Annual Stockholders Meeting April 16, 2009 Please turn off cell phones and other electronic devices. Exhibit 99.1 |

April 16, 2009 FORWARD LOOKING STATEMENTS The information contained in this presentation may include forward-looking statements which reflect Regions' current views with respect to future events and financial performance. The Private Securities Litigation Reform Act of 1995 ("the Act") provides a safe harbor for forward-looking statements which are identified as such and are accompanied by the identification of important factors that could cause actual results to differ materially from the forward-looking statements. For these statements, we, together with our subsidiaries, unless the context implies otherwise, claim the protection afforded by the safe harbor in the Act. Forward-looking statements are not based on historical information, but rather are related to future operations, strategies, financial results, or other developments. Forward-looking statements are based on management's expectations as well as certain assumptions and estimates made by, and information available to, management at the time the statements are made. Those statements are based on general assumptions and are subject to various risks, uncertainties, and other factors that may cause actual results to differ materially from the views, beliefs, and projections expressed in such statements. These risks, uncertainties and other factors include, but are not limited to, those described below: Regions' ability to achieve the earnings expectations related to businesses that have been acquired or that may be acquired in the future. Regions' ability to expand into new markets and to maintain profit margins in the face of competitive pressures. Regions’ ability to keep pace with technological changes. Regions’ ability to manage fluctuations in the value of assets and liabilities and off-balance sheet exposure so as to maintain sufficient capital and liquidity to support Regions’ business Regions' ability to develop competitive new products and services in a timely manner and the acceptance of such products and services by Regions' customers and potential customers. Regions' ability to effectively manage credit risk, interest rate risk, market risk, operational risk, legal risk, liquidity risk, and regulatory and compliance risk. The current stresses in the financial and real estate markets, including possible continued deterioration in property values The cost and other effects of material contingencies, including litigation contingencies. The effects of increased competition from both banks and non-banks. Possible changes in interest rates may increase funding costs and reduce earning asset yields, thus reducing margins. Possible changes in general economic and business conditions in the United States in general and in the communities Regions serves in particular. Possible changes in the creditworthiness of customers and the possible impairment of collectibility of loans. The effects of geopolitical instability and risks such as terrorist attacks. Possible changes in trade, monetary and fiscal policies, laws, and regulations, and other activities of governments, agencies, and similar organizations, including changes in accounting standards, may have an adverse effect on business. Possible changes in consumer and business spending and saving habits could affect Regions' ability to increase assets and to attract deposits. The effects of weather and natural disasters such as droughts and hurricanes. In October of 2008, Congress enacted, and the President signed into law, the Emergency Economic Stabilization Act of 2008 and on February 17, 2009 the American Recovery and Reinvestment Act of 2009 was signed into law. Additionally, the U.S. Treasury and federal banking regulators are implementing a number of programs to address capital and liquidity issues in the banking system, all of which may have significant effects on Regions and the financial services industry, the exact nature of which cannot be determined at this time. The foregoing list of factors is not exhaustive; for discussion of these and other risks that may cause actual results to differ from expectations, please look under the caption “Forward-Looking Statements” in Regions’ Annual Report on Form 10-K for the year ended December 31, 2008, as on file with the Securities and Exchange Commission. The words "believe," "expect," "anticipate," "project," and similar expressions often signify forward-looking statements. You should not place undue reliance on any forward-looking statements, which speak only as of the date made. Regions assumes no obligation to update or revise any forward-looking statements that are made from time to time. |

April 16, 2009 Company Profile Industry Overview Strength and Stability Business Performance Fact vs. Fiction |

April 16, 2009 Source: Based on June 30, 2008 FDIC Data obtained from SNL State Dep. ($B) Mkt. Share Rank AL $17.2 23% #1 TN 16.3 16 #1 FL 14.3 4 #4 MS 9.7 21 #1 LA 7.2 10 #3 GA 6.1 3 #6 AR 4.2 9 #2 TX 3.0 1 #17 IL 2.4 1 #24 MO 2.2 2 #9 IN 2.1 2 #9 Other 2.5 — — Regions Morgan Keegan Insurance Strong Southeastern Franchise |

