NEWPORT GOLD, INC.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definition of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

NEWPORT GOLD, INC.

There are statements in this report that are not historical facts. These “forward-looking statements” can be identified by use of terminology such as “believe,” “hope,” “may,” “anticipate,” “should,” “intend,” “plan,” “will,” “expect,” “estimate,” “project,” “positioned,” “strategy,” and similar expressions. You should be aware that these forward-looking statements are subject to risks and uncertainties that are beyond our control. For a discussion of these risks, you should read this entire report carefully, especially the risks discussed under the section entitled “Risk Factors.” Although management believes that the assumptions underlying the forward-looking statements included in this report are reasonable, these assumptions do not guarantee our future performance, and actual results could differ from those contemplated by these forward-looking statements. The assumptions used for purposes of the forward-looking statements specified in the following information represent estimates of future events and are subject to uncertainty as to possible changes in economic, legislative, industry, and other circumstances. As a result, the identification and interpretation of data and other information and their use in developing and selecting assumptions from and among reasonable alternatives require the exercise of judgment. To the extent that the assumed events do not occur, the outcome may vary substantially from anticipated or projected results, and, accordingly, no opinion is expressed about the achievability of those forward-looking statements. In light of these risks and uncertainties, there can be no assurance that the results and events contemplated by the forward-looking statements contained in this report will, in fact, transpire. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of their dates. We do not undertake any obligation to update or revise any forward-looking statements.

We have not had any bankruptcy, receivership or similar proceeding since incorporation. There have been no material reclassifications, mergers, consolidations or purchases or sales of any significant amount of assets not in the ordinary course of business since the date of incorporation.

Our principal executive offices are located at 8 Nettleton Court, Collingwood, Ontario, Canada L9Y 5B9 and our telephone number is (905) 542-4990.

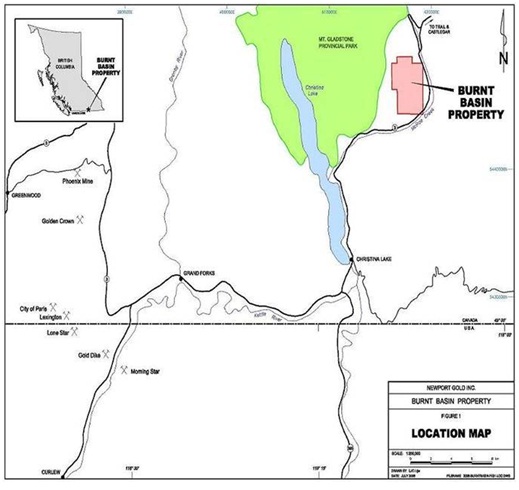

On July 21, 2003, we entered into an option agreement with Steve Baran to acquire certain mineral claims located in British Columbia, Canada known as the Burnt Basin mineral claims. The Burnt Basin property is owned by John W. Carson and the option agreement is subject to an underlying agreement between Mr. Carson and Mr. Baran, dated July 29, 2002. The Burnt Basin property is situated about 25 kilometers northeast of Grand Forks, British Columbia in Canada. The property covers an area of 1694 hectares and is comprised of 10 mineral claims.

Under the terms of the option agreement, we have acquired a 100% undivided interest in the property, subject to a 1% Net Smelter Return (NSR) royalty, in consideration for cash and share payments totaling $17,000 which has been paid and 225,000 shares of our common stock which have been issued, and by incurring exploration expenses totaling CDN $250,000 which condition has been met by the Company. The NSR royalty is payable to John Carson and is capped at CDN $250,000, and is provided by making annual CDN $10,000 prepaid NSR payments beginning in September 2003. To date, we have paid Mr. Carson CDN $100,000 of prepaid NSR royalties. A second 1% NSR Royalty was to have been paid to Steve Baran but, pursuant to a letter agreement dated as of March 26, 2013, Mr. Baran has agreed that no additional NSR payments shall be due to Mr. Baran now or in the future in connection with the Option Agreement.

NSR royalties are defined in the option agreement as the net proceeds realized from the sale to a bona fide purchaser in an arm’s length transaction of minerals recovered from ore mined from the claims. The net proceeds are determined by deducting from the dollar value paid for the recovered minerals, the cost of smelting and refining the ore/or concentrates thereof, marketing and insurance charges, and transportation costs, including the costs of transporting the ore and /or concentrates thereof to the milling facilities and to the smelter or refinery.

Provided we are able to obtain the necessary capital, we intend to commence and complete the updated Phase 1 program as recommended in the most recent technical report for the Burnt Basin property (see “Program of Exploration” below) over the next twelve months. In this regard, we anticipate that we will need at least $400,000 in financing in order to achieve our goals and objectives over the next twelve months, which includes $250,000 to complete the Phase 1 program and at least $150,000 for operations. This does not include any amounts which will be due to Derek Bartlett, our President, under the terms of his Management Services Agreement.

A mining claim is generally described to be that portion of the public mineral lands which a miner, for mining purposes, takes and holds in accordance with local mining laws but is also described to mean a parcel of land which might contain precious metals in the soil or rock. Prior to 2005, mineral claims in British Columbia were acquired by physically marking the claim boundaries on the ground. In 2005, an on-line system of staking was established in British Columbia, known as the Mineral Title Online System (“MTO”), where claims are acquired by selecting one or more predetermined grid cells. Sizes of these claims vary, depending on the number of grid cells selected. These on-line claims are referred to as MTO claims, where pre-2005 claims are referred to as legacy claims. The Burnt Basin property consists of 9 MTO claims and 1 legacy claim, covering a total area of 1694 hectares.

The Burnt Basin mineral claims were originally staked in 2002 by John Carson. Mr. Carson owns the mineral claims and optioned these claims to Mr. Baran on July 29, 2002, which was subsequently optioned to us on July 18, 2003. We, through an option agreement, hold the mining rights to the Burnt Basin mineral claims which thereby gives us or our designated agent, the rights to mine and recover all of the minerals contained within the surface boundaries of the claim continued vertically downward.

As mentioned above, prior to 2005, in order to stake a claim, it was physically marked on the ground whereby miners had to physically go to their desired parcel of land and place posts into the ground outlining the location of their claim. They then had to travel to their local mining recorder’s office to register the claim and pay the appropriate fees. This was known as a ground staking system. The legislation in British Columbia changed in December 2004 and became effective on January 12, 2005 which changed the system to a map based online system. For part of 2005, holders of such pre-2005 claims (legacy claims) were given an opportunity to convert the claims to the new system. With the exception of one claim, all of the pre-2005 claims on the Burnt Basin property were converted to new MTO claims. As a result, the Burnt Basin property now consists of 9 MTO claims and 1 legacy claim. See “Property Description and Location” below.

All Canadian lands and minerals which have not been granted to private persons are owned by either the federal or provincial governments in the name of Her Majesty. Ungranted minerals are commonly known as Crown minerals. Ownership rights to Crown minerals are vested by the Canadian Constitution in the province where the minerals are located. In the case of the Burnt Basin mineral claims, that is the province of British Columbia.

In the 19th century the practice of reserving the minerals from fee simple Crown grants was established. The legislation ensures that minerals are reserved from Crown land dispositions. The result is that the Crown is the largest mineral owner in Canada, both as fee simple owner of Crown lands and through mineral reservations in Crown grants. Most privately held mineral titles are acquired directly from the Crown. The Burnt Basin mineral claim is one such acquisition. Accordingly, fee simple title to the Burnt Basin mineral claims resides with the Crown. The Burnt Basin property is comprised of mining claims issued pursuant to the British Columbia Mineral Act to Mr. John Carson. The lessee has exclusive rights to mine and recover all of the minerals contained within the surface boundaries of the lease continued vertically downward.

