As filed with the Securities and Exchange Commission on January 27, 2004

Registration No. [ ]

Registration No. [ ]

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

MORRIS PUBLISHING GROUP, LLC

MORRIS PUBLISHING FINANCE CO.

(Exact names of registrants as specified in their charters)

(FOR CO-REGISTRANTS, PLEASE SEE “TABLE OF CO-REGISTRANTS”

ON THE FOLLOWING PAGE)

Georgia

Georgia

(State or other jurisdiction of incorporation or organization)

2711

2711

(Primary Standard Industrial Classification Code Numbers)

58-1445060

20-0183044

(I.R.S. Employer Identification Numbers)

725 Broad Street

Augusta, Georgia 30901

(706) 724-0851

(Address, including zip code, and telephone number, including area

code, of registrants’ principal executive offices)

William S. Morris IV

President and Chief Executive Officer

Morris Publishing Group, LLC

725 Broad Street

Augusta, Georgia 30901

(706) 724-0851

(Name, address, including zip code, and telephone number, including area code,

of agent for service)

Copy to:

Mark S. Burgreen, Esq.

Hull, Towill, Norman, Barrett & Salley, P.C.

801 Broad Street, 7th Floor

Augusta, Georgia 30901

(706) 722-4481

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box.¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.¨

CALCULATION OF REGISTRATION FEE

| | | | | | | | |

|

| Title of Each Class of Securities to be Registered | | Amount to be

Registered | | Proposed

Maximum

Offering Price

Per Unit (1) | | Proposed

Maximum

Aggregate

Offering Price | | Amount of

Registration

Fee |

|

7% Senior Subordinated Notes due 2013 | | $300,000,000 | | 100% | | $300,000,000 | | $24,270 |

|

Guarantees of 7% Senior Subordinated Notes due 2013(2) | | N/A | | N/A | | N/A | | N/A |

|

| (1) | Estimated solely for the purpose of calculating the amount of the registration fee in accordance with Rule 457 under the Securities Act of 1933. |

| (2) | Morris Publishing Group, LLC’s subsidiaries, listed in the table on the following page (the “Guarantors”), have guaranteed on a senior subordinated unsecured basis, jointly and severally, the payment of the principal of, premium, if any, and interest on the 7% Senior Subordinated Notes due 2013 being registered hereby (the “Guarantees”). The Guarantors are registering the Guarantees. Pursuant to Rule 457(n) under the Securities Act of 1933, as amended, no registration fee is required with respect to the Guarantees. |

The Registrants hereby amend this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrants shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

TABLE OF CO-REGISTRANTS

| | | | | | |

Name of Additional Registration

| | State of

Incorporation/

Formation

| | Primary Standard

Industrial

Classification

Code

| | I.R.S.

Employer

Identification

Number

|

Yankton Printing Company | | South Dakota | | 2711 | | 46-0208120 |

Broadcaster Press, Inc. | | South Dakota | | 2711 | | 46-0283275 |

The Sun Times, LLC | | Georgia | | 2711 | | 58-1445060 |

Homer News, LLC | | Georgia | | 2711 | | 58-1445060 |

Log Cabin Democrat, LLC | | Georgia | | 2711 | | 58-1445060 |

Athens Newspapers, LLC | | Georgia | | 2711 | | 58-1445060 |

Southeastern Newspapers Company, LLC | | Georgia | | 2711 | | 58-1445060 |

Stauffer Communications, Inc. | | Delaware | | 2711 | | 58-2450047 |

Florida Publishing Company | | Florida | | 2711 | | 58-2228216 |

Southwestern Newspapers Company, L.P. | | Texas | | 2711 | | 58-2361328 |

Fall Line Publishing, Inc. | | Georgia | | 2711 | | 58-1969520 |

The Blue Springs Examiner, LLC | | Missouri | | 2711 | | 58-1445060 |

The Examiner of Independence, LLC | | Missouri | | 2711 | | 58-1445060 |

The Newton Kansan, LLC | | Kansas | | 2711 | | 58-1445060 |

Oak Grove Shopper, LLC | | Missouri | | 2711 | | 58-1445060 |

The Oak Ridger, LLC | | Tennessee | | 2711 | | 58-1445060 |

MPG Allegan Property, LLC | | Georgia | | 2711 | | 58-1445060 |

MPG Holland Property, LLC | | Georgia | | 2711 | | 58-1445060 |

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer of sale is not permitted.

Subject to Completion Dated January 27, 2004

| | |

| | Morris Publishing Group, LLC Morris Publishing Finance Co. |

OFFER TO EXCHANGE

ALL OUTSTANDING

Series A 7% Senior Subordinated Notes Due 2013

FOR

Series B 7% Senior Subordinated Notes Due 2013

OF

Morris Publishing Group, LLC and

Morris Publishing Finance Co.

THE EXCHANGE OFFER WILL EXPIRE AT 5:00 P.M., NEW YORK CITY TIME

ON [ ], 2004, UNLESS EXTENDED

Morris Publishing Group, LLC and Morris Publishing Finance Co. hereby offer to exchange for their unregistered 7% Senior Subordinated Notes due 2013, of which $250.0 million aggregate principal amount were issued on August 7, 2003 and another $50.0 million aggregate principal amount were issued on September 24, 2003, an equal face amount of registered 7% Senior Subordinated Notes due 2013. The terms of the Series B registered notes, also referred to as exchange notes, are identical in all material respects to the Series A unregistered notes, also referred to as the original notes, except that the exchange notes are registered under the Securities Act of 1933 and the transfer restrictions and registration rights applicable to the original notes generally do not apply to the exchange notes. The original notes and the exchange notes offered by this prospectus are sometimes collectively referred to as the notes.

The exchange notes will mature on August 1, 2013. Interest on the exchange notes is payable semi-annually on February 1 and August 1 of each year.

We may redeem some or all of the exchange notes at any time on or after August 1, 2008. We may also redeem up to 35% of the aggregate principal amount of the exchange notes using the proceeds of one or more public equity offerings completed before August 1, 2006. The redemption prices are described beginning on page 76. If we sell certain of our assets or experience specific kinds of changes of control, we must offer to purchase the exchange notes.

The exchange notes will be our unsecured senior subordinated obligations and will be subordinated to all of our existing and future senior debt, rank equally with all of our existing and future senior subordinated debt and rank senior to all of our future subordinated debt. The exchange notes will be guaranteed, on a senior subordinated basis, by each of our existing and future restricted subsidiaries other than the co-issuer Morris Publishing Finance Co.

All original notes that are validly tendered and not validly withdrawn will be exchanged. Tenders of original notes may be withdrawn at any time prior to the expiration of the exchange offer. The exchange offer is subject to customary conditions, including the condition that the exchange offer not violate applicable law or any applicable interpretation of the staff of the Securities and Exchange Commission.

We will not receive any proceeds from the exchange offer.

See “Risk factors” beginning on page 14 for a discussion of certain risks that you should consider before you tender your original notes.

The exchange notes will not be listed on any securities exchange.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THESE SECURITIES OR PASSED UPON THE ACCURACY OR ADEQUACY OF THIS PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

The date of this Prospectus is [ ], 2004.

In making your investment decision, you should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with any other information. If you receive any other information, you should not rely on it.

We are offering to exchange the exchange notes for the original notes only in places where offers and sales are permitted.

You should not assume that the information contained in this prospectus is accurate as of any date other than the date on the front cover of this prospectus.

