New York Menlo Park Washington DC São Paulo London | Paris Madrid Tokyo Beijing Hong Kong | |||||

| ||||||

| Marc O. Williams | ||||||

Davis Polk & Wardwell LLP 450 Lexington Avenue New York, NY 10017 | 212 450 6145 tel 212 701 5843 fax marc.williams@davispolk.com | |||||

| November 8, 2011 | ||

| Re: | Anadys Pharmaceuticals, Inc. |

| Schedule TO-T filed by Bryce Acquisition Corporation and |

| Hoffmann La-Roche, Inc. |

| File No. 005-79854 |

Melissa Campbell Duru

Securities and Exchange Commission

Special Counsel

Office of Mergers & Acquisitions

100 F Street, N.E.

Washington, D.C. 20549-3628

Dear Ms. Duru:

This letter responds to comments of the Staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”) contained in the letter from the Staff dated November 4, 2011 (the “Comment Letter”) regarding the above-referenced Schedule TO of Hoffmann La-Roche, Inc. (“Parent”) and Bryce Acquisition Corporation (“Purchaser”) filed on October 25, 2011 (the “Schedule TO”). In conjunction with this letter, Parent and Purchaser are filing via EDGAR, for review by the Staff, Amendment No. 1 to the Schedule TO (“Amendment No. 1”).

Please find enclosed three copies of Amendment No. 1. The changes reflected in Amendment No. 1 include those made in response to the comments of the Staff in the Comment Letter. Set forth below are responses to the Staff’s comments numbered 1 through 6, as set forth in the Comment Letter.

| 1. | You disclose that payment will occur on the later of (i) the expiration date or (ii) the satisfaction or waiver of the conditions set forth in the Offer to Purchase. Please confirm that payment will be made promptly in accordance with Rule 14e-1(c) by clarifying that all conditions other than those conditions dependent upon the receipt of necessary government approvals, must be satisfied or waived at or prior to the expiration of the tender offer. |

Parent and Purchaser have revised Item 1 in the Schedule TO in response to this comment by adding the following text after the last word in the first sentence under the heading “When and how will I be paid for my tendered shares?” on page 4 of the Offer to Purchase: “and only if all conditions, other than those conditions dependent upon the receipt of government approvals, have been satisfied or waived at or prior to the expiration of the tender offer.”

| Melissa Campbell Duru | 2 | November 8, 2011 |

| 2. | We note that you will determine, in your sole discretion, all questions as to the form and validity (including time of receipt) of and acceptance for payment of shares or with respect to notices of withdrawal. You disclose that your determination will be “final and binding.” Please delete this language, or disclose that only a court of competent jurisdiction can make a determination that will be final and binding upon the parties. In addition, please disclose that security holders may challenge your determinations. |

Parent and Purchaser have revised Item 4 in the Schedule TO in response to this comment by (i) deleting the following text from the first sentence under the heading “Determination of Validity” on page 14 of the Offer to Purchase: “, and our determination shall be final and binding”, and (ii) adding the following sentence after the second sentence under the heading “Determination of Validity on page 14 of the Offer to Purchase: “Tendering stockholders have the right to challenge our determination with respect to their Shares.”

| 3. | You disclose your right to waive the conditions “at any time and from time to time, in the sole discretion of the Parent and Purchaser…” Please revise to further clarify that offer conditions, other than those dependent upon the receipt of government approvals, may only be asserted as of expiration of the offer as opposed to “from time to time.” |

Parent and Purchaser have revised Item 4 in the Schedule TO in response to this comment by adding the following text after the second comma in the first paragraph above the heading “Material Adverse Effect” on page 37 of the Offer to Purchase: “on or prior to the Expiration Date (and thereafter in relation to any conditions dependent upon the receipt of government approvals)”.

| 4. | When a condition is triggered and you decide to proceed with the offer anyway, we believe that this decision constitutes a waiver of the triggered condition. Depending on the materiality of the waived condition and the number of days remaining in the offer, you may be required to extend the offer and re-circulate new disclosure to security holders. Please confirm your understanding in your response letter. |

Parent and Purchaser confirm supplementally to the Staff that Parent and Purchaser are aware that waiver of a condition, depending on the materiality of the waived condition and the number of days remaining in the offer, may require extension of the offer and circulation of new disclosure to securityholders.

| 5. | When an offer condition is triggered by events that occur during the offer period and before the expiration of the offer, the offerors should inform holders of securities how it intends to proceed promptly, rather than wait until the end of the offer period, unless the condition is one where satisfaction of the condition may be determined only upon expiration. Please confirm your understanding in your response letter. |

Parent and Purchaser respectfully acknowledge awareness of the Staff’s position in this regard without necessarily agreeing with that position.

| Melissa Campbell Duru | 3 | November 8, 2011 |

| 6. | Supplementally provide us with a copy of the complaints listed in this section. Refer to Item 1011(a) of Regulation M-A. |

Parent and Purchaser provide supplementally the attached three complaints to the Staff (and a consolidated complaint). Parent and Purchaser have also revised Item 11 of the Schedule TO to include disclosure about the additional complaints, which were filed after the date of the Schedule TO.

***

Parent and Purchaser acknowledge that (1) Parent and Purchaser are responsible for the adequacy and accuracy of the disclosure in their filings, (2) Staff comments or changes to disclosure in response to Staff comments do not foreclose the Commission from taking any action with respect to the filing and (3) neither Parent nor Purchaser may assert Staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States.

We are grateful for your assistance in this matter. Please do not hesitate to call me at (212) 450-6145 with any questions you may have with respect to the foregoing.

| Very truly yours, |

/s/ Marc O. Williams

|

| Marc O. Williams |

1 |

| ROBBINS BRIAN J. ROBBINS UMEDA LLP (190264) |

2 |

| STEPHEN ARSHAN AMIRI J. ODDO (246874) (174828) |

3 |

| 600 EDWARD B Street, B. Suite GERARD 1900 (248053) |

4 |

| Telephone: San Diego, CA (619) 92101 525-3990 |

5 |

| Facsimile: (619) 525-3991 |

6 |

| Co-Lead and Liaison Counsel for Plaintiffs |

7 |

| [Additional counsel on signature page.] |

8 |

| SUPERIOR COURT OF THE STATE OF CALIFORNIA |

9 COUNTY OF SAN DIEGO

10 IN RE ANADYS PHARMACEUTICALS, ) Lead Case No. 37-2011-00099789-CU-BT-CTL

11 INC. SHAREHOLDER LITIGATION ) ) (Consolidated with Case No. 37-2011-

12 ) ) 00099895-CU-SL-CTL)

13 ) ) CLASS ACTION

14 ) ) UPON CONSOLIDATED SELF-DEALING COMPLAINT AND BREACH BASED OF

15 ) ) FIDUCIARY DUTY

16 ) ) 17 18 19 20 21 22 23 24 25 26 27 28

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

1 |

| SUMMARY OF THE ACTION |

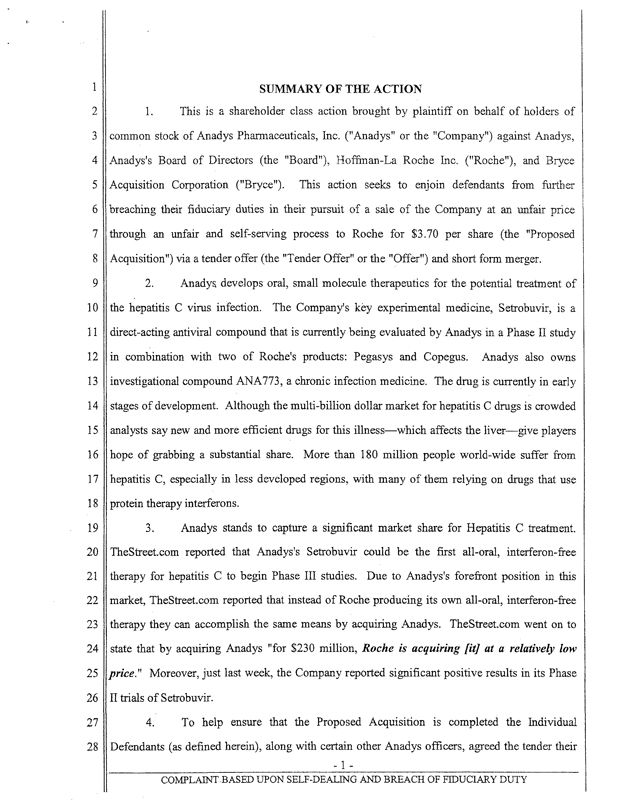

2 1. This is a consolidated shareholder class action brought by plaintiffs on behalf of 3 holders of common stock of Anadys Pharmaceuticals, Inc. (“Anadys” or the “Company”) against

4 |

| Anadys, Anadys’s Board of Directors (the “Board”), Hoffman-La Roche Inc. (“Roche”), and |

5 Bryce Acquisition Corporation (“Bryce”). This action seeks to enjoin defendants from further 6 breaching their fiduciary duties in their pursuit of a sale of the Company at an unfair price 7 through an unfair and self-serving process to Roche for $3.70 per share (the “Proposed

8 |

| Acquisition”) via a tender offer (the “Tender Offer” or the “Offer”) and short form merger. The |

9 Tender Offer commenced on October 25, 2011, and is set to expire on Tuesday, November 22,

10 2011.

