PRE PREL LIMINA IMINARY RY W WO ORKING RKING DRAF DRAFT T – – S SUB UBJECT JECT TO TO FURTHE FURTHER R RE REV VIE IEW W A AND ND MOD MODIFICA IFICATIO TION N Exhibit (c)(3)(A) PROJECT APPLE DISCUSSION MATERIALS June 1, 2023

PRELIMINARY WORKING DRAFT – SUBJECT TO FURTHER REVIEW AND MODIFICATION Intrepid Transaction Team Team Member Experience Selected Work Experience • Intrepid: 2015 – Present (Co-Founder & CEO) Skip McGee • Barclays: 2008 – 2014 (CEO, Americas) 30+ years Co-Founder & CEO • Lehman Brothers: 1993 – 2008 (Head of Global Investment Banking) • Intrepid: 2017 – Present (Head of Midstream) John Nesland • UBS: 2011 – 2017 (Head of Midstream and Downstream) Managing Director 24 years • Barclays: 2008 – 2011 (Managing Director) Head of Midstream • Lehman Brothers: 1999 – 2008 (Managing Director) • Intrepid: 2019 – Present (Head of M&A) Greg Sommer Managing Director• Deutsche Bank: 2010 – 2018 (Global Co-Head of Natural Resources Group) 30+ years Head of M&A • Citi: 1997 – 2010 (Managing Director, Head of Energy M&A) John Ed McGee• Intrepid: 2017 – Present 9 years Senior Vice President • Deutsche Bank: 2014 – 2017 Visesh Keerty • Intrepid: 2018 – Present 5 years Vice President Jennifer Trieschman• Intrepid: 2022 – Present 3 years Associate• Citi: 2020 – 2022 Will McLeroy 2 years• Intrepid: 2021 – Present Analyst 1

PRELIMINARY WORKING DRAFT – SUBJECT TO FURTHER REVIEW AND MODIFICATION Preliminary Near-term Timeline and Next Steps th Week of May 29 : ▪ Committee, GDC, MNAT and IFP kick-off meeting to discuss initial observations th Week of June 5 : ▪ Meeting with DINO/HEP to review the Proposal and commence due diligence – Establish VDR protocol and follow-up due diligence procedures ▪ IFP to commence modeling work/transaction analyses ▪ GDC to commence legal due diligence th Week of June 13 : ▪ IFP to evaluate projections and develop preliminary valuation framework ▪ Follow-up due diligence and Q&A th Week of June 20 : ▪ IFP/GDC to present diligence findings; IFP to present preliminary valuation to Conflicts Committee ▪ Committee to deliberate; IFP to incorporate Committee feedback into the analysis ▪ Committee, GDC and IFP to formulate optimal response to DINO – Propose specific counteroffer or reject the Proposal on the basis it is inadequate th Week of June 27 and Beyond: ▪ Negotiations to occur, analyses to be refined and continued work on transaction documentation 2

PRELIMINARY WORKING DRAFT – SUBJECT TO FURTHER REVIEW AND MODIFICATION Summary Due Diligence Topics and Documents ▪ DINO’s strategic rationale for the Proposal; rationale for consideration mix General ▪ HEP strategic alternatives considered in advance of the Proposal and Proposal ▪ Material communication with HEP investors (including the Sinclair Family) leading up to, and after, the date of the Proposal ▪ Detailed business update on DINO and HEP’s business segments/assets ▪ Review of historical dropdown transactions ▪ Detailed review of HEP’s contract structure and customers mix by business segments/assets Business and – Review of contract expirations, re-contracting events, rate redetermination, etc. Commercial – Review of contracts and agreements between DINO and HEP rd – Review of DINO vs. 3 party revenue/margin contribution ▪ Identify any go-forward opportunities (e.g., traditional oil & gas and energy transition growth projects) and challenges (e.g., maintenance, environmental, competition, etc.) ▪ Receive detailed DINO and HEP financial projection models ▪ Evaluate projections vs. Wall Street research projections and expectations from prior projection models; Financial determine if alternative assumptions / sensitivity scenarios are required ▪ Understand key assumptions for the proposed transaction (including cash tax impacts to DINO) 3

