Exhibit 4

Halcon Resources Corp. (“HK”) February 4, 2019

2 Maximizing Shareholder Value Problems: Market is punishing sub-scale over-levered operatorsHK is stuck, can’t grow out of its problems with current balance sheetHK corporate overhead (“G&A”) is extraordinarily high; especially executive comp.Solutions:Improve Corporate Governance to Better Align with ShareholdersWork with shareholders to appoint two independent Directors to the BoardSeparate Chairman and CEO rolesImmediately take steps to reduce G&A to $2-3 per boe Sell the Company to Larger Operator for Cash and/or StockWork with shareholders to appoint two new Directors to lead special committee to explore strategic alternatives to sell the Company for cash and/or stock Fir Tree Seeks Appointment of Two New Independent Directors to Lead Process to Sell the Company & Cut Corporate Overhead.

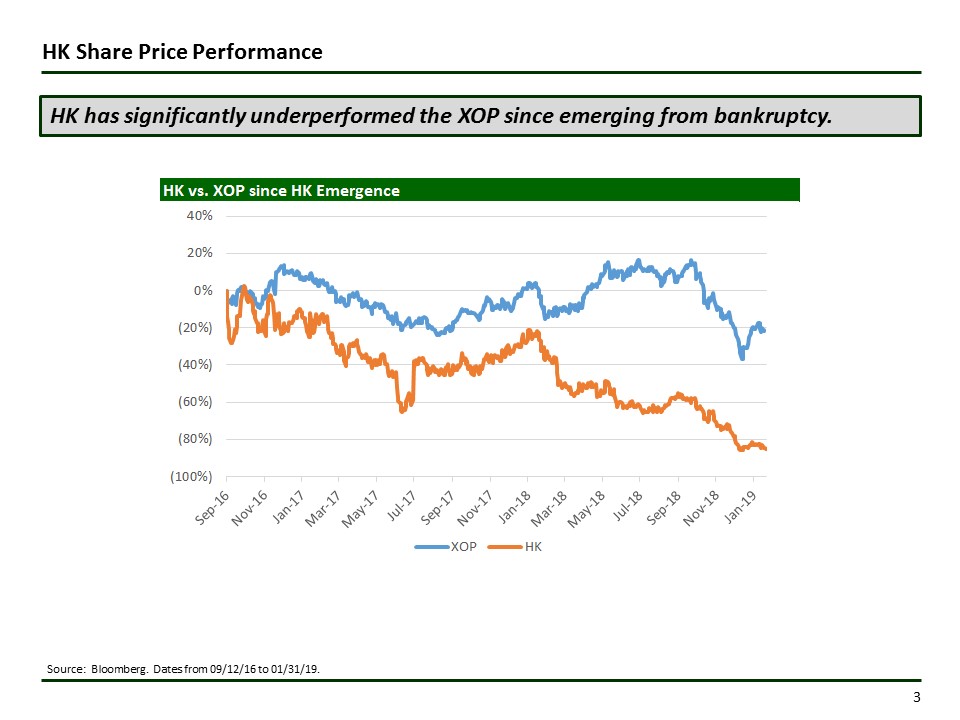

3 HK Share Price Performance HK has significantly underperformed the XOP since emerging from bankruptcy. Source: Bloomberg. Dates from 09/12/16 to 01/31/19.

