Exhibit 99.1

Investor Presentation

July 2005

Forward Looking Information and Non-GAAP Reconciliations

This presentation may include forward-looking statements. These forward-looking statements include comments with respect to our objectives and strategies and the results of our operations and our business. However, by their nature, these forward-looking statements involve numerous assumptions, uncertainties and opportunities, both general and specific. The risk exists that these statements may not be fulfilled. We caution readers of this presentation not to place undue reliance on these forward-looking statements, as a number of factors could cause future company results to differ materially from these statements. Forward-looking statements may be influenced in particular by factors such as fluctuations in interest rates and stock indices, the effects of competition in the areas in which we operate and changes in economic, political, regulatory and technological conditions. We caution that the foregoing list is not exhaustive. When relying on forward-looking statements to make decisions, investors should carefully consider the aforementioned factors as well as other uncertainties and events.

Throughout this presentation, certain non-GAAP metrics are provided that management believes provide useful information in understanding the financial performance of the Company. Reconciliations of the non-GAAP metrics to the comparable GAAP metrics are provided in the Company’s Annual Report on Form 10K for the year ended December 31, 2004, which is available on the Company’s website at www.plsb.com.

2

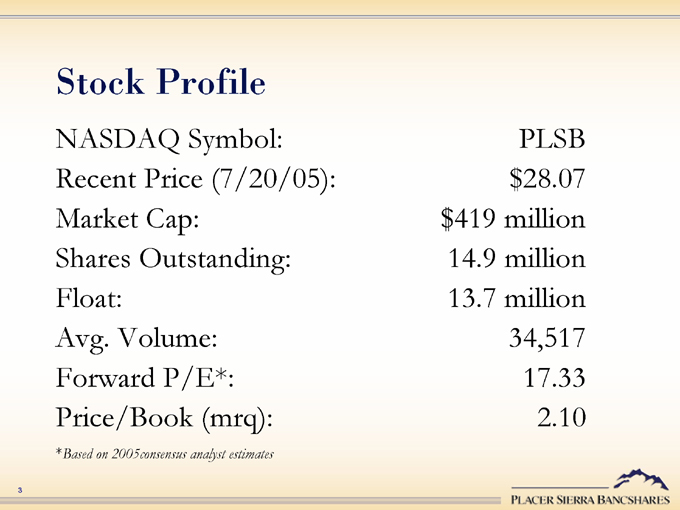

Stock Profile

NASDAQ Symbol: PLSB

Recent Price (7/20/05): $28.07

Market Cap: $419 million

Shares Outstanding: 14.9 million

Float: 13.7 million

Avg. Volume: 34,517

Forward P/E*: 17.33

Price/Book (mrq): 2.10

*Based on 2005consensus analyst estimates

3

Company Overview

Placer Sierra Bancshares

At $1.9 billion, Placer Sierra is the largest community bank headquartered in Central California Placer Sierra operates in the greater Sacramento, Central and Southern California high-growth market areas Experienced management team that has extensive knowledge of both Northern and Southern California banking markets Asset sensitive balance sheet well positioned for a rising interest rate environment Attractive banking franchise with low cost of deposits

5

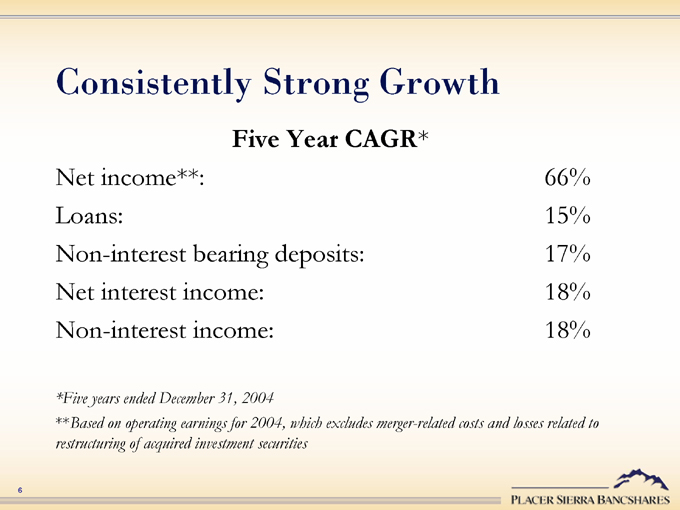

Consistently Strong Growth

Five Year CAGR*

Net income**: 66%

Loans: 15%

Non-interest bearing deposits: 17%

Net interest income: 18%

Non-interest income: 18%

*Five years ended December 31, 2004

**Based on operating earnings for 2004, which excludes merger-related costs and losses related to restructuring of acquired investment securities

