UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-21533 | |||||||

| ||||||||

Western Asset Inflation Management Fund Inc. | ||||||||

(Exact name of registrant as specified in charter) | ||||||||

| ||||||||

55 Water Street, New York, NY |

| 10041 | ||||||

(Address of principal executive offices) |

| (Zip code) | ||||||

| ||||||||

Robert I. Frenkel, Esq. Legg Mason & Co., LLC 100 First Stamford Place Stamford, CT 06902 | ||||||||

(Name and address of agent for service) | ||||||||

| ||||||||

Registrant’s telephone number, including area code: | (888)777-0102 |

| ||||||

| ||||||||

Date of fiscal year end: | December 31 |

| ||||||

| ||||||||

Date of reporting period: | December 31, 2009 |

| ||||||

ITEM 1. REPORT TO STOCKHOLDERS.

The Annual Report to Stockholders is filed herewith.

ANNUAL REPORT / DECEMBER 31, 2009

Western Asset Inflation Management Fund Inc.

(IMF)

Managed by WESTERN ASSET

|

|

|

| INVESTMENT PRODUCTS: NOT FDIC INSURED · NO BANK GUARANTEE · MAY LOSE VALUE |

|

|

|

|

Fund objective

The Fund’s primary investment objective is total return. Current income is a secondary investment objective.

What’s inside

Letter from the chairman | I |

|

|

Fund overview | 1 |

|

|

Fund at a glance | 5 |

|

|

Schedule of investments | 6 |

|

|

Statement of assets and liabilities | 11 |

|

|

Statements of operations | 12 |

|

|

Statements of changes in net assets | 13 |

|

|

Statements of cash flows | 14 |

|

|

Financial highlights | 16 |

|

|

Notes to financial statements | 17 |

|

|

Report of independent registered public accounting firm | 32 |

|

|

Board approval of management and subadvisory agreements | 33 |

|

|

Additional information | 39 |

|

|

Annual chief executive officer and chief financial officer certifications | 45 |

|

|

Dividend reinvestment plan | 46 |

|

|

Important tax information | 48 |

Legg Mason Partners Fund Advisor, LLC (“LMPFA”) is the Fund’s investment manager. Western Asset Management Company (“Western Asset”), Western Asset Management Company Limited (“Western Asset Limited”) and Western Asset Management Company Pte. Ltd. (“Western Singapore”) are the Fund’s subadvisers. LMPFA, Western Asset, Western Asset Limited and Western Singapore are wholly-owned subsidiaries of Legg Mason, Inc.

Letter from the chairman

Dear Shareholder,

At a meeting held in May 2009, the Fund’s Board of Directors approved a recommendation from Legg Mason Partners Fund Advisor, LLC, the Fund’s investment manager, to change the fiscal year-end of the Fund from October 31 to December 31. As a result of this change, shareholders are being provided with a short-period annual report for the two-month period from November 1, 2009 through December 31, 2009.

Please read on for a more detailed look at the prevailing economic and market conditions during the Fund’s abbreviated reporting period and to learn how those conditions have affected Fund performance. Important information with regard to recent regulatory developments that may affect the Fund is contained in the Notes to Financial Statements included in this report. Please refer to the Fund’s annual report for the period ended October 31, 2009 for additional information.

As always, thank you for your confidence in our stewardship of your assets. We look forward to helping you meet your financial goals.

Sincerely,

R. Jay Gerken, CFA

Chairman, President and Chief Executive Officer

January 29, 2010

Western Asset Inflation Management Fund Inc. |

Fund overview

Q. What is the Fund’s investment strategy?

A. The Fund’s primary investment objective is total return. Current income is a secondary objective. The Fund invests the majority of its assets in inflation-protected securities issued by U.S. and non-U.S. governments, their agencies or instrumentalities, and corporate securities that are structured to provide protection against inflation. We also have the flexibility to invest in certain other fixed-income securities that we believe will provide protection against inflation. Inflation-protected securities will include U.S. Treasury Inflation-Protected Securities (“TIPS”)i, as well as other bonds issued by U.S. and non-U.S. government agencies or instrumentalities or corporations and derivatives related to these securities.

At Western Asset Management Company (“Western Asset”), the Fund’s subadviser, we utilize a fixed-income team approach, with decisions derived from interaction among various investment management sector specialists. The sector teams are comprised of Western Asset’s senior portfolio managers, research analysts and an in-house economist. Under this team approach, management of client fixed-income portfolios will reflect a consensus of interdisciplinary views within the Western Asset organization.

Q. What were the overall market conditions during the Fund’s reporting period?

A. During the two-month reporting period from November 1, 2009 through December 31, 2009, U.S. Treasury yields moved higher (and their prices lower), whereas the spread sectors (non-Treasuries) generally performed well. The yields on two- and ten-year Treasuries began the period at 0.90% and 3.41%, respectively. Yields then moved steadily higher through the end of the year, as economic data was generally better than anticipated and expectations for inflation increased. When the period ended on December 31, 2009, the yields on two- and ten-year Treasuries were 1.14% and 3.85%, respectively. Inflation expectations led to increased demand for TIPS, and the Barclays Capital Global Real Index: U.S. TIPSii gained 0.53% during the two months ended December 31, 2009.

In contrast to the Treasury market, the spread sectors, overall, generated solid results during the two-month period. As was the case during much of 2009, the spread sectors benefited from improving credit conditions, encouraging economic data and increased investor risk appetite. Also supporting the spread sectors was strong demand from investors seeking incremental yields, given the low rates available from short-term fixed-income securities. All told, lower-quality bonds outperformed higher-quality bonds during the reporting period. From November 1st through December 31, 2009, as measured by the Barclays Capital U.S. Corporate Investment Grade Indexiii,

Western Asset Inflation Management Fund Inc. 2009 Annual Report |

Fund overview continued

higher-rated AA and A-rated bonds returned -0.17% and 0.22% respectively, while lower-rated BBB-rated bonds returned 1.53%.

Q. How did we respond to these changing market conditions?

A. There were a number of adjustments made to the portfolio during the reporting period. Given their price rally, we reduced our TIPS exposure and maintained a larger cash position as we sought compelling opportunities elsewhere.

During the reporting period, we utilized Treasury and Euro-bund futures to manage the Fund’s durationiv and yield curvev exposure. Interest rate swaps were utilized to manage our interest rate exposure at the long end of the yield curve. We also used index credit default swaps to manage the Fund’s exposure to the corporate market. Currency contracts were used to hedge our non-U.S. dollar security exposure. Overall, the use of these derivative instruments was slightly positive for performance.

Performance review

For the two-month period from November 1, 2009 through December 31, 2009, Western Asset Inflation Management Fund Inc. returned 0.62% based on its net asset value (“NAV”)vi and 1.62% based on its New York Stock Exchange (“NYSE”) market price per share. The Fund’s unmanaged benchmark, the Barclays Capital Global Real Index: U.S. TIPS, returned 0.53% for the same period. The Lipper Corporate Debt BBB-Rated Closed-End Funds Category Averagevii returned 1.43% over the same time frame. Please note that Lipper performance returns are based on each fund’s NAV.

During the two-month period, the Fund made distributions to shareholders totaling $0.10 per share. The performance table shows the Fund’s two-month total return based on its NAV and market price as of December 31, 2009. Past performance is no guarantee of future results.

PERFORMANCE SNAPSHOT as of December 31, 2009 (unaudited)

PRICE PER SHARE |

| 2-MONTH |

|

$17.69 (NAV) |

| 0.62% |

|

$16.15 (Market Price) |

| 1.62% |

|

All figures represent past performance and are not a guarantee of future results.

* Total returns are based on changes in NAV or market price, respectively. Total returns assume the reinvestment of all distributions in additional shares. Performance figures for periods shorter than one year represent cumulative figures and are not annualized. Results for longer periods may differ, in some cases, substantially.

2 | Western Asset Inflation Management Fund Inc. 2009 Annual Report |

Q. What were the leading contributors to performance?

A. The largest contributor to relative performance for the period was our out-of-benchmark exposure to the high-yield sector. Significant contributors to performance were Energy Future Holdings Corp., GMAC LLC and Ford Motor Credit Co. In each case, their spreads tightened during the period and they produced strong results. Our exposure to investment grade bonds was also rewarded. In particular, our Financials holdings boosted the Fund’s returns. Within the investment grade bond space, JPMorgan Chase & Co. and SLM Corp. were strong performers during the reporting period. Our exposure to structured mortgage obligations, namely collateralized mortgage obligations, was another meaningful contributor to performance. The asset class performed well given some improvements in the housing market.