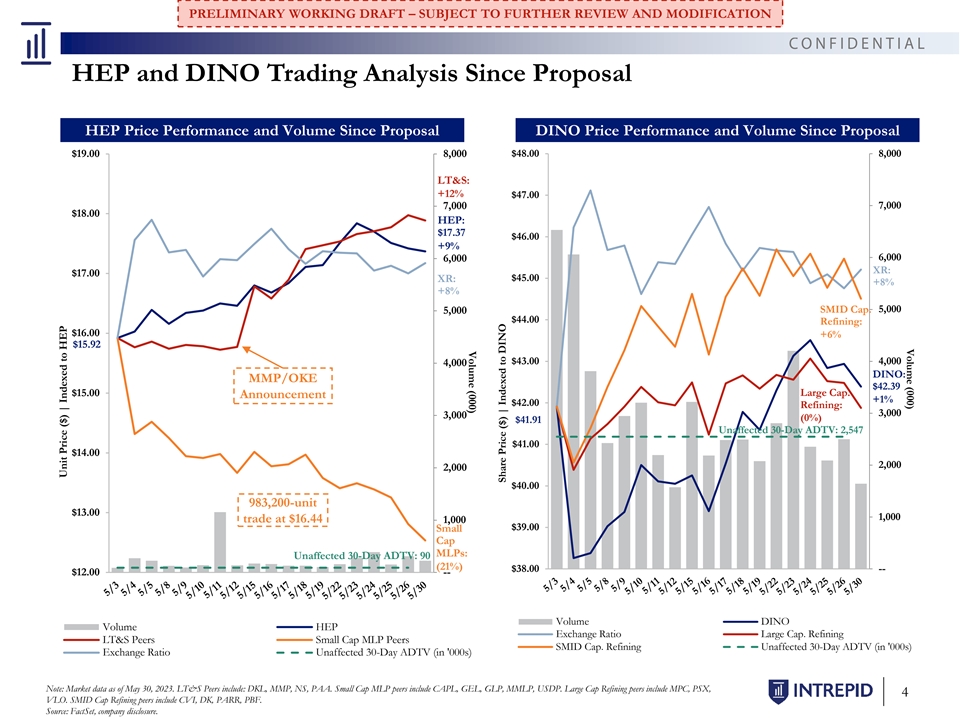

Volume (000) Volume (000) PRELIMINARY WORKING DRAFT – SUBJECT TO FURTHER REVIEW AND MODIFICATION HEP and DINO Trading Analysis Since Proposal HEP Price Performance and Volume Since Proposal DINO Price Performance and Volume Since Proposal $19.00 8,000 $48.00 8,000 LT&S: +12% $47.00 7,000 7,000 $18.00 HEP: $17.37 $46.00 +9% 6,000 6,000 XR: $17.00 $45.00 XR: +8% +8% 5,000 SMID Cap. 5,000 $44.00 Refining: $16.00 +6% $15.92 $43.00 4,000 4,000 DINO: MMP/OKE $42.39 $15.00 Large Cap. Announcement +1% $42.00 Refining: 3,000 3,000 (0%) $41.91 Unaffected 30-Day ADTV: 2,547 $41.00 $14.00 2,000 2,000 $40.00 983,200-unit $13.00 1,000 trade at $16.44 1,000 $39.00 Small Cap MLPs: Unaffected 30-Day ADTV: 90 (21%) $38.00 -- $12.00 -- Volume DINO Volume HEP Exchange Ratio Large Cap. Refining LT&S Peers Small Cap MLP Peers SMID Cap. Refining Unaffected 30-Day ADTV (in '000s) Exchange Ratio Unaffected 30-Day ADTV (in '000s) Note: Market data as of May 30, 2023. LT&S Peers include: DKL, MMP, NS, PAA. Small Cap MLP peers include CAPL, GEL, GLP, MMLP, USDP. Large Cap Refining peers include MPC, PSX, 4 VLO. SMID Cap Refining peers include CVI, DK, PARR, PBF. Source: FactSet, company disclosure. Unit Price ($) | Indexed to HEP Share Price ($) | Indexed to DINO

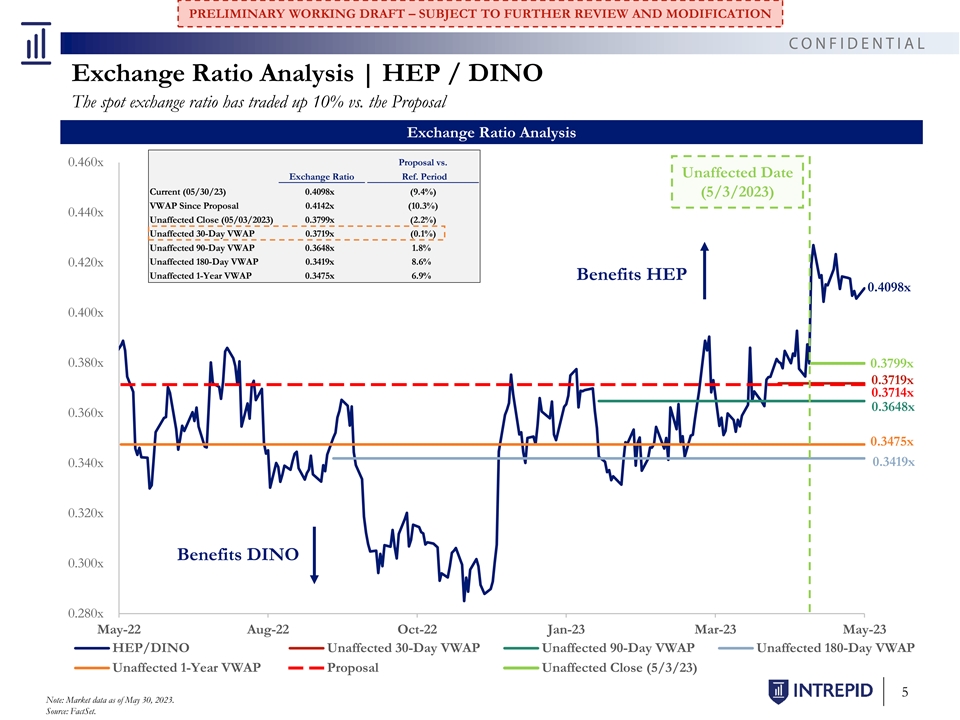

PRELIMINARY WORKING DRAFT – SUBJECT TO FURTHER REVIEW AND MODIFICATION Exchange Ratio Analysis | HEP / DINO The spot exchange ratio has traded up 10% vs. the Proposal Exchange Ratio Analysis Proposal vs. 0.460x Unaffected Date Exchange Ratio Ref. Period Current (05/30/23) 0.4098x (9.4%) (5/3/2023) VWAP Since Proposal 0.4142x (10.3%) 0.440x Unaffected Close (05/03/2023) 0.3799x (2.2%) Unaffected 30-Day VWAP 0.3719x (0.1%) Unaffected 90-Day VWAP 0.3648x 1.8% Unaffected 180-Day VWAP 0.3419x 8.6% 0.420x Unaffected 1-Year VWAP 0.3475x 6.9% Benefits HEP 0.4098x 0.400x 0.380x 0.3799x 0.3719x 0.3714x 0.3648x 0.360x 0.3475x 0.340x 0.3419x 0.320x Benefits DINO 0.300x 0.280x May-22 Aug-22 Oct-22 Jan-23 Mar-23 May-23 HEP/DINO Unaffected 30-Day VWAP Unaffected 90-Day VWAP Unaffected 180-Day VWAP Unaffected 1-Year VWAP Proposal Unaffected Close (5/3/23) 5 Note: Market data as of May 30, 2023. Source: FactSet.

