engage in negotiations to reach an agreement settling the terms of the reorganization. If an agreement is reached and it is approved by a judge, the proceeding is terminated. Any agreement among the creditors in the conciliation phase requires (i) the approval of creditors, recognized by the Mexican court as holders of our unsecured debt, holding a majority of the aggregate amount of our outstanding unsecured indebtedness recognized by the court and (ii) that more than one-half in number of

7

creditors, recognized by the Mexican court as holders of our unsecured debt, holding our outstanding unsecured indebtedness recognized by the court do not veto the agreement. If we initiated the prearrangedconcurso mercantil,we would present a restructuring agreement on substantially the same terms as the U.S. prepackaged plan. For a more complete discussion of the prearrangedconcurso mercantil,see "The Mexican Law of Commercial Reorganizations."

Advantages of the restructuring

We believe that the advantages of the restructuring to us and to you are:

- •

- improving our ability to continue operating as a going concern by extending the maturity of the 2003 notes and 2006 notes and thereby curing the payment default under the 2003 notes and cross-defaults under certain other obligations (see "Contractual Obligations"), and achieving the other objectives outlined below;

- •

- avoiding the risk of an involuntaryconcurso mercantil,the outcome of which is uncertain;

- •

- lowering our mandatory cash interest payment obligations to more closely align our debt service obligations with our current and projected cash flows;

- •

- allowing us sufficient time to resolve completely TFM's existing claims for a refund of certain VAT taxes; and

- •

- extending the scheduled maturity dates of the 2003 notes and the 2006 notes to provide us with additional time to improve our operations following the negative effects of the weak global economic conditions and the devaluation of the Mexican peso that we have experienced in the past several years.

All of the above benefits decrease the likelihood that we will default on future interest and principal payments on our indebtedness and increase the likelihood that we will be able to make timely payments of interest on the new notes and repay or refinance the new notes at maturity.

Additionally, we believe that if we are subject to an involuntaryconcurso mercantilthat is not conducted pursuant to the restructuring, there is an increased risk that you will receive significantly less consideration for your existing notes than you will receive if the restructuring is successfully completed as set forth herein. In an involuntaryconcurso mercantil,in contrast to a prearranged one entered into as a part of the restructuring, the parties to the voting agreements would not be bound to accept a proposal and therefore there can be no guarantee that we will reach agreement with our creditors and successfully emerge from the conciliation phase of theconcurso mercantil(or, in the event that such agreement is reached, that it will be approved by the requisite number of creditors and creditors holding the requisite amount of unsecured obligations), exposing us to a potential liquidation and sale of our assets as a result. We expect that the proceeds from any such liquidation would be less than what could be obtained in a sale outside of liquidation, resulting in a net recovery to you that is projected to be substantially less than you would receive under the restructuring. In addition, the LCR is largely untested and legal precedent guiding its interpretation is limited, particularly in an involuntary proceeding. The uncertainty inherent in proceedings under a law with limited precedent may lead to extended litigation. In the case of large, complex proceedings, its potential impact on the rights of creditors is impossible to predict with complete certainty. Finally, if we are declared subject to a reorganization under the LCR, and upon the filing of your claim against our estate and the court's recognition of your status as creditor of us, your claim would be unsecured and ranked with equal right to payment with all other unsecured claims filed against our estate.

8

The primary advantages to us and to you of consummating the restructuring through the exchange offer instead of the U.S. prepackaged plan or the prearrangedconcurso mercantilare that the successful consummation of the exchange offer:

- •

- will allow us to continue operating our business without the negative perception of a U.S. bankruptcy or a Mexicanconcurso mercantil;

- •

- can be completed in less time than, and without the additional expense of, a U.S. bankruptcy or a Mexicanconcurso mercantil,which could negatively impact our business;

- •

- significantly reduces the risk of legal action being brought against us in a Mexican court for payment of the existing notes; and

- •

- avoids the uncertainties, delays and litigation risks associated with a U.S. bankruptcy or a Mexicanconcurso mercantil.

