Exhibit 99.2

Thispresentation includes“forward-lookingstatements”within themeaningofthePrivateSecuritiesLitigationReformActof1995,Section 27AoftheSecurities Actof1933,asamended,and Section 21E of the Securities Exchange Act of 1934, as amended, with respect toMVB’s andIFHI’s beliefs, goals, intentions, and expectations regarding the proposed transaction, pro forma financial results, future operations, andcapital ratios, among other matters; our estimatesof future costs andbenefits of the actions we may take; our ability to achieve our financial and other strategic goals; the expected timing of completion of the proposed transaction; the expected cost savings, synergies and other anticipated benefits from the proposed transaction; and other statementsthatarenothistoricalfacts. Forward‐looking statements are typically identified by such words as“believe,”“expect,”“anticipate,”“intend,”“outlook,”“estimate,”“forecast,”“project,”“should,”“will,” and other similar wordsand expressions,andaresubjectto numerousassumptions,risks,anduncertainties, whichchangeovertime.Theseforward-lookingstatementsinclude,withoutlimitation, thoserelating totheterms,timingandclosingoftheproposedtransaction. Additionally, forward‐looking statements speak only as of the date they are made; MVB and IFHI do not assume any duty, and do not undertake, to update such forward‐looking statements, whetherwritten ororal,thatmaybemadefromtimetotime,whetherasaresultofnewinformation,futureevents,orotherwise.Furthermore, becauseforward‐lookingstatementsare subjectto assumptionsanduncertainties,actualresultsorfutureeventscoulddiffer,possiblymaterially,fromthoseindicatedinsuchforward-lookingstatementsasaresultofavarietyoffactors,manyof whicharebeyondthecontrolofMVBandIFHI.Suchstatementsarebasedupon thecurrentbeliefsandexpectationsofthemanagementofMVBandIFHIandaresubjectto significantrisksand uncertaintiesoutsideofthecontroloftheparties.Cautionshouldbeexercisedagainstplacingunduerelianceonforward-lookingstatements.Thefactorsthatcouldcauseactualresultstodiffer materially include the following: the occurrence of any event, change or other circumstances that could give rise to the right of one or both of the parties to terminate the definitive merger agreementbetweenMVBandIFHI;theoutcomeofanylegalproceedingsagainstMVBorIFHI;thepossibilitythattheproposedtransactionwillnotclosewhenexpectedoratallbecauserequired regulatory, shareholder or other approvals are not received or other conditions to the closing are not satisfied on a timely basis or at all, or are obtained subject to conditions that are not anticipated(andtheriskthatrequiredregulatoryapprovalsmayresultintheimpositionofconditionsthatcouldadverselyaffectthecombinedcompanyortheexpectedbenefitsoftheproposed transaction);theabilityofMVBandIFHI to meetexpectationsregardingthetiming,completionandaccountingandtax treatmentsoftheproposedtransaction;theriskthatanyannouncements relatingto theproposedtransactioncouldhaveadverseeffectsonthemarketpriceofthecommonstockofMVB;thepossibility thattheanticipatedbenefitsoftheproposedtransactionwillnot be realized when expected or at all, including as a result of the impact of, or problems arising from, the integration of the two companies or as a result of the strength of the economy and competitive factors in the areas where MVB and IFHI dobusiness; certain restrictions during the pendency of the proposed transaction that may impact theparties’ ability to pursue certain business opportunities or strategic transactions; the possibility that the transaction may be more expensive to complete than anticipated, including as a result of unexpected factors orevents; diversionofmanagement’sattentionfromongoingbusinessoperationsandopportunities;thepossibilitythatthepartiesmaybeunabletoachieveexpectedsynergiesandoperatingefficiencies in the merger within the expected timeframes or at all and to successfully integrateIFHI’s operations and those of MVB; such integration may be more difficult, time consuming or costly than expected;revenuesfollowingtheproposedtransactionmaybelowerthanexpected;IFHI’sandMVB’ssuccessin executingtheirrespectivebusinessplansandstrategiesandmanagingtherisks involvedin the foregoing; thedilution caused byMVB’sissuanceofadditional sharesofits capital stock in connection with the proposedtransaction; effects ofthe announcement, pendencyor completionoftheproposedtransactionontheabilityofIFHIandMVBtoretaincustomersandretainandhirekeypersonnelandmaintainrelationshipswiththeirsuppliers,andontheiroperating resultsandbusinessesgenerally;risksrelatedto thepotentialimpactofgeneraleconomic,politicalandmarketfactorsonthecompaniesortheproposedtransactionandotherfactorsthatmay affect future results of IFHI and MVB; uncertainty as to the extent of the duration, scope, and impacts of the COVID-19 pandemic and the effects of inflation on IFHI, MVB and the proposed transaction;theimpactofchanginginterestratesonIFHIandMVB;andtheotherfactorsdiscussedinthe“RiskFactors”and“Management’sDiscussionandAnalysisofFinancialConditionand Results ofOperations” sections ofMVB’s Annual Report on Form 10‐K for the year ended December 31, 2021, in the“RiskFactors” and“Management’s Discussion and Analysis of Financial ConditionandResultsofOperations”sectionsofMVB’sQuarterlyReportonForm10‐QforthequarterendedJune30,2022,andinotherreportsMVBfileswiththeU.S.SecuritiesandExchange Commission(the“SEC”). 2 2

