UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________________________________

FORM 6-K

REPORT OF FOREIGN ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16 OF THE

SECURITIES EXCHANGE ACT OF 1934

For the month of June 2013

(Commission File No. 001-32305)

________________________________

CORPBANCA

(Translation of registrant’s name into English)

________________________________

Rosario Norte 660

Las Condes

Santiago, Chile

(Address of registrant’s principal executive office)

________________________________

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Form 20-F x | Form 40-F o |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101 (b) (1):

Yes o | No x |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101 (b) (7):

Yes o | No x |

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes o | No x |

INFORMATION CONTAINED IN THIS FORM 6-K REPORT

Attached to this report on Form 6-K as Exhibit 99.1 is our press release dated June 4, 2013, announcing our consolidated financial results for the first quarter ended March 31, 2013.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereto duly authorized.

| CORPBANCA | ||

| (Registrant) | ||

| By: | /s/ Eugenio Gigogne | |

| Name: | Eugenio Gigogne | |

| Title: | Chief Financial Officer | |

Date: June 10, 2013

EXHIBIT INDEX

| Exhibit | Description | |

| 99.1 | Press release dated June 4, 2013. |

Exhibit 99.1

CorpBanca Announces

First Quarter 2013 Financial Report

Santiago, Chile, June 4, 2013. CORPBANCA (NYSE:BCA; BCS: CORPBANCA), a Chilean financial institution offering a wide variety of corporate and retail financial products and services, today announced its financial results for the first quarter ended March 31, 2013. This report is based on unaudited consolidated financial statements prepared in accordance with Chilean generally accepted accounting principles. Solely for the convenience of the reader, U.S. dollar amounts in this report have been translated from Chilean nominal pesos at our internal exchange rate as of March 31, 2013 of Ch$471.89 per U.S. dollar. Industry data contained herein has been obtained from the information provided by the Superintendency of Banks and Financial Institutions (“SBIF”).

Financial Highlights In 1Q 2013, Net Income attributable to shareholders totaled Ch$28,839 million (Ch$0.085 per share and US$0.269 per ADR), resulting in a 22.4% increase when compared to 1Q 2012 (YoY) and a 22.2% decreased when compared to 4Q 2012 (QoQ). The QoQ decline mainly reflects a lower inflation rate (measured as the variation of the UF) in the period: 0.13% in 1Q 2013 vs. 1.11% in 4Q 2012. Total loans (excluding interbank and contingent loans) reached Ch$10,094 billion as of March 31, 2013, allowing CorpBanca to achieve a market share of 9.9%, an increase of 191.6bp YoY and a decrease of 21.2bp QoQ. CorpBanca continues to be the fourth largest private bank in Chile in terms of loans and deposits. During 1Q 2013: Net operating profit decreased by 13.5% QoQ and increase 41.4% YoY; Net provisions for loan losses increase by 83.4% QoQ and 56.5% YoY; and Total operating expenses decrease by 18.4% QoQ and 52.5% YoY. | Mr. Fernando Massú, CEO In connection with Helm Bank acquisition, in 1Q 2013 CorpBanca raises more than US$620 million in new capital. Approximately 26% of the capital increase was successfully placed in the international market (~8x oversubscription), which resulted in new shareholders from the United States, England and Brazil. CorpBanca’s CEO, Fernando Massú, indicated that “the successfull international placement together with a massive subscription of preemptive rights (99%) is a testament to the confidence our shareholders have in the bank’s achievements during the last few years and its growth plans. This is further evidenced by high-demand by local and foreign investors’ interest in becoming a part of our expansion project.” The capital increase also involved the joining of strategic and long-term shareholders to CorpBanca’s ownership structure: International Finance Corporation (IFC) –member of the World Bank Group– subscribed and paid for a total amount of approximately US$225 million and Santo Domingo Group also increased its ownership in CorpBanca’s equity to 2.9%. |

Press Release

June 4, 2013

Page 2 / 21

General Information

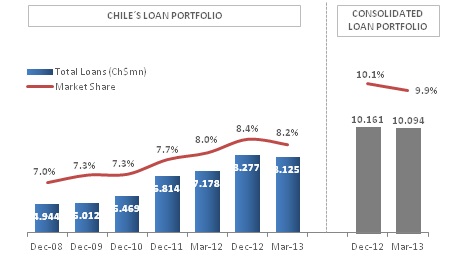

Market Share

| Our loan portfolio (excluding loans to banks) has grown at a compounded annual growth rate in nominal terms of 26.6% between December 31, 2009 and December 31, 2012. As of March 31, 2013, according to the SBIF, we were the fourth largest private bank in Chile in terms of the overall size of our loan portfolio (9.9% market share on a consolidated basis and 8.2% market share on an unconsolidated basis only taking into account our operations in Chile). |

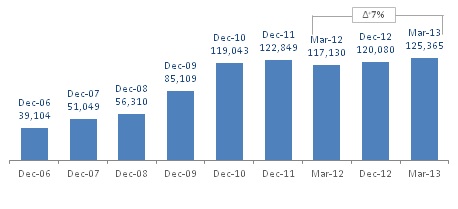

Net Income (12 months trailing in millions of Chilean pesos)

| Net Income for 1Q 2013 was Ch$28.8 billion. The chart shows the trend in our 12 months trailing Net Income from December 31, 2006 to March 31, 2013. During that period, our Net Income for the 12 months trailing March 31, 2013 was the highest we have ever earned. |

Press Release

June 4, 2013

Page 3 / 21

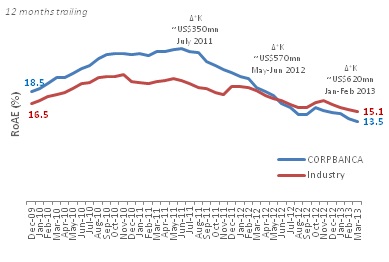

RoAE – RoAA

| We have achieved an average annual return on equity (RoAE*) of 20.1% between 2009 and 2012. Our three capital increases raised between 2011 and 2013 to fulfill our organic growth in Chile and our acquisition in Colombia –for a total amount of US$1,570 million approximately (+137.1%)– had impacted our RoAE since the third quarter 2011. * Equity: Average equity attributable to shareholders excluding net income and accrual for mandatory dividends. The increase in our corporate loans (with lower risk profiles and lower spreads than in our retail loans in 2011 and beginning of 2012); the accrual of Banco Santander Colombia’s Net Income for half of 2012; and the lower inflation rate observed in 2012 and YTD 2013 have also impacted our RoAA. The bank’s performance in 1Q 2013 was favorable considering the impact of the lower inflation in the Chilean banking system results. CorpBanca’s business diversification is being reflected in more stable revenues than peers since mid 2012. |

|

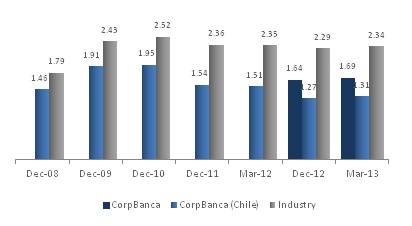

Risk Index (Loan loss allowances / Total loans)

| Consistent with one of our core strategies, CorpBanca has one of the lowest risk indexes (Loan loss allowances / Total loans) in the industry. Specifically, as of March 31, 2013, CorpBanca had the lowest risk index in its Chilean loan portfolio (1.3%) and the second lowest on a consolidated basis (1.7%) among the top eight Chilean banks representing more than 90% of market share in terms of total loans according to the SBIF. |

Press Release

June 4, 2013

Page 4 / 21

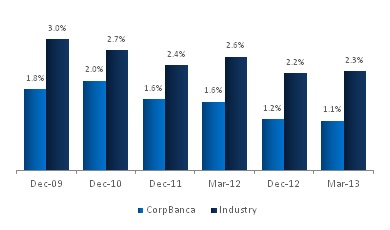

NPL (%)

| CorpBanca´s high asset quality has been maintained after the acquisition of Banco Santander Colombia which took place in May 2012. The chart illustrates how our consolidated NPL ratio continues to be better than the industry average in Chile. We believe that we have a risk management system that enables us to identify risks and resolve potential problems on a timely basis and we have made a series of investments to improve the technology we use to manage risk. We have also employed our risk management system and philosophy to identify potential acquisition targets with high asset quality. |

