Exhibit 99.1

SUMMARY

| | Years Ended | |

| | December 31,

2019 | | December 31,

2018 | |

FINANCIAL | | | | | |

(thousands of Canadian dollars, except per common share amounts) | | | | | |

Petroleum and natural gas sales | | $ | 1,805,919 | | $ | 1,428,870 | |

Adjusted funds flow (1) | | 902,426 | | 472,983 | |

Per share - basic | | 1.62 | | 1.35 | |

Per share - diluted | | 1.62 | | 1.35 | |

Net income (loss) | | (12,459 | ) | (325,309 | ) |

Per share - basic | | (0.02 | ) | (0.93 | ) |

Per share - diluted | | (0.02 | ) | (0.93 | ) |

| | | | | |

Capital Expenditures | | | | | |

Exploration and development expenditures (1) | | $ | 552,291 | | $ | 495,721 | |

Acquisitions, net of divestitures | | 2,180 | | 1,603,850 | |

Total oil and natural gas capital expenditures | | $ | 554,471 | | $ | 2,099,571 | |

| | | | | |

Net Debt | | | | | |

Bank loan (2) | | $ | 506,471 | | $ | 522,294 | |

Long-term notes (2) | | 1,337,200 | | 1,596,323 | |

Long-term debt | | 1,843,671 | | 2,118,617 | |

Working capital deficiency | | 28,120 | | 146,550 | |

Net debt (1) | | $ | 1,871,791 | | $ | 2,265,167 | |

| | | | | |

Shares Outstanding - basic (thousands) | | | | | |

Weighted average | | 557,048 | | 351,542 | |

End of period | | 558,305 | | 554,060 | |

Baytex Energy Corp. 2019 Annual Report

1

| | Years Ended | |

| | December 31,

2019 | | December 31,

2018 | |

OPERATING | | | | | |

Daily Production | | | | | |

Light oil and condensate (bbl/d) | | 43,587 | | 29,264 | |

Heavy oil (bbl/d) | | 26,741 | | 25,954 | |

NGL (bbl/d) | | 10,229 | | 9,745 | |

Total liquids (bbl/d) | | 80,557 | | 64,963 | |

Natural gas (mcf/d) | | 102,742 | | 92,971 | |

Oil equivalent (boe/d @ 6:1) (3) | | 97,680 | | 80,458 | |

| | | | | |

Netback (thousands of Canadian dollars) | | | | | |

Total sales, net of blending and other expense (4) | | $ | 1,737,124 | | $ | 1,360,038 | |

Royalties | | (320,241 | ) | (313,754 | ) |

Operating expense | | (397,716 | ) | (311,592 | ) |

Transportation expense | | (43,942 | ) | (36,869 | ) |

Operating netback | | $ | 975,225 | | $ | 697,823 | |

General and administrative | | (45,469 | ) | (45,825 | ) |

Cash financing and interest | | (107,417 | ) | (104,318 | ) |

Realized financial derivatives gain (loss) | | 75,620 | | (73,165 | ) |

Other (5) | | 4,467 | | (1,532 | ) |

Adjusted funds flow (1) | | $ | 902,426 | | $ | 472,983 | |

| | | | | |

Netback (per boe) | | | | | |

Total sales, net of blending and other expense(4) | | $ | 48.72 | | $ | 46.31 | |

Royalties | | (8.98 | ) | (10.68 | ) |

Operating expense | | (11.16 | ) | (10.61 | ) |

Transportation expense | | (1.23 | ) | (1.26 | ) |

Operating netback (1) | | $ | 27.35 | | $ | 23.76 | |

General and administrative | | (1.28 | ) | (1.56 | ) |

Cash financing and interest | | (3.01 | ) | (3.55 | ) |

Realized financial derivatives (loss) gain | | 2.12 | | (2.49 | ) |

Other (5) | | 0.13 | | (0.05 | ) |

Adjusted funds flow (1) | | $ | 25.31 | | $ | 16.11 | |

Notes:

(1) The terms “adjusted funds flow”, “exploration and development expenditures”, “net debt” and “operating netback” do not have any standardized meaning as prescribed by Canadian Generally Accepted Accounting Principles (“GAAP”) and therefore may not be comparable to similar measures presented by other companies where similar terminology is used. See the advisory on non-GAAP measures at the end of this press release.

(2) Principal amount of instruments. The carrying amount of debt issue costs associated with the bank loan and long-term notes are excluded on the basis that these amounts have been paid by Baytex and do not represent an additional source of capital or repayment obligations.

(3) Barrel of oil equivalent (“boe”) amounts have been calculated using a conversion rate of six thousand cubic feet of natural gas to one barrel of oil. The use of boe amounts may be misleading, particularly if used in isolation. A boe conversion ratio of six thousand cubic feet of natural gas to one barrel of oil is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead.

(4) Realized heavy oil prices are calculated based on sales dollars, net of blending and other expense. We include the cost of blending diluent in our realized heavy oil sales price in order to compare the realized pricing on our produced volumes to the WCS benchmark.

(5) Other is comprised of realized foreign exchange gain or loss, other income or expense, current income tax expense or recovery and payments on onerous contracts. Refer to the 2019 MD&A for further information on these amounts.

2

Advisory Regarding Forward-Looking Statements

In the interest of providing Baytex’s shareholders and potential investors with information regarding Baytex, including management’s assessment of Baytex’s future plans and operations, certain statements in this report are “forward-looking statements” within the meaning of the United States Private Securities Litigation Reform Act of 1995 and “forward-looking information” within the meaning of applicable Canadian securities legislation (collectively, “forward-looking statements”). In some cases, forward-looking statements can be identified by terminology such as “anticipate”, “believe”, “continue”, “could”, “estimate”, “expect”, “forecast”, “intend”, “may”, “objective”, “ongoing”, “outlook”, “potential”, “project”, “plan”, “should”, “target”, “would”, “will” or similar words suggesting future outcomes, events or performance. The forward-looking statements contained in this report speak only as of the date thereof and are expressly qualified by this cautionary statement.

Specifically, this report contains forward-looking statements relating to but not limited to: our business strategies, plans and objectives; that we have flexibility to execute our business plan driving free cash flow and strengthening our balance sheet; our 2020 production and capital expenditure guidance; that our exploration and development program is expended to be fully funded by adjusted funds flow at the forward strip and we have flexibility to adjust our spending plans; the percentage of our net crude oil exposure that is hedged for 2020; that after completing the announced redemption of long-term notes our credit facilities will be one-third undrawn, we will have over $300 million of liquidity and the weighted average cost of our debt will be approximately 6%; that we have a strong drilling inventory of approximately 10 or more years in each core asset; we are committed to stable production, generating free cash flow and strengthening our balance sheet.

In addition, information and statements relating to reserves are deemed to be forward-looking statements, as they involve implied assessment, based on certain estimates and assumptions, that the reserves described exist in quantities predicted or estimated, and that they can be profitably produced in the future.

These forward-looking statements are based on certain key assumptions regarding, among other things: petroleum and natural gas prices and differentials between light, medium and heavy oil prices; well production rates and reserve volumes; our ability to add production and reserves through our exploration and development activities; capital expenditure levels; our ability to borrow under our credit agreements; the receipt, in a timely manner, of regulatory and other required approvals for our operating activities; the availability and cost of labour and other industry services; interest and foreign exchange rates; the continuance of existing and, in certain circumstances, proposed tax and royalty regimes; our ability to develop our crude oil and natural gas properties in the manner currently contemplated; and current industry conditions, laws and regulations continuing in effect (or, where changes are proposed, such changes being adopted as anticipated). Readers are cautioned that such assumptions, although considered reasonable by Baytex at the time of preparation, may prove to be incorrect.

Actual results achieved will vary from the information provided herein as a result of numerous known and unknown risks and uncertainties and other factors. Such factors include, but are not limited to: the volatility of oil and natural gas prices and price differentials; availability and cost of gathering, processing and pipeline systems; failure to comply with the covenants in our debt agreements; the availability and cost of capital or borrowing; that our credit facilities may not provide sufficient liquidity or may not be renewed; risks associated with a third-party operating our Eagle Ford properties; the cost of developing and operating our assets; depletion of our reserves; risks associated with the exploitation of our properties and our ability to acquire reserves; new regulations on hydraulic fracturing; restrictions on or access to water or other fluids; changes in government regulations that affect the oil and gas industry; regulations regarding the disposal of fluids; changes in environmental, health and safety regulations; public perception and its influence on the regulatory regime; restrictions or costs imposed by climate change initiatives; variations in interest rates and foreign exchange rates; risks associated with our hedging activities; changes in income tax or other laws or government incentive programs; uncertainties associated with estimating oil and natural gas reserves; our inability to fully insure against all risks; risks of counterparty default; risks associated with acquiring, developing and exploring for oil and natural gas and other aspects of our operations; risks associated with large projects; risks related to our thermal heavy oil projects; alternatives to and changing demand for petroleum products; risks associated with our use of information technology systems; risks associated with the ownership of our securities, including changes in market-based factors; risks for United States and other non-resident shareholders, including the ability to enforce civil remedies, differing practices for reporting reserves and production, additional taxation applicable to non-residents and foreign exchange risk; and other factors, many of which are beyond our control.

