March 15, 2010

Via Edgar and Federal Express

John Hartz Senior Assistant Chief Accountant Division of Corporation Finance Securities and Exchange Commission 100 F Street, N.E. Washington, DC 20549-4631 |

| Re: | China Architectural Engineering, Inc. |

| Form 10-K for the Fiscal Year Ended December 31, 2008 |

| Definitive Proxy Statement on Schedule 14A filed April 30, 2009 |

| File No. 000-23539 |

| Form 10-Q for the Fiscal Quarter Ended March 31, 2009 |

| Form 10-Q for the Fiscal Quarter Ended June 30, 2009 |

| Form 10-Q for the Fiscal Quarter Ended September 30, 2009 |

| File No. 001-33709 |

Ladies and Gentlemen:

On behalf of China Architectural Engineering, Inc., a Delaware corporation (the “Company”), the undersigned is hereby providing the Company’s responses to the Securities and Exchange Commission comment letter dated February 22, 2010. The Company’s responses to the Staff’s comment letter, below, are in identical numerical sequence to the Commission comment letter, and each comment is repeated verbatim with the Company’s response immediately following.

General

| 1. | Comment: We note that you have not provided the Tandy language requested in our previous comment letter. In this regard, please provide us with the following statements, in writing, as signed by an employee of your company, acknowledging that: |

| · | the company is responsible for the adequacy and accuracy of the disclosure in their filings; |

| · | staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the filing; and |

| · | the company may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States. |

Response: The Company respectfully notes your comment and has included the Tandy representations in the concluding paragraphs of this letter. |

Mr. John Hartz

March 15, 2010

Page 2

Form 10-K for the Fiscal Year Ended December 31, 2008

Item 7. Management’s Discussion and Analysis of Financial Condition acid Results of Operations, page 26

Critical Accounting Policies, Estimates and Assumptions, page 27 Selling, General, And Administrative Costs, page 27

| 2. | Comment: We appreciate your response to prior comment 5; however, we are unclear as to how you determined this treatment was appropriate. In this regard, please tell us how your policy complies with the guidance in FASB ASC 605-35-45-1. Additionally, please tell us how much allowance for estimated losses on uncompleted contracts was charged to your income statement during the fiscal years ended 2007, 2008 and through the nine months ended September 30, 2009. |

Response: The Company respectfully note your comment and the Company hereby confirms that it, in accordance with ASC 605-35-45-1, includes allowances for estimated losses on uncompleted contracts in its costs of contract revenues, and the Company has never included allowances for estimated losses on uncompleted contracts in selling, general and administrative costs. |

Prior to the year ended December 31, 2009, there were no material estimated losses on uncompleted contracts according to the Company’s contract budget review process.

In 2009, as a result of the increased costs in the PRC, where the materials were procured, and the global economic recession, clients permitted a decreased margin charge as compared to previous years. As a result, there were estimated losses on uncompleted contracts identified and charged to the costs of contract revenues in the Company’s income statement. A substantial majority of this charge resulted from a project in Doha of Middle East, which revealed an estimated loss of approximately $3.8 million and the full amount of loss was charged to the income statement as costs of revenue earned in the year ended December 31, 2009.

The Company will revise its future filings to clarify and quantify its critical accounting policy with respect to allowances for estimated losses on uncompleted contracts as described above.