BIS Ratio (%) – TIER I (%)

| The increase of capital during 1Q 2013 reversed the decreasing trend in our BIS ratio during 2Q and 3Q 2012. After the incorporation of Helm Bank’s RWA and the goodwill deduction our BIS Ratio should be well above 13.0%. |

Press Release

June 4, 2013

Page 5 / 21

Branches – ATM – Headcount

| Our distribution network in Chile provides integrated financial services and products to our customers through several diverse channels, including ATMs, branches, internet banking and telephone banking. As of March 31, 2013, we operated 122 branch offices in Chile, which includes 66 branches operating as CorpBanca and 56 branches operating as Banco Condell, our consumer finance division. In addition, as of March 31, 2013, we owned and operated 464 ATMs in Chile, and our customers have access to over 9,313 ATMs (including BancoEstado’s ATMs) in Chile through our agreement with Redbanc S.A., or Redbanc. We utilize a number of different sales channels including account executives, telemarketing and the internet to attract new clients. Our branch system serves as the main distribution network for our full range of products and services. CorpBanca Colombia’s distribution channel also provides integrated financial services and products to its customers in Colombia through several diverse channels, including ATMs, branches, internet banking and telephone banking. As of March 31, 2013, CorpBanca Colombia operated 87 branch offices in Colombia and owned and operated 114 ATMs in Colombia, but providing its customers with access to over 12,280 ATMs through Colombia’s financial institutions. CorpBanca Colombia utilizes a number of different sales channels including account executives, telemarketing and the internet to attract new clients. CorpBanca Colombia’s branch system serves as the main distribution network for its full range of products and services. As of March 31, 2013, on a consolidated basis we had a headcount of 3,664 employees in Chile, 1,608 employees in Colombia and 23 employees in the United States. |

| |

|

Press Release

June 4, 2013

Page 6 / 21

Management’s Discussion and Analysis

I) Consolidated Financial Performance Review

Our consolidated Net Income attributable to shareholders reported on our consolidated financial statement in 1Q 2013 was Ch$28,839 million, a 22.4% or Ch$5,285 increase from Ch$23,554 million in 1Q 2012 and a 22.2% or Ch$8,226 million decrease from Ch$37,065 million in 4Q 2012. CorpBanca reached these revenues in 1Q 2013 in a highly competitive scenario with a low variation in the value of the UF –0.13% in 1 Q 2013 vs 1.11% in 4Q 2012– coupled with: (i) the incorporation of Banco Santander Colombia operation in 2Q 2012; (ii) interest expenses associated to the portion of the acquisition not financed by capital; and (iii) the branding change. This was partly offset by the organic growth in Chile, with a proportion of commercial loans somewhat larger than retail loans.

The following table set forth the components of our net income for the quarters ended March 31, 2013 and 2012 and December 31, 2012:

| Quarterly Consolidated Income Statements (unaudited) | ||||||

| Quarter | Change (%) | |||||

| (Expressed in millions of Chilean pesos) | 1Q13 | 4Q12 | 1Q12 | 1Q13/1Q12 | 1Q13/4Q12 | |

| Net interest income | 82,074 | 87,871 | 58,995 | 39.1% | -6.6% | |

| Net fee and commission income | 22,577 | 27,763 | 13,226 | 70.7% | -18.7% | |

| Treasury | 13,498 | 21,857 | 11,695 | 15.4% | -38.2% | |

| Other operating income | 3,533 | 3,106 | 2,123 | 66.4% | 13.7% | |

| Net operating profit before loan losses | 121,682 | 140,597 | 86,039 | 41.4% | -13.5% | |

Provision for loan losses (1) | (20,770) | (11,328) | (13,272) | 56.5% | 83.4% | |

| Net operating profit | 100,912 | 129,269 | 72,767 | 38.7% | -21.9% | |

| Operating expenses | (62,112) | (76,110) | (40,738) | 52.5% | -18.4% | |

| Other operating expenses | (4,125) | (5,314) | (4,433) | -6.9% | -22.4% | |

| Operating income | 34,675 | 47,845 | 27,596 | 25.7% | -27.5% | |

| Income from investments in other companies | 592 | 440 | 17 | 3382.4% | 34.5% | |

| Income before taxes | 35,267 | 48,285 | 27,613 | 27.7% | -27.0% | |

| Income tax expense | (5,699) | (10,864) | (4,568) | 24.8% | -47.5% | |

| Minority interest | (729) | (356) | 509 | - | 104.8% | |

| Net income attributable to shareholders | 28,839 | 37,065 | 23,554 | 22.4% | -22.2% | |

(1) Includes Provision for Contingent loans.

II) Unconsolidated Financial Performance Review: Chile and Colombia

In order to show the impact of the Colombian operation, the following table present the results generated in Chile as well as the one generated in Colombia. It is important to highlight the books of CorpBanca in Chile includes some expenses that are associated with the operation in Colombia in particularly the interest expense related to the portion of the acquisition which was not funded with capital, the amortization of the intangible assets due to the acquisition and some impacts in the mark-to-market to derivatives used for hedging tax expenses related to the acquisition of Banco Santander Colombia. The adjusted 1Q 2013 results presents in our opinion an unbiased result achieved in Chile:

| 1Q 2013 | 1Q 2013 Adjusted | Change (%) | |||||

| (Expressed in millions of Chilean pesos) | Consolida-ted | Chile | Colombia | Adjust-ments | Chile | Colombia | 1Q13/1Q12 Chile |

| Net interest income | 82,074 | 51,918 | 30,156 | 3,122 | 55,040 | 27,025 | 6.7% |

| Net fee and commission income | 22,577 | 15,504 | 7,073 | 15,504 | 7,073 | 17.2% | |

| Treasury | 13,498 | 1,679 | 11,819 | 2,633 | 4,312 | 9,186 | -63.1% |

| Other operating income | 3,533 | 1,533 | 2,000 | 1,533 | 2,000 | 27.8% | |

| Net operating profit before loan losses | 121,682 | 70,634 | 51,048 | 5,674 | 76,398 | 45,284 | -11.2% |

Provision for loan losses (1) | (20,770) | (11,361) | (9,409) | (11,361) | (9,409) | -14.4% | |

| Net operating profit | 100,912 | 59,273 | 41,639 | 5,764 | 65,037 | 35,875 | -10.6% |

| Operating expenses | (62,112) | (39,174) | (22,938) | (2,542) | (36,632) | (25,480) | -10.1% |

| Other operating expenses | (4,125) | (3,334) | (791) | (3,334) | (791) | -24.8% | |

| Operating income | 34,675 | 16,765 | 17,910 | 8,306 | 25,071 | 9,604 | -9.1% |

| Income from investments in other companies | 592 | - | 592 | - | - | 592 | - |

| Income before taxes | 35,267 | 16,765 | 18,502 | 8,306 | 25,071 | 10,196 | -9.2% |

| Efficiency Ratio | 51.0% | 49.3% | 54.0% | ||||

(1) Includes Provision for Contingent loans.

Press Release

June 4, 2013

Page 7 / 21

In terms of Adjusted Net Income before taxes it is observed that the operation in Colombia generated Ch$10,196 million while the Chilean operation generated Ch$25,071 million, a reduction of 9.2% YoY.

These figures show not only that the operation in Colombia was profitable in 1Q 2013 but also helped to diversified and reduced volatility of the revenues of the bank. The local results were affected by the lower inflation observed in 1Q 2013 as it did to the entire industry but due to lower operating expenses and low loan loss provision expenses, the Net Income before taxes were reduced by a much lower growth rate compare to the industry.

Consolidated Net interest income

Our net interest income was Ch$82,074 million in 1Q 2013, an increase of 39.1% as compared to Ch$58,995 million for the same period in 2012 and a decrease of 6.6% QoQ due to a lower inflation rate in 1Q 2013 compared to 4Q 2012. The YoY increase in net interest income was primarily the result of the incorporation of CorpBanca Colombia’s results following the Banco Santander Colombia Acquisition which took place in May 2012.