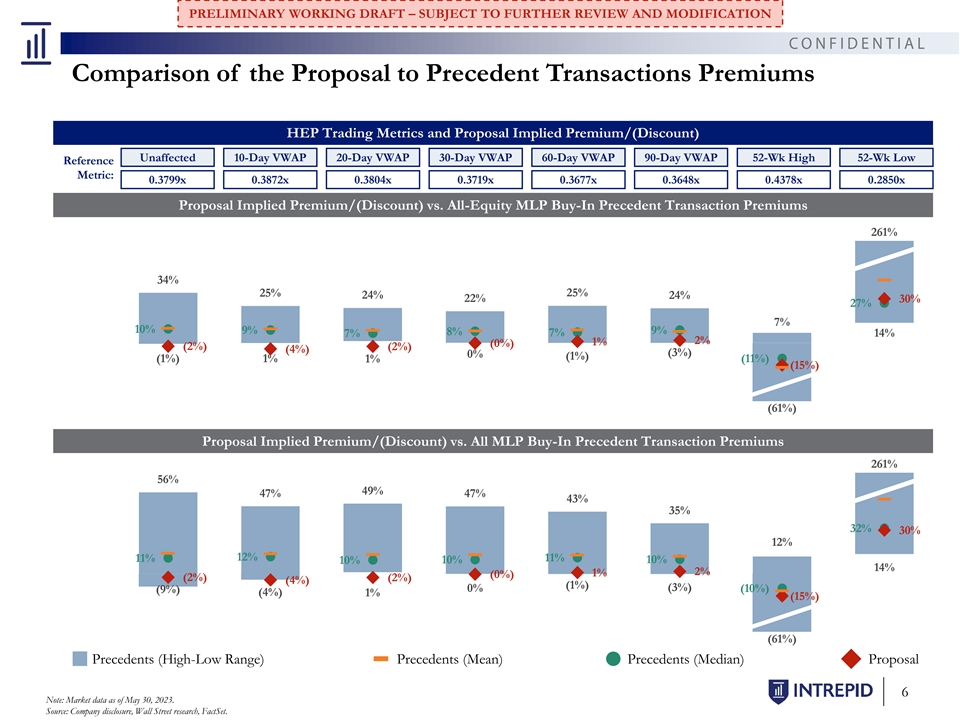

PRELIMINARY WORKING DRAFT – SUBJECT TO FURTHER REVIEW AND MODIFICATION Comparison of the Proposal to Precedent Transactions Premiums HEP Trading Metrics and Proposal Implied Premium/(Discount) Unaffected 10-Day VWAP 20-Day VWAP 30-Day VWAP 60-Day VWAP 90-Day VWAP 52-Wk High 52-Wk Low Reference Metric: 0.3799x 0.3872x 0.3804x 0.3719x 0.3677x 0.3648x 0.4378x 0.2850x Proposal Implied Premium/(Discount) vs. All-Equity MLP Buy-In Precedent Transaction Premiums 261% 34% 25% 25% 24% 24% 22% 30% 27% 7% 10% 9% 8% 9% 7% 7% 14% 2% 1% (0%) (2%) (2%) (4%) (3%) 0% (1%) (1%) 1% 1% (11%) (15%) (61%) Proposal Implied Premium/(Discount) vs. All MLP Buy-In Precedent Transaction Premiums 261% 56% 49% 47% 47% 43% 35% 32% 30% 12% 12% 11% 11% 10% 10% 10% 14% 1% 2% (0%) (2%) (2%) (4%) (1%) (3%) 0% (10%) (9%) (4%) 1% (15%) (61%) Precedents (High-Low Range) Precedents (Mean) Precedents (Median) Proposal 6 Note: Market data as of May 30, 2023. Source: Company disclosure, Wall Street research, FactSet.

