UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21504

Advent/Claymore Enhanced Growth & Income Fund

(Exact name of registrant as specified in charter)

1065 Avenue of the Americas, New York, NY 10018

(Address of principal executive offices) (Zip code)

Robert White, Treasurer

1065 Avenue of the Americas, New York, NY 10018

(Name and address of agent for service)

Registrant's telephone number, including area code: (212) 479-0675

Date of fiscal year end: October 31

Date of reporting period: April 30, 2010

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The registrant's semi-annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Investment Company Act”) is as follows:

Semiannual Report April 30, 2010 (Unaudited) | Advent/Claymore Enhanced Growth & Income Fund | LCM |

|  |

www.claymore.com/lcm ... your bridge to the LATEST, most up-to-date INFORMATION about the Advent/Claymore Enhanced Growth & Income Fund |

The shareholder report you are reading right now is just the beginning of the story. Online at www.claymore.com/lcm, you will find:

| • | Daily, weekly and monthly data on share prices, net asset values, distributions, and more |

| • | Portfolio overviews and performance analyses |

| • | Announcements, press releases and special notices |

| • | Fund and adviser contact information |

Advent Capital Management and Claymore are continually updating and expanding shareholder information services on the Fund’s website in an ongoing effort to provide you with the most current information about how your Fund’s assets are managed, and the results of our efforts. It is just one more small way we are working to keep you better informed about your investment in the Fund.

2 | Semiannual Report| April 30, 2010

LCM | Advent/Claymore Enhanced Growth & Income Fund

Dear Shareholder | |||

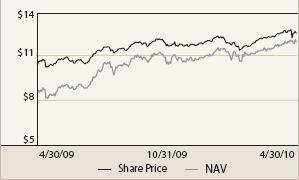

Tracy V. Maitland President and Chief Executive Officer | We thank you for your investment in the Advent/Claymore Enhanced Growth & Income Fund (the “Fund”). This report covers the Fund’s performance for the semiannual period ended April 30, 2010. Advent Capital Management, LLC serves as the Fund’s Investment Manager. Based in New York, New York, with additional investment personnel in London, England, Advent is a credit-oriented firm specializing in the management of global convertible, high-yield and equity securities across three lines of business—long-only strategies, hedge funds and closed-end funds. As of April 30, 2010, Advent managed approximately $5.25 billion in assets. Claymore Advisors, LLC (“Claymore”) serves as the Investment Adviser to the Fund. Claymore Securities, Inc. is an affiliate of Claymore Advisors, LLC. Claymore and its associated entities are wholly-owned subsidiaries of Guggenheim Partners, LLC (“Guggenheim Partners”), a global, diversified financial services firm with more than $100 billion in assets under supervision. At its reconvened special meeting of shareholders held on March 12, 2010, shareholders of the Fund approved a new investment advisory agreement between the Fund and Claymore. Shareholder approval of the investment advisory agreement was needed because the October 2009 acquisition of Claymore by Guggenheim Partners resulted in the automatic termination of the previous investment advisory agreement between the Fund and Claymore. Claymore Securities, Inc. offers strategic investment solutions for financial advisors and their clients. In total, Claymore entities provide supervision, management, or servicing on approximately $15.9 billion in assets as of March 31, 2010. The Fund’s primary investment objective is to seek current income and current gains from trading securities, with a secondary objective of long-term capital appreciation. Under normal market conditions, the Fund invests at least 70% of its managed assets in a diversified portfolio of equity securities and convertible securities of U.S. and non-U.S. issuers and up to 30% of assets in non-convertible high yield securities. Additionally, the Fund intends to engage in a strategy of writing (selling) covered call options on at least 50% of the securities held in the portfolio of the Fund, thus generating option writing premiums. Advent seeks international investment opportunities in each asset class, with an emphasis on large multinational companies. Appreciation potential is provided by investments in convertibles and common stock, while the allocation to high-yield securities is primarily a source of income. The balance between convertible securities, equities and high-yield securities and the degree to which the Fund engages in a covered call strategy will vary from time to time based on security valuations, interest rates, equity market volatility and other economic and market factors. This ability to move among the three asset classes is quite beneficial to the Fund’s ability to balance return and risk. An important new strategy for the Fund is the use of leverage (borrowing), which is being utilized to finance the purchase of additional securities that provide increased income and potentially greater appreciation potential for common shareholders than could be achieved from an unleveraged portfolio. All Fund returns cited—whether based on net asset value (“NAV”) or market price—assume the reinvestment of all distributions. For the six-month period ending April 30, 2010, the Fund generated a total return based on market price of 20.10% and a return of 12.48% based on NAV. As of April 30, 2010, the Fund’s market price of $12.01 represented a discount of 4.76% to NAV of $12.61. As of October 31, 2009, the Fund’s market price of $10.48 repre- | ||

Semiannual Report| April 30, 2010 | 3

LCM | Advent/Claymore Enhanced Growth & Income Fund | Dear Shareholder continued

sented a discount of 10.58% to NAV of $11.72. The market value of the Fund’s shares fluctuates from time to time, and it may be higher or lower than the Fund’s NAV. The Fund paid quarterly dividends of $0.264 in November 2009 and February 2010. The most recent dividend represents an annualized distribution rate of 8.79% based on the Fund’s closing market price of $12.01 on April 30, 2010. There is no guarantee of any future distributions or that the current returns and distribution rate will be maintained. We encourage shareholders to consider the opportunity to reinvest their distributions from the Fund through the Dividend Reinvestment Plan (“DRIP”), which is described in detail on page 30 of the Fund’s semiannual report. When shares trade at a discount to NAV, the DRIP takes advantage of the discount by reinvesting the quarterly dividend distribution in common shares of the Fund purchased in the market at a price less than NAV. Conversely, when the market price of the Fund’s common shares is at a premium above NAV, the DRIP reinvests participants’ dividends in newly-issued common shares at NAV, subject to an IRS limitation that the purchase price cannot be more than 5% below the market price per share. The DRIP provides a cost-effective means to accumulate additional shares and enjoy the benefits of compounding returns over time. The DRIP plan effectively provides an income averaging technique, which causes shareholders to accumulate a larger number of Fund shares when the market price is depressed than when the price is higher. The Fund is managed by a team of experienced and seasoned professionals led by myself in my capacity as Chief Investment Officer (as well as President and Founder) of Advent Capital Management, LLC. We encourage you to read the following Questions & Answers section, which provides more information about the factors that impacted the Fund’s performance. We thank you for your investment in the Fund and we are honored that you have chosen the Advent/Claymore Enhanced Growth & Income Fund as part of your investment portfolio. For the most up-to-date information on your investment, please visit the Fund’s website at www.claymore.com/lcm. |

| Sincerely, |

|

| Tracy V. Maitland |

| President and Chief Executive Officer of the Advent/Claymore Enhanced Growth & Income Fund |

| May 31, 2010 |

4 | Semiannual Report | April 30, 2010

LCM | Advent/Claymore Enhanced Growth & Income Fund

Questions & Answers |

Advent/Claymore Enhanced Growth & Income Fund (the “Fund”) is managed by a team of seasoned professionals at Advent Capital Management, LLC, led by Tracy V. Maitland, Advent’s President and Chief Investment Officer. In the following interview, the management team discusses the equity, convertible securities and high-yield markets and the performance of the Fund during the six-month period ended April 30, 2010.

1. Please remind us of this Fund’s objectives and how you seek to achieve them.

The Fund’s primary investment objective is to provide current income and current gains from trading in securities, with a secondary objective of long-term capital appreciation. Under normal market conditions, the Fund invests at least 70% of its assets in a diversified portfolio of equity securities and convertible securities of U.S. and non-U.S. issuers and up to 30% of its managed assets in non-convertible high yield securities. Additionally, the Fund engages in an option strategy of writing (selling) covered call options on at least 50% of the securities held in the portfolio of the Fund, thus generating option writing premiums. Advent seeks international investment opportunities in each asset class, with an emphasis on large multinational companies. Capital appreciation potential is provided by investments in convertibles and common stock, while the allocation to high-yield securities is primarily a source of income.

An important new strategy for the Fund is the use of leverage (borrowing), which is being utilized to finance the purchase of additional securities that provide increased income and potentially greater appreciation potential for common shareholders than could be achieved from an unleveraged portfolio. Seeing an opportunity to take advantage of the spread between historically low financing rates and significantly higher yields on income-producing securities such as convertible and high-yield securities, Advent requested and received from the Fund’s Board of Trustees authorization to engage in a leverage strategy. In order to undertake this strategy, the Fund entered into a credit facility with BNP Paribas, a major European bank, to opportunistically introduce leverage to enhance the total return potential via the Fund’s investment strategies. Initially, the Fund borrowed $50 million, or approximately 23% of its total assets, under this credit facility.

Although the use of financial leverage by the Fund may create an opportunity for increased return for common shareholders, it also results in additional risks and can magnify the effect of any losses. If the income and gains earned on securities purchased with the financial leverage proceeds are greater than the cost of the financial leverage, the common shareholders’ return will be greater than if financial leverage had not been used. Conversely, if the income or gains from the securities purchased with the proceeds of financial leverage are less than the cost of the financial leverage, common shareholders’ return will be less than if financial leverage had not been used. There is no assurance that a financial leverage strategy will be successful.

2. Please tell us about the economic and market environment over the last six months.

The economic recovery that began in the second half of 2009 appeared to solidify and strengthen in the first few months of 2010. The early stages of the recovery were driven mainly by monetary and fiscal stimulus and an upturn in the inventory cycle. More recently, activity in the U.S. economy appears to be more sustainable, with improving conditions in the labor market, firming aggregate demand and reviving confidence.

