Exhibit 99.1

ANNUAL INFORMATION FORM

2020

March 1, 2021

TABLE OF CONTENTS

| Page | |||||

| SELECTED TERMS | |||||

| ABBREVIATIONS | |||||

| CONVERSIONS AND CONVENTIONS | |||||

| SPECIAL NOTES TO READER | |||||

| CORPORATE STRUCTURE | |||||

| DEVELOPMENT OF OUR BUSINESS | |||||

| DESCRIPTION OF OUR BUSINESS | |||||

| PRINCIPAL PROPERTIES | |||||

| STATEMENT OF RESERVES DATA | |||||

| RISK FACTORS | |||||

| INDUSTRY CONDITIONS | |||||

| DIVIDENDS | |||||

| DESCRIPTION OF CAPITAL STRUCTURE | |||||

| RATINGS | |||||

| MARKET FOR SECURITIES | |||||

| DIRECTORS AND OFFICERS | |||||

| AUDIT COMMITTEE INFORMATION | |||||

| LEGAL PROCEEDINGS AND REGULATORY ACTIONS | |||||

| INTEREST OF INSIDERS AND OTHER MATERIAL TRANSACTIONS | |||||

| TRANSFER AGENT AND REGISTRAR | |||||

| MATERIAL CONTRACTS | |||||

| INTERESTS OF EXPERTS | |||||

| ADDITIONAL INFORMATION | |||||

APPENDICES:

APPENDIX A REPORT OF MANAGEMENT AND DIRECTORS ON OIL AND GAS DISCLOSURE

APPENDIX B REPORT ON RESERVES DATA BY INDEPENDENT QUALIFIED RESERVES EVALUATOR

APPENDIX C AUDIT COMMITTEE MANDATE AND TERMS OF REFERENCE

SELECTED TERMS

Capitalized terms in this document have the meanings set forth below:

Entities

Baytex or the Corporation means Baytex Energy Corp., a corporation incorporated under the ABCA.

Baytex Energy means Baytex Energy Ltd., a corporation amalgamated under the ABCA.

Baytex Partnership means Baytex Energy Limited Partnership, a limited partnership, the partners of which are Baytex Energy and Baytex Energy (LP) Ltd.

Baytex USA means Baytex Energy USA, Inc., a corporation organized under the laws of the State of Delaware.

Board or Board of Directors means the board of directors of Baytex.

NYSE means New York Stock Exchange.

OPEC means the Organization of the Petroleum Exporting Countries.

OPEC+ means OPEC plus a number of other oil exporting countries, including Russia.

Raging River means Raging River Exploration Inc.

SEC means the United States Securities and Exchange Commission.

Shareholders mean the holders from time to time of Common Shares.

subsidiary has the meaning ascribed thereto in the Securities Act (Ontario) and, for greater certainty, includes all corporations, partnerships and trusts owned, controlled or directed, directly or indirectly, by us.

TSX means the Toronto Stock Exchange.

we, us and our means Baytex and all its subsidiaries on a consolidated basis unless the context requires otherwise.

Securities and Other Terms

2014 Debt Indenture means the indenture, as amended, among Baytex, as issuer, certain of its subsidiaries, as guarantors, and Computershare Trust Company, N.A., as indenture trustee, dated June 6, 2014.

2020 Debt Indenture means the indenture among Baytex, as issuer, certain of its subsidiaries, as guarantors, and Computershare Trust Company, N.A., as indenture trustee, dated February 5, 2020.

2021 Debentures means the 6.75% series B senior unsecured debentures due February 17, 2021 which were redeemed as of September 13, 2019.

2022 Debentures means the 6.625% series C senior unsecured debentures due July 19, 2022 which were redeemed as of March 5, 2020.

2021 Notes means the 5.125% senior unsecured notes due June 1, 2021 issued by Baytex pursuant to the 2014 Debt Indenture which were redeemed as of February 20, 2020.

| 1 | |||||||

2024 Notes means the 5.625% senior unsecured notes due June 1, 2024 issued by Baytex pursuant to the 2014 Debt Indenture.

2027 Notes means the 8.750% senior unsecured notes due April 1, 2027 issued by Baytex pursuant to the 2020 Debt Indenture.

ABCA means the Business Corporations Act (Alberta), R.S.A. 2000, c. B-9, as amended, including the regulations promulgated thereunder.

AIF means this annual information form of the Corporation dated March 1, 2021 for the year ended December 31, 2020.

Canadian GAAP means generally accepted accounting principles in Canada, which are consistent with International Financial Reporting Standards as issued by the International Accounting Standards Board.

Common Shares means the common shares of Baytex.

Credit Facilities means our Revolving Credit Facilities and our Term Loan.

CSS means cyclic steam stimulation.

GHG means greenhouse gas.

MD&A means management's discussion and analysis of operating and financial results.

Revolving Credit Facilities means our US$575 million secured covenant-based credit facilities with a syndicate of financial institutions.

SAGD means steam-assisted gravity drainage.

Senior Notes means the 2024 Notes and the 2027 Notes.

Tax Act means the Income Tax Act (Canada), R.S.C. 1985, c. 1 (5th Supp.), as amended, including the regulations promulgated thereunder, as amended from time to time.

Term Loan means our $300 million secured term loan with a syndicate of financial institutions.

Independent Engineering

Baytex Reserves Report means the report of McDaniel dated February 4, 2021 entitled ‘‘Baytex Energy Corp., Evaluation of Petroleum Reserves, Based on Forecast Prices and Costs, As of December 31, 2020’’.

COGE Handbook means the Canadian Oil and Gas Evaluation Handbook maintained by the Society of Petroleum Evaluation Engineers (Calgary Chapter), as amended from time to time.

McDaniel means McDaniel & Associates Consultants Ltd., independent petroleum consultants.

NI 51-101 means National Instrument 51-101 "Standards of Disclosure for Oil and Gas Activities" of the Canadian Securities Administrators.

| 2 | |||||||

Reserves Definitions

Gross means:

(a)in relation to our interest in production and reserves, our interest (operating and non-operating) share before deduction of royalties and without including any of our royalty interests;

(b)in relation to wells, the total number of wells in which we have an interest; and

(c)in relation to properties, the total area of properties in which we have an interest.

Net means:

(a)in relation to our interest in production and reserves, our interest (operating and non-operating) share after deduction of royalty obligations, plus our royalty interest in production or reserves;

(b)in relation to wells, the number of wells obtained by aggregating our working interest in each of our gross wells; and

(c)in relation to our interest in a property, the total area in which we have an interest multiplied by our working interest.

Forecast Prices and Costs are prices and costs that are:

(a)generally acceptable as being a reasonable outlook of the future; and

(b)if, and only to the extent that, there are fixed or presently determinable future prices or costs to which Baytex is legally bound by a contractual or other obligation to supply a physical product, including those for an extension period of a contract that is likely to be extended, those prices or costs rather than the prices and costs referred to in paragraph (a).

Reserves and Reserve Categories

Reserves are estimated remaining quantities of oil and natural gas and related substances anticipated to be recoverable from known accumulations, from a given date forward, based on:

(a)analysis of drilling, geological, geophysical and engineering data;

(b)the use of established technology; and

(c)specified economic conditions (being the Forecast Prices and Costs used in the estimate).

Proved reserves are those reserves that can be estimated with a high degree of certainty to be recoverable. It is likely that the actual remaining quantities recovered will exceed the estimated proved reserves.

Probable reserves are those additional reserves that are less certain to be recovered than proved reserves. It is equally likely that the actual remaining quantities recovered will be greater or less than the sum of the estimated proved plus probable reserves.

The qualitative certainty levels referred to in the definitions above are applicable to individual reserves entities (which refers to the lowest level at which reserves calculations are performed) and to reported reserves (which refers to the highest level sum of individual entity estimates for which reserves are presented). Reported reserves should target the following levels of certainty under a specific set of economic conditions:

(i)at least a 90 percent probability that the quantities actually recovered will equal or exceed the estimated proved reserves; and

| 3 | |||||||

(ii)at least a 50 percent probability that the quantities actually recovered will equal or exceed the sum of the estimated proved plus probable reserves.

A qualitative measure of the certainty levels pertaining to estimates prepared for the various reserves categories is desirable to provide a clearer understanding of the associated risks and uncertainties. However, the majority of reserves estimates will be prepared using deterministic methods that do not provide a mathematically derived quantitative measure of probability. In principle, there should be no difference between estimates prepared using probabilistic or deterministic methods.

Development and Production Status

Each of the reserves categories (proved and probable) may be divided into developed and undeveloped categories:

(a)Developed reserves are those reserves that are expected to be recovered from existing wells and installed facilities or, if facilities have not been installed, that would involve a low expenditure (for example, when compared to the cost of drilling a well) to put the reserves on production. The developed category may be subdivided into the following categories:

i.Developed producing reserves are those reserves that are expected to be recovered from completion intervals open at the time of the estimate. These reserves may be currently producing or, if shut-in, they must have previously been on production, and the date of resumption of production must be known with reasonable certainty.

ii.Developed non-producing reserves are those reserves that either have not been on production, or have previously been on production, but are shut-in, and the date of resumption of production is unknown.

(b)Undeveloped reserves are those reserves expected to be recovered from known accumulations where a significant expenditure (for example, when compared to the cost of drilling a well) is required to render them capable of production. They must fully meet the requirements of the reserves classification (proved or probable) to which they are assigned.