Table of contents

Morris Publishing Group, LLC is a wholly-owned subsidiary of Morris Communications Company, LLC, a privately held media company. Morris Publishing Finance Co., a wholly-owned subsidiary of Morris Publishing Group, LLC, was incorporated in 2003 for the sole purpose of serving as a co-issuer of the notes in order to facilitate the offering. Morris Publishing Finance Co. does not have any operations or assets of any kind and will not have any revenues. Prospective investors in the exchange notes should not expect Morris Publishing Finance Co. to have the ability to service the interest and principal obligations on the exchange notes. Our principal executive offices are located at 725 Broad Street, Augusta, Georgia 30901, and our telephone number at that address is (706) 724-0851. Our parent company’s web site is located athttp://www.morris.com. The information on our parent’s web site is not part of this offering memorandum.

In this offering memorandum, “Morris Publishing,” “we,” “us” and “our” refer to Morris Publishing Group, LLC and its subsidiaries, except in the Description of the exchange notes and where the context otherwise excludes subsidiaries. “Morris Communications” refers to Morris Communications Company, LLC. Morris Publishing Group was formed in 2001 and assumed the operations of the newspaper business segment of our parent, Morris Communications. Discussions of Morris Publishing and our results of operations include the business as previously conducted by the Morris Communications newspaper business segment.

i

Industry and market data

Unless otherwise indicated, information contained in this prospectus concerning the newspaper industry, our general expectations concerning the industry and its segments and our market position and market share within the industry and its segments are derived from data from various third party sources as well as management estimates. Management’s estimates are derived from third party sources as well as data from our internal research and from assumptions made by us, based on such data and our knowledge of the newspaper industry which we believe to be reasonable. We have not independently verified any information from third party sources and cannot assure you of its accuracy or completeness. Our internal research has not been verified by any independent source. While we are not aware of any misstatements regarding any industry or similar data presented herein, such data involves risks and uncertainties, may not be reliable, and is subject to change based on various factors, including those discussed under the caption “Risk factors” in this offering memorandum.

Data on our market position and market share within our industry is based, in part, on independent industry publications, government publications, reports by market research firms or other published independent sources, including Newspaper Association of America and Audit Bureau of Circulation statistics. Unless otherwise indicated, all readership information contained in this offering memorandum for non-daily newspapers and free community newspapers is based upon our internal records, and represents approximate current or average readership.

Unless otherwise indicated, all circulation information contained in this offering memorandum represents unaudited approximate three month average daily or non-daily circulation, as the case may be, for the third quarter of 2003 derived from our internal records. Certain of our circulation figures for most of our daily newspapers and one of our weekly newspapers are subject to audit by the Audit Bureau of Circulation or Verified Audit Circulation. Our circulation figures for our other daily and weekly newspapers are not subject to audit by the Audit Bureau of Circulation or any other independent source, but we attempt to internally measure their circulation figures under the same guidelines as if they were audited by the Audit Bureau of Circulation or Verified Audit Circulation.

Disclosure regarding forward-looking statements

This prospectus contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These are statements that relate to future periods and include statements regarding our anticipated performance. You may find discussions containing such forward-looking statements in “Management’s discussion and analysis of financial condition and results of operations,” in our vision statement on the inside front cover, and within this offering memorandum generally.

Generally, the words anticipates, believes, expects, intends, estimates, projects, plans and similar expressions identify forward-looking statements. These forward-looking statements involve known and unknown risks, uncertainties and other important factors that could cause our actual results, performance or achievements or industry results, to differ materially from any future results, performance or achievements expressed or implied by these forward-looking statements. These risks, uncertainties and other important factors are disclosed under “Risk factors” and elsewhere in this offering memorandum, including, without limitation, in conjunction with the forward-looking statements included in this offering memorandum.

ii

Although we believe that these statements are based upon reasonable assumptions, we can give no assurance that these statements will be realized. Given these uncertainties, prospective investors are cautioned not to place undue reliance on these forward-looking statements. These forward-looking statements are made as of the date of this prospectus. We assume no obligation to update or revise them or provide reasons why actual results may differ. Important factors that could cause our actual results to differ materially from our expectations include, without limitation:

| | · | | delay in any economic recovery or the recovery not being as robust as might otherwise have been anticipated; |

| | · | | increases in financing, labor, health care and/or other costs, including costs of raw materials, such as newsprint; |

| | · | | general economic or business conditions, either nationally, regionally or in the individual markets in which we conduct business (and, in particular, the Jacksonville, Florida market), may deteriorate and have an adverse impact on our advertising or circulation revenues or on our business strategy; |

| | · | | competition, including from other newspapers, other traditional forms of advertising and forms made possible by the internet, may increase; |

| | · | | our ability to limit increases in our general and administrative costs and to achieve expected results from a cost savings plan designed to improve efficiencies and operations; |

| | · | | government regulation, including any effect on our ability to continue to maintain and increase circulation revenues due to recent national regulations that, in effect, permit households to exempt themselves from direct telephone marketing efforts; |

| | · | | our ability to retain management and other employees; |

| | · | | a significant deterioration in our labor relations; |

| | · | | our ability to successfully integrate newspaper businesses that we may acquire and our ability to achieve the anticipated returns on any such investments; |

| | · | | downgrades in our credit ratings; and |

| | · | | other risks and uncertainties, including those listed under the caption “Risk factors.” |

iii

Summary

This summary highlights the information contained elsewhere in this prospectus. Because this is only a summary, it does not contain all of the information that may be important to you. For a more complete understanding of this offering, we encourage you to read this entire prospectus and the documents to which this prospectus refers. You should read the following summary together with the more detailed information and combined financial statements and the notes to those statements included elsewhere in this prospectus. Unless otherwise indicated, financial information included in this prospectus is presented on an historical basis.

Overview

Morris Publishing is one of the oldest newspaper companies in the United States with 26 daily, ten non-daily and 23 free community newspapers in the United States. For the third quarter of 2003, our newspapers had unaudited average daily and Sunday paid circulation aggregating 684,697 and 765,464, respectively. Our largest newspapers (with their respective average daily circulations in parentheses) areThe Florida Times-Union, Jacksonville, Florida (166,812),The Augusta Chronicle, Georgia (74,584),The Topeka Capital-Journal,Kansas (58,383),Savannah Morning News, Georgia (54,308),Lubbock Avalanche-Journal, Texas (53,859) andAmarillo Globe-News, Texas (51,901). For the third quarter of 2003, we also had circulation each week of 52,986 non-daily newspapers and 390,588 free community newspapers or shoppers, in communities in or near our daily newspapers.

Our newspapers are geographically diverse, primarily serving mid-sized to small communities in Florida, Georgia, Texas, Kansas, Nebraska, Oklahoma, Michigan, Missouri, Minnesota, Alaska, Arkansas, South Dakota, Tennessee and South Carolina. The majority of our daily newspapers have no significant competition from other local daily newspapers in their respective communities.

We have historically been consistently profitable in varying economic climates, with generally stable operating results. Our total operating revenues for 2002 were $433.4 million and have been between $429.5 million and $455.4 million for each year since 1998. EBITDA (as defined—see footnote (a) on page 12) was $111.7 million in 2002 and has ranged from approximately $104.1 million to $120.1 million for each year since 1998. Our EBITDA margin (as defined) was 25.8% in 2002 and has ranged from 23.8% to 27.1% for each year since 1998 and was 21.4% for the nine months ending September 30, 2003. We have operated each of our 26 daily newspapers at least since 1995.

