EXHIBIT 99.2

|

| | |

| | T-Mobile US, Inc. |

| |

| | Investor Factbook |

| | T-Mobile US Reports Fourth Quarter and Full Year 2018 Results |

T-Mobile Reports Record Financials and Strong Customer Growth in FY 2018, Guidance Sets the Stage for a Strong 2019

Record Financial Performance in FY 2018 (all percentages year-over-year)

| |

| • | Record Service revenues of $8.2 billion, up 6% in Q4 2018 — up 6% to $32.0 billion in 2018 |

| |

| • | Record Total revenues of $11.4 billion, up 6% in Q4 2018 — up 7% to $43.3 billion in 2018 |

| |

| • | Strong Net income of $640 million, down 76% in Q4 2018 — down 36% to $2.9 billion in 2018 |

| |

| ◦ | Up 21% and 22% in Q4 2018 and 2018, respectively, excluding the impact of the Tax Cuts and Jobs Act (“TCJA”) of $2.2 billion in 2017 |

| |

| • | Diluted earnings per share (“EPS”) of $0.75 and $3.36 in Q4 2018 and 2018, respectively |

| |

| • | Record Q4 Adjusted EBITDA(1) of $3.0 billion, up 10% in Q4 2018 — up 11% to $12.4 billion in 2018 |

| |

| • | Strong Net cash provided by operating activities(2) of $954 million, up 10%, and $3.9 billion, up 2%, in Q4 2018 and 2018, respectively |

| |

| • | Record Free Cash Flow(1)(2) of $1.2 billion, up 7% in Q4 2018 — up 30% to $3.6 billion in 2018 |

Accelerating Customer Growth

| |

| • | Record 2.4 million total net additions in Q4 2018 — 7.0 million in 2018 |

| |

| • | 1.4 million branded postpaid net additions in Q4 2018, best in the industry — 4.5 million in 2018 |

| |

| • | 1.0 million branded postpaid phone net additions in Q4 2018, best in industry — 3.1 million in 2018 |

| |

| • | 135,000 branded prepaid net additions in Q4 2018, expect to be best in the industry — 460,000 in 2018 |

| |

| • | Q4 record-low branded postpaid phone churn of 0.99% in Q4 2018, down 19 bps YoY — 1.01% in 2018, down 17 bps from 2017 |

Building the First Real 5G Network While Improving 4G LTE

| |

| • | T-Mobile is building out standards-based 5G today, plans to have nationwide 5G coverage next year |

| |

| • | Aggressive deployment of 600 MHz using 5G ready equipment, now reaching over 2,700 cities and towns on 29 devices |

| |

| • | T-Mobile now covers more than 325 million people with 4G LTE |

| |

| • | Fastest 4G LTE network for 20th consecutive quarter based on analysis by Ookla® of Speedtest Intelligence® data |

Strong Outlook for 2019

| |

| • | Branded postpaid net customer additions of 2.6 to 3.6 million |

| |

| • | Net income is not available on a forward-looking basis(3) |

| |

| • | Adjusted EBITDA target, excluding the impact of the new lease standard, of $12.7 to $13.2 billion, which includes leasing revenues of $0.6 to $0.7 billion(1) |

| |

| • | Cash purchases of property and equipment, excluding capitalized interest of approximately $400 million, of $5.4 to $5.7 billion and cash purchases of property and equipment, including capitalized interest, of $5.8 to $6.1 billion |

| |

| • | Three-year compound annual growth rate (CAGR) from FY 2016 to FY 2019 for Net cash provided by operating activities is expected to be at 17% - 21%, up from prior guidance of 7% - 12%(2) |

| |

| • | Three-year CAGR from FY 2016 to FY 2019 for Free Cash Flow maintained at 46% - 48%(1)(2) |

________________________________________________________________

| |

| (1) | Adjusted EBITDA and Free Cash Flow are non-GAAP financial measures. These non-GAAP financial measures should be considered in addition to, but not as a substitute for, the information provided in accordance with GAAP. Reconciliations for these non-GAAP financial measures to the most directly comparable financial measures are provided in the Reconciliation of Non-GAAP Financial Measures to GAAP Financial Measures tables. |

| |

| (2) | In Q1 2018, the adoption of the new cash flow accounting standard resulted in a reclassification of cash flows related to the deferred purchase price from securitization transactions from operating activities to investing activities. In addition, cash flows related to debt prepayment and extinguishment costs were reclassified from operating activities to financing activities. In Q1 2018, we redefined Free Cash Flow to reflect the above changes in classification and present cash flows on a consistent basis for investor transparency. The effects of this change are applied retrospectively and are provided in the Reconciliation of Non-GAAP Financial Measures to GAAP Financial Measures tables. |

| |

| (3) | We are not able to forecast net income on a forward-looking basis without unreasonable efforts due to the high variability and difficulty in predicting certain items that affect GAAP net income including, but not limited to, income tax expense, stock-based compensation expense and interest expense. Adjusted EBITDA should not be used to predict net income as the difference between the two measures is variable. |

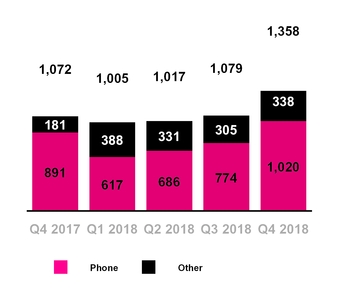

Total Branded Postpaid Net Additions

(in thousands)

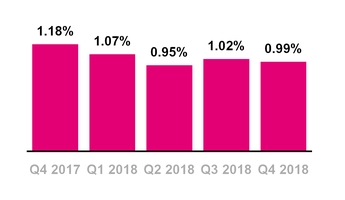

Branded Postpaid Phone Churn

CUSTOMER METRICS

Branded Postpaid Customers

| |

| ▪ | Branded postpaid phone net customer additions were 1,020,000 in Q4 2018, compared to 774,000 in Q3 2018 and 891,000 in Q4 2017. This marks the 20th consecutive quarter that T-Mobile led the industry in branded postpaid phone net customer additions. |

| |

| ▪ | The sequential increase was due to continued growth in existing and Greenfield markets including the growing success of new customer segments and rate plans such as T-Mobile ONE Unlimited 55+, T-Mobile ONE Military, T-Mobile for Business and T-Mobile Essentials, as well as higher gross customer additions driven by seasonality. |

| |

| ▪ | Year-over-year, branded postpaid phone net customer additions increased primarily due to record low fourth quarter churn and continued growth in existing and Greenfield markets including the growing success of new customer segments and rate plans such as T-Mobile ONE Unlimited 55+, T-Mobile ONE Military, T-Mobile for Business and T-Mobile Essentials. |

| |

| ▪ | Branded postpaid other net customer additions were 338,000 in Q4 2018, compared to 305,000 in Q3 2018 and 181,000 in Q4 2017. |

| |

| ▪ | The sequential and year-over-year increases were primarily due to higher gross customer additions from wearables. |

| |

| ▪ | Branded postpaid net customer additions were 1,358,000 in Q4 2018, compared to 1,079,000 in Q3 2018 and 1,072,000 in Q4 2017. |

| |

| ▪ | Branded postpaid phone churn was a Q4 record-low 0.99% in Q4 2018, down 3 basis points from 1.02% in Q3 2018 and down 19 basis points from 1.18% in Q4 2017. |

| |

| ▪ | The sequential and year-over-year decreases were due to increased customer satisfaction and loyalty from ongoing improvements to network quality, industry-leading customer service and the overall value of our offerings. |

| |

| ▪ | For the full-year 2018, branded postpaid phone net customer additions were 3,097,000, compared to 2,817,000 in 2017. The increase was primarily driven by lower churn and continued growth in existing and Greenfield markets including the growing success of new customer |

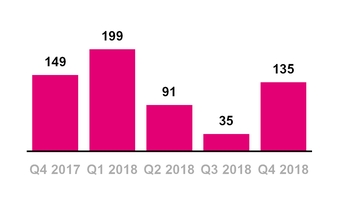

Total Branded Prepaid Net Additions

(in thousands)

segments and rate plans such as T-Mobile ONE Unlimited 55+, T-Mobile ONE Military, T-Mobile for Business and T-Mobile Essentials, partially offset by the impact from more aggressive service promotions and the launch of Un-carrier Next - All Unlimited with taxes and fees included in the first quarter of 2017.

| |

| ▪ | For the full-year 2018, branded postpaid other net customer additions were 1,362,000, compared to 803,000 in 2017. The increase was primarily due to higher gross customer additions from wearables and lower churn, partially offset by lower gross customer additions from other connected devices. |

| |

| ▪ | For the full-year 2018, branded postpaid net customer additions were 4,459,000, compared to 3,620,000 in 2017. Full-year 2018 branded postpaid net customer additions exceeded the top end of the revised and increased guidance range of 3.8 million to 4.1 million provided in connection with Q3 2018 earnings. |

| |

| ▪ | Branded postpaid phone churn was 1.01% for the full-year 2018, down 17 basis points compared to 1.18% in 2017 primarily from increased customer satisfaction and loyalty from ongoing improvements to network quality, industry-leading customer service and the overall value of our offerings. |

Branded Prepaid Customers

| |

| ▪ | Branded prepaid net customer additions were 135,000 in Q4 2018, compared to 35,000 in Q3 2018 and 149,000 in Q4 2017. |

| |

| ▪ | Sequentially, the increase was primarily due to lower churn combined with higher net adds from promotional rate plan and handset offers. |

| |

| ▪ | The year-over-year decrease was primarily due to increased competitive activity, partially offset by lower migrations to branded postpaid plans. |

| |

| ▪ | Migrations to branded postpaid plans reduced branded prepaid net customer additions in Q4 2018 by approximately 160,000, up from 140,000 in Q3 2018 and down from 180,000 in Q4 2017. |

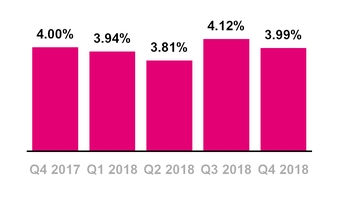

Branded Prepaid Churn

Total Branded Net Additions

(in thousands)

Wholesale Net Additions

(in thousands)

| |

| ▪ | Branded prepaid churn was 3.99% in Q4 2018, compared to 4.12% in Q3 2018 and 4.00% in Q4 2017. |

| |

| ▪ | In October 2018, MetroPCS was rebranded “Metro by T-Mobile.” This is part of an effort to highlight the links between MetroPCS and T-Mobile and better position MetroPCS to attract postpaid customers from competitors. As part of the re-branding, Metro by T-Mobile also launched several attractive new unlimited rate plans that include premium features such as Amazon Prime and Google One. |

| |

| ▪ | For the full-year 2018, branded prepaid net customer additions were 460,000, compared to 855,000 in 2017, primarily due to increased competitive activity, partially offset by lower migrations to branded postpaid plans. |

| |

| ▪ | Branded prepaid churn was 3.96% for the full-year 2018, down 8 basis points compared to 4.04% in 2017. The decrease was primarily due to the continued impact from the optimization of our third-party distribution channels which was substantially completed during the first quarter of 2017, partially offset by higher deactivations from a growing customer base and increased competitive activity. |

