UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21552

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

(Exact name of registrant as specified in charter)

270 Park Avenue, Floor 6

New York, NY 10017

(Address of principal executive offices) (Zip code)

Frank J. Nasta, Esq.

J.P. Morgan Investment Management Inc.

270 Park Avenue, Floor 9

New York, NY 10017

(Name and address of agent for service)

Copy to:

Richard Horowitz, Esq.

Dechert LLP

1095 Avenue of the Americas

New York, NY 10036

Registrant’s telephone number, including area code: (800) 480-4111

Date of fiscal year end: March 31

Date of reporting period: March 31, 2012

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Financial Statements

For the year ended March 31, 2012

This report is open and authorized for distribution only to qualified and accredited investors or financial intermediaries who have received a copy of the Fund’s Private Placement Memorandum. This document, although required to be filed with the SEC, may not be copied, faxed or otherwise distributed to the general public.

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Financial Statements

For the year ended March 31, 2012

Contents

Past performance is no guarantee of future results. Market volatility can significantly impact short-term performance. Results of an investment made today may differ substantially from the Fund’s historical performance. Investment return and principal value will fluctuate so that an investor’s interests, when redeemed, may be worth more or less than original cost.

Report of Independent Registered Public Accounting Firm

To the Board of Directors and Members of

J.P. Morgan Access Multi-Strategy Fund, L.L.C.:

In our opinion, the accompanying statement of assets, liabilities and members’ capital, including the schedule of investments, and the related statements of operations, of changes in members’ capital and of cash flows and the financial highlights present fairly, in all material respects, the financial position of J.P. Morgan Access Multi-Strategy Fund, L.L.C. (the “Fund”) at March 31, 2012, the results of its operations and its cash flows for the year then ended, the changes in its members’ capital for each of the two years in the period then ended and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of investments at March 31, 2012 by correspondence with the underlying investment funds, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

New York, New York

May 30, 2012

PricewaterhouseCoopers LLP, PricewaterhouseCoopers Center, 300 Madison Avenue New York, NY 10017 T: (646) 471 3000, F: (813) 286 6000, www.pwc.com/us

1

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Schedule of Investments

March 31, 2012

| | | | | | | | | | | | | | |

Investment Fund | | Cost ($) | | | Fair Value ($) | | | % of

Members’

Capital | | | Liquidity(e) |

Diversified | | | | | | | | | | | | | | |

D.E. Shaw Composite Fund, LLC | | | 45,947,521 | | | | 49,779,052 | | | | 5.59 | | | Quarterly* |

Hudson Bay Fund L.P. | | | 61,108,734 | | | | 67,092,368 | | | | 7.54 | | | Quarterly |

Och-Ziff Domestic Partners II, L.P. | | | 72,300,000 | | | | 75,662,688 | | | | 8.49 | | | Quarterly |

QVT Associates II, L.P. | | | 3,280,913 | | | | 3,583,656 | | | | 0.40 | | | In Liquidation*** |

QVT Associates II, L.P., SLV | | | 156,764 | | | | 676 | | | | 0.00 | (a) | | Side Pocket** |

| | | | | | | | | | | | | | |

Total | | | 182,793,932 | | | | 196,118,440 | | | | 22.02 | | | |

| | | | | | | | | | | | | | |

Event Driven - Core | | | | | | | | | | | | | | |

Apollo Asia Opportunity Fund, L.P. | | | 402,486 | | | | 523,715 | | | | 0.06 | | | Side Pocket** |

Corvex Partners L.P. | | | 10,000,000 | | | | 10,218,666 | | | | 1.15 | | | Quarterly |

Deephaven Event Fund LLC | | | 198,199 | | | | 54,672 | | | | 0.01 | | | In Liquidation*** |

Paulson Partners Enhanced, L.P. | | | 37,088,094 | | | | 33,878,308 | | | | 3.81 | | | Semi-Annual |

Perry Partners L.P. | | | 27,500,000 | | | | 26,663,931 | | | | 2.99 | | | Quarterly |

Taconic Opportunity Fund, L.P. | | | 17,778 | | | | 25,928 | | | | 0.00 | (a) | | Side Pocket** |

Third Point Partners Qualified L.P. (b) | | | 41,750,000 | | | | 44,304,152 | | | | 4.97 | | | Quarterly |

Tyrus Capital Event Fund, L.P. | | | 20,300,000 | | | | 20,881,321 | | | | 2.34 | | | Quarterly |

Tyrus Capital Opportunities Fund L.P. | | | 23,200,000 | | | | 23,555,046 | | | | 2.64 | | | Quarterly |

ValueAct Capital Partners, L.P. | | | 879,774 | | | | 1,320,371 | | | | 0.15 | | | Side Pocket** |

| | | | | | | | | | | | | | |

Total | | | 161,336,331 | | | | 161,426,110 | | | | 18.12 | | | |

| | | | | | | | | | | | | | |

Event Driven - Distressed | | | | | | | | | | | | | | |

Caspian Capital Partners, L.P. | | | 15,500,000 | | | | 17,316,790 | | | | 1.95 | | | Quarterly |

Strategic Value Restructuring Fund, L.P. | | | 1,943,982 | | | | 688,547 | | | | 0.07 | | | Side Pocket** |

SVRF (Onshore) Holdings LLC | | | 344,569 | | | | 281,825 | | | | 0.03 | | | Annual |

York Credit Opportunities Fund, L.P. (b) | | | 30,250,222 | | | | 31,793,135 | | | | 3.58 | | | Quarterly |

| | | | | | | | | | | | | | |

Total | | | 48,038,773 | | | | 50,080,297 | | | | 5.63 | | | |

| | | | | | | | | | | | | | |

Long/Short Equities | | | | | | | | | | | | | | |

Black Bear Fund I, L.P. | | | 90,769 | | | | 116,559 | | | | 0.01 | | | In Liquidation*** |

Brahman Partners III, L.P. | | | 46,850,000 | | | | 48,942,221 | | | | 5.50 | | | Quarterly |

Copper River Partners, L.P. | | | 57,214 | | | | 16,343 | | | | 0.00 | (a) | | In Liquidation*** |

Deerfield Partners, L.P. | | | 1,173,126 | | | | 1,907,562 | | | | 0.21 | | | Semi-Annual |

Glenview Institutional Partners, L.P. (b) | | | 38,722,799 | | | | 36,816,682 | | | | 4.13 | | | Quarterly* |

Maverick Fund USA Ltd. (b) | | | 48,650,000 | | | | 47,223,040 | | | | 5.31 | | | Monthly |

Standard Global Equity Partners SA, L.P. | | | 38,400,000 | | | | 38,260,846 | | | | 4.29 | | | Quarterly |

TPG-Axon Partners, L.P. | | | 36,350,000 | | | | 35,230,317 | | | | 3.96 | | | Quarterly |

| | | | | | | | | | | | | | |

Total | | | 210,293,908 | | | | 208,513,570 | | | | 23.41 | | | |

| | | | | | | | | | | | | | |

Opportunistic/Macro | | | | | | | | | | | | | | |

Black River Commodity Multi-Strategy Fund, LLC | | | 614,262 | | | | 548,114 | | | | 0.06 | | | Side Pocket** |

Brevan Howard, L.P. (b) | | | 29,029,710 | | | | 34,026,443 | | | | 3.82 | | | Monthly |

Caxton Global Investments USA, LLC (b) | | | 40,800,000 | | | | 42,696,052 | | | | 4.80 | | | Quarterly |

D.E. Shaw Oculus Fund LLC (b) | | | 40,392,961 | | | | 52,769,786 | | | | 5.93 | | | Quarterly* |

Two Sigma Horizon US Fund, L.P. | | | 20,000,000 | | | | 20,168,903 | | | | 2.26 | | | Quarterly |

| | | | | | | | | | | | | | |

Total | | | 130,836,933 | | | | 150,209,298 | | | | 16.87 | | | |

| | | | | | | | | | | | | | |

The accompanying notes are an integral part of these financial statements.