Q. What were the leading detractors from performance?

A. The Fund’s cash position was the largest detractor from relative results during the reporting period given the extremely low yields available from short-term money market instruments. Also modestly detracting from performance was the Fund’s underweight to TIPS. While our exposure to TIPS represented approximately 85% of the portfolio, having an underweight hurt our relative results. Elsewhere, an exposure to agency preferred securities was a drag on performance. These higher-quality securities lagged as the low-quality rally continued during the last two months of 2009.

Looking for additional information?

The Fund is traded under the symbol “IMF” and its closing market price is available in most newspapers under the NYSE listings. The daily NAV is available on-line under the symbol “XIMFX” on most financial websites. Barron’s and The Wall Street Journal’s Monday edition both carry closed-end fund tables that provide additional information. In addition, the Fund issues a quarterly press release that can be found on most major financial websites, as well as www.leggmason.com/cef.

In a continuing effort to provide information concerning the Fund, shareholders may call 1-888-777-0102 (toll free), Monday through Friday from 8:00 a.m. to 5:30 p.m. Eastern Standard Time, for the Fund’s current NAV, market price and other information.

Thank you for your investment in Western Asset Inflation Management Fund Inc. As always, we appreciate that you have chosen us to manage your assets and we remain focused on achieving the Fund’s investment goals.

Sincerely,

Western Asset Management Company

January 19, 2010

Western Asset Inflation Management Fund Inc. 2009 Annual Report |

Fund overview continued

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

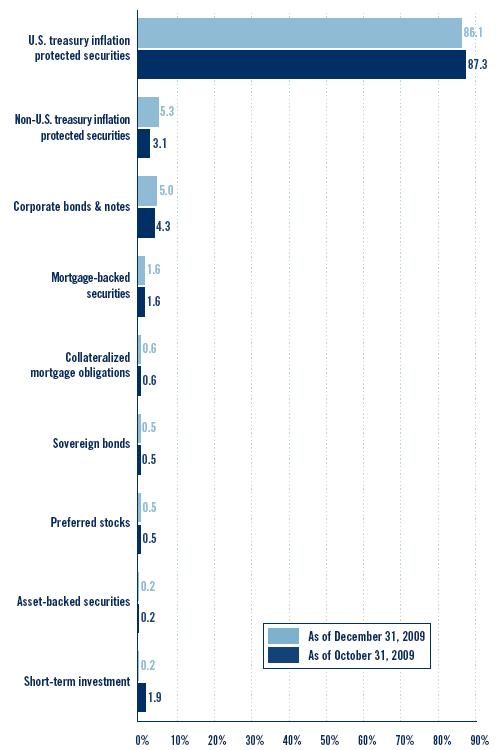

Portfolio holdings and breakdowns are as of December 31, 2009 and are subject to change and may not be representative of the portfolio managers’ current or future investments. Please refer to pages 6 through 10 for a list and percentage breakdown of the Fund’s holdings.

The mention of sector breakdowns is for informational purposes only and should not be construed as a recommendation to purchase or sell any securities. The information provided regarding such sectors is not a sufficient basis upon which to make an investment decision. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies discussed should consult their financial professional. The Fund’s top five sector holdings (as a percentage of total investments) as of December 31, 2009 were: U.S. Treasury Inflation Protected Securities (86.1%), Non-U.S. Treasury Inflation Protected Securities (5.3%), Corporate Bonds & Notes (5.0%), Mortgage-Backed Securities (1.6%) and Collateralized Mortgage Obligations (0.6%). The Fund’s portfolio composition is subject to change at any time.

RISKS: The Fund may use derivatives, such as options and futures, which can be illiquid, may disproportionately increase losses, and have a potentially large impact on Fund performance. If interest rates rise, but the rate of inflation does not, the Fund’s performance will be adversely affected. The Fund is subject to the risks associated with inflation-protected securities (“IPS”). Risks associated with IPS investments include liquidity risk, interest rate risk, prepayment risk, extension risk and deflation risk. Income distributions of the Fund are likely to fluctuate more than those of a conventional bond fund. As interest rates rise, bond prices fall, reducing the value of the Fund’s holdings. The Fund is not diversified, which means that it is permitted to invest a higher percentage of its assets in any one issuer than a diversified fund. This may magnify the Fund’s losses from events affecting a particular issuer. Foreign securities are subject to certain risks of overseas investing, including currency fluctuations and changes in political and economic conditions. High-yield bonds involve greater credit and liquidity risks than investment grade bonds. Leverage may result in greater volatility of NAV and the market price of common shares and increases a shareholder’s risk of loss. There is no assurance that the Fund’s leveraging strategy will be successful.

All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

i | U.S. Treasury Inflation-Protected Securities (“TIPS”) are inflation-indexed securities issued by the U.S. Treasury in five-year, ten-year and twenty-year maturities. The principal is adjusted to the Consumer Price Index, the commonly used measure of inflation. The coupon rate is constant, but generates a different amount of interest when multiplied by the inflation-adjusted principal. |

ii | The Barclays Capital Global Real Index: U.S. TIPS represents an unmanaged market index made up of U.S. Treasury Inflation-Linked Index securities. |

iii | The Barclays Capital U.S. Corporate Investment Grade Index is an unmanaged index consisting of publicly issued U.S. corporate and specified foreign debentures and secured notes that are rated investment grade (Baa3/BBB- or higher) by at least two ratings agencies, have at least one year to final maturity and have at least $250 million par amount outstanding. To qualify, bonds must be SEC-registered. |

iv | Duration is the measure of the price sensitivity of a fixed-income security to an interest rate change of 100 basis points. Calculation is based on the weighted average of the present values for all cash flows. |

v | The yield curve is the graphical depiction of the relationship between the yield on bonds of the same credit quality but different maturities. |

vi | Net asset value (“NAV”) is calculated by subtracting total liabilities and outstanding preferred stock (if any) from the closing value of all securities held by the Fund (plus all other assets) and dividing the result (total net assets) by the total number of the common shares outstanding. The NAV fluctuates with changes in the market prices of securities in which the Fund has invested. However, the price at which an investor may buy or sell shares of the Fund is the Fund’s market price as determined by supply of and demand for the Fund’s shares. |

vii | Lipper, Inc., a wholly-owned subsidiary of Reuters, provides independent insight on global collective investments. Returns are based on the two-month period from November 1, 2009 through December 31, 2009, including the reinvestment of all distributions, including returns of capital, if any, calculated among the 22 funds in the Fund’s Lipper category. |

4 | Western Asset Inflation Management Fund Inc. 2009 Annual Report |

Fund at a glance† (unaudited)

INVESTMENT BREAKDOWN (%) As a percent of total investments

† | The bar graphs above represent the composition of the Fund’s investments as of December 31, 2009 and October 31, 2009 and do not include derivatives. The Fund is actively managed. As a result, the composition of the Fund’s investments is subject to change at any time. |

Western Asset Inflation Management Fund Inc. 2009 Annual Report. |

Schedule of investments

December 31, 2009

WESTERN ASSET INFLATION MANAGEMENT FUND INC.