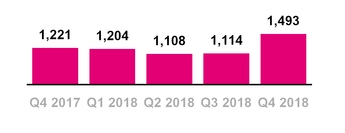

Total Branded Customers

| |

| ▪ | Total branded net customer additions were 1,493,000 in Q4 2018, compared to 1,114,000 in Q3 2018 and 1,221,000 in Q4 2017. |

| |

| ▪ | For the full-year 2018, total branded net customer additions were 4,919,000 compared to 4,475,000 in 2017. |

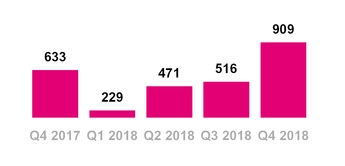

Wholesale Customers

| |

| ▪ | Wholesale net customer additions were 909,000 in Q4 2018, compared to net additions of 516,000 in Q3 2018 and 633,000 in Q4 2017. |

| |

| ▪ | Sequentially, the increase was primarily due to higher Machine-to-Machine (“M2M”) net customer additions. |

| |

| ▪ | Year-over-year, the increase was primarily due to higher M2M and mobile virtual network operator (“MVNO”) gross customer additions. |

| |

| ▪ | For the full-year 2018, wholesale net customer additions were 2,125,000 compared to 1,183,000 in 2017 primarily from lower deactivations driven by the removal of Lifeline program customers. |

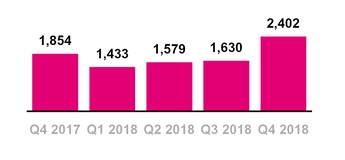

Total Net Additions

(in thousands)

Total Customers

| |

| ▪ | Total net customer additions were 2,402,000 in Q4 2018, compared to 1,630,000 in Q3 2018 and 1,854,000 in Q4 2017. This is the 23rd consecutive quarter in which T-Mobile has added more than one million total net customers. |

| |

| ▪ | T-Mobile ended Q4 2018 with 79.7 million total customers. |

| |

| ▪ | For the full-year 2018, total net customer additions were 7,044,000 compared to 5,658,000 in 2017. This was the fifth consecutive year in which total net customer additions exceeded 5 million. |

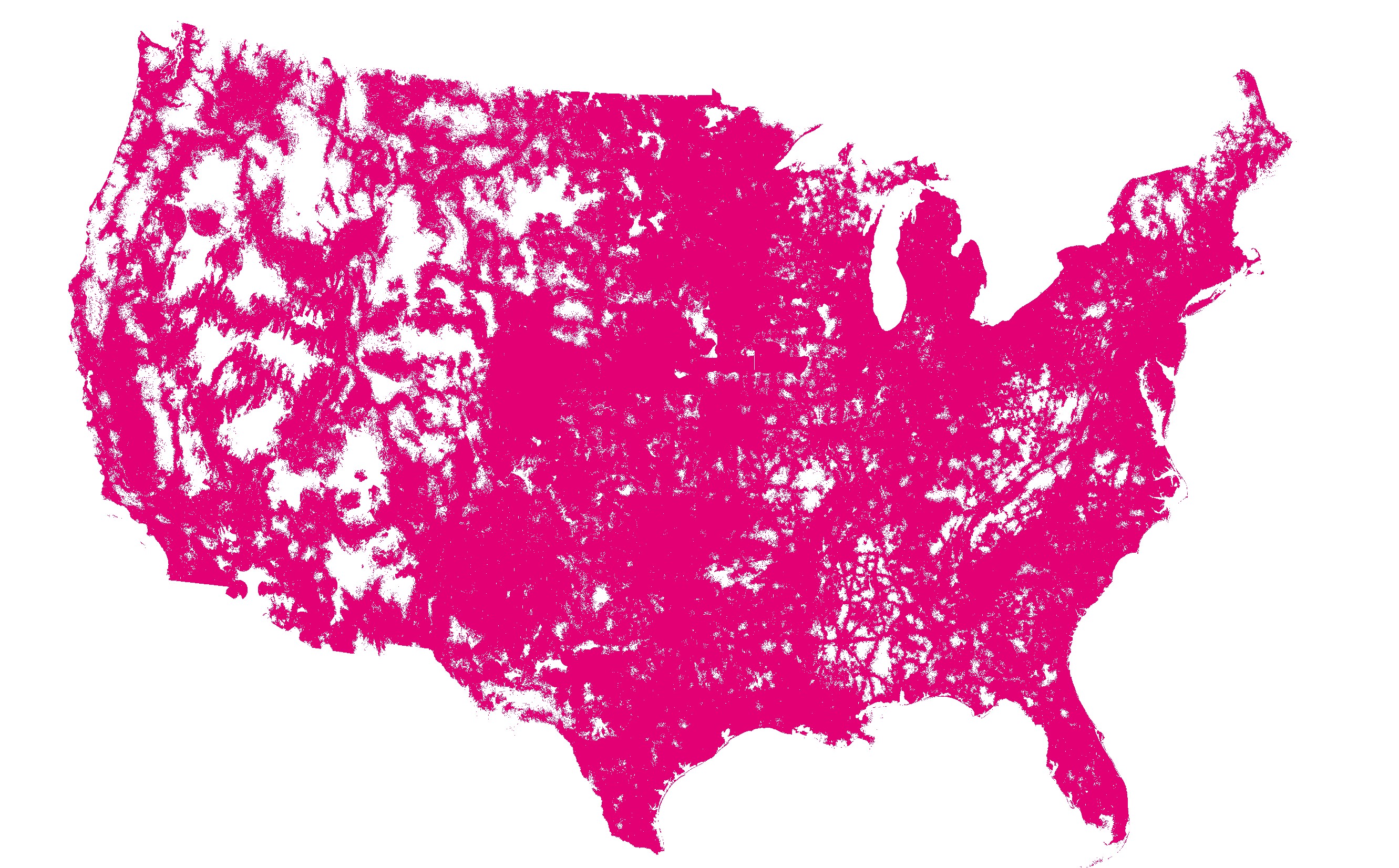

T-Mobile Coverage Map

(as of December 31, 2018)

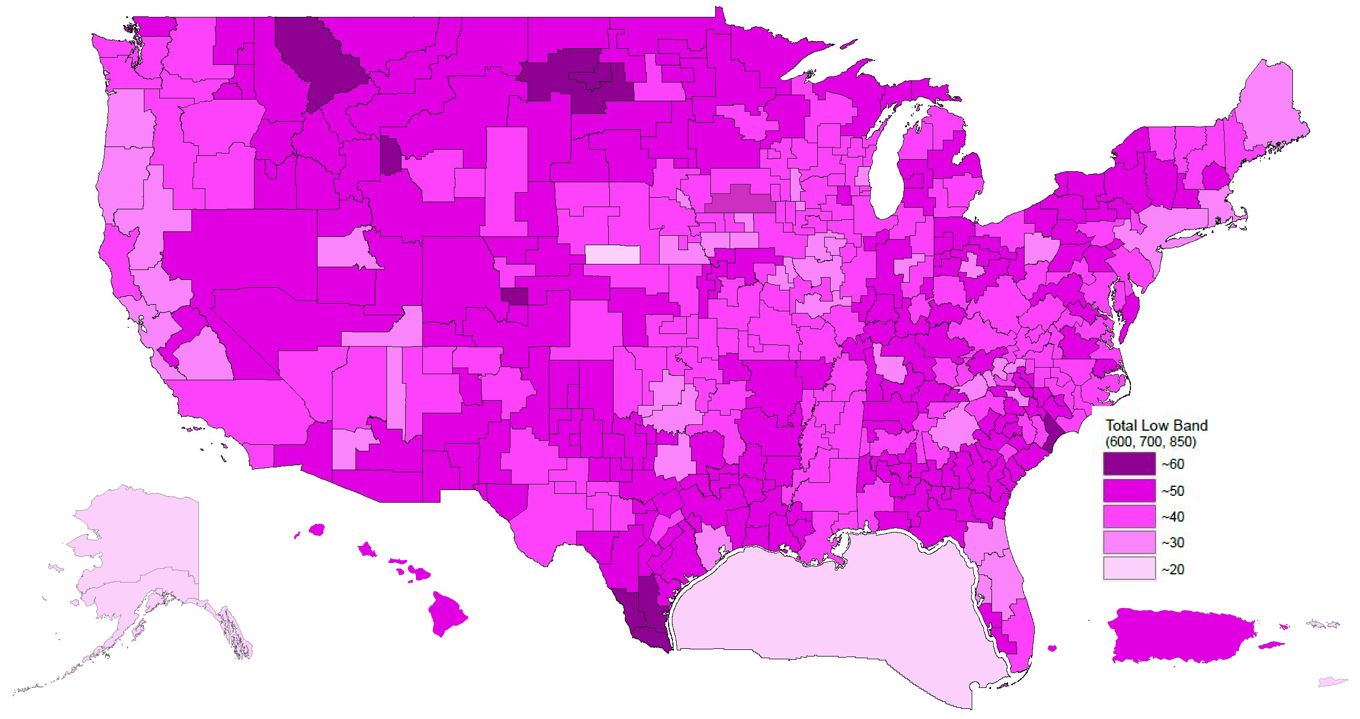

Depth of T-Mobile’s Nationwide Low-Band Spectrum (600 MHz and 700 MHz)

NETWORK

| |

| ▪ | T-Mobile continues to expand the footprint and increase the capacity of our network to better serve our customers. Our advancements in network technology and our spectrum resources ensure we can continue to increase the capabilities of our 4G LTE network as we prepare for our nationwide deployment of 5G. |

5G Update

| |

| ▪ | T-Mobile is building out 5G across the US, including six of the Top 10 markets, including New York and Los Angeles, in 2018. This network will be ready for the introduction of the first standards-based 5G smartphones in 2019. We plan on the delivery of a nationwide standards-based 5G network next year. |

| |

| ▪ | In 2018, T-Mobile entered into two multi-year contracts that will support the deployment of a nationwide 5G network. In July 2018, T-Mobile and Nokia entered into a multi-year $3.5 billion contract for Nokia to provide T-Mobile with complete end-to-end 5G technology, software and services. In September 2018, T-Mobile and Ericsson announced a multi-year $3.5 billion contract in which Ericsson will provide T-Mobile with the latest 5G New Radio (NR) hardware and software compliant with 3GPP standards. |

600 MHz Spectrum Update

| |

| ▪ | At the end of Q4 2018, T-Mobile owned a nationwide average of 31 MHz of 600 MHz low-band spectrum. T-Mobile now owns approximately 41 MHz in the low-band (600 MHz and 700 MHz). The spectrum covers 100% of the U.S. |

| |

| ▪ | T-Mobile has started deployment of 600 MHz spectrum on an aggressive schedule. At the end of Q4 2018, we were live in more than 2,700 cities and towns in 43 states and Puerto Rico covering hundreds of thousands of square miles. Combining 600 and 700 MHz spectrum, we have deployed low band spectrum to 301 million POPs. |

| |

| ▪ | T-Mobile has actively engaged with broadcasters to accelerate FCC spectrum clearance timelines, entering into 95 agreements with several parties. These agreements are expected to, in the aggregate, accelerate clearing, bringing the total clearing target to approximately 272 million POPs by year-end 2019. As of December 31, 2018, we had cleared approximately 135 million POPs. |

T-Mobile remains committed to assisting broadcasters occupying 600 MHz spectrum to move to new frequencies.

