UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 30, 2006

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 000-50845

MCCORMICK & SCHMICK’S SEAFOOD RESTAURANTS, INC.

(Exact Name of Registrant as Specified in its Charter)

| | |

| Delaware | | 20-1193199 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S Employer Identification No.) |

| | |

| |

| 720 SW Washington Street, Suite 550 Portland, Oregon | | 97205 |

| (Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code: (503) 226-3440

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, par value $0.001 per share

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark whether the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (Section 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| | | | |

Large accelerated filer ¨ | | Accelerated filer x | | Non-accelerated filer ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the voting and non-voting common stock held by non-affiliates (based on the closing price on December 30, 2006 on The Nasdaq Stock Market Global Market) was $225,072,336. There were 14,481,718 shares of common stock outstanding as of February 27, 2007.

DOCUMENTS INCORPORATED BY REFERENCE

Part III of this Form 10-K incorporates by reference information from the registrant’s Proxy Statement for the 2007 Annual Meeting of Stockholders.

TABLE OF CONTENTS

i

Forward Looking Statements

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Forward-looking statements represent our expectations or beliefs concerning future events, including the following: any statements regarding future sales, costs and expenses and gross profit percentages; any statements regarding the continuation of historical trends; any statements regarding the expected number of future restaurant openings and expected capital expenditures; and any statements regarding the sufficiency of our cash balances and cash generated from operating and financing activities for future liquidity and capital resource needs. In addition, the words “believes,” “anticipates,” “plans,” “expects,” “should,” “estimates” and similar expressions are intended to identify forward-looking statements. We have identified significant factors that could cause actual results to differ materially from those stated or implied in the forward-looking statements in Item 1A, “Risk Factors.”

Reorganization in Connection with Initial Public Offering

In connection with our initial public offering in July 2004, we converted McCormick & Schmick Holdings LLC, a Delaware limited liability company, into McCormick & Schmick’s Seafood Restaurants, Inc., a Delaware corporation. Because our operations are conducted by wholly owned subsidiaries, the conversion did not affect our financial statements, except with respect to information regarding the membership units in McCormick & Schmick Holdings LLC. Except where specifically noted, references in this Annual Report on Form 10-K to “we” or to “the Company” means McCormick & Schmick Holdings LLC for periods before July 20, 2004 and McCormick & Schmick’s Seafood Restaurants, Inc. for periods on and after July 20, 2004.

PART I

ITEM 1. BUSINESS

Overview

McCormick & Schmick’s Seafood Restaurants, Inc. is a leading national seafood restaurant operator in the affordable upscale dining segment. We have successfully grown our business during the past 35 years by focusing on serving a broad selection of fresh seafood. As of December 30, 2006 we had 66 restaurants in 24 states and the District of Columbia, including two restaurants operated pursuant to management contracts.

Our daily-printed menu typically contains between 85 and 100 made-to-order dishes, including an extensive selection of international, national, regional and local species of seafood. Our signature “Fresh List,” prominently displayed at the top of our daily-printed menu, features 30 to 40 varieties of fresh seafood, based on product availability, price and customer preferences. We also offer alternatives to seafood, including high quality beef, creative salads and fresh pasta dishes.

Our restaurants are designed to capture the distinctive characteristics of each local market, positioning us to compete successfully in a sector comprised primarily of locally owned and operated seafood restaurants. We seek to create an inviting atmosphere which allows us to attract a diverse customer base of men and women, primarily ages 30 to 60, typically college-educated and in the middle to upper-middle income brackets. We believe the combination of our restaurant atmosphere and our extensive menu offering and broad range of price points appeals to a diverse customer base from casual diners, families and tourists to business travelers and special occasion diners.

We believe we are the only high quality seafood restaurant that operates on a national scale. We believe we have successfully differentiated ourselves from our competitors by focusing on the following core strengths of our business model.

1

Fresh Seafood

Our primary business focus for more than 35 years has been to consistently offer a broad selection of fresh seafood, which we believe commands strong loyalty from our customers. Our daily-printed menu typically contains between 85 and 100 made-to-order dishes, including an extensive selection of nationally available species such as Atlantic lobster, Dungeness crab and Alaskan halibut, as well as seasonal products such as wild king salmon, Columbia River sturgeon, sashimi grade tuna, exotic Hawaiian catch and an extensive variety of cold water oysters. The executive chef and general manager at the majority of our restaurants tailor the menu, at least once daily, based on the availability of different species of fresh seafood, price and customer preferences.

We believe we successfully differentiate our concept from both independent local seafood restaurants and national and regional seafood restaurant chains by including in our daily-printed menu our signature “Fresh List” of typically 30 to 40 fresh seafood items, sourced from throughout the United States and from select international locations. We are able to offer a wide variety of consistently fresh, high quality seafood through our close relationships with reputable local and national seafood vendors. We encourage our vendors to adopt preferred and sustainable fishing practices to guarantee the current and future quality and supply of our seafood. During our daily “fresh talk,” the executive chef at each of our restaurants educates our restaurant staff on the menu items of the day so we can effectively communicate the sourcing, freshness, quality and method of preparation of our products to our customers.

Attraction of Our Full-Service Bar

We consider our bar operations to be an integral part of the “McCormick & Schmick’s” brand and central to our broad appeal. We believe the success of our first restaurant, Jake’s Famous Crawfish, was largely driven by its bar operation, which enhanced the dining room business by creating a social forum and building clientele. Our bar operation remains a cornerstone of our restaurant concept, showcasing our commitment to traditionalism and quality. We attract patrons to our bar as a final destination, where they can enjoy a broad selection of liquors, wines and beers in a traditional yet lively environment. Our cocktail drinks are created using traditional methods and are hand-shaken, hand-poured and made with freshly squeezed juices, underlining our focus on product quality. We also offer value-priced items from our full restaurant menu in our bars, which tends to attract younger customers whom we aim to develop into regular restaurant customers.

As a result of our focus on our bar operations as an integral part of our business, our bars drive sales to our restaurants. We run our bar operations as a profit center rather than a mere holding area for diners. In 2006, alcohol sales, predominantly from our bar, accounted for approximately 29% of our revenues and contributed higher gross margins than food sales. The higher gross margins we generate from bar sales allows us the flexibility to offer lower prices on some of our food menu items, helping us maintain our broad guest appeal.

Broad Appeal of Our Concept

We believe we appeal to a broad range of customers by providing an attractive price-value proposition, with prices that are generally more affordable than those of our upscale competitors. Additionally, we believe we offer service that is superior to that of most casual dining operators. The price of a typical meal, including beverages, ranges from $16 to $33 for lunch and $36 to $61 for dinner, with an average of approximately $21 and $48, respectively. Over the past few years, we have enhanced our menu to offer our customers a more affordable dining option by including a selection of lower priced items on our menu. For example, we offer a variety of lunch specials starting at $5.95. We believe even the price sensitive diner values our superior service, and we have received recognition from our customers and industry awards for our service quality.

The combination of our high quality seafood, pricing strategy and customer service enables us to attract a broad customer demographic. Most of our customers are 30 to 60 years old, primarily college-educated, in the middle to upper-middle income brackets and split relatively evenly between male and female customers, with a

2

significant number of our customers comprising the post-war baby boomer generation. These baby boomers, who are the largest segment of the U.S. population (approximately 26% of the total) and a primary driver in the restaurant industry, generally have the greatest level of disposable income and tend to be more focused on better health and specialized diets than other age groups. As our core customers, we believe baby boomers typically prefer restaurants that offer higher quality food items, stronger flavor profiles and wider menu diversity. In addition to this core customer base, our bar operations allow us to also capture the 25 to 35 year old professionals, positioning us to attract a younger clientele as dedicated restaurant customers.