ABBREVIATIONS

| Oil and Natural Gas Liquids | Natural Gas | |||||||||||||

| bbl | barrel | Mcf | thousand cubic feet | |||||||||||

| Mbbl | thousand barrels | MMcf | million cubic feet | |||||||||||

| MMbbl | million barrels | Bcf | billion cubic feet | |||||||||||

| NGL | natural gas liquids | Mcf/d | thousand cubic feet per day | |||||||||||

| bbl/d | barrels per day | MMcf/d | million cubic feet per day | |||||||||||

m3 | cubic metres | |||||||||||||

| MMbtu | million British Thermal Units | |||||||||||||

| 4 | |||||||

| Other | ||||||||||||||

| API | the measure of the density or gravity of liquid petroleum products as compared to water | |||||||||||||

| BOE or boe | barrel of oil equivalent, using the conversion factor of six Mcf of natural gas being equivalent to one bbl of oil. BOEs may be misleading, particularly if used in isolation. A BOE conversion ratio of 6 Mcf: 1 bbl is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. | |||||||||||||

| boe/d | barrels of oil equivalent per day | MEH | Magellan East Houston | |||||||||||

| Mboe | thousand barrels of oil equivalent | MSW | Mixed Sweet Blend | |||||||||||

| MMboe | million barrels of oil equivalent | WTI | West Texas Intermediate | |||||||||||

| NYMEX | the New York Mercantile Exchange | WCS | Western Canadian Select | |||||||||||

| AECO | the natural gas storage facility located at Suffield, Alberta | $ Million | millions of dollars | |||||||||||

| $000s | thousands of dollars | |||||||||||||

CONVERSIONS AND CONVENTIONS

The following table sets forth certain conversions between Standard Imperial Units and the International System of Units (or metric units).

| To Convert From | To | Multiply By | ||||||

| Mcf | Cubic metres | 28.174 | ||||||

| Cubic metres | Cubic feet | 35.494 | ||||||

| Bbl | Cubic metres | 0.159 | ||||||

| Cubic metres | Bbl | 6.293 | ||||||

| Feet | Metres | 0.305 | ||||||

| Metres | Feet | 3.281 | ||||||

| Miles | Kilometres | 1.609 | ||||||

| Kilometres | Miles | 0.621 | ||||||

| Acres | Hectares | 0.400 | ||||||

| Hectares | Acres | 2.500 | ||||||

Certain terms used herein are defined in NI 51-101 and, unless the context otherwise requires, shall have the same meanings in this AIF as in NI 51-101. Unless otherwise indicated, references in this AIF to "$" or "dollars" are to Canadian dollars and references to "US$" are to United States dollars. All financial information contained in this AIF has been presented in Canadian dollars in accordance with Canadian GAAP. All operational information contained in this AIF relates to our consolidated operations unless the context otherwise requires.

SPECIAL NOTES TO READER

Forward-Looking Statements

In the interest of providing our Shareholders and potential investors with information about us, including management's assessment of our future plans and operations, certain statements in this AIF are "forward-looking statements" within the meaning of the United States Private Securities Litigation Reform Act of 1995 and "forward-looking information" within the meaning of applicable Canadian securities legislation (collectively, "forward-looking statements"). In some cases, forward-looking statements can be identified by terminology such as "anticipate", "believe", "continue", "could", "estimate", "expect", "forecast", "intend", "may", "objective", "ongoing", "outlook", "potential", "project", "plan", "should", "target", "would", "will" or similar words suggesting future outcomes, events or performance. The forward-looking statements contained in this AIF speak only as of the date hereof and are expressly qualified by this cautionary statement.

| 5 | |||||||

Specifically, this AIF contains forward-looking statements relating to, but not limited to: our business strategies, plans and objectives; our 2021 capital budget; our goal of building value by developing our assets and completing selective acquisitions; development plans for our properties; undeveloped lease expiries; the payment of cash income taxes; our working interest production volume for 2021 based on the future net revenue disclosed in our reserves; that we market our production with attention to maximizing value and counterparty performance; the development plans for our undeveloped reserves; our future abandonment and reclamation liabilities; our funding sources for development capital expenditures; the impact of existing and proposed governmental and environmental regulation; and our assessment of our tax filing position for the years 2011 through 2015.

In addition, there are forward-looking statements in this AIF under the headings "General Description of Our Business" and "Statement of Reserves Data" as to our reserves, including with respect thereto, the future net revenues from our reserves, pricing and inflation rates, future development costs, the development of our proved undeveloped reserves and probable undeveloped reserves, future development costs, reclamation and abandonment obligations, tax horizon, exploration and development activities and production estimates.

These forward-looking statements are based on certain key assumptions regarding, among other things: oil and natural gas prices and differentials between light, medium and heavy oil prices; well production rates and reserve volumes; our ability to add production and reserves through our exploration and development activities; capital expenditure levels; our ability to borrow under our credit agreements; the receipt, in a timely manner, of regulatory and other required approvals for our operating activities; the availability and cost of labour and other industry services; interest and foreign exchange rates; the continuance of existing and, in certain circumstances, proposed tax and royalty regimes; our ability to develop our crude oil and natural gas properties in the manner currently contemplated; and current industry conditions, laws and regulations continuing in effect (or, where changes are proposed, such changes being adopted as anticipated). Readers are cautioned that such assumptions, although considered reasonable by Baytex at the time of preparation, may prove to be incorrect.

Actual results achieved will vary from the information provided herein as a result of numerous known and unknown risks and uncertainties and other factors. Such factors include, but are not limited to: the volatility of oil and natural gas prices and price differentials (including the impacts of Covid-19); the availability and cost of capital or borrowing; risks associated with our ability to exploit our properties and add reserves; availability and cost of gathering, processing and pipeline systems; that our credit facilities may not provide sufficient liquidity or may not be renewed; failure to comply with the covenants in our debt agreements; risks associated with a third-party operating our Eagle Ford properties; public perception and its influence on the regulatory regime; restrictions or costs imposed by climate change initiatives and the physical risks of climate change; new regulations on hydraulic fracturing; restrictions on or access to water or other fluids; changes in government regulations that affect the oil and gas industry; regulations regarding the disposal of fluids; changes in environmental, health and safety regulations; costs to develop and operate our properties; variations in interest rates and foreign exchange rates; risks associated with our hedging activities; retaining or replacing our leadership and key personnel; changes in income tax or other laws or government incentive programs; uncertainties associated with estimating oil and natural gas reserves; our inability to fully insure against all risks; risks of counterparty default; risks related to our thermal heavy oil projects; alternatives to and changing demand for petroleum products; risks associated with our use of information technology systems; results of litigation; risks associated with large projects; risks associated with the ownership of our securities, including changes in market-based factors; risks for United States and other non-resident shareholders, including the ability to enforce civil remedies, differing practices for reporting reserves and production, additional taxation applicable to non-residents and foreign exchange risk; and other factors, many of which are beyond our control.

Readers are cautioned that the foregoing list of risk factors is not exhaustive. New risk factors emerge from time to time, and it is not possible for management to predict all of such factors and to assess in advance the impact of each such factor on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking

| 6 | |||||||

statements. Readers should also carefully consider the matters discussed under the heading "Risk Factors" in this AIF.

The above summary of assumptions and risks related to forward-looking statements in this AIF has been provided in order to provide Shareholders and potential investors with a more complete perspective on our current and future operations and such information may not be appropriate for other purposes. There is no representation by us that actual results achieved will be the same in whole or in part as those referenced in the forward-looking statements and we do not undertake any obligation to update publicly or to revise any of the included forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required by applicable securities law. The forward-looking statements contained in this AIF are expressly qualified by this cautionary statement.

Access to Documents

Any document referred to in this AIF and described as being accessible on the SEDAR website at www.sedar.com or on EDGAR at www.sec.gov (including those documents referred to as being incorporated by reference in this AIF) may be obtained free of charge from us at Suite 2800, Centennial Place, East Tower, 520 - 3rd Avenue S.W., Calgary, Alberta, Canada, T2P 0R3.

CORPORATE STRUCTURE

General

Baytex Energy Corp. was incorporated on October 22, 2010 pursuant to the provisions of the ABCA. Baytex is the successor to the business of Baytex Energy Trust, which was transitioned to Baytex on December 31, 2010.

Our head and principal office is located at Suite 2800, Centennial Place, East Tower, 520 – 3rd Avenue S.W., Calgary, Alberta, Canada, T2P 0R3. Our registered office is located at 2400, 525 – 8th Avenue S.W., Calgary, Alberta, Canada, T2P 1G1.

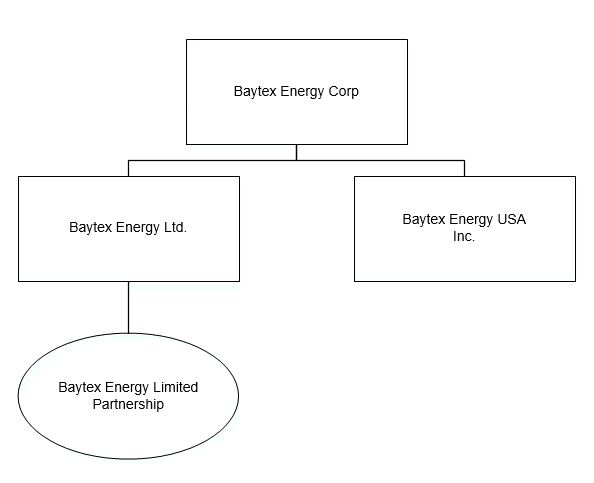

Inter-Corporate Relationships

The following table provides the name, the percentage of voting securities owned by us and the jurisdiction of incorporation, continuance, formation or organization of our material subsidiaries either, direct and indirect, as at the date hereof.

| Percentage of voting securities (directly or indirectly) | Jurisdiction of Incorporation/ Formation | ||||||||||

| Baytex Energy Ltd. | 100% | Alberta | |||||||||

| Baytex Energy USA, Inc. | 100% | Delaware | |||||||||

| Baytex Energy Limited Partnership | 100% | Alberta | |||||||||

| 7 | |||||||

Our Organizational Structure

The following simplified diagram shows the inter-corporate relationships among us and our material subsidiaries as of the date hereof.

DEVELOPMENT OF OUR BUSINESS

Developments in the Past Three Years

2018

In 2018 commodity prices improved relative to the prior year, but remained volatile. The price for WTI increased from Q1 through to Q3 and then dropped in Q4 to average US$64.77 for the year. The decrease in WTI during Q4 coincided with a widening of differentials for Canadian crude oil, which impacted our Canadian operations.

On June 18, Baytex and Raging River announced a strategic combination. The merger closed on August 22 and was effected by way of a plan of arrangement under the ABCA, whereby holders of Raging River common shares received, directly or indirectly, 1.36 Common Shares of Baytex for each Raging River share held. Upon closing of the strategic combination, holders of Baytex shares held 43% and holders of Raging River shares held 57% of the issued and outstanding shares of the combined company.

The transaction added approximately 23,000 boe/d of production from the Viking play in Saskatchewan and Alberta and 284,000 net acres of land in the emerging East Duvernay Shale play in Alberta. At closing, a combined leadership team from both companies was appointed.

Concurrent with closing, we announced an updated 2018 capital budget range of $450-$500 million and assumed the $300 million Term Loan from Raging River that is secured by the assets of Raging River.

Our production averaged 80,458 boe/d for the year and 98,890 boe/d in Q4, an increase from 2017, due to strong well performance and contributions from the Raging River combination.

On December 17, we announced a 2019 capital budget range of $550-$650 million designed to generate average annual production of 93,000-97,000 boe/d.

| 8 | |||||||

2019

In 2019 commodity prices decreased relative to 2018, with the WTI price averaging US$57.03/bbl for the year. The decrease in WTI was partially offset by a narrowing of differentials in Canada, with the WCS differential averaging US$12.75/bbl in 2019 as compared to US$26.31/bbl in 2018, which positively impacted our Canadian operations.