Item 8. Financial Statements, page F-1

General

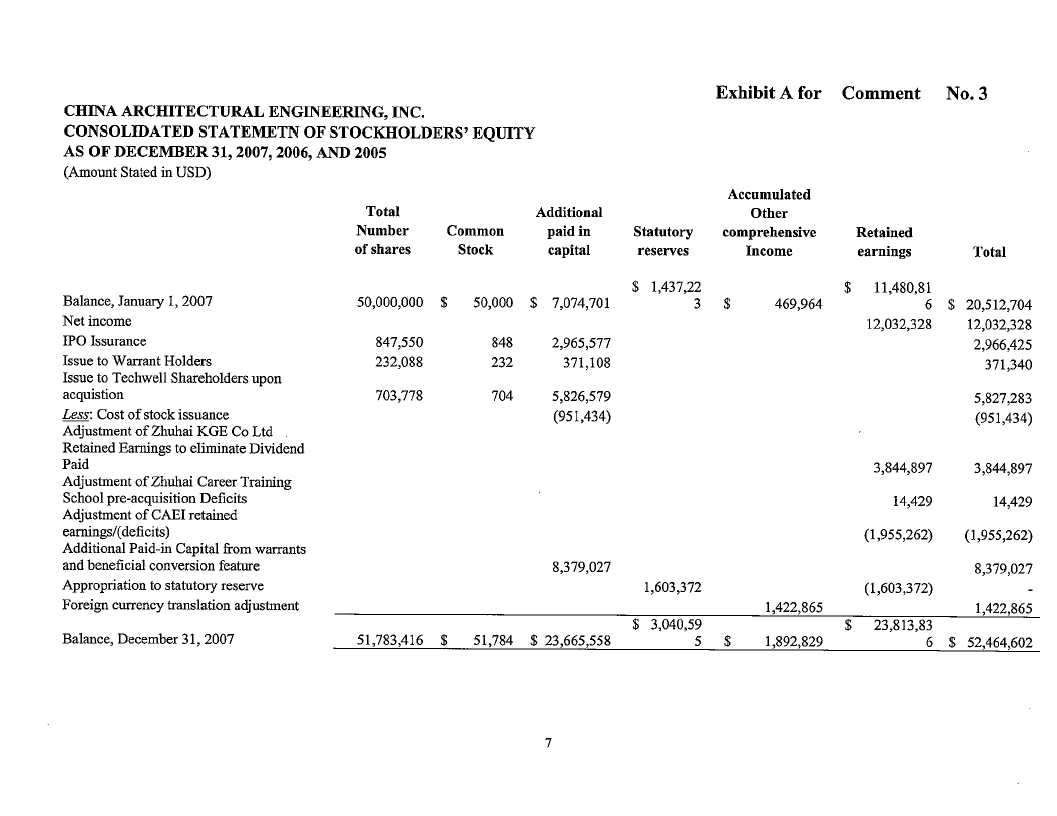

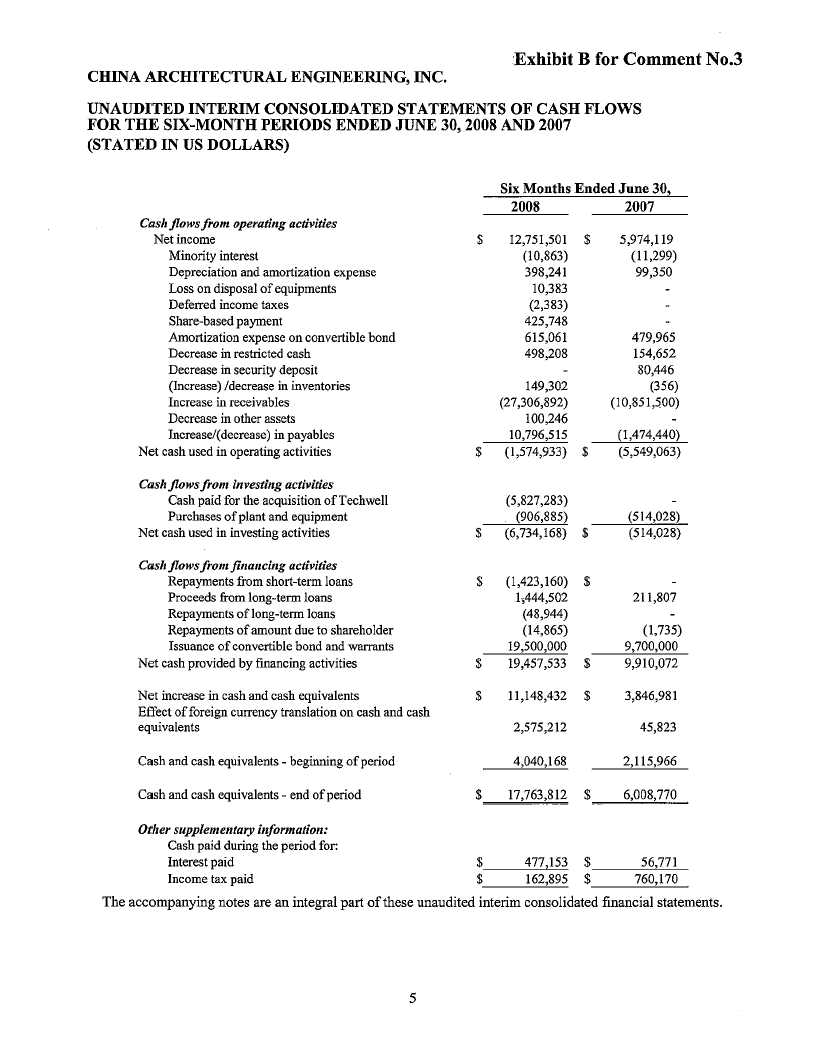

| 3. | Comment: We note your response to prior comment 8. Please tell us what consideration you have given to showing the issuance of shares for the Techwell acquisition as a separate line item on your statements of shareholders’ equity and reclassifying the cash portion of the transaction to cash used for investing activities in your statements of cash flows. |

Response: The Company respectfully notes your comment and has reviewed the treatment of the Techwell acquisition in the Company’s statements of cash flows. The acquisition of Techwell Engineering Ltd. on November 6, 2007 was consummated at an aggregate purchase price of $11,654,561, payable by equal proportion of cash in the amount $5,827,283 and issue of 703,778 CAEI shares possessing a value of $5,827,283. |

For the purpose of clarifying disclosure of 703,778 shares of the Company’s common stock issued to the previous shareholders of Techwell upon acquisition, the Company intends to revise the Statements of Stockholders’ Equity, including related footnotes, contained in future filings to reflect the Techwell acquisition as a separate line item. Please see Exhibit A attached hereto as a reference to the nature of the revisions. For the purpose of clarifying disclosure of the cash portion of purchase price $5,827,283, the Company intends to revise the Statements of Cash Flows, including related footnotes, contained in future filings to reflect the cash paid under investing activities. Please see Exhibit B attached hereto as a reference to the nature of the revisions. |