11 2. Anadys develops oral, small molecule therapeutics for the potential treatment of 12 the hepatitis C virus infection. The Company’s key experimental medicine, setrobuvir, is a 13 direct-acting antiviral compound that is currently being evaluated by Anadys in a Phase IIb study 14 in combination with two of Roche’s products: Pegasys and Copegus. Anadys also owns 15 investigational compound ANA773, a chronic infection medicine. The drug is currently in the 16 early stages of development. Although the multi-billion dollar market for hepatitis C drugs is 17 crowded, analysts say new and more efficient drugs for this illness—which affects the liver—18 give players hope of grabbing a substantial share. More than 180 million people world-wide 19 suffer from hepatitis C, especially in less developed regions, with many of them relying on drugs 20 that use protein therapy interferons.

21 3. Anadys stands to capture a significant market share for Hepatitis C treatment.

22 TheStreet.com reported that Anadys’s setrobuvir could be the first all-oral, interferon-free 23 therapy for hepatitis C to begin Phase III studies. Due to Anadys’s forefront position in this 24 market, TheStreet.com reported that instead of Roche producing its own all-oral, interferon-free 25 therapy, they can accomplish the same means by acquiring Anadys. TheStreet.com went on to 26 state that by acquiring Anadys “for $230 million, Roche is acquiring [it] at a relatively low 27 price.” Moreover, the Company recently reported significant positive results in its Phase IIb 28 trials of setrobuvir.

- 1—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

1 |

| 4. To help ensure that the Proposed Acquisition is completed, the Individual |

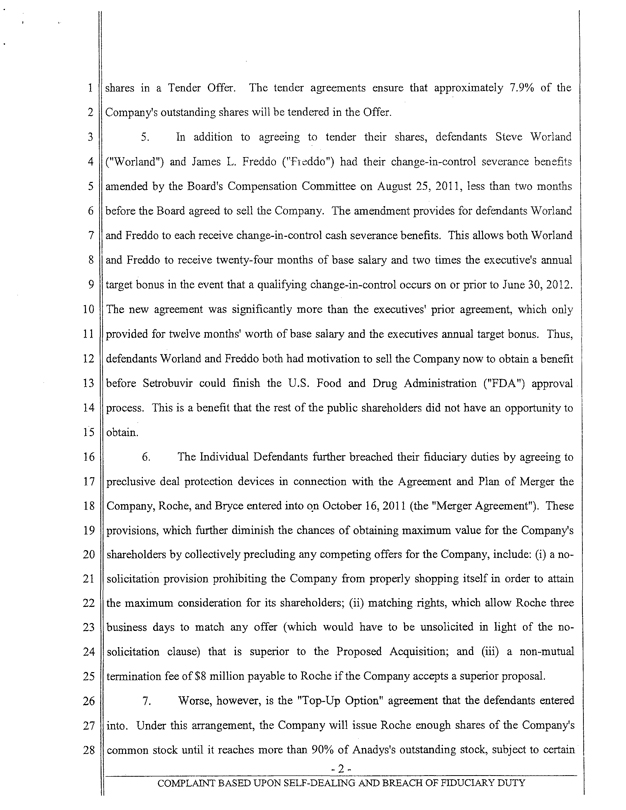

2 Defendants (as defined herein), along with certain other Anadys officers, agreed to tender their 3 shares in a Tender Offer. The tender agreements ensure that approximately 7.9% of the

4 |

| Company’s outstanding shares will be tendered in the Offer. |

5 |

| 5. In addition to agreeing to tender their shares, defendants Steve Worland |

6 (“Worland”) and James L. Freddo (“Freddo”) had their change-in-control severance benefits 7 amended by the Board’s Compensation Committee on August 25, 2011, less than two months 8 before the Board agreed to sell the Company. The amendment provides for defendants Worland 9 and Freddo to each receive change-in-control cash severance benefits consisting of twenty-four 10 months of base salary and two times the executive’s annual target bonus in the event that a 11 qualifying change-in-control occurs on or prior to June 30, 2012. The new agreement was 12 significantly more than the executives’ prior agreement, which only provided for twelve months’ 13 worth of base salary and the executives’ annual target bonus. Thus, defendants Worland and

14 Freddo both had motivation to sell the Company now to obtain a benefit before setrobuvir could 15 finish the U.S. Food and Drug Administration (“FDA”) approval process. This is a benefit that 16 the rest of the public shareholders did not have an opportunity to obtain.

17 6. The Individual Defendants further breached their fiduciary duties by agreeing to 18 preclusive deal protection devices in connection with the Agreement and Plan of Merger the

19 Company, Roche, and Bryce entered into on October 16, 2011 (the “Merger Agreement”). These 20 provisions, which further diminish the chances of obtaining maximum value for the Company’s 21 shareholders by collectively precluding any competing offers for the Company, include: (i) a no-22 solicitation provision prohibiting the Company from properly shopping itself in order to attain 23 the maximum consideration for its shareholders; (ii) matching rights, which allow Roche three 24 business days to match any offer (which would have to be unsolicited in light of the no-25 solicitation clause) that is superior to the Proposed Acquisition; and (iii) a non-mutual 26 termination fee of $8 million payable to Roche if the Company accepts a superior proposal.

27 7. Worse, however, is the “Top-Up Option” agreement that the defendants entered 28 into. Under this arrangement, even if Roche does not acquire via the Tender Offer the 90%

- 2—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

1 ownership needed to effectuate a short form merger and avoid a shareholder vote, the Company 2 has agreed to issue Roche enough shares of the Company’s common stock to allow it to reach 3 that 90% threshold.

4 |

| 8. On October 25, 2011, Anadys filed a Form SC 14D9 (“14D-9”) with the U.S. |

5 |

| Securities and Exchange Commission (“SEC”) and disseminated it to Anadys’s shareholders. |

6 The 14D-9, which recommends Anadys shareholders tender their shares in the Tender Offer, 7 omits and/or misrepresents material information, without which Anadys shareholders cannot 8 make a fully informed decision whether to tender their shares. The 14D-9 fails to inform the

9 Company’s shareholders why the Board pursued a sale of the Company at a time when it appears 10 the Company may be on the verge of becoming profitable. Defendants further fail to provide the

11 Company’s shareholders with material information and/or provides them with materially 12 misleading information concerning: (i) the process leading to the sale of the Company; (ii) the 13 financial analyses performed by Lazard Frères & Co. LLC (“Lazard”), the Company’s financial 14 advisor; and (iii) the Company’s financial projections. These material facts must be disclosed in 15 order for shareholders to have all material information and to understand the Company’s current 16 and projected future value in deciding whether to tender their shares in connection with the

17 Proposed Acquisition or to stay the course.

18 9. Because defendants dominate and control the business and corporate affairs of

19 Anadys, there exists an imbalance and disparity of economic power between them and the public 20 shareholders of Anadys. Therefore, it is inherently unfair for defendants to execute and pursue 21 any Proposed Acquisition agreement under which they will reap disproportionate benefits to the 22 exclusion of obtaining the maximum shareholder value. Nonetheless, instead of attempting to 23 negotiate a contract reflecting the best consideration reasonably available for Anadys’s 24 shareholders, who they are duty-bound to serve, defendants disloyally placed their own interests 25 and the interests of Roche first and tailored the terms and conditions of the Proposed Acquisition 26 to meet their own personal needs and objectives.

27 10. To remedy the Individual Defendants’ breaches of fiduciary duty and other 28 misconduct, plaintiffs seek, inter alia: (i) injunctive relief preventing consummation of the

- 3—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

1 Proposed Acquisition unless and until the Company adopts and implements a procedure or 2 process to obtain a transaction that provides the best possible terms for shareholders; (ii) a 3 directive to the Individual Defendants to exercise their fiduciary duties to obtain a transaction 4 which is in the best interests of Anadys shareholders; and (iii) rescission of, to the extent already 5 implemented, the Proposed Acquisition agreement or any of the terms thereof.

6 |

| JURISDICTION AND VENUE |

7 11. This Court has jurisdiction over the causes of action asserted herein pursuant to 8 the California Constitution, Article VI, §10, because this case is a cause not given by statute to 9 other trial courts.

10 12. This Court has jurisdiction over this action because certain of the defendants 11 conduct business in and/or have sufficient minimum contacts with California. Anadys is a 12 citizen of California as it has its principal place of business at 5871 Oberlin Drive, Suite 200, San

13 Diego, California.

14 13. Venue is proper in this Court because the conduct at issue took place and had an 15 effect in this County.

16 PARTIES

17 14. Plaintiff Fahd Hammad is a shareholder of Anadys.

18 15. Plaintiff Miguel Angel Alonso Maestro is a shareholder of Anadys.

19 16. Plaintiff Devorah Shabtal is a shareholder of Anadys.