Operating strategy

Our strategy is to increase our revenues and cash flows by growing market share and operating efficiently. Achieving this strategy is based upon the following initiatives:

| · | | Being a leader in providing local information and advertising. Our focus is to be, and we believe we are, the trusted source of local news and information and local advertising in the communities we serve. As the leading provider of local news and information in print and online formats in our markets, we believe we can both maintain and increase our readership and our share of local advertising expenditures. |

1

| · | | Increasing readership. We are committed to maintaining the high quality of our newspapers and their editorial integrity to assure continued reader loyalty. Through extensive market research we strive to deliver the service and content each of our markets demand. Many of our newspapers have won various editorial awards in their local markets. Furthermore, by introducing niche publications that address the needs of targeted groups and by offering earlier delivery times, we continue to create opportunities to introduce new readers to our newspapers. |

| · | | Growing advertising revenue. Through targeted market research we attempt to understand the needs of our advertisers. This market understanding enables us to develop programs that address the individual needs of our advertisers and to appeal to targeted groups of advertisers and readers with niche publications addressing specific areas such as real estate, automobiles, employment, farming, nursing, antiques, college student guides, foreign language, and other items of local interest. In addition, we are dedicated to establishing a better trained and focused sales staff. We expect these initiatives, combined with our focus on increasing readership, to enhance our opportunities to increase our revenues. |

| · | | Enhancing online initiatives. To further support our readership and revenue growth initiatives, we have made a substantial commitment to enhancing our local web sites that complement all of our daily newspapers. Over the last four years, our newspapers have won 16 national Digital Edge awards from the Newspaper Association of America. We continue to pursue various initiatives to attract new readers and grow revenues. |

| · | | Centralizing operations to support multiple publications. We create synergies and cost savings, including through cross-selling of advertising, centralizing news gathering and consolidating printing, production and back-office activities. This involves producing our weekly newspapers, free distribution shoppers and additional niche or regional publications using the facilities of our daily newspapers. We can thereby improve distribution, introduce new products and services in a cost-effective manner and increase readership, offering advertisers expanded reach both geographically and demographically. |

| · | | Focusing on cost control. We continue to focus on managing our operating costs. Recent initiatives to further reduce costs include creation, beginning in 2002, of a Shared Services Center, established by Morris Communications, serving Morris Publishing as well as other Morris Communications’ companies, which we expect over time will create cost synergies by leveraging technologies and simplifying, standardizing and centralizing most administrative functions, thereby reducing our headcount. Beginning in the fourth quarter of 2002 we began participation in a newsprint purchasing consortium. While initially near term costs will increase as we bring the Shared Services Center online, all of these initiatives, which are anticipated to be fully implemented by the end of 2005, are expected to result in aggregate annual cost savings of up to $10.0 million. |

| · | | Investing in strategic technologies. In conjunction with the Shared Services Center initiative, we will utilize technology to help streamline our back-office operations, improve efficiency, and reduce employee headcount. Additionally, we continue to explore technologies that will enable us to more efficiently print, produce and deliver our newspapers. |

2

Strategic acquisitions

We may, from time to time, seek strategic or targeted investments, including newspaper acquisitions and dispositions and, in that regard, we periodically review newspaper and other acquisition candidates that we believe are underperforming in terms of operating cash flows, are in the same geographic region as one of our existing newspapers where we can achieve an efficient operating cluster of newspapers, or otherwise present us with strategic opportunities for growth. Morris Publishing currently has no present commitments with respect to any material acquisitions, dispositions or joint ventures.

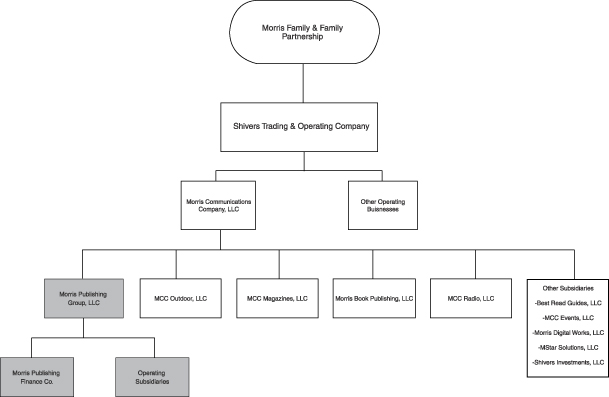

History and corporate structure

Morris Publishing is a private company owned by the William S. Morris III family, as a part of their Morris Communications group of companies. In 1929, William S. Morris, Jr., the father of today’s chairman, became a bookkeeper atThe Augusta Chronicle. In the 1940s William S. Morris, Jr. and another investor purchasedThe Augusta Chronicle. While Morris Communications’ principal business is newspaper publishing conducted by Morris Publishing, Morris Communications has other investments and operations including outdoor advertising, magazines and specialized publications, book publishing and distribution, radio broadcasting, visitor publications, event management and online services. The chart below is a summary of the organizational structure (with intermediate holding companies and lower tier subsidiaries eliminated):

3

Financing developments

On August 7, 2003, we issued $250.0 million aggregate principal amount of 7% senior subordinated notes due 2013 and on September 24, 2003, we issued an additional $50.0 million aggregate principal amount of 7% senior subordinated notes due 2013. Collectively, these notes constitute a single series of Series A notes in an aggregate principal amount of $300.0 million, and are the original notes for which the registered exchange notes are offered in exchange pursuant to this exchange offer.

On August 7, 2003, we also entered into new senior secured credit facilities, consisting of a $225.0 million term loan facility and a $175.0 million revolving loan facility. The proceeds of the initial issuance of $250.0 million of the original notes together with the proceeds of our new credit facility, were used to (i) repay our debt to Morris Communications, which repaid its existing credit facilities, the proceeds of which were used in large part to fund our business, and (ii) to fund our general corporate activities, including working capital requirements and capital expenditures. The proceeds of the subsequent issuance of the additional $50.0 million of the original notes were used to reduce existing indebtedness (but not available borrowings) under the new revolving credit facility.

4

The exchange offer

In August and September, 2003, we completed two private offerings aggregating $300.0 million in aggregate principal amount of 7% senior subordinated notes due 2013. In connection with the offerings of those original notes, we entered into registration rights agreements with the initial purchasers of those original notes in which we agreed to deliver this prospectus to you and to complete an exchange offer for those original notes. Below is a summary of the exchange offer.

| | |

| |

| Securities offered | | $300,000,000 aggregate principal amount of 7% senior subordinated notes due 2013. |

| |

| Exchange offer | | We are offering to exchange an aggregate of $300,000,000 principal amount of exchange notes for an aggregate of $300,000,000 principal amount of original notes. The original notes may be exchanged only in multiples of $1,000. |

| |

| Expiration date | | This exchange offer will expire at 5:00 p.m., New York City time, on [ ], 2004, unless we extend the offer. |

| |

| Procedures for tendering original notes | | The procedures for exchanging original notes involve notifying the exchange agent before the expiration date of the exchange offer of your intention to do so. The procedures for properly providing notice are described on page 66 of this prospectus under the heading “The exchange offer — Exchange offer procedures — How to tender.” |

| |

| Acceptance of original notes and delivery of exchange notes | | We will accept any original notes that are properly tendered for exchange before 5:00 p.m., New York City time, on the day this exchange offer expires. The exchange notes will be delivered promptly after expiration of this exchange offer. |

| |

| Exchange date | | We will notify the exchange agent of the date of acceptance of the original notes for exchange. |

| |

| Withdrawal rights | | If you tender your original notes for exchange in this exchange offer and later wish to withdraw them, you may do so at any time before 5:00 p.m., New York City time, on the day this exchange offer expires. |

| |

| Effect on holders of original notes | | Any original notes that remain outstanding after this exchange offer will continue to be subject to restrictions on their transfer. After the expiration of this exchange offer, holders |

