As filed with the Securities and Exchange Commission on December 14, 2004

Registration No. 333-

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Dex Media West LLC

Dex Media West Finance Co.

(Exact names of registrants as specified in their charters)

| | |

Dex Media West LLC Delaware | | Dex Media West Finance Co. Delaware |

(State or other jurisdiction of incorporation or organization) | | (State or other jurisdiction of incorporation or organization) |

| |

| 25-1903487 | | 20-0137059 |

| (I.R.S. Employer Identification No.) | | (I.R.S. Employer Identification No.) |

| |

| 2741 | | 9995 |

| (Primary Standard Industrial Classification Code Number) | | (Primary Standard Industrial Classification Code Number) |

198 Inverness Drive West

Englewood, Colorado 80112

(303) 784-2900

(Address, including zip code, and telephone number, including area code, of each of the registrants’ principal executive offices)

Robert M. Neumeister, Jr.

Executive Vice President and Chief Financial Officer

Dex Media West LLC

198 Inverness Drive West

Englewood, Colorado 80112

(303) 784-2900

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Gregory A. Ezring, Esq.

Monica K. Thurmond, Esq.

Latham & Watkins LLP

885 Third Avenue

Suite 1000

New York, New York 10022

(212) 906-1200

Approximate date of commencement of proposed exchange offer: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

CALCULATION OF REGISTRATION FEE

| | | | | | | | |

Title of Each Class of Securities to be Registered | | Amount to be Registered | | Proposed Maximum Offering Price Per Note(1) | | Proposed Maximum Aggregate Offering Price(1) | | Amount of Registration Fee |

5 7/8% Senior Notes due 2011 | | $300,000,000 | | 100% | | $300,000,000 | | $35,310.00 |

| (1) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(f) under the Securities Act. |

The registrants hereby amend this registration statement on such date or dates as may be necessary to delay its effective date until the registrants shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED DECEMBER 14, 2004.

PROSPECTUS

Dex Media West LLC

Dex Media West Finance Co.

Offer to Exchange

$300,000,000 principal amount of their 5 7/8% Series B Senior Notes due 2011,

which have been registered under the Securities Act,

for any and all of their outstanding 5 7/8% Series A Senior Notes due 2011.

We are offering to exchange our 5 7/8% Series B Senior Notes due 2011, or the “exchange notes,” for our currently outstanding 5 7/8% Series A Senior Notes due 2011, or the “outstanding notes.” The exchange notes are substantially identical to the outstanding notes, except that the exchange notes have been registered under the federal securities laws and will not bear any legend restricting their transfer. The exchange notes will represent the same debt as the outstanding notes, and we will issue the exchange notes under the same indenture.

The exchange notes will be guaranteed on a senior unsecured basis by each of our future subsidiaries that is a guarantor or direct borrower under our credit facilities. We currently do not have any subsidiaries other than Dex Media West Finance Co., which is our wholly owned subsidiary that was incorporated in Delaware for the purpose of serving as a co-issuer of the notes.

The principal features of the exchange offer are as follows:

| | • | The exchange offer expires at 12:00 midnight, New York City time, on , 2005, unless extended. |

| | • | We will exchange all outstanding notes that are validly tendered and not validly withdrawn prior to the expiration of the exchange offer. |

| | • | You may withdraw tendered outstanding notes at any time prior to the expiration of the exchange offer. |

| | • | The exchange of outstanding notes for exchange notes pursuant to the exchange offer will not be a taxable event for U.S. federal income tax purposes. |

| | • | We will not receive any proceeds from the exchange offer. |

| | • | We do not intend to apply for listing of the exchange notes on any securities exchange or automated quotation system. |

Each broker-dealer that receives exchange notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of such exchange notes. The letter of transmittal delivered with this prospectus states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an “underwriter” within the meaning of the Securities Act of 1933. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of exchange notes received in exchange for outstanding notes where such outstanding notes were acquired by such broker-dealer as a result of market-making activities or other trading activities. We have agreed that, for a period of 180 days after the completion of the exchange offer, we will make this prospectus available to any broker-dealer for use in connection with any such resale. See “Plan of Distribution.”

Investing in the exchange notes involves risks.

See “Risk Factors” beginning on page 17.

Neither the U.S. Securities and Exchange Commission nor any other federal or state agency has approved or disapproved of these securities to be distributed in the exchange offer, nor have any of these organizations determined that this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2004.

TABLE OF CONTENTS

Until , 2005, all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

We have not authorized any dealer, salesman or other person to give any information or to make any representation other than those contained or incorporated by reference in this prospectus. You must not rely upon any information or representation not contained or incorporated by reference in this prospectus as if we had authorized it. This prospectus does not constitute an offer to sell or a solicitation of an offer to buy any securities other than the registered securities to which it relates, nor does this prospectus constitute an offer to sell or a solicitation of an offer to buy securities in any jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such jurisdiction.

Prospectus Summary

This summary highlights information contained elsewhere in this prospectus. Because this is only a summary, it does not contain all of the information that may be important to you. This prospectus includes specific terms of the exchange offer, as well as information regarding our business and detailed financial data. The information regarding our business and the detailed financial data, while important to an understanding of our future cost structure, results of operations, financial position and cash flows, does not directly impact your decision as to whether or not to participate in the exchange offer. Information directly relating to the exchange offer can be found in this summary under the subheadings “—The Offering,” “—The Exchange Offer,” “—Terms of the Exchange Notes,” and elsewhere in this prospectus under the headings “The Exchange Offer” and “Description of Exchange Notes.” You should read this entire prospectus and should consider, among other things, the matters set forth under the headings “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes thereto appearing elsewhere in this prospectus.

In this prospectus:

| | • | “We,” “our” or “us” refers to our predecessor, Dex West, for periods prior to September 9, 2003, and refers to Dex Media West LLC (formerly known as GPP LLC) (“Dex Media West”), a co-issuer of the notes, for periods after September 9, 2003. In addition, where the context so requires, “we,” “our” or “us” refers to Dex Media West and Dex West collectively; |

| | • | “Dex West” and “Predecessor” refer to the historical operations of Qwest Dex Holdings, Inc. and its subsidiary in Arizona, Idaho, Montana, Oregon, Utah, Washington and Wyoming prior to September 9, 2003, the date that Dex Media West acquired Dex West; |

| | • | “Dex Media East” refers to Dex Media East LLC, an indirect subsidiary of Dex Media, Inc.; |

| | • | “Dex Media” refers to Dex Media, Inc., the indirect parent of Dex Media West and Dex Media East; |

| | • | “Issuers” refers to Dex Media West and Dex Media West Finance Co. (“Dex Media West Finance”); |

| | • | “Qwest” refers to Qwest Communications International Inc. and its subsidiaries, other than Qwest Corporation; |

| | • | “Qwest LEC” refers to Qwest Corporation, the local exchange carrier subsidiary of Qwest; |

| | • | “Seller” refers to Qwest Dex, Inc.; |

| | • | “Predecessor Period” refers to the period from January 1, 2003 through September 9, 2003; |

| | • | “Successor Period” refers to the period from September 10, 2003 through December 31, 2003; |

| | • | “Combined Year 2003” refers collectively to the combined Predecessor Period and Successor Period; |

| | • | “Parent Notes” refers collectively to the 8% Notes due 2013 and the 9% Discount Notes due 2013 that were issued by Dex Media on November 10, 2003 and the 9% Discount Notes due 2013 that were issued by Dex Media on February 11, 2004; |

| | • | “outstanding notes” refers to the 5 7/8% Series A Senior Notes due 2011 that were issued by the Issuers on November 24, 2004; |

