UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-21485

Cohen & Steers Infrastructure Fund, Inc.

(Exact name of registrant as specified in charter)

280 Park Avenue, New York, NY 10017

(Address of principal executive offices) (Zip code)

Dana A. DeVivo

Cohen & Steers Capital Management, Inc.

280 Park Avenue

New York, New York 10017

(Name and address of agent for service)

Registrant’s telephone number, including area code: (212) 832-3232

Date of fiscal year end: December 31

Date of reporting period: June 30, 2020

Item 1. Reports to Stockholders.

COHEN & STEERS INFRASTRUCTURE FUND, INC.

To Our Shareholders:

We would like to share with you our report for the six months ended June 30, 2020. The total returns for Cohen & Steers Infrastructure Fund, Inc. (the Fund) and its comparative benchmarks were:

| | | | |

| | | Six Months Ended

June 30, 2020 | |

Cohen & Steers Infrastructure Fund at Net Asset Valuea | | | -14.84 | % |

Cohen & Steers Infrastructure Fund at Market Valuea | | | -12.21 | % |

Blended Benchmark—80% FTSE Global Core Infrastructure 50/50 Net Tax Index / 20% ICE BofA Fixed Rate Preferred Securities Indexb | | | -11.13 | % |

S&P 500 Indexb | | | -3.08 | % |

The performance data quoted represent past performance. Past performance is no guarantee of future results. The investment return and the principal value of an investment will fluctuate and shares, if sold, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance results reflect the effects of leverage, resulting from borrowings under a credit agreement. Current total returns of the Fund can be obtained by visiting our website at cohenandsteers.com. The Fund’s returns assume the reinvestment of all dividends and distributions at prices obtained under the Fund’s dividend reinvestment plan. Index performance does not reflect the deduction of any fees, taxes or expenses. An investor cannot invest directly in an index. Performance figures for periods shorter than one year are not annualized.

Managed Distribution Policy

The Fund, acting in accordance with an exemptive order received from the U.S. Securities and Exchange Commission (SEC) and with approval of its Board of Directors (the Board), adopted a managed distribution policy under which the Fund intends to include long-term capital gains, where applicable, as part of the regular monthly cash distributions to its shareholders (the Plan). The Plan gives the Fund greater flexibility to realize long-term capital gains and to distribute those gains on a regular monthly basis. In accordance with the Plan, the Fund currently distributes $0.155 per share on a monthly basis.

| a | As a closed-end investment company, the price of the Fund’s exchange-traded shares will be set by market forces and can deviate from the net asset value (NAV) per share of the Fund. |

| b | The FTSE Global Core Infrastructure 50/50 Net Tax Index is a market-capitalization-weighted index of worldwide infrastructure and infrastructure-related securities and is net of dividend withholding taxes. Constituent weights are adjusted semi-annually according to three broad industry sectors: 50% utilities, 30% transportation, and a 20% mix of other sectors, including pipelines, satellites, and telecommunication towers. The ICE BofA Fixed Rate Preferred Securities Index tracks the performance of fixed-rate U.S. dollar-denominated preferred securities issued in the U.S. domestic market. The S&P 500 Index is an unmanaged index of 500 large-capitalization stocks that is frequently used as a general measure of U.S. stock market performance. |

1

COHEN & STEERS INFRASTRUCTURE FUND, INC.

The Fund may pay distributions in excess of the Fund’s investment company taxable income and net realized gains. This excess would be a return of capital distributed from the Fund’s assets. Distributions of capital decrease the Fund’s total assets and, therefore, could have the effect of increasing the Fund’s expense ratio. In addition, in order to make these distributions, the Fund may have to sell portfolio securities at a less than opportune time.

Shareholders should not draw any conclusions about the Fund’s investment performance from the amount of these distributions or from the terms of the Fund’s Plan. The Fund’s total return based on NAV is presented in the table above as well as in the Financial Highlights table.

The Plan provides that the Board of Directors may amend or terminate the Plan at any time without prior notice to Fund shareholders; however, at this time, there are no reasonably foreseeable circumstances that might cause the termination. The termination of the Plan could have the effect of creating a trading discount (if the Fund’s stock is trading at or above NAV) or widening an existing trading discount.

Market Review

Amid global upheaval from COVID-19, the typically defensive behavior of global listed infrastructure broke down in the six months ended June 2020. Infrastructure stocks began the year on solid footing, with share prices buoyed by increasing signs of stabilization amid widespread central bank easing efforts. Investors were also encouraged by a positive manufacturing outlook and progress on U.S.—China trade talks. However, markets were turned upside-down in February as virus cases spread globally.

Economic shutdowns directly impacted many infrastructure subsectors, compounding concerns that without sufficient fiscal and monetary policy actions, the drop in economic activity could lead to a liquidity-driven credit crisis. Unemployment surged, while other data pointed to considerable economic damage worldwide.

Markets staged a sharp recovery beginning in March as central banks cut interest rates, introduced or expanded asset purchases and employed other policies to provide liquidity and support functioning credit markets. Additionally, governments globally introduced massive relief packages, many amounting to 10% or more of their annual economic output. The policy responses came faster and more forcefully than in 2008. However, positive returns in the second quarter were not enough to overcome the declines in the first quarter.

Fund Performance

The Fund had a negative total return in the period and underperformed its blended benchmark on both a market price and NAV basis.

Amid broad market declines, the communications sector advanced strongly amid accelerating capital spending on wireless infrastructure. The sector benefited from an already healthy growth outlook that was bolstered by the likely persistence of remote work and education activity. The Fund’s overweight allocation and security selection in communications contributed to relative performance, including a beneficial out-of-benchmark allocation to data centers, which are seeing strong demand tied to increased data traffic.

Utilities, including water, electric and gas distribution companies, declined despite revenues being relatively insulated from the pandemic-related economic fallout. The portfolio’s security selection in

2

COHEN & STEERS INFRASTRUCTURE FUND, INC.

electric utilities and gas distribution aided relative performance. Notable contributors included overweight or out-of-index positions in companies focused on renewable energy. An overweight allocation and security selection in water companies also contributed to performance.

Transportation sectors declined on the uncertain growth outlook. Travel restrictions and reduced trade particularly impacted airports, though toll roads, marine and railways were also affected. In some instances, transportation infrastructure companies were further hindered by emergency government policies to help relieve burdens on struggling consumers. For instance, certain airports had to contend with reduced or suspended landing and/or parking fees, while some toll road charges were likewise provisionally suspended. Security selection in airports contributed to the Fund’s relative performance, as we chose not to own certain European companies that declined materially. The portfolio’s overweight and security selection in railways detracted, due in part to overweight positions in certain passenger rail companies in Japan and Europe.

Midstream energy declined materially as the abrupt halt to economic activity resulted in an unprecedented collapse in oil demand. The oil price decline that resulted was exacerbated by the breakdown of the supply discipline of the Organization of the Petroleum Exporting Countries and its allies, which added to an already oversupplied market. Counterparty credit risk and the potential for contract renegotiations between midstream companies and their upstream counterparties weighed heavily on the sector until oil prices began to recover as economies reopened. Security selection and an overweight allocation in midstream energy detracted from the Fund’s relative performance, largely stemming from the timing of allocations in a liquified natural gas exporter and a volumetrically sensitive gathering & processing company.

Returns for fixed income securities were negative for the period but generally outperformed equities. The economic shock from efforts to combat COVID-19 and an uncertain outlook drove credit spreads sharply wider in February and March, resulting in steep losses for preferreds and other credit-sensitive fixed income segments. Like equities, fixed income markets began a strong rebound in late March in response to highly supportive fiscal and monetary measures. Credit spreads narrowed significantly, and low rates further supported spreads via keen investor interest in income securities. However, except for the highest quality issues, positive returns in the second quarter were not enough to overcome declines in the first quarter. The Fund’s underweight allocation to fixed income detracted from relative performance.

Impact of Foreign Currency on Fund Performance

The currency impact of the Fund’s investments in foreign securities detracted from absolute performance during the period. Although the Fund reports its NAV and pays dividends in U.S. dollars, the Fund’s investments denominated in foreign currencies are subject to foreign currency risk. Overall, other currencies modestly depreciated against the U.S. dollar. Consequently, changes in the exchange rates between foreign currencies and the U.S. dollar were a net headwind for absolute returns.

Impact of Derivatives on Fund Performance

In connection with its use of leverage, the Fund pays interest on a portion of its borrowings based on a floating rate under the terms of its credit agreement. To reduce the impact that an increase in interest rates could have on the performance of the Fund with respect to these borrowings, the Fund

3

COHEN & STEERS INFRASTRUCTURE FUND, INC.

used forward starting interest rate swaps to extend the maturity of the fixed rate portion of the borrowing. The Fund’s use of swaps detracted from the Fund’s total return for the six months ended June 30, 2020.

Impact of Leverage on Fund Performance

The Fund employs leverage as part of a yield-enhancement strategy. Leverage, which can increase total return in rising markets (just as it can have the opposite effect in declining markets), significantly detracted from the Fund’s performance for the six-month period ended June 30, 2020.

Sincerely,

| | |

| |

|

ROBERT S. BECKER Portfolio Manager | | BEN MORTON Portfolio Manager |

| |

| |  |

WILLIAM F. SCAPELL Portfolio Manager | | ELAINE ZAHARIS-NIKAS Portfolio Manager |

The views and opinions in the preceding commentary are subject to change without notice and are as of the date of the report. There is no guarantee that any market forecast set forth in the commentary will be realized. This material represents an assessment of the market environment at a specific point in time, should not be relied upon as investment advice and is not intended to predict or depict performance of any investment.

Visit Cohen & Steers online at cohenandsteers.com

For more information about the Cohen & Steers family of mutual funds, visit cohenandsteers.com. Here you will find fund net asset values, fund fact sheets and portfolio highlights, as well as educational resources and timely market updates.

Our website also provides comprehensive information about Cohen & Steers, including our most recent press releases, profiles of our senior investment professionals and their investment approach to each asset class. The Cohen & Steers family of mutual funds specializes in liquid real assets, including real estate securities, listed infrastructure and natural resource equities, as well as preferred securities and other income solutions.

4

COHEN & STEERS INFRASTRUCTURE FUND, INC.

Our Leverage Strategy

(Unaudited)

Our current leverage strategy utilizes borrowings up to the maximum permitted by the Investment Company Act of 1940 to provide additional capital for the Fund, with an objective of increasing net income available for shareholders. As of June 30, 2020, leverage represented 29% of the Fund’s managed assets.

Through a combination of variable and fixed rate financing, the Fund has locked in interest rates on a significant portion of this additional capital through 2026 (where we effectively reduce our variable rate obligation and lock in our fixed rate obligation over various terms). Locking in a significant portion of our leveraging costs is designed to protect the dividend-paying ability of the Fund. The use of leverage increases the volatility of the Fund’s NAV in both up and down markets. However, we believe that locking in portions of the Fund’s leveraging costs for the various terms partially protects the Fund’s expenses from an increase in short-term interest rates.