Our broad appeal is supported by our catering and banquet services which we offer both in our restaurants and at other locations as customers request. Our presence in and near hotels enables us to expand the reach of our banquet offerings. In 2006, banquets accounted for approximately 10% of our revenues.

Entrepreneurial Culture with Corporate Control

A key component of our success for over 35 years has been our commitment to promoting and sustaining an entrepreneurial culture throughout our restaurants while maintaining strong corporate oversight and financial controls. Within this strong corporate infrastructure, each restaurant has profit and loss responsibility and a high degree of operating autonomy. The executive chef and general manager at each restaurant have the flexibility, within clearly defined corporate guidelines, to structure menus to cater to customer preferences in that restaurant’s market and respond to changes in product availability and market conditions. We offer quarterly and annual cash performance incentives to certain exempt employees at the restaurant level based on the restaurant’s revenues, costs and profitability, compliance with corporate administrative and payroll guidelines, and the success of other initiatives, such as local community involvement.

We believe our entrepreneurial culture helps us to attract and retain highly qualified and motivated individuals. We have historically retained substantially all of our regional chefs and regional managers and our retention rate for our restaurant general managers and executive chefs is approximately 87%. We believe our decentralized, employee-oriented, entrepreneurial culture creates a sense of pride in our company and allows us to ensure quality service execution at the restaurant level. We believe the stability of our management team and operating personnel, coupled with our disciplined but entrepreneurial culture, positions us for the continued success and growth of our concept.

Portability of Our Brand

We have expanded the McCormick & Schmick’s seafood restaurant concept throughout the United States and have competed successfully with both national and regional restaurant chains and independent local operators, due in part to the flexibility of our real estate model and our nationwide infrastructure. At December 30, 2006, we operated 66 restaurants in 24 states and the District of Columbia, including two pursuant to management contracts, and plan to open as many as 37 additional restaurants over the next three years, excluding our anticipated acquisition of The Boathouse restaurants.

Our restaurants are designed to have broad consumer appeal. We customize our restaurant design and appearance to appeal to local consumer affinities and preferences, and have many restaurants located in buildings that have local significance, including some historic buildings. We have a proven track record of successfully opening restaurants in a variety of sizes, typically ranging from 6,000 to 14,000 square feet and in a number of real estate formats, including both freestanding and in-line locations. The typical size for our current restaurant prototype is 8,000 square feet. We believe the flexibility of our real estate model is a competitive advantage, allowing us to cost-effectively and opportunistically open restaurants in attractive markets without being constrained by a standard prototype or other limiting real estate factors.

We compete on a restaurant-by-restaurant basis with independent local restaurant operators while leveraging the operating strengths of our national infrastructure. We have successfully executed our concept at the local

3

level while maintaining quality and consistency on a national basis in a manner that is not formulaic and that enables us to celebrate the uniqueness of each of our markets. We believe the breadth and scale of our restaurant operations and our more than 35 years of experience in the business give us a competitive advantage in terms of the quality, sourcing and freshness of our menu offerings, and flexibility of price points, making our model difficult to replicate. This competitive advantage contributes to our brand’s reputation for quality and service in the affordable upscale dining sector, which we believe commands strong loyalty from our customers.

Our Growth Strategy

We believe our flexible business model, combined with our fresh menu offerings, professional customer service and inviting restaurant environment, provide us with significant opportunities to further grow our business. Key elements of our growth strategy include the following:

Expansion in Existing Markets

We remain focused on the disciplined growth of our McCormick & Schmick’s brand in our existing markets. We believe we have established the necessary market analysis and site selection procedures for identifying new restaurant opportunities in these markets. In particular, we will continue to evaluate opportunities in affluent suburban areas near existing units in downtown areas to better diversify our presence in existing markets. This strategy enables us to achieve a higher degree of market penetration and brand awareness, resulting in increased repeat business from our broad and diverse customer base. Additionally, we will further leverage the economies of scale of our operations to enhance our competitive advantage against independent local competitors, principally in the areas of advertising, purchasing and distribution infrastructure. We intend to open six restaurants in existing U.S. markets in 2007.

Entry into New Markets

In selecting new market opportunities, we continue to focus on downtown and affluent suburban areas that have large middle to upper-middle income populations, have high customer traffic from thriving businesses or retail markets, and that are convenient for and appealing to business and leisure travelers. We will continue to promote the McCormick & Schmick’s brand image and our broad appeal by opening new restaurants in prime real estate locations and by customizing each new restaurant to the local market. We intend to open five restaurants in new U.S. markets in 2007.

The anticipated acquisition of The Boathouse restaurants will mark our entry into the Canadian market through a well established brand known for its premium locations, broad appeal and operational excellence. Under the purchase agreement, we will acquire five existing restaurants and one that is currently under construction, in the greater Vancouver B.C. area.

Capture of Ancillary Business Opportunities

We will continue to pursue secondary opportunities that are complementary to our primary concept and further our growth objectives. We operate seven restaurants under the name M&S Grill and one under the name Jake’s Grill, each of which offers an alternative menu to that of our seafood restaurants. These restaurants are located near our existing seafood restaurants to take advantage of management and operating efficiencies. We will also continue to consider catering opportunities and management agreements with hotels. We believe entering into management agreements with hotels gives our brand additional exposure to business and leisure travelers, requires minimal initial investment and is therefore low-risk and profitable. We operate two restaurants under management agreements with hotels.

4

Unit Level Economics

Our average investment per restaurant opened since 1997 has been approximately $2.8 million, including leasehold improvements, furniture, fixtures and equipment, and net of landlord incentive allowances. As a result of the reduction in the size of our restaurant prototype, to facilitate our entry into a greater variety of markets and provide us with increased flexibility with site selection, we anticipate that our average investment per restaurant will be approximately $2.4 million going forward. We believe our focus on a traditional décor has allowed us to benefit from lower restaurant-level maintenance or upgrade costs than those incurred by some of our competitors.

The average restaurant sales volume for restaurants opened from 1997 through 2003 was approximately $5.4 million by the third year of operations. These restaurants were, on average, approximately 10,000 square feet each. Since the beginning of 2002, we have opened 29 new company-owned restaurants, which averaged approximately 8,000 square feet each. Our growth model assumes average unit sales volumes for our 8,000 square feet restaurants of $4.4 million in the third year of operations.

Menu, Food Preparation, Quality Control and Purchasing

Most of our menu items are prepared from scratch daily at each restaurant and each order is assembled when the order is placed with the kitchen staff. Each restaurant has an executive chef responsible for overseeing kitchen operations, including planning the daily-printed menu and ordering necessary ingredients and supplies. Each executive chef is assisted by two to four sous chefs, who help to manage food preparation and service timing.

We maintain strict quality standards at all of our restaurants. We expect each of our employees to adhere to these standards, and it is the responsibility of the general manager and the executive chef at each restaurant to ensure these standards are upheld. We are committed to providing our guests with high quality, fresh products and superior service. We regularly hold regional management meetings designed to re-emphasize McCormick & Schmick’s philosophy, culture, standards of operation and culinary development. Through use of our standard training materials and our commitment to the hiring, development and training of chefs, we are able to maintain high standards and guidelines for our regularly purchased seafood species.

At the restaurant level, purchasing is primarily directed by the executive chef, who is trained in our purchasing practices and philosophy and is supervised by an experienced regional chef. To provide the freshest ingredients and products and to improve operating efficiencies between purchase and use, each executive chef determines the daily requirements for food ingredients, products and supplies. The executive chef orders accordingly from local suppliers and regional and national distributors. Fresh seafood is sourced through multiple vendors in varying geographic regions and delivered daily to each restaurant.