Mr. John Hartz

March 15, 2010

Page 3

Note 8 - Convertible Bonds and Bond Warrants, page F-24

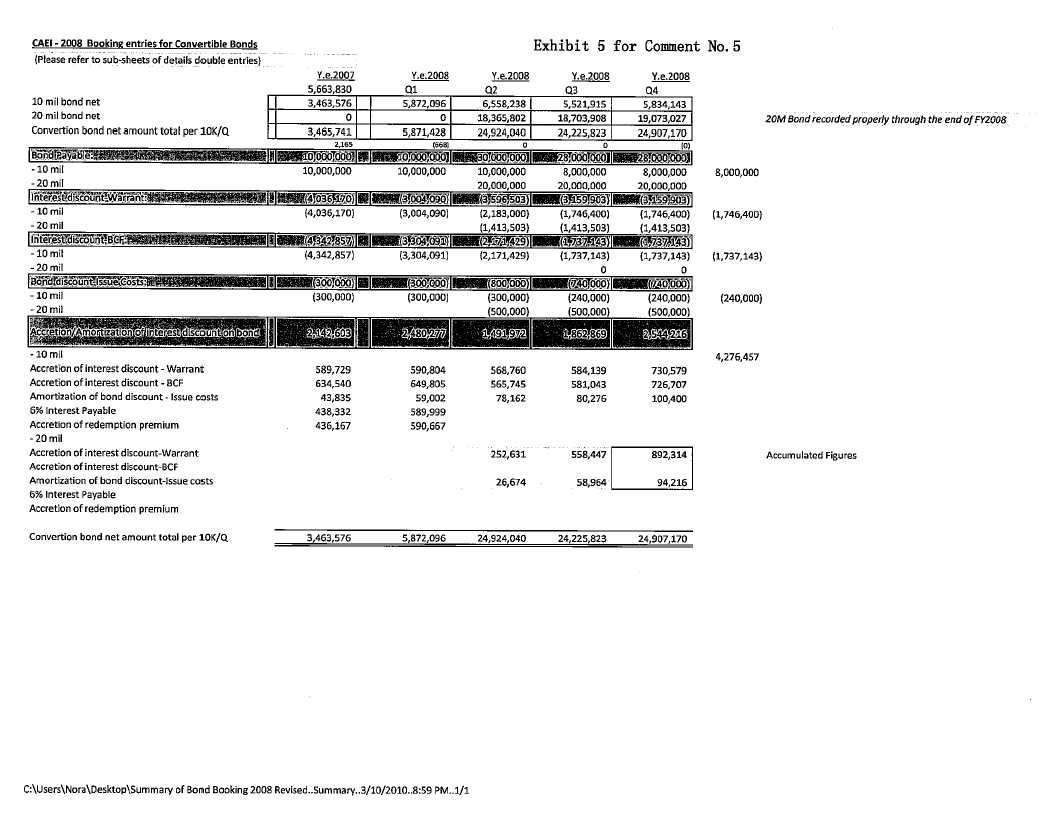

| 4. | Comment: We appreciate your response to prior comment 11; however, we are still unclear as to why the interest discount for your beneficial conversion feature decreased from $4,342,857 at December 31, 2007 to $1,737,143 at December 31, 2008. In this regard, please supplementally provide us with a detail of the amortization of the beneficial conversion feature for fiscal 2007 and 2008. In addition, we note from your statement of stockholders’ equity that you recognized a $2.6 million reduction to additional paid in capital from warrants and beneficial conversion feature. Please explain the nature of this item to us. |

Response: The Company respectfully notes your comment and hereby supplementally provides the requested information. |

a. Amortization of BCF. As more fully described in the Company's response to Comments No. 8, below, the beneficial conversion feature, or "BCF", is treated as an equity instrument and considered a bond discount and amortized over the first period of convertibility. The following is a table showing the movement of bond discount – BCF from December 31, 2007 to December 31, 2008:

Bond Discount - BCF

b. Reduction to Additional Paid In Capital. The $2.6 million reduction to additional paid in capital from warrants and BCF attributed to corrections made to these two accounts per total corrections shown above.