20 17. Defendant Anadys is a Delaware corporation and biopharmaceutical company 21 focused on improving patient care by developing novel medicines for the treatment of hepatitis

22 C. Anadys’s most advanced drug candidate, setrobuvir (ANA598), is a direct-acting antiviral 23 compound for chronic hepatitis C that is currently being evaluated by the Company in a Phase II 24 study in combination with Roche’s PEGylated interferon (Pegasys) and ribavirin (Copegus).

25 Additionally, the Company is developing ANA773, an oral, small-molecule inducer of 26 endogenous interferons that act via a Toll like receptor 7, or TLR7, pathway in hepatitis C.

27 Upon completion of the Proposed Acquisition, Anadys will become a wholly owned subsidiary 28 of Roche.

- 4—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

1 18. Defendant Worland is President, Chief Executive Officer (“CEO”), and a director 2 of Anadys and has been since August 2007. Worland has also served in various other positions 3 since joining Anadys in 2001 including Chief Scientific Officer; Executive Vice President, Head 4 of Research and Development; Executive Vice President, Pharmaceuticals; and President,

5 Pharmaceuticals. In connection with the Proposed Acquisition, Worland agreed to tender his 6 shares and support the Proposed Acquisition.

7 |

| 19. Defendant Freddo is Chief Medical Officer of Anadys and has been since July |

8 2006; Senior Vice President, Drug Development and has been since July 2008; and a director 9 and has been since January 2011. In connection with the Proposed Acquisition, Freddo agreed to 10 tender his shares and support the Proposed Acquisition.

11 20. Defendant Stelios Papadopoulos (“Papadopoulos”) is Chairman of the Board of

12 Anadys and has been since January 2011 and a director and has been since May 2000.

13 Papadopoulos co-founded Anadys. In connection with the Proposed Acquisition, Papadopoulos 14 agreed to tender his shares and support the Proposed Acquisition.

15 21. Defendant Kleanthis G. Xanthopoulos (“Xanthopoulos”) is an Anadys director 16 and has been since May 2000. Xanthopoulos was also President and CEO of Anadys from May

17 2000 to November 2006. Xanthopoulos co-founded Anadys. In connection with the Proposed

18 Acquisition, Xanthopoulos agreed to tender his shares and support the Proposed Acquisition.

19 22. Defendant Marios Fotiadis (“Fotiadis”) is an Anadys director and has been since

20 September 2002. In connection with the Proposed Acquisition, Fotiadis agreed to tender his 21 shares and support the Proposed Acquisition.

22 23. Defendant Mark G. Foletta (“Foletta”) is an Anadys director and has been since

23 September 2005. In connection with the Proposed Acquisition, Foletta agreed to tender his 24 shares and support the Proposed Acquisition.

25 24. Defendant Barry A. Labinger (“Labinger”) is an Anadys director and has been 26 since March 2011. In connection with the Proposed Acquisition, Labinger agreed to tender his 27 shares and support the Proposed Acquisition.

28

- 5—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

1 |

| 25. Defendant Brian S. Posner (“Posner”) is an Anadys director and has been since |

2 August 2011. In connection with the Proposed Acquisition, Posner agreed to tender his shares 3 and support the Proposed Acquisition.

4 |

| 26. Defendant Roche is a New Jersey corporation and a U.S. subsidiary of F. |

5 Hoffmann-La Roche Ltd (“FHL Roche”), which is a leader in research-focused healthcare with 6 combined strengths in pharmaceuticals and diagnostics. FHL Roche is the world’s largest 7 biotech company with medicines in oncology, virology, inflammation, metabolism, and the 8 central nervous system. FHL Roche is also the world leader in in-vitro diagnostics, tissue-based 9 cancer diagnostics, and a pioneer in diabetes management. Roche’s principal executive offices 10 are located at 340 Kingsland Street, Nutley, New Jersey.

11 27. Defendant Bryce is a Delaware corporation and a wholly owned subsidiary of

12 Roche. Bryce was formed solely for the purpose of engaging in the transactions of the Proposed

13 Acquisition. In connection with the Proposed Acquisition, Bryce will commence a cash Tender

14 Offer to acquire all of the outstanding Anadys shares of common stock. Upon completion of the

15 Proposed Acquisition, Bryce will merge with and into Anadys and cease its separate existence.

16 28. The defendants named above in ¶¶18-25 are sometimes collectively referred to 17 herein as the “Individual Defendants.”

18 29. The true names and capacities of defendants sued herein under California Code of

19 Civil Procedure §474 as Does 1 through 25, inclusive, are presently not known to plaintiffs, who 20 therefore sues these defendants by such fictitious names. Plaintiffs will seek to amend this

21 Complaint and include these Doe defendants’ true names and capacities when they are 22 ascertained. Each of the fictitiously named defendants is responsible in some manner for the 23 conduct alleged herein and for the injuries suffered by the Class (as defined herein).

24 INDIVIDUAL DEFENDANTS’ FIDUCIARY DUTIES

25 30. Under Delaware law, the officers and directors of a publicly traded corporation 26 have fiduciary duties of loyalty, good faith, and care to shareholders. To diligently comply with 27 these duties, neither the officers nor the directors may take any action that:

28 (a) adversely affects the value provided to the corporation’s shareholders;

- 6—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

1 |

| (b) will discourage, inhibit, or deter alternative offers to purchase control of 2 the corporation or its assets; |

3 |

| (c) contractually prohibits themselves from complying with their fiduciary 4 duties; |

5 (d) will otherwise adversely affect their duty to secure the best value 6 reasonably available under the circumstances for the corporation’s shareholders; and/or

7 (e) will provide the officers and/or directors with preferential treatment at the 8 expense of, or separate from, the public shareholders.

9 31. In accordance with their duties of loyalty and good faith, the Individual

10 Defendants, as officers and/or directors of Anadys, are obligated under Delaware law to refrain 11 from:

12 (a) participating in any transaction where the officers or directors’ loyalties 13 are divided;

14 (b) participating in any transaction where the officers or directors receive, or 15 are entitled to receive, a personal financial benefit not equally shared by the public shareholders 16 of the corporation; and/or

17 (c) unjustly enriching themselves at the expense or to the detriment of the 18 public shareholders.

19 32. Defendants, separately and together, in connection with the Proposed Acquisition, 20 are knowingly or recklessly violating their fiduciary duties and/or aiding and abetting such 21 breaches, including the Individual Defendants’ duties of loyalty, good faith, and independence 22 owed to plaintiffs and other public shareholders of Anadys. Certain of the Individual Defendants 23 stand on both sides of the transaction, are engaging in self-dealing, and are obtaining for 24 themselves personal benefits, including personal financial benefits not shared equally by 25 plaintiffs or the Class. Certain Anadys executives are also retaining their prestigious and 26 lucrative positions and compensation at the post-Proposed Acquisition company. These 27 executives have managed to secure for themselves substantial employment at the expense of the 28 shareholders’ best interests. Accordingly, the Proposed Acquisition will benefit the Individual

- 7—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

1 |

| Defendants in significant ways not shared with Class members. As a result of the Individual |

2 Defendants’ self-dealing and divided loyalties, neither plaintiffs nor the Class will receive 3 adequate or fair value for their Anadys common stock in the Proposed Acquisition.

4 33. Because the Individual Defendants are knowingly or recklessly breaching their 5 duties of loyalty, good faith, and independence in connection with the Proposed Acquisition, the 6 burden of proving the inherent or entire fairness of the Proposed Acquisition, including all 7 aspects of its negotiation, structure, price, and terms, is placed upon defendants as a matter of 8 law.

9 BACKGROUND TO THE PROPOSED ACQUISITION

10 34. Anadys develops oral, small molecule therapeutics for the potential treatment of 11 the hepatitis C virus infection. The Company’s key experimental medicine, setrobuvir, is a 12 direct-acting antiviral compound that is currently being evaluated by Anadys in a Phase IIb study 13 in combination with two of Roche’s products: Pegasys and Copegus. Anadys also owns 14 investigational compound ANA773, a chronic infection medicine. The drug is currently in early 15 stages of development.

16 35. In 2011, the FDA granted Fast Track Status to setrobuvir for the treatment of 17 chronic hepatitis C. Setrobuvir has a well-characterized safety database in which more than 350 18 subjects have received the agent to date. This year, Anadys announced a cross-company clinical 19 trial agreement with a large, commercial-stage biopharmaceutical company to study setrobuvir in 20 combination with another direct-acting antiviral (“DAA”) in healthy volunteers.

21 36. On October 13, 2011, Anadys announced positive twelve-week data for setrobuvir 22 in its Phase IIb hepatitis C study, indicating Anadys’s progress in developing a successful 23 medical treatment for hepatitis C. Commenting on the Phase IIb study’s positive results, 24 defendant Worland said, “[w]e are pleased with today’s data, which we believe demonstrate a 25 compelling profile for setrobuvir in significantly more patients . The antiviral response in 26 patients who had failed prior treatment is a particularly encouraging benchmark of setrobuvir’s 27 potency and high barrier to resistance. Coupled with a favorable safety profile to date, we believe 28

- 8—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

1 |

| today’s data position setrobuvir as a very attractive agent to be included in future DAA 2 combination regimens.” |

3 37. However, despite the massive potential upside for setrobuvir, including the recent 4 announcement of impressive Phase IIb clinical data, the Company has been searching for an 5 acquisition partner since early 2010. Defendants provide no reasons for why they were looking 6 to sell the Company at that time or why they decided to sell the Company now.