In the event that the restructuring cannot be consummated through the exchange offer, and the conditions to the U.S. prepackaged plan are satisfied, then the primary advantages of consummating the restructuring through the U.S. prepackaged plan would be that the successful consummation of the U.S. prepackaged plan:

- •

- would allow us to complete the restructuring with the affirmative votes of 662/3% in principal amount and more than one-half in number of those holders of existing notes voting on the plan, rather than having to obtain the 98% acceptance level required for the 2003 notes and the 95% acceptance level required for the 2006 notes in the exchange offer;

- •

- would extinguish all of our obligations and liabilities with regard to all of our existing notes, including any obligations or liabilities to holders of existing notes who do not vote in favor of the U.S. prepackaged plan, which will provide us with additional liquidity; and

- •

- would enable you to avoid the uncertainty concerning whether we can emerge in a timely manner or successfully from aconcurso mercantil.

In the event that the restructuring cannot be consummated through either the exchange offer or the U.S. prepackaged plan, we believe that we will nevertheless be able to consummate the restructuring through a prearrangedconcurso mercantilas we have entered into voting agreements with holders of existing notes holding a majority of the aggregate amount of our outstanding unsecured indebtedness, pursuant to which they have agreed to consent to, and not oppose, the restructuring.

Adverse effects of the restructuring on holders of existing notes

If the exchange offer is successful, you will receive new notes which will mature in 2007 (or 2008 in the event we extend the term of the new notes), significantly later than the 2003 notes and approximately one year later than the 2006 notes (or two years later than the 2006 notes in the event we extend the term of the new notes). Electing to receive the new notes involves risks and, after the restructuring, you may still receive less than the full principal amount of the new notes.

If the exchange offer is successful, we intend to repay any untendered 2003 notes at par value, plus accrued and unpaid interest. Following a successful exchange offer, the covenants in the indenture governing the new notes will be substantially similar to those of the 2006 notes except that the covenants governing debt incurrence, dividends, and asset sales will generally be more restrictive than those in the indenture governing the 2006 notes and generally require that we repay new notes with net proceeds from additional sources, if received by the Company, such as TFM's VAT claim. For a more detailed comparison of the covenants of the existing notes and the covenants of the new notes, see "Comparison of Material Differences Among the 2003 Notes, the 2006 Notes and the New Notes."

9

If you hold 2006 notes and do not participate in the exchange offer and it is successful, you will retain your 2006 notes, but there may be a substantially smaller market for the remaining 2006 notes, which will negatively impact the liquidity of those 2006 notes.Furthermore, any 2006 notes that remain outstanding following the exchange offer will be effectively and structurally subordinated to the new notes.In addition, the proposed amendment will remove substantially all of the restrictive covenants and certain events of default contained in the indenture currently governing the 2006 notes.

Your votes and elections related to the exchange offer and the U.S. prepackaged plan are not tied together. You are being asked to separately consider and indicate your acceptance or rejection of the exchange offer and the U.S. prepackaged plan. You are not required to accept or reject both the exchange offer and the U.S. prepackaged plan; rather, you may vote for or against each such alternative as you deem appropriate. If you tender into the exchange offer prior to the consent deadline, you will receive the consent fee.

Consequences if the restructuring fails

Our 2003 notes matured on May 15, 2003, and we did not have the liquidity to meet the principal and interest payments due on that date on the 2003 notes, or the interest payments due on that date on the 2006 notes. As a result, we defaulted on those obligations. These defaults, in turn, created cross-defaults under certain of our other obligations. Accordingly, the trustee or the holders of at least 25% of the principal amount of the 2006 notes has or have, as the case may be, the right to accelerate the 2006 notes, thereby requiring the immediate repayment of their entire principal amount. We do not have sufficient liquidity to pay the amounts that have become due on the 2003 notes, to pay the accrued and unpaid interest on the 2003 notes or the 2006 notes or, if the 2006 notes were accelerated, to repay the principal amount of the 2006 notes.

There can be no assurance that holders of the existing notes or other creditors will not attempt to institute legal proceedings to seek repayment of amounts owed to them. In addition, one or more of our creditors may seek to institute against us an involuntary U.S. bankruptcy proceeding or an involuntaryconcurso mercantilproceeding in Mexico. Additionally, we may choose to institute a voluntary non-prepackaged reorganization proceeding under Mexican or U.S. law.

In an involuntary Mexican reorganization proceeding, if (i) we are unable to reach an agreement with the creditors, recognized by the Mexican court as holders of our unsecured debt, holding a majority of the aggregate amount of our outstanding unsecured indebtedness recognized by the court or (ii) more than one-half in number of creditors, recognized by the Mexican court as holders of our unsecured debt, holding our outstanding unsecured indebtedness recognized by the court veto such agreement, during the conciliation phase of aconcurso mercantilproceeding, we could be forced to enter the bankruptcy, orquiebra,phase of a Mexican proceeding and could be subject to liquidation or be forced to sell all or substantially all of our assets.