Our production averaged 97,680 boe/d in 2019, above our guidance range and an increase from 2018, due to the contribution from the Raging River assets and strong well performance, while exploration and development expenditures were at the low end of our budget range for the year at $552 million. In September 2019 we early redeemed US$150 million principal amount of senior unsecured notes due February 2021.

On December 4, we announced a 2020 capital budget range of $500-$575 million designed to generate average annual production of 93,000-97,000 boe/d and the appointment of Mark R. Bly as Chair of the Board.

2020

2020 was an extremely challenging year. The spread of Covid-19 and the associated decrease in demand for crude oil combined with a decision by the members of OPEC to increase the supply of crude oil resulted in a significant reduction in commodity prices. Commodity prices increased from their lows following a production curtailment agreement between members of the OPEC+ group to limit supply, but remained below their previous levels as a result of decreased demand associated with continued efforts to limit the spread of Covid-19. The price for WTI averaged US$39.40/bbl for the year.

Prior to the market dislocations caused by the spread of Covid-19 we entered into a series of transactions to extend the maturity dates of our outstanding indebtedness. On February 5, we issued US$500 million principal amount of 2027 Notes. The proceeds of this issuance, along with available cash and liquidity available under our Credit Facilities, were used to redeem our US$400 million principal amount 2021 Notes on February 2020 and our $300 million principal amount 2022 Debentures on March 5, 2020. In addition, on March 2, 2020 we extended the maturity of our Credit Facilities to April 2, 2024. Following these transactions the nearest maturity date of our senior unsecured debt and Credit Facilities was extended from 2021 to 2024.

In response to decreased commodity prices, we took decisive steps to adjust our business model. We reduced our capital budget by 50% and shut-in approximately 25,000 boe/d of production for a portion of the year. As a result, production for the year averaged 79,781 boe/d, while exploration and development expenditures were $280 million.

On December 2 we announced a 2021 capital budget range of $220-275 million designed to generate average annual production of 73,000-77,000 boe/d, which reflects the re-set of our business that occurred in 2020.

NYSE Delisting

On March 24, 2020, we received a continued listing standards notice from the NYSE as the average closing price for our Common Shares was less than US$1.00 per share over a period of 30 consecutive trading days. Subsequently, on December 3, 2020, our Common Shares were delisted from the NYSE. Baytex’s Common Shares continue to trade on the TSX.

| 9 | |||||||

DESCRIPTION OF OUR BUSINESS

Overview

We are engaged in the acquisition, development and production of crude oil and natural gas in the Western Canadian Sedimentary Basin and the Eagle Ford in the United States. Approximately 82% of our production is weighted toward crude oil and NGLs. The Company and its predecessors have been in business for more than 25 years and our operating teams are well established with a track record of technical proficiency and operational success. Throughout our history we have endeavoured to add value by developing our assets and completing selective acquisitions.

Competitive Conditions

Baytex is a member of the oil and natural gas industry, which is highly competitive. Baytex competes with other companies for all of its business inputs, including exploitation and development prospects, access to commodity markets, acquisition opportunities, available capital and staffing. We believe our competitive position is, on the whole, similar to that of other oil and natural gas producers of a similar size and production profile. See Industry Conditions and Risk Factors.

Reorganizations

On July 15, 2018, we dissolved our general partnership, Baytex Energy Partnership, which had previously held a beneficial interest in the majority of our producing properties in Canada. The beneficial interest is now held by Baytex Energy. In addition, on August 22, 2018, in conjunction with the Raging River merger, all of the oil and gas properties of Raging River were transferred to the newly formed Baytex Partnership.

Environmental and Social Policies

We have an active program to monitor and comply with all environmental laws, rules and regulations applicable to our operations. Our policies require that all employees and contractors report all breaches or potential breaches of environmental laws, rules and regulations to our senior management and all applicable governmental authorities. Any material breaches of environmental law, rules and regulations must be reported to the Board of Directors. Our Health, Safety and Environment policy is available on our website at www.baytexenergy.com.

We have published a Corporate Responsibility Report every second year since 2012. This report details our efforts and performance with respect to people, the environment, our community and stakeholders, and responsible business practices. For example, our 2019 report announced our intention to reduce our corporate emission intensity (tonnes of CO2e per boe) by 30% by 2021, relative to our 2018 baseline. We exceeded this target in scope and timing, achieving a 46% reduction in our GHG emissions intensity through year-end 2020 and have now established a new target with an objective to reduce our corporate GHG emission intensity by a further 33% from current levels by 2025. This equates to an approximate 65% reduction by 2025, relative to our 2018 baseline. Our sustainability reports along with an annual update showing our 2019 metrics can be viewed on our website at www.baytexenergy.com/sustainability/sustainability-home.cfm.

In recognition of the importance of our health, safety and environment policy and targets, including our GHG reduction target, the reserves and sustainability committee of our board of directors has been given specific responsibility for the "oversight and monitoring of the Corporation’s performance related to health, safety, environment, climate and other sustainability matters." This change was recognized by amending the committee's mandate and terms of reference in July of 2020. In addition, Baytex was recognized by Corporate Knights as one of the Future 40 Responsible Corporate Leaders in Canada for 2018. See Industry Conditions and Risk Factors.

| 10 | |||||||

Cyclical and Seasonal Factors

Our operational results and financial condition are dependent on the prices received for our oil and natural gas production. Oil and natural gas prices have fluctuated widely during recent years. Such prices are determined by supply and demand factors, including weather and general economic conditions, as well as conditions in other oil and natural gas regions. Any decline in oil and natural gas prices could have an adverse effect on our financial condition. We mitigate such price risk by closely monitoring commodity markets, implementing our risk management programs and by maintaining financial liquidity. Additionally, we continually review our capital program and implement initiatives to adapt to such price changes. See Industry Conditions and Risk Factors.

The level of activity in the oil and gas industry is dependent on access to areas where operations are conducted. In Canada, seasonal weather variations, including spring break-up which occurs annually, affects access in certain circumstances. In Canada and the United States, unexpected adverse weather conditions, such as flooding, extreme cold weather, heavy snowfall, heavy rainfall and forest fires may restrict the Corporation's ability to access its properties. See Industry Conditions and Risk Factors.

Renegotiation or Termination of Contracts

As at the date hereof, we do not anticipate that any aspects of our business will be materially affected during the remainder of 2021 by the renegotiation or termination of contracts.

Personnel

As at December 31, 2020, we had 139 employees in our head office and 67 employees in our field operations.

PRINCIPAL PROPERTIES

The following is a description of our principal oil and natural gas properties on production or under development as at December 31, 2020. Unless otherwise specified, gross and net acres and well count information are as at December 31, 2020 and production information represents average working interest production for the year ended December 31, 2020.

Eagle Ford - Texas

Our Eagle Ford assets are located in the core of the liquids-rich Eagle Ford shale in South Texas. Our assets include non-operated working interests in approximately 78,212 (19,931 net) acres, comprised of four areas of mutual interest (Sugarloaf, Longhorn, Ipanema and Excelsior) with an average working interest of approximately 25%, together with field infrastructure and related assets. Our entire acreage position in the Eagle Ford is held by production and the assets are operated by an operating subsidiary of Marathon Oil Corporation (NYSE: MRO), pursuant to the terms of industry-standard joint operating agreements. Production in the area occurs from the hydraulic fracturing of horizontal wells.

During 2020, production from the Eagle Ford assets averaged approximately 31,179 boe/d, comprised of 24,069 bbl/d of light oil, condensate and NGL and 42,665 Mcf/d of shale gas. During this period, Baytex participated in the completion of 62 (14.1 net) wells, resulting in 52 (11.5 net) oil wells and 10 (2.6 net) natural gas wells. As at December 31, 2020, our proved plus probable reserves were 215 million boe (153 proved; 62 probable).

Viking - Alberta and Saskatchewan

Our Viking assets are located in the greater Dodsland area in southwest Saskatchewan and in the Esther area of southeastern Alberta. These assets were acquired through a business combination with Raging River and produce light oil from the Viking formation. Production in the area occurs primarily from the hydraulic fracturing of horizontal wells. In some areas, reservoirs are placed under waterflood. In 2020,

| 11 | |||||||

the Viking assets produced 19,614 boe/d, comprised of 17,771 bbl/d of light oil and NGL and 11,058 Mcf/d of natural gas. These assets are characterized by shallow wells with short cycle times and a manufacturing approach to development. In 2020, Baytex completed 120 (115.5 net) oil wells. As at December 31, 2020 we had proved plus probable reserves of 85 million boe (57 proved; 28 probable).

The undeveloped land base associated with the Viking assets consisted of 213,430 net acres at year-end 2020.

Peace River - Alberta

In the Peace River area of northwest Alberta we produce heavy gravity crude oil and natural gas from the Bluesky formation. Production in the area occurs through primary and polymer flooding recovery methods. During 2020, production from the area averaged approximately 11,810 boe/d, comprised of 9,853 bbl/d of heavy oil, 19 bbl/d of NGL and 11,630 Mcf/d of natural gas. In 2020, Baytex drilled 4 (4.0 net) horizontal multi-lateral wells in this area. As at December 31, 2020, we had proved plus probable reserves of 39 million boe (19 proved; 21 probable).

Baytex held approximately 271,463 net undeveloped acres in this area at year-end 2020.

Lloydminster - Alberta and Saskatchewan

Our Lloydminster assets consist of several geographically dispersed heavy oil operations that include primary and thermal production. In some cases, Baytex's heavy oil reservoirs are water flooded and polymer flooded. In 2020, production averaged approximately 11,525 boe/d, which was comprised of 8,776 bbl/d of heavy oil, 2,513 bbl/d of bitumen, 12 bbl/d of light oil, and 1,346 Mcf/d of natural gas. In 2020, Baytex drilled 29 (29.0 net) oil wells and 6 (6.0 net) stratigraphic wells in this area. As at December 31, 2020, we had proved plus probable reserves of 83 million boe (25 proved; 58 probable).

We held approximately 191,930 net undeveloped acres in this area at year-end 2020.