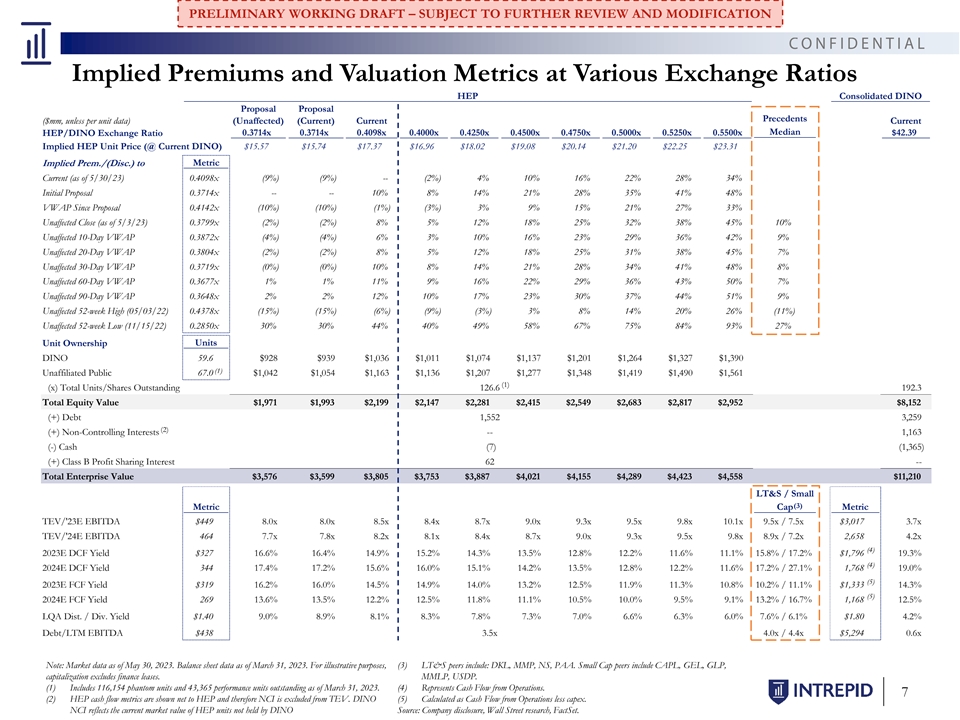

PRELIMINARY WORKING DRAFT – SUBJECT TO FURTHER REVIEW AND MODIFICATION Implied Premiums and Valuation Metrics at Various Exchange Ratios HEP Consolidated DINO Proposal Proposal Precedents ($mm, unless per unit data) (Unaffected) (Current) Current Current Median HEP/DINO Exchange Ratio 0.3714x 0.3714x 0.4098x 0.4000x 0.4250x 0.4500x 0.4750x 0.5000x 0.5250x 0.5500x $42.39 Implied HEP Unit Price (@ Current DINO) $15.57 $15.74 $17.37 $16.96 $18.02 $19.08 $20.14 $21.20 $22.25 $23.31 Metric Implied Prem./(Disc.) to Current (as of 5/30/23) 0.4098x (9%) (9%) -- (2%) 4% 10% 16% 22% 28% 34% Initial Proposal 0.3714x -- -- 10% 8% 14% 21% 28% 35% 41% 48% VWAP Since Proposal 0.4142x (10%) (10%) (1%) (3%) 3% 9% 15% 21% 27% 33% Unaffected Close (as of 5/3/23) 0.3799x (2%) (2%) 8% 5% 12% 18% 25% 32% 38% 45% 10% Unaffected 10-Day VWAP 0.3872x (4%) (4%) 6% 3% 10% 16% 23% 29% 36% 42% 9% Unaffected 20-Day VWAP 0.3804x (2%) (2%) 8% 5% 12% 18% 25% 31% 38% 45% 7% Unaffected 30-Day VWAP 0.3719x (0%) (0%) 10% 8% 14% 21% 28% 34% 41% 48% 8% Unaffected 60-Day VWAP 0.3677x 1% 1% 11% 9% 16% 22% 29% 36% 43% 50% 7% Unaffected 90-Day VWAP 0.3648x 2% 2% 12% 10% 17% 23% 30% 37% 44% 51% 9% Unaffected 52-week High (05/03/22) 0.4378x (15%) (15%) (6%) (9%) (3%) 3% 8% 14% 20% 26% (11%) Unaffected 52-week Low (11/15/22) 0.2850x 30% 30% 44% 40% 49% 58% 67% 75% 84% 93% 27% Units Unit Ownership DINO 59.6 $928 $939 $1,036 $1,011 $1,074 $1,137 $1,201 $1,264 $1,327 $1,390 (1) Unaffiliated Public 67.0 $1,042 $1,054 $1,163 $1,136 $1,207 $1,277 $1,348 $1,419 $1,490 $1,561 (1) (x) Total Units/Shares Outstanding 126.6 192.3 Total Equity Value $1,971 $1,993 $2,199 $2,147 $2,281 $2,415 $2,549 $2,683 $2,817 $2,952 $8,152 (+) Debt 1,552 3,259 (2) (+) Non-Controlling Interests -- 1,163 (-) Cash (7) (1,365) (+) Class B Profit Sharing Interest 62 -- Total Enterprise Value $3,576 $3,599 $3,805 $3,753 $3,887 $4,021 $4,155 $4,289 $4,423 $4,558 $11,210 LT&S / Small (3) Metric Cap Metric TEV/'23E EBITDA $449 8.0x 8.0x 8.5x 8.4x 8.7x 9.0x 9.3x 9.5x 9.8x 10.1x 9.5x / 7.5x $3,017 3.7x TEV/'24E EBITDA 464 7.7x 7.8x 8.2x 8.1x 8.4x 8.7x 9.0x 9.3x 9.5x 9.8x 8.9x / 7.2x 2,658 4.2x (4) 2023E DCF Yield $327 16.6% 16.4% 14.9% 15.2% 14.3% 13.5% 12.8% 12.2% 11.6% 11.1% 15.8% / 17.2% $1,796 19.3% (4) 2024E DCF Yield 344 17.4% 17.2% 15.6% 16.0% 15.1% 14.2% 13.5% 12.8% 12.2% 11.6% 17.2% / 27.1% 1,768 19.0% (5) 2023E FCF Yield $319 16.2% 16.0% 14.5% 14.9% 14.0% 13.2% 12.5% 11.9% 11.3% 10.8% 10.2% / 11.1% $1,333 14.3% (5) 2024E FCF Yield 269 13.6% 13.5% 12.2% 12.5% 11.8% 11.1% 10.5% 10.0% 9.5% 9.1% 13.2% / 16.7% 1,168 12.5% LQA Dist. / Div. Yield $1.40 9.0% 8.9% 8.1% 8.3% 7.8% 7.3% 7.0% 6.6% 6.3% 6.0% 7.6% / 6.1% $1.80 4.2% Debt/LTM EBITDA $438 3.5x 4.0x / 4.4x $5,294 0.6x Note: Market data as of May 30, 2023. Balance sheet data as of March 31, 2023. For illustrative purposes, (3) LT&S peers include: DKL, MMP, NS, PAA. Small Cap peers include CAPL, GEL, GLP, capitalization excludes finance leases. MMLP, USDP. (1) Includes 116,154 phantom units and 43,365 performance units outstanding as of March 31, 2023. (4) Represents Cash Flow from Operations. 7 (2) HEP cash flow metrics are shown net to HEP and therefore NCI is excluded from TEV. DINO (5) Calculated as Cash Flow from Operations less capex. NCI reflects the current market value of HEP units not held by DINO Source: Company disclosure, Wall Street research, FactSet.