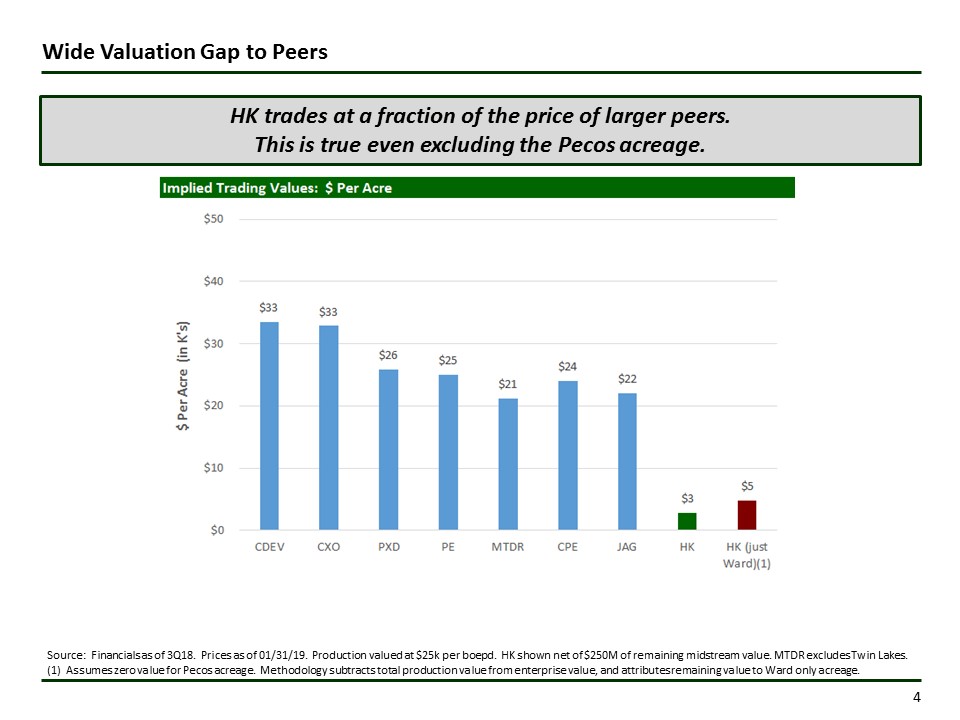

4 Wide Valuation Gap to Peers HK trades at a fraction of the price of larger peers. This is true even excluding the Pecos acreage. Source: Financials as of 3Q18. Prices as of 01/31/19. Production valued at $25k per boepd. HK shown net of $250M of remaining midstream value. MTDR excludes Twin Lakes.(1) Assumes zero value for Pecos acreage. Methodology subtracts total production value from enterprise value, and attributes remaining value to Ward only acreage.

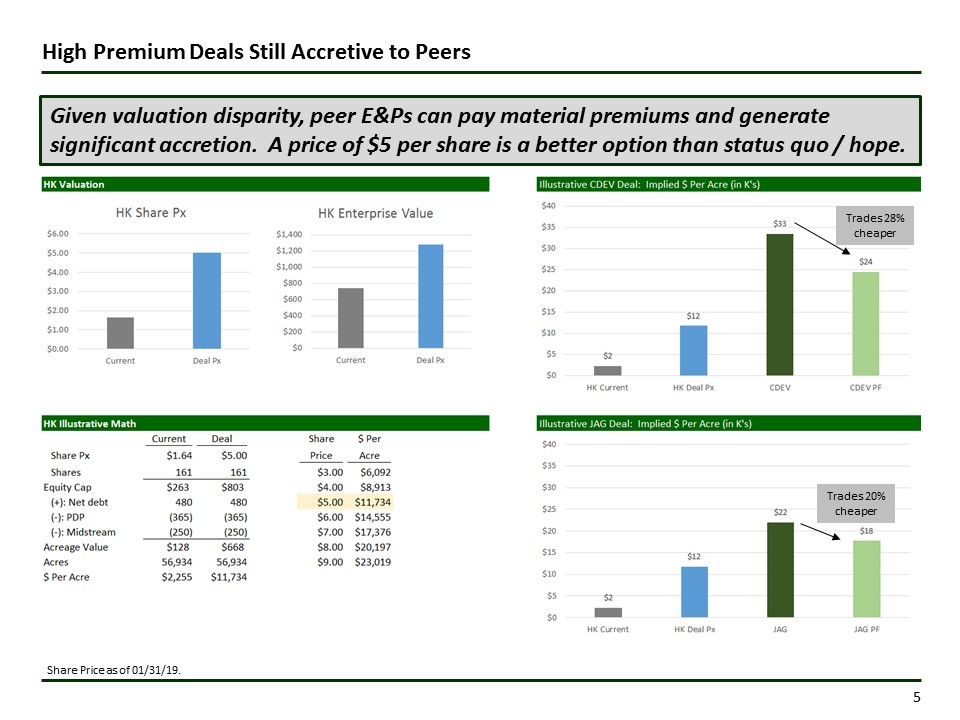

5 High Premium Deals Still Accretive to Peers Given valuation disparity, peer E&Ps can pay material premiums and generate significant accretion. A price of $5 per share is a better option than status quo / hope. Illustrative JAG Deal Illustrative CDEV Deal Trades 28% cheaper Trades 20% cheaper Share Price as of 01/31/19.

