February 28, 2011

Via EDGAR (Correspondence)

U.S. Securities and Exchange Commission

Division of Corporate Finance

100 F Street, N.E.

Washington, D.C. 20549

Attention: Mr. Kevin W. Vaughn, Accounting Branch Chief

Re: CORPBANCA

Form 20-F for the Fiscal Year Ended December 31, 2009

Filed June 30, 2010

File No. 001-32305

Dear Mr. Vaughn:

We are submitting this letter in response to the written comments sent by the staff (the “Staff”) of the United States Securities and Exchange Commission (the “SEC”) contained in the letter dated February 17, 2011 (the “Comment Letter”) as a result of the letter submitted before the SEC, on November 29, 2010 (the “Response Letter”), by CorpBanca (the “Company”), regarding the letter issued by the SEC dated September 24, 2010 with respect to the annual report Form 20-F for the fiscal year ended December 31, 2009 (No. 001-32305) (the “Form 20-F”) filed on June 30, 2010 by the Company.

Certain of the Staff’s comments call for explanation of, or supplemental information as to, various matters relating to disclosures provided in the Form 20-F and the Response Letter. Responses to these comments are set forth in this letter.

For your convenience, our responses are set forth below, with the headings and numbered items of this letter corresponding to the headings and numbered items contained in the Comment Letter. For the convenience of the Staff, each of the comments from the Comment Letter is restated in bold italics prior to the Company’s response. Capitalized terms used but not defined in this letter shall have the respective meanings given to such terms in the Form 20-F. All page number references in the Company’s responses are to page numbers in the Form 20-F.

Form 20-F for the Fiscal Year Ended December 31, 2009

Loan portfolio, page 49

| 1. | We note your response to comment 3 in your letter dated November 29, 2010. Please revise your proposed disclosure to clarify how you “bring into play their allowances” and how that results in a concession. |

We acknowledge the Staff’s comment and as requested we hereby explain that what we meant by “bring into play their allowances” is that we bring into play the re-estimation of expected losses and focus on improving collections. As mentioned in our Response Letter, an important part of our renegotiation process is to have a complete view of the borrower’s situation, which includes evaluating the loan to value ratio.

Page 2

We also propose to add the following discussion on page 49 of Form 20-F:

“We use several types of concessions, frequently used in the market, to renegotiate our loans, including but no limited to, payment extensions, new operations or external refinancing to reduce the probability of losing the amount of the loan that the client has with us and improve collections.”

Models Based on Group Analysis, page 58

| 2. | We note your response to comments 4 and 6 in your letter dated November 29, 2010. |

| a) | Please tell us the loss emergence periods for each significant type and tell us how that period is incorporated in your allowance for loan loss methodology. |

We respectfully advise the Staff that, local regulation provides for a provision and allowance for credit losses based on “probable losses” notion which indicates that despite the borrower’s performing or non-performing status, the credit exposure should be provisioned based on its probable losses. This means that the loss emergence periods or the time that a delinquent loan could not be written off, is not relevant for provisioning purposes. Local regulation focuses the loss emergence period on the nature of the borrower, the loan and the collateral. Accordingly, consumer loans are 180 days, non-secured commercial loans are 24 months, secured commercial loans are 36 months and mortgage-backed loans are 48 months.

| b) | Please tell us how different loss emergence periods impact the provision formula disclosed in response 4c. |

We respectfully advise the Staff that the provision formula (based on probable losses) provided in the Response Letter under section 4c, is only applied to loans treated on a commercial individual basis model (loans over Ch$200 million). Therefore, the loss emergence period is not relevant in the formula.

| c) | Please tell us the definition of default importance as used in response 4c. |

We respectfully advise the Staff that “default importance” as used in the Response Letter under section 4c refers to the Loss Given Default.

d) Please tell us how you incorporate the fairly long term triggers to write off a loan (24-48 months) in your allowance methodology. Specifically discuss how you reconcile this long charge-off methodology with the fact that you only use a one year historical default period in your methodology.