We encourage each of our restaurants to purchase seafood from a network of preferred vendors we have identified as consistently supplying seafood that meets our high standards. The identification and selection of seafood suppliers is reviewed regularly based on product quality, sanitation, fishing practices, pricing and customer service. We prefer suppliers who use day-boats rather than those who are at sea for multiple days because their product is typically fresher. We believe our national and regional presence allows us to achieve better quality and pricing terms for key products, such as fresh fin fish and shellfish, than most of our competitors. Other food products, such as high quality beef and dry goods, are sourced primarily from SYSCO Corporation, a national food distributor, while liquor, beer and wine are purchased from local distributors. SYSCO accounted for approximately 13% of our food purchases in 2006. No other vendor accounted for more than 10% of our purchases in 2006.

Restaurant Design and Atmosphere

Our restaurant designs and décor are intended to capture distinctive attributes of each local market, varying from traditional New England-style fish houses to contemporary dinner houses with waterfront views. Some of our restaurants are located in historic buildings, which reinforces our commitment to local design elements and

5

further promotes the appeal and ambience of our restaurants. Our flexible approach to our restaurant designs contributes to the uniqueness of each restaurant and allows us to successfully compete in a sector comprised primarily of independent, locally-owned and operated seafood restaurants.

Our restaurants are generally modeled after two styles:

| | • | | “turn-of-the-century” style, which blends different types and colors of wood; and |

| | • | | classic art deco style. |

Additionally, our interior décor fosters an inviting atmosphere that we believe is equally appealing to both men and women.

Our wait staff and bartenders are typically uniformed in traditional white jackets and black ties and are committed to providing our guests with superior service to further enhance their dining experience.

6

Restaurant Locations, Lease Arrangements and Management Fee Arrangements

At December 30, 2006, we operated 66 restaurants in 24 states and the District of Columbia. We lease all of our restaurant sites, except for the two we operate under management agreements. Terms vary by restaurant, but we generally lease space for 10 to 20 years and negotiate one to three five-year renewal options.

| | | | |

Restaurant Name | | City | | Year Opened |

Alabama | | | | |

McCormick & Schmick’s Seafood Restaurant | | Birmingham | | 2004 |

| | |

Arizona | | | | |

McCormick & Schmick’s Seafood Restaurant | | Phoenix | | 1999 |

| | |

California | | | | |

McCormick & Schmick’s Seafood Restaurant | | Irvine | | 1989 |

McCormick & Kuleto’s Seafood Restaurant | | San Francisco | | 1991 |

McCormick & Schmick’s Seafood Restaurant | | Los Angeles | | 1992 |

McCormick & Schmick’s Seafood Restaurant | | Pasadena | | 1993 |

McCormick & Schmick’s a Pacific Seafood Grill | | Beverly Hills | | 1994 |

McCormick & Schmick’s Seafood Restaurant | | El Segundo | | 1998 |

Spenger’s Fresh Fish Grotto | | Berkeley | | 1999 |

The Seafood Brasserie* | | Santa Rosa | | 2002 |

McCormick & Schmick’s Seafood Restaurant | | San Jose | | 2004 |

McCormick & Schmick’s Seafood Restaurant* | | San Diego | | 2004 |

McCormick & Schmick’s Seafood Restaurant | | Burbank | | 2006 |

| | |

Colorado | | | | |

McCormick’s Fish House & Bar | | Denver | | 1987 |

McCormick & Schmick’s Seafood Restaurant | | Denver | | 2004 |

| | |

District of Columbia | | | | |

McCormick & Schmick’s Seafood Restaurant | | Washington | | 1996 |

M&S Grill | | Washington | | 1998 |

McCormick & Schmick’s Seafood Restaurant | | Washington | | 2004 |

Jimmy’s on K Street | | Washington | | 2006 |

| | |

Florida | | | | |

McCormick & Schmick’s Seafood Restaurant | | Orlando | | 2002 |

McCormick & Schmick’s Seafood Restaurant | | Boca Raton | | 2006 |

| | |

Georgia | | | | |

McCormick & Schmick’s Seafood Restaurant | | Atlanta | | 2000 |

McCormick & Schmick’s Seafood Restaurant | | Atlanta | | 2002 |

| | |

Illinois | | | | |

McCormick & Schmick’s Seafood Restaurant | | Chicago | | 1998 |

McCormick & Schmick’s Seafood Restaurant | | Chicago | | 2006 |

| | |

Indiana | | | | |

McCormick & Schmick’s Seafood Restaurant | | Indianapolis | | 2005 |

| | |

Maryland | | | | |

McCormick & Schmick’s Seafood Restaurant | | Baltimore | | 1998 |

McCormick & Schmick’s Seafood Restaurant | | Bethesda | | 1999 |

M&S Grill | | Baltimore | | 2003 |

| | |

Massachusetts | | | | |

McCormick & Schmick’s Seafood Restaurant | | Boston | | 2000 |

McCormick & Schmick’s Seafood Restaurant | | Boston | | 2001 |

| | |

Michigan | | | | |

McCormick & Schmick’s Seafood Restaurant | | Troy | | 2001 |

7

| | | | |

Restaurant Name | | City | | Year Opened |

| | |

Minnesota | | | | |

McCormick & Schmick’s Seafood Restaurant | | Minneapolis | | 2000 |

M&S Grill | | Minneapolis | | 2006 |

| | |

Missouri | | | | |

McCormick & Schmick’s Seafood Restaurant | | Kansas City | | 2000 |

M&S Grill | | Kansas City | | 2005 |

| | |

Nevada | | | | |

McCormick & Schmick’s Seafood Restaurant | | Las Vegas | | 1998 |

| | |

New Jersey | | | | |

McCormick & Schmick’s Seafood Restaurant | | Hackensack | | 2002 |

McCormick & Schmick’s Seafood Restaurant | | Bridgewater | | 2003 |

| | |

New York | | | | |

McCormick & Schmick’s Seafood Restaurant | | New York | | 2004 |

| | |

North Carolina | | | | |

McCormick & Schmick’s Seafood Restaurant | | Charlotte | | 2005 |

McCormick & Schmick’s Seafood Restaurant | | Charlotte | | 2005 |

| | |

Ohio | | | | |

McCormick & Schmick’s Seafood Restaurant | | Columbus | | 2006 |

McCormick & Schmick’s Seafood Restaurant | | Cincinnati | | 2006 |

| | |

Oregon | | | | |

Jake’s Famous Crawfish | | Portland | | 1972 |

McCormick & Schmick’s Seafood Restaurant | | Portland | | 1979 |

McCormick’s Fish House & Bar | | Beaverton | | 1981 |

McCormick & Schmick’s Harborside at the Marina | | Portland | | 1985 |

Jake’s Grill / Jake’s Catering | | Portland | | 1994 |

The Heathman Restaurant | | Portland | | 2000 |

M&S Grill | | Tigard | | 2005 |

| | |

Pennsylvania | | | | |

McCormick & Schmick’s Seafood Restaurant | | Philadelphia | | 2001 |

McCormick & Schmick’s Seafood Restaurant | | Pittsburgh | | 2005 |

| | |

Rhode Island | | | | |

McCormick & Schmick’s Seafood Restaurant | | Providence | | 2004 |

| | |

Texas | | | | |

McCormick & Schmick’s Seafood Restaurant | | Houston | | 1999 |

McCormick & Schmick’s Seafood Restaurant | | Dallas | | 2003 |

McCormick & Schmick’s Seafood Restaurant | | Austin | | 2004 |

| | |

Virginia | | | | |

McCormick & Schmick’s Seafood Restaurant | | Reston | | 1997 |

McCormick & Schmick’s Seafood Restaurant | | McLean | | 2000 |

M&S Grill | | Reston | | 2004 |

McCormick & Schmick’s Seafood Restaurant | | Arlington | | 2004 |

| | |

Washington | | | | |

McCormick’s Fish House & Bar | | Seattle | | 1977 |

McCormick & Schmick’s Seafood Restaurant | | Seattle | | 1984 |

McCormick & Schmick’s Catering at the Museum of Flight in Seattle | | Seattle | | 1994 |