FACE |

| SECURITY |

| VALUE |

| |

U.S. TREASURY INFLATION PROTECTED SECURITIES — 86.1% |

|

|

| |||

|

| U.S. Treasury Bonds, Inflation Indexed: |

|

|

| |

194,787 |

| 3.375% due 1/15/12 |

| $ | 208,574 |

|

12,251,233 |

| 3.000% due 7/15/12 |

| 13,187,301 |

| |

5,802,511 |

| 1.875% due 7/15/13 |

| 6,118,475 |

| |

13,629,837 |

| 2.375% due 1/15/25 |

| 14,415,679 |

| |

13,755,838 |

| 2.000% due 1/15/26 |

| 13,849,337 |

| |

4,003,617 |

| 1.750% due 1/15/28 |

| 3,849,101 |

| |

2,416,440 |

| 2.500% due 1/15/29 |

| 2,597,861 |

| |

4,444,565 |

| 3.875% due 4/15/29(a) |

| 5,733,142 |

| |

|

| U.S. Treasury Notes, Inflation Indexed: |

|

|

| |

2,929,652 |

| 2.375% due 4/15/11 |

| 3,019,830 |

| |

2,527,027 |

| 2.000% due 1/15/14 |

| 2,675,490 |

| |

9,362,550 |

| 1.625% due 1/15/15 |

| 9,748,755 |

| |

11,588,450 |

| 2.000% due 1/15/16 |

| 12,252,074 |

| |

2,494,055 |

| 2.500% due 7/15/16 |

| 2,719,104 |

| |

2,992,394 |

| 1.625% due 1/15/18 |

| 3,067,904 |

| |

9,523,370 |

| 1.375% due 7/15/18 |

| 9,557,597 |

| |

906,165 |

| 2.125% due 1/15/19 |

| 962,375 |

| |

2,531,050 |

| 1.875% due 7/15/19 |

| 2,631,105 |

| |

|

| TOTAL U.S. TREASURY INFLATION PROTECTED SECURITIES |

| 106,593,704 |

| |

ASSET-BACKED SECURITIES — 0.2% |

|

|

| |||

FINANCIALS — 0.2% |

|

|

| |||

|

| Home Equity — 0.2% |

|

|

| |

329,564 |

| Asset-Backed Funding Certificates, 2.406% due 1/25/34(b) |

| 131,167 |

| |

73,417 |

| Finance America Net Interest Margin Trust, 5.250% due 6/27/34(c)(d)(e)(g) |

| 35 |

| |

130,221 |

| GSAMP Trust, 1.381% due 11/25/34(b) |

| 11,720 |

| |

345,872 |

| Renaissance Home Equity Loan Trust, 2.131% due 3/25/34(b) |

| 121,579 |

| |

8,853 |

| SACO I Trust, 0.431% due 4/25/35(b)(c) |

| 3,585 |

| |

71,380 |

| Sail Net Interest Margin Notes, 5.500% due 3/27/34(c)(e)(g) |

| 0 |

| |

|

| TOTAL ASSET-BACKED SECURITIES |

| 268,086 |

| |

COLLATERALIZED MORTGAGE OBLIGATIONS — 0.6% |

|

|

| |||

95,928 |

| American Home Mortgage Investment Trust, 1.031% due 11/25/45(b) |

| 76 |

| |

3,299,792 |

| Federal National Mortgage Association (FNMA), STRIPS, IO, 5.500% due 7/1/18(e)(f) |

| 407,640 |

| |

197,547 |

| Merit Securities Corp., 1.731% due 9/28/32(b)(c) |

| 160,994 |

| |

See Notes to Financial Statements.

|

| Western Asset Inflation Management Fund Inc. 2009 Annual Report |

WESTERN ASSET INFLATION MANAGEMENT FUND INC.

FACE |

| SECURITY |

| VALUE |

| |

|

| Structured Asset Securities Corp.: |

|

|

| |

50,315 |

| 1.331% due 2/25/28(b) |

| $ | 43,048 |

|

179,738 |

| 1.231% due 3/25/28(b) |

| 157,004 |

| |

|

| TOTAL COLLATERALIZED MORTGAGE OBLIGATIONS |

| 768,762 |

| |

CORPORATE BONDS & NOTES — 5.0% |

|

|

| |||

ENERGY — 0.0% |

|

|

| |||

|

| Oil, Gas & Consumable Fuels — 0.0% |

|

|

| |

29,000 |

| Pemex Project Funding Master Trust, Senior Bonds, 6.625% due 6/15/35 |

| 27,649 |

| |

FINANCIALS — 4.5% |

|

|

| |||

|

| Capital Markets — 0.0% |

|

|

| |

1,050,000 |

| Kaupthing Bank HF, Subordinated Notes, 7.125% due 5/19/16(c)(e)(g) |

| 2,730 |

| |

|

| Commercial Banks — 0.1% |

|

|

| |

550,000 |

| Glitnir Banki HF, Subordinated Notes, 6.693% due 6/15/16(c)(e)(g) |

| 1,430 |

| |

160,000 |

| RSHB Capital, Loan Participation Notes, Senior Secured Bonds, 6.299% due 5/15/17(c) |

| 161,920 |

| |

|

| Total Commercial Banks |

| 163,350 |

| |

|

| Consumer Finance — 3.4% |

|

|

| |

1,500,000 |

| Ford Motor Credit Co., Senior Notes, 1.854% due 1/15/10(b) |

| 1,501,875 |

| |

|

| GMAC LLC: |

|

|

| |

921,000 |

| 2.456% due 12/1/14(b)(c) |

| 742,556 |

| |

92,000 |

| Senior Notes, 7.500% due 12/31/13(c) |

| 89,700 |

| |

111,000 |

| Subordinated Notes, 8.000% due 12/31/18(c) |

| 98,790 |

| |

|

| SLM Corp., Medium-Term Notes: |

|

|

| |

1,000,000 |

| 1.097% due 2/1/10(b) |

| 1,002,110 |

| |

540,000 |

| 5.375% due 1/15/13 |

| 509,744 |

| |

270,000 |

| 5.375% due 5/15/14 |

| 249,275 |

| |

|

| Total Consumer Finance |

| 4,194,050 |

| |

|

| Diversified Financial Services — 1.0% |

|

|

| |

430,000 |

| Citigroup Inc., Senior Notes, 6.010% due 1/15/15 |

| 439,544 |

| |

685,000 |

| JPMorgan Chase & Co., Junior Subordinated Notes, 7.900% due 4/30/18(b)(h) |

| 708,861 |

| |

100,000 |

| TNK-BP Finance SA, Senior Notes, 7.875% due 3/13/18(c) |

| 103,250 |

| |

|

| Total Diversified Financial Services |

| 1,251,655 |

| |

|

| TOTAL FINANCIALS |

| 5,611,785 |

| |

UTILITIES — 0.5% |

|

|

| |||

|

| Electric Utilities — 0.2% |

|

|

| |

250,000 |

| EEB International Ltd., Senior Bonds, 8.750% due 10/31/14(c) |

| 271,250 |

| |

See Notes to Financial Statements.

Western Asset Inflation Management Fund Inc. 2009 Annual Report |

|

|

Schedule of investments continued

December 31, 2009

WESTERN ASSET INFLATION MANAGEMENT FUND INC.

FACE |

| SECURITY |

| VALUE |

| |

|

| Independent Power Producers & Energy Traders — 0.3% |

|

|

| |

|

| Energy Future Holdings Corp., Senior Notes: |

|

|

| |

12,000 |

| 10.875% due 11/1/17 |

| $ | 9,870 |

|

391,013 |

| 11.250% due 11/1/17(i) |

| 278,597 |

| |

|

| Total Independent Power Producers & Energy Traders |

| 288,467 |

| |

|

| TOTAL UTILITIES |

| 559,717 |

| |

|

| TOTAL CORPORATE BONDS & NOTES |

| 6,199,151 |

| |

MORTGAGE-BACKED SECURITIES — 1.6% |

|

|

| |||

FHLMC — 1.3% |

|

|

| |||

|

| Federal Home Loan Mortgage Corp. (FHLMC), Gold: |

|

|

| |

69,595 |

| 7.000% due 6/1/17(f) |

| 73,606 |

| |

1,407,423 |

| 8.500% due 9/1/24(f) |

| 1,594,820 |

| |

|

| TOTAL FHLMC |

| 1,668,426 |

| |

FNMA — 0.3% |

|

|

| |||

|

| Federal National Mortgage Association (FNMA): |

|

|

| |

38,772 |

| 5.500% due 1/1/14(f) |

| 41,340 |

| |

291,231 |

| 7.000% due 10/1/18-6/1/32(f) |

| 324,112 |

| |

|

| TOTAL FNMA |

| 365,452 |

| |

|

| TOTAL MORTGAGE-BACKED SECURITIES |

| 2,033,878 |

| |

NON-U.S. TREASURY INFLATION PROTECTED SECURITIES — 5.3% |

|

|

| |||

|

| Australia — 3.0% |

|

|

| |

2,650,000 | AUD | Australia Government, Bonds, 4.000% due 8/20/20 |

| 3,689,159 |

| |

|

| Canada — 2.3% |

|

|

| |

2,234,758 | CAD | Government of Canada, Bonds, 4.250% due 12/1/21 |

| 2,819,126 |

| |

|

| TOTAL NON-U.S. TREASURY INFLATION PROTECTED SECURITIES |

| 6,508,285 |

| |

SOVEREIGN BONDS — 0.5% |

|

|

| |||

|

| Argentina — 0.2% |

|

|

| |

|

| Republic of Argentina: |

|

|

| |

75,000 | EUR | 9.750% due 11/26/03(g) |

| 42,469 |

| |

150,000 | EUR | 8.500% due 7/1/04(g) |

| 87,357 |

| |

100,000 | EUR | 10.250% due 1/26/07(g) |

| 61,105 |

| |

225,000 | EUR | Medium-Term Notes, 9.000% due 5/24/05(c)(g) |

| 132,245 |

| |

|

| Total Argentina |

| 323,176 |

| |

|

| Mexico — 0.3% |

|

|

| |

306,000 |

| United Mexican States, Medium-Term Notes, 6.750% due 9/27/34 |

| 324,360 |

| |

|

| Russia — 0.0% |

|

|

| |

556 |

| Russian Federation, 8.250% due 3/31/10(c) |

| 567 |

| |

|

| TOTAL SOVEREIGN BONDS |

| 648,103 |

| |

See Notes to Financial Statements.

|

| Western Asset Inflation Management Fund Inc. 2009 Annual Report |

WESTERN ASSET INFLATION MANAGEMENT FUND INC.