Duvernay - Alberta

On August 22, 2018, as a result of the the merger with Raging River, Baytex acquired a land position in the emerging East Duvernay resource play in central Alberta. Production in the area occurs from the hydraulic fracturing of horizontal wells. In 2020, the Duvernay assets produced 1,507 boe/d, comprised of 1,235 bbl/d of light oil and NGL and 1,634 Mcf/d of natural gas. During 2020, Baytex drilled 2 (2.0 net) oil wells. As at December 31, 2020, our proved plus probable reserves are 17 million boe (8 proved; 9 probable) and our net undeveloped lands totaled approximately 249,613 net acres.

| 12 | |||||||

Average Production

The following table indicates our average daily production from our principal properties for the year ended December 31, 2020.

| Heavy Oil (bbl/d) | Bitumen (bbl/d) | Light and Medium Oil (bbl/d) | Tight Oil (bbl/d) | NGL(1) (bbl/d) | Shale Gas (Mcf/d) | Natural Gas (Mcf/d) | Oil Equivalent (boe/d) | |||||||||||||||||||||||||||||||||||||||||||

| Canada - Heavy | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Peace River | 9,853 | — | — | — | 19 | — | 11,630 | 11,810 | ||||||||||||||||||||||||||||||||||||||||||

| Lloydminster | 8,776 | 2,513 | 12 | — | — | — | 1,346 | 11,525 | ||||||||||||||||||||||||||||||||||||||||||

| Total | 18,629 | 2,513 | 12 | — | 19 | — | 12,976 | 23,335 | ||||||||||||||||||||||||||||||||||||||||||

| Canada - Light | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Viking | — | — | 17,603 | — | 168 | — | 11,058 | 19,614 | ||||||||||||||||||||||||||||||||||||||||||

| Duvernay | — | — | — | 797 | 438 | 1,634 | — | 1,507 | ||||||||||||||||||||||||||||||||||||||||||

| Remaining properties | — | — | 528 | — | 762 | — | 17,131 | 4,146 | ||||||||||||||||||||||||||||||||||||||||||

| Total | — | — | 18,131 | 797 | 1,368 | 1,634 | 28,189 | 25,267 | ||||||||||||||||||||||||||||||||||||||||||

| United States | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Eagle Ford | — | — | — | 13,001 | 11,068 | 42,665 | — | 31,179 | ||||||||||||||||||||||||||||||||||||||||||

| Grand Total | 18,629 | 2,513 | 18,143 | 13,798 | 12,455 | 44,299 | 41,165 | 79,781 | ||||||||||||||||||||||||||||||||||||||||||

Note:

(1)Includes condensate.

Costs Incurred

The following table summarizes the property acquisition, exploration and development costs by country for the year ended December 31, 2020.

| ($000s) | Canada | United States | Total | |||||||||||||||||

| Property acquisition costs | ||||||||||||||||||||

| Proved properties | — | — | — | |||||||||||||||||

| Unproved properties | — | — | — | |||||||||||||||||

| Property disposition | (182) | — | (182) | |||||||||||||||||

| Total Property acquisition costs, net | (182) | — | (182) | |||||||||||||||||

Development Costs (1) | 170,462 | 105,388 | 275,850 | |||||||||||||||||

Exploration Costs (2) | 4,490 | — | 4,490 | |||||||||||||||||

| Total | 174,770 | 105,388 | 280,158 | |||||||||||||||||

Notes:

(1)Development and facilities expenditures.

(2)Cost of land, geological and geophysical capital expenditures.

| 13 | |||||||

Oil and Gas Wells

The following table sets forth the number and status of wells in which we have a working interest as at December 31, 2020.

| Oil Wells | Natural Gas Wells | ||||||||||||||||||||||||||||||||||||||||||||||

| Producing | Non-Producing | Producing | Non-Producing | ||||||||||||||||||||||||||||||||||||||||||||

| Gross | Net | Gross | Net | Gross | Net | Gross | Net | ||||||||||||||||||||||||||||||||||||||||

| Alberta | 812 | 674.7 | 1,268 | 837.4 | 346 | 256.1 | 726 | 572.4 | |||||||||||||||||||||||||||||||||||||||

| BC | — | — | 1 | 0.5 | — | — | 2 | 0.9 | |||||||||||||||||||||||||||||||||||||||

| Saskatchewan | 2,815 | 2,552.1 | 1,984 | 1,904.6 | 450 | 361.2 | 398 | 358.1 | |||||||||||||||||||||||||||||||||||||||

| Texas | 831 | 186.1 | 59 | 13.4 | 370 | 103.4 | 26 | 5.7 | |||||||||||||||||||||||||||||||||||||||

| Total | 4,458 | 3,412.9 | 3,312 | 2,755.9 | 1,166 | 720.7 | 1,152 | 937.1 | |||||||||||||||||||||||||||||||||||||||

Properties with No Attributed Reserves

The following table sets forth our undeveloped land holdings as at December 31, 2020.

| Undeveloped Acres | |||||||||||

| Gross | Net | ||||||||||

| Alberta | 837,774 | 753,776 | |||||||||

| Saskatchewan | 354,654 | 321,665 | |||||||||

| Total | 1,192,428 | 1,075,441 | |||||||||

Undeveloped land holdings are lands that have not been assigned reserves as at December 31, 2020. None of these undeveloped properties have high expected development or operating costs or contractual sales obligations to produce and sell at substantially lower prices than could be realized under normal market conditions.

We estimate the value of our net undeveloped land holdings at December 31, 2020 to be approximately $129.7 million, as compared to $161.6 million as at December 31, 2019. This internal evaluation generally represents the estimated replacement cost of our undeveloped land and excludes approximately 82,533 net acres of our undeveloped land that we expect to expire on or before December 31, 2021. In determining replacement cost, we analyzed land sale prices paid at provincial crown land sales for properties in the vicinity of our undeveloped land holdings over the preceding three years.

Tax Horizon

Baytex does not expect to pay any material cash income taxes prior to 2029. This estimate and any amount of income tax we may be required to pay in the future is highly sensitive to assumptions regarding commodity prices, production, cash flow, capital expenditure levels and changes in governing tax laws. For additional information, see Note 15 of our audited consolidated financial statements for the year ended December 31, 2020 and the information under the heading "Income Taxes" in our MD&A for the year ended December 31, 2020.

| 14 | |||||||

Exploration and Development Activities

The following table sets forth the gross and net exploratory and development wells in which we participated during the year ended December 31, 2020.

| Exploratory Wells | Development Wells | Total Wells | |||||||||||||||||||||||||||||||||

| Gross | Net | Gross | Net | Gross | Net | ||||||||||||||||||||||||||||||

| Oil | — | — | 193 | 147.6 | 193 | 147.6 | |||||||||||||||||||||||||||||

| Natural Gas | — | — | 11 | 4.9 | 11 | 4.9 | |||||||||||||||||||||||||||||

| Stratigraphic | 6 | 6.0 | — | — | 6 | 6.0 | |||||||||||||||||||||||||||||

| Service | — | — | — | — | — | — | |||||||||||||||||||||||||||||

| Dry | — | — | — | — | — | — | |||||||||||||||||||||||||||||

| Total | 6 | 6.0 | 204 | 152.5 | 210 | 158.5 | |||||||||||||||||||||||||||||

Production Estimates

The following table sets out the volumes of our working interest production estimated for the year ending December 31, 2021, which is reflected in the estimate of future net revenue disclosed in the forecast price tables contained under "Statement of Reserves Data - Disclosure of Reserves Data".

| Heavy Oil (bbl/d) | Bitumen (bbl/d) | Light and Medium Oil (bbl/d) | Tight Oil (bbl/d) | NGL (bbl/d)(1) | Shale Gas (Mcf/d) | Natural Gas (Mcf/d) | Oil Equivalent (boe/d) | ||||||||||||||||||||||||||||||||||||||||

| CANADA | |||||||||||||||||||||||||||||||||||||||||||||||

| Total Proved | 18,099 | 1,562 | 14,628 | 1,054 | 1,540 | 2,066 | 42,734 | 44,349 | |||||||||||||||||||||||||||||||||||||||

| Total Proved plus Probable | 19,228 | 1,738 | 16,198 | 1,180 | 1,758 | 2,291 | 45,699 | 48,100 | |||||||||||||||||||||||||||||||||||||||

| UNITED STATES | |||||||||||||||||||||||||||||||||||||||||||||||

| Total Proved | — | — | — | 11,621 | 12,587 | 39,630 | — | 30,813 | |||||||||||||||||||||||||||||||||||||||

| Total Proved plus Probable | — | — | — | 11,914 | 12,855 | 40,393 | — | 31,500 | |||||||||||||||||||||||||||||||||||||||

| TOTAL | |||||||||||||||||||||||||||||||||||||||||||||||

| Total Proved | 18,099 | 1,562 | 14,628 | 12,674 | 14,127 | 41,696 | 42,734 | 75,162 | |||||||||||||||||||||||||||||||||||||||

| Total Proved plus Probable | 19,228 | 1,738 | 16,198 | 13,094 | 14,612 | 42,684 | 45,699 | 79,600 | |||||||||||||||||||||||||||||||||||||||

Note:

(1)Includes condensate.

The two properties that account for 20% or more of the estimated 2021 production volumes are the Eagle Ford and the Viking. Estimated 2021 production volumes for the Eagle Ford is 30,813 boe/d on a total proved basis and 31,500 boe/d on a total proved plus probable basis. Estimated 2021 production volumes for the Viking is 15,873 boe/d on a total proved basis and 17,611 boe/d on a total proved plus probable basis.

| 15 | |||||||

Production History

The following table summarizes certain information in respect of the production, product prices received, royalties paid, production costs and resulting netback associated with our reserves data for the periods indicated below.

| Three Months Ended | Year Ended | ||||||||||||||||||||||||||||

| Dec. 31, 2020 | Sep. 30, 2020 | Jun. 30, 2020 | Mar. 31, 2020 | Dec. 31, 2020 | |||||||||||||||||||||||||

Average Sales Volume (1) | |||||||||||||||||||||||||||||

| CANADA | |||||||||||||||||||||||||||||

| Light Oil (bbl/d) | 13,947 | 17,396 | 18,165 | 23,115 | 18,143 | ||||||||||||||||||||||||

| Heavy Oil (bbl/d) | 19,553 | 19,676 | 9,555 | 25,710 | 18,629 | ||||||||||||||||||||||||

| Bitumen (bbl/d) | 2,172 | 2,462 | 2,277 | 3,144 | 2,513 | ||||||||||||||||||||||||

| Tight Oil (bbl/d) | 1,134 | 704 | 428 | 921 | 797 | ||||||||||||||||||||||||

NGL (bbl/d) (2) | 1,495 | 1,429 | 1,102 | 1,522 | 1,387 | ||||||||||||||||||||||||

| Total liquids (bbl/d) | 38,301 | 41,667 | 31,527 | 54,412 | 41,469 | ||||||||||||||||||||||||

| Shale Gas (Mcf/d) | 1,929 | 1,839 | 670 | 2,094 | 1,634 | ||||||||||||||||||||||||

| Natural Gas (Mcf/d) | 40,188 | 43,141 | 36,312 | 45,006 | 41,165 | ||||||||||||||||||||||||

| Total (boe/d) | 45,321 | 49,164 | 37,691 | 62,262 | 48,602 | ||||||||||||||||||||||||

| UNITED STATES | |||||||||||||||||||||||||||||

| Tight Oil (bbl/d) | 10,484 | 11,717 | 14,440 | 15,406 | 13,001 | ||||||||||||||||||||||||