5

| | |

| | | of original notes will not (with limited exceptions) have any further rights under the registration rights agreements. Any market for original notes that are not exchanged could be adversely affected by the completion of this exchange offer. See “Risk factors — The original notes are, and will continue to be, subject to restrictions on transfer, and the trading market, if any, for original notes may be adversely affected by completion of this exchange offer” on page 25. |

| |

| Resale of the exchange notes | | Based on the position of the staff of the Division of Corporation Finance of the SEC as stated in certain interpretive letters issued to third parties in other transactions, we believe that the exchange notes acquired in this exchange offer may be freely traded without compliance with the provisions of the Securities Act of 1933, as amended, that call for registration and delivery of a prospectus, except as described in the following paragraphs. See “Plan of distribution” on page 126. |

| |

| | | In order to participate in the exchange offer, you will be required to make specified representations in a letter of transmittal, including that: |

| |

| | | · you are not an “affiliate” of ours, as defined in Rule 405 of the Securities Act of 1933; · you are not a broker-dealer who owns original notes acquired directly from us; · you will acquire the exchange notes in the ordinary course of business; and · you have not agreed with anyone to distribute the exchange notes. |

| |

| | | If you are a broker-dealer that purchased original notes for your own account as part of market-making or other trading activities, you may represent to us that you have not agreed with us or our affiliates to distribute the exchange notes. If you make this representation, you must agree to deliver a prospectus in connection with any resale of the exchange notes and you need not make the last representation provided for above. |

6

| | |

| Accrued interest on the original notes | | Any interest that has accrued on an original note before its exchange in this exchange offer will be payable on the exchange note on the first interest payment date after the completion of this exchange offer. If your original notes are accepted for exchange, then you will receive interest on the exchange notes and not on the original notes. |

| |

| Tax consequences | | The exchange of the original notes for the exchange notes will not be a taxable exchange for United States federal income tax purposes. See “Certain U.S. federal income tax considerations” on page 120. |

| |

| Exchange agent | | Wachovia Bank is serving as the exchange agent. Its address and telephone number are provided in this prospectus under the heading “The exchange offer — Exchange agent” on page 71. |

| |

| Use of proceeds | | We will not receive any cash proceeds from this exchange offer. |

Please review the information in the section “The exchange offer” for more detailed information concerning the exchange offer.

7

Terms of the exchange notes

The following summary contains basic information about the exchange notes and is not intended to be complete. It does not contain all the information that is important to you. For a more complete understanding of the exchange notes, please refer to the section of this prospectus entitled “Description of the exchange notes.”

| Issuers | | Morris Publishing Group, LLC and Morris Publishing Finance Co. |

| |

| Securities offered | | $300,000,000 aggregate principal amount of 7% senior subordinated notes due 2013. |

| |

| Maturity date | | August 1, 2013. |

| |

| Interest rate | | 7% per year. |

| |

| Interest payment dates | | February 1 and August 1 of each year, beginning on February 1, 2004. |

| |

| Guarantees | | Each of our existing and future restricted subsidiaries, other than the co-issuer Morris Publishing Finance Co., will jointly, severally and unconditionally guarantee the notes on a senior subordinated basis. |

| |

| Ranking | | The exchange notes will be our unsecured senior subordinated obligations and will be subordinated to all of our existing and future senior debt, including secured indebtedness under our new credit facilities, rank equally with all of our existing and future senior subordinated debt and rank senior to all of our future subordinated debt. |

| |

| | | The guarantees by our restricted subsidiaries will be subordinated to existing and future senior debt of such subsidiaries, including each such subsidiary’s guarantee of the indebtedness under our new credit facilities. The guarantees will rank equally with all of the guarantors’ existing and future senior subordinated debt, and rank senior to all of the guarantors’ future subordinated debt. The notes will be effectively subordinated to all of our and our subsidiaries existing and future secured debt to the extent of the value of collateral securing each debt. The notes will be effectively subordinated to all existing and future liabilities, including trade payables, of any subsidiary that is not a guarantor. |

8

| | | As of September 30, 2003, after giving effect to our new credit facilities and the sale of the notes and the application of the proceeds therefrom, the notes and the subsidiary guarantees would have been subordinated to $244.0 million of senior debt, not including $156.0 million of additional borrowing capacity we expect to have available under our new credit facilities. |

| |

| Optional redemption | | We may redeem some or all of the notes at any time on or after August 1, 2008. We may also redeem up to 35% of the aggregate principal amount of the notes using the proceeds of certain public equity offerings on or before August 1, 2006. The redemption prices are described under “Description of the exchange notes — Redemption.” |

| |

| Change of control and asset sales | | If we experience specific kinds of changes of control or we sell assets under certain circumstances, we will be required to make an offer to purchase the notes at the prices listed in “Description of the exchange notes — Redemption.” We may not have sufficient funds available at the time of any change of control, to effect the purchase. |

| |

| Certain covenants | | The indenture restricts our ability and the ability of our restricted subsidiaries to, among other things: |

| |

| | | · incur additional debt and issue preferred stock; |

| |

| | | · make certain distributions, investments and other restricted payments; |

| |

| | | · create certain liens; |

| |

| | | · enter into transactions with affiliates; |

| |

| | | · limit the ability of restricted subsidiaries to make payments to us; |

| |

| | | · merge, consolidate or sell substantially all of our assets; |

| |

| | | · issue preferred stock of a restricted subsidiary; |

| |

| | | · sell certain assets; and |

| |

| | | · enter into new lines of business. |

9

| | |

| | | These covenants are subject to important exceptions and qualifications, which are described under the heading ”Description of the exchange notes” in this offering memorandum. |

| |

| Exchange offer; registration rights | | Under registration rights agreements with the initial purchasers, we and the guarantors agreed to use our reasonable best efforts to cause to become effective a registration statement with respect to an offer to exchange the notes for the exchange notes. If we are not able to effect the exchange offer, we will use our commercially reasonable efforts to file and cause to become effective a shelf registration statement relating to resales of the notes. We will be obligated to pay additional interest on the notes if we do not complete the exchange by May 3, 2004 or, if required, the shelf registration statement is not declared effective by May 3, 2004. |

Risk factors. See “Risk factors” on page 14 of this prospectus for a discussion of certain factors that you should carefully consider before investing in the notes.

10

Summary historical financial data

The summary historical financial data of Morris Publishing set forth below should be read in conjunction with our combined financial statements, including the notes thereto, and “Management’s discussion and analysis of financial condition and results of operations” included elsewhere in this prospectus. The combined statement of income and other operating and financial information data for each of the years ended December 31, 2002, 2001 and 2000 and the combined balance sheet data as of December 31, 2002 and 2001 are derived from our audited combined financial statements included elsewhere in this prospectus . We do not have audited financial statements for the years ended December 31, 1999 or 1998 and, therefore, the combined statement of income and other operating and financial information data for the years ended December 31, 1999 and 1998 and the combined balance sheet data as of December 31, 2000, 1999 and 1998 are derived from our unaudited combined financial statements. See “Risk factors.” Net cash flow information for 1999 and 1998 is not available. The combined statement of income and other operating and financial information data for the nine months ended September 30, 2003 and 2002 and the combined balance sheet data as of September 30, 2003 are derived from our unaudited combined financial statements. In our opinion, the information as of September 30, 2003 and for the nine months ended September 30, 2003 and 2002 reflects all adjustments, consisting only of normal and recurring adjustments, necessary to fairly present the results of operations and financial condition. Results for interim periods should not be considered indicative of results for any other periods.