SHARES |

| SECURITY |

| VALUE |

| ||

PREFERRED STOCKS — 0.5% |

|

|

| ||||

CONSUMER DISCRETIONARY — 0.0% |

|

|

| ||||

|

| Automobiles — 0.0% |

|

|

| ||

300 |

| Ford Motor Co., Series F, 7.550% |

| $ | 5,499 |

| |

FINANCIALS — 0.5% |

|

|

| ||||

|

| Consumer Finance — 0.1% |

|

|

| ||

230 |

| GMAC Inc., 7.000%(c)* |

| 151,613 |

| ||

|

| Diversified Financial Services — 0.2% |

|

|

| ||

1,000 |

| Preferred Plus, Trust, Series FRD-1, 7.400% |

| 18,500 |

| ||

6,800 |

| Saturns, Series F 2003-5, 8.125% |

| 151,980 |

| ||

|

| Total Diversified Financial Services |

| 170,480 |

| ||

|

| Thrifts & Mortgage Finance — 0.2% |

|

|

| ||

109,225 |

| Federal Home Loan Mortgage Corp. (FHLMC), 8.375%(b)(f)* |

| 114,686 |

| ||

98,300 |

| Federal National Mortgage Association (FNMA), 8.250%(b)(f)* |

| 108,130 |

| ||

|

| Total Thrifts & Mortgage Finance |

| 222,816 |

| ||

|

| TOTAL FINANCIALS |

| 544,909 |

| ||

|

| TOTAL PREFERRED STOCKS |

| 550,408 |

| ||

|

| TOTAL INVESTMENTS BEFORE SHORT-TERM INVESTMENT |

| 123,570,377 |

| ||

|

|

|

|

|

| ||

FACE |

|

|

|

|

| ||

SHORT-TERM INVESTMENT — 0.2% |

|

|

| ||||

|

| Repurchase Agreement — 0.2% |

|

|

| ||

| 273,000 |

| Morgan Stanley tri-party repurchase agreement dated 12/31/09, 0.005% due 1/4/10; Proceeds at maturity — $273,000; (Fully collateralized by U.S. government agency obligation, 0.900% due 4/8/10; Market value — $282,454) (Cost — $273,000) |

| 273,000 |

| |

|

| TOTAL INVESTMENTS — 100.0% |

| $ | 123,843,377 |

| |

See Notes to Financial Statements.

Western Asset Inflation Management Fund Inc. 2009 Annual Report |

|

|

Schedule of investments continued

December 31, 2009

WESTERN ASSET INFLATION MANAGEMENT FUND INC.

* | Non-income producing security. | |

† | Face amount denominated in U.S. dollars, unless otherwise noted. | |

(a) | All or a portion of this security is held at the broker as collateral for open futures contracts. | |

(b) | Variable rate security. Interest rate disclosed is that which is in effect at December 31, 2009. | |

(c) | Security is exempt from registration under Rule 144A of the Securities Act of 1933. This security may be resold in transactions that are exempt from registration, normally to qualified institutional buyers. This security has been deemed liquid pursuant to guidelines approved by the Board of Directors, unless otherwise noted. | |

(d) | Security is valued in good faith at fair value by or under the direction of the Board of Directors (See Note 1). | |

(e) | Illiquid security. | |

(f) | On September 7, 2008, the Federal Housing Finance Agency placed Fannie Mae (FNMA) and Freddie Mac (FHLMC) into conservatorship. | |

(g) | The coupon payment on these securities is currently in default as of December 31, 2009. | |

(h) | Security has no maturity date. The date shown represents the next call date. | |

(i) | Payment-in-kind security for which part of the income earned may be paid as additional principal. | |

# | Aggregate cost for federal income tax purposes is $124,144,435. | |

|

| |

Abbreviations used in this schedule: | ||

AUD | – Australian Dollar | |

CAD | – Canadian Dollar | |

EUR | – Euro | |

GMAC | – General Motors Acceptance Corp. | |

GSAMP | – Goldman Sachs Alternative Mortgage Products | |

IO | – Interest Only | |

STRIPS | – Separate Trading of Registered Interest and Principal Securities | |

See Notes to Financial Statements.

|

| Western Asset Inflation Management Fund Inc. 2009 Annual Report |

Statement of assets and liabilities

December 31, 2009

ASSETS: |

|

|

|

Investments, at value (Cost — $123,559,736) |

| $123,843,377 |

|

Foreign currency, at value (Cost — $74,939) |

| 78,535 |

|

Cash |

| 10,181 |

|

Interest receivable |

| 1,061,091 |

|

Deposits with brokers for open futures contracts |

| 82,147 |

|

Receivable for open forward currency contracts |

| 50,430 |

|

Prepaid expenses |

| 5,408 |

|

Total Assets |

| 125,131,169 |

|

LIABILITIES: |

|

|

|

Investment management fee payable |

| 63,965 |

|

Payable for open forward currency contracts |

| 26,184 |

|

Payable to broker — variation margin on open futures contracts |

| 24,367 |

|

Directors’ fees payable |

| 4,535 |

|

Accrued expenses |

| 120,890 |

|

Total Liabilities |

| 239,941 |

|

TOTAL NET ASSETS |

| $124,891,228 |

|

NET ASSETS: |

|

|

|

Par value ($0.001 par value; 7,061,160 shares issued and outstanding; 100,000,000 shares authorized) |

| $ 7,061 |

|

Paid-in capital in excess of par value |

| 137,774,165 |

|

Undistributed net investment income |

| 24,771 |

|

Accumulated net realized loss on investments, futures contracts, swap contracts and foreign currency transactions |

| (13,170,559 | ) |

Net unrealized appreciation on investments, futures contracts and foreign currencies |

| 255,790 |

|

TOTAL NET ASSETS |

| $124,891,228 |

|

Shares Outstanding |

| 7,061,160 |

|

Net Asset Value |

| $17.69 |

|

See Notes to Financial Statements.

Statements of operations

FOR THE PERIOD ENDED DECEMBER 31, 2009 |

| 2009† |

| 2009 |

|

INVESTMENT INCOME: |

|

|

|

|

|

Interest |

| $ 646,394 |

| $ 2,291,971 |

|

Dividends |

| 283 |

| 104,686 |

|

Total Investment Income |

| 646,677 |

| 2,396,657 |

|

EXPENSES: |

|

|

|

|

|

Investment management fee (Note 2) |

| 127,789 |

| 863,078 |

|

Audit and tax |

| 30,900 |

| 63,855 |

|

Shareholder reports |

| 20,000 |

| 72,941 |

|

Excise tax (Note 1) |

| 10,000 |

| 12,389 |

|

Directors’ fees |

| 9,969 |

| 33,449 |

|

Legal fees |

| 9,350 |

| 58,886 |

|

Transfer agent fees |

| 4,500 |

| 19,103 |

|

Stock exchange listing fees |

| 3,957 |

| 20,320 |

|

Insurance |

| 934 |

| 4,361 |

|

Custody fees |

| 600 |

| 1,743 |

|

Interest expense (Note 3) |

| 521 |

| 111,046 |

|

Miscellaneous expenses |

| 690 |

| 6,124 |

|

Total Expenses |

| 219,210 |

| 1,267,295 |

|

Less: Compensating balance credits (Note 1) |

| — |

| (124 | ) |

Net Expenses |

| 219,210 |

| 1,267,171 |

|

NET INVESTMENT INCOME |

| 427,467 |

| 1,129,486 |

|

REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS, |

|

|

|

|

|

FUTURES CONTRACTS, WRITTEN OPTIONS, SWAP CONTRACTS AND |

|

|

|

|

|

FOREIGN CURRENCY TRANSACTIONS (NOTES 1, 3 AND 4): |

|

|

|

|

|

Net Realized Gain (Loss) From: |

|

|

|

|

|

Investment transactions |

| 14,756 |

| (2,178,788 | ) |

Futures contracts |

| 78,698 |

| (893,191 | ) |

Written options |

| — |

| 171,961 |

|

Swap contracts |

| 642,386 |

| 2,708 |

|

Foreign currency transactions |

| (139,675 | ) | 263,666 |

|

Net Realized Gain (Loss) |

| 596,165 |

| (2,633,644 | ) |

Change in Net Unrealized Appreciation/Depreciation From: |

|

|

|

|

|

Investments |

| 302,931 |

| 23,202,356 |

|

Futures contracts |

| (75,400 | ) | 19,716 |

|

Written options |

| — |

| (2,781 | ) |

Swap contracts |

| (563,504 | ) | 944,943 |

|

Foreign currencies |

| 96,338 |

| (428,175 | ) |

Change in Net Unrealized Appreciation/Depreciation |

| (239,635 | ) | 23,736,059 |

|

Net Gain on Investments, Futures Contracts, Written Options, Swap Contracts and Foreign Currency Transactions |

| 356,530 |

| 21,102,415 |

|

INCREASE IN NET ASSETS FROM OPERATIONS |

| $ 783,997 |

| $22,231,901 |

|

† For the period November 1, 2009 through December 31, 2009.