The North American economies appear to be generally stronger than most other world economies. The recovery is still in an early stage in Europe, and European economies were affected by a range of problems including travel disruptions due to volcanic ash from Iceland and concerns about sovereign debt of some countries in the spring of 2010. In Asia, the Chinese government has demonstrated its intention to rein in a potentially overheating economy, while the Japanese economy is reasonably strong.

During the six months from October 31, 2009 through April 30, 2010, equity markets, credit markets and the markets for convertible securities continued the recovery that began in the first quarter of 2009. Most of the indices used by the Fund’s managers to gauge market performance were up more than 10% for the six months ended April 30, 2010; the exception was the Morgan Stanley Capital International Europe-Australasia-Far East (MSCI EAFE) Index, which returned 2.75% for the six-month period. Return of the Merrill Lynch All U.S. Convertibles Index for the six-month period ended April 30, 2010, was 16.28%. The Standard & Poor’s 500 Index, which is generally regarded as a good indicator of the broad U.S. stock market, returned 15.66% for the same period. Return of the Merrill Lynch High Yield Master II Index, which measures performance of the high-yield bond market, was 11.65% for the six months ended April 30, 2010.

3. How did the Fund perform in this environment?

Benefiting from strength in equity, credit and convertible markets, as well as favorable investment decisions made by the Investment Manager, the Fund performed very well. For the six-month period ending April 30, 2010, the Fund generated a total return based on market price of 20.10% and a return of 12.48% based on NAV. As of April 30, 2010, the Fund’s market price of $12.01 represented a discount of 4.76% to NAV of $12.61. All Fund returns cited—whether based on net asset value (“NAV”) or market price—assume the reinvestment of all distributions.

For comparison, the CBOE S&P 500 2% OTM BuyWrite Index (BXY), an index that measures performance of 2% out-of-the-money S&P 500 Index call options, returned 12.36% over the same period.

Semiannual Report | April 30, 2010 | 5

LCM | Advent/Claymore Enhanced Growth & Income Fund | Questions and Answers continued

The market value and NAV of the Fund’s shares fluctuate from time to time, and the Fund’s market value may be higher or lower than its NAV. The current discount to NAV provides an opportunity for investors to purchase shares of the Fund below the market value of the securities in the underlying portfolio. The Adviser believes that, over the long term, the progress of the NAV will be reflected in the market price return to shareholders.

4. How was the Fund’s portfolio allocated among asset classes over the last six months?

The Fund was designed to be diversified among asset classes but to also have the flexibility to reallocate assets, as appropriate. Investments are allocated globally among stocks, convertible securities and high-yield bonds.

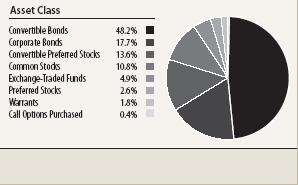

At the end of the previous fiscal year, October 31, 2009, 82.1% of the Fund’s assets were in convertible securities; of this 61.4% was in convertible bonds and 20.7% in convertible preferreds. At that time, 8.6% of the Fund’s assets were invested in equities and 7.4% in high yield bonds. As of April 30, 2010, the total exposure to convertibles was 61.8%, including both convertible bonds and preferreds. As of April 30, 2010, 10.8% of the Fund’s portfolio was invested in common stocks, 2.6% in preferred stocks, and 4.9% in ETFs.

Seeing a more normalized credit market but still a steep yield curve, with low short term rates and relatively high long term rates, as discussed above, the Fund’s Adviser secured a credit line. The Fund borrowed $50 million at very low interest rates and invested in higher yielding investments with longer maturities to take advantage of the steep yield curve. (The yield curve is a graph with a left-to-right line that shows how high or low yields are, from the shortest to the longest maturities. Typically, the line rises from left to right as investors who are willing to tie up their money for a longer period are rewarded with higher yields.) Over half of the borrowed money was invested in high yield bonds which subsequently appreciated in value, resulting in a significant increase in percentage of the Fund’s assets allocated to high-yield bonds, which represented 17.7% of the portfolio as of April 30, 2010.

In terms of industry representation, the emphasis has been shifted to more economically sensitive sectors such as industrials, financials and consumer discretionary, with a corresponding reduction in more stable sectors such as health care. Many of the Fund’s health care holdings had performed quite well, providing an opportunity to realize gains by selling some holdings such as Human Genome Sciences, Inc.(0.4% of long-term investments), a commercially focused biopharmaceutical company. The exposure to the basic materials sector has been reduced, despite the desire to increase exposure to economically sensitive sectors, because many holdings in this sector had moved up sharply. A position in Freeport-McMoRan Copper & Gold, Inc. (0.1% of long-term investments), a mining company that performed very well in 2009, was reduced, with the proceeds invested in other securities that had not yet recovered significantly but whose growth prospects looked favorable.

The Fund’s foreign exposure was not changed significantly. As of April 30, 2010, 22.0% of the portfolio was in securities of companies headquartered outside the U.S.; international investments represented 24.3% of the portfolio as of October 31, 2009.

5. Which investment decisions had the greatest effect on the Fund’s performance?

The decision to begin using leverage was an important contributor, and the timing of the implementation of leverage was highly advantageous. The new line of credit became available in January 2010 at a time the high yield market was experiencing a setback. The Adviser was able to take advantage of this market correction to invest in high yield bonds, which performed very well through the end of the period.

One of the top performing issues was a mandatory convertible preferred stock issued in late 2009 by Citigroup, Inc. (1.6% of long-term investments).The Investment Manager took advantage of this issue from a large money center bank that is believed to be in the early stages of recovering from financial problems experienced in 2008 and early 2009. Also highly positive was a large position in warrants of Bank of America Corp. (1.2% of long-term investments). Valuation analysis indicated that the price of these warrants sold at auction was cheap, and it seems likely that there will be high demand for these longer-term warrants if the underlying stock continues to recover. Also positive was an investment in warrants of JPMorgan Chase & Co. (0.6% of long-term investments), a financial holding company. Warrants provide a means of gaining exposure to the equities of these financial institutions without actually owning the stock. Also, warrants typically have an asymmetry that is somewhat akin to convertibles in that they

6 | Semiannual Report | April 30, 2010

LCM | Advent/Claymore Enhanced Growth & Income Fund | Questions and Answers continued

tend to capture more of the upside than the downside, especially when they have a few years to run.

As the portfolio has been adjusted to include more economically sensitive names, some industrial companies made significant contributions to performance. Among these were auto manufacturer Ford Motor Co. (1.4% of long-term investments), which has experienced a strong comeback after being down sharply in 2008. The Fund held two Ford bonds and a preferred issue, and all contributed to performance over the six-month period. Other industrial names that contributed include Navistar International Corp. (0.6% of long-term investments), which manufactures trucks, engines and parts; Danaher Corp. (0.6% of long-term investments), a diversified industrial company; and Kansas City Southern (not held in portfolio at period end), a railroad company. And while the energy sector as a whole did not perform well, one holding that stood out is Whiting Petroleum Corporation (0.7% of long-term investments), an independent oil and gas company.

In the interest of balance, it is appropriate to comment on holdings that detracted from performance, but actually there were not many, and the losses they generated were relatively small. One position that detracted from performance was Actelion Finance SCA (0.6% of long-term investments), a Swiss biopharmaceutical Company that focuses on the discovery, development and commercialization of treatments. Its main drug, Tracleer, has been proven effective for certain types of lung ailments, but the stock dropped when trials for using this drug for other conditions were not successful. The Fund held an Actelion convertible bond that was purchased at a price approximately 10% above its value at maturity in two years. This bond provided the opportunity to participate in a high volatility scenario in a conservative way, since Actelion is a financially sound company with a considerable cash position. While the equity participation did not work out as hoped, the bond was down much less than the stock.

Some of the Fund’s natural gas holdings were laggards, reflecting weak natural gas prices. A bond of Goodrich Petroleum Corp. (0.7% of long-term investments), an independent oil and gas company, provided income, but the stock and the bond were down. Other energy names that detracted were natural gas producer Chesapeake Energy Corp. (0.7% of long-term investments) and Frontier Oil Corporation (not held in portfolio at period end), a refiner that had suffered from industry-wide weakness in refining margins.

6. What was the impact of the Fund’s covered call strategy?

Early in the period, in the fall of 2009, there was considerable market volatility, and the covered call options written on the Fund’s holdings generated attractive premiums, providing additional income. As the period progressed, market volatility declined and the premiums available for writing calls were less, even though there was considerable volatility in individual stocks. So, although the strategy was continued as expected, the risk-reward attractiveness for this strategy was lessened. Therefore, fewer call contracts were written, and they did not provide as much income as this strategy historically has. Going forward, during periods when overall volatility expands, Advent intends to increase the call writing activity accordingly, with the beneficial impact on income accruing to the Fund.

The Fund intends to write covered call options on at least 50% of the securities held in the portfolio, generally 10% to 15% out of the money. As of April 30, 2010, options were written against approximately 55% of the total securities in the Fund.

The Fund’s covered call overlay serves mainly to help meet distribution goals and, to a lesser extent, to help maintain the Fund’s NAV during market setbacks. Option premiums, dividends, interest and capital appreciation are all part of the total return. Most of the covered call writing centers on the Fund’s U.S. equity and convertible investments, because the U.S. has a broad and deep options market, while many international companies that we find attractive lack listed options.