2

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Schedule of Investments (continued)

March 31, 2012

| | | | | | | | | | | | | | |

Investment Fund | | Cost ($) | | | Fair Value ($) | | | % of

Members’

Capital | | | Liquidity(e) |

Relative Value | | | | | | | | | | | | | | |

BAM Opportunity Fund SPV, LLC | | $ | 153,109 | | | $ | 75,677 | | | | 0.01 | | | Side Pocket** |

Centar Select, L.P. | | | 465,928 | | | | 481,424 | | | | 0.05 | | | In Liquidation*** |

Golden Tree Partners, L.P. Class C (b) | | | 43,350,000 | | | | 45,098,829 | | | | 5.07 | | | Quarterly* |

Good Hill SPV, Ltd. | | | 213,659 | | | | 207,330 | | | | 0.02 | | | In Liquidation*** |

Horizon Portfolio L.P. | | | 18,200,000 | | | | 18,900,447 | | | | 2.12 | | | Quarterly |

Knighthead Domestic Fund, L.P. | | | 646,760 | | | | 836,994 | | | | 0.09 | | | Quarterly |

Magnetar Capital Fund, L.P. | | | 675,563 | | | | 543,265 | | | | 0.06 | | | Side Pocket** |

Magnetar Risk Linked Fund (US) Ltd. | | | 2,274,484 | | | | 2,437,136 | | | | 0.28 | | | Side Pocket** |

Magnetar SPV LLC | | | 218,114 | | | | 277,653 | | | | 0.03 | | | In Liquidation*** |

Magnetar Structured Credit Fund, L.P. | | | 2,544,944 | | | | 3,315,032 | | | | 0.37 | | | Semi-Annual |

Marathon Credit Opportunity Fund, L.P. | | | 40,506,882 | | | | 40,180,102 | | | | 4.52 | | | Semi-Annual |

Orchard Centar, L.P. | | | 1,060,654 | | | | 1,524,540 | | | | 0.17 | | | Quarterly |

Plainfield 2009 Liquidating LLC | | | 222,899 | | | | 71,773 | | | | 0.01 | | | In Liquidation*** |

Waterfall Eden Fund, L.P. Designated | | | 1,588,907 | | | | 665,512 | | | | 0.07 | | | In Liquidation*** |

Waterfall Victoria Fund, L.P. | | | 813,932 | | | | 944,236 | | | | 0.11 | | | Semi-Annual* |

| | | | | | | | | | | | | | |

Total | | | 112,935,835 | | | | 115,559,950 | | | | 12.98 | | | |

| | | | | | | | | | | | | | |

Total Investments in Investment Funds | | | 846,235,712 | | | | 881,907,665 | | | | 99.03 | | | |

Short-Term Investment | | | | | | | | | | | | | | |

Investment Company | | | | | | | | | | | | | | |

J.P. Morgan Prime Money Market Fund,

Institutional Class Shares, 0.01% (c) (d) | | | 44,828,055 | | | | 44,828,055 | | | | 5.03 | | | Daily |

| | | | | | | | | | | | | | |

Total Investments | | | 891,063,767 | | | | 926,735,720 | | | | 104.06 | | | |

Other Liabilities, less Other Assets | | | | | | | (36,214,801 | ) | | | (4.06 | ) | | |

| | | | | | | | | | | | | | |

Members’ Capital | | | | | | | 890,520,919 | | | | 100.00 | | | |

| | | | | | | | | | | | | | |

| (a) | Amount rounds to less than 0.01%. |

| (b) | Partially or wholly held in a pledged account by the Custodian as collateral for existing line of credit. |

| (c) | Investment in affiliate. Money market fund registered under the Investment Company Act of 1940, as amended, and advised by J.P. Morgan Investment Management Inc. |

| (d) | The rate shown is the current yield as of March 31, 2012. |

| (e) | Certain funds may be subject to an initial lockup period. |

| * | An amount less than 5% of this investment is currently in a side pocket. |

| ** | A side pocket is an account within the Investment Fund that has additional restrictions on liquidity. |

| *** | The Investment Fund is in the process of ceasing its operations or has created a special purpose vehicle to handle the orderly disposition of the underlying assets, which may result in the Fund’s delayed receipt of redemption proceeds. |

The accompanying notes are an integral part of these financial statements.

3

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Schedule of Investments (continued)

March 31, 2012

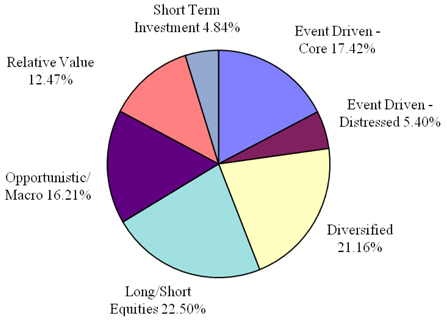

Investment Strategy as a Percentage of Total Investments

The management agreements of the general partners/managers provide for compensation to such general partners/managers in the form of management fees ranging from 0% to 3% annually of net assets and incentives of 15% to 30% of net profits earned.

The accompanying notes are an integral part of these financial statements.

4

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Statement of Assets, Liabilities and Members’ Capital

March 31, 2012

| | | | |

Assets | | | | |

Investments, at fair value (cost $891,063,767) | | $ | 926,735,720 | |

Cash | | | 268,048 | |

Investments paid in advance (see Note 2c) | | | 13,000,000 | |

Receivable for investment funds sold | | | 1,524,227 | |

Prepaid expenses | | | 81,579 | |

Due from Investment Manager | | | 5,044 | |

Dividends receivable | | | 4,341 | |

Interest receivable | | | 138 | |

| | | | |

Total assets | | | 941,619,097 | |

| | | | |

Liabilities | | | | |

Contributions received in advance (see Note 6) | | | 30,200,887 | |

Tender offer proceeds payable | | | 19,171,285 | |

Management Fee payable | | | 947,177 | |

Professional fees payable | | | 509,241 | |

Administration Fee payable | | | 113,661 | |

Credit facility fees payable | | | 5,000 | |

Other accrued expenses | | | 150,927 | |

| | | | |

Total liabilities | | | 51,098,178 | |

| | | | |

Members’ capital | | $ | 890,520,919 | |

| | | | |

The accompanying notes are an integral part of these financial statements.

5

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Statement of Operations

For the year ended March 31, 2012

| | | | |

Investment income | | | | |

Interest | | $ | 7,933 | |

Dividend income | | | 14,663 | |

Other income | | | 34,497 | |

| | | | |

Total investment income | | | 57,093 | |

| | | | |

Expenses | | | | |

Management Fee (see Note 3) | | | 9,430,367 | |

Administration Fee (see Note 3) | | | 1,171,621 | |

Professional fees | | | 510,046 | |

Fund accounting and custodian fees | | | 484,972 | |

Investor servicing fees | | | 356,150 | |

Credit facility fees | | | 265,715 | |

Insurance | | | 59,010 | |

Interest | | | 20,509 | |

Directors’ and Chief Compliance Officer’s fees | | | 6,987 | |

Other expenses | | | 153,477 | |

| | | | |

Total expenses | | | 12,458,854 | |

| | | | |

Less: Waivers and/or expense reimbursements (see Note 3) | | | (13,661 | ) |

| | | | |

Net expenses | | | 12,445,193 | |

| | | | |

Net investment income/(loss) | | | (12,388,100 | ) |

| | | | |

Realized and unrealized gain (loss) | | | | |

Net realized gain/(loss) from investment fund transactions | | | 3,937,138 | |

Net change in unrealized appreciation (depreciation) on investment funds | | | 5,001,010 | |

| | | | |

Net realized and unrealized gain (loss) | | | 8,938,148 | |

| | | | |

Net decrease in members’ capital derived from operations | | $ | (3,449,952 | ) |

| | | | |

The accompanying notes are an integral part of these financial statements.

6

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Statements of Changes in Members’ Capital

For the year ended March 31, 2012

| | | | | | | | | | | | | | | | |

| | | Managing

Member | | | Special

Member | | | Other

Members | | | Total | |

From investment activities | | | | | | | | | | | | | | | | |

Net investment loss | | $ | (196 | ) | | $ | (8,256 | ) | | $ | (12,379,648 | ) | | $ | (12,388,100 | ) |

Net realized gain/(loss) from investment fund transactions | | | 128 | | | | 7,373 | | | | 3,929,637 | | | | 3,937,138 | |

Net change in unrealized appreciation/(depreciation) on investment funds | | | (44 | ) | | | (34,661 | ) | | | 5,035,715 | | | | 5,001,010 | |

Performance allocation | | | — | | | | 275,233 | | | | (275,233 | ) | | | — | |

| | | | | | | | | | | | | | | | |

Net increase/(decrease) in members’ capital derived from operations | | | (112 | ) | | | 239,689 | | | | (3,689,529 | ) | | | (3,449,952 | ) |

From members’ capital transactions | | | | | | | | | | | | | | | | |

Capital contributions | | | — | | | | — | | | | 439,406,160 | | | | 439,406,160 | |

Repurchase fee | | | 1 | | | | 13 | | | | 16,259 | | | | 16,273 | |

Capital redemptions | | | — | | | | (587,987 | ) | | | (47,408,146 | ) | | | (47,996,133 | ) |

| | | | | | | | | | | | | | | | |

Net increase/(decrease) in members’ capital derived from capital transactions | | | 1 | | | | (587,974 | ) | | | 392,014,273 | | | | 391,426,300 | |

| | | | | | | | | | | | | | | | |

Net change in members’ capital | | | (111 | ) | | | (348,285 | ) | | | 388,324,744 | | | | 387,976,348 | |

