12th Annual Wachovia Global Real Estate Securities

Conference

December 9, 2008

DISCLAIMER

This presentation may include certain “forward-looking statements” within the meaning

of the Private Securities Litigation Reform Act of 1995. These forward-looking

statements include, but are not limited to, our plans, objectives, expectations and

intentions and other statements contained in this document that are not historical facts

and statements identified by words such as “expects”, “anticipates”, “intends”, “plans”,

“believes”, “seeks”, “estimates” or words of similar meaning. These statements are

based on our current beliefs or expectations and are inherently subject to significant

uncertainties and changes in circumstances, many of which are beyond our control.

Actual results may differ materially from these expectations due to changes in global

political, economic, business, competitive, market and regulatory risk factors.

Information concerning risk factors that could affect Kite Realty Group Trust’s actual

results is contained in the Company’s reports filed from time to time with the Securities

and Exchange Commission, including its 2007 Annual Report on Form 10-K and its

quarterly reports on Form 10-Q. Kite Realty Group Trust does not undertake any

obligation to update any forward-looking statements contained in this document, as a

result of new information, future events or otherwise.

2

COMPANY OVERVIEW

Balance Sheet Management

Continue to Manage Debt Maturities

Execute Capital Plan

Development

Complete Current Development Pipeline

$105 million total cost with approximately $60 million spent

75% Pre-leased or Committed

Delay visible shadow pipeline until significant leasing is

accomplished and third party construction financing is in place

Internal Growth

Operational Efficiencies

Minimize Existing Vacancy

PRIMARY OBJECTIVES FOR THE COMPANY

3

Consumer Behavior

Nationwide consumption levels will fluctuate, but a portion of the consumer’s behavior is derived from

necessity. Grocery-anchored centers and value-oriented retailers such as Target and Wal-Mart will

continue to create shopping center traffic.

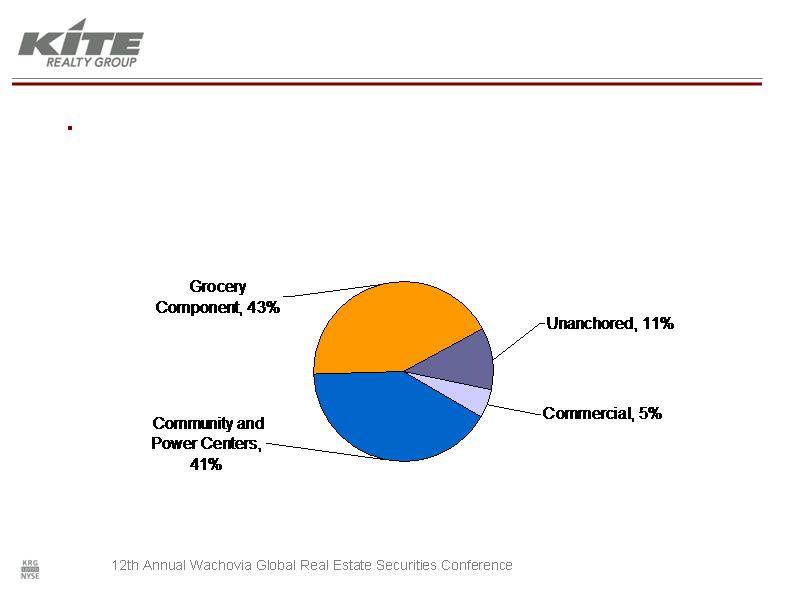

COMPANY OVERVIEW

(1) Includes Projected Total GLA for properties in the Current Development/Redevelopment Pipeline. Total GLA includes owned GLA, square

footage attributable to non-owned outlot structures on land that the Company owns, and non-owned anchor space that currently exists or is

under construction.

