UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

x QUARTERLY REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Quarterly Period Ended July 31, 2007

o TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Transition Period from _________ to _________

Commission file number: 000-51321

TRIANGLE PETROLEUM CORPORATION

(Name of Small Business Issuer in Its Charter)

Nevada | | 98-0430762 |

(State or other jurisdiction of incorporation or organization) | | (IRS Employer Identification No.) |

Suite 1250, 521 - 3 Avenue SW

Calgary, Alberta

Canada T2P 3T3

(Address of Principal Executive Offices)

(403) 262-4471

(Registrant’s telephone number, including area code)

(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer o | accelerated filer o | Non-accelerated filer x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

As of September 7, 2007, there were 37,113,602 shares of registrant’s common stock outstanding.

TRIANGLE PETROLEUM CORPORATION AND SUBSIDIARIES

INDEX |

| | | | |

| PART I. | FINANCIAL INFORMATION | |

| | | | |

| | ITEM 1. | Consolidated balance sheets at July 31, 2007 (unaudited) and January 31, 2007 | 3 |

| | | | |

| | | Consolidated statements of operations for the three and six months ended July 31, 2007 and 2006 and accumulated from December 11, 2003 (date of inception) to July 31, 2007 (unaudited) | 4 |

| | | | |

| | | Consolidated statements of cash flows for the six months ended July 31, 2007 and 2006 (unaudited) | 5 |

| | | | |

| | | Notes to unaudited consolidated financial statements | 6 - 17 |

| | | | |

| | ITEM 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 18-29 |

| | | | |

| | ITEM 3. | Quantitative and Qualitative Disclosures About Market Risk | 30 |

| | | | |

| | ITEM 4. | Controls and Procedures | 31 |

| | | | |

| PART II. | OTHER INFORMATION | |

| | | | |

| | ITEM 1 | Legal proceedings | 32 |

| | ITEM 1A | Risk factors | 32 |

| | ITEM 2 | Unregistered sales of equity securities and use of proceeds | 33 |

| | ITEM 3 | Defaults upon senior securities | 34 |

| | ITEM 4 | Submission of matters to a vote of security holders | 34 |

| | ITEM 5 | Other information | 34 |

| | ITEM 6 | Exhibits | 34 |

| | | | |

| | SIGNATURES | 35 |

Triangle Petroleum Corporation

(An Exploration Stage Company)

Consolidated Balance Sheets

(Expressed in U.S. dollars)

| | | July 31, 2007 $ | | January 31, 2007 $ | |

| | | (Unaudited) | | | |

| | | | | | |

| ASSETS | | | | | | | |

| | | | | | | | |

| Current Assets | | | | | | | |

| | | | | | | | |

| Cash and cash equivalents | | | 17,287,642 | | | 5,798,982 | |

| Prepaid expenses (Note 3) | | | 280,916 | | | 2,519,009 | |

| Other receivables | | | 845,120 | | | 344,342 | |

| | | | | | | | |

| Total Current Assets | | | 18,413,678 | | | 8,662,333 | |

| | | | | | | | |

| Debt Issue Costs, net | | | 685,000 | | | 916,353 | |

| | | | | | | | |

| Property and Equipment (Note 4) | | | 77,153 | | | 67,091 | |

| | | | | | | | |

| Oil and Gas Properties (Note 5) | | | 24,364,524 | | | 21,101,495 | |

| | | | | | | | |

| Total Assets | | | 43,540,355 | | | 30,747,272 | |

| | | | | | | | |

| | | | | | | | |

| LIABILITIES AND STOCKHOLDERS’ EQUITY | | | | | | | |

| | | | | | | | |

| Current Liabilities | | | | | | | |

| | | | | | | | |

| Accounts payable | | | 1,317,348 | | | 4,199,961 | |

| Accrued interest on convertible debt | | | 2,156,677 | | | 2,095,989 | |

| Accrued liabilities (Note 6) | | | 2,688,264 | | | 466,112 | |

| Convertible debentures, current portion (Note 8(a)) | | | - | | | 2,234,374 | |

| | | | | | | | |

| Total Current Liabilities | | | 6,162,289 | | | 8,996,436 | |

| | | | | | | | |

| Asset Retirement Obligations (Note 7) | | | 275,014 | | | 90,913 | |

| | | | | | | | |

| Convertible Debentures, less unamortized discount of $6,034,655 and $8,688,063 (Note 8) | | | 14,465,345 | | | 15,077,563 | |

| | | | | | | | |

| Total Liabilities | | | 20,902,648 | | | 24,164,912 | |

| | | | | | | | |

| Contingencies and Commitments (Notes 1 and 13) | | | | | | | |

| Subsequent Event (Note 15) | | | | | | | |

| | | | | | | | |

| Stockholders’ Equity | | | | | | | |

| | | | | | | | |

Common Stock (Note 10) Authorized: 100,000,000 shares, par value $0.00001 Issued: 37,113,602 shares (January 31, 2007 - 22,475,866 shares) | | | 371 | | | 225 | |

| | | | | | | | |

| Additional Paid-In Capital | | | 60,174,581 | | | 33,213,108 | |

| | | | | | | | |

| Deficit Accumulated During the Exploration Stage | | | (37,537,245 | ) | | (26,630,973 | ) |

| | | | | | | | |

| Total Stockholders’ Equity | | | 22,637,707 | | | 6,582,360 | |

| | | | | | | | |

| Total Liabilities and Stockholders’ Equity | | | 43,540,355 | | | 30,747,272 | |

The accompanying notes are an integral part of these consolidated financial statements

Triangle Petroleum Corporation

(An Exploration Stage Company)

Consolidated Statements of Operations

(Expressed in U.S. dollars)

(Unaudited)

| | | Accumulated from December 11, 2003 (Date of Inception) to July 31, | | Three Months Ended July 31, | | Three Months Ended July 31, | | Six Months Ended July 31, | | Six Months Ended July 31, | |

| | | 2007 | | 2007 | | 2006 | | 2007 | | 2006 | |

| | | $ | | $ | | $ | | $ | | $ | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Revenue | | | 295,283 | | | 144,297 | | | - | | | 240,941 | | | - | |

| | | | | | | | | | | | | | | | | |

| Operating Expenses | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| Oil and gas production | | | 121,517 | | | 91,154 | | | - | | | 121,517 | | | - | |

| Depletion, depreciation and accretion | | | 247,418 | | | 135,721 | | | - | | | 211,189 | | | - | |

| Depreciation - property and equipment | | | 52,858 | | | 14,834 | | | 6,458 | | | 21,614 | | | 12,238 | |

| General and administrative | | | 15,989,936 | | | 1,495,159 | | | 2,464,697 | | | 3,723,647 | | | 4,614,124 | |

| Impairment loss on oil and gas properties | | | 6,190,615 | | | 3,891,403 | | | 44,937 | | | 3,891,403 | | | 44,937 | |

| | | | | | | | | | | | | | | | | |

| Total Operating Expenses | | | 22,602,344 | | | 5,628,271 | | | 2,516,092 | | | 7,969,370 | | | 4,671,299 | |

| | | | | | | | | | | | | | | | | |

| Net Loss from Operations | | | (22,307,061 | ) | | (5,483,974 | ) | | (2,516,092 | ) | | (7,728,429 | ) | | (4,671,299 | ) |

| | | | | | | | | | | | | | | | | |

| Other Income (Expense) | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| Accretion of discounts on convertible debentures | | | (12,662,402 | ) | | (1,205,915 | ) | | (1,700,194 | ) | | (2,653,409 | ) | | (3,752,068 | ) |

| Amortization of debt issue costs | | | (695,000 | ) | | (113,645 | ) | | (94,098 | ) | | (231,353 | ) | | (176,389 | ) |

| Interest expense | | | (2,784,736 | ) | | (306,396 | ) | | (442,258 | ) | | (688,747 | ) | | (838,889 | ) |

| Interest income | | | 944,425 | | | 203,243 | | | 170,030 | | | 395,666 | | | 278,756 | |

| | | | | | | | | | | | | | | | | |

| Total Other Income (Expense) | | | (15,197,713 | ) | | (1,422,713 | ) | | (2,066,520 | ) | | (3,177,843 | ) | | (4,488,590 | ) |

| | | | | | | | | | | | | | | | | |

| Net Loss Before Discontinued Operations | | | (37,504,774 | ) | | (6,906,687 | ) | | (4,582,612 | ) | | (10,906,272 | ) | | (9,159,889 | ) |

| | | | | | | | | | | | | | | | | |

| Discontinued Operations | | | (32,471 | ) | | - | | | - | | | - | | | - | |

| | | | | | | | | | | | | | | | | |

| Net Loss for the Period | | | (37,537,245 | ) | | (6,906,687 | ) | | (4,582,612 | ) | | (10,906,272 | ) | | (9,159,889 | ) |

| | | | | | | | | | | | | | | | | |

| Net Loss Per Share | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| Basic and Diluted | | | | | | (0.21 | ) | | (0.23 | ) | | (0.30 | ) | | (0.47 | ) |

| | | | | | | | | | | | | | | | | |

| Weighted Average Number of Shares Outstanding | | | | | | 33,344,000 | | | 20,013,000 | | | 36,019,000 | | | 19,487,000 | |