Members’ capital at beginning of year | | | 12,119 | | | | 1,433,198 | | | | 501,099,254 | | | | 502,544,571 | |

| | | | | | | | | | | | | | | | |

Members’ capital at end of year | | $ | 12,008 | | | $ | 1,084,913 | | | $ | 889,423,398 | | | $ | 890,520,919 | |

| | | | | | | | | | | | | | | | |

For the year ended March 31, 2011

| | | | | | | | | | | | | | | | |

| | | Managing

Member | | | Special

Member | | | Other

Members | | | Total | |

From investment activities | | | | | | | | | | | | | | | | |

Net investment loss | | $ | (219 | ) | | $ | (3,594 | ) | | $ | (4,832,717 | ) | | $ | (4,836,530 | ) |

Net realized gain/(loss) from investment fund transactions | | | 350 | | | | 2,620 | | | | 8,274,988 | | | | 8,277,958 | |

Net change in unrealized appreciation/(depreciation) on investment funds | | | 554 | | | | 19,819 | | | | 16,038,071 | | | | 16,058,444 | |

Performance allocation | | | — | | | | 1,357,688 | | | | (1,357,688 | ) | | | — | |

| | | | | | | | | | | | | | | | |

Net increase/(decrease) in members’ capital derived from operations | | | 685 | | | | 1,376,533 | | | | 18,122,654 | | | | 19,499,872 | |

From members’ capital transactions | | | | | | | | | | | | | | | | |

Capital contributions | | | — | | | | — | | | | 363,914,889 | | | | 363,914,889 | |

Capital redemptions | | | — | | | | (33,696 | ) | | | (49,855,572 | ) | | | (49,889,268 | ) |

| | | | | | | | | | | | | | | | |

Net increase/(decrease) in members’ capital derived from capital transactions | | | — | | | | (33,696 | ) | | | 314,059,317 | | | | 314,025,621 | |

| | | | | | | | | | | | | | | | |

Net change in members’ capital | | | 685 | | | | 1,342,837 | | | | 332,181,971 | | | | 333,525,493 | |

Members’ capital at beginning of year | | | 11,434 | | | | 90,361 | | | | 168,917,283 | | | | 169,019,078 | |

| | | | | | | | | | | | | | | | |

Members’ capital at end of year | | $ | 12,119 | | | $ | 1,433,198 | | | $ | 501,099,254 | | | $ | 502,544,571 | |

| | | | | | | | | | | | | | | | |

The accompanying notes are an integral part of these financial statements.

7

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Statement of Cash Flows

For the year ended March 31, 2012

| | | | |

Cash flows from operating activities | | | | |

Net decrease in members’ capital derived from operations | | $ | (3,449,952 | ) |

Adjustments to reconcile net decrease in members’ capital derived from operations to net cash used in operating activities: | | | | |

Purchases of investment funds | | | (441,917,604 | ) |

Proceeds from disposition of investment funds | | | 44,325,045 | |

Purchases of short-term investments, net | | | (44,828,055 | ) |

Net realized gain on investment fund transactions | | | (3,937,138 | ) |

Net change in unrealized appreciation/(depreciation) on investment funds | | | (5,001,010 | ) |

Decrease in interest receivable | | | 733 | |

Decrease in investments paid in advance | | | 74,400,000 | |

Decrease in receivable for investment funds sold | | | 18,946,240 | |

Increase in dividends receivable | | | (4,341 | ) |

Increase in prepaid expenses | | | (29,985 | ) |

Increase in Due from Investment Manager | | | (5,044 | ) |

Decrease in interest payable | | | (14,270 | ) |

Increase in Administration Fee payable | | | 50,418 | |

Increase in Credit facility fees payable | | | 5,000 | |

Increase in Management Fee payable | | | 419,979 | |

Increase in Professional fees payable | | | 59,246 | |

Increase in Other accrued expenses | | | 60,451 | |

| | | | |

Net cash used in operating activities | | | (360,920,287 | ) |

| | | | |

Cash flows from financing activities | | | | |

Capital contributions, including change in contributions received in advance | | | 399,102,189 | |

Capital redemptions, including change in tender offer proceeds payable | | | (34,014,914 | ) |

Principal payment on loan | | | (15,000,000 | ) |

| | | | |

Net cash provided by financing activities | | | 350,087,275 | |

| | | | |

Net decrease in cash and cash equivalents | | | (10,833,012 | ) |

Cash and cash equivalents at beginning of year | | | 11,101,060 | |

| | | | |

Cash at end of year | | $ | 268,048 | |

| | | | |

SUPPLEMENTAL CASH FLOW INFORMATION | | | | |

Cash paid during the year for interest | | $ | 34,779 | |

| | | | |

The accompanying notes are an integral part of these financial statements.

8

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Financial Highlights

Ratios and Other Financial Highlights

The following represents the ratios to average net assets and other financial highlights information for Members’ Capital other than the Managing Member and the Special Member.

| | | | | | | | | | | | | | | | | | | | |

| | | For The Years Ended March 31 | |

| | | 2012 | | | 2011 | | | 2010 | | | 2009 | | | 2008 | |

Total return before performance allocation | | | (0.92 | %) | | | 5.99 | % | | | 9.32 | % | | | (17.36 | %) | | | 5.18 | % |

Performance allocation | | | (0.03 | %) | | | (0.36 | %) | | | (0.09 | %) | | | 0.00 | % | | | (0.23 | %) |

| | | | | | | | | | | | | | | | | | | | |

Total return after performance allocation | | | (0.95 | %) | | | 5.63 | % | | | 9.23 | % | | | (17.36 | %) | | | 4.95 | % |

Ratios to average net assets: | | | | | | | | | | | | | | | | | | | | |

Expenses, before waivers | | | 1.70 | %(a) | | | 1.91 | %(a) | | | 1.94 | % | | | 1.87 | % | | | 1.82 | % |

Expenses, net of waivers | | | 1.70 | %(a) | | | 1.90 | %(a) | | | 1.94 | % | | | 1.87 | % | | | 1.82 | % |

Performance allocation | | | 0.04 | % | | | 0.53 | % | | | 0.09 | % | | | 0.00 | % | | | 0.24 | % |

| | | | | | | | | | | | | | | | | | | | |

Expenses, net of performance allocation and net of waivers | | | 1.74 | % | | | 2.43 | % | | | 2.03 | % | | | 1.87 | % | | | 2.06 | % |

Net investment loss, before waivers | | | (1.69 | %)(a) | | | (1.91 | %)(a) | | | (1.94 | %) | | | (1.82 | %) | | | (1.68 | %) |

Net investment loss, net of waivers | | | (1.69 | %)(a) | | | (1.90 | %)(a) | | | (1.94 | %) | | | (1.82 | %) | | | (1.68 | %) |

Portfolio turnover rate | | | 6.21 | % | | | 37.88 | % | | | 44.97 | % | | | 23.76 | % | | | 20.89 | % |

Members’ Capital applicable to Other Members | | $ | 889,423,398 | | | $ | 501,099,254 | | | $ | 168,917,283 | | | $ | 180,386,527 | | | $ | 148,750,929 | |

The above ratios and total returns are calculated for Other Members taken as a whole. An individual investor’s return may vary from these returns based on the timing of capital contributions and performance allocation.

The above expense ratios do not include the expenses from the underlying fund investments. However, total returns take into account all expenses.

| (a) | The Investment Manager waived and/or reimbursed a portion of its fees for the period pursuant to the agreement between the Fund and the Investment Manager. |

The accompanying notes are an integral part of these financial statements.

9

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Notes to Financial Statements March 31, 2012

1. Organization

J.P. Morgan Access Multi-Strategy Fund, L.L.C. (the “Fund”) was organized as a limited liability company on April 6, 2004 under the laws of the State of Delaware and is registered under the Investment Company Act of 1940 (the “1940 Act”), as a closed-end, non-diversified, management investment company. The Fund’s investment objective is to generate consistent capital appreciation over the long term, with relatively low volatility and a low correlation with traditional equity and fixed-income markets. The Fund will seek to accomplish this objective by allocating its assets primarily among professionally selected investment funds (“Investment Funds”) that are managed by experienced third-party investment advisers (“Portfolio Managers”) who invest in a variety of markets and employ, as a group, a range of investment techniques and strategies. There can be no assurance that the Fund will achieve its investment objective.

