EXHIBIT 99.2

CUSTOMER METRICS

Branded Postpaid Customers

| |

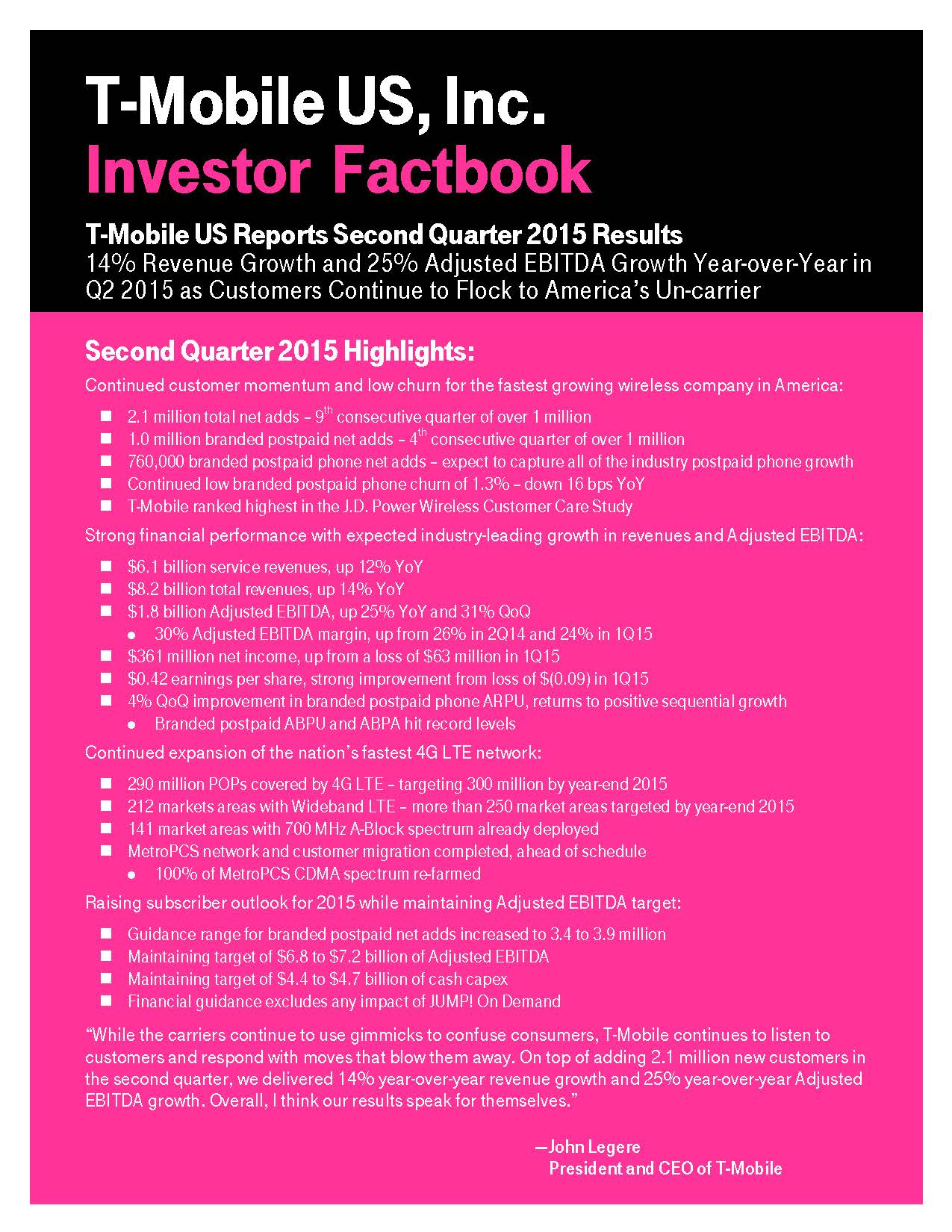

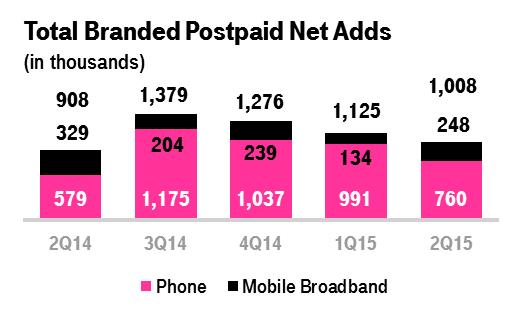

| ▪ | Branded postpaid net customer additions were 1,008,000 in the second quarter of 2015 compared to 1,125,000 in the first quarter of 2015 and 908,000 in the second quarter of 2014. This marked the fourth consecutive quarter in which branded postpaid net customer additions were greater than one million, a clear indicator of the continued success of the Un-carrier initiatives and strong uptake of promotions for services and devices. |

| |

| ▪ | T-Mobile is expected to again lead the industry in branded postpaid phone net customer additions with 760,000 in the second quarter of 2015, compared to 991,000 in the first quarter of 2015 and 579,000 in the second quarter of 2014. Branded postpaid phone gross additions in the second quarter of 2015 declined by 9% on a sequential basis, but were up 9% year-over-year. T-Mobile is expected to have captured all of the industry’s postpaid phone growth in the second quarter of 2015. |

| |

| ▪ | Branded postpaid mobile broadband net customer additions were 248,000 in the second quarter of 2015, compared to 134,000 in the first quarter of 2015 and 329,000 in the second quarter of 2014. |

| |

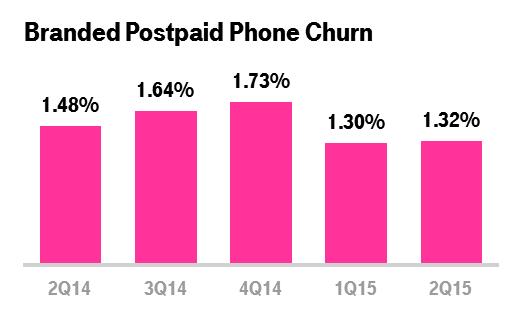

| ▪ | Branded postpaid phone churn was 1.32% in the second quarter of 2015, down 16 basis points compared to 1.48% in the second quarter of 2014 and up two basis points compared to 1.30% in the first quarter of 2015. The year-over-year improvement reflects ongoing improvements in the Company’s network, customer service, and the overall value of its offerings in the marketplace, resulting in increased customer satisfaction and loyalty. |

Branded Prepaid Customers

| |

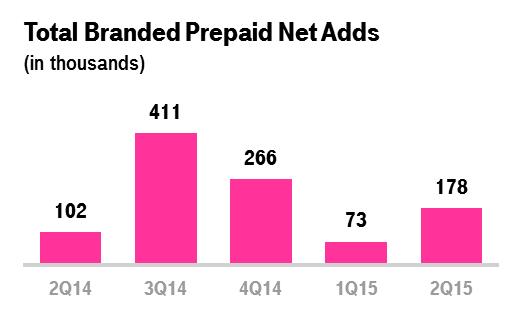

| ▪ | Branded prepaid net customer additions were 178,000 in the second quarter of 2015, compared to 73,000 in the first quarter of 2015 and 102,000 in the second quarter of 2014. The higher level of branded prepaid net customer additions in the second quarter of 2015 was driven by successful promotions for services and devices and slightly lower sequential customer migrations from branded prepaid to branded postpaid. |

| |

| ▪ | Migrations to branded postpaid plans reduced branded prepaid net customer additions in the second quarter of 2015 by approximately 175,000, down from 195,000 in the first quarter of 2015 and up from 85,000 in the second quarter of 2014. |

| |

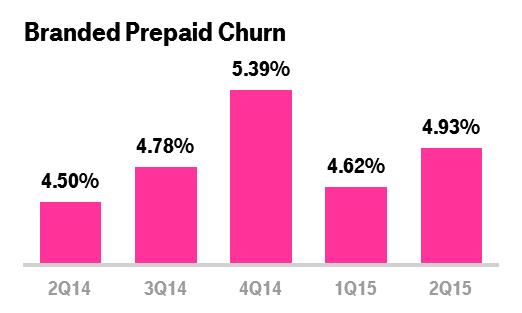

| ▪ | Branded prepaid churn was 4.93% in the second quarter of 2015, up 31 basis points from 4.62% in the first quarter of 2015 and up 43 basis points from 4.50% in the second quarter of 2014. Sequentially and year-over-year, the increase in churn was principally due to ongoing competitive activity in the marketplace. |

Total Branded Customers

| |

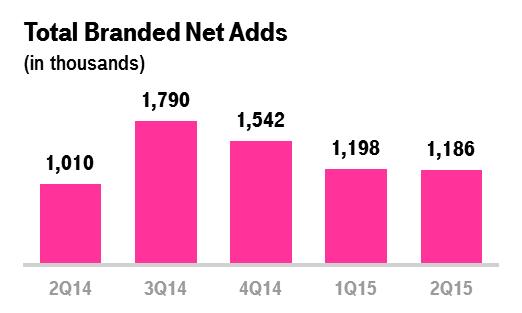

| ▪ | Total branded net customer additions were 1,186,000 in the second quarter of 2015 compared to 1,198,000 in the first quarter of 2015 and 1,010,000 in the second quarter of 2014. This was the sixth consecutive quarter in which branded net customer additions surpassed the one million milestone. |

Wholesale Customers

| |

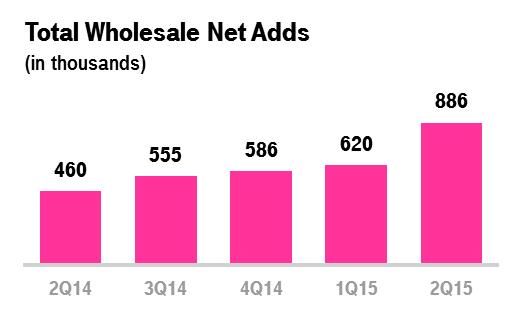

| ▪ | Total wholesale net customer additions were 886,000 in the second quarter of 2015 compared to 620,000 in the first quarter of 2015 and 460,000 in the second quarter of 2014. |

| |

| ▪ | MVNO net customer additions were 919,000 in the second quarter of 2015 compared to 479,000 in the first quarter of 2015 and 235,000 in the second quarter of 2014. |

| |

| ▪ | M2M net customer losses were 33,000 in the second quarter of 2015 compared to net customer additions of 141,000 in the first quarter of 2015 and 225,000 in the second quarter of 2014. |

Total Customers

| |

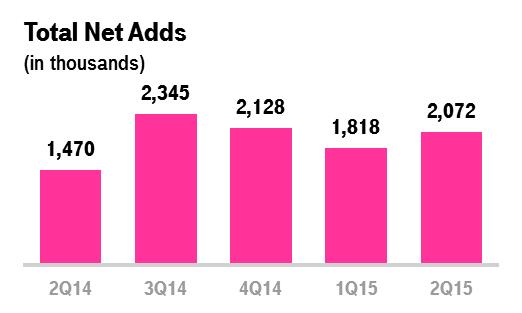

| ▪ | Total net customer additions were 2,072,000 in the second quarter of 2015 compared to 1,818,000 in the first quarter of 2015 and 1,470,000 in the second quarter of 2014. This was the ninth consecutive quarter in which total net customer additions exceeded one million. It was also the fourth time in the last six quarters in which total net customer additions exceeded two million. |

| |

| ▪ | Since the launch of its first Un-carrier initiative nine quarters ago, T-Mobile has added more than 16 million total customers. |

| |

| ▪ | T-Mobile ended the second quarter of 2015 with more than 58.9 million total customers. |

NETWORK

Network Modernization Update

| |

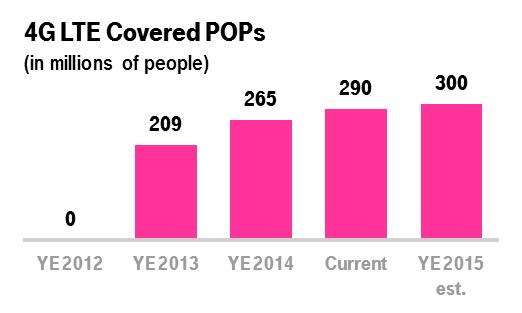

| ▪ | T-Mobile’s 4G LTE network now covers 290 million people, up from 275 million at the end of the first quarter of 2015 and 233 million at the end of the second quarter of 2014. |

| |

| ▪ | The Company is targeting a total 4G LTE population coverage of 300 million people by year-end 2015. During 2015, the Company expects to add one million square miles of territory under its 4G LTE coverage. |

| |

| ▪ | Wideband LTE, which refers to markets that have bandwidth of at least 15+15 MHz dedicated to 4G LTE, is currently available in 212 market areas and is now expected to be available in more than 250 market areas by year-end 2015. Customers in Wideband LTE markets are regularly observing peak speeds in the 70 Mbps range, with maximum real-world speeds in excess of 145 Mbps. |