4G LTE Download Speeds and

Upload Speeds - Q4 2018

(in Mbps, D/L at Base, U/L at Top)

Based on analysis by Ookla® of Speedtest Intelligence® data.

| |

| ▪ | We currently have 29 devices compatible with 600 MHz including the latest iPhone generation. |

| |

| ▪ | We expect our 600 MHz spectrum holdings will be used to deploy America’s first nationwide standards-based 5G network next year. 600 MHz 4G LTE radios are software upgradeable to support 5G as it becomes available later this year. |

Spectrum Position

| |

| ▪ | At the end of Q4 2018, T-Mobile owned an average of 110 MHz of spectrum nationwide. The spectrum comprises an average of 31 MHz in the 600 MHz band, 10 MHz in the 700 MHz band, 29 MHz in the 1900 MHz PCS band and 40 MHz in the AWS band. |

| |

| ▪ | T-Mobile also owns millimeter wave spectrum that comprises an average of 264 MHz covering over 110 million POPs in the 28 GHz band and 105 MHz covering nearly 45 million POPs in the 39 GHz band. |

| |

| ▪ | We will evaluate future spectrum purchases in current and upcoming auctions and in the secondary market to augment our current spectrum position. |

Network Coverage Growth

| |

| ▪ | T-Mobile continues to expand its coverage breadth and covered more than 325 million people with 4G LTE at the end of Q4 2018. As promised, T-Mobile has achieved effective network population coverage parity with Verizon. |

| |

| ▪ | At the end of Q4 2018, T-Mobile had equipment deployed on approximately 64,000 macro towers and 21,000 small cell/distributed antenna system (“DAS”) sites. We remain on plan to roll out approximately 20,000 small cells through 2019. |

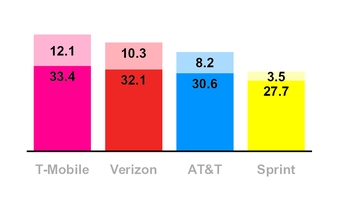

Network Speed Leadership

| |

| ▪ | We offer the fastest nationwide 4G LTE upload and download speeds in the United States. This is the 20th consecutive quarter we have led the industry in both categories, and this is based on the results of millions of user-generated speed tests. |

| |

| ▪ | In Q4 2018, T-Mobile’s average 4G LTE download speed was 33.4 Mbps, compared to Verizon at 32.1 Mbps, AT&T at 30.6 Mbps and Sprint at 27.7 Mbps. |

| |

| ▪ | In Q4 2018, T-Mobile’s average 4G LTE upload speed was 12.1 Mbps, compared to Verizon at 10.3 Mbps, AT&T at 8.2 Mbps and Sprint at 3.5 Mbps. |

Demonstrating the effect of attenuation on 600 MHz versus mmWave spectrum at CES

Network Capacity Growth

| |

| ▪ | T-Mobile continues to expand its capacity through the re-farming of existing spectrum and implementation of new technologies including Voice over LTE (“VoLTE”), Carrier Aggregation, 4x4 multiple-input and multiple-output (“MIMO”), 256 Quadrature Amplitude Modulation (“QAM”), and License Assisted Access (“LAA”). |

| |

| ▪ | VoLTE comprised 87% of total voice calls in Q4 2018, compared to 85% in Q3 2018 and up from almost 80% in Q4 2017. Moving voice traffic to VoLTE frees up spectrum and allows for the transition of spectrum currently used for 2G and 3G to 4G LTE. T-Mobile is leading the U.S. wireless industry in the rate of VoLTE adoption. |

| |

| ▪ | Carrier aggregation is live for T-Mobile customers in 923 markets. This advanced technology delivers superior speed and performance by bonding multiple discrete spectrum channels together. |

| |

| ▪ | 4x4 MIMO is currently available in 564 markets. This technology effectively delivers twice the speed and incremental network capacity to customers by doubling the number of data paths between the cell site and a customer’s device. We started deploying massive MIMO (FD-capable and 5G with future software upgrades) in selected locations in late 2018. |

| |

| ▪ | T-Mobile has rolled out 256 QAM in 988 markets. 256 QAM increases the number of bits delivered per transmission to enable faster speeds. T-Mobile is the first carrier globally to have rolled out the combination of carrier aggregation, 4x4 MIMO and 256 QAM. This trifecta of standards has been rolled out to more than 500 markets. |

| |

| ▪ | T-Mobile has also started rolling out License Assisted Access, a technology which utilizes unused 5 GHz spectrum to augment available bandwidth. The first LAA small cell went live in New York City in Q4 2017 and the technology has since been rolled out to nearly 1,700 cell sites, the vast majority being small cells. Deployments of LAA have also commenced in 28 cities including Los Angeles, Philadelphia, Washington DC, Atlanta, Houston, Las Vegas, San Diego and New Orleans. In areas where LAA has been deployed, customers with capable handsets have observed real-life speeds in excess of 500 Mbps. |

| |

| ▪ | In July 2018, T-Mobile launched its Narrowband Internet of Things (NB-IoT) service nationwide, making it the first to launch NB-IoT in the U.S. and the first in the world to launch NB-IoT in the guard bands for improved efficiency. Built on the 3GPP standard, NB-IoT is a low power, wide area network (LPWAN) LTE-Advanced technology that provides a pathway to 5G IoT and enables many comparable benefits like low power usage, long battery life and low |

device cost.

PROPOSED SPRINT TRANSACTIONS

| |

| ▪ | On April 29, 2018, T-Mobile announced that it had entered into a Business Combination Agreement with Sprint to merge in an all-stock transaction at a fixed exchange ratio of 0.10256 shares of T-Mobile common stock for each share of Sprint common stock, or 9.75 shares of Sprint common stock for each share of T-Mobile common stock (the “Merger”). The Merger, and other transactions contemplated by the Business Combination Agreement, are referred to as the “Transactions”. |

| |

| ▪ | The combined company will be named “T-Mobile” and, as a result of the Merger, is expected to be able to rapidly launch a nationwide 5G network, accelerate innovation and increase competition in the U.S. wireless, video and broadband industries. Neither T-Mobile nor Sprint on its own could generate comparable benefits to consumers. The combined company is expected to trade under the (TMUS) symbol on NASDAQ. |

| |

| ▪ | The Transactions are subject to customary closing conditions, including regulatory approvals, which we expect to receive in the first half of 2019. |

| |

| ▪ | In Q4 2018, costs related to the Sprint transaction were $102 million. In 2018, costs related to the Sprint transaction were $196 million. These costs are included in SG&A expenses and Net income but are excluded from Adjusted EBITDA. |

|

| | | | | | | | | | | | | | | | | | | | | | | |

| Impact from New revenue standard |

| (in millions, except per share and operating metric amounts) |

| | Q4 2018 | | FY 2018 |

| Increase (decrease) | Previous revenue standard | | New revenue standard | | Differ-ence | | Previous revenue standard | | New revenue standard | | Differ-ence |

| Revenues | | | | | | | | | | | |

| Total service revenues | $ | 8,238 |

| | $ | 8,189 |

| | $ | (49 | ) | | $ | 32,027 |

| | $ | 31,992 |

| | $ | (35 | ) |

| Equipment revenues | 2,825 |

| | 2,940 |

| | 115 |

| | 9,616 |

| | 10,009 |

| | 393 |

|

| Other revenues | 316 |

| | 316 |

| | — |

| | 1,309 |

| | 1,309 |

| | — |

|

| Total revenues | 11,379 |

| | 11,445 |

| | 66 |

| | 42,952 |

| | 43,310 |

| | 358 |

|

| Operating expenses | | | | | | | | | | | |

| Cost of services | 1,578 |

| | 1,602 |

| | 24 |

| | 6,233 |

| | 6,307 |

| | 74 |

|

| Cost of equipment sales | 3,574 |

| | 3,568 |

| | (6 | ) | | 12,065 |

| | 12,047 |

| | (18 | ) |

| Selling, general and administrative | 3,533 |

| | 3,498 |

| | (35 | ) | | 13,257 |

| | 13,161 |

| | (96 | ) |

| Depreciation and amortization | 1,640 |

| | 1,640 |

| | — |

| | 6,486 |

| | 6,486 |

| | — |

|

| Total operating expenses | 10,325 |

| | 10,308 |

| | (17 | ) | | 38,041 |

| | 38,001 |

| | (40 | ) |

| Operating income | 1,054 |

| | 1,137 |

| | 83 |

| | 4,911 |

| | 5,309 |

| | 398 |

|

| Other expense, net | (299 | ) | | (299 | ) | | — |

| | (1,392 | ) | | (1,392 | ) | | — |

|

| Income before income taxes | 755 |

| | 838 |

| | 83 |

| | 3,519 |

| | 3,917 |

| | 398 |

|

| Income tax expense | (176 | ) | | (198 | ) | | (22 | ) | | (926 | ) | | (1,029 | ) | | (103 | ) |

| Net income | $ | 579 |

| | $ | 640 |

| | $ | 61 |

| | $ | 2,593 |

| | $ | 2,888 |

| | $ | 295 |

|

| Earnings per share - basic | $ | 0.68 |

| | $ | 0.75 |

| | $ | 0.07 |

| | $ | 3.05 |

| | $ | 3.40 |

| | $ | 0.35 |

|

| Earnings per share - diluted | $ | 0.68 |

| | $ | 0.75 |

| | $ | 0.07 |

| | $ | 3.02 |

| | $ | 3.36 |

| | $ | 0.34 |

|

| | | | | | | | | | | | |

| Operating metrics | | | | | | | | | | | |

| Branded postpaid phone ARPU | $ | 46.27 |

| | $ | 46.29 |

| | $ | 0.02 |

| | $ | 46.45 |

| | $ | 46.40 |

| | $ | (0.05 | ) |

| Branded postpaid ABPU | $ | 57.66 |

| | $ | 57.66 |

| | $ | — |

| | $ | 58.49 |

| | $ | 58.44 |

| | $ | (0.05 | ) |

| Branded prepaid ARPU | $ | 38.47 |

| | $ | 38.39 |

| | $ | (0.08 | ) | | $ | 38.56 |

| | $ | 38.53 |

| | $ | (0.03 | ) |

| | | | | | | | | | | | |

| Non-GAAP financial measures | | | | | | | | | | | |

Adjusted EBITDA (1) | $ | 2,887 |

| | $ | 2,970 |

| | $ | 83 |

| | $ | 12,000 |

| | $ | 12,398 |

| | $ | 398 |

|

| |

| (1) | Adjusted EBITDA is a non-GAAP financial measure. This non-GAAP financial measure should be considered in addition to, but not as a substitute for, the information provided in accordance with GAAP. A reconciliation of this non-GAAP financial measure to the most directly comparable financial measure is provided in the Reconciliation of Non-GAAP Financial Measures to GAAP Financial Measures tables. |