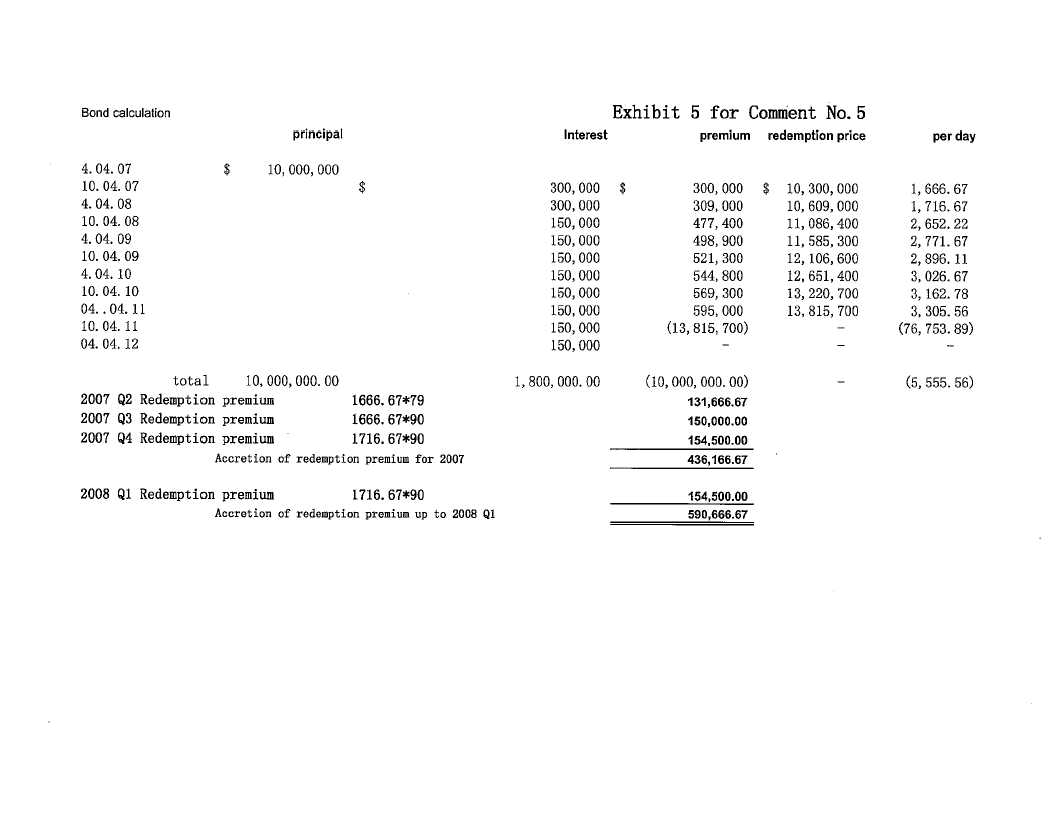

| 5. | Comment: We appreciate your response to prior comment 12 in regard to the details of the accretion of interest discount and accrual of interest payable disclosed on page F-29. Please tell us why the 6% interest payable and the accretion of redemption premium is the same amount on your Exhibit 5 included in your response. |

Response: The Company respectfully notes your comment and supplementally informs you that, upon further review of the calculation worksheets, the Company noted a minor discrepancy in determining the amount of accretion of redemption premium which is $436,167 and is not the same amount as the 6% interest payable of $438,332 at December 31, 2007. Accordingly, the accretion of redemption premium for first quarter of 2008 would be $590,667. The worksheet, as revised, is attached hereto as Exhibit 5. |

Mr. John Hartz

March 15, 2010

Page 4

Note 11 - Commitments and Contingencies, page F-32

B. Pending Litigation, page F-32

| 6. | Comment: We note your responses to our prior comments 13 and 14. Please revise future filings to disclose the following: |

| • | Your belief, if true, that the outcome of the Techwell lawsuit will not have a material adverse impact on your financial condition, results of operations or liquidity. | |

| • | The fact that the Dubai Project was the primary focus of Techwell. | |

| • | The impact of the Dubai Project on your results in each period presented. | |

| • | The fact that the Dubai Project is complete at the end of 2009. |

Response: We respectfully note your comment and the Company confirms that it will include the aforementioned items of disclosure in future filings. |

Please note that the Company has provided the following additional related disclosures in its Annual Report on Form 10-K for fiscal 2009 that was filed with the Commission on March 4, 2010:

| (a) | On pages 17 and 29, the Company disclosed the amount of profit contribution from Techwell that would be lost if the Company would lose in this case and that the project was 95% complete, as follows: “In the event we lose ownership of Techwell, we will lose the approximately $17.3 million of profit contribution since the acquisition of Techwell.” “With less than 5% of its contract remaining to be completed, Techwell was removed by the master contractor of the project, which also called for and received payment of $2.1 million in performance bonds and $7.3 million in advance payment bonds that were issued on Techwell's behalf for the project.” |

| (b) | On pages 11 and 29, the Company disclosed that Techwell is the means through which the Company was conducting the Dubai project. |

| (c) | On pages 5 and 39, the Company disclosed the percentage of the Company’s total contract revenues in 2009 for which the Dubai project accounted and that no similar projects will be conducted in 2010, as follows: “During 2009, we completed approximately 37 projects, with our three largest projects being the Dubai Metro Red Line, Guangdong Science City Headquarter Phase I, and Doha High Rise Office Tower, which accounted for approximately 43.2 %, 9.2 % and 7.0% of our contract revenues, respectively, for the year ended December 31, 2009. We do not expect to engage in international projects in 2010.” |

In addition to the foregoing, the Company undertakes to, prior to each filing, provide additional clarifying disclosures and conduct an evaluation of the current status of the Techwell litigation and update and revise the disclosures regarding whether the Company continues to believe that the outcome of the Techwell lawsuit will not have a material adverse impact on its financial condition, results of operations or liquidity.

Mr. John Hartz

March 15, 2010

Page 5

Form 10-Q for the Fiscal Quarter Ended September 30, 2009

Item 1. Financial Statements, page 1

Note 2 - Summary of Significant Accounting Policies, page 7

(f) Goodwill and intangible Assets, page 8

| 7. | Comment: To the extent that any of your reporting units have estimated fair values that are not substantially in excess of the carrying value and to the extent that goodwill for these reporting units, in the aggregate or individually, if impaired, could materially impact your operating results or total shareholders’ equity, please provide the following disclosures for each of these reporting units in future filings: |

| · | Identify each individual and applicable reporting unit. |

| · | The percentage by which fair value exceeds carrying value as of the most recent step-one test. |

| · | A description of the material assumptions that drive estimated fair value. |

| · | A discussion of any uncertainties associated with each key assumptions. |

| · | A discussion of any potential events, trends and/or circumstances that could have a negative effect on estimated fair value. |

If you have determined that estimated fair value substantially exceeds carrying values or your reporting unit, please disclose that determination. Refer to Item 303 of Regulation S-K.