These and additional risk factors are discussed in our Annual Information Form, Annual Report on Form 40-F and Management’s Discussion and Analysis for the year ended December 31, 2019, to be filed with Canadian securities regulatory authorities and the U.S. Securities and Exchange Commission not later than March 31, 2020 and in our other public filings

The above summary of assumptions and risks related to forward-looking statements has been provided in order to provide shareholders and potential investors with a more complete perspective on Baytex’s current and future operations and such information may not be appropriate for other purposes.

There is no representation by Baytex that actual results achieved will be the same in whole or in part as those referenced in the forward-looking statements and Baytex does not undertake any obligation to update publicly or to revise any of the included forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required by applicable securities law.

All amounts in this report are stated in Canadian dollars unless otherwise specified.

3

Non-GAAP Financial and Capital Management Measures

In this report, we refer to certain financial measures (such as adjusted funds flow, EBITDA, exploration and development expenditures, free cash flow, net debt and operating netback) which do not have any standardized meaning prescribed by Canadian GAAP (“non-GAAP measures”) and are considered non-GAAP measures. While adjusted funds flow, EBITDA, exploration and development expenditures, free cash flow, net debt and operating netback are commonly used in the oil and gas industry, our determination of these measures may not be comparable with calculations of similar measures for other issuers.

Adjusted funds flow is not a measurement based on generally accepted accounting principles (“GAAP”) in Canada, but is a financial term commonly used in the oil and gas industry. We define adjusted funds flow as cash flow from operating activities adjusted for changes in non-cash operating working capital and asset retirement obligations settled. Our determination of adjusted funds flow may not be comparable to other issuers. We consider adjusted funds flow a key measure that provides a more complete understanding of operating performance and our ability to generate funds for exploration and development expenditures, debt repayment, settlement of our abandonment obligations and potential future dividends. In addition, we use a ratio of net debt to adjusted funds flow to manage our capital structure. We eliminate settlements of abandonment obligations from cash flow from operations as the amounts can be discretionary and may vary from period to period depending on our capital programs and the maturity of our operating areas. The settlement of abandonment obligations are managed with our capital budgeting process which considers available adjusted funds flow. Changes in non-cash working capital are eliminated in the determination of adjusted funds flow as the timing of collection, payment and incurrence is variable and by excluding them from the calculation we are able to provide a more meaningful measure of our cash flow on a continuing basis. For a reconciliation of adjusted funds flow to cash flow from operating activities, see Management’s Discussion and Analysis of the operating and financial results for the year ended December 31, 2019.

EBITDA is not a measurement based on GAAP in Canada. EBITDA is defined as net income or loss adjusted for financing and interest expenses, unrealized gains and losses on financial derivatives, income tax, non-recurring losses, payments on lease obligations, certain specific unrealized and non-cash transactions (including depletion, exploration and evaluation expenses, unrealized gains and losses on financial derivatives and foreign exchange and share-based compensation).

Exploration and development expenditures is not a measurement based on GAAP in Canada. We define exploration and development expenditures as additions to exploration and evaluation assets combined with additions to oil and gas properties. Our definition of exploration and development expenditures may not be comparable to other issuers. We use exploration and development expenditures to measure and evaluate the performance of our capital programs. The total amount of exploration and development expenditures is managed as part of our budgeting process and can vary from period to period depending on the availability of adjusted funds flow and other sources of liquidity.

Free cash flow is not a measurement based on GAAP in Canada. We define free cash flow as adjusted funds flow less exploration and development expenditures (both non-GAAP measures discussed above), payments on lease obligations, and asset retirement obligations settled. Our determination of free cash flow may not be comparable to other issuers. We use free cash flow to evaluate funds available for debt repayment, common share repurchases, potential future dividends and acquisition and disposition opportunities.

Net debt is not a measurement based on GAAP in Canada. We define net debt to be the sum of cash, trade and other accounts receivable, trade and other accounts payable, and the principal amount of both the long-term notes and the bank loan. Our definition of net debt may not be comparable to other issuers. We believe that this measure assists in providing a more complete understanding of our cash liabilities and provides a key measure to assess our liquidity. We use the principal amounts of the bank loan and long-term notes outstanding in the calculation of net debt as these amounts represent our ultimate repayment obligation at maturity. The carrying amount of debt issue costs associated with the bank loan and long-term notes is excluded on the basis that these amounts have already been paid by Baytex at inception of the contract and do not represent an additional source of capital or repayment obligation.

Operating netback is not a measurement based on GAAP in Canada, but is a financial term commonly used in the oil and gas industry. Operating netback is equal to petroleum and natural gas sales less blending expense, royalties, production and operating expense and transportation expense divided by barrels of oil equivalent sales volume for the applicable period. Our determination of operating netback may not be comparable with the calculation of similar measures for other entities. We believe that this measure assists in characterizing our ability to generate cash margin on a unit of production basis and is a key measure used to evaluate our operating performance.

4

MESSAGE TO SHAREHOLDERS

While we have been a publicly listed corporation for more than 25 years, we are taking steps to systematically transform Baytex. We are now a company with a diversified North American oil portfolio designed to generate free cash flow. We have shifted our portfolio to predominantly high operating netback, light oil assets while also reducing our cash cost structure and improving capital efficiencies. More recently, we have refinanced our long-term notes and extended the term of our revolving credit facilities to 2024. These steps give us the confidence and flexibility to execute our business plan to continue driving free cash flow and strengthening our balance sheet.

Despite the many challenges facing our industry today, we recognize that developing environmentally and socially responsible energy plays an important role in raising the standard of living for people around the world. In 2019 we continued our excellent health, safety and environmental performance and published our fourth biennial corporate sustainability report. This report demonstrates our commitment to transparency and to managing the environmental and social impacts of our business. We have elevated our standards, establishing a target to reduce our greenhouse gas emissions intensity by 30% over the next three years. We believe our safety and environmental leadership will serve us well as we continue to adapt to changing market conditions.

We have a high quality and diversified oil portfolio and our operating teams are well established with a track record of delivering results. In Canada, we have one of the largest conventional oil portfolios, including high operating netback, light oil production in the Viking and low decline, heavy oil production at Peace River and Lloydminster. We also hold a dominant land position in the emerging light oil resource play in the East Shale Duvernay, which has similar geologic and reservoir characteristics to our Eagle Ford shale asset in the United States. Our position in the Eagle Ford is defined by one of the highest quality, lowest-cost U.S. resource plays with outstanding drilling economics.

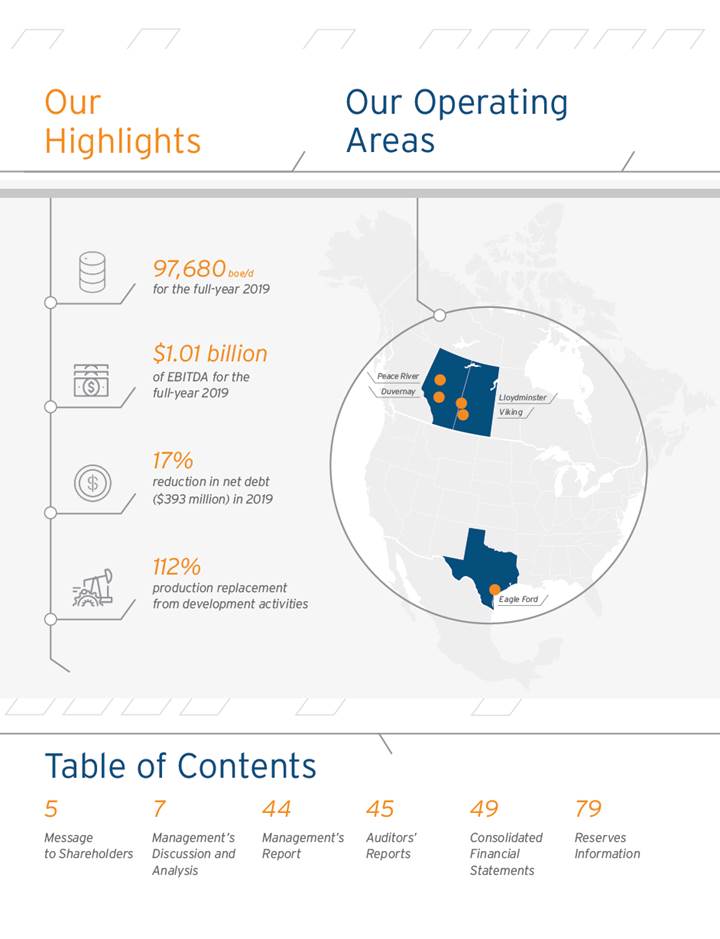

Our 2019 operating and financial results demonstrate the benefits of this diversified oil weighted portfolio and our commitment to allocate capital effectively, generate free cash flow and further strengthen our balance sheet. We produced 97,680 boe/d (82% liquids) and exceeded the high end of our annual guidance with capital expenditures at the low end of guidance totaling $552 million. This resulted in the following financial results:

· EBITDA of $1 billion and free cash flow of $329 million.

· Net debt reduction of 17%, or $393 million, due to the strong free cash flow and a strengthening of the Canadian dollar relative to the U.S. dollar.

· Redeemed our US$150 million principal amount of 6.75% senior unsecured notes nearly two years early.

We also demonstrated reserves growth with proved developed producing reserves increasing 5%, finding & development costs of $13/boe and a recycle ratio of 2.3x. In aggregate, we replaced 112% of 2019 production, adding 40 million boe of proved plus probable reserves through development activities. In the Eagle Ford, strong well performance continues to be driven by enhanced completions across our acreage position. In the Viking, over 90% of our drilling is now comprised of extended reach horizontal wells. In our heavy oil assets we delivered stable production with limited capital investment. We also continued to advance our Duvernay shale light oil asset with two strong wells in the East Shale Basin.