7 38. In March 2010, the Company met with investment banking firms for the purpose 8 of engaging a financial advisor to explore potential strategic opportunities, including a sale of the

9 Company. The Company eventually retained Lazard as its financial advisor.

10 39. Throughout 2010 and into September 2011, Anadys held substantive discussions 11 with a number of interested parties, such as those referred to in the 14D-9 as Party A, Party B, 12 and Party C, regarding a potential sale of the Company. Defendants, however, favored Roche 13 throughout the process by, among other things, meeting with and updating Roche regularly 14 regarding the status of the Company’s clinical trials. Starting in July 2011, defendants also gave

15 Roche access to an electronic data room containing setrobuvir clinical data, which was not 16 provided to other parties.

17 40. On or about August 26, 2011, Roche submitted its initial offer to purchase

18 Anadys for the price of $3.00 per share. On or about September 2, 2010, the Board met and 19 determined that Roche’s initial offer “did not represent the full value of the Company” and 20 rejected the proposed price.

21 41. On October 4, 2011, Company representatives provided Roche with a first look at 22 the Company’s promising setrobuvir Phase IIb clinical study and the status of the Company’s 23 planned clinical trial of ANA773.

24 42. Two days later, on October 6, 2011, Roche sent the Company a revised offer of 25 $3.70 per share in cash. Although the revised proposal was $0.70 higher, it actually reflected a 26 lower premium to the closing price of the stock for the previous trading day than the initial offer 27 of $3.00.

28

- 9—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

1 43. On October 7, 2011, the Board met to discuss the revised offer and determined 2 that $3.70 still undervalued the Company, and authorized Lazard to present a counteroffer of

3 |

| $4.50. Lazard relayed the message to Roche but Roche stood firm on its $3.70 revised offer. |

4 |

| The Board made no further attempts to get a higher price once Roche responded that its final 5 offer was $3.70. |

6 44. While the 14D-9 purports that the Company was also speaking with other 7 potential suitors at or around this time in 2011, it does not disclose the nature of those 8 discussions.

9 45. On October 12, 2011, the Board met with senior management to consider Roche’s 10 offer. While the Board considered that the Company purportedly needed $850 million in capital 11 to fund clinical development of setrobuvir and ANA773, defendants provide no explanation of 12 that amount, such as how soon the Company needed it, the breakdown of how much was needed 13 for setrobuvir as opposed to ANA773, or how much cash was needed to just get setrobuvir 14 through Phase III. Moreover, the Company’s financial projections provided in the 14D-9 show 15 that, while the Company does not expect to be profitable for the next few years, it projects 16 revenue to be in the hundreds of millions by 2017 and to grow at a staggering rate thereafter. For 17 instance, the Company expects total revenue to be over a billion dollars by 2022. Despite these 18 bright future forecasts, the Board decided to sell the Company to Roche for $3.70.

19 46. On October 13, 2011, as previously alleged, Anadys released interim antiviral 20 response and safety data from its ongoing Phase IIb study of setrobuvir.

21 47. On October 16, 2011, the Board met and approved the Merger Agreement with

22 Roche for $3.70 per share in cash.

23 THE PROPOSED ACQUISITION

24 48. On October 17, 2011, Anadys and Roche jointly issued the following press 25 release announcing that the Individual Defendants had agreed to sell Anadys to Roche for $3.70 26 per Anadys share:

27 San Diego, October 17, 2011 — Anadys Pharmaceuticals, Inc. (NASDAQ: ANDS) today announced that it has entered into a definitive merger agreement to 28

- 10—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

be acquired by Roche (SIX: RO, ROG; OTCQX: RHHBY). Under the terms of 1 the merger agreement, Roche will commence an all cash tender offer for all 2 outstanding shares of common stock of Anadys at USD 3.70 per share.

3 |

| The USD 3.70 per share cash offer price represents a 256% premium over the closing price of USD 1.04 on October 14, 2011. |

4 |

|

Steve Worland, President and Chief Executive Officer of Anadys, said: “Since

5 Anadys’ formation, our focus has been on driving forward research and development that would make a real difference to the lives of patients, especially 6 those with hepatitis. With Roche’s considerable capabilities and experience in

7 HCV, we believe this acquisition provides the best chance of success for the new potential treatments to reach patients. I would like to thank all our contributors for 8 their dedicated efforts to advance the compounds to their current position.”

9 Jean-Jacques Garaud, Global Head of Roche Pharma Research and Early Development, said: “This acquisition augments Roche’s already strong HCV

10 portfolio. Our aim is to offer physicians and hepatitis patients a powerful 11 combination of therapies that bring us closer to a cure, even without the use of interferon. Anadys’ compounds provide additional modes of action that could lead 12 to interferon-free treatment regimens without viral resistance.”

13 Anadys’ Board of Directors determined that the merger agreement and the transactions contemplated thereby are advisable, fair to and in the best interests of

14 Anadys and its stockholders, and recommends that Anadys’ stockholders tender their shares and, if necessary, adopt the merger agreement.

15

16 Each of Anadys’ directors and executive officers has agreed to tender their shares in the offer.

17

The closing of the tender offer will be subject to the tender of a number of shares 18 that, together with the shares owned by Roche, represent a majority of the total number of outstanding shares (assuming the exercise of all vested and unvested 19 options and warrants having an exercise price per share less than the tender offer 20 price) and other customary conditions. In addition, the transaction is subject to the expiration or termination of the waiting period under the Hart-Scott- Rodino

21 Antitrust Improvements Act of 1976. The tender offer is expected to close within 22 the fourth quarter of 2011.

The terms and conditions of the tender offer will be described in the tender offer 23 documents, which will be filed with the U.S. Securities and Exchange Commission (“SEC”).

24

25 Lazard is acting as financial advisor to Anadys and Cooley LLP is serving as Anadys’ legal advisor.

26

About Anadys

27 Anadys Pharmaceuticals, Inc. is a biopharmaceutical company dedicated to 28 improving patient care by developing novel medicines for the treatment of

- 11—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

hepatitis C. The Company believes hepatitis C represents a large unmet medical 1 need in which meaningful improvements in treatment outcomes may be attainable 2 with the introduction of new medicines. Anadys is conducting a Phase IIb study of setrobuvir (ANA598), the Company’s DAA, added to current standard of care 3 for the treatment of hepatitis C. The Company is also developing ANA773, the Company’s oral, small-molecule inducer of endogenous interferons that acts via 4 the Toll like receptor 7, or TLR7, pathway in hepatitis C.

5 49. On October 19, 2011, Anadys filed a Form 8-K with the SEC, wherein it 6 disclosed the Merger Agreement. The announcement and filing reveal that the Proposed

7 Acquisition is the product of a flawed sales process and, unless the Offer price is increased, 8 would be consummated at an unfair price. The Merger Agreement also reveals that the

9 Individual Defendants agreed to numerous draconian deal protection devices designed to 10 preclude any competing bids for Anadys.

11 50. Under the Merger Agreement, Anadys is subject to a no-solicitation clause that 12 prohibits the Company from seeking a superior offer for its shareholders. Specifically, Section

13 5.3(a) of the Merger Agreement states:

14 During the Pre-Closing Period, the Company shall not directly or indirectly, and shall not authorize or permit any other Acquired Corporation or any

15 Representative of any of the Acquired Corporations directly or indirectly to, (i) solicit, initiate or knowingly take any action to facilitate or encourage the 16 submission or announcement of any Acquisition Proposal (including by granting any waiver under Section 203 of the DGCL), (ii) furnish any information 17 regarding, or afford access to the business, properties, assets, books or records (except as required by applicable Legal Requirements) of, any of the Acquired

18 Corporations to any Person in connection with or in response to a bona fide Acquisition Proposal or an inquiry or indication of interest that could reasonably 19 be expected to lead to an Acquisition Proposal, (iii) engage in discussions or negotiations with any Person with respect to any Acquisition Proposal or any 20 inquiry or indication of interest that could reasonably be expected to lead to an Acquisition Proposal, (iv) approve, endorse or recommend any Acquisition

21 Proposal, or (v) enter into any agreement in principle, letter of intent, term sheet, merger agreement, acquisition agreement, option agreement or similar document 22 or any Contract contemplating or otherwise relating to any Acquisition Transaction.