The Burnt Basin mineral claims are unencumbered and there are no competitive conditions which affect the Burnt Basin mineral claims. Further, there is no insurance covering the Burnt Basin mineral claims. We believe that no insurance is necessary since the Burnt Basin mineral claims is unimproved and contains no buildings or improvements.

Environmental Laws

We will also have to sustain the cost of reclamation and environmental remediation for all work undertaken which causes sufficient surface disturbance to necessitate reclamation work. Both reclamation and environmental remediation refer to putting disturbed ground back as close to its original state as possible. Other potential pollution or damage must be cleaned-up and renewed along standard guidelines outlined in the usual permits. Reclamation is the process of bringing the land back to a natural state after completion of exploration activities. Environmental remediation refers to the physical activity of taking steps to remediate, or remedy, any environmental damage caused, i.e. refilling trenches after sampling or cleaning up fuel spills. Our Phase 1 and 2 programs do not require any reclamation or remediation other than minor clean up and removal of supplies because of minimal disturbance to the ground. The amount of these costs is not known at this time as we do not know the extent of the exploration program we will undertake, beyond completion of the recommended two phases described above. Because there is presently no information on the size, tenure, or quality of any resource or reserve at this time, it is impossible to assess the impact of any capital expenditures on our earnings or competitive position in the event a potentially economic deposit is discovered.

Available Information

We are subject to the informational requirements of the Securities Exchange Act of 1934, as amended, and file annual, quarterly and current reports, proxy statements and other information with the Securities and Exchange Commission (“SEC”). Such reports, proxy statements and other information may be inspected at the public reference room of the SEC at 100 F Street, N.E., Washington D.C. 20549. Copies of such material can be obtained from the facility at prescribed rates. Please call the SEC toll free at 1-800-SEC-0330 for information about its public reference room. Because we file documents electronically with the SEC, you may also obtain this information by visiting the SEC’s Internet website at http://www.sec.gov.

Item 1A. Risk Factors.

An investment in our securities is highly speculative and extremely risky. You should carefully consider the following risks, in addition to the other information contained in this report, before deciding to invest in our securities.

Risks Related to Our Business

Our auditors have expressed substantial doubt about our ability to continue as a going concern.

Our financial statements have been prepared assuming that we will continue as a going concern. The general business strategy of the Company is to explore and research existing mineral properties and to potentially acquire further claims either directly or through the acquisition of operating entities. The continued operations of the Company depends upon the recoverability of mineral property reserves, confirmation of the Company’s interest in the underlying mineral claims, the ability of the Company to obtain necessary financing to complete the development of these claims and upon the future profitable production of the claims. There continues to be insufficient funds to provide enough working capital to fund ongoing operations for the next twelve months. Management intends to raise additional capital through share issuances to finance its exploration on the Burnt Basin Property although there can be no assurance that management will be successful in these efforts.

The Company has a working capital deficit at December 31, 2012 of $164,000, has an accumulated deficit during the exploration stage of $4,487,000 and has not generated any operating revenue to date. These factors raise substantial doubt about the Company’s ability to continue as a going-concern, which is dependent on the Company’s ability to obtain and maintain an appropriate level of financing on a timely basis and to achieve sufficient cash flows to cover obligations and expenses. The outcome of the above matters cannot be predicted at this time. The financial statements do not give effect to any adjustments to the amounts and classifications of assets and liabilities, which might be necessary should the Company be unable to continue as a going-concern.

Unfavorable economic conditions may have a material adverse effect on us since raising capital to continue our operations could be more difficult.

Uncertainty and negative trends in general economic conditions in the United States, Canada and abroad, including significant tightening of credit markets and a general economic decline, have created a difficult operating environment for our business and other companies in our industry. Depending upon the ultimate severity and duration of any economic downturn, the resulting effects on our business could be materially adverse if we are unable to raise the working capital required to carry out our business plan.

If we do not have the funds to make required payments on our mineral claims, we could lose our rights to the claims.

To retain our interests in our mineral claims, we have to make certain required payments. If we do not have the funds to make these payments as they come due, we may lose our interests in such mineral claims.

Under the terms of the option agreement for the Burnt Basin property, we are required among other things to pay a 1% NSR royalty to John Carson (the owner of the property) capped at CDN $250,000, that will be provided by making annual CDN $10,000 prepaid NSR payments beginning in September 2003. While all such prepaid NSR royalties have been paid to date, no assurance can be made that we will be able to continue to make such payments in the future. If we are unable to meet such payment obligations, Mr. Carson may have the right to seek to void any interests we have in the property.

If we are unable to perform required assessment work annually, we could lose our rights to the claims.

Mineral claims within the province of British Columbia require assessment work (such as geological mapping, geochemical or geophysical surveys, trenching or diamond drilling) be completed each year to maintain title to the ground. New regulations regarding work obligations to maintain tenure went into effect in British Columbia on July 1, 2012. As of July 1, 2012, annual work commitments are determined by a four tier structure, as follows:

$5.00 per hectare for anniversary years 1 & 2

$10.00 per hectare for anniversary years 3 & 4

$15.00 per hectare for anniversary years 5 & 6

$20.00 per hectare for subsequent anniversary years

All claims in British Columbia will be set back to the year 1 requirement, regardless of how many years have elapsed since staking. For the Burnt Basin property, this means that the annual work commitment to advance the expiry dates by 2 years (to Dec. 30, 2017) will be $5 per hectare per year, or a total of about $16,940 for 2 years. Thereafter the work commitment increases, according to the above schedule. Expenditures exceeding the minimum requirement can be credited to future years assessment credits, to a maximum of 10 years in advance. Presently, the Burnt Basin claims are in good standing until the year 2015, and further work is not required until that time. If we are unable after that time to perform any additional assessment work, we may not be able to maintain our rights to the claims.

The exploration and mining industry is highly competitive.

We face significant competition in our business of exploration and mining, a business in which we will compete with other mineral resource exploration and development companies for financing and for the acquisition of new mineral properties. Many of the mineral resource exploration and development companies with whom we compete have greater financial and technical resources than us. Accordingly, these competitors may be able to spend greater amounts on acquisitions of mineral properties of merit, on exploration of their mineral properties and on development of their mineral properties. In addition, they may be able to afford greater geological expertise in the targeting and exploration of mineral properties. This competition could result in competitors having mineral properties of greater quality and interest to prospective investors who may finance additional exploration and development. This competition could adversely impact on our ability to finance further exploration and to achieve the financing necessary for us to develop our mineral properties.

Our mineral exploration efforts are highly speculative; we have not yet established any proven or probable reserves.

Mineral exploration is highly speculative. It involves many risks and is often non-productive. Even if we believe we have found a valuable mineral deposit, it may be several years before production is possible. During that time, it may become no longer feasible to produce those minerals for economic, regulatory, political, or other reasons. Additionally, we may be required to make substantial capital expenditures and to construct mining and processing facilities. As a result of these costs and uncertainties, we may be unable to start, or if started, to finish our exploration activities. In addition, we have not to date established any proven or probable reserves on our mining properties and there can be no assurance that such reserves will ever be established.

Mining operations in general involve a high degree of risk, which we may be unable, or may not choose to insure against, making exploration and/or development activities we may pursue subject to potential legal liability for certain claims.