Although the Fund has the ability to write calls on the entire portfolio, covered calls are generally written on no more than 60–65% of the total portfolio. Calls are usually written on just a portion of a position so that if the price of the security rises substantially and the call is exercised, a portion of the position is still maintained. Calls with varying maturities and strike prices are typically tiered so that not all expire at the same time or are exercised at the same price.

| What is a covered call? |

| A call is an option (or contract) that gives its holder the right, but not the obligation, to buy shares of the underlying security at a specified price on or before a pre-determined expiration date. After this predeter- mined date, the option and its corresponding rights expire. A covered call is when the seller of the call option also owns the security on which the call is written. Covered call strategies are generally used as a hedge—to limit losses by obtaining premium income from the sale of calls, while still maintaining upside potential. |

Semiannual Report | April 30, 2010 | 7

LCM | Advent/Claymore Enhanced Growth & Income Fund | Questions and Answers continued

7. What is the current outlook for the markets and the Fund?

The Fund’s management team continues to see opportunities in convertible securities and high yield bonds. There is also further potential in equities as economies around the world continue to recover. Continued strength in equities is likely to lead to rewarding returns from convertible securities.

A major advantage of this Fund is its ability to invest in multiple asset classes, adjusting the asset mix according to the opportunities available in various markets around the world. As the equity market rises, as it has in recent months, the equity sensitivity of a portfolio of convertible securities increases. When the equity market is weak, convertibles’ declining sensitivity, combined with interest income, mitigates the downside.

Advent believes that, over the long term, careful security selection and asset allocation will help the Fund’s performance by providing favorable returns in rising markets and a level of income that can help provide some protection for overall returns during down markets.

Index Definitions

Indices are unmanaged and it is not possible to invest directly in an index.

The MSCI EAFE Index is a free float-adjusted market capitalization weighted index designed to reflect the movements of stock markets in developed countries of Europe and the Pacific Basin. The index is calculated in U.S. dollars and is constructed to represent about 60% of market capitalization in each country.

The Merrill Lynch All U.S. Convertibles Index is comprised of approximately 500 issues of convertible bonds and preferred stock of all qualities.

S&P 500 Index is a capitalization-weighted index of 500 stocks. The index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

Merrill Lynch High Yield Master II Index is a commonly used benchmark index for high yield corporate bonds. It is a measure of the broad high yield market.

The CBOE S&P 500 2% OTM BuyWrite Index (BXY) uses the same methodology as the widely accepted CBOE S&P 500 BuyWrite Index (BXM), but the BXY Index is calculated using out-of-the-money S&P 500 Index (SPX) call options, rather than at-the-money SPX call options. The BXY strategy diversifies the buy-write opportunities currently provided by the BXM. The BXY Index yields lower monthly premiums in return for a greater participation in the upside moves of the S&P 500.

LCM Additional Risks and Disclosure

The views expressed in his report reflect those of the Portfolio Managers and Claymore only through the report period as stated on the cover. These views are subject to change at any time, based on market and other conditions and should not be construed as a recommendation of any kind. The material may also contain forward-looking statements that involve risk and uncertainty, and there is no guarantee they will come to pass. There can be no assurance that the Fund will achieve its investment objectives. The value of the fund will fluctuate with the value of the underlying securities. Historically, closed-end funds often trade at a discount to their net asset value. The Fund is subject to investment risk, including the possible loss of the entire amount that you invest. Past performance does not guarantee future results.

Convertible Securities. The Fund is not limited in the percentage of its assets that may be invested in convertible securities. Convertible securities generally offer lower interest or dividend yields than non-convertible securities of similar quality. The market values of convertible securities tend to decline as interest rates increase and, conversely, to increase as interest rates decline. However, the convertible security’s market value tends to reflect the market price of the common stock of the issuing company when that stock price is greater than the convertible’s “conversion price,” which is the predetermined price at which the convertible security could be exchanged for the associated stock.

Synthetic Convertible Securities. The value of a synthetic convertible security will respond differently to market fluctuations than a convertible security because a synthetic convertible security is composed of two or more separate securities, each with its own market value. In addition, if the value of the underlying common stock or the level of the index involved in the convertible component falls below the exercise price of the warrant or option, the warrant or option may lose all value.

Equity Securities Risk. Equity risk is the risk that securities held by the Fund will fall due to general market or economic conditions, perceptions regarding the industries in which the issuers of securities held by the Fund participate, and the particular circumstances and performance of particular companies whose securities the Fund holds.

Risks Associated with Options on Securities. There are significant differences between the securities and options markets that could result in an imperfect correlation between these markets, causing a given transaction not to achieve its objectives. A decision as to whether, when and how to use options involves the exercise of skill and judgment, and even a well-conceived transaction may be unsuccessful to some degree because of market behavior or unexpected events. As the writer of a covered call option, the Fund forgoes, during the option’s

8 | Semiannual Report | April 30, 2010

LCM | Advent/Claymore Enhanced Growth & Income Fund | Questions and Answers continued

life, the opportunity to profit from increases in the market value of the security covering the call option above the sum of the premium and the strike price of the call, but has retained the risk of loss should the price of the underlying security decline. The writer of an option has no control over the time when it may be required to fulfill its obligation as a writer of the option. Once an option writer has received an exercise notice, it cannot effect a closing purchase transaction in order to terminate its obligation under the option and must deliver the underlying security at the exercise price.

Lower Grade Securities. The Fund may invest an unlimited amount in lower grade securities. Investing in lower grade securities (commonly known as “junk bonds”) involves additional risks, including credit risk. Credit risk is the risk that one or more securities in the Fund’s portfolio will decline in price, or fail to pay interest or principal when due, because the issuer of the security experiences a decline in its financial status.

Leverage Risk. Certain risks are associated with the leveraging of common stock. Both the net asset value and the market value of shares of common stock may be subject to higher volatility and a decline in value.

Foreign Securities and Emerging Markets Risk. Investing in non-U.S. issuers may involve unique risks, such as currency, political, economic and market risk. In addition, investing in emerging markets entails additional risk including, but not limited to (1) news and events unique to a country or region (2) smaller market size, resulting in lack of liquidity and price volatility (3) certain national policies which may restrict the Fund’s investment opportunities.

Illiquid Investments. The Fund may invest without limit in illiquid securities. The Fund may also invest without limit in Rule 144A Securities. Although many of the Rule 144A Securities in which the Fund invests may be, in the view of the Investment Manager, liquid, if qualified institutional buyers are unwilling to purchase these Rule 144A Securities, they may become illiquid. Illiquid securities may be difficult to dispose of at a fair price at the times when the Fund believes it is desirable to do so. The market price of illiquid securities generally is more volatile than that of more liquid securities, which may adversely affect the price that the Fund pays for or recovers upon the sale of illiquid securities.

In addition to the risks described above, the Fund is also subject to: Interest Rate Risk, Credit Risk, Call Risk, Currency Risks, Management Risk, Strategic Transactions, Anti-Takeover Provisions, and Market Disruption Risk. Please see www.claymore.com/lcm for a more detailed discussion about Fund risks and considerations.

Semiannual Report | April 30, 2010 | 9

LCM | Advent/Claymore Enhanced Growth & Income Fund

Fund Summary | As of April 30, 2010 (unaudited) |

| Fund Statistics | ||

| Share Price | $12.01 | |

| Common Share Net Asset Value | $12.61 | |

| Premium/Discount to NAV | -4.76% | |

| Net Assets ($000) | $171,498 |

| Total Returns | ||

| (Inception 1/31/05) | Market | NAV |

| Six- Month non-annualized | 20.10% | 12.48% |

| One Year | 56.83% | 32.34% |

| Three Year - average annual | -5.59% | -6.21% |

| Five Year - average annual | 2.58% | 2.04% |

| Since Inception - average annual | -0.01% | 0.75% |

| % of Long Term | ||

| Top Ten Industries | Investments | |

| Telecommunications | 6.9% | |

| Banks | 5.9% | |

| Pharmaceuticals | 5.8% | |

| Oil & Gas | 5.7% | |

| Insurance | 5.6% | |

| Exchange-Traded Funds | 4.9% | |

| Biotechnology | 4.1% | |

| Healthcare-Products | 3.7% | |

| Mining | 3.5% | |

| Computers | 3.4% |

| % of Long Term | ||

| Top Ten Issuers | Investments | |

| Citigroup, Inc. | 2.5% | |

| EMC Corp. | 2.2% | |

| Bank of America Corp. | 2.0% | |

| International Game Technology | 1.9% | |

| Lucent Technologies Capital Trust I | 1.8% | |

| Wells Fargo & Co. | 1.6% | |

| Apria Healthcare Group, Inc. | 1.5% | |

| JPMorgan Chase & Co. | 1.5% | |

| Beckman Coulter, Inc. | 1.5% | |

| Clear Channel Worldwide Holdings, Inc. | 1.5% |

Past performance does not guarantee future results. All portfolio data is subject to change daily. For more current information, please visit www.claymore.com/lcm. The above summaries are provided for informational purposes only and should not be viewed as recommendations.