Network Speed

| |

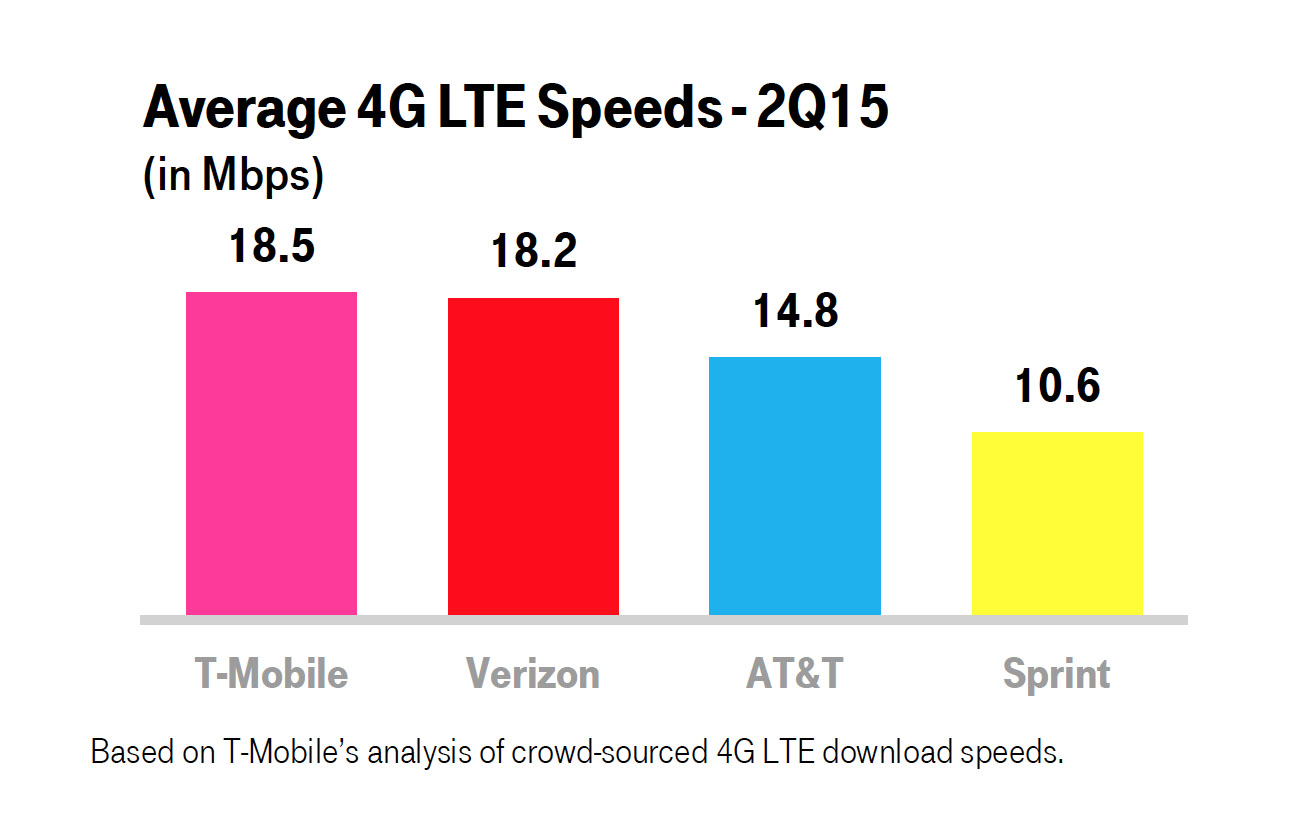

| ▪ | T-Mobile has the fastest nationwide 4G LTE network in the U.S. based on download speeds from millions of user- generated tests. This is the sixth consecutive quarter that T-Mobile has led the industry in average download speeds. |

| |

| ▪ | In the second quarter of 2015, T-Mobile’s average 4G LTE download speed was 18.5 Mbps compared to Verizon at 18.2 Mbps, AT&T at 14.8 Mbps, and Sprint at 10.6 Mbps. |

Spectrum

| |

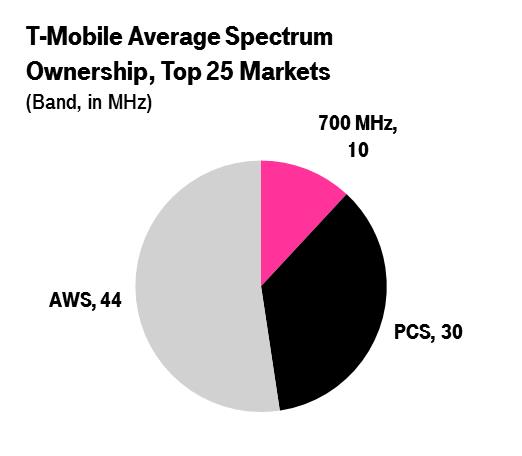

| ▪ | At the end of the second quarter of 2015, T-Mobile owned an average of 84 MHz of spectrum across the top 25 markets in the U.S. The spectrum is comprised of an average of 10 MHz in the 700 MHz band, 30 MHz in the 1900 MHz PCS band, and 44 MHz in the AWS band. |

| |

| ▪ | The Company expects to participate in future FCC spectrum auctions including the broadcast incentive auction. |

A-Block Update

| |

| ▪ | T-Mobile owns 700 MHz A-Block spectrum covering 190 million people or approximately 60% of the U.S. population and approximately 70% of the Company’s existing branded customer base. The spectrum covers 9 of the top 10 market areas and 24 of the top 30 market areas in the U.S. |

| |

| ▪ | Approximately 98% of the population covered by the Company’s A-Block spectrum is free and clear and ready to be deployed or will be ready for deployment in 2015. That is up from approximately 50% at the time of the original A-Block spectrum purchase from Verizon in the first quarter of 2014. |

| |

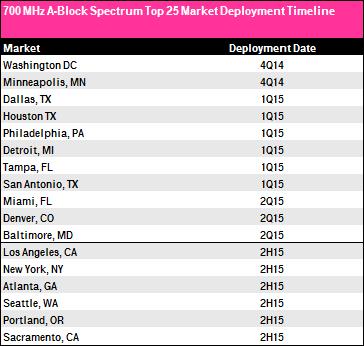

| ▪ | T-Mobile has deployed its 700 MHz A-Block spectrum in 141 market areas. New launches in the second quarter of 2015 included the cities of Miami, Denver, Baltimore, Kansas City, Austin, and West Palm Beach. The Company plans to continue to aggressively roll-out new 700 MHz sites with new launches planned for Los Angeles, New York, Atlanta, Seattle, Portland, and Sacramento in 2015, among others. |

METROPCS

| |

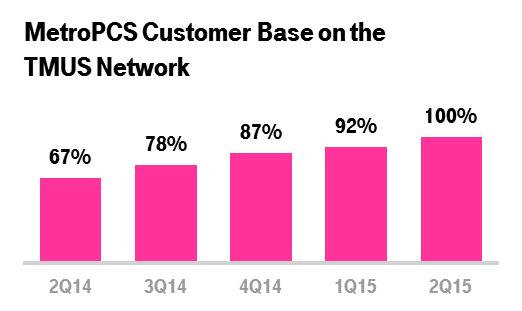

| ▪ | On July 1, 2015, T-Mobile officially completed the shutdown of the MetroPCS CDMA network with the decommissioning of the CDMA portion of the MetroPCS networks in Dallas, New York, Miami, Jacksonville, Orlando, and Tampa. Since the close of the business combination in May 2013, nearly 9 million legacy MetroPCS customers have been migrated to the T-Mobile network. |

| |

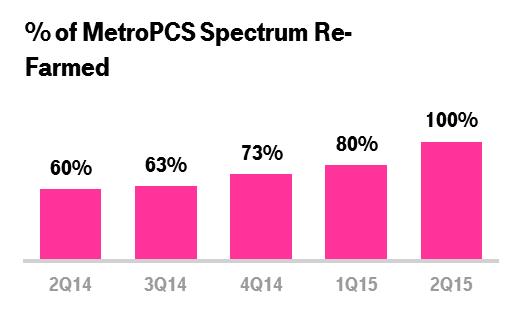

| ▪ | 100% of the MetroPCS spectrum on a MHz/POP basis has now been re-farmed and integrated into the T-Mobile network, compared to 80% at the end of the first quarter of 2015. |

| |

| ▪ | Total decommissioning costs for CDMA network shutdowns were $34 million in the second quarter of 2015, compared to $128 million in total decommissioning costs in the first quarter of 2015. The sequential decrease in total decommissioning costs was primarily due to the timing of the CDMA network shutdowns. Typically, there is a lag of approximately 3 to 6 months between network shutdown and the recognition of decommissioning costs and realization of synergies. |

| |

| ▪ | The Company expects to incur additional network decommissioning costs in the range of $350 to $450 million with substantially all the costs to be recognized through the rest of 2015. Network decommissioning costs primarily relate to the acceleration of lease costs for decommissioned cell sites and are excluded from Adjusted EBITDA. |

UN-CARRIER INITIATIVES

| |

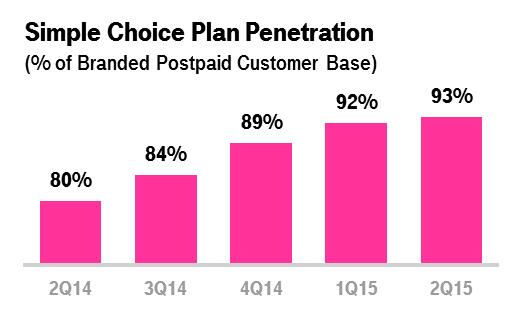

| ▪ | At the end of the second quarter of 2015, 93% of the branded postpaid customer base was on a Simple Choice plan, up from 92% at the end of the first quarter of 2015 and 80% at the end of the second quarter of 2014. |

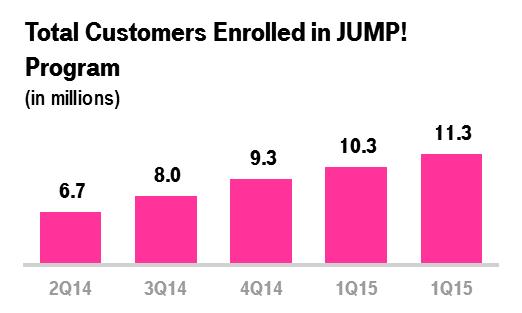

| |

| ▪ | At the end of the second quarter of 2015, 11.3 million customers were enrolled in the JUMP! program, up from 10.3 million at the end of the first quarter of 2015 and 6.7 million at the end of the second quarter of 2014. |

Un-carrier Updates

| |

| ▪ | JUMP! On Demand: On June 28, 2015, T-Mobile updated its JUMP! program to enable customers to have a low monthly payment that covers the cost of leasing a new device plus the freedom to swap their leased device for a new one up to three times in twelve months with no extra fee. Under this program, at lease inception, devices are transferred from inventory to property and equipment. Devices are then depreciated to their estimated residual value. Revenues associated with the leased devices are recognized over the term of the lease. |

| |

| ▪ | Mobile without Borders: This program, launched on July 15, 2015, expands the benefits of T-Mobile’s Simple Choice plan by extending coverage and calling across the U.S, Canada, and Mexico at no extra charge. The upgrade makes Simple Choice the first and only wireless plan to span the entire continent. |

| |

| ▪ | 10 GB for All: On July 15, 2015, T-Mobile updated its Family Plan program to enable qualifying family plan customers to get 10 GB of 4G LTE data at a great rate. Plans start at $100 per month for two lines each with up to 10 GB of 4G LTE data and each additional line is $20 per month. For a limited time, the fourth line is free. |

| |

| ▪ | Amping Music Freedom and iPhone®: On July 28, 2015, T-Mobile updated its Music Freedom program by adding Apple Music to its list of services that stream free on T-Mobile. In addition, every customer who gets a new iPhone 6 with JUMP! On Demand™ this summer can lock in the promotional price of $15 per month and simply swap it for the next comparable iPhone, if they upgrade before the end of the year. Lastly, all customers who get a new iPhone 6 with JUMP! On Demand will have exclusive priority access among T-Mobile’s customers to the next iPhone. |