Our operations are subject to all of the hazards and risks normally encountered in the exploration, development and production of minerals. These include unusual and unexpected geological formations, rock falls, flooding and other conditions involved in the drilling and removal of material, any of which could result in damage to, or destruction of, mines and other producing facilities, damage to life or property, environmental damage and possible legal liability. Although we plan to take adequate precautions to minimize these risks, and risks associated with equipment failure or failure of retaining dams which may result in environmental pollution, there can be no assurance that even with our precautions, damage or loss will not occur and that we will not be subject to liability which will have a material adverse effect on our business, results of operation and financial condition.

Because of the unique difficulties and uncertainties inherent in mineral exploration ventures, we face a high risk of business failure.

Stockholders should be aware of the difficulties normally encountered by new mineral exploration companies and the high rate of failure of such enterprises. The likelihood of success must be considered in light of the problems, expenses, difficulties, complications and delays encountered in connection with the exploration of the mineral properties that we plan to undertake. These potential problems include, but are not limited to, unanticipated problems relating to exploration, and additional costs and expenses that may exceed current estimates. Most exploration projects do not result in the discovery of commercially mineable deposits. Problems such as unusual or unexpected formations and other conditions are involved in mineral exploration and often result in unsuccessful exploration efforts.

Because of the inherent dangers involved in mineral exploration, there is a risk that we may incur liability or damages as we conduct our business.

The search for valuable minerals involves numerous hazards. As a result, we may become subject to liability for such hazards, including pollution, cave-ins and other hazards against which we cannot insure or against which we may elect not to insure. At the present time, we have no coverage to insure against these hazards. The payment of such liabilities may result in our inability to complete our planned exploration program and/or obtain additional financing to fund our exploration program.

We have no known ore reserves and we cannot guarantee we will find any mineral reserves or if we find minerals, that production will be profitable.

We have no known ore reserves. We have not identified gold or other metal or mineral in proven economic amounts on the property and we cannot guaranty that we will ever find any such minerals. Even if we find that there are mineral reserves on our property, we cannot guaranty that we will be able to recover these minerals. Even if we recover mineral reserves, we cannot guaranty that we will make a profit. If we cannot find mineral reserves or it is not economical to recover these mineral reserves, we will have to cease operations. Because the probability that any of the prospects will ever have mineral reserves is extremely low, any funds spent on exploration will probably be lost.

Weather interruptions in the province of British Columbia may affect and delay our exploration operations.

While exploration can generally be performed year round in the province of British Columbia, such region is periodically subject to extreme weather conditions such as severe snow or rain that could cause roads leading to our claims to be impassible. When roads are impassable, we are unable to easily conduct exploration operations on our property.

Our exploration efforts and limited capital may limit our ability to find mineralized material. If we do not find mineralized material, we will cease operations.

Because we are small and do not have much capital, we must limit our exploration. Because we may have to limit our exploration, we may not find mineralized material, although our property may contain mineralized material. If we do not find mineralized material, we will cease operations.

We may not have access to all of the supplies and materials we need to begin exploration which could cause us to delay or suspend operations.

Competition and unforeseen limited sources of supplies in the industry could result in occasional spot shortages of supplies, such as explosives, and certain equipment such as bulldozers and excavators that we might need to conduct exploration. We have not attempted to locate or negotiate with any suppliers of products, equipment or materials. We will attempt to locate products, equipment and materials in the future. If we cannot find the products and equipment we need, we will have to suspend our exploration plans until we do find the products and equipment we need.

We have not yet discovered any mineral reserves. Even if we are successful in discovering mineral reserves we may not be able to realize a profit from its sale. If we cannot make a profit, we will have to cease operations until market conditions improve or cease operations altogether.

In order to maintain operations, we will have to sell any minerals we extract from our property for more than it costs us to mine it. (The lower the price the mineral, the more difficult it is to do this.) If we cannot make a profit, we will have to cease operations until the price of minerals found on our property increases or cease operations altogether. The cost to mine minerals is fixed and as a result, the lower the market price, the lower the likelihood we will be able to make a profit.

If other professional duties of our current management team interfere or conflict with their duties for the Company, our business, results of operations and financial condition could be materially and adversely affected.

Our officers and directors do not devote all of their time and energy to the business of the Company and are involved in other businesses including other mining companies. If the performance of their duties on behalf of such other entities interfere or conflict with their duties as officers and directors of the Company, we may not be able to achieve our anticipated growth and our business, results of operations and financial condition could be materially adversely affected. In addition, a conflict of interest between the Company and one of these other mining companies may arise from time to time. We have not formulated a policy for the resolution of such potential conflicts of interest. Failure by management to resolve conflicts of interest in favor of the Company could result in liability of management to us. However, any attempt by stockholders to enforce a liability of management to us would most likely be prohibitively expensive and time consuming.

Risks Related to Our Common Stock

We do not intend to pay dividends in the foreseeable future.

We have never declared or paid a dividend on our common stock. We intend to retain earnings, if any, for use in the operation and expansion of our business and, therefore, do not anticipate paying any dividends in the foreseeable future.

The trading price of our common stock may be volatile.

We currently anticipate that the market for our common stock will remain limited, sporadic, and illiquid until such time as we generate significant revenues, if ever, and that the market for our common stock will be subject to wide fluctuations in response to several factors, including, but not limited to the risk factors set forth in this report as well as the depth and liquidity of the market for our common stock, investor perceptions of the Company, and general economic and similar conditions. In addition, we believe that there are a small number of market makers that make a market in our common stock. The actions of any of these market makers could substantially impact the volatility of the Company’s common stock.

Efforts to comply with recently enacted changes in securities laws and regulations will increase our costs and require additional management resources, and we still may fail to comply.

As directed by Section 404 of the Sarbanes-Oxley Act of 2002, the Securities and Exchange Commission adopted rules requiring public companies to include a report of management on our internal controls over financial reporting in their annual reports on Form 10-K. If we are unable to conclude that we have effective internal controls over financial reporting, investors could lose confidence in the reliability of our financial statements, which could result in a decrease in the value of our securities.

Substantial sales of our common stock could adversely affect our stock price.

We had 57,310,070 shares of common stock outstanding as of December 31, 2012. Sales of a substantial number of shares of common stock, or the perception that such sales could occur, could adversely affect the market price of our common stock by introducing a large number of sellers to the market. Such sales could cause the market price of our common stock to decline. We cannot predict whether future sales of our common stock, or the availability of our common stock for sale, will adversely affect the market price for our common stock or our ability to raise capital by offering equity securities.

Our common stock is a penny stock.

Our common stock is classified as a penny stock, which trades over-the-counter. As a result, an investor may find it more difficult to dispose of or obtain accurate quotations as to the price of the shares of the common stock. In addition, the “penny stock” rules adopted by the Securities and Exchange Commission subject the sale of the shares of the common stock to certain regulations which impose sales practice requirements on broker-dealers. For example, broker-dealers selling such securities must, prior to effecting the transaction, provide their customers with a document that discloses the risks of investing in such securities. Furthermore, if the person purchasing the securities is someone other than an accredited investor or an established customer of the broker-dealer, the broker-dealer must also approve the potential customer’s account by obtaining information concerning the customer’s financial situation, investment experience and investment objectives. The broker-dealer must also make a determination whether the transaction is suitable for the customer and whether the customer has sufficient knowledge and experience in financial matters to be reasonably expected to be capable of evaluating the risk of transactions in such securities. Accordingly, the Commission’s rules may result in the limitation of the number of potential purchasers of the shares of the common stock. In addition, the additional burdens imposed upon broker-dealers by such requirements may discourage broker-dealers from effecting transactions in the Common Stock, which could severely limit the market of the Company’s common stock.

The over-the-counter market is vulnerable to market fraud.

Securities which trade over-the-counter are frequent targets of fraud or market manipulation, both because of their generally low prices and because reporting requirements for such securities are less stringent than those of the stock exchanges or NASDAQ.