The increase in our interest income was lower than the increase in our total interest-earning assets due to a lower variation in the UF of 1.07% vs. 0.13% in 1Q 2012 and 2013, respectively. Net interest margin (net interest income divided by average interest-earning assets) decreased by 3.5% from 2.93% to 2.83% as a result of the above mentioned factors relating to our net interest income. Nevertheless, on twelve months trailing net interest margin trend is positive increasing from 2.8% as of March, 2012 to 3.2% as of March 2013.

Consolidated Fees and income from services

| Quarter | Change (%) | |||||

| (Expressed in millions of Chilean pesos) | 1Q13 | 4Q12 | 1Q12 | 1Q13/1Q12 | 1Q13/4Q12 | |

| Banking services(*) | 16,535 | 10,431 | 8,283 | 99.6% | 58.5% | |

| Securities brokerage services | 332 | 599 | 487 | -31.8% | -44.6% | |

| Mutual fund management | 1,321 | 1,517 | 1,284 | 2.9% | -12.9% | |

| Insurance brokerage | 2,307 | 2,523 | 1,728 | 33.5% | -8.6% | |

| Financial advisory services | 1,540 | 3,539 | 991 | 55.4% | -56.5% | |

| Legal advisory services | 543 | 489 | 453 | 19.8% | 11.0% | |

| Net fee and commission income | 22,577 | 19,098 | 13,226 | 70.7% | 18.2% | |

| (*) Includes consolidation adjustments. | ||||||

Our net service fee income for 1Q 2013 was Ch$22,577 million, representing a 70.7% increase when compared to Ch$13.226 million for 1Q 2012. The increase in our net income from fees and services was primarily the result of (i) the consolidation of CorpBanca Colombia following the Banco Santander Colombia Acquisition, (ii) the increase in collections, billings and payments income, (iii) the increase in fees from letters of credit and guarantees, and (iv) the increase in income from card service fees. The increase in these fees and commissions categories is due to the organic growth generated in Chile during 2012 which resulted in a larger volume of operations.

Press Release

June 4, 2013

Page 8 / 21

Consolidated Trading and investment

| Quarter | Change (%) | |||||

| (Expressed in millions of Chilean pesos) | 1Q13 | 4Q12 | 1Q12 | 1Q13/1Q12 | 1Q13/4Q12 | |

| Trading and investment income: | ||||||

| Trading investments | 3,132 | 2,153 | 3,266 | -4.1% | 45.5% | |

| Trading financial derivatives contracts | (3,446) | 2,986 | (739) | 366.4% | - | |

| Other | 6,515 | 11,371 | 2,245 | 190.2% | -42.7% | |

| Net income from financial operations | 6,201 | 16,510 | 4,772 | 29.9% | -62.4% | |

| Foreign exchange profit (loss), net | 7,297 | 5,347 | 6,922 | 5.4% | 36.5% | |

| Net treasury position | 13,498 | 21,857 | 11,694 | 15.4% | -38.2% | |

Net trading activities increased by Ch$1,429 million or 29.9% YoY to Ch$6,201 million for 1Q 2013 from Ch$4,772 million. Net foreign exchange gains slightly increased by Ch$375 million YoY to Ch$7,297 million in 1Q 2013 from Ch$6,922 million in 1Q 2012. A significant number of derivatives are client-driven or used in order to either achieve economic hedge or accounting hedges.

Consolidated Provisions for loan losses (for Commercial and Retail loans) (1)

| Quarter | Change (%) | |||||

| (Expressed in millions of Chilean pesos) | 1Q13 | 4Q12 | 1Q12 | 1Q13/1Q12 | 1Q13/4Q12 | |

| Commercial, net of loan loss recoveries | (11,510) | (4,366) | (8,640) | 33.2% | 163.6% | |

| Residential mortgage, net of loan loss recoveries | (731) | 2,409 | (643) | 13.7% | - | |

| Consumer, net of loan loss recoveries | (8,372) | (10,662) | (4,862) | 72.2% | 21.5% | |

| Others | (28) | (1) | 46 | - | - | |

| Net provisions for loan losses | (20,641) | (12,620) | (14,099) | 46.4% | 63.6% | |

(1) Excludes provision for Contingent loans.

Provisions for loan losses increased by 46.4% YoY to Ch$20,641 million in 1Q 2013 compared to Ch$14,099 million in 1Q 2012 explained by the incorporation of CorpBanca Colombia’s loan portfolio. Regarding the operation in Chile, loan loss provision expenses were reduced YoY as a consequence of lower risk levels.

Consolidated Operating expenses

| Quarter | Change (%) | |||||

| (Expressed in millions of Chilean pesos) | 1Q13 | 4Q12 | 1Q12 | 1Q13/1Q12 | 1Q13/4Q12 | |

| Personnel salaries and expenses | 29,732 | 39,022 | 24,449 | 21.6% | -23.8% | |

| Administrative expenses | 24,742 | 30,057 | 14,235 | 73.8% | -17.7% | |

| Depreciation and amortization | 7,638 | 7,031 | 2,054 | 271.9% | 8.6% | |

| Impairment | - | - | - | - | - | |

| Operating expenses | 62,112 | 76,110 | 40,738 | 52.5% | -18.4% | |

Operating expenses increased by Ch$21,374 million YoY, or 52.5%, in the year ended December 31, 2012 from Ch$40,738 million in 1Q 2012. The increase in operating expenses was primarily the result of the incorporation of the results of CorpBanca Colombia following the Banco Santander Colombia Acquisition, including an increase in administration expenses by 73.8% related to our rebranding efforts in Colombia in connection with the Banco Santander Colombia Acquisition as described in more detail below and personnel salaries and expenses by 21.6%.

Press Release

June 4, 2013

Page 9 / 21

The increase in our personnel salaries and expenses is attributable to the expansion of our geographic footprint and an increase in the diverse financial products we offer. We also had an increase of 73.8% in administration expenses due to the one-time expenses mentioned above, including Banco Santander Colombia’s rebranding and personnel performance bonuses, and an increase in depreciation and amortization of 271.9% as a result of the amortization of the intangibles assets related to Banco Santander Colombia Acquisition.

III) Consolidated Assets and liabilities

Consolidated Loan portfolio (1)

| As of the three months ended | Change (%) | |||||

| (Expressed in millions of Chilean pesos) | mar-13 | dic-12 | mar-12 | Mar-13/Mar-12 | Mar-13/Dec-12 | |

| Wholesale lending | 7,433,704 | 7,513,969 | 5,549,634 | 33.9% | -1.1% | |

| Chile | 6,322,723 | 6,418,447 | 5,549,634 | 13.9% | -1.5% | |

| Commercial loans | 5,480,390 | 5,564,788 | 4,766,144 | 15.0% | -1.5% | |

| Foreign trade loans | 436,196 | 424,824 | 388,195 | 12.4% | 2.7% | |

| Leasing and Factoring | 406,137 | 428,835 | 395,295 | 2.7% | -5.3% | |

| Colombia | 1,110,981 | 1,095,522 | - | - | 1.4% | |

| Commercial loans | 1,110,457 | 1,095,441 | - | - | 1.4% | |

| Foreign trade loans | - | - | - | - | - | |

| Leasing and Factoring | 524 | 81 | - | - | 546.9% | |

| Retail lending | 2,660,624 | 2,646,629 | 1,627,979 | 63.4% | 0.5% | |

| Chile | 1,889,470 | 1,858,717 | 1,627,979 | 16.1% | 1.7% | |

| Consumer loans | 480,916 | 476,275 | 425,136 | 13.1% | 1.0% | |

| Residential mortgage loans | 1,408,554 | 1,382,442 | 1,202,843 | 17.1% | 1.9% | |

| Colombia | 771,154 | 787,912 | - | - | -2.1% | |

| Consumer loans | 616,385 | 633,457 | - | - | -2.7% | |

| Residential mortgage loans | 154,769 | 154,455 | - | - | 0.2% | |

| TOTAL LOANS | 10,094,328 | 10,160,598 | 7,177,613 | 40.6% | -0.7% | |

| Chile | 8,212,193 | 8,277,164 | 7,177,613 | 14.4% | -0.8% | |

| Colombia | 1,882,135 | 1,883,434 | - | - | -0.1% | |

(1) Contingent loans under IFRS are not considered part of the Loan portfolio.