Morris Publishing was formed in late 2001 as part of a corporate reorganization of our parent, Morris Communications and, therefore, does not have a recent operating history as an independent company. Our historical combined financial statements contained in this prospectus reflect periods during which we did not operate as an independent company. See Note 1 to Notes to Combined Financial Statements.

The financial information we have included in this prospectus reflects the historical results of operations and cash flows of Morris Publishing with allocations made for corporate and other services provided to us by Morris Communications. Operating costs and expenses reflect our direct costs together with certain allocations by Morris Communications for corporate services, debt and other shared services that have been charged to us based on usage or other methodologies we believe are appropriate for such expenses. In the opinion of management, these allocations have been made on a reasonable basis and approximate all the material incremental costs we would have incurred had we been operating on a stand-alone basis; however, there has been no independent study or any attempt to obtain quotes from third parties to determine what the costs of obtaining such services would have been.

11

| | |

| | | Nine months ended

September 30,

| | | Year ended December 31,

| |

(Dollars in thousands)

| | 2003

| | | 2002

| | | 2002

| | | 2001

| | | 2000

| | | 1999

| | | 1998

| |

| | | | |

Combined statement of income data | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Operating revenues: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Advertising | | $ | 255,889 | | | $ | 251,432 | | | $ | 342,976 | | | $ | 341,947 | | | $ | 356,825 | | | $ | 341,733 | | | $ | 329,257 | |

Circulation | | | 53,504 | | | | 53,897 | | | | 71,906 | | | | 74,756 | | | | 76,492 | | | | 77,079 | | | | 77,713 | |

Other | | | 13,529 | | | | 13,643 | | | | 18,480 | | | | 20,781 | | | | 22,098 | | | | 25,079 | | | | 22,510 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Total operating revenues | | | 322,922 | | | | 318,972 | | | | 433,362 | | | | 437,484 | | | | 455,415 | | | | 443,891 | | | | 429,480 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Operating expenses: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Labor and employee benefits | | | 127,363 | | | | 118,817 | | | | 162,540 | | | | 163,097 | | | | 161,189 | | | | 153,364 | | | | 142,393 | |

Newsprint, ink and supplements | | | 37,616 | | | | 36,254 | | | | 48,815 | | | | 62,193 | | | | 66,431 | | | | 61,599 | | | | 66,200 | |

Other operating costs | | | 82,627 | | | | 77,254 | | | | 110,059 | | | | 106,219 | | | | 113,029 | | | | 108,369 | | | | 106,431 | |

Depreciation and amortization | | | 11,042 | | | | 13,538 | | | | 18,129 | | | | 31,817 | | | | 31,762 | | | | 30,419 | | | | 29,794 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Total operating expenses | | | 258,648 | | | | 245,863 | | | | 339,543 | | | | 363,326 | | | | 372,411 | | | | 353,751 | | | | 344,818 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Operating income | | | 64,274 | | | | 73,109 | | | | 93,819 | | | | 74,158 | | | | 83,004 | | | | 90,140 | | | | 84,662 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Other expense (income): | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Interest expense, including amortization of debt issuance costs | | | 18,164 | | | | 19,350 | | | | 25,056 | | | | 33,424 | | | | 45,230 | | | | 37,737 | | | | 37,181 | |

Loss on extinguishment of debt | | | 5,957 | | | | — | | | | — | | | | 1,578 | | | | — | | | | — | | | | — | |

Other, net | | | 172 | | | | 137 | | | | 187 | | | | 286 | | | | (103 | ) | | | (266 | ) | | | (344 | ) |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Total other expenses | | | 24,293 | | | | 19,487 | | | | 25,243 | | | | 35,288 | | | | 45,127 | | | | 37,471 | | | | 36,837 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Income before income taxes and minority interest | | | 39,981 | | | | 53,622 | | | | 68,576 | | | | 38,870 | | | | 37,877 | | | | 52,669 | | | | 47,825 | |

Provision for income taxes | | | 15,400 | | | | 20,859 | | | | 26,897 | | | | 16,890 | | | | 17,619 | | | | 23,213 | | | | 20,409 | |

Minority interest, net | | | — | | | | — | | | | — | | | | — | | | | 282 | | | | 400 | | | | 305 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Net income | | $ | 24,581 | | | $ | 32,763 | | | $ | 41,679 | | | $ | 21,980 | | | $ | 19,976 | | | $ | 29,056 | | | $ | 27,111 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Combined balance sheet data at period end | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total assets | | $ | 501,646 | | | | — | | | $ | 480,370 | | | $ | 483,705 | | | $ | 489,763 | | | $ | 495,049 | | | $ | 517,432 | |

Goodwill and other intangibles | | | 259,108 | | | | — | | | | 258,763 | | | | 258,389 | | | | 265,036 | | | | 274,745 | | | | 285,639 | |

Total long-term debt and capital lease obligations | | | 544,000 | | | | — | | | | 516,000 | | | | 538,046 | | | | 566,128 | | | | 544,627 | | | | 582,537 | |

Member’s deficit | | | (134,090 | ) | | | — | | | | (114,013 | ) | | | (129,514 | ) | | | (158,926 | ) | | | (142,909 | ) | | | (155,245 | ) |

| | | | | | | |

Other operating and financial information data | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

EBITDA (a) | | $ | 69,163 | | | $ | 86,494 | | | $ | 111,740 | | | $ | 104,079 | | | $ | 114,196 | | | $ | 120,140 | | | $ | 114,215 | |

EBITDA margin (b) | | | 21.4 | % | | | 27.1 | % | | | 25.8 | % | | | 23.8 | % | | | 25.1 | % | | | 27.1 | % | | | 26.6 | % |

Earnings to fixed charges (c) (g) | | | 3.1 | x | | | (f | ) | | | 3.7 | x | | | 2.1 | x | | | 1.8 | x | | | (f | ) | | | (f | ) |

Net cash flows provided by (used in): | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Operating activities | | | 53,841 | | | | 53,757 | | | | 64,789 | | | | 60,836 | | | | 44,897 | | | | (f | ) | | | (f | ) |

Investing activities | | | (25,725 | ) | | | (17,647 | ) | | | (16,757 | ) | | | (36,864 | ) | | | (35,409 | ) | | | (f | ) | | | (f | ) |

Financing activities | | | (25,915 | ) | | | (35,053 | ) | | | (48,224 | ) | | | (27,644 | ) | | | (14,492 | ) | | | (f | ) | | | (f | ) |

Total long-term debt / EBITDA (g) | | | 5.8 | x (d) | | | (f | ) | | | 4.6 | x | | | 5.2 | x | | | 5.0 | x | | | 4.5 | x | | | 5.1 | x |

EBITDA / Interest expense, including amortization of debt issuance costs (g) | | | 4.1 | x (e) | | | (f | ) | | | 4.5 | x | | | 3.1 | x | | | 2.5 | x | | | 3.2 | x | | | 3.1 | x |

| (a) | | Earnings before net interest expense, including amortization of debt issuance costs, provision for income taxes, depreciation and amortization expense (“EBITDA”) is not a measure of performance defined in accordance with accounting principles generally accepted in the United States of America. However, we believe that EBITDA is useful to investors in evaluating our performance because it is a commonly used financial analysis tool for measuring and comparing media companies in areas of operating performance and is a measure of income available to pay interest expense. EBITDA should not be considered as an |