Response: The Company respectfully notes your comment and confirms that it will provide the referenced disclosures for each of its reporting units in future filings to the extent that any of its reporting units have estimated fair values that are not substantially in excess of the carrying value and to the extent that goodwill for these reporting units, in the aggregate or individually, if impaired, could materially impact your operating results or total shareholders’ equity. |

The Company notes that it has added a Risk Factor on page 15 of the Annual Report on Form 10-K disclosing the risks related to potential impairment of the Company’s goodwill, as follows:

A decline in our stock price and market capitalization, such as our stock price decline in 2009, could result in an impairment of a material amount of our goodwill, which could reduce our earnings. Goodwill may be impaired if the estimated fair value of one or more of our reporting units’ goodwill is less than the carrying value of the unit’s goodwill. In 2007, we acquired Techwell Engineering, and its accordingly recorded goodwill assets in the amount of approximately $8.0 million, which represents a significant portion of our assets. We perform an analysis on our goodwill balances to test for impairment on an annual basis and whenever events occur that indicate an impairment could exist. There are several instances that may cause us to further test our goodwill for impairment between the annual testing periods including: (i) continued deterioration of market and economic conditions that may adversely impact our ability to meet our projected results; (ii) declines in our stock price caused by continued volatility in the financial markets that may result in increases in our weighted-average cost of capital or other inputs to our goodwill assessment; (iii) the occurrence of events that may reduce the fair value of a reporting unit below its carrying amount, such as the sale of a significant portion of one or more of our reporting units.

Our impairment review did not indicate an impairment of the goodwill, however while this review indicated that the estimated fair value exceeded the carrying value of goodwill, it is reasonably possible that changes in the numerous variables associated with the judgments, assumptions and estimates we made in assessing the fair value of our goodwill, could cause the respective value of this or other reporting units to become impaired. If our goodwill is impaired, we would be required to record a non-cash charge that could have a material adverse effect on our condensed consolidated financial statements.”

Mr. John Hartz

March 15, 2010

Page 6

In addition, please note the following information for which the Company intends to add to future filings as required:

| a. The Company’s goodwill is fully attributable to a subsidiary, Techwell. |

| b. As of December 31, 2009, based on calculations conducted by the Company, the fair value exceeds carrying value by approximately 22%. |

c. Material assumptions include: (1) The reporting unit continues to have the profitable operations for a period of next 10 years; (2) the revenue has the steady annual growth rate ranging from 5% to 8% as in line with the estimated growth rate of PRC economy as the unit will transition into conducting projects in the PRC and Hong Kong; (3) costs of funds kept stable for the period of next 10 years resulting in a stable discount rate for the projection of estimated fair value; and (4) no material change in the prevailing payment terms of the construction industry that allowing the working capital requirement kept at a low level at 15%. |

| d. Uncertainties include: (1) The ability of the reporting unit to continue as a profitable operation may be affected by changes in technologies and the market of the construction industry; (2) the growth of the PRC economy may not be as steady as projected that in turn affect the steady growth of the revenue of the reporting unit, (3) it is also uncertain about the capital market that affect the costs of fund of the company; and (4) the prevailing payment terms used in the construction industry may be changed as a result of changes in the business environment for the construction industry. |

| e. Potential events include (1) the appreciation of the value of RMB that would slow down the export and in turn the economic development of China that in turn have negative effect of property development industry in China; and (2) the controlling policies towards the property market by the PRC government. |

Note 8 - Convertible Bonds and Bond Warrants, page 16

| 8. | Comment: We note your response to our prior comment 15. Please tell us how you have considered EITF 07-5 and ASC 815-10-65-3 in determining whether the conversion option needs to be classified as a liability and fair valued every reporting period. |

Response: The Company respectfully notes your comment and supplementally provides to you its considerations of the accounting literature in relation to the determination that the conversion option is not required to be classified as a liability and fair valued every reporting period. |

The beneficial conversion feature (“BCF”) is treated as an equity instrument and considered a bond discount and amortized over the first period of convertibility. SFAS 133 paragraph 11 provides that “notwithstanding the conditions of paragraphs 6-10, the reporting entity shall not consider the following contracts to be derivative instruments for purposes of this statement: a) Contracts issued or held by that reporting entity that are both (1) indexed to its own stock and (2) classified in stockholders’ equity in its statement of financial position.”