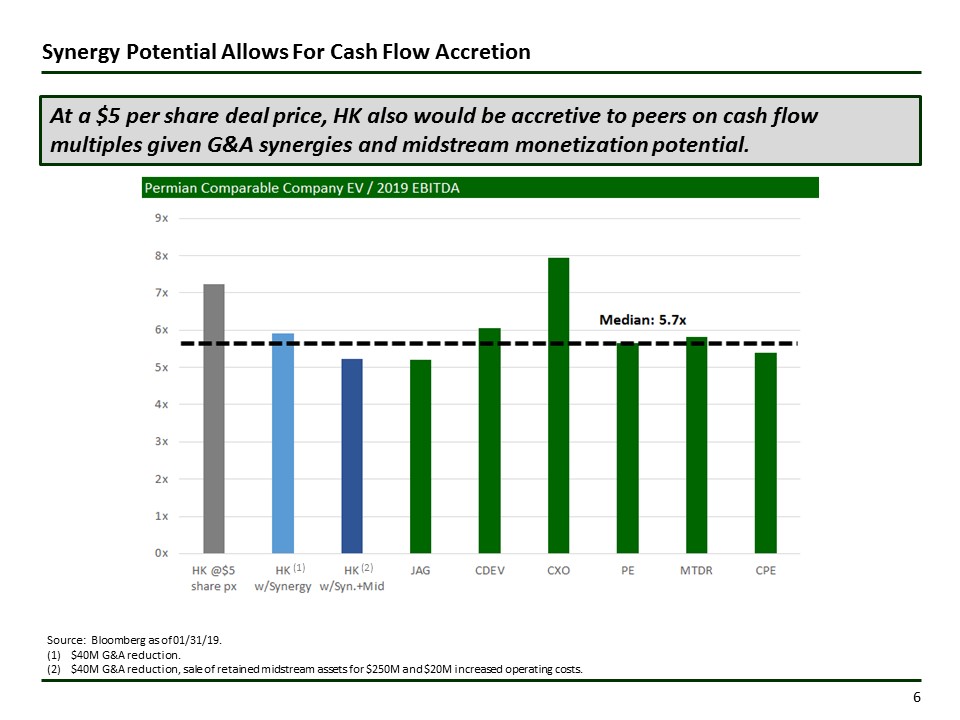

6 Synergy Potential Allows For Cash Flow Accretion At a $5 per share deal price, HK also would be accretive to peers on cash flow multiples given G&A synergies and midstream monetization potential. Illustrative JAG Deal Illustrative CDEV Deal Source: Bloomberg as of 01/31/19.$40M G&A reduction.$40M G&A reduction, sale of retained midstream assets for $250M and $20M increased operating costs. (1) (2)

7 G&A is Extraordinarily High No matter how you cut it G&A spend is excessive – especially for a poorly performing small cap company. Source: Company filings, Bloomberg and DrillingInfo.Run-rate adjusted G&A = 3Q18YTD EBITDA annualized, excluding stock compensation and other transaction adjustments.Active wells for Delaware Basin only.