6

Long-Term Performance Goals

ROE: 15%

ROA: 1.50%-1.60%

EPS Growth: 20%/Year

Loan Growth: 13%/Year

Deposit Growth: 14%/Year

Efficiency Ratio: 50%-55%

7

Operating and Growth Strategies

Capitalize on growth opportunities in both our Northern and Southern California markets

Expand through strategically placed new branches in Northern and Central California

Acquire one or more retail banking franchises in Southern California to complement Bank of Orange County’s well established commercial lending business

Continue to aggressively recruit experienced commercial bankers with portfolios of loyal customers

8

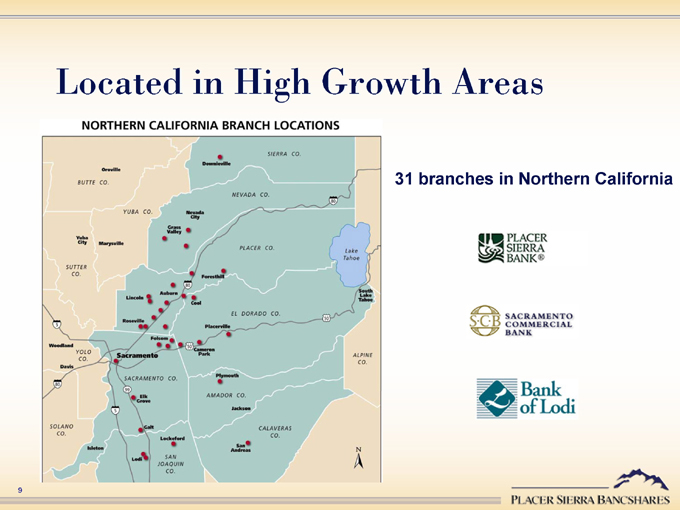

Located in High Growth Areas

NORTHERN CALIFORNIA BRANCH LOCATIONS

31 branches in Northern California

9

Northern California Market Opportunity

Expand down Highway 99 to the cities of Modesto, Fresno and Bakersfield

SVP from Bank of America hired to oversee expansion

Loan production office established in May 2005 in Fresno

10

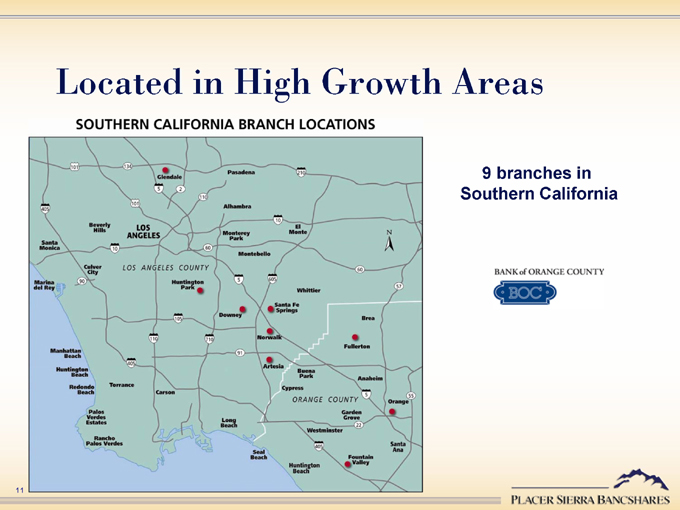

Located in High Growth Areas

SOUTHERN CALIFORNIA BRANCH LOCATIONS

9 branches in Southern California

11

Southern California Market Opportunity

Expand into Riverside and San Bernardino Counties

Former CEO of Pacific Century Bank hired to oversee expansion

12