23

51. Though the Merger Agreement ostensibly has a “fiduciary out” provision that 24 allows the Company to negotiate with other bidders, this provision is actually illusory. In order 25 for Anadys to negotiate with any other suitors, the potential acquirer would first have to make an 26 unsolicited written offer. Because the Company is prohibited under the Merger Agreement from 27 providing any non-public information to, much less communicating with, a third-party regarding 28

- 12—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

1 |

| a superior proposal prior to its receipt of a superior offer, no other bidder will emerge to make 2 such an offer. |

3 52. Further discouraging superior offers, Roche is entitled to a matching rights period 4 of three business days under the Merger Agreement. Specifically, Section 1.2(b)(ii) of the

5 |

| Merger Agreement provides that the Company may not accept a competing bid unless: |

6 |

| (1) the Company’s Board of Directors determines in good faith, after consultation with the Company’s outside legal counsel, that the failure to make the Adverse |

7 Change Recommendation would be reasonably likely to constitute a breach of the fiduciary duties of the Board of Directors of the Company to the Company’s 8 stockholders under applicable Legal Requirements; (2) the Company shall have given Parent a Change of Recommendation Notice at least three business days 9 prior to making any Adverse Change Recommendation; (3) the Company shall have provided to Parent the most current version of the proposed agreement under 10 which such Acquisition Proposal is proposed to be consummated and the identity of the third party making the Acquisition Proposal and, after consultation with 11 outside legal counsel, the Company’s Board of Directors shall have determined, in good faith, that such Acquisition Proposal is a Superior Offer; (4) the Company

12 shall have given Parent the three business days after the Change of Recommendation Notice to propose revisions to the terms of this Agreement or 13 make another proposal and shall have negotiated in good faith with Parent with respect to such proposed revisions or other proposal, if any; and (5) after 14 considering the results of such negotiations and giving effect to the proposals made by Parent, if any, after consultation with outside legal counsel, the

15 Company’s Board of Directors shall have determined, in good faith, that such Acquisition Proposal is a Superior Offer and that the failure to make the Adverse

16 Change Recommendation would constitute a breach of fiduciary duties of the Board of Directors of the Company to the Company’s stockholders under 17 applicable Legal Requirements (it being understood and agreed that any amendment to the financial terms or other material terms of any such Acquisition

18 Proposal shall require a new written notification from the Company and a new three business day period under this Section 1.2(b)(ii)).

19 This provision sets further limitations on the Company’s ability to accept an

20 53.

21 unsolicited superior proposal should one present itself. According to the matching rights 22 provision, the Company must notify Roche of the bidder’s offer, and should the Board determine 23 that the unsolicited offer is superior, Roche is granted three business days to amend the terms of 24 the Merger Agreement to make a counter offer that only needs to be as favorable to the

25 Company’s shareholders as the unsolicited offer. Roche is able to match the unsolicited offer 26 because it is granted unfettered access to the unsolicited offer, in its entirety, eliminating any 27 leverage that the Company has in receiving the unsolicited offer. Accordingly, no rival bidder is 28

- 13—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

1 likely to emerge because the Merger Agreement unfairly assures that any “auction” will be 2 competitively skewed in favor of Roche.

3 |

| 54. Also, pursuant to Section 8.3(b) of the Merger Agreement, Anadys must pay |

4 Roche an $8 million termination fee if it accepts a superior proposal. This provision all but 5 ensures that no competing offer will be forthcoming. The termination fee is over 3.7% of the 6 total equity value of the Proposed Acquisition and equates to over $0.14 per Anadys share that 7 would be paid to Roche rather than the Company’s shareholders in the case that any competing 8 bidder does emerge. Notably, the Merger Agreement does not provide for any reciprocal 9 termination fee payable to Anadys.

10 55. Finally, the Individual Defendants are attempting to silence dissent among the

11 Company’s shareholders by granting Anadys a “Top-Up Option” in Section 1.4 of the Merger

12 Agreement. The Top-Up Option allows Roche, in the event that it falls short in the Tender Offer 13 of the 90% threshold needed to complete the Proposed Acquisition via a short-form merger, to 14 acquire all the unissued stock the Company is authorized to issue under its certificate of 15 incorporation until Roche acquires one share more than 90% of Anadys’s outstanding stock.

16 This will allow Roche to acquire Anadys without seeking shareholder approval of the Proposed

17 Acquisition.

18 56. These onerous and preclusive deal protection devices operate in conjunction to 19 ensure that no competing offers will emerge for the Company and that the unfair transaction is 20 consummated so that the Individual Defendants can secure their own personal benefits under the

21 Proposed Acquisition. Accordingly, the Individual Defendants’ efforts to put their own personal 22 interests before that of the Company’s shareholders have resulted in a proposed transaction 23 presented to Anadys shareholders at an untenable and inadequate Offer price.

24 THE PROPOSED ACQUISITION UNDERVALUES ANADYS

25 57. The Proposed Acquisition significantly undervalues the Company and its future 26 prospects. Anadys has demonstrated and has in fact projected that it is well-positioned for future 27 expansion and growth through its stellar products in development. The Company has begun 28 realizing the positive impact of its efforts to bring setrobuvir to market. Indeed, on October 13,

- 14—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

1 2011, the Company issued a press release titled “Anadys Announces Positive 12-Week Data for 2 setrobuvir in Phase 2B Hepatitis C Study.” The press release stated that setrobuvir had a

3 |

| “Strong Antiviral Response in Prior Partial Responders and Relapsers” and showed “Favorable |

4 |

| Safety Data with AE Profile Comparable to Control Group.” In the press release, defendant |

5 Worland stated that the data “demonstrate[s] a compelling profile for setrobuvir in significantly 6 more patients” and that the results were “particularly encouraging.” Nonetheless, with the

7 |

| Company’s blockbuster drug showing promising signs and progressing through the FDA |

8 approval process, the Board has agreed to sell Anadys to Roche now in exchange for the 9 inadequate proposed consideration.

10 58. Anadys stands to capture a significant market share for hepatitis C treatment.

11 TheStreet.com reported that Anadys’s setrobuvir could be the first all-oral, interferon-free 12 therapy for hepatitis C to begin Phase III studies. Due to Anadys’s lead position in this market,

13 TheStreet.com reported that instead of Roche producing its own all-oral, interferon-free therapy 14 they can accomplish the same means ��by acquiring or partnering Hep C drugs others consider to 15 be weak or non-competitive on their own. That description fits Anadys’ lead drug setrobuvir, 16 which for $230 million, Roche is acquiring at a relatively low price.” Moreover, the Company 17 recently reported significant positive results in its Phase IIb trials.

18 THE 14D-9 CONTAINS MATERIAL MISSTATEMENTS AND/OR OMISSIONS

19 59. The 14D-9, filed by the Company with the SEC on October 25, 2011, and 20 disseminated to Anadys shareholders, recommends that Anadys shareholders tender their shares 21 for the $3.70 in cash offered in the Proposed Acquisition. However, the 14D-9 misrepresents or 22 omits material information necessary for Anadys’s public shareholders to make an informed 23 decision regarding whether to tender their shares in connection with the Proposed Acquisition.

24 Specifically, defendants fail to provide the Company’s shareholders with material information 25 and/or provides them with materially misleading information concerning: (i) the process leading 26 to the sale of the Company; (ii) the financial analyses performed by Lazard, the Company’s 27 financial advisor; and (iii) the Company’s financial projections.

28

- 15—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

1 |

| Inadequate Disclosure Concerning the Process |

2 60. The 14D-9 fails to disclose the reasons why the Company decided to sell itself 3 now for cash, as opposed to remaining as a standalone and allowing shareholders to reap the 4 benefits of the Company’s products reaching the market.

5 61. The 14D-9 fails to disclose how the Board determined that the Company needed 6 $850 million in capital to fund the clinical development of setrobuvir and ANA773, and provides 7 no explanation of how soon the Company needs it, the breakdown of how much is needed for 8 setrobuvir as opposed to ANA773, or how much cash is needed just to get setrobuvir through

9 Phase III.

10 62. The 14D-9 fails to close the data supporting the indication that “future Hepatitis C

11 treatments would likely require a combination of direct acting optiviral drugs and that setrobuvir 12 would likely have greater commercial value if it were part of a portfolio of other direct acting 13 antiviral drugs.”

14 63. The reasons given by Party A, Party B, and Party C for not submitting proposals 15 to acquire the Company.

16 64. The rationale for the Board’s abandonment of its position that the Company was 17 worth at least $4.50 per share.

18 Inadequate Disclosure Concerning Lazard’s Financial Analysis

19 65. In Lazard’s Sum-of-the-Parts Net Present Value Analysis, the 14D-9 does not 20 disclose the inputs and assumptions used to calculate the discount rate range of 15.0%—19.0%.

21 The 14D-9 also does not disclose the separate implied present values of setrobuvir, the net 22 operating losses (“NOLs”), ANA773, and the projected net cash as of December 31, 2011.

23 66. In Lazard’s Selected Companies Analysis, the 14D-9 does not disclose the 24 summary statistics, calculated technology values, expected number of marketed products, and 25 calculated multiples for each of the selected companies.

26 67. In Lazard’s Selected Precedent Transactions Analysis, the 14D-9 does not 27 disclose the summary statistics and calculated technology values for each of the selected 28 transactions.