NGL (bbl/d) (2) | 9,003 | 10,272 | 12,450 | 12,575 | 11,068 | ||||||||||||||||||||||||

| Total liquids (bbl/d) | 19,487 | 21,989 | 26,890 | 27,981 | 24,069 | ||||||||||||||||||||||||

| Shale Gas (Mcf/d) | 33,999 | 39,965 | 47,564 | 49,256 | 42,665 | ||||||||||||||||||||||||

| Total (boe/d) | 25,154 | 28,650 | 34,817 | 36,190 | 31,179 | ||||||||||||||||||||||||

| TOTAL | |||||||||||||||||||||||||||||

| Light Oil (bbl/d) | 13,947 | 17,396 | 18,165 | 23,115 | 18,143 | ||||||||||||||||||||||||

| Heavy Oil (bbl/d) | 19,553 | 19,676 | 9,555 | 25,710 | 18,629 | ||||||||||||||||||||||||

| Bitumen (bbl/d) | 2,172 | 2,462 | 2,277 | 3,144 | 2,513 | ||||||||||||||||||||||||

| Tight Oil (bbl/d) | 11,618 | 12,421 | 14,868 | 16,327 | 13,798 | ||||||||||||||||||||||||

NGL (bbl/d) (2) | 10,498 | 11,701 | 13,552 | 14,097 | 12,455 | ||||||||||||||||||||||||

| Total liquids (bbl/d) | 57,788 | 63,656 | 58,417 | 82,393 | 65,538 | ||||||||||||||||||||||||

| Shale Gas (Mcf/d) | 35,928 | 41,804 | 48,234 | 51,350 | 44,299 | ||||||||||||||||||||||||

| Natural Gas (Mcf/d) | 40,188 | 43,141 | 36,312 | 45,006 | 41,165 | ||||||||||||||||||||||||

| Total (boe/d) | 70,475 | 77,814 | 72,508 | 98,452 | 79,781 | ||||||||||||||||||||||||

| 16 | |||||||

| Three Months Ended | Year Ended | ||||||||||||||||||||||||||||

| Dec. 31, 2020 | Sep. 30, 2020 | Jun. 30, 2020 | Mar. 31, 2020 | Dec. 31, 2020 | |||||||||||||||||||||||||

| CANADA | |||||||||||||||||||||||||||||

Average Net Production Prices (3) | |||||||||||||||||||||||||||||

| Light Oil ($/bbl) | 47.16 | 46.70 | 24.01 | 49.18 | 41.93 | ||||||||||||||||||||||||

| Heavy Oil ($/bbl) | 26.94 | 28.24 | 16.92 | 20.64 | 23.85 | ||||||||||||||||||||||||

| Bitumen ($/bbl) | 36.22 | 35.31 | 18.49 | 21.64 | 27.47 | ||||||||||||||||||||||||

| Tight Oil ($/bbl) | 50.48 | 48.02 | 56.94 | 55.41 | 52.21 | ||||||||||||||||||||||||

NGL ($/bbl) (2) | 19.48 | 17.79 | 11.65 | 16.90 | 16.79 | ||||||||||||||||||||||||

| Shale Gas ($/Mcf) | 2.70 | 2.27 | 1.94 | 1.96 | 2.27 | ||||||||||||||||||||||||

| Natural Gas ($/Mcf) | 2.49 | 2.13 | 1.85 | 2.00 | 2.12 | ||||||||||||||||||||||||

| Total ($/boe) | 32.10 | 32.76 | 19.79 | 30.62 | 29.42 | ||||||||||||||||||||||||

| Royalties | |||||||||||||||||||||||||||||

Light Oil and NGL ($/bbl) (2)(4) | 3.92 | 3.15 | 1.90 | 3.39 | 3.07 | ||||||||||||||||||||||||

| Heavy Oil ($/bbl) | 2.51 | 2.91 | 2.07 | 2.91 | 2.70 | ||||||||||||||||||||||||

| Bitumen ($/bbl) | 3.13 | 3.45 | 1.69 | 1.85 | 2.49 | ||||||||||||||||||||||||

| Tight Oil ($/bbl) | 8.12 | 5.38 | 6.72 | 2.30 | 5.65 | ||||||||||||||||||||||||

| Shale Gas ($/Mcf) | 0.14 | 0.04 | 0.10 | 0.08 | 0.09 | ||||||||||||||||||||||||

| Natural Gas ($/Mcf) | 0.14 | 0.11 | 0.13 | 0.09 | 0.12 | ||||||||||||||||||||||||

| Total ($/boe) | 2.90 | 2.72 | 1.80 | 2.74 | 2.59 | ||||||||||||||||||||||||

Operating Expenses (5) | |||||||||||||||||||||||||||||

Light Oil and NGL ($/bbl) (2)(4) | 13.23 | 11.66 | 12.18 | 11.99 | 12.21 | ||||||||||||||||||||||||

| Heavy Oil ($/bbl) | 16.44 | 14.36 | 20.34 | 16.34 | 16.35 | ||||||||||||||||||||||||

| Bitumen ($/bbl) | 14.84 | 11.76 | 10.71 | 10.32 | 11.75 | ||||||||||||||||||||||||

| Tight Oil ($/bbl) | 9.43 | 8.50 | 10.76 | 11.23 | 9.89 | ||||||||||||||||||||||||

| Shale Gas ($/Mcf) | 1.57 | 1.42 | 1.79 | 1.87 | 1.65 | ||||||||||||||||||||||||

| Natural Gas ($/Mcf) | 2.38 | 1.99 | 2.23 | 2.34 | 2.23 | ||||||||||||||||||||||||

| Total ($/boe) | 14.73 | 12.73 | 14.33 | 13.93 | 13.89 | ||||||||||||||||||||||||

| Transportation Expenses | |||||||||||||||||||||||||||||

Light Oil and NGL ($/bbl) (2)(4) | 0.69 | 0.65 | 0.94 | 1.06 | 0.86 | ||||||||||||||||||||||||

| Heavy Oil ($/bbl) | 2.33 | 2.22 | 2.68 | 2.74 | 2.48 | ||||||||||||||||||||||||

| Bitumen ($/bbl) | 2.12 | 1.52 | 1.71 | 1.51 | 1.69 | ||||||||||||||||||||||||

| Tight Oil ($/bbl) | 1.18 | 1.07 | 1.31 | 1.18 | 1.17 | ||||||||||||||||||||||||

| Shale Gas ($/Mcf) | 0.20 | 0.18 | 0.22 | 0.20 | 0.19 | ||||||||||||||||||||||||

| Natural Gas ($/Mcf) | 0.25 | 0.20 | 0.19 | 0.24 | 0.22 | ||||||||||||||||||||||||

| Total ($/boe) | 1.60 | 1.41 | 1.47 | 1.83 | 1.60 | ||||||||||||||||||||||||

Netback Received (3)(6) | |||||||||||||||||||||||||||||

Light Oil and NGL ($/bbl) (2)(4) | 26.64 | 29.05 | 8.29 | 30.75 | 24.00 | ||||||||||||||||||||||||

| Heavy Oil ($/bbl) | 5.66 | 8.75 | (8.17) | (1.35) | 2.32 | ||||||||||||||||||||||||

| Bitumen ($/bbl) | 16.13 | 18.58 | 4.38 | 7.96 | 11.54 | ||||||||||||||||||||||||

| Tight Oil ($/bbl) | 31.75 | 33.07 | 38.15 | 40.70 | 35.50 | ||||||||||||||||||||||||

| Shale Gas ($/Mcf) | 0.79 | 0.63 | (0.17) | (0.19) | 0.34 | ||||||||||||||||||||||||

| Natural Gas ($/Mcf) | (0.28) | (0.17) | (0.70) | (0.67) | (0.45) | ||||||||||||||||||||||||

| Total ($/boe) | 12.87 | 15.90 | 2.19 | 12.12 | 11.34 | ||||||||||||||||||||||||

| 17 | |||||||

| Three Months Ended | Year Ended | ||||||||||||||||||||||||||||

| Dec. 31, 2020 | Sep. 30, 2020 | Jun. 30, 2020 | Mar. 31, 2020 | Dec. 31, 2020 | |||||||||||||||||||||||||

| UNITED STATES | |||||||||||||||||||||||||||||

Average Net Production Prices (3) | |||||||||||||||||||||||||||||

| Tight Oil ($/bbl) | 53.37 | 51.82 | 32.97 | 62.76 | 50.15 | ||||||||||||||||||||||||

NGL ($/bbl) (2) | 32.87 | 30.34 | 22.73 | 36.71 | 30.53 | ||||||||||||||||||||||||

| Shale Gas ($/Mcf) | 3.26 | 2.50 | 2.38 | 2.63 | 2.65 | ||||||||||||||||||||||||

| Total ($/boe) | 38.41 | 35.55 | 25.05 | 43.05 | 35.38 | ||||||||||||||||||||||||

| Royalties | |||||||||||||||||||||||||||||

| Tight Oil ($/bbl) | 16.75 | 16.48 | 10.53 | 19.47 | 15.77 | ||||||||||||||||||||||||

NGL ($/bbl) (2) | 8.42 | 7.85 | 5.78 | 9.51 | 7.86 | ||||||||||||||||||||||||

| Shale Gas ($/Mcf) | 0.83 | 0.70 | 0.60 | 0.68 | 0.69 | ||||||||||||||||||||||||

| Total ($/boe) | 11.11 | 10.53 | 7.26 | 12.51 | 10.31 | ||||||||||||||||||||||||

Operating Expenses (5)(7) | |||||||||||||||||||||||||||||

| Tight Oil ($/bbl) | 7.92 | 6.03 | 7.74 | 7.76 | 7.39 | ||||||||||||||||||||||||

NGL ($/bbl) (2) | 7.92 | 6.03 | 7.74 | 7.76 | 7.39 | ||||||||||||||||||||||||

| Shale Gas ($/Mcf) | 1.32 | 1.00 | 1.29 | 1.29 | 1.23 | ||||||||||||||||||||||||

| Total ($/boe) | 7.92 | 6.03 | 7.74 | 7.76 | 7.39 | ||||||||||||||||||||||||

Netback Received (3)(6) | |||||||||||||||||||||||||||||

| Tight Oil ($/bbl) | 28.70 | 29.31 | 14.70 | 35.53 | 26.99 | ||||||||||||||||||||||||

NGL ($/bbl) (2) | 16.53 | 16.46 | 9.21 | 19.44 | 15.28 | ||||||||||||||||||||||||

| Shale Gas ($/Mcf) | 1.11 | 0.80 | 0.49 | 0.66 | 0.73 | ||||||||||||||||||||||||

| Total ($/boe) | 19.38 | 18.99 | 10.05 | 22.78 | 17.68 | ||||||||||||||||||||||||

Notes:

(1)Before deduction of royalties.