Increased dealer compensation could adversely affect stock price.

Over-the-counter market dealers’ spreads (the difference between the bid and ask prices) may be large, causing higher purchase prices and less sale proceeds for investors.

Item 1B. Unresolved Staff Comments.

We are a smaller reporting company as defined by Rule 12b-2 of the Securities Exchange Act of 1934 and are not required to provide the information under this item.

See “Item 1. Description of Business” for a description of our mining property interests.

The Company neither rents nor owns any properties. The Company uses the office space and equipment of its management which offices are located at 8 Nettleton Court, Collingwood, Ontario, Canada L9Y 5B9.

Item 3. Legal Proceedings.

We are not currently a party to any pending material legal proceeding nor are we aware of any proceeding contemplated by any individual, company, entity or governmental authority involving the Company.

Item 4. Mine Safety Disclosures.

Not applicable.

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Market Information

Our common stock is quoted on the OTCQB, officially part of the OTC Market Group’s OTC Link quotation system, under the symbol “NWPG”. The OTCQB is a relatively new market started in April 2010 for OTC traded companies that are current in their reporting obligations to the SEC. The following table sets forth the range of high and low sales prices per share of the common stock for each of the calendar quarters identified below. These quotations represent inter-dealer prices, without retail mark-up, markdown or commission, and may not represent actual transactions.

| Year ending December 31, 2011 | | High | | | Low | |

| | | | | | | |

| Jan, 1, 2011 to March 31, 2011 | | $ | 0.055 | | | $ | 0.015 | |

| April 1, 2011 to June 30, 2011 | | $ | 0.20 | | | $ | 0.04 | |

| July 1, 2011 to Sept. 30, 2011 | | $ | 0.15 | | | $ | 0.05 | |

| Oct. 1, 2011 to Dec. 31, 2011 | | $ | 0.10 | | | $ | 0.0312 | |

| | | | | | | | | |

| Year ending December 31, 2012 | | High | | | Low | |

| | | | | | | | | |

| Jan, 1, 2012 to March 31, 2012 | | $ | 0.05 | | | $ | 0.01 | |

| April 1, 2012 to June 30, 2012 | | $ | 0.05 | | | $ | 0.02 | |

| July 1, 2012 to Sept. 30, 2012 | | $ | 0.08 | | | $ | 0.02 | |

| Oct. 1, 2012 to Dec. 31, 2012 | | $ | 0.10 | | | $ | 0.07 | |

Holders

As of December 31, 2012, there were approximately 150 stockholders of record of our common stock. This does not reflect persons or entities that hold their stock in nominee or “street name”.

Dividends

The Company has not paid any cash dividends to date, and it has no intention of paying any cash dividends on its common stock in the foreseeable future. The declaration and payment of dividends is subject to the discretion of its Board of Directors and to certain limitations imposed under Nevada corporate law. The timing, amount and form of dividends, if any, will depend on, among other things, results of operations, financial condition, cash requirements and other factors deemed relevant by the Board of Directors.

Recent Sales of Unregistered Securities

The following sets forth certain information concerning securities which were sold or issued by us without the registration of the securities under the U.S. Securities Act of 1933, as amended (the “Securities Act”) in reliance on exemptions from such registration requirements during the years ended December 31, 2011 and 2012:

During the quarter ended September 30, 2011, the Company sold in a private placement with three investors a total of 2,000,000 units at a price of $0.10 per unit for gross proceeds of $200,000. Each unit consisted of one share of common stock and one common stock purchase warrant with an exercise price of $0.10 that expires two years from date of issuance. The securities were issued in reliance upon the exemption from registration pursuant to Section 4(2) of the Securities Act of 1933, as amended, and Regulation S thereunder. All investors represented and warranted that they were non-U.S. persons within the meaning of Regulation S.

During the quarter ended September 30, 2012, the Company sold in a private placement with three investors a total of 1,940,000 units at a price of $0.05 per unit for gross proceeds of $97,848. Each unit consisted of one share of common stock and one common stock purchase warrant with an exercise price of $0.05 that expires two years from date of issuance. Insofar that the units were paid for by the investors in Canadian dollars, such investors agreed that any additional purchase price which may have been paid for the units (which in this case was $848 in the aggregate), due to the differences in the exchange rate between U.S. and Canadian dollars, shall be deemed a capital contribution. The securities were issued in reliance upon the exemption from registration pursuant to Section 4(2) of the Securities Act of 1933, as amended, and Regulation S thereunder. All investors represented and warranted that they were non-U.S. persons within the meaning of Regulation S.

On December 28, 2012, Derek Bartlett, President and Chief Executive Officer of the Company, assigned to Alex Johnston all of Mr. Bartlett’s right, title and interest in and to a debt owing from the Company to Mr. Bartlett of U.S. $370,927 for accrued officer salaries (the “Assigned Bartlett Debt”). Pursuant to a Conversion and Subscription Agreement dated December 28, 2012 between the Company and Mr. Johnston, Mr. Johnston agreed to convert the Assigned Bartlett Debt into 18,546,350 shares of common stock of the Company, and the Company agreed to issue such shares to Mr. Johnston, in full and complete settlement of the Assigned Bartlett Debt. The securities were issued in reliance upon the exemption from registration pursuant to Section 4(2) of the Securities Act of 1933, as amended, and Regulation S thereunder. Mr. Johnston represented and warranted that he was a non-U.S. person within the meaning of Regulation S.

Item 6. Selected Financial Data.

We are a smaller reporting company as defined by Rule 12b-2 of the Securities Exchange Act of 1934 and are not required to provide the information under this item.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

This discussion summarizes the significant factors affecting the operating results, financial condition, liquidity and cash flows of the Company and its subsidiaries for the fiscal years ended December 31, 2012 and 2011. The discussion and analysis that follows should be read together with the consolidated financial statements of Newport Gold, Inc. and the notes to the consolidated financial statements included elsewhere in this report. Except for historical information, the matters discussed in this section are forward looking statements that involve risks and uncertainties and are based upon judgments concerning various factors that are beyond the Company’s control.

OVERVIEW

Newport Gold, Inc., a pre-exploration stage company, was incorporated on July 16, 2003 in the State of Nevada, and is involved in the acquisition, exploration and development of mineral and energy properties. We have two subsidiary companies, 2038052 Ontario Inc., an Ontario incorporated company, and NPG Mining Corp., a British Columbia incorporated company. Unless otherwise noted, references in this report to the “Company,” “we,” “our,” or “us” mean Newport Gold, Inc. and its wholly-owned Canadian subsidiaries, 2038052 Ontario Inc. and NPG Mining Corp.

On July 21, 2003, we entered into an option agreement with Steve Baran to acquire certain mineral claims located in British Columbia, Canada known as the Burnt Basin mineral claims. The Burnt Basin property is owned by John W. Carson and the option agreement is subject to an underlying agreement between Mr. Carson and Mr. Baran, dated July 29, 2002. The Burnt Basin property is situated about 25 kilometers northeast of Grand Forks, British Columbia in Canada. The property covers an area of 1694 hectares and is comprised of 10 mineral claims.

Under the terms of the option agreement, we have acquired a 100% undivided interest in the property, subject to a 1% Net Smelter Return (NSR) royalty , in consideration for cash and share payments totaling $17,000 which has been paid and 225,000 shares of our common stock which have been issued, and by incurring exploration expenses totaling CDN $250,000 which condition has been met by the Company. The NSR royalty is payable to John Carson and is capped at CDN $250,000, and is provided by making annual CDN $10,000 prepaid NSR payments beginning in September 2003. To date, we have paid Mr. Carson CDN $100,000 of prepaid NSR royalties. A second 1% NSR Royalty was to have been paid to Steve Baran but, pursuant to a letter agreement dated as of March 26, 2013, Mr. Baran has agreed that no additional NSR payments shall be due to Mr. Baran now or in the future in connection with the Option Agreement.