DEVICES

| |

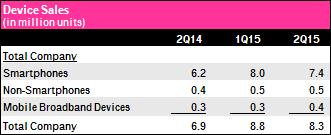

| ▪ | Total device sales were 8.3 million units in the second quarter of 2015 compared to 8.8 million units in the first quarter of 2015 and 6.9 million units in the second quarter of 2014. |

| |

| ▪ | Total smartphone sales were 7.4 million units in the second quarter of 2015 compared to 8.0 million units in the first quarter of 2015 and 6.2 million units in the second quarter of 2014. |

| |

| ▪ | The upgrade rate for branded postpaid customers was approximately 9% in the second quarter of 2015 compared to approximately 8% in the first quarter of 2015 and approximately 8% in the second quarter of 2014. |

EQUIPMENT INSTALLMENT PLANS (EIP)

| |

| ▪ | T-Mobile financed $1.697 billion of equipment sales on EIP in the second quarter of 2015, up 14.4% from $1.483 billion in the first quarter of 2015 and up 26.5% from $1.342 billion in the second quarter of 2014. The sequential and year-over-year increase was due to higher gross customer additions, growth in devices financed through EIP, including customers choosing to JUMP!, and a higher average price per device sold. |

| |

| ▪ | Customers on Simple Choice plans had associated EIP billings of $1.393 billion in the second quarter of 2015, up 7.8% from $1.292 billion in the first quarter of 2015 and up 72.0% from $810 million in the second quarter of 2014. |

| |

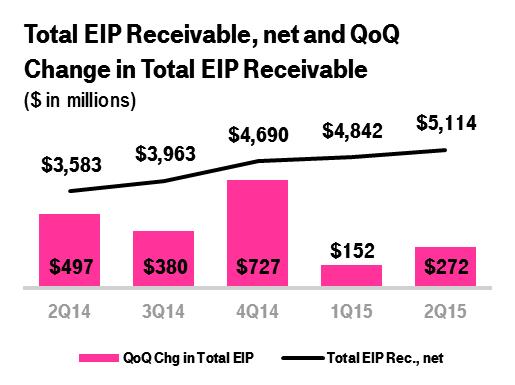

| ▪ | Total EIP receivables, net of imputed discount and allowances for credit losses, were $5.114 billion at the end of the second quarter of 2015 compared to $4.842 billion at the end of the first quarter of 2015 and $3.583 billion at the end of the second quarter of 2014. The $272 million sequential increase in total EIP receivables, net in the second quarter of 2015 was higher than the sequential increase of $152 million in the first quarter of 2015, and reflects growth in devices financed through EIP. |

| |

| ▪ | The Company continues to expect that the growth in total EIP receivables, net will moderate significantly in 2015 compared to 2014. |

CUSTOMER QUALITY

| |

| ▪ | EIP receivables classified as Prime were 52% of total EIP receivables at the end of the second quarter of 2015, flat from the prior quarter and down one percentage point compared to the end of the second quarter of 2014. |

| |

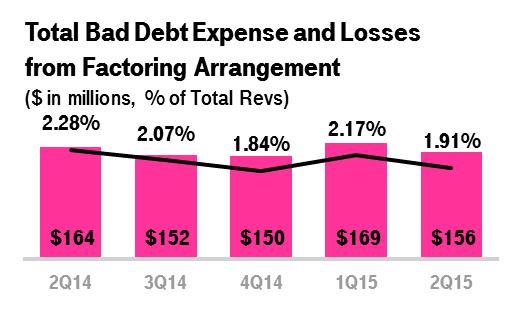

| ▪ | Total bad debt expense and losses from the factoring arrangement was $156 million in the second quarter of 2015 compared to $169 million in the first quarter of 2015 and $164 million in the second quarter of 2014. Year-over-year, total bad debt expense and losses from the factoring arrangement as a percentage of total revenues decreased 37 basis points. Sequentially, total bad debt expense and losses from the factoring arrangement as a percentage of total revenues decreased 26 basis points, primarily due to a non-recurring impact from a change to the factoring arrangement in the first quarter of 2015. |

REVENUE METRICS

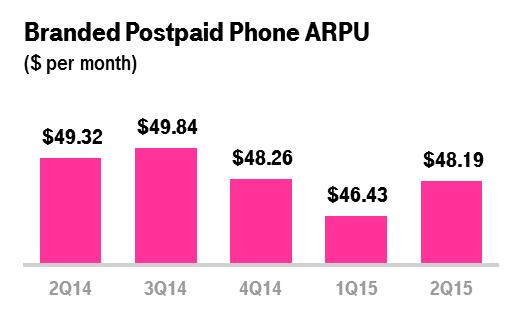

Branded Postpaid Phone ARPU

| |

| ▪ | Branded postpaid phone ARPU was $48.19 in the second quarter of 2015, up 3.8% from $46.43 in the first quarter of 2015 and down 2.3% from $49.32 in the second quarter of 2014. Sequentially, the increase in branded postpaid phone ARPU was primarily due to the non-cash net revenue deferrals for Data Stash recognized in the first quarter of 2015. Year-over-year, the decrease was primarily due to dilution from continued growth of customers on Simple Choice plans and promotions targeting multiple phone lines, including the “4 for $100” offer. |

| |

| ▪ | Excluding the impacts of the non-cash net revenue deferrals for Data Stash, branded postpaid phone ARPU increased 1.0% sequentially. |

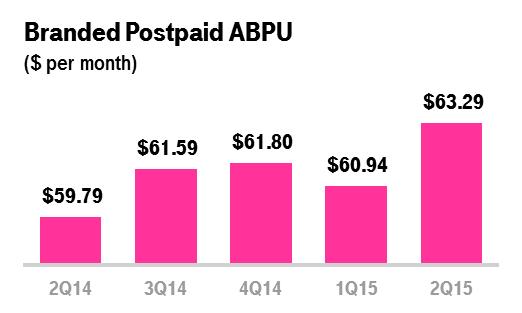

Branded Postpaid ABPU

| |

| ▪ | Branded postpaid ABPU was a record $63.29 in the second quarter of 2015, up 3.9% from $60.94 in the first quarter of 2015 and up 5.9% from $59.79 in the second quarter of 2014. Sequentially, the increase in branded postpaid ABPU was primarily due to the non-cash net revenue deferrals for Data Stash recognized in the first quarter of 2015 and growth in EIP billings on a per user basis. Year-over-year, the increase was primarily due to growth in EIP billings on a per user basis, offset in part by lower branded postpaid phone ARPU. |

| |

| ▪ | Excluding the impacts of the non-cash net revenue deferrals for Data Stash, branded postpaid ABPU increased 1.7% sequentially. |

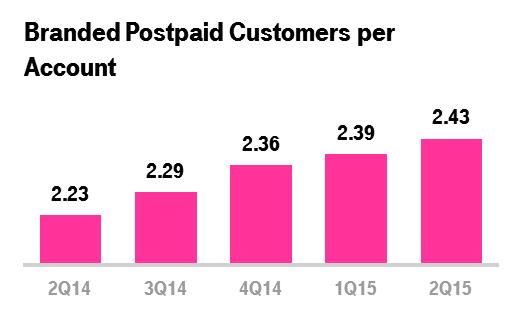

Branded Postpaid Customers per Account

| |

| ▪ | Branded postpaid customers per account was 2.43 at the end of the second quarter of 2015, compared to 2.39 at the end of the first quarter of 2015 and 2.23 at the end of the second quarter of 2014. The sequential and year-over-year increase was primarily a result of service promotions targeting multiple phone lines, including the “4 for $100” offer, and increased penetration of mobile broadband devices. |

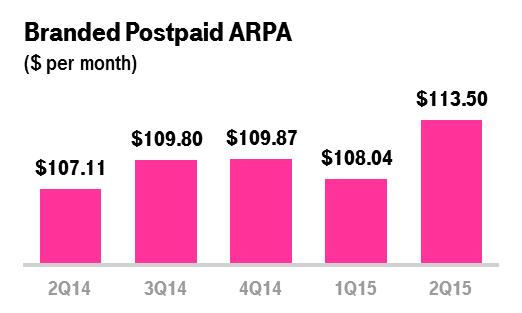

Branded Postpaid ARPA

| |

| ▪ | Branded postpaid ARPA was $113.50 in the second quarter of 2015, up 5.1% from $108.04 in the first quarter of 2015 and up 6.0% from $107.11 in the second quarter of 2014. Sequentially, the increase in branded postpaid ARPA was primarily due to the non-cash net revenue deferrals for Data Stash recognized in the first quarter of 2015 and an increase in the number of branded postpaid customers per account. Year-over-year, the increase was primarily due to higher regulatory program revenues and an increase in the number of branded postpaid customers per account, partially offset by dilution from continued growth of customers on promotions targeting multiple phone lines, including the “4 for $100” offer. |

| |

| ▪ | Excluding the impacts of the non-cash net revenue deferrals for Data Stash, branded postpaid ARPA increased 2.1% sequentially. |

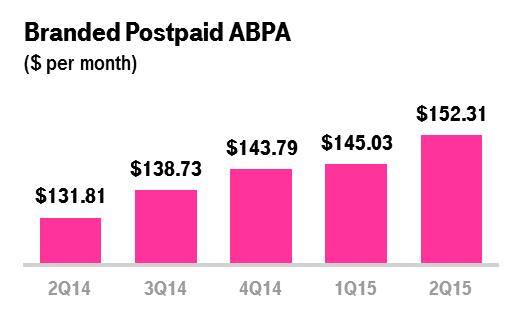

Branded Postpaid ABPA

| |

| ▪ | Branded postpaid ABPA was a record $152.31 in the second quarter of 2015, up 5.0% from $145.03 in the first quarter of 2015 and up 15.6% from $131.81 in the second quarter of 2014. Sequentially, the increase in branded postpaid ABPA was primarily due to the non-cash net revenue deferrals for Data Stash recognized in the first quarter of 2015, growth in EIP billings, and an increase in the number of branded postpaid customers per account. Year-over-year, the increase was primarily due to growth in EIP billings and an increase in the number of branded postpaid customers per account. |

| |

| ▪ | Excluding the impacts of the non-cash net revenue deferrals for Data Stash, branded postpaid ABPA increased 2.8% sequentially. |

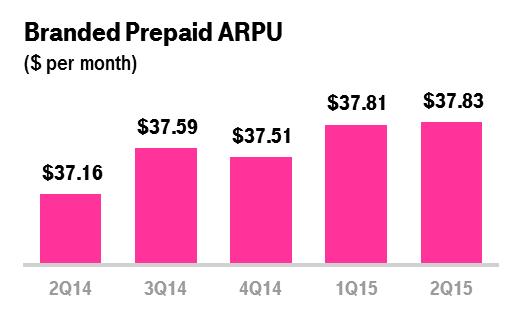

Branded Prepaid ARPU

| |

| ▪ | Branded prepaid ARPU was $37.83 in the second quarter of 2015, essentially flat from $37.81 in the first quarter of 2015 and up 1.8% from $37.16 in the second quarter of 2014. Year-over-year, the increase in branded prepaid ARPU was primarily due to an increase in data attach rates. |