| | • | “exchange notes” refers to the 5 7/8% Series B Senior Notes due 2011 offered by the Issuers pursuant to this prospectus; |

| | • | “notes” refers collectively to the outstanding notes and the exchange notes; and |

| | • | “directory” refers to telephone directory. |

1

Background Information

On August 19, 2002, Dex Holdings LLC, the parent of Dex Media, entered into two purchase agreements with Qwest to acquire the directory businesses of Qwest Dex, Inc., the directory services subsidiary of Qwest, in two separate phases. In connection with the first phase, Dex Holdings LLC assigned its right to purchase the directory businesses in Colorado, Iowa, Minnesota, Nebraska, New Mexico, North Dakota and South Dakota, or the “Dex East States,” to its indirect subsidiary, Dex Media East. Dex Media East LLC consummated the first phase of the acquisition on November 8, 2002 and currently operates the acquired directory businesses in the Dex East States. In connection with the second phase, Dex Holdings LLC assigned its right to purchase the directory businesses in Arizona, Idaho, Montana, Oregon, Utah, Washington and Wyoming, or the “Dex West States,” to us and we consummated the second phase of the acquisition on September 9, 2003. We operate the directory businesses that we acquired in the Dex West States.

We have operated as a stand-alone company since September 9, 2003. The historical information, including the historical financial data, included in this prospectus for periods prior to September 9, 2003 is that of our predecessor, Dex West. The acquisition has been accounted for under the purchase method of accounting. Under this method, the pre-acquisition deferred revenue and related deferred costs associated with directories that were published prior to the acquisition date were not carried over to our balance sheet. The effect of this accounting treatment is to reduce revenue and related costs that would otherwise have been recognized during the twelve months subsequent to the acquisition date. The unaudited pro forma financial information included elsewhere in this prospectus eliminates the effects of these adjustments to deferred revenue and related deferred expenses at the acquisition date. This pro forma financial information presents the results of operations for the year ended December 31, 2003 as if the acquisition had occurred on the first day of the applicable period. Pro forma financial information in this prospectus has been derived from this information. For purposes of comparison in this prospectus, we have also provided the combined results of the Predecessor Period and Successor Period, which include the effects of purchase accounting, to provide additional information about our results.

Our Company

We are the exclusive publisher of the “official” yellow pages and white pages directories for Qwest in the Dex West States. Our contractual agreements with Qwest grant us the right to be the exclusive incumbent publisher of the “official” yellow pages and white pages directories for Qwest in the Dex West States until November 2052 and prevent Qwest from competing with us in the directory products business in the Dex West States until November 2042.

We seek to bring buyers together with our advertising customers through a cost-effective, bundled advertising solution that includes print, CDROM and Internet-based directories. We generate our revenues primarily through the sale of print directory advertising. For the year ended December 31, 2003, after giving pro forma effect to the transactions related to the acquisition of Dex West, we generated $918.0 million in revenue, $519.1 million in EBITDA and $28.1 million in net income. For the nine months ended September 30, 2004, we generated approximately $646.0 million in revenue, $345.4 million in EBITDA and $1.9 million in net loss. Our ability to generate EBITDA, along with low capital expenditure requirements and cash income taxes, allows our business to provide significant free cash flow. See “—Summary Historical and Pro Forma Financial Data.”

For the Combined Year 2003, we published 112 directories and distributed approximately 23 million copies of these directories to business and residential customers throughout the Dex West States. In addition, our Internet-based directory, DexOnline.com, which provides an integrated complement to our print directories, includes more than 15 million business listings and 200 million residential listings from across the United States. Approximately 96% of our revenue from directory services for the Combined Year 2003 came from the sale of advertising in yellow pages directories, and approximately 4% of our revenue from directory services for the same period came from the sale of advertising in white pages directories.

2

We believe that our advertising customers value: (i) our lower cost per usage versus other directories and higher return on investment than other forms of local advertising; (ii) our broad distribution to potential buyers of our advertisers’ products and services; (iii) our ability to provide potential buyers with an authoritative reference source to search for products and services; and (iv) the quality of our client service and support. We have advertising customers across a diverse range of industries and we believe our customer retention rates exceed the averages of other incumbent publishers, or those owned by or affiliated with incumbent local exchange carriers. In 2003, we had over 200,000 local advertising accounts consisting primarily of small and medium-sized businesses and over 4,000 national advertising accounts. As a result of our conversion to the Amdocs software system, certain of our customer account categories will be reclassified, which may result in a change in how we report our total number of customer accounts.

Our Industry

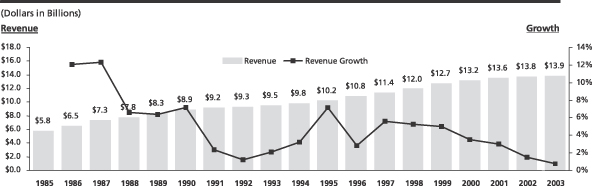

The U.S. directory advertising industry generated approximately $14 billion in revenues in 2003 and has been characterized by stability and revenue growth in every year since 1985. Unlike overall advertising spending, directory advertising revenues have grown despite changes in the U.S. economy’s business cycle. For example, during the last two recessions in 1991 and 2001, the U.S. directory advertising industry experienced positive growth, while other major advertising media, including radio, television and newspapers, experienced revenue declines.

We believe that this growth is a result of several advantages that directory advertising has relative to other forms of advertising. First, directory advertising is often the primary form of paid advertising used by small and medium-sized businesses due to its low cost relative to other media, broad demographic distribution, enduring presence and high usage rates. Second, we believe that directory advertising is attractive to businesses looking to advertise their products or services because consumers generally view telephone directories as a free, comprehensive, single source of information. Third, we believe that the “directional” nature of directory advertising is especially valuable to advertisers because directory advertisements reach consumers at a time when buyers are actively seeking information and are prepared to make a purchase. Finally, we believe that directory advertising generates a higher return on investment for small and medium-sized businesses than most other major media, including newspapers, television, radio and the Internet.

Over the past decade, growth by independent publishers and out-of-territory expansion by some incumbent publishers have significantly increased competition in the directory advertising industry. However, the directory advertising industry is still largely dominated by the incumbent publishers, as evidenced by their generating approximately 86% of the industry’s total revenue in 2003.

Our Strengths

While the directory advertising industry has become increasingly competitive, we believe that we possess the following strengths that will enable us to continue to compete successfully in the local advertising market:

| | • | Scale and leading market position.We are the largest directory publisher and the exclusive directory publisher for Qwest in the Dex West States. We believe that our scale and our incumbent position provide us with a substantial competitive advantage over independent directory advertising providers. Further, both our strong brand and long history as the incumbent yellow pages directory positions us as the “official” directory for both consumers and local advertisers, many of whom select our directories as their primary advertising medium. |

| | • | Superior value proposition for our target advertisers.We believe that directory advertising provides our target advertisers with a greater value proposition than other media. We believe that our directory advertising has a lower cost per usage than other competing directories and higher return on investment than other local advertising alternatives, including newspapers, television, radio and the Internet. |