As indicated above, we have met the cash, share and expenditure commitments outlined in the agreement and have earned the 100% interest in the property, subject to the NSR commitment. Pursuant to transfers of ownership filed with the Province of British Columbia in August 2008, such 100% undivided interest in the Burnt Basin mineral claims are now held by us. Such interests are registered in the name of NPG Mining Corp., a British Columbia incorporated company and wholly owned subsidiary of Newport Gold, Inc. We do not hold any title to any surface rights within the limits of the property.

NSR royalties are defined in the option agreement as the net proceeds realized from the sale to a bona fide purchaser in an arm’s length transaction of minerals recovered from ore mined from the claims. The net proceeds are determined by deducting from the dollar value paid for the recovered minerals, the cost of smelting and refining the ore/or concentrates thereof, marketing and insurance charges, and transportation costs, including the costs of transporting the ore and /or concentrates thereof to the milling facilities and to the smelter or refinery.

Between 2004 and 2006, we completed small prospecting and rock sampling programs on the claims for assessment purposes. During 2007, we completed an exploration program on the property which consisted of airborne geophysics, prospecting, rock sampling, grid work and soil sampling, ground geophysics and excavator trenching. No drilling was done on the property due to lack of funds and no exploration work of any kind was done during the 2008 and 2009 field seasons for the same reasons. In October 2011, a small rock sampling program on the Molly Gibson gold zone Burnt Basin property was conducted in which 68 samples were taken and 29 assayed. We have also commissioned and obtained technical reports, with the latest one dated June 15, 2012 which included recommendations for further work.

We are presently in the pre-exploration stage and there is no assurance that a commercially viable mineral deposit exists in the property until further exploration is done and a comprehensive evaluation concludes economic and legal feasibility.

The Burnt Basin mineral claims are without known economic mineralization and the proposed program is exploratory in nature. We must conduct exploration to determine what amount of minerals, if any, exist on the property and if any minerals which are found can be economically extracted and profitably processed.

To achieve our goals and objectives for the next 12 months, and order to commence our proposed two-phase exploration program on the Burnt Basin property, we plan to raise additional capital through private placements of our equity securities and, if available on satisfactory terms, debt financing. If we are unsuccessful in obtaining new capital, our ability to continue our exploration programs and meet our current financial obligations could be adversely affected and we could forfeit our rights and interests in the property.

Results of Operations

We had no revenues in the years ended December 2012 and 2011.

We reported a total comprehensive loss during 2012 of $223,000 compared to a total comprehensive loss of $238,000 during 2011. Such change was primarily due to a decrease in geological consulting fees which were $21,000 in 2012 compared to $36,000 in 2011, and a decrease in filing and transfer agent fees which were $12,000 in 2012 compared to $21,000 in 2011, partially offset by an increase in accounting and legal fees which were $73,000 in 2012 compared to $58,000 in 2011. Geological and consulting fees were greater in 2011 compared to 2012 primarily due to the sampling program on the Molly Gibson gold zone Burnt Basin property which was conducted in October 2011.

Officer compensation was $110,000 in 2012 and $120,000 in 2011. Compensation for the Company’s President has been accrued at $10,000 per month which accrual began as of January 1, 2010. Office and travel expenses were $5,000 in each of 2012 and 2011. Interest was $2,000 in 2012 compared to $1,000 in 2011 and depreciation was zero in 2012 compared to $800 in 2011. There were also bank charges in 2012 of $600 for which there was not a comparable item in 2011.

Since inception from July 16, 2003 to December 31, 2012, we had a total comprehensive loss of $4,338,000.

Liquidity and Capital Resources

On December 31, 2012, we had working capital deficit of $164,000 and a stockholders’ deficiency of $128,000, compared to working capital deficit of $411,000 and a stockholders’ deficiency of $376,000 on December 31, 2011. On December 31, 2012, we had cash of $27,000, total assets of $62,000 and total liabilities of $190,000 compared to cash of $42,000, total assets of $77,000 and total liabilities of $453,000 on December 31, 2011.

Cash used in operating expenses was $(113,000) for the year ended December 31, 2012 which was primarily the result of a net loss of $(223,000), offset by changes in accrued officers salaries of $100,000 and accounts payable and accrued liabilities of $8,000. Cash used in operating expenses was $(129,000) for the year ended December 31, 2011 which was primarily the result of a net loss of $(241,000) and changes in accounts payable and accrued liabilities of $(9,000), offset by accrued salaries of $120,000.

There was no cash provided by or used in investing activities for the years ended December 31, 2012 and 2011.

Cash provided by financing activities was $98,000 for the year ended December 31, 2012 due to the net proceeds from the sale of common stock and warrants of $98,000. Cash provided by financing activities was $164,000 for the year ended December 31, 2011 primarily due to the net proceeds from the sale of common stock and warrants of $194,000 offset by loan payable-shareholders of $(30,000).

There was also non-cash investing and financing activities of $371,000 in 2012 due to the conversion of the debt of $371,000 owing to Derek Bartlett which was assigned to Alex Johnston which debt was converted into 18,546,350 shares of common stock of the Company.

Our financial statements have been prepared assuming that we will continue as a going concern. The general business strategy of the Company is to explore and research existing mineral properties and to potentially acquire further claims either directly or through the acquisition of operating entities. The continued operations of the Company depends upon the recoverability of mineral property reserves, confirmation of the Company’s interest in the underlying mineral claims, the ability of the Company to obtain necessary financing to complete the development of these claims and upon the future profitable production of the claims. There continues to be insufficient funds to provide enough working capital to fund ongoing operations for the next twelve months. Management intends to raise additional capital through share issuances to finance its exploration on the Burnt Basin property although there can be no assurance that management will be successful in these efforts.

The Company has a working capital deficit at December 31, 2012 of $164,000, has an accumulated deficit during the exploration stage of $4,487,000 and has not generated any operating revenue to date. These factors raise substantial doubt about the Company’s ability to continue as a going-concern, which is dependent on the Company’s ability to obtain and maintain an appropriate level of financing on a timely basis and to achieve sufficient cash flows to cover obligations and expenses. The outcome of the above matters cannot be predicted at this time. The financial statements do not give effect to any adjustments to the amounts and classifications of assets and liabilities, which might be necessary should the Company be unable to continue as a going-concern.

In addition to raising additional capital through shares issuances, we have obtained unsecured loans from shareholders and other third parties in the past and we expect will be seek additional loans in the future from certain shareholders and others, if necessary, in order to fund our current operations including meeting the annual CDN $10,000 prepaid NSR payments to John Carson. In this regard, although there can be no assurance, we expect we will be able to obtain such capital through share issuances and/or loans. In addition, in order to fund the cash requirements which will be necessary for the two phase work program on the Burnt Basin property, it may be necessary for us to seek a joint venture partner to help fund the project. While only preliminary discussions have been held with certain possible partners, we believe we will be able to obtain such a joint venture partner if financial circumstances make such action necessary. If we are unable to raise additional capital, obtain additional loans or engage a joint venture partner who can help fund the Burnt Basin project, we will not be able to continue operations for more than the next few months. However, we are confident that one or more of the foregoing arrangements will be able to be effected in the near term, which will allow us to continue operations during and beyond the next twelve months.