New Revenue Standard

| |

| ▪ | The discussion and analysis below reflect the impact from ASU 2014-09, “Revenue from Contracts with Customers (Topic 606)” and related amendments (“new revenue standard”). |

| |

| ▪ | Financial statement results under the new revenue standard, as compared to the previous revenue standard, for the current reporting period are reflected in the table. |

| |

| ▪ | The most significant impacts to financial statement result as reported under the new revenue standard, as compared to the previous revenue standard, for the current reporting period are as follows: |

| |

| ▪ | Under the new revenue standard, certain commissions paid to dealers previously recognized as a reduction to Equipment revenues in our Consolidated Statements of Comprehensive Income are now recorded as commission costs in Selling, general and administrative expense. |

| |

| ▪ | Contract costs capitalized for new contracts accumulated in Other assets in our Consolidated Balance Sheets during 2018. As a result, there was a net benefit to Operating income in our Consolidated Statements of Comprehensive Income during 2018 as capitalization of costs exceeded amortization. As capitalized costs amortize into expense over time, the accretive benefit to Operating income realized in 2018 is expected to moderate in 2019 and normalize in 2020. |

| |

| ▪ | Certain promotions previously recognized as a reduction in Equipment revenues in our Consolidated Statements of Comprehensive Income are now recorded as a reduction in Service revenues. |

| |

| ▪ | Certain revenues previously recognized as Equipment revenues in our Consolidated Statements of Comprehensive Income are now recorded as Service revenues. |

| |

| ▪ | Certain contract fulfillment costs have been reclassified to Cost of services in our Consolidated Statements of Comprehensive Income from Selling, general and administrative expenses. |

| |

| ▪ | Wholesale revenues for minimum guaranteed amounts (guarantee shortfall) are recognized when it is probable that a reversal of such revenue will not occur, which may impact the timing of recognition as compared to the previous standard. |

| |

| ▪ | For contracts with promotional bill credits that are contingent on the customer maintaining a service contract that results in an extended service contract, a contract asset is recorded when control of the equipment transfers to the customer and is subsequently recognized as a reduction to Total service revenues in our Consolidated Statements of Comprehensive Income over the extended contract term. |

|

| | | | | | | | | | | | | | | | | | | | |

| Hurricane Impacts net of reimbursements |

| (in millions, except per share and operating metric amounts) |

| Increase (decrease) | | Q4 2017 | | Q3 2018 | | Q4 2018 | | FY 2017 | | FY 2018 |

| | | Net | | Net | | Net | | Net | | Net |

| Revenues | | | | | | | | | | |

| Branded postpaid revenues | | $ | (17 | ) | | $ | — |

| | $ | — |

| | $ | (37 | ) | | $ | — |

|

| Of which, branded postpaid phone revenues | | (16 | ) | | — |

| | — |

| | (35 | ) | | — |

|

| Branded prepaid revenues | | — |

| | — |

| | — |

| | (11 | ) | | — |

|

| Total service revenues | | (17 | ) | | — |

| | — |

| | (48 | ) | | — |

|

| Equipment revenues | | — |

| | — |

| | — |

| | (8 | ) | | — |

|

| Other revenues | | — |

| | 71 |

| | — |

| | — |

| | 71 |

|

| Total revenues | | $ | (17 | ) | | $ | 71 |

| | $ | — |

| | $ | (56 | ) | | $ | 71 |

|

| Operating expenses | | | | | | | | | | |

| Cost of services | | $ | 36 |

| | $ | (54 | ) | | $ | 12 |

| | $ | 105 |

| | $ | (76 | ) |

| Cost of equipment sales | | — |

| | — |

| | 1 |

| | 4 |

| | 1 |

|

| Selling, general and administrative | | — |

| | (13 | ) | | 1 |

| | 36 |

| | (12 | ) |

| Of which, bad debt expense | | — |

| | — |

| | — |

| | 20 |

| | — |

|

| Total operating expenses | | $ | 36 |

| | $ | (67 | ) | | $ | 14 |

| | $ | 145 |

| | $ | (87 | ) |

| Operating income (loss) | | $ | (53 | ) | | $ | 138 |

| | $ | (14 | ) | | $ | (201 | ) | | $ | 158 |

|

| Net income (loss) | | $ | (40 | ) | | $ | 88 |

| | $ | (11 | ) | | $ | (130 | ) | | $ | 99 |

|

| Earnings per share - basic | | $ | (0.05 | ) | | $ | 0.10 |

| | $ | (0.01 | ) | | $ | (0.16 | ) | | $ | 0.12 |

|

| Earnings per share - diluted | | $ | (0.05 | ) | | $ | 0.10 |

| | $ | (0.01 | ) | | $ | (0.15 | ) | | $ | 0.12 |

|

| | | | | | | | | | | |

| Operating metrics | | | | | | | | | | |

| Bad debt expense and losses from sales of receivables as a percentage of total revenues | | — | % | | — | % | | — | % | | 0.05 | % | | — | % |

| Branded postpaid phone ARPU | | $ | (0.16 | ) | | $ | — |

| | $ | — |

| | $ | (0.09 | ) | | $ | — |

|

| Branded postpaid ABPU | | $ | (0.15 | ) | | $ | — |

| | $ | — |

| | $ | (0.08 | ) | | $ | — |

|

| Branded prepaid phone ARPU | | $ | — |

| | $ | — |

| | $ | — |

| | $ | (0.05 | ) | | $ | — |

|

| | | | | | | | | | | |

| Non-GAAP financial measures | | | | | | | | | | |

| Adjusted EBITDA | | $ | (53 | ) | | $ | 138 |

| | $ | (14 | ) | | $ | (201 | ) | | $ | 158 |

|

HURRICANE IMPACTS

| |

| ▪ | During 2018, we recognized $61 million in costs related to hurricanes, including $36 million in incremental costs to maintain services primarily in Puerto Rico related to hurricanes that occurred in 2017 and $25 million related to hurricanes that occurred in 2018. Additional costs related to a hurricane that occurred in 2018 are expected to be immaterial in the first quarter of 2019. |

| |

| ▪ | During 2018, we received reimbursement payments from our insurance carriers of $307 million related to hurricanes, of which $93 million was previously accrued for as a receivable as of December 31, 2017. |

| |

| ▪ | We have accrued insurance recoveries related to a hurricane that occurred in 2018 of approximately $5 million for the year ended December 31, 2018 as an offset to the costs incurred within Cost of services in our Consolidated Statements of Comprehensive Income and as an increase to Other current assets in our Consolidated Balance Sheets. |

|

| | | | | |

| Devices Sold or Leased |

| (in million units) |

| | Q4 2017 | | Q3 2018 | | Q4 2018 |

| Total Company | | | | | |

| Phones | 9.7 | | 8.1 | | 8.3 |

| Mobile broadband and IoT devices | 0.7 | | 0.6 | | 0.7 |

| Total Company | 10.4 | | 8.7 | | 9.0 |

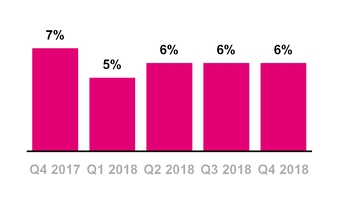

Branded Postpaid Upgrade Rate

DEVICES

| |

| ▪ | Total devices sold or leased were 9.0 million units in Q4 2018, compared to 8.7 million units in Q3 2018 and 10.4 million units in Q4 2017. |

| |

| ▪ | Total phones (smartphones and non-smartphones) sold or leased were 8.3 million units in Q4 2018, compared to 8.1 million units in Q3 2018 and 9.7 million units in Q4 2017. |

| |

| ▪ | The upgrade rate for branded postpaid customers was approximately 6% in Q4 2018, flat sequentially and down from 7% in Q4 2017. |

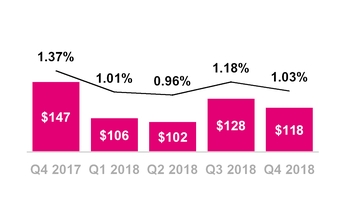

Total EIP Receivables, net and QoQ

Change in Total EIP Receivables

($ in millions)

QoQ Chng in Total EIP — Total EIP Rec., net

DEVICE FINANCING

Equipment Installment Plans (EIP)

| |

| ▪ | T-Mobile provided $2.203 billion in gross EIP device financing to its customers in Q4 2018, up 25.0% from $1.762 billion in Q3 2018 and up 5.4% from $2.090 billion in Q4 2017. |

| |

| ▪ | Sequentially the increase was primarily due to higher EIP unit sales and higher average revenue per device sold. |

| |

| ▪ | Year-over-year the increase was primarily from higher average revenue per device sold, offset by a decrease in EIP unit sales. |

| |

| ▪ | Customers on T-Mobile plans had associated EIP billings of $1.66 billion in Q4 2018, up 3.9% compared to $1.60 billion in Q3 2018 and up 5.2% from $1.58 billion in Q4 2017. EIP billings include prepayments and adjustments. |

| |

| ▪ | Total EIP receivables, net of imputed discount and allowances for credit losses, were $4.09 billion at the end of Q4 2018, compared to $3.59 billion at the end of Q3 2018 and $3.56 billion at the end of Q4 2017. |

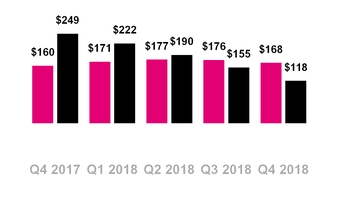

Leased Devices Transferred to P&E,

Net and Lease Revenues

($ in millions)

Leased Devices Trans. to P&E

Leasing Plans

| |

| ▪ | Leased devices transferred to property and equipment from inventory, net was $118 million in Q4 2018, compared to $155 million in Q3 2018 and $249 million in Q4 2017. |

| |

| ▪ | The sequential and year-over-year decrease was primarily due to a lower number of devices leased. |

| |

| ▪ | Depreciation expense associated with leased devices was $234 million in Q4 2018, compared to $245 million in Q3 2018 and $196 million in Q4 2017. |

| |

| ▪ | Leased devices included in property and equipment, net was $537 million at the end of Q4 2018, compared to $653 million at the end of Q3 2018 and $792 million at the end of Q4 2017. |

| |

| ▪ | Lease revenues were $168 million in Q4 2018, compared to $176 million in Q3 2018 and $160 million in Q4 2017. |

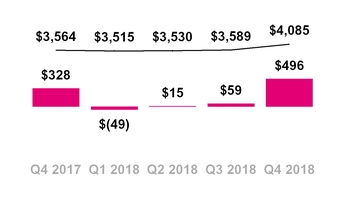

Total Bad Debt Expense and Losses from Sales of Receivables

($ in millions, % of Total Revs)