Financial Performance

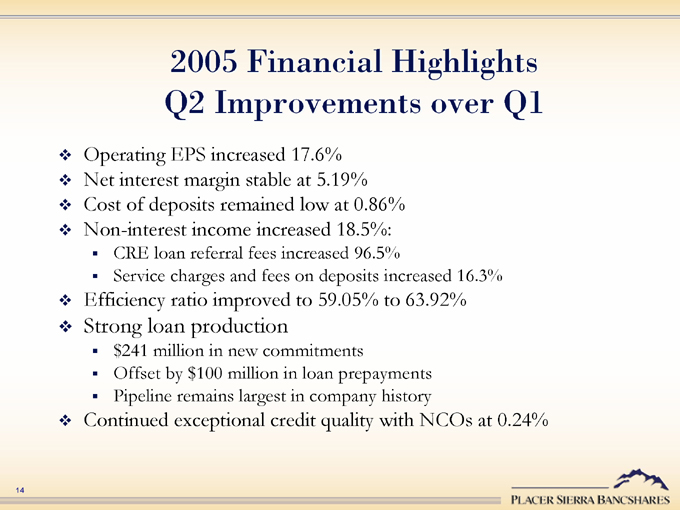

2005 Financial Highlights Q2 Improvements over Q1

Operating EPS increased 17.6% Net interest margin stable at 5.19% Cost of deposits remained low at 0.86% Non-interest income increased 18.5%:

CRE loan referral fees increased 96.5%

Service charges and fees on deposits increased 16.3%

Efficiency ratio improved to 59.05% to 63.92%

Strong loan production

$241 million in new commitments Offset by $100 million in loan prepayments Pipeline remains largest in company history

Continued exceptional credit quality with NCOs at 0.24%

14

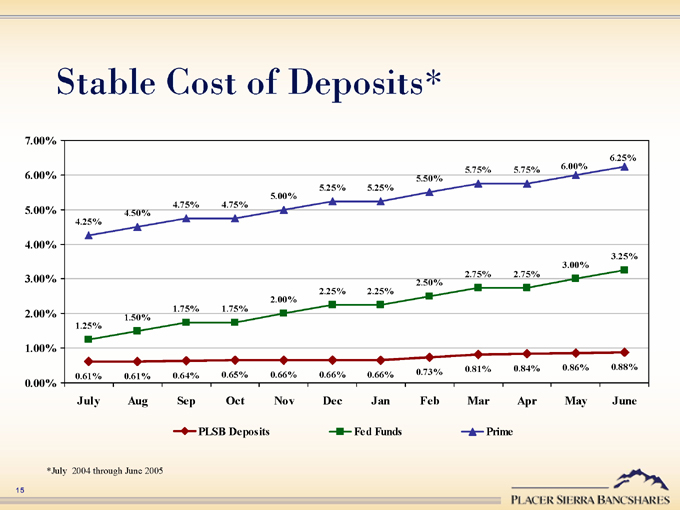

Stable Cost of Deposits*

7.00% 6.00% 5.00% 4.00% 3.00% 2.00% 1.00% 0.00%

July Aug Sep Oct Nov Dec Jan Feb Mar Apr May June

4.25% 1.25% 0.61%

4.50% 1.50% 0.61%

4.75% 1.75% 0.64%

4.75% 1.75% 0.65%

5.00% 2.00% 0.66%

5.25% 2.25% 0.66%

5.25% 2.25% 0.66%

5.50% 2.50% 0.73%

5.75% 2.75% 0.81%

5.75% 2.75% 0.84%

6.00% 3.00% 0.86%

6.25% 3.25% 0.88%

PLSB Deposits

Fed Funds

Prime

*July 2004 through June 2005

15

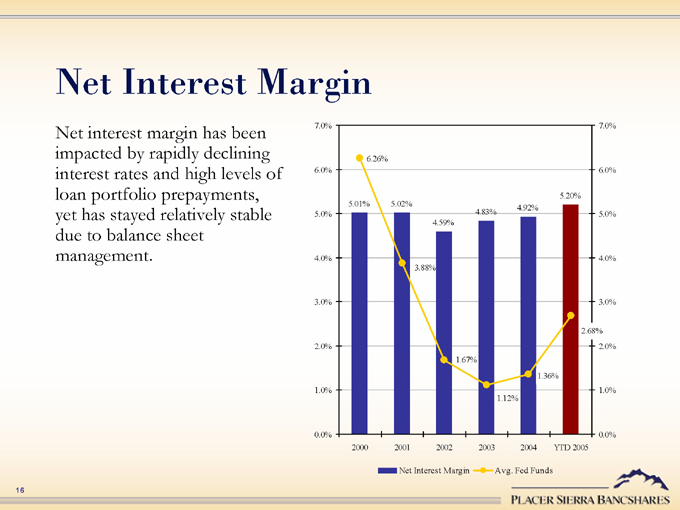

Net Interest Margin

Net interest margin has been impacted by rapidly declining interest rates and high levels of loan portfolio prepayments, yet has stayed relatively stable due to balance sheet management.