J.P. Morgan Investment Management, Inc. (“JPMIM” or the “Investment Manager”), a corporation formed under the laws of the State of Delaware and a wholly-owned subsidiary of JPMorgan Chase & Co. (“JPMorgan Chase”), is responsible for the day-to-day management of the Fund, subject to policies adopted by the Board of Directors (the “Board”). The Investment Manager has in turn delegated substantially all investment authority and the allocation of the Fund’s assets among the Investment Funds and other instruments to J.P. Morgan Private Investments Inc. (the “Sub-Advisor” or “JPMPI”), a corporation formed under the laws of the State of Delaware and a wholly-owned subsidiary of JPMorgan Chase. The Sub-Advisor will allocate Fund assets among the Investment Funds and other investments that, in its view, represent attractive investment opportunities. The Investment Manager also serves as the managing member of the Fund (the “Managing Member”).

Both the Investment Manager and the Sub-Advisor are registered as investment advisers under the Investment Advisers Act of 1940, as amended (the “Advisers Act”).

2. Significant Accounting Policies

a. Use of Estimates

The following is a summary of significant accounting policies followed by the Fund in preparation of its financial statements. The policies are in accordance with accounting principles generally accepted in the United States of America (“GAAP”). The preparation of financial statements in conformity with GAAP requires the Investment Manager to make estimates and assumptions that affect the amounts reported in the financial statements and accompanying notes. Actual results could differ from these estimates.

b. Valuation of Investments

The net asset value of the Fund is determined as of the last day of each month in accordance with the valuation principles set forth below or as may be determined from time to time pursuant to policies established by the Board. The Fund’s investments in the Investment Funds are considered to be illiquid and can only be redeemed periodically. The Board has approved procedures pursuant to which the Fund values its investments in Investment Funds at fair value. In accordance with these procedures, fair value as of each month-end ordinarily is the net asset value determined as of such month-end for each Investment Fund in accordance with the Investment Fund’s valuation policies and reported at the time of the Fund’s valuation.

10

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Notes to Financial Statements March 31, 2012 (continued)

2. Significant Accounting Policies (continued)

b. Valuation of Investments (continued)

The Fund uses the net asset value to determine the fair value of all underlying investments which (a) do not have readily determinable fair values and (b) either have the attributes of an investment company or prepare their financial statements consistent with measurement principles of an investment company. As a general matter, the fair value of the Fund’s interest in an Investment Fund will represent the amount that the Fund could reasonably expect to receive from an Investment Fund if the Fund’s interest were redeemed at the time of the valuation, based on information reasonably available at the time the valuation is made and that the Fund believes to be reliable. Considerable judgment is required to interpret the factors used to develop estimates at fair value. These factors include, but are not limited to, a review of the underlying securities of the Investment Fund when available, ongoing due diligence of the style, strategy and valuation methodology employed by each Investment Fund, and a review of market inputs that may be expected to impact the performance of a particular Investment Fund. The use of different factors and estimation methodologies could have a significant effect on the estimated fair value and could be material to the financial statements. In the unlikely event that an Investment Fund does not report a month-end net asset value to the Fund on a timely basis, the Fund would determine the fair value of such Investment Fund based on the most recent value reported by the Investment Fund, as well as any other relevant information available at such time. Some of the Investment Funds may invest all or a portion of their assets in investments which may be illiquid. Some of these investments are held in “side pockets”, sub funds within the Investment Funds, which provide for their separate liquidation potentially over a much longer period than the liquidity an investment in the Investment Funds may provide. Should the Fund seek to liquidate its investment in an Investment Fund which maintains investments in a side pocket arrangement or which holds substantially all of its assets in illiquid securities, the Fund might not be able to fully liquidate its investment without delay, which could be considerable. In such cases, during the period until the Fund is permitted to fully liquidate its interest in the Investment Funds, the value of its investment could fluctuate.

Investments in other open-end investment companies are valued at such company’s net asset value per share as of the report date.

The Fund discloses the fair value of its investments in a hierarchy that prioritizes the inputs to valuation techniques used to measure the fair value. Fair value is defined as the price that the Fund would receive to sell an investment or pay to transfer a liability in an orderly transaction with an independent buyer in the principal market, or in the absence of a principal market, the most advantageous market for the investment or liability.

Valuations reflected in this report are as of the report date. As a result, changes in valuation due to market events and/or issuer related events after the report date and prior to issuance of the report are not reflected herein.

11

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Notes to Financial Statements March 31, 2012 (continued)

2. Significant Accounting Policies (continued)

b. Valuation of Investments (continued)

The various inputs that are used in determining the fair value of the Fund’s investments are summarized into the three broad levels listed below

| | • | | Level 1 inputs are quoted prices in active markets for identical securities; |

| | • | | Level 2 inputs are other significant observable inputs (including the Investment Fund’s ability to be redeemed within 12 months of the reporting date at fair value). |

| | • | | Level 3 inputs are significant unobservable inputs and include restrictions on redemptions of the Investment Funds due to terms of the investment or gates, suspensions, etc. imposed by the Investment Fund such that the Fund cannot redeem at fair value within 12 months of the reporting date. |

A financial instrument’s level within the fair value hierarchy is based on the lowest level of any input both individually and in aggregate that is significant to the fair value measurement. The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following table represents each valuation input, by strategy, as presented on the Schedule of Investments:

| | | | | | | | | | | | | | | | |

Investments in Investment Funds | | Total Fair

Value at

03/31/2012 | | | Level 1 | | | Level 2 | | | Level 3 | |

Diversified | | $ | 196,118,440 | | | $ | — | | | $ | 192,066,357 | | | $ | 4,052,083 | |

Event Driven - Core | | | 161,426,110 | | | | — | | | | 159,501,424 | | | | 1,924,686 | |

Event Driven - Distressed | | | 50,080,297 | | | | — | | | | 49,109,925 | | | | 970,372 | |

Long/Short Equities | | | 208,513,570 | | | | — | | | | 136,333,669 | | | | 72,179,901 | |

Opportunistic/Macro | | | 150,209,298 | | | | — | | | | 149,661,184 | | | | 548,114 | |

Relative Value | | | 115,559,950 | | | | — | | | | 109,947,327 | | | | 5,612,623 | |

Short-Term Investment | | | | | | | | | | | | | | | | |

Investment Company | | | 44,828,055 | | | | 44,828,055 | | | | — | | | | — | |

| | | | | | | | | | | | | | | | |

Total Investments | | $ | 926,735,720 | | | $ | 44,828,055 | | | $ | 796,619,886 | | | $ | 85,287,779 | |

| | | | | | | | | | | | | | | | |

The following is a summary of each strategy for which significant unobservable inputs (Level 3) were used in determining fair value:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Investment Strategy | | Balance as of

March 31, 2011 | | | Transfers

into Level 3

(a) | | | Transfers

out of Level 3

(a) | | | Net realized

gain / (loss) | | | Net change in

unrealized

appreciation /

(depreciation) | | | Net purchases

/ (sales) | | | Balance as of

March 31, 2012 | |

Diversified | | $ | 2,107,663 | | | $ | 5,997,398 | | | $ | (108,390 | ) | | $ | 881,675 | | | $ | (639,343 | ) | | $ | (4,186,920 | ) | | $ | 4,052,083 | |

Event Driven - Core | | | 2,098,284 | | | | — | | | | (2,758 | ) | | | (4,193 | ) | | | 239,093 | | | | (405,740 | ) | | | 1,924,686 | |

Event Driven - Distressed | | | 1,821,931 | | | | — | | | | — | | | | (21,856 | ) | | | (349,899 | ) | | | (479,804 | ) | | | 970,372 | |

Long/Short Equities | | | 315,040 | | | | 40,565,611 | | | | — | | | | (136,634 | ) | | | (4,235,835 | ) | | | 35,671,719 | | | | 72,179,901 | |

Opportunistic/Macro | | | 862,424 | | | | — | | | | — | | | | (12,113 | ) | | | (130,929 | ) | | | (171,268 | ) | | | 548,114 | |

Relative Value | | | 6,414,172 | | | | 223,962 | | | | — | | | | (778,989 | ) | | | 431,093 | | | | (677,615 | ) | | | 5,612,623 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total | | $ | 13,619,514 | | | $ | 46,786,971 | | | $ | (111,148 | ) | | $ | (72,110 | ) | | $ | (4,685,820 | ) | | $ | 29,750,372 | | | $ | 85,287,779 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

12

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Notes to Financial Statements March 31, 2012 (continued)

2. Significant Accounting Policies (continued)

b. Valuation of Investments (continued)

(a) The Fund recognizes transfers into and out of the levels indicated above at the beginning of the reporting period. Transfers from Level 2 to Level 3 were primarily related to the change in liquidity terms of the underlying Investment Funds during the reporting period. Transfers from Level 3 to Level 2 were primarily related to the expiration of lock-up periods imposed by the underlying Investment Funds and due to liquidity provisions considered by the Fund. There were no transfers between Level 1 and Level 2 during the year ended March 31, 2012.