McCormick & Schmick’s Harborside on Lake Union | | Seattle | | 1996 |

McCormick & Schmick’s Seafood Restaurant | | Bellevue | | 2005 |

| * | We operate these restaurants under management agreements. |

8

Site Selection

We believe our site selection strategy is critical to our growth strategy. We carefully consider potential markets and we devote a substantial amount of time and effort evaluating each potential restaurant site. We identify new restaurant development opportunities through an established real estate broker network and developer relationships. Our site specifications are flexible and we believe this allows us to consider a broader range of possible locations than most of our regional and national competitors. The criteria we consider in developing our expansion plans and in siting new restaurants include:

| | • | | population density and the income and educational level of the population; |

| | • | | competitive conditions and price points; |

| | • | | estimates of the return on investment; |

| | • | | available square footage and lease economics; |

| | • | | the proximity of hotels and office space and the density of pedestrian and vehicle traffic; |

| | • | | the suitability of the site for an affordable, upscale restaurant with a traditional ambience; |

| | • | | capacity expansion possibilities; and |

| | • | | management’s experience in the market and the locations of our existing restaurants. |

A majority of our restaurants are located in high-traffic, metropolitan areas and several are located in historic buildings. We believe there are many additional markets that meet our demographic and geographic profiles.

Of our 66 restaurants, including the two we operate under management agreements, 24 were opened within the last three years and 31 were opened within the last five years. Although our expansion has increased in the last five years, we believe it has been steady, controlled and prudent. We opened seven restaurants in 2006 and our plan for 2007 includes the opening of eleven restaurants, excluding the anticipated acquisition of existing and opening of any new Boathouse restaurants. We anticipate opening twelve, fourteen and sixteen restaurants in 2008, 2009 and 2010, respectively. The typical lead-time from the selection of a location to the opening of a restaurant at that location is approximately twelve to fifteen months.

Marketing and Advertising

The goals of our marketing efforts are to:

| | • | | increase comparable restaurant sales by attracting new guests; |

| | • | | increase the frequency of visits by our current guests; |

| | • | | support new restaurant openings to achieve sales and profit goals; and |

| | • | | communicate and promote the uniqueness, appeal, quality and consistency of our brand. |

In 2006, 75% of our marketing expenditures were at the local level, which constituted approximately 2% of revenues.

Local Marketing

Approximately 60 days before a scheduled restaurant opening, our local public relations firms collaborate with the local media to publicize our restaurant opening and to generate awareness of our brand. For example, we typically host several social events in the local community to generate publicity before the official opening of a restaurant. Post-opening, we maintain a strong relationship with our public relations firms and remain focused on

9

our commitment to promoting our brand in the local market through various programs, such as cooking demonstrations by our chefs or discussions on seafood and related offerings on local news broadcasts. We also advertise with local daily and weekly publications, key monthly magazines and local business journals in most urban markets.

Our restaurants actively promote our special holiday programs and sponsor community events, such as donations, charitable and non-profit organizations and visual and performing cultural arts activities. We believe that, in addition to benefiting our local communities, these activities generate positive media attention and publicity for our brand and enhance our local public image.

National Marketing

In 2006, we incurred approximately 32% of our advertising expenditures at the national level which comprised 15% of our total marketing expenditures. Our campaign focuses on national periodicals such as United Airlines’, Delta Airlines’, Southwest Airlines’ and Alaska Airlines’ in-flight magazines and WHERE Magazine. Additionally, we advertise across the national network of The Business Journal publication.

To reinforce our broad differentiation, we highlight the breadth and freshness of our seafood in both local and national advertising. We periodically offer promotional certificates and maintain contact with organizations in the travel and convention industries, such as hotels, travel agents, convention centers and local shops, to further enhance both brand and restaurant location awareness and to target specific guest groups.

Operations

Restaurant Management

Our restaurant operations are organized into three divisions (West Coast, Southeast and Northeast), each with a vice president of operations overseeing all aspects of restaurant operations within the designated division, including financial performance, new restaurant openings, capital expenditure requests, management development and marketing. Each of our vice presidents reports to our executive vice president of operations.

Fourteen multi-restaurant managers, of whom seven are regional managers and seven are regional chefs, are each responsible for five to eleven restaurants and report to a vice president of operations. Both regional managers and regional chefs are responsible for overall restaurant operations, but have an increased focus on their respective areas of expertise. For example, regional chefs focus more heavily on negotiating food costs, ensuring high food quality, developing and nurturing executive and sous chefs and being responsive to overall kitchen staff needs. Regional managers focus primarily on revenues, profitability, front-of-house management and marketing activities.

Our typical restaurant management team consists of a general manager and an executive chef, two to four assistant managers, two to four sous chefs and, in some cases, a meeting planner/banquet coordinator. The remaining restaurant-level employees are hourly personnel varying in number based on restaurant size. Our typical restaurant employs 80 to 90 full-time and part-time employees. The general manager is responsible for all management functions, including purchasing (other than food), hiring and firing and oversight of restaurant-level bookkeeping and cash controls. The executive chef is responsible for managing all kitchen functions, including training, menu design and food purchasing, quality and presentation.

We emphasize frequent interaction between our vice presidents, regional managers and restaurant level management. As a result, neither vice presidents nor regional managers operate out of our corporate office and are routinely accessible to restaurant staff.

All management levels in operations, from vice presidents to assistant managers, participate in incentive bonus programs. These incentive programs are designed to establish specific goals and objectives and to ensure accountability and reward performance.

10

Restaurant Operations

Our restaurants are generally open 365 days each year, serve lunch and dinner and are generally open from 11:00 a.m. to 11:00 p.m. Sunday through Thursday and 11:00 a.m. to 1:00 a.m. Friday and Saturday. In 2006, dinner comprised approximately 76% of our revenues, while lunch comprised approximately 24% of revenues, and our restaurants served an average of 1,088 guests per week during lunch and 1,575 guests per week during dinner. To accommodate guests who have limited time available during lunch, we offer a 45-minute lunch guarantee.

Additionally, we offer catering and banquet services both in our restaurants and at other locations as customers request. Our presence in and near hotels enables us to expand the reach of our banquet offerings. In 2006, banquets accounted for approximately 10% of our revenues.

Employees

As of December 30, 2006 we employed 5,866 persons, of whom 564 were salaried and 5,302 were hourly personnel. None of our employees are represented by unions and, in general, we consider our relationship with our employees to be good. Our employees are summarized by major functional area in the table below.

| | |

Functional Area | | Number of

Employees |

VPs/regional managers/regional chefs | | 18 |

General managers | | 69 |

Assistant managers | | 211 |

Executive chefs | | 68 |

Sous chefs | | 152 |

Non-salaried restaurant staff | | 5,263 |

Corporate salaried | | 46 |

Corporate non-salaried | | 39 |

| | |

Total | | 5,866 |

| | |

Management Information Systems

All of our information processing is managed from our headquarters in Portland, Oregon. Point-of-sale terminals at each restaurant allow us to generate the daily reports needed to manage our restaurants and our business. These reports include, among other things, daily and weekly revenues, guest counts, meal period sales breakouts and food and liquor consumption. The data from the point-of-sale system is electronically transferred each night to a third party intranet provider, with the data then accessible by us through the Internet. Financial operating results are reviewed at the corporate office and studied by restaurant level and regional management. Variances from expectations are analyzed and addressed at frequent financial meetings.