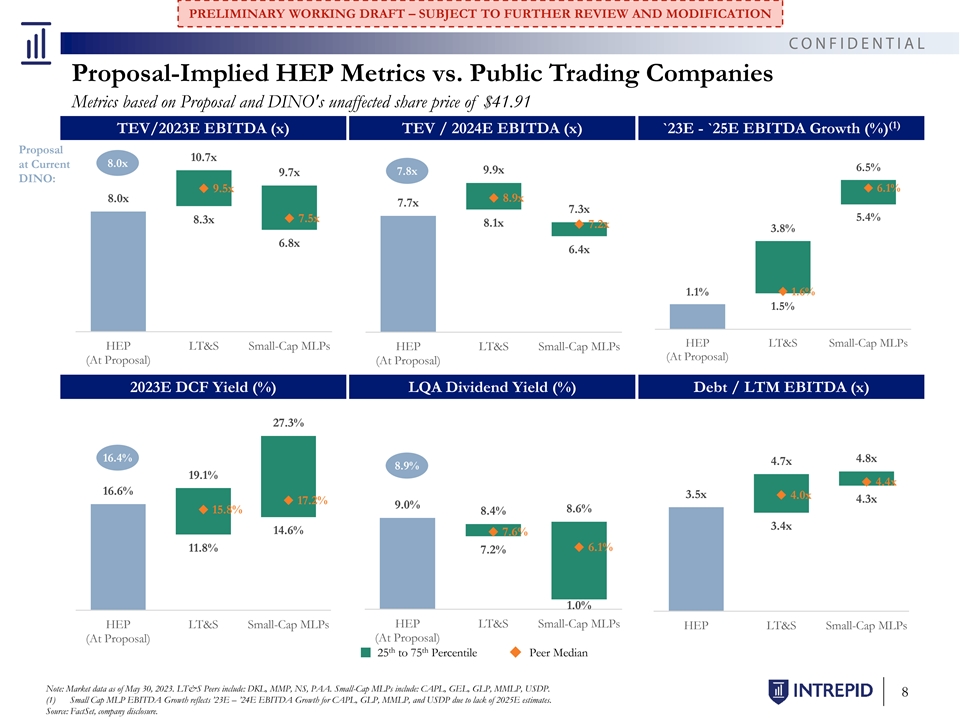

PRELIMINARY WORKING DRAFT – SUBJECT TO FURTHER REVIEW AND MODIFICATION Proposal-Implied HEP Metrics vs. Public Trading Companies Metrics based on Proposal and DINO's unaffected share price of $41.91 (1) TEV/2023E EBITDA (x) TEV / 2024E EBITDA (x) `23E - `25E EBITDA Growth (%) Proposal 10.7x 8.0x at Current 6.5% 9.9x 7.8x 9.7x DINO: 9.5x 6.1% 8.9x 8.0x 7.7x 7.3x 5.4% 7.5x 8.3x 8.1x 7.2x 3.8% 6.8x 6.4x 1.1% 1.6% 1.5% HEP LT&S Small-Cap MLPs HEP LT&S Small-Cap MLPs HEP LT&S Small-Cap MLPs (At Proposal) (At Proposal) (At Proposal) 2023E DCF Yield (%) LQA Dividend Yield (%) Debt / LTM EBITDA (x) 27.3% 16.4% 4.8x 4.7x 8.9% 19.1% 4.4x 16.6% 3.5x 4.0x 4.3x 17.2% 9.0% 8.6% 15.8% 8.4% 3.4x 14.6% 7.6% 6.1% 11.8% 7.2% 1.0% HEP LT&S Small-Cap MLPs HEP LT&S Small-Cap MLPs HEP LT&S Small-Cap MLPs (At Proposal) (At Proposal) th th 25 to 75 Percentile Peer Median Note: Market data as of May 30, 2023. LT&S Peers include: DKL, MMP, NS, PAA. Small-Cap MLPs include: CAPL, GEL, GLP, MMLP, USDP. 8 (1) Small Cap MLP EBITDA Growth reflects ’23E – ’24E EBITDA Growth for CAPL, GLP, MMLP, and USDP due to lack of 2025E estimates. Source: FactSet, company disclosure.

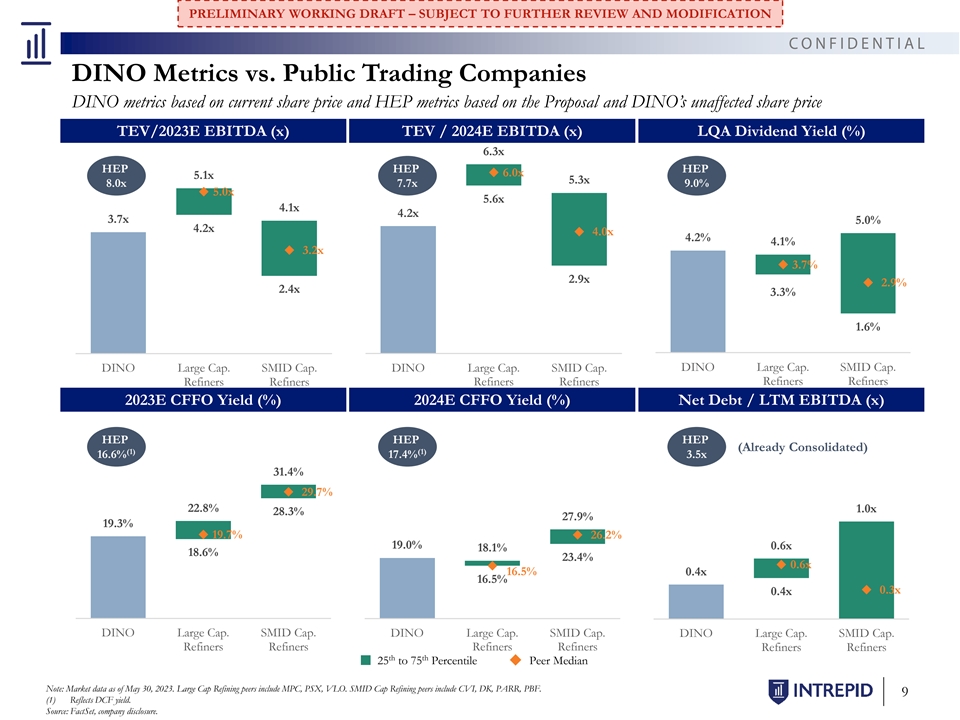

PRELIMINARY WORKING DRAFT – SUBJECT TO FURTHER REVIEW AND MODIFICATION DINO Metrics vs. Public Trading Companies DINO metrics based on current share price and HEP metrics based on the Proposal and DINO’s unaffected share price TEV/2023E EBITDA (x) TEV / 2024E EBITDA (x) LQA Dividend Yield (%) 6.3x HEP HEP HEP 6.0x 5.1x 5.3x 8.0x 7.7x 9.0% 5.0x 5.6x 4.1x 4.2x 3.7x 5.0% 4.2x 4.0x 4.2% 4.1% 3.2x 3.7% 2.9x 2.9% 2.4x 3.3% 1.6% DINO Large Cap. SMID Cap. DINO Large Cap. SMID Cap. DINO Large Cap. SMID Cap. Refiners Refiners Refiners Refiners Refiners Refiners 2023E CFFO Yield (%) 2024E CFFO Yield (%) Net Debt / LTM EBITDA (x) HEP HEP HEP (Already Consolidated) (1) (1) 16.6% 17.4% 3.5x 31.4% 29.7% 22.8% 1.0x 28.3% 27.9% 19.3% 19.7% 26.2% 19.0% 0.6x 18.1% 18.6% 23.4% 0.6x 16.5% 0.4x 16.5% 0.3x 0.4x DINO Large Cap. SMID Cap. DINO Large Cap. SMID Cap. DINO Large Cap. SMID Cap. Refiners Refiners Refiners Refiners Refiners Refiners th th 25 to 75 Percentile Peer Median Note: Market data as of May 30, 2023. Large Cap Refining peers include MPC, PSX, VLO. SMID Cap Refining peers include CVI, DK, PARR, PBF. 9 (1) Reflects DCF yield. Source: FactSet, company disclosure.