7.0% 6.0% 5.0% 4.0% 3.0% 2.0% 1.0% 0.0%

2000 2001 2002 2003 2004 YTD 2005

7.0% 6.0% 5.0% 4.0% 3.0% 2.0% 1.0% 0.0%

5.01% 6.26% 5.02% 3.88% 4.59% 1.67% 4.83% 1.12% 4.92% 1.36% 5.20% 2.68%

Net Interest Margin Avg. Fed Funds

16

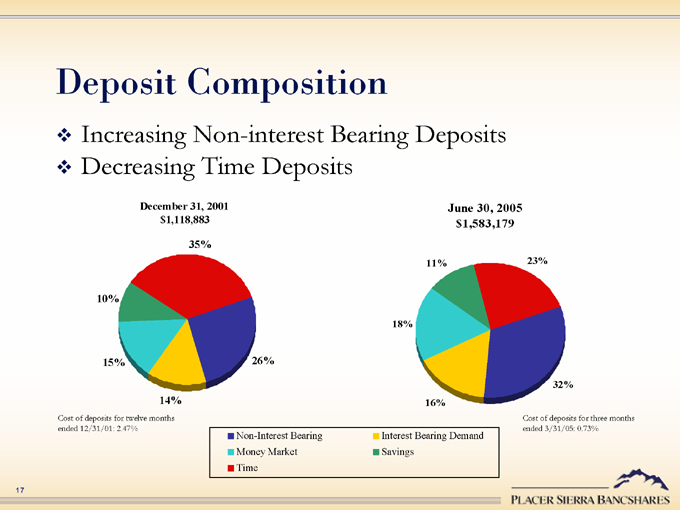

Deposit Composition

Increasing Non-interest Bearing Deposits Decreasing Time Deposits

December 31, 2001 $1,118,883

35% 26% 14% 15% 10%

Cost of deposits for twelve months ended 12/31/01: 2.47%

June 30, 2005 $1,583,179

23% 32% 16% 18% 11%

Cost of deposits for three months ended 3/31/05: 0.73%

Non-Interest Bearing Money Market Time

Interest Bearing Demand Savings

17

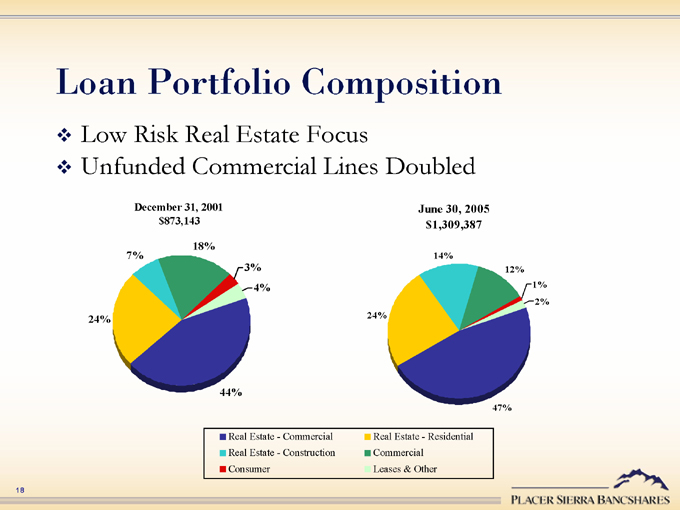

Loan Portfolio Composition

Low Risk Real Estate Focus

Unfunded Commercial Lines Doubled

December 31, 2001 $873,143

18% 3% 4% 44% 24% 7%

June 30, 2005 $1,309,387

14% 12% 1% 2% 47% 24%

Real Estate—Commercial Real Estate—Construction Consumer

Real Estate—Residential Commercial Leases & Other

18

2005 Expectations

Comfortable with full year consensus estimate of $1.62

Consistent improvement in bottom-line performance throughout the year Funded full year loan growth of 11%-12%

Loan production expected to be significantly higher—targeting $800 million in new commitments in 2005 CRE loan production being sold to generate near-term income to support expansion in Fresno and Southern California

Full year deposit growth of 14%-15%

Net interest margin should trend down to low 5% range by end of the year Growth in earning assets expected to more than offset reduction in net interest margin Continued high credit quality

19

Investor Presentation

July 2005