The accompanying notes are an integral part of these consolidated financial statements

Triangle Petroleum Corporation

(An Exploration Stage Company)

Consolidated Statements of Cash Flows

(Expressed in U.S. dollars)

(Unaudited)

| | | Six Months Ended July 31, | | Six Months Ended July 31, | |

| | | 2007 | | 2006 | |

| | | $ | | $ | |

| | | | | | |

| Operating Activities | | | | | | | |

| | | | | | | | |

| Net loss | | | (10,906,272 | ) | | (9,159,889 | ) |

| | | | | | | | |

| Adjustments to reconcile net loss to net cash used in operating activities: | | | | | | | |

| | | | | | | | |

| Accretion of discount on convertible debentures | | | 2,653,408 | | | 3,752,068 | |

| Amortization of debt issue costs | | | 231,353 | | | 176,389 | |

| Depletion, depreciation and accretion | | | 211,189 | | | - | |

| Depreciation - property and equipment | | | 21,614 | | | 12,238 | |

| Impairment loss on oil and gas properties | | | 3,891,403 | | | - | |

| Stock-based compensation | | | 2,153,614 | | | 3,562,145 | |

| | | | | | | | |

| Changes in operating assets and liabilities: | | | | | | | |

| | | | | | | | |

| Prepaid expenses | | | (49,853 | ) | | - | |

| Other receivables | | | (45,633 | ) | | 207,257 | |

| Accounts payable | | | 209,412 | | | (281,735 | ) |

| Accrued interest on convertible debentures | | | 60,688 | | | - | |

| Accrued liabilities | | | 224,234 | | | - | |

| Due to related parties | | | - | | | 6,912 | |

| | | | | | | | |

| Net Cash Used in Operating Activities | | | (1,344,843 | ) | | (1,724,615 | ) |

| | | | | | | | |

| Investing Activities | | | | | | | |

| Purchase of property and equipment | | | (31,676 | ) | | (20,879 | ) |

| Oil and gas property expenditures | | | (8,165,422 | ) | | (2,259,157 | ) |

| Proceeds received from sale of oil and gas properties | | | 983,902 | | | - | |

| | | | | | | | |

| Changes in investing assets and liabilities | | | 738,693 | | | 1,008,036 | |

| | | | | | | | |

| Net Cash Used in Investing Activities | | | (6,474,503 | ) | | (1,272,000 | ) |

| | | | | | | | |

| Financing Activities | | | | | | | |

| Proceeds from issuance of common stock | | | 20,824,000 | | | 5,000,000 | |

| Common stock issuance costs | | | (1,515,994 | ) | | (425,000 | ) |

| | | | | | | | |

| Net Cash Provided in Financing Activities | | | 19,308,006 | | | 4,575,000 | |

| | | | | | | | |

| Increase in Cash and Cash Equivalents | | | 11,488,660 | | | 1,578,385 | |

| | | | | | | | |

| Cash and Cash Equivalents - Beginning of Period | | | 5,798,982 | | | 17,394,422 | |

| | | | | | | | |

| Cash and Cash Equivalents - End of Period | | | 17,287,642 | | | 18,972,807 | |

| | | | | | | | |

| Non-cash Investing and Financing Activities: | | | | | | | |

| | | | | | | | |

| Common stock issued for conversion of debentures | | | 5,500,000 | | | 900,000 | |

| | | | | | | | |

| Supplemental Disclosures: | | | | | | | |

| | | | | | | | |

| Interest paid | | | 628,058 | | | - | |

| Income taxes paid | | | - | | | - | |

The accompanying notes are an integral part of these consolidated financial statements

Triangle Petroleum Corporation

(An Exploration Stage Company)

Notes to the Consolidated Financial Statements

(Expressed in U.S. dollars, except as noted)

(Unaudited)

| 1. | Nature of Operations and Continuance of Business |

The Company was incorporated in the State of Nevada on December 11, 2003 under the name Peloton Resources Inc. In December 2003, the Company purchased six mineral claims situated in the Greenwood Mining Division in the Province of British Columbia, Canada. The Company’s principal business plan was to acquire, explore and develop mineral properties and to ultimately seek earnings by exploiting the mineral claims. During the fiscal year ended January 31, 2006, the Company abandoned its mineral property as a result of poor exploration results, and changed the Company’s principal business to that of acquisition, exploration and development of oil and gas resource properties. On May 10, 2005, the Company changed its name to Triangle Petroleum Corporation.

The Company has been in the exploration stage since its formation in December 2003 and has not yet realized any significant revenues from its planned operations. It is primarily engaged in the acquisition, exploration and development of oil and gas resource properties. The Company has incurred losses of $37,537,245 since inception on December 11, 2003 to July 31, 2007. During the year ended January 31, 2006, the Company issued $26,000,000 of convertible debentures. During the year ended January 31, 2007, the Company issued an additional $5,000,000 of convertible debentures. During the six month period ended July 31, 2007, the Company issued 10,462,000 shares of common stock for net proceeds of $19,308,006. The Company’s oil and gas capital expenditures over the next twelve months are expected to be approximately $14,800,000. As at July 31, 2007, the Company had cash and cash equivalents of $17,287,642.

Although existing cash resources are currently expected to provide sufficient funds through the upcoming fiscal year, the capital expenditures required to achieve planned principal operations may be substantial. The continuation of the Company as a going concern for a period longer than the current fiscal year is dependent upon the ability of the Company to obtain necessary equity financing to continue operations and to determine the existence, discovery and successful exploitation of economically recoverable reserves in its resource properties, confirmation of the Company’s interests in the underlying properties, and the attainment of profitable operations.

| 2. | Summary of Significant Accounting Policies |

These financial statements and related notes are presented in accordance with accounting principles generally accepted in the United States, and are expressed in US dollars. These consolidated financial statements include the accounts of the Company and its two wholly-owned subsidiaries, Elmworth Energy Corporation, incorporated in the Province of Alberta, Canada, and Triangle USA Petroleum Corporation, incorporated in the State of Colorado, USA. All significant intercompany balances and transactions have been eliminated. The Company’s fiscal year-end is January 31.

| b) | Interim Financial Statements |

The interim unaudited consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States for interim financial information and with the instructions to Securities and Exchange Commission (“SEC”) Form 10-QSB. They do not include all of the information and footnotes required by generally accepted accounting principles for complete financial statements. Therefore, these financial statements should be read in conjunction with the Company’s audited consolidated financial statements and notes thereto for the year ended January 31, 2007, included in the Company’s Annual Report on Form 10-KSB filed on May 1, 2007 with the SEC.

The consolidated financial statements included herein are unaudited; however, they contain all normal recurring accruals and adjustments that, in the opinion of management, are necessary to present fairly the Company’s consolidated financial position at July 31, 2007 and January 31, 2007, and the consolidated results of its operations and consolidated cash flows for the six months ended July 31, 2007 and 2006. The results of operations for the three and six months ended July 31, 2007 are not necessarily indicative of the results to be expected for future quarters or the full year.

The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. The Company regularly evaluates estimates and assumptions related to useful life and recoverability of long-lived assets, proved and unproved oil and gas expenditures, asset retirement obligations, stock-based compensation and deferred income tax asset valuation allowances. The Company bases its estimates and assumptions on current facts, historical experience and various other factors that it believes to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities and the accrual of costs and expenses that are not readily apparent from other sources. The actual results experienced by the Company may differ materially and adversely from the Company’s estimates. To the extent there are material differences between the estimates and the actual results, future results of operations will be affected.