Non-GAAPFinancialMeasures Inadditionto resultspresentedinaccordancewithGAAP,thispresentationcontainscertainnon-GAAPfinancialmeasures.MVBbelievesthatprovidingcertainnon-GAAPfinancialmeasuresprovidesinvestorswithinformationuseful inunderstandingperformancetrendsand financialposition.MVBusesthesemeasuresforinternal planningandforecastingpurposes.MVBanditssecuritiesanalysts,investorsandotherinterestedparties,also usethesemeasures to reviewpeercompanyoperatingperformance.MVBbelievesthatthispresentation anddiscussion,togetherwiththeaccompanyingreconciliations,providesanunderstandingoffactorsandtrendsaffectingMVB’sbusinessesandallowsinvestorstoviewperformanceinamannersimilartomanagement.Thesenon-GAAPmeasuresshouldnotbeconsidereda substitutefor GAAPbasismeasuresandresults,andinvestorsarestrongly encouraged to reviewtheconsolidatedfinancialstatementsin theirentiretyandnotto relyonanysinglefinancial measure.Becausenon-GAAPfinancial measuresarenotstandardized, itmaynotbe possible to compare these financial measures with othercompanies’ non-GAAP financial measures having the same or similar names. Reconciliations of these non-GAAP financial measures to the most directly comparable U.S. GAAP financial measures are provided in the Appendixtothispresentation. MVBusescertainnon-GAAPfinancialmeasures,suchastangiblebookvaluepershareandtangiblecommonequitytotangibleassets,toprovideinformationusefultoinvestorsinunderstandingMVB’soperatingperformanceandtrendsandtofacilitatecomparisonswiththe performanceof its peers. The non-GAAP financial measures used may differ from the non-GAAP financial measuresother financial institutionsuse to measure their resultsof operations. Reconciliationsof these non-GAAP financial measures to the most directly comparable U.S.GAAPfinancialmeasuresareprovidedintheAppendixtothispresentation. UnauditedProspectiveFinancialInformation MVBandIFHIdonot,asa matterofcourse,publiclydiscloseforecastsorinternalprojectionsoftheirfuturefinancialperformance,revenues,earnings,financialconditionorotherresultsgiven,amongotherreasons,theinherentuncertaintyoftheunderlyingassumptionsand estimates, other than, from time to time, certain expected financial results and operational metrics for the current period and certain future periods in regular earnings press releases and other investor materials. However, MVB is including in this communication certain unauditedprospectiveinformationthatwasmadeavailableinthecourseofduediligenceandutilizedinthefairnessopinionrenderedbyitsfinancialadvisor.NeitherMVBnorIFHIendorsestheprospectivefinancialinformationasnecessarilypredictiveoffutureresults. AdditionalInformationandWheretoFindIt In connection with the proposed transaction, MVB will file a registration statement on Form S-4 with the SEC. The registration statement will include a joint proxy statement of MVB and IFHI, which also constitutes a prospectus of MVB, that will be sent toIFHI’s andMVB’s shareholdersseekingcertainapprovalsrelatedtotheproposedtransaction. Theinformationcontainedhereindoesnotconstituteanoffertosellorasolicitationofanoffertobuyanysecuritiesorasolicitationofanyvoteorapproval,norshalltherebeanysaleofsecuritiesinanyjurisdictioninwhichsuchoffer,solicitationorsalewouldbeunlawfulprior to registration or qualification under the securities lawsof any such jurisdiction. INVESTORS AND SECURITY HOLDERS OF IFHI AND MVB AND THEIR RESPECTIVE AFFILIATES ARE URGED TO READ, WHEN AVAILABLE, THE REGISTRATION STATEMENT ON FORM S-4, THE JOINT PROXYSTATEMENT/PROSPECTUSTOBEINCLUDEDWITHINTHEREGISTRATIONSTATEMENTONFORMS-4ANDANYOTHERRELEVANTDOCUMENTSFILEDORTOBEFILEDWITHTHESECINCONNECTIONWITHTHEPROPOSEDTRANSACTION,ASWELLASANYAMENDMENTSOR SUPPLEMENTS TO THOSE DOCUMENTS, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT IFHI, MVB AND THE PROPOSED TRANSACTION. Investors and security holders will be able to obtain a free copy of the registration statement, including the joint proxy statement/prospectus,aswellasotherrelevantdocumentsfiled byMVBwiththeSEC containinginformationaboutIFHIandMVB,withoutcharge, attheSEC’swebsite(http://www.sec.gov). Inaddition,copiesofdocumentsfiledwiththeSEC byMVBwillbemadeavailable freeofcharge in the“InvestorRelations”section ofMVB’swebsite, https://www.mvbbanking.com,under theheading“SEC Filings;”andinvestors mayobtainfree copiesofthejointproxy statement/prospectus (whenavailable)bycontactingIFHI,8450 Falls ofNeuseRoad, Suite202,Raleigh,NC27615,telephone:(252)482-4400. ParticipantsinSolicitation IFHI,MVB,andcertainoftheirrespectivedirectorsandexecutiveofficersmaybedeemedtobeparticipantsinthesolicitationofproxiesinrespectoftheproposedtransactionundertherulesoftheSEC. InformationregardingMVB’sdirectorsandexecutiveofficersisavailable in itsdefinitiveproxy statement, which was filedwith theSECon April7, 2022, andcertain other documents filed byMVBwiththe SEC.Other information regarding theparticipants inthe solicitation ofproxies in respectoftheproposed transaction anda descriptionoftheir direct and indirect interests, by security holdings or otherwise, will be contained in the joint proxy statement/prospectus and other relevant materials to be filed with the SEC. Free copies of these documents, when available, may be obtained as described in the preceding paragraph. 3 3