See Notes to Financial Statements.

|

| Western Asset Inflation Management Fund Inc. 2009 Annual Report |

Statements of changes in net assets

FOR THE PERIOD ENDED DECEMBER 31, 2009 |

| 2009† |

| 2009 |

| 2008 |

|

OPERATIONS: |

|

|

|

|

|

|

|

Net investment income |

| $ 427,467 |

| $ 1,129,486 |

| $ 9,801,229 |

|

Net realized gain (loss) |

| 596,165 |

| (2,633,644 | ) | 2,656,108 |

|

Change in net unrealized appreciation/depreciation |

| (239,635 | ) | 23,736,059 |

| (26,246,351 | ) |

Increase (Decrease) in Net Assets From Operations |

| 783,997 |

| 22,231,901 |

| (13,789,014 | ) |

DISTRIBUTIONS TO SHAREHOLDERS FROM (NOTE 1): |

|

|

|

|

|

|

|

Net investment income |

| (706,116 | ) | (5,366,481 | ) | (6,169,419 | ) |

Decrease in Net Assets From Distributions to Shareholders |

| (706,116 | ) | (5,366,481 | ) | (6,169,419 | ) |

FUND SHARE TRANSACTIONS: |

|

|

|

|

|

|

|

Cost of tendered shares (0, 0 and 762,841 tendered shares, respectively) (Note 6) |

| — |

| — |

| (14,096,519 | ) |

Decrease in Net Assets From Fund Share Transactions |

| — |

| — |

| (14,096,519 | ) |

INCREASE (DECREASE) IN NET ASSETS |

| 77,881 |

| 16,865,420 |

| (34,054,952 | ) |

NET ASSETS: |

|

|

|

|

|

|

|

Beginning of period |

| 124,813,347 |

| 107,947,927 |

| 142,002,879 |

|

End of period* |

| $124,891,228 |

| $124,813,347 |

| $107,947,927 |

|

* Includes undistributed net investment income of: |

| $24,771 |

| $325,978 |

| $3,845,289 |

|

† For the period November 1, 2009 through December 31, 2009.

See Notes to Financial Statements.

Statement of cash flows

For the Period Ended December 31, 2009†

CASH FLOWS PROVIDED (USED) BY OPERATING ACTIVITIES: |

|

|

| |

Interest and dividends received |

| $ | 231,927 |

|

Operating expenses paid |

| (209,888 | ) | |

Interest paid |

| (1,391 | ) | |

Net sales and maturities of short-term investments |

| 2,289,000 |

| |

Realized gain on futures contracts |

| 78,698 |

| |

Realized gain on swap contracts |

| 642,386 |

| |

Realized loss on foreign currency transactions |

| (139,675 | ) | |

Net change in unrealized depreciation on futures contracts |

| (75,400 | ) | |

Net change in unrealized appreciation on foreign currencies |

| 96,338 |

| |

Purchases of long-term investments |

| (3,171,356 | ) | |

Proceeds from disposition of long-term investments |

| 11,541,704 |

| |

Change in cash deposits with brokers for futures contracts |

| (33,884 | ) | |

Change in premium for swap contracts |

| (817,218 | ) | |

Change in payable to broker — variation margin |

| 48,440 |

| |

Change in receivable/payable for open forward currency contracts |

| (99,652 | ) | |

Change in payable on swap contracts |

| (13,960 | ) | |

Net Cash Provided by Operating Activities |

| 10,366,069 |

| |

CASH FLOWS USED BY FINANCING ACTIVITIES: |

|

|

| |

Cash distributions paid on Common Stock |

| (706,116 | ) | |

Cash paid on reverse repurchase agreements |

| (9,651,600 | ) | |

Net Cash Used by Financing Activities |

| (10,357,716 | ) | |

NET INCREASE IN CASH |

| 8,353 |

| |

Cash, beginning of year |

| 80,363 |

| |

Cash, end of year |

| $ | 88,716 |

|

RECONCILIATION OF INCREASE IN NET ASSETS FROM OPERATIONS TO NET CASH FLOWS PROVIDED (USED) BY OPERATING ACTIVITIES: |

|

|

| |

Increase in Net Assets From Operations |

| $ | 783,997 |

|

Accretion of discount on investments |

| (230,719 | ) | |

Amortization of premium on investments |

| 91,574 |

| |

Decrease in investments, at value |

| 10,905,165 |

| |

Increase in interest and dividends receivable |

| (275,605 | ) | |

Decrease in premium for written swaps |

| (817,218 | ) | |

Decrease in swap contracts payable |

| (13,960 | ) | |

Decrease in payable for open forward currency contracts |

| (99,652 | ) | |

Increase in payable to broker — variation margin |

| 48,440 |

| |

Increase in deposits with brokers for futures contracts |

| (33,884 | ) | |

Decrease in prepaid expenses |

| 4,891 |

| |

Decrease in interest payable |

| (870 | ) | |

Increase in accrued expenses |

| 3,910 |

| |

Total Adjustments |

| 9,582,072 |

| |

NET CASH FLOWS PROVIDED BY OPERATING ACTIVITIES |

| $ | 10,366,069 |

|

† For the period November 1, 2009 through December 31, 2009.

See Notes to Financial Statements.

|

| Western Asset Inflation Management Fund Inc. 2009 Annual Report |

Statement of cash flows

For the Year Ended October 31, 2009

CASH FLOWS PROVIDED (USED) BY OPERATING ACTIVITIES: |

|

|

| |

Interest and dividends received |

| $ | 3,545,932 |

|

Operating expenses paid |

| (1,261,617 | ) | |

Interest paid |

| (112,371 | ) | |

Net purchases of short-term investments |

| (722,000 | ) | |

Realized loss on futures contracts |

| (893,191 | ) | |

Realized gain on options |

| 171,961 |

| |

Realized gain on swap contracts |

| 2,708 |

| |

Realized gain on foreign currency transactions |

| 263,666 |

| |

Net change in unrealized appreciation on futures contracts |

| 19,716 |

| |

Net change in unrealized depreciation on foreign currencies |

| (428,175 | ) | |

Purchases of long-term investments |

| (82,641,443 | ) | |

Proceeds from disposition of long-term investments |

| 100,002,407 |

| |

Cash deposits with brokers for futures contracts |

| (48,263 | ) | |

Change in premium for swap contracts |

| (760,390 | ) | |

Change in receivable from broker — variation margin |

| 134,844 |

| |

Change in receivable/payable for open forward currency contracts |

| 435,076 |

| |

Change in payable on swap contracts |

| (10,116 | ) | |

Net Cash Provided by Operating Activities |

| 17,698,744 |

| |

CASH FLOWS USED BY FINANCING ACTIVITIES: |

|

|

| |

Cash distributions paid on Common Stock |

| (5,366,481 | ) | |

Cash paid on reverse repurchase agreements |

| (12,252,708 | ) | |

Net Cash Used by Financing Activities |

| (17,619,189 | ) | |

NET INCREASE IN CASH |

| 79,555 |

| |

Cash, beginning of year |

| 808 |

| |

Cash, end of year |

| $ | 80,363 |

|

RECONCILIATION OF INCREASE IN NET ASSETS FROM OPERATIONS TO NET CASH FLOWS PROVIDED (USED) BY OPERATING ACTIVITIES: |

|

|

| |

Increase in Net Assets From Operations |

| $ | 22,231,901 |

|

Accretion of discount on investments |

| 624,742 |

| |

Amortization of premium on investments |

| 483,216 |

| |

Increase in investments, at value |

| (419,374 | ) | |

Decrease in payable for securities purchased |

| (6,412,266 | ) | |

Decrease in interest and dividends receivable |

| 41,317 |

| |

Decrease in premium for written options |

| (15,906 | ) | |

Increase in premium for written swaps |

| 760,390 |

| |

Decrease in swap contracts payable |

| (10,116 | ) | |

Increase in deposits with brokers for futures contracts |

| (48,263 | ) | |

Increase in payable for open forward currency contracts |

| 435,076 |

| |

Increase in payable to broker — variation margin |

| 134,844 |

| |

Increase in prepaid expenses |

| (682 | ) | |

Decrease in interest payable |

| (1,325 | ) | |

Decrease in accrued expenses |

| (104,810 | ) | |

Total Adjustments |

| (4,533,157 | ) | |

NET CASH FLOWS PROVIDED BY OPERATING ACTIVITIES |

| $ | 17,698,744 |

|

See Notes to Financial Statements.