CUSTOMER QUALITY

| |

| ▪ | Total bad debt expense and losses from sales of receivables was $118 million in Q4 2018, compared to $128 million in Q3 2018 and $147 million in Q4 2017. |

| |

| ▪ | As a percentage of total revenues, total bad debt expense and losses from sales of receivables was 1.03% in Q4 2018, compared to 1.18% in Q3 2018 and 1.37% in Q4 2017. |

| |

| ▪ | Sequentially, total bad debt expense and losses from sales of receivables decreased by $10 million. As a percentage of total revenues, bad debt expense and losses from sales of receivables decreased by 15 basis points. |

| |

| ▪ | Year-over-year, total bad debt expense and losses from sales of receivables decreased by $29 million. As a percentage of total revenues, bad debt expense and losses from sales of receivables decreased by 34 basis points. The decrease reflects our ongoing focus on managing customer quality. |

| |

| ▪ | Including the EIP receivables sold, total EIP receivables classified as Prime were 53% of total EIP receivables at the end of Q4 2018, compared to 52% at the end of Q3 2018 and 54% at the end of Q4 2017. |

| |

| ▪ | For full-year 2018, total bad debt expense and losses from sales of receivables decreased to $454 million from $687 million in 2017. As a percentage of total revenues, total bad debt expense and losses from sales of receivables was 1.05% in 2018 compared to 1.69% in 2017. The decreases in both measures reflect our ongoing focus on managing customer quality. The negative impact from hurricane costs, net of insurance reimbursements, on bad debt expense was $20 million in full-year 2017 compared to no impact in full-year 2018. |

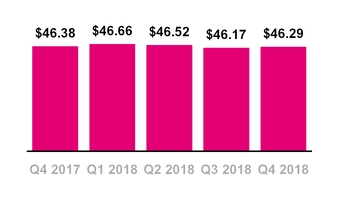

Branded Postpaid Phone ARPU

($ per month)

Branded Postpaid ABPU

($ per month)

OPERATING METRICS

Branded Postpaid Phone ARPU

| |

| ▪ | Branded postpaid phone ARPU was $46.29 in Q4 2018, up 0.3% from $46.17 in Q3 2018 and down 0.2% from $46.38 in Q4 2017. |

| |

| ▪ | Sequentially, branded postpaid phone ARPU was essentially flat. |

| |

| ▪ | Year-over-year, the slight decrease was primarily due to the growing success of new customer segments and rate plans such as T-Mobile ONE Unlimited 55+, T-Mobile ONE Military, T-Mobile for Business and T-Mobile Essentials, the impact of the ongoing growth in our Netflix offering, which totaled $0.44 for Q4 2018 and decreased branded postpaid phone ARPU by $0.33 compared to Q4 2017, as well as a reduction in certain non-recurring charges. These decreases were partially offset by a net reduction in promotional activities and an increase in insurance revenues. |

| |

| ▪ | For full-year 2018, branded postpaid phone ARPU was $46.40, down 1.2% from 2017, primarily due the growing success of new customer segments and rate plans such as T-Mobile ONE Unlimited 55+, T-Mobile ONE Military, T-Mobile for Business and T-Mobile Essentials, the impact of the ongoing growth in our Netflix offering, which totaled $0.35 for full-year 2018 and decreased branded postpaid phone ARPU by $0.32 compared to full-year 2017, and a reduction in certain non-recurring charges. The negative impact of the new revenue standard was $0.05. These decreases were partially offset by a net reduction in promotional activities. |

| |

| ▪ | We expect full-year 2019 branded postpaid phone ARPU to remain generally stable compared to full-year 2018. |

Branded Postpaid ABPU

| |

| ▪ | Branded postpaid ABPU was $57.66 in Q4 2018, down 0.1% from $57.69 in Q3 2018 and down 3.7% from $59.88 compared to Q4 2017. |

| |

| ▪ | The sequential and year-over-year decreases were primarily due to growth in the branded postpaid other customer base, which has a lower ARPU than branded postpaid phones. |

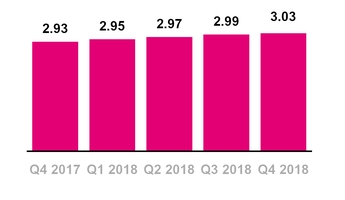

Branded Postpaid Customers per Account

Branded Prepaid ARPU

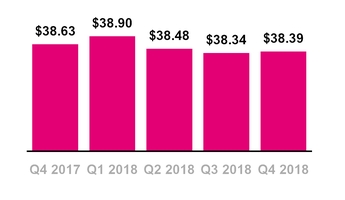

($ per month)

| |

| ▪ | For full-year 2018, branded postpaid ABPU was $58.44, down 3.4% from 2017 primarily due to lower branded postpaid phone ARPU, lower lease revenues, and growth in the branded postpaid other customer base with lower ARPU than branded postpaid phone. |

| |

| ▪ | We believe Branded postpaid ABPU was an important metric during the transition from classic plans to EIP based plans as it helped explain the customer billing relationship in a period which had shifts in customer billings from branded postpaid service revenues to equipment sales revenues. We believe the usefulness of ABPU to management, investors and analysts has decreased in recent period as the remaining classic plan base is immaterial and branded postpaid service revenue and branded postpaid phone ARPU metrics in periods presented are now comparable. We therefore plan to discontinue reporting ABPU beginning with the quarter ended March 31, 2019. |

Branded Postpaid Customers per Account

| |

| ▪ | Branded postpaid customers per account was 3.03 at the end of Q4 2018, compared to 2.99 at the end of Q3 2018 and 2.93 at the end of Q4 2017. |

| |

| ▪ | The sequential and year-over-year increase was primarily due to continued growth of new customer segments and rate plans such as T-Mobile ONE Unlimited 55+, T-Mobile ONE Military, T-Mobile for Business and T-Mobile Essentials, promotional activities targeting families and the success of connected devices. |

Branded Prepaid ARPU

| |

| ▪ | Branded prepaid ARPU was $38.39 in Q4 2018, up 0.1% from $38.34 in Q3 2018 and down 0.6% compared to $38.63 in Q4 2017. |

| |

| ▪ | The sequential increase was primarily due to the continued growth of Metro by T-Mobile customers. |

| |

| ▪ | The year-over-year decrease was primarily from dilution from promotional rate plans, partially offset by the continued growth of Metro by T-Mobile customers. |

| |

| ▪ | For full-year 2018, branded prepaid ARPU was $38.53, down 0.4% compared to $38.69 in 2017 primarily from dilution from promotional rate plans, partially offset by the continued growth of Metro by T-Mobile customers. |

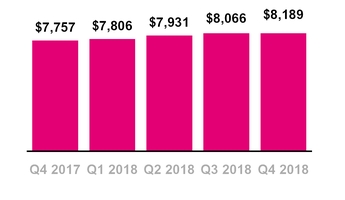

Service Revenues

($ in millions)

REVENUES

Service Revenues

| |

| ▪ | T-Mobile led the industry in year-over-year service revenue percentage growth in Q4 2018. This marks the 19th consecutive quarter that T-Mobile has led the industry in this measure. |

| |

| ▪ | Service revenues were a record-high $8.19 billion in Q4 2018, up 1.5% from $8.07 billion in Q3 2018 and up 5.6% from $7.76 billion in Q4 2017. Excluding the combined impacts from the new revenue standard and hurricanes, service revenues increased 2.7% from Q3 2018 and 6.0% from Q4 2017. |

| |

| ▪ | Sequentially, the increase was primarily due to: |

| |

| ◦ | Branded postpaid revenues increased 2.7% primarily from growth in our customer base driven by the continued growth in existing and Greenfield markets including the growing success of new customer segments and rate plans such as T-Mobile ONE Unlimited 55+, T-Mobile ONE Military, T-Mobile for Business and T-Mobile Essentials, as well as higher gross customer additions driven by seasonality and higher branded postpaid phone ARPU. |

| |

| ◦ | Wholesale revenues decreased 10.1% as expected primarily from lower commitment revenues, most of which were recognized in Q3 2018 in accordance with the new revenue recognition standard. |

| |

| ▪ | Year-over-year, the increase was primarily due to: |

| |

| ◦ | Branded postpaid revenues increased 8.0% primarily from higher average branded postpaid phone customers, primarily from growth in our customer base driven by the continued growth in existing and Greenfield markets including the growing success of new customer segments and rate plans such as T-Mobile ONE Unlimited 55+, T-Mobile ONE Military, T-Mobile for Business and T-Mobile Essentials, along with lower churn and higher average branded postpaid other customers; partially offset by lower branded postpaid phone ARPU. |

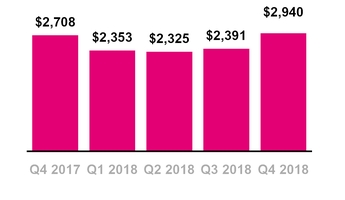

Equipment Revenues

($ in millions)

| |

▪ | For the full-year 2018, service revenues were $31.99 billion, up 6.1% compared to $30.16 billion in 2017. Excluding the combined impacts from the new revenue standard and hurricanes, service revenues increased 6.0% from 2017. |

| |

| ▪ | Branded postpaid revenues increased 7.3% due to higher average branded postpaid phone customers, primarily from growth in our customer base driven by the continued growth in existing and Greenfield markets including the growing success of new customer segments and rate plans such as T-Mobile ONE Unlimited 55+, T-Mobile ONE Military, T-Mobile for Business and T-Mobile Essentials, along with lower churn and higher average branded postpaid other customers; partially offset by lower branded postpaid phone ARPU and the negative impact of the new revenue standard of $25 million. |

| |

| ▪ | Branded prepaid revenues increased 2.3% primarily from higher average branded prepaid customers driven by the success of our Metro by T-Mobile brand; partially offset by lower branded prepaid ARPU and the negative impact of the new revenue standard of $10 million. |

| |

| ▪ | Roaming and other service revenues increased 51.7% primarily from an increase in international and domestic roaming revenues. |

Equipment Revenues

| |

| ▪ | Equipment revenues were $2.94 billion in Q4 2018, up 23.0% from $2.39 billion in Q3 2018 and up 8.6% from $2.71 billion in Q4 2017. Equipment revenues in Q4 2018 were comprised of lease revenues of $168 million and non-lease revenues of $2.77 billion. Excluding the combined impacts from the new revenue standard and hurricanes, equipment revenues increased 23.6% from Q3 2018 and 4.3% from Q4 2017. |

| |

| ▪ | Sequentially, the increase was primarily due to a higher average revenue per device sold due to an increase in the high-end device mix and a decrease in promotions, a 4% increase in the number of |

devices sold, excluding purchased leased devices, and an increase in accessory revenues, partially offset by a decrease of $39 million primarily related to lower proceeds from liquidation of returned customer handsets.

| |

| ▪ | Year-over-year, the increase was primarily due to a higher average revenue per device sold due to an increase in the high-end device mix and a positive impact from the new revenue standard of $115 million, partially offset by a 9% decrease in the number of devices sold and a decrease of $58 million primarily related to lower proceeds from liquidation of returned customer handsets. |

| |

| ▪ | The year-over-year positive impact from the new revenue standard of $115 million was primarily related to certain commission costs of $107 million previously recorded as a reduction in Equipment revenues now recorded as Selling, general and administrative expenses and promotions previously recorded as a reduction in Equipment revenues now recorded as a reduction in Service revenues, partially offset by promotional bill credits now capitalized as a contract asset and certain Equipment revenues now recognized as service revenues. |

| |

| ▪ | For the full-year 2018, equipment revenues were $10.01 billion, up 6.8% compared to $9.38 billion in 2017. Excluding the combined impacts from the new revenue standard and hurricanes, equipment revenues increased 2.5% from 2017. |

| |

| ▪ | The increase was primarily due to an increase of $1.1 billion in device sales revenues, excluding purchased leased devices, primarily due to: |

| |

| ◦ | Higher average revenue per device sold due to an increase in the high-end device mix; and |

| |

| ◦ | A positive impact from the new revenue standard of $393 million primarily related to certain commission costs of $438 million previously recorded as a reduction in Equipment revenues now recorded as Selling, general and administrative expenses and certain promotions previously recorded as a reduction in Equipment revenues now recorded as a reduction in Service revenues, partially offset by certain promotional bill credits now capitalized as contract assets and certain Equipment revenues now recognized as Service revenues; partially offset by |

| |

| ◦ | A 6% decrease in the number of devices sold, excluding purchased leased devices. |

Total Revenues

($ in millions)

| |

| ◦ | These increases were partially offset by a decrease of $310 million from lower volumes of purchased leased devices at the end of the lease |

term and a decrease of $185 million in lease revenues from JUMP! On Demand customers preferring affordable device options on leasing programs with lower monthly lease payments and shifting focus to our EIP financing option for high-end devices.