4 4

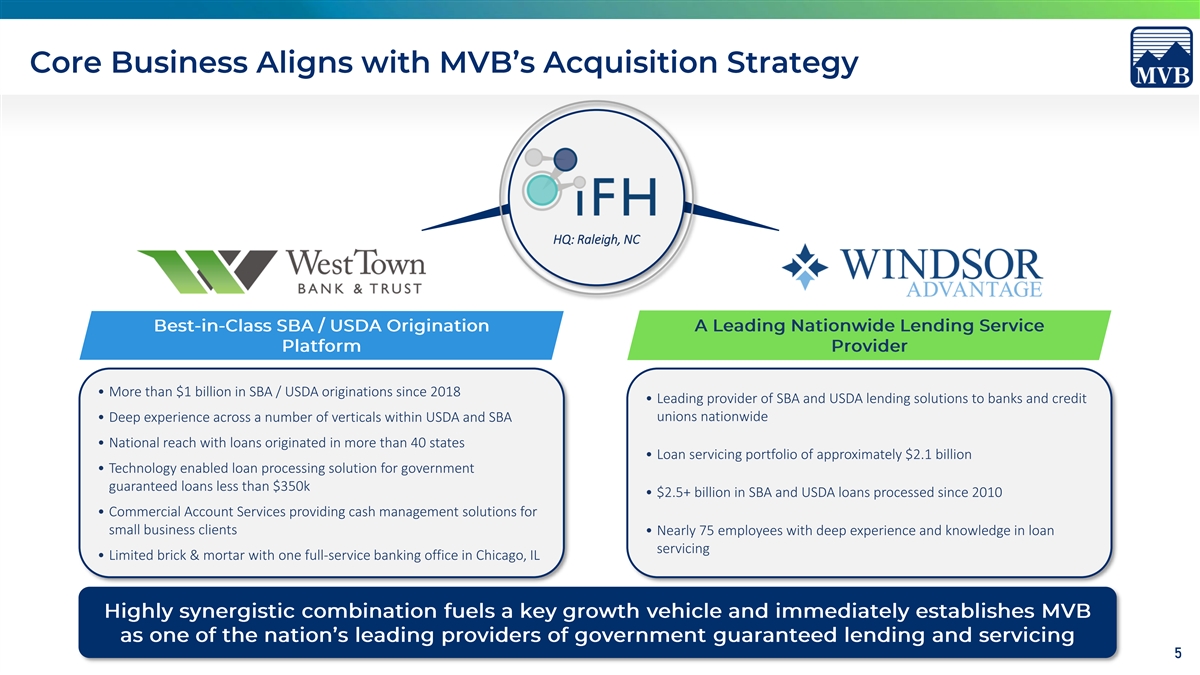

HQ: Raleigh, NC • More than $1 billion in SBA / USDA originations since 2018 • Leading provider of SBA and USDA lending solutions to banks and credit unions nationwide • Deep experience across a number of verticals within USDA and SBA • National reach with loans originated in more than 40 states • Loan servicing portfolio of approximately $2.1 billion • Technology enabled loan processing solution for government guaranteed loans less than $350k • $2.5+ billion in SBA and USDA loans processed since 2010 • Commercial Account Services providing cash management solutions for small business clients • Nearly 75 employees with deep experience and knowledge in loan servicing • Limited brick & mortar with one full-service banking office in Chicago, IL 5 5