Industry and Competition

Industry

We operate in a highly competitive industry that is affected by changes in consumer eating habits and dietary preferences, population trends and traffic patterns, and local and national economic conditions. Key competitive factors in the industry include the taste, quality and price of the food products offered, quality and speed of guest service, brand name identification, attractiveness of facilities, restaurant location, and overall dining experience. We believe we compete favorably with respect to each of these factors and have successfully overcome the following barriers faced by seafood restaurants:

| | • | | developing and maintaining consistent, reliable sources of high quality, fresh seafood; |

| | • | | hedging against increases in seafood costs is often not possible; |

11

| | • | | preparing and handling seafood is more complicated than for other types of cuisine; and |

| | • | | consumer tastes in seafood products vary from region to region. |

Competition

While we compete with a range of restaurant operators for consumers’ dining preferences and with both restaurants and retailers for site locations and personnel requirements, we consider our principal competitors to include the following:

| | • | | independent, local seafood houses; |

| | • | | regional seafood restaurant concepts, such as Cameron Mitchell’s, King’s Seafood, Landry’s Seafood, Legal Sea Foods, Oceanaire and Roy’s; and |

| | • | | upscale “steak and chop” houses such as Capital Grille, Morton’s, Ruth’s Chris, Smith & Wollensky and The Palm, among others. |

Available Information

We make available free of charge on or through our website at www.mccormickandschmicks.com our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after we file these materials with the Securities and Exchange Commission. These materials are also available on the Security and Exchange Commission’s website atwww.sec.gov.

ITEM 1A. RISK FACTORS

Restaurant companies have been the target of class-actions and other lawsuits alleging, among other things, violation of federal and state law.

We are subject to a variety of claims arising in the ordinary course of our business brought by or on behalf of our customers or employees, including personal injury claims, contract claims, and employment-related claims. In recent years, a number of restaurant companies have been subject to lawsuits, including class-action lawsuits, alleging violations of federal and state law regarding workplace, employment and similar matters. A number of these lawsuits have resulted in the payment of substantial damages by the defendants. Similar lawsuits have been instituted against us from time to time. Regardless of whether any claims against us are valid or whether we are ultimately determined to be liable, claims may be expensive to defend and may divert time and money away from our operations and hurt our performance. A judgment significantly in excess of our insurance coverage for any claims could materially adversely affect our financial condition or results of operations, and adverse publicity resulting from these allegations may materially adversely affect our business. We may incur substantial damages and expenses resulting from lawsuits, which could have a material adverse effect on our business.

Our ability to expand our restaurant base is influenced by many factors beyond our control and therefore we may not be able to achieve our planned growth.

Our growth strategy depends in large part on our ability to open new restaurants and to operate these restaurants profitably. Delays or failures in opening new restaurants could impair our ability to meet our growth objectives. We have in the past experienced delays in restaurant openings and may experience similar delays in the future. Our ability to expand our business successfully will depend upon numerous factors, including:

| | • | | hiring, training and retaining skilled management, chefs and other qualified personnel to open, manage and operate new restaurants; |

| | • | | locating and securing a sufficient number of suitable new restaurant sites in new and existing markets on acceptable lease terms; |

12

| | • | | managing the amount of time and construction and development costs associated with the opening of new restaurants; |

| | • | | obtaining adequate financing for the construction of new restaurants; |

| | • | | securing governmental approvals and permits required to open new restaurants in a timely manner, if at all; |

| | • | | successfully promoting our new restaurants and competing in the markets in which our new restaurants are located; and |

| | • | | general economic conditions. |

Some of these factors are beyond our control. We may not be able to achieve our expansion goals and our new restaurants may not be able to achieve operating results similar to those of our existing restaurants.

Unexpected expenses and low market acceptance could adversely affect the profitability of restaurants that we open in new markets.

Our growth strategy includes opening restaurants in markets where we have little or no operating experience and in which potential customers may not be familiar with our restaurants. The success of these new restaurants may be affected by different competitive conditions, consumer tastes and discretionary spending patterns, and our ability to generate market awareness and acceptance of the McCormick & Schmick’s brand. As a result, we may incur costs related to the opening, operation and promotion of these new restaurants that are greater than those incurred in other areas. Even though we may incur substantial additional costs with these new restaurants, they may attract fewer customers than our more established restaurants in existing markets. Sales at restaurants we open in new markets may take longer to reach our average annual sales, if at all. As a result, the results of operations at our new restaurants may be inferior to those of our existing restaurants. We may not be able to profitably open restaurants in new markets.

Our growth may strain our infrastructure and resources, which could slow our development of new restaurants and adversely affect our ability to manage our existing restaurants.

We opened seven company-owned restaurants in 2005 and seven in 2006. We plan to open eleven company-owned restaurants in 2007, excluding the anticipated acquisition of the Boathouse restaurants. Our expansion and our future growth may strain our restaurant management systems and resources, financial controls and information systems. Those demands on our infrastructure and resources may also adversely affect our ability to manage our existing restaurants. If we fail to continue to improve our infrastructure or to manage other factors necessary for us to meet our expansion objectives, our operating results could be materially and adversely affected.

Our ability to raise capital in the future may be limited, which could adversely impact our growth.

Changes in our operating plans, acceleration of our expansion plans, lower than anticipated sales, increased expenses or other events described in this section may require us to seek additional debt or equity financing. Financing may not be available on acceptable terms and our failure to raise capital when needed could negatively impact our growth and our financial condition and results of operations. Additional equity financing may be dilutive to the holders of our common stock, and debt financing, if available, may involve significant cash payment obligations and covenants that restrict our ability to operate our business.

Our operations are susceptible to changes in food availability and costs, which could adversely affect our operating results.

Our profitability depends significantly on our ability to anticipate and react to changes in seafood costs. We rely on local, regional and national suppliers to provide our seafood. Increases in distribution costs or sale prices

13

or failure to perform by these suppliers could cause our food costs to increase. We could also experience significant short-term disruptions in our supply if a significant supplier failed to meet its obligations. The supply of seafood is more volatile than other types of food. The type, variety, quality and price of seafood is subject to factors beyond our control, including weather, governmental regulation, availability and seasonality, each of which may affect our food costs or cause a disruption in our supply. Changes in the price or availability of certain types of seafood could affect our ability to offer a broad menu and price offering to customers and could materially adversely affect our profitability.

Our operating results may fluctuate significantly and could fall below the expectations of securities analysts and investors due to seasonality and other factors, resulting in a decline in our stock price.

Our operating results may fluctuate significantly because of several factors, including:

| | • | | our ability to achieve and manage our planned expansion; |

| | • | | our ability to achieve market acceptance, particularly in new markets; |

| | • | | our ability to raise capital in the future; |

| | • | | changes in the availability and costs of food; |

| | • | | the loss of key management personnel; |

| | • | | the concentration of our restaurants in specific geographic areas; |

| | • | | our ability to protect our name and logo and other proprietary information; |

| | • | | changes in consumer preferences or discretionary spending; |

| | • | | fluctuations in the number of visitors or business travelers to downtown locations; |

| | • | | health concerns about seafood or other foods; |

| | • | | our ability to attract, motivate and retain qualified employees; |

| | • | | increases in labor costs, including statutory minimum wage increases; |

| | • | | the impact of federal, state or local government regulations relating to our employees or the sale or preparation of food and the sale of alcoholic beverages; |

| | • | | the impact of litigation; |

| | • | | the effect of competition in the restaurant industry; and |

| | • | | economic trends generally. |

Our business also is subject to seasonal fluctuations. As a result, our quarterly and annual operating results and restaurant sales may fluctuate significantly as a result of seasonality and the factors discussed above. Accordingly, results for any one fiscal quarter are not necessarily indicative of results to be expected for any other quarter or for any year and comparable restaurant sales for any particular future period may decrease. Our operating results may also fall below the expectations of securities analysts and investors. In that event, the price of our common stock would likely decrease.