The Fund had no unfunded capital commitments as of March 31, 2012.

The change in unrealized appreciation/(depreciation) attributable to securities owned at March 31, 2012, which were valued using significant unobservable inputs (Level 3), is as follows:

| | | | |

Investments in

Investment Funds | | Net change in

unrealized

appreciation/

(depreciation) | |

Diversified | | $ | (98,232 | ) |

Event Driven - Core | | | 239,093 | |

Event Driven - Distressed | | | (165,103 | ) |

Long / Short Equities | | | (4,143,208 | ) |

Opportunistic / Macro | | | (130,929 | ) |

Relative Value | | | 465,143 | |

| | | | |

Total | | $ | (3,833,236 | ) |

| | | | |

Diversified

Portfolio Managers utilizing this strategy use two or more of the below strategies. Investment Funds within this strategy are generally subject to 30 - 75 day redemption notice periods. Less than 1 percent of the fair value of the investments in Investment Funds in this strategy is in side pockets or liquidating trusts. The remaining Investment Funds have quarterly liquidity and may be subject to lockups of up to two years. During the year ended March 31, 2012, the Fund had ten transfers into Level 3 with a fair market value of $5,997,398 and the Fund had seven transfers out of Level 3 with a fair market value of $108,390. Also, during the year ended March 31, 2012, Level 3 sales for this strategy totaled $4,816,920.

13

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Notes to Financial Statements March 31, 2012 (continued)

2. Significant Accounting Policies (continued)

b. Valuation of Investments (continued)

Event Driven - Core

Portfolio Managers utilizing this strategy invest in securities of companies involved in mergers, acquisitions, restructurings, liquidations, spin-offs, or other special situations that alter a company’s financial structure or operating strategy. Risk management and hedging techniques are typically employed by the Portfolio Managers to seek to protect the portfolio from deals that fail to materialize. In addition, accurately forecasting the timing of a transaction is an important element affecting the realized return. Portfolio Managers in this strategy may use leverage. Investment Funds within this strategy are generally subject to 60 - 93 day redemption notice periods. Approximately 1 percent of the fair value of investments in Investment Funds in this strategy is in side pockets or liquidating trusts. The remaining Investment Funds have quarterly to annual liquidity. Certain funds may have lock up periods of up to one year as of March 31, 2012. During the year ended March 31, 2012, the Fund had one transfer out of Level 3 with a fair market value of $2,758. Also, during the year ended March 31, 2012, Level 3 sales for this strategy totaled $405,740.

Event Driven - Distressed

Portfolio Managers utilizing this strategy invest in debt and equity securities of companies in financial difficulty, reorganization or bankruptcy, nonperforming and sub-performing bank loans, and emerging market debt. Portfolios are usually concentrated in debt instruments. The Portfolio Managers differ in their preference for actively participating in the workout and restructuring process and the extent to which they use leverage. Investment Funds within this strategy are generally subject to 60 - 95 day redemption notice periods. Approximately 2 percent of the fair value of investments in Investment Funds in this strategy is in side pockets or liquidating trusts. The Investment Funds have quarterly to annual liquidity. During the year ended March 31, 2012, the Fund had no transfers into or out of Level 3. During the year ended March 31, 2012, Level 3 sales for this strategy totaled $479,804.

Long/Short Equities

Portfolio Managers utilizing this strategy make long and short investments in equity securities that are deemed by the Portfolio Managers to be under or overvalued. The Portfolio Managers typically do not attempt to neutralize the amount of long and short positions (i.e., they will be net long or net short). The Portfolio Managers may specialize in a particular industry or may allocate holdings across industries. Although the strategy is more commonly focused on U.S. markets, a growing number of Portfolio Managers invest globally. Portfolio Managers in this strategy usually employ a low to moderate degree of leverage. Investment Funds within this strategy are generally subject to 30 - 90 day redemption notice periods. Less than 1 percent of the fair value of investments in Investment Funds in this strategy is in side pockets or liquidating trusts. The Investment Funds have monthly to semi-annual liquidity. Certain funds may have lock up periods of up to two years as of March 31, 2012. During the year ended March 31, 2012, the Fund had two transfers into Level 3 with a fair market value of $40,565,613. Also, during the year ended March 31, 2012, Level 3 purchases for this strategy totaled $35,800,000 and sales for this strategy totaled $128,281.

14

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Notes to Financial Statements March 31, 2012 (continued)

2. Significant Accounting Policies (continued)

b. Valuation of Investments (continued)

Opportunistic/Macro

Portfolio Managers utilizing this strategy invest in a wide variety of instruments using a broad range of strategies, often assuming an aggressive risk posture. Most Portfolio Managers utilizing this strategy rely on a combination of macro-economic models and fundamental research to invest across countries, markets, sectors and companies, and have the flexibility to invest in numerous financial instruments. Futures and options are often used for hedging and speculation in order to quickly position a portfolio to profit from changing markets. The use of leverage varies considerably. Investment Funds within this strategy are generally subject to 45 - 95 day redemption notice periods. Less than 1 percent of the fair value of investments in Investment Funds in this strategy is in side pockets or liquidating trusts. The Investment Funds have monthly to quarterly liquidity. Certain funds may have lock up periods of up to one year as of March 31, 2012. During the year ended March 31, 2012, the Fund had no transfers into or out of Level 3. Also, during the year ended March 31, 2012, Level 3 sales for this strategy totaled $171,268.

Relative Value

Portfolio Managers utilizing this strategy make simultaneous purchases and sales of similar securities to exploit pricing differentials or have long exposure in non-equity oriented beta opportunities (such as credit). The Portfolio Managers attempt to neutralize long and short positions to minimize the impact of general market movements. Different relative value strategies include convertible bond arbitrage, statistical arbitrage, pairs trading, yield curve arbitrage and basis trading. The types of instruments traded vary considerably depending on the Portfolio Manager’s relative value strategy. Because the strategy attempts to capture relatively small mis-pricings between two related securities, moderate to substantial leverage is often employed to produce attractive rates of return. Investment Funds within this strategy are generally subject to 45 - 120 day redemption notice periods. Approximately 6 percent of the fair value of investments in Investment Funds in this strategy is in side pockets or liquidating trusts. The Investment Funds have quarterly to semi-annual liquidity. Certain funds may have lock up periods of up to one year as of March 31, 2012. During the year ended March 31, 2012, the Fund had two transfers into Level 3 with a fair market value of $223,962. Also, during the year ended March 31, 2012, Level 3 purchases and sales for this strategy totaled $545,452 and $1,223,067, respectively.

Any restriction noted above was imposed at various points throughout the year, at the discretion of the underlying Investment Funds and the time at which the restriction might lapse cannot be estimated.

c. Investments Paid in Advance

Investments paid in advance represent funds which have been sent to Investment Funds prior to March 31, 2012 but are not effective until April 1, 2012. See Note 10.

15

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Notes to Financial Statements March 31, 2012 (continued)

2. Significant Accounting Policies (continued)

d. Distributions from Investment Funds

Distributions received, whether in the form of cash or securities, are applied as a reduction of the investment’s cost when identified by the Investment Fund as a return of capital. Once the investment’s cost is received, any further distributions are recognized as realized gains.

e. Income Recognition and Security Transactions

Interest income is recorded on an accrual basis. Realized gains and losses from Investment Fund transactions are calculated on the identified cost basis. Investments are recorded on the effective date of the subscription in the Investment Fund. All changes in the value of the Investment Funds are included as unrealized appreciation or depreciation in the Statement of Operations.

f. Fund Expenses

The Fund bears all expenses incurred in its business other than those that the Investment Manager assumes. The expenses of the Fund include, but are not limited to, the following: all costs and expenses related to investment transactions and positions for the Fund’s account; legal fees; accounting and auditing fees; custodial fees; costs of computing the Fund’s net asset value; costs of insurance; registration expenses; expenses of meetings of the Board and Members; all costs with respect to communications to Members; and other types of expenses as may be approved from time to time by the Board.

g. Income Taxes

The Fund intends to operate and has elected to be treated as a partnership for federal income tax purposes. Accordingly, no provision for the payment of federal, state or local income taxes has been provided. Each Member is individually required to report on its own tax return its distributive share of the Fund’s taxable income or loss.