Subsequent to year-end, we issued US$500 million principal amount of 8.75% senior unsecured notes, maturing on April 1, 2027 which enabled us to redeem two series of notes; US$400 million principal amount of 5.125% senior unsecured notes due June 1, 2021 and $300 million principal amount of 6.625% senior unsecured notes due July 19, 2022. Following the redemption of these notes, our next long-term note maturity is June 2024.

We also extended the maturities of our revolving credit facilities and term loan to April 2, 2024. These credit facilities, which total $1.046 billion, are not borrowing base facilities and do not require annual or semi-annual reviews. Following all of these steps, our credit facilities are approximately one-third undrawn and we retain over $300 million of liquidity with a weighted average interest rate on our long-term debt of approximately 6%.

5

Looking Forward

We maintain an attractive and deep inventory of development locations with approximately ten years or more of remaining drilling opportunities in each of our core assets. We remain committed to delivering stable production, maximizing free cash flow and further strengthening our balance sheet.

Our 2020 annual guidance is unchanged as we target production of 93,000 to 97,000 boe/d with exploration and development expenditures of $500 to $575 million. At the time of writing, our exploration and development program is expected to be fully funded from adjusted funds flow at the forward strip and we have the operational flexibility to adjust our spending plans based on changes in commodity prices.

We maintain a consistent approach to risk management and marketing, utilizing various financial derivative contracts and crude-by-rail to reduce the volatility in our adjusted funds flow. For 2020, we have entered into hedges on approximately 48% of our net crude oil exposure, largely utilizing a 3-way option structure that provides WTI price protection at US$58/bbl with upside participation to US$63/bbl. We are also contracted to deliver 11,500 bbl/d of our heavy oil volumes to market by rail.

Baytex’s success is due to very engaged Board, management and employee group who are all strongly aligned and committed to driving value for shareholders. With the combined team, we are confident we have the skills, experience and focus that will create a more prosperous future.

We look forward to executing our plans in 2020 for the ongoing benefit of all stakeholders and we thank you for your continued support.

Sincerely, | |

| |

| |

/s/ Edward D. LaFehr | |

Edward D. LaFehr | |

President and Chief Executive Officer | |

| |

March 4, 2020 | |

6

MANAGEMENT’S DISCUSSION AND ANALYSIS

The following is management’s discussion and analysis (“MD&A”) of the operating and financial results of Baytex Energy Corp. for the years ended December 31, 2019 and 2018. This information is provided as of March 3, 2020. In this MD&A, references to “Baytex”, the “Company”, “we”, “us” and “our” and similar terms refer to Baytex Energy Corp. and its subsidiaries on a consolidated basis, except where the context requires otherwise. The results for the three months and year ended December 31, 2019 (“Q4/2019” and “2019”) have been compared with the results for the three months and year ended December 31, 2018 (“Q4/2018” and “2018”). This MD&A should be read in conjunction with the Company’s audited consolidated financial statements (“consolidated financial statements”) for the years ended December 31, 2019 and 2018, together with the accompanying notes and the Annual Information Form for the year ended December 31, 2019. These documents and additional information about Baytex are accessible on the SEDAR website at www.sedar.com and through the U.S. Securities and Exchange Commission at www.sec.gov. All amounts are in Canadian dollars, unless otherwise stated, and all tabular amounts are in thousands of Canadian dollars, except for percentages and per common share amounts or as otherwise noted.

In this MD&A, barrel of oil equivalent (“boe”) amounts have been calculated using a conversion rate of six thousand cubic feet of natural gas to one barrel of oil, which represents an energy equivalency conversion method applicable at the burner tip and does not represent a value equivalency at the wellhead. While it is useful for comparative measures, it may not accurately reflect individual product values and may be misleading if used in isolation.

This MD&A contains forward-looking information and statements along with certain measures which do not have any standardized meaning prescribed by Canadian Generally Accepted Accounting Principles (“GAAP”). The terms “adjusted funds flow”, “operating netback”, “exploration and development expenditures”, “free cash flow”, “net debt”, and “bank EBITDA” do not have any standardized meaning as prescribed by GAAP and therefore may not be comparable to similar measures presented by other companies where similar terminology is used. We refer you to the advisory on forward-looking information and statements and a summary of our non-GAAP measures at the end of the MD&A.

BAYTEX ENERGY CORP.

Baytex Energy Corp. is a North American focused oil and gas company based in Calgary, Alberta. The company operates in Canada and the United States. The Canadian operating segment includes our light oil assets in the Viking and Duvernay, our heavy oil assets in Peace River and Lloydminster and our conventional oil and natural gas assets in Western Canada. The U.S. operating segment includes our Eagle Ford assets in Texas.

STRATEGIC COMBINATION

On August 22, 2018, Baytex and Raging River Exploration Inc. (“Raging River”) completed the strategic combination of the two companies (the “Strategic Combination”) by way of a plan of arrangement whereby Baytex acquired all of the issued and outstanding common shares of Raging River. The Strategic Combination increased our light oil exposure and operational control of our properties while improving our leverage ratios. Production from Raging River’s properties is approximately 90% light oil from the Viking and Duvernay. The addition of the primarily operated assets to our portfolio increased our inventory of drilling prospects and increased our ability to effectively allocate capital. Our comparative 2018 results include the results from Raging River from the closing date August 22, 2018.

2019 ANNUAL HIGHLIGHTS

Baytex delivered solid operating and financial results for 2019. Production of 97,680 boe/d for 2019 exceeded the top end of our 2019 annual guidance while exploration and development expenditures of $552.3 million were at the low end of guidance. Strong well performance along with the disciplined execution of our exploration and development program resulted in free cash flow of $328.8 million for 2019 which contributed to a $393.4 million decrease in net debt.

In Canada, production of 58,625 boe/d for 2019 was 15,243 boe/d higher than 43,382 boe/d in 2018 which reflects the impact of the Strategic Combination along with our exploration and development program. Exploration and development expenditures of $374.4 million were focused on our Viking light oil property along with additional heavy oil development at Peace River and Lloydminster. Exploration and development expenditures included costs associated with drilling 279 (247.8 net) light oil wells in the Viking and Duvernay along with 42 (42.0 net) heavy oil wells during 2019.

In the U.S., strong well performance from wells brought on stream during 2019 contributed to production of 39,055 boe/d which was 1,980 boe/d higher than 37,076 boe/d for 2018 despite relatively consistent completion activity in both periods. We invested $177.9 million on exploration and development activity during 2019 and drilled 96 (20.2 net) wells and commenced production from

7

109 (25.1 net) wells. During 2018 we drilled 91 (20.8 net) wells and commenced production from 120 (26.2 net) wells on our Eagle Ford properties.

In 2019, we benefited from narrower Canadian light and heavy oil differentials after production curtailments mandated by the Government of Alberta came into effect in January 2019. The Edmonton par light oil benchmark averaged $69.22/bbl in 2019 which represents a differential of US$4.86/bbl to the West Texas Intermediate (“WTI”) benchmark price as compared to a US$11.30/bbl differential in 2018 and a US$26.51/bbl differential in Q4/2018. The Western Canadian Select (“WCS”) heavy oil differential averaged US$12.75/bbl in 2019 relative to a differential of US$26.31/bbl in 2018 and a differential of US$39.42/bbl in Q4/2018. Stronger Canadian oil differentials helped to mitigate the impact of a lower WTI benchmark price which was US$57.03/bbl in 2019 compared to US$64.77/bbl during 2018.

We generated adjusted funds flow of $902.4 million in 2019 which was $429.4 million higher than $473.0 million for 2018. The increase is primarily due to a $277.4 million increase in operating netback driven by increased production from the Strategic Combination, strong well performance from our development program and tighter oil differentials on our Canadian production. Realized gains on financial derivatives of $75.6 million in 2019 also contributed to the increase in adjusted funds flow relative to 2018 when we recorded realized losses on financial derivatives of $73.2 million. The $429.4 million increase in adjusted funds flow contributed to the $312.9 million decrease in our net loss to $12.5 million for 2019 compared to a net loss of $325.3 million in 2018. In 2019, we recorded impairments of $187.8 million due to a sustained decline in Canadian heavy oil prices which resulted in a change in development plans for our thermal projects at Peace River compared to total impairments of $285.3 million in 2018 related to our Conventional and Eagle Ford assets.

Free cash flow of $328.8 million for 2019 reflects our strong operational and financial results along with the disciplined execution of our exploration and development program. Free cash flow generated in 2019 contributed to a $393.4 million decrease in net debt to $1,871.8 million at December 31, 2019, as compared to $2,265.2 million at December 31, 2018. Net debt also decreased due to a strengthening of the Canadian dollar at December 31, 2019 which reduced the reported amount of our U.S. dollar denominated net debt by $62.8 million relative to December 31, 2018.

2020 SENIOR NOTE FINANCING

On February 5, 2020, we issued US$500 million of senior unsecured notes bearing interest at 8.75% payable semi-annually which mature on April 1, 2027 (the “8.75% Senior Notes”). These notes are redeemable at our option, in whole or in part, at specified redemption prices after April 1, 2023 and will be redeemable at par from April 1, 2026 to maturity.