- 16—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

1 |

| 68. The 14D-9 does not disclose whether Lazard has performed any work for Roche 2 in the past two years. |

3 |

| Inadequate Disclosure Concerning the Company Financial Projections |

4 69. With respect to the Company’s financial projections, the 14D-9 does not disclose 5 for each of the years 2012 through 2030:

6 |

| (a) separate probability adjusted projected revenues for setrobuvir and |

7 |

| ANA773; |

8 |

| (b) separate annual probabilities used for setrobuvir and ANA773; |

9 (c) separate research and development costs for setrobuvir and ANA773;

10 (d) why the usage of NOLs assumed to be limited to $4.1million/year; and

11 (e) how much of the projected $850 million additional capital is for 12 development of setrobuvir as compared to ANA773.

13 70. The aforementioned disclosure deficiencies constitute material information 14 necessary for shareholders adequately assess the Proposed Acquisition.

15 71. Accordingly, plaintiffs seek injunctive and other equitable relief to prevent the 16 irreparable injury that Company shareholders will continue to suffer absent judicial intervention.

17 SELF-DEALING

18 72. By reason of their positions with Anadys, the Individual Defendants had access to 19 non-public information concerning the financial condition and prospects of the Company. Thus, 20 there exists an imbalance and disparity of knowledge and economic power between the

21 Individual Defendants and the public shareholders of Anadys. Therefore, it is inherently unfair 22 for the Individual Defendants to pursue any proposed acquisition agreement under which they 23 will reap disproportionate benefits to the exclusion of obtaining the best value for shareholders.

24 Instead, certain of the Individual Defendants disloyally placed their own interests first, and 25 tailored the terms and conditions of the Proposed Acquisition to meet their own personal needs 26 and objectives.

27 73. In particular, on August 26, 2011, Anadys filed a Form 8-K with the SEC

28 disclosing that on August 25, 2011, the Compensation Committee of the Board of Anadys

- 17—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

1 approved certain change in control severance benefits for its executive officers, including 2 defendants Papadopoulos, Worland, and Freddo. With respect to the Company’s executive 3 officers, these recently approved change in control severance benefits consist of a lump sum 4 payment of twelve months base salary and a full annual target bonus (or the amount of the last 5 annual bonus actually paid, if higher) less standard deductions and withholdings in the event of a 6 qualifying job loss during the period commencing six months prior to and ending twenty-four 7 months following a change in control. The foregoing benefits are in addition to the benefits 8 currently available under the Amended and Restated Severance and Change in Control

9 Agreement, effective as of August 25, 2011, provided to each of the Company’s executive 10 officers, bringing the total “double-trigger” change in control cash severance benefits payable to 11 each of the Company’s executive officers to twenty-four months of base salary and two times the 12 executive’s annual target bonus in the event that a qualifying change in control occurs on or prior 13 to June 30, 2012.

14 74. The foregoing golden parachute compensation, which was approved shortly 15 before these same executives approved the Merger Agreement and agreed to tender their shares 16 in the Tender Offer, is further evidence of the flawed process leading up to the Company’s entry 17 into to the Merger Agreement.

18 75. The Proposed Acquisition is wrongful, unfair, and harmful to Anadys’s public 19 stockholders, and represents an effort by defendants to aggrandize their own financial position 20 and interests at the expense of and to the detriment of the Class members. Specifically, 21 defendants are attempting to deny plaintiffs and the Class their shareholder rights through the 22 sale of Anadys via an unfair process. Accordingly, the Proposed Acquisition will benefit 23 defendants at the expense of Anadys shareholders.

24 76. In light of the foregoing, the Individual Defendants must, as their fiduciary 25 obligations require:

26 ? Act independently so that the interests of Anadys’s public stockholders will be protected; 27

? Adequately ensure that no conflicts of interest exist between defendants’ own 28 interests and their fiduciary obligation to maximize stockholder value or, if such

- 18—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

conflicts exist, to ensure that all conflicts be resolved in the best interests of

1 |

| Anadys’s public stockholders; and |

2 |

| ? Solicit competing bids to the Roche’s offer to ensure that the Company’s shareholders are receiving the maximum value for their shares. |

3 |

|

4 |

| CLASS ACTION ALLEGATIONS |

5 77. Plaintiffs bring this action for themselves and on behalf of all holders of Anadys 6 common stock which have been or will be harmed by the conduct described herein (the “Class”).

7 |

| Excluded from the Class are the defendants and any individual or entity affiliated with any 8 defendant. |

9 78. This action is properly maintainable as a class action.

10 79. The Class is so numerous that joinder of all members is impracticable. According 11 to the Company’s SEC filings, there were more than 57.1 million shares of Anadys common 12 stock outstanding as of October 14, 2011.

13 80. There are questions of law and fact which are common to the Class and which 14 predominate over questions affecting any individual Class member. The common questions 15 include, the following:

16 (a) whether the Individual Defendants have breached their fiduciary duties of 17 undivided loyalty, independence, or due care with respect to plaintiffs and the other members of 18 the Class in connection with the Proposed Acquisition;

19 (b) whether the Individual Defendants are engaging in self-dealing in 20 connection with the Proposed Acquisition;

21 (c) whether the Individual Defendants have breached any of their other 22 fiduciary duties owed to plaintiffs and the other members of the Class in connection with the

23 Proposed Acquisition, including the duties of good faith, diligence, and fair dealing;

24 (d) whether the Individual Defendants have disclosed all material information 25 regarding the Proposed Acquisition;

26 (e) whether Anadys aided and abetted the Individual Defendants’ breaches of 27 fiduciary duties; 28

- 19—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

1 |

| (f) whether Roche and/or Bryce aided and abetted the Individual Defendants’ 2 breaches of fiduciary duties; and |

3 (g) whether plaintiffs and the other members of the Class would suffer 4 irreparable injury were the transactions complained of herein consummated.

5 81. Plaintiffs’ claims are typical of the claims of the other members of the Class and 6 plaintiffs do not have any interests adverse to the Class.

7 82. Plaintiffs have retained competent counsel experienced in litigation of this nature 8 and will fairly and adequately represent and protect the interests of the Class.

9 83. The prosecution of separate actions by individual members of the Class would 10 create a risk of inconsistent or varying adjudications with respect to individual members of the

11 Class which would establish incompatible standards of conduct for the party opposing the Class.

12 84. Plaintiffs anticipate that there will be no difficulty in the management of this 13 litigation. A class action is superior to other available methods for the fair and efficient 14 adjudication of this controversy.

15 85. Defendants have acted on grounds generally applicable to the Class with respect 16 to the matters complained of herein, thereby making appropriate the relief sought herein with 17 respect to the Class as a whole.

18 FIRST CAUSE OF ACTION

19 Claim for Breach of Fiduciary Duties Against the Individual Defendants and Does 1-15

20 86. Plaintiffs incorporate by reference and reallege each and every allegation 21 contained above, as though fully set forth herein.

22 87. The Individual Defendants and Does 1-15 have violated the fiduciary duties of 23 care, loyalty, good faith, and independence owed to the public shareholders of Anadys and have 24 acted to put their personal interests ahead of the interests of Anadys’s shareholders.

25 88. By the acts, transactions, and courses of conduct alleged herein, the Individual

26 Defendants and Does 1-15, individually and acting as a part of a common plan, are attempting to 27 unfairly deprive plaintiffs and other members of the Class of the true value inherent in and 28 arising from Anadys.

- 20—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

1 |

| 89. As demonstrated by the allegations above, the Individual Defendants and Does 1- |

2 15 failed to exercise the care required, and breached their duties of loyalty, good faith, and 3 independence owed to the shareholders of Anadys because, among other reasons:

4 |

| (a) they omitted material information from the 14D-9; |

5 |

| (b) they failed to take steps to maximize the value of Anadys to its public 6 shareholders; |

7 |

| (c) they failed to properly value Anadys and its various assets and operations; 8 and |

9 (d) they ignored or did not protect against the numerous conflicts of interest 10 resulting from the officers’ and directors’ own interrelationships or connection with the Proposed

11 Acquisition.

12 90. Because Individual Defendants and Does 1-15 dominate and control the business 13 and corporate affairs of Anadys, and have access to private, corporate information concerning

14 Anadys’s assets, business, and future prospects, there exists an imbalance and disparity of 15 knowledge and economic power between them and the public shareholders of Anadys which 16 makes it inherently unfair for them to pursue and recommend any proposed acquisition wherein 17 they will reap disproportionate benefits to the exclusion of maximizing shareholder value.

18 91. By reason of the foregoing acts, practices, and courses of conduct, the Individual

19 Defendants and Does 1-15 have failed to exercise ordinary care and diligence in the exercise of 20 their fiduciary obligations toward plaintiffs and the other members of the Class.

21 92. Unless enjoined by this Court, the Individual Defendants and Does 1-15 will 22 continue to breach their fiduciary duties owed to plaintiffs and the Class, and may consummate 23 the Proposed Acquisition which will exclude the Class from its fair share of Anadys’s valuable 24 assets and operations, and/or benefit defendants in the unfair manner complained of herein, all to 25 the irreparable harm of the Class.

26 93. The Individual Defendants and Does 1-15 are engaging in self-dealing, are not 27 acting in good faith toward plaintiffs and the other members of the Class, and have breached and 28 are breaching their fiduciary duties to the members of the Class.