(2)NGL includes condensate.

(3)Before the effects of commodity derivative instruments.

(4)In Canada, NGL volumes are grouped with light oil volumes for reporting purposes.

(5)Operating expenses are composed of direct costs incurred to operate both oil and gas wells. A number of assumptions are required to allocate these costs between oil, natural gas and NGL production.

(6)Netback is calculated by subtracting royalties, operating and transportation expenses from revenues.

(7)In the U.S., transportation expense is included in operating expenses for reporting purposes.

| 18 | |||||||

Marketing Arrangements and Forward Contracts

In Canada, we market our oil and natural gas production with attention to maximizing value and counterparty performance. We have a portfolio of sales contracts with a variety of pricing mechanisms, term commitments and customers. For our heavy oil volumes, this includes rail commitments. In the United States, production from our assets is marketed by the operator.

The Corporation also has a risk management policy pursuant to which we utilize various derivative financial instruments and physical sales contracts to manage our exposure to fluctuations in commodity prices, foreign exchange and interest rates. We also use derivative instruments in various operational markets to optimize our supply or production chain.

When marketing and hedging we engage a number of reputable counterparties to ensure competitiveness, while also managing counterparty credit exposure. For details on our contractual commitments to sell natural gas and crude oil which were outstanding at February 24, 2021, see Note 18 to our audited consolidated financial statements for the year ended December 31, 2020. See Risk Factors.

STATEMENT OF RESERVES DATA

The Baytex Reserves Report has been prepared in accordance with the standards contained in the COGE Handbook and the reserves definitions contained in NI 51‑101. The statement of reserves data and other oil and natural gas information set forth below is dated December 31, 2020. The effective date of the Baytex Reserves Report is December 31, 2020 and the preparation date of the statement is February 4, 2021. The Baytex Reserves Report was prepared using the average commodity price forecasts and inflation rates of McDaniel, GLJ Petroleum Consultants Ltd. and Sproule Associates Limited as of January 1, 2021.

Disclosure of Reserves Data

The tables below are a combined summary as at December 31, 2020 of our proved and probable heavy oil, bitumen, light and medium oil, tight oil, NGL, conventional natural gas and shale gas reserves and the net present value of the future net revenue attributable to such reserves evaluated in the Baytex Reserves Report. Our reserves are located in Canada (Alberta and Saskatchewan) and the United States (Texas).

All evaluations of future net revenue are after the deduction of future income tax expenses (unless otherwise noted in the tables), royalties, development costs, production costs and well abandonment costs but before consideration of indirect costs such as administrative, overhead and other miscellaneous expenses. The estimated future net revenue contained in the following tables does not necessarily represent the fair market value of our reserves. There is no assurance that the forecast price and cost assumptions contained in the Baytex Reserves Report will be attained and variations could be material. The tables summarize the data contained in the Baytex Reserves Report and, as a result, may contain slightly different numbers and columns in the tables may not add due to rounding. Other assumptions and qualifications relating to costs and other matters are summarized in the notes to or following the tables below.

The recovery and reserves estimates described herein are estimates only and there is no guarantee that the estimated reserves will be recovered. Readers should review the definitions and information contained in "Selected Terms - Reserves Definitions", "- Reserves and Reserve Categories" and "- Development and Production Status" in conjunction with the following tables and notes. For more information as to the risks involved, see "Risk Factors".

| 19 | |||||||

| SUMMARY OF OIL AND NATURAL GAS RESERVES AS OF DECEMBER 31, 2020 FORECAST PRICES AND COSTS | ||||||||||||||||||||||||||||||||||||||

| CANADA | ||||||||||||||||||||||||||||||||||||||

| TIGHT OIL | LIGHT AND MEDIUM OIL | HEAVY OIL | ||||||||||||||||||||||||||||||||||||

| RESERVES CATEGORY | Gross (Mbbl) | Net (Mbbl) | Gross (Mbbl) | Net (Mbbl) | Gross (Mbbl) | Net (Mbbl) | ||||||||||||||||||||||||||||||||

| PROVED: | ||||||||||||||||||||||||||||||||||||||

| Developed Producing | 1,268 | 1,154 | 20,404 | 19,106 | 19,917 | 18,404 | ||||||||||||||||||||||||||||||||

| Developed Non‑Producing | — | — | 61 | 59 | 1,997 | 1,895 | ||||||||||||||||||||||||||||||||

| Undeveloped | 3,112 | 2,810 | 31,601 | 29,630 | 13,499 | 12,385 | ||||||||||||||||||||||||||||||||

| TOTAL PROVED | 4,380 | 3,963 | 52,067 | 48,795 | 35,412 | 32,684 | ||||||||||||||||||||||||||||||||

| PROBABLE | 4,748 | 4,188 | 25,688 | 23,461 | 30,544 | 27,640 | ||||||||||||||||||||||||||||||||

| TOTAL PROVED PLUS PROBABLE | 9,128 | 8,151 | 77,755 | 72,256 | 65,956 | 60,324 | ||||||||||||||||||||||||||||||||

| CANADA | ||||||||||||||||||||||||||||||||||||||

| BITUMEN | SHALE GAS | CONVENTIONAL NATURAL GAS (1) | ||||||||||||||||||||||||||||||||||||

| RESERVES CATEGORY | Gross (Mbbl) | Net (Mbbl) | Gross (MMcf) | Net (MMcf) | Gross (MMcf) | Net (MMcf) | ||||||||||||||||||||||||||||||||

| PROVED: | ||||||||||||||||||||||||||||||||||||||

| Developed Producing | 1,144 | 1,027 | 3,041 | 2,790 | 43,384 | 40,568 | ||||||||||||||||||||||||||||||||

| Developed Non‑Producing | 160 | 152 | — | — | 15,072 | 13,080 | ||||||||||||||||||||||||||||||||

| Undeveloped | 4,433 | 4,213 | 6,203 | 5,754 | 29,438 | 26,071 | ||||||||||||||||||||||||||||||||

| TOTAL PROVED | 5,737 | 5,393 | 9,244 | 8,544 | 87,894 | 79,720 | ||||||||||||||||||||||||||||||||

| PROBABLE | 46,093 | 40,064 | 9,497 | 8,825 | 86,778 | 80,679 | ||||||||||||||||||||||||||||||||

| TOTAL PROVED PLUS PROBABLE | 51,830 | 45,456 | 18,741 | 17,369 | 174,671 | 160,398 | ||||||||||||||||||||||||||||||||

| CANADA | ||||||||||||||||||||||||||||||||||||||

NATURAL GAS LIQUIDS (2) | TOTAL RESERVES | |||||||||||||||||||||||||||||||||||||

| RESERVES CATEGORY | Gross (Mbbl) | Net (Mbbl) | Gross (Mboe) | Net (Mboe) | ||||||||||||||||||||||||||||||||||

| PROVED: | ||||||||||||||||||||||||||||||||||||||

| Developed Producing | 1,739 | 1,515 | 52,210 | 48,432 | ||||||||||||||||||||||||||||||||||

| Developed Non‑Producing | 485 | 389 | 5,214 | 4,676 | ||||||||||||||||||||||||||||||||||

| Undeveloped | 2,244 | 1,992 | 60,829 | 56,334 | ||||||||||||||||||||||||||||||||||

| TOTAL PROVED | 4,468 | 3,896 | 118,254 | 109,442 | ||||||||||||||||||||||||||||||||||

| PROBABLE | 4,841 | 4,309 | 127,959 | 114,578 | ||||||||||||||||||||||||||||||||||

| TOTAL PROVED PLUS PROBABLE | 9,309 | 8,205 | 246,212 | 224,020 | ||||||||||||||||||||||||||||||||||

| 20 | |||||||

| UNITED STATES | ||||||||||||||||||||||||||||||||||||||

| TIGHT OIL | SHALE GAS | NATURAL GAS LIQUIDS (2) | ||||||||||||||||||||||||||||||||||||

| RESERVES CATEGORY | Gross (Mbbl) | Net (Mbbl) | Gross (MMcf) | Net (MMcf) | Gross (Mbbl) | Net (Mbbl) | ||||||||||||||||||||||||||||||||

| PROVED: | ||||||||||||||||||||||||||||||||||||||

| Developed Producing | 22,204 | 16,292 | 94,280 | 69,651 | 29,930 | 22,120 | ||||||||||||||||||||||||||||||||

| Developed Non‑Producing | 38 | 28 | 473 | 350 | 154 | 114 | ||||||||||||||||||||||||||||||||

| Undeveloped | 26,694 | 19,561 | 122,338 | 89,885 | 37,923 | 27,873 | ||||||||||||||||||||||||||||||||

| TOTAL PROVED | 48,936 | 35,881 | 217,090 | 159,886 | 68,007 | 50,107 | ||||||||||||||||||||||||||||||||

| PROBABLE | 19,894 | 14,589 | 87,355 | 64,235 | 27,920 | 20,544 | ||||||||||||||||||||||||||||||||

| TOTAL PROVED PLUS PROBABLE | 68,830 | 50,470 | 304,445 | 224,121 | 95,927 | 70,651 | ||||||||||||||||||||||||||||||||

| UNITED STATES | ||||||||||||||||||||||||||||||||||||||

| TOTAL RESERVES | ||||||||||||||||||||||||||||||||||||||

| RESERVES CATEGORY | Gross (Mboe) | Net (Mboe) | ||||||||||||||||||||||||||||||||||||

| PROVED: | ||||||||||||||||||||||||||||||||||||||

| Developed Producing | 67,847 | 50,020 | ||||||||||||||||||||||||||||||||||||

| Developed Non‑Producing | 271 | 201 | ||||||||||||||||||||||||||||||||||||

| Undeveloped | 85,006 | 62,414 | ||||||||||||||||||||||||||||||||||||

| TOTAL PROVED | 153,125 | 112,636 | ||||||||||||||||||||||||||||||||||||

| PROBABLE | 62,373 | 45,839 | ||||||||||||||||||||||||||||||||||||

| TOTAL PROVED PLUS PROBABLE | 215,497 | 158,475 | ||||||||||||||||||||||||||||||||||||

| TOTAL | ||||||||||||||||||||||||||||||||||||||

| TIGHT OIL | LIGHT AND MEDIUM OIL | HEAVY OIL | ||||||||||||||||||||||||||||||||||||

| RESERVES CATEGORY | Gross (Mbbl) | Net (Mbbl) | Gross (Mbbl) | Net (Mbbl) | Gross (Mbbl) | Net (Mbbl) | ||||||||||||||||||||||||||||||||