The instrument, BCF, is not indexed to anything other than the Company’s own stock. It is not indexed to another observable market index. The number of shares issuable upon conversion of debt is controlled by variables all related to the fair value of the instrument. Therefore, the Company is not subject to SFAS 133 Accounting for Derivations. The Company has taken into the further clarifications as provided by EITF 07-5 and ASC 815-10-65-3 (Implementation rules and timeline). After consideration of the accounting rules, as discussed above, the Company determined that the conversion option does not require to be classified as a liability.

Note 11 - Discontinued Operation Loss, page 18

Mr. John Hartz

March 15, 2010

Page 7

| 9. | Comment: Please provide us with a specific and comprehensive discussion of how you determined that it was appropriate to treat the Shenzhen office’s downsize and move to a smaller office as a discontinued operation. See FASB ASC 205-20-45 and FASB ASC 420-10-05 for guidance. |

Response: The Company respectfully notes your comment and hereby provides information regarding the determination of the accounting treatment for the Company’s discontinued operations. The Company’s accounting policies recognize discontinued operations in accordance with ASC 205-20-45 and ASC 420-10-05. The operation was reported discontinued as the operation and its cash flows will be eliminated from the ongoing operations of the company and the company will not have any significant continuing involvement in the operations of the discontinued component. The costs associated with the disposal were accounted for in accordance to the disposal costs obligations guidance as specified under the standards.] |

In September 2009, the original Shenzhen Office was abandoned and discontinued operation. The purpose of the original Shenzhen office was design and engineering support services to the Company’s international projects. A new, smaller sized Shenzhen Office was set-up to serve the domestic market in China. The Company believes that the Discontinued Operation Loss of $1.9 million was properly presented in the income statement in compliance of FASB ASC 205-200 45 and 420-10-05 because the downsize of Shenzhen office was properly considered as the discontinued operation as (1) there was no operations and cash flows regarding the ceased operation in the office, i.e. design and engineering support services to the international projects after the Company restructured to focus back to domestic market in PRC and (2) the new, small size Shenzhen office has no significant involvement in the ceased operation, i.e. no more significant support services to international projects.

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations, page 22

Results of Operations, page 25

| 10. | Comment: We appreciate your response to prior comment 6 and remind you to quantify, in future filings, the reasons for the changes in your results from period-to period. |

Response: We respectfully note your comment and the Company confirms that it will quantify, in future filings, the reasons for the changes in its results of operations from period-to period, commencing with the Annual Report on Form 10-K for fiscal 2009. |

Liquidity and Capital Resources, page 27

| 11. | Comment: With a view towards future disclosure, please provide us with a more specific and comprehensive discussion regarding the timing of collections your accounts receivable balance. We note your disclosures on page 29 that your settlement period can be as high as one year. However, given that your contract receivables balance at September 30, 2009 is almost as large your contract revenues earned during the nine months then ended, we believe additional information should be provided. Such information should include, but not be limited to, the underlying contracts representing the receivables, the aging of the receivables, when you expect to collect payment and any significant payment events that occurred subsequent to your balance sheet date. |

Response: The Company respectfully notes your comment and, with respect towards expanding disclosures in the Company’s future filings, the Company hereby provides additional information regarding the timing of collection of account receivable balances. Below are the details and normal timing of the Company’s collection of accounts receivables, which may vary in on a case-by-case basis. |

(a) It takes approximately one month for our client to collect the payment application from contractors for the contract work completed.

Mr. John Hartz

March 15, 2010

Page 8

(b) Thereafter, it takes approximately one to two months for the verification, agreement and certification of work completed, with timing to largely depend on whether there is disagreement in the calculation of certified value between the parties.

(c) Moreover, if it is the case that the application is to finalize the project account, it may take up to three months.

(d) Additionally, in the event that the client is not the owner of the project, it normally requires an additional one to two months for processing and obtaining the funds from the owner.