Leverage Factsa,b

| | |

Leverage (as a % of managed assets) | | 29% |

% Variable Rate Financing | | 15% |

Variable Rate | | 1.0% |

% Fixed Rate Financingc,d | | 85% |

Weighted Average Rate on Fixed Financing | | 3.4% |

Weighted Average Term on Fixed Financing | | 3.0 years |

The Fund seeks to enhance its dividend yield through leverage. The use of leverage is a speculative technique and there are special risks and costs associated with leverage. The NAV of the Fund’s shares may be reduced by the issuance and ongoing costs of leverage. So long as the Fund is able to invest in securities that produce an investment yield that is greater than the total cost of leverage, the leverage strategy will produce higher current net investment income for shareholders. On the other hand, to the extent that the total cost of leverage exceeds the incremental income gained from employing such leverage, shareholders would realize lower net investment income. In addition to the impact on net income, the use of leverage will have an effect of magnifying capital appreciation or depreciation for shareholders. Specifically, in an up market, leverage will typically generate greater capital appreciation than if the Fund were not employing leverage. Conversely, in down markets, the use of leverage will generally result in greater capital depreciation than if the Fund had been unlevered. To the extent that the Fund is required or elects to reduce its leverage, the Fund may incur breakage fees under the Fund’s credit arrangement and may need to liquidate investments, including under adverse economic conditions which may result in capital losses potentially reducing returns to shareholders. There can be no assurance that a leveraging strategy will be successful during any period in which it is employed.

| a | Data as of June 30, 2020. Information is subject to change. |

| b | See Note 8 in Notes to Financial Statements. |

| c | Represents a combination of fixed rate borrowings and fixed payer interest rate swap contracts. |

| d | The Fund entered into a forward-starting interest rate swap contract with interest receipts and payments commencing on December 28, 2020 (effective date). |

5

COHEN & STEERS INFRASTRUCTURE FUND, INC.

June 30, 2020

Top Ten Holdingsa

(Unaudited)

| | | | | | | | |

Security | | Value | | | % of

Managed

Assets | |

| | |

NextEra Energy, Inc. | | $ | 199,210,688 | | | | 6.7 | |

Crown Castle International Corp. | | | 167,039,733 | | | | 5.6 | |

American Tower Corp. | | | 127,784,946 | | | | 4.3 | |

Transurban Group | | | 123,860,765 | | | | 4.2 | |

Duke Energy Corp. | | | 87,297,161 | | | | 3.0 | |

Enbridge, Inc. | | | 77,065,223 | | | | 2.6 | |

Union Pacific Corp. | | | 73,689,329 | | | | 2.5 | |

National Grid PLC | | | 61,376,148 | | | | 2.1 | |

Canadian National Railway Co. | | | 55,557,510 | | | | 1.9 | |

American Water Works Co., Inc. | | | 54,616,556 | | | | 1.8 | |

| a | Top ten holdings (excluding short-term investments and derivative instruments) are determined on the basis of the value of individual securities held. The Fund may also hold positions in other securities issued by the companies listed above. See the Schedule of Investments for additional details on such other positions. |

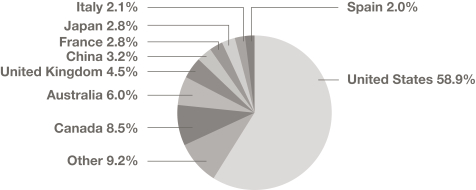

Country Breakdownb

(Based on Managed Assets)

(Unaudited)

| b | Excludes derivative instruments. |

6

COHEN & STEERS INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS

June 30, 2020 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Shares/Units | | | Value | |

COMMON STOCK | | | 116.0% | | | | | | | | | |

AUSTRALIA | | | 7.9% | | | | | | | | | |

AIRPORTS | | | 0.9% | | | | | | | | | |

Sydney Airport | | | | 4,639,253 | | | $ | 18,309,225 | |

| | | | | | | | | | | | |

ELECTRIC | | | 1.1% | | | | | | | | | |

Spark Infrastructure Group | | | | 16,454,821 | | | | 24,576,086 | |

| | | | | | | | | | | | |

REAL ESTATE | | | 0.1% | | | | | | | | | |

DIVERSIFIED | | | 0.1% | | | | | | | | | |

Charter Hall Group | | | | 53,037 | | | | 359,298 | |

Mirvac Group | | | | 293,675 | | | | 443,626 | |

Stockland | | | | 51,588 | | | | 119,622 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 922,546 | |

| | | | | | | | | | | | |

INDUSTRIALS | | | 0.0% | | | | | | | | | |

Goodman Group | | | | 17,700 | | | | 182,633 | |

| | | | | | | | | | | | |

TOTAL REAL ESTATE | | | | | | | | 1,105,179 | |

| | | | | | | | | | | | |

TOLL ROADS | | | 5.8% | | | | | | | | | |

Transurban Groupa | | | | 12,630,198 | | | | 123,860,765 | |

| | | | | | | | | | | | |

TOTAL AUSTRALIA | | | | | | | | 167,851,255 | |

| | | | | | | | | | | | |

AUSTRIA | | | 0.0% | | | | | | | | | |

REAL ESTATE—DIVERSIFIED | | | | | | | | | | | | |

CA Immobilien Anlagen AG | | | | 3,294 | | | | 110,133 | |

| | | | | | | | | | | | |

BELGIUM | | | 0.5% | | | | | | | | | |

ELECTRIC | | | 0.5% | | | | | | | | | |

Elia Group SA/NV | | | | 90,275 | | | | 9,821,104 | |

| | | | | | | | | | | | |

REAL ESTATE | | | 0.0% | | | | | | | | | |

RESIDENTIAL | | | 0.0% | | | | | | | | | |

Aedifica SA | | | | 1,700 | | | | 186,167 | |

| | | | | | | | | | | | |

SELF STORAGE | | | 0.0% | | | | | | | | | |

Warehouses De Pauw CVA | | | | | | | 4,804 | | | | 131,980 | |

| | | | | | | | | | | | |

TOTAL REAL ESTATE | | | | | | | | 318,147 | |

| | | | | | | | | | | | |

TOTAL BELGIUM | | | | | | | | 10,139,251 | |

| | | | | | | | | | | | |

BRAZIL | | | 1.9% | | | | | | | | | |

INFRASTRUCTURE—WATER | | | 0.7% | | | | | | | | | |

Cia de Saneamento do Parana | | | | 2,615,636 | | | | 15,155,788 | |

| | | | | | | | | | | | |

See accompanying notes to financial statements.

7

COHEN & STEERS INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2020 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Shares/Units | | | Value | |

RAILWAYS | | | 0.6% | | | | | | | | | |

Rumo SAb | | | | 3,222,328 | | | $ | 13,326,374 | |

| | | | | | | | | | | | |

TOLL ROADS | | | 0.6% | | | | | | | | | |

CCR SA | | | | 4,219,079 | | | | 11,249,636 | |

| | | | | | | | | | | | |

TOTAL BRAZIL | | | | | | | | 39,731,798 | |

| | | | | | | | | | | | |

CANADA | | | 10.3% | | | | | | | | | |

ELECTRIC | | | 1.3% | | | | | | | | | |

Hydro One Ltd., 144Ac | | | | 1,454,804 | | | | 27,357,945 | |

| | | | | | | | | | | | |

INFRASTRUCTURE | | | 4.1% | | | | | | | | | |

FREIGHT RAILS | | | 2.6% | | | | | | | | | |

Canadian National Railway Co. | | | | 627,965 | | | | 55,557,510 | |

| | | | | | | | | | | | |

MIDSTREAM—C-CORP | | | 1.5% | | | | | | | | | |

Pembina Pipeline Corp. | | | | | | | 1,219,255 | | | | 30,481,375 | |

| | | | | | | | | | | | |

TOTAL INFRASTRUCTURE | | | | | | | | 86,038,885 | |

| | | | | | | | | | | | |

PIPELINES—C-CORP | | | 4.9% | | | | | | | | | |

Enbridge, Inc. (USD)a | | | | 2,534,490 | | | | 77,065,223 | |

TC Energy Corp.a | | | | 640,660 | | | | 27,370,566 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 104,435,789 | |

| | | | | | | | | | | | |

REAL ESTATE | | | 0.0% | | | | | | | | | |

OFFICE | | | 0.0% | | | | | | | | | |

Allied Properties REIT | | | | 8,503 | | | | 256,543 | |

| | | | | | | | | | | | |

RESIDENTIAL | | | 0.0% | | | | | | | | | |

Boardwalk REIT | | | | 9,531 | | | | 208,579 | |

| | | | | | | | | | | | |

TOTAL REALESTATE | | | | | | | | 465,122 | |

| | | | | | | | | | | | |

TOTAL CANADA | | | | | | | | 218,297,741 | |

| | | | | | | | | | | | |

CHINA | | | 4.5% | | | | | | | | | |

GAS DISTRIBUTION | | | 1.3% | | | | | | | | | |

Enn Energy Holdings Ltd. (H shares) | | | | 2,344,221 | | | | 26,490,825 | |

| | | | | | | | | | | | |

PIPELINES—C-CORP | | | 0.6% | | | | | | | | | |

Beijing Enterprises Holdings Ltd. (H shares)a | | | | 3,899,500 | | | | 13,094,797 | |

| | | | | | | | | | | | |

REAL ESTATE | | | 0.7% | | | | | | | | | |

DATA CENTERS | | | 0.7% | | | | | | | | | |

GDS Holdings Ltd., ADR (H shares)a,b,d | | | | 191,667 | | | | 15,268,193 | |

| | | | | | | | | | | | |

See accompanying notes to financial statements.