A decline in visitors or business travelers to downtown areas where our restaurants are located could negatively affect our restaurant sales.

Many of our restaurants are located in downtown areas. We depend on both local residents and business travelers to frequent these locations. If the number of visitors to downtown areas declines due to economic or other conditions, changes in consumer preferences, changes in discretionary consumer spending or for other reasons, our revenues could decline significantly and our results of operations could be adversely affected.

14

If we lose the services of any of our key management personnel our business could suffer.

We depend on the services of our key senior management personnel. If we lose the services of any members of our senior management or key personnel for any reason, we may be unable to replace them with qualified personnel, which could have a material adverse effect on our business and growth. We do not carry key person life insurance on any of our executive officers.

Many of our restaurants are concentrated in local or regional areas and, as a result, we are sensitive to economic and other trends and developments in these areas.

We operate five restaurants in the Seattle, Washington area, seven in the Portland, Oregon area and twelve in California; our East Coast restaurants are concentrated in and around Washington, D.C. As a result, adverse economic conditions, weather and labor markets in any of these areas could have a material adverse effect on our overall results of operations.

In addition, given our geographic concentrations, negative publicity regarding any of our restaurants in these areas could have a material adverse effect on our business and operations, as could other regional occurrences such as local strikes, oil spills, terrorist attacks, energy shortages or increases in energy prices, droughts or earthquakes or other natural disasters.

Our success depends on our ability to protect our proprietary information. Failure to protect our trademarks, service marks or trade secrets could adversely affect our business.

Our business prospects depend in part on our ability to develop favorable consumer recognition of the McCormick & Schmick’s name. Although McCormick & Schmick’s, M&S Grill and other of our service marks are federally registered trademarks with the United States Patent and Trademark Office, our trademarks could be imitated in ways that we cannot prevent. In addition, we rely on trade secrets, proprietary know-how, concepts and recipes. Our methods of protecting this information may not be adequate, however, and others could independently develop similar know-how or obtain access to our trade secrets, know-how, concepts and recipes.

Moreover, we may face claims of misappropriation or infringement of third parties’ rights that could interfere with our use of our proprietary know-how, concepts, recipes or trade secrets. Defending these claims may be costly and, if unsuccessful, may prevent us from continuing to use this proprietary information in the future, and may result in a judgment or monetary damages.

We do not maintain confidentiality and non-competition agreements with all of our executives, key personnel or suppliers. If competitors independently develop or otherwise obtain access to our know-how, concepts, recipes or trade secrets, the appeal of our restaurants could be reduced and our business could be harmed.

Our insurance policies may not provide adequate levels of coverage against all claims.

We believe we maintain insurance coverage that is customary for businesses of our size and type. However, there are types of losses we may incur that cannot be insured against or that we believe are not commercially reasonable to insure. These losses, if they occur, could have a material and adverse effect on our business and results of operations.

Expanding our restaurant base by opening new restaurants in existing markets could reduce the business of our existing restaurants.

Our growth strategy includes opening restaurants in markets in which we already have existing restaurants. We may be unable to attract enough customers to the new restaurants for them to operate at a profit. Even if we

15

are able to attract enough customers to the new restaurants to operate them at a profit, those customers may be former customers of one of our existing restaurants in that market and the opening of new restaurants in the existing market could reduce the revenue of our existing restaurants in that market.

We may not be able to successfully integrate into our business the operations of restaurants that we acquire, which may adversely affect our business, financial condition and results of operations.

We anticipate completing our acquisition of The Boathouse restaurants in March 2007. These restaurants will be the first we own outside of the United States, and we do not have experience operating restaurants in British Columbia, Canada. We may seek to selectively acquire other existing restaurants and integrate them into our business operations. Achieving the expected benefits of The Boathouse restaurants and any other restaurants that we acquire will depend in large part on our ability to successfully integrate the operations of the acquired restaurants and personnel in a timely and efficient manner. The risks involved in such restaurant acquisitions and integration include:

| | • | | challenges and costs associated with the acquisition and integration of restaurant operations located in markets where we have limited or no experience; |

| | • | | possible disruption to our business as a result of the diversion of management’s attention from its normal operational responsibilities and duties; and |

| | • | | consolidation of the corporate, information technology, accounting and administrative infrastructure and resources of the acquired restaurants into our business. |

If we cannot overcome the challenges and risks that we face in integrating the operations of newly acquired restaurants, our business, financial condition and results of operations could be adversely affected.

Negative publicity concerning food quality, health and other issues and costs or liabilities resulting from litigation may have a material adverse effect on our results of operations.

We are sometimes the subject of complaints or litigation from customers alleging illness, injury or other food quality, health or operational concerns. Litigation or adverse publicity resulting from these allegations may materially and adversely affect us or our restaurants, regardless of whether the allegations are valid or whether we are liable. Further, these claims may divert our financial and management resources from revenue-generating activities and business operations.

Health concerns relating to the consumption of seafood or other foods could affect consumer preferences and could negatively impact our results of operations.

We may lose customers based on health concerns about the consumption of seafood or negative publicity concerning food quality, illness and injury generally, such as negative publicity concerning the accumulation of mercury or carcinogens in seafood, e-coli, “mad cow” or “foot-and-mouth” disease, publication of government or industry findings about food products served by us or other health concerns or operating issues stemming from one of our restaurants. In addition, our operational controls and training may not be fully effective in preventing all food-borne illnesses. Some food-borne illness incidents could be caused by food suppliers and transporters and would be outside of our control. Any negative publicity, health concerns or specific outbreaks of food-borne illnesses attributed to one or more of our restaurants, or the perception of an outbreak, could result in a decrease in guest traffic to our restaurants and could have a material adverse effect on our business.

16

Changes in consumer preferences or discretionary consumer spending could negatively impact our results of operations.

The restaurant industry is characterized by the introduction of new concepts and is subject to rapidly changing consumer preferences, tastes and purchasing habits. Our continued success depends in part upon the popularity of seafood and the style of dining we offer. Shifts in consumer preferences away from this cuisine or dining style could materially and adversely affect our operating results. Our success will depend in part on our ability to anticipate and respond to changing consumer preferences, tastes and purchasing habits, and to other factors affecting the restaurant industry, including new market entrants and demographic changes. If we change our concept and menu to respond to changes in consumer tastes or dining patterns, we may lose customers who do not like the new concept or menu, and may not be able to attract a sufficient new customer base to produce the revenue needed to make the restaurant profitable. Our success also depends to a significant extent on numerous factors affecting discretionary consumer spending, including economic conditions, disposable consumer income and consumer confidence. Adverse changes in these factors could reduce guest traffic or impose practical limits on pricing, either of which could harm our results of operations.

Labor shortages or increases in labor costs could slow our growth or harm our business.

Our success depends in part upon our ability to attract, motivate and retain a sufficient number of qualified employees, including regional operational managers and regional chefs, restaurant general managers and executive chefs, necessary to continue our operations and keep pace with our growth. Qualified individuals are in short supply and competition for these employees is intense. If we are unable to recruit and retain sufficient qualified individuals, our business and our growth could be adversely affected. Additionally, competition for qualified employees could require us to pay higher wages, which could result in higher labor costs. If our labor costs increase, our results of operations will be negatively affected.

We may incur costs or liabilities and lose revenue, and our growth strategy may be adversely impacted, as a result of government regulation.

Our restaurants are subject to various federal, state and local government regulations, including those relating to employees, the preparation and sale of food and the sale of alcoholic beverages. These regulations affect our restaurant operations and our ability to open new restaurants.