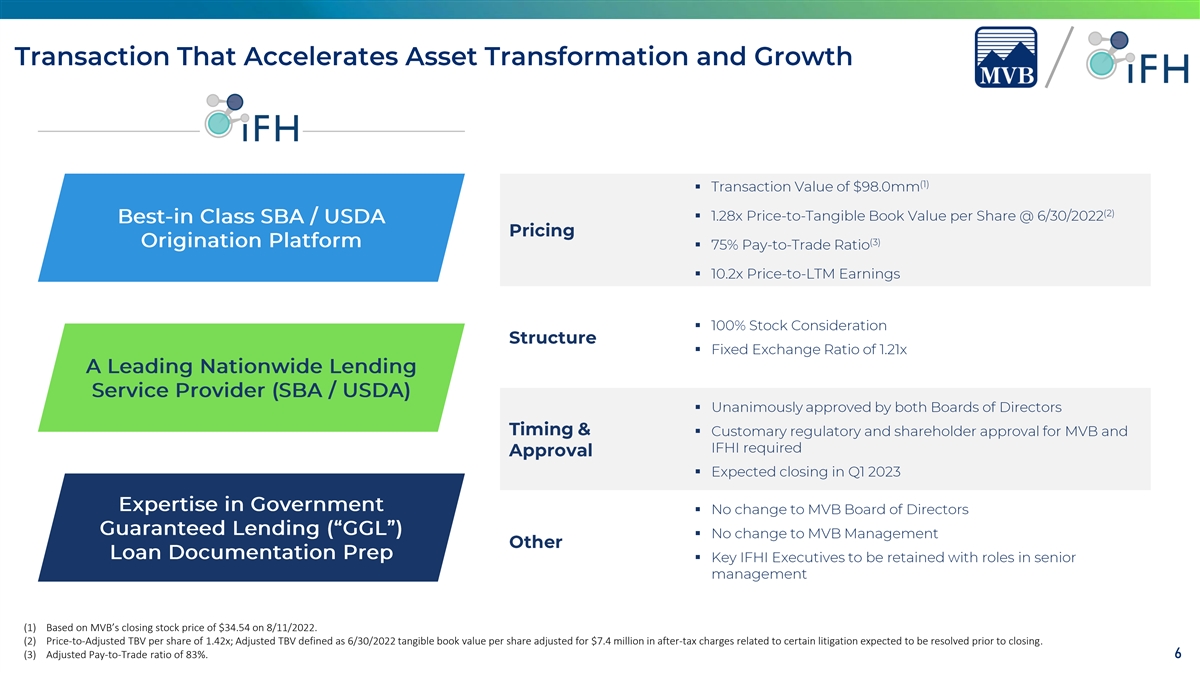

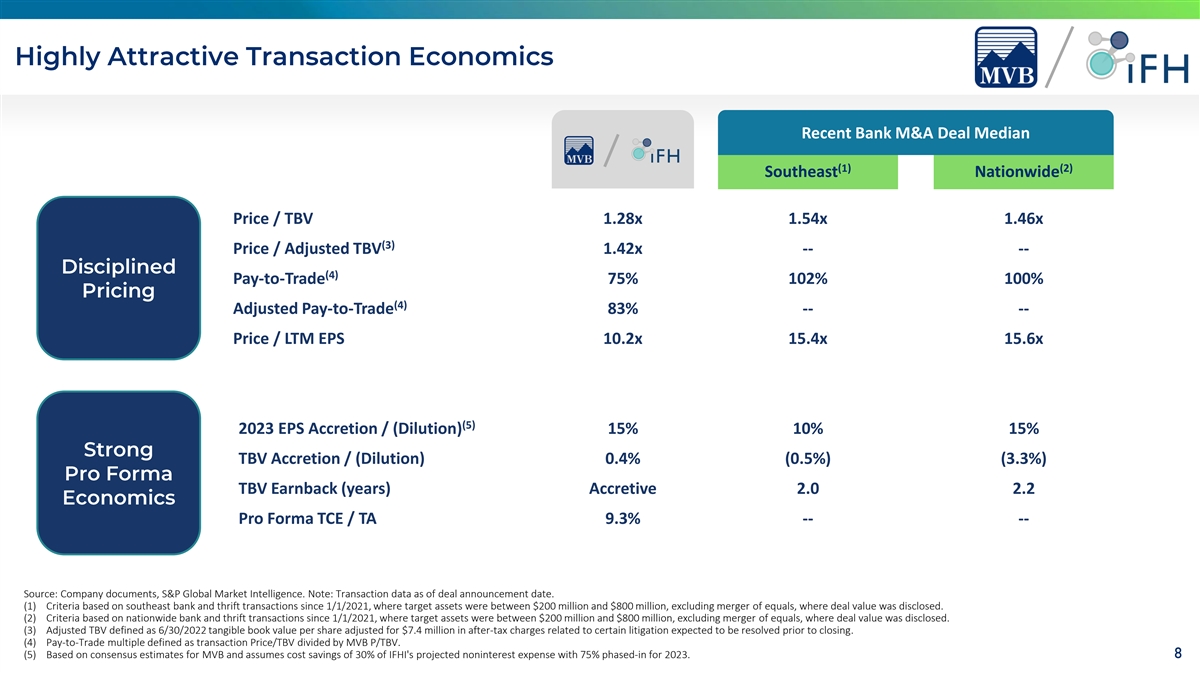

§ § § § § § § § § § § § (1) Based on MVB’s closing stock price of $34.54 on 8/11/2022. (2) Price-to-Adjusted TBV per share of 1.42x; Adjusted TBV defined as 6/30/2022 tangible book value per share adjusted for $7.4 million in after-tax charges related to certain litigation expected to be resolved prior to closing. (3) Adjusted Pay-to-Trade ratio of 83%. 66

Accelerates MVB’s F-1 Strategy to Close in on Targeted Revenue Growth § $50 million in revenue earned by IFHI for the 12 months ending 6/30/2022 § Originated more than $1 billion in GGL loans since 2018 § Will leverage best-in-class capabilities across verticals to scale GGL business and deliver superior performance Adds Talent and Infrastructure to Fuel Government Guaranteed Lending Growth Vehicle § Windsor Advantage currently services approximately $2.1 billion in loans, generating approximately $17 million in revenue for the 12 months ending 6/30/2022 § ~$60 million of loans held-for-sale as of 6/30/2022 and robust GGL origination pipeline expected to drive near-term revenue growth Strong Cultural and Operational Alignment § Committed management team focused on long-term performance with entrepreneurial spirit § Branch light model with $400mm+ assets designed to support continued operating leverage and limit expense drag § Numerous overlapping backend and IT systems provide efficiencies and realization of cost saves Compelling Financial Impact § Accretive to tangible book value per share (1) § Accretive to earnings per share § Accretive to all capital ratios to support future growth § Robust internal rate of return (IRR) and return on invested capital (ROIC) (1) Based on consensus estimates for MVB and assumes cost savings of 30% of IFHI's projected noninterest expense with 75% phased-in for 2023 and 100% thereafter. 77

Recent Bank M&A Deal Median (1) (2) Southeast Nationwide Price / TBV 1.28x 1.54x 1.46x (3) Price / Adjusted TBV 1.42x -- -- (4) Pay-to-Trade 75% 102% 100% (4) Adjusted Pay-to-Trade 83% -- -- Price / LTM EPS 10.2x 15.4x 15.6x (5) 2023 EPS Accretion / (Dilution) 15% 10% 15% TBV Accretion / (Dilution) 0.4% (0.5%) (3.3%) TBV Earnback (years) Accretive 2.0 2.2 Pro Forma TCE / TA 9.3% -- -- Source: Company documents, S&P Global Market Intelligence. Note: Transaction data as of deal announcement date. (1) Criteria based on southeast bank and thrift transactions since 1/1/2021, where target assets were between $200 million and $800 million, excluding merger of equals, where deal value was disclosed. (2) Criteria based on nationwide bank and thrift transactions since 1/1/2021, where target assets were between $200 million and $800 million, excluding merger of equals, where deal value was disclosed. (3) Adjusted TBV defined as 6/30/2022 tangible book value per share adjusted for $7.4 million in after-tax charges related to certain litigation expected to be resolved prior to closing. (4) Pay-to-Trade multiple defined as transaction Price/TBV divided by MVB P/TBV. (5) Based on consensus estimates for MVB and assumes cost savings of 30% of IFHI's projected noninterest expense with 75% phased-in for 2023. 8 8