12

| | alternative to net income as an indicator of our performance or as an alternative to net cash provided by operating activities as a measure of liquidity and may not be comparable to similarly titled measures used by other companies. |

The following table reconciles net income to EBITDA:

| | | |

| | | Nine months

ended September 30,

| | | | | Year ended December 31,

| |

(Dollars in thousands)

| | 2003

| | | 2002

| | | | | 2002

| | | 2001

| | | 2000

| | | 1999

| | | 1998

| |

Net income | | $ | 24,581 | | | $ | 32,763 | | | | | $ | 41,679 | | | $ | 21,980 | | | $ | 19,976 | | | $ | 29,056 | | | $ | 27,111 | |

Add: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Interest expense | | | 18,164 | | | | 19,350 | | | | | | 25,056 | | | | 33,424 | | | | 45,230 | | | | 37,737 | | | | 37,181 | |

Interest income | | | (24 | ) | | | (16 | ) | | | | | (21 | ) | | | (32 | ) | | | (391 | ) | | | (285 | ) | | | (280 | ) |

Provision for income taxes | | | 15,400 | | | | 20,859 | | | | | | 26,897 | | | | 16,890 | | | | 17,619 | | | | 23,213 | | | | 20,409 | |

Depreciation and amortization expense | | | 11,042 | | | | 13,538 | | | | | | 18,129 | | | | 31,817 | | | | 31,762 | | | | 30,419 | | | | 29,794 | |

| | |

|

|

| |

|

|

| | | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

EBITDA | | $ | 69,163 | | | $ | 86,494 | | | | | $ | 111,740 | | | $ | 104,079 | | | $ | 114,196 | | | $ | 120,140 | | | $ | 114,215 | |

| | |

|

|

| |

|

|

| | | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | |

|

| (b) | | EBITDA Margin is EBITDA divided by total operating revenues. |

| (c) | | Earnings to fixed charges is defined as income before income taxes and minority interest plus fixed charges, divided by fixed charges. Fixed charges are interest expense including amortization of debt issuance costs, plus one-third of rent expense. |

| (d) | | Amounts shown for the nine months ended September 30, 2003 are based upon EBITDA for the twelve months ended September 30, 2003. This amount has been calculated based on EBITDA for the year ended December 31, 2002, plus EBITDA for the nine months ended September 30, 2003, less EBITDA for the nine months ended September 30, 2002. |

| (e) | | Amounts shown for the nine months ended September 30, 2003 are based upon EBITDA and interest expense, including amortization of debt issuance costs, for the twelve months ended September 30, 2003. These amounts have been calculated based on the EBITDA and interest expense, including amortization of debt issuance costs, for the year ended December 31, 2002, plus the related amounts for the nine months ended September 30, 2003, less the related amounts for the nine months ended September 30, 2002. |

| (g) | | Our interest expense would have increased by $6,287 and $6,391, respectively, for the nine months ended September 30, 2003 and the year ended December 31, 2002, assuming we had issued the notes at 7% per annum and the new credit facilities at the beginning of such periods, based on assumed interest rates. |

Resulting pro forma ratios would have been as follows:

| | |

| | | Nine months ended

September 30, 2003

| | Year ended

December 31, 2002

|

Pro forma earnings to fixed charges | | 2.6x | | 3.1x |

13

Risk factors

In deciding whether to participate in the exchange offer, you should carefully consider the risks described below, which could cause our operating results and financial condition to be materially adversely affected, as well as other information and data included in this prospectus.

Risks relating to our business and our industry

A decline in advertising revenue, our largest source of revenue, would adversely affect us.

A primary source of our revenue is advertising. For both 2002 and the nine months ending September 30, 2003, advertising revenues, which include retail, national and classified advertising revenues, constituted approximately 79% of our total operating revenues. A reduction in demand for advertising could result from:

| | · | | a general decline in economic conditions; |

| | · | | a decline in economic conditions in particular markets where we conduct business, and in particular the Jacksonville, Florida market where we derived approximately 30.6% of our revenues for the year ending December 31, 2002; |

| | · | | a decline in the circulation of our newspapers; |

| | · | | a decline in the popularity of our editorial content; |

| | · | | a change in the demographic makeup of the population where our newspapers are sold; |

| | · | | a decrease in the price of local and national advertising; |

| | · | | the activities of our competitors, including increased competition from other forms of advertising-based mediums, including local, regional and national newspapers, shoppers, radio and television broadcasters, cable television (national and local), direct mail and electronic media (including the internet); and |

| | · | | a decline in the amount spent on advertising in general. |

Our revenues are cyclical and may decrease due to an economic downturn.

Newspaper companies tend to follow a distinct and recurring seasonal pattern. The first quarter of the year tends to be the weakest quarter because advertising volume is then at its lowest level. Correspondingly, the fourth quarter tends to be the strongest quarter as it includes holiday season advertising. As a result, our combined results may not be comparable from quarter to quarter.

Our advertising revenues, as well as those of the newspaper industry in general, may be cyclical and dependent upon general economic conditions. We cannot assure you that the demand for our services will continue at current levels. The newspaper industry in general, like other media, has suffered from the continued downturn in the national economy. Historically advertising revenues have increased with the beginning of an economic recovery, principally with increases in classified advertising for employment, real estate and automobiles. Decreases in advertising revenues have historically corresponded with general economic downturns and regional and local recessionary conditions. While we believe that the geographic diversity of our operations mitigates, to some degree, the effects of regional and local economic downturns, a decline in the national economy generally may adversely affect our operating results.

14

A decline in circulation revenue would adversely affect us.

We also rely on circulation revenue, which is affected by, among other things, competition and consumer trends, including declining consumer spending on newspapers. Circulation is a significant source of our revenue. Circulation revenue and our ability to achieve price increases for our print products are affected by:

| | · | | competition from other publications and other forms of media available in our various markets, including network, cable and satellite television, the internet and radio; |

| | · | | declining consumer spending on discretionary items like newspapers; |

| | · | | competing uses of free time; and |

| | · | | declining number of regular newspaper buyers. |

Fluctuations in newsprint costs, or increases in labor or health care costs could adversely affect our financial results.

Newsprint, ink and supplements are the major components of our cost of raw materials. Newsprint, ink and supplements accounted for 11.3% and 14.2% of our total operating revenues in 2002 and 2001, respectively. Historically newsprint prices have fluctuated substantially. Accordingly, our earnings are sensitive to changes in newsprint prices. We have no long-term supply contracts and we have not attempted to hedge fluctuations in the normal purchases of newsprint or enter into contracts with embedded derivatives for the purchase of newsprint. If the price of newsprint increases materially, our operating results could be adversely affected. In addition, substantial increases in labor or health care costs could also affect our operating results.

Competition could have a material adverse effect on us.

Revenue generation in the newspaper industry is dependent primarily upon the sale of advertising and paid circulation. Competition and pricing are largely based on readership, market penetration, quality and servicing the specialized needs of advertisers and readers. Currently, our daily newspapers generally do not directly compete in their respective communities with other daily newspapers covering local news. Competition for advertising and circulation, however, also comes from regional and national newspapers, radio and television broadcast, cable television (national and local), non-daily newspapers, direct mail, electronic media (including the internet) and other communications and advertising media that operate in our markets. Certain of our competitors are larger and have greater financial resources than we have. The extent and nature of such competition is, in large part, determined by the location and demographics of the market and the number of media alternatives in those markets. For more information on our competition and factors that could affect our competitive position, see “Business—Competition.”