8

COHEN & STEERS INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2020 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Shares/Units | | | Value | |

DIVERSIFIED | | | 0.0% | | | | | | | | | |

China Overseas Land & Investment Ltd. (H Shares) | | | | 41,000 | | | $ | 125,191 | |

China Resources Land Ltd. (H shares) | | | | 32,000 | | | | 122,310 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 247,501 | |

| | | | | | | | | | | | |

FINANCE | | | 0.0% | | | | | | | | | |

ESR Cayman Ltd., 144A (H Shares)b,c | | | | 116,800 | | | | 277,323 | |

| | | | | | | | | | | | |

TOTAL REAL ESTATE | | | | | | | | | | | 15,793,017 | |

| | | | | | | | | | | | |

TELECOMMUNICATION SERVICES | | | 0.0% | | | | | | | | | |

China Mobile Ltd. (H shares) | | | | 96,500 | | | | 651,573 | |

| | | | | | | | | | | | |

TOLL ROADS | | | 1.2% | | | | | | | | | |

Jiangsu Expressway Co., Ltd. (H shares) | | | | 15,514,000 | | | | 18,233,971 | |

Zhejiang Expressway Co., Ltd., Class H (H shares) | | | | 8,712,000 | | | | 6,186,988 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 24,420,959 | |

| | | | | | | | | | | | |

WATER | | | 0.7% | | | | | | | | | |

Guangdong Investment Ltd. (H shares)a | | | | 8,878,425 | | | | 15,314,292 | |

| | | | | | | | | | | | |

TOTAL CHINA | | | | | | | | 95,765,463 | |

| | | | | | | | | | | | |

FRANCE | | | 2.4% | | | | | | | | | |

ENERGY—OIL & GAS | | | 0.1% | | | | | | | | | |

Total SA | | | | 40,237 | | | | 1,551,475 | |

| | | | | | | | | | | | |

REAL ESTATE | | | 0.0% | | | | | | | | | |

DIVERSIFIED | | | 0.0% | | | | | | | | | |

Covivio | | | | 2,558 | | | | 185,541 | |

| | | | | | | | | | | | |

NET LEASE | | | 0.0% | | | | | | | | | |

ARGAN SA | | | | 1,607 | | | | 147,626 | |

| | | | | | | | | | | | |

OFFICE | | | 0.0% | | | | | | | | | |

Gecina SA | | | | 1,040 | | | | 128,447 | |

| | | | | | | | | | | | |

RETAIL | | | 0.0% | | | | | | | | | |

Klepierre SA | | | | 14,578 | | | | 291,397 | |

| | | | | | | | | | | | |

TOTAL REAL ESTATE | | | | | | | | 753,011 | |

| | | | | | | | | | | | |

TOLL ROADS | | | 2.3% | | | | | | | | | |

Eiffage SA | | | | 196,705 | | | | 18,031,276 | |

Vinci SAa | | | | 323,870 | | | | 30,030,266 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 48,061,542 | |

| | | | | | | | | | | | |

TOTAL FRANCE | | | | | | | | 50,366,028 | |

| | | | | | | | | | | | |

See accompanying notes to financial statements.

9

COHEN & STEERS INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2020 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Shares/Units | | | Value | |

GERMANY | | | 0.1% | | | | | | | | | |

REAL ESTATE | | | | | | | | | | | | |

OFFICE | | | 0.0% | | | | | | | | | |

Alstria Office REIT AG | | | | 6,891 | | | $ | 102,560 | |

| | | | | | | | | | | | |

RESIDENTIAL | | | 0.1% | | | | | | | | | |

Deutsche Wohnen SE | | | | 10,600 | | | | 476,317 | |

Instone Real Estate Group AG, 144Ab,c | | | | 8,451 | | | | 183,352 | |

LEG Immobilien AG | | | | 2,154 | | | | 273,204 | |

Vonovia SE | | | | 10,663 | | | | 651,755 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,584,628 | |

| | | | | | | | | | | | |

TOTAL GERMANY | | | | | | | | 1,687,188 | |

| | | | | | | | | | | | |

HONG KONG | | | 1.2% | | | | | | | | | |

ELECTRIC | | | 1.1% | | | | | | | | | |

Power Assets Holdings Ltd.a | | | | 4,369,500 | | | | 23,875,212 | |

| | | | | | | | | | | | |

REAL ESTATE | | | 0.1% | | | | | | | | | |

DIVERSIFIED | | | 0.1% | | | | | | | | | |

Hang Lung Properties Ltd. | | | | 171,000 | | | | 406,514 | |

New World Development Co., Ltd. | | | | 96,254 | | | | 457,022 | |

Sun Hung Kai Properties Ltd. | | | | 43,500 | | | | 555,723 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 1,419,259 | |

| | | | | | | | | | | | |

RETAIL | | | 0.0% | | | | | | | | | |

Link REIT | | | | 35,907 | | | | 294,802 | |

| | | | | | | | | | | | |

TOTAL REAL ESTATE | | | | | | | | 1,714,061 | |

| | | | | | | | | | | | |

TOTAL HONG KONG | | | | | | | | 25,589,273 | |

| | | | | | | | | | | | |

ITALY | | | 2.9% | | | | | | | | | |

INFRASTRUCTURE—GAS—DISTRIBUTION | | | 0.4% | | | | | | | | | |

Snam S.p.A. | | | | 1,863,711 | | | | 9,085,866 | |

| | | | | | | | | | | | |

TOLL ROADS | | | 1.4% | | | | | | | | | |

Atlantia S.p.A. | | | | 1,744,401 | | | | 28,216,225 | |

| | | | | | | | | | | | |

UTILITIES—ELECTRIC UTILITIES | | | 1.1% | | | | | | | | | |

Enel S.p.A. | | | | 2,698,607 | | | | 23,338,744 | |

| | | | | | | | | | | | |

TOTAL ITALY | | | | | | | | 60,640,835 | |

| | | | | | | | | | | | |

See accompanying notes to financial statements.

10

COHEN & STEERS INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2020 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Shares/Units | | | Value | |

JAPAN | | | 3.4% | | | | | | | | | |

ELECTRIC | | | 1.7% | | | | | | | | | |

Chubu Electric Power Co.a | | | | 1,379,800 | | | $ | 17,305,368 | |

Chugoku Electric Power Co., Inc./The | | | | 1,461,100 | | | | 19,479,428 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 36,784,796 | |

| | | | | | | | | | | | |

GAS DISTRIBUTION | | | 0.7% | | | | | | | | | |

Tokyo Gas Co., Ltd.a | | | | 647,700 | | | | 15,508,916 | |

| | | | | | | | | | | | |

RAILWAYS | | | 0.8% | | | | | | | | | |

East Japan Railway Co.a | | | | 92,000 | | | | 6,375,162 | |

West Japan Railway Co.a | | | | 179,300 | | | | 10,056,751 | |

| | | | | |

| | | | | | | | 16,431,913 | |

| | | | | |

REAL ESTATE | | | 0.2% | | | | | | �� | | | |

DIVERSIFIED | | | 0.2% | | | | | | | | | |

Activia Properties, Inc. | | | | 75 | | | | 259,884 | |

Japan Prime Realty Investment Corp. | | | | 92 | | | | 269,893 | |

Mitsubishi Estate Co., Ltd. | | | | 38,000 | | | | 566,269 | |

Mitsui Fudosan Co., Ltd. | | | | 31,100 | | | | 552,483 | |

NIPPON REIT Investment Corp. | | | | 86 | | | | 278,004 | |

Nomura Real Estate Master Fund, Inc. | | | | 189 | | | | 226,365 | |

Tokyu Fudosan Holdings Corp. | | | | 24,940 | | | | 117,329 | |

United Urban Investment Corp. | | | | 231 | | | | 248,798 | |

| | | | | |

| | | | | | | | 2,519,025 | |

| | | | | |

INDUSTRIALS | | | 0.0% | | | | | | | | | |

GLP J-REIT | | | | 230 | | | | 332,362 | |

| | | | | |

OFFICE | | | 0.0% | | | | | | | | | |

Nippon Building Fund, Inc. | | | | 55 | | | | 313,234 | |

| | | | | |

RESIDENTIAL | | | 0.0% | | | | | | | | | |

Daiwa House REIT Investment Corp. | | | | 124 | | | | 291,723 | |

| | | | | |

TOTAL REAL ESTATE | | | | | | | | 3,456,344 | |

| | | | | |

TOTAL JAPAN | | | | | | | | 72,181,969 | |

| | | | | |

MEXICO | | | 1.2% | | | | | | | | | |

AIRPORTS | | | 0.6% | | | | | | | | | |

Grupo Aeroportuario del Pacifico SAB de CV, Class B | | | | 1,709,329 | | | | 12,339,266 | |

| | | | | |

See accompanying notes to financial statements.

11

COHEN & STEERS INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2020 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Shares/Units | | | Value | |

ELECTRIC | | | 0.6% | | | | | | | | | |

Infraestructura Energetica Nova SAB de CV | | | | 4,804,786 | | | $ | 13,819,940 | |

| | | | | |

TOTAL MEXICO | | | | | | | | 26,159,206 | |

| | | | | |

NETHERLANDS | | | 0.6% | | | | | | | | | |

MARINE PORTS | | | | | | | | | | | | |

Koninklijke Vopak NV | | | | 250,000 | | | | 13,223,590 | |

| | | | | |

NEW ZEALAND | | | 1.3% | | | | | | | | | |

AIRPORTS | | | | | | | | | | | | |

Auckland International Airport Ltd.a | | | | 6,665,359 | | | | 28,346,164 | |

| | | | | |

NORWAY | | | 0.0% | | | | | | | | | |

REAL ESTATE—OFFICE | | | | | | | | | | | | |

Entra ASA, 144Ac | | | | 8,074 | | | | 103,498 | |

| | | | | |

SINGAPORE | | | 0.1% | | | | | | | | | |

REAL ESTATE | | | | | | | | | | | | |

DIVERSIFIED | | | 0.1% | | | | | | | | | |

CapitaLand Commercial Trust | | | | 107,200 | | | | 131,198 | |

City Developments Ltd. | | | | 49,000 | | | | 299,443 | |

Keppel DC REIT | | | | 149,400 | | | | 273,600 | |

| | | | | |

| | | | | | | | 704,241 | |

| | | | | |

HEALTH CARE | | | 0.0% | | | | | | | | | |

Parkway Life Real Estate Investment Trust | | | | 87,000 | | | | 209,049 | |

| | | | | |

INDUSTRIALS | | | 0.0% | | | | | | | | | |

Mapletree Industrial Trust | | | | 117,800 | | | | 245,050 | |

| | | | | |

TOTAL SINGAPORE | | | | | | | | 1,158,340 | |

| | | | | |

SPAIN | | | 2.6% | | | | | | | | | |

AIRPORTS | | | 2.2% | | | | | | | | | |

Aena SME SA, 144Ac | | | | 354,268 | | | | 47,380,372 | |

| | | | | |

COMMUNICATIONS | | | 0.4% | | | | | | | | | |

Cellnex Telecom SA, 144Ac | | | | 133,230 | | | | 8,137,387 | |

| | | | | |

TOTAL SPAIN | | | | | | | | 55,517,759 | |

| | | | | |

SWEDEN | | | 0.1% | | | | | | | | | |

COMMUNICATIONS | | | 0.1% | | | | | | | | | |

Telia Co. AB | | | | 179,800 | | | | 672,668 | |

| | | | | |

See accompanying notes to financial statements.