REVENUES

Service Revenues

| |

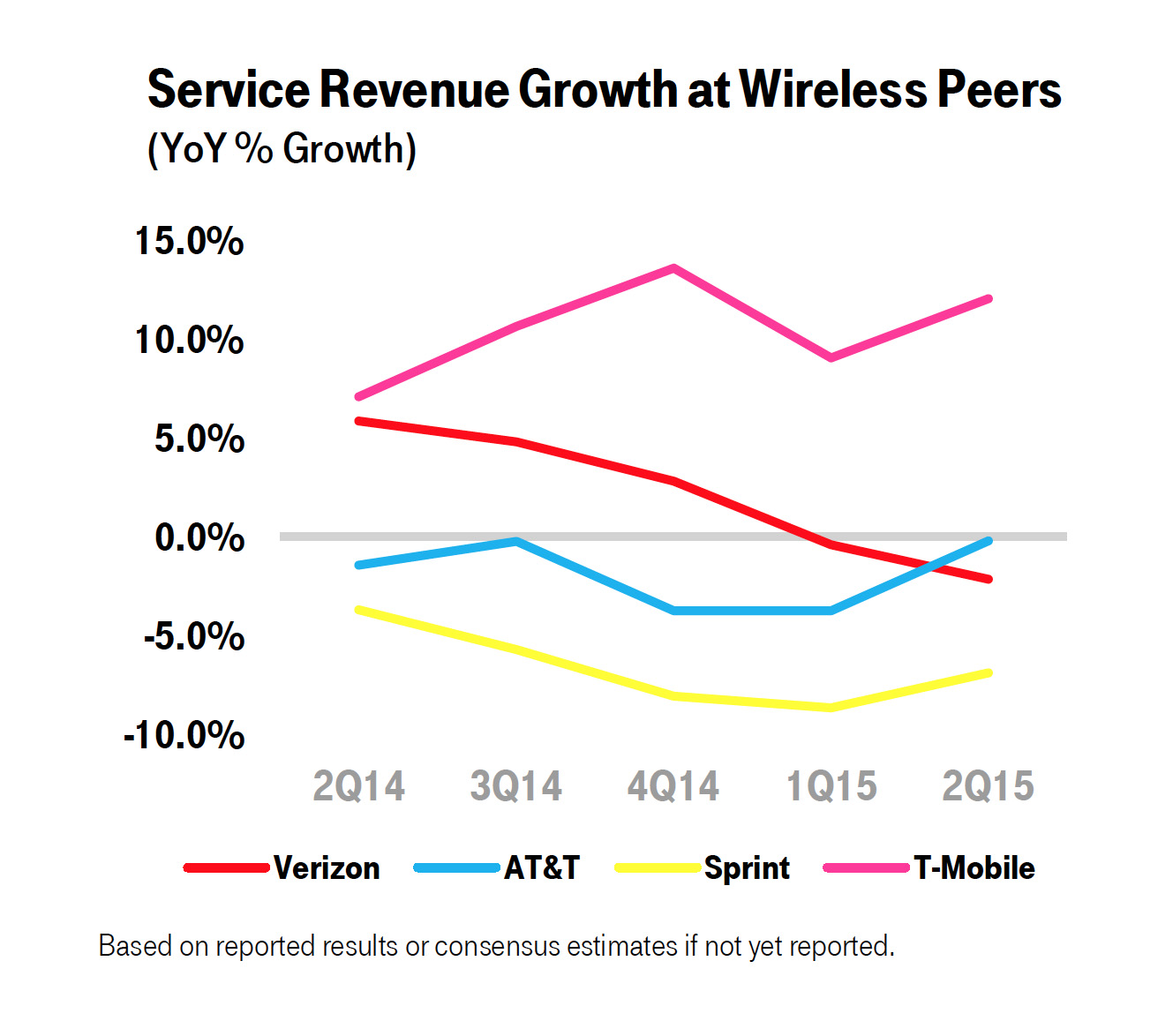

| ▪ | T-Mobile is expected to again lead the industry in year-over-year service revenue growth in the second quarter of 2015. This would mark the fifth consecutive quarter that T-Mobile has led the industry in year-over-year service revenue growth. |

| |

| ▪ | Service revenues were $6.144 billion in the second quarter of 2015, up 5.6% from $5.819 billion in the first quarter of 2015 and up 12.0% from $5.484 billion in the second quarter of 2014. The year-over-year service revenue growth of 12.0% was an acceleration in the growth rate of three percentage points compared to the first quarter of 2015. |

| |

| ▪ | Sequentially, the increase in service revenues was primarily due to growth in the Company’s customer base from the continued success of T-Mobile’s Un-carrier initiatives and strong customer response to promotional activities targeting families as well as the non-cash net revenue deferrals for Data Stash recognized in the first quarter of 2015. |

| |

| ▪ | Year-over-year, the increase in service revenues was primarily due to growth in the Company’s customer base from the continued success of T-Mobile’s Un-carrier initiatives as well as the success of the MetroPCS brand, partially offset by lower branded postpaid phone ARPU. |

| |

| ▪ | Excluding the impacts of the non-cash net revenue deferrals for Data Stash, service revenues increased 3.7% sequentially. |

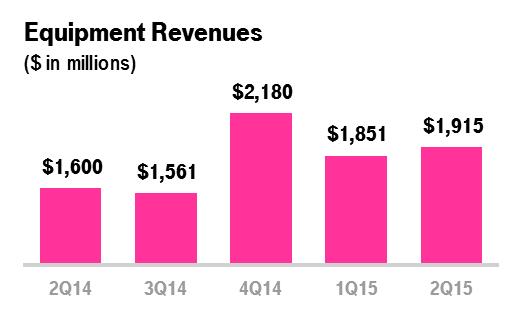

Equipment Revenues

| |

| ▪ | Equipment revenues were $1.915 billion in the second quarter of 2015, up 3.5% from $1.851 billion in the first quarter of 2015 and up 19.7% from $1.600 billion in the second quarter of 2014. |

| |

| ▪ | Sequentially, the increase in equipment revenues was primarily due to a higher average revenue per device sold, partially offset by a decrease in the number of devices sold. |

| |

| ▪ | Year-over-year, the increase in equipment revenues was primarily due to an increase in the number of devices sold, including higher device upgrade volumes. |

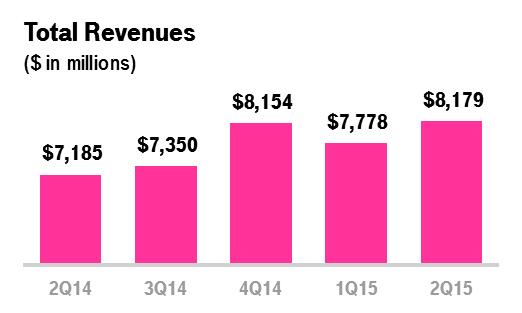

Total Revenues

| |

| ▪ | T-Mobile is expected to again lead the industry in year-over-year total revenue growth in the second quarter of 2015. |

| |

| ▪ | Total revenues were $8.179 billion in the second quarter of 2015, up 5.2% from $7.778 billion in the first quarter of 2015 and up 13.8% from $7.185 billion in the second quarter of 2014. |

OPERATING EXPENSES

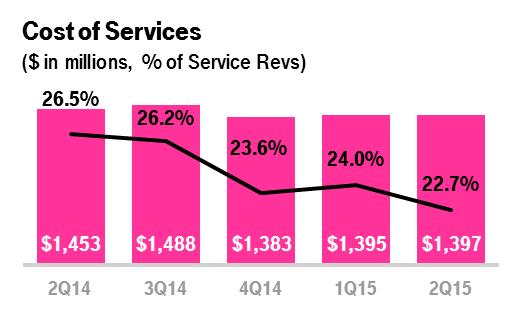

Cost of Services

| |

| ▪ | Cost of services was $1.397 billion in the second quarter of 2015, essentially flat compared to $1.395 billion in the first quarter of 2015 and down 3.9% from $1.453 billion in the second quarter of 2014. Sequentially, increases in cost of services due to the network expansion and 700 MHz A-Block build out were largely offset by lower lease expense. The year-over-year decrease was primarily due to network synergies realized from the decommissioning of the MetroPCS CDMA network. |

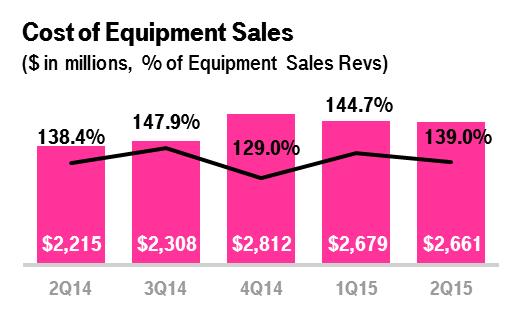

Cost of Equipment Sales

| |

| ▪ | Cost of equipment sales was $2.661 billion in the second quarter of 2015, down 0.7% from $2.679 billion in the first quarter of 2015 and up 20.1% from $2.215 billion in the second quarter of 2014. The sequential decrease was primarily due to a decrease in the number of devices sold, offset in part by a higher average cost per device sold. The year-over-year increase was primarily due to an increase in the number of devices sold, including higher device upgrade volumes. |

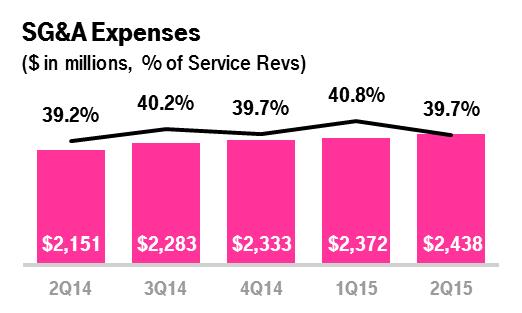

Selling, General and Admin. (“SG&A”) Expenses

| |

| ▪ | SG&A expenses were $2.438 billion in the second quarter of 2015, up 2.8% from $2.372 billion in the first quarter of 2015 and up 13.3% from $2.151 billion in the second quarter of 2014. The sequential and year-over-year increase was primarily due to higher employee-related expenses associated with an increase in the number of retail, administrative and customer support employees to support the growing customer base and higher commissions. Additionally, an increase in promotional costs contributed to the year-over-year increase. |

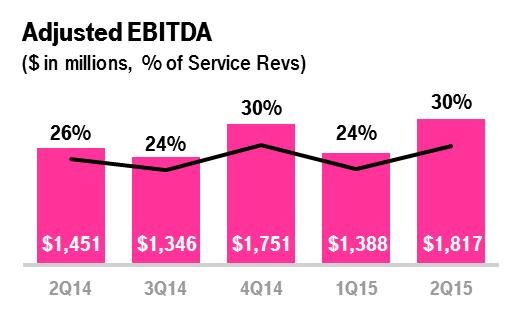

ADJUSTED EBITDA

| |

| ▪ | T-Mobile is expected to again lead the industry in year-over-year Adjusted EBITDA growth in the second quarter of 2015. |

| |

| ▪ | Adjusted EBITDA was $1.817 billion in the second quarter of 2015, up 30.9% from $1.388 billion in the first quarter of 2015 and up 25.2% from $1.451 billion in the second quarter of 2014. |

| |

| ▪ | Sequentially, the increase in Adjusted EBITDA was primarily due to higher service revenues from growth in the customer base, decreased losses on equipment sales, and the impact of the non-cash net revenue deferrals for Data Stash recognized in the first quarter of 2015, partially offset by higher selling, general and administrative expenses associated with customer growth. |

| |

| ▪ | Year-over-year, the increase in Adjusted EBITDA was primarily due to higher service revenues from growth in the customer base and lower cost of services, partially offset by higher selling, general and administrative expenses associated with customer growth. |

| |

| ▪ | Adjusted EBITDA in the second quarter of 2015 was impacted by the non-cash net revenue deferrals for Data Stash of $3 million, compared to the $112 million non-cash net revenue deferrals in the first quarter of 2015. Excluding the impacts of the non-cash net revenue deferrals for Data Stash, Adjusted EBITDA in the second quarter of 2015 increased 21.3% sequentially. |

| |

| ▪ | Adjusted EBITDA margin was 30% in the second quarter of 2015 compared to 24% in the first quarter of 2015 and 26% in the second quarter of 2014. |