(e) One to two months the client to pay the contractors.

As a result of the summary above, these processes exhibit that the period of receivable collection may range from three months up to one year.

More specifically, one of the causes for the increase in contract receivables is the delay in payment by client of the Dubai projects since April 2009. The underlying receivable as of September 30, 2009 from the Dubai projects was equal to $19.2 million, which represented 23% of the total contract receivables as of such date. The Company has employed a claim consultant, Hill International, to facilitate the Company’s claim for the back payment. The Company currently expects that there will be progress and payments will be received as early as the third quarter of 2010.

In addition to the foregoing, the Company hereby supplementally provides in Appendix A, attached hereto, additional information as of December 31, 2009 in tabular format with respect to the Company’s largest account receivables, including information pertaining to the underlying contracts representing the receivables, the portioned aging of the contract receivables, and expected collection dates.

The Company undertakes to expand disclosures in future filings to take into account the above information, in addition to any significant payment events that occurred subsequent to your balance sheet date.

Further to our response to Comment No. 1, the undersigned, on behalf of the Company, hereby acknowledges and agrees that:

| • | the Company is responsible for the adequacy and accuracy of the disclosure in its filings; |

| • | staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the filing; and |

| • | the Company may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States. |

Mr. John Hartz

March 15, 2010

Page 9

Please do not hesitate to contact Anh Q. Tran, Esq. of K&L Gates, LLP, company counsel, at (310) 552-5083, with any questions regarding the matters discussed in this letter.

Sincerely,

/s/ Luo Ken Yi

Luo Ken Yi

Chief Executive Officer

and Chairman of the Board

| cc: | Dale Welcome, U.S. Securities and Exchange Commission Anh Q. Tran, K&L Gates, LLP |

| APPENDIX A |

| Aging of the Receivables | ||||||||||||||||||||

Contracts | Dollar amount of receivable($) | Percentage of ARs Outstanding | 1-30 days | 31-60 days | 61-90 days | 91-120 days | 121-365 days | Over 365 days | Over 730 days | Expected collection date (Over the time period stated below re Note 2) | ||||||||||

| 1. Dubai Contracts | $42,110,046 | 43.94% | $42,110,046 | Within 9 months | ||||||||||||||||

| 2. International Race Course Phase II, Wuhan | 4,262,705 | 4.45% | 3,354,749 | 294,127 | 613,829 | Within 3 to 12 months | ||||||||||||||

| 3. National Theatre, Guangzhou City | 3,349,582 | 3.50% | 3,349,582 | Within 1 to 12 months | ||||||||||||||||

| 4. Guangdong Science City Headquarter Phase I | 2,958,564 | 3.09% | 133,135 | 1,017,746 | 1,535,495 | 272,188 | Within 1 to 12 months | |||||||||||||

| 5. Receivables equal or over $1 million (11 nos.) | 14,494,698 | 15.13% | 1,782,848 | 420,346 | 1,884,311 | 5,421,017 | 4,986,176 | Within 3 to 12 months | ||||||||||||

| 6. Receivables below $1 million (around 160 nos.) | 28,655,894 | 29.90% | 1,576,074 | 1,146,236 | 916,989 | 487,150 | 5,387,308 | 8,052,306 | 11,089,831 | Within 3 to 12 months | ||||||||||

| Total | $95,831,489 | 100% | $52,306,434 | $2,163,982 | $2,452,484 | $1,473,811 | $7,885,448 | $13,473,323 | $16,076,007 | |||||||||||

| 54.6% | 2.3% | 2.6% | 1.5% | 8.2% | 14.1%, (Included retention money, re note 1 below) | 16.7% (Included retention money, re note 1 below) | ||||||||||||||

Note 1 - Among the receivables outstanding over 365 days and 730 days of $29,549,330 (30.8%), including $10,600,842 (11.1%) of retention money which would only be settled after the retention periods of two or three years. |

Note 2- As of the nature of contract income which accumulates the receivables over a period of time (e.g., with monthly certification of work completed but payment being after 3 to 12 months), the settlement of the accumulated receivables will be spread over a period of time (e.g., over one to 12 months with settlement of the earliest certified work completed first, then the next earliest, then the next earliest, and so forth). |