Provided we are able to obtain the necessary capital, we intend to commence and complete the updated Phase 1 program as recommended in the most recent technical report for the Burnt Basin property over the next twelve months. In this regard, we anticipate that we will need at least $400,000 in financing in order to achieve our goals and objectives over the next twelve months, which includes $250,000 to complete the Phase 1 program and at least $150,000 for operations. This does not include any amounts which will be due to Derek Bartlett, our President, under the terms of his Management Services Agreement.

We were able to raise $200,000 in equity financing in the third quarter of 2011, $98,000 in the third quarter of 2012 and intend to attempt to raise additional funds in 2013. No assurance can be given that these efforts will be successful or that we will be able to raise sufficient capital to fund our operations over the next twelve months. However, assuming we are successful in raising needed funds, we expect to commence the Phase 1 program as soon as possible in 2013 and hope to complete Phase 1 during 2013, although extreme weather conditions could delay the progress of the Phase 1 program. The updated Phase 2 program, which is contingent on the results achieved in the Phase 1 program, will hopefully be able to commence in the latter part of 2013 or into 2014. However, if it turns out that we have not raised enough financing to complete the Phase 2 program, we may be forced to seek additional financing or attempt to obtain a joint venture partner if we have not already done so in connection with the financing needed for the Phase 1 program. Again, no assurance can be made that these efforts in obtaining additional financing or a joint venture partner will be successful.

Off-Balance Sheet Arrangements

We do not have any off balance sheet arrangements that are reasonably likely to have a current or future effect on our financial condition, revenues, and results of operations, liquidity or capital expenditures.

Significant Accounting Policies

Our discussion and analysis of the Company’s financial condition and results of operations are based upon our consolidated financial statements which have been prepared in conformity with U.S. generally accepted accounting principles. Our significant accounting policies are described in Note 3 to the consolidated financial statements included elsewhere herein. The application of our critical accounting policies is particularly important to the portrayal of our financial position and results of operations. The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America require management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenues and expenses during the reporting period. Significant estimates include the recoverability of resource properties, accrued liabilities, rate of amortization and the valuation allowance for deferred income tax assets. Management believes the estimates are reasonable; however, actual results could differ from those estimates and could impact future results of operations and cash flows. Described below are the most significant policies we apply in preparing our financial statements.

Foreign Currency Translation – Our operations and activities are conducted principally in Canada; hence the Canadian dollar is the functional currency. We translate financial statements into the functional currency as follows: non-monetary assets and liabilities are translated at historical rates; monetary assets and liabilities are translated at exchange rates in effect at the end of the year; and expenses are translated at average rates for the year. Gains and losses from translation of foreign currency into the functional currency are included in current results of operations. Gains and losses resulting from foreign currency transactions are also included in current results of operations. Our reporting currency is the United States dollar. We translate financial statements into the reporting currency as follows: assets and liabilities are translated at the rates of exchange on the balance sheet date, and revenues and expenses are translated at average rates of exchange during the period. The resulting translation adjustments are included as part of other comprehensive income.

Mineral Property Acquisition Payments and Exploration Costs- We follow accounting standards for mineral rights, which concluded that mineral rights are tangible assets. Accordingly, we capitalize certain costs related to the acquisition of mineral rights. If a commercially mineable ore body is discovered, such costs are amortized when production begins using the unit-of-production method based on proven and probable reserves. If no commercially viable ore body is discovered, or such rights are otherwise determined to have no value, such costs are expensed in the period in which it is determined the property has no future economic value.

Impairment of Long-Lived Assets - Management of the Company periodically reviews the net carrying value of its mineral properties and interests on a property-by-property basis. These reviews consider the net realizable value of each property to determine whether a permanent impairment in value has occurred and the need for any asset write-down. An impairment loss will be recognized when the estimated future cash flows (undiscounted) expected to result from the use of an asset are less than the carrying amount of the asset. Measurement of an impairment loss will be based on the estimated fair value of the asset if the asset is expected to be held and used.

Depreciation - Equipment is recorded at cost. Expenditures for major additions and improvements are capitalized; minor replacements, maintenance and repairs are charged to expense as incurred. When property and equipment are retired or otherwise disposed of, the cost and accumulated depreciation are removed from the accounts and any resulting gain or loss is included in the results of operations for the respective period. Amortization is provided over the estimated useful lives of the related assets using the declining-balance method for financial statement purposes. Amortization of equipment is calculated at 30% on the declining-balance basis.

Asset Retirement Obligations – We have adopted the provisions of US GAAP, “Accounting for Asset Retirement Obligations”. The basis of this policy is the recognition of a legal liability for obligations relating to the retirement of property, plant and equipment, and obligations arising from the acquisition, construction, development or normal operations of those assets. Such asset retirement costs must be recognized at fair value when a reasonable estimate of fair value can be estimated in the period in which the liability is incurred. A corresponding increase to the carrying amount of the related asset, where one is identifiable, is recorded and amortized over the life of the asset. Where a related future value is not easily identifiable with a liability, the change in fair value over the course of the year is expensed. The amount of the liability is subject to re-measurement at each reporting period. The estimates are based principally on legal and regulatory requirements.

It is possible that our estimates of its ultimate reclamation and closure liabilities could change as a result of changes in regulations, changes in the extent of environmental remediation required, changes in the means of reclamation, or changes in cost estimates. Changes in estimates are accounted for prospectively commencing in the period the estimate is revised. No liability has been recorded as the Company is in the exploration stage on its properties and, accordingly, no environmental disturbances have occurred.

Fair Value of Financial Instruments - Financial assets and liabilities recorded on the accompanying balance sheets are categorized based on the inputs to the valuation techniques as follows:

Level 1 - Financial assets and liabilities whose values are based on unadjusted quoted prices for identical assets or liabilities in an active market that the company has the ability to access at the measurement date (examples include active exchange-traded equity securities, listed derivatives and most United States Government and agency securities).

Level 2 - Financial assets and liabilities whose values are based on quoted prices in markets where trading occurs infrequently or whose values are based on quoted prices of instruments with similar attributes in active markets. Level 2 inputs include the following:

| | • | Quoted prices for identical or similar assets or liabilities in non-active markets (examples include corporate and municipal bonds which trade infrequently); |

| | • | Inputs other than quoted prices that are observable for substantially the full term of the asset or liability (examples include interest rate and currency swaps); and |

| | • | Inputs that are derived principally from or corroborated by observable market data for substantially the full term of the asset or liability (examples include certain securities and derivatives). |

Level 3 - Financial assets and liabilities whose values are based on prices or valuation techniques that require inputs that are both unobservable and significant to the overall fair value measurement. These inputs reflect management’s own assumptions about the assumptions a market participant would use in pricing the asset or liability.

An asset or liability’s level within the fair value hierarchy is based on the lowest level of any input that is significant to the fair value measurement. Availability of observable inputs can vary and is affected by a variety of factors. We use judgment in determining fair value of assets and liabilities and Level 3 assets and liabilities involve greater judgment than Level 1 and Level 2 assets or liabilities.

Stock Based Compensation - We account for share-based compensation in accordance with ASC Topic 718, Compensation - Stock Compensation (ASC 718). Under the provisions of ASC 718, share-based compensation cost is measured at the grant date, based on the calculated fair value of the award, and is recognized as an expense over the employee’s requisite service period (generally the vesting period of the equity grant).

Recent Accounting Pronouncements

In March 2011, accounting standards update on “Troubled Debt Restructuring” was issued. The update clarifies which loan modifications constitute troubled debt restructurings. It is intended to assist creditors in determining whether a modification of the terms of a receivable meets the criteria to be considered a troubled debt restructuring, both for purposes of recording an impairment loss and for disclosure of troubled debt restructurings. In evaluating whether a restructuring constitutes a troubled debt restructuring, a creditor must separately conclude that both of the following exist: (a) the restructuring constitutes a concession; and (b) the debtor is experiencing financial difficulties. We adopted the amendment on January 1, 2012. This adoption of this amendment did not have a material impact on our operations.