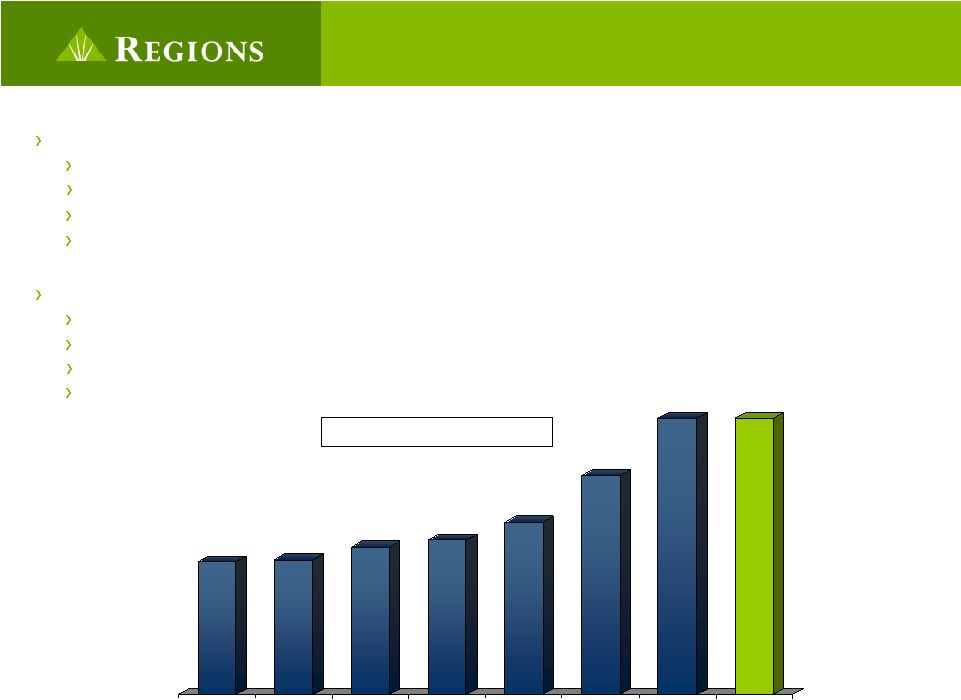

April 16, 2009 Revenue ($ in millions) $624 $634 $694 $727 $810 $1,029 $1,300 $1,300 2001 2002 2003 2004 2005 2006 2007 2008 Profile Over 1,100 financial advisors operating from over 330 offices More than $63 billion in customer assets under management Over $62 billion in trust assets under management Expanded investment banking capabilities in 2008 through acquisitions of Revolution Partners and Burke Capital Group Recognition 10th largest municipal bond underwriter in the nation in 2008 Top underwriter of municipal bonds in the South Central U.S. for 16 consecutive years Focus List of stocks ranked #1 for 5 year performance (2004-2008) Ranked #1 underwriter of municipal bonds in the Southeast Morgan Keegan is among the 15 largest broker/dealer firms in the US |

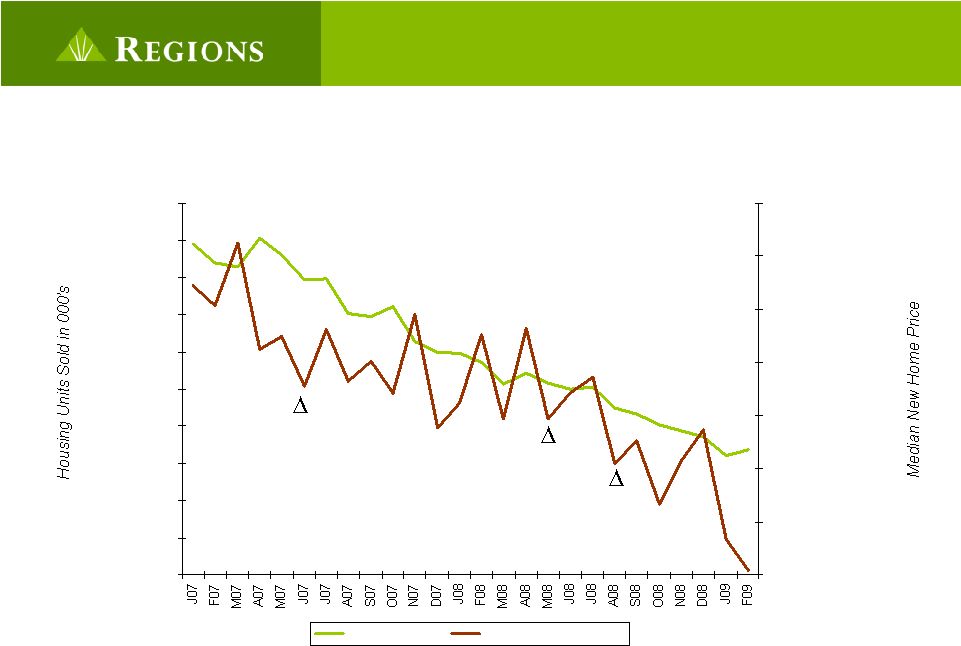

April 16, 2009 Source: US Census Bureau Reports Real estate decline turns into a systemic financial crisis 0 100 200 300 400 500 600 700 800 900 1000 $200,000 $210,000 $220,000 $230,000 $240,000 $250,000 $260,000 $270,000 New Home Sales Median New Home Price Sub-Prime Crisis Bear Stearns Collapse Bank Failures Begin |