3

| | • | Established and experienced sales force.As of September 30, 2004, we had 553 sales representatives who have been employed by Dex Media for an average of nine years. We believe that our sales force’s experience, tenure and local market knowledge is a competitive advantage which has enabled us to develop longstanding relationships with our advertisers and has been a key factor in our ability to exceed the average revenue growth of the incumbent industry for the Combined Year 2003. |

| | • | Stable and recurring revenue.Our Business produces stable and recurring revenue because of our large diversified customer base, high account retention and renewal rates and limited exposure to national advertising. For the Combined Year 2003, our account renewal rate was 91%, no single account contributed more than 0.4% of total revenue (excluding Qwest) and no single directory heading contributed more than 2.7% of total revenue. |

| | • | Strong financial profile generates significant free cash flow.Our Business generates significant free cash flow due to its recurring revenue combined with the high margins associated with our incumbent position, low capital expenditures and favorable tax position. For the nine months ended September 30, 2004, we generated $206.2 million in cash provided by operating activities and $180.6 million in free cash flow. For the year ended December 31, 2003, on a pro forma basis giving effect to the transactions related to the acquisition of Dex West, we generated $519.1 million in EBITDA and $28.1 million in net loss from $918.0 million of revenue. For the nine months ended September 30, 2004, we generated $345.4 million in EBITDA and $1.9 million in net loss from $646.0 million of revenue. Over the past three years ending December 31, 2003, we have invested an average of $19.3 million per year in capital expenditures on a combined basis, including capitalized software development costs. We also benefit from the favorable income tax treatment associated with the $4.2 billion step-up in the tax basis of our assets from the acquisition of Dex West, which is amortized for tax purposes on a straight-line basis for 15 years. In the nine months ended September 30, 2004, our free cash flow, along with a portion of the net proceeds related to Dex Media’s initial public offering, allowed us to repay $188.2 million of our indebtedness. |

| | • | Experienced management team.We have assembled a strong and experienced senior management team across all areas of our organization, including sales, finance, operations, marketing and customer service. Our senior management team has an average of approximately 20 years of experience in their respective areas of expertise. |

Our Strategy

We intend to leverage our incumbent position and strong brand while maintaining an entrepreneurial culture that encourages our employees to identify and capitalize on new opportunities to enhance our position in the Dex West States. We believe that our directory advertisements enable our customers to connect with potential buyers in a very cost effective manner, which, when combined with our competitive strengths, will allow us to grow our revenues and cash flows. The principal elements of our business strategy include:

| | • | Introducing new products that enhance the value proposition for our customers. We have a long history of introducing and selling new products, product extensions and other innovations that offer creative opportunities for our advertisers to find new customers and generate additional revenue for their products and services. As the incumbent directory publisher in the Dex West States, we have a large number of existing advertisers to whom we can effectively market our new products to generate additional revenue. We believe that our ability to innovate our product line will continue to serve as a competitive advantage. |

| | • | Increasing revenue and customer growth through segmented pricing.Historically, the directory advertising industry has utilized a simplified approach to pricing, with set rates based upon the size and features (e.g., use of color, graphics, etc.) of the advertisement regardless of heading category. We are now instituting a more sophisticated pricing strategy, which prices advertisements by heading category. We believe that implementing this strategy will improve revenue growth by allowing us to respond to the different demand characteristics of various heading categories and to better align our pricing with our customers’ perceptions of value. |

4

| | • | Further penetrating our addressable markets through enhanced sales force productivity. We believe a significant opportunity exists for our established local sales force to further penetrate the addressable markets that we serve and increase the sales of our services to existing customers. Over the past year, we have taken a number of steps to improve sales force effectiveness including: (i) servicing our customers on a more cost-effective means based on the revenue generated by such customers, (ii) rescheduling the launch and duration of sales campaigns to maximize available selling days and (iii) implementing standardized sales practices and procedures across all markets. |

| | • | Increasing the value proposition for our customers through a content-driven Internet strategy. We currently provide an Internet-based directory, DexOnline.com, which includes fully searchable content derived from more than 240,000 yellow pages display advertisements from our directories. The site incorporates free text search capabilities, with a single search box that is similar in design and functionality to popular search engines. We believe that the competitive advantage of DexOnline.com versus search engines is that our content is structured to deliver information on local services and products. We are also reviewing opportunities to expand our electronic product line in appropriately structured and cost-effective relationships with other Internet directory providers, portals and search engines. We are committed to developing these opportunities in a manner that will benefit us, and at a scale which is justified by usage and utility to our advertisers. |

| | • | Strengthen our competitive position by aggressively promoting our superior value proposition. We are investing in brand awareness campaigns that reinforce the benefits that our directories and DexOnline.com offer to advertisers and consumers. Our marketing plan highlights the advantages we enjoy as an incumbent publisher by positioning us as the “official” directory with the broad distribution, high usage and low cost per usage, which are attributes that advertisers require. |

| | • | Enhancing our operational efficiency by converting to the Amdocs software system. We are in the process of migrating from our legacy process management infrastructure to Amdocs, an industry-standard software system, that will allow us to better manage every aspect of our production cycle from initial sales call through distribution of our directories. We expect the implementation of this system will allow us to improve our operational efficiency and benefit from the associated cost savings. |

The Acquisition Transactions

The transactions summarized below, pursuant to which we became a stand-alone company, include the acquisition of Dex West, the issuance of our outstanding 8 1/2% senior notes and 9 7/8% senior subordinated notes, borrowings under our credit facilities and the equity contribution by the Sponsors and their assignees and designees. We refer to these transactions in this prospectus as the transactions related to the acquisition of Dex West.

On August 19, 2002, Dex Holdings, which is equally controlled by The Carlyle Group, or “Carlyle,” and Welsh, Carson, Anderson & Stowe, or “WCAS,” and is the parent of Dex Media, entered into two purchase agreements with Qwest to acquire the directory businesses of Qwest Dex, the directory services subsidiary of Qwest, for an aggregate consideration of $7.1 billion (excluding fees and expenses). The acquisition was structured to be completed in two phases to accommodate the regulatory requirements in the applicable states. In the first phase, consummated on November 8, 2002, Dex Media East acquired Qwest Dex’s directory businesses in the Dex East States for a total consideration to Seller of approximately $2.8 billion (excluding fees and expenses), which it currently operates. In 2003, Dex Media East published 147 directories and distributed approximately 20 million copies of these directories in metropolitan areas and local communities in the Dex East States. As of December 31, 2003, Dex Media East had a total of 197,000 local advertising accounts consisting primarily of small and medium-sized businesses. In the second phase, consummated on September 9, 2003, we acquired Qwest Dex’s directory businesses in the Dex West States, which we currently operate, for a total consideration to Seller of approximately $4.3 billion (excluding fees and expenses), of which Dex Media East paid $210.0 million.

5

Upon the consummation of the acquisition on September 9, 2003, we became a stand-alone company separate from Qwest. In this prospectus, we have made certain estimates of stand-alone costs associated with operating as a separate entity from Qwest. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

In connection with the acquisition of Dex West, our contractual agreement with Qwest grants us the exclusive right to be its and its successors’ and assignees’ official directory publisher in the Dex West States until November 7, 2052 and Qwest has agreed not to compete with us in the directory products business in the Dex West States until November 7, 2042.

Management personnel providing services to us are currently employed by Dex Media and made available to us and Dex Media East. As of January 1, 2004, non-senior management personnel providing services to us are currently employed by Dex Media Service LLC, a bankruptcy-remote entity owned 49% by Dex Media West, Inc., 49% by Dex Media East, Inc. and 2% by Dex Media and are made available to us and Dex Media East. Dex Media Service LLC was formed as a bankruptcy-remote entity pursuant to the terms of our credit facilities and Dex Media East’s credit facilities in order to mitigate the risk of not having available to us or Dex Media East the services of our non-management employees if the other entity merges, is acquired or files for bankruptcy. In the case of management personnel and non-management personnel providing services solely to us, 100% of the actual cost incurred to employ such individuals is allocated to us. If an individual provides services both to us and to Dex Media East, to the extent that a specified percentage of use of such shared individual can be determined, our specified portion of the actual cost incurred to employ such individuals is allocated to us. All other portions of the actual cost incurred to employ the shared individuals that cannot be allocated as described above are allocated between us and Dex Media East in proportion to our relative revenues. See “The Acquisition Transactions—Agreements Between Us and Our Affiliates—Employee Cost Sharing Agreement.”