12

COHEN & STEERS INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2020 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Shares/Units | | | Value | |

REAL ESTATE | | | 0.0% | | | | | | | | | |

DIVERSIFIED | | | 0.0% | | | | | | | | | |

Castellum AB | | | | 14,059 | | | | 263,437 | |

Fastighets AB Balder, Class Bb | | | | 6,005 | | | | 229,758 | |

| | | | | |

| | | | | | | | 493,195 | |

| | | | | |

RETAIL | | | 0.0% | | | | | | | | | |

Catena AB | | | | 3,719 | | | | 147,057 | |

| | | | | |

TOTAL REAL ESTATE | | | | | | | | 640,252 | |

| | | | | |

TOTAL SWEDEN | | | | | | | | 1,312,920 | |

| | | | | |

SWITZERLAND | | | 0.4% | | | | | | | | | |

AIRPORTS | | | | | | | | | | | | |

Flughafen Zurich AG | | | | 61,160 | | | | 7,987,938 | |

| | | | | | | | | | | | |

THAILAND | | | 2.2% | | | | | | | | | |

AIRPORTS | | | | | | | | | | | | |

Airports of Thailand PCL | | | | 23,767,900 | | | | 46,790,963 | |

| | | | | |

UNITED KINGDOM | | | 3.7% | | | | | | | | | |

ELECTRIC | | | 2.9% | | | | | | | | | |

National Grid PLC | | | | 5,030,669 | | | | 61,376,148 | |

| | | | | |

INFRASTRUCTURE | | | 0.7% | | | | | | | | | |

Pennon Group PLC | | | | 1,154,106 | | | | 15,981,718 | |

| | | | | |

REAL ESTATE | | | 0.1% | | | | | | | | | |

DIVERSIFIED | | | 0.0% | | | | | | | | | |

LondonMetric Property PLC | | | | 55,225 | | | | 144,154 | |

| | | | | |

HEALTH CARE | | | 0.0% | | | | | | | | | |

Assura PLC | | | | 192,227 | | | | 186,530 | |

| | | | | |

INDUSTRIALS | | | 0.1% | | | | | | | | | |

Segro PLC | | | | 39,654 | | | | 438,572 | |

| | | | | |

RESIDENTIAL | | | 0.0% | | | | | | | | | |

Grainger PLC | | | | 37,586 | | | | 133,371 | |

UNITE Group PLC | | | | 10,217 | | | | 118,972 | |

| | | | | |

| | | | | | | | | | | 252,343 | |

| | | | | |

SELF STORAGE | | | 0.0% | | | | | | | | | |

Safestore Holdings PLC | | | | 20,166 | | | | 181,768 | |

| | | | | |

TOTAL REAL ESTATE | | | | | | | | 1,203,367 | |

| | | | | |

TOTAL UNITED KINGDOM | | | | | | | | 78,561,233 | |

| | | | | |

See accompanying notes to financial statements.

13

COHEN & STEERS INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2020 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Shares/Units | | | Value | |

UNITED STATES | | | 68.7% | | | | | | | | | |

COMMUNICATIONS—TOWERS | | | 15.1% | | | | | | | | | |

American Tower Corp.a,d | | | | 494,256 | | | $ | 127,784,946 | |

Crown Castle International Corp.a,d | | | | 998,146 | | | | 167,039,733 | |

SBA Communications Corp.a | | | | 83,267 | | | | 24,806,905 | |

| | | | | |

| | | | | | | | | | | 319,631,584 | |

| | | | | |

CONSUMER—CYCLICAL—HOTELS, RESTAURANTS & LEISURE | | | 0.0% | | | | | | | | | |

Boyd Gaming Corp. | | | | 7,110 | | | | 148,599 | |

| | | | | |

DIVERSIFIED | | | 0.4% | | | | | | | | | |

Macquarie Infrastructure Co. LLCa,d | | | | 316,453 | | | | 9,711,943 | |

| | | | | |

ELECTRIC | | | 31.1% | | | | | | | | | |

Alliant Energy Corp.a,d | | | | 1,054,083 | | | | 50,427,331 | |

CMS Energy Corp.a,d | | | | 765,293 | | | | 44,708,417 | |

Dominion Energy, Inc.a,d | | | | 517,111 | | | | 41,979,071 | |

DTE Energy Co.a,d | | | | 328,852 | | | | 35,351,590 | |

Duke Energy Corp.a,d | | | | 1,092,717 | | | | 87,297,161 | |

Edison Internationala,d | | | | 561,544 | | | | 30,497,455 | |

Evergy, Inc.a,d | | | | 760,272 | | | | 45,076,527 | |

FirstEnergy Corp.a,d | | | | 1,120,153 | | | | 43,439,533 | |

NextEra Energy, Inc.a,d | | | | 829,457 | | | | 199,210,688 | |

NorthWestern Corp.a | | | | 549,218 | | | | 29,943,365 | |

Xcel Energy, Inc.a,d | | | | 800,703 | | | | 50,043,937 | |

| | | | | |

| | | | | | | | 657,975,075 | |

| | | | | |

ENERGY | | | 0.5% | | | | | | | | | |

Magellan Midstream Partners LPa | | | | 244,125 | | | | 10,538,876 | |

| | | | | |

GAS DISTRIBUTION | | | 1.1% | | | | | | | | | |

Atmos Energy Corp.a,d | | | | 134,430 | | | | 13,386,539 | |

NiSource, Inc.a,d | | | | 462,529 | | | | 10,517,910 | |

| | | | | |

| | | | | | | | | | | 23,904,449 | |

| | | | | |

INDUSTRIALS | | | 0.1% | | | | | | | | | |

United Parcel Service, Inc. Class Ba | | | | 27,024 | | | | 3,004,528 | |

| | | | | |

INFRASTRUCTURE—ELECTRIC | | | 4.2% | | | | | | | | | |

CenterPoint Energy, Inc.‡ | | | | 1,197,779 | | | | 22,362,534 | |

Pinnacle West Capital Corp.‡ | | | | 483,454 | | | | 35,432,344 | |

PNM Resources, Inc. | | | | 509,474 | | | | 19,584,180 | |

Public Service Enterprise Group, Inc.‡ | | | | 232,010 | | | | 11,405,612 | |

| | | | | |

| | | | | | | | | | | 88,784,670 | |

| | | | | |

See accompanying notes to financial statements.

14

COHEN & STEERS INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2020 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Shares/Units | | | Value | |

INTEGRATED TELECOMMUNICATIONS SERVICES | | | 0.2% | | | | | | | | | |

Verizon Communications, Inc.a | | | | 62,022 | | | $ | 3,419,273 | |

| | | | | |

PIPELINES | | | 6.0% | | | | | | | | | |

PIPELINES—C-CORP | | | 4.4% | | | | | | | | | |

Kinder Morgan, Inc.a,d | | | | 3,055,885 | | | | 46,357,776 | |

ONEOK, Inc.a,d | | | | 554,288 | | | | 18,413,447 | |

Plains GP Holdings LP, Class A‡,a | | | | 1,219,622 | | | | 10,854,636 | |

Williams Cos., Inc.a,d | | | | 903,919 | | | | 17,192,539 | |

| | | | | |

| | | | | | | | | | | 92,818,398 | |

| | | | | |

PIPELINES—MLP | | | 1.6% | | | | | | | | | |

Enterprise Products Partners LPa,d | | | | 632,713 | | | | 11,496,395 | |

MPLX LPa,d | | | | 514,959 | | | | 8,898,492 | |

Noble Midstream Partners LPa | | | | 681,713 | | | | 5,767,292 | |

Western Midstream Partners LPa,b,d | | | | 840,056 | | | | 8,434,162 | |

| | | | | |

| | | | | | | | | | | 34,596,341 | |

| | | | | |

TOTAL PIPELINES | | | | | | | | 127,414,739 | |

| | | | | |

RAILWAYS | | | 6.0% | | | | | | | | | |

Norfolk Southern Corp.a,d | | | | 304,962 | | | | 53,542,178 | |

Union Pacific Corp.a,d | | | | 435,851 | | | | 73,689,329 | |

| | | | | |

| | | | | | | | | | | 127,231,507 | |

| | | | | |

REAL ESTATE | | | 1.4% | | | | | | | | | |

DATA CENTERS | | | 0.7% | | | | | | | | | |

CyrusOne, Inc.a,d | | | | 203,769 | | | | 14,824,195 | |

Equinix, Inc. | | | | 1,314 | | | | 922,822 | |

| | | | | |

| | | | | | | | | | | 15,747,017 | |

| | | | | |

HEALTH CARE | | | 0.2% | | | | | | | | | |

Healthcare Trust of America, Inc., Class A | | | | 7,719 | | | | 204,708 | |

Healthpeak Properties, Inc. | | | | 15,865 | | | | 437,239 | |

Medical Properties Trust, Inc.a | | | | 24,878 | | | | 467,706 | |

Omega Healthcare Investors, Inc. | | | | 5,932 | | | | 176,358 | |

Ventas, Inc. | | | | 25,787 | | | | 944,320 | |

Welltower, Inc. | | | | 21,514 | | | | 1,113,350 | |

| | | | | |

| | | | | | | | | | | 3,343,681 | |

| | | | | |

HOTEL | | | 0.0% | | | | | | | | | |

Hilton Worldwide Holdings, Inc. | | | | 2,804 | | | | 205,954 | |

| | | | | |

See accompanying notes to financial statements.

15

COHEN & STEERS INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2020 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Shares/Units | | | Value | |

INDUSTRIALS | | | 0.1% | | | | | | | | | |

Americold Realty Trust | | | | 8,815 | | | $ | 319,985 | |

Duke Realty Corp. | | | | 11,459 | | | | 405,534 | |

Prologis, Inc. | | | | 20,543 | | | | 1,917,278 | |

| | | | | |

| | | | | | | | | | | 2,642,797 | |

| | | | | |

NET LEASE | | | 0.1% | | | | | | | | | |

Agree Realty Corp. | | | | 6,649 | | | | 436,906 | |

VICI Properties, Inc. | | | | 34,946 | | | | 705,560 | |

| | | | | |

| | | | | | | | | | | 1,142,466 | |

| | | | | |

OFFICE | | | 0.0% | | | | | | | | | |

Boston Properties, Inc. | | | | 1,307 | | | | 118,127 | |

Kilroy Realty Corp. | | | | 5,903 | | | | 346,506 | |

| | | | | |

| | | | | | | | | | | 464,633 | |

| | | | | |

RESIDENTIAL | | | 0.1% | | | | | | | | | |

Essex Property Trust, Inc. | | | | 3,884 | | | | 890,096 | |

Invitation Homes, Inc. | | | | 25,635 | | | | 705,732 | |

UDR, Inc. | | | | 17,819 | | | | 666,074 | |

| | | | | |

| | | | | | | | | | | 2,261,902 | |

| | | | | |

SELF STORAGE | | | 0.1% | | | | | | | | | |

Extra Space Storage, Inc. | | | | 5,009 | | | | 462,681 | |

Public Storagea | | | | 7,309 | | | | 1,402,524 | |

| | | | | |

| | | | | | | | | | | 1,865,205 | |

| | | | | |

SHOPPING CENTERS | | | 0.1% | | | | | | | | | |

COMMUNITY CENTER | | | 0.0% | | | | | | | | | |

Kimco Realty Corp. | | | | 46,434 | | | | 596,212 | |

| | | | | |

REGIONAL MALL | | | 0.1% | | | | | | | | | |

Simon Property Group, Inc. | | | | 11,113 | | | | 759,907 | |

| | | | | |

TOTAL SHOPPING CENTERS | | | | | | | | 1,356,119 | |

| | | | | |

TOTAL REAL ESTATE | | | | | | | | 29,029,774 | |

| | | | | |

WATER | | | 2.6% | | | | | | | | | |

American Water Works Co., Inc.a,d | | | | 424,503 | | | | 54,616,556 | |

| | | | | |

TOTAL UNITED STATES | | | | | | | | 1,455,411,573 | |

| | | | | |

TOTAL COMMON STOCK

(Identified cost—$1,985,201,264) | | | | | | | | 2,456,934,118 | |

| | | | | |

See accompanying notes to financial statements.

