DEVELOPMENT & REDEVELOPMENT PIPELINE

Information as of September 30, 2007

55.3%

82.9%

75.7%

79.0%

80.9%

80.3%

100.0%

17.3%

33.4%

70.3%

87.5%

89.2%

Percent

Committed3

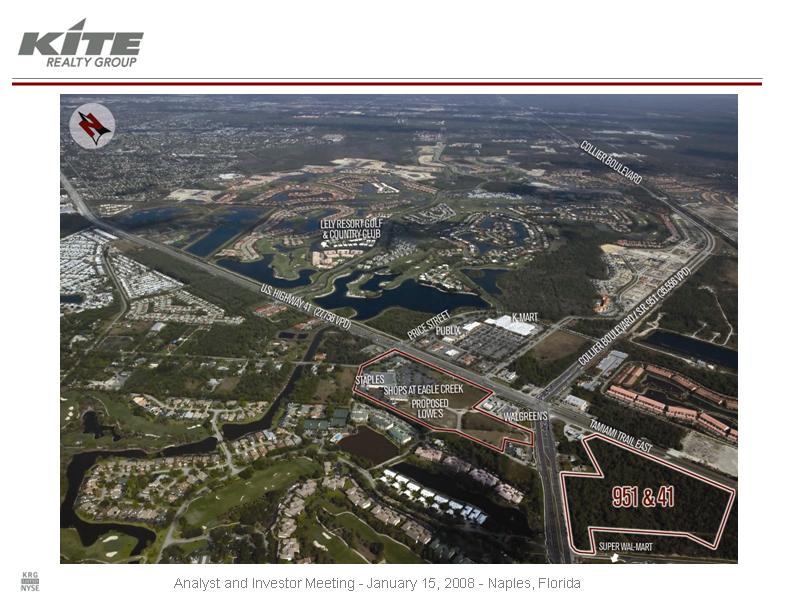

Staples

$3,500

72,271

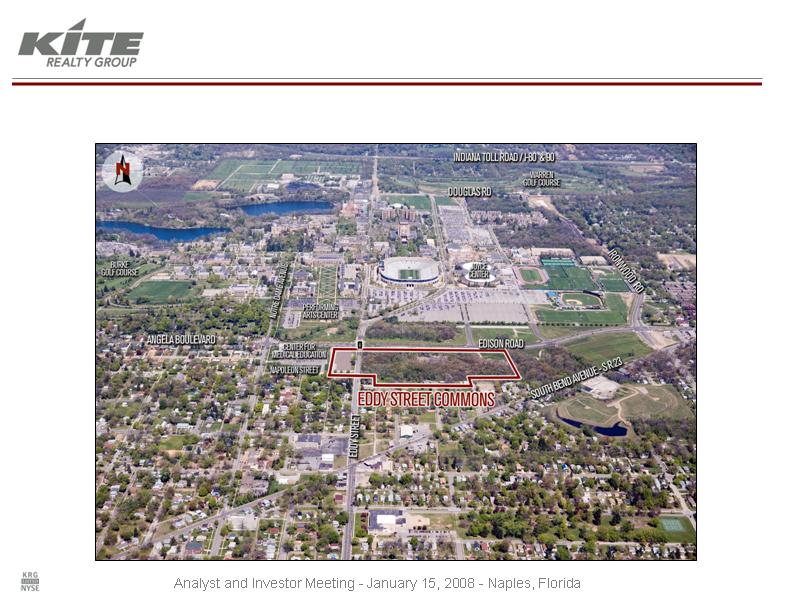

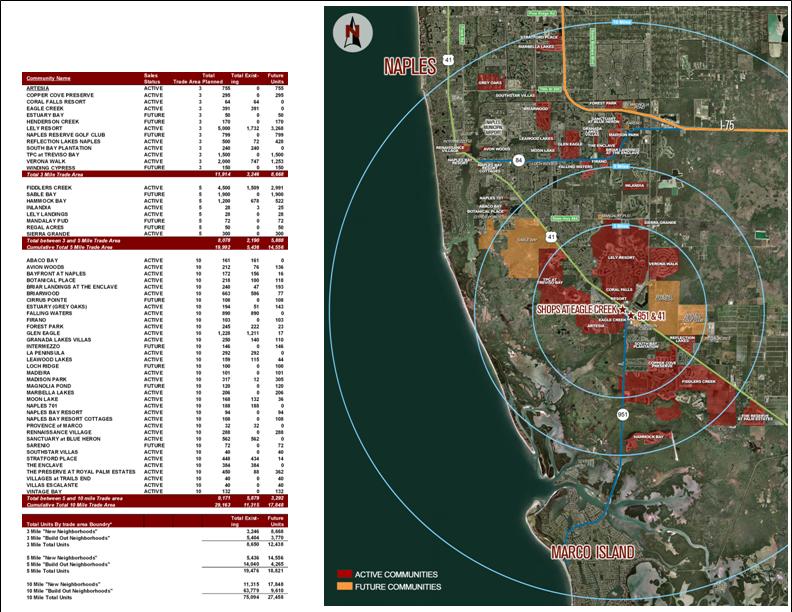

Naples, FL

Shops at Eagle Creek

$18,500

757,271

Sub-Total

Redevelopments

Target (non-owned), Lowe’s

$15,000

685,000

Indianapolis, IN

Glendale Town Center

$167,200

1,283,864

Sub-Total

Whole Foods, Staples

$47,000

163,600

Ft. Lauderdale, FL

Cobblestone Plaza 2

Seattle, WA

Tri-Cities, WA

Chicago, IL

Indianapolis, IN

Indianapolis, IN

Crown Point, IN

Tampa, FL

Naples, FL

MSA

Project

Projected

Total GLA1

Total Est.

Cost (000s)

Anchor Tenants

Tarpon Springs Plaza

276,346

$29,200

Target (non-owned), Staples,

Cost Plus, AC Moore

Bayport Commons 2

286,000

$25,000

Target (non-owned), Michael’s,

Best Buy, PetSmart

Beacon Hill Phase Il 2

19,160

$5,000

Strack & VanTil's (non-owned),

Walgreens (non-owned)

Bridgewater Marketplace I

50,820

$11,300

Walgreens (non-owned)

54th & College

20,100

$2,500

Fresh Market

Naperville Marketplace

151,607

$16,500

Caputo's Fresh Market (non-owned), TJ

Maxx

Sandifur Plaza 2

27,231

$6,400

Walgreens

Gateway Shopping Ctr 2

289,000

$24,300

Ross, PetSmart, Kohl’s (non-owned),

Winco (non-owned)

Total Dev. and Redev. Pipeline

2,041,135

$185,700

(1) Includes owned GLA, plus square footage attributable to non-owned outlot structures and non-owned outlot anchor space.

(2) Held in a joint venture entity.

(3) Percent Committed (as used in the table above and elsewhere in the presentation includes leases under negotiation for which the

company has signed non-binding letter of intent.

13