See "The Mexican Law of Commercial Reorganizations" for a further description of a Mexican reorganization proceeding. We expect that the proceeds from any potential liquidation and sale of our assets as a result of aquiebrawould be less than what could be obtained in a sale outside of liquidation, would not be sufficient to satisfy all of our obligations to you, and would result in a net recovery to you that is projected to be substantially less than you would receive under the restructuring. See "Risk Factors—Factors relating to the restructuring."

10

The Exchange Offer and Consent Solicitation

| Securities For Which We Are Making the Exchange Offer | We are making an exchange offer for the full principal amount outstanding of both our 2003 notes and 2006 notes. | |||

New Tender Required | This prospectus and solicitation statement includes a new exchange offer and a U.S. prepackaged bankruptcy plan solicitation. Our last set of exchange offers, which were made pursuant to a prospectus dated April 29, 2003, have been terminated and all tendered existing notes have been returned to their original holders. Even if you participated in our last set of exchange offers, if you would like to participate in the new exchange offer or vote on the U.S. prepackaged plan, you must complete and mail the relevant transmittal documents and bankruptcy ballots enclosed with this prospectus and solicitation statement. | |||

Consideration Offered in the Exchange Offer | Principal Amount: $1,000 principal amount of new notes maturing in 2007 for each $1,000 principal amount of existing notes properly tendered and accepted in the exchange offer. | |||

Accrued Interest: All accrued and unpaid interest on the existing notes tendered and accepted in the exchange offer (including interest on the 2003 notes for the period from and after May 15, 2003) will be payable through the issuance of new notes with a principal amount equal to such accrued and unpaid interest to, but not including, the settlement date, provided, that (i) the interest accrual rate on the existing notes for this purpose shall be (A) 91/2% for the 2003 notes and 101/4% for the 2006 notes for the period through May 14, 2003 and (B) 11.50% for the period from and after May 15, 2003; and (ii) there shall be no interest paid on accrued interest. | ||||

With an assumed settlement date of July 21, 2004, (i) for every $1,000 principal amount of 2003 notes tendered and accepted in the exchange offer, tendering holders would receive $185.6 principal amount of new notes in payment of accrued interest and (ii) for every $1,000 principal amount of 2006 notes tendered and accepted in the exchange offer, tendering holders would receive $189.4 principal amount of new notes in payment of accrued interest. For a more detailed description of how accrued interest will be calculated, see "The Exchange Offer and Consent Solicitation—General." | ||||

11

Consent Fee: In addition, we will issue to each holder of existing notes that tenders its existing notes by the consent deadline ( , 2004), the consent fee, which is equal to a pro rata portion (calculated on the basis of the claim amount of each holder of existing notes) of $21,094,605 principal amount of new notes (which represents, in the aggregate, 5% of the sum of the principal amount of the existing notes plus respective accrued interest to December 24, 2003). Since only holders who tender existing notes prior to the consent deadline will be eligible to receive the consent fee, if less than all of the existing notes are tendered prior to the consent deadline, the eligible holders of existing notes will receive a larger consent fee. | ||||

If holders of at least 98% in aggregate outstanding principal amount of the 2003 notes and 95% in aggregate outstanding principal amount of the 2006 notes tender prior to the consent deadline, (i) for every $1,000 principal amount of 2003 notes tendered, tendering holders will receive $57 principal amount of new notes in payment of the consent fee and (ii) for every $1,000 principal amount of 2006 notes tendered, tendering holders will receive $59 principal amount of new notes in payment of the consent fee. | ||||

We may elect to extend the consent deadline in our sole discretion. The new notes to be issued in payment of the consent fee, which we refer to as the "additional new notes," will be issued on the settlement date of the exchange offer. Following the successful consummation of the restructuring, the additional new notes issued therein shall have identical terms to the new notes. For a more detailed description of the additional new notes, see "The Exchange Offer and Consent Solicitation—General," "Summary—The Exchange Offer and Consent Solicitation—Voting Agreements," and "The U.S. Prepackaged Plan." | ||||