Property Type Allocation by Projected Total GLA 1

Information as of September 30, 2008

4

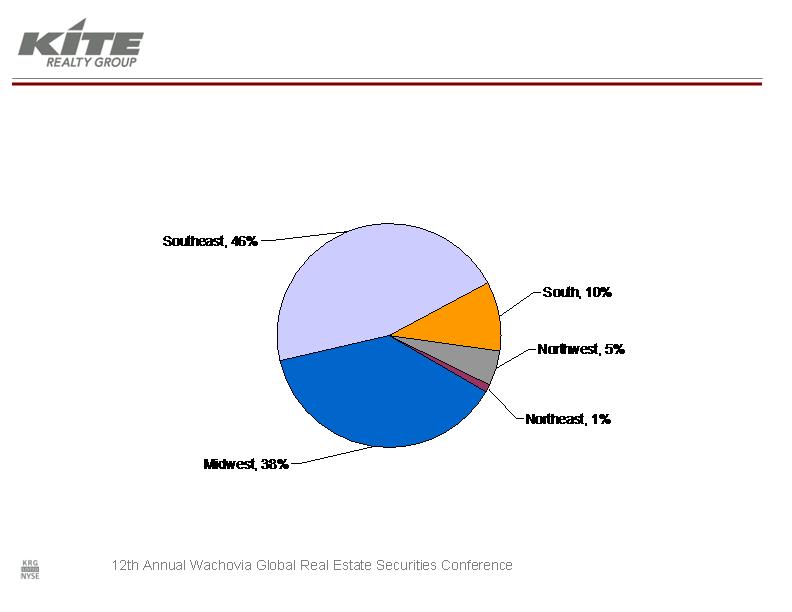

(1) Total GLA includes owned GLA, square footage attributable to non-owned outlot structures on land that the Company owns and

non-owned anchor space that currently exists or is under construction.

(2) Includes Projected Total GLA for properties in the Current Development, Redevelopment, and Visible Shadow Pipelines.

Projected Total GLA Including Pipelines 1,2

GEOGRAPHIC DIVERSIFICATION

COMPANY OVERVIEW

Information as of September 30, 2008

5

6

(1) As of December 4, 2008.

Information as of September 30, 2008 except as noted

COMPANY OVERVIEW

STRONG TENANT DIVERSITY

% of Portfolio

S&P

Annualized Base Rent

Credit Rating

1

1

Lowe's Home Improvement

3.4%

A+

2

PetSmart

2.7%

BB

3

Publix

2.4%

n/a

4

Marsh Supermarkets

2.1%

n/a

5

Bed Bath & Beyond

2.1%

BBB

6

Circuit City

2.0%

n/a

7

Office Depot

1.8%

BB

8

Staples

1.6%

BBB

9

Dick's Sporting Goods

1.6%

n/a

10

Ross Dress for Less

1.6%

BBB

Total

21.3%

Top 10 Retail Tenants by Base Rent

GROWTH STRATEGY

STRONG UPSIDE

Only 2% occupied

Growth source throughout 2009

LOW RISK PROFILE

75% leased or committed

55% funded

Entitlement and major construction risk has been removed – focus is on

executing small shop leases and build out tenant spaces

EMBEDDED GROWTH: CURRENT DEVELOPMENTS

Information as of September 30, 2008

7

GROWTH STRATEGY

Existing Vacancy

Operating retail portfolio is 91.9% leased

Negotiating lease for 23,000 square foot junior anchor space vacated in

early 2008 - represents 0.5% increase in occupancy

Operational Efficiencies

Leveraging bargaining power with national providers

Maintain class-A properties while managing to the CAM caps

Controlling variable costs – insurance and real estate taxes

3rd Party Construction and Service Fee Revenue

Leveraging our in-house construction company to generate FFO

Utilize current infrastructure to attract 3rd party contracts

EMPHASIZING INTERNAL GROWTH

Information as of September 30, 2008

8

DEVELOPMENT & REDEVELOPMENT PIPELINE

(1)

Includes owned GLA, plus square footage attributable to non-owned outlot structures and non-owned outlot anchor space.

(2)

Held in a joint venture entity.

(3)

Percent Committed includes leases under negotiation for which the company has signed non-binding letter of intent

(4)

The Company is the master developer for this project, and its share of Phase I estimated project costs is approximately $35 million.

9

Information as of September 30, 2008

Project

MSA

Projected

Total GLA

1

% Leased /

Committed

3

Total Est. Cost

(000s)

Anchor Tenants

Cobblestone Plaza

2

Ft. Lauderdale, FL

163,600

79.7%

$47,000

Whole Foods Market, Staples, Party

City

South Elgin Commons I

Chicago, IL

45,000

100.0%

$9,200

LA Fitness

Beacon Hill Phase Il

2

Crown Point, IN

19,160

33.4%

$5,000

Strack & VanTil's (non-owned),

Walgreens (non-owned)

Spring Mill Medical II

2

Indianapolis, IN

41,000

100.0%

$8,500

Medical Practice Groups

Eddy Street Commons I

4

South Bend, IN

465,000

61.2%

$35,000

Follette Bookstore, retail, office

733,760

74.6%

$104,700

Redevelopments

Shops at Eagle Creek

Naples, FL

72,271

$3,500

Staples

Rivers Edge Shopping Ctr

Indianapolis, IN

110,875

$5,000

Pending

Bolton Plaza

Jacksonville, FL

172,938

$6,200

Pending

Courthouse Shadows

Naples, FL

134,867

$2,500

Publix, Office Max

Four Corner Square

Seattle, WA

29,177

$500

Johnson Hardware, Walgreens

520,128

$17,700

Total Current Development Pipeline

Total Redevelopment Pipeline

VISIBLE SHADOW PIPELINE

(1)

Total Estimated Cost and Estimated Total GLA based on preliminary siteplans.