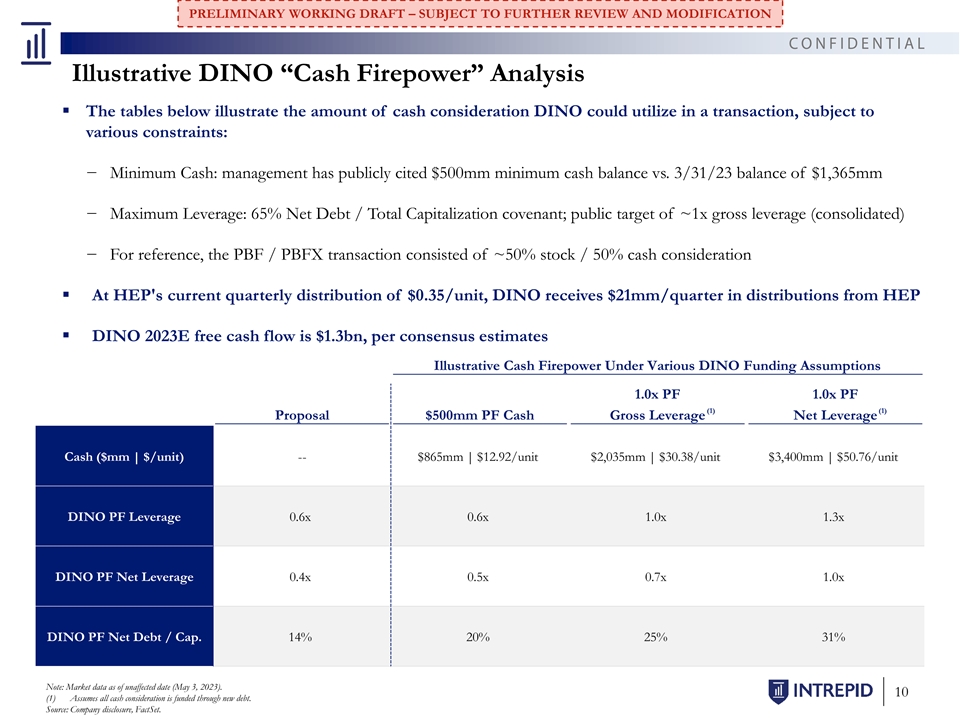

PRELIMINARY WORKING DRAFT – SUBJECT TO FURTHER REVIEW AND MODIFICATION Illustrative DINO “Cash Firepower” Analysis ▪ The tables below illustrate the amount of cash consideration DINO could utilize in a transaction, subject to various constraints: − Minimum Cash: management has publicly cited $500mm minimum cash balance vs. 3/31/23 balance of $1,365mm − Maximum Leverage: 65% Net Debt / Total Capitalization covenant; public target of ~1x gross leverage (consolidated) − For reference, the PBF / PBFX transaction consisted of ~50% stock / 50% cash consideration ▪ At HEP's current quarterly distribution of $0.35/unit, DINO receives $21mm/quarter in distributions from HEP ▪ DINO 2023E free cash flow is $1.3bn, per consensus estimates Illustrative Cash Firepower Under Various DINO Funding Assumptions 1.0x PF 1.0x PF (1) (1) Proposal $500mm PF Cash Gross Leverage Net Leverage Cash ($mm | $/unit) -- $865mm | $12.92/unit $2,035mm | $30.38/unit $3,400mm | $50.76/unit DINO PF Leverage 0.6x 0.6x 1.0x 1.3x DINO PF Net Leverage 0.4x 0.5x 0.7x 1.0x DINO PF Net Debt / Cap. 14% 20% 25% 31% Note: Market data as of unaffected date (May 3, 2023). 10 (1) Assumes all cash consideration is funded through new debt. Source: Company disclosure, FactSet.

PRELIMINARY WORKING DRAFT – SUBJECT TO FURTHER REVIEW AND MODIFICATION APPENDIX 11

PRELIMINARY WORKING DRAFT – SUBJECT TO FURTHER REVIEW AND MODIFICATION Select Research Analyst Commentary Since Announcement Select Commentary | Broker and Credit Research “[We believe it is] a starting point for negotiation. DINO follows the “However with DINO trading down 8% and HEP down 2% the market majority of its refining peers with the MLP buy-in, while we take a appears to be signaling the probability of a higher bid noting similar wait-and-see approach on its ultimate value creation. Further on the patterns for other such deals. Strategically, the deal logic is sound, as it corporate structure, under new leadership, management continues to receive removes value leakage in the form of HEP’s 8.6% distribution yield, and questions on the potential unlock of value of the Lubes business, which it preserves cash for the parent co.” appears receptive to, but perhaps only after certain organic initiatives are May 4, 2023 completed” “From DINO’s perspective, we think the buy-in will help to simplify the May 8, 2023 corporate structure and lower some costs. HEP has indicated its independent conflict committee will “review, evaluate and negotiate” the transaction, “DINO announced today a non-binding offer to purchase all outstanding which leaves the possibility that the exchange ratio could change units of HEP in a bid to simplify the company’s corporate structure, reduce modestly, in our view. We think the simplification makes sense, as the costs, and further optimize its portfolio. Consolidating the MLP into the original intent for the MLP no longer holds water given changes in corporate structure has historically been viewed as positive, in our capital market access and investor preferences” view.” May 4, 2023 May 4, 2023 “The deal may simplify structure but in our view there are no real “We would view this transaction as supportive of the company’s credit synergies so it would be dilutive for DINO shareholders. Based on ratio quality because it will streamline its corporate structure and reduce of 0.3714, we estimate DINO will have to issue 24.8M new shares which some cash leakage at HEP associated with its status as a public entity. equates to 12.7% increase in share count. If DINO raises the bid by 10% to Our rating on DINO is unchanged because it reflects our view of the close this deal (as we have seen with some prior transactions), then enterprise on a consolidated basis, including HEP.” ratio would move to 0.40.” May 4, 2023 May 4, 2023 “The ratings of HF Sinclair are unchanged by its offer to acquire the “The deal looks less attractive on an EV/EBITDA multiple, with DINO publicly held common units of HEP. HEP’s debt is already consolidated trading at ~5x our 2025 normalized EBITDA and HEP at >8x. The on HF Sinclair's balance sheet and factored into our credit analysis of HF discrepancy between the two methodologies is due to HEP distributing a Sinclair… HEP’s ratings are not likely to be downgraded given the portion of FCF. We believe FCF is more representative of the deal's likelihood that the proposed acquisition will close.” value.” May 8, 2023 May 4, 2023 12 Source: Wall Street research, Bloomberg, FactSet.