Share Price & NAV Performance

Portfolio Composition (% of Total Investments)

10 | Semiannual Report | April 30, 2010

LCM | Advent/Claymore Enhanced Growth & Income Fund

Portfolio of Investments | As of April 30, 2010 (unaudited) |

| Principal | |||

| Amount | Value |

| Long-Term Investments — 125.2% | |||||

| Convertible Bonds — 60.6% | |||||

| Agriculture – 1.3% | |||||

| CNY | 15,000,000 | China Green Holdings Ltd., Ser. CGHL, NR | |||

| 0.00%, 10/29/10 (Bermuda) (c ) | $ | 2,265,356 | |||

| Airlines – 0.6% | |||||

| $ | 1,000,000 | UAL Corp., CCC | |||

| 4.50%, 6/30/21 (a) | 1,011,200 | ||||

| Apparel – 1.2% | |||||

| HK$ | 13,000,000 | Yue Yuen Industrial Holdings Ltd., NR | |||

| 0.00%, 11/17/11 (Bermuda) | 2,007,181 | ||||

| Auto Manufacturers – 1.6% | |||||

| $ | 900,000 | Ford Motor Co., CCC | |||

| 4.25%, 11/15/16 (a) | 1,400,625 | ||||

| $ | 1,100,000 | Navistar International Corp., B | |||

| 3.00%, 10/15/14 (a) | 1,289,750 | ||||

| 2,690,375 | |||||

| Biotechnology – 4.6% | |||||

| $ | 1,075,000 | American Oriental Bioengineering, Inc., NR | |||

| 5.00%, 7/15/15 (e) | 874,781 | ||||

| $ | 1,000,000 | Amgen, Inc., A+ | |||

| 0.375%, 2/1/13 | 1,006,250 | ||||

| $ | 2,500,000 | Amylin Pharmaceuticals, Inc., NR | |||

| 3.00%, 6/15/14 (a) | 2,200,000 | ||||

| $ | 450,000 | Human Genome Sciences, Inc., NR | |||

| 2.25%, 10/15/11 | 830,812 | ||||

| $ | 2,450,000 | Life Technologies Corp., BBB- | |||

| 3.25%, 6/15/25 | 2,958,375 | ||||

| 7,870,218 | |||||

| Building Materials – 1.3% | |||||

| $ | 1,996,000 | Cemex SAB de CV, NR | |||

| 4.875%, 3/15/15 (Mexico) (a)(e) | 2,290,410 | ||||

| Chemicals – 0.4% | |||||

| HK$ | 4,450,000 | Sinofert Holdings Ltd., NR | |||

| 0.00%, 8/7/11 (Bermuda) | 770,611 | ||||

| Coal – 1.0% | |||||

| $ | 1,000,000 | Massey Energy Co., BB- | |||

| 3.25%, 8/1/15 (a) | 841,250 | ||||

| $ | 800,000 | Peabody Energy Corp., B+ | |||

| 4.75%, 12/15/41 (a) | 875,000 | ||||

| 1,716,250 | |||||

| Computers – 2.3% | |||||

| $ | 2,000,000 | EMC Corp., A- | |||

| 1.75%, 12/1/11 (a) | 2,522,500 | ||||

| $ | 700,000 | EMC Corp., A- | |||

| 1.75%, 12/1/13 (a) | 911,750 | ||||

| $ | 400,000 | Maxtor Corp./Seagate Technology, B | |||

| 2.375%, 8/15/12 (Cayman Islands) (a) | 466,000 | ||||

| 3,900,250 |

| Electrical Components & Equipment – 1.6% | |||||

| CNY | 15,900,000 | China High Speed Transmission Equipment Group Co., Ltd., Ser. CHIS, NR | |||

| 0.00%, 5/14/11 (Cayman Islands) (c ) | 2,789,990 | ||||

| Electronics – 1.5% | |||||

| JPY | 220,000,000 | Toshiba Corp., BBB | |||

| 0.00%, 7/21/11 (Japan) | 2,587,037 | ||||

| Engineering & Construction – 1.1% | |||||

| $ | 1,400,000 | Jaiprakash Associates Ltd., NR | |||

| 0.00%, 9/12/12 (India) | 1,830,500 | ||||

| Entertainment – 2.3% | |||||

| $ | 3,150,000 | International Game Technology, BBB | |||

| 3.25%, 5/1/14 (a)(e) | 4,012,312 | ||||

| Forest Products & Paper – 1.2% | |||||

| $ | 1,925,000 | Sino-Forest Corp., BB | |||

| 4.25%, 12/15/16 (Canada) (e) | 2,054,938 | ||||

| Healthcare – Products – 3.7% | |||||

| $ | 2,900,000 | Beckman Coulter, Inc., BBB | |||

| 2.50%, 12/15/36 | 3,240,750 | ||||

| $ | 1,950,000 | Hologic, Inc., BB- | |||

| 2.00%, 12/15/37 (f) | 1,755,000 | ||||

| $ | 1,130,000 | NuVasive, Inc., NR | |||

| 2.25%, 3/15/13 | 1,269,838 | ||||

| 6,265,588 | |||||

| Holdings Companies – Diversified – 0.9% | |||||

€ | 1,000,000 | Industrivarden AB, Ser. INDU, A | |||

| 2.50%, 2/27/15 (Sweden) | 1,524,447 | ||||

| Insurance – 1.1% | |||||

| $ | 1,625,000 | MGIC Investment Corp., CCC+ | |||

| 5.00%, 5/1/17 (a) | 1,807,813 | ||||

| Internet – 0.8% | |||||

| $ | 1,225,000 | Symantec Corp., NR | |||

| 1.00%, 6/15/13 (a) | 1,310,750 | ||||

| Iron/Steel – 0.8% | |||||

| $ | 1,200,000 | Steel Dynamics, Inc., BB+ | |||

| 5.125%, 6/15/14 (a) | 1,378,500 | ||||

| Lodging – 3.2% | |||||

| HK$ | 18,100,000 | Champion Path Holdings Ltd., NR | |||

| 0.00%, 10/28/15 (Hong Kong) | 2,590,338 | ||||

| $ | 2,611,000 | MGM Mirage, CCC+ | |||

| 4.25%, 4/15/15 (a)(e) | 2,842,727 | ||||

| 5,433,065 | |||||

| Media – 0.6% | |||||

| $ | 1,050,000 | XM Satellite Radio, Inc., CCC+ | |||

| 7.00%, 12/1/14 (e) | 1,119,563 | ||||

| Mining – 4.0% | |||||

| $ | 2,200,000 | Enercoal Resources Pte Ltd., NR | |||

| 9.25%, 8/5/14 (Indonesia) | 2,240,049 | ||||

| $ | 1,325,000 | Goldcorp, Inc., BBB+ | |||

| 2.00%, 8/1/14 (Canada) (a)(e) | 1,578,406 | ||||

| $ | 1,600,000 | Jaguar Mining, Inc., NR | |||

| 4.50%, 11/1/14 (Canada) (e) | 1,782,000 |

See notes to financial statements.

Semiannual Report | April 30, 2010 | 11

LCM | Advent/Claymore Enhanced Growth & Income Fund | Portfolio of Investments (unaudited) continued