Triangle Petroleum Corporation

(An Exploration Stage Company)

Notes to the Consolidated Financial Statements

(Expressed in U.S. dollars, except as noted)

(Unaudited)

| 2. | Summary of Significant Accounting Policies (continued) |

| d) | Foreign Currency Translation |

The Company's functional and reporting currency is the United States dollar and management has adopted SFAS No. 52, “Foreign Currency Translation”. Monetary assets and liabilities denominated in foreign currencies are translated into United States dollars at rates of exchange in effect at the balance sheet date. Non-monetary assets, liabilities and items recorded in income arising from transactions denominated in foreign currencies are translated at rates of exchange in effect at the date of the transaction. Foreign currency transactions are primarily undertaken in Canadian dollars. The Company has not, to the date of these financials statements, entered into derivative instruments to offset the impact of foreign currency fluctuations.

| e) | Cash and Cash Equivalents |

The Company considers all highly liquid instruments with maturity of three months or less at the time of issuance to be cash equivalents.

Property and equipment consists of computer hardware, geophysical software, furniture and equipment and leasehold improvements, and is recorded at cost. Computer hardware and geophysical software are depreciated on a straight-line basis over their estimated useful lives of three years. Furniture and equipment are depreciated on a straight-line basis over their estimated useful lives of five years. Leasehold improvements are depreciated on a straight-line basis over their estimated useful lives of five years.

In accordance with SFAS No. 144, “Accounting for the Impairment or Disposal of Long-Lived Assets”, the Company tests long-lived assets or asset groups for recoverability when events or changes in circumstances indicate that their carrying amount may not be recoverable. Circumstances which could trigger a review include, but are not limited to: significant decreases in the market price of the asset; significant adverse changes in the business climate or legal factors; accumulation of costs significantly in excess of the amount originally expected for the acquisition or construction of the asset; current period cash flow or operating losses combined with a history of losses or a forecast of continuing losses associated with the use of the asset; and current expectation that the asset will more likely than not be sold or disposed significantly before the end of its estimated useful life.

Recoverability is assessed based on the carrying amount of the asset and its fair value which is generally determined based on the sum of the undiscounted cash flows expected to result from the use and the eventual disposal of the asset, as well as specific appraisal in certain instances. An impairment loss is recognized when the carrying amount is not recoverable and exceeds fair value.

The Company utilizes the full-cost method of accounting for petroleum and natural gas properties. Under this method, the Company capitalizes all costs associated with acquisition, exploration and development of oil and natural gas reserves, including leasehold acquisition costs, geological and geophysical expenditures, lease rentals on undeveloped properties and costs of drilling of productive and non-productive wells into the full cost pool on a country by country basis. When the Company obtains proven oil and gas reserves, capitalized costs, including estimated future costs to develop the proved reserves and estimated abandonment costs, net of salvage, will be depleted on the units-of-production method using estimates of proved reserves. The costs of unproved properties are not amortized until it is determined whether or not proved reserves can be assigned to the properties. Until such determination is made the Company assesses quarterly whether impairment has occurred, and includes in the amortization base drilling exploratory dry holes associated with unproved properties.

The Company applies a ceiling test to the capitalized cost in the full cost pool. The ceiling test limits such cost to the estimated present value, using a ten percent discount rate, of the future net revenue from proved reserves, based on current economic and operating conditions. Specifically, the Company computes the ceiling test so that capitalized cost, less accumulated depletion and related deferred income tax, do not exceed an amount (the ceiling) equal to the sum of: (A) The present value of estimated future net revenue computed by applying current prices of oil and gas reserves (with consideration of price changes only to the extent provided by contractual arrangements) to estimated future production of proved oil and gas reserves as of the date of the latest balance sheet presented, less estimated future expenditures (based on current cost) to be incurred in developing and producing the proved reserves computed using a discount factor of ten percent and assuming continuation of existing economic conditions; plus (B) the cost of property not being amortized; plus (C) the lower of cost or estimated fair value of unproven properties included in the costs being amortized; less (D) income tax effects related to differences between the book and tax basis of the property.

Triangle Petroleum Corporation

(An Exploration Stage Company)

Notes to the Consolidated Financial Statements

(Expressed in U.S. dollars, except as noted)

(Unaudited)

2. | Summary of Significant Accounting Policies (continued) |

For unproven properties, the Company excludes from capitalized costs subject to depletion, all costs directly associated with the acquisition and evaluation of the unproved property until it is determined whether or not proved reserves can be assigned to the property. Until such a determination is made, the Company assesses the property at least annually to ascertain whether impairment has occurred. In assessing impairment the Company considers factors such as historical experience and other data such as primary lease terms of the property, average holding periods of unproved property, and geographic and geologic data. The Company adds the amount of impairment assessed to the cost to be amortized subject to the ceiling test.

| h) | Asset Retirement Obligations |

The Company recognizes a liability for future retirement obligations associated with the Company’s oil and gas properties. The estimated fair value of the asset retirement obligation is based on the current cost escalated at an inflation rate and discounted at a credit adjusted risk-free rate. This liability is capitalized as part of the cost of the related asset and amortized over its useful life. The liability accretes until the Company settles the obligation.

In accordance with the Accounting Principles Board Opinion 21 “Interest on Receivables and Payables”, the Company recognizes debt issue costs on the balance sheet as deferred charges, and amortizes the balance over the term of the related debt. The Company follows the guidance in the EITF 95-13 “Classification of Debt Issue Costs in the Statement of Cash Flows” and classifies cash payments for debt issue costs as a financing activity.

The Company recognizes oil and gas revenue when production is sold at a fixed or determinable price, persuasive evidence of an arrangement exists, delivery has occurred and title has transferred, and collectibility is reasonably assured.

The Company has adopted SFAS No. 109 “Accounting for Income Taxes” as of its inception. Pursuant to SFAS No. 109 the Company is required to compute tax asset benefits for net operating losses carried forward. Potential benefits of income tax losses are not recognized in the accounts until realization is more likely than not. The potential benefits of net operating losses have not been recognized in these financial statements because the Company cannot be assured it is more likely than not it will utilize the net operating losses carried forward in future years.

On February 1, 2007, the Company adopted Financial Accounting Standards Board Interpretation No. 48, “Accounting for Uncertainty in Income Taxes - an interpretation of FASB Statement No. 109” (“FIN 48”). FIN 48 prescribes a measurement process for recording in the financial statements uncertain tax positions taken or expected to be taken in a tax return. Additionally, FIN 48 provides guidance regarding uncertain tax positions relating to derecognition, classification, interest and penalties, accounting in interim periods, disclosure and transition. At July 31, 2007, the Company had no material uncertain tax positions.

| | l) | Basic and Diluted Net Income (Loss) Per Share |

The Company computes net income (loss) per share in accordance with SFAS No. 128, "Earnings per Share" (SFAS 128). SFAS 128 requires presentation of both basic and diluted earnings per share (EPS) on the face of the income statement. Basic EPS is computed by dividing net income (loss) available to common shareholders (numerator) by the weighted average number of shares outstanding (denominator) during the period. Diluted EPS gives effect to all dilutive potential common shares outstanding during the period including stock options, and warrants, using the treasury stock method, and convertible securities, using the if-converted method. In computing diluted EPS, the average stock price for the period is used in determining the number of shares assumed to be purchased from the exercise of stock options or warrants. Diluted EPS excludes all dilutive potential shares if their effect is anti-dilutive. Shares underlying these securities totaled approximately 16,376,000 as of July 31, 2007.

The fair values of financial instruments, which include cash and cash equivalents, other receivables, accounts payable, accrued interest on convertible debt, accrued liabilities, and convertible debentures approximate their carrying values due to the relatively short maturity of these instruments. The fair value of convertible debentures are estimated to approximate their carrying values based on borrowing rates currently available to the Company for debt with similar terms.

Triangle Petroleum Corporation

(An Exploration Stage Company)

Notes to the Consolidated Financial Statements

(Expressed in U.S. dollars, except as noted)

(Unaudited)

2. | Summary of Significant Accounting Policies (continued) |

The Company does not believe that it is exposed to interest rate risk. The Company maintains its cash accounts in one commercial bank located in Calgary, Alberta, Canada. The Company's cash accounts consist of uninsured and insured business checking accounts and deposits maintained principally in U.S. dollars. Financial instruments that potentially subject the Company to concentrations of credit risk consist primarily of cash in excess of federally insured amounts. As at July 31, 2007, the Company has not engaged in any transactions that would be considered derivative instruments on hedging activities. To date, the Company has not incurred a loss relating to this concentration of credit risk.