The Investment Manager evaluates tax positions taken or expected to be taken in the course of preparing the Fund’s financial statements to determine whether the tax positions are “more-likely-than-not” of being sustained by the applicable tax authority. Tax positions with respect to tax at the Fund level not deemed to meet the “more-likely-than-not” threshold would be recorded as a tax benefit or expense in the current year. The Investment Manager is not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits or expense will significantly change in the next twelve months. The Investment Manager’s conclusions regarding tax positions will be subject to review and may be adjusted at a later date based on factors including, but not limited to, on-going analyses of tax laws, regulations and interpretations thereof.

The Fund’s Federal tax returns for the prior three fiscal years remain subject to examination by the Internal Revenue Service. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statement of Operations. During the year ended March 31, 2012, the Fund did not incur any interest or penalties.

16

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Notes to Financial Statements March 31, 2012 (continued)

2. Significant Accounting Policies (continued)

h. Cash

Cash represents deposits of $268,048 held in an interest bearing account at The Bank of New York Mellon. Amounts in excess of the insurance limit of the Federal Deposit Insurance Corporation (“FDIC”) are subject to counterparty credit risk should The Bank of New York Mellon be unable to fulfill its obligations.

3. Management Fee, Related Party Transactions and Other

The Fund has entered into an investment management agreement (the “Investment Management Agreement”) with the Investment Manager. In consideration of the advisory services provided by the Investment Manager to the Fund, the Fund pays the Investment Manager a management fee of 1.25% per year (the “Management Fee”), payable monthly at the rate of 1/12 of 1.25% of the month-end capital account balance of each Member, before giving effect to repurchases, Repurchase Fees (if any, as defined below) or the Performance Allocation (as defined below), but after giving effect to the Fund’s other expenses. The Management Fee is an expense paid out of the Fund’s assets. The Management Fee is paid monthly in arrears within 30 days after the end of each month. For the year ended March 31, 2012, the Management Fee earned by JPMIM totaled $9,430,367, none of which was waived.

The Investment Manager, on behalf of the Fund, has entered into an investment sub-advisory agreement with JPMPI. For its services as sub-advisor, the Investment Manager pays JPMPI a monthly sub-advisory fee of 1/12 of 1.10% of the month-end capital balance of each Member of the Fund.

The Sub-Advisor is the special member of the Fund (the “Special Member”). The Special Member is entitled to all incentive-based performance allocations, if any, from Members’ accounts.

Pursuant to an Administration Agreement, JPMorgan Funds Management, Inc. (“JPMFM” or the “Administrator”), an indirect, wholly-owned subsidiary of JPMorgan Chase, provides certain administration services to the Fund. In consideration of these services, the Administrator receives a fee (the “Administration Fee”) monthly at the annual rate of 0.15% of the Fund’s average daily net assets. For the year ended March 31, 2012, the Administration Fee earned by JPMFM totaled $1,171,621.

BNY Mellon Investment Servicing (US) Inc. (“BNY Mellon”) serves as the Fund’s sub-administrator (the “Sub-administrator”). For its services as Sub-administrator, BNY Mellon receives a portion of the fees payable to the Administrator.

The Bank of New York Mellon (the “Custodian”) serves as custodian of the Fund’s assets and provides custodial services to the Fund. As compensation for services, the Fund pays the Custodian a monthly fee of 0.005% of the Fund’s average gross assets, with a minimum monthly fee of $795.

17

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Notes to Financial Statements March 31, 2012 (continued)

3. Management Fee, Related Party Transactions and Other (continued)

The Investment Manager, or an affiliate of the Investment Manager, has contractually agreed to waive fees and/or reimburse the Fund to the extent that total annual operating expenses (excluding acquired fund fees and expenses, interest, brokerage commissions, other transaction-related expenses and any extraordinary expenses as well as any Performance Allocation) exceed 1.92% on an annualized basis of the Fund’s net assets as of the end of each month. This expense limitation agreement was in effect for the year ended March 31, 2012.

The Fund may invest in one or more money market funds advised by the Investment Manager or its affiliates. The Investment Manager, Administrator and Distributor, as shareholder servicing agent waive fees in an amount sufficient to offset the respective fees each charges to the affiliated money market fund on the Fund’s investment in such affiliated money market fund. A portion of the waiver is voluntary. The amount of waivers resulting from investments in the money market fund for the year ended March 31, 2012 was $13,661.

Certain officers of the Fund are affiliated with the Investment Manager and the Administrator. Such officers, with the exception of the Chief Compliance Officer, receive no compensation from the Fund for serving in their respective roles.

The Fund has adopted a Director Deferred Compensation Plan (the “Plan”) which allows the Independent Directors to defer the receipt of all or a portion of compensation related to performance of their duties as a Director. The deferred fees are invested in various J.P. Morgan Funds until distribution in accordance with the Plan.

4. Line of Credit

From time to time, the Fund may borrow cash from a major institution under a credit agreement up to a maximum of 10% of the Fund’s net assets with a cap of $15 million. Prior to March 2, 2012 the cap was $30 million. Interest, which is calculated based on any outstanding balance, and a LIBOR-based rate, is payable monthly to the lending institution. The Fund also pays a monthly fee on the unused amount on the line of credit. During the year ended March 31, 2012, the Fund had 28 days during the period in which it utilized the credit facility. During those 28 days, the average borrowings outstanding per day were $10,000,000 at an average annual interest rate of 2.64%. The Fund had no outstanding balance on this Credit facility as of March 31, 2012. Interest expense and Credit facility fees incurred for the year ended March 31, 2012 amounted to $20,509 and $265,715, respectively, and are included in the Statement of Operations.

5. Security Transactions

Aggregate purchases and sales of Investment Funds for the year ended March 31, 2012 amounted to $441,917,604 and $44,325,267, respectively.

At March 31, 2012, the estimated cost of investments for federal income tax purposes was substantially the same as the cost for financial reporting purposes. Accordingly, gross unrealized appreciation on investments was $47,652,117 and gross unrealized depreciation was $11,979,942, resulting in net unrealized depreciation of $35,672,175.

18

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Notes to Financial Statements March 31, 2012 (continued)

6. Contributions, Redemptions, and Performance Allocation

Generally, initial and additional contributions for Interests (“Interests”) by eligible investors may be accepted at such times as the Fund may determine. The Fund reserves the right to reject any contributions for Interests in the Fund. The initial acceptance for contributions for Interests was April 1, 2004 (the “Initial Closing Date”). After the Initial Closing Date, the Fund generally accepts contributions for Interests as of the first day of each month. At March 31, 2012 the Fund received $30,200,887 in contribution proceeds in advance of the April 1, 2012 contribution date. This amount is included in the Statement of Assets, Liabilities and Members’ Capital.

The Fund from time to time may offer to repurchase Interests pursuant to written tenders by Members. These repurchases will be made at such times, and in such amounts, and on such terms as may be determined by the Board, in its sole discretion. The Investment Manager and the Managing Member expect to typically recommend to the Board that the Fund offer to repurchase Interests from Members of up to 25% of the Fund’s net assets quarterly, effective as of the last day of March, June, September, and December. A 1.5% repurchase fee (the “Repurchase Fee”) payable to the Fund will be charged for repurchases of Members’ Interests at any time prior to the day immediately preceding the one-year anniversary of a Member’s purchase of its Interests. For the year ended March 31, 2012, the Fund charged Repurchase Fees totaling $16,273.

At the end of each Allocation Period of the Fund, any net capital appreciation or net capital depreciation of the Fund (both realized and unrealized), as the case may be, is allocated to the capital accounts of all of the Members (including the Special Member and the Managing Member) in proportion to their respective opening capital account balances for such Allocation Period. The initial “Allocation Period” began on the Initial Closing Date, with each subsequent Allocation Period beginning immediately after the close of the preceding Allocation Period. Each Allocation Period closes on the first to occur of (1) the last day of each month, (2) the date immediately prior to the effective date of (a) the admission of a new Member or (b) an increase in a Member’s capital contribution, (3) the effective date of any repurchase of Interests, or (4) the date when the Fund dissolves.

At the end of each calendar year, each Member’s return on investment for the period in which they were invested in the Fund is determined and a portion of the net capital appreciation allocated to each Member’s capital account during the period (the “Performance Allocation”), net of the Member’s allocable share of the Management Fee and the Manager Administrative Services Fee, equal to 10% of the portion of such net capital appreciation that exceeds the Preferred Return (as defined below) will be reallocated to the capital account of the Special Member. The “Preferred Return” is equal to the 3-month U.S. Treasury Bill yield (as defined below) for each month during the relevant calendar year (or any shorter period of calculation). The “3-month U.S. Treasury Bill yield” for any month shall equal one-twelfth of the annual yield for the 3-month U.S. Treasury Bill for the first business day of the then current calendar quarter as set forth in the U.S. Federal Reserve Statistical Release H.15 (519) under the caption “Treasury constant maturities”, or if such measurement is not available, such other source as the Managing Member may determine appropriate in its discretion.