As of September 30, 2004, Dex Media and its subsidiaries, including us, had consolidated indebtedness of $5,839 million, including total indebtedness of Dex Media East of $1,790 million.

Recent Developments

Amendment of Our Credit Agreement

We used the proceeds of the offering of the outstanding notes to repay Tranche A term loans under our credit facilities, which are provided by a syndicate of Lenders led by JPMorgan Chase Bank, N.A., as administrative and collateral agent, and Bank of America, N.A., Lehman Commercial Paper, Inc., Wachovia Bank, National Association and Deutsche Bank Trust Company Americas, as co-syndication agents. In connection with the offering, we amended this facility to, among other things, allow for a repricing of our Tranche B term loans.

Dex Media Initial Public Offering

Effective July 27, 2004, our indirect parent, Dex Media, consummated its initial public offering of common stock. Part of the proceeds related to the initial public offering were used to redeem $18.2 million of our outstanding 9 7/8% senior subordinated notes on August 26, 2004 at a redemption price of 109.875% along with the accrued and unpaid interest. In connection with Dex Media’s initial public offering, we made a one time payment of $5.0 million to each of Carlyle and WCAS to eliminate the $2.0 million annual advisory fee payable under the management consulting agreements.

6

The Offering

On November 24, 2004, we and Dex Media West Finance completed an offering of $300.0 million in aggregate principal amount of 5 7/8% Senior Notes due 2011, which was exempt from registration under the Securities Act.

Outstanding Notes | We and Dex Media West Finance sold the outstanding notes to J.P. Morgan Securities Inc., the initial purchaser, on November 24, 2004. The initial purchaser subsequently resold the outstanding notes to qualified institutional buyers pursuant to Rule 144A under the Securities Act and to non-U.S. persons outside the United States in reliance on Regulation S under the Securities Act. |

Registration Rights Agreement | In connection with the sale of the outstanding notes, we and Dex Media West Finance entered into a registration rights agreement with the initial purchaser. Under the terms of that agreement, we each agreed to: |

| | • | use all commercially reasonable efforts to file a registration statement for the exchange offer and to consummate the exchange offer within 270 days after the initial issuance of the outstanding notes; |

| | • | use all commercially reasonable efforts to consummate the exchange offer within 60 days after the effective date of our registration statement; and |

| | • | file a shelf registration statement for the sale of the outstanding notes under certain circumstances and use all commercially reasonable efforts to cause such shelf registration statement to become effective under the Securities Act. |

| | If we or Dex Media West Finance do not meet one of these requirements, we and Dex Media West Finance must pay additional interest on the outstanding notes at a rate of 0.25% per annum for the first 90-day period, increasing by an additional 0.25% per annum with respect to each 90-day period until the exchange offer is completed or the shelf registration statement is declared effective, up to a maximum of 1.0% per annum of the principal amount of the notes. The exchange offer is being made pursuant to the registration rights agreement and is intended to satisfy the rights granted under the registration rights agreement, which rights terminate upon completion of the exchange offer. |

7

The Exchange Offer

The following is a brief summary of terms of the exchange offer. For a more complete description of the exchange offer, see “The Exchange Offer.”

Securities Offered | $300.0 million in aggregate principal amount of 5 7/8% Series B Senior Notes due 2011. |

Exchange Offer | The exchange notes are being offered in exchange for a like principal amount of outstanding notes. We will accept any and all outstanding notes validly tendered and not withdrawn prior to 12:00 midnight, New York City time, on , 2005. Holders may tender some or all of their outstanding notes pursuant to the exchange offer. However, outstanding notes may be tendered only in integral multiples of $1,000 in principal amount. The form and terms of the exchange notes are the same as the form and terms of the outstanding notes except that: |

| | • | the exchange notes have been registered under the federal securities laws and will not bear any legend restricting their transfer; |

| | • | the exchange notes bear a series B designation and a different CUSIP number than the outstanding notes; and |

| | • | the holders of the exchange notes will not be entitled to certain rights under the registration rights agreement, including the provisions for an increase in the interest rate on the outstanding notes in some circumstances relating to the timing of the exchange offer. See “The Exchange Offer.” |

Expiration Date | The exchange offer will expire at 12:00 midnight, New York City time, on , 2005, unless we decide to extend the exchange offer. |

Conditions to the Exchange Offer | The exchange offer is subject to certain customary conditions, some of which may be waived by us. See “The Exchange Offer—Conditions to the Exchange Offer.” |

Procedures for Tendering Outstanding Notes | If you wish to accept the exchange offer, you must complete, sign and date the letter of transmittal, or a facsimile of the letter of transmittal, in accordance with the instructions contained in this prospectus and in the letter of transmittal. You should then mail or otherwise deliver the letter of transmittal, or facsimile, together with the outstanding notes to be exchanged and any other required documentation, to the exchange agent at the address set forth in this prospectus and in the letter of transmittal. |

8

| | By executing the letter of transmittal, you will represent to us that, among other things: |

| | • | any exchange notes to be received by you will be acquired in the ordinary course of business; |

| | • | you have no arrangement or understanding with any person to participate in the distribution (within the meaning of the Securities Act) of the exchange notes in violation of the provisions of the Securities Act; |

| | • | you are not an “affiliate” (within the meaning of Rule 405 under Securities Act) of Dex Media West or Dex Media West Finance; and |

| | • | if you are a broker-dealer that will receive exchange notes for your own account in exchange for outstanding notes that were acquired as a result of market-making or other trading activities, then you will deliver a prospectus in connection with any resale of such exchange notes. See “The Exchange Offer—Procedures for Tendering Outstanding Notes” and “Plan of Distribution.” |

Effect of Not Tendering | Any outstanding notes that are not tendered or that are tendered but not accepted will remain subject to the restrictions on transfer. Since the outstanding notes have not been registered under the federal securities laws, they bear a legend restricting their transfer absent registration or the availability of a specific exemption from registration. Upon the completion of the exchange offer, we will have no further obligations, except under limited circumstances, to provide for registration of the outstanding notes under the federal securities laws. See “The Exchange Offer—Effect of Not Tendering.” |

Interest on the Exchange Notes and the Outstanding Notes | The exchange notes will bear interest from the most recent interest payment date to which interest has been paid on the notes or, if no interest has been paid, from November 24, 2004. Interest on the outstanding notes accepted for exchange will cease to accrue upon the issuance of the exchange notes. |

Withdrawal Rights | Tenders of outstanding notes may be withdrawn at any time prior to 12:00 midnight, New York City time, on the expiration date. |

Federal Tax Consequences | There will be no federal income tax consequences to you if you exchange your outstanding notes for exchange notes in the exchange offer. See “Material Federal Income Tax Consequences.” |

Use of Proceeds | We will not receive any proceeds from the issuance of exchange notes pursuant to the exchange offer. |

Exchange Agent | U.S. Bank National Association, the trustee under the indenture, is serving as exchange agent in connection with the exchange offer. |

9

Terms of the Exchange Notes

The following is a brief summary of the terms of the exchange notes. The financial terms and covenants of the exchange notes are the same as the outstanding notes. For a more complete description of the terms of the exchange notes, see “Description of Exchange Notes.”