Source: Company documents, S&P Global Market Intelligence. Note: Financials based on 6/30/2022 bank holding company data. (1) See pages 18-19 for non-GAAP reconciliations. (2) Includes ~$60 million in held-for-sale loans. (3) Pro forma totals exclude purchase accounting adjustments. (4) Pro forma projected TCE/TA at closing including purchase accounting adjustments. 99

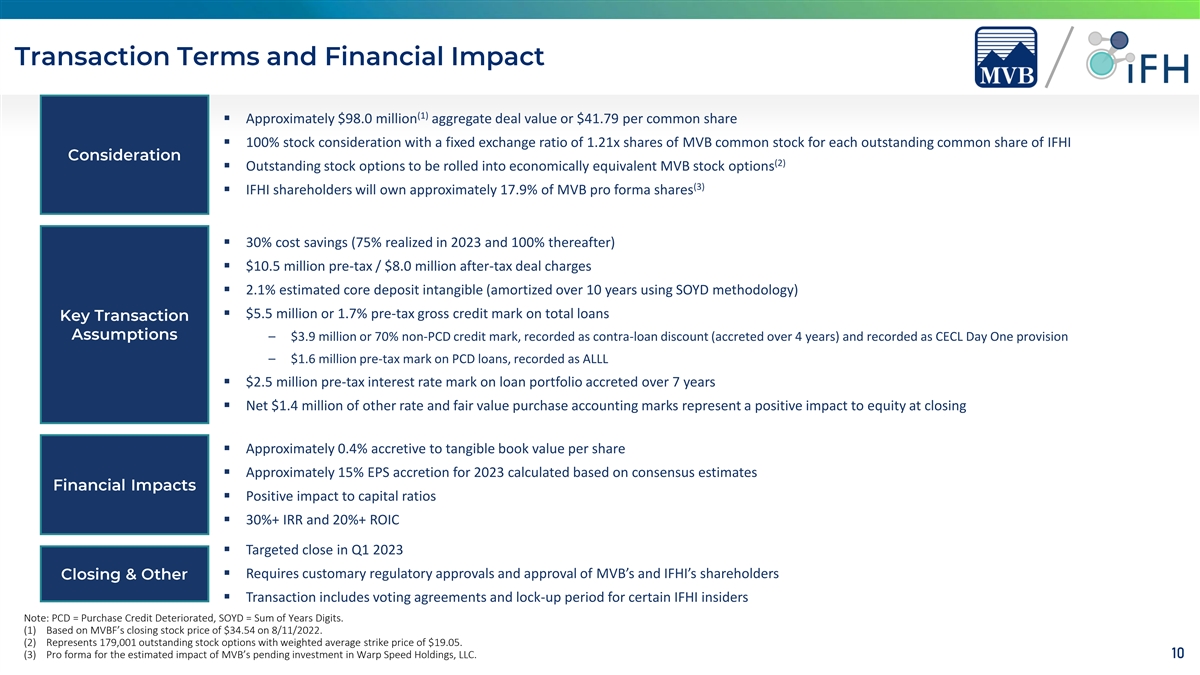

(1) § Approximately $98.0 million aggregate deal value or $41.79 per common share § 100% stock consideration with a fixed exchange ratio of 1.21x shares of MVB common stock for each outstanding common share of IFHI (2) § Outstanding stock options to be rolled into economically equivalent MVB stock options (3) § IFHI shareholders will own approximately 17.9% of MVB pro forma shares § 30% cost savings (75% realized in 2023 and 100% thereafter) § $10.5 million pre-tax / $8.0 million after-tax deal charges § 2.1% estimated core deposit intangible (amortized over 10 years using SOYD methodology) § $5.5 million or 1.7% pre-tax gross credit mark on total loans – $3.9 million or 70% non-PCD credit mark, recorded as contra-loan discount (accreted over 4 years) and recorded as CECL Day One provision – $1.6 million pre-tax mark on PCD loans, recorded as ALLL § $2.5 million pre-tax interest rate mark on loan portfolio accreted over 7 years § Net $1.4 million of other rate and fair value purchase accounting marks represent a positive impact to equity at closing § Approximately 0.4% accretive to tangible book value per share § Approximately 15% EPS accretion for 2023 calculated based on consensus estimates § Positive impact to capital ratios § 30%+ IRR and 20%+ ROIC § Targeted close in Q1 2023 § Requires customary regulatory approvals and approval of MVB’s and IFHI’s shareholders § Transaction includes voting agreements and lock-up period for certain IFHI insiders Note: PCD = Purchase Credit Deteriorated, SOYD = Sum of Years Digits. (1) Based on MVBF’s closing stock price of $34.54 on 8/11/2022. (2) Represents 179,001 outstanding stock options with weighted average strike price of $19.05. (3) Pro forma for the estimated impact of MVB’s pending investment in Warp Speed Holdings, LLC. 10 10