Our total loans increased by 40.6% or Ch$2,196.7 billion YoY from Ch$7,177.6 billion to Ch$10,094.3 billion. This increase is primarily the result of the addition of CorpBanca Colombia’s loan portfolio following the Banco Santander Colombia Acquisition, which represented 65% of our total loan portfolio increase YoY.

Our wholesale lending increased 33.9% or Ch$1,884.1 billion YoY but decrease 1.1% or Ch$80.3 billion QoQ reflecting a 1.5% decrease in commercial loans in Chile where we are growing at a slower pace than in previous periods in order to enhance business relationship with our clients and improve our profitability. CorpBanca significantly increased its market share in Chile during 2012 (8.8% in 2010 and 10.2% in 1Q 2013) becoming principal bank of the upper end of large corporations.

Our retail lending increased 63.4% or Ch$1,032.6 billion YoY and increased 0.5% or Ch$14.0 billion QoQ mainly due to a 1.9% or Ch$26.0 billion increase in our residential mortgage loans in Chile QoQ that offset a 2.7% decrease in consumer loans in Colombia.

Consolidated Securities Portfolio

| As of the three months ended | Change (%) | |||||

| (Expressed in millions of Chilean pesos) | mar-13 | dic-12 | mar-12 | Mar-13/Mar-12 | Mar-13/Dec-12 | |

| Trading investments | 251,527 | 159,898 | 167,880 | 49.8% | 57.3% | |

| Available-for-sale investments | 892,798 | 1,112,435 | 602,554 | 48.2% | -19.7% | |

| Held-to-maturity investments | 116,439 | 104,977 | 10,741 | 984.1% | 10.9% | |

| Total Financial Investments | 1,260,764 | 1,377,310 | 781,175 | 61.4% | -8.5% | |

Press Release

June 4, 2013

Page 10 / 21

Our investment portfolio consists of trading, available-for-sale and held-to-maturity securities. Trading instruments correspond to fixed income securities acquired to generate gains from short-term price fluctuations or brokerage margins. Trading instruments are stated at fair value.

Investment instruments are classified in two categories: held-to-maturity investments and instruments available-for-sale. We currently have a small amount of held-to-maturity investments. All other investment instruments are considered available-for-sale. Investment instruments are initially recognized at cost, which includes transaction costs. Instruments available-for-sale at each subsequent period-end are valued at their fair value according to market prices or based on valuation models. Unrealized gains or losses arising from changes in the fair value are charged or credited to equity accounts.

Our total financial investments increased by 49.8% or Ch$479.6 billion YoY. This increase is primarily the result of the addition of CorpBanca Colombia’s investment portfolio following the Banco Santander Colombia Acquisition. QoQ total financial investments decrease by 8.5% or Ch$116.5 billion reflecting the 19.7% decrease in our available-for-sale investments.

Consolidated Funding strategy

| As of the three months ended | Change (%) | |||||

| (Expressed in millions of Chilean pesos) | mar-13 | dic-12 | mar-12 | Mar-13/Mar-12 | Mar-13/Dec-12 | |

| Demand deposits | 1,318,360 | 1,112,675 | 677,854 | 94.5% | 18.5% | |

| Time deposits and saving accounts | 6,638,416 | 7,682,675 | 5,124,225 | 29.5% | -13.6% | |

| Investments sold under repurchase agreements | 247,066 | 257,721 | 112,775 | 119.1% | -4.1% | |

| Mortgage finance bonds | 139,416 | 147,688 | 172,469 | -19.2% | -5.6% | |

| Bonds | 1,413,184 | 1,044,124 | 1,073,574 | 31.6% | 35.3% | |

| Subordinated bonds | 752,473 | 694,792 | 423,639 | 77.6% | 8.3% | |

| Interbank borrowings | 18,658 | 18,120 | 19,181 | -2.7% | 3.0% | |

| Foreign borrowings | 924,108 | 969,521 | 714,516 | 29.3% | -4.7% | |

Our current funding strategy is to continue utilizing all sources of funding in accordance with their costs, their availability and our general asset and liability management strategy.

On July 29, 2010, we entered into a US$167.5 million senior unsecured syndicated term loan facility with BNP Paribas, as Administrative Agent, and BNP Paribas Securities Corp., Citigroup Global Markets Inc., Commerzbank Aktiengesellschaft, Standard Chartered Bank and Wells Fargo Securities, LLC, as lead arrangers and book-runners. The proceeds of the loan were used mainly to fund our lending activities and for general corporate purposes. On July 24, 2012, we have entered into a US$174.4 million amended and restated senior unsecured syndicated term loan facility with Standard Chartered Bank, as administrative agent, HSBC Securities (USA) Inc. and Wells Fargo Securities, LLC, as lead arrangers and book-runners, and Commerzbank Aktiengesellschaft, as lead arranger.

On August 1, 2010, we implemented a local bond program for a maximum amount of UF150 million at any time outstanding. Under the local bond program, we are able to issue two types of bonds: (i) senior bonds, up to an aggregate amount of UF100 million, which can be divided into 28 series of senior bonds (from AB to AZ and from BA to BC), with a maturity ranging from 3 to 30 years and an interest rate of 3%, and (ii) subordinated bonds, up to an aggregate amount of UF50 million, which can be divided into 16 series (from BD to BS), with a maturity ranging from 20 to 35 years and an interest rate of 4%. For all the series of bonds that could be issued under the local bond program, the amortization of capital will be made in full at maturity. The principal owed in connection with outstanding senior and subordinated bonds is due at maturity and interest relating thereto is due bi-annually. The objective of the local bond program is to structure the future issuances of debt of CorpBanca in a way that provides for diverse alternatives of placements in order to manage efficiently its outstanding indebtedness. Under the local bond program, in 2010, we issued bonds in the Chilean market in the amount of UF18.8 million (Ch$403,364). In addition, on October 29, 2012 and October 31, 2012, we issued subordinated bonds in the local

Press Release

June 4, 2013

Page 11 / 21

Chilean market in the aggregate amount of UF6.6 million (Ch$149,779 million). As of March 31, 2013, we have outstanding senior bonds in the aggregate amount of Ch$1,413.2billion and outstanding subordinated bonds in the aggregate amount of Ch$752.5 billion.

On November 3, 2010, we issued US$178.1 million in Reg S notes in the international market. As of March 31, 2013, the Reg S notes have been paid off.

At the end of 2011, global financial markets faced a complex scenario in terms of liquidity due to uncertainty in European economies. Liquidity was constrained and risk premiums reached yearly highs in practically all global markets, including in Chile. Despite such circumstances, as of March 31, 2013, we maintained a reserve in liquid assets (mainly consisting of securities issued by the Central Bank of Chile and Treasury Bonds of Colombia’s Government) of Ch$1,074,743 million. In addition, as of March 31, 2013, we maintained sufficient levels of cash and deposits in banks in the amount of Ch$571.9 billion to satisfy our wholesale short-term obligations in the amount of Ch$174,612.0 million.

On January 16, 2013, CorpBanca issued US$800 million aggregate principal amount of 3.125% Senior Notes. CorpBanca expects to use the net proceeds of this offering for general corporate purposes, primarily to fund lending activities.

Consolidated Shareholders’ Equity

As of March 31, 2013, we were the fourth largest private bank in Chile, based on our shareholders’ equity (excluding net income and accrual for mandatory dividends) of Ch$1,223.2 billion and loans of Ch$10,094.3 billion. After a capital of 47,000,000,000 common shares during the quarter, we had 340,358,194.2 thousand shares outstanding and a market capitalization of Ch$2,204.5 billion (based on a share price of Ch$6.477 pesos per share) as of March 31, 2013.