On February 20, 2020, we used a portion of the net proceeds from the issuance of the 8.75% Senior Notes to redeem our US$400 million principal amount of our 5.125% senior unsecured notes due June 1, 2021 at par plus accrued interest. We also issued a redemption notice for the $300 million principal amount of our 6.625% senior unsecured notes due July 19, 2022 for early redemption on March 6, 2020 at 101.104% of the principal amount plus accrued interest. After completing the early redemption of the 6.625% senior unsecured notes our next unsecured debt maturity is June 1, 2024 when the US$400 million principal amount of 5.625% notes are due.

8

GUIDANCE

The following table compares our 2019 annual guidance compared to our 2019 results.

| | Original guidance (1) | | 2019 | |

Exploration and development expenditures ($ millions) | | $550 - $650 | | $552.3 | |

Production (boe/d) | | 93,000 - 97,000 | | 97,680 | |

| | | | | |

Expenses: | | | | | |

Royalty rate (%) | | 20.0 | | 18.4 | |

Operating ($/boe) | | $10.75 - $11.25 | | $11.16 | |

Transportation ($/boe) | | $1.25 - $1.35 | | $1.23 | |

General and administrative ($ millions) | | ~ $46 ($1.30/boe) | | $45.5 ($1.28/boe) | |

Cash interest ($ millions) | | ~ $112 ($3.23/boe) | | $107.4 ($3.01/boe) | |

(1) As announced on December 17, 2018. Includes updated guidance on May 2, 2019 for general and administrative expenses to reflect a change associated with the adoption of IFRS 16.

On December 4, 2019 our Board of Directors approved our 2020 capital budget of $500 - $575 million which is designed to generate production of 93,000 - 97,000 boe/d. The program is expected to be equally weighted between the first and second half of 2020 and we will maintain operational flexibility to adjust spending in response to commodity prices.

The following table summarizes our 2020 guidance as released on December 4, 2019.

| | 2020 Guidance | |

Exploration and development expenditures ($ millions) | | $500 - $575 million | |

Production (boe/d) | | 93,000 - 97,000 | |

| | | |

Expenses: | | | |

Royalty rate (%) | | 18.0 - 18.5 | |

Operating ($/boe) | | $11.25 - $12.00 | |

Transportation ($/boe) | | $1.20 - $1.30 | |

General and administrative ($ millions) | | $45 ($1.30/boe) | |

Cash interest ($ millions) | | $112 ($3.23/boe) | |

| | | |

Leasing expenditures ($ millions) | | $7 | |

Asset retirement obligations ($ millions) | | $19 | |

9

RESULTS OF OPERATIONS

The Canadian operating segment includes our light oil assets in Viking and Duvernay, our heavy oil assets in Peace River and Lloydminster and our conventional oil and natural gas assets in Western Canada. The U.S. operating segment includes our Eagle Ford assets in Texas.

Production

| | Years Ended December 31 | |

| | 2019 | | 2018 | |

Daily Production | | Canada | | U.S. | | Total | | Canada | | U.S. | | Total | |

Liquids (bbl/d) | | | | | | | | | | | | | |

Light oil and condensate | | 22,358 | | 21,229 | | 43,587 | | 8,959 | | 20,305 | | 29,264 | |

Heavy oil | | 26,741 | | — | | 26,741 | | 25,954 | | — | | 25,954 | |

Natural Gas Liquids (“NGL”) | | 1,364 | | 8,865 | | 10,229 | | 1,199 | | 8,546 | | 9,745 | |

Total liquids (bbl/d) | | 50,463 | | 30,094 | | 80,557 | | 36,112 | | 28,851 | | 64,963 | |

Natural gas (mcf/d) | | 48,969 | | 53,773 | | 102,742 | | 43,622 | | 49,349 | | 92,971 | |

Total production (boe/d) | | 58,625 | | 39,055 | | 97,680 | | 43,382 | | 37,076 | | 80,458 | |

| | | | | | | | | | | | | |

Production Mix | | | | | | | | | | | | | |

Light oil and condensate | | 38 | % | 54 | % | 45 | % | 21 | % | 55 | % | 37 | % |

Heavy oil | | 46 | % | — | % | 27 | % | 60 | % | — | % | 32 | % |

NGL | | 2 | % | 23 | % | 10 | % | 3 | % | 23 | % | 12 | % |

Natural gas | | 14 | % | 23 | % | 18 | % | 16 | % | 22 | % | 19 | % |

Strong operational performance in 2019 resulted in production of 97,680 boe/d which exceeded the high end of our annual production guidance of 93,000 to 97,000 boe/d. Production for 2019 was 17,222 boe/d higher than 80,458 boe/d in 2018 due to the Strategic Combination along with production related to our exploration and development program.

In Canada, production of 58,625 boe/d in 2019 was up 35% from 43,382 boe/d in 2018. The increase in production in 2019 relative to 2018 is primarily due to the Strategic Combination along with strong well performance from our exploration and development program. Production from our Viking and Duvernay properties consists of approximately 90% light oil which resulted in a higher proportion of our Canadian production being comprised of light oil in 2019 compared to 2018.

U.S. production averaged 39,055 boe/d in 2019 which is up 5% from 37,076 boe/d for 2018. We experienced strong production results from wells brought on stream in 2019 which resulted a 1,980 boe/d increase in production compared to 2018 despite consistent completion activity in both periods. During 2019 we commenced production from 109 (25.1 net) wells compared to 120 (26.2 net) wells during 2018.

Commodity Prices

The prices received for our crude oil and natural gas production directly impact our earnings, adjusted funds flow and our financial position.

Crude Oil

Global benchmark prices for crude oil were lower in 2019 as forecasted demand levels were impacted by the ongoing trade dispute between the U.S. and China which more than offset the effect of compliance with OPEC production curtailments along with U.S. imposed sanctions on Iran and Venezuela. North American benchmark prices for 2019 were lower than 2018 as a result of increasing supply from U.S. production along with uncertainty around future global demand for crude oil. Canadian oil differentials were tighter in 2019 compared to 2018 due to the Government of Alberta’s production curtailments which came into effect in January of 2019. While our 2019 production levels were not significantly impacted by the Government of Alberta’s curtailment program we benefited from narrower differentials for our Canadian light and heavy oil production in 2019.

We compare the price received for our U.S. crude oil production to the Louisiana Light Sweet (“LLS”) stream at St. James, Louisiana, which is a representative benchmark for light oil pricing at the U.S. Gulf Coast. During 2019, the LLS benchmark averaged US$62.84/bbl representing a premium of US$5.81/bbl relative to WTI, compared to an LLS price of US$70.09/bbl or a premium of US$5.32/bbl to WTI for 2018.

10

We compare the price received for our light oil production in Canada to the Edmonton par benchmark oil price which is the representative benchmark for light grades of crude oil in Western Canada. The Edmonton par price averaged $69.22/bbl for 2019 which is consistent with $69.31/bbl for 2018 despite the decline in WTI pricing over the same periods as differentials were tighter in 2019. Edmonton par traded at a US$4.86/bbl discount to WTI in 2019 compared to a US$11.30/bbl discount for 2018.

The price received for our heavy oil production in Canada is based on the WCS benchmark price which is the representative benchmark for heavy grades of crude oil in Western Canada. With curtailments, we benefited from a narrower WCS heavy oil differential in 2019 which averaged US$12.75/bbl in 2019 as compared to US$26.31/bbl for 2018. As a result, the WCS heavy oil benchmark price of $58.75/bbl increased $8.90/bbl from $49.85/bbl in 2018 despite a $8.28/bbl decrease in WTI (expressed in Canadian dollars) over the same periods.

Natural Gas

U.S. natural gas prices for 2019 were lower than 2018 as U.S. natural gas production has outpaced growth in natural gas demand. Canadian natural gas prices remained challenged during 2019 as a lack of egress from Western Canada continues to impact natural gas prices in the region.

Our U.S. natural gas production is priced in reference to the New York Mercantile Exchange (“NYMEX”) natural gas index. The NYMEX natural gas benchmark averaged US$2.63/mmbtu in 2019 which is lower than US$3.09/mmbtu in 2018. Record natural gas production levels in the U.S. have resulted in an oversupplied North American market and lower natural gas prices in 2019 relative to 2018.

In Canada, we receive natural gas pricing based on the AECO benchmark which continues to trade at a discount to NYMEX as a result of increasing supply and limited market access for Canadian natural gas production. The AECO benchmark averaged $1.62/ mcf during 2019 which is $0.08/mcf higher than the benchmark average of $1.54/mcf during 2018.

| | Years Ended December 31 | |

| | 2019 | | 2018 | | Change | |

Benchmark Averages | | | | | | | |

WTI oil (US$/bbl)(1) | | 57.03 | | 64.77 | | (7.74 | ) |

LLS oil (US$/bbl)(2) | | 62.84 | | 70.09 | | (7.25 | ) |

LLS oil differential to WTI (US$/bbl) | | 5.81 | | 5.32 | | 0.49 | |

Edmonton par oil ($/bbl) | | 69.22 | | 69.31 | | (0.09 | ) |

Edmonton par oil differential to WTI (US$/bbl) | | (4.86 | ) | (11.30 | ) | 6.44 | |

WCS heavy oil ($/bbl)(3) | | 58.75 | | 49.85 | | 8.90 | |

WCS heavy oil differential to WTI (US$/bbl) | | (12.75 | ) | (26.31 | ) | 13.56 | |

AECO natural gas price ($/mcf)(4) | | 1.62 | | 1.54 | | 0.08 | |

NYMEX natural gas price (US$/mmbtu)(5) | | 2.63 | | 3.09 | | (0.46 | ) |

CAD/USD average exchange rate | | 1.3269 | | 1.2962 | | 0.0307 | |

(1) WTI refers to the arithmetic average of NYMEX prompt month WTI for the applicable period.