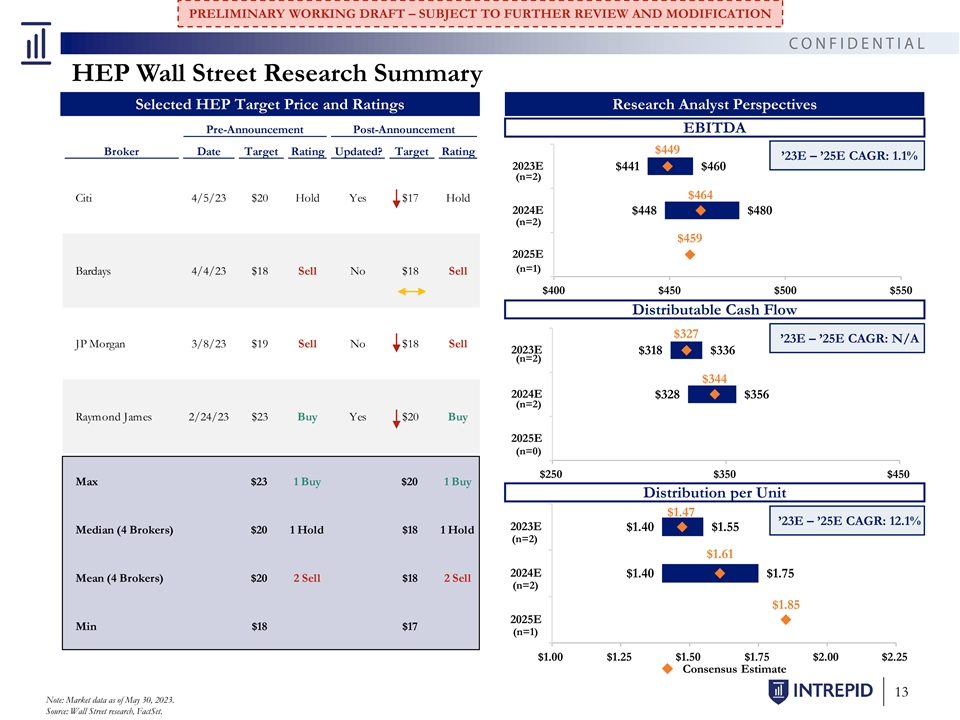

PRELIMINARY WORKING DRAFT – SUBJECT TO FURTHER REVIEW AND MODIFICATION HEP Wall Street Research Summary Selected HEP Target Price and Ratings Research Analyst Perspectives Pre-Announcement Post-Announcement EBITDA $449 Broker Date Target Rating Updated? Target Rating ’23E – ’25E CAGR: 1.1% 2023E $441 $460 (n=2) $464 Citi 4/5/23 $20 Hold Yes $17 Hold 2024E $448 $480 (n=2) $459 2025E (n=1) Barclays 4/4/23 $18 Sell No $18 Sell $400 $450 $500 $550 Distributable Cash Flow $327 ’23E – ’25E CAGR: N/A JP Morgan 3/8/23 $19 Sell No $18 Sell 2023E $318 $336 (n=2) $344 2024E $328 $356 (n=2) Raymond James 2/24/23 $23 Buy Yes $20 Buy 2025E (n=0) $250 $350 $450 Max $23 1 Buy $20 1 Buy Distribution per Unit $1.47 ’23E – ’25E CAGR: 12.1% 2023E $1.40 $1.55 Median (4 Brokers) $20 1 Hold $18 1 Hold (n=2) $1.61 2024E $1.40 $1.75 Mean (4 Brokers) $20 2 Sell $18 2 Sell (n=2) $1.85 2025E Min $18 $17 (n=1) $1.00 $1.25 $1.50 $1.75 $2.00 $2.25 Consensus Estimate 13 Note: Market data as of May 30, 2023. Source: Wall Street research, FactSet.