16

COHEN & STEERS INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2020 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Shares/Units | | | Value | |

PREFERRED SECURITIES—$25 PAR VALUE | | | 7.1% | | | | | | | | | |

BERMUDA | | | 0.1% | | | | | | | | | |

INSURANCE | | | | | | | | | | | | |

PROPERTY CASUALTY | | | 0.1% | | | | | | | | | |

Enstar Group Ltd., 7.00% to 9/1/28, Series D

(USD)e,f | | | | 77,050 | | | $ | 1,866,151 | |

| | | | | |

REINSURANCE | | | 0.0% | | | | | | | | | |

RenaissanceRe Holdings Ltd., 5.75%, Series F

(USD)f | | | | 7,000 | | | | 181,230 | |

| | | | | |

TOTAL BERMUDA | | | | | | | | 2,047,381 | |

| | | | | |

CANADA | | | 0.2% | | | | | | | | | |

PIPELINES | | | 0.1% | | | | | | | | | |

Enbridge, Inc., 6.375% to 4/15/23, due 4/15/78,

Series B (USD)e | | | | 77,150 | | | | 1,874,745 | |

| | | | | |

UTILITIES | | | 0.1% | | | | | | | | | |

Algonquin Power & Utilities Corp., 6.875% to

10/17/23, due 10/17/78 (USD)e | | | | 38,890 | | | | 1,020,863 | |

Algonquin Power & Utilities Corp., 6.20% to 7/1/24,

due 7/1/79, Series 19-A (USD)e | | | | 65,127 | | | | 1,703,722 | |

| | | | | |

| | | | | | | | | | | 2,724,585 | |

| | | | | |

TOTAL CANADA | | | | | | | | 4,599,330 | |

| | | | | |

NETHERLANDS | | | 0.1% | | | | | | | | | |

INSURANCE | | | | | | | | | | | | |

Aegon Funding Co. LLC, 5.10%, due 12/15/49 (USD)a | | | | 132,100 | | | | 3,035,658 | |

| | | | | |

UNITED STATES | | | 6.7% | | | | | | | | | |

BANKS | | | 2.8% | | | | | | | | | |

Bank of America Corp., 6.00%, Series EEa,f | | | | 100,000 | | | | 2,584,000 | |

Bank of America Corp., 6.00%, Series GGa,f | | | | 204,775 | | | | 5,580,119 | |

Bank of America Corp., 5.875%, Series HHf | | | | 82,800 | | | | 2,177,640 | |

Bank of America Corp., 5.375%, Series KKf | | | | 55,130 | | | | 1,416,841 | |

Bank of America Corp., 5.00%, Series LL‡,f | | | | 101,143 | | | | 2,554,872 | |

Capital One Financial Corp., 6.00%, Series H‡,f | | | | 37,407 | | | | 932,931 | |

Capital One Financial Corp., 4.80%, Series Jf | | | | 90,575 | | | | 1,898,452 | |

Citigroup Capital XIII, 7.13% (3 Month US LIBOR + 6.37%), due 10/30/40 (FRN)g | | | | 145,444 | | | | 3,854,266 | |

Citigroup, Inc., 6.30%, Series Sa,f | | | | 97,743 | | | | 2,503,198 | |

See accompanying notes to financial statements.

17

COHEN & STEERS INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2020 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Shares/Units | | | Value | |

Citizens Financial Group, Inc., 5.00%, Series Ef | | | | 58,500 | | | $ | 1,316,250 | |

GMAC Capital Trust I, 6.177% (3 Month US LIBOR + 5.785%), due 2/15/40, Series 2 (TruPS) (FRN)a,g | | | | 216,141 | | | | 4,845,881 | |

Huntington Bancshares, Inc., 6.25%, Series Da,f | | | | 73,122 | | | | 1,831,706 | |

JPMorgan Chase & Co., 6.10%, Series AAa,f | | | | 121,901 | | | | 3,097,504 | |

JPMorgan Chase & Co., 5.75%, Series DDf | | | | 15,000 | | | | 396,300 | |

New York Community Bancorp, Inc., 6.375% to 3/17/27, Series Aa,e,f | | | | 58,930 | | | | 1,430,231 | |

Regions Financial Corp., 5.70% to 5/15/29, Series Ca,e,f | | | | 181,815 | | | | 4,485,376 | |

Synovus Financial Corp., 5.875% to 7/1/24, Series Ee,f | | | | 82,725 | | | | 1,799,269 | |

Wells Fargo & Co., 5.25%, Series Pa,f | | | | 110,900 | | | | 2,753,647 | |

Wells Fargo & Co., 5.85% to 9/15/23, Series Qa,e,f | | | | 129,292 | | | | 3,201,270 | |

Wells Fargo & Co., 6.00%, Series Ta,f | | | | 24,750 | | | | 632,115 | |

Wells Fargo & Co., 5.70%, Series Wa,f | | | | 143,039 | | | | 3,630,330 | |

Wells Fargo & Co., 5.625%, Series Ya,f | | | | 99,275 | | | | 2,517,614 | |

Wells Fargo & Co., 4.75%, Series Za,f | | | | 206,575 | | | | 4,800,803 | |

| | | | | |

| | | | | | | | | | | 60,240,615 | |

| | | | | |

ELECTRIC | | | 1.3% | | | | | | | | | |

CMS Energy Corp., 5.875%, due 3/1/79a | | | | 99,975 | | | | 2,620,345 | |

DTE Energy Co., 5.375%, due 6/1/76, Series Ba | | | | 182,874 | | | | 4,599,281 | |

Duke Energy Corp., 5.75%, Series Aa,f | | | | 181,350 | | | | 4,881,942 | |

Integrys Holding, Inc., 6.00% to 8/1/23, due 8/1/73a,e | | | | 174,388 | | | | 4,446,894 | |

NextEra Energy Capital Holdings, Inc., 5.65%, due 3/1/79, Series Na | | | | 115,742 | | | | 3,098,413 | |

Southern Co./The, 5.25%, due 12/1/77a | | | | 99,672 | | | | 2,512,731 | |

Southern Co./The, 4.95%, due 1/30/80, Series 2020a | | | | 230,000 | | | | 5,773,000 | |

| | | | | |

| | | | | | | | | | | 27,932,606 | |

| | | | | |

FINANCIAL | | | 0.8% | | | | | | | | | |

DIVERSIFIED FINANCIAL SERVICES | | | 0.3% | | | | | | | | | |

Apollo Global Management, Inc., 6.375%, Series Af | | | | 57,982 | | | | 1,488,978 | |

National Rural Utilities Cooperative Finance Corp., 5.50%, due 5/15/64, Series USa | | | | 90,000 | | | | 2,360,700 | |

Synchrony Financial, 5.625%, Series Af | | | | 93,732 | | | | 2,003,053 | |

| | | | | |

| | | | | | | | | | | 5,852,731 | |

| | | | | |

INVESTMENT BANKER/BROKER | | | 0.5% | | | | | | | | | |

Morgan Stanley, 6.875% to 1/15/24, Series Fa,e,f | | | | 100,436 | | | | 2,669,589 | |

See accompanying notes to financial statements.

18

COHEN & STEERS INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2020 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Shares/Units | | | Value | |

Morgan Stanley, 6.375% to 10/15/24, Series Ia,e,f | | | | 178,969 | | | $ | 4,640,666 | |

Morgan Stanley, 5.85% to 4/15/27, Series Ka,e,f | | | | 110,200 | | | | 2,836,548 | |

| | | | | |

| | | | | | | | | | | 10,146,803 | |

| | | | | |

TOTAL FINANCIAL | | | | | | | | 15,999,534 | |

| | | | | |

INDUSTRIALS—CHEMICALS | | | 0.3% | | | | | | | | | |

CHS, Inc., 7.10% to 3/31/24, Series 2a,e,f | | | | 135,283 | | | | 3,264,379 | |

CHS, Inc., 6.75% to 9/30/24, Series 3a,e,f | | | | 137,935 | | | | 3,285,611 | |

| | | | | |

| | | | | | | | | | | 6,549,990 | |

| | | | | |

INSURANCE | | | 0.6% | | | | | | | | | |

LIFE/HEALTH INSURANCE | | | 0.4% | | | | | | | | | |

Athene Holding Ltd., 6.35% to 6/30/29, Series Aa,e,f | | | | 115,223 | | | | 2,809,137 | |

Equitable Holdings, Inc., 5.25%, Series Af | | | | 52,000 | | | | 1,191,840 | |

MetLife, Inc., 4.75%, Series Ff | | | | 68,800 | | | | 1,690,416 | |

Voya Financial, Inc., 5.35% to 9/15/29, Series Be,f | | | | 97,375 | | | | 2,375,950 | |

| | | | | |

| | | | | | | | | | | 8,067,343 | |

| | | | | |

MULTI-LINE | | | 0.2% | | | | | | | | | |

Allstate Corp./The, 5.10%, Series Ha,f | | | | 146,650 | | | | 3,719,044 | |

American International Group, Inc., 5.85%, Series Af | | | | 11,342 | | | | 291,603 | |

Hanover Insurance Group, Inc./The, 6.35%, due 3/30/53 | | | | 50,210 | | | | 1,272,321 | |

| | | | | |

| | | | | | | | | | | 5,282,968 | |

| | | | | |

REINSURANCE | | | 0.0% | | | | | | | | | |

Arch Capital Group Ltd., 5.25%, Series Ef | | | | 10,833 | | | | 259,559 | |

| | | | | |

TOTAL INSURANCE | | | | | | | | 13,609,870 | |

| | | | | |

INTEGRATED TELECOMMUNICATIONS SERVICES | | | 0.1% | | | | | | | | | |

AT&T, Inc., 5.625%, due 8/1/67 | | | | 50,000 | | | | 1,326,500 | |

| | | | | |

PIPELINES | | | 0.2% | | | | | | | | | |

Energy Transfer Operating LP, 7.375% to 5/15/23,

Series Ca,e,f | | | | 142,225 | | | | 2,732,142 | |

Energy Transfer Operating LP, 7.625% to 8/15/23,

Series De,f | | | | 89,991 | | | | 1,751,225 | |

Energy Transfer Operating LP, 7.60% to 5/15/24,

Series Ee,f | | | | 25,586 | | | | 526,048 | |

| | | | | |

| | | | | | | | | | | 5,009,415 | |

| | | | | |

See accompanying notes to financial statements.