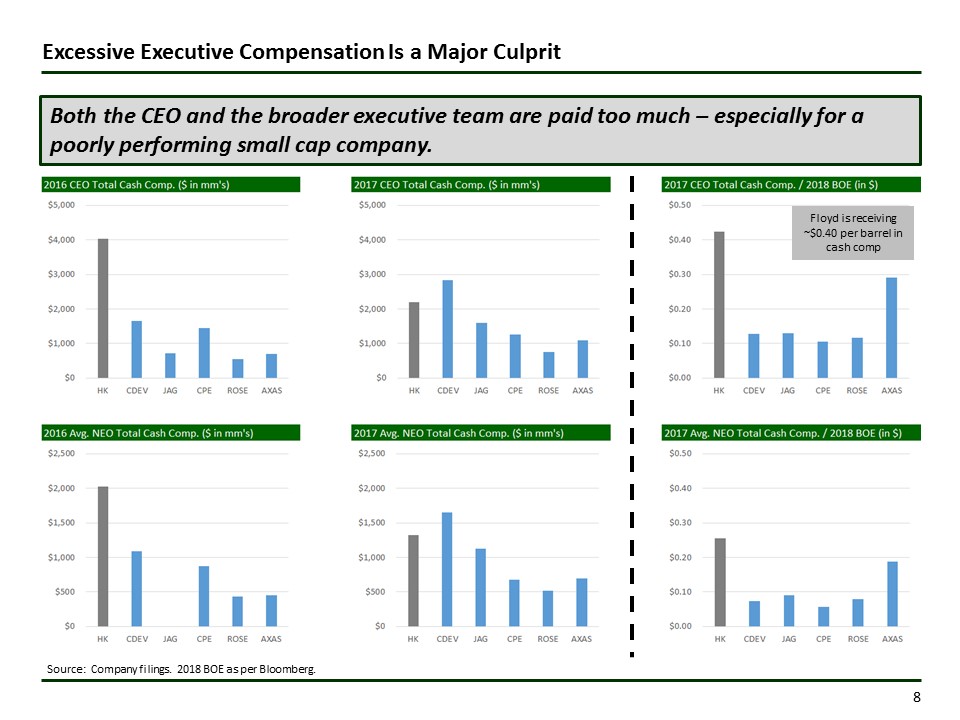

8 Excessive Executive Compensation Is a Major Culprit Both the CEO and the broader executive team are paid too much – especially for a poorly performing small cap company. Source: Company filings. 2018 BOE as per Bloomberg. Floyd is receiving ~$0.40 per barrel in cash comp

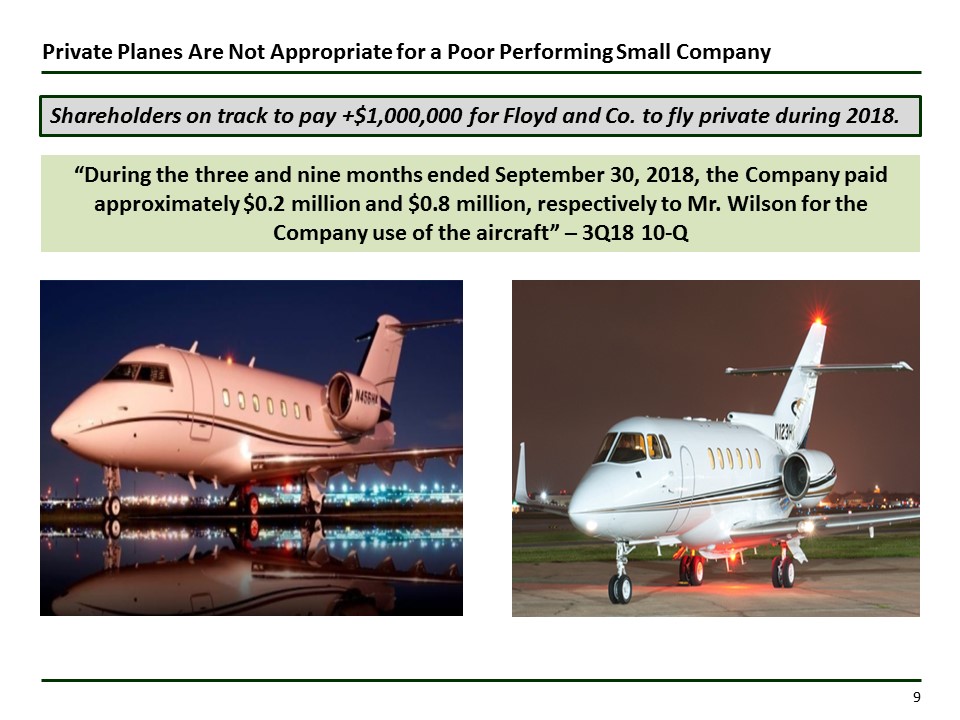

9 Private Planes Are Not Appropriate for a Poor Performing Small Company Shareholders on track to pay +$1,000,000 for Floyd and Co. to fly private during 2018. “During the three and nine months ended September 30, 2018, the Company paid approximately $0.2 million and $0.8 million, respectively to Mr. Wilson for the Company use of the aircraft” – 3Q18 10-Q