Total Revenues

| |

| ▪ | Total revenues were a record-high $11.45 billion in Q4 2018, up 5.6% from $10.84 billion in Q3 2018 and up 6.4% from $10.76 billion in Q4 2017. |

| |

| ▪ | For the full-year 2018, total revenues were $43.31 billion, up 6.7% compared to $40.60 billion in 2017. This marks the fifth consecutive year that T-Mobile has led the industry in total revenue percentage growth. |

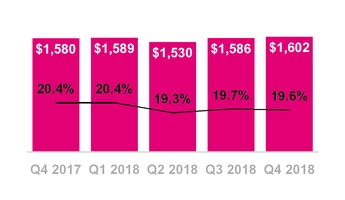

Cost of Services

($ in millions, % of Service Revs)

OPERATING EXPENSES

Cost of Services

| |

| ▪ | Cost of services was $1.60 billion in Q4 2018, up 1.0% from $1.59 billion in Q3 2018 and up 1.4% from $1.58 billion in Q4 2017. |

| |

| ▪ | Sequentially, the increase was primarily due to the positive impact of insurance reimbursements related to hurricanes, net of costs, in Q3 2018 and the impact of the accelerated rollout of low band spectrum, partially offset by lower regulatory program costs. |

| |

| ▪ | Cost of services as a percentage of Service revenues decreased by 10 basis points sequentially. Excluding the combined impacts from the new revenue standard and hurricanes, Cost of services as a percentage of Service revenues would have decreased by 110 basis points. |

| |

| ▪ | Year-over-year, the increase was primarily due to higher lease and employee-related costs associated with network expansion and the impact from the new revenue standard of $24 million. These increases were partially offset by lower regulatory program costs and the lower costs incurred related to hurricanes, net of insurance recoveries, of $12 million in Q4 2018 compared to $36 million in Q4 2017. |

| |

| ▪ | As a percentage of Service revenues, Cost of services decreased by 80 basis points year-over-year. Excluding the combined impacts from the new revenue standard and hurricanes, Cost of services as a percentage of Service revenues would have decreased by 90 basis points. |

| |

| ▪ | For the full-year 2018, Cost of services was $6.31 billion, up 3.4% compared to $6.10 billion in 2017, and up 5.2% excluding the combined impacts from the new revenue standard and hurricanes. This increase was primarily due to higher lease, employee-related and repair and maintenance expenses associated with our network expansion and the impact from the new revenue standard of $74 million primarily related to certain contract fulfillment costs reclassified to Cost of services from Selling, general and administrative expenses. These increases were partially offset by lower regulatory program costs and the positive impact from insurance reimbursements related to hurricanes, net of costs, of $76 million in 2018, compared to costs incurred related to hurricanes, net of insurance recoveries, of $105 million in 2017. |

| |

| ▪ | As a percentage of Service revenues, Cost of services declined 50 basis points from 20.2% in 2017 to 19.7% in 2018. Excluding the combined impacts from the new revenue standard and hurricanes, Cost of services as a percentage of Service revenues decreased by 10 basis points for the full-year. |

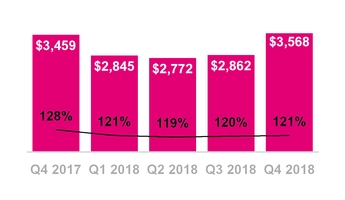

Cost of Equipment Sales

($ in millions, % of Equipment Revs)

Cost of Equipment Sales

| |

| ▪ | Cost of equipment sales was $3.57 billion in Q4 2018, up 24.7% from $2.86 billion in Q3 2018 and up 3.2% from $3.46 billion in Q4 2017. |

| |

| ▪ | Sequentially, the increase was primarily due to a $694 million increase in device cost of equipment sales, excluding purchased leased devices, primarily from a higher average cost per device sold, primarily due to an increase in the high-end device mix, and a 4% increase in the number of devices sold excluding purchased leased devices. This increase was partially offset by lower inventory adjustments. |

| |

| ▪ | Year-over-year, the increase was primarily due to an increase of $171 million in device cost of equipment sales, excluding purchased leased devices, primarily due to a higher average cost per device sold, primarily due to an increase in the high-end device mix, partially offset by a 9% decrease in the number of devices sold excluding purchased leased devices. |

| |

| ▪ | For the full-year 2018, Cost of equipment sales was $12.05 billion, up 3.8% compared to $11.61 billion in 2017. This increase was primarily from an increase of $947 million in device cost of equipment sales, excluding purchased leased devices, primarily due to a higher average cost per device sold, primarily due to an increase in the high-end device mix, partially offset by a 6% decrease in the number of devices sold, excluding purchased leased devices. This increase was partially offset by a decrease of $342 million in leased device cost of equipment sales, primarily from lower volumes of purchased leased devices at the end of the lease term and a decrease of $178 million primarily due to lower inventory adjustments and lower warranty program costs. |

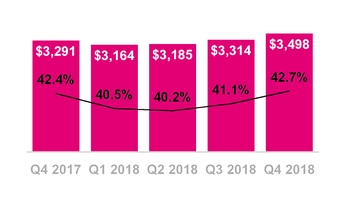

SG&A Expense

($ in millions, % of Service Revs)

Selling, General and Admin. (SG&A) Expense

| |

| ▪ | SG&A expense was $3.50 billion in Q4 2018, up 5.6% from $3.31 billion in Q3 2018 and up 6.3% from $3.29 billion in Q4 2017. |

| |

| ▪ | Sequentially, the increase was primarily due to higher promotional and advertising costs and Costs associated with the Transactions of $102 million in Q4 2018 compared to $53 million in Q3 2018. As a percentage of Service revenues, SG&A expense increased 160 basis points sequentially. |

| |

| ▪ | Excluding the combined impacts from the new revenue standard, hurricanes and Costs associated with the Transactions, SG&A expense as a percentage of Service revenues would have increased by 70 basis points. |

| |

| ▪ | Year-over-year, the increase was primarily due to: |

| |

| ▪ | Higher employee-related costs and costs related to managed services, higher commissions driven by compensation structure and channel mix changes, higher outsourcing expense and Costs associated with the Transactions of $102 million in Q4 2018. |

| |

| ▪ | These increases were partially offset by lower bad debt expense and lower promotional and advertising costs reflecting our ongoing focus on managing customer quality. As a percentage of Service revenues, SG&A expense increased 30 basis points year-over-year. |

| |

| ▪ | Excluding the combined impacts from the new revenue standard, hurricanes and Costs associated with the Transactions, SG&A expense as a percentage of Service revenues would have decreased by 70 basis points. |

| |

| ▪ | For the full-year 2018, SG&A expenses were $13.16 billion, up 7.4% compared to $12.26 billion in 2017 due to: |

| |

| ▪ | Higher employee-related costs and costs related to managed services, higher commissions driven by compensation structure and channel mix changes and Costs associated with the Transactions of $196 million; partially offset by |

| |

| ▪ | The positive impact from the new revenue standard of $96 million, primarily due to capitalized commission costs in excess of the related amortization of $495 million and certain contract fulfillment costs reclassified to Cost of services from Selling, general and administrative expenses; partially offset by commission costs of $438 million previously recorded as a reduction in Equipment revenues now recognized in Selling, general and administrative expense; |

| |

| ▪ | Lower bad debt expense and losses from sales of receivables reflecting our ongoing focus on managing customer quality, lower promotional and advertising costs, lower handset repair services costs due to lower demand for repaired phones for the fulfillment of warranty and insurance claims following the introduction of the AppleCare+ Program in the third quarter of 2017; and |

| |

| ▪ | The positive impact from insurance reimbursements related to hurricanes, net of costs, of $12 million in 2018, compared to costs incurred related to hurricanes of $36 million in 2017. |

| |

| ▪ | As a percentage of Service revenues, SG&A expense increased 50 basis points to 41.1% during 2018. Excluding the combined impacts from the new revenue standard, hurricanes and Costs associated with the Transactions, SG&A expenses as a percentage of Service revenues would have increased 30 basis points. |

D&A Expense

($ in millions, % of Total Revs)

Depreciation and Amortization (D&A)

| |

| ▪ | D&A was $1.64 billion in Q4 2018, up 0.2% from $1.64 billion in Q3 2018 and up 10.4% from $1.49 billion in Q4 2017. |

| |

| ▪ | D&A related to leased devices was $234 million in Q4 2018, compared to $245 million in Q3 2018 and $196 million in Q4 2017. |

| |

| ▪ | Non-lease-related D&A was $1.41 billion in Q4 2018, compared to $1.39 billion in Q3 2018 and $1.29 billion in Q4 2017. |

| |

| ▪ | Sequentially, the increase was primarily due to the continued build-out of our 4G LTE network. |

| |

| ▪ | Year-over-year, the increase was primarily due to the continued build-out of our 4G LTE network, deployment of low band spectrum and 5G compatible radios and higher depreciation expense related to our JUMP! On Demand program. |

| |

| ▪ | For the full-year 2018, D&A was $6.49 billion, up 8.4% compared to $5.98 billion in 2017 primarily from the continued build-out of our 4G LTE network and deployment of low band spectrum and 5G compatible radios, and the implementation of the first component of our new billing system, partially offset by lower depreciation expense related to our JUMP! On Demand program resulting from an increase in the affordable device mix. |

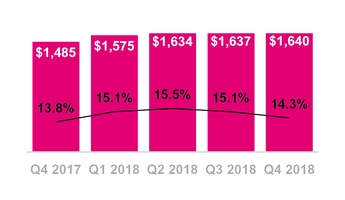

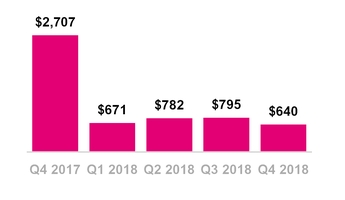

Net Income

($ in millions)

Q4 2017 Net income includes the impact from the Tax Cuts Jobs Act (“TCJA”) of $2.18 billion.