Issuers | Dex Media West LLC, a Delaware limited liability company, and Dex Media West Finance Co., a Delaware corporation. |

Securities | $300.0 million in aggregate principal amount of 5 7/8% Series B Senior Notes due 2011. |

Maturity | November 15, 2011. |

Interest Payment Dates | May 15 and November 15 of each year, commencing on May 15, 2005. |

Guarantees | The notes will be guaranteed on a senior unsecured basis by each of our future subsidiaries that is a guarantor or direct borrower under our credit facilities, if any. We currently do not have any subsidiaries other than Dex Media West Finance, which is a co-issuer of the notes. |

Ranking | The exchange notes will be senior unsecured obligations of the Issuers and will: |

| | • | rank equally in right of payment to all existing and future senior indebtedness of the Issuers; |

| | • | rank senior in right of payment to all existing and future senior subordinated indebtedness and subordinated indebtedness of the Issuers; and |

| | • | be effectively subordinated in right of payment to the secured debt of the Issuers, to the extent of the value of the assets securing such debt, and all liabilities and preferred stock of each of the Issuers’ future subsidiaries that do not guarantee the senior notes. |

| | Similarly, any future exchange note guarantees will be senior unsecured obligations of the guarantors and will: |

| | • | rank equally in right of payment to all of the applicable guarantor’s senior indebtedness; |

| | • | rank senior in right of payment to all of the applicable guarantor’s senior subordinated indebtedness and subordinated indebtedness of the Issuers; and |

| | • | be effectively subordinated in right of payment to all secured debt of such guarantor, to the extent of the value of the assets securing such debt, and all liabilities and preferred stock of any subsidiary of a guarantor if that subsidiary is not a guarantor. |

10

| | As of September 30, 2004, after giving effect to the offering of the outstanding notes and the application of the proceeds therefrom, (1) the aggregate amount of senior indebtedness of the Issuers was $2,253.0 million, including the notes, of which $1,568.0 million was secured indebtedness, (2) $100.0 million was available for additional borrowing under our revolving credit facility, all of which would have been secured indebtedness, (3) the Issuers had no senior subordinated indebtedness, other than the $761.8 million of our outstanding 9 7/8% senior subordinated notes, and no subordinated indebtedness, and (4) Dex Media West Finance had no indebtedness other than the notes, the 8 1/2% senior notes, the 9 7/8% senior subordinated notes and its guarantee under our credit facilities. |

Optional Redemption | We may redeem some or all of the exchange notes at any time at the redemption prices listed under “Description of Exchange Notes—Optional Redemption.” |

| | In addition, before November 15, 2007, we may redeem up to 35% of each of the exchange notes with the net cash proceeds from certain equity offerings at the prices listed under “Description of Exchange Notes—Optional Redemption.” |

Change of Control | Upon the occurrence of a change of control, unless we have exercised our right to redeem all of the exchange notes of an issue as described above, you will have the right to require us to purchase all or a portion of your exchange notes at a purchase price in cash equal to 101% of the principal amount, plus accrued and unpaid interest, if any, to the date of purchase. See “Description of Exchange Notes—Change of Control.” |

Covenants | The indenture governing the exchange notes contains covenants that will impose significant restrictions on our business. The restrictions these covenants place on us, Dex Media West Finance and our future restricted subsidiaries include limitations on our ability and the ability of our future restricted subsidiaries to: |

| | • | incur additional indebtedness; |

| | • | pay dividends or make distributions in respect of our capital stock or to make certain other restricted payments or investments; |

| | • | sell assets, including capital stock of future restricted subsidiaries; |

| | • | agree to payment restrictions affecting our future restricted subsidiaries; |

| | • | consolidate, merge, sell or otherwise dispose of all or substantially all of our assets; |

| | • | enter into transactions with our affiliates; and |

| | • | designate any of our future subsidiaries as unrestricted subsidiaries. |

11

| | These covenants are subject to important exceptions and qualifications, which are described under “Description of Exchange Notes—Certain Covenants.” |

No Public Market for the Exchange Notes | The exchange notes are new issues of securities and will not be listed on any securities exchange or included in any automated quotation system. The initial purchaser of the outstanding notes has advised us that it intends to make a market in the exchange notes. The initial purchaser is not obligated, however, to make a market in the exchange notes, and any such market-making may be discontinued by the initial purchaser in its discretion at any time without notice. See “Plan of Distribution.” |

PORTAL Trading of the Exchange Notes | We expect the exchange notes to be eligible for trading on the Private Offerings, Resales and Trading through Automated Linkages, or “PORTAL,” System of the National Association of Securities Dealers, Inc. |

Risk Factors

You should carefully consider all the information in this prospectus prior to participating in the exchange offer. In particular, we urge you to consider carefully the factors set forth under “Risk Factors” beginning immediately after this “Prospectus Summary.”

Our principal executive offices are located at 198 Inverness Drive West, Englewood, Colorado 80112. Our telephone number is (303) 784-2900. Our internet address is http://www.dexmedia.com. The contents of our website are not part of this prospectus.

12

Summary Historical and Pro Forma Financial Data

The summary historical financial data for the years ended December 31, 2001 and 2002, for the Predecessor Period, the Successor Period and as of December 31, 2002 and 2003, have been derived from our consolidated financial statements, included elsewhere in this prospectus, which have been audited by KPMG LLP, independent registered public accounting firm. The results of operations for the Predecessor Period, the Successor Period and the nine months ended September 30, 2004, are not necessarily indicative of the results to be expected for any future period. The summary historical financial data as of September 30, 2004, for the period from September 10 to September 30, 2003 and for the nine months ended September 30, 2004 have been derived from our unaudited consolidated financial statements and related notes thereto, which have been prepared on a basis consistent with our annual consolidated financial statements and related notes thereto.

The pro forma financial information included below and in Note 5 to our audited consolidated financial statements included elsewhere in this prospectus eliminates the effects on our revenue and cost of revenue of the adjustments to deferred revenue and related deferred expenses at the acquisition date and presents our pro forma results of operations for the year ended December 31, 2003 as if the acquisition of Dex West had occurred on January 1, 2003.

Because our relationship with Qwest Dex, as well as Qwest and its other affiliates, changed as a result of the acquisition of Dex West, we expect that our cost structure will change from that reflected in our summary historical operating results. These cost structure changes are reflected in our pro forma financial data. As a result, our summary historical results of operations, financial position and cash flows would have been different if we had operated as a stand-alone company without the shared resources of Qwest and its affiliates. The summary pro forma financial data is for informational purposes only and should not be considered indicative of actual results that would have been achieved had the transactions related to the acquisition of Dex West actually been consummated on the date indicated and do not purport to be indicative of results of operations as of any future date or for any future period. The following data should be read in conjunction with “Unaudited Pro Forma Financial Information,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “The Acquisition Transactions” and our consolidated financial statements and related notes thereto included elsewhere in this prospectus.