12

The following is a summary comparison of the material economic terms of the 2003 notes, the 2006 notes and the new notes. For a more detailed comparison of the existing notes with the new notes, see "Comparison of Material Differences Among the 2003 Notes, the 2006 Notes and the New Notes."

| | 2003 Notes | 2006 Notes | | |||

|---|---|---|---|---|---|---|

| | CUSIP Number: 893868AA7 ISIN Number: US893868AA72 | CUSIP Number: 893868AC3 ISIN Number: US893868AC39 | New Notes | |||

| Principal Amount Outstanding (Aggregate) | $176,875,000 | $200,000,000 | New notes will be issued in payment of up to $376,875,000 plus (i) accrued and unpaid interest on the existing notes at the respective interest rate set forth in this prospectus through the settlement date, (ii) the consent fee in the amount of $21,094,605, (iii) new notes in payment in full of the $6.5 million payable owing to Promotora Servia, (iv), if applicable, the delay fee (as set forth below and in "The Exchange Offer and Consent Solicitation—The Voting Agreements"), and (v) at our election and to the extent permitted by the new notes indenture, interest on the new notes. | |||

| Interest Rate | 91/2% | 101/4% | 101/2–13% (as set forth in "The Exchange Offer and Consent Solicitation—The New Notes") | |||

| Payment Frequency | May 15 and November 15 of each year | May 15 and November 15 of each year | Semi-annually on and for the first three years from the settlement date. If we elect to extend the maturity of the new notes, quarterly in advance during the extension term commencing on the third anniversary of the settlement date. | |||

| Maturity | May 15, 2003 | November 15, 2006 | The third anniversary of the settlement date, or the fourth anniversary of the settlement date if we elect to extend the maturity. | |||

| Guarantees | None. | None. | The guarantors, our wholly owned direct or indirect subsidiaries, will irrevocably and unconditionally guarantee on a senior secured basis all of our obligations under the new notes indenture, the new notes and the Collateral Documents, including the payment of principal and premium, if any, interest and additional amounts, if any, on the new notes in full, as and when due, regardless of any defense, right of set-off or counterclaim that we may have or assert, except to the extent paid by us. See "The Guarantors and Security" for a more detailed description of the guarantors and the Collateral Documents. | |||

13

| Security and Collateral | Not applicable. | Not applicable. | Our obligations under the new notes and the Collateral Documents and the obligations of the guarantors under the guarantees, as applicable, will be secured by a first priority security interest in (i) all of the shares of the stock of our subsidiaries which we or the guarantors directly hold, including the MM Shares held by TMM Holdings, subject to certain restrictions in our existing joint venture arrangements and to certain rights of holders of certificates issued by a trust pursuant to the securitization facility, and (ii) all of our and the guarantors' present and future tangible and intangible assets, subject to certain prior existing security arrangements and appropriate and customary carve-outs and release and substitution provisions to permit us and our subsidiaries to conduct business in the ordinary course. |

14

| Consent Solicitation | Concurrently with the exchange offer, we are soliciting consents to the proposed amendment to the indenture governing the 2006 notes from holders of the 2006 notes. For a complete description of the proposed amendment, see "The Proposed Amendment."Holders of the 2006 notes who tender their 2006 notes in the exchange offer will be deemed to have given their consent to the proposed amendment by so tendering.The indenture governing the 2006 notes provides that consents from holders of a majority in aggregate principal amount of the 2006 notes outstanding must be received in order to amend such indenture. However, the consent solicitation is subject to additional conditions as described in detail under "The Exchange Offer and Consent Solicitation—Conditions to the Exchange Offer." | |||

Expiration Date | The exchange offer will expire at 11:59 p.m., New York City time, on , 2004, unless extended by us in our sole discretion. We will announce any extension of the expiration date no later than 9:00 a.m., New York City time, on the business day following the previously scheduled expiration date. | |||

Settlement Date | The new notes, including the new notes issuable in payment of the accrued and unpaid interest to the settlement date and the additional new notes issued in payment of the consent fee, will be issued on the settlement date, which will be the third business day after the expiration date, or as soon thereafter as practicable. | |||