We respectfully inform the Staff that in the commercial portfolio the default probability is estimated by using a 12 month forward period. Consequently, the default probability represents the probability of a non-deteriorated client moving to a deteriorated category (G5 or higher). Conversely, Loss Given Default is estimated by using a 36 month forward period, covering both products with 24 and 36 month write off periods. Mortgage loans’ LGS –with a longer write off period- are estimated by using different methodologies. As mentioned in the Response Letter, an allowance methodology is based on probable losses. The write-off policy is provided by the regulator.

Page 3

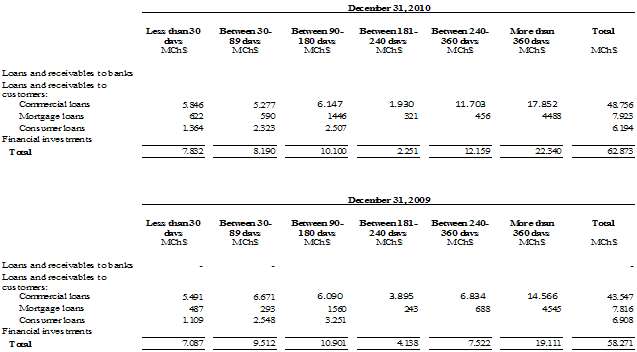

| 3. | We note your response to comment 6 in your letter dated November 29, 2010. In light of your charge-off periods ranging up to 48 months, please revise your proposed disclosure to include additional granularity related to the “more than 89 days” amount. |

We acknowledge the Staff’s comment and have amended the discussion proposed for page 75 on the Form 20-F in the Response Letter in order to provide for greater detail regarding the “more than 89 days” amount to read as follows:

“The following tables set forth the aging of our past due loans:

Provision for Loan Losses, page 78

| 4. | We note your response to comment 7 in your letter dated November 29, 2010. Your response does not appear to quantify the impact of each disclosed factor in the increase in your provision, nor did you indicate you would revise disclosure in future filings. Therefore, we again ask you to quantify the significant factors that led to the significant increase in your provision and to revise future filings accordingly. |

In response to the Staff’s comment, to accurately quantify in detail the impact of the salmon industry crisis within our portfolio, below is a table which contains details of the provision for loan losses for this sector.

Page 4

| Client (salmon sector) | Total Loans 2009 (Ch$M ) | Provision for loan losses in 2009 (Ch$M) | |||||

| SALMONES MULTIEXPORT S.A. | 9,400 | 2,277 | |||||

| INVERTEC PESQUERA MAR DE CHILOE S.A. | 10,190 | 3,872 | |||||

| CULTIVOS YADRAN S.A. | 7,130 | 1,640 | |||||

| CULTIVOS MARINOS CHILOE S.A. | 8,320 | 1,248 | |||||

| AUSTRALIS MAR S.A. | 5,102 | 0 | |||||

| EMPRESAS AQUACHILE S.A. | 4,383 | 1,008 | |||||

| SALMOFOOD S.A. | 1,410 | 324 | |||||

| SALMONES FRIOSUR S.A. | 2,577 | 31 | |||||

| SALMONES CHILOE S.A. | 2,475 | 599 | |||||

| PISCICULTURA AQUASAN S.A. | 1,524 | -1 | |||||

| SALMONES MAULLIN LIMITADA | 2,320 | 534 | |||||

| TRUSAL S.A. | 2,152 | 495 | |||||

| SERVICIOS DE ACUICULTURA ACUIMAG S.A. | 1,276 | 16 | |||||

| AUSTRAL FOOD S.A. | 740 | 185 | |||||

| PIGMENTOS NATURALES S.A. | 806 | 10 | |||||

| Total | 59,804 | 12,237 | |||||

Pursuant to the information filed by the Company before the SBIF, the provision for loan losses for 2008 and 2009 was Ch$56,561 million, and Ch$ 68,855 million, respectively. Almost the entire increased amount is explained by the provision for loan losses related to the salmon industry. In future filings we will include a specific disclosure similar to the one mentioned above, if a comparable situation occurs again.