19

COHEN & STEERS INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2020 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Shares/Units | | | Value | |

REAL ESTATE | | | 0.2% | | | | | | | | | |

DIVERSIFIED | | | 0.1% | | | | | | | | | |

VEREIT, Inc., 6.70%, Series Fa,f | | | | 66,586 | | | $ | 1,665,982 | |

| | | | | |

REINSURANCE | | | 0.1% | | | | | | | | | |

Arch Capital Group Ltd., 5.45%, Series Fa,f | | | | 80,000 | | | | 1,959,200 | |

| | | | | |

TOTAL REAL ESTATE | | | | | | | | 3,625,182 | |

| | | | | |

UTILITIES | | | 0.4% | | | | | | | | | |

NiSource, Inc. 0.0% to 3/15/24, Series Ba,e,f | | | | 92,315 | | | | 2,382,650 | |

South Jersey Industries, Inc., 5.625%, due 9/16/79 | | | | 95,800 | | | | 2,363,386 | |

Spire, Inc., 5.90%, Series Aa,f | | | | 101,071 | | | | 2,624,814 | |

| | | | | |

| | | | | | | | | | | 7,370,850 | |

| | | | | |

TOTAL UNITED STATES | | | | | | | | 141,664,562 | |

| | | | | |

TOTAL PREFERRED SECURITIES—$25 PAR VALUE

(Identified cost—$153,596,234) | | | | | | | | 151,346,931 | |

| | | | | |

| | | |

| | | | | | Principal

Amount | | | | |

PREFERRED SECURITIES—CAPITAL SECURITIES | | | 16.0% | | | | | | | | | |

AUSTRALIA | | | 0.5% | | | | | | | | | |

INSURANCE-PROPERTY CASUALTY | | | 0.4% | | | | | | | | | |

QBE Insurance Group Ltd., 6.75% to 12/2/24, due 12/2/44 (USD)e,h | | | $ | 5,155,000 | | | | 5,697,538 | |

QBE Insurance Group Ltd., 5.875% to 6/17/26, due 6/17/46, Series EMTN (USD)e,h | | | | 1,800,000 | | | | 1,922,057 | |

| | | | | |

| | | | | | | | 7,619,595 | |

| | | | | |

MATERIAL—METALS & MINING | | | 0.1% | | | | | | | | | |

BHP Billiton Finance USA Ltd., 6.75% to 10/20/25, due 10/19/75, 144A (USD)a,c,e | | | | 1,600,000 | | | | 1,846,792 | |

| | | | | |

TOTAL AUSTRALIA | | | | | | | | 9,466,387 | |

| | | | | |

BRAZIL | | | 0.0% | | | | | | | | | |

BANKS | | | | | | | | | | | | |

Itau Unibanco Holding SA, 4.50% to 11/21/24, due 11/21/29, 144A (USD)a,c,e,i | | | | 800,000 | | | | 759,712 | |

| | | | | |

See accompanying notes to financial statements.

20

COHEN & STEERS INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2020 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Principal

Amount | | | Value | |

CANADA | | | 1.5% | | | | | | | | | |

PIPELINES | | | 1.1% | | | | | | | | | |

Enbridge, Inc., 6.25% to 3/1/28, due 3/1/78 (USD)a,e | | | $ | 3,289,000 | | | $ | 3,245,404 | |

Enbridge, Inc., 6.00% to 1/15/27, due 1/15/77, Series 16-A (USD)a,e | | | | 4,155,000 | | | | 4,107,657 | |

Transcanada Trust, 5.50% to 9/15/29, due 9/15/79 (USD)a,e | | | | 8,620,000 | | | | 8,613,492 | |

Transcanada Trust, 5.875% to 8/15/26, due 8/15/76, Series 16-A (USD)a,e | | | | 5,765,000 | | | | 6,101,340 | |

| | | | | |

| | | | | | | | 22,067,893 | |

| | | | | |

UTILITIES | | | 0.4% | | | | | | | | | |

Emera, Inc., 6.75% to 6/15/26, due 6/15/76, Series 16-A (USD)a,e | | | | 8,000,000 | | | | 8,666,040 | |

| | | | | |

TOTAL CANADA | | | | | | | | 30,733,933 | |

| | | | | |

FINLAND | | | 0.1% | | | | | | | | | |

BANKS | | | | | | | | | | | | |

Nordea Bank Abp, 6.625% to 3/26/26, 144A (USD)a,c,e,f,i | | | | 1,400,000 | | | | 1,495,529 | |

| | | | | |

FRANCE | | | 1.6% | | | | | | | | | |

BANKS | | | 1.5% | | | | | | | | | |

BNP Paribas SA, 6.625% to 3/25/24, 144A (USD)a,c,e,f,i | | | | 3,660,000 | | | | 3,746,925 | |

BNP Paribas SA, 7.00% to 8/16/28, 144A (USD)a,c,e,f,i | | | | 1,000,000 | | | | 1,086,435 | |

BNP Paribas SA, 7.195% to 6/25/37, 144A (USD)a,c,e,f | | | | 2,900,000 | | | | 3,135,139 | |

BNP Paribas SA, 7.375% to 8/19/25, 144A (USD)a,c,e,f,i | | | | 3,600,000 | | | | 3,949,002 | |

BNP Paribas SA, 7.625% to 3/30/21, 144A (USD)a,c,e,f,i | | | | 2,400,000 | | | | 2,437,500 | |

Credit Agricole SA, 6.875% to 9/23/24, 144A (USD)a,c,e,f,i | | | | 2,600,000 | | | | 2,683,057 | |

Credit Agricole SA, 7.875% to 1/23/24, 144A (USD)a,c,e,f,i | | | | 400,000 | | | | 435,462 | |

Credit Agricole SA, 8.125% to 12/23/25, 144A (USD)a,c,e,f,i | | | | 3,550,000 | | | | 4,066,969 | |

Societe Generale SA, 6.75% to 4/6/28, 144A (USD)a,c,e,f,i | | | | 3,400,000 | | | | 3,385,771 | |

Societe Generale SA, 7.375% to 9/13/21, 144A (USD)a,c,e,f,i | | | | 3,600,000 | | | | 3,639,312 | |

Societe Generale SA, 8.00% to 9/29/25, 144A (USD)a,c,e,f,i | | | | 1,800,000 | | | | 2,007,867 | |

| | | | | |

| | | | | | | | 30,573,439 | |

| | | | | |

INSURANCE—MULTI-LINE | | | 0.1% | | | | | | | | | |

AXA SA, 6.379% to 12/14/36, 144A (USD)a,c,e,f | | | | 1,600,000 | | | | 2,058,184 | |

| | | | | |

TOTAL FRANCE | | | | | | | | 32,631,623 | |

| | | | | |

See accompanying notes to financial statements.

21

COHEN & STEERS INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2020 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Principal

Amount | | | Value | |

HONG KONG | | | 0.1% | | | | | | | | | |

BANKS | | | | | | | | | | | | |

Bank of China Hong Kong Ltd., 5.90% to 9/14/23, 144A (USD)a,c,e,f | | | $ | 2,200,000 | | | $ | 2,351,052 | |

| | | | | |

ITALY | | | 0.1% | | | | | | | | | |

BANKS | | | | | | | | | | | | |

Intesa Sanpaolo SpA, 7.70% to 9/17/25, 144A (USD)a,c,e,f,i | | | | 2,900,000 | | | | 2,897,600 | |

| | | | | |

JAPAN | | | 0.5% | | | | | | | | | |

INSURANCE | | | | | | | | | | | | |

LIFE/HEALTH INSURANCE | | | 0.4% | | | | | | | | | |

Dai-ichi Life Insurance Co., Ltd., 5.10% to 10/28/24, 144A (USD)a,c,e,f | | | | 2,000,000 | | | | 2,206,390 | |

Nippon Life Insurance Co., 5.10% to 10/16/24, due 10/16/44, 144A (USD)a,c,e | | | | 5,000,000 | | | | 5,568,682 | |

| | | | | |

| | | | | | | | 7,775,072 | |

| | | | | |

PROPERTY CASUALTY | | | 0.1% | | | | | | | | | |

Mitsui Sumitomo Insurance Co., Ltd., 4.95% to 3/6/29, 144A (USD)a,c,e,f | | | | 2,400,000 | | | | 2,749,956 | |

| | | | | |

TOTAL JAPAN | | | | | | | | 10,525,028 | |

| | | | | |

NETHERLANDS | | | 0.2% | | | | | | | | | |

BANKS | | | | | | | | | | | | |

ING Groep N.V., 5.75% to 11/16/26 (USD)a,e,f,i | | | | 1,800,000 | | | | 1,788,003 | |

ING Groep N.V., 6.875% to 4/16/22 (USD)e,f,h,i | | | | 3,000,000 | | | | 3,109,680 | |

| | | | | |

TOTAL NETHERLANDS | | | | | | | | 4,897,683 | |

| | | | | |

NORWAY | | | 0.2% | | | | | | | | | |

BANKS | | | | | | | | | | | | |

DNB Bank ASA, 6.50% to 3/26/22 (USD)e,f,h,i | | | | 3,000,000 | | | | 3,090,000 | |

| | | | | |

SPAIN | | | 0.2% | | | | | | | | | |

BANKS | | | | | | | | | | | | |

Banco Bilbao Vizcaya Argentaria SA, 6.50% to 3/5/25,

Series 9 (USD)a,e,f,i | | | | 3,800,000 | | | | 3,690,831 | |

| | | | | |

See accompanying notes to financial statements.

22

COHEN & STEERS INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2020 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Principal

Amount | | | Value | |

SWEDEN | | | 0.1% | | | | | | | | | |

BANKS | | | | | | | | | | | | |

Skandinaviska Enskilda Banken AB, 5.125% to 5/13/25 (USD)e,f,h,i | | | $ | 400,000 | | | $ | 389,347 | |

Svenska Handelsbanken AB, 6.25% to 3/1/24, Series EMTN (USD)e,f,h,i | | | | 2,200,000 | | | | 2,322,276 | |

| | | | | |

TOTAL SWEDEN | | | | | | | | 2,711,623 | |

| | | | | |

SWITZERLAND | | | 1.2% | | | | | | | | | |

BANKS | | | 1.1% | | | | | | | | | |

Credit Suisse Group AG, 7.125% to 7/29/22 (USD)e,f,h,i | | | | 2,600,000 | | | | 2,680,444 | |

Credit Suisse Group AG, 6.375% to 8/21/26, 144A (USD)a,c,e,f,i | | | | 3,000,000 | | | | 3,049,005 | |

Credit Suisse Group AG, 7.25% to 9/12/25, 144A (USD)a,c,e,f,i | | | | 1,400,000 | | | | 1,439,473 | |

Credit Suisse Group AG, 7.50% to 12/11/23, 144A (USD)a,c,e,f,i | | | | 400,000 | | | | 431,968 | |

Credit Suisse Group AG, 7.50% to 7/17/23, 144A (USD)a,c,e,f,i | | | | 4,800,000 | | | | 4,990,104 | |

UBS Group Funding Switzerland AG, 7.00% to 1/31/24, 144A (USD)a,c,e,f,i | | | | 4,600,000 | | | | 4,781,447 | |

UBS Group Funding Switzerland AG, 6.875% to 3/22/21 (USD)e,f,h,i | | | | 1,600,000 | | | | 1,623,496 | |

UBS Group Funding Switzerland AG, 6.875% to 8/7/25 (USD)e,f,h,i | | | | 3,200,000 | | | | 3,372,000 | |

UBS Group Funding Switzerland AG, 7.125% to 8/10/21 (USD)e,f,h,i | | | | 1,600,000 | | | | 1,635,414 | |

| | | | | |

| | | | | | | | 24,003,351 | |

| | | | | |

INSURANCE—PROPERTY CASUALTY | | | 0.1% | | | | | | | | | |

Swiss Re Finance Luxembourg SA, 5.00% to 4/2/29, due 4/2/49, 144A (USD)a,c,e | | | | 2,000,000 | | | | 2,250,500 | |

| | | | | |

TOTAL SWITZERLAND | | | | | | | | 26,253,851 | |

| | | | | |

UNITED KINGDOM | | | 2.6% | | | | | | | | | |

BANKS | | | 2.3% | | | | | | | | | |

Barclays PLC, 7.875% to 3/15/22 (USD)e,f,h,i | | | | 3,800,000 | | | | 3,873,112 | |

Barclays PLC, 8.00% to 6/15/24 (USD)a,e,f,i | | | | 2,200,000 | | | | 2,280,906 | |

HBOS Capital Funding LP, 6.85% (USD)f,h | | | | 2,400,000 | | | | 2,437,584 | |

HSBC Capital Funding Dollar 1 LP, 10.176% to 6/30/30, 144A (USD)a,c,e,f | | | | 8,950,000 | | | | 14,148,294 | |

See accompanying notes to financial statements.