SFAS No. 130, “Reporting Comprehensive Income,” establishes standards for the reporting and display of comprehensive loss and its components in the financial statements. As at July 31, 2007 and 2006, the Company has no items that represent comprehensive loss and, therefore, has not included a schedule of comprehensive loss in the financial statements.

| p) | Stock-Based Compensation |

The Company records stock based compensation in accordance with SFAS 123(R), “Share-Based Payments,” which requires the measurement and recognition of compensation expense, based on estimated fair values, for all share-based awards, made to employees and directors, including stock options. In March 2005, the Securities and Exchange Commission issued SAB 107 relating to SFAS 123(R). The Company applied the provisions of SAB 107 in its adoption of SFAS 123(R).

All transactions in which goods or services are received for the issuance of equity instruments are accounted for based on the fair value of the consideration received or the fair value or the equity instrument issued, whichever is the more reliable measure.

SFAS 123(R) requires companies to estimate the fair value of share-based awards on the date of grant using an option-pricing model. The Company uses the Black-Scholes option-pricing model as its method of determining fair value. This model is affected by the Company’s stock price as well as assumptions regarding a number of subjective variables. These subjective variables include, but are not limited to the Company’s expected stock price volatility over the term of the awards, and actual and projected employee stock option exercise behaviors. The value of the portion of the award that is ultimately expected to vest is recognized as an expense in the consolidated statement of operations over the requisite service period.

No tax benefits were attributed to stock-based compensation expense because a full valuation allowance was maintained for all net deferred tax assets.

| q) | Recently Issued Accounting Pronouncements |

In February 2007, the Financial Accounting Standards Board (FASB) issued SFAS No. 159, “The Fair Value Option for Financial Assets and Financial Liabilities - Including an Amendment of FASB Statement No. 115”. This statement permits entities to choose to measure many financial instruments and certain other items at fair value. Most of the provisions of SFAS No. 159 apply only to entities that elect the fair value option. However, the amendment to SFAS No. 115 “Accounting for Certain Investments in Debt and Equity Securities” applies to all entities with available-for-sale and trading securities. SFAS No. 159 is effective as of the beginning of an entity’s first fiscal year that begins after November 15, 2007. Early adoption is permitted as of the beginning of a fiscal year that begins on or before November 15, 2007, provided the entity also elects to apply the provision of SFAS No. 157, “Fair Value Measurements”. The adoption of this statement is not expected to have a material effect on the Company's financial statements.

In September 2006, the FASB issued SFAS No. 157, “Fair Value Measurements”. The objective of SFAS No. 157 is to increase consistency and comparability in fair value measurements and to expand disclosures about fair value measurements. SFAS No. 157 defines fair value, establishes a framework for measuring fair value in generally accepted accounting principles, and expands disclosures about fair value measurements. SFAS No. 157 applies under other accounting pronouncements that require or permit fair value measurements and does not require any new fair value measurements. The provisions of SFAS No. 157 are effective for fair value measurements made in fiscal years beginning after November 15, 2007. The adoption of this statement is not expected to have a material effect on the Company's future reported financial position or results of operations.

| r) | Recently Adopted Accounting Pronouncements |

In September 2006, the SEC issued Staff Accounting Bulletin (“SAB”) No. 108, “Considering the Effects of Prior Year Misstatements when Quantifying Misstatements in Current Year Financial Statements.” SAB No. 108 addresses how the effects of prior year uncorrected misstatements should be considered when quantifying misstatements in current year financial statements. SAB No. 108 requires companies to quantify misstatements using a balance sheet and income statement approach and to evaluate whether either approach results in quantifying an error that is material in light of relevant quantitative and qualitative factors. SAB No. 108 is effective for periods ending after November 15, 2006. The adoption of SAB No. 108 did not have a material effect on the Company’s financial statements.

Triangle Petroleum Corporation

(An Exploration Stage Company)

Notes to the Consolidated Financial Statements

(Expressed in U.S. dollars, except as noted)

(Unaudited)

2. | Summary of Significant Accounting Policies (continued) |

| r) | Recently Adopted Accounting Pronouncements (continued) |

In September 2006, the FASB issued SFAS No. 158, “Employers’ Accounting for Defined Benefit Pension and Other Postretirement Plans - an amendment of FASB Statements No. 87, 88, 106, and 132(R)”. This statement requires employers to recognize the overfunded or underfunded status of a defined benefit postretirement plan (other than a multiemployer plan) as an asset or liability in its statement of financial position and to recognize changes in that funded status in the year in which the changes occur through comprehensive income of a business entity or changes in unrestricted net assets of a not-for-profit organization. This statement also requires an employer to measure the funded status of a plan as of the date of its year-end statement of financial position, with limited exceptions. The provisions of SFAS No. 158 are effective for employers with publicly traded equity securities as of the end of the fiscal year ending after December 15, 2006. The adoption of this statement did not have a material effect on the Company's financial statements.

In March 2006, the FASB issued SFAS No. 156, "Accounting for Servicing of Financial Assets, an amendment of FASB Statement No. 140, Accounting for Transfers and Servicing of Financial Assets and Extinguishments of Liabilities". This statement requires all separately recognized servicing assets and servicing liabilities be initially measured at fair value, if practicable, and permits for subsequent measurement using either fair value measurement with changes in fair value reflected in earnings or the amortization and impairment requirements of Statement No. 140. The subsequent measurement of separately recognized servicing assets and servicing liabilities at fair value eliminates the necessity for entities that manage the risks inherent in servicing assets and servicing liabilities with derivatives to qualify for hedge accounting treatment and eliminates the characterization of declines in fair value as impairments or direct write-downs. SFAS No. 156 is effective for an entity's first fiscal year beginning after September 15, 2006. The adoption of this statement did not have a material effect on the Company's financial statements.

In February 2006, the FASB issued SFAS No. 155, "Accounting for Certain Hybrid Financial Instruments-an amendment of FASB Statements No. 133 and 140", to simplify and make more consistent the accounting for certain financial instruments. SFAS No. 155 amends SFAS No. 133, "Accounting for Derivative Instruments and Hedging Activities", to permit fair value re-measurement for any hybrid financial instrument with an embedded derivative that otherwise would require bifurcation, provided that the whole instrument is accounted for on a fair value basis. SFAS No. 155 amends SFAS No. 140, "Accounting for the Impairment or Disposal of Long-Lived Assets", to allow a qualifying special-purpose entity to hold a derivative financial instrument that pertains to a beneficial interest other than another derivative financial instrument. SFAS No. 155 applies to all financial instruments acquired or issued after the beginning of an entity's first fiscal year that begins after September 15, 2006, with earlier application allowed. The adoption of this statement did not have a material effect on the Company's future reported financial position or results of operations.

Certain reclassifications have been made to the prior period’s financial statements to conform to the current period’s presentation.

The components of prepaid expenses are as follows:

| | | July 31, 2007 $ | | January 31, 2007 $ | |

| | | | | | |

| Office space deposit | | | 23,821 | | | - | |

| Prepaid insurance | | | 89,217 | | | 151,086 | |

| Prepaid joint-venture exploration costs | | | 79,977 | | | 2,367,923 | |

| Professional and consulting services | | | 46,005 | | | - | |

| Software subscriptions | | | 41,896 | | | - | |

| | | | | | | | |

| Total prepaid expenses | | | 280,916 | | | 2,519,009 | |

Triangle Petroleum Corporation

(An Exploration Stage Company)

Notes to the Consolidated Financial Statements

(Expressed in U.S. dollars, except as noted)

(Unaudited)

| | | Cost $ | | Accumulated Depreciation $ | | July 31, 2007 Net Carrying Value $ | | January 31, 2007 Net Carrying Value $ | |

| | | | | | | | | | |

| | | | | | | | | | |

| Computer hardware | | | 66,229 | | | 26,940 | | | 39,289 | | | 31,906 | |

| Furniture and equipment | | | 47,438 | | | 12,775 | | | 34,663 | | | 25,164 | |

| Geophysical software | | | 8,000 | | | 5,218 | | | 2,782 | | | 5,086 | |

| Leasehold improvements | | | 7,927 | | | 7,508 | | | 419 | | | 4,935 | |

| | | | | | | | | | | | | | |

| | | | 129,594 | | | 52,441 | | | 77,153 | | | 67,091 | |

The following table summarizes information regarding the Company's oil and gas acquisition, exploration and development activities:

| | | $ | | $ | |

| | | | | | |

| Proved Properties | | | | | | | |

| | | | | | | | |

Exploration costs | | | 8,882,540 | | | 2,965,420 | |

Less: | | | | | | | |

Accumulated depletion | | | (244,625 | ) | | (36,229 | ) |

Impairment costs | | | (6,190,615 | ) | | (2,299,212 | ) |

| | | | | | | | |

| | | | 2,447,300 | | | 629,979 | |

| | | | | | | | |

| Unproven Properties | | | | | | | |

| | | | | | | | |

Acquisition costs | | | 15,111,414 | | | 14,405,798 | |

Exploration costs | | | 6,805,810 | | | 6,065,718 | |

| | | | | | | | |

| | | | 21,917,224 | | | 20,471,516 | |

| | | | | | | | |

| Net Carrying Value | | | 24,364,524 | | | 21,101,495 | |

All of the Company’s oil and gas properties are located in the United States and Canada. The Company is currently participating in oil and gas exploration activities in Arkansas, Montana, Wyoming and Texas, USA, and Nova Scotia, New Brunswick and Alberta, Canada.