(2)

Acquired in a joint venture with Prudential Real Estate Investors. KRG’s ownership interest will change to 20% upon commencement of

construction.

(3)

Held in a joint venture entity.

10

Information as of September 30, 2008

Project

KRG %

Owned

MSA

Est. Total

GLA

1

Est. Total

Cost (000s)

1

Potential Tenancy

Unconsolidated:

Parkside Town Commons

2

40%

Raleigh, NC

1,500,000

$148,000

Frank Theatres, Discount Dept. Stores, Jr. Boxes,

Restaurants

KRG Current Share

$59,200

Consolidated:

Delray Marketplace

3

50%

Delray Beach, FL

318,000

$100,000

Publix, Frank Theatres, Jr. Boxes, Shops,

Restaurants

Maple Valley

100%

Seattle, WA

126,823

$32,000

Hardware Store, Shops, Drug Store

Broadstone Station (Apex)

100%

Raleigh, NC

345,000

$25,600

Super Wal-Mart (non-owned), Jr. Boxes, Shops,

Pad sales

South Elgin Commons II

100%

Chicago, IL

263,000

$17,000

Jr. Boxes, SuperTarget (non-owned)

New Hill Place I

100%

Raleigh, NC

364,000

$60,000

Target, Frank Theaters

1,416,823

$234,600

Total Consolidated Visible Shadow Pipeline

DEVELOPMENT PIPELINE

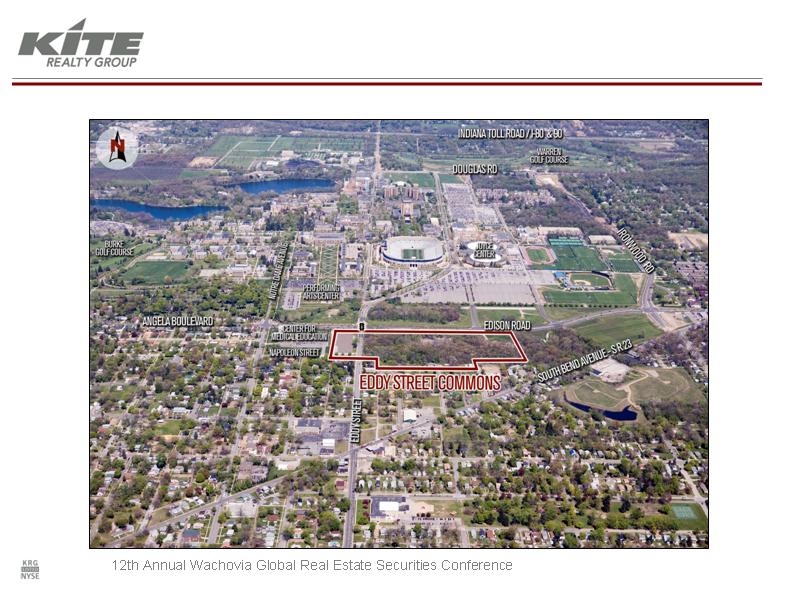

A CASE STUDY IN RISK MITIGATION: EDDY STREET COMMONS

11

DEVELOPMENT PIPELINE

A CASE STUDY IN RISK MITIGATION: EDDY STREET COMMONS

$200 million mixed-use development next to the University of Notre Dame in South

Bend, IN will be completed in phases

$35 million Phase I, which will include retail and office, was recently added to the

Current Development Pipeline. Phase I will also include a $35 million multi-family

component that will be developed and operated by a third party.