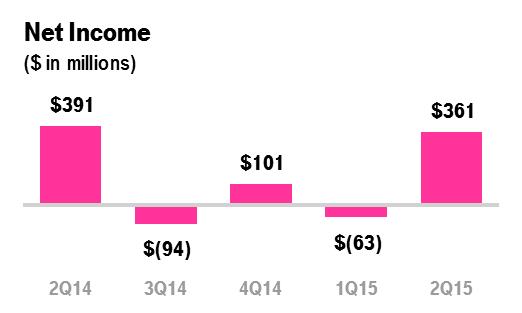

NET INCOME AND EARNINGS PER SHARE

| |

| ▪ | Net income was $361 million in the second quarter of 2015 compared to a net loss of $63 million in the first quarter of 2015 and net income of $391 million in the second quarter of 2014. The sequential increase in net income was primarily due to higher operating income in the second quarter of 2015. The year-over-year decline was primarily due to gains on disposal of spectrum licenses of $747 million recognized in the second quarter of 2014, partially offset by a decrease in income tax expense primarily due to the impact of income tax benefits for discrete items recognized in the second quarter of 2015, including recent changes in state and local income tax laws and the recognition of certain federal tax credits. |

| |

| ▪ | Earnings per share was $0.42 in the second quarter of 2015 compared to a loss per share of $(0.09) in the first quarter of 2015 and earnings per share of $0.48 in the second quarter of 2014. |

| |

| ▪ | T-Mobile expects to report positive earnings per share for all the remaining quarters and the full-year of 2015. |

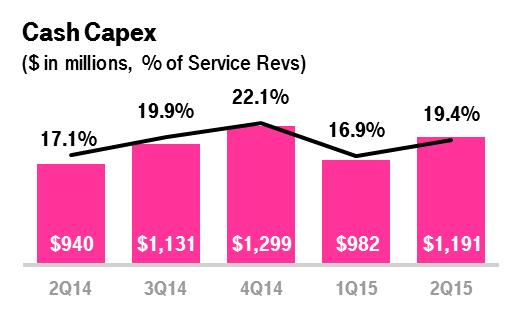

CAPITAL EXPENDITURES

| |

| ▪ | Cash capital expenditures for property and equipment were $1.191 billion in the second quarter of 2015 compared to $982 million in the first quarter of 2015 and $940 million in the second quarter of 2014. The sequential and year-over-year increase was primarily due to the timing of network spend in connection with T-Mobile’s modernization program and the build out for the 4G LTE on the 700 MHz A-Block and 1900 MHz PCS spectrum. |

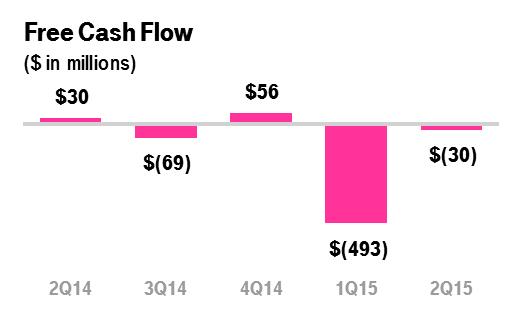

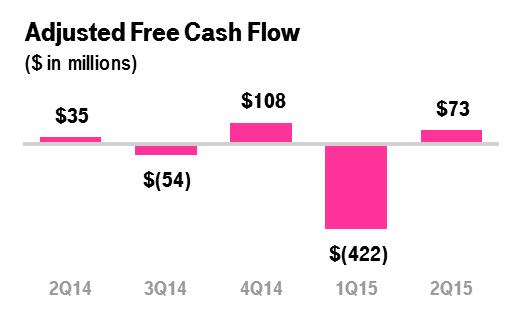

FREE CASH FLOW

| |

| ▪ | Beginning in the second quarter of 2015, T-Mobile will report Free Cash Flow, which is defined as net cash provided by operating activities less cash capital expenditures, and cease reporting Simple Free Cash Flow, which is defined as Adjusted EBITDA less cash capital expenditures. T-Mobile believes that Free Cash Flow provides a more complete representation of the cash available to pay debt and provide further investment in the business. |

| |

| ▪ | Net cash provided by operating activities was $1.161 billion in the second quarter of 2015, compared to $489 million in the first quarter of 2015 and $970 million in the second quarter of 2014. |

| |

| ▪ | Free Cash Flow was a loss of $30 million in the second quarter of 2015, compared to a loss of $493 million in the first quarter of 2015 and Free Cash Flow of $30 million in the second quarter of 2014. Sequentially, the improvement in Free Cash Flow was due to higher operating income and increases from changes in net working capital, partially offset by higher cash capital expenditures. Year-over-year, the decrease was primarily due to decreases from changes in net working capital and higher cash capital expenditures, partially offset by higher operating income. |

| |

| ▪ | Adjusted Free Cash Flow was $73 million in the second quarter of 2015, compared to a loss of $422 million in the first quarter of 2015 and Adjusted Free Cash Flow of $35 million in the second quarter of 2014. Adjusted Free Cash Flow excludes decommissioning payments related to the one-time shutdown of the CDMA portion of the MetroPCS network from Free Cash Flow. |

| |

| ▪ | The Company continues to expect that Free Cash Flow will be positive for the full-year 2015. |

CAPITAL STRUCTURE

| |

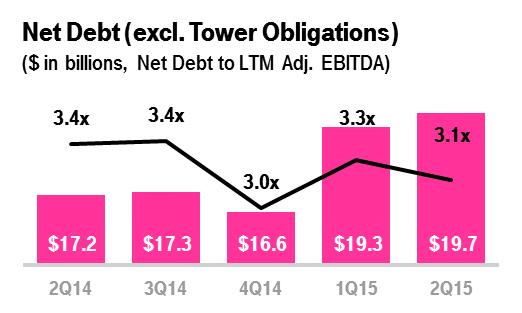

| ▪ | Net debt, excluding tower obligations, at the end of the second quarter of 2015 was $19.7 billion. |

| |

| ▪ | Total debt, excluding tower obligations, at the end of the second quarter of 2015 was $22.4 billion and was comprised of short-term debt of $0.4 billion, long-term debt to affiliates of $5.6 billion, and long-term debt of $16.4 billion. |

| |

| ▪ | The ratio of net debt, excluding tower obligations, to Adjusted EBITDA for the trailing last twelve month (“LTM”) period was 3.1x at the end of the second quarter of 2015 compared to 3.3x at the end of the first quarter of 2015 and 3.4x at the end of the second quarter of 2014. |

| |

| ▪ | The Company’s cash position remains strong with $2.6 billion in cash at the end of the second quarter of 2015. The cash balance declined in the second quarter of 2015 compared to the end of the first quarter of 2015 due primarily to a decrease in accounts payable and accrued liabilities related to the timing of vendor payments. |

GUIDANCE

| |

| ▪ | T-Mobile expects to drive further customer momentum while delivering strong growth in Adjusted EBITDA. |

| |

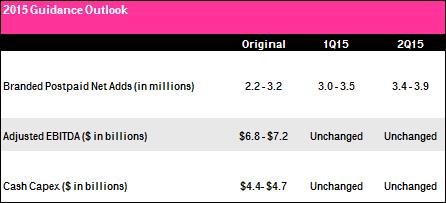

| ▪ | With the success of T-Mobile's Simple Choice plan and the continued evolution of the Un-carrier strategy, branded postpaid net customer additions for full-year 2015 are now expected to be between 3.4 and 3.9 million, an increase from the previous guidance of 3.0 to 3.5 million. |

| |

| ▪ | For full-year 2015, T-Mobile expects Adjusted EBITDA to be in the range of $6.8 to $7.2 billion, which is unchanged from previous guidance despite the increase in branded postpaid net customer additions guidance. |

| |

| ▪ | Cash capital expenditures for full-year 2015 are expected to be in the range of $4.4 to $4.7 billion, which is unchanged from previous guidance. |

| |

| ▪ | T-Mobile’s financial guidance for full-year 2015 excludes any benefit from the impact of JUMP! On Demand. The Company intends to disclose the aggregate non-cash impact from JUMP! On Demand and Data Stash in future quarters. In the second quarter of 2015, there were no significant impacts to financial results from JUMP! On Demand and Data Stash. |

OTHER EVENTS

J.D. Power Recognizes T-Mobile for Customer Care

| |

| ▪ | On July 30, 2015, J.D. Power recognized T-Mobile for its leadership in Customer Care Performance, awarding the Company the highest ranking among full service wireless providers in the J.D. Power 2015 Wireless Customer Care Full-Service Study - Volume 2. Regaining the highest ranking reinforces T-Mobile’s track record as an organization with a strong focus and commitment to providing an outstanding customer experience whether you call in, come in to the store, or access online. |

UPCOMING EVENTS (All dates and attendance tentative)

| |

| ▪ | Oppenheimer 18th Annual Technology, Internet and Communications Conference, August 11-12, 2015, Boston, MA |

| |

| ▪ | Goldman Sachs 24th Annual Communacopia Conference, September 16-18, 2015, New York, NY |

| |

| ▪ | T-Mobile US, Inc. Q3 2015 Earnings Report, October 28, 2015 |

CONTACT INFORMATION

Press:

Media Relations

T-Mobile US, Inc.

mediarelations@t-mobile.com

http://newsroom.t-mobile.com

Investor Relations:

Nils Paellmann, nils.paellmann@t-mobile.com

Ben Barrett, ben.barrett@t-mobile.com

Chezzarae Hart, chezzarae.hart@t-mobile.com

Cristal Dunkin, cristal.dunkin@t-mobile.com

877-281-TMUS or 212-358-3210

investor.relations@t-mobile.com

http://investor.t-mobile.com

T-Mobile US, Inc.

Condensed Consolidated Balance Sheets

(Unaudited)

|

| | | | | | | |

| (in millions, except share and per share amounts) | June 30,

2015 | | December 31,

2014 |

| Assets | | | |

| Current assets | | | |

| Cash and cash equivalents | $ | 2,642 |

| | $ | 5,315 |

|

| Accounts receivable, net of allowances of $91 and $83 | 1,827 |

| | 1,865 |

|

| Equipment installment plan receivables, net | 3,503 |

| | 3,062 |

|

| Accounts receivable from affiliates | 52 |

| | 76 |

|

| Inventories | 1,135 |

| | 1,085 |

|

| Deferred tax assets, net | 1,479 |

| | 988 |

|

| Other current assets | 1,019 |

| | 1,593 |

|

| Total current assets | 11,657 |

| | 13,984 |

|

| Property and equipment, net | 16,910 |

| | 16,245 |

|

| Goodwill | 1,683 |

| | 1,683 |

|

| Spectrum licenses | 24,272 |

| | 21,955 |

|

| Other intangible assets, net | 735 |

| | 870 |

|

| Equipment installment plan receivables due after one year, net | 1,611 |

| | 1,628 |

|

| Other assets | 320 |

| | 288 |

|

| Total assets | $ | 57,188 |

| | $ | 56,653 |

|

| Liabilities and Stockholders' Equity | | | |

| Current liabilities | | | |

| Accounts payable and accrued liabilities | $ | 6,645 |

| | $ | 7,364 |

|

| Current payables to affiliates | 101 |

| | 231 |

|

| Short-term debt | 386 |

| | 87 |

|

| Deferred revenue | 574 |

| | 459 |

|

| Other current liabilities | 558 |

| | 635 |

|

| Total current liabilities | 8,264 |

| | 8,776 |

|

| Long-term debt | 16,386 |

| | 16,273 |

|

| Long-term debt to affiliates | 5,600 |

| | 5,600 |

|

| Long-term financial obligation | 2,526 |

| | 2,521 |

|

| Deferred tax liabilities | 5,306 |

| | 4,873 |

|

| Deferred rents | 2,411 |

| | 2,331 |

|

| Other long-term liabilities | 642 |

| | 616 |

|

| Total long-term liabilities | 32,871 |

| | 32,214 |

|

| Commitments and contingencies | | | |

| Stockholders' equity | | | |

| 5.50% Mandatory Convertible Preferred Stock Series A, par value $0.00001 per share, 100,000,000 shares authorized; 20,000,000 and 20,000,000 shares issued and outstanding; $1,000 and $1,000 aggregate liquidation value | — |

| | — |

|

| Common Stock, par value $0.00001 per share, 1,000,000,000 shares authorized; 816,196,073 and 808,851,108 shares issued, 814,813,568 and 807,468,603 shares outstanding | — |

| | — |

|

| Additional paid-in capital | 38,595 |

| | 38,503 |

|

| Treasury stock, at cost, 1,382,505 and 1,382,505 shares issued | — |

| | — |

|

| Accumulated other comprehensive income | 1 |

| | 1 |

|

| Accumulated deficit | (22,543 | ) | | (22,841 | ) |

| Total stockholders' equity | 16,053 |

| | 15,663 |

|

| Total liabilities and stockholders' equity | $ | 57,188 |

| | $ | 56,653 |

|

T-Mobile US, Inc.