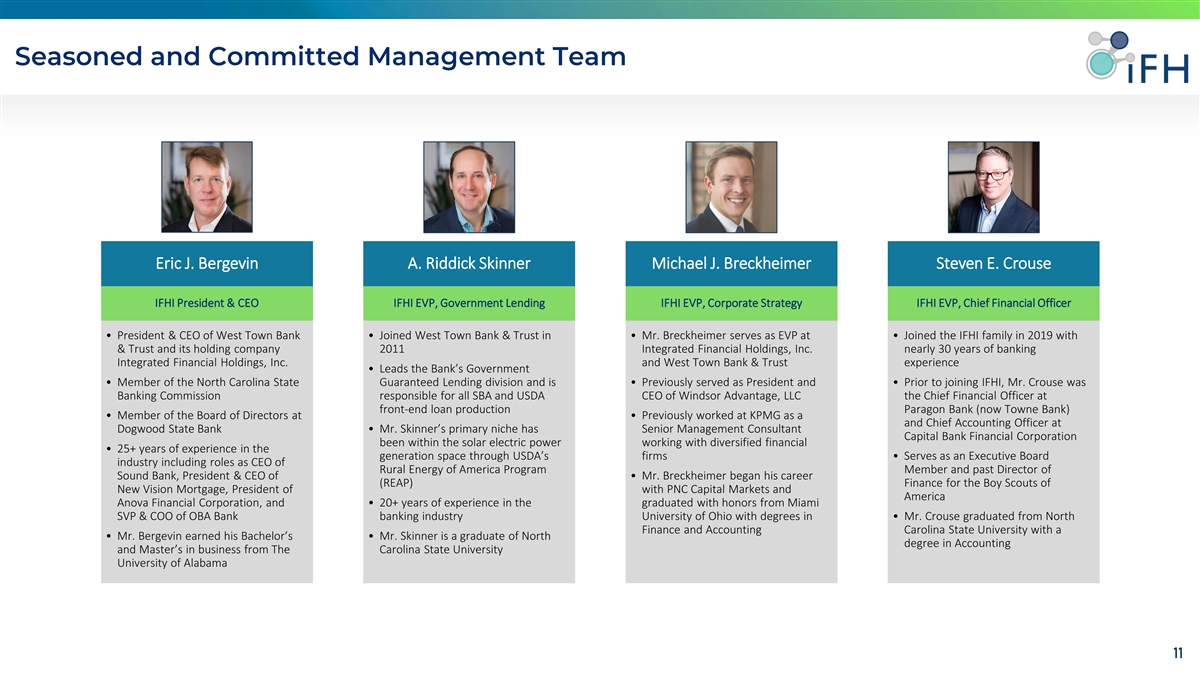

Eric J. Bergevin A. Riddick Skinner Michael J. Breckheimer Steven E. Crouse IFHI President & CEO IFHI EVP, Government Lending IFHI EVP, Corporate Strategy IFHI EVP, Chief Financial Officer • President & CEO of West Town Bank • Joined West Town Bank & Trust in • Mr. Breckheimer serves as EVP at • Joined the IFHI family in 2019 with & Trust and its holding company 2011 Integrated Financial Holdings, Inc. nearly 30 years of banking Integrated Financial Holdings, Inc. and West Town Bank & Trust experience • Leads the Bank’s Government • Member of the North Carolina State Guaranteed Lending division and is • Previously served as President and • Prior to joining IFHI, Mr. Crouse was Banking Commission responsible for all SBA and USDA CEO of Windsor Advantage, LLC the Chief Financial Officer at front-end loan production Paragon Bank (now Towne Bank) • Member of the Board of Directors at • Previously worked at KPMG as a and Chief Accounting Officer at Dogwood State Bank • Mr. Skinner’s primary niche has Senior Management Consultant Capital Bank Financial Corporation been within the solar electric power working with diversified financial • 25+ years of experience in the generation space through USDA’s firms • Serves as an Executive Board industry including roles as CEO of Rural Energy of America Program Member and past Director of Sound Bank, President & CEO of • Mr. Breckheimer began his career (REAP) Finance for the Boy Scouts of New Vision Mortgage, President of with PNC Capital Markets and America Anova Financial Corporation, and • 20+ years of experience in the graduated with honors from Miami SVP & COO of OBA Bank banking industry University of Ohio with degrees in • Mr. Crouse graduated from North Finance and Accounting Carolina State University with a • Mr. Bergevin earned his Bachelor’s • Mr. Skinner is a graduate of North degree in Accounting and Master’s in business from The Carolina State University University of Alabama 11 11

Dollars in Millions 2019 2020 2021 2022YTD Balance Sheet ($M) Total Assets $314 $389 $453 $435 Total Gross Loans 236 285 288 326 Total Deposits 220 301 348 334 Common Equity 68 77 89 93 (1) Tangible Common Equity 47 57 69 73 Profitability ($M) Net Interest Income $13.6 $14.5 $16.3 $10.4 Noninterest Income 17.2 33.5 41.1 17.1 Total Revenue 30.8 48.0 57.5 27.4 Pre-Tax Income 7.5 10.2 13.0 6.8 Profitability Metrics: ROAA 2.72 % 2.50 % 2.98 % 2.29 % ROAE 14.7 12.3 15.3 11.1 Cost of Funds 1.59 1.26 0.77 0.64 Net Interest Margin 4.82 4.76 4.31 5.60 Noninterest Income / Revenue 56.0 69.8 71.6 62.2 Asset Quality (2) 4.01 % 2.79 % 1.65 % 1.07 % NPAs / Assets Reserves / Loans Held for Investment 1.72 1.99 2.14 2.39 NCOs / Avg Loans 0.40 1.22 0.55 (0.11) Capital Ratios (1) TCE / TA (Consolidated) 16.0 % 15.3 % 15.7 % 17.6 % Tier 1 Leverage Ratio (Bank Level) 12.7 10.1 11.5 12.2 Tier 1 Capital Ratio (Bank Level) 15.0 12.0 15.9 15.5 Total Risk Based Capital Ratio (Bank Level) 16.2 13.3 17.2 16.8 Source: Company documents, S&P Global Market Intelligence. Note: 2022YTD period represents financial data for the six months ending 6/30/2022. (1) See page 18 for a non-GAAP reconciliation. (2) NPAs / Assets excludes restructured loans from nonperforming assets. 12 12