(2) LLS refers to the Argus trade month average for Louisiana Light Sweet oil.

(3) WCS refers to the average posting price for the benchmark WCS heavy oil.

(4) AECO refers to the AECO arithmetic average month-ahead index price published by the Canadian Gas Price Reporter (“CGPR”).

(5) NYMEX refers to the NYMEX last day average index price as published by the CGPR.

11

| | Years Ended December 31 | |

| | 2019 | | 2018 | |

| | Canada | | U.S. | | Total | | Canada | | U.S. | | Total | |

Average Realized Sales Prices(1) | | | | | | | | | | | | | |

Light oil and condensate ($/bbl) | | $ | 65.99 | | $ | 77.46 | | $ | 71.57 | | $ | 51.78 | | $ | 85.96 | | $ | 75.50 | |

Heavy oil ($/bbl)(2) | | 44.20 | | — | | 44.20 | | 36.20 | | — | | 36.20 | |

NGL ($/bbl) | | 16.93 | | 18.74 | | 18.50 | | 33.21 | | 31.10 | | 31.36 | |

Natural gas ($/mcf) | | 1.71 | | 3.43 | | 2.61 | | 1.48 | | 4.20 | | 2.92 | |

Weighted average ($/boe)(2) | | $ | 47.15 | | $ | 51.08 | | $ | 48.72 | | $ | 34.76 | | $ | 59.83 | | $ | 46.31 | |

(1) Baytex’s risk management strategy employs both oil and natural gas financial and physical forward contracts (fixed price forward sales and collars) and heavy oil differential physical delivery contracts (fixed price and percentage of WTI). The pricing information in this table excludes the impact of financial derivatives.

(2) Realized heavy oil prices are calculated based on sales volumes and sales dollars, net of blending and other expense.

Average Realized Sales Prices

Our weighted average sales price was $48.72/boe for 2019 which is up $2.41/boe from $46.31/boe for 2018. Our realized price in the U.S. was $51.08/boe in 2019 which is $8.75/boe lower than $59.83/boe in 2018 due to the decrease in U.S. crude oil benchmark prices. In Canada, our realized price of $47.15/boe for 2019 was $12.39/boe higher than $34.76/boe for 2018. Canadian realized prices increased as narrower differentials improved heavy and light oil prices which more than offset the impact of a lower WTI price and we had a higher proportion of light oil from the Strategic Combination.

We compare our light oil realized price in Canada to the Edmonton par benchmark price. Our realized light oil and condensate price in 2019 was $65.99/bbl representing a discount of $3.23/bbl to the Edmonton par benchmark compared to 2018 when our realized price was $51.78/bbl or a discount of $17.53/bbl. The majority of our 2018 light oil production occurred after closing of the Strategic Combination and was impacted by a sharp widening of Canadian oil differentials in Q4/2018 which resulted in a wider discount to the Edmonton par benchmark reported for the annual period. The discount of $3.23/bbl for 2019 is relatively consistent with our realized Q4/2018 discount of $2.14/bbl to Edmonton par.

We compare the price received for our U.S. light oil and condensate production to the LLS benchmark. Our realized light oil and condensate price averaged $77.46/bbl for 2019 compared to $85.96/bbl for 2018. Expressed in U.S. dollars, our realized light oil and condensate price of US$58.38/bbl for 2019 reflects a US$4.46/bbl discount to the LLS benchmark for 2019 compared to a discount of US$3.77/bbl in 2018. In 2019, our price realizations relative to LLS was impacted by a change in certain marketing contracts to be priced on the Magellan East Houston (“MEH”) benchmark which represents light oil pricing at the Magellan East crude oil terminal in Houston, Texas. In 2020, we expect to compare our realized light oil price to the MEH benchmark as the majority of our light oil and condensate contracts are now referenced to the MEH benchmark price.

Our realized heavy oil price, net of blending and other expense averaged $44.20/bbl in 2019 compared to $36.20/bbl in 2018. The $8.00/bbl increase in our realized heavy oil price for 2019 is fairly consistent with the $8.90/bbl increase in the WCS benchmark from 2018. Our realized heavy oil price did not increase as much as the WCS benchmark due to certain WTI based heavy oil rail contracts that were entered into prior to the Government of Alberta’s decision to curtail production which resulted in a narrowing of the WCS differential.

Our realized NGL price as a percentage of WTI can vary from period to period based on the product mix of our NGL volumes and changes in the market prices of the underlying products. Our realized NGL price was $18.50/bbl in 2019 or 24% of WTI (expressed in Canadian dollars) compared to $31.36/bbl or 37% of WTI (expressed in Canadian dollars) in 2018. The decrease in our NGL price for 2019 is consistent with the increase in the production and supply of NGLs in North America which resulted in lower market prices for propane and butane relative to 2018.

We compare our realized natural gas price in Canada to the AECO benchmark price. Our realized natural gas price for 2019 was $1.71/mcf compared to $1.48/mcf in 2018. The $0.23/mcf increase in our realized natural gas price in 2019 is higher than the $0.08/mcf increase in the AECO natural gas price over the same period as the natural gas in our Viking asset acquired in the Strategic Combination received higher natural gas pricing relative to our legacy Baytex properties in Canada. In the U.S., our realized natural gas price was US$2.58/mmbtu for 2019 compared to US$3.24/mmbtu in 2018. Our realized natural gas price in the U.S. is relatively consistent with the NYMEX benchmark in 2019 and 2018.

12

Petroleum and Natural Gas Sales

| | Years Ended December 31 | |

| | 2019 | | 2018 | |

($ thousands) | | Canada | | U.S. | | Total | | Canada | | U.S. | | Total | |

Oil sales | | | | | | | | | | | | | |

Light oil and condensate | | $ | 538,487 | | $ | 600,163 | | $ | 1,138,650 | | $ | 169,335 | | $ | 637,055 | | $ | 806,390 | |

Heavy oil | | 500,187 | | — | | 500,187 | | 411,794 | | — | | 411,794 | |

NGL | | 8,430 | | 60,647 | | 69,077 | | 14,531 | | 97,008 | | 111,539 | |

Total liquids sales | | 1,047,104 | | 660,810 | | 1,707,914 | | 595,660 | | 734,063 | | 1,329,723 | |

Natural gas sales | | 30,620 | | 67,385 | | 98,005 | | 23,555 | | 75,592 | | 99,147 | |

Total petroleum and natural gas sales | | 1,077,724 | | 728,195 | | 1,805,919 | | 619,215 | | 809,655 | | 1,428,870 | |

Blending and other expense | | (68,795 | ) | — | | (68,795 | ) | (68,832 | ) | — | | (68,832 | ) |

Total sales, net of blending and other expense | | $ | 1,008,929 | | $ | 728,195 | | $ | 1,737,124 | | $ | 550,383 | | $ | 809,655 | | $ | 1,360,038 | |

Total sales, net of blending and other expense, of $1,737.1 million for 2019 increased $377.1 million from $1,360.0 million reported for 2018. Total sales, net of blending and other expense, was higher in 2019 due to production from the Strategic Combination along with strong operational results from our exploration and development program and from a $2.41/boe increase in our weighted average realized price compared to 2018.

In Canada, total sales, net of blending and other expense, was $1,008.9 million for 2019 which is an increase of $458.5 million from $550.4 million reported for 2018. Total petroleum and natural gas sales increased with production from the Strategic Combination and our exploration and development program. The 15,243 boe/d increase in production for 2019 resulted in a $193.4 million increase in total sales, net of blending and other expense, relative to 2018. Our average realized price for 2019 was $12.39/boe higher than 2018 as a result of stronger heavy and light oil and condensate price realizations from narrower oil differentials. The increase in our realized price in 2019 resulted in a $265.1 million increase in total sales, net of blending and other expense, relative to 2018.

In the U.S., petroleum and natural gas sales were $728.2 million for 2019 which is a decrease of $81.5 million from $809.7 million reported for 2018. Our realized price for 2019 was $8.75/boe lower due to the decline in U.S. benchmark prices and resulted in a $124.7 million decrease in total petroleum and natural gas sales relative to 2018. The decrease in total sales due to lower realized pricing was partially offset by a 1,979 boe/d increase in production in 2019 which resulted in a $43.2 million increase in total sales compared to 2018.

Royalties

Royalties are paid to various government entities and to land and mineral rights owners. Royalties are calculated based on gross revenues or on operating netbacks less capital investment for specific heavy oil projects, and are generally expressed as a percentage of total sales, net of blending and other expense. The actual royalty rates can vary for a number of reasons, including the commodity produced, royalty contract terms, commodity price level, royalty incentives and the area or jurisdiction.

| | Years Ended December 31 | |

| | 2019 | | 2018 | |

($ thousands except for % and per boe) | | Canada | | U.S. | | Total | | Canada | | U.S. | | Total | |

Royalties | | $ | 107,467 | | $ | 212,774 | | $ | 320,241 | | $ | 72,700 | | $ | 241,054 | | $ | 313,754 | |

Average royalty rate(1) | | 10.7 | % | 29.2 | % | 18.4 | % | 13.2 | % | 29.8 | % | 23.1 | % |

Royalty rate per boe | | $ | 5.02 | | $ | 14.93 | | $ | 8.98 | | $ | 4.59 | | $ | 17.81 | | $ | 10.68 | |

(1) Average royalty rate is calculated as royalties divided by total sales, net of blending and other expense.