| (a) | The Company, through a series of joint venture agreements with different parties, has $5,313,346 (January 31, 2007 - $6,808,802) of unproven oil and gas expenditures in Alberta and Nova Scotia, Canada. In respect to these unproven oil and gas expenditures, the Company has expended $398,745 (January 31, 2007 - $443,759) to acquire land, $2,059,151 (January 31, 2007 - $2,031,168) for geological and geophysical expenditures, and $2,855,450 (2007 - $4,333,875) for drilling related costs. |

| (b) | On July 18, 2007, the Company sold its 27% interest in 12,100 gross acres in northeast Hill County of Texas for gross proceeds of $983,902. The Company had incurred land and geological and geophysical costs of $1,929,305 related to this prospect which resulted in a loss of $945,403 being recorded on the Company books. |

| (c) | The Company’s proved property costs exceeded the ceiling test limitation as at July 31, 2007. As a result, the Company recorded a $2,946,000 non-cash impairment loss. |

| (d) | The Company entered into a joint venture agreement whereby the Company received $500,000 in exchange for a 17.5% working interest in a producing well in the Wapiti area of northern Alberta, Canada. This receipt was offset directly against the Company’s share of drilling the subject well. |

Triangle Petroleum Corporation

(An Exploration Stage Company)

Notes to the Consolidated Financial Statements

(Expressed in U.S. dollars, except as noted)

(Unaudited)

| 5. | Oil and Gas Properties (continued) |

The Company's unproven acquisition and exploration costs were distributed in the following geographic areas:

| | | July 31, 2007 $ | | January 31, 2007 $ | |

| | | | | | |

| Alberta | | | 4,577,474 | | | 6,154,643 | |

| Arkansas | | | 13,037,119 | | | 7,569,101 | |

| Nova Scotia | | | 735,872 | | | 654,159 | |

| Rocky Mountains (Colorado, Montana, Wyoming) | | | 2,267,407 | | | 2,187,391 | |

| Texas | | | 1,299,352 | | | 3,906,222 | |

| | | | | | | | |

| | | | 21,917,224 | | | 20,471,516 | |

The components of accrued liabilities are as follows:

| | | July 31, 2007 $ | | January 31, 2007 $ | |

| | | | | | |

| Oil and gas expenditures | | | 2,688,264 | | | 466,112 | |

| 7. | Asset Retirement Obligations |

| | | July 31, 2007 $ | | January 31, 2007 $ | |

| | | | | | |

| Beginning asset retirement obligations | | | 90,913 | | | 33,000 | |

| Additions related to new properties | | | - | | | - | |

| Liabilities incurred | | | 153,264 | | | 56,446 | |

| Deletions related to property disposals | | | - | | | - | |

| Accretion | | | 30,837 | | | 1,467 | |

| | | | | | | | |

| Total asset retirement obligations | | | 275,014 | | | 90,913 | |

The Company is required to recognize an estimated liability for future costs associated with the abandonment of its oil and gas properties including without limitation the costs of reclamation of drilling sites, storage and transmission facilities and access roads. The Company bases its estimate of the liability on management’s industry experience and on its current understanding of federal and state regulatory requirements. The present value calculations require an estimate of the economic lives of the Company’s properties, assumptions of future inflation rates to apply to external estimates and the determination of the credit-adjusted risk-free rate to use. The estimated asset retirement obligations are reflected in depreciation, depletion and accretion calculations over the remaining life of the oil and gas properties.

| (a) | On June 14, 2005, the Company entered into a securities purchase agreement with a single accredited investor (the “Purchase Agreement”) pursuant to which the investor purchased an 8% convertible debenture with a principal amount of $1,000,000, and a warrant to purchase 1,000,000 shares of the Company’s common stock, exercisable at a price of $1.00 per share until June 15, 2008. Pursuant to the Purchase Agreement, the investor had the right to purchase up to $5,000,000 of additional convertible debentures and warrants to purchase 5,000,000 shares of common stock which was exercised on July 14, 2005, in exchange for an 8% convertible debenture with a principal amount of $5,000,000 and warrants to purchase 5,000,000 shares of the Company’s common stock, exercisable at a price of $1.00 per share until June 15, 2008. |

The total convertible debentures of $6,000,000 were due and payable on June 10, 2007. The principal and accrued interest on these convertible debentures may be converted into shares of the Company’s common stock at a rate of $1.00 per share, at the option of the holder. The investor has contractually agreed to restrict the ability to convert the convertible debentures to an amount which would not exceed the difference between the number of shares of common stock beneficially owned by the holder or issuable upon exercise of the warrant held by such holder and 4.99% of the outstanding shares of common stock of the Company. The securities were issued in a private placement transaction pursuant to Regulation D under the Securities Act of 1933, as amended. The

Triangle Petroleum Corporation

(An Exploration Stage Company)

Notes to the Consolidated Financial Statements

(Expressed in U.S. dollars, except as noted)

(Unaudited)

8. | Convertible Debentures (continued) |

Company filed an SB-2 Registration Statement registering the resale of shares of the Company's common stock issuable upon conversion of these convertible debentures and exercise of the warrants.

In accordance with EITF 98-5 “Accounting for Convertible Securities with Beneficial Conversion Features or Contingently Adjustable Conversion Ratios”, the Company recognized the value of the embedded beneficial conversion feature of $2,666,667 as additional paid-in capital and an equivalent discount which will be expensed over the term of the convertible debentures. In addition, in accordance with EITF 00-27 “Application of Issue No. 98-5 to Certain Convertible Instruments”, the Company has allocated the proceeds of issuance between the convertible debt and the detachable warrants based on their relative fair values. Accordingly, the Company recognized the fair value of the detachable warrants of $3,333,333 as additional paid-in capital and an equivalent discount against the convertible debentures. During the year ended January 31, 2006, a debenture with a principal amount of $900,000 was converted into 900,000 shares of common stock. The unamortized discount on the respective convertible debenture of $378,722 was charged to accretion expense. During the year ended January 31, 2007, debentures with a principal amount of $2,350,000 were converted into 2,350,000 shares of common stock. The unamortized discount on the respective convertible debentures of $1,049,247 was charged to accretion expense. During the six month period ended July 31, 2007, debentures with a principal amount of $2,750,000 was converted into 2,750,000 shares of common stock. The unamortized discount on the respective convertible debenture of $151,815 was charged to accretion expense. As at July 31, 2007, all of these $6,000,000 convertible debentures were converted into common stock of the company, as such the carrying value of the convertible debentures was $nil (January 31, 2007 - $2,234,374). On June 21, 2007, accrued interest of $628,058 was paid.

| (b) | On December 8, 2005, the Company entered into a Securities Purchase Agreement with a single investor pursuant to which the investor purchased 5% secured convertible debentures in the aggregate principal amount of $15,000,000. The gross proceeds of this financing will be received as follows: |

| | (i) | $5,000,000 was received on closing; |

| | (ii) | $5,000,000 was received on the second business day prior to the filing date of the SB-2 Registration Statement; and |

| | (iii) | $5,000,000 was received on the fifth business day following the effective date of the SB-2 Registration Statement |

The Company agreed to pay an 8% fee on the receipt of each installment, and a $15,000 structuring fee. The convertible debentures mature on the third anniversary of the date of issue (the “Maturity Date”) and bear interest at 5% per annum. The Company is not required to make any payments until the Maturity Date. The investor may convert, at any time, any amount outstanding under the convertible debentures into shares of common stock of the Company at a conversion price per share equal to the lesser of $5.00 or 90% of the average of the three lowest daily volume weighted average prices of the common stock, as quoted by Bloomberg, LP, of the ten trading days immediately preceding the date of conversion.

The Company, at its option has the right, with three business days advance written notice, to redeem a portion or all amounts outstanding under these convertible debentures prior to the Maturity Date provided that the closing bid price of the common stock is less than $5.00 at the time of the redemption. In the event of redemption, the Company is obligated to pay an amount equal to the principal amount being redeemed plus a 20% redemption premium, and accrued interest.