- 21—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

1 94. As a result of the Individual Defendants and Does 1-15’s unlawful actions, 2 plaintiffs and the other members of the Class will be irreparably harmed in that they will not 3 receive their fair portion of the value of Anadys’s assets and operations. Unless the Proposed

4 Acquisition is enjoined by the Court, the Individual Defendants and Does 1-15 will continue to 5 breach their fiduciary duties owed to plaintiffs and the members of the Class, will not engage in 6 arm’s-length negotiations on the Proposed Acquisition terms, and may consummate the Proposed

7 |

| Acquisition, all to the irreparable harm of the members of the Class. |

8 95. Plaintiffs and the members of the Class have no adequate remedy at law. Only 9 through the exercise of this Court’s equitable powers can plaintiffs and the Class be fully 10 protected from the immediate and irreparable injury which defendants’ actions threaten to inflict.

11 SECOND CAUSE OF ACTION

12 Claim for Aiding and Abetting Breaches of Fiduciary Duty Against Anadys

13 96. Plaintiffs incorporate by reference and reallege each and every allegation 14 contained above, as though fully set forth herein.

15 97. Defendant Anadys aided and abetted the Individual Defendants and Does 1-15 in 16 breaching their fiduciary duties owed to the public shareholders of Anadys, including plaintiffs 17 and the members of the Class.

18 98. The Individual Defendants and Does 1-15 owed to plaintiffs and the members of 19 the Class certain fiduciary duties as fully set out herein.

20 99. By committing the acts alleged herein, the Individual Defendants and Does 1-15 21 breached their fiduciary duties owed to plaintiffs and the members of the Class.

22 100. Anadys colluded in or aided and abetted the Individual Defendants and Does 1-

23 15’s breaches of fiduciary duties, and was an active and knowing participant in the Individual

24 Defendants and Does 1-15’s breaches of fiduciary duties owed to plaintiffs and the members of 25 the Class.

26 101. Plaintiffs and the members of the Class shall be irreparably injured as a direct and 27 proximate result of the aforementioned acts.

28

- 22—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

THIRD CAUSE OF ACTION

1 |

|

Claim for Aiding and Roche, Abetting Bryce, Breaches and Does of 16-25 Fiduciary Duty Against

2 |

|

3 102. Plaintiffs incorporate by reference and reallege each and every allegation 4 contained above, as though fully set forth herein.

5 |

| 103. Roche, Bryce, and Does 16-25 aided and abetted the Individual Defendants and |

6 Does 1-15 in breaching their fiduciary duties owed to the public shareholders of the Company, 7 including plaintiffs and the members of the Class.

8 104. The Individual Defendants and Does 1-15 owed to plaintiffs and the members of 9 the Class certain fiduciary duties as fully set out herein.

10 105. By committing the acts alleged herein, the Individual Defendants and Does 1-15 11 breached their fiduciary duties owed to plaintiffs and the members of the Class.

12 106. Roche, Bryce, and Does 16-25 colluded in or aided and abetted the Individual

13 Defendants and Does 1-15’s breaches of fiduciary duties, and were active and knowing 14 participants in the Individual Defendants and Does 1-15’s breaches of fiduciary duties owed to 15 plaintiffs and the members of the Class.

16 107. Roche, Bryce, and Does 16-25 participated in the breach of the fiduciary duties by 17 the Individual Defendants and Does 1-15 for the purpose of advancing their own interests.

18 Roche, Bryce, and Does 16-25 obtained and will obtain both direct and indirect benefits from 19 colluding in or aiding and abetting the Individual Defendants and Does 1-15’s breaches. Roche,

20 Bryce, and Does 16-25 will benefit, inter alia, from the acquisition of the Company at an 21 inadequate and unfair price if the Proposed Acquisition is consummated.

22 108. Plaintiffs and the members of the Class shall be irreparably injured as a direct and 23 proximate result of the aforementioned acts.

24 PRAYER FOR RELIEF

25 WHEREFORE, plaintiffs demand injunctive relief, in their favor and in favor of the

26 Class and against defendants as follows:

27 A. Declaring that this action is properly maintainable as a class action;

28 B. Declaring and decreeing that the Proposed Acquisition represents a breach of the

- 23—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

1 |

| fiduciary duties of defendants and is therefore unlawful and unenforceable; |

2 |

| C. Rescinding, to the extent already implemented, the Proposed Acquisition; |

3 D. Enjoining defendants, their agents, counsel, employees, and all persons acting in 4 concert with them from consummating the Proposed Acquisition, unless and until the Company 5 adopts and implements a procedure or process reasonably designed to enter into a merger 6 agreement providing the best possible value for shareholders;

7 E. Directing the Individual Defendants and Does 1-15 to exercise their fiduciary 8 duties to commence a sale process that is reasonably designed to secure the best possible 9 consideration for Anadys and obtain a transaction which is in the best interests of Anadys’s 10 shareholders;

11 F. Imposition of a constructive trust in favor of plaintiffs and members of the Class, 12 upon any benefits improperly received by defendants as a result of their wrongful conduct;

13 G. Awarding plaintiffs the costs and disbursements of this action, including 14 reasonable attorneys’ and experts’ fees; and

15 H. Granting such other and further equitable relief as this Court may deem just and 16 proper.

17 Dated: November 3, 2011 ROBBINS BRIAN J. ROBBINS UMEDA LLP

18 STEPHEN ARSHAN AMIRI J. ODDO

19 EDWARD B. GERARD

20

STEPHEN J. ODDO 21 600 B Street, Suite 1900

22 San Diego, CA 92101 Telephone: (619) 525-3990

23 Facsimile: (619) 525-3991

24 Co-Lead and Liaison Counsel for Plaintiffs

25 FARUQI & FARUQI, LLP Vahn Alexander, Esq.

26 1901 Avenue of the Stars, Second Floor Los Angeles, CA 90067

27 Telephone: (310) 461-1426 Facsimile: (310) 461-1427 28

- 24—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

FARUQI & FARUQI LLP

1 |

| Juan E. Monteverde, Esq. |

369 Lexington Avenue, 10th Floor

2 |

| New York, NY 10017 Telephone: (212) 983-9330 |

3 |

| Facsimile: (212) 983-9331 |

4 |

| Co-Lead Counsel for Plaintiffs 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 |

27 669224

28

- 25—

CONSOLIDATED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY

1 FARUQI & FARUQI, LLP VAHN ALEXANDER (167373) 2 CHRISTOPHER B. HAYES (277000) 1901 Avenue of the Stars, Second Floor 3 Los Angeles, CA 90067 Telephone: (310) 461-1426 4 Facsimile: (310) 461-1427 Email: valexander@faruqilaw.com 5 chayes@faruqilaw.com 6 Attorneys for Plaintiff 7 8 SUPERIOR COURT OF THE STATE OF CALIFORNIA 9 COUNTY OF SAN DIEGO 10 11 ) MIGUEL ANGEL ALONSO MAESTRO, Case No.: 12 Individually and on Behalf of All Others ) Similarly Situated, ) 13 . . ) CLASS ACTION COMPLAINT FOR 14 Plaintiff, ) BREACH OF FIDUCIARY DUTY v. ) 15 ) 16 ANADYS PHARMACEUTICALS, INC., JURY DEMAND BRIAN S. POSNER, KLEANTHIS G. ) 17 XANTHOPOULOS, STEPHEN T. ) WORLAND, MARK G. FOLETTA, BARRY ) 18 A. LABINGER, MARIOS FOTIADIS, ) STELIOS PAPADOPOULOS, JAMES L. ) 19 FREDDO, HOFFMANN-LA ROCHE INC., ) BRYCE ACQUISITION CORPORATION, and) 20 ROCHE HOLDINGS, INC., ) 21 ) 22 Defendants. ) 23 24 25 26 27 28 -1- CLASS ACTION COMPLAINT FOR BREACH OF FIDUCIARY DUTY