Total royalties for 2019 were $320.2 million or 18.4% of total sales, net of blending and other expense, compared to $313.8 million or 23.1% in 2018. Our average royalty rate of 18.4% for 2019 is below our annual guidance of approximately 20.0% and decreased from 2018 mainly due to the Strategic Combination.

In Canada, total royalties were $107.5 million or 10.7% of sales, net of blending and other expense, for 2019 compared to $72.7 million or 13.2% of sales, net of blending and other expense, in 2018. Our overall royalty rate in Canada decreased following the Strategic Combination due to the lower royalty rate on our Viking and Duvernay properties as compared to our heavy oil properties. Total royalties of $107.5 million in 2019 were higher than $72.7 million in 2018 due to the increase in total sales, net of blending and other expense.

13

Total royalties in the U.S. were $212.8 million or 29.2% of sales for 2019 compared to $241.1 million or 29.8% of sales reported for 2018. The royalty rate on our U.S. production does not vary with price but can vary across our acreage. Royalties for 2019 averaged 29.2% of petroleum and natural gas sales which is consistent with 29.8% for 2018. The decrease in total royalties in 2019 compared to 2018 is consistent with the decrease in total petroleum and natural gas sales over the same period.

Operating Expense

| | Years Ended December 31 | |

| | 2019 | | 2018 | |

($ thousands except for per boe) | | Canada | | U.S. | | Total | | Canada | | U.S. | | Total | |

Operating expense | | $ | 298,303 | | $ | 99,413 | | $ | 397,716 | | $ | 221,717 | | $ | 89,875 | | $ | 311,592 | |

Operating expense per boe | | $ | 13.94 | | $ | 6.97 | | $ | 11.16 | | $ | 14.00 | | $ | 6.64 | | $ | 10.61 | |

Operating expense was $397.7 million ($11.16/boe) in 2019 compared to $311.6 million ($10.61/boe) for 2018. The increase in total operating expense can be attributed to higher production in 2019 along with an increase in the proportion of our annual production from Canada relative to 2018. Operating expense of $11.16/boe for 2019 is consistent with expectations and is within our 2019 annual guidance range of $10.75 - $11.25/boe.

In Canada, operating expense was $298.3 million ($13.94/boe) for 2019 compared to $221.7 million ($14.00/boe) for 2018. The increase in total operating expense in Canada is a result of the additional production from the Strategic Combination as our per unit operating expense of $13.94/boe is consistent with $14.00/boe in 2018. U.S. operating expense was $99.4 million ($6.97/boe) for 2019 compared to $89.9 million ($6.64/boe) for 2018. The increase in total operating expense reflects higher U.S. production combined with a weaker Canadian dollar during 2019 compared to 2018. Expressed in U.S. dollars, per boe operating expense of US$5.25/boe in 2019 is consistent with US$5.12/boe in 2018.

Transportation Expense

Transportation expense includes the costs to move production from the field to the sales point. The largest component of transportation expense relates to the trucking of oil in Canada to pipeline and rail terminals which can vary from period to period depending on hauling distances as we seek to optimize sales prices and trucking rates.

| | Years Ended December 31 | |

| | 2019 | | 2018 | |

($ thousands except for per boe) | | Canada | | U.S. | | Total | | Canada | | U.S. | | Total | |

Transportation expense | | $ | 43,942 | | $ | — | | $ | 43,942 | | $ | 36,869 | | $ | — | | $ | 36,869 | |

Transportation expense per boe | | $ | 2.05 | | $ | — | | $ | 1.23 | | $ | 2.33 | | $ | — | | $ | 1.26 | |

We reported transportation expense of $1.23/boe for 2019 which is slightly below our annual guidance range of $1.25 - $1.35/boe for 2019. Transportation expense was $43.9 million ($1.23/boe) for 2019 was higher than $36.9 million ($1.26/boe) for 2018 and reflects additional oil trucking and transportation costs associated with our Viking and Duvernay light oil properties acquired as part of the Strategic Combination.

Blending and Other Expense

Blending and other expense primarily includes the cost of blending diluent purchased in order to reduce the viscosity of our heavy oil transported through pipelines to meet pipeline specifications. The purchased diluent is recorded as blending and other expense. The price received for the blended product is recorded as heavy oil sales revenue. We net blending and other expense against heavy oil sales to compare the realized price on our produced volumes to benchmark pricing. Accordingly, our heavy oil sales price realization can fluctuate depending on the quantity and price of blending diluent required to meet pipeline specifications.

Blending and other expense was $68.8 million for 2019 and 2018 as total blending volumes and prices were relatively consistent in both periods.

14

Financial Derivatives

As part of our normal operations, we are exposed to movements in commodity prices, foreign exchange rates and interest rates. In an effort to manage these exposures, we utilize various financial derivative contracts which are intended to partially reduce the volatility in our adjusted funds flow. Contracts settled in the period result in realized gains or losses based on the market price compared to the contract price and the notional volume outstanding. Changes in the fair value of unsettled contracts are reported as unrealized gains or losses in the period as the forward markets for commodities and currencies fluctuate and as new contracts are executed.

| | Years Ended December 31 | |

($ thousands) | | 2019 | | 2018 | | Change | |

Realized financial derivatives gain (loss) | | | | | | | |

Crude oil | | $ | 72,052 | | $ | (74,902 | ) | $ | 146,954 | |

Natural gas | | 3,577 | | 1,765 | | 1,812 | |

Interest and financing | | (9 | ) | (28 | ) | 19 | |

Total | | 75,620 | | (73,165 | ) | 148,785 | |

Unrealized financial derivatives gain (loss) | | | | | | | |

Crude oil | | (80,602 | ) | 117,087 | | (197,689 | ) |

Natural gas | | (1,857 | ) | (697 | ) | (1,160 | ) |

Interest and financing | | (358 | ) | 325 | | (683 | ) |

Total | | (82,817 | ) | 116,715 | | (199,532 | ) |

Total financial derivatives gain (loss) | | | | | | | |

Crude oil | | (8,550 | ) | 42,185 | | (50,735 | ) |

Natural gas | | 1,720 | | 1,068 | | 652 | |

Interest and financing | | (367 | ) | 297 | | (664 | ) |

Total | | $ | (7,197 | ) | $ | 43,550 | | $ | (50,747 | ) |

We recorded a total financial derivatives loss of $7.2 million for 2019. Realized financial derivatives gains of $75.6 million for 2019 were primarily a result of the market prices for crude oil settling at levels below those set in our derivative contracts. The unrealized loss on financial derivatives of $82.8 million for 2019 reflects the realization of our net financial derivatives asset recorded at December 31, 2018 along with changes in the fair value of our contracts entered for 2020.

Realized gains on crude oil financial derivatives of $72.1 million in 2019 are a result of market prices for Brent and WTI settling at levels below the prices set in our contracts outstanding during the period. Our natural gas financial derivatives generated gains of $3.6 million and were a result of the NYMEX index averaging less that the fixed price on our NYMEX contracts in place for 2019.

Unrealized losses of $82.8 million recorded for 2019 reflects the decrease in the fair value of our net unrealized financial derivatives position from December 31, 2018. At December 31, 2018, our net asset of $79.6 million was primarily associated with contracts for 2019 which generated realized gains of $75.6 million during 2019. The unrealized loss for 2019 also reflects changes in value for our 2020 financial derivative contracts which resulted in a net liability of $3.2 million at December 31, 2019.

15

We had the following commodity financial derivative contracts as at March 3, 2020.

| | Remaining Period | | Volume | | Price/Unit (1) | | Index |

Oil | | | | | | | | |

Basis swap | | Jan 2020 to Dec 2020 | | 2,500 bbl/d | | WTI less US$16.10/bbl | | WCS |

Basis swap (6) | | Apr 2020 to Dec 2020 | | 4,000 bbl/d | | WTI less US$16.38/bbl | | WCS |

Basis swap | | Jan 2020 to Dec 2020 | | 2,000 bbl/d | | WTI less US$6.50/bbl | | MSW |

Basis swap (6) | | Apr 2020 to Dec 2020 | | 3,000 bbl/d | | WTI less US$5.92/bbl | | MSW |

Fixed - Sell | | Jan 2020 to Mar 2020 | | 6,000 bbl/d | | US$56.60/bbl | | WTI |

Fixed - Sell | | Jan 2020 to Dec 2020 | | 2,000 bbl/d | | US$58.00/bbl | | WTI |

3-way option (2) | | Jan 2020 to Dec 2020 | | 3,000 bbl/d | | US$50.00/US$56.00/US$61.35 | | WTI |

3-way option (2) | | Jan 2020 to Dec 2020 | | 3,000 bbl/d | | US$50.00/US$57.00/US$60.00 | | WTI |

3-way option (2) | | Jan 2020 to Dec 2020 | | 4,500 bbl/d | | US$50.00/US$57.00/US$62.00 | | WTI |