In connection with the Purchase Agreement, the Company also entered into a registration rights agreement (the “Registration Rights Agreement”) providing for the filing of an SB-2 Registration Statement (the “Registration Statement”) with the U.S. Securities and Exchange Commission (“SEC”) registering the common stock issuable upon conversion of the convertible debentures. The Company was obligated to use its best efforts to cause the Registration Statement to be declared effective no later than June 30, 2006 and to insure that the Registration Statement remains in effect until all of the shares of common stock issuable upon conversion of the convertible debentures have been sold. In the event of a default of its obligations under the Registration Rights Agreement, including its agreement to file the Registration Statement with the SEC no later than January 22, 2006, or if the Registration Statement was not declared effective by June 30, 2006, it is required pay to the investor, as liquidated damages, for each month that the Registration Statement has not been filed or declared effective, as the case may be, either a cash amount or shares of common stock equal to 2% of the liquidated value of the convertible debentures. The Company filed an SB-2 Registration Statement on January 18, 2006 that was declared effective May 26, 2006.

The investor has agreed to restrict its ability to convert the convertible debentures and receive shares of the Company’s common stock such that the number of shares of common stock held by the investor in the aggregate and its affiliates after such conversion or exercise does not exceed 4.9% of the then issued and outstanding shares of the Company’s common stock.

In connection with the Securities Purchase Agreement, the Company and each of its subsidiaries executed security agreements (the “Security Agreements”) in favor of the investor granting them a first priority security interest in all of the Company’s goods, inventory, contractual rights and general intangibles, receivables, documents, instruments, chattel paper, and intellectual property. The Security Agreements state that if an event of default occurs under the convertible debentures or Security Agreements, the investor has the right to take possession of the collateral, to operate the Company’s business using the collateral, and have the right to assign, sell, lease or otherwise dispose of and deliver all or any part of the collateral, at public or private sale or otherwise to satisfy the Company’s obligations under these agreements.

Triangle Petroleum Corporation

(An Exploration Stage Company)

Notes to the Consolidated Financial Statements

(Expressed in U.S. dollars, except as noted)

(Unaudited)

| 8. | Convertible Debentures (continued) |

In accordance with EITF 98-5 “Accounting for Convertible Securities with Beneficial Conversion Features or Contingently Adjustable Conversion Ratios”, the Company recognized the value of the embedded beneficial conversion feature of $2,697,057 as additional paid-in capital and an equivalent discount which will be expensed over the term of convertible debentures. During the year ended January 31, 2007, debentures with a principal amount of $1,750,000 were converted into 943,336 shares of common stock. The unamortized discount on the respective convertible debentures of $48,980 was charged to accretion expense. During the six month period ended July 31, 2007, debentures with a principal amount of $2,750,000 were converted into 1,425,736 shares of common stock. The unamortized discount on the respective convertible debentures of $52,808 was charged to accretion expense. The carrying value of the convertible debentures will be accreted to the face value of $10,500,000 to maturity. To July 31, 2007, the Company accrued interest of $991,610 (January 31, 2007 - $693,699) has been included in accrued liabilities. To July 31, 2007, accumulated accretion of $1,484,320 (January 31, 2007 - $1,697,551) has increased the carrying value of the convertible debentures to $9,287,263 (January 31, 2007 - $11,552,449).

| (c) | On December 28, 2005, the Company entered into a Securities Purchase Agreement with two accredited investors providing for the sale by the Company to the investors of 7.5% convertible debentures in the aggregate principal amount of $10,000,000, of which $5,000,000 was advanced immediately, and 1,250,000 warrants (the “Warrants”) to purchase 1,250,000 shares of the Company’s common stock, exercisable at a price of $5.00 per share until December 28, 2006, of which 625,000 were issued. The second installment of $5,000,000 and 625,000 warrants was advanced on January 18, 2006, upon the filing of an SB-2 Registration Statement by the Company with the SEC. The warrants expired in full without exercise during the fiscal year ended January 31, 2007. |

The convertible debentures mature on the third anniversary of the date of issuance (the “Maturity Date”) and bear interest at the annual rate of 7.5%. The Company is not required to make any payments until the Maturity Date. The investors may convert, at any time, any amount outstanding under the convertible debentures into shares of common stock of the Company at a conversion price per share of $4.00.

In connection with the Securities Purchase Agreement, the Company also entered into a registration rights agreement (the “Registration Rights Agreement”) providing for the filing of a registration statement (the “Registration Statement”) with the SEC registering the common stock issuable upon conversion of the convertible debentures and Warrants. The Company was obligated to use its best efforts to cause the Registration Statement to be declared effective no later than May 28, 2006 and to insure that the registration statement remains in effect until all of the shares of common stock issuable upon conversion of the convertible debentures have been sold. In the event of a default of its obligations under the Registration Rights Agreement, including its agreement to file the Registration Statement with the SEC no later than February 26, 2006, or if the Registration Statement was not declared effective by June 30, 2006, the Company is required pay to the investors, as liquidated damages, for each month that the Registration Statement has not been filed or declared effective, as the case may be, a cash amount equal to 1% of the liquidated value of the convertible debentures. The Company filed an SB-2 Registration Statement on January 18, 2006 that was declared effective May 25, 2006.

Each investor has agreed to restrict its ability to convert the convertible debentures or exercise the Warrants and receive shares of the Company’s common stock such that the number of shares of common stock held by them in the aggregate and their affiliates after such conversion or exercise does not exceed 4.99% of the then issued and outstanding shares of the Company’s common stock.

In accordance with EITF 98-5 “Accounting for Convertible Securities with Beneficial Conversion Features or Contingently Adjustable Conversion Ratios”, the Company recognized the value of the embedded beneficial conversion feature of $6,609,128 as additional paid-in capital and an equivalent discount which will be expensed over the term of the convertible debentures. In addition, in accordance with EITF 00-27 “Application of Issue No. 98-5 to Certain Convertible Instruments”, the Company has allocated the proceeds of issuance between the convertible debt and the detachable warrants based on their relative fair values. Accordingly, the Company recognized the fair value of the detachable warrants of $3,390,872 as additional paid-in capital and an equivalent discount against the convertible debentures. The Company will record further interest expense over the term of the Convertible Debentures of $10,000,000 resulting from the difference between the stated value and carrying value at the date of issuance. The carrying value of the convertible debentures will be accreted to the face value of $10,000,000 to maturity. To July 31, 2007, accrued interest of $1,165,068 (January 31, 2007 - $793,150) has been included in accrued liabilities, and accumulated accretion expense of $5,178,082 (January 31, 2007 - $3,525,114) increased the carrying value of the Convertible Debentures to $5,178,082 (January 31, 2007 - $3,525,114).

| 9. | Related Party Transactions |

| | a) | During the six months ended July 31, 2007, the Company incurred $15,000 (2006 - $10,000) in director’s fees. |

| | b) | Effective February 1, 2006, the Company agreed to pay a salary of Cdn$12,000 per month to the President of the Company. On November 1, 2006, the Company agreed to pay a salary of Cdn$24,000 per month to the President of the Company. During the six months ended July 31, 2007, $127,049 (2006 - $62,939) was charged to operations. |

Triangle Petroleum Corporation

(An Exploration Stage Company)

Notes to the Consolidated Financial Statements

(Expressed in U.S. dollars, except as noted)