On January 18, 2013, we raised capital in the aggregate amount of Ch$66,751.2 million through the issuance of 10,680,200,621 common shares, including common shares in the form of ADSs, in the United States and elsewhere outside of Chile (ii) on February 7, 2013, we raised capital in the aggregate amount of Ch$106,361.9 million in connection with the investment by certain investment funds of the International Finance Corporation, or IFC, a member of the World Bank Group, and IFC Asset Management Company to acquire a 5% equity interest in CorpBanca, or the IFC Investment, pursuant to an investment agreement with CorpGroup, Compañía Inmobiliaria y de Inversiones Saga Ltda., and CorpGroup Inversiones Bancarias Ltda., and (iii) on February 14, 2013, we raised capital in the aggregate amount of Ch$120,927.7 million during a preemptive rights offering under Chilean law in connection with the authorization by the Board of Directors on November 27, 2012 to issue 47,000,000,000 common shares.

IV) Other Related Information

CorpBanca to become a major player in the Colombian banking industry:

CorpBanca announces an agreement to acquire Helm Bank, positioning itself as the 5th largest bank in Colombia

On October 11, 2012, CorpBanca announced the entry into an agreement by and among Corp Group Holding Inversiones Limitada, or the HB Purchaser, and affiliates of Helm Corporation to acquire a 100% equity interest in Helm Bank S.A. through a merger with Banco CorpBanca Colombia S.A. as the surviving corporation. The aforementioned acquisition is herein referred to as the Helm Bank Acquisition. The total purchase price of the Helm Bank Acquisition is US$1.278 billion plus interest accruing on such amount at the rate of 0.5% per month from January 1, 2013, until the purchase price is paid. Subject to the terms and conditions set forth in the HB Purchase Agreement, at the closing date of the Helm Bank Acquisition, the HB Purchaser shall assign all of its rights and obligations under the HB Purchase Agreement to CorpBanca Colombia, which ultimately will acquire Helm

Press Release

June 4, 2013

Page 12 / 21

Bank. Within ninety days after the closing of the Helm Bank Acquisition, CorpBanca Colombia is obligated to commence a tender offer (oferta pública de adquisición) to acquire all of the preferred stock of Helm Bank from the current holders of such preferred stock pursuant to Colombian law.

In addition, CorpBanca intends to acquire an 80% equity interest in Helm Corredor de Seguros S.A., an insurance broker, for US$17.12 million. The Helm Bank Acquisition and the acquisition of Helm Insurance are subject to customary closing conditions, including regulatory approval in Chile, Colombia, Panama and the Cayman Islands. CorpBanca’s management expects that the purchases will be completed next month. Upon completion of the acquisitions, CorpBanca will consolidate the operations of Helm Bank with and into CorpBanca Colombia, thereby reaffirming its long-term commitment to the Colombian market.

In order to finance the Helm Bank Acquisition, CorpBanca Colombia plans to raise capital in an amount not to exceed US$1 billion and finance the remainder of the acquisitions with its own funds. The planned capital increase will be subscribed by (i) CorpBanca for approximately US$365 million, (ii) Helm Corporation for approximately US$440 million, and (iii) Corpgroup Interhold Limitada for approximately US$180 million. CorpBanca will have a controlling interest in the merged bank with an approximate 67% equity interest and Helm Corporation will retain an approximate 20% equity interest.

In order to finance this additional investment in Colombia as well to finance CorpBanca’s medium-term organic growth in Chile, between January and February, 2013 we raised capital in the aggregate amount of Ch$294,040.8 million.

CorpBanca Colombia provides a broad range of commercial and retail banking services to its customers, operating principally in the cities of Bogotá, Medellín, Cali, Bucaramanga and Barranquilla. As of March 31, 2013, according to the Colombian Superintendency of Finance, CorpBanca Colombia was the 12th largest bank in Colombia in terms of total assets, the 10th largest bank in Colombia in terms of total loans and the 12th largest bank in Colombia, in terms of total deposits reported under local regulatory and accounting principles. As of March 31, 2013, CorpBanca Colombia had deposits and financial claims (“current accounts and demand deposits” and “time deposits and savings accounts”) of COP$6,000,293 million, which consisted of savings deposits, fixed-term deposit certificates, current accounts, financial claims for banking services and other commitments. As of March 31, 2013, CorpBanca Colombia had 114 ATMs and 269,522 individual banking customers and 29,247 commercial banking customers (including SMEs, corporations, institutions and wholesale customers). In 1Q 2013, CorpBanca Colombia’s Net Income totaled COP$56,708 million, compared to COP$42,907 million in 4Q 2013. As of March 31, 2013, CorpBanca Colombia had (i) total assets of COP$9,648,779 million, including total loans of COP$7,077,031 million; (ii) total shareholders’ equity of COP$1.006.653 million; and (iii) 87 branches and offices and 1,608 employees.

As of March 31, 2013, Helm Bank was the 7th largest bank in Colombia in terms of total assets and total deposits. As of March 31, 2012, Helm Bank had total assets of US$6,427 billion, loans of US$4,675 billion, total deposits of US$4,522 billion and a net equity of US$805 million. With more than 205,000 customers and 89 branches, Helm Bank specializes in the corporate segment, medium enterprises and personal accounts with middle to high income. In the last five years, Helm Bank has continuously received high customer satisfaction ratings.

The merger will create the 5th largest bank in Colombia in terms of total assets and loans with a significant presence in segments such as corporate clients and high and medium income individuals. The combined bank will become a larger-scale player across all product lines, with a balanced mix of businesses focused on commercial and retail operations. As of March 31, 2013, Banco CorpBanca Colombia and Helm Bank together had more than US$11.600 billion in assets, US$8,400 billion in loans and approximately US$7.800 billion in total deposits, which represented 6.8% market share in loans and 6.2% market share in total deposits. In addition, according to pro forma figures, the merged bank has healthy credit quality and a Return on Average Equity (RoAE) of approximately 15.5% for the 12 months trailing March 31, 2013.

Press Release

June 4, 2013

Page 13 / 21

Customers of both entities will be able to take advantage of a larger number of products given the different strengths of both banks. The integration of Banco CorpBanca Colombia’s and Helm Bank’s central systems will also reduce costs. CorpBanca estimates that the merger will result in cost savings around US$100 million per year after taxes. CorpBanca believes that the merger will be an important source of value creation via optimization of costs/expenses and income through net interest margin, generating attractive returns for shareholders after the merger costs are absorbed.

The merged bank will have an expected total pro forma solvency indicator of 17.0% by the end of the first half 2013, which is higher than each of both banks has on an individual basis under current Colombian regulation. Meanwhile, CorpBanca estimates that it will continue to have adequate levels of capitalization in order to finance its growth in the near to medium term. CorpBanca estimates that its pro forma BIS Ratio will be in the range of 12.5% to 13.0% by the end of 2013.

CorpBanca Colombia(1) | Helm Bank(1) | Merged Bank | |||||||||

| Pro forma | |||||||||||

(Expressed in millions of US$)(2) | Mar.2013(3) | MkSh | Ranking | Mar.2013(3) | MkSh | Ranking | Mar.2013(3) | MkSh | Ranking | |||||

| Total Assets | 5,266 | 2.8% | 12° | 6,427 | 3.4% | 10° | 11,693 | 6.1% | 5° | ||

| Total Loans | 3,731 | 3.0% | 10° | 4,675 | 3.8% | 8° | 8,406 | 6.8% | 5° | ||

| Total Deposits | 3,275 | 2.6% | 13° | 4,522 | 3.6% | 10° | 7,797 | 6.2% | 6° | ||

| Equity | 549 | 14° | 805 | 9° | 1,354 | ||||||

Net Income (LTM) | *98.0 | 11° | 95.5 | 13° | *193.5 | ||||||

RoAA (LTM) | *2.0% | 13° | 1.5% | 17° | *1.7% | ||||||

RoAE (LTM) | *19.6% | 5° | 12.8% | 16° | *15.5% | ||||||

Efficiency Ratio (LTM) | *53.1% | 10° | 51.4% | 8° | *52.2% | ||||||

| NPL | 2.1% | 4° | 2.8% | 7° | 2.5% | ||||||

| BIS Ratio** | 13.5% | 12° | 11.1% | 20° | 12.2% | ||||||

| Branches | 87 | n.a. | 89 | n.a. | 176 | n.a. | |||||

| Headcount | 1,608 | n.a. | 2,159 | n.a. | 3,767 | n.a. | |||||

| (1) | Unconsolidated financial statements (unaudited). Source: Banco CorpBanca Colombia S.A., Helm Bank S.A. and the Colombian Superintendency of Finance. |