Each of our restaurants must obtain licenses from regulatory authorities to sell liquor, beer and wine, and each restaurant must obtain a food service license from local health authorities. Each liquor license must be renewed annually and may be revoked at any time for cause, including violation by us or our employees of any laws and regulations relating to the minimum drinking age, advertising, wholesale purchasing and inventory control. In California, where we operate twelve restaurants, the number of alcoholic beverage licenses available is limited and licenses are traded at market prices.

The failure to maintain our food and liquor licenses and other required licenses, permits and approvals could adversely affect our operating results. Difficulties or failure in obtaining the required licenses and approvals could delay or result in our decision to cancel the opening of new restaurants.

We are subject to “dram shop” statutes in some states. These statutes generally allow a person injured by an intoxicated person to recover damages from an establishment that wrongfully served alcoholic beverages to the intoxicated person. A judgment substantially in excess of our insurance coverage could harm our operating results and financial condition.

17

Various federal and state labor laws govern our relationship with our employees and affect operating costs. These laws include minimum wage requirements, overtime pay, unemployment tax rates, workers’ compensation rates, and citizenship requirements. Additional government-imposed increases in minimum wages, overtime pay, paid leaves of absence and mandated health benefits, increased tax reporting and tax payment requirements for employees who receive gratuities, or a reduction in the number of states that allow tips to be credited toward minimum wage requirements could harm our operating results and financial condition.

The Federal Americans with Disabilities Act prohibits discrimination on the basis of disability in public accommodations and employment. Although our restaurants are designed to be accessible to the disabled, we could be required to make modifications to our restaurants to provide service to, or make reasonable accommodations for, disabled persons.

Our operations and profitability are susceptible to the effects of violence, war and economic trends.

Terrorist attacks and other acts of violence or war and U.S. military reactions to such attacks may negatively affect our operations and an investment in our shares of common stock. The terrorist attacks in New York and Washington, D.C. on September 11, 2001 led to a temporary interruption in deliveries from some of our suppliers and, we believe, contributed to the decline in average annual comparable restaurant sales in 2001 and 2002.

Future acts of violence or war could cause a decrease in travel and in consumer confidence, decrease consumer spending, result in increased volatility in the United States and worldwide financial markets and economy, or result in an economic recession in the United States or abroad. They could also impact consumer leisure habits, for example, by increasing time spent watching television news programs at home, and may reduce the number of times consumers dine out, which could adversely impact our revenue. Any of these occurrences could harm our business, financial condition or results of operations, and may result in the volatility of the market price for our securities and on the future price of our securities.

Terrorist attacks could also directly impact our physical facilities or those of our suppliers, and attacks or armed conflicts may make travel and the transportation of our supplies and products more difficult and more expensive and could ultimately affect our revenues.

We may not be able to compete successfully with other restaurants, which could adversely affect our results of operations.

The restaurant industry is intensely competitive with respect to price, service, location, food quality, ambiance and the overall dining experience. Our competitors include a large and diverse group of restaurant chains and individual restaurants that range from independent local operators to well capitalized national restaurant companies. Some of our competitors have been in existence for a substantially longer period than we have and may be better established in the markets where our restaurants are or may be located. Some of our competitors may have substantially greater financial, marketing and other resources than we do. If our restaurants are unable to compete successfully with other restaurants in new and existing markets, our results of operations will be adversely affected. We also compete with other restaurants for experienced management personnel and hourly employees, and with other restaurants and retail establishments for quality restaurant sites.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

Our corporate headquarters are located in Portland, Oregon. We occupy this facility under a lease that terminates in December 2009. We lease all of our restaurant facilities, except for one we own and expect to open in 2007 and two that we operate under management agreements.

18

ITEM 3. LEGAL PROCEEDINGS

Occasionally, we are a defendant in litigation arising in the ordinary course of our business, including claims resulting from “slip and fall” accidents, employment related claims and claims from guests or employees alleging illness, injury or other food quality, health or operational concerns. None of these types of litigation, most of which are covered by insurance, has had a material effect on our business, results of operations, financial position or cash flows.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

No matters were submitted to a vote of stockholders during the fourth quarter of the fiscal year covered by this report.

ITEM 4A. EXECUTIVE OFFICERS AND OTHER KEY EMPLOYEES

Douglas L. Schmick (age 59) co-founded McCormick & Schmick’s in 1972 and was appointed chief executive officer in February 2007 and chairman of the board of directors in 2004. From 1997 through January 2007 he served as president and from 1997 through 1999, he also served as chief executive officer and served as secretary, treasurer, and chief executive officer from 1974 through 1997. Mr. Schmick has served on the board of directors since August 22, 2001. Mr. Schmick received his Bachelor of Science degree from the University of Idaho.

Emanuel (Manny) N. Hilario (age 39) joined McCormick & Schmick’s in April 2004 as chief financial officer. For the four years before joining us, Mr. Hilario was with Angelo and Maxie’s, Inc. (formerly Chart House Enterprises, Inc.) most recently as chief financial officer. From December 1997 until April 2000, Mr. Hilario was with ACCO North America, a wholly owned subsidiary of Fortune Brands, where he held various positions. Previously, he spent nine years with McDonald’s Corporation. Mr. Hilario received his Bachelor of Science and Commerce degree in accounting from Santa Clara University and is a certified public accountant.

Michael B. Liedberg (age 44) joined McCormick & Schmick’s in January 2004 and was appointed executive vice president of operations in January 2007. From 2004 through 2006, he was vice president of operations. Mr. Liedberg has over 20 years of management experience in the restaurant industry including service as the president and chief executive officer of Desert Moon Restaurants from December 2001 to January 2004. Before 2001, Mr. Liedberg held various positions for thirteen years with Avado Brands, Inc. Mr. Liedberg’s education includes a certificate from the Management Program at Georgia Institute of Technology and a Human Resources Certificate from the University of Georgia.

Jerry R. Kelso (age 53) has been our chief internal audit and compliance officer since April 2004. Mr. Kelso joined us in 1984 as our controller and was vice president of finance and chief financial officer from 1988 to April 2004. He previously worked for local certified public accounting firms. Mr. Kelso received his Bachelor of Arts degree from Central Washington State College and became a certified public accountant in 1983.

Jeffrey H. Skeele (age 52) has been a vice president of operations of McCormick & Schmick’s since 1998. He also has held the positions of senior manager (1991-1996) and general manager (1986-1988). From 1988 to 1991, Mr. Skeele was a vice president at West Group Partners. Mr. Skeele graduated from the University of Oregon.

David E. Jenkins (age 60) has been a vice president of operations since joining McCormick & Schmick’s in 1997. Before that, Mr. Jenkins was a regional manager of Island Restaurants (1992-1996), the owner and operator of Santa Fe East (1988-1991), a general manager of Landi Brothers (1982-1987), and the general manager of Hamburger Hamlet (1978-1981). Mr. Jenkins received his Bachelor of Arts degree from the University of Tampa.

19

Martin P. Gardner (age 46) has been our vice president of finance since January 2007. Mr. Gardner joined us in 2004 and previously served as our director of finance. From 2000 to 2004 Mr. Gardner was corporate controller of Lexar, Inc. From 1995 to 2000, Mr. Gardner held various management positions, including corporate controller, for Mattson Technology, Inc. Mr. Gardner received his Bachelor of Science degree in accounting from San Jose State University, his Master of Science degree in finance from Golden Gate University and is a certified public accountant.

William H.P. King (age 55) has been vice president of culinary development & training of McCormick & Schmick’s since 2006. Mr. King joined McCormick & Schmick’s in 1985 and has held various positions, including executive chef, regional senior chef and executive director of training & culinary development. Mr. King attended Cornell University’s School of Hotel and Restaurant Administration and has over 30 years experience in the culinary and hospitality industry.