Voting Agreements | As of May 7, 2004, noteholders representing approximately 71% of the outstanding principal amount of the 2003 notes and approximately 72% of the outstanding principal amount of the 2006 notes (or approximately 72% of the aggregate outstanding principal amount of the existing notes) have entered into voting agreements pursuant to which they have agreed to tender their existing notes in the exchange offer and consent to the proposed amendment (if they are holders of 2006 notes) and to vote in favor of, and not oppose, the U.S. prepackaged plan or, in the alternative, the prearrangedconcurso mercantil,in the event the Company determines to commence a prearranged bankruptcy proceeding in Mexico. Pursuant to the voting agreements, we have agreed to use commercially reasonable efforts to have the registration statement declared effective by the SEC as promptly as practicable and commence the exchange offer, the consent solicitation and, if the exchange offer is not successful, either a U.S. prepackaged plan or a prearrangedconcurso mercantil,as we determine in our sole discretion. As a result of the level of participation by holders of existing notes in the voting agreements referred to above, we believe that, if the conditions to the exchange offer are not satisfied, we should have sufficient acceptances to permit us to complete the restructuring either through the U.S. prepackaged plan or, if we determine to pursue a prearrangedconcurso mercantil,through a prearrangedconcurso mercantil,in each case without requiring the approval of any other holders of the existing notes or any of our other creditors. However, since we are not able to determine with certainty how many, by number, of holders of our existing notes would vote on the U.S. prepackaged plan if we do not complete the exchange offer and we pursue the U.S. prepackaged plan, or if we determine to pursue aconcurso mercantil proceeding, would be recognized as creditors or vote in a prearranged concurso mercantil, we cannot assure you that the vote of the holders subject to the voting agreements would be sufficient to confirm the U.S. prepackaged plan or to complete a prearrangedconcurso mercantil. | |||

15

If all of the conditions to the exchange offer have not been sooner satisfied and/or waived, but sufficient consents are received from the requisite number of holders and principal amount of existing notes to constitute an "accepting class" under the U.S. Bankruptcy Code, then within 30 business days following the commencement of the exchange offer or five business days following the expiration of the exchange offer, whichever is later, the voting agreements require us to commence the U.S. prepackaged plan or, in the alternative, the prearrangedconcurso mercantil;provided, that if we are using commercially reasonable efforts to commence the prearrangedconcurso mercantil,the voting agreements provide that we shall have an additional 30 business days in order to commence the prearrangedconcurso mercantil. | ||||

Furthermore, the voting agreements required us, upon receipt of voting agreements executed by holders of at least 51% in aggregate principal amount of the existing notes, to deposit into escrow an aggregate amount of additional new notes to be issued in payment of the consent fee equal to $21,094,605, which will begin to accrue interest as of the date such additional new notes are released from escrow and distributed to the holders, as described below. The additional new notes together with the related indenture and security agreement were deposited into escrow as of January 13, 2004. The voting agreements provide that the additional new notes are to be released from escrow and distributed as follows: | ||||

• | if the exchange offer is consummated, the additional new notes will be distributed, on the settlement date, pro rata to the holders of existing notes who executed voting agreements or irrevocably consented to the restructuring of the existing notes prior to the consent deadline, or, if required by applicable law, distributed pro rata to all exchanging holders of existing notes; | |||

• | if the restructuring is completed through either the U.S. prepackaged plan or the prearrangedconcurso mercantil,the additional new notes will be distributed pro rata to all of the holders of the existing notes; | |||

• | in the event that (i) holders representing the greater of (x) 51% of the existing notes and (y) in the event the Company elects to commence the U.S. prepackaged plan, the requisite number of holders and principal amount of existing notes to constitute an "accepting class" under the U.S. Bankruptcy Code have entered into voting agreements and are not in default under such voting agreements, and, if we are unsuccessful in completing the restructuring prior to September 30, 2004 (the "outside date"), then, on the outside date, the additional new notes shall be released from escrow and distributed pro rata to the holders of existing notes who are then subject to voting agreements and not in default thereunder, subject to certain exceptions as described in the voting agreements; and | |||

16

• | in the event that (i) holders representing at least 51% of the existing notes have entered into voting agreements and are not in default under the voting agreements, and (ii) we default under the voting agreements (and we fail to cure such default prior to the outside date) and (iii) the restructuring has not been consummated prior to the outside date, then, on the outside date, the additional new notes shall be released from escrow and distributed pro rata to the holders of existing notes who are then subject to voting agreements, subject to certain exceptions as described in the voting agreements. | |||