| PROVED: | ||||||||||||||||||||||||||||||||||||||

| Developed Producing | 23,473 | 17,445 | 20,404 | 19,106 | 19,917 | 18,404 | ||||||||||||||||||||||||||||||||

| Developed Non‑Producing | 38 | 28 | 61 | 59 | 1,997 | 1,895 | ||||||||||||||||||||||||||||||||

| Undeveloped | 29,805 | 22,371 | 31,601 | 29,630 | 13,499 | 12,385 | ||||||||||||||||||||||||||||||||

| TOTAL PROVED | 53,316 | 39,844 | 52,067 | 48,795 | 35,412 | 32,684 | ||||||||||||||||||||||||||||||||

| PROBABLE | 24,642 | 18,777 | 25,688 | 23,461 | 30,544 | 27,640 | ||||||||||||||||||||||||||||||||

| TOTAL PROVED PLUS PROBABLE | 77,958 | 58,621 | 77,755 | 72,256 | 65,956 | 60,324 | ||||||||||||||||||||||||||||||||

| 21 | |||||||

| TOTAL | ||||||||||||||||||||||||||||||||||||||

| BITUMEN | SHALE GAS | CONVENTIONAL NATURAL GAS (1) | ||||||||||||||||||||||||||||||||||||

| RESERVES CATEGORY | Gross (Mbbl) | Net (Mbbl) | Gross (MMcf) | Net (MMcf) | Gross (MMcf) | Net (MMcf) | ||||||||||||||||||||||||||||||||

| PROVED: | ||||||||||||||||||||||||||||||||||||||

| Developed Producing | 1,144 | 1,027 | 97,321 | 72,440 | 43,384 | 40,568 | ||||||||||||||||||||||||||||||||

| Developed Non‑Producing | 160 | 152 | 473 | 350 | 15,072 | 13,080 | ||||||||||||||||||||||||||||||||

| Undeveloped | 4,433 | 4,213 | 128,541 | 95,639 | 29,438 | 26,071 | ||||||||||||||||||||||||||||||||

| TOTAL PROVED | 5,737 | 5,393 | 226,334 | 168,429 | 87,894 | 79,720 | ||||||||||||||||||||||||||||||||

| PROBABLE | 46,093 | 40,064 | 96,852 | 73,061 | 86,778 | 80,679 | ||||||||||||||||||||||||||||||||

| TOTAL PROVED PLUS PROBABLE | 51,830 | 45,456 | 323,186 | 241,490 | 174,671 | 160,398 | ||||||||||||||||||||||||||||||||

| TOTAL | ||||||||||||||||||||||||||||||||||||||

NATURAL GAS LIQUIDS (2) | TOTAL RESERVES | |||||||||||||||||||||||||||||||||||||

| RESERVES CATEGORY | Gross (Mbbl) | Net (Mbbl) | Gross (Mboe) | Net (Mboe) | ||||||||||||||||||||||||||||||||||

| PROVED: | ||||||||||||||||||||||||||||||||||||||

| Developed Producing | 31,669 | 23,635 | 120,057 | 98,452 | ||||||||||||||||||||||||||||||||||

| Developed Non‑Producing | 639 | 504 | 5,485 | 4,877 | ||||||||||||||||||||||||||||||||||

| Undeveloped | 40,167 | 29,865 | 145,835 | 118,748 | ||||||||||||||||||||||||||||||||||

| TOTAL PROVED | 72,475 | 54,003 | 271,378 | 222,077 | ||||||||||||||||||||||||||||||||||

| PROBABLE | 32,760 | 24,853 | 190,332 | 160,417 | ||||||||||||||||||||||||||||||||||

| TOTAL PROVED PLUS PROBABLE | 105,235 | 78,856 | 461,710 | 382,495 | ||||||||||||||||||||||||||||||||||

Notes:

(1)Conventional natural gas includes associated, non-associated and solution gas.

(2)Natural gas liquids includes condensate.

| 22 | |||||||

| SUMMARY OF NET PRESENT VALUES OF FUTURE NET REVENUE AS OF DECEMBER 31, 2020 FORECAST PRICES AND COSTS | ||||||||||||||||||||||||||||||||||||||

| CANADA | BEFORE INCOME TAXES DISCOUNTED AT (%/year) | UNIT VALUE BEFORE TAX | ||||||||||||||||||||||||||||||||||||

| RESERVES CATEGORY | 0% ($000s) | 5% ($000s) | 10% ($000s) | 15% ($000s) | 20% ($000s) | 10% $/boe | ||||||||||||||||||||||||||||||||

| PROVED: | ||||||||||||||||||||||||||||||||||||||

| Developed Producing | (212,944) | 225,006 | 347,308 | 377,104 | 376,315 | 7.17 | ||||||||||||||||||||||||||||||||

| Developed Non‑Producing | 63,367 | 54,775 | 48,227 | 43,104 | 38,998 | 10.31 | ||||||||||||||||||||||||||||||||

| Undeveloped | 772,595 | 504,623 | 322,020 | 198,702 | 114,400 | 5.72 | ||||||||||||||||||||||||||||||||

| TOTAL PROVED | 623,019 | 784,404 | 717,555 | 618,910 | 529,712 | 6.56 | ||||||||||||||||||||||||||||||||

| PROBABLE | 2,063,798 | 1,193,123 | 771,076 | 538,642 | 398,195 | 6.73 | ||||||||||||||||||||||||||||||||

| TOTAL PROVED PLUS PROBABLE | 2,686,817 | 1,977,527 | 1,488,630 | 1,157,552 | 927,907 | 6.65 | ||||||||||||||||||||||||||||||||

| UNITED STATES | BEFORE INCOME TAXES DISCOUNTED AT (%/year) | UNIT VALUE BEFORE TAX | ||||||||||||||||||||||||||||||||||||

| RESERVES CATEGORY | 0% ($000s) | 5% ($000s) | 10% ($000s) | 15% ($000s) | 20% ($000s) | 10% $/boe | ||||||||||||||||||||||||||||||||

| PROVED: | ||||||||||||||||||||||||||||||||||||||

| Developed Producing | 1,302,148 | 977,768 | 770,723 | 640,474 | 552,298 | 15.41 | ||||||||||||||||||||||||||||||||

| Developed Non‑Producing | 5,416 | 3,925 | 3,062 | 2,512 | 2,134 | 15.23 | ||||||||||||||||||||||||||||||||

| Undeveloped | 1,448,365 | 938,293 | 649,814 | 472,772 | 356,197 | 10.41 | ||||||||||||||||||||||||||||||||

| TOTAL PROVED | 2,755,929 | 1,919,986 | 1,423,599 | 1,115,758 | 910,629 | 12.64 | ||||||||||||||||||||||||||||||||

| PROBABLE | 1,310,312 | 643,996 | 366,587 | 231,987 | 158,347 | 8.00 | ||||||||||||||||||||||||||||||||

| TOTAL PROVED PLUS PROBABLE | 4,066,241 | 2,563,981 | 1,790,186 | 1,347,746 | 1,068,976 | 11.30 | ||||||||||||||||||||||||||||||||

| TOTAL | BEFORE INCOME TAXES DISCOUNTED AT (%/year) | UNIT VALUE BEFORE TAX | ||||||||||||||||||||||||||||||||||||

| RESERVES CATEGORY | 0% ($000s) | 5% ($000s) | 10% ($000s) | 15% ($000s) | 20% ($000s) | 10% $/boe | ||||||||||||||||||||||||||||||||

| PROVED: | ||||||||||||||||||||||||||||||||||||||

| Developed Producing | 1,089,204 | 1,202,774 | 1,118,031 | 1,017,579 | 928,612 | 11.36 | ||||||||||||||||||||||||||||||||

| Developed Non‑Producing | 68,783 | 58,700 | 51,289 | 45,616 | 41,132 | 10.52 | ||||||||||||||||||||||||||||||||

| Undeveloped | 2,220,960 | 1,442,916 | 971,834 | 671,474 | 470,597 | 8.18 | ||||||||||||||||||||||||||||||||

| TOTAL PROVED | 3,378,948 | 2,704,390 | 2,141,154 | 1,734,669 | 1,440,342 | 9.64 | ||||||||||||||||||||||||||||||||

| PROBABLE | 3,374,110 | 1,837,118 | 1,137,663 | 770,629 | 556,542 | 7.09 | ||||||||||||||||||||||||||||||||

| TOTAL PROVED PLUS PROBABLE | 6,753,057 | 4,541,509 | 3,278,817 | 2,505,298 | 1,996,884 | 8.57 | ||||||||||||||||||||||||||||||||

| 23 | |||||||

| SUMMARY OF NET PRESENT VALUES OF FUTURE NET REVENUE AS OF DECEMBER 31, 2020 FORECAST PRICES AND COSTS | ||||||||||||||||||||||||||||||||

| CANADA | AFTER INCOME TAXES DISCOUNTED AT (%/year)(1) | |||||||||||||||||||||||||||||||

| RESERVES CATEGORY | 0% ($000s) | 5% ($000s) | 10% ($000s) | 15% ($000s) | 20% ($000s) | |||||||||||||||||||||||||||

| PROVED: | ||||||||||||||||||||||||||||||||

| Developed Producing | (212,944) | 225,006 | 347,308 | 377,104 | 376,315 | |||||||||||||||||||||||||||

| Developed Non‑Producing | 63,367 | 54,775 | 48,227 | 43,104 | 38,998 | |||||||||||||||||||||||||||

| Undeveloped | 772,595 | 504,623 | 322,020 | 198,702 | 114,400 | |||||||||||||||||||||||||||

| TOTAL PROVED | 623,019 | 784,404 | 717,555 | 618,910 | 529,712 | |||||||||||||||||||||||||||

| PROBABLE | 1,933,722 | 1,115,340 | 722,951 | 507,973 | 378,137 | |||||||||||||||||||||||||||

| TOTAL PROVED PLUS PROBABLE | 2,556,741 | 1,899,744 | 1,440,506 | 1,126,884 | 907,849 | |||||||||||||||||||||||||||

| UNITED STATES | AFTER INCOME TAXES DISCOUNTED AT (%/year)(1) | |||||||||||||||||||||||||||||||

| RESERVES CATEGORY | 0% ($000s) | 5% ($000s) | 10% ($000s) | 15% ($000s) | 20% ($000s) | |||||||||||||||||||||||||||