| Principal | |||

| Amount | Value |

| Mining (continued) | |||||

| $ | 1,000,000 | Newmont Mining Corp., BBB+ | |||

| 1.25%, 7/15/14 | $ | 1,342,500 | |||

| 6,942,955 | |||||

| Miscellaneous Manufacturing – 2.4% | |||||

| $ | 1,000,000 | Danaher Corp., A+ | |||

| 0.00%, 1/22/21 (a) | 1,217,500 | ||||

| $ | 1,100,000 | Textron, Inc., Ser. TXT, Ser. BBB- | |||

| 4.50%, 5/1/13 (a) | 2,037,750 | ||||

| $ | 1,025,000 | Trinity Industries, Inc., BB- | |||

| 3.875%, 6/1/36 (a) | 876,375 | ||||

| 4,131,625 | |||||

| Oil and Gas – 3.8% | |||||

| $ | 2,000,000 | Carrizo Oil & Gas, Inc., NR | |||

| 4.375%, 6/1/28 (a) | 1,790,000 | ||||

| $ | 1,150,000 | Chesapeake Energy Corp., BB | |||

| 2.25%, 12/15/38 (a) | 849,562 | ||||

| $ | 1,700,000 | Goodrich Petroleum Corp., NR | |||

| 5.00%, 10/1/29 (a) | 1,538,500 | ||||

| $ | 2,300,000 | PetroBakken Energy Ltd., Ser. REGS, NR | |||

| 3.125%, 2/8/16 (Canada) | 2,286,478 | ||||

| 6,464,540 | |||||

| Oil and Gas Services – 1.3% | |||||

| $ | 1,050,000 | Cameron International Corp., BBB+ | |||

| 2.50%, 6/15/26 (a) | 1,324,312 | ||||

| $ | 560,000 | Core Laboratories LP, NR | |||

| 0.25%, 10/31/11 (Netherlands) (a) | 905,800 | ||||

| 2,230,112 | |||||

| Pharmaceuticals – 5.7% | |||||

| CHF | 1,265,000 | Actelion Finance SCA, NR | |||

| 0.00%, 11/22/11 (Switzerland) | 1,194,742 | ||||

| $ | 1,350,000 | Allergan, Inc., NR | |||

| 1.50%, 4/1/26 | 1,528,875 | ||||

| $ | 2,750,000 | Cephalon, Inc., NR | |||

| 2.50%, 5/1/14 (a) | 3,076,562 | ||||

| $ | 2,000,000 | Mylan, Inc., BB- | |||

| 1.25%, 3/15/12 (a) | 2,215,000 | ||||

| $ | 1,400,000 | Teva Pharmaceutical Finance Co. LLC, Ser. C, A- | |||

| 0.25%, 2/1/26 (Israel) (a) | 1,762,250 | ||||

| 9,777,429 | |||||

| Real Estate – 1.9% | |||||

| $ | 1,617,000 | Forest City Enterprises, Inc., B- | |||

| 5.00%, 10/15/16 (a)(e) | 2,150,610 | ||||

| HK$ | 8,900,000 | Soho China Ltd., NR | |||

| 3.75%, 7/2/14 (Cayman Islands) | 1,163,079 | ||||

| 3,313,689 | |||||

| Retail – 1.1% | |||||

| $ | 500,000 | Saks, Inc., B- | |||

| 2.00%, 3/15/24 (a) | 500,625 | ||||

| $ | 1,250,000 | Sonic Automotive, Inc., B- | |||

| 5.00%, 10/1/29 (a) | 1,389,063 | ||||

| 1,889,688 |

| Semiconductors – 2.6% | |||||

| $ | 750,000 | Intel Corp., A- | |||

| 3.25%, 8/1/39 (a)(e) | 917,812 | ||||

| $ | 2,000,000 | ON Semiconductor Corp., B+ | |||

| 2.625%, 12/15/26 (a) | 2,057,500 | ||||

| $ | 1,500,000 | Xilinx, Inc., BB | |||

| 3.125%, 3/15/37 (a) | 1,410,000 | ||||

| 4,385,312 | |||||

| Telecommunications – 3.9% | |||||

| $ | 2,500,000 | ADC Telecommunications, Inc., NR | |||

| 0.8308%, 6/15/13 (a)(d) | 2,212,500 | ||||

| $ | 1,000,000 | Arris Group, Inc., NR | |||

| 2.00%, 11/15/26 | 1,012,500 | ||||

| $ | 1,000,000 | CommScope, Inc., B | |||

| 3.25%, 7/1/15 (a) | 1,357,500 | ||||

| JPY | 68,000,000 | Softbank Corp., BB+ | |||

| 1.75%, 3/31/14 (Japan) | 892,033 | ||||

| $ | 1,000,000 | Virgin Media, Inc., B | |||

| 6.50%, 11/15/16 (a) | 1,246,250 | ||||

| 6,720,783 | |||||

| Utility – 0.8% | |||||

€ | 1,000,000 | International Power Jersey II Ltd., BB | |||

| 3.25%, 7/20/13 (United Kingdom) | 1,411,423 | ||||

| Total Convertible Bonds – 60.6% | |||||

| (Cost $95,028,492) | 103,903,910 | ||||

| Corporate Bonds – 22.2% | |||||

| Beverage – 1.8% | |||||

| $ | 3,000,000 | Constellation Brands, Inc., BB | |||

| 7.25%, 9/1/16 | 3,078,750 | ||||

| Chemicals – 1.2% | |||||

| $ | 2,000,000 | LBI Escrow Corp., BB | |||

| 8.00%, 11/1/17 (e) | 2,072,500 | ||||

| Diversified Financial Services – 1.9% | |||||

| $ | 1,350,000 | Capital One Capital V, BB | |||

| 10.25%, 8/15/39 | 1,620,000 | ||||

| $ | 1,500,000 | CIT Group Funding Co. of Delaware LLC, B+ | |||

| 10.25%, 5/1/14 | 1,560,000 | ||||

| 3,180,000 | |||||

| Electric – 1.5% | |||||

| $ | 2,500,000 | NRG Energy, Inc., BB- | |||

| 7.25%, 2/1/14 | 2,534,375 | ||||

| Food – 1.2% | |||||

| $ | 1,000,000 | Smithfield Foods, Inc., B- | |||

| 7.00%, 8/1/11 | 1,025,000 | ||||

| $ | 1,000,000 | Smithfield Foods, Inc., B+ | |||

| 10.00%, 7/15/14, Senior Secured Notes (e) | 1,122,500 | ||||

| 2,147,500 | |||||

| Healthcare-Products – 1.0% | |||||

| $ | 1,500,000 | Biomet, Inc., B- | |||

| 10.00%, 10/15/17 | 1,650,000 |

See notes to financial statements.

12 | Semiannual Report | April 30, 2010

LCM | Advent/Claymore Enhanced Growth & Income Fund | Portfolio of Investments (unaudited) continued

| Principal | |||

| Amount | Value |

| Healthcare – Services – 2.9% | |||||

| $ | 3,000,000 | Apria Healthcare Group, Inc., BB+ | |||

| 11.25%, 11/1/14 (e) | $ | 3,296,250 | |||

| $ | 1,500,000 | HCA, Inc., BB- | |||

| 9.25%, 11/15/16 | 1,621,875 | ||||

| 4,918,125 | |||||

| Insurance – 2.5% | |||||

| $ | 1,000,000 | AXA SA, BBB | |||

| 6.379%, 12/14/36 (France) (d)(e) | 890,000 | ||||

| $ | 1,850,000 | Liberty Mutual Group, Inc., BB | |||

| 10.75%, 6/15/58 (d)(e) | 2,155,250 | ||||

| $ | 1,000,000 | Metlife, Inc., BBB | |||

| 10.75%, 8/1/39 | 1,288,353 | ||||

| 4,333,603 | |||||

| Machinery-Diversified – 1.5% | |||||

| $ | 2,500,000 | Case New Holland, Inc., BB+ | |||

| 7.75%, 9/1/13 (e) | 2,631,250 | ||||

| Media – 2.8% | |||||

| $ | 3,000,000 | Clear Channel Worldwide Holdings, Inc., B | |||

| 9.25%, 12/15/17 (e) | 3,213,750 | ||||

| 500,000 | Univision Communications, Inc., B- | ||||

| 12.00%, 7/1/14 (e) | 552,500 | ||||

| $ | 1,000,000 | UPC Holding BV, B- | |||

| 9.875%, 4/15/18 (Netherlands) (e) | 1,055,000 | ||||

| 4,821,250 | |||||

| Pharmaceuticals – 1.0% | |||||

| $ | 1,665,000 | Axcan Intermediate Holdings, Inc., B | |||

| 12.75%, 3/1/16 | 1,748,250 | ||||

| Retail – 1.5% | |||||

| $ | 2,450,000 | Toys R Us Property Co. LLC, B+ | |||

| 8.50%, 12/1/17 (e) | 2,590,875 | ||||

| Telecommunications – 1.4% | |||||

| $ | 1,873,000 | iPCS, Inc., BB- | |||

| 2.37%, 5/1/13 (d) | 1,769,985 | ||||

| $ | 500,000 | NII Capital Corp., BB- | |||

| 10.00%, 8/15/16 (e) | 555,000 | ||||

| 2,324,985 | |||||

| Total Corporate Bonds – 22.2% | |||||

| (Cost $35,772,627) | 38,031,463 |

| Number | |||

| of Shares | Value |

| Convertible Preferred Stocks – 17.0% | |||||

| Agriculture – 1.1% | |||||

| 46,850 | Archer-Daniels-Midland Co., 6.25%, 2011 (a) | 1,855,260 | |||

| Auto Manufacturers – 0.9% | |||||

| 31,200 | Ford Motor Co. Capital Trust II, 6.50%, 2032 (a) | 1,525,680 | |||

| Banks – 5.9% | |||||

| 1,650 | Bank of America Corp., Ser. L, 7.25%, 2049 (a) | 1,620,283 | |||

| 26,070 | Citigroup, Inc., 7.50%, 2012 | 3,436,547 |

| 15,626 | Keycorp, Ser. A, 7.75%, 2049 (a) | 1,640,730 | ||

| 3,565 | Wells Fargo & Co., Ser. L, 7.50%, 2049 (a) | 3,515,090 | ||

| 10,212,650 | ||||

| Electric – 1.2% | ||||

| 31,050 | Great Plains Energy, Inc., 12.00%, 2012 | 2,035,327 | ||

| Food Products – 1.1% | ||||

| 155,600 | 2009 Dole Food Automatic Common Exchange Security Trust, | |||

| 7.00%, 2012 (e) | 1,830,727 | |||

| Insurance – 3.2% | ||||

| 103,049 | Hartford Financial Services Group, Inc., 7.25%, 2013 (a) | 2,733,890 | ||

| 103,775 | XL Capital Ltd., 10.75%, 2011 (Cayman Islands) (a) | 2,782,208 | ||

| 5,516,098 | ||||

| Oil & Gas – 0.9% | ||||

| 6,888 | Whiting Petroleum Corp., 6.25%, 2049 (a) | 1,517,771 | ||

| Real Estate – 0.5% | ||||

| 14,996 | Forest City Enterprises, Inc., Ser. A, 7.00%, 2049 (a) | 932,564 | ||

| Telecommunications – 2.2% | ||||

| 4,617 | Lucent Technologies Capital Trust I, 7.75%, 2017 (France) | 3,829,802 | ||

| Total Convertible Preferred Stocks – 17.0% | ||||

| (Cost $24,868,868) | 29,255,879 | |||

| Common Stocks — 13.6% | ||||

| Agriculture – 1.0% | ||||

| 21,000 | Lorillard, Inc. (a) | 1,645,770 | ||

| Banks – 0.4% | ||||

| 5,000 | Bank of America Corp. (a) | 89,150 | ||

| 20,000 | Sumitomo Mitsui Financial Group, Inc. (Japan) | 663,759 | ||

| 752,909 | ||||

| Biotechnology – 0.5% | ||||

| 30,000 | American Oriental Bioengineering, Inc. (b) | 121,500 | ||

| 35,000 | Amylin Pharmaceuticals, Inc. (a)(b) | 722,400 | ||

| 843,900 | ||||

| Computers – 1.9% | ||||

| 8,000 | Apple, Inc. (b) | 2,088,960 | ||

| 64,000 | EMC Corp. (a)(b) | 1,216,640 | ||

| 3,305,600 | ||||

| Electrical Components & Equipment – 0.2% | ||||

| 110,000 | China High Speed Transmission Equipment Co. Ltd. (Cayman Islands) | 264,374 | ||

| Engineering & Construction – 0.4% | ||||

| 12,500 | Fluor Corp. (a) | 660,500 | ||

| Entertainment – 0.0% | ||||

| 1,000 | International Game Technology (a) | 21,080 | ||

| Food – 0.5% | ||||

| 44,710 | Smithfield Foods, Inc. (a)(b) | 837,865 | ||

| Insurance – 0.1% | ||||

| 25,000 | MGIC Investment Corp. (a)(b) | 260,750 | ||

| Iron/Steel – 0.1% | ||||

| 2,700 | ArcelorMittal (Luxembourg) (a) | 104,841 |

See notes to financial statements.