3-way option (2) | | Jan 2020 to Dec 2020 | | 3,000 bbl/d | | US$50.00/US$58.00/US$62.00 | | WTI |

3-way option (2) | | Jan 2020 to Dec 2020 | | 1,000 bbl/d | | US$51.00/US$58.00/US$60.50 | | WTI |

3-way option (2) | | Jan 2020 to Dec 2020 | | 1,000 bbl/d | | US$51.00/US$58.00/US$60.83 | | WTI |

3-way option (2) | | Jan 2020 to Dec 2020 | | 1,500 bbl/d | | US$51.00/US$59.00/US$65.60 | | WTI |

3-way option (2) | | Jan 2020 to Dec 2020 | | 1,500 bbl/d | | US$51.00/US$59.00/US$66.00 | | WTI |

3-way option (2) | | Jan 2020 to Dec 2020 | | 1,000 bbl/d | | US$51.00/US$59.50/US$66.15 | | WTI |

3-way option (2) | | Jan 2020 to Dec 2020 | | 1,000 bbl/d | | US$51.00/US$60.00/US$65.60 | | WTI |

3-way option (2) | | Jan 2020 to Dec 2020 | | 1,000 bbl/d | | US$51.00/US$60.00/US$66.00 | | WTI |

3-way option (2) | | Jan 2020 to Dec 2020 | | 1,000 bbl/d | | US$51.00/US$60.00/US$66.05 | | WTI |

3-way option (2) | | Jan 2020 to Dec 2020 | | 2,000 bbl/d | | US$51.00/US$60.00/US$66.70 | | WTI |

Swaption (3) | | Jan 2021 to Dec 2021 | | 3,000 bbl/d | | US$64.50/bbl | | Brent |

Swaption (4) | | Jan 2021 to Dec 2021 | | 3,000 bbl/d | | US$70.00/bbl | | Brent |

Swaption (4) | | Jan 2021 to Dec 2021 | | 3,000 bbl/d | | US$60.75/bbl | | WTI |

| | | | | | | | |

Natural Gas | | | | | | | | |

3-way option (2) | | Jan 2020 to Dec 2020 | | 5,000 mmbtu/d | | US$2.25/US$2.60/US$2.85 | | NYMEX |

Swaption (5) | | Jan 2021 to Dec 2021 | | 5,000 mmbtu/d | | US$2.90/mmbtu | | NYMEX |

(1) Based on the weighted average price per unit for the period.

(2) Producer 3-way option consists of a sold call, a bought put and a sold put. To illustrate, in a US$50.00/US$58.00/US$62.00 contract, Baytex receives WTI plus US$8.00/bbl when WTI is at or below US$50.00/bbl; Baytex receives US$58.00/bbl when WTI is between US$50.00/bbl and US$58.00/bbl; Baytex receives the market price when WTI is between US$58.00/bbl and US$62.00/bbl; and Baytex receives US$62.00/bbl when WTI is above US$62.00/bbl.

(3) For these contracts, the counterparty has the right, if exercised on September 30, 2020, to enter a swap transaction for the remaining term, notional volume and fixed price per unit indicated above.

(4) For these contracts, the counterparty has the right, if exercised on December 31, 2020, to enter a swap transaction for the remaining term, notional volume and fixed price per unit indicated above.

(5) For these contracts, the counterparty has the right, if exercised on December 23, 2020, to enter a swap transaction for the remaining term, notional volume and fixed price per unit indicated above.

(6) Contracts entered subsequent to December 31, 2019.

Operating Netback

| | Years Ended December 31 | |

| | 2019 | | 2018 | |

($ per boe except for volume) | | Canada | | U.S. | | Total | | Canada | | U.S. | | Total | |

Total production (boe/d) | | 58,625 | | 39,055 | | 97,680 | | 43,382 | | 37,076 | | 80,458 | |

Operating netback: | | | | | | | | | | | | | |

Total sales, net of blending and other expense | | $ | 47.15 | | $ | 51.08 | | $ | 48.72 | | $ | 34.76 | | $ | 59.83 | | $ | 46.31 | |

Royalties | | (5.02 | ) | (14.93 | ) | (8.98 | ) | (4.59 | ) | (17.81 | ) | (10.68 | ) |

Operating expense | | (13.94 | ) | (6.97 | ) | (11.16 | ) | (14.00 | ) | (6.64 | ) | (10.61 | ) |

Transportation expense | | (2.05 | ) | — | | (1.23 | ) | (2.33 | ) | — | | (1.26 | ) |

Operating netback | | $ | 26.14 | | $ | 29.18 | | $ | 27.35 | | $ | 13.84 | | $ | 35.38 | | $ | 23.76 | |

Realized financial derivatives gain (loss) | | — | | — | | 2.12 | | — | | — | | (2.49 | ) |

Operating netback after financial derivatives | | $ | 26.14 | | $ | 29.18 | | $ | 29.47 | | $ | 13.84 | | $ | 35.38 | | $ | 21.27 | |

16

Operating netback after financial derivatives of $29.47/boe increased $8.20/boe from $21.27/boe for 2018. Operating netback of $27.35/boe for 2019 was $3.59/boe higher than $23.76/boe for 2018 due to stronger realized pricing as a result of narrower light and heavy oil differentials relative to 2018. We recorded realized gains on financial derivatives of $2.12/boe in 2019 which resulted in a $4.61/boe increase in operating netback after financial derivatives compared to 2018 when we recorded losses of $2.49/boe.

In Canada, our operating netback was $26.14/boe in 2019 compared to $13.84/boe in 2018. The increase in our operating netback in Canada was driven by stronger realized pricing due the increase in light oil production following the Strategic Combination along with narrower Canadian oil differentials in 2019 relative to 2018. Our operating netback in the U.S. of $29.18/boe in 2019 was lower than $35.38/boe in 2018 due to the impact of lower U.S. benchmark prices on our realized sales price.

General and Administrative Expense

General and administrative (“G&A”) expense includes head office and corporate costs such as salaries and employee benefits, public company costs and administrative recoveries earned for operating capital and production activities on behalf of our working interest partners. G&A expense fluctuates with head office staffing levels and the level of operated capital and production activity during the period.

| | Years Ended December 31 | |

($ thousands except for per boe) | | 2019 | | 2018 | | Change | |

Gross general and administrative expense | | $ | 51,660 | | $ | 56,318 | | $ | (4,658 | ) |

Overhead recoveries | | (6,191 | ) | (10,493 | ) | 4,302 | |

General and administrative expense | | $ | 45,469 | | $ | 45,825 | | $ | (356 | ) |

General and administrative expense per boe | | $ | 1.28 | | $ | 1.56 | | $ | (0.28 | ) |

We reported G&A expense of $45.5 million ($1.28/boe) compared to $45.8 million ($1.56/boe) for 2018. G&A expense for 2019 was in line with expectations and our annual guidance of approximately $46 million ($1.30/boe).

G&A expense of $45.5 million ($1.28/boe) for 2019 is slightly lower than $45.8 million ($1.56/boe) for 2018 which only includes the additional staff and costs associated with the Strategic Combination following closing on August 22, 2018. In 2019 we continued to optimize our business following integration of the two companies which resulted in a decrease in G&A expense per boe in 2019 relative to 2018 and reflects the efficiencies we were able to realize by combining the two organizations. A $4.1 million decrease in rent expense in 2019 relative to 2018 was primarily due to the change in the accounting for leases which resulted in a change to the presentation of payments for office leases.

Financing and Interest Expense

Financing and interest expense includes interest on our bank loan, long-term notes and lease obligations as well as non-cash financing costs and the accretion on our asset retirement obligations. Financing and interest expense varies depending on debt levels outstanding during the period and the applicable borrowing rates, CAD/USD foreign exchange rates, along with the carrying amount of asset retirement obligations and the discount rates used to present value these obligations.

| | Years Ended December 31 | |

($ thousands except for per boe) | | 2019 | | 2018 | | Change | |

Interest on bank loan | | $ | 20,376 | | $ | 15,637 | | $ | 4,739 | |

Interest on long-term notes | | 86,431 | | 88,681 | | (2,250 | ) |

Interest on lease obligations | | 610 | | — | | 610 | |

Cash financing and interest expense | | 107,417 | | 104,318 | | 3,099 | |

Accretion of debt issue costs | | 4,735 | | 3,854 | | 881 | |

Accretion of asset retirement obligation | | 13,713 | | 10,914 | | 2,799 | |

Financing and interest expense | | $ | 125,865 | | $ | 119,086 | | $ | 6,779 | |

Cash interest per boe | | $ | 3.01 | | $ | 3.55 | | $ | (0.54 | ) |

Financing and interest expense per boe | | $ | 3.53 | | $ | 4.06 | | $ | (0.53 | ) |

17

We reported financing and interest expense of $125.9 million ($3.53/boe) for 2019 compared to $119.1 million ($4.06/boe) for 2018. Cash interest expense of $107.4 million ($3.01/boe) for 2019 was below our 2019 annual guidance of approximately $112 million ($3.23/boe). We allocated our free cash flow to debt reduction and redeemed the US$150 million principal amount of 6.75% senior unsecured notes in September of 2019 and reduced borrowings on our credit facilities throughout 2019 which resulted in lower cash interest expense relative to our annual guidance.