| (2) | U.S. dollar amounts have been translated from Colombian pesos at an exchange rate of Col$1,832.20 per U.S. dollar as of March 31, 2013. |

| (3) | Annualized ratios where appropriate. |

| * | Excludes 2012’s Rebranding costs. |

| ** | Includes Market Risk. |

V) Ownership structure and share performance

Ownership structure

As of March 31, 2013, CorpBanca was controlled by Corp Group Banking S.A. and other companies related to Mr. Alvaro Saieh and his family:

| Stock Holder | % of Total Share Capital |

| Corp Group Banking S.A. | 45.0568% |

| Cía. Inmob. y de Inversiones Saga S.A. | 5.4934% |

| Cía. de Seguros CorpVida S.A. | 2.0960% |

| Cía. de Seguros CorpSeguros S.A. | 0.8092% |

| Other investment companies | 0.0012% |

| Total Saieh Group | 53.4567% |

Press Release

June 4, 2013

Page 14 / 21

| IFC | 5.0000% |

| Sierra Nevada Investment Chile Dos Ltda. (Santo Domingo Group) | 2.8843% |

| Others | 38.6590% |

| ADRs holders and Foreign investors | 12.0191% |

| AFPs (Administradoras de Fondos de Pensiones) | 7.5141% |

| Securities Brokerage | 6.0672% |

| Other minority shareholders | 13.0586% |

| Total | 100.0000% |

ADR price evolution and local share price evolution

| ADR Price | |

| 03/28/2013 | US$20.91 |

| Maximum (LTM) | US$22.19 |

| Minimum (LTM) | US$17.11 |

Press Release

June 4, 2013

Page 15 / 21

| Local Share Price | |

| 03/28/2013 | Ch$6.477 |

| Maximum (LTM) | Ch$6.98 |

| Minimum (LTM) | Ch$5.50 |

| Market capitalization | US$4,671 million |

| P/E (LTM) | 17.58 |

| P/BV (03/28/2013) | 3.59 |

| Dividend yield* | 2.5% |

| * Based on closing price on the day the dividend payment was announced. |

Dividends

The following table shows dividends per share distributed during the past five years:

| Charged to Fiscal Year | Year paid | Net Income (Ch$mn) | % Distributed | Distributed Income (Ch$mn) | Pesos per Share (Ch$ of each year) |

| 2008 | 2009 | 56,310 | 100% | 56,310 | 0.254525860 |

| 2009 | 2010 | 85,109 | 100% | 85,109 | 0.375082130 |

| 2010 | 2011 | 119,043 | 100% | 119,043 | 0.524628030 |

| 2011 | 2012 | 122,849 | 100% | 122,849 | 0.490694036 |

| 2012 | 2013 | 120,080 | 50% | 60,040 | 0.176402388 |

Press Release

June 4, 2013

Page 16 / 21

VI) Credit risk ratings

International credit risk ratings

On a global scale, the bank is rated by two world-wide recognized agencies: Moody´s Investors Service and Standard & Poor´s Ratings Services (S&P).

On October 11, 2012, Moody´s Investors Service changed the outlook on the ratings of CorpBanca to 'Negative' from 'Stable' following CorpBanca´s announcement to acquire Helm Bank S.A. (Colombia). The 'Negative' outlook was placed on CorpBanca’s 'D+' standalone bank financial strength rating (BFSR) and 'baa3' baseline credit assessment (BCA) and the bank’s 'Baa1' long term local and foreign currency deposit ratings. The bank´s 'Prime-2' short term local and foreign currency deposit were unaffected by this action.

The 'Negative' outlook reflects the potential for negative pressure on the bank’s financial fundamentals as a result of its second large cross border bank acquisition in less than 12 months. The acquisition of Helm represents a doubling of the bank’s exposure in the Colombian market within a very short time frame. The 'Negative' outlook also encompasses the risk of greater than expected integration and credit costs, as well as the costs of acquiring and merging the two banks in Colombia, away from CorpBanca´s traditional Chilean footprint.

Moody’s said that CorpBanca’s acquisition of Helm makes strategic sense as it is designed to consolidate the bank’s position in Colombia’s growing economy and financial system with a critical mass of market share (around 7%). This enhanced market share together with Helm Bank’s portfolio and customer base of large corporations will bolster CorpBanca´s ability to compete with the large Colombian banks that dominate the domestic banking industry.

| Moody´s | Rating |

| Long-term foreign currency deposits | Baa1 |

| Short-term fforeign currency deposits | Prime-2 |

| Bank financial strength | D+ |

| Outlook | Negative |

On October 9, 2012, Standard & Poor´s Ratings Services placed its 'BBB+' ratings on CorpBanca on 'CreditWatch with negative implications' on agreement to buy Helm Bank, reflecting the potential impact of the increased exposure to Colombia. S&P will evaluate the acquisition's impact on CorpBanca's anchor stand-alone credit profile, capital charges, risk adjusted capital ratios, and the resulting capital structure. S&P intend to resolve the CreditWatch listings after completion of regulatory approvals in Chile and Colombia.

| Standard & Poor´s | Rating |

| Long-term issuer credit rating | BBB+ |

| Short-term issuer credit rating | A-2 |

| CreditWatch | Negative |

Local Credit risk ratings

On a national scale, the bank is rated by Feller Rate –a Strategic Affiliate of Standard & Poor´s–, by International Credit Rating Chile (ICR) and by Humphreys.

On October 11, 2012, Feller Rate changed the 'CreditWatch with developing implications' placing the 'AA' ratings of CorpBanca on 'CreditWatch Negative'. At the same time, preliminary maintained the 'Primera Clase Nivel 1' rating on its shares. The change in the implications of CreditWatch to 'Negative' from 'Developing' considered the bank’s announcement to acquire Helm Bank S.A. in Colombia through its Colombian subsidiary, Banco CorpBanca Colombia S.A. To resolve the CreditWatch listings, Feller Rate will consider more detailed financial and business profiles of the consolidated entity, as well as the expected capital adequacy ratios for the forecoming periods.

Press Release

June 4, 2013

Page 17 / 21

| Feller Rate | Rating |

| Long-term issuer credit rating | AA |

| Senior unsecured bonds | AA |

| Subordinated bonds | AA- |

| Short-term issuer credit rating | Nivel 1+ |

| Shares | 1ª Clase Nivel 1 |

| CreditWatch | Negative |

On October 12, 2012, ICR changed the outlook on the ratings of CorpBanca to 'En Observación' from 'Stable' following CorpBanca´s announcement to acquire Helm Bank S.A. (Colombia). The change in the outlook reflects that once the required funding is raised and the merger between CorpBanca Colombia and Helm Bank is materialized, there is uncertainty that CorpBanca achieves enough regulatory equity to fulfill BIS Ratio and leverage level required to mitigate the risk of incorporate a large amount of assets from a country with a risk level greater than Chilean. The foregoing is without prejudice that the bank meets the minimum regulatory levels.

| ICR | Rating |

| Long-term issuer credit rating | AA |

| Senior unsecured bonds | AA |

| Subordinated bonds | AA- |

| Short-term issuer credit rating | Nivel 1+ |

| Shares | 1ª Clase Nivel 1 |

| Outlook | En Observación |

In October 2012, Humphreys rated in 'AA-' long term deposit and senior unsecured debt, in 'Nivel 1+' short term deposit and in 'A+' long term subordinated debt. The ratings’ Outlook was placed in 'En Observación' reflecting CorpBanca´s announcement to acquire Helm Bank S.A. (Colombia).