Semiannual Report | April 30, 2010 | 13

LCM | Advent/Claymore Enhanced Growth & Income Fund | Portfolio of Investments (unaudited) continued

| Number | |||

| of Shares | Value |

| Lodging – 0.1% | ||||

| 30,820 | Morgans Hotel Group Co. (b) | $ | 261,045 | |

| Mining – 0.4% | ||||

| 2,000 | Freeport-McMoRan Copper & Gold, Inc. (a) | 151,060 | ||

| 30,000 | Xstrata PLC (United Kingdom) | 498,916 | ||

| 649,976 | ||||

| Miscellaneous Manufacturing – 1.6% | ||||

| 54,100 | Honeywell International, Inc. (a) | 2,568,127 | ||

| 7,000 | Textron, Inc. (a) | 159,880 | ||

| 2,000 | Trinity Industries, Inc. (a) | 49,780 | ||

| 2,777,787 | ||||

| Oil & Gas – 2.4% | ||||

| 27,500 | Chesapeake Energy Corp. (a) | 654,500 | ||

| 20,000 | Exxon Mobil Corp. (a) | 1,357,000 | ||

| 5,000 | Goodrich Petroleum Corp. (a)(b) | 84,650 | ||

| 25,900 | PetroBakken Energy Ltd. (Canada) | 705,515 | ||

| 65,000 | Valero Energy Corp. (a) | 1,351,350 | ||

| 4,153,015 | ||||

| Pharmaceuticals – 0.5% | ||||

| 1,000 | Cephalon, Inc. (a)(b) | 64,200 | ||

| 100,000 | Somaxon Pharmaceuticals, Inc. (b) | 719,000 | ||

| 1,000 | Teva Pharmaceutical Industries Ltd., ADR (Israel) (a) | 58,730 | ||

| 841,930 | ||||

| Retail – 0.9% | ||||

| 69,637 | RadioShack Corp. (a) | 1,500,677 | ||

| Semiconductors – 1.4% | ||||

| 80,000 | Intel Corp. (a) | 1,826,400 | ||

| 75,000 | ON Semiconductor Corp. (a)(b) | 595,500 | ||

| 2,000 | Xilinx, Inc. (a) | 51,560 | ||

| 2,473,460 | ||||

| Telecommunications – 1.2% | ||||

| 3,400 | ADC Telecommunications, Inc. (a)(b) | 27,234 | ||

| 5,000 | CommScope, Inc. (a)(b) | 162,900 | ||

| 10,000 | QUALCOMM, Inc. (a) | 387,400 | ||

| 49,000 | Verizon Communications, Inc. (a) | 1,415,610 | ||

| 1,993,144 | ||||

| Total Common Stocks – 13.6% | ||||

| (Cost $22,598,432) | 23,348,623 | |||

| Exchange-Traded Funds – 6.2% | ||||

| 132,000 | Financial Select Sector SPDR Fund (a) | 2,131,800 | ||

| 94,300 | Industrial Select Sector SPDR Fund (a) | 3,077,009 | ||

| 40,000 | iPATH S&P 500 VIX Short-Term Futures ETN (b) | 847,200 | ||

| 85,000 | PowerShares DB US Dollar Index Bullish Fund (b) | 2,035,750 | ||

| 40,100 | ProShares UltraShort Basic Materials (a) | 1,384,653 | ||

| 28,000 | ProShares UltraShort FTSE/Xinhua China 25 (a) | 1,146,040 | ||

| (Cost $10,224,931) | 10,622,452 |

| Preferred Stock – 3.3% | ||||||

| Banks – 1.0% | ||||||

| 2,000 | Ally Financial, 7.00%, (e) | 1,698,688 | ||||

| Diversified Financial Services – 2.3% | ||||||

| 75,000 | Citigroup Capital XII, 8.50% | 1,953,750 | ||||

| 80,000 | JPMorgan Chase Capital XXIX, 6.70% | 1,940,000 | ||||

| 3,893,750 | ||||||

| Total Preferred Stock – 3.3% | ||||||

| (Cost $5,654,000) | 5,592,438 | |||||

| Warrants – 2.3% | ||||||

| 676,513 | Bank of America Corp. (a) | 2,557,219 | ||||

| 96,659 | JPMorgan Chase & Co. (a) | 1,342,594 | ||||

| (Cost $2,913,758) | 3,899,813 | |||||

| Total Long-Term Investments – 125.2% | ||||||

| (Cost $197,061,108) | 214,654,578 | |||||

| Contracts | ||||||

| (100 shares | Expiration | Exercise | ||||

| per contract) | Options Purchased(b) | Date | Price | Value | ||

| Call Options Purchased – 0.5% | ||||||

| 1,000 | General Electric Co. | May 2010 | 20.00 | 16,000 | ||

| 1,000 | Exxon Mobil Corp. (a) | July 2010 | 60.00 | 830,000 | ||

| (Cost $850,460) | 846,000 | |||||

| Total Investments – 125.7% | ||||||

| (Cost $197,911,568) | 215,500,578 | |||||

| Other Assets in excess of Liabilities – 3.6% | 6,115,264 | |||||

| Total Options Written (Premiums received $104,950) – (0.1%) | (117,878) | |||||

| Borrowings – (29.2%) | (50,000,000) | |||||

| Net Assets – 100.0% | $ | 171,497,964 |

AB – Stock Company

ADR – American Depositary Receipt

BV – Limited Liability Company

LLC – Limited Liability Corp.

LP – Limited Partnership

PLC – Public Limited Company

Pte – Public Trading Enterprise

SA – Corporation

SAB de CV – Publicly Traded Company

SCA – Limited Partnership

| (a) | All or a portion of this security position represents cover (directly or through conversion rights) for outstanding options written. |

| (b) | Non-income producing security. |

| (c) | The reference entity is denominated in Chinese Yuan, but traded in U.S. dollars. |

| (d) | Variable rate or floating rate security. The rate shown is as of April 30, 2010. |

| (e) | Securities are exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers. At April 30, 2010, these securities amounted to 25.2% of net assets. |

| (f) | Security becomes a 0% coupon, accreting bond after December 15, 2013 with a 2.0% principal accretion rate. Ratings shown are per Standard & Poor’s. Securities classified as NR are not rated by Standard & Poors. |

See notes to financial statements.

14 | Semiannual Report | April 30, 2010

LCM | Advent/Claymore Enhanced Growth & Income Fund | Portfolio of Investments (unaudited) continued

| Contracts | |||||||||

| (100 shares | Expiration | Exercise | Market | ||||||

| per contract) | Call Options Written(a) | Date | Price | Value | |||||

| 49 | ADC Telecommunications, Inc. | May 2010 | $ | 7.50 | $ | 3,553 | |||

| 50 | Amylin Pharmaceuticals, Inc. | June 2010 | 24.00 | 3,250 | |||||

| 27 | ArcelorMittal | June 2010 | 46.00 | 1,080 | |||||

| 10 | Archer-Daniels-Midland Co. | May 2010 | 31.00 | 75 | |||||

| 50 | Bank of America Corp. | May 2010 | 20.00 | 300 | |||||

| 40 | Cameron International Corp. | May 2010 | 50.00 | 400 | |||||

| 10 | Carrizo Oil & Gas, Inc. | May 2010 | 30.00 | 50 | |||||

| 3 | Cemex SAB de CV | June 2010 | 14.00 | 45 | |||||

| 10 | Cephalon, Inc. | May 2010 | 70.00 | 400 | |||||

| 50 | Chesapeake Energy Corp. | May 2010 | 25.00 | 2,100 | |||||

| 50 | CommScope, Inc. | May 2010 | 30.00 | 16,000 | |||||

| 10 | CommScope, Inc. | May 2010 | 35.00 | 350 | |||||

| 10 | Core Laboratories LP | June 2010 | 155.00 | 3,300 | |||||

| 10 | Danaher Corp. | May 2010 | 85.00 | 1,550 | |||||

| 100 | EMC Corp. | May 2010 | 21.00 | 400 | |||||

| 20 | Exxon Mobil Corp. | June 2010 | 75.00 | 400 | |||||

| 100 | Financial Select Sector SPDR Fund | May 2010 | 18.00 | 200 | |||||

| 50 | Fluor Corp. | May 2010 | 50.00 | 19,500 | |||||

| 20 | Ford Motor Co. | May 2010 | 15.00 | 140 | |||||

| 20 | Forest City Enterprises, Inc. | June 2010 | 17.50 | 450 | |||||

| 20 | Freeport-McMoRan Copper & Gold, Inc. | August 2010 | 90.00 | 3,900 | |||||

| 25 | Goldcorp, Inc. | May 2010 | 42.00 | 5,475 | |||||

| 25 | Goodrich Petroleum Corp. | May 2010 | 20.00 | 375 | |||||

| 10 | Hartford Financial Services Group, Inc. | June 2010 | 35.00 | 150 | |||||

| 50 | Honeywell International, Inc. | May 2010 | 48.00 | 4,000 | |||||

| 100 | Industrial Select Sector SPDR Fund | June 2010 | 34.00 | 4,200 | |||||

| 100 | Intel Corp. | May 2010 | 25.00 | 500 | |||||

| 10 | International Game Technology | May 2010 | 20.00 | 1,490 | |||||

| 10 | JPMorgan Chase & Co. | May 2010 | 50.00 | 30 | |||||

| 20 | KeyCorp | May 2010 | 9.00 | 1,000 | |||||

| 50 | Lorillard, Inc. | May 2010 | 85.00 | 625 | |||||

| 20 | Massey Energy Co. | May 2010 | 46.00 | 500 | |||||

| 50 | MGIC Investment Corp. | June 2010 | 12.50 | 1,850 | |||||

| 20 | MGM Mirage | May 2010 | 17.00 | 1,120 | |||||

| 25 | Mylan, Inc. | May 2010 | 24.00 | 150 | |||||

| 10 | Navistar International Corp. | May 2010 | 55.00 | 175 | |||||

| 100 | ON Semiconductor Corp. | June 2010 | 10.00 | 1,000 | |||||

| 20 | Peabody Energy Corp. | May 2010 | 49.00 | 1,740 | |||||

| 10 | ProShares UltraShort Basic Materials | May 2010 | 49.00 | 300 | |||||

| 40 | ProShares UltraShort FTSE/Xinhua China 25 | May 2010 | 50.00 | 2,000 | |||||