To remain competitive, we must constantly expand and develop new publications and services.

Our future success depends in part on our ability to continue offering new publications and services that successfully gain market acceptance by addressing the needs of specific audience groups within our target markets. The process of internally researching, developing, launching, gaining acceptance and establishing profitability for a new publication or service, is inherently risky and costly. We cannot assure you that our efforts to introduce new publications or services will be successful.

15

We are subject to legal proceedings that, if determined adversely to us, could adversely affect our financial results.

We are subject to legal proceedings that arise in the ordinary course of our business. We do not expect that the outcome of any pending legal proceedings will have a material adverse impact upon our business. However, the damages that may be claimed in these legal proceedings could be substantial, including claims for punitive or extraordinary damages. It is possible that, if the outcomes of these legal proceedings are not favorable to us, it could adversely affect our future financial results. In addition, our results of operations, financial condition or liquidity may be adversely affected if in the future our insurance coverage proves to be inadequate or unavailable or there is an increase in liabilities for which we are self-insured.

The interests of our parent, Morris Communications, and its ultimate owners, the Morris family, may be different than yours, and they may take actions that may be viewed as adversely affecting our business or the notes.

Morris Communications, its ultimate parent company, Shivers Trading & Operating Company, and the Morris family have interests in other businesses, including businesses which also derive revenue from advertising. There can be no assurance that Morris Communications or the Morris family will exercise control in our best interests as opposed to their own best interests.

Control

The Morris family, including William S. Morris III, our chairman, and his son, William S. Morris IV, our president and chief executive officer, beneficially own all of the equity interests in Morris Communications, our parent company, through their ownership of the stock of Shivers Trading & Operating Company. By virtue of such equity ownership, the Morris family has the sole power to:

| | · | | elect the entire board of directors of Shivers Trading & Operating Company, Morris Communications and each of their subsidiaries, including us; |

| | · | | control all of our management and policies, including as to the making of payments to Morris family members or other affiliates, whether by way of dividend, stock repurchase, compensation or otherwise or the entering into other transactions with Morris Communications, its subsidiaries or other affiliates, or other transactions that could result in a change of control of Morris Communications or Morris Publishing; and |

| | · | | determine the outcome of any corporate matter or transaction, including mergers, joint ventures, consolidations and asset sales, equity issuances or debt incurrences. |

Currently five of the six directors on the boards of directors of Shivers Trading & Operating Company, Morris Communications and each of their subsidiaries (including our board) are members of the Morris family and the sixth is Craig S. Mitchell who is also the Senior Vice President – Finance, Secretary and Treasurer of Shivers Trading & Operating Company, Morris Communications and each of their subsidiaries. Mr. Mitchell serves at the pleasure of the Morris family. None of these boards has a separate audit committee and will not necessarily have as a member a “financial expert” as defined under the rules of the Commission as a result of the Sarbanes-Oxley Act of 2002. We have been advised that the Morris family does not plan to appoint any non-family members to any such boards, other than the current single existing non-family member director, or any “independent” directors. No member of any such board of directors has been elected, or is anticipated to be elected, to represent the interests of the holders of the notes.

16

In addition, as private companies, Shivers Trading & Operating Company, Morris Communications and its subsidiaries, including Morris Publishing, have not been required to comply with the corporate governance or other provisions of the Sarbanes-Oxley Act or any of the corporate governance or other rules and regulations of any stock exchange or national stock quotation system. While Morris Publishing will become subject to certain provisions of the Sarbanes-Oxley Act when the exchange offer is completed, those provisions will not require Morris Publishing to have independent directors or an audit committee.

Because the Morris family’s interests as an equity holder may conflict with the interests of holders of the notes, Morris Communications may cause us to take actions that, in their judgment, could enhance their equity investment, even though such actions might involve risks to you as a holder of the notes.

While we have been advised that the Morris family has no intention to engage in a transaction that would lead to a change of control of Shivers Trading & Operating Company, Morris Communications or Morris Publishing, no assurances can be given that future events or other circumstances may arise that would lead to a possible change of control. Finally, the unavailability for any reason of the managerial services presently provided by the Morris family (particularly our chairman William S. Morris III and our chief executive officer William S. Morris IV) to Morris Publishing, could be disruptive to our business for some period of time.

Transactions with affiliates

Various entities which are affiliated with Morris Communications and the Morris family have engaged, and may in the future engage, in transactions with us some of which may be viewed, from the perspective of a holder of the notes, as significant. These transactions may not necessarily be consummated on an arm’s-length basis and therefore may not be as favorable to us as those that could be negotiated with non-affiliated third parties. See “Certain relationships and related transactions” for a description of such transactions and relationships that existed prior to the offering of the notes.

After giving effect to this offering, we will continue to engage in transactions with affiliates including the following:

| | · | | We are managed by Morris Communications pursuant to a management agreement and also participate in its Shared Services Center operated by its subsidiary, MStar Solutions, LLC. |

| | · | | Under the management agreement we share our home office facilities in Augusta, Georgia with Morris Communications. |

| | · | | In addition to the management services, we may share other facilities and costs with Morris Communications and its other subsidiaries. Shared costs may include joint promotions or the use of facilities, equipment, supplies or employees of one division for the benefit of an affiliate and the costs will be allocated among the various entities by Morris Communications. |

| | · | | Rental arrangements with a company controlled by Morris family members for the use of one of our Savannah, Georgia newspaper operations. |

| | · | | In the ordinary course of our business, we may sell goods and services to our affiliates, including newspaper advertising, on terms that we determine to be equivalent to arm’s-length transactions with unrelated third parties. |

17

| | · | | In the ordinary course of our business, we may purchase goods and services from our affiliates, such as radio or outdoor advertising and promotions, space in hotels owned by affiliates, or farm products from farms owned by affiliates, on terms that we determine to be equivalent to arm’s-length transactions with unrelated third parties. |

| | · | | We may provide loans to Morris Communications or its subsidiaries. Any such loans may utilize borrowing capacity under our new credit facilities that may otherwise have been available for our business purposes. It is expected that the principal external source of liquidity for Morris Communications and its other subsidiaries will be loans by or distributions from Morris Publishing. |

| | · | | We are a single member limited liability company that is disregarded for federal income tax purposes and we are part of the consolidated tax return of our ultimate parent corporation and its subsidiaries. We participate in a tax sharing agreement with our affiliates whereby we are required to pay to Morris Communications an amount equal to the taxes we would have been required to pay as if we were a separate taxable corporation. We may become jointly and severally liable for all income tax liability of the group in the event other subsidiaries are unable to pay the taxes attributable to their operations. |

For further discussion of transactions with affiliates, see “Certain relationships and related transactions.”

Conflicting business interests

Other subsidiaries of Morris Communications operate businesses that also derive revenue from advertising, including broadcast radio stations, outdoor advertising, magazines and specialized publications. These other subsidiaries may compete with us for advertising revenues.