13

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Predecessor

| | | Dex Media West LLC

| |

(Dollars in thousands) | | Year Ended December 31,

| | | Period from

January 1 to

September 9,

2003

| | | Period from

September 10

to December 31,

2003

| | | Unaudited

Period from

September 10

to September 30,

2003

| | | Unaudited

Nine Months

Ended

September 30,

2004

| | | Unaudited

Pro Forma

Year Ended

December 31,

2003

| |

| | 2001

| | | 2002

| | | | | | |

Statement of operations data: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Revenue(a) | | $ | 880,212 | | | $ | 900,200 | | | $ | 630,160 | | | $ | 213,997 | | | $ | 14,571 | | | $ | 645,979 | | | $ | 917,978 | |

Cost of revenue(a) | | | 272,732 | | | | 281,754 | | | | 193,282 | | | | 63,661 | | | | 4,819 | | | | 198,272 | | | | 277,998 | |

General and administrative expense | | | 74,973 | | | | 93,723 | | | | 74,241 | | | | 45,299 | | | | 7,359 | | | | 102,325 | | | | 120,918 | |

Depreciation and amortization expense | | | 16,706 | | | | 15,934 | | | | 8,153 | | | | 80,692 | | | | 14,682 | | | | 186,686 | | | | 257,428 | |

Merger-related expenses(b) | | | 5,579 | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | |

Impairment charges(c) | | | 8,976 | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Total operating expenses | | | 378,966 | | | | 391,411 | | | | 275,676 | | | | 189,652 | | | | 26,860 | | | | 487,283 | | | | 656,344 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

| Operating income (loss) | | | 501,246 | | | | 508,789 | | | | 354,484 | | | | 24,345 | | | | (12,289 | ) | | | 158,696 | | | | 261,634 | |

Other (income) expense: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Interest income | | | (3,858 | ) | | | (1,486 | ) | | | (2,336 | ) | | | (685 | ) | | | (102 | ) | | | (577 | ) | | | (685 | ) |

Interest expense(d)(e) | | | 167,500 | | | | 144,724 | | | | 113,627 | | | | 70,492 | | | | 16,580 | | | | 162,338 | | | | 216,473 | |

Other (income) expense, net(f) | | | 7,614 | | | | — | | | | — | | | | — | | | | — | | | | 17 | | | | — | |

Provision for income taxes | | | 123,713 | | | | 138,208 | | | | 91,441 | | | | (17,654 | ) | | | (11,190 | ) | | | (1,225 | ) | | | 17,788 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Net income (loss) | | $ | 206,277 | | | $ | 227,343 | | | $ | 151,752 | | | $ | (27,808 | ) | | $ | (17,577 | ) | | $ | (1,857 | ) | | $ | 28,058 | |

| | |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

|

Balance sheet data (at period end): | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total cash and cash equivalents | | $ | 64,385 | | | $ | 161,338 | | | | n/a | | | $ | 4,658 | | | $ | 8,393 | | | $ | 2,915 | | | | | |

Working capital (deficit)(g) | | | (1,916,609 | ) | | | (528,439 | ) | | | n/a | | | | 20,226 | | | | 47,240 | | | | (33,536 | ) | | | | |

Total assets | | | 417,760 | | | | 576,146 | | | | n/a | | | | 4,466,831 | | | | 4,546,721 | | | | 4,316,965 | | | | | |

Total senior debt | | | — | | | | — | | | | n/a | | | | 2,423,000 | | | | 2,518,000 | | | | 2,253,000 | | | | | |

Total debt(h) | | | 2,062,286 | | | | 750,000 | | | | n/a | | | | 3,203,000 | | | | 3,298,000 | | | | 3,014,800 | | | | | |

Owner’s equity (deficit) | | | (1,886,312 | ) | | | (471,913 | ) | | | n/a | | | | 1,058,906 | | | | 1,080,887 | | | | 1,062,144 | | | | | |

Other financial data: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

EBITDA(i)(e) | | $ | 510,338 | | | $ | 524,723 | | | $ | 362,637 | | | $ | 105,037 | | | $ | 2,393 | | | $ | 345,365 | | | $ | 519,062 | |

Capital expenditures | | | 10,825 | | | | 20,852 | | | | 15,850 | | | | 10,388 | | | | 1,893 | | | | 25,676 | | | | | |

Cash paid for interest | | | 165,658 | | | | 150,496 | | | | 67,408 | | | | 14,297 | | | | 865 | | | | 170,140 | | | | | |

Ratio of earnings to fixed charges(j) | | | 2.9x | | | | 3.5x | | | | 3.1x | | | | — | | | | — | | | | — | | | | 1.2x | |

Other operational data: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Local advertiser renewal rate | | | 93 | % | | | 92 | % | | | n/a | | | | 91 | % | | | n/a | | | | n/a | | | | | |

Number of directories published | | | 119 | | | | 121 | | | | 77 | | | | 35 | | | | 11 | | | | 96 | | | | | |

| (a) | Our revenue and cost of revenue for the twelve months following the consummation of the acquisition of Dex West was $120.6 million and $31.6 million lower, respectively, than our revenue and cost of revenue would otherwise have been because the acquisition has been accounted for under the purchase method of accounting. Under the purchase method of accounting, the deferred revenue and deferred directory costs associated with directories that had previously been published will not be carried over to our balance sheet. The purchase method of accounting for the acquisition of Dex West has not affected our revenue and directory costs in periods subsequent to this twelve-month period. This purchase accounting adjustment is non-recurring and has, and will have, no impact on cash flows. |

| (b) | Merger-related expenses reflect expenses incurred in connection with Qwest’s acquisition of US WEST, or the “Merger,” including contractual settlements incurred to cancel various commitments no longer deemed necessary as a result of the Merger, severance and employee-related expenses and rebranding expenses. |

| (c) | Impairment charges reflect capitalized software costs that were written off as certain internal software projects were discontinued. |

| (d) | Prior to November 2002, historical interest expense includes interest on that portion of a Qwest Dex line of credit borrowing arrangement with an affiliate of Qwest which was apportioned to us. Note 3(s) to our consolidated financial statements included in this prospectus sets forth additional information regarding this |

14

| | apportionment. Subsequent to September 2002 and prior to September 9, 2003, historical interest expense includes the interest on $750.0 million in debt issued by Qwest Dex and amortization of debt issuance costs. Subsequent to September 9, 2003, interest expense includes interest on our credit facilities and our outstanding 8 1/2% senior notes and 9 7/8% senior subordinated notes and includes $5.9 million of amortization of debt issuance costs relating to our credit facilities and such notes. |

| (e) | The pro forma interest expense reflects an interest rate of 8 1/2% for our outstanding senior notes, an interest rate of 9 7/8% for our outstanding senior subordinated notes, an estimated interest expense relating to our credit facilities (including the commitment fees on the unused portion of our revolving credit facility) and amortization of related debt issuance costs. For the calculation of cash paid for interest with respect to our credit facilities, we used a weighted average interest rate of 4.0% and an average London Interbank Offered Rate (“LIBOR”) of 1.1%. |

LIBOR interest rates have fluctuated significantly in recent years. If we had assumed a LIBOR interest rate of 3% in calculating the pro forma interest expense for our credit facilities, pro forma interest expense would have increased by approximately $41.0 million for the year ended December 31, 2003.

| (f) | In 2001, other (income) expense primarily represents a $8.0 million loss related to other than temporary declines in the value of certain investments. |

| (g) | Working capital is defined as current assets less current liabilities. For predecessor periods, working capital includes cash and short-term borrowings from affiliates that were not acquired or assumed by Dex Media West from Qwest Dex. These short-term borrowings were eliminated after the consummation of the transactions related to the acquisition of Dex West. The following table summarizes the effects of these items on working capital for the periods indicated: |

| | | | | | | | |

| | | Predecessor

| |

| | | Year Ended December 31,

| |

| (In thousands) | | 2001

| | | 2002

| |

Working capital (deficit) | | $ | (1,916,609 | ) | | $ | (528,439 | ) |

Cash and cash equivalents | | | (64,385 | ) | | | (161,338 | ) |

Short term borrowings | | | 2,062,286 | | | | 750,000 | |

| | |

|

|

| |

|

|

|

Working capital, excluding cash and short-term borrowings | | $ | 81,292 | | | $ | 60,223 | |

| | |

|

|

| |

|

|

|

Working capital, excluding cash and short-term borrowings is included in this prospectus to provide additional information with respect to the working capital of Dex Media West, as it excludes cash and short-term borrowings that were not acquired or assumed by Dex Media West from Qwest Dex. Working capital, excluding cash and short term borrowings, is not calculated under generally accepted accounting principles, or GAAP, and should not be considered in isolation or as a substitute for working capital prepared in accordance with GAAP. In addition, working capital, excluding cash and short term borrowings, as presented is not necessarily comparable to other similarly titled captions of other companies due to the potential inconsistencies in the method of calculation.