The voting agreements may be terminated at any time prior to the settlement date (x) in their entirety, by holders who have entered into voting agreements and hold at least 51% in aggregate principal amount of the existing notes held by all holders who have entered into voting agreements, and (y) by each holder of existing notes who has signed a voting agreement as to itself only: (i) if we default under the voting agreements, (ii) after July 22, 2004, provided that we may extend this date to a date not later than August 5, 2004 in connection with an extension of the exchange offer (provided that if we have commenced the U.S. prepackaged plan or prearrangedconcurso mercantilby July 22, 2004, or August 5, 2004, as applicable, such date shall be September 30, 2004), (iii) if an order is entered that has the practical effect of preventing or delaying confirmation of the U.S. prepackaged plan, and such order is not stayed, reserved or vacated before the earlier of 30 days thereafter or September 30, 2004, (iv) if the U.S. bankruptcy court denies confirmation of the U.S. prepackaged plan and we fail to file a new or amended plan meeting the requirements of the voting agreements before the earlier of 30 days thereafter or September 30, 2004, (v) if the U.S. prepackaged plan is converted to a case under Chapter 7 or a liquidating Chapter 11 case under the U.S. Bankruptcy Code or a bankruptcy liquidation proceeding under Mexican law, (vi) if there is issued or reinstated anymedida cautelar,suspension order or similar order by a court or other governmental body of competent jurisdiction that affects or could affect our obligations with respect to the existing notes or the voting agreements and (A) such proceeding or order is issued or reinstated at the request or with the acquiescence of us or (B) in all other circumstances, if such order is not stayed, reversed or vacated before the earlier of 30 days thereafter or September 30, 2004, or (vii) if we pay any sum on account of any judgment granted in favor of any holder of existing notes or enter into any settlement thereof without the consent of the holders of at least 51% in aggregate principal amount of existing | ||||

| notes held by all holders who have entered into voting agreements. | ||||

17

The voting agreements may be terminated by us at any time prior to the settlement date after July 22, 2004 (or August 5, 2004 if the exchange offer is extended through such date), if we have not defaulted upon or breached certain covenants under the voting agreements. However, if, we have commenced the U.S. prepackaged plan or the prearrangedconcurso mercantil by July 22, 2004, or August 5, 2004 (in connection with an extension of the exchange offer), such date shall be September 30, 2004. | ||||

The new notes to be issued to the holders of existing notes who have entered into voting agreements are being issued in a private placement that will close simultaneously with the public exchange offer and such securities will be "restricted securities" under the Securities Act. We have agreed to register these new notes as soon as practicable by filing and having declared effective a registration statement under the Securities Act to permit resales of the new notes received in the private exchange offer. | ||||

The voting agreements also provide that if we (i) have not commenced the U.S. prepackaged plan or prearrangedconcurso mercantil by June 15, 2004, (ii) have not launched the exchange offer, consummated the exchange offer or commenced the U.S. prepackaged plan or the prearrangedconcurso mercantil by July 22, 2004 or August 5, 2004, as applicable, or (iii) commit certain defaults as described in the voting agreements, then the holders who have entered into voting agreements shall be entitled to receive a delay fee with respect to the existing notes held by such holders equal to the amount of interest that would accrue during the delay period on such existing notes equal to the difference between 13.5% per annum and the rate of interest on the existing notes that would otherwise be applicable during the delay period. The delay fee shall be earned during the delay period, which is from and after (A) June 15, 2004, since we did not launch the exchange offer by such time, (B) July 22, 2004, if we have not launched the exchange offer, consummated the exchange offer or commenced the U.S. prepackaged plan or the prearrangedconcurso mercantil, or (C) the date of a Company default under the voting agreements, to and including the earliest to occur of (w) the date we commence the U.S. prepackaged plan or the prearrangedconcurso mercantil, (x) the date we cure the applicable default under clause (iii) above, (y) September 30, 2004, and (z) the settlement date. If the settlement date does not occur pursuant to the exchange offer and September 30, 2004 occurs after the commencement of the U.S. prepackaged plan or the prearrangedconcurso mercantil, then the delay fee shall be deemed to have accrued on all existing notes and all holders of existing notes will be entitled to receive the delay fee for the applicable delay period. The delay fee shall be paid in additional new notes and delivered to the holders on the earlier to occur of September 30, 2004 and the settlement date. | ||||