Condensed Consolidated Statements of Comprehensive Income (Loss)

(Unaudited)

|

| | | | | | | | | | | | | | | | | | | |

| | Three Months Ended | | Six Months Ended June 30, |

| (in millions, except shares and per share amounts) | June 30,

2015 | | March 31,

2015 | | June 30,

2014 | | 2015 | | 2014 |

| Revenues | | | | | | | | | |

| Branded postpaid revenues | $ | 4,075 |

| | $ | 3,774 |

| | $ | 3,511 |

| | $ | 7,849 |

| | $ | 6,958 |

|

| Branded prepaid revenues | 1,861 |

| | 1,842 |

| | 1,736 |

| | 3,703 |

| | 3,384 |

|

| Wholesale revenues | 164 |

| | 158 |

| | 172 |

| | 322 |

| | 346 |

|

| Roaming and other service revenues | 44 |

| | 45 |

| | 65 |

| | 89 |

| | 133 |

|

| Total service revenues | 6,144 |

| | 5,819 |

| | 5,484 |

| | 11,963 |

| | 10,821 |

|

| Equipment revenues | 1,915 |

| | 1,851 |

| | 1,600 |

| | 3,766 |

| | 3,048 |

|

| Other revenues | 120 |

| | 108 |

| | 101 |

| | 228 |

| | 191 |

|

| Total revenues | 8,179 |

| | 7,778 |

| | 7,185 |

| | 15,957 |

| | 14,060 |

|

| Operating expenses | | | | | | | | | |

| Cost of services, exclusive of depreciation and amortization shown separately below | 1,397 |

| | 1,395 |

| | 1,453 |

| | 2,792 |

| | 2,917 |

|

| Cost of equipment sales | 2,661 |

| | 2,679 |

| | 2,215 |

| | 5,340 |

| | 4,501 |

|

| Selling, general and administrative | 2,438 |

| | 2,372 |

| | 2,151 |

| | 4,810 |

| | 4,247 |

|

| Depreciation and amortization | 1,075 |

| | 1,087 |

| | 1,129 |

| | 2,162 |

| | 2,184 |

|

| Cost of MetroPCS business combination | 34 |

| | 128 |

| | 22 |

| | 162 |

| | 34 |

|

| Gains on disposal of spectrum licenses | (23 | ) | | — |

| | (747 | ) | | (23 | ) | | (757 | ) |

| Total operating expenses | 7,582 |

| | 7,661 |

| | 6,223 |

| | 15,243 |

| | 13,126 |

|

| Operating income | 597 |

| | 117 |

| | 962 |

| | 714 |

| | 934 |

|

| Other income (expense) | | | | | | | | | |

| Interest expense to affiliates | (92 | ) | | (64 | ) | | (85 | ) | | (156 | ) | | (103 | ) |

| Interest expense | (257 | ) | | (261 | ) | | (271 | ) | | (518 | ) | | (547 | ) |

| Interest income | 114 |

| | 112 |

| | 83 |

| | 226 |

| | 158 |

|

| Other income (expense), net | 1 |

| | (8 | ) | | (12 | ) | | (7 | ) | | (18 | ) |

| Total other expense, net | (234 | ) | | (221 | ) | | (285 | ) | | (455 | ) | | (510 | ) |

| Income (loss) before income taxes | 363 |

| | (104 | ) | | 677 |

| | 259 |

| | 424 |

|

| Income tax expense (benefit) | 2 |

| | (41 | ) | | 286 |

| | (39 | ) | | 184 |

|

| Net income (loss) | 361 |

| | (63 | ) | | 391 |

| | 298 |

| | 240 |

|

| Dividends on preferred stock | (14 | ) | | (14 | ) | | — |

| | (28 | ) | | — |

|

| Net income (loss) attributable to common stockholders | $ | 347 |

| | $ | (77 | ) | | $ | 391 |

| | $ | 270 |

| | $ | 240 |

|

| Other comprehensive loss, net of tax | | | | | | | | | |

| Unrealized loss on available-for-sale securities, net of tax effect of $0, $0, $0, $0 and $(1) | — |

| | — |

| | — |

| | — |

| | (3 | ) |

| Other comprehensive loss, net of tax | — |

| | — |

| | — |

| | — |

| | (3 | ) |

| Total comprehensive income (loss) | $ | 361 |

| | $ | (63 | ) | | $ | 391 |

| | $ | 298 |

| | $ | 237 |

|

| Earnings (loss) per share | | | | | | | | | |

| Basic | $ | 0.43 |

| | $ | (0.09 | ) | | $ | 0.49 |

| | $ | 0.33 |

| | $ | 0.30 |

|

| Diluted | $ | 0.42 |

| | $ | (0.09 | ) | | $ | 0.48 |

| | $ | 0.33 |

| | $ | 0.30 |

|

| Weighted average shares outstanding | | | | | | | | | |

| Basic | 811,605,031 |

| | 808,605,526 |

| | 803,923,913 |

| | 810,113,564 |

| | 803,226,194 |

|

| Diluted | 821,122,537 |

| | 808,605,526 |

| | 813,556,137 |

| | 819,548,539 |

| | 812,903,135 |

|

T-Mobile US, Inc.

Condensed Consolidated Statements of Cash Flows

(Unaudited)

|

| | | | | | | |

| | Six Months Ended June 30, |

| (in millions) | 2015 | | 2014 |

| Operating activities | | | |

| Net cash provided by operating activities | $ | 1,650 |

| | $ | 1,729 |

|

| | | | |

| Investing activities | | | |

| Purchases of property and equipment | (2,173 | ) | | (1,887 | ) |

| Purchases of spectrum licenses and other intangible assets | (1,844 | ) | | (2,367 | ) |

| Other, net | (12 | ) | | (21 | ) |

| Net cash used in investing activities | (4,029 | ) | | (4,275 | ) |

| | | | |

| Financing activities | | | |

| Repayments of short-term debt for purchases of inventory, property and equipment, net | (248 | ) | | (231 | ) |

| Other, net | (46 | ) | | (34 | ) |

| Net cash used in financing activities | (294 | ) | | (265 | ) |

| | | | |

| Change in cash and cash equivalents | (2,673 | ) | | (2,811 | ) |

| | | | |

| Cash and cash equivalents | | | |

| Beginning of period | 5,315 |

| | 5,891 |

|

| End of period | $ | 2,642 |

| | $ | 3,080 |

|

T-Mobile US, Inc. Supplementary Operating and Financial Data

|

| | | | | | | | | | | | | | | | | | | | | | | |

| | Quarter | | Six Months Ended June 30, |

| (in thousands) | Q1 2014 | | Q2 2014 | | Q3 2014 | | Q4 2014 | | Q1 2015 | | Q2 2015 | | 2014 | | 2015 |

| Customers, end of period | | | | | | | | | | | | | | | |

| Branded postpaid phone customers | 23,054 |

| | 23,633 |

| | 24,807 |

| | 25,844 |

| | 26,835 |

| | 27,595 |

| | 23,633 |

| | 27,595 |

|

| Branded postpaid mobile broadband customers | 568 |

| | 897 |

| | 1,102 |

| | 1,341 |

| | 1,475 |

| | 1,723 |

| | 897 |

| | 1,723 |

|

| Total branded postpaid customers | 23,622 |

| | 24,530 |

| | 25,909 |

| | 27,185 |

| | 28,310 |

| | 29,318 |

| | 24,530 |

| | 29,318 |

|

| Branded prepaid customers | 15,537 |

| | 15,639 |

| | 16,050 |

| | 16,316 |

| | 16,389 |

| | 16,567 |

| | 15,639 |

| | 16,567 |

|

| Total branded customers | 39,159 |

| | 40,169 |

| | 41,959 |

| | 43,501 |

| | 44,699 |

| | 45,885 |

| | 40,169 |

| | 45,885 |

|

| M2M customers | 3,822 |

| | 4,047 |

| | 4,269 |

| | 4,421 |

| | 4,562 |

| | 4,529 |

| | 4,047 |

| | 4,529 |

|

| MVNO customers | 6,094 |

| | 6,329 |

| | 6,662 |

| | 7,096 |

| | 7,575 |

| | 8,494 |

| | 6,329 |

| | 8,494 |

|

| Total wholesale customers | 9,916 |

| | 10,376 |

| | 10,931 |

| | 11,517 |

| | 12,137 |

| | 13,023 |

| | 10,376 |

| | 13,023 |

|

| Total customers, end of period | 49,075 |

| | 50,545 |

| | 52,890 |

| | 55,018 |

| | 56,836 |

| | 58,908 |

| | 50,545 |

| | 58,908 |

|

|

| | | | | | | | | | | | | | | | | | | | | | | |

| | Quarter | | Six Months Ended June 30, |

| (in thousands) | Q1 2014 | | Q2 2014 | | Q3 2014 | | Q4 2014 | | Q1 2015 | | Q2 2015 | | 2014 | | 2015 |

| Net customer additions (losses) | | | | | | | | | | | | | | | |

| Branded postpaid phone customers | 1,256 |

| | 579 |

| | 1,175 |

| | 1,037 |

| | 991 |

| | 760 |

| | 1,835 |

| | 1,751 |

|

| Branded postpaid mobile broadband customers | 67 |

| | 329 |

| | 204 |

| | 239 |

| | 134 |

| | 248 |

| | 396 |

| | 382 |

|

| Total branded postpaid customers | 1,323 |

| | 908 |

| | 1,379 |

| | 1,276 |

| | 1,125 |

| | 1,008 |

| | 2,231 |

| | 2,133 |

|

| Branded prepaid customers | 465 |

| | 102 |

| | 411 |

| | 266 |

| | 73 |

| | 178 |

| | 567 |

| | 251 |

|

| Total branded customers | 1,788 |

| | 1,010 |

| | 1,790 |

| | 1,542 |

| | 1,198 |

| | 1,186 |

| | 2,798 |

| | 2,384 |

|

| M2M customers | 220 |

| | 225 |

| | 222 |

| | 152 |

| | 141 |

| | (33 | ) | | 445 |

| | 108 |

|

| MVNO customers | 383 |

| | 235 |

| | 333 |

| | 434 |

| | 479 |

| | 919 |

| | 618 |

| | 1,398 |

|

| Total wholesale customers | 603 |

| | 460 |

| | 555 |

| | 586 |

| | 620 |

| | 886 |

| | 1,063 |

| | 1,506 |

|

| Total net customer additions | 2,391 |

| | 1,470 |

| | 2,345 |

| | 2,128 |

| | 1,818 |

| | 2,072 |

| | 3,861 |

| | 3,890 |

|

Note: Certain customer numbers may not add due to rounding.

|

| | | | | | | | | | | | | | | | | | | | | | | |

| | Quarter | | Six Months Ended June 30, |

| | Q1 2014 | | Q2 2014 | | Q3 2014 | | Q4 2014 | | Q1 2015 | | Q2 2015 | | 2014 | | 2015 |

| Branded postpaid phone churn | 1.47 | % | | 1.48 | % | | 1.64 | % | | 1.73 | % | | 1.30 | % | | 1.32 | % | | 1.47 | % | | 1.31 | % |

| Branded prepaid churn | 4.34 | % | | 4.50 | % | | 4.78 | % | | 5.39 | % | | 4.62 | % | | 4.93 | % | | 4.42 | % | | 4.78 | % |