Three goals were set and accomplished before significant capital was spent:

The land was fully entitled with a planned unit development designation

Tax Increment Financing (TIF) and other municipal incentives totaling $35M

were funded

Final deal structure with the University of Notre Dame was completed and Kite

acquired and ground leases separate parcels

Joint venture arrangements for multi-family and hotel components will be utilized to

mitigate risk and maximize expertise

Additional land for residential units can be acquired from the University at our

discretion and will be based solely on residential market demand

Information as of September 30, 2008

12

DEVELOPMENT PIPELINE

A CASE STUDY IN RISK MITIGATION: EDDY STREET COMMONS

Phase I – Retail, Office, Multi-family, Parking Garage

13

STRONG DEMOGRAPHICS

SUCCESS NOT DEPENDENT ON GROWTH

Source: Applied Geographic Solutions

$488M

$190M

Expenditure Potential

$466M

$186M

Expenditure Potential

$84,716

$87,910

Average HH Income

$77,007

$77,012

Average HH Income

2.3%

2.8%

Projected Annual Growth

1.8%

1.8%

Projected Annual Growth

133,272

51,023

2012 Est. Population

136,673

54,416

2012 Est. Population

118,951

44,549

2007 Est. Population

124,977

49,691

2007 Est. Population

5 Mile

3 Mile

Development Pipeline

5 Mile

3 Mile

Operating Portfolio

Radius

Radius

Operating Portfolio vs. Development Pipeline

Portfolio Demographic Comparison

14

Credit Facility and Cash 1 : $100 million

Potential Asset Sales: $20 to 25 million

Targeted Asset Transfer to JVs: $25 to $30 million

Targeted Liquidity Level: $75 to $100 million

EXECUTE ON STRATEGY TO ENSURE CAPITAL AVAILABILITY

CAPITAL PLAN

Information as of September 30, 2008 except as noted

(1) Includes common equity offering net proceeds of approximately $47.8 million that were received in October 2008.

15

MANAGING DEBT MATURITIES

AGGRESSIVE REFINANCING, SOLID EXECUTION

Information as of September 30, 2008

16

(1)

In October 2008, the Company extended the maturity dates from 2009 to 2010 on its variable rate debt at four of its consolidated

properties. As a result, $60.9 million of obligation previously due in 2009 are now due in 2010, as reflected the table above.

(2)

The Company is pursuing a loan commitment in place to extend the maturity date from 2009 to 2011 on variable rate debt of

approximately $21.0 million at one of its properties and another loan commitment currently in place for $22.4 million of new

borrowings at one of its unencumbered properties, the proceeds of which the Company anticipates utilizing to extinguish debt at

three of its operating properties.

(3)

Amount due in 2011 includes the outstanding balance on our unsecured revolving credit facility, which has a one-year extension

option.

Including

As of

% of

Q4 2008

% of

9/30/08

Total

Refinancings

1, 2

Total

2008

$18,684

3%

$0

0%

2009

$190,284

26%

$107,770

15%

2010

$13,373

2%

$74,238

10%

2011

3

$229,798

32%

$270,131

37%

2012

$38,905

5%

$38,905

5%

Thereafter

$236,263

32%

$236,263

32%

Total Maturities

$727,307

100%

$727,307

100%

COMMITTED MANAGEMENT

Senior management owns approximately 21 percent of the Company and has

acquired over 400,000 shares and 800,000 units since the IPO at a cost of

approximately $21M

0.2%

9 years

EVP & CFO

Dan Sink

20.6%

7.3%

18 years

Chairman & CEO

John Kite

3.6%

14 years

President & COO

Tom McGowan

9.5%

48 years

Chairman Emeritus

Al Kite

Ownership 1

Tenure with

Company

(1) As of November 7, 2008, and includes units of Operating Partnership.

17

OPERATING METRICS

For the Three Months Ended September 30, 2008

2.5x

2.6x

Fixed Charge Coverage 2

5.3%

5.3%

G&A / Revenue from Rental

Properties

94.8%

92.5%

Portfolio % Leased

71%

64%

FFO Payout %

70.8%

72.8%

NOI / Revenue

Selected

Peer Group

Average 1

KRG

(1)

Peer Group consists of KIM, DDR, AKR, REG and RPT.

(2)

Defined as EBITDA divided by Interest Expense plus Preferred Dividends.

18

CORPORATE PROFILE

Kite Realty Group Trust is a full-service, vertically integrated real estate investment trust

engaged primarily in the ownership, operation, management, leasing, acquisition,

construction, expansion, and development of high quality neighborhood and community

shopping centers in selected growth markets in the United States. The Company owns

interests in a portfolio of operating retail properties, retail properties under development,

operating commercial properties, a related parking garage, commercial property under

development and parcels of land that may be used for future development of retail or

commercial properties.

Our strategy is to maximize the cash flow of its operating properties, successfully complete

the construction and lease-up of the development portfolio and identify additional growth

opportunities in the form of new developments and acquisitions. A significant volume of

growth opportunity is sourced through the extensive network of tenant, corporate and

institutional relationships that have been established over the last four decades. Current

investments are focused in the development and acquisition of high quality, well located

shopping centers.

19