Financial Statements

Consolidated Statements of Income, page F-4

| 5. | We note your response to comment 11 in your letter dated November 29, 2010. Please revise your subtotals that include “operating income” to more accurately and transparently describe the amounts reflected in those subtotals. For example, consider revising “operating income before loan losses” to something similar to “operating income, net of interest expense and expenses from service fees, before loan losses” since this subtotal includes certain expenses and is not simply gross operating income. Alternatively, discontinue the use of “operating income” where certain expenses are included in the subtotal. |

We acknowledge the Staff’s comment and have amended the discussion to include the following changes in the presentation of our financial statements.

Page 5

| Current Presentation | Suggested Presentation | |

| Interest income | Interest income | |

| Interest expense | Interest expense | |

| Net interest income | Net interest income | |

| Fees and income from services | Income from service fees | |

| Expenses from services | Expenses from service fees | |

| Fees and income from services, net | Net service fee income | |

| Trading and investment income, net | Trading and investment income, net | |

| Foreign exchange gains (losses), net | Foreign exchange gains (losses), net | |

| Other operating income | Other operating income | |

| Trading and investment, foreign exchange gains and other operating income | ||

| Operating income | Operating income before loan losses | |

| Provisions for loan losses | Provisions for loan losses | |

| Net Operating Income | Total Operating income, net of loan losses, interest, and fees | |

| Personnel salaries expenses | Personnel salaries expenses | |

| Administration expenses | Administration expenses | |

| Depreciation and amortization | Depreciation and amortization | |

| Impairment | Impairment | |

| Other operating expenses | Other operating expenses | |

| Total Operating Expenses | Total Operating Expenses | |

| Net Operating Income | Total Net Operating Income | |

| Income attributable to investments in other companies | Income attributable to investments in other companies | |

| Income before income taxes | Income before income taxes | |

| Income taxes | Income taxes | |

| Net income for the year | Net income for the year | |

Note 2 – First Time Adoption of Financial International Reporting Standards

Main changes to the accounting policies, page F-34

Page 6

| 6. | We note your response to comments 19 and 22 in your letter dated November 29, 2010. Please clarify whether you actually adjusted the amount of your allowance for loan losses at December 31, 2008 and 2009 as presented in the financial statements included in your December 31, 2009 Form 20-F or whether you simply changed your methodology to an IFRS complaint version going forward. If you did adjustments to the amounts recorded, please explain to us where the adjustment is presented in the reconciliations of the financial statements disclosed in Note 2d starting on page F-37 |

We respectfully advise the Staff that we did not adjust our allowance for loan losses. Instead, we changed our allowance for loan loss methodology to an IFRS compliant version going forward.

b. Main changes to the accounting policies – 8. price-level restatement, page F-35

| 7. | We note your response to comment 21 in your letter dated November 29, 2010. Please revise future filings to include the information included in your response in the final paragraph explaining why you did not reverse the price-level restatement for paid-in-capital |

We acknowledge the Staff’s Comments and in future filings we will add an explanatory note to our Statements of Changes in Shareholders Equity stating that the December 31, 2008 paid-in-capital balance includes price-level restatement adjustments that have not been reversed due to compliance with local regulations.

In future filings, we propose to include the following discussion as an explanatory note on our Statements of Changes in Shareholders Equity on our 2010 Form 20-F:

“The December 31, 2008 paid-in-capital balance includes price-level restatement adjustments that were not reversed when we adopted IFRS in 2009. We elected not to reverse such price-level restatement adjustments based on SVS Circular N°456 which indicates that the impact of deflation shall apply to paid-in-capital accounts as paid-in-capital accounts during the transition period to IFRS accounting is set forth in the Company’s bylaws, which were amended based on the distribution of the revalued equity and approved at the annual shareholder’s meeting held pursuant to Article 10, section 2 of Chile Law N°18.046 Sociedades Anónimas.”

Page 7

We thank you for your prompt attention to this letter responding to the Comment Letter and look forward to hearing from you at your earliest convenience. Please direct any questions concerning this response to the undersigned at Rosario Norte 660, 10th floor, Las Condes, Santiago - Chile.

Yours truly,

/s/ John Paul Fischer

John Paul Fischer

Head of Investor Relations.

Tel: 562-660 2141

john.fischer@corpbanca.cl

c.c. Mr. Michael C. Volley

Mr. Howard M. Kleinman

Dechert LLP

Tel. 212-698-3567

howard.kleinman@dechert.com