(Unaudited)

| 9. | Related Party Transactions (continued) |

| | c) | On June 23, 2005, the Company entered into a management consulting agreement with the President of the Company’s Canadian subsidiary (Elmworth Energy Corporation). Under the terms of the agreement, the Company must pay $20,000 per month for an initial term of two years, and, unless notice of termination is given by either party, is automatically renewed for one year periods. During the six months ended July 31, 2007, $120,000 (2006 - $120,000) was charged to operations. |

| | d) | Effective January 1, 2006, the Company agreed to pay a salary of Cdn$12,000 per month to the then Chief Financial Officer. During the six months ended July 31, 2007, $63,525 (2006 - $62,939) was charged to operations. |

| | | Shares | | Common Stock | | Additional Paid-In Capital | |

| | | | | $ | | $ | |

| | | | | | | | |

| January 31, 2006 | | | 19,182,530 | | | 192 | | | 27,623,110 | |

| Conversion of notes | | | 3,293,336 | | | 33 | | | 4,239,912 | |

| Stock based compensation | | | - | | | - | | | 1,338,686 | |

| Donated capital | | | - | | | - | | | 11,400 | |

| January 31, 2007 | | | 22,475,866 | | | 225 | | | 33,213,108 | |

| Conversion of debentures (c) | | | 4,175,736 | | | 41 | | | 5,499,958 | |

| Private placement (d) | | | 10,412,000 | | | 104 | | | 20,823,896 | |

| Financing fees (d) | | | - | | | - | | | (1,515,994 | ) |

| Investor relations services (e) | | | 50,000 | | | 1 | | | 108,499 | |

| Stock-based compensation (a, b and Note 11) | | | - | | | - | | | 2,045,114 | |

| July 31, 2007 | | | 37,113,602 | | | 371 | | | 60,174,581 | |

| | (a) | On May 16, 2005, the Company issued 4,000,000 shares of common stock to the President of the Company at $0.01 per share for cash proceeds of $40,000. As the shares were issued for below fair value, a discount on the issuance of shares of $4,160,000 was recorded as deferred compensation. During the year ended January 31, 2007, $2,080,000 was charged to operations. During the six month period ended July 31, 2007, $606,667 was charged to operations. |

| | (b) | On June 2, 2005, the Company issued 2,000,000 shares of common stock to the President of the Company’s subsidiary at $0.01 per share for cash proceeds of $20,000. As the shares were issued for below fair value, a discount on the issuance of shares of $2,700,000 was recorded as deferred compensation. During the year ended January 31, 2007, $1,350,000 was charged to operations. During the six month period ended July 31, 2007, $450,000 was charged to operations. |

| | (c) | Conversion of debentures |

| Date | | Shares | | Common Stock | | Additional Paid-In Capital | |

| | | # | | $ | | $ | |

| | | | | | | | |

| February 20, 2007 | | | 108,923 | | | 1 | | | 249,999 | |

| March 6, 2007 | | | 900,000 | | | 9 | | | 899,991 | |

| March 7, 2007 | | | 106,696 | | | 1 | | | 249,999 | |

| April 11, 2007 | | | 129,333 | | | 1 | | | 249,999 | |

| April 30, 2007 | | | 128,939 | | | 1 | | | 249,999 | |

| May 4, 2007 | | | 748,000 | | | 7 | | | 747,993 | |

| May 11, 2007 | | | 130,494 | | | 2 | | | 249,999 | |

| May 21, 2007 | | | 265,041 | | | 3 | | | 499,997 | |

| June 15, 2007 | | | 279,002 | | | 3 | | | 499,997 | |

| June 21, 2007 | | | 1,102,000 | | | 11 | | | 1,101,989 | |

| June 25, 2007 | | | 138,742 | | | 1 | | | 249,998 | |

| June 28, 2007 | | | 138,566 | | | 1 | | | 249,998 | |

| | | | | | | | | | | |

| Total | | | 4,175,736 | | | 41 | | | 5,499,958 | |

| (d) | On February 26, 2007, the Company issued 10,412,000 shares of common stock pursuant to a private placement for net proceeds of $19,308,006 after issue costs of $1,515,994. Pursuant to the terms of sale, the Company agreed to cause a resale registration statement covering the common stock to be filed no later than 30 days after the closing and declared effective no later than 120 days after the closing. If the Company fails to comply with the registration statement filing or effective date requirements, it will be required to pay the investors a fee equal to 1% of the aggregate amount invested by the purchasers per each 30 day period of delay, not to exceed 10%. On March 14, 2007, the registration statement was declared effective. In connection with the financing the Company paid the placement agents of the offering a cash fee of 6.5% of the proceeds of the offering. |

Triangle Petroleum Corporation

(An Exploration Stage Company)

Notes to the Consolidated Financial Statements

(Expressed in U.S. dollars, except as noted)

(Unaudited)

| 10. | Common Stock (continued) |

| (e) | On June 26, 2007, the Company issued 50,000 shares of common stock at a fair value of $108,500 for investor relation services rendered. |

Effective August 5, 2005, the Company approved the 2005 Incentive Stock Plan (the “Plan”) to issue up to 2,000,000 shares of common stock. Pursuant to the Plan, stock options vest 20% upon granting and 20% every six months. As at July 31, 2007, the Company had 220,000 stock options available for granting pursuant to the Plan. The Plan allows for the granting of stock options at a price of not less than fair value of the stock and for a term not to exceed five years. The total number of options granted to any person shall not exceed 5% of the issued and outstanding common stock of the Company.

The weighted average grant date fair value of stock options granted during the six month periods ended July 31, 2007 and 2006 was $1.93 and $3.10, respectively. No stock options were exercised during the six month periods ended July 31, 2007 and 2006. During the six month period ended July 31, 2007 and 2006, the Company recorded stock-based compensation of $988,447 and $1,331,825, respectively, as general and administrative expense.

A summary of the Company’s stock option activity is as follows:

| | | Number of Options | | Weighted Average Exercise Price $ | | Weighted Average Remaining Contractual Term | | Aggregate Intrinsic Value $ | |

| | | | | | | | | | |

| Outstanding, January 31, 2007 | | | 1,630,000 | | | 3.31 | | | | | | | |

| | | | | | | | | | | | | | |

| Granted | | | 150,000 | | | 2.19 | | | | | | | |

| | | | | | | | | | | | | | |

| Outstanding, July 31, 2007 | | | 1,780,000 | | | 3.22 | | | 3.51 | | | ំ | |

| | | | | | | | | | | | | | |

| Exercisable, July 31, 2007 | | | 1,214,000 | | | 3.35 | | | 3.36 | | | ំ | |

The fair value of each option grant was estimated on the date of the grant using the Black-Scholes option pricing model with the following weighted average assumptions:

| | | Period Ended July 31, 2007 | | Period Ended July 31, 2006 | |

| | | | | | |

| Expected dividend yield | | | 0 | % | | 0 | % |

| Expected volatility | | | 135 | % | | 178 | % |

| Expected life (in years) | | | 5.0 | | | 2.5 | |

| Risk-free interest rate | | | 4.53 | % | | 4.56 | % |

As at July 31, 2007, there was $1,488,223 (January 31, 2007 - $2,187,094) of total unrecognized compensation costs related to nonvested share-based compensation arrangements granted under the Plan which are expected to be recognized over a weighted-average period of 10 months. The total fair value of shares vested during the periods ended July 31, 2007 and 2006 was $988,447 and $1,331,825, respectively.

A summary of the status of the Company’s nonvested shares as of July 31, 2007, and changes during the period ended July 31 2007, is presented below:

| Nonvested shares | | Number of Shares | | Weighted-Average Grant-Date Fair Value $ | |

| | | | | | |

| Nonvested at January 31, 2007 | | | 782,000 | | | 2.80 | |

| | | | | | | | |

| Granted | | | 150,000 | | | 1.93 | |

| Forfeited | | | ំ | | | ំ | |

| Vested | | | (366,000 | ) | | 2.70 | |

| | | | | | | | |

| Nonvested at July 31, 2007 | | | 566,000 | | | 2.63 | |

Triangle Petroleum Corporation

(An Exploration Stage Company)

Notes to the Consolidated Financial Statements

(Expressed in U.S. dollars, except as noted)

(Unaudited)

| 12. | Share Purchase Warrants |

The following table summarizes the continuity of the Company’s share purchase warrants:

| | | Number of Warrants | | Weighted average exercise price $ | |

| | | | | | |

| | | | | | |

| Balance, January 31, 2006 | | | 7,250,000 | | | 1.69 | |

| Expired | | | (1,250,000 | ) | | 5.00 | |

| | | | | | | | |

| Balance, January 31, 2007 and July 31, 2007 | | | 6,000,000 | | | 1.00 | |

As at July 31, 2007, the following share purchase warrants were outstanding:

| Number of Warrants | Exercise Price | Expiry Date |

| | | |

| 6,000,000 | $ 1.00 | June 15, 2008 |

On February 28, 2007, the Company entered into a lease agreement commencing May 1, 2007 for office premises for a 6 year term expiring May 1, 2013. Annual rent under the new lease is payable at $176,445 (Cdn$207,680) for the first three years and $183,062 (Cdn$215,468) for the remaining three years. The Company must also pay its share of building operating costs and taxes. During the six months ended July 31, 2007, the Company paid rent expense of $77,141 (2006 - $22,682). Future minimum lease payments over the next five fiscal years are as follows:

| 2008 | | $ | 90,000 | |

| 2009 | | | 179,000 | |

| 2010 | | | 179,000 | |

| 2011 | | | 179,000 | |

| 2012 | | | 179,000 | |

| | | | | |

| | | $ | 806,000 | |

The Company operates as one operating segment which is the acquisition, exploration and development of oil and gas resource properties. The Chief Executive Officer is the Company’s Chief Operating Decision Maker (CODM) as defined by SFAS 131, “Disclosure about Segments of an Enterprise and Related Information.” The CODM allocates resources and assesses the performance of the Company based on the results of operations.