April 16, 2009 Banking landscape permanently changed Failed Firms “Assisted Deals” New Bank Holding Companies • Placed into conservatorship • Certain assets and liabilities acquired by JP Morgan • “Assisted” Deal with Citi superseded by Wells Fargo acquisition • PNC acquires • Merges with Bank of America • First bank to fail 7/08 |

April 16, 2009 Dividend Actions – Industry-wide and beyond 16 of top 20 banks have cut their dividend in the last 12 months Regions PNC SunTrust State Street US BanCorp Marshall & Ilsley JPMorgan Chase Fifth Third Wells Fargo Capital One Bank of America Huntington Citigroup KeyCorp Zions Comerica Non-bank Companies General Electric Dow Chemical Pfizer Harley Davidson |

April 16, 2009 Strengthens capital and protects long-term value of our Company Preserves approximately $780 million per year in capital Dividend Reduction Preserves Capital |

April 16, 2009 We have taken Substantial Steps to Reduce Credit Risk Sold Equifirst (subprime originations) in 1Q07 Ensured loan portfolio remains free of Structured Investment Vehicles, non-traditional mortgages and Collateral Debt Obligations Reduced Commercial Real Estate exposure Sold or moved to held for sale $1.6 billion in problem assets Implemented a comprehensive Customer Assistance Program |

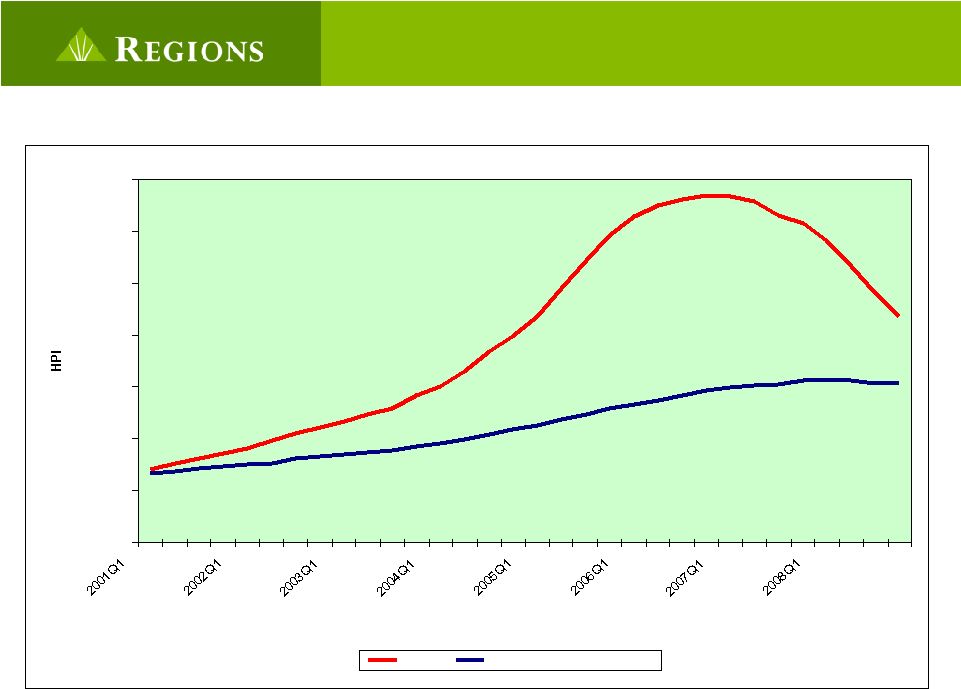

April 16, 2009 Home Prices Fall in Florida; Remainder of Region’s Footprint Steady Source: OFHEO Index 150 200 250 300 350 400 450 500 Period FL Avg. Footprint Avg. Excluding FL |

April 16, 2009 Maintaining focus through the cycle Nature of problem credits has not changed – continued focus on identification and resolution Homebuilder, Condominiums and Home Equity Other construction lending is performing satisfactorily Conservative, consistent loss reserve process Thorough valuation review process Emphasize markets of concern |

April 16, 2009 Troubled Asset Relief Program (TARP) Participation strongly encouraged by U.S. Treasury “Well Capitalized” before government investment High-cost capital Repayment as soon as possible |

April 16, 2009 Positive business results in key areas Significant customer deposit growth - momentum extending into 2009 Record new account openings driven by LifeGreen® accounts Record mortgage application volume High customer retention Service quality |

April 16, 2009 Focusing on the facts will help rebuild consumer confidence All banks are not the same TARP is not a bailout Banks are lending Banks are helping struggling home owners |

April 16, 2009 Focused on what we can control in our business Operate with a Clear Purpose Continue Being a Safe Harbor for Customer Deposits Focus on the Fundamentals of our Business Do What is Right for Customers and Communities |

|