Western Asset Inflation Management Fund Inc. 2009 Annual Report |

|

|

Financial highlights

FOR A SHARE OF CAPITAL STOCK OUTSTANDING THROUGHOUT EACH YEAR ENDED DECEMBER 31, UNLESS OTHERWISE NOTED:

|

| 20091,2 |

| 20092,3 |

| 20082,3 |

| 20072,3 |

| 20062,3 |

| 20052,3 |

|

NET ASSET VALUE, BEGINNING OF PERIOD |

| $17.68 |

| $15.29 |

| $18.15 |

| $17.89 |

| $19.22 |

| $19.74 |

|

INCOME (LOSS) FROM OPERATIONS: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Net investment income |

| 0.06 |

| 0.16 |

| 1.32 |

| 0.66 |

| 0.86 |

| 1.00 |

|

Net realized and unrealized gain (loss) |

| 0.05 |

| 2.99 |

| (3.39 | ) | 0.28 |

| (0.55 | ) | (0.34 | ) |

Total income (loss) from operations |

| 0.11 |

| 3.15 |

| (2.07 | ) | 0.94 |

| 0.31 |

| 0.66 |

|

LESS DISTRIBUTIONS FROM: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Net investment income |

| (0.10 | ) | (0.76 | ) | (0.83 | ) | (0.72 | ) | (1.26 | ) | (1.18 | ) |

Net realized gains |

| — |

| — |

| — |

| — |

| (0.38 | ) | — |

|

Return of capital |

| — |

| — |

| — |

| — |

| (0.04 | ) | — |

|

Total distributions |

| (0.10 | ) | (0.76 | ) | (0.83 | ) | (0.72 | ) | (1.68 | ) | (1.18 | ) |

Increase in Net Asset Value due to shares repurchased in tender offer |

| — |

| — |

| 0.04 |

| 0.04 |

| 0.04 |

| — |

|

NET ASSET VALUE,END OF PERIOD |

| $17.69 |

| $17.68 |

| $15.29 |

| $18.15 |

| $17.89 |

| $19.22 |

|

MARKET PRICE, END OF PERIOD |

| $16.15 |

| $15.99 |

| $13.49 |

| $16.16 |

| $15.87 |

| $17.02 |

|

Total return, based on NAV 4,5 |

| 0.62 | % | 21.09 | % | (11.87 | )% | 5.65 | % | 1.98 | % | 3.42 | % |

Total return, based on Market Price 5 |

| 1.62 | % | 24.67 | % | (12.15 | )% | 6.51 | % | 2.96 | % | (2.32 | )% |

NET ASSETS, END OF PERIOD (000s) |

| $124,891 |

| $124,813 |

| $107,948 |

| $142,003 |

| $155,075 |

| $185,105 |

|

RATIOS TO AVERAGE NET ASSETS: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross expenses |

| 1.04 | %6 | 1.09 | % | 1.40 | % | 1.45 | %7 | 3.64 | % | 2.42 | % |

Gross expenses, excluding interest expense |

| 1.04 | 6 | 0.99 |

| 1.03 |

| 0.95 | 7 | 1.17 |

| 1.04 |

|

Net expenses |

| 1.04 | 6 | 1.09 | 8 | 1.40 | 8 | 1.45 | 7,9 | 3.64 | 9 | 2.42 |

|

Net expenses, excluding interest expense |

| 1.04 | 6 | 0.99 | 8 | 1.03 | 8 | 0.94 | 7,9 | 1.17 | 9 | 1.04 |

|

Net investment income |

| 2.03 | 6 | 0.97 |

| 7.16 |

| 3.69 |

| 4.75 |

| 5.10 |

|

PORTFOLIO TURNOVER RATE |

| 2 | % | 45 | %10 | 70 | %10 | 39 | %10 | 33 | % | 42 | % |

1 | For the period October 31, 2009 through December 31, 2009. |

2 | Per share amounts have been calculated using the average shares method. |

3 | For the year ended October 31. |

4 | Performance figures may reflect fee waivers and/or expense reimbursements. In the absence of fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. Total returns for periods of less than one year are not annualized. |

5 | The total return calculation assumes that distributions are reinvested in accordance with the Fund’s dividend reinvestment plan. Past performance is no guarantee of future results. Total returns for periods of less than one year are not annualized. |

6 | Annualized. |

7 | Included in the expense ratios are certain non-recurring restructuring (and reorganization, if applicable) fees that were incurred by the Fund during the period. Without these fees, the gross and net expense ratios including and excluding interest expense would not have changed. |

8 | The impact to the expense ratio was less than 0.01% as a result of compensating balance agreements. |

9 | Reflects fee waivers and/or expense reimbursements. |

10 | Excluding mortgage dollar roll transactions. If mortgage dollar roll transactions had been included, the portfolio turnover rate would have been 55%, 122% and 55% for the years ended October 31, 2009, 2008 and 2007, respectively. |

See Notes to Financial Statements.

|

| Western Asset Inflation Management Fund Inc. 2009 Annual Report |

Notes to financial statements

1. Organization and significant accounting policies

Western Asset Inflation Management Fund Inc. (the “Fund”) was incorporated in Maryland on March 16, 2004 and is registered as a non-diversified, closed-end management investment company under the Investment Company Act of 1940, as amended (the “1940 Act”). The Board of Directors authorized 100 million shares of $0.001 par value common stock. The Fund’s primary investment objective is total return. Current income is a secondary objective.

The following are significant accounting policies consistently followed by the Fund and are in conformity with U.S. generally accepted accounting principles (“GAAP”). Estimates and assumptions are required to be made regarding assets, liabilities and changes in net assets resulting from operations when financial statements are prepared. Changes in the economic environment, financial markets and any other parameters used in determining these estimates could cause actual results to differ. Subsequent events have been evaluated through February 23, 2010, the issuance date of the financial statements.

(a) Investment valuation. Debt securities are valued at the mean between the last quoted bid and asked prices provided by an independent pricing service that are based on transactions in debt obligations, quotations from bond dealers, market transactions in comparable securities and various other relationships between securities. Publicly traded foreign government debt securities are typically traded internationally in the over-the-counter market, and are valued at the mean between the last quoted bid and asked prices as of the close of business of that market. Equity securities for which market quotations are available are valued at the last reported sales price or official closing price on the primary market or exchange on which they trade. Futures contracts are valued daily at the settlement price established by the board of trade or exchange on which they are traded. When prices are not readily available, or are determined not to reflect fair value, such as when the value of a security has been significantly affected by events after the close of the exchange or market on which the security is principally traded, but before the Fund calculates its net asset value, the Fund values these securities at fair value as determined in accordance with the procedures approved by the Fund’s Board of Directors. Short-term obligations with maturities of 60 days or less are valued at amortized cost, which approximates fair value.

The Fund has adopted Financial Accounting Standards Board Codification Topic 820 (“ASC Topic 820”). ASC Topic 820 establishes a single definition of fair value, creates a three-tier hierarchy as a framework for measuring fair value based on inputs used to value the Fund’s investments, and requires additional disclosure about fair value. The hierarchy of inputs is summarized below.

· Level 1 — quoted prices in active markets for identical investments

· Level 2 — other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.)

Western Asset Inflation Management Fund Inc. 2009 Annual Report |

|

Notes to financial statements continued

· Level 3 — significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments)

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The Fund uses valuation techniques to measure fair value that are consistent with the market approach and/or income approach, depending on the type of the security and the particular circumstance. The market approach uses prices and other relevant information generated by market transactions involving identical or comparable securities. The income approach uses valuation techniques to convert future amounts to a single present amount.