No Performance Allocation is made, however, with respect to a Member’s capital account until any cumulative net capital depreciation previously allocated to such Member’s capital account plus any Management Fees and Manager Administrative Service Fees charged to such capital account (the “Loss Carryforward”) have been recovered. Any Loss Carryforward of a Member is reduced proportionately to reflect the repurchase of any portion of that Member’s

19

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Notes to Financial Statements March 31, 2012 (continued)

6. Contributions, Redemptions, and Performance Allocation (continued)

Interest. Upon a repurchase of an Interest (other than at the end of a calendar year) from a Member, a Performance Allocation will be determined and allocated to the Special Member, and in the case of any repurchase of a partial Interest, on a “first in - first out” basis (i.e., the portion of the Interest being repurchased and the amount with respect to which the Performance Allocation is calculated) will be deemed to have been taken from the first capital contribution of such Member (as such contribution has been adjusted for net capital appreciation or depreciation, Management Fees, Manager Administrative Services Fees and other expenses) until it is decreased to zero and from each subsequent capital contribution until such contribution (as adjusted) is decreased to zero.

Performance Allocation is earned on a calendar year basis, accrued and presented on the Statement of Changes in Members’ Capital on a fiscal basis. The Performance Allocation for the fiscal year ended March 31, 2011 and the fiscal year ended March 31, 2012 was $1,357,688 and $275,233, respectively. These amounts are reported as Performance Allocation on the Statement of Changes in Members’ Capital.

The Performance Allocation for the fiscal year ended March 31, 2011 is comprised of the amounts noted below:

| | | | | | | | | | | | |

| | | Performance

Allocation Accrual | | | Performance Allocation

on Redemptions | | | Total | |

12/31/2010 | | $ | 578,382 | * | | $ | 2,968 | | | $ | 581,350 | |

3/31/2011 | | $ | 774,034 | | | $ | 2,304 | | | $ | 776,338 | |

| | | | | | | | | | | | |

| | | | | | | | | | $ | 1,357,688 | |

| * | Represents the actual Performance Allocation at the end of the calendar year. |

The Performance Allocation for the fiscal year ended March 31, 2012 is comprised of the amounts noted below:

| | | | | | | | | | | | |

| | | Performance

Allocation Accrual | | | Performance Allocation

on Redemptions | | | Total | |

12/31/2011 | | $ | (774,034 | )** | | $ | 11,221 | | | $ | (762,813 | ) |

3/31/2012 | | $ | 1,026,279 | *** | | $ | 11,767 | | | $ | 1,038,046 | |

| | | | | | | | | | | | |

| | | | | | | | | | $ | 275,233 | |

| ** | Represents the reversal of the prior fiscal year’s accrual, as no actual Performance Allocation occurred. |

| *** | The amount accrued for the period January 1, 2012 to March 31, 2012. This amount is subject to change as actual Performance Allocation occurs at the end of the calendar year. |

20

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Notes to Financial Statements March 31, 2012 (continued)

7. Risk Exposure

In the normal course of business, the Investment Funds (in which the Fund invests) trade various financial instruments and enter into various investment activities with off-balance sheet risk. These include, but are not limited to, short-selling activities, writing option contracts, contracts for differences, and interest rate, credit default and total return equity swaps contracts. The Fund’s risk of loss in these Investment Funds is limited to the value of the Fund’s investments in the Investment Funds.

In pursuing its investment objectives, the Fund invests in Investment Funds that are not registered under the 1940 Act. These Investment Funds may utilize diverse investment strategies, which are not generally managed against traditional investment indices. The Investment Funds selected by the Fund will invest in and actively trade securities and other financial instruments using a variety of strategies and investment techniques that may involve significant risks. Such risks arise from the volatility of the equity, fixed income, commodity and currency markets, leverage both on and off balance sheet associated with borrowings, short sales and derivative instruments, the potential illiquidity of certain instruments including emerging markets, private transactions, derivatives, and counterparty and broker defaults. Various risks are also associated with an investment in the Fund, including risks relating to the multi-manager structure of the Fund, risks relating to compensation arrangements and risks related to limited liquidity of the Interests. The Investment Funds provide for periodic redemptions generally ranging from weekly to annually, and may be subject to various lock-up provisions and early withdrawal fees.

The investments of the Investment Funds are subject to normal market fluctuations and other risks inherent in investing in securities and there can be no assurance that any appreciation in value will occur. The value of investments can fall as well as rise and investors may not realize the amount that they invest.

Although the Investment Manager will seek to select Investment Funds that offer the opportunity to have their shares or units redeemed within a reasonable timeframe, there can be no assurance that the liquidity of the investments of such Investment Funds will always be sufficient to meet redemption requests as, and when, made.

The Investment Manager may invest the Fund’s assets in Investment Funds that invest in illiquid securities and do not permit frequent withdrawals. Illiquid securities owned by Investment Funds are riskier than liquid securities because the Investment Funds may not be able to dispose of the illiquid securities if their investment performance deteriorates, or may be able to dispose of the illiquid securities only at a greatly reduced price. Similarly, the illiquidity of the Investment Funds may cause Members to incur losses because of an inability to withdraw their investments from the Fund during or following periods of negative performance.

The Investment Funds may invest in the securities of foreign companies that involve special risks and considerations not typically associated with investing in U.S. companies. These risks include devaluation of currencies, less reliable information about issuers, different securities transaction clearance and settlement practices, and future adverse political and economic developments. Moreover, securities of many foreign companies and their markets may be less liquid and their prices more volatile than those securities of comparable U.S. companies.

21

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Notes to Financial Statements March 31, 2012 (continued)

8. Indemnifications

In the normal course of business, the Fund enters into contracts that contain a variety of representations that provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, the Fund expects the risk of loss to be remote.

9. Concentrations

An affiliate of the Fund’s Investment Manager has investment discretion with respect to their client’s holdings in the Fund, which collectively represent a significant portion of the Fund’s assets. Significant Member transactions, if any, may impact the Fund’s performance.

10. Commitments

At March 31, 2012, the Fund had made no redemption requests from underlying Investment Funds and made the following commitments to purchase Investment Funds:

| | | | |

| Investment Fund | | Amount | |

Standard Global Equity Partners SA, L.P. | | $ | 4,000,000 | |

Corvex Partners, L.P. | | | 9,000,000 | |

| | | | |

Total | | $ | 13,000,000 | |

| | | | |

22

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Directors and Officers Biographical Data (unaudited)

The business of the Fund is managed under the direction of the Board of Directors. Subject to the provisions of the operating agreement and Delaware law, the Directors have all powers necessary and convenient to carry out this responsibility. The Directors and officers of the Fund, their ages and descriptions of their principal occupations during the past five years are listed below.

| | | | | | |

Name (Year of Birth)

Positions With

The Fund | | Principal Occupation(s) During

the Past 5 Years | | Number of

Portfolios in

Fund Complex

Overseen by

Director(1) | | Other Directorships Held

by Director |

Independent Directors | | | | | | |

| | | |

William J. Armstrong (1941);

Director since 2010. | | Retired; CFO and Consultant, EduNeering, Inc. (internet business education supplier) (2000—2001); Vice President and Treasurer, Ingersoll-Rand Company (manufacturer of industrial equipment) (1972—2000). | | 167 | | None. |

| | | |

John F. Finn (1947);

Director since 2010. | | Chairman (1985-present), President and Chief Executive Officer, Gardner, Inc. (supply chain management company serving industrial and consumer markets) (1974—present). | | 167 | | Director, Cardinal Health, Inc (CAH) (1994—present); Director, Greif, Inc. (GEF) (industrial package products and services) (2007-present). |

| | | |

Dr. Matthew Goldstein (1941);

Director since 2010. | | Chancellor, City University of New York (1999—present); President, Adelphi University (New York) (1998—1999). | | 167 | | Director, New Plan Excel (NXL) (1999-2005); Director, National Financial Partners (NFP) (2003-2005); Director, Bronx-Lebanon Hospital Center; Director, United Way of New York City (2002-present). |

| | | |

Robert J. Higgins (1945);

Director since 2010. | | Retired; Director of Administration of the State of Rhode Island (2003—2004); President — Consumer Banking and Investment Services, Fleet Boston Financial (1971—2001). | | 167 | | None. |

| | | |

Peter C. Marshall (1942);

Director since 2010. | | Self-employed business consultant (2002—present). | | 167 | | Director, Center for Communication, Hearing and Deafness (1990-present). |

23

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Directors and Officers Biographical Data (unaudited) (continued)

| | | | | | |

Name (Year of Birth)

Positions With

The Fund | | Principal Occupation(s) During

the Past 5 Years | | Number of

Portfolios in

Fund Complex

Overseen by

Director(1) | | Other Directorships Held

by Director |

Independent Directors | | | | | | |

| | | |

Marilyn McCoy* (1948);

Director since 2010. | | Vice President of Administration and Planning, Northwestern University (1985—present). | | 167 | | Trustee, Carleton College (2003—present). |

| | | |

William G. Morton, Jr. (1937);

Director since 2010. | | Retired; Chairman Emeritus (2001— 2002), and Chairman and Chief Executive Officer, Boston Stock Exchange (1985— 2001). | | 167 | | Director, Radio Shack Corp.