In August 2007, the Company granted 1,100,000 stock options to employees and consultants exercisable at $2.00 per share with an expiry five years from issuance pursuant to the 2007 Incentive Stock Plan.

ITEM 2. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

This report includes certain forward-looking statements. Forward-looking statements are statements that predict the occurrence of future events and are not based on historical fact. Forward-looking statements may be identified by the use of forward-looking terminology, such as “may”, “shall”, “will”, “could”, “expect”, “estimate”, “anticipate”, “predict”, “probable”, “possible”, “should”, “continue”, or similar terms, variations of those terms or the negative of those terms. We have written the forward-looking statements specified in the following information on the basis of assumptions we consider to be reasonable. However, we cannot predict our future operating results. Any representation, guarantee, or warranty should not be inferred from those forward-looking statements.

The assumptions we used for purposes of the forward-looking statements specified in the following information represent estimates of future events and are subject to uncertainty in economic, legislative, industry, and other circumstances. As a result, judgment must be exercised in the identification and interpretation of data and other information and in their use in developing and selecting assumptions from and among reasonable alternatives. To the extent that the assumed events do not occur, the outcome may vary substantially from anticipated or projected results. Accordingly we express no opinion on the achievability of those forward-looking statements. We cannot guarantee that any of the assumptions relating to the forward-looking statements specified in the following information are accurate. We assume no obligation to update any such forward-looking statements.

Prior to May 2005, we were known as Peloton Resources Inc., a mining exploration company. Peloton was actively searching for ore bodies containing gold in British Columbia. A consultant was hired to assess the economic viability of exploring for and developing gold reserves on Peloton’s properties. Based upon his report, Peloton decided to abandon all mining activities and to commence shifting towards an oil and gas exploration company. In connection with the shift in operational focus, we changed our name to Triangle Petroleum Corporation.

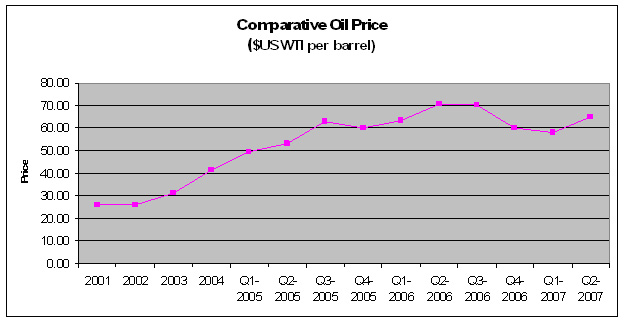

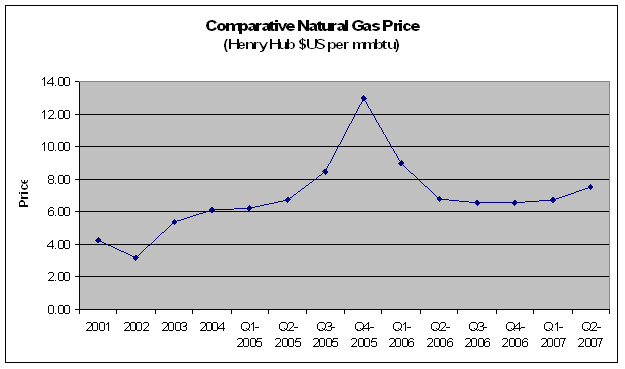

The changeover from a mining to an oil and gas exploration company has taken place over the past two years, during one of the strongest markets for oil and natural gas. The average monthly price for West Texas Intermediate (WTI) crude oil and natural gas (Henry Hub Nymex), currently, as compared to the past, is as follows:

Although these strong commodity prices have resulted in extremely competitive conditions for the supply of products and services for exploration companies, our outlook remains positive. Despite these strong fundamentals, it should be noted that significant short term fluctuations in North American natural gas prices have occurred based upon seasonal weather patterns and gas storage levels. It should also be noted that actual prices received for oil and gas are typically less than the WTI and Henry Hub prices, respectively. This discount varies from time to time and is based on location, quality and other factors.

Plan of Operations

Since our inception, we have had the opportunity to screen various projects in a variety of geographic locations with numerous potential joint venture partners. The project areas outlined below were carefully selected based on our belief in balancing overall project risk against potential project returns and the anticipated time horizons required to achieve such returns. The three core project areas (Canadian Shale, Fayetteville Shale and Rocky Mountain Conventional Programs) represent distinctive exploration opportunities. In conjunction with our joint venture partners, we intend to execute our operating plan in order to realize the full value of the initial land base that has been established. The remaining two project areas (Barnett Shale and Western Canadian Programs) are currently designated as non-core due to existing market conditions related to land acquisition costs, drilling costs and completion costs.

Eastern Canada - Canadian Shale Gas Program

Over the last 18 months, a multi-disciplined geoscience team has screened prospective basins in Eastern Canada. The screening process includes an assessment of the geologic history for a given area, estimates of pressure and temperature profiles and a determination of the ability to fracture stimulate a prospective shale package.

As a direct result of implementing this strategy, we have executed a farm-in agreement with a Canadian company to pursue a shale gas opportunity in Eastern Canada. The project covers approximately 68,000 gross acres and we believe it to be located in a favorable geological setting based on technical work performed to date and drilling activity in the area. Additional laboratory measurements will be taken on core samples and drill cuttings, which are available from previously drilled conventional wells. We will be entitled to earn an average 70% working interest in the block subsequent to the acquisition and evaluation of a seismic program and then electing to drill a test well no later than December 31, 2008.

In addition, we have committed to another project located in the Windsor Area of Nova Scotia, Canada covering approximately 516,000 gross acres. Based on an extensive screening process and technical work performed to date, this area is also believed to be located in a highly favorable geological setting. Additional laboratory measurements have been taken on core samples and drill cuttings which are available from previously drilled conventional wells. We will be entitled to earn an average 70% working interest in the block subsequent to drilling a test well no later than September 15, 2008.

The first Nova Scotia test well has spudded in late August 2007. Our current Windsor Basin exploration program is estimated to cost approximately $8.2 million.

A drilling rig has been contracted and drilling has commenced on the first of two vertical wells in the Windsor Basin. Both wells are expected to be drilled to a depth of approximately 4,500 to 5,000 feet and drilling should be complete by early October. These wellsite locations were chosen based upon the geological work indicated above and the close proximity to a conventional well drilled in 1975. During the drilling of these two wells, we will perform extensive coring and logging.

In addition to the two vertical wells, we are planning to acquire a 25 square mile 3-D and a 30 mile 2-D seismic program in order to further define the Horton Shale over a select area of the land block. The seismic program is currently in the permitting and field logistics phase and is expected to be acquired this fall. Processing of the data is scheduled to occur over the winter months.

We will develop a hydraulic fracture stimulation program for the two wells once the analysis of the core samples, logs, and other tests have been completed. Completion and flow testing of both wells is anticipated to occur in the fourth quarter of our fiscal year. The technical evaluation of the drilling, coring, seismic and completion programs will allow our exploration team to quantify the gas in place estimates. These results will then be reviewed and verified by independent industry experts by the end of our fiscal year.

Arkoma Basin Arkansas - Fayetteville Shale Program

We originally committed $16 million to a joint venture in the Fayetteville Shale of the Arkoma Basin with Kerogen Resources. We and Kerogen have equal 50% working interest positions in approximately 20,000 gross acres leased to date in Conway and Faulkner Counties. A measured pace of additional leasing is planned to complement the 2007 drilling program. As at July 31, 2007, we had advanced approximately $7.9 million to fund our share of land costs, $1.8 million for seismic and an additional $3.0 million to fund our share of costs related to the first vertical well.

The first vertical test well of the Fayetteville joint venture reached its targeted depth of 8,300 feet on April 4, 2007. Drill cuttings and other samples were taken from the well and sent in for further lab work and analysis. Concurrent with the first drilling operation, a new multi-component 3-D seismic survey had also commenced. The seismic survey was shot over approximately half of the 24 square mile target area and sent for processing in April 2007. Depending on the results of the seismic program, the vertical test well and leasing of additional acreage, we may initiate a horizontal drilling program.

States of Colorado, Montana and Wyoming - Rocky Mountain Program