The following is a summary of the inputs used in valuing the Fund’s assets carried at fair value:

DESCRIPTION |

| QUOTED PRICES |

| OTHER |

| SIGNIFICANT |

| TOTAL |

| |||

Long-term investments†: |

|

|

|

|

|

|

|

|

|

|

|

|

U.S. treasury inflation protected securities |

| — |

|

| $106,593,704 |

|

| — |

| $106,593,704 |

|

|

Asset-backed securities |

| — |

|

| 268,051 |

|

| $35 |

| 268,086 |

|

|

Collateralized mortgage obligations |

| — |

|

| 768,762 |

|

| — |

| 768,762 |

|

|

Corporate bonds & notes |

| — |

|

| 6,199,151 |

|

| — |

| 6,199,151 |

|

|

Mortgage-backed securities |

| — |

|

| 2,033,878 |

|

| — |

| 2,033,878 |

|

|

Non-U.S. treasury inflation protected securities |

| — |

|

| 6,508,285 |

|

| — |

| 6,508,285 |

|

|

Sovereign bonds |

| — |

|

| 648,103 |

|

| — |

| 648,103 |

|

|

Preferred stocks: |

|

|

|

|

|

|

|

|

|

|

|

|

Consumer discretionary |

| $ 5,499 |

|

| — |

|

| — |

| 5,499 |

|

|

Financials |

| 393,296 |

|

| 151,613 |

|

| — |

| 544,909 |

|

|

Total long-term investments |

| $398,795 |

|

| $123,171,547 |

|

| $35 |

| $123,570,377 |

|

|

Short-term investments† |

| — |

|

| 273,000 |

|

| — |

| 273,000 |

|

|

Total investments |

| $398,795 |

|

| $123,444,547 |

|

| $35 |

| $123,843,377 |

|

|

Other financial instruments: |

|

|

|

|

|

|

|

|

|

|

|

|

Futures contracts |

| (55,684 | ) |

| — |

|

| — |

| (55,684 | ) |

|

Forward foreign currency contracts |

| — |

|

| 24,246 |

|

| — |

| 24,246 |

|

|

Total other financial instruments |

| $ (55,684 | ) |

| $ 24,246 |

|

| — |

| $ (31,438 | ) |

|

Total |

| $343,111 |

|

| $123,468,793 |

|

| $35 |

| $123,811,939 |

|

|

† See Schedule of Investments for additional detailed categorizations.

|

| Western Asset Inflation Management Fund Inc. 2009 Annual Report |

Following is a reconciliation of investments in which significant unobservable inputs (Level 3) were used in determining fair value:

INVESTMENTS IN SECURITIES |

| ASSET-BACKED |

| TOTAL |

|

Balance as of October 31, 2009 |

| — |

| — |

|

Accrued premiums/discounts |

| — |

| — |

|

Realized gain/(loss) |

| — |

| — |

|

Change in unrealized appreciation (depreciation) |

| — |

| — |

|

Net purchases (sales) |

| — |

| — |

|

Net transfers in and/or out of Level 3 |

| $35 |

| $35 |

|

Balance as of December 31, 2009 |

| $35 |

| $35 |

|

Change in unrealized appreciation (depreciation) for investments in securities still held at December 31, 20091 |

| $ 0 |

| $ 0 |

|

1 | This amount is included in the change in net unrealized appreciation (depreciation) in the accompanying Statement of Operations. Change in unrealized appreciation (depreciation) includes net unrealized appreciation (depreciation) resulting from changes in investment values during the reporting period and the reversal of previously recorded unrealized appreciation (depreciation) when gains or losses are realized. |

(b) Repurchase agreements. The Fund may enter into repurchase agreements with institutions that its investment adviser has determined are creditworthy. Each repurchase agreement is recorded at cost. Under the terms of a typical repurchase agreement, a fund takes possession of an underlying debt obligation subject to an obligation of the seller to repurchase, and of the fund to resell, the obligation at an agreed-upon price and time, thereby determining the yield during a fund’s holding period. When entering into repurchase agreements, it is the Fund’s policy that its custodian or a third party custodian, acting on the Fund’s behalf, take possession of the underlying collateral securities, the market value of which, at all times, at least equals the principal amount of the repurchase transaction, including accrued interest. To the extent that any repurchase transaction maturity exceeds one business day, the value of the collateral is marked to market and measured against the value of the agreement to ensure the adequacy of the collateral. If the counterparty defaults, the Fund generally has the right to use the collateral to satisfy the terms of the repurchase transaction. However, if the market value of the collateral declines during the period in which the Fund seeks to assert its rights or if bankruptcy proceedings are commenced with respect to the seller of the security, realization of the collateral by the Fund may be delayed or limited.

(c) Reverse repurchase agreements. The Fund may enter into reverse repurchase agreements. Under the terms of a typical reverse repurchase agreement, a Fund sells a security subject to an obligation to repurchase the security from the buyer at an agreed-upon time and price. In the event the buyer of securities under a reverse repurchase agreement files for bankruptcy or becomes insolvent, the fund’s use of the proceeds of the agreement may be restricted pending a determination by the counterparty, or its trustee or

Western Asset Inflation Management Fund Inc. 2009 Annual Report |

|

Notes to financial statements continued

receiver, whether to enforce the Fund’s obligation to repurchase the securities. In entering into reverse repurchase agreements, the Fund will maintain cash, U.S. government securities or other liquid debt obligations at least equal in value to its obligations with respect to reverse repurchase agreements or will take other actions permitted by law to cover its obligations.

(d) Futures contracts. The Fund may use futures contracts to gain exposure to, or hedge against, changes in the value of interest rates or foreign currencies. A futures contract represents a commitment for the future purchase or sale of an asset at a specified price on a specified date.

Upon entering into a futures contract, the Fund is required to deposit cash or cash equivalents with a broker in an amount equal to a certain percentage of the contract amount. This is known as the “initial margin” and subsequent payments (“variation margin”) are made or received by the Fund each day, depending on the daily fluctuation in the value of the contract. For certain futures, including foreign denominated futures, variation margin is not settled daily, but is recorded as a net variation margin payable or receivable. Futures contracts are valued daily at the settlement price established by the board of trade or exchange on which they are traded. The daily changes in contract value are recorded as unrealized gains or losses in the Statement of Operations and the Fund recognizes a realized gain or loss when the contract is closed.

Futures contracts involve, to varying degrees, risk of loss in excess of the amounts reflected in the financial statements. In addition, there is the risk that the Fund may not be able to enter into a closing transaction because of an illiquid secondary market.

(e) Written options. When the Fund writes an option, an amount equal to the premium received by the Fund is recorded as a liability, the value of which is marked to market daily to reflect the current market value of the option written. If the option expires, the premium received is recorded as a realized gain. When a written call option is exercised, the difference between the premium received plus the option exercise price and the Fund’s basis in the underlying security (in the case of a covered written call option), or the cost to purchase the underlying security (in the case of an uncovered written call option), including brokerage commission, is recognized as a realized gain or loss. When a written put option is exercised, the amount of the premium received is subtracted from the cost of the security purchased by the Fund from the exercise of the written put option to form the Fund’s basis in the underlying security purchased. The writer or buyer of an option traded on an exchange can liquidate the position before the exercise of the option by entering into a closing transaction. The cost of a closing transaction is deducted from the original premium received resulting in a realized gain or loss to the Fund.

The risk in writing a covered call option is that the Fund may forego the opportunity of profit if the market price of the underlying security increases and the option is exercised. The risk in writing a put option is that the Fund may incur a loss if the market price of the underlying security decreases and the

|

| Western Asset Inflation Management Fund Inc. 2009 Annual Report |

option is exercised. The risk in writing a call option is that the Fund is exposed to the risk of loss if the market price of the underlying security increases. In addition, there is the risk that the Fund may not be able to enter into a closing transaction because of an illiquid secondary market.

(f) Mortgage dollar rolls. The Fund may enter into mortgage dollar rolls in which the Fund sells mortgage-backed securities for delivery in the current month, realizing a gain or loss, and simultaneously contracts to repurchase substantially similar (same type, coupon and maturity) securities to settle on a specified future date.

The Fund executes its mortgage dollar rolls entirely in the to-be-announced (“TBA”) market, whereby the Fund makes a forward commitment to purchase a security and, instead of accepting delivery, the position is offset by a sale of the security with a simultaneous agreement to repurchase at a future date. The Fund accounts for mortgage dollar rolls as purchases and sales.

The risk of entering into mortgage dollar rolls is that the market value of the securities the Fund is obligated to repurchase under the agreement may decline below the repurchase price. In the event the buyer of securities under a mortgage dollar roll files for bankruptcy or becomes insolvent, the Fund’s use of the proceeds of the mortgage dollar roll may be restricted pending a determination by the counterparty, or its trustee or receiver, whether to enforce the Fund��s obligation to repurchase the securities.

(g) Securities traded on a to-be-announced basis. The Fund may trade securities on a TBA basis. In a TBA transaction, the Fund commits to purchasing or selling securities which have not yet been issued by the issuer and for which specific information, such as the face amount, maturity date and underlying pool of investments in U.S. government agency mortgage pass-through securities, is not announced. Securities purchased on a TBA basis are not settled until they are delivered to the Fund. Beginning on the date the Fund enters into a TBA transaction, cash, U.S. government securities or other liquid high-grade debt obligations are segregated in an amount equal in value to the purchase price of the TBA security. These securities are subject to market fluctuations and their current value is determined in the same manner as for other securities.