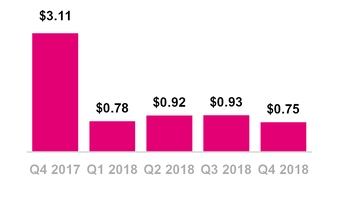

Diluted Earnings Per Share

Q4 2017 EPS includes the impact from TCJA of $2.50.

NET INCOME AND

DILUTED EARNINGS PER SHARE (“EPS”)

| |

| ▪ | Net income was $640 million in Q4 2018, down 19% from $795 million in Q3 2018 and down 76% from $2.71 billion in Q4 2017. EPS was $0.75 in Q4 2018, down from $0.93 in Q3 2018 and down from $3.11 in Q4 2017. |

| |

| ▪ | Sequentially, the decreases in Net income and EPS were primarily due to lower Operating income, partially offset by lower Income tax expense. Net income and EPS included the following: |

| |

| ◦ | The negative impact from the Transactions on Net income and EPS for Q4 2018 of $88 million and $0.10, respectively, compared to a negative impact of $53 million and $0.06 in Q3 2018, respectively. |

| |

| ◦ | The negative impact from hurricane costs, net of insurance reimbursements, on Net income and EPS for Q4 2018 of $11 million and $0.01, respectively, compared to the positive impact on Net income and EPS from insurance reimbursements related to hurricanes, net of costs, of $88 million and $0.10, respectively, for Q3 2018. |

| |

| ◦ | The lower net positive impact from the new revenue standard on Net income and EPS in Q4 2018 of $61 million and $0.07, respectively, compared to $101 million and $0.12 in Q3 2018, respectively. |

| |

| ▪ | Year-over-year, the decreases in Net income and EPS were primarily due to the positive impact of the TCJA on Net income in Q4 2017. Net income and EPS included the following: |

| |

| ◦ | Higher effective tax rates in 2018. A lower effective income tax rate in 2017 was primarily due to the impact of the TCJA, which resulted in a net tax benefit of $2.18 billion in Q4 2017. The EPS impact of the TCJA was $2.50 in Q4 2017. |

| |

| ◦ | The positive tax-effected impact from spectrum gains on Net income and EPS was $124 million and $0.15, respectively in Q4 2017. There were no spectrum gains in Q4 2018. |

| |

| ◦ | The negative impact from the Transactions on Net income and EPS for Q4 2018 of $88 million and $0.10, respectively. |

| |

| ◦ | The net positive impact from the new revenue standard on Net income and EPS in Q4 2018 was $61 million and $0.07, respectively. |

| |

| ◦ | The negative impact from hurricane costs, net of insurance reimbursements, on Net income and EPS for Q4 2018 of $11 million and $0.01, respectively compared to a negative impact of $40 million and $0.05, respectively for Q4 2017. |

| |

| ◦ | Net income margin was 8% in Q4 2018, compared to 10% in Q3 2018 and 35% in Q4 2017. Net income margin is calculated as net income divided by service revenues. |

| |

| ▪ | For the full-year 2018, Net income was $2.89 billion down 36% from $4.54 billion in 2017 and EPS was $3.36, down from $5.20 in 2017. |

| |

| ▪ | The decrease in Net income and EPS was primarily due to the positive impact of the TCJA on Net income in Q4 2017, partially offset by higher Operating income and lower Other income (expense), net. Net income and EPS included the following: |

| |

| ◦ | The impact from the TCJA on net income and EPS for 2017 was $2.18 billion and $2.49, respectively. |

| |

| ◦ | Costs associated with the Transactions on Net income and EPS was $180 million and $0.21, respectively, in 2018. |

| |

| ◦ | The tax-effected impact from spectrum gains on Net income and EPS was $174 million and $0.20, respectively, in 2017. There were no spectrum gains in 2018. |

| |

| ◦ | The net positive impact of the new revenue standard on net income and EPS was $295 million and $0.34, respectively. |

| |

| ◦ | Insurance reimbursements related to hurricanes, net of costs, on Net income and EPS for 2018 was $99 million and $0.12, respectively, compared to costs of $130 million and $0.15, respectively, in 2017. |

| |

| ▪ | Net income margin was 9% in 2018, compared to 15% in 2017. The impact of the TCJA on net income margin was 7% in 2017. |

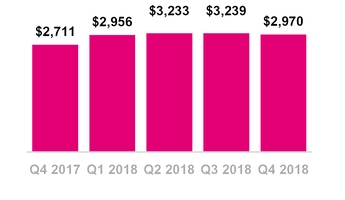

Adjusted EBITDA

($ in millions)

ADJUSTED EBITDA

| |

| ▪ | Adjusted EBITDA was $3.0 billion in Q4 2018, down 8.3% from $3.2 billion in Q3 2018 and up 9.6% from $2.7 billion in Q4 2017. |

| |

| ▪ | Sequentially, the decrease in Adjusted EBITDA was primarily due to higher costs, specifically SG&A expenses, and the negative impact of hurricane costs, net of insurance reimbursements, compared to a positive impact of insurance reimbursements related to hurricanes, net of costs, in Q3 2018, partially offset by higher Total revenues and a lower positive impact from the new revenue standard. |

| |

| ◦ | The negative impact from hurricane costs, net of insurance reimbursements, was $14 million in Q4 2018 compared to the positive impact of insurance reimbursements related to hurricanes, net of costs, of $138 million in Q3 2018. |

| |

| ◦ | The net positive impact from the new revenue standard was $83 million in Q4 2018 compared to $136 million in Q3 2018. |

| |

| ◦ | Excluding the combined impacts from the hurricanes and the new revenue standard in Q4 2018 and Q3 2018, Adjusted EBITDA declined by 2.2% sequentially. |

| |

| ▪ | Year-over-year, the increase in Adjusted EBITDA was primarily due to higher revenues, the positive impact from the new revenue standard, lower negative impact from hurricane costs, net of insurance reimbursements, and lower losses on equipment, partially offset by higher SG&A expenses and gains on disposal of spectrum licenses in Q4 2017. |

| |

| ◦ | The net positive impact from the new revenue standard of $83 million in Q4 2018. |

| |

| ◦ | The negative impact from hurricane costs, net of insurance reimbursements, was $14 million in Q4 2018 compared to $53 million in Q4 2017. |

| |

| ◦ | There were no gains on disposal of spectrum licenses in Q4 2018 compared to $168 million Q4 2017. |

| |

| ◦ | Excluding the combined impacts from the hurricanes, the new revenue standard and gains on the disposal of spectrum in Q4 2018 and Q4 2017, Adjusted EBITDA increased by 11.7% year-over-year. |

| |

| ▪ | Adjusted EBITDA margin was 36% in Q4 2018, compared to 40% in Q3 2018 and 35% in Q4 2017. Adjusted EBITDA margin is calculated as Adjusted EBITDA divided by Service revenues. |

| |

| ▪ | Adjusted EBITDA was $12.40 billion for full-year 2018, up 10.6% from $11.21 billion in full-year 2017. This increase was primarily due to higher service revenues, the positive impact from the new revenue standard, higher other revenues, lower net losses on equipment and the positive impact from insurance reimbursements related to hurricanes, net of costs, partially offset by higher SG&A expenses, lower gains on disposal of spectrum licenses, and higher cost of services. |

| |

| ▪ | The net positive impact from the new revenue standard was $398 million in 2018. |

| |

| ▪ | The positive impact from insurance reimbursements related to hurricanes, net of costs, was of $158 million in 2018 compared to the negative impact of hurricane costs, net of insurance reimbursements, of $201 million in 2017. |

| |

| ▪ | There were no gains on disposal of spectrum licenses in 2018 compared to $235 million in 2017. |

| |

| ▪ | Excluding the combined impacts from the hurricanes, the new revenue standard and gains on the disposal of spectrum in 2018 and 2017, Adjusted EBITDA increased by 5.9% year-over-year. |

| |

| ▪ | Adjusted EBITDA margin was 39% in 2018, compared to 37% in 2017. Adjusted EBITDA margin is calculated as Adjusted EBITDA divided by Service revenues. |

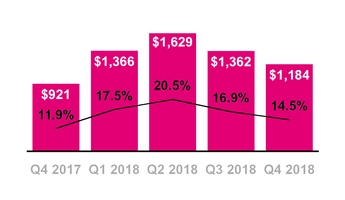

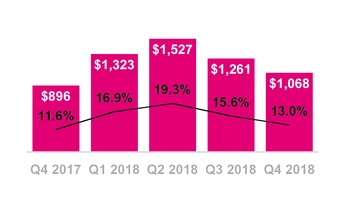

Cash Purchases of Property and Equipment

($ in millions, % of Service Revs)

Cash Purchases of Property and Equipment, Excluding Capitalized Interest

($ in millions, % of Service Revs)

CAPITAL EXPENDITURES

| |

| ▪ | Cash purchases of property and equipment were $1.18 billion in Q4 2018, compared to $1.36 billion in Q3 2018 and $921 million in Q4 2017. |

| |

| ▪ | Sequentially, the decrease was primarily due to fluctuations in the timing of the build-out of our network, including the build-out of the 600 MHz low-band spectrum. |

| |

| ▪ | Year-over-year the increase was primarily due to the accelerated rollout of our 600 MHz low-band spectrum and laying the groundwork for 5G. |

| |

| ▪ | Cash purchases of property and equipment, excluding capitalized interest, were $1.07 billion in Q4 2018, compared to $1.26 billion in Q3 2018 and $896 million in Q4 2017. |

| |

| ▪ | Capitalized interest included in cash purchases of property and equipment was $116 million in Q4 2018, compared to $101 million in Q3 2018 and $25 million in Q4 2017. |

| |

| ▪ | For the full year 2018, cash purchases of property and equipment were $5.54 billion compared to $5.24 billion for the full year 2017. The increase was primarily due to growth in network build as we continued deployment of low band spectrum, including the continued deployment of 600 MHz, and started laying the groundwork for 5G. |

| |

| ▪ | For the full year 2018, cash purchases of property and equipment excluding capitalized interest were $5.18 billion compared to $5.10 billion full year 2017. |

| |

| ▪ | Capitalized interest included in cash capital expenditures was $362 million for the full year 2018 and $136 million for the full year 2017. |

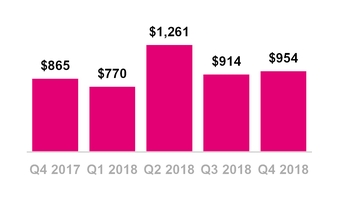

Net Cash Provided by Operating Activities(1)