1 Plaintiff Miguel Angel Alonso Maestro (“Plaintiff”), by his attorneys, makes the following 2 allegations based upon information and belief, except as to allegations specifically pertaining to 3 himself and his counsel, which are based on personal knowledge. 4 SUMMARY 5 1. This is a shareholder class action complaint on behalf of the holders of the common 6 stock of Anadys Pharmaceuticals, Inc. (“Anadys” or the “Company”) against Anadys and its Board 7 of Directors (the “Board”), arising out of a proposed transaction through which the Company will 8 merge with Hoffman-La Roche Inc. (“Hoffman-La Roche”), a wholly-owned subsidiary of Roche 9 Holdings, Inc. (“Roche Holdings”), for inadequate consideration. 10 2. On October 17, 2011, Anadys issued a press release announcing that it had entered 11 into a definitive agreement with Hoffman-La Roche pursuant to which Hoffman-La Roche would 12 acquire Anadys, through its wholly-owned subsidiary, Bryce Acquisition Corporation (“Merger 13 Sub”), in an all-cash deal valued at approximately $230 million (“Merger Agreement”). Under the 14 terms of the Merger Agreement, Merger Sub will commence a cash tender offer (the “Tender 15 Offer”) to purchase all outstanding shares of Anadys common stock at a purchase price of $3.70 per 16 share in cash, to be followed by a merger of Merger Sub with and into the Company (collectively, 17 the Tender Offer and the second-step merger are referred to herein as the “Proposed Transaction”). 18 Roche Holdings is a party to the Merger Agreement as a guarantor of the obligations of both 19 Hoffman-La Roche and Merger Sub under that agreement. 20 3. As described below, both the value to Anadys shareholders contemplated in the 21 Proposed Transaction and the process by which defendants propose to consummate the Proposed 22 Transaction are fundamentally unfair to Plaintiff and the other public shareholders of the Company. 23 The Individual Defendants’ (as defined herein) conduct constitutes a breach of their fiduciary duties 24 owed to Anadys shareholders, and a violation of applicable legal standards governing the Individual 25 Defendants’ conduct. 26 4. To remedy defendants’ breaches of fiduciary duty and other misconduct, Plaintiff 27 seeks, inter alia: (i) injunctive relief preventing consummation of the Proposed Transaction, unless 28 -2- CLASS ACTION COMPLAINT FOR BREACH OF FIDUCIARY DUTY

1 and until the Company adopts and implements a procedure or process to obtain a transaction that 2 provides the highest value for shareholders; (ii) a directive to the Individual Defendants to exercise 3 their fiduciary duties to obtain a transaction which is in the best interests of Anadys’ shareholders; 4 and (iii) rescission of, to the extent already implemented, the Merger Agreement or any of the terms 5 thereof. 6 PARTIES 7 5. Plaintiff, Miguel Angel Alonso Maestro is, and has been at all relevant times, the 8 owner of shares of common stock of Anadys. 9 6. Defendant Anadys is a Delaware corporation, with its principal executive offices 10 located at 5871 Oberlin Drive, Suite 200, San Diego, CA 92121. Anadys, a biopharmaceutical 11 company, engages in developing novel medicines for the treatment of hepatitis C in the United 12 States. It develops ANA598, a direct-acting antiviral that is in Phase lib study for the treatment of 13 hepatitis C; and ANA773, an oral small-molecule inducer of endogenous interferons that acts 14 through the Toll-like receptor 7 pathway for the treatment of hepatitis C and cancer. 15 7. Defendant Brian S. Posner (“Posner”) has served as a member of the Board since 16 August2011. 17 8. Defendant Kleanthis G. Xanthopoulos (“Xanthopoulos”) is a co-founder of the 18 Company. Xanthopoulos has served as a Director of the Company since May 2000 and as President 19 and Chief Executive Officer of the Company from May 2000 to November 2006. He also serves as 20 a member of Anadys’ Audit Committee. 21 9. Defendant Stephen T. Worland (“Worland”) has served as President and Chief 22 Executive Officer of the Company, as well as a member of the Board, since 2007. Worland has 23 held various roles at Anadys since joining the Company in 2001, including Chief Scientific Officer, 24 Executive Vice President, and Head of Research & Development. 25 10. Defendant Mark G. Foletta (“Foletta”) has served as a Director of the Company 26 since September 2005. He also serves as a member of Anadys’ Audit Committee. 27 28 -3- CLASS ACTION COMPLAINT FOR BREACH OF FIDUCIARY DUTY

1 11. Defendant Barry A. Labinger (“Labinger”) has served as a Director of the Company 2 since March 2011. 3 12. Defendant Marios Fotiadis (“Fotiadis”) has served as a Director of the Company 4 since September 2002. He also serves as a member of Anadys’ Audit and Compensation 5 Committees. 6 13. Defendant Stelios Papadopoulos (“Papadopoulos”) has served as a Director of the 7 Company since May 2000. Papadopoulos has also served as the Chairman of the Board since 8 January 2011. Papadopoulos co-founded Anadys along with Xanthopoulos in 2000. 9 14. Defendant James L. Freddo (“Freddo”) has sewed as a Director of the Company 10 since January 2011. Freddo joined Anadys in July 2006 as Chief Medical Officer and was named 11 Senior Vice President, Drug Development and Chief Medical Officer in July 2008. 12 15. Posner, Xanthopoulos, Worland, Foletta, Labinger, Fotiadis, Papadopoulos, and 13 Freddo are referred to herein as the “Individual Defendants.” 14 16. Defendant Hoffmann-La Roche is a New Jersey corporation with its principal 15 executive offices located at 340 Kingsland St., Nutley, NJ 07110-1199. Hoffman-La Roche is part 16 of Roche USA and is one of the primary US research facilities for its parent, Swiss drug giant 17 Roche Holdings. It serves as a lead location for Roche’s oncology, inflammatory disease, virology, 18 and metabolism R&D programs, developing drugs to treat conditions including tumorous cancers, 19 asthma, rheumatoid arthritis, diabetes, and heart disease. Hoffmann-La Roche also has extensive 20 programs in gene-based and protein-based biotechnology research. 21 17. Defendant Merger Sub is a Delaware corporation and a wholly-owned subsidiary of 22 Hoffman-La Roche. Hoffman-La Roche and Merger Sub are collectively referred to herein as 23 “Hoffman-La Roche.” 24 18. Defendant Roche Holdings is a Delaware corporation and the parent company of 25 Hoffman-La Roche. 26 19. All defendants are sometimes collectively referred to herein as “Defendants.” 27 28 —4- CLASS ACTION COMPLAINT FOR BREACH OF FIDUCIARY DUTY

JURISDICTION AND VENUE 2 20. This Court has jurisdiction over the cause of action asserted herein pursuant to the 3 California Constitution, Article VI, §10, because this case is a cause not given by statute to other 4 trial courts. 5 21. This Court has jurisdiction over Anadys as the Company conducts business in 6 California. Anadys’ principal executive offices are located at 5871 Oberlin Drive, Suite 200, San 7 Diego, CA 92121. Moreover, various Annual Meetings of Stockholders have been held in 8 California. This action is not removable. 9 22. Venue is proper in this Court because the conduct at issue took place and had an 10 effect in this County. 11 INDIVIDUAL DEFENDANTS’ FIDUCIARY DUTIES 12 23. By reason of the Individual Defendants’ positions with the Company as officers 13 and/or directors, they are in a fiduciary relationship with Plaintiff and the other public shareholders 14 of Anadys and owe them, as well as the Company, a duty of highest good faith, fair dealing, loyalty, 15 as well as a duty to maximize shareholder value. 16 24. Where the officers and/or directors of a publicly traded corporation undertake a 17 transaction that will result in either: (i) a change in corporate control; (ii) a break up of the 18 corporation’s assets; or (iii) sale of the corporation, the directors have an affirmative fiduciary 19 obligation to obtain the highest value reasonably available for the corporation’s shareholders, and if 20 such transaction will result in a change of corporate control, the shareholders are entitled to receive 21 a significant premium. To diligently comply with their fiduciary duties, the directors and/or officers 22 may not take any action that: 23 a. adversely affects the value provided to the corporation’s shareholders; 24 b. favors themselves or will discourage or inhibit alternative offers to purchase 25 control of the corporation or its assets; 26 c. contractually prohibits them from complying with their fiduciary duties; 27 28 -5- CLASS ACTION COMPLAINT FOR BREACH OF FIDUCIARY DUTY

1 d. will otherwise adversely affect their duty to search for and secure the best 2 value reasonably available under the circumstances for the corporation’s 3 shareholders; and/or 4 e. will provide the directors and/or officers with preferential treatment at the 5 expense of, or separate from, the public shareholders. 6 25. In accordance with their duties of loyalty and good faith, the Individual Defendants, 7 as directors and/or officers of Anadys, are obligated to refrain from: 8 a. participating in any transaction where the directors or officers’ loyalties are 9 divided; 10 b. participating in any transaction where the directors or officers receive, or are 11 entitled to receive, a personal financial benefit not equally shared by the public 12 shareholders of the corporation; and/or 1.3 c. unjustly enriching themselves at the expense or to the detriment of the public 14 shareholders. 15 26. Plaintiff alleges herein that the Individual Defendants, separately and together, in 16 connection with the Proposed Transaction are knowingly or recklessly violating their fiduciary 17 duties, including their duties of loyalty, good faith and care owed to Plaintiff and other shareholders 18 of Anadys, or are aiding and abetting others in violating those duties. 19 CONSPIRACY. AIDING AND ABETTING AND CONCERTED ACTION 20 27. In committing the wrongful acts alleged herein, each of the Defendants has pursued, 21 or joined in the pursuit of, a common course of conduct, and acted in concert with and conspired 22 with one another, in furtherance of their common plan or design. In addition to the wrongful 23 conduct herein alleged as giving rise to primary liability, Defendants further aided and abetted 24 and/or assisted each other in breach of their respective duties as herein alleged. 25 28. During all relevant times hereto, Defendants, and each of them, initiated a course of 26 conduct which was designed to and did: (i) permit Hoffman-La Roche to attempt to eliminate the 27 shareholders’ equity interest in Anadys pursuant to a defective sales process; and (ii) permit 28 -6-