| (h) | Prior to November 2002, total debt includes that portion of a Qwest Dex line of credit borrowing arrangement with an affiliate of Qwest which was apportioned to us. Note 3(s) to our consolidated financial statements included in this prospectus sets forth additional information regarding this apportionment. Subsequent to September 2002 and prior to September 9, 2003, total debt includes the $750.0 million of debt issued by Qwest Dex. Subsequent to September 9, 2003, total debt consists of our credit facilities and our outstanding 8 1/2% senior notes and 9 7/8% senior subordinated notes. |

| (i) | EBITDA represents net income (loss) before interest expense, income taxes, and depreciation and amortization expense. |

15

The following table summarizes the calculation of EBITDA for the periods indicated:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Predecessor

| | Dex Media West LLC

|

| | | Year Ended December 31,

| | Period from

January 1 to

September 9,

2003

| | Period from

September 10 to

December 31,

2003

| | | Period from

September 10 to

September 30,

2003

| | | Unaudited Nine

Months Ended

September 30,

2004

| | | Unaudited

Pro Forma

Year Ended

December 31,

2003

|

| (In thousands) | | 2001

| | 2002

| | | | | |

Net income (loss) | | $ | 206,277 | | $ | 227,343 | | $ | 151,752 | | $ | (27,808 | ) | | $ | (17,577 | ) | | $ | (1,857 | ) | | $ | 28,058 |

Adjustments to net income (loss): | | | | | | | | | | | | | | | | | | | | | | | | |

Income taxes | | | 123,713 | | | 138,208 | | | 91,441 | | | (17,654 | ) | | | (11,190 | ) | | | (1,225 | ) | | | 17,788 |

Interest expense, net | | | 163,642 | | | 143,238 | | | 111,291 | | | 69,807 | | | | 16,478 | | | | 161,761 | | | | 215,788 |

Depreciation and amortization | | | 16,706 | | | 15,934 | | | 8,153 | | | 80,692 | | | | 14,682 | | | | 186,686 | | | | 257,428 |

| | |

|

| |

|

| |

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

EBITDA | | $ | 510,338 | | $ | 524,723 | | $ | 362,637 | | $ | 105,037 | | | $ | 2,393 | | | $ | 345,365 | | | $ | 519,062 |

| | |

|

| |

|

| |

|

| |

|

|

| |

|

|

| |

|

|

| |

|

|

Management uses EBITDA as a measure of operating performance of its directory publishing business. Excluding certain items from net income allows management to view trends and changes in margins and pre-tax profitability, excluding the effects of interest expense and amortization of intangible assets recorded in the acquisition and depreciation of property and equipment. EBITDA is also used by management to assess the ability of Dex Media West to satisfy our debt service, capital expenditures and working capital requirements, and to assess certain covenants in our borrowing arrangements that are tied to similar measures. However, EBITDA presented in this prospectus is calculated in a different manner than comparable terms in our debt agreements.

The use of EBITDA instead of net income has limitations, including the inability to determine profitability, the exclusion of interest expense and significant cash requirements associated therewith, and the exclusion of income tax expenses or benefits which ultimately may be realized through the payment or receipt of cash. Amortization expense, although a material component of net income, will be comprised substantially of amortization of acquired intangible assets by Dex Media West. Management believes it is acceptable to exclude depreciation and amortization from net income because Dex West has not historically been required to invest significant amounts in property, plant or equipment in its primary business. Net income and a reconciliation of net income to EBITDA are provided above to compensate for these material limitations.

EBITDA is not calculated under GAAP and should not be considered in isolation or as a substitute for net income, cash flows or other income or cash flow data prepared in accordance with GAAP or as a measure of our profitability or liquidity. While EBITDA and similar variations thereof are frequently used as a measure of operations and the ability to meet debt service requirements, these terms are not necessarily comparable to other similarly titled captions of other companies due to the potential inconsistencies in the method of calculation.

| (j) | The ratio of earnings to fixed charges is computed by dividing earnings by fixed charges. For this purpose, earnings include pre-tax income from continuing operations and fixed charges include interest, whether expensed or capitalized, and an estimate of the interest within rental expense. For the period from September 10 to December 31, 2003, the period from September 10 to September 30, 2003, and the nine months ended September 30, 2004, earnings were inadequate to cover fixed charges. The deficiencies were $45.5 million, $17.6 million, and $1.9 million, respectively. |

16

Risk Factors

You should carefully consider the risks described below as well as the other information contained in this prospectus before making a decision to participate in the exchange offer. Any of the following risks could materially adversely affect our business, financial condition or results of operations.

Risks Related to Our Business

The loss of any of our key agreements with Qwest could have a material adverse effect on our business.

In connection with the transactions related to the acquisition of Dex West, we entered into several agreements with Qwest, including a publishing agreement, a non-competition agreement and a billing and collection services agreement. Under the publishing agreement, we are the exclusive official publisher of directories for Qwest in the Dex West States until November 7, 2052. We believe that acting as the exclusive official publisher of directories for the incumbent telephone company provides us with a competitive advantage. Under the non-competition agreement, Qwest agreed until November 7, 2042 not to sell directory products consisting principally of listings and classified advertisements for subscribers in the geographic areas in the Dex West States in which Qwest provides local telephone service that are directed primarily at customers in those geographic areas. Under the billing and collection services agreement, Qwest agreed until December 31, 2008 to continue to bill and collect, on our behalf, amounts owed by our accounts, which are also Qwest local telephone customers, for our directory services. For the Combined Year 2003, Qwest billed approximately 47% of our local account billings on our behalf as part of Qwest’s telephone bill and held these collections in joint accounts with Qwest’s own collections. The termination of any of these agreements or the failure by Qwest to satisfy its obligations under these agreements could have a material adverse effect on our business. See “The Acquisistion Transactions—Agreements Between Us or Dex Media and Qwest.”