| 100 | QUALCOMM, Inc. | May 2010 | 40.00 | 4,100 | |||||

| 75 | RadioShack Corp. | May 2010 | 26.00 | 750 | |||||

| 20 | Saks, Inc. | May 2010 | 10.00 | 1,000 | |||||

| 10 | Maxtor Corp./Seagate Technology | May 2010 | 20.00 | 200 | |||||

| 25 | Smithfield Foods, Inc. | May 2010 | 22.50 | 125 | |||||

| 25 | Sonic Automotive, Inc. | May 2010 | 12.50 | 500 |

| 20 | Steel Dynamics, Inc. | June 2010 | 19.00 | 250 | |||

| 10 | Symantec Corp. | May 2010 | 19.00 | 150 | |||

| 10 | Teva Pharmaceutical Industries Ltd. | June 2010 | 65.00 | 320 | |||

| 100 | Textron, Inc. | May 2010 | 25.00 | 3,000 | |||

| 20 | Trinity Industries, Inc. | May 2010 | 22.50 | 5,400 | |||

| 10 | UAL Corp. | May 2010 | 25.00 | 310 | |||

| 50 | Valero Energy Corp. | May 2010 | 20.00 | 6,100 | |||

| 10 | Verizon Communications, Inc. | May 2010 | 31.00 | 30 | |||

| 10 | Virgin Media, Inc. | May 2010 | 20.00 | 150 | |||

| 10 | Wells Fargo & Co. | May 2010 | 34.00 | 570 | |||

| 10 | Whiting Petroleum Corp. | June 2010 | 95.00 | 2,600 | |||

| 20 | Xilinx, Inc. | May 2010 | 29.00 | 150 | |||

| 10 | XL Capital Ltd. | May 2010 | 22.00 | 50 |

| Total Call Options Written | |||||||

| (Premiums received $82,180) | 109,878 |

Put Options Written(a) | |||||||

| 1,000 | General Electric Co. | May 2010 | 17.00 | 8,000 | |||

| (Premiums received $22,770) |

| Total Options Written | ||||||||

| (Premiums received $104,950) | $ | 117,878 |

(a) Non-income producing security.

See notes to financial statements.

Semiannual Report | April 30, 2010 | 15

LCM | Advent/Claymore Enhanced Growth & Income Fund

Statement of Assets and Liabilities | April 30, 2010 (unaudited) |

| Assets | ||||

| Investments, at value (cost $197,911,568) | $ | 215,500,578 | ||

| Cash & Cash Equivalents | 7,414,208 | |||

| Receivable for securities sold | 2,340,646 | |||

| Dividends and interest receivable | 1,676,918 | |||

| Foreign currency, at value (cost $487,813) | 488,311 | |||

| Unrealized appreciation on foreign exchange currency contracts | 251,946 | |||

| Tax Reclaims receivable | 56,281 | |||

| Other assets | 23,645 | |||

| Total assets | 227,752,533 | |||

| Liabilities | ||||

| Borrowings | 50,000,000 | |||

| Payable for securities purchased | 5,797,474 | |||

| Options written, at value (premiums received of $104,950) | 117,878 | |||

| Investment Management fee payable | 93,016 | |||

| Investment Advisory fee payable | 89,368 | |||

| Administrative fee payable | 4,805 | |||

| Interest due on borrowings | 3,715 | |||

| Unrealized depreciation on foreign exchange currency contracts | 100 | |||

| Accrued expenses and other liabilities | 148,213 | |||

| Total liabilities | 56,254,569 | |||

| Net Assets | $ | 171,497,964 | ||

| Composition of Net Assets | ||||

| Common stock, $0.001 par value per share; unlimited number of shares authorized, 13,603,025 shares issued and outstanding | $ | 13,603 | ||

| Additional paid-in capital | 243,316,208 | |||

| Accumulated net realized loss on investments, options, swaps and foreign currency transactions | (84,725,492 | ) | ||

| Accumulated net unrealized appreciation on investments, options and foreign currency translation | 17,828,836 | |||

| Distributions in excess of net investment income | (4,935,191 | ) | ||

| Net Assets | $ | 171,497,964 | ||

| Net Asset Value | ||||

| (based on 13,603,025 common shares outstanding) | $ | 12.61 | ||

See notes to financial statements.

16 | Semiannual Report | April 30, 2010

LCM | Advent/Claymore Enhanced Growth & Income Fund

Statement of Operations | For the six months ended April 30, 2010 (unaudited) |

| Investment Income | ||||||||

| Interest | $ | 2,432,894 | ||||||

| Dividends (net of foreign withholding taxes of $1,071) | 1,319,702 | |||||||

| Total income | $ | 3,752,596 | ||||||

| Expenses | ||||||||

| Investment Management fee | 462,789 | |||||||

| Investment Advisory fee | 444,641 | |||||||

| Line of credit fee | 144,479 | |||||||

| Professional fees | 92,461 | |||||||

| Trustees’ fees and expenses | 74,352 | |||||||

| Fund accounting | 32,782 | |||||||

| Printing expense | 31,471 | |||||||

| Administration fee | 24,758 | |||||||

| Custodian fee | 20,368 | |||||||

| Insurance | 11,472 | |||||||

| NYSE listing fee | 10,498 | |||||||

| Transfer agent fee | 9,511 | |||||||

| Miscellaneous | 6,815 | |||||||

| Interest Expense | 119,052 | |||||||

| Total expenses | 1,485,449 | |||||||

| Net investment income | 2,267,147 | |||||||

| Realized and Unrealized Gain (Loss) on Investments, Options and Foreign Currency Transactions | ||||||||

| Net realized gain (loss) on: | ||||||||

| Investments | 11,937,201 | |||||||

| Options | (537,260 | ) | ||||||

| Foreign currency transactions | 37,813 | |||||||

| Change in net unrealized appreciation (depreciation) on: | ||||||||

| Investments | 5,951,511 | |||||||

| Options | (552,126 | ) | ||||||

| Foreign currency translation | 206,308 | |||||||

| Net realized and unrealized gain on investments, options and foreign currency transactions | 17,043,447 | |||||||

| Net Increase in Net Assets Resulting from Operations | $ | 19,310,594 | ||||||

See notes to financial statements.

Semiannual Report | April 30, 2010 | 17

LCM | Advent/Claymore Enhanced Growth & Income Fund

Statement of Changes in Net Assets |

For the Six | For the | |||||||

Months ended | Year Ended | |||||||

April 30, 2010(unaudited) | October 31, 2009 | |||||||

| Change in Net Assets from Operations | ||||||||

| Net investment income | $ | 2,267,147 | $ | 5,333,606 | ||||

| Net realized gain (loss) on investments, options, swaps and foreign currency transactions | 11,437,754 | (47,458,544 | ) | |||||

| Net change in unrealized appreciation (depreciation) on investments, options and | ||||||||

| foreign currency translation | 5,605,693 | 68,646,666 | ||||||

| Net increase in net assets resulting from operations | 19,310,594 | 26,521,728 | ||||||

| Distributions to Common Shareholders from | ||||||||

| Net investment income | (7,182,397 | ) | (9,090,807 | ) | ||||

| Return of Capital | – | (6,443,848 | ) | |||||

| Total dividends and distributions to common shareholders | (7,182,397 | ) | (15,534,655 | ) | ||||

| Total increase in net assets | 12,128,197 | 10,987,073 | ||||||

| Net Assets | ||||||||

| Beginning of year | 159,369,767 | 148,382,694 | ||||||

| End of year (including distributions in excess of net investment income of | ||||||||

| $(4,935,191) and $(19,941), respectively) | $ | 171,497,964 | $ | 159,369,767 | ||||

See notes to financial statements.

18 | Semiannual Report | April 30, 2010

LCM | Advent/Claymore Enhanced Growth & Income Fund

Statement of Cash Flows | For the six months ended April 30, 2010 (unaudited) |

| Cash Flows from Operating Activities: | ||||

| Net increase in net assets resulting from operations | $ | 19,310,594 | ||

Adjustments to Reconcile Net Increase in Net Assets Resulting from Operations to Net Cash Used in Operating and Investing Activities: | ||||

| Net change in unrealized appreciation on investments | (5,951,511 | ) | ||

| Net change in unrealized depreciation on options | 552,126 | |||

| Net change in unrealized appreciation on foreign currency transactions | (206,308 | ) | ||

| Net realized gain on investments | (11,937,201 | ) | ||

| Net realized loss on options | 537,260 | |||

| Net realized gain on foreign currency transactions | (37,813 | ) | ||

| Purchase of long-term investments | (165,410,961 | ) | ||

| Proceeds from sale of long-term investments | 113,219,905 | |||

| Cost of written options assigned and closed | (528,053 | ) | ||

| Net Amortization of premium and other | (1,886,173 | ) | ||

| Decrease in receivable for securities sold | 5,764,992 | |||

| Increase in dividends and interest receivable | (441,999 | ) | ||

| Decrease in foreign currency | 12,951 | |||

| Decrease in tax reclaims receivable | 25,065 | |||

| Decrease in other assets | 15,814 | |||

| Increase in payable for investments purchased | 4,805,528 | |||

| Increase in interest due on borrowings | 3,715 | |||

| Premiums received on call options written | 626,371 | |||

| Increase in investment management fee payable | 22,282 | |||

| Increase in investment advisory fee payable | 21,407 | |||

| Increase in administrative fee payable | 1,067 | |||

| Decrease in accrued expenses and other liabilities | (19,462 | ) | ||

| Net Cash Provided in Operating and Investing Activities | (41,500,404 | ) | ||

| Cash Flows From 4Financing Activities: | ||||

| Dividends paid to common shareholders | (7,182,397 | ) | ||

| Proceeds from borrowings | 50,000,000 | |||

| Net Cash Provided by Financing Activities | 42,817,603 | |||

| Net increase in cash | 1,317,199 | |||

| Cash at Beginning of Period | 6,097,009 | |||

| Cash at End of Period | $ | 7,414,208 | ||

| Supplemental Disclosure of Cash Flow Information: Cash paid during the period for interest | $ | 115,337 | ||

See notes to financial statements.