T-Mobile US, Inc. Supplementary Operating and Financial Data (continued)

|

| | | | | | | | | | | | | | | |

| | Quarter | | Six Months Ended June 30, |

| | Q1 2014 | | Q2 2014 | | Q3 2014 | | Q4 2014 | | Q1 2015 | | Q2 2015 | | 2014 | | 2015 |

| Financial Metrics | | | | | | | | | | | | | | | |

| Service revenues (in millions) | $5,337 | | $5,484 | | $5,684 | | $5,870 | | $5,819 | | $6,144 | | $10,821 | | $11,963 |

| Total revenues (in millions) | $6,875 | | $7,185 | | $7,350 | | $8,154 | | $7,778 | | $8,179 | | $14,060 | | $15,957 |

| Adjusted EBITDA (in millions) | $1,088 | | $1,451 | | $1,346 | | $1,751 | | $1,388 | | $1,817 | | $2,539 | | $3,205 |

| Adjusted EBITDA margin | 20% | | 26% | | 24% | | 30% | | 24% | | 30% | | 23% | | 27% |

| Net income (loss) (in millions) | $(151) | | $391 | | $(94) | | $101 | | $(63) | | $361 | | $240 | | $298 |

| Cash capex - Property & Equipment (in millions) | $947 | | $940 | | $1,131 | | $1,299 | | $982 | | $1,191 | | $1,887 | | $2,173 |

| | | | | | | | | | | | | | | | |

| Revenue Metrics | | | | | | | | | | | | | | | |

| Branded postpaid ARPA | $108.97 | | $107.11 | | $109.80 | | $109.87 | | $108.04 | | $113.50 | | $108.02 | | $110.81 |

| Branded postpaid ABPA | $129.74 | | $131.81 | | $138.73 | | $143.79 | | $145.03 | | $152.31 | | $130.79 | | $148.72 |

| Branded postpaid accounts, end of period | 10,812 | | 11,017 | | 11,297 | | 11,506 | | 11,831 | | 12,061 | | 11,017 | | 12,061 |

| Branded postpaid customers per account | 2.18 | | 2.23 | | 2.29 | | 2.36 | | 2.39 | | 2.43 | | 2.23 | | 2.43 |

| Branded postpaid phone ARPU | $50.48 | | $49.32 | | $49.84 | | $48.26 | | $46.43 | | $48.19 | | $49.89 | | $47.33 |

| Branded postpaid ABPU | $59.54 | | $59.79 | | $61.59 | | $61.80 | | $60.94 | | $63.29 | | $59.67 | | $62.14 |

| Branded prepaid ARPU | $36.09 | | $37.16 | | $37.59 | | $37.51 | | $37.81 | | $37.83 | | $36.63 | | $37.82 |

| | | | | | | | | | | | | | | | |

| Devices | | | | | | | | | | | | | | | |

| Smartphone sales units (in millions) | 6.9 | | 6.2 | | 6.9 | | 8.0 | | 8.0 | | 7.4 | | 13.1 | | 15.4 |

| Branded postpaid handset upgrade rate | 7% | | 8% | | 9% | | 11% | | 8% | | 9% | | 15% | | 17% |

| | | | | | | | | | | | | | | | |

| Equipment Installment Plans | | | | | | | | | | | | | | | |

| EIP financed (in millions) | $1,249 | | $1,342 | | $1,317 | | $1,902 | | $1,483 | | $1,697 | | $2,591 | | $3,180 |

| EIP billings (in millions) | $657 | | $810 | | $967 | | $1,162 | | $1,292 | | $1,393 | | $1,467 | | $2,685 |

| EIP receivables, net (in millions) | $3,086 | | $3,583 | | $3,963 | | $4,690 | | $4,842 | | $5,114 | | $3,583 | | $5,114 |

| | | | | | | | | | | | | | | | |

| Customer Quality | | | | | | | | | | | | | | | |

| EIP receivables classified as prime | 53% | | 53% | | 53% | | 54% | | 52% | | 52% | | 53% | | 52% |

| Total bad debt expense and losses from factoring arrangement (in millions) | $157 | | $164 | | $152 | | $150 | | $169 | | $156 | | $321 | | $325 |

T-Mobile US, Inc.

Reconciliation of Non-GAAP Financial Measures to GAAP Financial Measures

(Unaudited)

This Investor Factbook includes non-GAAP financial measures. The non-GAAP financial measures should be considered in addition to, but not as a substitute for, the information provided in accordance with GAAP. Reconciliations for the non-GAAP financial measures to the most directly comparable GAAP financial measures are provided below.

Adjusted EBITDA is reconciled to net income (loss) as follows:

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Quarter | | Six Months Ended June 30, |

| (in millions) | Q1 2014 | | Q2 2014 | | Q3 2014 | | Q4 2014 | | Q1 2015 | | Q2 2015 | | 2014 | | 2015 |

| Net income (loss) | $ | (151 | ) | | $ | 391 |

| | $ | (94 | ) | | $ | 101 |

| | $ | (63 | ) | | $ | 361 |

| | $ | 240 |

| | $ | 298 |

|

| Adjustments: | | | | | | | | | | | | | | | |

| Interest expense to affiliates | 18 |

| | 85 |

| | 83 |

| | 92 |

| | 64 |

| | 92 |

| | 103 |

| | 156 |

|

| Interest expense | 276 |

| | 271 |

| | 260 |

| | 266 |

| | 261 |

| | 257 |

| | 547 |

| | 518 |

|

| Interest income | (75 | ) | | (83 | ) | | (97 | ) | | (104 | ) | | (112 | ) | | (114 | ) | | (158 | ) | | (226 | ) |

| Other expense (income), net | 6 |

| | 12 |

| | 14 |

| | (21 | ) | | 8 |

| | (1 | ) | | 18 |

| | 7 |

|

| Income tax expense (benefit) | (102 | ) | | 286 |

| | (117 | ) | | 99 |

| | (41 | ) | | 2 |

| | 184 |

| | (39 | ) |

| Operating income (loss) | (28 | ) | | 962 |

| | 49 |

| | 433 |

| | 117 |

| | 597 |

| | 934 |

| | 714 |

|

| Depreciation and amortization | 1,055 |

| | 1,129 |

| | 1,138 |

| | 1,090 |

| | 1,087 |

| | 1,075 |

| | 2,184 |

| | 2,162 |

|

| Cost of MetroPCS business combination | 12 |

| | 22 |

| | 97 |

| | 168 |

| | 128 |

| | 34 |

| | 34 |

| | 162 |

|

| Stock based compensation | 49 |

| | 63 |

| | 45 |

| | 54 |

| | 56 |

| | 71 |

| | 112 |

| | 127 |

|

Gains on disposal of spectrum licenses (1) | — |

| | (731 | ) | | 11 |

| | — |

| | — |

| | — |

| | (731 | ) | | — |

|

| Other, net | — |

| | 6 |

| | 6 |

| | 6 |

| | — |

| | 40 |

| | 6 |

| | 40 |

|

| Adjusted EBITDA | $ | 1,088 |

| | $ | 1,451 |

| | $ | 1,346 |

| | $ | 1,751 |

| | $ | 1,388 |

| | $ | 1,817 |

| | $ | 2,539 |

| | $ | 3,205 |

|

| |

| (1) | Gains on disposal of spectrum licenses may not agree to the Condensed Consolidated Statements of Comprehensive Income (Loss) primarily due to certain routine operating activities, such as insignificant or routine spectrum license exchanges that would be expected to reoccur, and are therefore included in Adjusted EBITDA. |

T-Mobile US, Inc.

Reconciliation of Non-GAAP Financial Measures to GAAP Financial Measures (continued)

(Unaudited)

The following tables illustrate the calculation of ARPA and ABPA and reconcile these measures to the related service revenues, which we consider to be the most directly comparable GAAP financial measure to ARPA and ABPA:

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Quarter | | Six Months Ended June 30, |

| (in millions, except average number of accounts, ARPA and ABPA) | Q1 2014 | | Q2 2014 | | Q3 2014 | | Q4 2014 | | Q1 2015 | | Q2 2015 | | 2014 | | 2015 |

| Calculation of Branded Postpaid ARPA | | | | | | | | | | | | | | | |

| Branded postpaid service revenues | $ | 3,447 |

| | $ | 3,511 |

| | $ | 3,670 |

| | $ | 3,764 |

| | $ | 3,774 |

| | $ | 4,075 |

| | $ | 6,958 |

| | $ | 7,849 |

|

| Divided by: Average number of branded postpaid accounts (in thousands) and number of months in period | 10,543 |

| | 10,928 |

| | 11,141 |

| | 11,421 |

| | 11,645 |

| | 11,966 |

| | 10,736 |

| | 11,806 |

|

| Branded postpaid ARPA | $ | 108.97 |

| | $ | 107.11 |

| | $ | 109.80 |

| | $ | 109.87 |

| | $ | 108.04 |

| | $ | 113.50 |

| | $ | 108.02 |

| | $ | 110.81 |

|

| | | | | | | | | | | | | | | | |

| Calculation of Branded Postpaid ABPA | | | | | | | | | | | | | | | |

| Branded postpaid service revenues | $ | 3,447 |

| | $ | 3,511 |

| | $ | 3,670 |

| | $ | 3,764 |

| | $ | 3,774 |

| | $ | 4,075 |

| | $ | 6,958 |

| | $ | 7,849 |

|

| Add: EIP billings | 657 |

| | 810 |

| | 967 |

| | 1,162 |

| | 1,292 |

| | 1,393 |

| | 1,467 |

| | 2,685 |

|

| Total billings for branded postpaid customers | $ | 4,104 |

| | $ | 4,321 |

| | $ | 4,637 |

| | $ | 4,926 |

| | $ | 5,066 |

| | $ | 5,468 |

| | $ | 8,425 |

| | $ | 10,534 |

|

| Divided by: Average number of branded postpaid accounts (in thousands) and number of months in period | 10,543 |

| | 10,928 |

| | 11,141 |

| | 11,421 |

| | 11,645 |

| | 11,966 |

| | 10,736 |

| | 11,806 |

|

| Branded postpaid ABPA | $ | 129.74 |

| | $ | 131.81 |

| | $ | 138.73 |

| | $ | 143.79 |

| | $ | 145.03 |

| | $ | 152.31 |

| | $ | 130.79 |

| | $ | 148.72 |

|

T-Mobile US, Inc.

Reconciliation of Non-GAAP Financial Measures to GAAP Financial Measures (continued)

(Unaudited)

The following tables illustrate the calculation of ARPU and ABPU and reconcile these measures to the related service revenues, which we consider to be the most directly comparable GAAP financial measure to ARPU and ABPU:

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Quarter | | Six Months Ended June 30, |

| (in millions, except average number of customers, ARPU and ABPU) | Q1 2014 | | Q2 2014 | | Q3 2014 | | Q4 2014 | | Q1 2015 | | Q2 2015 | | 2014 | | 2015 |

| Calculation of Branded Postpaid Phone ARPU | | | | | | | | | | | | | | | |

| Branded postpaid service revenues | $ | 3,447 |

| | $ | 3,511 |

| | $ | 3,670 |

| | $ | 3,764 |

| | $ | 3,774 |

| | $ | 4,075 |

| | $ | 6,958 |

| | $ | 7,849 |

|

| Less: Branded postpaid mobile broadband revenues | (47 | ) | | (54 | ) | | (68 | ) | | (92 | ) | | (109 | ) | | (135 | ) | | (101 | ) | | (244 | ) |

| Branded postpaid phone service revenues | $ | 3,400 |

| | $ | 3,457 |

| | $ | 3,602 |

| | $ | 3,672 |

| | $ | 3,665 |

| | $ | 3,940 |

| | $ | 6,857 |

| | $ | 7,605 |

|

| Divided by: Average number of branded postpaid phone customers (in thousands) and number of months in period | 22,447 |

| | 23,368 |

| | 24,091 |

| | 25,359 |

| | 26,313 |

| | 27,250 |

| | 22,908 |

| | 26,781 |

|

| Branded postpaid phone ARPU | $ | 50.48 |

| | $ | 49.32 |

| | $ | 49.84 |

| | $ | 48.26 |

| | $ | 46.43 |

| | $ | 48.19 |

| | $ | 49.89 |

| | $ | 47.33 |

|

| | | | | | | | | | | | | | | | |

| Calculation of Branded Postpaid ABPU | | | | | | | | | | | | | | | |

| Branded postpaid service revenues | $ | 3,447 |

| | $ | 3,511 |

| | $ | 3,670 |

| | $ | 3,764 |

| | $ | 3,774 |

| | $ | 4,075 |

| | $ | 6,958 |

| | $ | 7,849 |

|

| Add: EIP billings | 657 |

| | 810 |

| | 967 |

| | 1,162 |

| | 1,292 |

| | 1,393 |

| | 1,467 |

| | 2,685 |

|

| Total billings for branded postpaid customers | $ | 4,104 |

| | $ | 4,321 |

| | $ | 4,637 |

| | $ | 4,926 |

| | $ | 5,066 |

| | $ | 5,468 |

| | $ | 8,425 |

| | $ | 10,534 |

|

| Divided by: Average number of branded postpaid customers (in thousands) and number of months in period | 22,975 |

| | 24,092 |

| | 25,095 |

| | 26,572 |

| | 27,717 |

| | 28,797 |

| | 23,533 |

| | 28,257 |

|

| Branded postpaid ABPU | $ | 59.54 |

| | $ | 59.79 |

| | $ | 61.59 |

| | $ | 61.80 |

| | $ | 60.94 |

| | $ | 63.29 |

| | $ | 59.67 |

| | $ | 62.14 |

|

| | | | | | | | | | | | | | | | |

| Calculation of Branded Prepaid ARPU | | | | | | | | | | | | | | | |

| Branded Prepaid Service Revenues | $ | 1,648 |

| | $ | 1,736 |

| | $ | 1,790 |

| | $ | 1,812 |

| | $ | 1,842 |

| | $ | 1,861 |

| | $ | 3,384 |

| | $ | 3,703 |

|

| Divided by: Average number of branded prepaid customers (in thousands) and number of months in period | 15,221 |

| | 15,569 |

| | 15,875 |

| | 16,097 |

| | 16,238 |

| | 16,396 |

| | 15,395 |

| | 16,317 |

|

| Branded prepaid ARPU | $ | 36.09 |

| | $ | 37.16 |

| | $ | 37.59 |

| | $ | 37.51 |

| | $ | 37.81 |

| | $ | 37.83 |

| | $ | 36.63 |

| | $ | 37.82 |

|

T-Mobile US, Inc.