Qwest is currently highly leveraged and has a significant amount of debt service obligations over the near term and thereafter. In addition, Qwest has faced and may continue to face significant liquidity issues as well as issues relating to its compliance with certain covenants contained in the agreements governing its indebtedness. Based on Qwest’s public filings and announcements, Qwest has recently taken measures to improve its near-term liquidity and covenant compliance. However, Qwest still has a substantial amount of indebtedness outstanding and substantial debt service requirements. Consequently, it may be unable to meet its debt service obligations without obtaining additional financing or improving operating cash flow. Accordingly, we cannot assure you that Qwest will not ultimately seek protection under U.S. bankruptcy laws. In any such proceeding, our agreements with Qwest, and Qwest’s ability to provide the services under those agreements, could be adversely impacted. For example:

| | • | Qwest, or a trustee acting on its behalf, could seek to reject our agreements with Qwest as “executory” contracts under U.S. bankruptcy law, thus allowing Qwest to avoid its obligations under such contracts. Loss of substantial rights under these agreements could effectively require us to operate our business as an independent directory business, which could have a material adverse effect on our business. |

| | • | Qwest could seek to sell certain of its assets, including the assets relating to Qwest’s local telephone business, to third parties pursuant to the approval of the bankruptcy court. In such case, the purchaser of any such assets might be able to avoid, among other things, our publishing agreement and non-competition agreement with Qwest. |

| | • | We may have difficulties obtaining the funds collected by Qwest on our behalf pursuant to the billing and collection services agreement at the time such proceeding is instituted, although pursuant to such agreement, Qwest prepares settlement statements 10 times per month for each state in the Dex West States summarizing the amounts due to us and purchases our accounts receivable billed by it within approximately nine business days following such settlement date. Further, if Qwest continued to bill our customers pursuant to the billing and collection services agreement following any such bankruptcy filing, customers of Qwest may be less likely to pay on time, or at all, bills received, including the |

17

| | amount owed to us. Qwest has completed the preparation of its billing and collection system so that we will be able to transition from the Qwest billing and collection system to our own billing and collection system within approximately two weeks should we choose to do so. See “The Acquisistion Transactions—Agreements Between Us or Dex Media and Qwest—Billing and Collection Services Agreement.” |

We operate in the competitive directory advertising industry.

The U.S. directory advertising industry is competitive. There are a number of independent directory publishers, such as TransWestern Publishing Company LLC and the U.S. business of Yell Group Ltd., with which we compete in one or more of the Dex West States. In addition, we compete with other directory publishers in some of our markets, including Verizon Communications Inc., and these other directory publishers could elect to publish directories in the future in any of our markets in which they do not currently publish directories. For example, new competitive directories were introduced in four of our top ten markets in 2003 compared to just one new competitive directory in 2002. In the Dex States, our competitors publish and deliver approximately 230 directories. Our two largest competitors are Yell Group and Verizon. On average, there are two to three competing directories in each of our local markets. Through our Internet-based directory, we compete with these publishers and with other Internet sites providing classified directory information, such as Switchboard.com, yellowpages.com, Citysearch.com and Zagat.com, and with search engines and portals, such as Yahoo!, Google, MSN, and others, some of which have entered into affiliate agreements with other major directory publishers. We cannot assure you that we will be able to compete effectively with these other companies, some of which may have greater resources than we do, for advertising in the future. In addition, we compete against other media, including newspapers, radio, television, the Internet, billboards and direct mail, for business and professional advertising, and we cannot assure you that we will be able to compete successfully against these and other media for such advertising.

The Telecommunications Act of 1996 effectively opened local telephone markets to increased competition. Consequently, there can be no assurance that Qwest will remain the dominant local telephone service provider in its local service area. If Qwest were no longer the dominant local telephone service provider in its local service area, we may not realize some of the anticipated benefits under our publishing agreement with Qwest, which could have a material adverse effect on our business.

We could be materially adversely affected by declining usage of printed yellow pages directories.

We believe that overall usage of printed yellow pages directories in the United States declined by a compound annual rate of approximately 2% between 1998 and 2003. Notwithstanding these declines in usage, we have been able to increase our annual revenue in recent years through, among other things, increases in our advertising prices and new product offerings and enhanced features such as color advertisements and awareness products. There can be no assurance that usage of our print yellow pages directories will not continue to decline at the existing rate or more severely. In addition, there can be no assurance that we will be able to continue to increase prices or increase revenues from the new product offerings and enhanced features.

Any declines in usage could impair our ability to maintain or increase our advertising prices, cause businesses that purchase advertising in our yellow pages directories to reduce or discontinue those purchases and discourage businesses that do not purchase advertising in our yellow pages directories from doing so.

Although we believe that the decline in the usage of our printed directories will be offset in part by an increase in usage of our Internet-based directory, we cannot assure you that we will be able to provide services over the Internet successfully or to compete successfully with other Internet-based directory services. Any of the factors that may contribute to a decline in usage of our printed directories, or a combination of them, could impair our revenue and have a material adverse effect on our business.

18

Qwest, the former owner of our business, is the subject of ongoing investigations by the SEC and the U.S. Attorney’s office.

On March 8, 2002, Qwest, the former owner of our business, received a request from the Denver regional office of the SEC to voluntarily produce documents and information as part of an informal inquiry into certain of its accounting practices. On April 3, 2002, the SEC issued an order authorizing a formal investigation of Qwest. The matters under investigation include, among others, the revenue recognition practices of Qwest Dex. In addition, two former Chief Executive Officers (one of whom is our current Chief Executive Officer) and two former Chief Financial Officers (one of whom is our current Vice President, Financial Planning and Analysis) of Qwest Dex were subpoenaed in August 2002 and have provided documents and testimony to the SEC. In the investigation, the SEC may issue additional subpoenas seeking documents and/or testimony from other current and former Qwest Dex employees. On October 21, 2004, without admitting or denying the allegations in the SEC’s complaint, Qwest consented to the entry of a judgment enjoining it from violating the antifraud, reporting, books and records, internal control, proxy and securities registration provisions of the federal securities laws. As part of the judgment, Qwest agreed to pay a civil penalty of $250.0 million and $1 disgorgement. The SEC is continuing its investigation of Qwest’s financial reporting. We cannot assure you that the SEC investigation will not result in any additional enforcement action against Qwest Dex, its employees or those of our employees who were formerly employees of Qwest Dex.

In addition, on July 9, 2002, Qwest was informed by the U.S. Attorney’s Office for the District of Colorado that it had begun a criminal investigation of Qwest. Although the U.S. Attorney’s Office has not disclosed the subject matter of the investigation, it has indicated that it is investigating the matters under inquiry in the SEC investigation. It is not clear whether this investigation involves the business or management of Qwest Dex’s directory business (other than its former revenue recognition policy under the point of publication method) or employees who historically worked for the Qwest Dex business, most of whom are now our employees. We do not have any knowledge that former employees of Qwest Dex, most of whom are now our employees, are the subject of the U.S. Attorney’s investigation. None of the former employees of Qwest Dex have informed us that they are the targets of the U.S. Attorney’s investigation or have been contacted by the U.S. Attorney’s office in connection with the investigation.

Although we acquired only the assets of the Qwest Dex business located in the Dex West States and not the Qwest Dex corporate entity and we did not assume in the acquisition of Dex West any liabilities relating to the SEC or the U.S. Attorney’s Office investigations, there can be no assurances that these investigations or other investigations will not have a material adverse effect on our business.

Our business could suffer if there is a prolonged economic downturn.

We derive our net revenue from the sale of advertising in our directories. Our advertising revenue, as well as that of yellow pages publishers in general, generally does not fluctuate widely with economic cycles. However, a prolonged national or regional economic recession could have a material adverse effect on our business.

Our dependence on third-party providers of printing, distribution and delivery services could materially adversely affect us.

We depend on third parties for the printing and distribution of our directories. For the printing of our directories, Dex Media has a contract with R.R. Donnelley & Sons Company and we have a contract with Quebecor World Directory Sales Corporation, or “Quebecor,” for the printing of our directories which expire on December 31, 2011 and July 30, 2008, respectively. Because of the large print volume and specialized binding of directories, there are only a small number of companies in the printing industry that could service our needs. Accordingly, the inability or unwillingness of Donnelley or Quebecor to provide printing services to us on acceptable terms or at all could have a material adverse effect on our business.

Dex Media has a contract with a single company, Product Development Corporation, or “PDC,” for the distribution of our directories. This contract expires on May 31, 2009. There are only a small number of

19