(h) Stripped securities. The Fund may invest in “Stripped Securities,” a term used collectively for components, or strips, of fixed income securities. Stripped securities can be principal only securities (“PO”), which are debt obligations that have been stripped of unmatured interest coupons or, interest only securities (“IO”), which are unmatured interest coupons that have been stripped from debt obligations. The market value of Stripped Securities will fluctuate in response to changes in economic conditions, rates of pre-payment, interest rates and the market’s perception of the securities. However, fluctuations in response to interest rates may be greater in Stripped Securities than for debt obligations of comparable maturities that pay interest currently. The amount of fluctuation may increase with a longer period of maturity.

Western Asset Inflation Management Fund Inc. 2009 Annual Report |

|

|

Notes to financial statements continued

The yield to maturity on IO’s is sensitive to the rate of principal repayments (including prepayments) on the related underlying debt obligation and principal payments may have a material effect on yield to maturity. If the underlying debt obligation experiences greater than anticipated prepayments of principal, the Fund may not fully recoup its initial investment in IO’s.

(i) Forward foreign currency contracts. The Fund may enter into a forward foreign currency contract to hedge against foreign currency exchange rate risk on its non-U.S. dollar denominated securities or to facilitate settlement of a foreign currency denominated portfolio transaction. A forward foreign currency contract is an agreement between two parties to buy and sell a currency at a set price with delivery and settlement at a future date. The contract is marked to market daily and the change in value is recorded by the Fund as an unrealized gain or loss. When a forward foreign currency contract is closed, through either delivery or offset by entering into another forward foreign currency contract, the Fund recognizes a realized gain or loss equal to the difference between the value of the contract at the time it was opened and the value of the contract at the time it is closed.

Forward foreign currency contracts involve elements of market risk in excess of the amounts reflected on the Statement of Assets and Liabilities. The Fund bears the risk of an unfavorable change in the foreign exchange rate underlying the forward foreign currency contract. Risks may also arise upon entering into these contracts from the potential inability of the counterparties to meet the terms of their contracts.

(j) Swap agreements. The Fund may invest in swaps for the purpose of managing its exposure to interest rate, credit or market risk, or for other purposes. The use of swaps involves risks that are different from those associated with ordinary portfolio transactions.

Swap contracts are marked to market daily and changes in value are recorded as unrealized appreciation/(depreciation). Gains or losses are realized upon termination of the swap agreement. Periodic payments and premiums received or made by the Fund are recognized in the Statement of Operations as realized gains or losses, respectively. Collateral, in the form of restricted cash or securities, may be required to be held in segregated accounts with the Fund’s custodian in compliance with the terms of the swap contracts. Securities held as collateral for swap contracts are identified in the Schedule of Investments and restricted cash, if any, is identified on the Statement of Assets and Liabilities. Risks may exceed amounts recorded in the Statement of Assets and Liabilities. These risks include changes in the returns of the underlying instruments, failure of the counterparties to perform under the contracts’ terms, and the possible lack of liquidity with respect to the swap agreements.

Payments received or made at the beginning of the measurement period are reflected as a premium or deposit, respectively, on the Statement of Assets and Liabilities. These upfront payments are amortized over the life of the swap and

|

| Western Asset Inflation Management Fund Inc. 2009 Annual Report |

are recognized as realized gain or loss in the Statement of Operations. A liquidation payment received or made at the termination of the swap is recognized as realized gain or loss in the Statement of Operations. Net periodic payments received or paid by the Fund are recognized as realized gain or loss at the time of receipt or payment in the Statement of Operations.

Credit default swaps. The Fund may enter into credit default swap (“CDS”) contracts for investment purposes, to manage its credit risk or to add leverage. CDS agreements involve one party making a stream of payments to another party in exchange for the right to receive a specified return in the event of a default by a third party, typically corporate or sovereign issuers, on a specified obligation, or in the event of a write-down, principal shortfall, interest shortfall or default of all or part of the referenced entities comprising a credit index. The Fund may use a CDS to provide protection against defaults of the issuers (i.e., to reduce risk where the Fund has exposure to a sovereign issuer) or to take an active long or short position with respect to the likelihood of a particular issuer’s default. As a seller of protection, the Fund generally receives an upfront payment or a stream of payments throughout the term of the swap provided that there is no credit event. If the Fund is a seller of protection and a credit event occurs, as defined under the terms of that particular swap agreement, the maximum potential amount of future payments (undiscounted) that the Fund could be required to make under a credit default swap agreement would be an amount equal to the notional amount of the agreement. These amounts of potential payments will be partially offset by any recovery of values from the respective referenced obligations. As a seller of protection, the Fund effectively adds leverage to its portfolio because, in addition to its total net assets, the Fund is subject to investment exposure on the notional amount of the swap. As a buyer of protection, the Fund generally receives an amount up to the notional value of the swap if a credit event occurs.

Implied spreads are the theoretical prices a lender receives for credit default protection. When spreads rise, market perceived credit risk rises and when spreads fall, market perceived credit risk falls. The implied credit spread of a particular referenced entity reflects the cost of buying/selling protection and may include upfront payments required to enter into the agreement. Wider credit spreads and decreasing market values, when compared to the notional amount of the swap, represent a deterioration of the referenced entity’s credit soundness and a greater likelihood or risk of default or other credit event occurring as defined under the terms of the agreement. Credit spreads utilized in determining the period end market value of credit default swap agreements on corporate or sovereign issues are disclosed in the Notes to Financial Statements and serve as an indicator of the current status of the payment/performance risk and represent the likelihood or risk of default for credit derivatives. For credit default swap agreements on asset-backed securities and credit indices, the quoted market prices and resulting values, particularly in relation to the notional amount of the contract as well as the annual payment rate, serve as an indication of the current status of the payment/performance risk.

Western Asset Inflation Management Fund Inc. 2009 Annual Report |

|

|

Notes to financial statements continued

The Fund’s maximum risk of loss from counterparty risk, as the protection buyer, is the fair value of the contract (this risk is mitigated by the posting of collateral by the counterparty to the Fund to cover the Fund’s exposure to the counterparty). As the protection seller, the Fund’s maximum risk is the notional amount of the contract. Credit default swaps are considered to have credit risk-related contingent features since they require payment by the protection seller to the protection buyer upon the occurrence of a defined credit event.

Entering into a CDS agreement involves, to varying degrees, elements of credit, market and documentation risk in excess of the related amounts recognized on the Statement of Assets and Liabilities. Such risks involve the possibility that there will be no liquid market for these agreements, that the counterparty to the agreement may default on its obligation to perform or disagree as to the meaning of the contractual terms in the agreement, and that there will be unfavorable changes in net interest rates.

Interest rate swaps. The Fund may enter into interest rate swap contracts. Interest rate swaps are agreements between two parties to exchange cash flows based on a notional principal amount. The Fund may elect to pay a fixed rate and receive a floating rate, or, receive a fixed rate and pay a floating rate on a notional principal amount. The net interest received or paid on interest rate swap agreements is accrued daily as interest income. Interest rate swaps are marked to market daily based upon quotations from market makers and the change, if any, is recorded as an unrealized gain or loss in the Statement of Operations. When a swap contract is terminated early, the Fund records a realized gain or loss equal to the difference between the original cost and the settlement amount of the closing transaction.

The risks of interest rate swaps include changes in market conditions that will affect the value of the contract or changes in the present value of the future cash flow streams and the possible inability of the counterparty to fulfill its obligations under the agreement. The Fund’s maximum risk of loss from counterparty credit risk is the discounted net value of the cash flows to be received from the counterparty over the contract’s remaining life, to the extent that that amount is positive. This risk is mitigated by the posting of collateral by the counterparty to the Fund to cover the Fund’s exposure to the counterparty.

(k) Inflation-indexed bonds. Inflation-indexed bonds are fixed-income securities whose principal value or interest rate is periodically adjusted according to the rate of inflation. As the index measuring inflation changes, the principal value or interest rate of inflation-indexed bonds will be adjusted accordingly. Inflation adjustments to the principal amount of inflation-indexed bonds are reflected as an increase or decrease to investment income on the Statement of Operations. Repayment of the original bond principal upon maturity (as adjusted for inflation) is guaranteed in the case of U.S. Treasury inflation-indexed bonds. For bonds that do not provide a similar guarantee, the adjusted principal value of the bond repaid at maturity may be less than the original principal.

|

| Western Asset Inflation Management Fund Inc. 2009 Annual Report |

(l) Foreign currency translation. Investment securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollar amounts based upon prevailing exchange rates on the date of valuation. Purchases and sales of investment securities and income and expense items denominated in foreign currencies are translated into U.S. dollar amounts based upon prevailing exchange rates on the respective dates of such transactions.

The Fund does not isolate that portion of the results of operations resulting from fluctuations in foreign exchange rates on investments from the fluctuations arising from changes in market prices of securities held. Such fluctuations are included with the net realized and unrealized gain or loss on investments.