23

COHEN & STEERS INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2020 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Principal

Amount | | | Value | |

HSBC Holdings PLC, 6.375% to 3/30/25 (USD)a,e,f,i | | | $ | 1,600,000 | | | $ | 1,643,676 | |

HSBC Holdings PLC, 6.50% to 3/23/28 (USD)a,e,f,i | | | | 2,800,000 | | | | 2,875,782 | |

HSBC Holdings PLC, 6.875% to 6/1/21 (USD)a,e,f,i | | | | 3,400,000 | | | | 3,450,386 | |

Lloyds Banking Group PLC, 7.50% to 6/27/24 (USD)a,e,f,i | | | | 3,534,000 | | | | 3,673,664 | |

Lloyds Banking Group PLC, 7.50% to 9/27/25 (USD)a,e,f,i | | | | 1,800,000 | | | | 1,868,668 | |

Nationwide Building Society, 10.25%, due 12/6/99f,h | | | | 435,000 | | | | 843,549 | |

Royal Bank of Scotland Group PLC, 7.648% to 9/30/31

(USD)a,e,f | | | | 2,512,000 | | | | 3,639,185 | |

Royal Bank of Scotland Group PLC, 8.00% to 8/10/25

(USD)a,e,f,i | | | | 3,600,000 | | | | 3,981,888 | |

Royal Bank of Scotland Group PLC, 8.625% to 8/15/21

(USD)a,e,f,i | | | | 3,200,000 | | | | 3,334,304 | |

Standard Chartered PLC, 7.75% to 4/2/23, 144A (USD)c,e,f,i | | | | 600,000 | | | | 626,544 | |

| | | | | |

| | | | | | | | | | | 48,677,542 | |

| | | | | |

INTEGRATED TELECOMMUNICATIONS SERVICES | | | 0.1% | | | | | | | | | |

Vodafone Group PLC, 7.00% to 1/4/29, due 4/4/79

(USD)a,e | | | | 2,850,000 | | | | 3,342,936 | |

| | | | | | | | | | | | |

OIL & GAS | | | 0.2% | | | | | | | | | |

BP Capital Markets PLC, 4.875% to 3/22/30 (USD)a,e,f | | | | 3,550,000 | | | | 3,674,250 | |

| | | | | | | | | | | | |

TOTAL UNITED KINGDOM | | | | | | | | 55,694,728 | |

| | | | | | | | | | | | |

UNITED STATES | | | 7.1% | | | | | | | | | |

BANKS | | | 3.8% | | | | | | | | | |

AgriBank FCB, 6.875% to 1/1/24a,e,f | | | | 37,000 | † | | | 3,922,000 | |

Bank of America Corp., 6.10% to 3/17/25, Series AAa,e,f | | | | 2,186,000 | | | | 2,307,749 | |

Bank of America Corp., 5.875% to 3/15/28, Series FFa,e,f | | | | 4,682,000 | | | | 4,792,183 | |

Bank of America Corp., 6.25% to 9/5/24, Series Xa,e,f | | | | 4,700,000 | | | | 4,874,262 | |

Bank of America Corp., 6.50% to 10/23/24, Series Za,e,f | | | | 3,806,000 | | | | 4,097,777 | |

Citigroup, Inc., 5.90% to 2/15/23a,e,f | | | | 5,675,000 | | | | 5,645,887 | |

Citigroup, Inc., 5.95% to 5/15/25, Series Pa,e,f | | | | 6,000,000 | | | | 5,969,005 | |

Citigroup, Inc., 6.25% to 8/15/26, Series Ta,e,f | | | | 4,850,000 | | | | 5,149,269 | |

Citigroup, Inc., 5.00% to 9/12/24, Series Ua,e,f | | | | 3,040,000 | | | | 2,867,052 | |

Citizens Financial Group, Inc., 5.65% to 10/6/25, Series Fe,f | | | | 2,000,000 | | | | 2,032,500 | |

Citizens Financial Group, Inc., 6.375% to 4/6/24, Series Ca,e,f | | | | 1,200,000 | | | | 1,116,000 | |

CoBank ACB, 6.25% to 10/1/22, Series Fa,e,f | | | | 52,500 | † | | | 5,414,062 | |

CoBank ACB, 6.25% to 10/1/26, Series Ia,e,f | | | | 2,866,000 | | | | 2,866,000 | |

Comerica, Inc., 5.625% to 7/1/25e,f | | | | 1,500,000 | | | | 1,525,950 | |

See accompanying notes to financial statements.

24

COHEN & STEERS INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2020 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Principal

Amount | | | Value | |

Farm Credit Bank of Texas, 6.75% to 9/15/23, 144Aa,c,e,f | | | $ | 35,300 | † | | $ | 3,706,500 | |

Farm Credit Bank of Texas, 10.00%, Series 1a,f | | | | 2,000 | † | | | 2,020,000 | |

Goldman Sachs Group, Inc./The, 5.30% to 11/10/26, Series Oa,e,f | | | | 1,645,000 | | | | 1,659,047 | |

Goldman Sachs Group, Inc./The, 5.50% to 8/10/24, Series Qa,e,f | | | | 1,690,000 | | | | 1,753,068 | |

Huntington Bancshares, Inc., 5.625% to 7/15/30, Series Fe,f | | | | 1,500,000 | | | | 1,554,750 | |

JPMorgan Chase & Co., 4.23%

(3 Month US LIBOR + 3.47%), Series I (FRN)a,f,g | | | | 2,034,000 | | | | 1,855,494 | |

JPMorgan Chase & Co., 6.75% to 2/1/24, Series Sa,e,f | | | | 2,790,000 | | | | 3,005,117 | |

JPMorgan Chase & Co., 6.10% to 10/1/24, Series Xa,e,f | | | | 500,000 | | | | 512,709 | |

Truist Financial Corp., 5.125% to 12/15/27, Series Me,f | | | | 500,000 | | | | 482,931 | |

Truist Financial Corp., 4.80% to 9/01/24, Series Na,e,f | | | | 1,810,000 | | | | 1,668,689 | |

Truist Financial Corp., 5.10% to 3/1/30, Series Qe,f | | | | 4,210,000 | | | | 4,357,771 | |

Wells Fargo & Co., 5.95%, due 12/1/86a | | | | 2,830,000 | | | | 3,413,396 | |

Wells Fargo & Co., 5.875% to 6/15/25, Series Ua,e,f | | | | 1,891,000 | | | | 1,969,187 | |

| | | | | |

| | | | | | | | | | | 80,538,355 | |

| | | | | |

COMMUNICATIONS—TOWERS | | | 0.5% | | | | | | | | | |

Crown Castle International Corp., 6.875%, due 8/1/20,

Series A (Convertible) | | | | 7,400 | † | | | 11,022,443 | |

| | | | | |

ELECTRIC | | | 0.3% | | | | | | | | | |

CenterPoint Energy, Inc., 6.125% to 9/1/23,

Series Aa,e,f | | | | 1,960,000 | | | | 1,900,547 | |

Dominion Energy, Inc., 4.65% to 12/15/24,

Series Ba,e,f | | | | 327,000 | | | | 320,487 | |

Duke Energy Corp., 4.875% to 9/16/24a,e,f | | | | 3,580,000 | | | | 3,580,774 | |

| | | | | |

| | | | | | | | | | | 5,801,808 | |

| | | | | |

FINANCIAL—INVESTMENT BANKER/BROKER | | | 0.3% | | | | | | | | | |

Charles Schwab Corp./The, 5.375% to 6/1/25,

Series G‡,e,f | | | | 4,736,000 | | | | 5,071,404 | |

Morgan Stanley, 5.55% to 10/15/20, Series Ja,e,f | | | | 1,809,000 | | | | 1,662,836 | |

| | | | | |

| | | | | | | | | | | 6,734,240 | |

| | | | | | | | | | | | |

FOOD | | | 0.2% | | | | | | | | | |

Dairy Farmers of America, Inc., 7.875%, 144Ac,f,j | | | | 60,000 | † | | | 5,160,000 | |

| | | | | |

See accompanying notes to financial statements.