| Humphreys | Rating |

| Long-term issuer credit rating | AA- |

| Senior unsecured bonds | AA- |

| Subordinated bonds | A+ |

| Short-term issuer credit rating | Nivel 1+ |

| Shares | 1ª Clase Nivel 1 |

| Outlook | En Observación |

Press Release

June 4, 2013

Page 18 / 21

VII) Quarterly Consolidated Income Statements (unaudited)

For the three months ended | Change (%) | |||||||

Mar-13 | Mar-13 | Dec-12 | Mar-12 | Mar-13/Mar-12 | Mar-13/Dec-12 | |||

US$ths | Ch$mn | |||||||

Interest income | 444,101 | 209,256 | 251,874 | 161,986 | 29.2% | -16.9% | ||

Interest expense | (269,917) | (127,182) | (164,003) | (102,991) | 23.5% | -22.5% | ||

Net interest income | 174,185 | 82,074 | 87,871 | 58,995 | 39.1% | -6.6% | ||

Fee and commission income | 59,632 | 28,098 | 34,288 | 16,547 | 69.8% | -18.1% | ||

Fee and commission expense | (11,717) | (5,521) | (6,525) | (3,321) | 66.2% | -15.4% | ||

Net fee and commission income | 47,915 | 22,577 | 27,763 | 13,226 | 70.7% | -18.7% | ||

Net income from financial operations | 13,160 | 6,201 | 16,510 | 4,772 | 29.9% | -62.4% | ||

Foreign exchange profit (loss), net | 15,486 | 7,297 | 5,347 | 6,923 | 5.4% | 36.5% | ||

Total financial transactions, net | 28,647 | 13,498 | 21,857 | 11,695 | 15.4% | -38.2% | ||

Other operating income | 7,498 | 3,533 | 3,106 | 2,123 | 66.4% | 13.7% | ||

Net operating profit before loan losses | 258,244 | 121,682 | 140,597 | 86,039 | 41.4% | -13.5% | ||

Provision for loan losses (1) | (44,080) | (20,770) | (11,328) | (13,272) | 56.5% | 83.4% | ||

Net operating profit | 214,164 | 100,912 | 129,269 | 72,767 | 38.7% | -21.9% | ||

Personnel salaries and expenses | (63,100) | (29,732) | (39,022) | (24,449) | 21.6% | -23.8% | ||

Administrative expenses | (52,510) | (24,742) | (30,057) | (14,235) | 73.8% | -17.7% | ||

Depreciation and amortization | (16,210) | (7,638) | (7,031) | (2,054) | 271.9% | 8.6% | ||

Impairment | - | - | - | - | - | - | ||

Operating expenses | (131,819) | (62,112) | (76,110) | (40,738) | 52.5% | -18.4% | ||

Other operating expenses | (8,754) | (4,125) | (5,314) | (4,433) | -6.9% | -22.4% | ||

Total operating expenses | (140,574) | (66,237) | (81,424) | (45,171) | 46.6% | -18.7% | ||

Operating income | 73,590 | 34,675 | 47,845 | 27,596 | 25.7% | -27.5% | ||

Income from investments in other companies | 1,256 | 592 | 440 | 17 | 3382.4% | 34.5% | ||

Income before taxes | 74,847 | 35,267 | 48,285 | 27,613 | 27.7% | -27.0% | ||

Income tax expense | (12,095) | (5,699) | (10,864) | (4,568) | 24.8% | -47.5% | ||

Net income from ordinary activities | 62,752 | 29,568 | 37,421 | 23,045 | 28.3% | -21.0% | ||

Net income from discontinued operations | - | - | - | - | - | - | ||

Net income attributable to: | ||||||||

Minority interest | (1,547) | (729) | (356) | 509 | - | 104.8% | ||

Net income attributable to shareholders | 61,205 | 28,839 | 37,065 | 23,554 | 22.4% | -22.2% | ||

(1) Includes Provision for Contingent loans and net of loan loss recoveries.

Press Release

June 4, 2013

Page 19 / 21

VIII) Consolidated Balance Sheet (unaudited)

| As of the three months ended | Change (%) | |||||||

| Mar-13 | Mar-13 | Dec-12 | Mar-12 | Mar-13/Mar-12 | Mar-13/Dec-12 | |||

| US$ths | Ch$mn | |||||||

| Assets | ||||||||

| Cash and deposits in banks | 1,213,629 | 571,850 | 520,228 | 531,718 | 7.5% | 9.9% | ||

| Unsettled transactions | 443,051 | 208,761 | 123,777 | 255,465 | -18.3% | 68.7% | ||

| Trading investments | 533,812 | 251,527 | 159,898 | 167,880 | 49.8% | 57.3% | ||

| Available-for-sale investments | 1,894,773 | 892,798 | 1,112,435 | 602,554 | 48.2% | -19.7% | ||

| Held-to-maturity investments | 247,117 | 116,439 | 104,977 | 10,741 | 984.1% | 10.9% | ||

| Investments under resale agreements | 403,209 | 189,988 | 21,313 | 17,330 | 996.3% | 791.4% | ||

| Financial derivatives contracts | 532,513 | 250,915 | 268,027 | 242,468 | 3.5% | -6.4% | ||

| Interbank loans, net | 507,625 | 239,188 | 482,371 | 304,157 | -21.4% | -50.4% | ||

| Loans and accounts receivable from customers | 21,423,050 | 10,094,327 | 10,160,597 | 7,177,612 | 40.6% | -0.7% | ||

| Loan loss allowances | (361,555) | (170,361) | (166,707) | (108,738) | 56.7% | 2.2% | ||

| Loans and accounts receivable from customers, net of loan loss allowances | 21,061,497 | 9,923,967 | 9,993,891 | 7,068,875 | 40.4% | -0.7% | ||

| Investments in other companies | 12,341 | 5,815 | 5,793 | 3,583 | 62.3% | 0.4% | ||

| Intangible assets | 970,855 | 457,457 | 481,682 | 11,823 | 3769.2% | -5.0% | ||

| Property, plant and equipment | 133,343 | 62,830 | 65,086 | 56,194 | 11.8% | -3.5% | ||

| Current taxes | - | - | - | 10,682 | -100.0% | - | ||

| Deferred taxes | 85,295 | 40,190 | 40,197 | 29,756 | 35.1% | 0.0% | ||

| Other assets | 272,313 | 128,311 | 148,549 | 130,922 | -2.0% | -13.6% | ||

| Total Assets | 28,311,371 | 13,340,035 | 13,528,223 | 9,444,147 | 41.3% | -1.4% | ||

| Liabilities | ||||||||

| Deposits and other demand liabilities | 2,797,937 | 1,318,360 | 1,112,675 | 677,854 | 94.5% | 18.5% | ||

| Unsettled transactions | 365,515 | 172,227 | 68,883 | 223,674 | -23.0% | 150.0% | ||

| Investments sold under repurchase agreements | 524,345 | 247,066 | 257,721 | 112,775 | 119.1% | -4.1% | ||

| Time deposits and other time liabilities | 14,088,618 | 6,638,416 | 7,682,675 | 5,124,225 | 29.5% | -13.6% | ||

| Financial derivatives contracts | 391,876 | 184,648 | 193,844 | 156,826 | 17.7% | -4.7% | ||

| Interbank borrowings | 1,964,511 | 925,658 | 969,521 | 714,516 | 29.6% | -4.5% | ||

| Issued debt instruments | 4,892,024 | 2,305,073 | 1,886,604 | 1,669,682 | 38.1% | 22.2% | ||

| Other financial liabilities | 36,308 | 17,108 | 18,120 | 19,181 | -10.8% | -5.6% | ||

| Current taxes | 19,705 | 9,285 | 9,057 | 108 | 8497.2% | 2.5% | ||

| Deferred taxes | 227,808 | 107,341 | 117,753 | 26,041 | 312.2% | -8.8% | ||

| Provisions | 165,659 | 78,057 | 139,850 | 24,299 | 221.2% | -44.2% | ||

| Other liabilities | 131,611 | 62,014 | 75,205 | 36,008 | 72.2% | -17.5% | ||

| Total Liabilities | 25,605,919 | 12,065,253 | 12,531,908 | 8,785,189 | 37.3% | -3.7% | ||