($ in millions)

| |

| (1) | In Q1 2018, the adoption of the new cash flow accounting standard resulted in a reclassification of cash flows related to the deferred purchase price from securitization transactions from operating activities to investing activities. In addition, cash flows related to debt prepayment and extinguishment costs were reclassified from operating activities to financing activities. The effects of this change are applied retrospectively and are provided in the Reconciliation of Non-GAAP Financial Measures to GAAP Financial Measures tables. |

CASH FLOW

Operating Activities

| |

| ▪ | Net cash provided by operating activities was $954 million in Q4 2018, compared to $914 million in Q3 2018 and $865 million in Q4 2017. |

| |

| ▪ | Sequentially, the increase was primarily due to lower net cash outflows from working capital changes, partially offset by lower Net income and net non-cash adjustments to Net income. |

| |

| ◦ | The change in working capital was primarily due to increases in Accounts payable and accrued liabilities, partially offset by higher cash outflows in EIP receivables and Accounts receivable. |

| |

| ▪ | Year-over-year, the increase was primarily due to an increase in net non-cash adjustments to Net income, partially offset by lower Net income and higher net cash outflows from working capital changes. |

| |

| ◦ | The change in Net income and the net non-cash adjustments to Net income were primarily due to Deferred income tax expense in Q4 2018, compared to a large benefit related to the TCJA in Q4 2017, and the absence of Gains on disposal of spectrum licenses in Q4 2018. |

| |

| ◦ | The change in working capital was primarily due to a paydown of Accounts payable and accrued liabilities, partially offset by a decrease in cash outflows related to changes in Inventories. |

| |

| ▪ | For the full-year 2018, net cash provided by operating activities was $3.90 billion compared to $3.83 billion for full year 2017. This increase was primarily due to higher net non-cash adjustments to Net income, partially offset by lower Net income and higher net cash outflows from working capital changes. |

| |

| ▪ | The change in Net income and the net non-cash adjustments to Net income were primarily from the impacts of the TCJA in 2017 and the absence of Gains on disposal of spectrum licenses in 2018. |

| |

| ▪ | The higher net use in working capital was primarily from a paydown of Accounts payable and changes in Accounts receivable, partially offset by changes in Inventories and EIP receivables. |

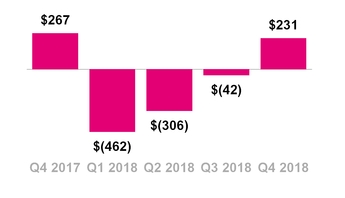

Net Cash Provided by (Used in) Investing Activities(1)

($ in millions)

| |

| (1) | In Q1 2018, the adoption of the new cash flow accounting standard resulted in a reclassification of cash flows related to the deferred purchase price from securitization transactions from operating activities to investing activities. In addition, cash flows related to debt prepayment and extinguishment costs were reclassified from operating activities to financing activities. The effects of this change are applied retrospectively and are provided in the Reconciliation of Non-GAAP Financial Measures to GAAP Financial Measures tables. |

Net Cash Provided by (Used in)

Financing Activities (1)

($ in millions)

| |

| (1) | In Q1 2018, the adoption of the new cash flow accounting standard resulted in a reclassification of cash flows related to the deferred purchase price from securitization transactions from operating activities to investing activities. In addition, cash flows related to debt prepayment and extinguishment costs were reclassified from operating activities to financing activities. The effects of this change are applied retrospectively and are provided in the Reconciliation of Non-GAAP Financial Measures to GAAP Financial Measures tables. |

Investing Activities

| |

| ▪ | Net cash from investing activities was an inflow $231 million in Q4 2018, compared to an outflow of $42 million in Q3 2018 and an inflow of $267 million in Q4 2017. Net cash used for securitization was $36 million in Q4 2018 compared to $18 million in Q3 2018 and net cash proceeds from securitization of $95 million in Q4 2017. |

| |

| ▪ | Sequentially, the change was primarily due to lower purchases of property and equipment, including capitalized interest, and higher proceeds related to our deferred purchase price from securitization transactions. |

| |

| ▪ | Year-over-year, the change was primarily due to higher purchases of property and equipment, including capitalized interest, partially offset by higher proceeds related to our deferred purchase price from securitization transactions. |

| |

| ▪ | For the full-year 2018, cash used in investing activities was $579 million compared to $6.7 billion for full year 2017. The decrease was primarily due to a decrease in purchases of spectrum licenses and higher proceeds related to our deferred purchase price from securitization transactions, partially offset by cash used for our acquisitions of Layer3 and IWS in 2018 and an increase in purchases of property and equipment, including capitalized interest. Net cash used for securitization was $179 million in 2018 as compared to net cash proceeds from securitization of $28 million in 2017. |

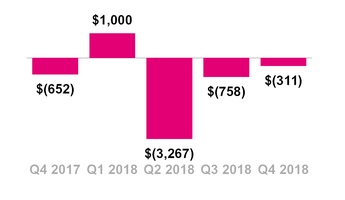

Financing Activities

| |

| ▪ | Net cash used in financing activities was $311 million in Q4 2018, compared to $758 million in Q3 2018 and $652 million in Q4 2017. |

| |

| ▪ | Sequentially, the change was primarily due to lower repayments of the revolving credit facility and short-term debt, partially offset by lower proceeds from the revolving credit facility. |

| |

| ▪ | Year-over-year, the change was primarily due to no purchases of common stock in Q4 2018 and higher proceeds from borrowing on the revolving credit facility, partially offset by higher repayments of the revolving credit facility and repayments of capital lease obligations. |

| |

| ▪ | For the full-year 2018, cash used in financing activities was $3.34 billion compared to $1.37 billion for full year 2017. The change was primarily due to lower proceeds from the issuance of long-term debt and higher repurchases of common stock, partially offset by lower repayments of long-term debt. |

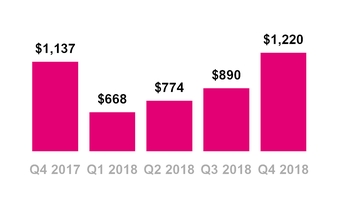

Free Cash Flow (1)

($ in millions)

| |

| (1) | In Q1 2018, the adoption of the new cash flow accounting standard resulted in a reclassification of cash flows related to the deferred purchase price from securitization transactions from operating activities to investing activities. In addition, cash flows related to debt prepayment and extinguishment costs were reclassified from operating activities to financing activities. In Q1 2018, we redefined Free Cash Flow to reflect the above changes in classification and present cash flows on a consistent basis for investor transparency. The effects of this change are applied retrospectively. |

FREE CASH FLOW

| |

| ▪ | Free Cash Flow was $1.22 billion in Q4 2018, compared to $890 million in Q3 2018 and $1.14 billion in Q4 2017. |

| |

| ▪ | Sequentially, the increase was due to lower cash purchases of property and equipment, higher proceeds related to our deferred purchase price from securitization transactions and higher net cash provided by operating activities, as described above. |

| |

| ▪ | Year-over-year, the increase was due to higher proceeds related to our deferred purchase price from securitization transactions and higher net cash provided by operating activities, as described above, partially offset by higher cash purchases of property and equipment. |

| |

| ▪ | Net cash used for securitization was $36 million in Q4 2018 compared to $18 million in Q3 2018 and net cash proceeds from securitization of $95 million in Q4 2017. |

| |

| ▪ | For the full-year 2018, Free Cash Flow was $3.55 billion compared to $2.73 billion for full year 2017. The increase was due to higher proceeds related to our deferred purchase price from securitization transactions and net cash provided by operating activities, partially offset by an increase in cash purchases of property and equipment. The increase in purchases of property and equipment was primarily due to growth in our network build, including the continued deployment of 600 MHz, and laying the groundwork for 5G. Net cash used for securitization was $179 million in 2018 as compared to net cash proceeds from securitization of $28 million in 2017. |

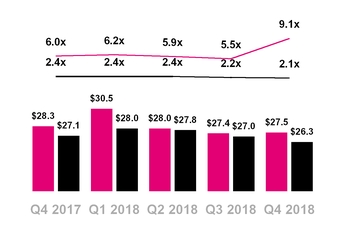

Total Debt and Net Debt (excl. Tower Obligations)

Net Debt to LTM Net Income

Net Debt to LTM Adjusted EBITDA

($ in billions)

Total Debt (excl. Tower Obligations) Net Debt (excl. Tower Obligations) — Net Debt (excl. Tower Obligations) to LTM Net income

— Net Debt (excl. Tower Obligations) to LTM Adj. EBITDA

CAPITAL STRUCTURE

| |

| ▪ | Total debt, excluding tower obligations, at the end of Q4 2018 was $27.5 billion and was comprised of the following: |

| |

| ▪ | $841 million of short-term debt, |

| |

| ▪ | $12.1 billion of long-term debt, and |

| |

| ▪ | $14.6 billion of long-term debt to affiliates. |

| |

| ▪ | Net debt, excluding tower obligations, at the end of Q4 2018 was $26.3 billion. |

| |

| ▪ | The ratio of net debt, excluding tower obligations, to net income for the trailing last twelve months (“LTM”) period was 9.1x at the end of Q4 2018, compared to 5.5x at the end of Q3 2018 and 6.0x at the end of Q4 2017. The increase in the ratio of net debt, excluding tower obligations, to net income for the LTM sequentially and year-over-year was primarily due the impact of the Q4 2017 income tax benefit, which was included in the LTM period ended Q3 2018 and Q4 2017. |

| |

| ▪ | The ratio of net debt, excluding tower obligations, to Adjusted EBITDA for the trailing LTM period was 2.1x at the end of Q4 2018, compared to 2.2x at the end of Q3 2018 and 2.4x at the end of Q4 2017. |

|

| | | |

| 2019 Guidance Outlook |

| |

| | FY 2019 |

| Branded Postpaid Net Adds (in millions) | 2.6 | | 3.6 |

| Adjusted EBITDA ($ in billions) | $12.7 | | $13.2 |

| Cash purchases of prop and equip excl Cap Int of approx. $400 million ($ in billions) | $5.4 | | $5.7 |

| Net cash provided by op act 3-yr CAGR | 17% | | 21% |

| Free Cash Flow three-year CAGR | 46% | | 48% |

GUIDANCE

| |

| ▪ | Branded postpaid net customer additions: Branded postpaid net customer additions for the full-year 2019 are expected to be 2.6 to 3.6 million. |

| |

| ▪ | Net Income: We are not able to forecast net income on a forward-looking basis without unreasonable efforts due to the high variability and difficulty in predicting certain items that affect GAAP net income including, but not limited to, income tax expense, stock-based compensation expense and interest expense. Adjusted EBITDA should not be used to predict net income as the difference between the two measures is variable. The new leasing standard is expected to increase Net Income by $140 to $180 million. |

| |

| ▪ | Adjusted EBITDA: For the full-year 2019, excluding the impact of the new lease standard, Adjusted EBITDA is expected to be in the range of $12.7 to $13.2 billion. This target includes expected leasing revenues of $0.6 to $0.7 billion and takes into account the network expansion, the deployment of our 600 MHz spectrum, and the build-out of our 5G network, driving up Cost of Services by $200 to $300 million year-over-year. The new lease standard is expected to decrease Adjusted EBITDA by $40 to $80 million. |

| |