Semiannual Report | April 30, 2010 | 19

LCM | Advent/Claymore Enhanced Growth & Income Fund

Financial Highlights |

| Per share operating performance for a common share outstanding throughout the period | For the Six Months Ended April 30, 2010 (unaudited) | For the Year Ended October 31, 2009 | For the Year Ended October 31, 2008 | For the Year Ended October 31, 2007 | For the Year Ended October 31, 2006 | For the Period January 31,2005 through October 31, 2005 |

| Net asset value, beginning of period | $ | 11.72 | $ | 10.91 | $ | 20.09 | $ | 19.41 | $ | 18.51 | $ | 19.10 | (a) | |||||||||||

| Income from investment operations | ||||||||||||||||||||||||

Net investment income (b) | 0.17 | 0.39 | 0.47 | 0.44 | 0.58 | 0.47 | ||||||||||||||||||

Net realized and unrealized gain (loss) on investments, options, swaps and foreign currency transactions | 1.25 | 1.56 | (8.05 | ) | 1.84 | 1.92 | (0.22 | ) | ||||||||||||||||

| Total from investment operations | 1.42 | 1.95 | (7.58 | ) | 2.28 | 2.50 | 0.25 | |||||||||||||||||

Common shares’ offering expenses charged to paid-in capital | – | – | – | – | – | (0.04 | ) | |||||||||||||||||

| Distributions to Common Shareholders | ||||||||||||||||||||||||

| Net investment income | (0.53 | ) | (0.67 | ) | (0.90 | ) | (1.60 | ) | (1.60 | ) | (0.80 | ) | ||||||||||||

| Return of capital | – | (0.47 | ) | (0.70 | ) | – | – | – | ||||||||||||||||

Total dividends and distributions to Common Shareholders | (0.53 | ) | (1.14 | ) | (1.60 | ) | (1.60 | ) | (1.60 | ) | (0.80 | ) | ||||||||||||

| Net asset value, end of period | $ | 12.61 | $ | 11.72 | $ | 10.91 | $ | 20.09 | $ | 19.41 | $ | 18.51 | ||||||||||||

| Market value, end of period | $ | 12.01 | $ | 10.48 | $ | 8.97 | $ | 17.46 | $ | 18.78 | $ | 16.83 | ||||||||||||

Total investment return (c) | ||||||||||||||||||||||||

| Net asset value | 12.48 | % | 19.74 | % | -40.37 | % | 12.24 | % | 14.11 | % | 1.12 | % | ||||||||||||

| Market value | 20.10 | % | 34.17 | % | -42.88 | % | 1.08 | % | 22.20 | % | -12.08 | % | ||||||||||||

| Ratios and supplemental data | ||||||||||||||||||||||||

| Net assets, end of period (thousands) | $ | 171,498 | $ | 159,370 | $ | 148,383 | $ | 273,288 | $ | 263,648 | $ | 251,349 | ||||||||||||

Ratios to Average Net Assets applicable to Common Shares: | ||||||||||||||||||||||||

| Operating Expenses | 1.60 | %(e) | 1.42 | % | 1.34 | % | 1.26 | % | 1.29 | % | 1.38 | %(e) | ||||||||||||

Interest Expense (d) | 0.15 | %(e) | N/A | N/A | N/A | N/A | N/A | |||||||||||||||||

| Total Expenses | 1.75 | %(e) | N/A | N/A | N/A | N/A | N/A | |||||||||||||||||

Net investment income, including interest expense | 2.79 | %(e) | 3.68 | % | 2.91 | % | 2.21 | % | 3.09 | % | 3.37 | %(e) | ||||||||||||

Portfolio turnover rate (f) | 64 | % | 236 | % | 192 | % | 181 | % | 415 | % | 246 | % | ||||||||||||

| Senior Indebtedness | ||||||||||||||||||||||||

Total Borrowings outstanding (in thousands) | $ | 50,000 | N/A | N/A | N/A | N/A | N/A | |||||||||||||||||

Asset Coverage per $1000 of indebtedness (g) | $ | 4,430 | N/A | N/A | N/A | N/A | N/A |

| * | Commencement of investment operations. |

| (a) | Before deduction of offering expenses charged to capital. |

| (b) | Based on average shares outstanding during the period. |

| (c) | Total investment return is calculated assuming a purchase of a common share at the beginning of the period and a sale on the last day of the period reported either at net asset value (“NAV”) or market price per share. Dividends and distributions are assumed to be reinvested at NAV for NAV returns or the prices obtained under the Fund’s Dividend Reinvestment Plan for market value returns. Total investment return does not reflect brokerage commissions. A return calculated for a period of less than one year is not annualized. |

| (d) | Interest expense ratio relates to interest associated with borrowings. |

| (e) | Annualized. |

| (f) | Portfolio turnover is not annualized for periods less than one year. |

| (g) | Calculated by subtracting the Fund’s total liabilities (not including the borrowings) from the Fund’s total assets and dividing by the total borrowings. |

See notes to financial statements.

20 | Semiannual Report | April 30, 2010

LCM | Advent/Claymore Enhanced Growth & Income Fund

Notes to Financial Statements | April 30, 2010 (unaudited) |

Note 1 – Organization:

Advent/Claymore Enhanced Growth & Income Fund (the “Fund”) was organized as a Delaware statutory trust on January 30, 2004. The Fund is registered as a diversified, closed-end management investment company under the Investment Company Act of 1940, as amended.

The Fund’s primary investment objective is to provide current income and current gains from trading in securities, with a secondary objective of long-term capital appreciation. The Fund will pursue its investment objectives by investing its assets in dividend and interest paying equity securities, convertible securities and non-convertible high-yield securities. Also, in pursuit of the Fund’s primary investment objective, the Fund intends to engage in an option strategy of writing (selling) covered call options on at least 50% of the securities held in the portfolio.

Note 2 – Accounting Policies:

The preparation of the financial statements in accordance with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from these estimates.

The following is a summary of significant accounting policies followed by the Fund.

(a) Valuation of Investments

Equity securities listed on an exchange are valued at the last reported sale price on the primary exchange on which they are traded. Equity securities traded on an exchange for which there are no transactions on a given day are valued at the mean of the closing bid and asked prices. Securities traded on NASDAQ are valued at the NASDAQ Official Closing Price. Equity securities not listed on a securities exchange or NASDAQ are valued at the mean of the closing bid and asked prices. Debt securities are valued by independent pricing services or dealers using the closing bid prices for such securities or, if such prices are not available, at prices for securities of comparable maturity, quality and type. Futures contracts are valued using the settlement price established each day on the exchange on which they are traded. Exchange-traded options are valued at the closing price, if traded that day. If not traded, they are valued at the mean of the bid and asked prices on the primary exchange on which they are traded. For those securities where quotations or prices are not available, valuations are determined in accordance with procedures established in good faith by the Board of Trustees. Short-term securities with remaining maturities of 60 days or less are valued at amortized cost, which approximates market value.

For those securities where quotations or prices are not available, the valuations are determined in accordance with procedures established in good faith by the Board of Trustees. Valuations in accordance with these procedures are intended to reflect each security’s (or asset’s) “fair value”. Such “fair value” is the amount that the Fund might reasonably expect to receive for the security (or asset) upon its current sale. Each such determination should be based on a consideration of all relevant factors, which are likely to vary from one pricing context to another. Examples of such factors may include, but are not limited to: (i) the type of security, (ii) the initial cost of the security, (iii) the existence of any contractual restrictions on the security’s disposition, (iv) the price and extent of public trading in similar securities of the issuer or of comparable companies, (v) quotations or evaluated prices from broker-dealers and/or pricing services, (vi) information obtained from the issuer, analysts, and/or the appropriate stock exchange (for exchange traded securities), (vii) an analysis of the company’s financial statements, and (viii) an evaluation of the forces that influence the issuer and the market(s) in which the security is purchased and sold (e.g. the existence of pending merger activity, public offerings or tender offers that might affect the value of the security). There were no securities fair valued in accordance with such procedures established by the Board of Trustees at April 30, 2010.

GAAP requires disclosure of fair valuation measurements as of each measurement date. In compliance with GAAP, the Fund follows a fair value hierarchy that distinguishes between market data obtained from independent sources (observable inputs) and the Fund’s own market assumptions (unobservable inputs). These inputs are used in determining the value of the Fund’s investments and summarized in the following fair value hierarchy:

Level 1 – quoted prices in active markets for identical securities

Level 2 – quoted prices in inactive markets or other significant observable inputs (e.g. quoted prices for similar securities; interest rates; prepayment speed; credit risk; yield curves)

Level 3 – significant unobservable inputs (e.g. discounted cash flow analysis; non-market based methods used to determine fair value)