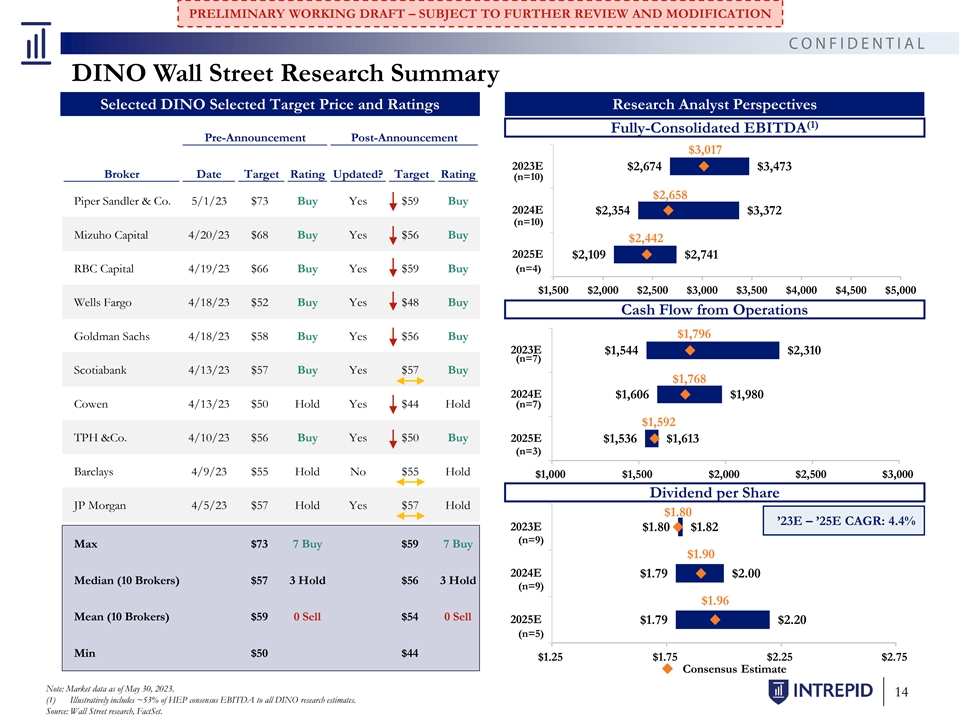

PRELIMINARY WORKING DRAFT – SUBJECT TO FURTHER REVIEW AND MODIFICATION DINO Wall Street Research Summary Selected DINO Selected Target Price and Ratings Research Analyst Perspectives (1) Fully-Consolidated EBITDA Pre-Announcement Post-Announcement $3,017 2023E $2,674 $3,473 Broker Date Target Rating Updated? Target Rating (n=10) $2,658 Piper Sandler & Co. 5/1/23 $73 Buy Yes $59 Buy 2024E $2,354 $3,372 (n=10) Mizuho Capital 4/20/23 $68 Buy Yes $56 Buy $2,442 2025E $2,109 $2,741 RBC Capital 4/19/23 $66 Buy Yes $59 Buy (n=4) $1,500 $2,000 $2,500 $3,000 $3,500 $4,000 $4,500 $5,000 Wells Fargo 4/18/23 $52 Buy Yes $48 Buy Cash Flow from Operations $1,796 Goldman Sachs 4/18/23 $58 Buy Yes $56 Buy 2023E $1,544 $2,310 (n=7) Scotiabank 4/13/23 $57 Buy Yes $57 Buy $1,768 2024E $1,606 $1,980 Cowen 4/13/23 $50 Hold Yes $44 Hold (n=7) $1,592 TPH &Co. 4/10/23 $56 Buy Yes $50 Buy 2025E $1,536 $1,613 (n=3) Barclays 4/9/23 $55 Hold No $55 Hold $1,000 $1,500 $2,000 $2,500 $3,000 Dividend per Share JP Morgan 4/5/23 $57 Hold Yes $57 Hold $1.80 ’23E – ’25E CAGR: 4.4% 2023E $1.80 $1.82 (n=9) Max $73 7 Buy $59 7 Buy $1.90 2024E $1.79 $2.00 Median (10 Brokers) $57 3 Hold $56 3 Hold (n=9) $1.96 Mean (10 Brokers) $59 0 Sell $54 0 Sell 2025E $1.79 $2.20 (n=5) Min $50 $44 $1.25 $1.75 $2.25 $2.75 Consensus Estimate Note: Market data as of May 30, 2023. 14 (1) Illustratively includes ~53% of HEP consensus EBITDA to all DINO research estimates. Source: Wall Street research, FactSet.

PRELIMINARY WORKING DRAFT – SUBJECT TO FURTHER REVIEW AND MODIFICATION Disclaimer These materials have been prepared by Intrepid Partners, LLC (“Intrepid”) for the Conflicts Committee (the “Committee”) of the Board of Directors of Holly Logistic Services, L.L.C. (the “General Partner”), the ultimate general partner of Holly Energy Partners, L.P. (“HEP”), to whom such materials are directly addressed and delivered. These materials are confidential and may not be used or relied upon by any other person or for any purpose other than as specifically contemplated by a written agreement with Intrepid. These materials have been developed by and are proprietary to Intrepid and were prepared exclusively for the benefit and internal use of the Committee in connection with evaluating the Proposed Transaction with HEP and HF Sinclair Corporation (“DINO”). These materials are based upon information provided by or on behalf of the management of DINO and the General Partner, from public sources, or otherwise reviewed by Intrepid. Intrepid has relied upon and assumes no responsibility for independent investigation or verification of such information and has relied upon such information being complete and accurate in all material respects. To the extent such information includes estimates and forecasts of future performance prepared by or reviewed with management of DINO or the General Partner and/or other potential transaction participants or obtained from public sources, Intrepid has assumed that such estimates and forecasts have been reasonably prepared on bases reflecting the best currently available estimates and judgments of management of DINO, and the General Partner or such other potential transaction participants (or, with respect to estimates and forecasts obtained from public sources, represent reasonable estimates). Actual results may differ materially from such estimates and forecasts. No representation or warranty, express or implied, is made as to the accuracy or completeness of such information, and nothing contained herein is, or shall be relied upon as, a representation or warranty, whether as to the past, the present or the future. The materials and related commentary are not intended to provide the only basis for evaluating, and should not be considered a recommendation with respect to, the consideration paid, the proposed transaction or any transaction or other matter. These materials are also subject to the qualifications and limitations described in any accompanying written opinion letter. These materials were compiled on a confidential basis solely for use by the Committee and may not be relied on by any other party (including stakeholders in either entity), even if such parties are provided a copy of these materials. These materials were prepared without a view to public disclosure or filing thereof under state or federal laws, and may not be redistributed, reproduced, distributed, passed to others, transmitted, quoted or referred to, in whole or in part, without the prior written permission of Intrepid in accordance with the terms of our engagement letter with the Committee. These materials speak only as of the date on the cover and Intrepid assumes no obligation to update these materials or inform any recipient of changed circumstances, events or information. These materials were prepared for a specific use by specific persons and were not prepared to conform with any disclosure standards under securities laws or otherwise. In the ordinary course of its business, each of Intrepid and its affiliates may actively trade or hold the securities of DINO, HEP or other parties involved in a proposed transaction for its own account or for the account of its customers and, accordingly, may at any time hold a long or short position in such securities. Intrepid will receive a fee in connection with delivery of an opinion relating to the proposed transaction. These materials do not constitute, nor do they form part of, an offer or solicitation to sell or purchase any securities or instruments and are not a commitment by Intrepid or any of its affiliates to provide, arrange or underwrite any financing for any transaction or to purchase any security in connection therewith. These materials may not reflect information known to other professionals in other business areas of Intrepid and its affiliates. Intrepid and its affiliates do not provide legal, regulatory, accounting, bankruptcy, securities or tax advice. Any statements contained herein as to tax matters were neither written nor intended by Intrepid or its affiliates to be used and cannot be used by any taxpayer for the purpose of avoiding tax penalties that may be imposed on such taxpayer. Each person should seek legal, regulatory accounting and tax advice based on his, her or its particular circumstances from independent advisors regarding the evaluation and impact of any transactions or matters described herein.