Rules of the Federal Communications Commission, or FCC, limit the cross-ownership of a broadcast radio station and a newspaper in the same market. Morris Communications owns other subsidiaries which own radio broadcast licenses that are subject to regulation by the FCC. These subsidiaries currently hold, under waivers granted by the FCC, radio broadcast licenses in two of Morris Publishing’s newspaper markets: Amarillo, Texas and Topeka, Kansas. A subsidiary of Morris Communications has also received from the FCC a twelve month waiver to hold a radio broadcast license for a station it expects to acquire with a service contour that includes Newton, Kansas, which is also one of our newspaper markets. The FCC recently adopted ownership rules that would permit cross-ownership of a broadcast radio station and a newspaper in the same market in many instances, but these rules have been challenged in the U.S. Court of Appeals for the Third Circuit, which has stayed the rules’ effective date pending outcome of the litigation. Should the new rules become effective, we believe that the radio broadcast licenses held for these locations will be able to continue to be held without waivers. If, however, the court challenge seeking to overturn the rules is successful, or if Congress were to overturn the new ownership rules or to impose new limitations on newspaper-broadcast cross-ownership, Morris Communications and Morris Publishing might need to divest either their radio broadcast licenses for these markets or their newspaper interests in these markets. Further, FCC cross-ownership rules may have the effect of preventing us from pursuing or consummating a newspaper acquisition that our management would have otherwise pursued in markets in which Morris Communications owns radio stations.

18

If we fail to implement our business strategy, our business will be adversely affected.

Our future financial performance and success are dependent in large part upon our ability to successfully implement our business strategy. We cannot assure you that we will be able to successfully implement our business strategy or be able to improve our operating results. In particular, we cannot assure you that we will be able to maintain circulation of our publications, obtain new sources of advertising revenues, generate additional revenues by building on the brand names of our publications or raise the cover prices of our publications without causing a decline in circulation.

Implementation of our business strategy could be affected by a number of factors beyond our control, such as increased competition, general economic conditions, legal developments or increased operating costs or expenses. In particular, there has been a recent trend of increased consolidation among major retailers, including as a result of bankruptcies of certain retailers. This trend may adversely affect our results of operations by reducing the number of advertisers using our products and increasing the purchasing power of the consolidated retailers, thereby leading to a decline in our advertising revenues. Any failure by us to successfully implement our business strategy may adversely affect our ability to service our indebtedness, including our ability to make principal and interest payments on the notes. We may, in addition, decide to alter or discontinue certain aspects of our business strategy at any time.

Consolidation in the markets in which we operate could place us at a competitive disadvantage.

Recently, some of the markets in which we operate have experienced significant consolidation. In particular, the combinations of traditional media content companies and new media distribution companies have resulted in new business models and strategies. Should the revised ownership rules adopted by the FCC withstand court and Congressional challenges, they will increase the potential of consolidation for our sector. We cannot predict with certainty the extent to which these types of business combinations may occur or the impact that they may have. These combinations could potentially place us at a competitive disadvantage with respect to negotiations, sales, resources and our ability to develop and to take advantage of new media technologies.

We may pursue acquisitions, but we may not be able to identify attractive acquisition candidates, successfully integrate acquired operations or realize the intended benefits of our acquisitions and we may enter into joint ventures.

We may pursue growth in part through the acquisition of additional newspapers or certain other businesses and assets and we may enter into joint ventures. This strategy is subject to numerous risks, including:

| | · | | an inability to obtain sufficient financing to complete our acquisitions; |

| | · | | increases in purchase prices for newspaper assets due to increased competition for acquisition opportunities; |

| | · | | an inability to negotiate definitive purchase agreements on satisfactory terms; |

| | · | | difficulty in obtaining regulatory approval; |

| | · | | difficulty in integrating the operations, systems and management of acquired assets and absorbing the increased demands on our administrative, operational and financial resources; |

19

| | · | | the diversion of our management’s attention from their other responsibilities; |

| | · | | the loss of key employees following completion of our acquisitions; |

| | · | | the failure to realize the intended benefits of our acquisitions; |

| | · | | our being subject to unknown liabilities; and |

| | · | | participation in joint ventures may limit our access to the cash flow of assets contributed to the joint venture. |

Our inability to effectively address these risks could force us to revise our business plan, incur unanticipated expenses or forego additional opportunities for expansion.

The financial data presented in this prospectus for the years ended December 31, 1998 and 1999 have not been audited and we cannot assure you as to their comparability with respect to subsequent years that have been audited.

The only audited financial data available for the years ended December 31, 1998 and 1999 are for our parent, Morris Communications, which was formerly audited by Arthur Andersen LLP. We have not obtained audits of our business for the years ended December 31, 1998 and 1999. The unaudited financial information for the years ended December 31, 1998 and 1999 are based upon the financial records of the Morris Communications newspaper business segment and reflect certain adjustments and allocations that our management believes are reasonable. However, we cannot assure you that the financial data provided for the years ended December 31, 1998 and 1999 are comparable to subsequent years that have been audited.

We are subject to extensive environmental regulations.

We are subject to a variety of environmental laws and regulations concerning, among other things, emissions to the air, waste water and storm water discharges, handling, storage and disposal of wastes, recycling, remediation of contaminated sites, or otherwise relating to protection of the environment. Environmental laws and regulations and their interpretation have changed rapidly in recent years and may continue to do so in the future. Failure to comply with present or future requirements could result in material liability to us. Some environmental laws impose strict, and under certain circumstances joint and several, liability for costs of remediation of soil and groundwater contamination at our facilities or those where our wastes have been disposed. Our current and former properties may have had historic uses which may require investigation or remedial measures. We believe we are in substantial compliance with all applicable environmental requirements. However, we cannot guarantee that material costs and/or liabilities will not occur in the future including those which may arise from discovery of currently unknown conditions.

The new FTC Do Not Call rule will adversely effect our ability to sell newspaper subscriptions by telephone marketing.

We utilize telephone direct marketing efforts to maintain and increase our newspaper circulation. Pursuant to the Telemarketing and Consumer Fraud and Abuse Prevention Act, the Federal Trade Commission, or FTC, has issued the Telemarketing Sales Rule prohibiting a telemarketer from calling persons who have registered on the recently-created National Do Not Call Registry. As of October, 2003 the FTC, the Federal Communications Commission and state law enforcement officials may enforce violations. Once consumers register online or by

20

telephone with the registry, most telemarketers, generally other than those calling to solicit political or charitable contributions, will be required to remove telephone numbers on the registry from their call lists. Persons who have registered by August 31, 2003 must be removed from telemarketer lists by October 1, 2003 and covered telemarketers may not call persons who register after September 1, 2003 within three months of the date of registration. Thus, the issuance of the Telemarketing Sales Rule will limit our ability to engage in telephone marketing efforts.

Risks relating to the notes

Our substantial indebtedness could adversely affect our business and prevent us from fulfilling our obligations under the notes.

We have a substantial amount of indebtedness. As of September 30, 2003, we had $544.0 million of debt outstanding, consisting of approximately $244.0 million of senior debt and $300.0 million of senior subordinated notes. In addition, the indenture governing the notes and our new credit facilities allow us to incur substantial additional indebtedness in the future. As of September 30, 2003, we had $156.0 million available to borrow under our new credit facilities. Our substantial indebtedness may have important consequences to you, including:

| | · | | making it more difficult for us to satisfy our obligations with respect to the notes; |

| | · | | limiting cash flow available to fund our working capital, capital expenditures, potential acquisitions or other general corporate requirements; |

| | · | | increasing our vulnerability to general adverse economic and industry conditions; |

| | · | | limiting our ability to obtain additional financing to fund future working capital, capital expenditures, potential acquisitions or other general corporate requirements; |

| | · | | limiting our flexibility in planning for, or reacting to, changes in our business and industry; |

| | · | | placing us at a competitive disadvantage compared to our competitors with less indebtedness; and |

| | · | | making it more difficult for us to comply with financial covenants in our new credit facilities. |

We may be unable to generate sufficient cash flow to satisfy our debt service obligations.