In May 2011, the FASB issued ASU 2011-04, “Fair Value Measurement (Topic 820), Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and IFRS”. The amendment results in a consistent definition of fair value and ensures the fair value measurement and disclosure requirements are similar between GAAP and International Financial Reporting Standards (“IFRS”). This amendment changes certain fair value measurement principles and enhances the disclosure requirements particularly for Level 3 fair value measurements. This amendment will be effective for the Company on January 1, 2012. We adopted the amendment on January 1, 2012 on a prospective basis. The adoption of ASU No. 2011-04 had no material effect on our financial statements.

In June 2011, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) No. 2011-05, Presentation of Comprehensive Income, which revises the manner in which entities present comprehensive income in their financial statements. The ASU removes the presentation options in Accounting Standard Codification Topic 220 and requires entities to report components of comprehensive income in either 1) a continuous statement of comprehensive income or 2) two separate but consecutive statements. In December 2011, FASB issued Accounting Standards Update (“ASU”) No. 2011-12, “Comprehensive Income” which effectively defers the changes in ASU No. 2011-05, “Presentation of Comprehensive Income” that relate to the presentation of reclassification adjustments out of accumulated other comprehensive income to the first quarter of 2012 for the Company. We adopted the amendments on January 1, 2012 and presented a continuous statement of comprehensive loss.

In December 2011, the FASB issued ASU 2011-11, “Balance Sheet (Topic 210), Disclosures about Offsetting Assets and Liabilities”. The guidance in this update requires the Company to disclose information about offsetting and related arrangements to enable users of its financial statements to understand the effect of those arrangements on its financial position. The pronouncement is effective for fiscal years and interim periods beginning on or after January 1, 2013 with retrospective application for all comparative periods presented. The Company’s adoption of the new standard is not expected to have a material effect on the Company’s consolidated financial position or results of operations.

In July 2012, the FASB issued ASU 2012-02, “Testing Indefinite-Lived Intangible Assets for Impairment”, which provides companies with the option to first assess qualitative factors in determining whether the existence of events and circumstances indicates that it is more likely than not that an indefinite-lived intangible asset is impaired. If, after assessing the totality of events and circumstances, an entity concludes that it is not more likely than not that an indefinite-lived intangible asset is impaired, then the entity is not required to take further action. However, if an entity concludes otherwise, then it is required to determine the fair value of the indefinite-lived intangible asset and perform the quantitative impairment test by comparing the fair value with the carrying value. Previously, companies were required to perform the quantitative impairment test at least annually. The new accounting guidance is effective for annual and interim impairment tests performed for fiscal years beginning after September 15, 2012. We do not anticipate the adoption of the new accounting guidance to have a significant effect on our financial condition or results of operations.

In February 2013, the FASB issued Accounting Standards Update (“ASU”) 2013-02, “Comprehensive Income (Topic 220) Reporting Amounts Reclassified Out Of Accumulated Other Comprehensive Income.” ASU 2013-02 requires entities to report either on their income statement or disclose in footnotes to the financial statements the effects on net income from significant items that are classified out of the accumulated other comprehensive income for all reporting periods (annual and interim) covered by the financial statements. The standard also requires cross-reference to other disclosures currently required under GAAP for other reclassification items that are not required to be reclassified directly to net income. This standard is effective for us for fiscal periods beginning after December 15, 2012 and we expect the adoption of ASU 2013-02 to have no material impact on our financial position and results of operations.

In January 2013, the FASB issued ASU 2013-01, “Clarifying the Scope of Disclosures about Offsetting Assets and Liabilities.” The FASB issued ASU 2013-01 in response to concerns raised by constituents regarding the potential broad scope of disclosure requirements upon adoption of ASU 2011-11. It limits the scope of the new balance sheet offsetting disclosures to derivatives, repurchase agreements and securities lending transactions to the extent that they are (1) offsetting in the financial statements or (2) subject to an enforceable master netting arrangement or similar agreement. ASU 2013-01 will be effective for us on January 1, 2013. We expect the adoption of this standard to have no material effect on our financial position and results of operations.

Item 7A. Quantitative and Qualitative Disclosures About Market Risk.

We are a smaller reporting company as defined by Rule 12b-2 of the Securities Exchange Act of 1934 and are not required to provide the information under this item.

Item 8. Financial Statements and Supplementary Data.

NEWPORT GOLD, INC.

(An Exploration Stage Company)

CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2012

NEWPORT GOLD, INC.

INDEX

| | PAGE |

| | |

| INDEPENDENT AUDITOR’S REPORT OF REGISTERED PUBLIC ACCOUNTING FIRM | F-2 |

| | |

| CONSOLIDATED BALANCE SHEETS | F-3 |

| | |

| CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS | F-4 |

| | |

| CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY (DEFICIT) | F-5 to F-6 |

| | |

| CONSOLIDATED STATEMENTS OF CASH FLOWS | F-7 |

| | |

| NOTES TO CONSOLIDATED FINANCIAL STATEMENTS | F-8 to F-15 |

INDEPENDENT AUDITOR’S REPORT OF REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and Stockholders of Newport Gold, Inc. (An Exploration Stage Company)

Report on the Financial Statements

We have audited the accompanying consolidated financial statements of Newport Gold, Inc. (An Exploration Stage Company) (the “Company”), which comprise the consolidated balance sheets as of December 31, 2012 and 2011, and the related consolidated statements of operations and comprehensive loss, changes in stockholders’ equity (deficit), and cash flows for the years ended December 31, 2012 and 2011 and for the period July 16, 2003 (inception) to December 31, 2012 and the related notes to the consolidated financial statements.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audit. We conducted our audit in accordance with the standards of the Public Company Accounting Oversight Board (“PCAOB”). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of the Company as at December 31, 2012 and 2011 and the results of its operations and its cash flows for the years then ended and for the period from July 16, 2003 (inception) to December 31, 2012, in accordance with accounting principles generally accepted in the United States of America.

Emphasis of Matter

The accompanying consolidated financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 2 to the consolidated financial statements, the Company has suffered recurring losses from operations and has a net capital deficiency that raise substantial doubt about its ability to continue as a going concern. Management’s plans in regard to these matters are also described in Note 2. The consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty. Our opinion is not modified with respect to this matter.

| /s/ Fazzari + Partners LLP | |

| Fazzari + Partners LLP | |

Chartered Accountants Licensed Public Accountants | Vaughan, Ontario, Canada April 1, 2013 |

NEWPORT GOLD, INC.