25

COHEN & STEERS INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2020 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Principal

Amount | | | Value | |

INFRASTRUCTURE | | | 0.3% | | | | | | | | | |

ELECTRIC | | | 0.1% | | | | | | | | | |

CMS Energy Corp., 4.75% to 3/1/30, due 6/1/50‡,a,e | | | $ | 2,300,000 | | | $ | 2,349,693 | |

| | | | | |

GAS—DISTRIBUTION | | | 0.2% | | | | | | | | | |

Sempra Energy, 4.875% to 10/15/25e,f | | | | 3,780,000 | | | | 3,789,450 | |

| | | | | | | | | | | | |

TOTAL INFRASTRUCTURE | | | | | | | | 6,139,143 | |

| | | | | | | | | | | | |

INSURANCE | | | 1.4% | | | | | | | | | |

LIFE/HEALTH INSURANCE | | | 1.0% | | | | | | | | | |

MetLife Capital Trust IV, 7.875%, due 12/15/37, 144A (TruPS)a,c | | | | 4,500,000 | | | | 5,708,543 | |

MetLife, Inc., 9.25%, due 4/8/38, 144Aa,c | | | | 6,500,000 | | | | 9,025,672 | |

MetLife, Inc., 3.888% (3 Month US LIBOR + 3.575%),

Series C (FRN)a,f,g | | | | 3,200,000 | | | | 2,894,000 | |

MetLife, Inc., 5.875% to 3/15/28, Series Da,e,f | | | | 2,530,000 | | | | 2,674,466 | |

Voya Financial, Inc., 5.65% to 5/15/23, due 5/15/53a,e | | | | 500,000 | | | | 504,623 | |

Voya Financial, Inc., 6.125% to 9/15/23, Series Aa,e,f | | | | 1,310,000 | | | | 1,282,195 | |

| | | | | |

| | | | | | | | | | | 22,089,499 | |

| | | | | |

MULTI-LINE | | | 0.1% | | | | | | | | | |

American International Group, Inc., 8.175% to 5/15/38,

due 5/15/68a,e | | | | 925,000 | | | | 1,182,445 | |

| | | | | |

PROPERTY CASUALTY | | | 0.2% | | | | | | | | | |

Assurant, Inc., 7.00% to 3/27/28, due 3/27/48a,e | | | | 3,200,000 | | | | 3,288,717 | |

Liberty Mutual Group, Inc., 7.80%, due 3/7/87, 144Aa,c | | | | 1,680,000 | | | | 2,016,714 | |

| | | | | |

| | | | | | | | | | | 5,305,431 | |

| | | | | |

REINSURANCE | | | 0.1% | | | | | | | | | |

AXIS Specialty Finance LLC, 4.90% to 1/15/30,

due 1/15/40a,e | | | | 1,760,000 | | | | 1,655,049 | |

| | | | | |

TOTAL INSURANCE | | | | | | | | 30,232,424 | |

| | | | | |

PIPELINES | | | 0.1% | | | | | | | | | |

Energy Transfer Operating LP, 7.125% to 5/15/30,

Series Ga,e,f | | | | 2,780,000 | | | | 2,380,375 | |

| | | | | |

See accompanying notes to financial statements.

26

COHEN & STEERS INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2020 (Unaudited)

| | | | | | | | | | | | |

| | | | | | Principal

Amount | | | Value | |

UTILITIES | | | 0.2% | | | | | | | | | |

NextEra Energy Capital Holdings, Inc., 5.65% to 5/1/29,

due 5/1/79a,e | | | $ | 2,870,000 | | | $ | 3,136,013 | |

| | | | | |

TOTAL UNITED STATES | | | | | | | | 151,144,801 | |

| | | | | |

TOTAL PREFERRED SECURITIES—CAPITAL SECURITIES

(Identified cost—$316,992,038) | | | | | | | | 338,344,381 | |

| | | | | |

| | | |

| | | | | | Shares | | | | |

SHORT-TERM INVESTMENTS | | | 0.8% | | | | | | | | | |

MONEY MARKET FUNDS | | | | | | | | | | | | |

State Street Institutional Treasury Money Market Fund,

Premier Class, 0.11%k | | | | 16,410,711 | | | | 16,410,711 | |

| | | | | |

TOTAL SHORT-TERM INVESTMENTS

(Identified cost—$16,410,711) | | | | | | | | 16,410,711 | |

| | | | | |

TOTAL INVESTMENTSIN SECURITIES

(Identified cost—$2,472,200,247) | | | 139.9% | | | | | | | | 2,963,036,141 | |

WRITTEN OPTION CONTRACTS | | | (0.1) | | | | | | | | (2,242,770 | ) |

LIABILITIESIN EXCESSOF OTHER ASSETS | | | (39.8) | | | | | | | | (843,188,580 | ) |

| | | | | | | | | | | | |

NET ASSETS (Equivalent to $22.64 per share based on 93,522,809 shares of common stock outstanding) | | | 100.0% | | | | | | | $ | 2,117,604,791 | |

| | | | | | | | | | | | |

Exchange-Traded Option Contracts

Written Options

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| Description | | Exercise

Price | | | Expiration

Date | | | Number of

Contracts | | | Notional

Amountl | | | Premiums

Received | | | Value | |

Call—Crown Castle International Corp. | | $ | 160.00 | | | | 7/17/20 | | | | (1,878 | ) | | $ | (31,428,330 | ) | | $ | (653,457 | ) | | $ | (1,690,200 | ) |

Call—GDS Holdings Ltd. | | | 80.00 | | | | 7/17/20 | | | | (967 | ) | | | (7,703,122 | ) | | | (138,327 | ) | | | (299,770 | ) |

Put—Norfolk Southern Corp. | | | 165.00 | | | | 7/17/20 | | | | (800 | ) | | | (14,045,600 | ) | | | (336,652 | ) | | | (252,800 | ) |

| |

| | | | | | | | | | | (3,645 | ) | | $ | (53,177,052 | ) | | $ | (1,128,436 | ) | | $ | (2,242,770 | ) |

| |

See accompanying notes to financial statements.

27

COHEN & STEERS INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2020 (Unaudited)

Centrally Cleared Interest Rate Swap Contracts

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | |

| Notional Amount | | Fixed

Rate

Payablem | | | Fixed Payment

Frequency | | | Floating

Rate

Receivablem

(resets monthly) | | | Floating

Payment

Frequency | | | Maturity

Date | | | Value | | | Upfront

Receipts

(Payments) | | | Unrealized (Depreciation) | |

$212,500,000 | | | 1.240 | % | | | Monthly | | | | 1 Month LIBOR | | | | Monthly | | | | 2/3/26 | | | $ | (10,427,632 | ) | | $ | (97,997 | ) | | $ | (10,525,629 | ) |

| |

The total amount of all interest rate swap contracts as presented in the table above are representative of the volume of activity for this derivative type during the six months ended June 30, 2020.

Glossary of Portfolio Abbreviations

| | |

ADR | | American Depositary Receipt |

EMTN | | Euro Medium Term Note |

FRN | | Floating Rate Note |

LIBOR | | London Interbank Offered Rate |

MLP | | Master Limited Partnership |

REIT | | Real Estate Investment Trust |

TruPS | | Trust Preferred Securities |

USD | | United States Dollar |

Note: Percentages indicated are based on the net assets of the Fund.

| ‡ | All or a portion of the security is pledged in connection with exchange-traded written option contracts. $34,107,672 in aggregate has been pledged as collateral. |

| a | All or a portion of the security is pledged as collateral in connection with the Fund’s credit agreement. $1,785,614,876 in aggregate has been pledged as collateral. |

| b | Non-income producing security. |

| c | Securities exempt from registration under Rule 144A of the Securities Act of 1933. These securities may only be resold to qualified institutional buyers. Aggregate holdings amounted to $193,281,977 which represents 9.1% of the net assets of the Fund, of which 0.2% are illiquid. |

| d | A portion of the security has been rehypothecated in connection with the Fund’s credit agreement. $740,670,279 in aggregate has been rehypothecated. |

| e | Security converts to floating rate after the indicated fixed-rate coupon period. |

| f | Perpetual security. Perpetual securities have no stated maturity date, but they may be called/redeemed by the issuer. |

| g | Variable rate. Rate shown is in effect at June 30, 2020. |

See accompanying notes to financial statements.

28

COHEN & STEERS INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS—(Continued)

June 30, 2020 (Unaudited)

| h | Securities exempt from registration under Regulation S of the Securities Act of 1933. These securities are subject to resale restrictions. Aggregate holdings amounted to $32,996,497 which represents 1.6% of the net assets of the Fund, of which 0.0% are illiquid. |

| i | Contingent Capital security (CoCo). CoCos are debt or preferred securities with loss absorption characteristics built into the terms of the security for the benefit of the issuer. Aggregate holdings amounted to $98,593,559 which represents 4.7% of the net assets of the Fund. (3.3% of the managed assets of the Fund). |

| j | Security value is determined based on significant unobservable inputs (Level 3). |

| k | Rate quoted represents the annualized seven-day yield. |

| l | Amount represents number of contracts multiplied by notional contract size multiplied by the underlying price. |

| m | Represents a forward-starting interest rate swap with interest receipts and payments commencing on December 28, 2020 (effective date). |

| | | | |

Sector Summary | | % of Managed

Assets | |

Electric | | | 30.0 | |

Communications | | | 11.4 | |

Pipelines | | | 9.3 | |

Banks | | | 9.0 | |

Toll Roads | | | 7.9 | |

Infrastructure | | | 7.5 | |

Airports | | | 5.4 | |

Railways | | | 5.3 | |

Other | | | 3.1 | |

Water | | | 2.4 | |

Gas Distribution | | | 2.2 | |

Insurance | | | 2.1 | |

Real Estate | | | 2.1 | |

Utilities | | | 1.5 | |

Financial | | | 0.8 | |

| | | | |

| | | 100.0 | |

| | | | |

See accompanying notes to financial statements.

29

COHEN & STEERS INFRASTRUCTURE FUND, INC.

STATEMENT OF ASSETS AND LIABILITIES

June 30, 2020 (Unaudited)

| | | | |

ASSETS: | | | | |

Investments in securities, at valuea (Identified cost—$2,472,200,247) | | $ | 2,963,036,141 | |

Cash collateral pledged for interest rate swap contracts | | | 6,021,972 | |

Foreign currency, at value (Identified cost—$2,319,488) | | | 2,314,817 | |

Receivable for: | | | | |

Dividends and interest | | | 9,775,066 | |

Investment securities sold | | | 236,868 | |

Variation margin on interest rate swap contracts | | | 97,428 | |

Other assets | | | 77,366 | |

| | | | |

Total Assets | | | 2,981,559,658 | |

| | | | |

LIABILITIES: | | | | |

Written option contracts, at value (Premiums received—$1,128,436) | | | 2,242,770 | |

Payable for: | | | | |

Credit agreement | | | 850,000,000 | |

Investment securities purchased | | | 5,183,401 | |

Interest expense | | | 2,128,767 | |

Investment management fees | | | 2,116,020 | |

Foreign capital gains tax | | | 1,198,642 | |

Dividends declared | | | 564,822 | |

Administration fees | | | 149,366 | |

Directors’ fees | | | 3,231 | |

Due to custodian | | | 22 | |

Other liabilities | | | 367,826 | |

| | | | |

Total Liabilities | | | 863,954,867 | |

| | | | |

NET ASSETS | | $ | 2,117,604,791 | |

| | | | |

NET ASSETS consist of: | | | | |

Paid-in capital | | $ | 1,681,302,490 | |

Total distributable earnings/(accumulated loss) | | | 436,302,301 | |

| | | | |

| | $ | 2,117,604,791 | |

| | | | |

NET ASSET VALUE PER SHARE: | | | | |

($2,117,604,791 ÷ 93,522,809 shares outstanding) | | $ | 22.64 | |

| | | | |

MARKET PRICE PER SHARE | | $ | 22.05 | |

| | | | |

MARKET PRICE PREMIUM (DISCOUNT) TO NET ASSET VALUE PER SHARE | | | (2.61 | )% |

| | | | |

| a | Includes $1,785,614,876 pledged as collateral, of which $740,670,279 has been rehypothecated, in connection with the Fund’s credit agreement, as described in Note 8. |

See accompanying notes to financial statements.

30

COHEN & STEERS INFRASTRUCTURE FUND, INC.

STATEMENT OF OPERATIONS