Steven B. Foote (age 47) has been a vice president of operations of McCormick & Schmick’s since January 2007. Mr. Foote also has held the positions of regional senior chef (2003-2006) and executive chef (1999-2003). Mr. Foote had over 12 years of chef and related culinary experience prior to joining McCormick & Schmick’s.

20

PART II

ITEM 5. MARKET FOR THE REGISTRANT’S COMMON EQUITY AND RELATED STOCKHOLDER MATTERS

Market Information

Our common stock is listed on the NASDAQ Global Stock Market under the symbol “MSSR”. The table below sets forth the high and low closing price for our common stock in the first, second, third and fourth quarters of fiscal 2006 and 2005, as reported by the NASDAQ Global Stock Market.

| | | | | | |

| | | Sales Price |

| | | High | | Low |

4th Quarter 2006 | | $ | 26.50 | | $ | 21.46 |

3rd Quarter 2006 | | | 24.33 | | | 17.15 |

2nd Quarter 2006 | | | 27.52 | | | 21.25 |

1st Quarter 2006 | | | 25.47 | | | 20.16 |

4th Quarter 2005 | | | 25.86 | | | 19.21 |

3rd Quarter 2005 | | | 19.80 | | | 15.02 |

2nd Quarter 2005 | | | 16.75 | | | 14.82 |

1st Quarter 2005 | | | 17.58 | | | 13.85 |

21

Stock Performance Graph

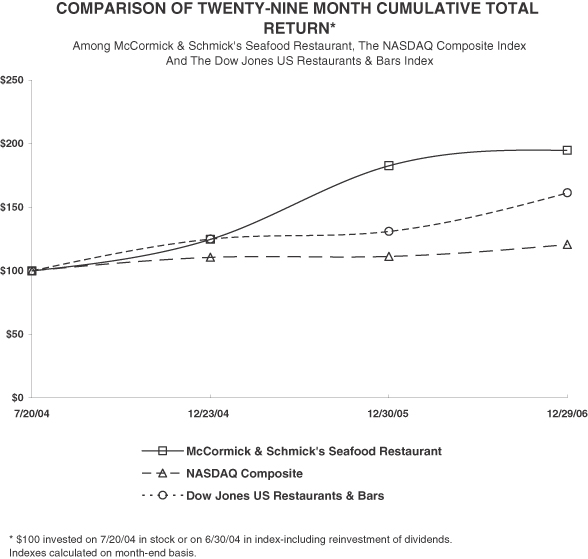

The following graph compares the total return on an indexed basis of a $100 investment in our common stock, the Nasdaq Composite Index and the Dow Jones U.S. Restaurants and Bars Index. For comparison purposes, the data points of our common stock are as of July 20, 2004, the day our common stock was first sold in our initial public offering, and December 23, 2004, December 30, 2005, and December 29, 2006, the last trading day in our fiscal years 2004, 2005 and 2006, respectively. The data points for both the NASDAQ Composite Index and the Dow Jones U.S. Restaurants & Bars Index are as of July 20, 2004 and the last trading day in December 2004, 2005 and 2006. The historical stock performance presented below is not intended to and may not be indicative of future stock performance.

| | | | | | | | | | | | |

| | | 7/04 | | 12/04 | | 12/05 | | 12/06 |

McCormick & Schmick’s Seafood Restaurant | | $ | 100.00 | | $ | 124.80 | | $ | 182.74 | | $ | 194.81 |

NASDAQ Composite | | $ | 100.00 | | $ | 110.69 | | $ | 111.35 | | $ | 120.82 |

Dow Jones US Restaurants & Bars | | $ | 100.00 | | $ | 125.02 | | $ | 131.08 | | $ | 161.43 |

22

Holders of Record

As of February 27, 2007 there were approximately 31 holders of record of our common stock.

Dividend Policy

We expect to retain all of our earnings to finance the expansion and development of our business and we have not paid dividends in the prior two fiscal years and have no plans to pay cash dividends to our stockholders for the foreseeable future. The payment of dividends is within the discretion of our board of directors and will depend upon our earnings, capital requirements and operating and financial condition, among other factors. Our revolving credit agreement restricts our ability to pay dividends.

Securities Authorized for Issuance Under Equity Compensation Plans

The following table provides information about compensation plans (including individual compensation arrangements) under which our equity securities are authorized for issuance to employees or non-employees (such as directors and consultants), at December 30, 2006.

| | | | | | | |

| | | Number of

securities to be

issued upon

exercise of

outstanding options | | Weighted-

average

exercise price of

outstanding

options | | Number of securities

remaining available for

future issuance under

equity compensation

plans (excluding

securities reflected in

column(a)) |

| | | (a) | | (b) | | (c) |

Equity compensation plans approved by security holders: | | | | | | | |

2004 Stock Incentive Plan | | 832,846 | | $ | 12.00 | | 520,028 |

Issuer Purchases of Equity Securities

We did not repurchase any of our equity securities during 2006.

23

ITEM 6. SELECTED FINANCIAL DATA

The selected consolidated financial and operating data below are derived from our consolidated financial statements for the fiscal years 2002, 2003, 2004, 2005 and 2006, which have been audited by an independent registered public accounting firm.

The selected consolidated financial and operating data below represent portions of our financial statements, which should be read together with Part II—Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the related notes included in Part II—Item 8. Historical results are not necessarily indicative of future performance.

| | | | | | | | | | | | | | | | | | | |

| | | Year Ended | |

| | | 2002 | | | 2003 | | | 2004 | | | 2005 | | 2006 | |

| | | (in thousands, except per share data) | |

Statement of Operations Data: | | | | | | | | | | | | | | | | | | | |

Revenues | | $ | 180,104 | | | $ | 196,717 | | | $ | 238,757 | | | $ | 278,813 | | $ | 308,323 | |

| | | | | | | | | | | | | | | | | | | |

Restaurant operating costs | | | | | | | | | | | | | | | | | | | |

Food and beverage | | | 53,168 | | | | 57,959 | | | | 70,873 | | | | 81,630 | | | 89,443 | |

Labor | | | 56,147 | | | | 61,644 | | | | 75,081 | | | | 86,823 | | | 95,886 | |

Operating | | | 26,406 | | | | 29,244 | | | | 35,204 | | | | 41,857 | | | 46,044 | |

Occupancy | | | 15,349 | | | | 16,890 | | | | 21,401 | | | | 24,790 | | | 27,650 | |

| | | | | | | | | | | | | | | | | | | |

Total restaurant operating costs | | | 151,070 | | | | 165,737 | | | | 202,559 | | | | 235,100 | | | 259,023 | |

| | | | | |

General and administrative expenses | | | 7,576 | | | | 9,769 | | | | 12,062 | | | | 15,105 | | | 16,651 | |

Restaurant pre-opening costs | | | 1,006 | | | | 1,219 | | | | 2,393 | | | | 2,496 | | | 2,892 | |

Depreciation and amortization | | | 8,808 | | | | 9,853 | | | | 10,723 | | | | 9,608 | | | 10,640 | |

Management fees and covenants not to compete | | | 2,550 | | | | 2,550 | | | | 4,241 | | | | — | | | — | |

Impairment of assets | | | — | | | | 1,513 | | | | — | | | | — | | | — | |

| | | | | | | | | | | | | | | | | | | |

Total costs and expenses | | | 171,010 | | | | 190,641 | | | | 231,978 | | | | 262,309 | | | 289,206 | |

| | | | | | | | | | | | | | | | | | | |

Operating income | | | 9,094 | | | | 6,076 | | | | 6,779 | | | | 16,504 | | | 19,117 | |

Interest expense (income), net | | | 3,720 | | | | 3,069 | | | | 2,680 | | | | 550 | | | (228 | ) |

Accrued dividends and accretion on mandatorily redeemable preferred stock | | | — | | | | 1,901 | | | | 5,759 | | | | — | | | — | |