Conditions to the Exchange Offer and Consent Solicitation | The exchange offer and consent solicitation are subject to the terms and conditions set forth under "The Exchange Offer and Consent Solicitation—Conditions to the Exchange Offer," including the condition that we receive valid and unrevoked tenders from holders of at least 98% in aggregate outstanding principal amount of the 2003 notes and 95% in aggregate outstanding principal amount of the 2006 notes. | |||

18

Procedures for Tendering | Any holder of existing notes that wishes to participate in the exchange offer must tender its existing notes on or after the date of this prospectus and solicitation statement, even if such existing notes have been tendered to us for exchange in our previous exchange offers. If your existing notes are held by a broker, dealer, commercial bank, trust company or other custodian and you wish to tender them in the exchange offer, you should promptly contact the custodian and instruct the custodian to tender on your behalf. | |||

If your existing notes are held by you as physical certificates registered in your name, and you wish to tender them in the exchange offer, you must (a) deliver these existing notes to a broker, dealer, commercial bank, trust company or other custodian that can act on your behalf and that has an account at the Depository Trust Company ("DTC") and (b) instruct this custodian to tender your existing notes on your behalf. We are requiring this because the new notes will be available only in book-entry form through accounts at DTC. To participate in the exchange offer you must tender existing notes through a DTC account and have the new notes you will receive credited to a DTC account. If you need any assistance doing this, contact the information agent at its phone number listed on the back cover page of this prospectus and solicitation statement. | ||||

Existing notes held through DTC must be tendered only by book-entry transfer using DTC's ATOP (Automated Tender Offer Program) system. In order for a book-entry transfer to constitute a valid tender of your existing notes in the exchange offer, the exchange agent must receive an agent's message confirming your acceptance of the terms of the exchange offer and the book-entry transfer of your existing notes into the exchange agent's account at DTC prior to the expiration date.Holders of existing notes tendering via DTC's ATOP system need not deliver a completed letter of transmittal to the exchange agent.See "The Exchange Offer and Consent Solicitation—Procedures for Tendering." | ||||

If your existing notes are held through Euroclear Bank S.A./N.V., as operator of the Euroclear System ("Euroclear") or Clearstream Banking, société anonyme ("Clearstream, Luxembourg"), you must comply with the procedures established by Euroclear or Clearstream, Luxembourg, as applicable, for tendering your existing notes in the exchange offer. Euroclear and Clearstream, Luxembourg intend to collect from their direct participants (a) instructions to (1) tender existing notes held by them on behalf of their direct participants in the exchange offer, (2) "block" any transfer of existing notes so tendered until the completion of the exchange offer, and (3) debit their account on the settlement date in respect of all existing notes accepted for exchange by us; and (b) irrevocable authorizations to disclose the names of the direct participants and information about the foregoing instructions. Upon the receipt of these instructions, Euroclear and Clearstream, Luxembourg will advise, indirectly, the exchange agent of the amount of existing notes being tendered and other required information. Euroclear and Clearstream, Luxembourg may impose additional deadlines in order to process properly these instructions. As a part of tendering through Euroclear or Clearstream, Luxembourg, you are required to become aware of any such deadlines. | ||||

19

Consequences to Holders of Existing Notes Not Tendering in the Exchange Offer | For a description of the consequences to holders of existing notes of not tendering in the exchange offer, see "Risk Factors—Factors relating to the restructuring." | |||

No Withdrawal Rights | Tenders for exchange of existing notes that are made on or after the date of this prospectus and solicitation statement are irrevocable and may not be withdrawn, except for circumstances in which we make a material amendment to the exchange offer or waive a material condition thereto, or except as permitted by the voting agreements in the case of holders of existing notes who have entered into such voting agreements. See "The Exchange Offer and Consent Solicitation—Expiration Date; Extensions; Amendments; Termination," "No Withdrawal Rights" and "—Voting Agreements." | |||

Exchange Agent | The Bank of New York is serving as the exchange agent (the "exchange agent") for the exchange offer. You can find the address and telephone number for The Bank of New York on the back cover page of this prospectus and solicitation statement. | |||

Solicitation Agent, Information Agent and Voting Agent | Innisfree M&A Incorporated is serving as the solicitation agent, information agent and voting agent (the "solicitation agent") for the exchange offer, consent solicitation and the U.S. prepackaged plan. You can find the address and telephone number for Innisfree M&A Incorporated on the back cover page of this prospectus and solicitation statement. | |||

Use of Proceeds | We will not realize any proceeds from the exchange offer. | |||

20

The New Notes