Assets & Loans Net Interest Income & Noninterest Income (Dollars in Millions) (Dollars in Millions) Assets Loans Held-for-Investment Loans Held-for-Sale Net Interest Income Noninterest Income $41.1 $453 $435 $33.5 $389 $326 $314 $288 $285 $236 $17.2 $17.1 $16.3 $14.5 $13.6 $10.4 2019 2020 2021 2022YTD 2019 2020 2021 2022YTD 2019 2020 2021 2022YTD Total Revenue Noninterest Income / Revenue (%) (Dollars in Millions) 71.6% $57.5 69.8% 62.2% $48.0 56.0% $30.8 $27.4 2019 2020 2021 2022YTD 2019 2020 2021 2022YTD Source: Company documents, S&P Global Market Intelligence. Note: 2022YTD period represents financial data for the six months ending 6/30/2022. 13 13

Gross Loans Total Deposits Consumer, Home Equity & Construction & Land Other 4.6% Noninterest- 1.6% Jumbo Time Residential Deposits bearing Mortgage Deposits 23.2% 10.7% 25.7% Owner- Occupied CRE 23.4% C & I 56.4% Retail Time IB Demand, Nonowner- Savings & Occupied CRE Deposits MMDA 2.2% 30.2% Multifamily 20.9% 1.1% Credit Metrics Deposit Highlights ü ü § Source: Company documents, S&P Global Market Intelligence. Note: Bank-level data as of 6/30/2022. (1) NPAs / Assets excludes restructured loans from nonperforming assets. (2) For the twelve months ended 6/30/2022. 14 14

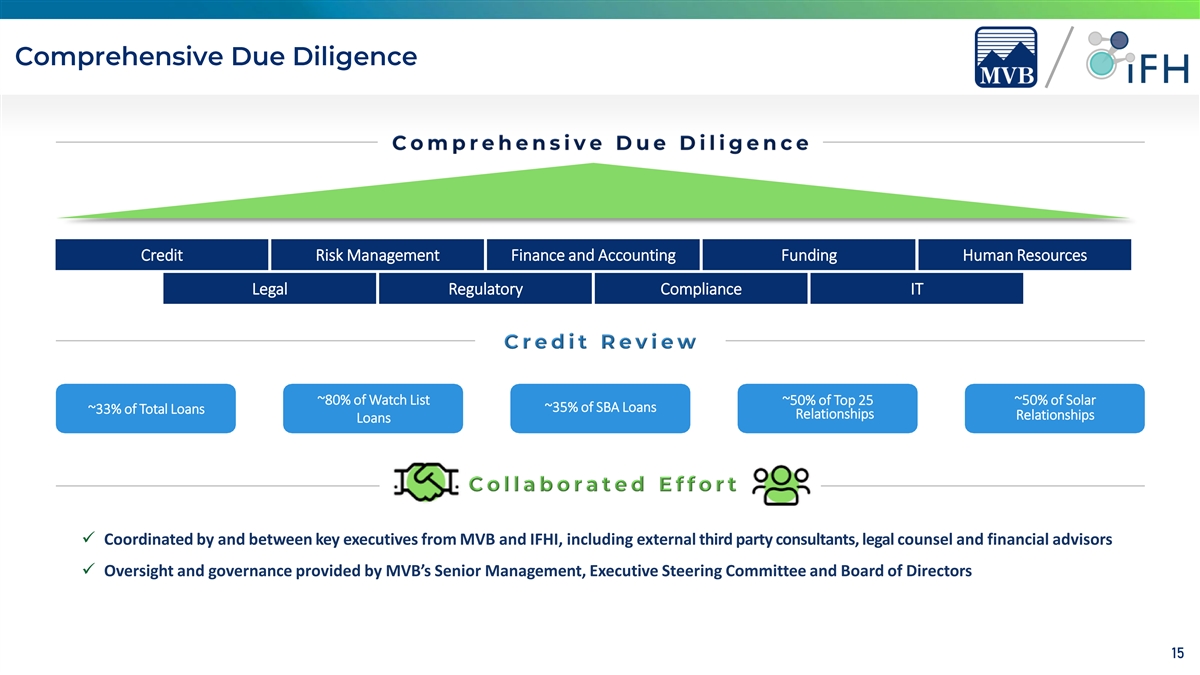

Credit Credit Risk Management Finance and Accounting Funding Human Resources Legal Regulatory Compliance IT ~80% of Watch List ~50% of Top 25 ~50% of Solar ~35% of SBA Loans ~33% of Total Loans Relationships Relationships Loans ü Coordinated by and between key executives from MVB and IFHI, including external third party consultants, legal counsel and financial advisors ü Oversight and governance provided by MVB’s Senior Management, Executive Steering Committee and Board of Directors 15 15