Reconciliation of Non-GAAP Financial Measures to GAAP Financial Measures (continued)

(Unaudited)

Net debt (excluding Tower Obligations) to last twelve months adjusted EBITDA ratio is calculated as follows:

|

| | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended |

| (in millions, except net debt ratio) | Mar 31,

2014 | | Jun 30,

2014 | | Sep 30,

2014 | | Dec 31,

2014 | | Mar 31,

2015 | | Jun 30,

2015 |

| Short-term debt | $ | 151 |

| | $ | 272 |

| | $ | 1,168 |

| | $ | 87 |

| | $ | 467 |

| | $ | 386 |

|

| Long-term debt to affiliates | 5,600 |

| | 5,600 |

| | 5,600 |

| | 5,600 |

| | 5,600 |

| | 5,600 |

|

| Long-term debt | 14,331 |

| | 14,369 |

| | 16,284 |

| | 16,273 |

| | 16,261 |

| | 16,386 |

|

| Less: Cash and cash equivalents | (5,471 | ) | | (3,080 | ) | | (5,787 | ) | | (5,315 | ) | | (3,032 | ) | | (2,642 | ) |

| Net Debt (excluding Tower Obligations) | $ | 14,611 |

| | $ | 17,161 |

| | $ | 17,265 |

| | $ | 16,645 |

| | $ | 19,296 |

| | $ | 19,730 |

|

Divided by: Last twelve months Adjusted EBITDA (1) | $ | 4,936 |

| | $ | 5,122 |

| | $ | 5,124 |

| | $ | 5,636 |

| | $ | 5,936 |

| | $ | 6,302 |

|

| Net Debt (excluding Tower Obligations) to Last Twelve Months Adjusted EBITDA Ratio | 3.0 |

| | 3.4 |

| | 3.4 |

| | 3.0 |

| | 3.3 |

| | 3.1 |

|

| |

| (1) | March 31, 2014 Adjusted EBITDA for the last twelve months includes Pro Forma combined results from Q2 2013 to reflect the results of MetroPCS prior to the business combination. |

Free cash flow and adjusted free cash flow are calculated as follows:

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Quarter | | Six Months Ended June 30, |

| (in millions) | Q1 2014 | | Q2 2014 | | Q3 2014 | | Q4 2014 | | Q1 2015 | | Q2 2015 | | 2014 | | 2015 |

| Net cash provided by operating activities | $ | 759 |

| | $ | 970 |

| | $ | 1,062 |

| | $ | 1,355 |

| | $ | 489 |

| | $ | 1,161 |

| | $ | 1,729 |

| | $ | 1,650 |

|

| Cash purchases of property and equipment | (947 | ) | | (940 | ) | | (1,131 | ) | | (1,299 | ) | | (982 | ) | | (1,191 | ) | | (1,887 | ) | | (2,173 | ) |

| Free Cash Flow | (188 | ) | | 30 |

| | (69 | ) | | 56 |

| | (493 | ) | | (30 | ) | | (158 | ) | | (523 | ) |

| MetroPCS CDMA network decommissioning payments | 9 |

| | 5 |

| | 15 |

| | 52 |

| | 71 |

| | 103 |

| | 14 |

| | 174 |

|

| Adjusted Free Cash Flow | $ | (179 | ) | | $ | 35 |

| | $ | (54 | ) | | $ | 108 |

| | $ | (422 | ) |

| $ | 73 |

|

| $ | (144 | ) |

| $ | (349 | ) |

Definitions of Terms

Operating and financial measures are utilized by T-Mobile's management to evaluate its operating performance and, in certain cases, its ability to meet liquidity requirements. Although companies in the wireless industry may not define measures in precisely the same way, T-Mobile believes the measures facilitate key operating performance comparisons with other companies in the wireless industry to provide management, investors, and analysts with useful information to assess and evaluate past performance and assist in forecasting future performance.

| |

| 1. | Customer - SIM card with a unique T-Mobile mobile identity number which generates revenue. Branded customers generally include customers that are qualified either for postpaid service, where they generally pay after incurring service, or prepaid service, where they generally pay in advance. Wholesale customers include Machine-to-Machine (M2M) and Mobile Virtual Network Operator (MVNO) customers that operate on T-Mobile's network, but are managed by wholesale partners. |

| |

| 2. | Churn - Number of customers whose service was discontinued as a percentage of the average number of customers during the specified period. |

| |

| 3. | Customers per account - The number of branded postpaid customers as of the end of the period divided by the number of branded postpaid accounts as of the end of the period. An account may include branded postpaid phone and mobile broadband customers. |

| |

| 4. | Average Revenue Per Account (ARPA) - Average monthly branded postpaid service revenue earned per account. Branded postpaid service revenues for the specified period divided by the average number of branded postpaid accounts during the period, further divided by the number of months in the period. T-Mobile considers branded postpaid ARPA to be indicative of its revenue growth potential given the increase in the average number of branded postpaid phone customers per account and increased penetration of mobile broadband devices. |

Average Billings Per Account (ABPA) - Average monthly branded postpaid service revenue earned from customers plus equipment installment plan (EIP) billings divided by the average number of branded postpaid accounts during the period, further divided by the number of months in the period. T-Mobile believes average branded postpaid customer billings per account is indicative of estimated cash collections, including equipment installments, from T-Mobile's customers each month on a per account basis.

Average Revenue Per User (ARPU) - Average monthly service revenue earned from customers. Service revenues for the specified period divided by the average customers during the period, further divided by the number of months in the period.

Branded postpaid phone ARPU excludes mobile broadband customers and related revenues.

Average Billings per User (ABPU) - Average monthly branded postpaid service revenue earned from customers plus EIP billings divided by the average branded postpaid customers during the period, further divided by the number of months in the period. T-Mobile believes branded postpaid ABPU is indicative of estimated cash collections, including equipment installments, from T-Mobile's customers each month.

Service revenues - Branded postpaid, including handset insurance, branded prepaid, wholesale, and roaming and other service revenues.

| |

| 5. | Cost of services - Costs directly attributable to providing wireless service through the operation of T-Mobile's network, including direct switch and cell site costs, such as rent, network access and transport costs, utilities, maintenance, associated labor costs, long distance costs, regulatory program costs, roaming fees paid to other carriers and data content costs. |

Cost of equipment sales - Costs of devices and accessories sold to customers and dealers, device costs to fulfill insurance and warranty claims, write-downs of inventory related to shrinkage and obsolescence, and shipping and handling costs.

Selling, general and administrative expenses - Costs not directly attributable to providing wireless service for the operation of sales, customer care and corporate activities. These include commissions paid to dealers and retail employees for activations and upgrades, labor and facilities costs associated with retail sales force and administrative space, marketing and promotional costs, customer support and billing, bad debt expense and administrative support activities.

| |

| 6. | Adjusted EBITDA - Earnings before interest expense (net of interest income), tax, depreciation, amortization, stock-based compensation and expenses not reflective of T-Mobile's ongoing operating performance. Adjusted EBITDA margin is Adjusted EBITDA divided by service revenues. Adjusted EBITDA is a non-GAAP financial measure utilized by T-Mobile's management to monitor the financial performance of its operations. T-Mobile uses Adjusted EBITDA internally as a metric to evaluate and compensate its personnel and management for their performance, and as a benchmark to evaluate T-Mobile's operating performance in comparison to its competitors. Management also uses Adjusted EBITDA to measure its ability to provide cash flows to meet future debt service, capital expenditures and working capital requirements, and to fund future growth. T-Mobile believes analysts and investors use Adjusted EBITDA as a supplemental measure to evaluate overall operating performance and facilitate comparisons with other wireless communications companies. Adjusted EBITDA has limitations as an analytical tool and should not be considered in isolation or as a substitute for income from operations, net income, or any other measure of financial performance reported in accordance with GAAP. The reconciliation of Adjusted EBITDA to net income (loss) is detailed in the Reconciliation of Non-GAAP Financial Measures to GAAP Financial Measures schedule. |

| |

| 7. | Cash capital expenditures - Amounts paid for construction and the purchase of property and equipment. |

| |

| 8. | Smartphones - UMTS/HSPA/HSPA+ 21/HSPA+ 42/4G LTE enabled converged devices, which integrate voice and data services. |

| |

| 9. | Free Cash Flow - Net cash provided by operating activities less cash capital expenditures for property and equipment. Free Cash Flow is utilized by T-Mobile's management, investors, and analysts to evaluate cash available to pay debt and provide further investment in the business. The reconciliation of Free Cash Flow to net cash provided by operating activities is detailed in the Reconciliation of Non-GAAP Financial Measures to GAAP Financial Measures schedule. |

| |

| 10. | Adjusted Free Cash Flow - Free Cash Flow excluding decommissioning payments related to the shutdown of the CDMA portion of the MetroPCS network. |

| |

| 11. | Net debt - Short-term debt, long-term debt to affiliates, and long-term debt (excluding tower obligations), less cash and cash equivalents. |

Forward-Looking Statements

This Investor Factbook includes "forward-looking statements" within the meaning of the U.S. federal securities laws. Any statements made herein that are not statements of historical fact, including statements about T-Mobile US, Inc.'s plans, outlook, beliefs, opinion, projections, guidance, strategy, integration of MetroPCS, expected network modernization and other advancements, are forward-looking statements. Generally, forward-looking statements may be identified by words such as "anticipate," "expect," "suggests," "plan," “project,” "believe," "intend," "estimates," "targets," "views," "may," "will," "forecast," and other similar expressions. The forward-looking statements speak only as of the date made, are based on current assumptions and expectations, and involve a number of risks and uncertainties. Important factors that could affect future results and cause those results to differ materially from those expressed in the forward-looking statements include, among others, the following: our ability to compete in the highly competitive U.S. wireless telecommunications industry; adverse conditions in the U.S. and international economies and markets; significant capital commitments and the capital expenditures required to effect our business plan; our ability to adapt to future changes in technology, enhance existing offerings, and introduce new offerings to address customers' changing demands; changes in legal and regulatory requirements, including any change or increase in restrictions on our ability to operate our network; our ability to successfully maintain and improve our network, and the possibility of incurring additional costs in doing so; major equipment failures; severe weather conditions or other force majeure events; and other risks described in our filings with the Securities and Exchange Commission, including those described in our Annual Report on Form 10-K filed with the Securities and Exchange Commission on February 19, 2015. You should not place undue reliance on these forward-looking statements. We do not undertake to update forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

About T-Mobile US, Inc.

As America's Un-carrier, T-Mobile US, Inc. (NYSE: TMUS) is redefining the way consumers and businesses buy wireless services through leading product and service innovation. The Company's advanced nationwide 4G LTE network delivers outstanding wireless experiences to approximately 59 million customers who are unwilling to compromise on quality and value. Based in Bellevue, Washington, T-Mobile US provides services through its subsidiaries and operates its flagship brands, T-Mobile and MetroPCS. For more information, please visit http://www.T-Mobile.com.