Financing and interest expense was $125.9 million for 2019 which is $6.8 million higher than $119.1 million reported for 2018. Interest on our bank loan of $20.4 million in 2019 increased $4.7 million relative to $15.6 million in 2018 due to the increase in loan balances following the assumption of net debt associated with the Strategic Combination. The weighted average interest rate on the credit facilities for 2019 was 4.0% as compared to 4.3% for 2018. We redeemed the US$150 million principal amount of 6.75% senior unsecured notes on September 13, 2019 which resulted in lower interest on our long-term notes in 2019 compared to 2018. Total accretion was higher in 2019 as our asset retirement obligation increased with the Strategic Combination.

Exploration and Evaluation Expense

Exploration and evaluation (“E&E”) expense is related to the expiry of leases and the derecognition of costs for exploration programs that have not demonstrated commercial viability and technical feasibility. E&E expense will vary depending on the timing of lease expiries, the accumulated costs of expiring leases, and the economic facts and circumstances related to the Company’s exploration programs. E&E expense was $11.8 million for 2019 compared to $21.7 million for 2018.

Depletion and Depreciation

Depletion and depreciation expense varies with the carrying amount of the Company’s oil and gas properties, the amount of proved plus probable reserves volumes and the rate of production for the period.

| | Years Ended December 31 | |

($ thousands except for per boe) | | 2019 | | 2018 | | Change | |

Depletion | | $ | 725,267 | | $ | 556,634 | | $ | 168,633 | |

Depreciation | | 6,419 | | 2,050 | | 4,369 | |

Depletion and depreciation | | $ | 731,686 | | $ | 558,684 | | $ | 173,002 | |

Depletion and depreciation per boe | | $ | 20.52 | | $ | 19.02 | | $ | 1.50 | |

Depletion and depreciation expense was $731.7 million ($20.52/boe) for 2019 compared to $558.7 million ($19.02/boe) reported for 2018. Total depletion and depreciation expense was higher in 2019 due to the Strategic Combination which resulted in a higher depletable base and production relative to 2018 which only includes the additional depletion expense after closing on August, 22, 2018. The depletion rate increased following the Strategic Combination in 2018 due to the addition of proved plus probable reserves at a higher cost than our historical depletion rate.

Impairment

In 2019, we recorded impairment expense of $187.8 million on our Peace River CGU which reflects a sustained decline in heavy oil prices in Canada which resulted in a change in the development plans for our thermal projects at Peace River. We did not identify any indicators of impairment or impairment reversals on our remaining CGUs.

In 2018, we recorded total impairments of $285.3 million on our Conventional CGU and our Eagle Ford CGU. We recorded a $65.0 million impairment on our Conventional assets in Canada due to a sustained decline in natural gas prices and a reduction in planned exploration and development expenditures on these assets. We also recorded a $220.3 million impairment in our Eagle Ford CGU in 2018 as the rate of future development outlined by the operator was reduced and resulted in a decline in the net present value of our proved plus probable reserves with no significant changes to proved plus probable reserves volumes. We did not identify any indicators of impairment or impairment reversals on our remaining CGUs.

Share-Based Compensation Expense

Share-based compensation (“SBC”) expense associated with the Share Award Incentive Plan is recognized in net income or loss over the vesting period of the share awards with a corresponding increase in contributed surplus. The issuance of common shares upon the conversion of share awards is recorded as an increase in shareholders’ capital with a corresponding reduction in contributed surplus. SBC expense varies with the quantity of unvested share awards outstanding and the grant date fair value assigned to the share awards.

18

We recorded SBC expense of $15.9 million for 2019 which is lower than $19.5 million reported for 2018. SBC expense is lower in 2019 due to the lower total value of awards granted in 2019 compared to 2018 which included additional SBC expense associated with the Strategic Combination.

As a result of the Strategic Combination, Baytex became the successor to Raging River’s Share Awards Plan, 2012 Option Plan and 2016 Option Plan (collectively, the “Raging River Plans”). Although no new grants will be made under the Raging River Plans, share awards and options held under the Raging River Plans in existence at August 22, 2018 were converted to share awards and options to purchase shares in Baytex.

Foreign Exchange

Unrealized foreign exchange gains and losses represent the change in value of the long-term notes and bank loan denominated in U.S. dollars. The long-term notes and bank loan are translated to Canadian dollars on the balance sheet date using the closing CAD/USD exchange rate. When the Canadian dollar strengthens against the U.S. dollar at the end of the current period compared to the previous period an unrealized gain is recorded and conversely when the Canadian dollar weakens at the end of the current period compared to the previous period an unrealized loss is recorded. Realized foreign exchange gains and losses are due to day-to-day U.S. dollar denominated transactions occurring in our Canadian operations.

| | Years Ended December 31 | |

($ thousands except for exchange rates) | | 2019 | | 2018 | | Change | |

Unrealized foreign exchange (gain) loss | | $ | (62,753 | ) | $ | 106,143 | | $ | (168,896 | ) |

Realized foreign exchange loss | | 966 | | 2,151 | | (1,185 | ) |

Foreign exchange (gain) loss | | $ | (61,787 | ) | $ | 108,294 | | $ | (170,081 | ) |

CAD/USD exchange rates: | | | | | | | |

At beginning of period | | 1.3646 | | 1.2518 | | | |

At end of period | | 1.2965 | | 1.3646 | | | |

We recorded an unrealized foreign exchange gain of $62.8 million for 2019 due to a strengthening of the Canadian dollar relative to the U.S. dollar at December 31, 2019 compared to December 31, 2018. The Canadian dollar weakened relative to the U.S. dollar at December 31, 2018 compared to December 31, 2017 which resulted in an unrealized foreign exchange loss of $106.1 million in 2018.

Realized foreign exchange gains and losses will fluctuate depending on the amount and timing of day-to-day U.S. dollar denominated transactions for our Canadian operations. We recorded a realized foreign exchange loss of $1.0 million for 2019 compared to a loss of $2.2 million for 2018.

Income Taxes

| | Years Ended December 31 | |

($ thousands) | | 2019 | | 2018 | | Change | |

Current income tax expense (recovery) | | $ | 2,093 | | $ | (35 | ) | $ | 2,128 | |

Deferred income tax recovery | | (68,555 | ) | (101,732 | ) | 33,177 | |

Total income tax recovery | | $ | (66,462 | ) | $ | (101,767 | ) | $ | 35,305 | |

Current income expense was $2.1 million for 2019 compared to a nominal recovery recorded in 2018. The current tax expense for 2019 reflects state taxes owing on our U.S. operations.

We recorded a deferred income tax recovery of $68.6 million for 2019 compared to $101.7 million for 2018. We recorded a lower deferred income tax recovery in 2019 primarily due to the increase in adjusted funds flow relative to 2018. The deferred tax recovery for 2019 includes a $6.1 million recovery associated with the reduction in corporate tax rates in Alberta along with a $44.6 million recovery associated with the impairment of oil and gas properties. In 2018 the deferred income tax recovery included a $63.4 million recovery associated with the impairment of oil and gas properties.

In June 2016, certain indirect subsidiaries received reassessments from the Canada Revenue Agency (the “CRA”) that deny $591 million of non-capital loss deductions relevant to the calculation of income taxes for the years 2011 through 2015. In September 2016, we filed notices of objection with the CRA appealing each reassessment received. There has been no change in the status of these reassessments since an Appeals Officer was assigned to our file in July 2018. We remain confident that our original tax filings are correct and intend to defend these tax filings through the appeals process.

19

Canadian Tax Pools ($ thousands) | | December 31, 2019 | | December 31, 2018 | |

Canadian oil and natural gas property expenditures | | $ | 492,616 | | $ | 529,044 | |

Canadian development expenditures | | 696,298 | | 765,289 | |

Canadian exploration expenditures | | 9,726 | | 8,875 | |

Undepreciated capital costs | | 433,768 | | 502,320 | |

Non-capital losses | | 705,298 | | 593,251 | |

Financing costs and other | | 4,424 | | 33,866 | |

Total Canadian tax pools | | $ | 2,342,130 | | $ | 2,432,645 | |

| | | | | |

U.S. Tax Pools ($ thousands) | | | | | |

Depletion | | $ | 156,184 | | $ | 180,367 | |

Intangible drilling costs | | 18,618 | | 133,345 | |

Tangibles | | 64,496 | | 69,138 | |

Non-capital losses | | 1,009,260 | | 1,140,579 | |

Other | | 452,710 | | 407,654 | |

Total U.S. tax pools | | $ | 1,701,268 | | $ | 1,931,083 | |

Net Income (Loss) and Adjusted Funds Flow

| | Years Ended December 31 | |

($ thousands) | | 2019 | | 2018 | | Change | |

Petroleum and natural gas sales | | $ | 1,805,919 | | $ | 1,428,870 | | $ | 377,049 | |

Royalties | | (320,241 | ) | (313,754 | ) | (6,487 | ) |

Revenue, net of royalties | | 1,485,678 | | 1,115,116 | | 370,562 | |

| | | | | | | |

Expenses | | | | | | | |

Operating | | (397,716 | ) | (311,592 | ) | (86,124 | ) |

Transportation | | (43,942 | ) | (36,869 | ) | (7,073 | ) |

Blending and other | | (68,795 | ) | (68,832 | ) | 37 | |

Operating netback | | $ | 975,225 | | $ | 697,823 | | $ | 277,402 | |

General and administrative | | (45,469 | ) | (45,825 | ) | 356 | |

Cash financing and interest | | (107,417 | ) | (104,318 | ) | (3,099 | ) |