(An Exploration Stage Company)

Consolidated Balance Sheets

(In U.S. Dollars)

| | | December 31, | | | December 31, | |

| | | 2012 | | | 2011 | |

| Assets | | | | | | |

| | | | | | | |

| Current | | | | | | |

| Cash and cash equivalents | | $ | 26,580 | | | $ | 41,847 | |

| Prepaid expenses | | | 233 | | | | 233 | |

| | | | 26,813 | | | | 42,080 | |

| Long-term | | | | | | | | |

| Mineral interests (Note 5) | | | 35,397 | | | | 35,397 | |

| Equipment (Note 6) | | | - | | | | - | |

| | | | 35,397 | | | | 35,397 | |

| Total Assets | | $ | 62,210 | | | $ | 77,477 | |

| | | | | | | | | |

| Liabilities | | | | | | | | |

| | | | | | | | | |

| Current | | | | | | | | |

| Accounts payable and accrued liabilities | | $ | 156,161 | | | $ | 147,778 | |

| Accrued officers salaries (Note 7) | | | - | | | | 271,000 | |

| Due to related parties (Note 7) | | | 34,240 | | | | 34,240 | |

| Total Liabilities | | | 190,401 | | | | 453,018 | |

| | | | | | | | | |

| Stockholders' Deficit | | | | | | | | |

| | | | | | | | | |

Common stock - Authorized 100,000,000 common shares with a par value of $0.001 per share. Issued and outstanding 57,310,070 at December 31, 2012 and 36,823,720 at December 31, 2011. (Note 8) | | | 57,310 | | | | 36,823 | |

| Additional paid-in capital | | | 4,152,905 | | | | 3,694,895 | |

| Subscriptions receivable | | | - | | | | 8,010 | |

| Accumulated other comprehensive income | | | 148,872 | | | | 148,750 | |

| Accumulated deficit - during exploration stage | | | (4,487,278 | ) | | | (4,264,019 | ) |

| Total Stockholders' Deficit | | | (128,191 | ) | | | (375,541 | ) |

| | | | | | | | | |

| Total Liabilities and Stockholders' Deficit | | $ | 62,210 | | | $ | 77,477 | |

The accompanying notes are an integral part of these consolidated financial statements.

NEWPORT GOLD, INC.

(An Exploration Stage Company)

Consolidated Statements of Operations and Comprehensive Loss

(In U.S. Dollars)

| | | | | | | | | July 16, 2003 | |

| | | Twelve Months Ended | | | (inception) to | |

| | | December 31, | | | December 31, | |

| | | 2012 | | | 2011 | | | 2012 | |

| Expenses | | | | | | | | | |

| Officers compensation | | $ | 110,027 | | | $ | 120,000 | | | $ | 527,547 | |

| Accounting and legal | | | 72,811 | | | | 57,754 | | | | 499,536 | |

| Geological consulting fees | | | 21,185 | | | | 35,827 | | | | 560,402 | |

| Office and travel | | | 5,430 | | | | 4,575 | | | | 93,391 | |

| Interest | | | 1,712 | | | | 1,382 | | | | 3,311 | |

| Bank charges | | | 580 | | | | | | | | 580 | |

| Write-down of mineral interest | | | - | | | | - | | | | 2,397,663 | |

| Investor relations | | | - | | | | - | | | | 115,535 | |

| Consulting | | | - | | | | - | | | | 110,000 | |

| Resource property expenditures | | | - | | | | - | | | | 86,852 | |

| Filing and transfer agent fees | | | 11,514 | | | | 20,565 | | | | 69,455 | |

| Occupancy costs | | | - | | | | - | | | | 17,514 | |

| Depreciation | | | - | | | | 820 | | | | 5,620 | |

| Foreign exchange (gain) | | | - | | | | - | | | | (128 | ) |

| | | | | | | | | | | | | |

| Net (loss) | | | (223,259 | ) | | | (240,923 | ) | | | (4,487,278 | ) |

| | | | | | | | | | | | | |

| Foreign currency translation adjustment | | | 122 | | | | 2,620 | | | | 148,872 | |

| | | | | | | | | | | | | |

| Total comprehensive (loss) | | $ | (223,137 | ) | | $ | (238,303 | ) | | $ | (4,338,406 | ) |

| | | | | | | | | | | | | |

| Net loss per share - basic and diluted | | $ | (0.01 | ) | | $ | (0.01 | ) | | $ | | |

| | | | | | | | | | | | | |

| Weighted average number of common shares outstanding - basic and diluted | | | 39,196,767 | | | | 35,573,720 | | | | | |

The accompanying notes are an integral part of these consolidated financial statements.

NEWPORT GOLD, INC.

(An Exploration Stage Company)

Consolidated Statements of Changes in Stockholders’ Equity (Deficit)

For the period July 16, 2003 (Inception) through December 31, 2012

(In U.S. Dollars)

| | | | | | | | | | | | | | | | | | Accumulated | | | | |

| | | Common Stock | | | Additional | | | Share | | | Other | | | Deficit During | | | Total | |

| | | Par Value $0.001 | | | Paid-in | | | Subscriptions | | | Comprehensive | | | Exploration | | | Stockholders' | |

| | | Shares | | | Amount | | | Capital | | | Received | | | Income | | | Stage | | | Equity (Deficit) | |

| | | | | | | | | | | | | | | | | | | | | | |

| Share subscriptions | | | | | | | | | | | | | | | | | | | | | |

| -cash | | | - | | | $ | - | | | $ | - | | | $ | 93,150 | | | $ | - | | | $ | - | | | $ | 93,150 | |

| -property | | | - | | | | - | | | | - | | | | 22,500 | | | | - | | | | - | | | | 22,500 | |

| Foreign currency | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| translation adjustment | | | - | | | | - | | | | - | | | | - | | | | (3,409 | ) | | | - | | | | (3,409 | ) |

| Net Loss | | | - | | | | - | | | | - | | | | - | | | | - | | | | (161,681 | ) | | | (161,681 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Balance December 31, 2003 | | | - | | | | - | | | | - | | | | 115,650 | | | | (3,409 | ) | | | (161,681 | ) | | | (49,440 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Foreign currency | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| translation adjustment | | | - | | | | - | | | | - | | | | - | | | | (1,124 | ) | | | - | | | | (1,124 | ) |

| Net Loss | | | - | | | | - | | | | - | | | | - | | | | - | | | | (95,960 | ) | | | (95,960 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Balance December 31, 2004 | | | - | | | | - | | | | - | | | | 115,650 | | | | (4,533 | ) | | | (257,641 | ) | | | (146,524 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Share subscriptions | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| -cash | | | - | | | | - | | | | - | | | | 144,000 | | | | - | | | | - | | | | 144,000 | |

| Foreign currency | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| translation adjustment | | | - | | | | - | | | | - | | | | - | | | | (2,476 | ) | | | - | | | | (2,476 | ) |

| Net Loss | | | - | | | | - | | | | - | | | | - | | | | - | | | | (93,207 | ) | | | (93,207 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Balance December 31, 2005 | | | - | | | | - | | | | - | | | | 259,650 | | | | (7,009 | ) | | | (350,848 | ) | | | (98,207 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Common shares issued | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| -for cash | | | 4,200,000 | | | | 4,200 | | | | 271,800 | | | | - | | | | - | | | | - | | | | 276,000 | |

| -for mining claims | | | 2,500,000 | | | | 2,500 | | | | 247,500 | | | | - | | | | - | | | | - | | | | 250,000 | |

| -for share subscriptions | | | 8,375,000 | | | | 8,375 | | | | 251,275 | | | | (259,650 | ) | | | - | | | | - | | | | - | |

| Foreign currency | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| translation adjustment | | | - | | | | - | | | | - | | | | - | | | | 577 | | | | - | | | | 577 | |

| Net Loss | | | - | | | | - | | | | - | | | | - | | | | - | | | | (339,331 | ) | | | (339,331 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Balance December 31, 2006 | | | 15,075,000 | | | | 15,075 | | | | 770,575 | | | | - | | | | (6,432 | ) | | | (690,179 | ) | | | 89,039 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Common shares issued | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| -for mining claims | | | 3,111,500 | | | | 3,111 | | | | 1,848,789 | | | | - | | | | - | | | | - | | | | 1,851,900 | |

| Foreign currency | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| translation adjustment | | | - | | | | - | | | | - | | | | - | | | | 159,375 | | | | - | | | | 159,375 | |