(1987-2008); Trustee, Stratton Mountain School (2001—present). |

| | | |

Dr. Robert A. Oden, Jr. (1946);

Director since 2010. | | Retired; President, Carleton College (2002—2010); President, Kenyon College (1995—2002). | | 167 | | Trustee, American University in Cairo (1999-present); Trustee, Dartmouth-Hitchcock Medical Center (2011-present); Trustee, American Schools of Oriental Research (2011-present); Trustee, Carleton College (2002- 2010). |

| | | |

Fergus Reid, III (1932);

Director since 2010. | | Chairman, Joe Pietryka Inc. (formerly, Lumelite Corporation) (plastics manufacturing) (2003—present); Chairman and Chief Executive Officer, Lumelite Corporation (1985—2002). | | 167 | | Trustee, Morgan Stanley Funds (107 portfolios) (1992—present). |

| | | |

Frederick W. Ruebeck (1939);

Director since 2010. | | Consultant (2000-present); Advisor, JP Greene & Associates, LLC (broker-dealer) (2000—2009); Chief Investment Officer, Wabash College (2004— present); Director of Investments, Eli Lilly and Company (pharmaceuticals) (1988—1999). | | 167 | | Trustee, Wabash College (1988—present); Chairman, Indianapolis Symphony Orchestra Foundation (1994—present). |

| | | |

James J. Schonbachler (1943);

Director since 2010. | | Retired; Managing Director of Bankers Trust Company (financial services) (1968—1998). | | 167 | | None. |

24

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Directors and Officers Biographical Data (unaudited) (continued)

| | | | | | |

Name (Year of Birth)

Positions With

The Fund | | Principal Occupation(s) During

the Past 5 Years | | Number of

Portfolios in

Fund Complex

Overseen by

Director(1) | | Other Directorships Held

by Director |

Interested Directors | | | | | | |

| | | |

Frankie D. Hughes ** (1952);

Director since 2010. | | President and Chief Investment Officer, Hughes Capital Management, Inc. (fixed income asset management) (1993-present). | | 167 | | Trustee, The Victory Portfolios (2000-2008). |

| | | |

| Leonard M. Spalding, Jr. *** (1935); Director since 2010. | | Retired; Chief Executive Officer, Chase Mutual Funds (investment company) (1989—1998); President and Chief Executive Officer, Vista Capital Management (investment management) (1990—1998); Chief Investment Executive, Chase Manhattan Private Bank (investment management) (1990—1998). | | 167 | | Director, Glenview Trust Company, LLC (2001—present); Trustee, St. Catharine College (1998—present); Trustee, Bellarmine University (2000—present); Director, Springfield- Washington County Economic Development Authority (1997—present). |

| (1) | A Fund Complex means two or more registered investment companies that hold themselves out to investors as related companies for purposes of investment and investor services or have a common investment adviser or have an investment adviser that is an affiliated person of the investment adviser of any of the other registered investment companies. The J.P. Morgan Funds Complex for which the Board of Directors serves currently includes eleven registered investment companies (167 funds). |

| * | Ms. McCoy has served as Vice President of Administration and Planning for Northwestern University since 1985. William M. Daley was the Head of Corporate Responsibility for JPMorgan Chase & Co. prior to January 2011 and served as a member of the Board of Trustees of Northwestern University from 2005 through 2010. JPMIM, the Funds’ investment adviser, is a wholly-owned subsidiary of JPMorgan Chase & Co. Three other members of the Board of Trustees of Northwestern University are executive officers of registered investment advisers (not affiliated with JPMorgan) that are under common control with subadvisers to certain J.P. Morgan Funds. |

| ** | Ms. Hughes is treated as an “interested person” based on the portfolio holdings of clients of Hughes Capital Management, Inc. |

| *** | Mr. Spalding is treated as an “interested person” due to his ownership of JPMorgan Chase stock. |

Each Director serves for an indefinite term, subject to the Fund’s current retirement policy, which is age 75 for all Directors, except that the Board has determined Messrs. Reid and Spalding should continue to serve until December 31, 2012. The Board of Directors decides upon general policies and is responsible for overseeing the business affairs of the Fund.

The contact address for each of the Directors is 270 Park Avenue, New York, NY 10017.

25

J.P. Morgan Access Multi-Strategy Fund, L.L.C.

Directors and Officers Biographical Data (unaudited) (continued)

| | |

Name (Year of Birth),

Positions Held with the Fund | | Principal Occupation(s) During the Past

5 Years |

Officers | | |

| |

Patricia A. Maleski (1960);

President and Chief Administrative Officer (2010) Principal Executive Officer | | Managing Director, J.P. Morgan Investment Management Inc. and Chief Administrative Officer, J.P. Morgan Funds and Institutional Pooled Vehicles since 2010; previously, Treasurer and Principal Financial Officer of the Trusts from 2008 to 2010; previously, Head of Funds Administration and Board Liaison, J.P. Morgan Funds prior to 2010. Ms. Maleski has been with JPMorgan Chase & Co. since 2001. |

| |

Joy C. Dowd (1972);

Treasurer and Principal Financial Officer (2010) | | Assistant Treasurer of the Trusts from 2009 to 2010; Executive Director, JPMorgan Funds Management, Inc. from February 2011; Vice President, JPMorgan Funds Management, Inc. from December 2008 to February 2011; prior to joining JPMorgan Chase, Ms. Dowd worked in MetLife’s investments audit group from 2005 through 2008. |

| |

Frank J. Nasta (1964);

Secretary (2010) | | Managing Director and Associate General Counsel, JPMorgan Chase since 2008; Previously, Director, Managing Director, General Counsel and Corporate Secretary, J. & W. Seligman & Co. Incorporated; Secretary of each of the investment companies of the Seligman Group of Funds and Seligman Data Corp.; Director and Corporate Secretary, Seligman Advisors, Inc. and Seligman Services, Inc. |

| |

Stephen M. Ungerman (1953);

Chief Compliance Officer (2010) | | Managing Director, JPMorgan Chase & Co.; Mr. Ungerman has been with JPMorgan Chase & Co. since 2000. |

| |

Elizabeth A. Davin (1964);

Assistant Secretary (2010)* | | Executive Director and Assistant General Counsel, JPMorgan Chase since 2005; Senior Counsel, JPMorgan Chase (formerly Bank One Corporation) from 2004 to 2005. |

| |

Jessica K. Ditullio (1962);

Assistant Secretary (2010)* | | Executive Director and Assistant General Counsel, JPMorgan Chase since February, 2011; Ms. Ditullio has served as an attorney with various titles for JPMorgan Chase (formerly Bank One Corporation) since 1990. |

| |

John T. Fitzgerald (1975);

Assistant Secretary (2010) | | Executive Director and Assistant General Counsel, JPMorgan Chase since February 2011; formerly, Vice President and Assistant General Counsel, JPMorgan Chase from 2005 until February 2011. |

| |

Gregory S. Samuels (1980);

Assistant Secretary (2010) | | Vice President and Assistant General Counsel, JPMorgan Chase since 2010; Associate, Ropes & Gray (law firm) from 2008 to 2010; Associate, Clifford Chance LLP (law firm) from 2005 to 2008. |

| |

Brian L. Duncan (1965);

Assistant Treasurer (2010)* | | Vice President, JPMorgan Funds Management, Inc. since June 2007; prior to joining JPMorgan Chase, Mr. Duncan worked for Penn Treaty American Corporation as Vice President and Controller from 2004 through 2007. |

| |

Jeffrey D. House (1972);

Assistant Treasurer (2010)* | | Vice President, JPMorgan Funds Management, Inc. since July 2006. |

| |

Joseph Parascondola (1963);

Assistant Treasurer (2011) | | Vice President, JPMorgan Funds Management, Inc. since August 2006. |

| |

Matthew J. Plastina (1970);

Assistant Tresurer (2011) | | Vice President, JPMorgan Funds Management, Inc. since August 2010; prior to August 2010, Vice President and Controller, Legg Mason Global Asset Management. |

| |