| Equity | ||||||||

| Capital | 1,658,692 | 781,559 | 638,234 | 507,108 | 54.1% | 22.5% | ||

| Reserves | 901,394 | 424,728 | 275,552 | 139,140 | 205.3% | 54.1% | ||

| Valuation adjustment | (122,138) | (57,550) | (31,881) | (8,308) | 592.7% | 80.5% | ||

| Retained Earnings: | ||||||||

| Retained earnings or prior periods | 127,422 | 60,040 | - | - | - | - | ||

| Income for the period | 61,205 | 28,839 | 120,080 | 23,554 | 22.4% | -76.0% | ||

| Minus: Provision for mandatory dividend | (30,603) | (14,420) | (60,040) | (7,066) | 104.1% | -76.0% | ||

| Attributable to bank shareholders | 2,595,972 | 1,223,196 | 941,945 | 654,428 | 86.9% | 29.9% | ||

| Non-controlling interest | 109,480 | 51,586 | 54,370 | 4,530 | 1038.8% | -5.1% | ||

| Total Equity | 2,705,452 | 1,274,782 | 996,315 | 658,958 | 93.5% | 27.9% | ||

| Total equity and liabilities | 28,311,371 | 13,340,035 | 13,528,223 | 9,444,147 | 41.3% | -1.4% | ||

Press Release

June 4, 2013

Page 20 / 21

IX) Quarterly Consolidated Evolution Selected Performance Ratios (unaudited)

| As of and for the three months ended | |||||

| Mar-12 | Jun-12 | Sep-12 | Dec-12 | Mar-13 | |

| Capitalization | |||||

TIER I (Core capital) Ratio(4) | 8.14% | 8.02% | 8.01% | 8.19% | 10.63% |

BIS Ratio(4) | 12.41% | 10.83% | 10.80% | 11.05% | 14.76% |

| Shareholders' equity / Total assets | 6.98% | 7.40% | 7.44% | 7.36% | 9.56% |

| Shareholders' equity / Total liabilities | 7.50% | 8.00% | 8.03% | 7.95% | 10.57% |

| Asset quality | |||||

| Risk Index (Loan loss allowances / Total loans ) | 1.51% | 1.69% | 1.69% | 1.64% | 1.69% |

Prov. for loan losses / Avg. total loans(1) | 0.76% | 0.41% | 0.73% | 0.46% | 0.82% |

Prov. for loan losses / Avg. total assets(1) | 0.58% | 0.30% | 0.54% | 0.34% | 0.62% |

| Prov. for loan losses / Net operating profit before loans losses | 15.4% | 8.9% | 14.4% | 8.1% | 17.1% |

| Prov. for loan losses / Net income | 57.6% | 30.9% | 55.5% | 30.3% | 70.2% |

PDL / Total loans(5) | 0.66% | 0.62% | 0.63% | 0.54% | 0.48% |

| Coverage PDL´s | 230.5% | 271.4% | 270.3% | 305.2% | 350.7% |

NPL / Total loans(6) | 1.56% | 1.43% | 1.50% | 1.30% | 1.24% |

| Coverage NPL´s | 100.4% | 150.7% | 142.7% | 161.0% | 173.4% |

| Profitability | |||||

Net interest income / Avg. interest-earning assets(1)(2) (NIM) | 2.93% | 2.12% | 2.11% | 3.07% | 2.83% |

Net operating profit before loan losses / Avg. total assets(1) | 3.75% | 3.41% | 3.75% | 4.25% | 3.62% |

Net operating profit before loan losses / Avg. interest-earning assets(1)(2) | 4.28% | 4.01% | 4.41% | 4.92% | 4.20% |

RoAA (before taxes), over Avg. total assets(1) | 1.21% | 1.23% | 0.98% | 1.46% | 1.05% |

RoAA (before taxes), over Avg. interest-earning assets(1)(2) | 1.37% | 1.45% | 1.15% | 1.69% | 1.22% |

RoAE (before taxes)(1)(3) | 18.4% | 18.3% | 14.7% | 23.3% | 13.8% |

RoAA, over Avg. total assets(1) | 1.01% | 0.98% | 0.97% | 1.13% | 0.88% |

RoAA, over Avg. interest-earning assets(1)(2) | 1.15% | 1.15% | 1.14% | 1.31% | 1.02% |

RoAE(1)(3) | 14.66% | 14.06% | 13.33% | 15.95% | 10.50% |

| Efficiency | |||||

Operating expenses / Avg. total assets(1) | 1.78% | 1.71% | 1.89% | 2.30% | 1.85% |

Operating expenses/ Avg. total loans(1) | 2.33% | 2.31% | 2.56% | 3.06% | 2.45% |

| Operating expenses / Operating revenues | 47.3% | 50.2% | 50.4% | 54.1% | 51.0% |

| Market information (period-end) | |||||

| Diluted Earnings per share before taxes (Ch$ per share) | 0.1103 | 0.1195 | 0.1092 | 0.1646 | 0.1036 |

| Diluted Earnings per ADR before taxes (US$ per ADR) | 0.3384 | 0.3578 | 0.3457 | 0.5153 | 0.3294 |

| Diluted Earnings per share (Ch$ per share) | 0.0941 | 0.0959 | 0.1068 | 0.1263 | 0.0847 |

| Diluted Earnings per ADR (US$ per ADR) | 0.2886 | 0.2871 | 0.3380 | 0.3955 | 0.2693 |

Total Shares Outstanding (Thousands)(4) | 250,358,194.2 | 293,358,194.2 | 293,358,194.2 | 293,358,194.2 | 340,358,194.2 |

| Peso exchange rate for US$1.0 | 488.93 | 501.07 | 473.94 | 479.16 | 471.89 |

| Quarterly UF variation | 1.07% | 0.42% | -0.16% | 1.11% | 0.13% |

(1) Annualized figures when appropriate.

(2) Interest-earning assets: Total loans and financial investments.

(3) Equity: Average equity attributable to shareholders excluding net income and accrual for mandatory dividends.

(4) During the second and first quarters 2012 and 21013, respectively, the bank increased its capital base.

(5) PDL: Past due loans; all installments that are more than 90 days overdue.

(6) NPL: Non-performing loans; full balance of loans with one installment 90 days or more overdue.

Press Release

June 4, 2013

Page 21 / 21

CAUTION REGARDING FORWARD-LOOKING STATEMENTS

This press release contains forward-looking statements. Forward-looking information is often, but not always, identified by the use of words such as “anticipate”, “believe”, “expect”, “plan”, “intend”, “forecast”, “target”, “project”, “may”, “will”, “should”, “could”, “estimate”, “predict” or similar words suggesting future outcomes or language suggesting an outlook. Forward-looking statements and information are based on current beliefs as well as assumptions made by and information currently available to CorpBanca concerning anticipated financial performance, business prospects, strategies and regulatory developments. Although management considers these assumptions to be reasonable based on information currently available to it, they may prove to be incorrect. By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks that predictions, forecasts, projections and other forward-looking statements will not be achieved. We caution readers not to place undue reliance on these statements as a number of important factors could cause the actual results to differ materially from the beliefs, plans, objectives, expectations and anticipations, estimates and intentions expressed in such forward-looking statements. More information on potential factors that could affect CorpBanca’s financial results is included from time to time in the “Risk Factors” section of CorpBanca’s Annual Report on Form 20-F for the fiscal year ended December 31, 2012, filed with the SEC. Furthermore, the forward-looking statements contained in this press release are made as of the date of this press release and CorpBanca does not undertake any obligation to update publicly or to revise any of the included forward-looking statements, whether as a result of new information, future events or otherwise. The forward-looking statements contained in this press release are expressly qualified by this cautionary statement.

CONTACT INFORMATION:

Eugenio Gigogne

CFO, CorpBanca

Santiago, Chile

Phone: (562) 2660-2555

investorrelations@corpbanca.cl

Claudia Labbé

Manager Investor Relations, CorpBanca

Santiago, Chile

Phone: (562) 2660-2699

claudia.labbe@corpbanca.cl

Nicolas Bornozis

President, Capital Link

New York, USA

Phone: (212) 661-7566

nbornozis@capitallink.com