| PROVED: | ||||||||||||||||||||||||||||||||

| Developed Producing | 1,271,733 | 965,689 | 764,223 | 635,897 | 548,406 | |||||||||||||||||||||||||||

| Developed Non‑Producing | 5,050 | 3,802 | 3,011 | 2,485 | 2,117 | |||||||||||||||||||||||||||

| Undeveloped | 1,192,125 | 800,643 | 570,465 | 424,685 | 326,074 | |||||||||||||||||||||||||||

| TOTAL PROVED | 2,468,908 | 1,770,134 | 1,337,699 | 1,063,067 | 876,596 | |||||||||||||||||||||||||||

| PROBABLE | 1,025,337 | 503,878 | 287,133 | 182,589 | 125,724 | |||||||||||||||||||||||||||

| TOTAL PROVED PLUS PROBABLE | 3,494,246 | 2,274,012 | 1,624,832 | 1,245,655 | 1,002,321 | |||||||||||||||||||||||||||

| TOTAL | AFTER INCOME TAXES DISCOUNTED AT (%/year)(1) | |||||||||||||||||||||||||||||||

| RESERVES CATEGORY | 0% ($000s) | 5% ($000s) | 10% ($000s) | 15% ($000s) | 20% ($000s) | |||||||||||||||||||||||||||

| PROVED: | ||||||||||||||||||||||||||||||||

| Developed Producing | 1,058,789 | 1,190,696 | 1,111,530 | 1,013,001 | 924,720 | |||||||||||||||||||||||||||

| Developed Non‑Producing | 68,417 | 58,577 | 51,238 | 45,589 | 41,114 | |||||||||||||||||||||||||||

| Undeveloped | 1,964,720 | 1,305,266 | 892,485 | 623,387 | 440,474 | |||||||||||||||||||||||||||

| TOTAL PROVED | 3,091,927 | 2,554,539 | 2,055,253 | 1,681,977 | 1,406,309 | |||||||||||||||||||||||||||

| PROBABLE | 2,959,059 | 1,619,217 | 1,010,084 | 690,562 | 503,861 | |||||||||||||||||||||||||||

| TOTAL PROVED PLUS PROBABLE | 6,050,986 | 4,173,756 | 3,065,338 | 2,372,539 | 1,910,170 | |||||||||||||||||||||||||||

Note:

(1)The after-tax net present value of future net revenue from our oil and gas properties reflects the tax burden on the properties on a theoretical stand-alone basis. It does not consider our corporate structure or any tax planning and therefore does not provide an estimate of the cumulative after-tax value of our consolidated business entities, which may be significantly different.

| 24 | |||||||

| TOTAL FUTURE NET REVENUE (UNDISCOUNTED) AS OF DECEMBER 31, 2020 FORECAST PRICES AND COSTS | |||||||||||||||||||||||||||||||||||||||||||||||

| ($000s) | REVENUE | ROYALTIES | OPERAT-ING COSTS | DEVELOP-MENT COSTS | WELL ABANDON-MENT COSTS(1) | FUTURE NET REVENUE BEFORE INCOME TAXES | INCOME TAXES | FUTURE NET REVENUE AFTER INCOME TAXES | |||||||||||||||||||||||||||||||||||||||

| TOTAL PROVED RESERVES | |||||||||||||||||||||||||||||||||||||||||||||||

| Canada | 5,567,569 | 455,145 | 2,144,427 | 1,299,523 | 1,045,456 | 623,019 | — | 623,019 | |||||||||||||||||||||||||||||||||||||||

| United States | 8,479,630 | 2,632,828 | 2,174,258 | 794,061 | 122,555 | 2,755,929 | 287,021 | 2,468,908 | |||||||||||||||||||||||||||||||||||||||

| Total | 14,047,199 | 3,087,972 | 4,318,684 | 2,093,584 | 1,168,011 | 3,378,948 | 287,021 | 3,091,927 | |||||||||||||||||||||||||||||||||||||||

| TOTAL PROVED PLUS PROBABLE RESERVES | |||||||||||||||||||||||||||||||||||||||||||||||

| Canada | 11,956,297 | 1,194,711 | 4,551,586 | 2,412,068 | 1,111,116 | 2,686,817 | 130,076 | 2,556,741 | |||||||||||||||||||||||||||||||||||||||

| United States | 12,670,305 | 3,938,602 | 3,327,708 | 1,193,818 | 143,936 | 4,066,241 | 571,995 | 3,494,246 | |||||||||||||||||||||||||||||||||||||||

| Total | 24,626,602 | 5,133,313 | 7,879,294 | 3,605,886 | 1,255,052 | 6,753,057 | 702,071 | 6,050,986 | |||||||||||||||||||||||||||||||||||||||

Note:

(1)Includes well abandonment, decommissioning and reclamation costs for all producing and non-producing wells and facilities and to be incurred as a result of future development activity.

| FUTURE NET REVENUE BY PRODUCT TYPE AS OF DECEMBER 31, 2020 FORECAST PRICES AND COSTS | |||||||||||

| RESERVES CATEGORY | PRODUCT TYPE | FUTURE NET REVENUE BEFORE INCOME TAXES (discounted at 10%/year) ($000s) | UNIT VALUE (1) ($/bbl; $/Mcf) | ||||||||

| Proved | Light and Medium Crude Oil (including solution gas and associated byproducts) | 536,996 | 11.01 | ||||||||

| Heavy Crude Oil (including solution gas and associated byproducts) | 73,802 | 2.26 | |||||||||

| Bitumen (including solution gas and associated byproducts) | 37,270 | 6.91 | |||||||||

| Tight Oil (including solution gas and associated byproducts) | 914,305 | 22.95 | |||||||||

| Natural Gas (associated and non-associated) (including associated byproducts) | 34,057 | 0.84 | |||||||||

| Shale Gas (including associated byproducts) | 544,724 | 4.89 | |||||||||

| Total | 2,141,154 | ||||||||||

| Proved plus Probable | Light and Medium Crude Oil (including solution gas and associated byproducts) | 971,298 | 13.44 | ||||||||

| Heavy Crude Oil (including solution gas and associated byproducts) | 247,365 | 4.10 | |||||||||

| Bitumen (including solution gas and associated byproducts) | 132,290 | 2.91 | |||||||||

| Tight Oil (including solution gas and associated byproducts) | 1,184,743 | 20.21 | |||||||||

| Natural Gas (associated and non-associated) (including associated byproducts) | 53,856 | 0.58 | |||||||||

| Shale Gas (including associated byproducts) | 689,264 | 4.45 | |||||||||

| Total | 3,278,817 | ||||||||||

Note:

(1)Unit values are based on major product type net reserves volumes.

| 25 | |||||||

Pricing Assumptions

The forecast cost and price assumptions include increases in actual wellhead selling prices and take into account inflation with respect to future operating and capital costs. The reference pricing used in the Baytex Reserves Report is as follows:

SUMMARY OF PRICING AND INFLATION RATE ASSUMPTIONS FORECAST PRICES AND COSTS AS AT DECEMBER 31, 2020 (1) | ||||||||||||||||||||||||||||||||||||||||||||

| Year | Oil | Natural Gas | Inflation Rate (7) (%/Yr) | Exchange Rate (8) ($US/$Cdn) | ||||||||||||||||||||||||||||||||||||||||

WTI Crude Oil (2) ($US/bbl) | Edmonton Light Crude Oil (3) ($Cdn/bbl) | Western Canadian Select(4) ($Cdn/bbl) | Henry Hub (5) ($US/MMbtu) | AECO Spot (6) ($Cdn/MMbtu) | ||||||||||||||||||||||||||||||||||||||||

| Historical | ||||||||||||||||||||||||||||||||||||||||||||

| 2016 | 43.30 | 53.90 | 39.15 | 2.50 | 2.10 | 1.4 | 0.755 | |||||||||||||||||||||||||||||||||||||

| 2017 | 50.90 | 62.85 | 50.70 | 3.00 | 2.40 | 1.6 | 0.770 | |||||||||||||||||||||||||||||||||||||

| 2018 | 64.95 | 69.65 | 49.95 | 3.05 | 1.55 | 2.2 | 0.770 | |||||||||||||||||||||||||||||||||||||

| 2019 | 57.00 | 69.00 | 58.70 | 2.55 | 1.60 | 2.0 | 0.755 | |||||||||||||||||||||||||||||||||||||

| 2020 | 39.20 | 45.00 | 35.35 | 2.05 | 2.25 | 0.2 | 0.745 | |||||||||||||||||||||||||||||||||||||

Forecast (9) | ||||||||||||||||||||||||||||||||||||||||||||

| 2021 | 47.17 | 55.76 | 44.63 | 2.83 | 2.78 | — | 0.768 | |||||||||||||||||||||||||||||||||||||

| 2022 | 50.17 | 59.89 | 48.18 | 2.87 | 2.70 | 1.3 | 0.765 | |||||||||||||||||||||||||||||||||||||

| 2023 | 53.17 | 63.48 | 52.10 | 2.90 | 2.61 | 2.0 | 0.763 | |||||||||||||||||||||||||||||||||||||

| 2024 | 54.97 | 65.76 | 54.10 | 2.96 | 2.65 | 2.0 | 0.763 | |||||||||||||||||||||||||||||||||||||

| 2025 | 56.07 | 67.13 | 55.19 | 3.02 | 2.70 | 2.0 | 0.763 | |||||||||||||||||||||||||||||||||||||

| 2026 | 57.19 | 68.53 | 56.29 | 3.08 | 2.76 | 2.0 | 0.763 | |||||||||||||||||||||||||||||||||||||

| 2027 | 58.34 | 69.95 | 57.42 | 3.14 | 2.81 | 2.0 | 0.763 | |||||||||||||||||||||||||||||||||||||

| 2028 | 59.50 | 71.40 | 58.57 | 3.20 | 2.87 | 2.0 | 0.763 | |||||||||||||||||||||||||||||||||||||

| 2029 | 60.69 | 72.88 | 59.74 | 3.26 | 2.92 | 2.0 | 0.763 | |||||||||||||||||||||||||||||||||||||

| 2030 | 61.91 | 74.34 | 60.93 | 3.33 | 2.98 | 2.0 | 0.763 | |||||||||||||||||||||||||||||||||||||

Notes:

(1)Each price from the forecast was adjusted for quality differentials and transportation costs applicable to the specified product and evaluation area.