16 16

17

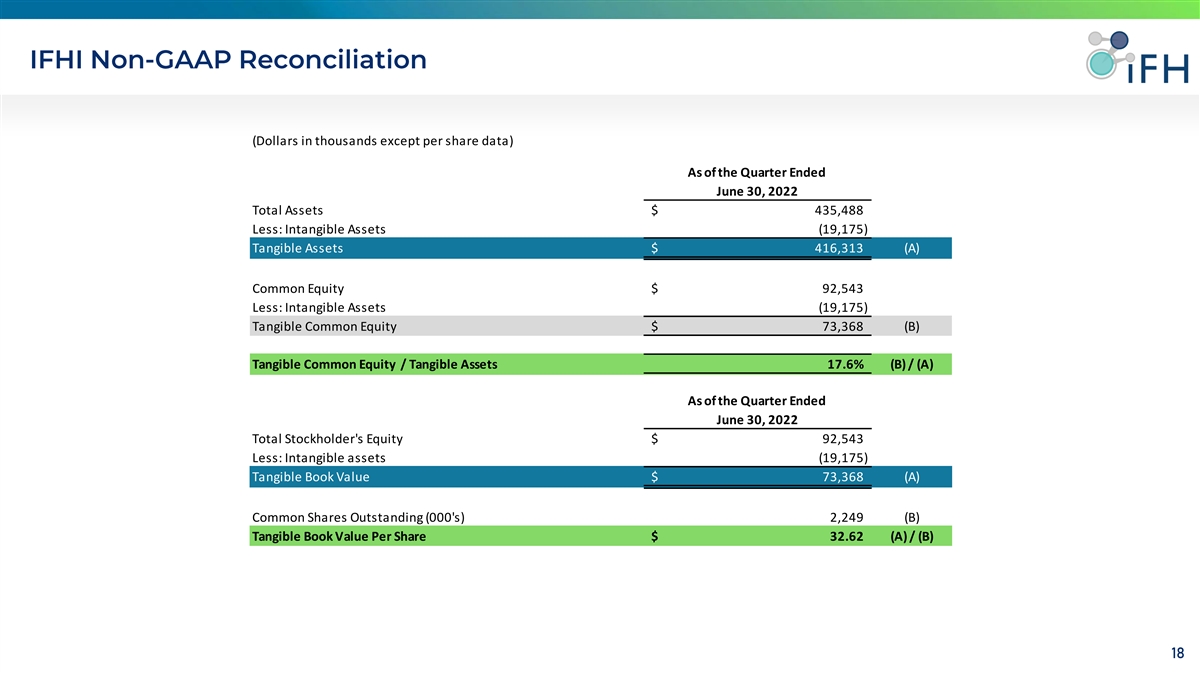

(Dollars in thousands except per share data) As of the Quarter Ended June 30, 2022 Total Assets $ 435,488 Less: Intangible Assets (19,175) Tangible Assets $ 4 16,313 (A) Common Equity $ 92,543 Less: Intangible Assets (19,175) Tangible Common Equity $ 7 3,368 (B) Tangible Common Equity / Tangible Assets 17.6% (B) / (A) As of the Quarter Ended June 30, 2022 Total Stockholder's Equity $ 92,543 Less: Intangible assets (19,175) Tangible Book Value $ 7 3,368 (A) Common Shares Outstanding (000's) 2,249 (B) Tangible Book Value Per Share $ 3 2.62 (A) / (B) 18 18

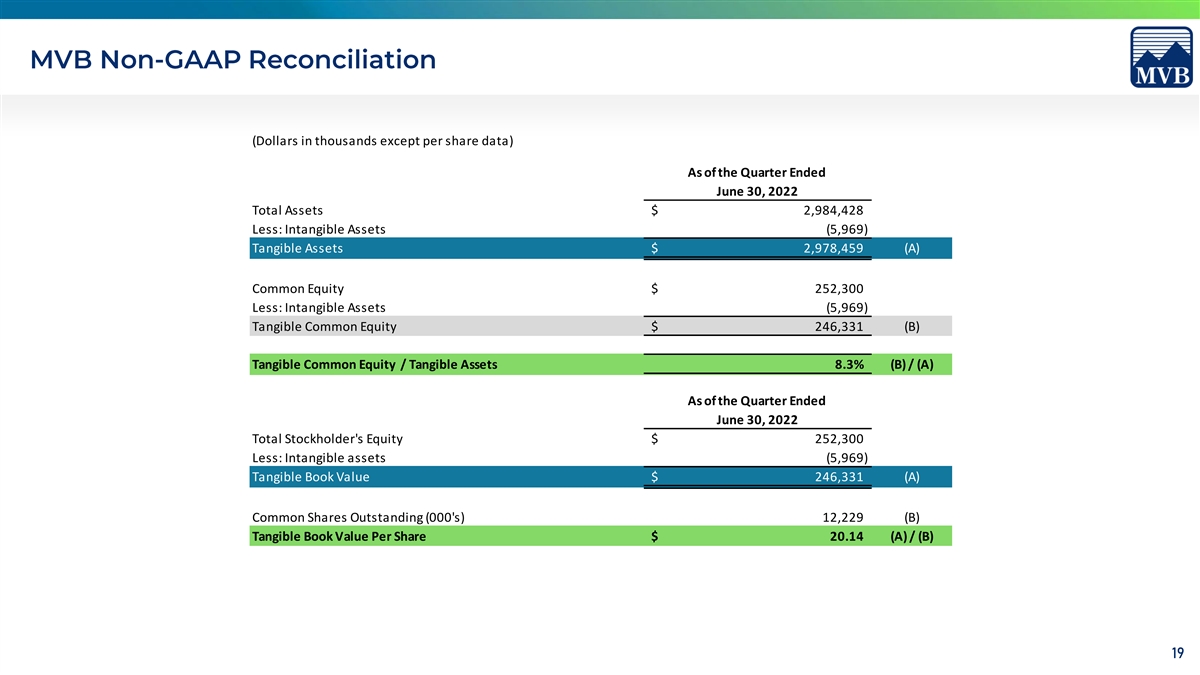

(Dollars in thousands except per share data) As of the Quarter Ended June 30, 2022 Total Assets $ 2,984,428 Less: Intangible Assets (5,969) Tangible Assets $ 2,978,459 (A) Common Equity $ 2 52,300 Less: Intangible Assets (5,969) Tangible Common Equity $ 2 46,331 (B) Tangible Common Equity / Tangible Assets 8.3% (B) / (A) As of the Quarter Ended June 30, 2022 Total Stockholder's Equity $ 252,300 Less: Intangible assets (5,969) Tangible Book Value $ 2 46,331 (A) Common Shares Outstanding (000's) 1 2,229 (B) Tangible Book Value Per Share $ 2 0.14 (A) / (B) 19 19